Stochastic control and non-equilibrium

thermodynamics: fundamental limits

Abstract

We consider damped stochastic systems in a controlled (time-varying) quadratic potential and study their transition between specified Gibbs-equilibria states in finite time. By the second law of thermodynamics, the minimum amount of work needed to transition from one equilibrium state to another is the difference between the Helmholtz free energy of the two states and can only be achieved by a reversible (infinitely slow) process. The minimal gap between the work needed in a finite-time transition and the work during a reversible one, turns out to equal the square of the optimal mass transport (Wasserstein-2) distance between the two end-point distributions times the inverse of the duration needed for the transition. This result, in fact, relates non-equilibrium optimal control strategies (protocols) to gradient flows of entropy functionals via and the Jordan-Kinderlehrer-Otto scheme. The purpose of this paper is to introduce ideas and results from the emerging field of stochastic thermodynamics in the setting of classical regulator theory, and to draw connections and derive such fundamental relations from a control perspective in a multivariable setting.

I Introduction

The quest to quantify the efficiency of the steam engine during industrial revolution of the 19th century precipitated the development of thermodynamics. While its birth predates the atomic hypothesis, its modern day formulation makes mention of “macroscopic” systems that consist of a huge number of “microscopic” particles (e.g., of the order of Avogadro’s number), effectively modeled using probabilistic tools. Its goal is to describe transitions between admissible end-states of such macroscopic systems and to quantify energy and heat transfer between the systems and the “heat bath” that they may be in contact with. In spite of the name suggesting “dynamics,” the classical theory relied heavily on the concept of quasi-static transitions, i.e., transitions that are infinitely slow. More realistic finite-time transitions has been the subject of “non-equilibrium thermodynamics,” a discipline that has not reached yet the same level of maturity, but one which is currently experiencing a rapid phase of new developments. Indeed, recent developments have launched a phase referred to as stochastic thermodynamics and stochastic energetics [1, 2, 3, 4, 5, 6, 7, 8, 9, 10, 11, 12], that aims to quantify non-equilibrium thermodynamic transitions. The reader is referred to a nice and detailed review article [12] for an overview of this subject. Our goal in this paper is to develop such a framework, focusing on the stochastic control of linear uncertain systems in a quadratic (controlled) potential, in a way that is reminiscent of what is known as covariance control [13, 14, 15, 16], and obtain simple derivation of fundamental bounds on the required control and dissipation in achieving relevant control objectives.

Specifically, we consider transitions of a thermodynamic system, represented by overdamped motion of particles in a (quadratic) potential, from one stationary stochastic state to another over a finite-time window . The system is modeled by the (vector-valued) Ornstein-Uhlenbeck process

| (1) |

with and a standard (-vector-valued) Wiener process representing a thermal bath of temperature ; the parameter

Here is the Boltzmann constant [2], the Hookean force field is the gradient of a time-varying quadratic Hamiltonian

| (2) |

and the controlled parameter , , is scheduled so as to steer the system from a specified initial distribution for , to a final one for , over the specified time window. The random variables are taken to be Gaussian with zero mean and covariances , respectively. That is, the distributions of the state at the two end points have probability densities are , or more explicitly,

and we seek to determine the minimum amount of work needed to effect the transition.

From a controls perspective, our problem amounts to covariance control of bilinear systems. Indeed, the dynamics are driven by the product of the control input times the state . By adjusting the quadratic potential, it is possible to steer the system from one Gaussian distribution to another in finite time . When this is the case, we are interested in the optimal control strategy (, ) that minimizes the required control energy.

As noted in the abstract, this minimum control energy is greater than the Helmholtz free energy difference between the two states (second law of thermodynamics). Starting with the works by Jarzynski [1, 2] and Crooks [3], great new insights began to shed light on the precise amount of work required for such finite-time transitions. Most famously, the Jarzynski equality

| (3) |

relates the equilibrium quantity (free energy difference between equilibrium states) to an averaged non-equilibrium quantity (exponential of the work; see our discussion below) over possible trajectories of the system in any finite-time transition. Throughout, denotes the expectation on the path space of system trajectories and

where again represents temperature of the heat bath and the Boltzmann constant; has units of “inverse-work.” The Jarzynski identity holds for arbitrary time-dependent driving force and not necessarily gradient of a quadratic potential. This type of result has led to a number of so-called Fluctuation Theorems in the literature, some of which have profound implications in biology and medicine [12, 17, 18].

Although the Jarzynski equality is quite remarkable, it doesn’t provide an explicit gap between the free energy difference and the average work . This gap is essential if we would like to find an optimal strategy with minimum work to move a thermodynamical system from one state to another. Following up on the Jarzynski equality, the authors of [6, 19] analyze the minimum energy control problems in the cases of a Brownian particle dragged by a harmonic optical trap through a viscous fluid, and of a Brownian particle subject to an optical trap with time dependent stiffness, in both overdamped and underdamped setting. Further, in [20, 11], the authors provide an optimal solution that relates the work dissipation to a Wasserstein distance. It can be viewed as a stronger version of the Second Law of Thermodynamics for certain Langevin stochastic processes in finite-time.

The present work is closely related to both [20, 11] as well as [6, 19]. Compared to [20, 11], our approach gives a control-theoretic account to the fluctuation type results in the case for Gaussian distributions. In addition, we provide an alternative proof for general cases with connections to the gradient flows with respect to the Wasserstein geometry [21]. The major difference to [6, 19] is that we consider the general matrix cases in this paper. We remark that the problems studied in [20, 11] and [6, 19] are not equivalent. These two can be connected through an relaxation step as discussed in Section VI.

The rest of the paper is organized as follows. In Section II we go over some key concepts in stochastic thermodynamics and optimal mass transport. The minimum energy control problem between two zero-mean Gaussian distributions is formulated and solved in Section III. The results’ implication in the second law of thermodynamics is discussed in Section IV. The result is extended to the nonzero mean setting in Section V. A modification of our problem without terminal constraint on distributions is solved in Section VI. After that, in Section VII, by leveraging the optimal mass transport theory, we solve the minimum energy control problem with general marginal distributions. Last, for comparison, we go over a simple proof of the Jarzynski equality in Section VIII. We conclude with several numerical examples in Section IX.

II Preliminaries

This work bridges stochastic control, stochastic thermodynamics and optimal mass transport. Below we introduce some key concepts in stochastic thermodynamics and optimal mass transport that are relevant.

II-A Stochastic thermodynamics

Stochastic thermodynamics [12, 22] is one approach to study thermodynamical systems via stochastic calculus. A basic model in this framework is

| (4) |

Here is the Hamiltonian of the system and the noise describes the effect of the heat bath. When the Hamiltonian is fixed, the state distribution converges to a Boltzmann distribution

where is a partition function. This is known as the equilibrium steady state. We denote the internal energy and Helmholtz free energy in the equilibrium steady state by and respectively. They are defined by [22]

and

Clearly, they satisfy the relation

| (5) |

with the entropy being

II-B Optimal mass transport

We only cover concepts that are related to the present work. We refer the reader to [24] for complete details. Consider two measures on with equal total mass. Without loss of generality, we take and to be probability distributions. In the Kantorovich’s formulation of optimal mass transport with quadratic cost, one seeks a joint distribution on , referred to as “coupling” of and , that minimizes the total cost, and so that the marginals along the two coordinate directions coincide with and , respectively, that is,

| (7) |

The above optimal transport problem has a surprising stochastic control formulation, which reads as

| (8a) | |||

| (8b) | |||

| (8c) | |||

Briefly, we seek a feedback control strategy with minimum energy that drives the state of an integrator from an initial probability distribution to a terminal probability distribution .

Both of the above problems have unique solutions under the assumption that the marginal distributions are absolutely continuous. The square root of the minimum of the cost ((7) or (8)) defines a Riemannian metric on , the space of probability distributions on with finite second-order moments. This metric is known as the Wasserstein metric [21, 25, 24, 26]. On this Riemannian-type manifold, the geodesic curve connecting and is given by , the probability density of under the optimal control policy. This is called displacement interpolation [27] and it satisfies

| (9) |

When both of the marginals are Gaussian distributions, the problem has a closed-form solution [28, 29, 30]. Denote the mean and covariance of by and , respectively. Let be two Gaussian random vectors associated with , respectively. Then the cost in (7) becomes

| (10) |

where are zero-mean versions of and . We minimize (10) over all the possible Gaussian joint distributions between and , which gives

| (11) |

with . The constraint is a semidefinite one, so the above problem is one of semidefinite programming (SDP). The minimum is achieved in closed-form by the unique minimizer

| (12) |

corresponding to the minimum value

| (13) |

The resulting displacement interpolation is a Gaussian distribution with mean and covariance

| (14) |

III Regulation via a time-varying potential

We consider the stochastic dynamical system in (1). As mentioned earlier, it represents a thermodynamical system with a quadratic Hamiltonian (2), overdamped and attached to a heat bath that is modeled by the stochastic excitation . The initial state is a Gaussian random vector , i.e., one having covariance and mean . The initial distribution is usually taken to be the stationary distribution with potential remaining constant on by keeping over , in which case , but this assumption is not required. We are interested in steering the state to the terminal distribution through selecting an optimal (least energy) time-varying control matrix variable satisfying the boundary conditions .

The control energy (work) delivered to the system along any particular sample path by the time-varying potential (2) is

where . Thus, by averaging over all possible sample paths, we obtain

Here, is the state covariance which, according to standard linear systems theory, evolves according to the Lyapunov equation

| (15) |

The control may be discontinuous, reflecting instantaneous changes in the Hamiltonian , in which case, the expression for the work becomes the Lebesgue-Stieltjes integral

| (16) |

where represent limits from below and above, respectively, so as to account for the discontinuities.

Theorem 2

Problem 1 has a unique minimizer

as follows:

-

(i)

If , then and

-

(ii)

If , then

(17) and

(18a) (18b) with

(19a) (19b)

Proof 1

Case (i) is trivial. We only discuss case (ii) in detail. Applying integration by parts to (16), we obtain

| (20) |

Notice that

is precisely the change in the average energy (expectation of the Hamiltonian) and is independent of the control . More specifically,

Substituting (15) into (20) yields

| (21) |

We change variables, replacing by

in both, the constraint (15) as well as (21). These now become

| (22) | ||||

| (23) |

respectively. From (22),

It follows that

is independent of the choice of or . Thus, minimization of (21) (equivalently, minimization of (23)) is equivalent to minimization of

| (24) |

subject to the choice of that satisfies (22) and the boundary conditions and . Then,

| (25) |

Setting , the functional becomes convex in . Then,

subject to the linear constraint

| (26) |

has a unique solution. In fact, a closed-form expression can be obtained by considering the necessary conditions that are being dictated by the stationarity of the Lagrangian

Specifically, the first variation with respect to gives that

Then, the variation with respect to gives

| (27) |

Assuming that is nonsingular,

From (22),

for a suitable choice of a matrix . Then, are determined from the boundary conditions,

It follows that

from which we deduce that is the geometric mean of and (see [31]), viz.,

Thus, we conclude (19).

Remark 3

The optimal control in (18a) is continuous function on . The limit values at are

and

respectively. These may not be consistent with the boundary conditions , which dictates the discontinuities of the optimal control at . When both the initial and terminal states are stationary, namely, , such discontinuities go to zero as the length of time goes to infinity.

IV Second law of thermodynamics and optimal transport

The problem to minimize in (24) is in fact a Monge-Kantorovich optimal transport problem with marginals and , and quadratic cost functional [24, 26]. Specifically,

| (29) |

This follows directly from (28) and (13). Alternatively, consider the stochastic control formulation (8) of optimal transport. The optimal solution, see e.g., [32, 33], is in the linear state feedback form . With ,

and

The optimal is symmetric and therefore coincides with the minimizer of up to a scaling in time. The factor shows up due to the fact that the time window in standard optimal transport is while in our problem it is . Naturally, it follows from this equivalence that the probability density flow of under optimal control is a (scaled) geodesic (displacement interpolation) between and with respect to the Wasserstein metric . Indeed, it can be verified that in (18b) is

which is consistent with the geodesic formula in (14). Thus, we obtain the following:

Theorem 4

The probability density flow of in Problem 1 with optimal control is the (scaled) displacement interpolation between and .

From (29) and Theorem 2, the minimum of is

Using the “log det = trace log” equality, and the fact that the entropy of Gaussian distributions is

and, in view of , we get that the minimum value of is

| (30) |

Next note that the change in the Helmholtz free energy (see (6)) is

Putting all this together, we get that

Theorem 5

| (31) |

Recall that for reversible processes, one has

and for general processes

These are equivalent to the second law of thermodynamics, which says that the total entropy of an isolated system is nondecreasing. Theorem 5 provides a stronger lower bound for entropy production of a finite-time process, and this bound connects thermodynamics and optimal mass transport!

The difference is the entropy production, or work dissipation, and denoted . This is the same as in the proof of Theorem 2. Theorem 5 provides a fundamental lower bound of work dissipation

for a irreversible process evolving in a finite time-interval . As we discussed earlier, this lower bound is achieved by the optimal protocol (18a) and the corresponding probability density flow is the displacement interpolation between and .

In general, for any feasible protocol , the work dissipation depends only on the probability density flow from to .

Theorem 6

| (32c) | |||||

Indeed, once the probability density flow is fixed, we can get through (32c)-(32c) and then through (32c). In fact, this is nothing but the length (scaled by ) of the curve on the manifold of probability densities equipped with the Wasserstein metric [26].

Remark 7

Minimizing the work is equivalent to minimizing the work dissipation as relies only on the boundary conditions. When there is no constraint on the choice of Hamiltonian , the optimal strategy is given by Theorem 2, which leads to a probability density flow that is the displacement interpolation between and . On the other hand, when there exist constraints on , in view of the above argument, we can lift the problem to the space of probability densities, and seek a feasible time-varying Hamiltonian such that the resulting density flow has minimum length on the manifold of probability densities equipped with the Wasserstein metric . This may lead to a promising direction to solve constrained thermodynamical control problems.

V Hamiltonian with nonzero center

In this section, we extend our framework to the cases when the centers of the Hamiltonian potentials are allowed to change over time. Specifically, consider the stochastic thermodynamical system

| (33) |

which corresponds to the Hamiltonian

with time-varying center . Assume the initial and terminal Gaussian distributions are . Our goal is to drive the system from initial distribution to terminal distribution with minimum cost via changing the strength as well as the center of the potential well at the same time.

The mean and covariance of evolve according to

| (34a) | |||

| and | |||

| (34b) | |||

The average work is

Problem 8

Find a time-varying from to and a time-varying from to such that has as the marginal distributions and the average work is minimized.

Theorem 9

The optimal and are as in the zero-mean case, and the optimal satisfy

| (35) |

and

| (36) |

The corresponding work is

| (37) | |||||

Proof 2

We first simplify the work to

The last two terms depend only on the boundary conditions. The first two terms are totally decoupled; one depends only on while the other on . Therefore, we can minimize these two terms independently. Clearly, the optimal are identical to that in the zero-mean case (Theorem 2). To obtain , we minimize subject to the boundary conditions . Thus, the optimal is the linear interpolation between and . Plugging it into (34b) concludes the optimal .

As we have already seen in Section III, the optimal strength of the potential usually has discontinuities at the boundary points . We next argue that similar phenomenon happens for the center of the potential. From (36) we get

These usually don’t match the boundary conditions . When both the initial and terminal states are stationary, in which case , the discontinuity gaps at go to zero as goes to infinity.

VI Relaxation

In this section, we consider a modified version of Problem 1. We specify a terminal value for the potential by fixing while we relax the terminal constraint , which is commonly set to be . This value for the covariance will be then attained asymptotically since, even if we do not specify the terminal distribution, it will converge to the Boltzmann distribution due to fluctuation-dissipation effects. Therefore, if our goal is to simply minimize the work, there is no need to insist on setting . More precisely, we address the following.

Problem 10

There are several possible approaches to solve the above problem. One of them is applying standard calculus of variations, just like what we did in the proof of Problem 1. Here, we adopt an alternative idea which solves the problem in two steps. We first find the solution for a given terminal value and then minimize the cost function over all possible . Evidently, the first step is equivalent to solving Problem 1. The optimal cost is given by (31), which is

where are the zero-mean Gaussian distributions with covariances . The free energy is

By (11), the distance between two Gaussian distributions is given by the solution of the SDP

Plugging them into the cost yields the convex optimization formulation of Problem 10

| (39a) | |||

| (39b) | |||

After solving (39), we can obtain the solution of Problem 10 via that of Problem 1 with the optimal as a boundary condition.

Theorem 11

Proof 3

First we construct a Lagrangian

with Lagrange multiplier

Minimizing over leads to the constraint

and over yields as minimizer

| (41) |

Therefore, we obtain the dual problem

| (42a) | |||

| (42b) | |||

In the above, for fixed , the minimizer over is clearly . Thus, (42) is equivalent to the convex optimization problem

| (43) |

Its first order optimality condition is

or equivalently

Let , then

It follows that

If we pick the solution

| (44) |

then satisfies the constraint . Thus, in view of the strong convexity of (43), we conclude that with in (44) is the unique solution to (43). The optimal follow from (12) and (41). This completes the proof.

We establish similar results when the centers of the potentials are nonzero. Denote by , the centers of the initial and target potentials. We seek an optimal control for the following problem.

Problem 12

Find from to and from to over time that minimize the total work subject to constraint (34) as well as boundary condition .

The idea is the same as in the zero-mean case. Straight forward calculation gives

This together with (11) and (38) points to the convex optimization formulation

| (45a) | |||

| (45b) | |||

We note that in (45) the minimization over and that over are decoupled. Thus, we have two independent optimization problems. The solution to the former is given by Theorem 11 and the solution to the latter is given in closed-form as

| (46) |

Next we use the above results to recover two scalar cases that have been solved in Schmiedl and Seifert [6].

VI-A Case study I: Moving laser trap

Suppose the strength of the potential is fixed to be . Our goal is to choose proper function from to such that the work is minimized. The initial state is assumed to be at equilibrium, i.e., .

VI-B Case study II: Time-dependent strength of the trap

VII Connection to JKO gradient flow

The result (31) is closely related to the celebrated Jordan-Kinderlehrer-Otto (JKO) flow [21]. In fact, we obtain an alternative proof of Theorem 5 for general marginal distributions based on the results in [21].

The JKO scheme gives that the Fokker-Planck equation as the gradient flow of the free energy with respect to the Wasserstein metric . Indeed, according to [21], the Fokker-Planck equation

| (47) |

can be viewed as the gradient flow of the free energy

| (48) |

with respect to the Wasserstein metric on the manifold of probability densities. More specifically, discretizing the above in the time domain, we obtain the celebrated JKO scheme. This amounts to the fact that , where is the solution to (47) and is the step size, minimizes

| (49) |

over as goes to . This is akin to our result (31). Next we discuss the connection between the two.

Since minimizes (49), we have

| (50) |

This is the Wasserstein counterpart of

when minimizes the left-hand side (LHS), which follows from the approximation

Rearranging (50) leads to

| (51) |

Now summing up the above we obtain

| (52) |

where is the number of steps. Applying both Cauchy-Schwarz and the triangular inequality yields

| (53) | |||||

Finally, by letting goes to we establish

which is a special case of (31) when . Indeed, when the potential is time-invariant, there is no work being done.

When is time-varying, the analysis is similar. The Fokker-Planck equation is

| (54) |

and the approximation (50) becomes

where . Following the same steps as in the time-invariant case, we conclude

| (55) |

Thus, the amount of work needed is always lower-bounded by the change of free energy plus the optimal transport cost between the marginal state distributions . Moreover, in view of (53), the equality holds when the density flow is the displacement interpolation between and . The optimal Hamiltonian is

where is the unique solution (under the constraint that ) to

which, by standard optimal mass transport theory [34], always exists.

Therefore, we conclude that Theorem 5 holds for general marginal distributions providing we are free to change the Hamiltonian in whatever way we like. The above analysis also reveals that, for general time-varying Hamiltonian, we can calculate the work using the solution to (54).

Theorem 13

| (56b) | |||||

We note that this is a generalization to Theorem 6 to general marginal distributions.

Remark 14

Finally, we note the counterpart of the above result for gradient dynamics

in a Euclidean space. In general,

In the special case when is independent of time,

VIII The Jarzynski equality

Different from the above results, the Jarzynski equality [1, 2] provides an alternative way to compare work and free energy. It reads,

| (57) |

under the assumption that the initial state is at equilibrium. Here is the difference of free energy at equilibrium, viz.,

Note that the Jarzynski equality implies by Jensen’s inequality. Indeed,

The relation then follows from the monotonicity of the exponential function.

We next recall a simple derivation of the Jarzynski equation. Let be the density of , and let

We have that

| (58) |

To see this, first rewrite (1) in the reverse direction utilizing Doob’s -transform,

| (59) |

This is quite standard. Here, is a reverse Wiener process, whose current increment is independent with the future. We deduce that

from which (58) follows. Combining (58) and the Fokker-Planck equation

we establish that satisfies

Finally, we claim that

with . To see this, we just need to notice

as well as

Clearly the boundary condition also holds as

IX Numerical examples

Consider a laser trap in one dimensional space whose strength and center location can both vary over time. The initial Hamiltonian and terminal Hamiltonian are set to be quadratic with parameters

respectively. The initial state distribution is assumed to be stationary, that is,

We further choose to be and to be to simplify the calculation. Our goal is to drive the state distribution to the stationary distribution corresponding to , which is

via adjusting the Hamiltonian . The optimal strategy is given in Section III if we want to achieve this distribution at . Plugging the above parameters into Theorem 2, we get the optimal strategy and density flow being

and

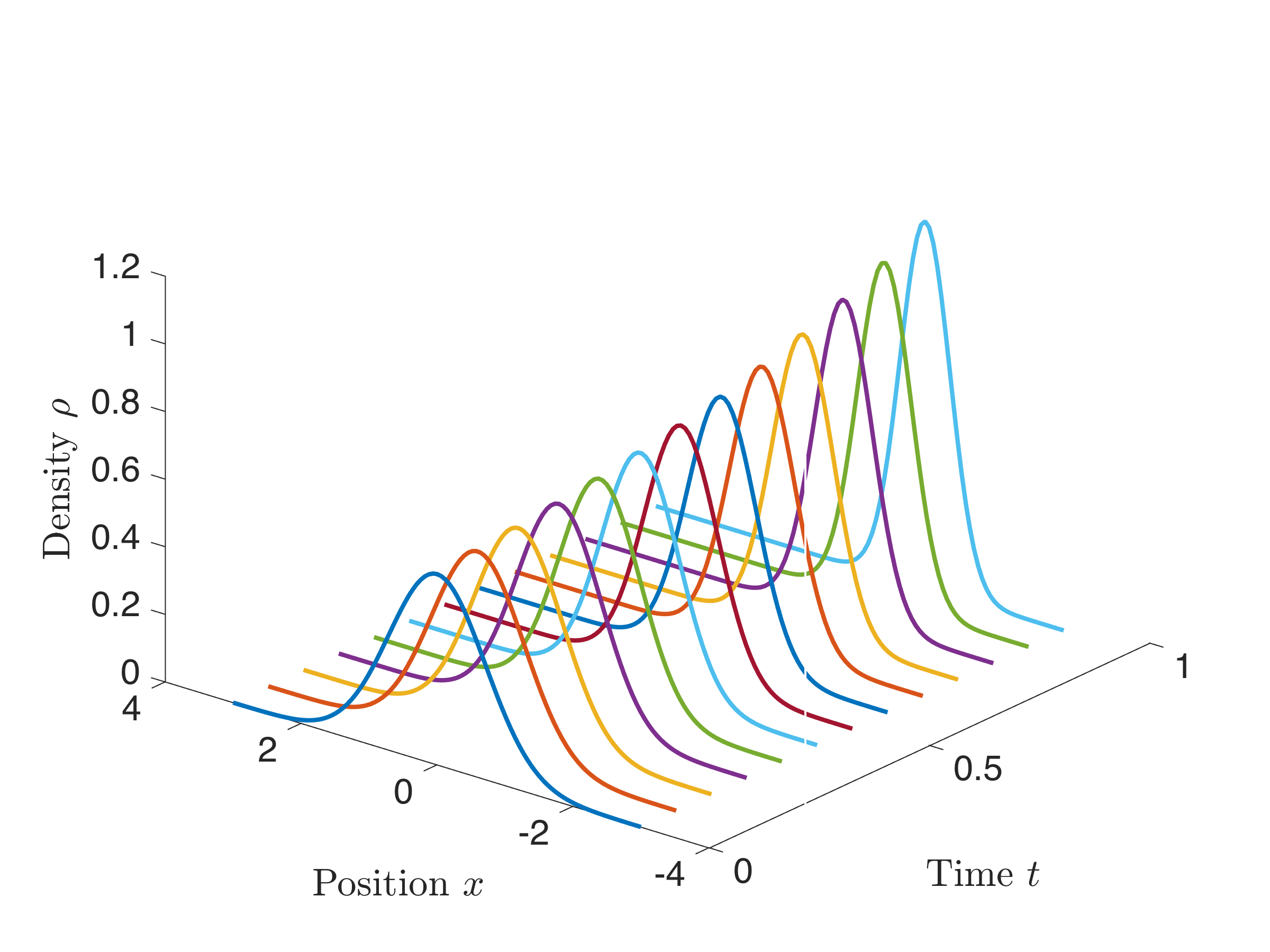

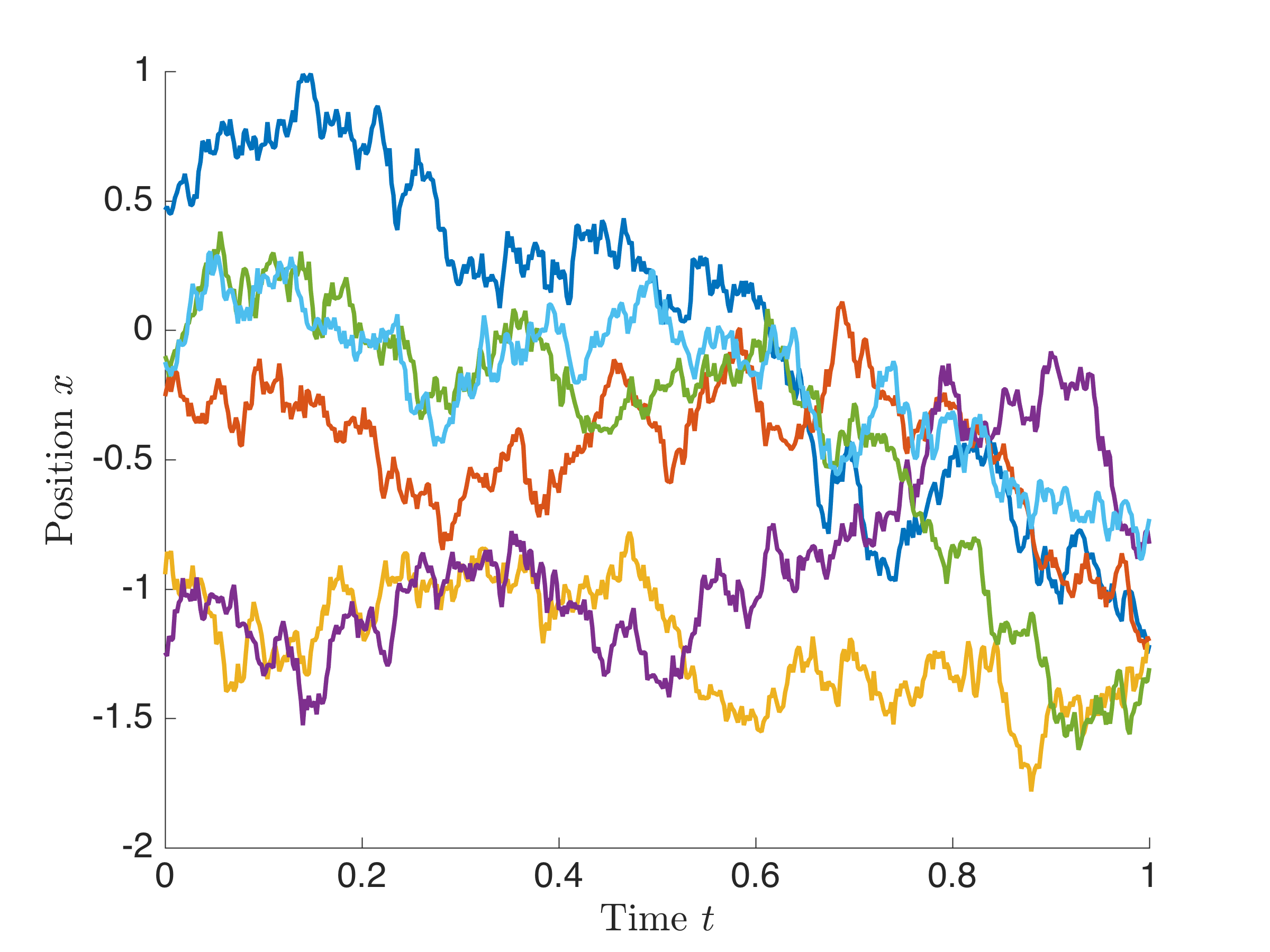

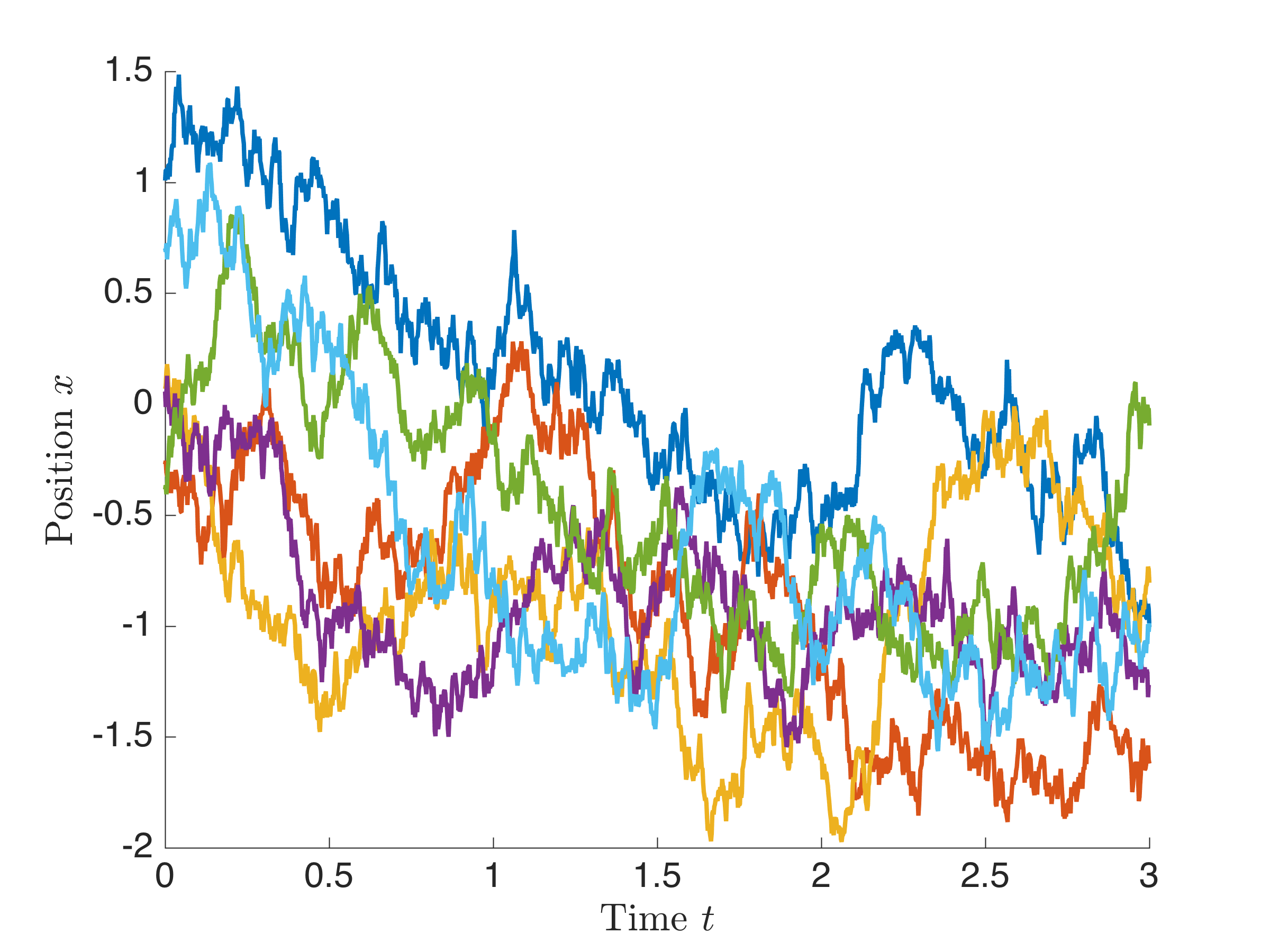

respectively for all . The minimum work is . The Hamiltonian jumps from to at the terminal time point , after which, both the Hamiltonian and state density remain time-invariant. Figure 1 depicts the evolution of the probability density of the state. Several typical sample paths are plotted in Figure 2. Clearly the sample paths are consistent with the density flow.

Next we move to another scenario discussed in Section VI where the constraint on the terminal state distribution doesn’t exist. Following the discussion in Section VI, we obtain the optimal terminal distribution at to be

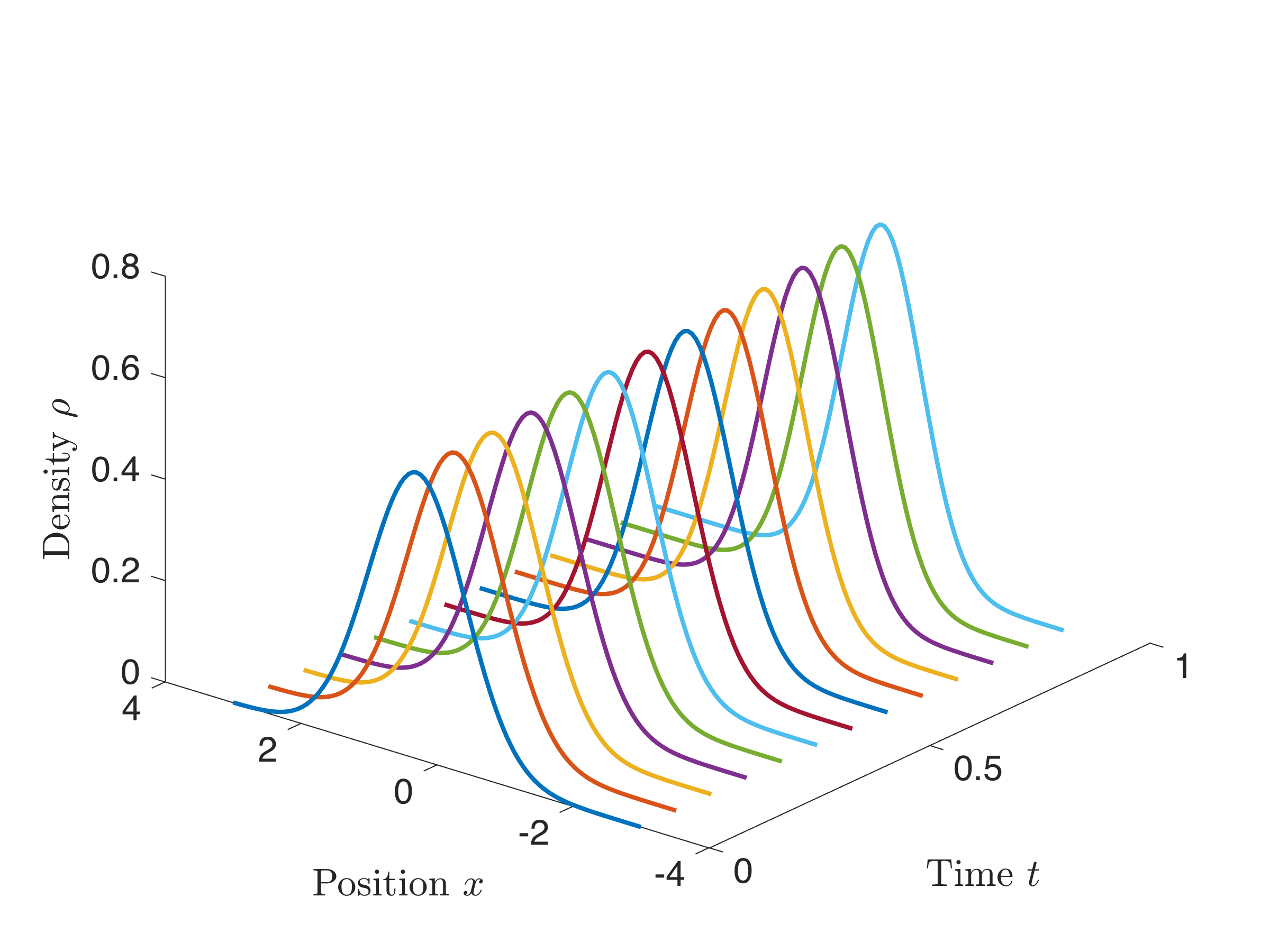

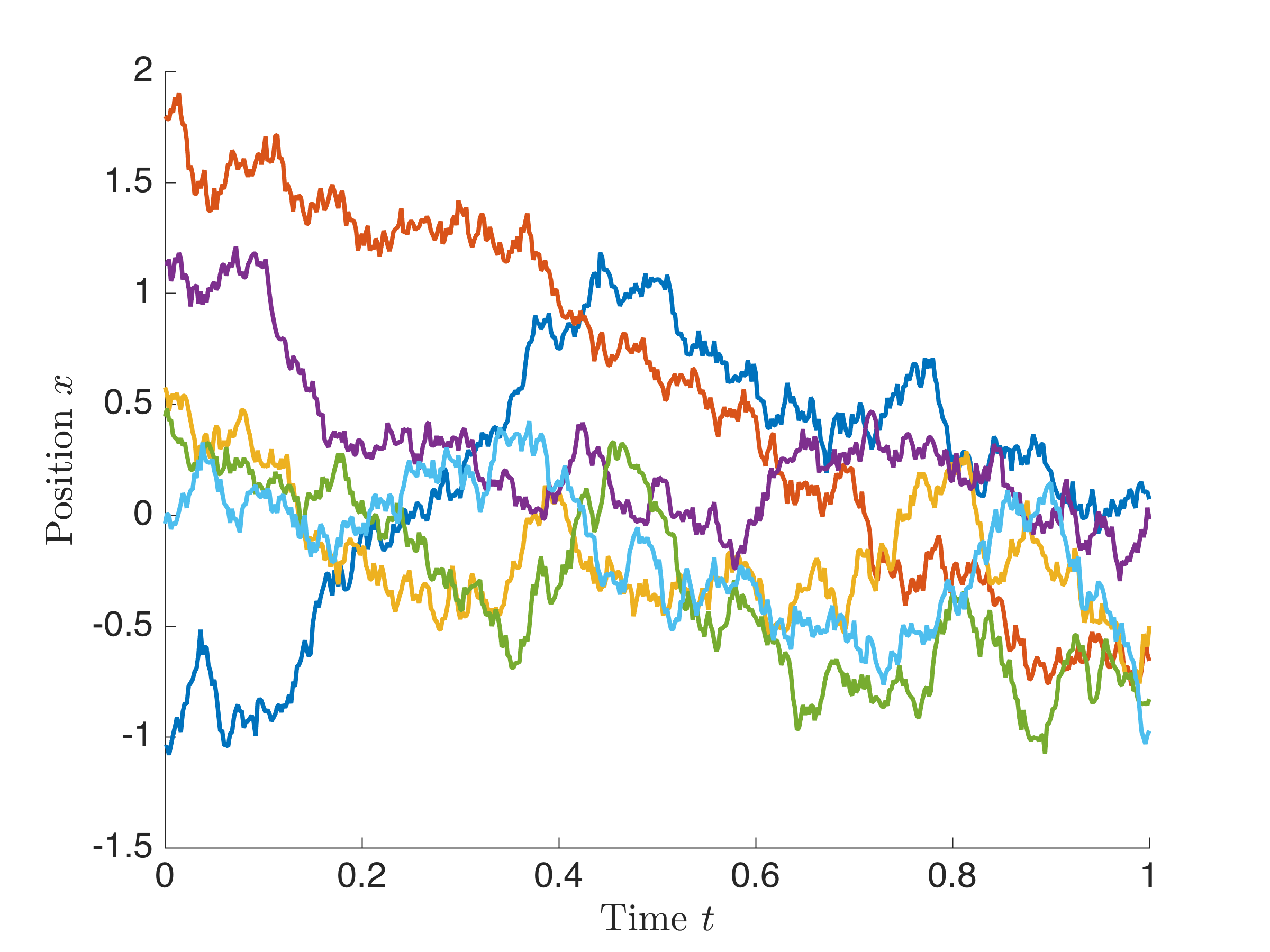

The corresponding optimal strategy and density flow can be again obtained using Theorem 2. The minimum work is , which is less than in the previous setting. In this case, the terminal distribution is not stationary with respect to anymore, therefore, the state density will vary after the terminal time . Eventually, due to fluctuation, the state density will converge to the stationary distribution . In Figure 3, we can see clearly that the evolution of the state distribution doesn’t match the terminal condition . This can also be seen from the sample paths in Figure 4. However, if we run the system long enough, then the state distribution will converge to the stationary one, as shown in Figure 5, due to fluctuation.

X Conclusion

We described the problem of controlling non-equilibrium thermodynamical systems with harmonic Hamiltonian, from a given initial state to a final state, by adjusting the parameter specifying the Hamiltonian in finite time. This led to some interesting connections to optimal mass transport theory, and gave a new twist to understanding the second law of thermodynamics building on the seminal results of Jarzynski and the recent advances in stochastic thermodynamics, e.g., see [12]. We expect that the theory will lead to insights in the case of potentials with several wells and to connections with the theory of large deviations and information theory with optimal mass transport [23, 35, 36]. We anticipate interesting connections to the celebrated Landauer principle [37], which provides a fundamental lower bound of the energy consumption to erase one bit of information. In recent years, many experiments have been performed aiming to achieve the bound [38, 39, 40]. This bound, however, theoretically can only be achieved through reversible processes. The constraint to erase a bit in finite time, unavoidably, introduces a gap. Our aim is to gain insights into such a gap using optimal transport theory and stochastic control.

Acknowledgements

This project was supported by AFOSR grants (FA9550-15-1-0045 and FA9550-17-1-0435), ARO grant (W911NF-17-1-049), grants from the National Center for Research Resources (P41-RR-013218) and the National Institute of Biomedical Imaging and Bioengineering (P41-EB-015902), NCI grant (1U24CA18092401A1), NIA grant (R01 AG053991), and a grant from the Breast Cancer Research Foundation.

References

- [1] C. Jarzynski, “Nonequilibrium equality for free energy differences,” Physical Review Letters, vol. 78, no. 14, p. 2690, 1997.

- [2] ——, “Equilibrium free-energy differences from nonequilibrium measurements: A master-equation approach,” Physical Review E, vol. 56, no. 5, p. 5018, 1997.

- [3] G. E. Crooks, “Entropy production fluctuation theorem and the nonequilibrium work relation for free energy differences,” Physical Review E, vol. 60, no. 3, p. 2721, 1999.

- [4] D. Carberry, J. C. Reid, G. Wang, E. M. Sevick, D. J. Searles, and D. J. Evans, “Fluctuations and irreversibility: An experimental demonstration of a second-law-like theorem using a colloidal particle held in an optical trap,” Physical Review Letters, vol. 92, no. 14, p. 140601, 2004.

- [5] U. Seifert, “Entropy production along a stochastic trajectory and an integral fluctuation theorem,” Physical Review Letters, vol. 95, no. 4, p. 040602, 2005.

- [6] T. Schmiedl and U. Seifert, “Optimal finite-time processes in stochastic thermodynamics,” Physical Review Letters, vol. 98, no. 2, p. 108301, 2007.

- [7] C. Jarzynski, “Comparison of far-from-equilibrium work relations,” Comptes Rendus Physique, vol. 8, no. 5, pp. 495–506, 2007.

- [8] R. Kawai, J. Parrondo, and C. Van den Broeck, “Dissipation: The phase-space perspective,” Physical Review Letters, vol. 98, no. 8, p. 080602, 2007.

- [9] K. Sekimoto, Stochastic Energetics. Springer, 2010, vol. 799.

- [10] C. Jarzynski, “Equalities and inequalities: irreversibility and the second law of thermodynamics at the nanoscale,” Annu. Rev. Condens. Matter Phys., vol. 2, no. 1, pp. 329–351, 2011.

- [11] E. Aurell, K. Gawȩdzki, C. Mejía-Monasterio, R. Mohayaee, and P. Muratore-Ginanneschi, “Refined second law of thermodynamics for fast random processes,” Journal of Statistical Physics, vol. 147, no. 3, pp. 487–505, 2012.

- [12] U. Seifert, “Stochastic thermodynamics, fluctuation theorems and molecular machines,” Reports on Progress in Physics, vol. 75, no. 12, p. 126001, 2012.

- [13] A. Hotz and R. E. Skelton, “Covariance control theory,” International Journal of Control, vol. 46, no. 1, pp. 13–32, 1987.

- [14] Y. Chen, T. T. Georgiou, and M. Pavon, “Optimal steering of a linear stochastic system to a final probability distribution, Part I,” IEEE Trans. on Automatic Control, vol. 61, no. 5, pp. 1158–1169, 2016.

- [15] ——, “Optimal steering of a linear stochastic system to a final probability distribution, Part II,” IEEE Trans. on Automatic Control, vol. 61, no. 5, pp. 1170–1180, 2016.

- [16] ——, “Optimal steering of a linear stochastic system to a final probability distribution, Part III,” IEEE Trans. on Automatic Control, to appear, 2018.

- [17] R. Marsland and J. England, “Far-from-equilibrium distribution from near-steady-state work fluctuations,” Phys. Rev. E, vol. 92, no. 5, 2015.

- [18] R. Sandhu, T. Georgiou, E. Reznik, L. Zhu, I. Kolesov, Y. Senbabaoglu, and A. Tannenbaum, “Graph curvature for differentiating cancer networks,” Scientific Reports, vol. 5, p. 12323, 2015.

- [19] A. Gomez-Marin, T. Schmiedl, and U. Seifert, “Optimal protocols for minimal work processes in underdamped stochastic thermodynamics,” The Journal of Chemical Physics, vol. 129, no. 2, p. 024114, 2008.

- [20] E. Aurell, C. Mejía-Monasterio, and P. Muratore-Ginanneschi, “Optimal protocols and optimal transport in stochastic thermodynamics,” Physical Review Letters, vol. 106, no. 25, p. 250601, 2011.

- [21] R. Jordan, D. Kinderlehrer, and F. Otto, “The variational formulation of the Fokker–Planck equation,” SIAM Journal on Mathematical Analysis, vol. 29, no. 1, pp. 1–17, 1998.

- [22] D. Owen, A First Course in the Mathematical Foundations of Thermodynamics. Springer, 1984.

- [23] J. M. Parrondo, J. M. Horowitz, and T. Sagawa, “Thermodynamics of information,” Nature Physics, vol. 11, no. 2, p. 131, 2015.

- [24] C. Villani, Topics in Optimal Transportation. American Mathematical Soc., 2003, no. 58.

- [25] F. Otto, “The geometry of dissipative evolution equations: the porous medium equation,” Communications in Partial Differential Equations, 2001.

- [26] C. Villani, Optimal Transport: Old and New. Springer, 2008, vol. 338.

- [27] R. J. McCann, “A convexity principle for interacting gases,” Advances in Mathematics, vol. 128, no. 1, pp. 153–179, 1997.

- [28] A. Takatsu, “Wasserstein geometry of gaussian measures,” Osaka Journal of Mathematics, vol. 48, no. 4, pp. 1005–1026, 2011.

- [29] D. Dowson and B. Landau, “The fréchet distance between multivariate normal distributions,” Journal of Multivariate Analysis, vol. 12, no. 3, pp. 450–455, 1982.

- [30] X. Jiang, Z.-Q. Luo, and T. T. Georgiou, “Geometric methods for spectral analysis,” IEEE Transactions on Signal Processing, vol. 60, no. 3, pp. 1064–1074, 2012.

- [31] R. Bhatia, Matrix analysis. Springer Science & Business Media, 2013, vol. 169.

- [32] Y. Chen, T. T. Georgiou, and M. Pavon, “Optimal transport over a linear dynamical system,” IEEE Transactions on Automatic Control, vol. 62, no. 5, pp. 2137–2152, 2017.

- [33] ——, “On the relation between optimal transport and Schrödinger bridges: A stochastic control viewpoint,” Journal of Optimization Theory and Applications, vol. 169, no. 2, pp. 671–691, 2016.

- [34] J. D. Benamou and Y. Brenier, “A computational fluid mechanics solution to the Monge-Kantorovich mass transfer problem,” Numerische Mathematik, vol. 84, no. 3, pp. 375–393, 2000.

- [35] C. Léonard, “From the Schrödinger problem to the Monge–Kantorovich problem,” Journal of Functional Analysis, vol. 262, no. 4, pp. 1879–1920, 2012.

- [36] ——, “A survey of the Schrödinger problem and some of its connections with optimal transport,” Dicrete Contin. Dyn. Syst. A, vol. 34, no. 4, pp. 1533–1574, 2014.

- [37] R. Landauer, “Irreversibility and heat generation in the computing process,” IBM Journal of Research and Development, vol. 5, no. 3, pp. 183–191, 1961.

- [38] A. Bérut, A. Arakelyan, A. Petrosyan, S. Ciliberto, R. Dillenschneider, and E. Lutz, “Experimental verification of landauer’s principle linking information and thermodynamics,” Nature, vol. 483, no. 7388, p. 187, 2012.

- [39] S. Talukdar, S. Bhaban, and M. V. Salapaka, “Memory erasure using time-multiplexed potentials,” Physical Review E, vol. 95, no. 6, p. 062121, 2017.

- [40] ——, “Energetics of erasing a single bit memory,” arXiv preprint arXiv:1609.02187, 2016.