Combined-BayesGOF-Jan2018

Bayesian Modeling via Goodness-of-fit

Subhadeep Mukhopadhyay, Douglas Fletcher

Temple University, Department of Statistical Science

Philadelphia, Pennsylvania, 19122, U.S.A.

Dedicated to 80th birthday anniversary of Brad Efron

Abstract

The two key issues of modern Bayesian statistics are: (i) establishing principled approach for distilling statistical prior that is consistent with the given data from an initial believable scientific prior; and (ii) development of a consolidated Bayes-frequentist data analysis workflow that is more effective than either of the two separately. In this paper, we propose the idea of “Bayes via goodness-of-fit” as a framework for exploring these fundamental questions, in a way that is general enough to embrace almost all of the familiar probability models. Several examples, spanning application areas such as clinical trials, metrology, insurance, medicine, and ecology show the unique benefit of this new point of view as a practical data science tool.

Keywords: Exploratory Bayes Modeling; Prior uncertainty modeling; Empirical Bayes.

1 Introduction

Bayesians and frequentists have long been ambivalent toward each other [efron1986isn, sims2010, stigler1982thomas]. The concept of “prior” remains the center of this 250 years old tug-of-war: frequentists view prior as a weakness that can hamper scientific objectivity and can corrupt the final statistical inference, whereas Bayesians view it as a strength to incorporate relevant domain-knowledge into the data analysis. The question naturally arises: how can we develop a consolidated Bayes-frequentist data analysis workflow [robbins1956, good1992bayes, rubin1984aos, efron2003robbins] that enjoys the best of both worlds? The objective of this paper is to develop one such modeling framework.

We observe samples from a known probability distribution , where the unobserved parameters are independent realizations from unknown . Given such a model, Bayesian inference typically aims at answering the following two questions:

-

•

MacroInference: How should we combine model parameters to come up with an overall, macro-level aggregated statistical behavior of ?

-

•

MicroInference: Given the observables , how should we simultaneously estimate individual micro-level parameters ?

Thanks to Bayes’ rule, answers to these questions are fairly straightforward and automatic once we have the observed data and a specific choice for . A common practice is to choose as the parametric conjugate prior , where the hyper-parameters are either selected based on an investigator’s expert input or estimated from the data (current/historical) when little prior information is available .

Motivating Questions. However, an applied Bayesian statistician may find it unsatisfactory to work with an initial believable prior at its face value, without being able to interrogate its credibility in the light of the observed data [dempster1975sub, Berger1994robust] as this choice unavoidably shapes his or her final inferences and decisions. A good statistical practice thus demands greater transparency to address this trust-deficit. What is needed is a justifiable class of prior distributions to answer the following pre-inferential modeling questions: Why should I believe your prior? How to check its appropriateness (self-diagnosis)? How to quantify and characterize the uncertainty of the a priori selected ? Can we use that information to “refine” the starting prior (auto-correction), which is to be used for subsequent inference? In the end, the question remains: how can we develop a systematic and principled approach to go from a scientific prior to a statistical prior that is consistent with the current data? A resolution of these questions is necessary to develop a “dependable and defensible” Bayesian data analysis workflow, which is the goal of the “Bayes via goodness-of-fit” technology.

Summary of Contributions. This paper provides some practical strategies for addressing these questions by introducing a general modeling framework, along with concrete guidelines for applied users. The major practical advantages of our proposal are: (i) computational ease (it does not require Markov chain Monte Carlo (MCMC), variational methods, or any other sophisticated computational techniques); (ii) simplicity and interpretability of the underlying theoretical framework which is general enough to include almost all commonly encountered models; and (iii) easy integration with mainframe Bayesian analysis that makes it readily applicable to a wide range of problems. The next section introduces a new class of nonparametric priors along with its role in exploratory graphical diagnostic and uncertainty quantification. The estimation theory, algorithm, and real data examples are discussed in Section 3. Consequences for inference are discussed in Section 4, which include methods of combining heterogeneous studies and a generalized nonparametric Stein-prediction formula that selectively borrows strength from ‘similar’ experiments in an automated manner. Section 4.2 describes a new theory of ‘learning from uncertain data,’ which is an important problem in many application fields including metrology, physics, and chemistry. Section 4.4 solves a long-standing puzzle of modern empirical Bayes, originally posed by Herbert Robbins [robbins1980]. We conclude the paper with some final remarks in Section 5. Connections with other Bayesian cultures are presented in the supplementary material to ensure the smooth flow of main ideas. Real-data Applications. To demonstrate the versatility of the proposed “Bayes via goodness-of-fit” data analysis scheme, we selected examples from a wide range of models including normal, Poisson, and Binomial distributions. The full catalog of datasets is presented in Supplementary Table 6. Notation. The notation and denote the density and distribution function of the starting prior, while and denote the density and distribution function of the unknown oracle prior. We will denote the conjugate prior with hyperparameters and by . Let be the space of square integrable functions with inner product . denotes th shifted orthonormal Legendre polynomials on . They form a complete orthonormal basis for . Whereas is the modified shifted Legendre polynomials of rank-G transform , which are basis of the Hilbert space . The composition of functions is denoted by the usual ‘’ sign.

2 The Model

Our model-building approach proceeds sequentially as follows: (i) it starts with a scientific (or empirical) parametric prior , (ii) inspects the adequacy and the remaining uncertainty of the elicited prior using a graphical exploratory tool, (iii) estimates the necessary “correction” for assumed by looking at the data, (iv) generates the final statistical estimate , and (v) executes macro and micro-level inference. We seek a method that can yield answers to all five of the phases using only a single algorithm.

2.1 New Family of Prior Densities

This section serves two purposes: it provides a universal class of prior density models, followed by its Fourier non-parametric representation in a specialized orthonormal basis.

Definition 1.

The Skew-G class of density models is given by

| (2.1) |

where for and consequently .

A few notes on the model specification:

-

•

It has a unique two-component structure that combines assumed parametric with the -function. The function can be viewed as a “correction” density to counter the possible misspecification bias of .

-

•

The density function can also be viewed as describing the “excess” uncertainty of the assumed . For that reason we call it the U-function.

- •

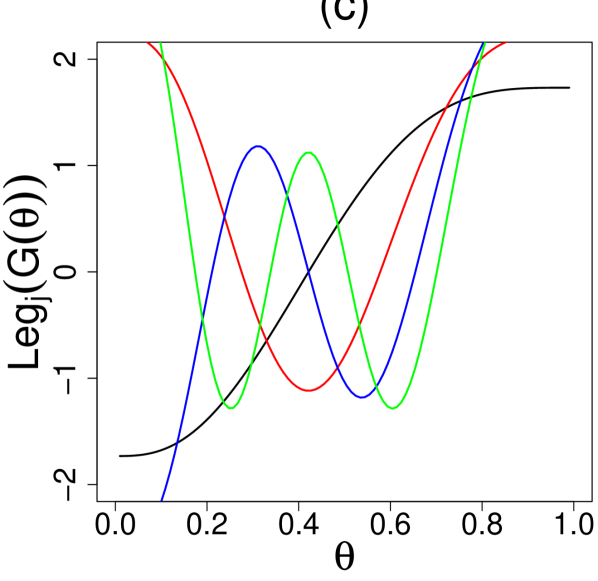

Since the square integrable lives in the Hilbert space , we can approximate it by projecting into the orthonormal basis satisfying . We choose to be , a member of the LP-class of rank-polynomials [mukhopadhyay2014lp]. The system possesses two attractive properties: they are polynomials of rank transform thus constitutes a robust basis, and they are orthonormal with respect to , for any arbitrary (continuous). This is not to be confused with standard Legendre polynomials , which are orthonormal with respect to measure. For more details, see Supplementary Appendix B. The above discussion paves the way for the following definition.

Definition 2.

distribution if it admits the following representation:

| (2.2) |

The LP-Fourier coefficients are the key parameters that help us to express mathematically the “gap” between a priori anticipated and the true prior . When all the expansion coefficients are zero, we automatically recover .

We will now spend a few words on the LP-DS() class of prior models:

-

•

When is a member of class of priors, the orthogonal LP-transform coefficients (2.2) satisfy

(2.3) Thus, given a random sample from , we could easily estimate the unknown LP-coefficients, and, thus, and , by computing the sample mean . But unfortunately, the ’s are unobserved. Section 3 describes an estimation strategy that can deal with the situation at hand. Before introducing this technique, however, we must acclimate the reader with the role played by the U-function for uncertainty quantification and characterization of the initial believable prior . That’s the objective of the next Section 2.2.

-

•

Under definition 2, we have . The truncation point in (2.2) reflects the concentration of permissible around a known . While this class of priors is rich enough to approximate any reasonable prior with the desired accuracy in the large- limit, one can easily exclude absurdly rough densities and focus on a neighborhood around the domain-knowledge-based by choosing not “too big.”

-

•

The motivations behind the name ‘DS-Prior’ are twofold. First, our formulation operationalizes I. J. Good’s ‘Successive Deepening’ idea [good1983EDA] for Bayesian data analysis:

A hypothesis is formulated, and, if it explains enough, it is judged to be probably approximately correct. The next stage is to try to improve it. The form that this approach often takes in EDA is to examine residuals for patterns, or to treat them as if they were original data (I. J. Good, 1983, p. 289).

Secondly, our prior has two components: A Scientific that encodes an expert’s knowledge and a Data-driven . That is to say that our framework embraces data and science, both, in a testable manner [gelman2017prior].

2.2 Exploratory Diagnostics and U-Function

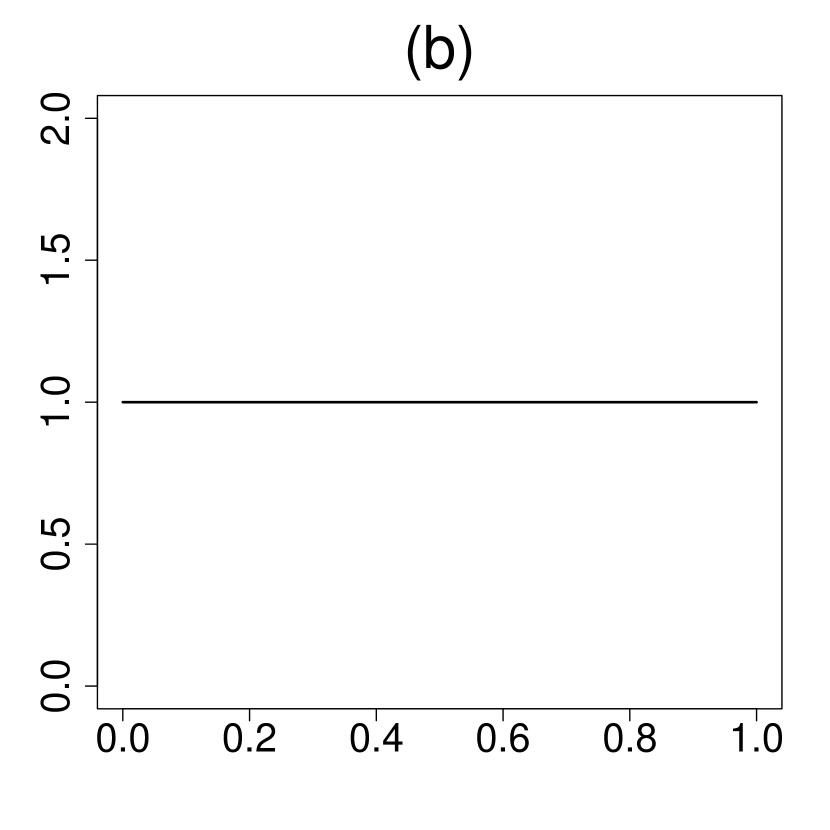

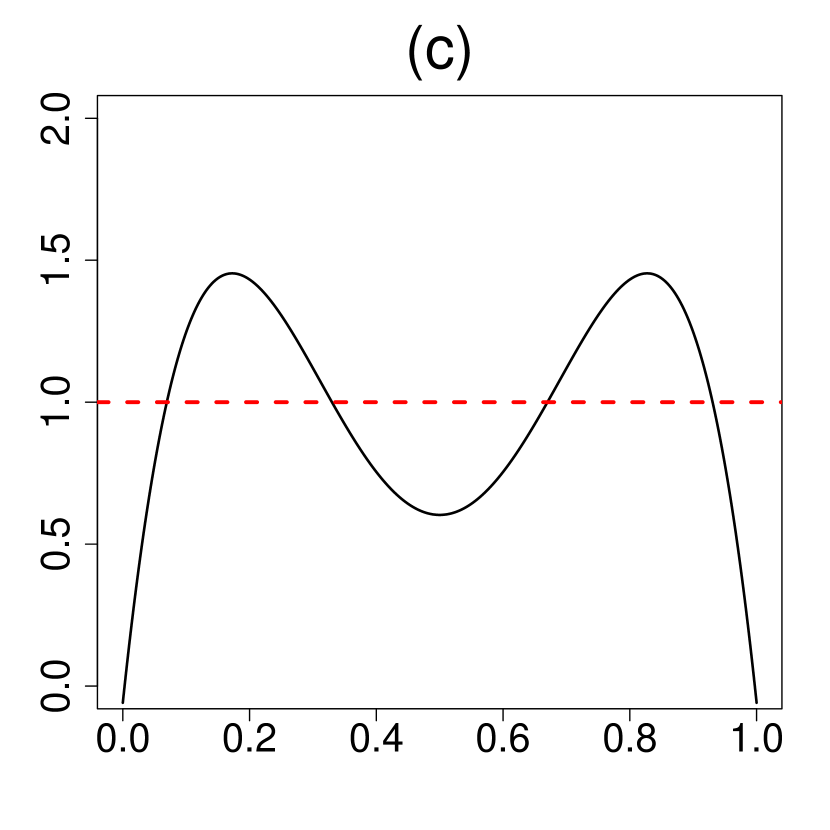

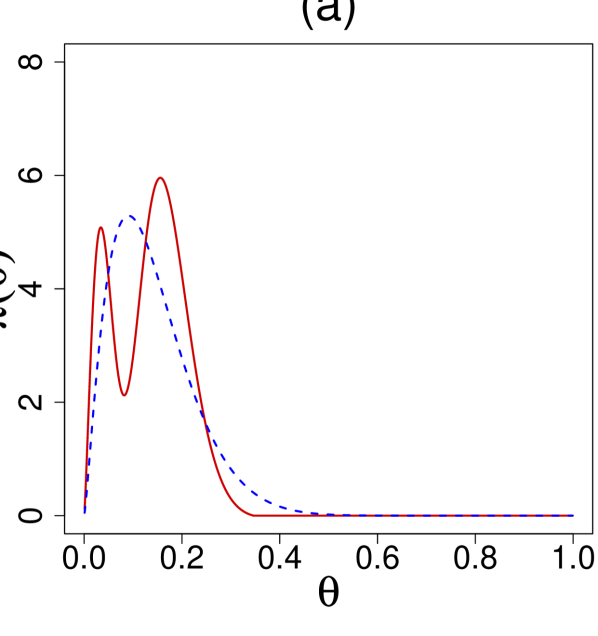

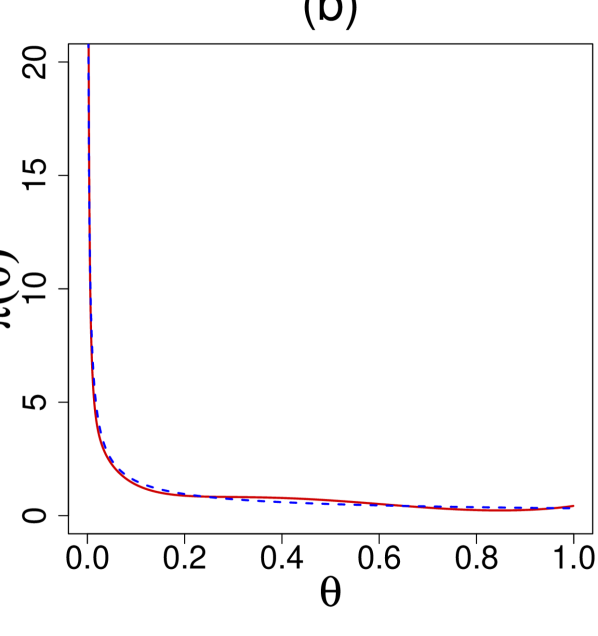

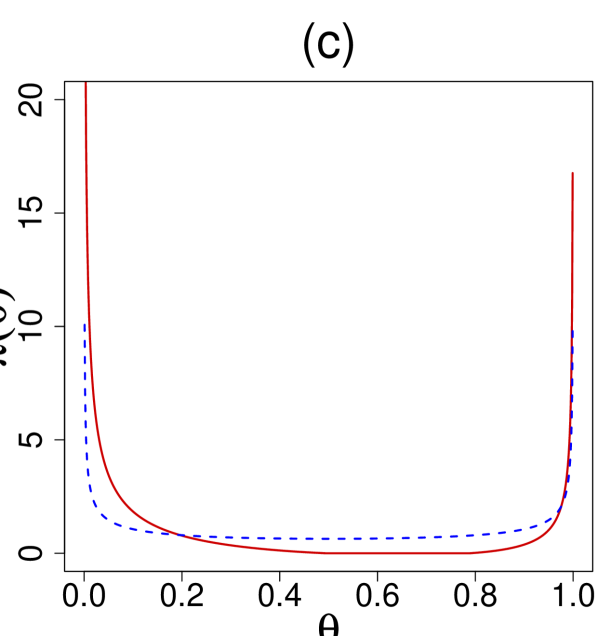

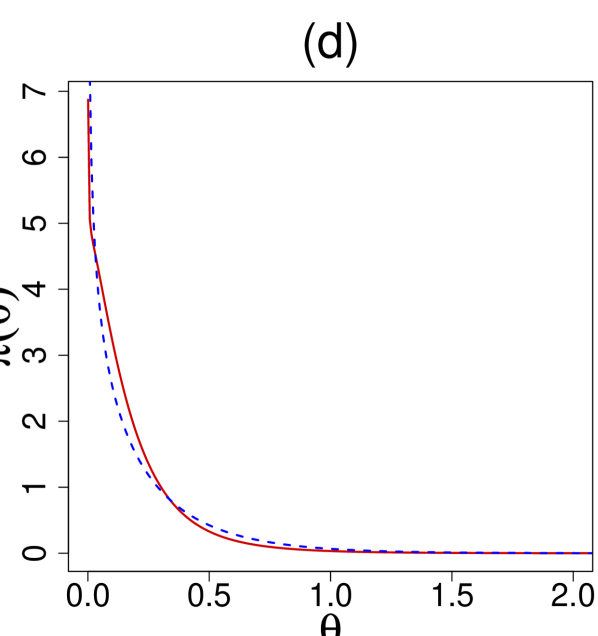

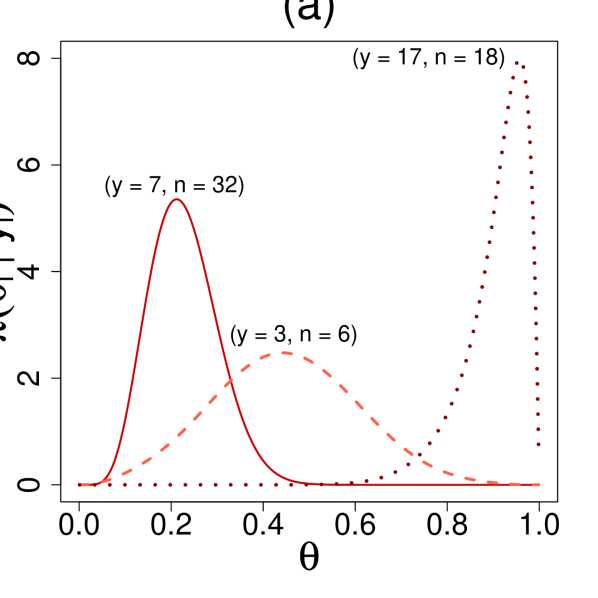

Is your data compatible with the pre-selected ? If yes, the job is done without getting into the arduous business of nonparametric estimation. If no, we can model the “gap” between the parametric and the true unknown prior , which is often far easier than modeling from scratch (hence, one can learn from small number of cases)! If the observed look very unexpected given , it is completely reasonable to question the sanctity of such a self-selected prior. Here we provide a formal nonparametric exploratory procedure to describe comprehensively the uncertainty about the choice of . Using the algorithm detailed in the next section, we estimate U-functions for four real data sets. Among them, the first three are binomial variate and the last one normal. The results are shown in Fig. 1.

-

•

The rat tumor data [gelman2013bayesian] consists of observations of endometrial stromal polyp incidence in groups of female rats. For each group, is the number of rats with polyps and is the total number of rats in the experiment.

-

•

The terbinafine data [young2008pooling] comprise studies, which investigate the proportion of patients whose treatment terminated early due to some adverse effect of an oral anti-fungal agent: is the number of terminated treatments and is the total number of patients in the experiment.

-

•

The rolling tacks [beckett1994spectral] data involve flipping a common thumbtack times. It consists of pairs, , where represents the number of times the thumbtack landed point up.

-

•

The ulcer data consist of forty randomized trials of a surgical treatment for stomach ulcers conducted between 1980 and 1989 [sacks1990endoscopic, efron1996empirical]. Each of the trials has an estimated log-odds ratio that measures the rate of occurrence of recurrent bleeding given the surgical treatment.

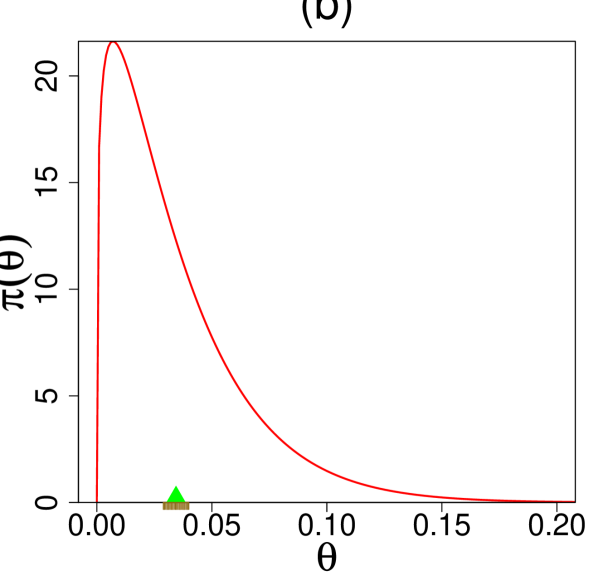

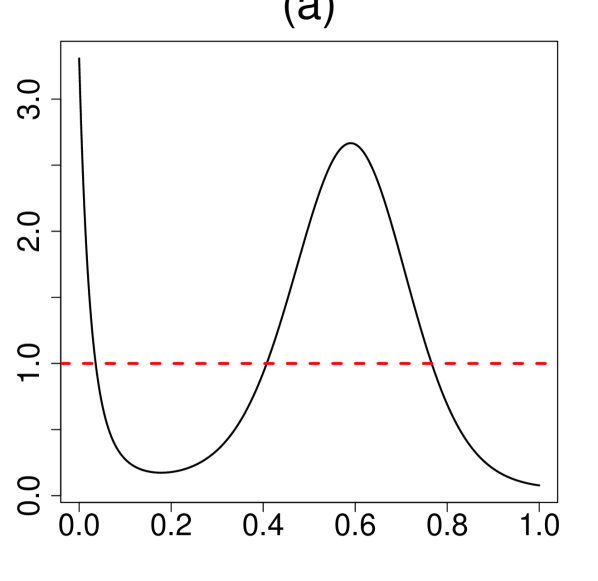

Throughout, we have used the maximum likelihood estimates (MLE) for estimating the initial starting value of the hyperparameters. However, one can use any other reasonable choice, which may involve expert’s judgment. What is important to note is the shape of the ; more specifically, its departure from uniformity, indicates the assumed conjugate prior needs a ‘repair’ to resolve the prior-data conflict. For example, the flat shape of the estimated in Fig. 1(b) indicates that our initial selection of is appropriate for the terbinafine and ulcer data. Therefore, one can proceed in turning the “Bayesian crank” with confidence using the parametric beta and normal prior respectively.

In contrast, Figs. 1(a,c) provide a strong warning in using for the rat tumor and the rolling tacks experiments. The smooth estimated U-functions expose the nature of the discrepancy that exists between and the observed data by having an “extra” mode. Clearly, the answer does not lie in choosing a different as this cannot rectify the missing bimodality. This brings us to an important point: the full Bayesian analysis, by assigning hyperprior distribution on and , is not always a fail-safe strategy and should be practiced with caution (not in a blind mechanical way). The bottom line is uncertainty in the prior probability model uncertainty in . A foolproof prior uncertainty model, thus, has to allow ignorance in terms of the functional shape around . The foregoing discussion motivates the following entropy-like measure of uncertainty.

Definition 3.

The statistic for uncertainty quantification is defined as follows:

| (2.4) |

The motivation behind this definition comes from applying Parseval’s identity in (2.2): . Thus, the proposed measure captures the departure of the U-function from uniformity. The following result connects our statistic with relative entropy.

Theorem 1.

The uncertainty quantification statistic satisfies the following relation:

| (2.5) |

where is the Kullback–Leibler (KL) divergence between the true prior and its parametric approximate .

Proof.

Express KL-information divergence using U-functions by substituting :

| (2.6) |

Complete the proof by approximating in (2.6) via Taylor series . ∎

We conclude this section with a few additional remarks:

-

•

Our exploratory uncertainty diagnostic tool encourages “interactive” data analysis that is similar in spirit to Gelman et al.[gelman1996PDC]. Subject-matter experts can use this tool to “play” with different hyperparameter choices in order to filter out the reasonable ones. This functionality might be especially valuable when multiple expert opinions are available.

-

•

When shows evidence of the prior-data conflict, the question remains: what to do next? It is not enough to check the adequacy without informing the user an explanation for the misfit or what is the “deeper” structure that is missing in the starting parametric prior. Fortunately, our model suggests a simple, yet formal, guideline for upgrading: , where the shape of captures the patterns which were not a priori anticipated. Hence our formalism simultaneously addresses the problem of uncertainty quantification and the subsequent model synthesis.

3 Estimation Method

3.1 Theory

In this Section, we lay out the key theoretical results that we use for designing our algorithm. Before deriving the general expressions under the LP- model, it is helpful to start by recalling the results for the basic conjugate model, i.e., and for . Table 1 provides the marginal and the posterior distribution for four commonly encountered distributions, with the Bayes estimate of being denoted as . The subscript ‘’ in these expressions underscores the fact that they are calculated for the conjugate -model.

| Family | Conjugate -prior | Marginal [] | Posterior [] |

|---|---|---|---|

Next, we seek to extend these parametric results to LP-nonparametric setup in a systematic way. Especially, without deriving analytical expressions for each case separately, we want to establish a more general representation theory that is valid for all of the above and, in fact, extends to any conjugate pairs, explicating the underlying unity of our formulation.

Theorem 2.

Consider the following model:

where is a member of family (2.2), being the associated conjugate prior. Under this framework, the following holds:

-

(a)

The marginal distribution of is given by

(3.1) where .

-

(b)

A closed-form expression for the posterior distribution of given is

(3.2) -

(c)

For any general random variable , the Bayes conditional mean estimator can be expressed as follows:

(3.3)

Proof.

The marginal distribution for -nonparametric model can be represented as:

Expanding the U-function in the LP-bases (2.2) yields

| (3.4) |

The next step is to recognize that

| (3.5) |

Substituting (3.5) in the second term of (3.4) leads to

| (3.6) |

Complete the proof of part (a) by replacing (3.6) into (3.4). For part (b) of posterior distribution calculation we have

| (3.7) |

Combine (3.1) and (3.5) to verify that

| (3.8) |

Finish the proof of part (b) by replacing (3.8) into (3.7). Part (c) is straightforward as

which is same as

3.2 Algorithm

The critical parameters of our model are the LP-Fourier coefficients, which, as is evident from (2.3), could be estimated simply by their empirical counterpart . But as we pointed out earlier, are unobservable. How can we then estimate those parameters? While the ’s are unseen, it is interesting to note that they have left their footprints in the observables with distribution . Following the spirit of the EM-algorithm, an obvious proxy for would be its posterior mean , which also naturally arises in the expression (3.1). This leads to the following ‘ghost’ LP-estimates:

| (3.9) |

satisfying , by virtue of the law of iterated expectations. These estimates can then be refined via iterations. Type-II Method of Moments: Estimation of LP-Coefficients in Step 0. Input: Data and . Choice of and : based on expert’s knowledge, otherwise, we use MLE empirical estimate as our default starting choice. Step 1. Initialize: for . For iteration , perform steps (2-3) until convergence: .

Step 2. Compute by plugging into (3.3), where . Step 3. Determine the ‘ghost’ LP-estimates:

Step 4. Return the final estimated LP-coefficients of model together with and .

We conclude this section with a few remarks on the algorithm:

-

•

Taking inspiration from I. J. Good’s type II maximum likelihood nomenclature [good1983book], we call our algorithm Type-II Method of Moments (MOM), whose computation is remarkably tractable and does not require any numerical optimization routine.

-

•

To enhance the results, we smooth the output of MOM-II algorithm as follows: determine significantly non-zero LP-coefficients via Schwartz’s BIC-based smoothing. Arrange ’s in a decreasing magnitude and choose that maximizes

See Supplementary Appendix D for more details. Furthermore, Supplementary Appendix I discusses how MOM-II Bayes algorithm can be adapted to yield LP-maximum entropy prior density estimate [lpmode2017].

3.3 Results

In addition to the rat tumor data (cf. Section 2.2), here we introduce and analyze three additional datasets: two binomial and one Poissonian example.

-

•

The surgical node data [efron2014bayes] involves number of malignant lymph nodes removed during intestinal surgery. Each of the patients underwent surgery for cancer, during which surgeons removed surrounding lymph nodes for testing. Each patient has a pair of data (), where represents the total nodes removed from patient and are the number of malignant nodes among them.

-

•

The Navy shipyard data [martz1974empirical] consists of samples of the number of defects found in lots of welding material.

-

•

The insurance data [efron2016computer], shown in Table 4, provides a single year of claims data for an automobile insurance company in Europe. The counts represent the total number of people who had claims in a single year.

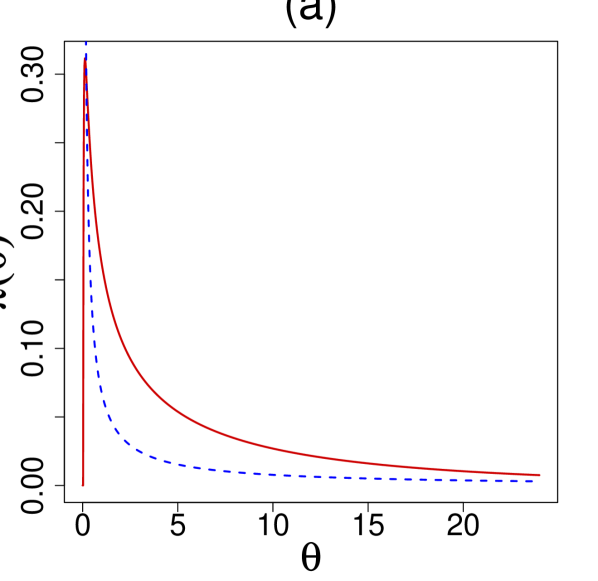

Figure 2 displays the estimated LP- priors along with the default parametric (empirical Bayes) counterparts. The estimated LP-Fourier coefficients together with the choices of hyperparameters are summarized below:

-

(a)

Rat tumor data, is the beta distribution with MLE , :

(3.10) -

(b)

Surgical node data, is the beta distribution with MLE , :

(3.11) -

(c)

Navy shipyard data, is the Jeffreys prior with , :

(3.12) -

(d)

Insurance data, is the gamma distribution with MLE and :

(3.13)

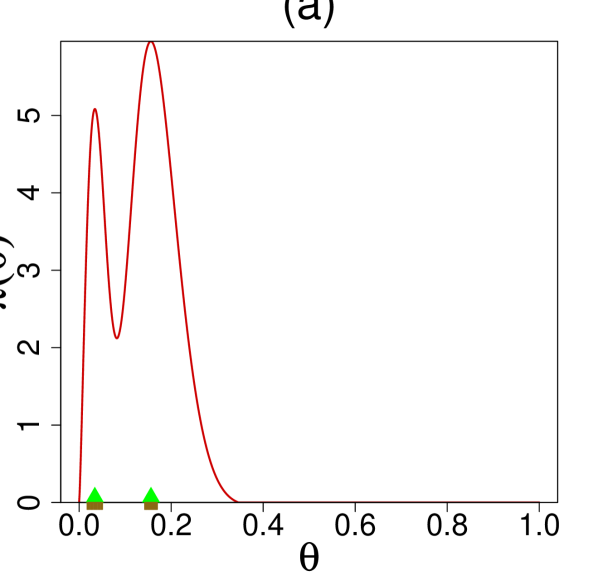

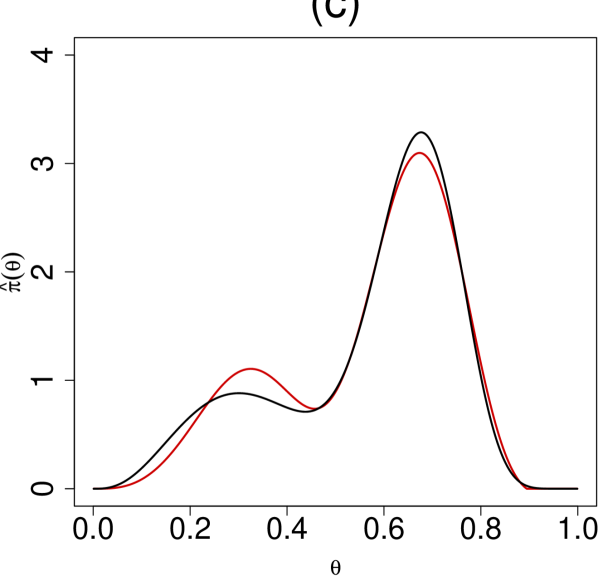

The rat tumor data shows a prominent bimodal shape, which should not come as a surprise in light of Fig. 1(a). For the surgical data, DS-prior puts excess mass around , which concurs with the findings of Efron [efron2014bayes, Sec 4.2]. In the case of the Navy shipyard data, our analysis corrects the starting “U” shaped Jeffreys prior to make it asymmetric with an extended peak at . This is quite justifiable looking at the proportions in the given data: . Finally, for the insurance data, the starting gamma prior requires a second-order (dispersion parameter) correction to yield a bona-fide (3.13), which makes it slightly wider in the middle with sharper peak and tail.

4 Inference

4.1 MacroInference

A single study hardly provides adequate evidence for a definitive conclusion due to the limited sample size. Thus, often the scientific interest lies in combining several related but (possibly) heterogeneous studies to come up with an overall macro-level inference that is more accurate and precise than the individual studies. This type of inference is a routine exercise in clinical trials and public policy research.

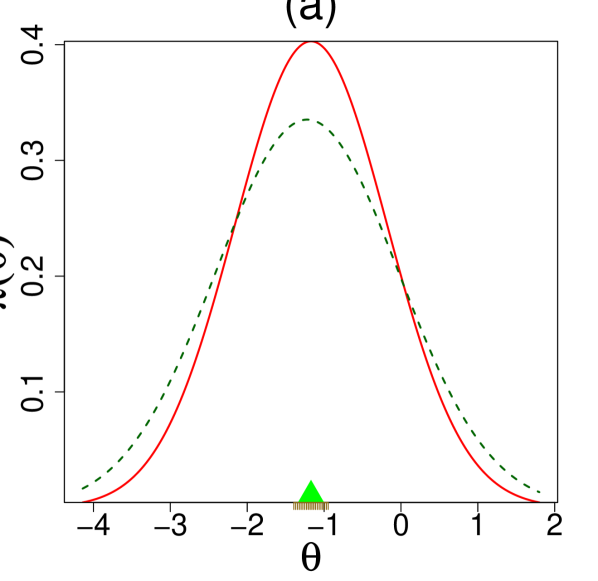

Terbinafine data analysis. For the terbinafine data, the aim is to combine treatment arms with varying event rates and produce a pooled proportion of patients who withdrew from the study because of the adverse effects of oral anti-fungal agents. Recall that our U-function diagnostic in Fig. 1(b) indicated the parametric beta-binomial model with MLE estimates and as a justifiable choice for this data. Thus the adverse event probabilities across studies can be summarized by the prior mean . We apply parametric bootstrap using -sampler (see Supplementary Appendix C) with to compute the standard error (SE): , highlighted in the Fig. 3(b). If one assumes a single binomial distribution for all the groups (i.e., under homogeneity), then the ‘naive’ average would lead to an overoptimistic biased estimate . In this example, heterogeneity arises due to overdispersion among the exchangeable studies. But there could be other ways too. An example is given in the following case study.

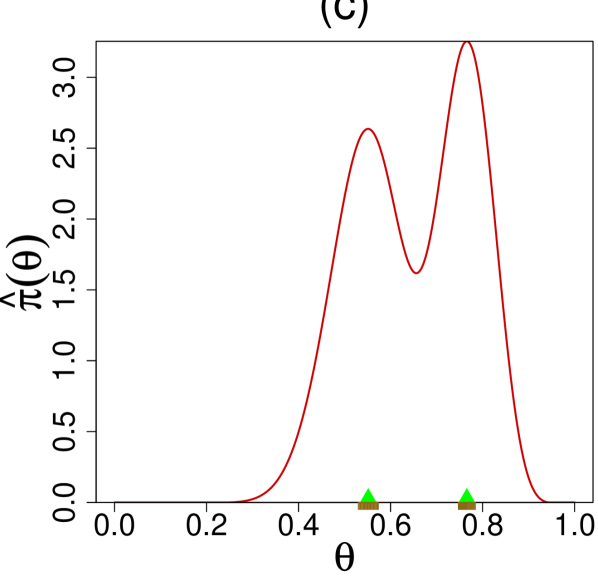

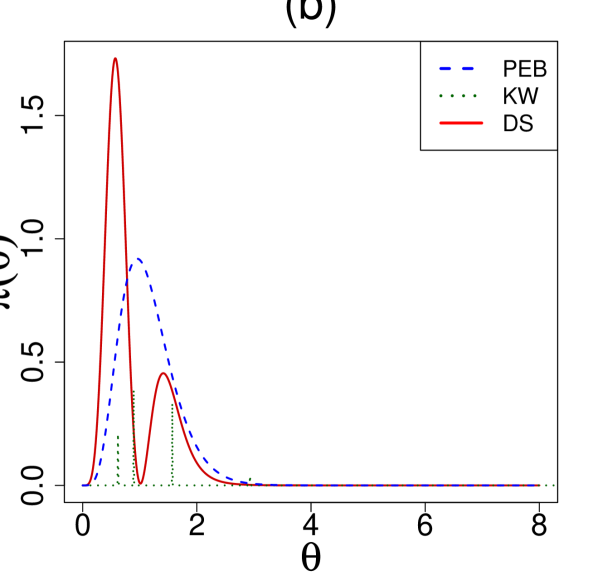

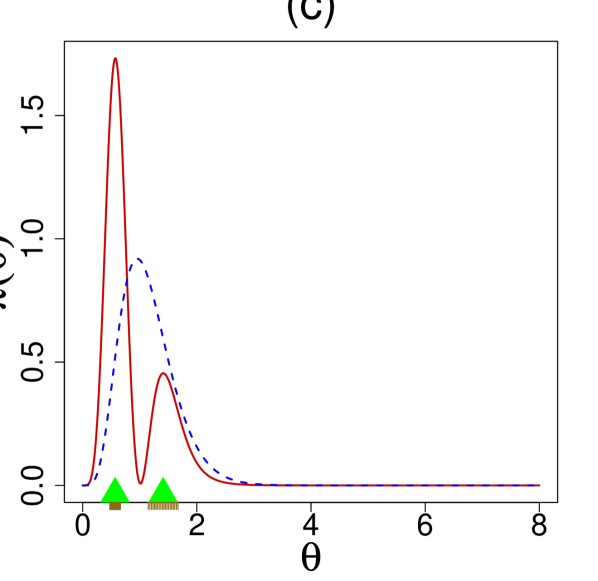

Rat tumor and rolling tacks data analysis. Can we always extract a “single” overall number to aptly describe parallel studies? Not true, in general. In order to appreciate this, let us look at Figs. 3 (a,c), which depict the estimated DS-prior for the rat tumor and rolling tacks data. We highlight two key observations:

1. Mixed population. The bimodality indicates the existence of two distinct groups of ’s. We call this “structured heterogeneity,” which is in between two extremes: homogeneity and complete heterogeneity (where there is no similarity between the ’s whatsoever). The presence of two clusters for the rolling tacks data was previously detected by Jun Liu [liu1996nonparametric]. The author further noted, “Clearly, this feature is unexpected and cannot be revealed by a regular parametric hierarchical analysis using the Beta-binomial priors.” One plausible explanation for this two-group structure was attributed to the fact that the tack data were produced by two persons with some systematic difference in their flipping. On the other hand, the bimodal shape of the rat example was not previously anticipated [tarone1982use, dempster1983combining, gelman2013bayesian].

The resulting two groups of rat tumor experiments are enumerated in the Table 2. Although we do not have the necessary biomedical background to scientifically justify this new discovery, we are aware that potentially numerous factors (e.g., experimental design, underlying conditions, selection of specific groups of female rats) may contribute to creating this systemic variation.

| Group | Studies |

|---|---|

| 1 | (0,20), (0,20), (0,20), (0,20), (0,20), (0,20), (0,20), (0,19), (0,19), (0,19), (0,19) |

| (0,18), (0,18), (0,17), (1,20), (1,20), (1,20), (1,20), (1,19), (1,19), (1,18), (1,18) | |

| 2 | (3,27), (2,25), (2,24), (2,23), (2,20), (2,20), (2,20), (2,20), (2,20), (2,20), (1,10) |

| (5,49), (2,19), (5,46), (2,17), (7,49), (7,47), (3,20), (3,20), (2,13), (9,48), (10,50) | |

| (4,20), (4,20), (4,20), (4,20), (4,20), (4,20), (4,20), (10,48), (4,19), (4,19), (4,19) | |

| (5,22), (11,46), (12,49), (5,20), (5,20), (6,23), (5,19), (6,22), (6,20), (6,20), (6,20) | |

| (16,52), (15,46), (15,47), (9,24) |

2. From single mean to multiple modes. An attempt to combine the two subpopulations using a single prior mean (as carried out for the terbinafine example) would result in overestimating one group and underestimating another. We prefer modes of , along with their SEs, as a good representative summary, which can be easily computed by the nonparametric smooth bootstrap via sampler.

Learning from big heterogeneous studies is one of the most important yet unsettled matters of modern macroinference [cox1988, efron1996empirical]. Our key insight is the realization that the ‘science of combining’ critically depends on the shape of the estimated prior. One interesting and commonly encountered case is multimodal structure of the learned prior. In such situations, instead of the prior-mean summary, we recommend group-specific modes. Our algorithm is also capable of finding data-driven clusters of the partially exchangeable studies in a fully automated manner.

4.2 Learning From Uncertain Data

An important problem of measurement science that routinely appears in metrology, chemistry, physics, biology, and engineering can be stated as follows: measurements are made by different laboratories in the form of along with their estimated standard errors . Given this uncertain data, a fundamental problem of interest is inference concerning: (i) estimation of the consensus value of the measurand, and (ii) evaluation of the associated uncertainty. The data in Table 3 are an example of such an inter-laboratory study involving measurements for the level of arsenic in oyster tissue. The study was part of the National Oceanic and Atmospheric Administration’s National Status and Trends Program Ninth Round Intercomparison Exercise [willie1995ninth].

| Laboratory | 1 | 2 | 3 | 4 | 5 | 25 | 26 | 27 | 28 | |

|---|---|---|---|---|---|---|---|---|---|---|

| Measurement () | 9.78 | 10.18 | 10.35 | 11.60 | 12.01 | 14.70 | 15.00 | 15.10 | 15.50 | |

| Uncertainty () | 0.30 | 0.46 | 0.07 | 0.78 | 2.62 | 0.30 | 1.00 | 0.20 | 1.60 |

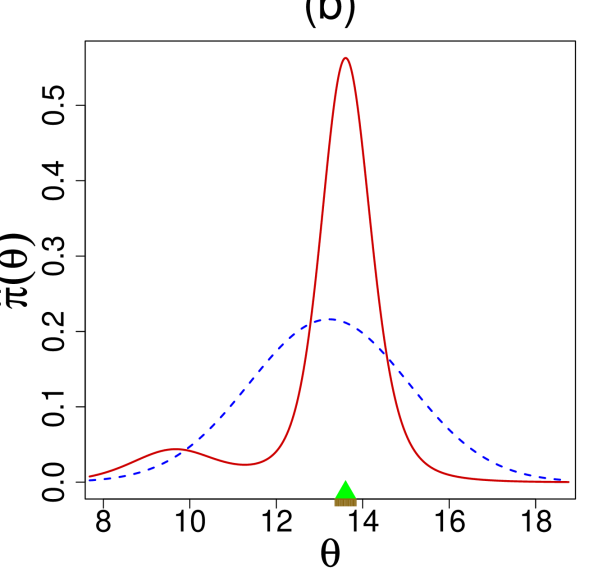

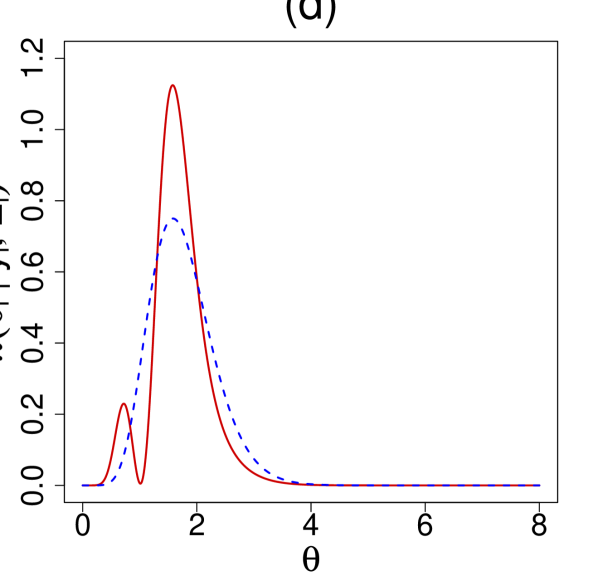

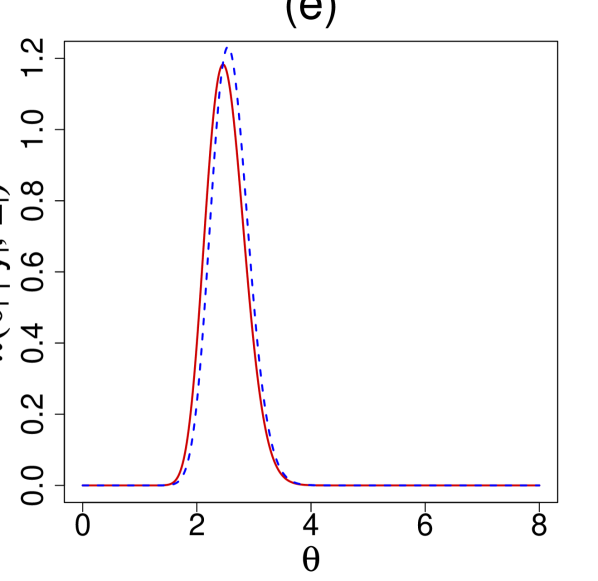

Arsenic data analysis. We start with the DS-measurement model: and with being . The shape of the estimated U-function in Fig. 4(a) indicates that the pre-selected prior is clearly unacceptable for arsenic data, thereby disqualifying the classical Gaussian random effects model [rukhin1998]. The DS-corrected shows some interesting asymmetric pattern with two-bumps. The left-mode represents measurements from three laboratories that are unlike the majority. The result of our macro-inference is shown in Fig. 4(b), which delivers the consensus value . This is clearly far more resistant to fairly extreme low measurements and surprisingly, also more accurate when compared to the parametric EB estimate . Most importantly, our scheme provides an automated solution to the fundamental problem of which (as well as how) measurements from the participating laboratories should be combined to form a best consensus value. Possolo [possolo2013five] fits a Bayesian hierarchical model with prior as Student’s , where the degrees of freedom was also treated as a random variable over some arbitrary range . Although a heavy-tailed Student’s t-distribution is a good choice to ‘robustify’ the analysis, it fails to capture the inherent asymmetry and the finer modal structure on the left. Distinguishing long-tail from bimodality is an important problem of applied statistics by itself. To summarize, there are several attractive features of our general approach: (i) it adapts to the structure of the data, yet (ii) allows the use of expert opinion to go from knowledge-based prior to statistical prior; (iii) if multiple expert opinions are available, one can also use the U-diagnostic for reconciliation–exploratory uncertainty assessment; (iv) it avoids the questionable exercise of detecting and discarding apparently unusual measurements [possolo2009lab], and finally (v) our theory is still applicable for very small number of parallel cases (cf. Fig. 2(c)), a situation which is not uncommon in inter-laboratory studies.

4.3 MicroInference

The objective of microinference is to estimate a specific microlevel given . Consider the rat tumor example where, along with earlier studies, we have an additional current experimental data, that shows out of rats developed tumors. How can we estimate the probability of a tumor for this new clinical study? There could be at least three ways to answer this question:

-

•

Frequentist MLE estimate: An obvious estimate would be the sample proportion . This operates in an isolated manner, completely ignoring the additional historical information of studies.

-

•

Parametric empirical Bayes estimate: It is reasonable to expect that the historical data from earlier studies may be related to the current st study, thus borrowing information can result in improved estimator of . Bayes posterior mean estimate operationalizes this heuristic, which in the Binomial case takes the following form:

(4.1) This is famously known as Stein’s shrinkage formula [stein1956, efron1975], as it pulls the sample proportions toward the overall mean of the prior . For smaller () studies, shrinkage intensity is higher, which allows them to learn from other experiments.

-

•

Nonparametric Elastic-Bayes estimate: Is it a wise strategy to shrink all ’s toward the grand mean ? Interestingly, this shrinking point is near the valley between the twin-peaks of the rat tumor prior density estimate (verify from Fig. 3(a)) and therefore may not represent a preferred location. Then, where to shrink? Ideally, we want to learn only from the relevant subset of the full dataset–selective shrinkage, e.g., for rat data, it would be the group 2 of Table 2. This brings us to the question: how to rectify the parametric empirical Bayes estimate ? The formula (3.3) gives us the required (nonlinear) adjusting factor:

(4.2) dictating the magnitude and direction of shrinkage in a completely data-driven manner via LP-Fourier coefficients. Note that when , i.e., all the are zero, (4.2) reproduces the parametric . Due to its flexibility and adaptability, we call this the Elastic-Bayes estimate. This can be considered as a nonparametric class of shrinkage estimators that starts with the classical Stein’s formula and rectifies it by looking at the data.

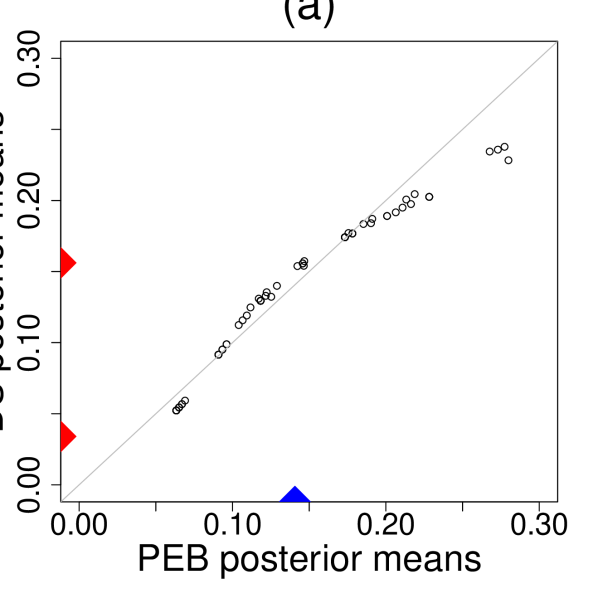

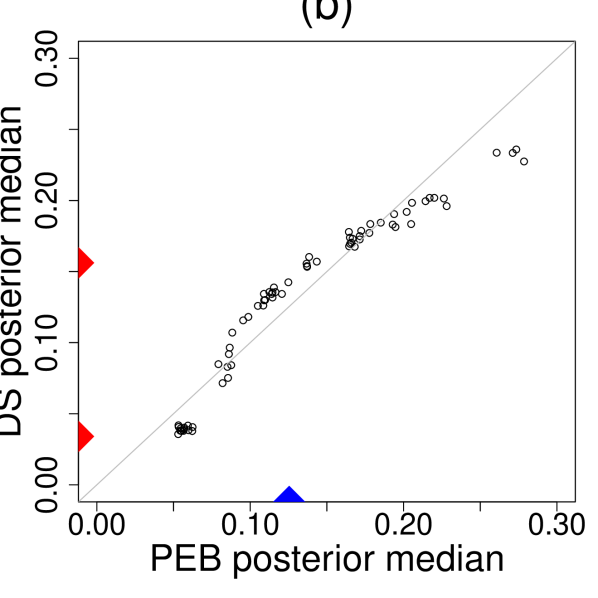

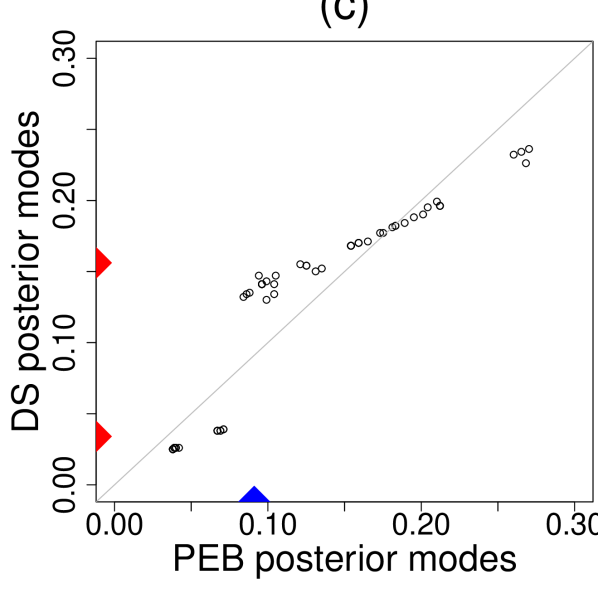

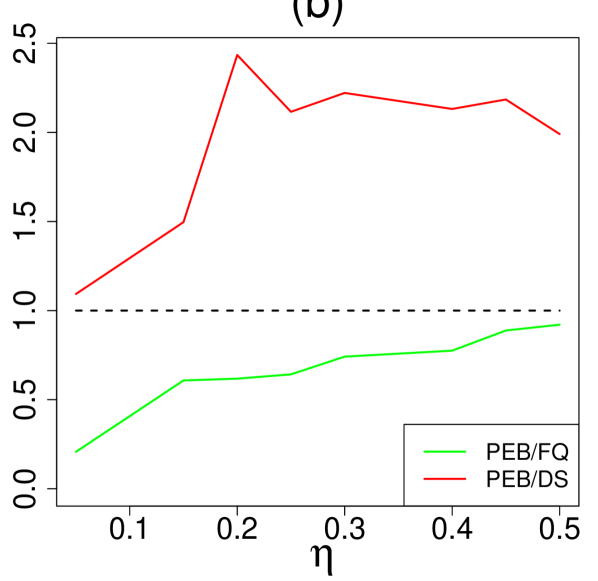

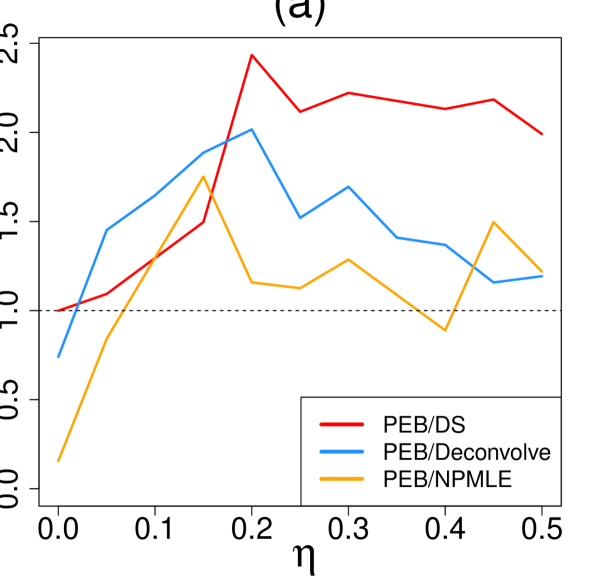

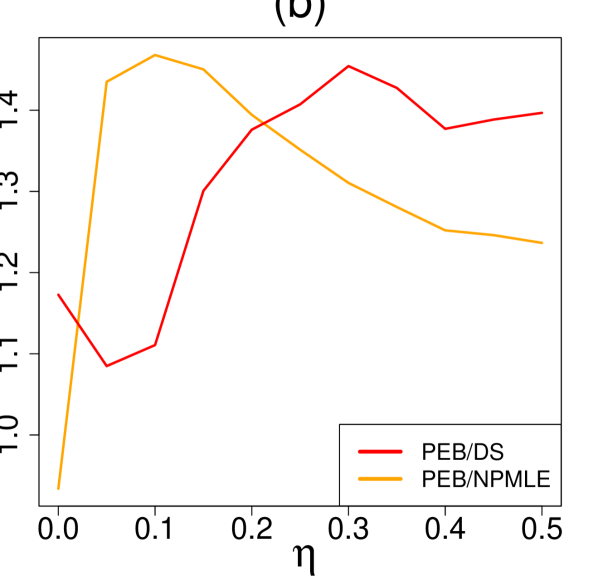

Rat tumor example. Figure 5 compares Stein’s empirical Bayes estimate with our Elastic-Bayes estimate for the all tumor rates. Posterior mean, median, and mode of ’s are shown side by side in three plots. The departure from the reference line is a consequence of “adaptive shrinkage.” Elastic-Bayes automatically shrinks the empirical towards the representative modes ( and ), whereas the Stein’s PEB estimate uses the grand mean () as the shrinking target for all the tumor rates. This is particularly prominent in Fig. 5 (c) for maximum a posteriori (MAP) estimates. As before, for heterogeneous population, we prescribe posterior mode as the final prediction. The Pharma-example. Our DS Elastic-Bayes estimate is especially powerful in the presence of prior-data conflict. To illustrate this point, we report a small simulation study. The goal is to compare MSE for frequentist MLE, parametric empirical Bayes, and nonparametric Elastic-Bayes estimates for a new study in various levels of prior-data conflict. To capture the prior-data conflict, we consider the following model for and :

The parameter varies from 0 to 0.50 in increments of 0.05; as increases we introduce more heterogeneity into the true prior distribution and exacerbate the prior-data conflict between and ; see Fig. 6(a). We simulated from , with which we generate . Using the Type-II MoM algorithm on the simulated data set, we found . After generating , we then determined the frequentist MLE, parametric EB (PEB), and the nonparametric elastic Bayes estimates of the mode. For each value of , we repeated this process times and found the mean squared error (MSE) for each estimate. To better illustrate the impact of prior-data conflicts, we used ratio of PEB MSE to frequentist MSE and PEB MSE to DS MSE. The results are shown in Fig. 6 (b).

The Elastic-Bayes estimate outperforms the Stein’s estimate for all . More importantly the efficiency of our estimate continues to increase with the heterogeneity. This is happening because elastic Bayes performs selective shrinkage of sample proportion towards the appropriate mode (near ) and thus gains “strength” by combining information from ‘similar’ studies even when the contamination in the study population increases. An interesting observation is the performance of the frequentist MLE estimate; as the data becomes more heterogeneous, the frequentist MLE shows improvement with respect to the Stein’s PEB estimate. Our simulation depicts a scenario that is very common in historic-controlled clinical trials, where the heterogeneity arises due to changing conditions. Additional comparisons with other empirical Bayes procedures can be found in Supplementary Appendix G.

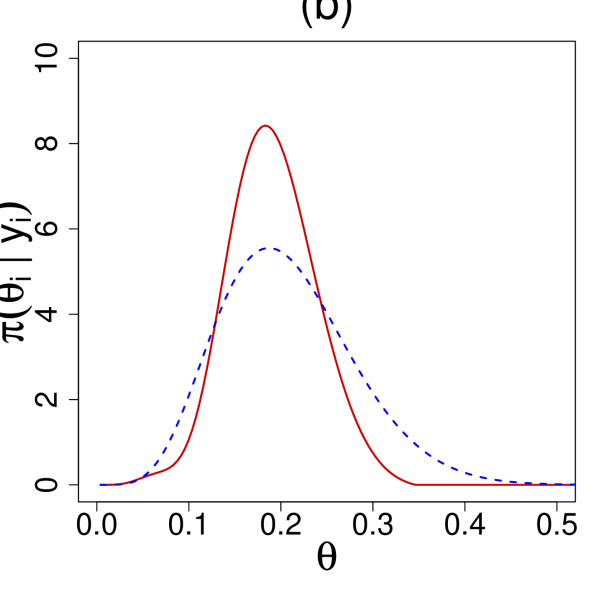

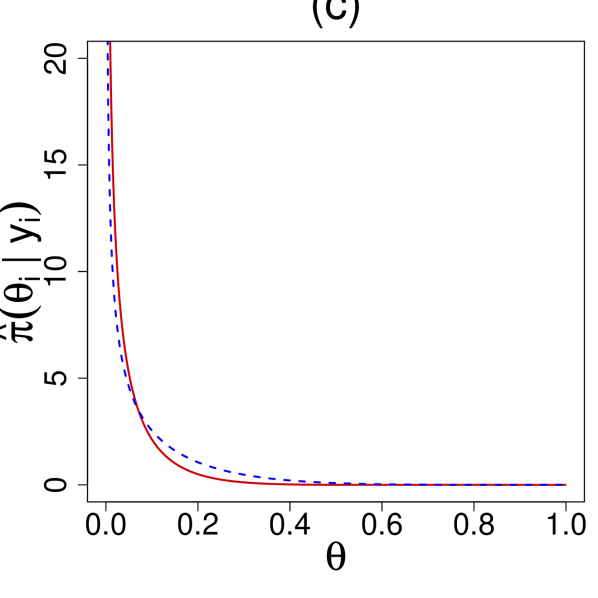

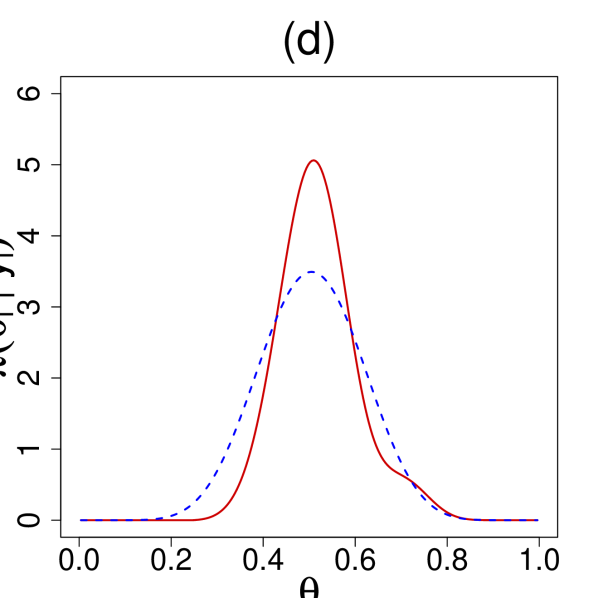

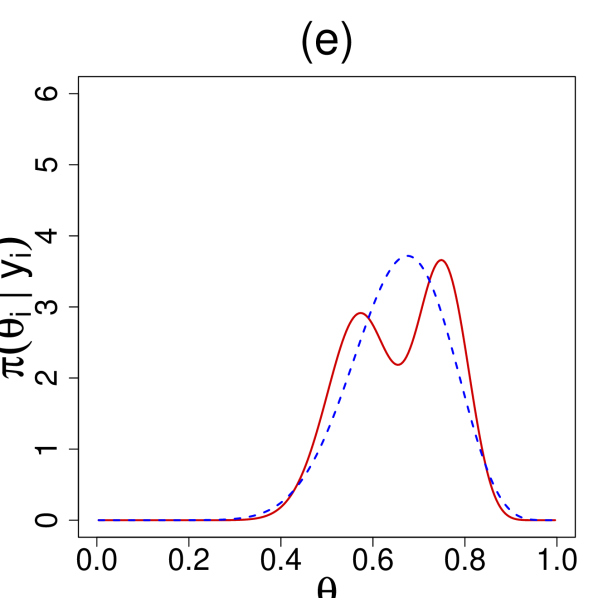

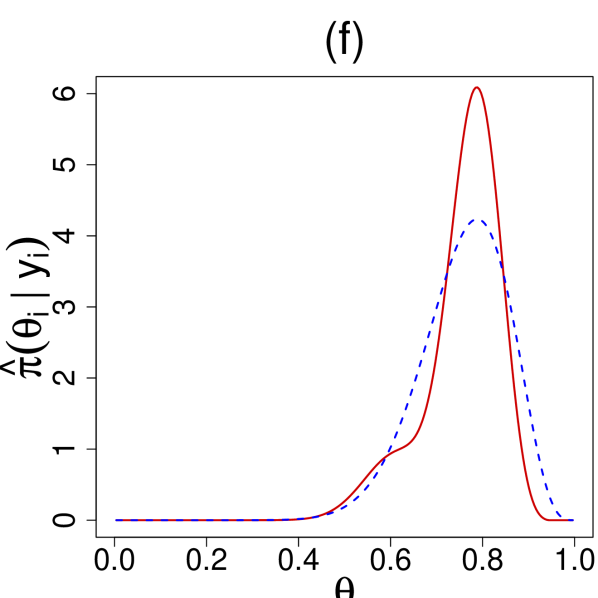

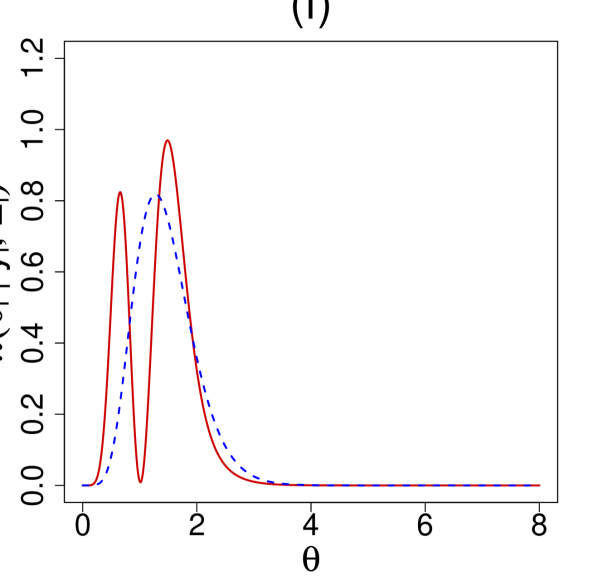

Three additional real examples. Figure 7 shows the posterior plots for specific studies in four of our data sets: surgical node, rat tumor, Navy shipyard, and rolling tacks. In studies like the surgical node data, personalized predictions are typically valuable. Figure 7(a) shows posterior distributions for three selected patients, which are indistinguishable from Efron’s deconvolution answer [cox2017statistical, Fig. 4]; the patient with and shows almost certainly , i.e., he or she is highly prone to positive lymph nodes, and thus should be referred to follow-up therapy. With regard to the rat tumor data, Fig. 7(b) depicts the DS-posterior distribution of along with its parametric counterpart . Interestingly, the DS nonparametric posterior shows less variability; this possibly has to do with the selective learning ability of our method, which learns from similar studies (e.g. group 2), rather than the whole heterogeneous mix of studies. We see similar phenomena in the rolling tacks data, where panel (d): , is more reflective of the first mode and panel (f): , of the second. Panel (e) shows the bimodal posterior for case. Finally, the Navy shipyard data (Fig. 7 (c)) exhibits another advantage of DS priors: it works equally well for small . The DS-posterior mean estimate for is , which is consistent with the findings of Sivaganesan and Berger [sivaganesan1993robust, p. 117].

4.4 Poisson Smoothing: The Two Cultures

We consider the problem of estimating a vector of Poisson intensity parameters from a sample of , where the Bayes estimate is given by:

| (4.3) |

Two primary approaches for estimating (4.3):

-

•

Parametric Culture [fisher1943, maritz1969]: If one assumes to be the parametric conjugate Gamma distribution , then it is straightforward to show that Stein’s estimate takes the following analytical form , weighted average of the MLE and the prior mean .

-

•

Nonparametric Culture [robbins1956, efron2003robbins, koenker2016]: This was born out of Herbert Robbins’ ingenious observation that (4.3) can alternatively be written in terms of marginal distribution , and thus can be estimated non-parametrically by substituting empirical frequencies. This remarkable “prior-free” representation, however, does not hold in general for other distributions. As a result, there is a need to develop methods that can bite the bullet and estimate the prior from the data. Two such promising methods are Bayes deconvolution [efron2003robbins] and the Kiefer-Wolfowitz non-parametric MLE (NPMLE) [kiefer1956, koenker2016]. Efron’s technique can be viewed as smooth nonparametric approach, whereas NPMLE generates a discrete (atomic) probability measure. For more discussion, see Supplementary Appendix A2.

The Third Culture. Each EB modeling culture has its own strengths and shortcomings. For example, PEB methods are extremely efficient when the true prior is Gamma. On the other hand, the NEB methods possess extraordinary robustness in the face of a misspecified prior yet they are inefficient when in fact . Noticing this trade-off, Robbins raised the following intriguing question [robbins1980]: how can this efficiency-robustness dilemma be resolved in a logical manner? To address this issue, we must design a data analysis protocol that offers a mechanism to answer the following intermediate modeling questions (before jumping to estimate ): Can we assess whether or not a Gamma-prior is adequate in light of the sample-information? In the event of a prior-data conflict, how can we estimate the ‘missing shape’ in a completely data-driven manner? All of these questions are at the heart of our ‘Bayes via goodness-of-fit’ formulation, whose goal is to develop a third culture of generalized empirical Bayes (gEB) modeling by uniting the parametric and non-parametric philosophies. Compute the DS Elastic-Bayes estimate by substituting in the Eq. (4.2), which reduces to the PEB answer when (i.e, the true prior is a Gamma) and modifies non-parametrically, only when needed; thereby turning Robbins’ vision into action (see Supplementary Appendices A and G for more discussions on this point).

| Claims | 0 | 1 | 2 | 3 | 4 | 5 | 6 | 7 |

|---|---|---|---|---|---|---|---|---|

| Counts | 7840 | 1317 | 239 | 42 | 14 | 4 | 4 | 1 |

| Gamma PEB | 0.164 | 0.398 | 0.633 | 0.87 | 1.10 | 1.34 | 1.57 | 1.80 |

| Robbins’ EB | 0.168 | 0.363 | 0.527 | 1.33 | 1.43 | 6.00 | 1.75 | — |

| Deconvolve | 0.164 | 0.377 | 0.642 | 1.14 | 2.13 | 3.45 | 4.47 | 5.08 |

| NPMLE | 0.168 | 0.362 | 0.534 | 1.24 | 2.21 | 2.53 | 2.58 | 2.58 |

| DS Elastic-Bayes | 0.156 | 0.322 | 0.517 | 0.744 | 1.02 | 1.56 | 3.01 | 5.24 |

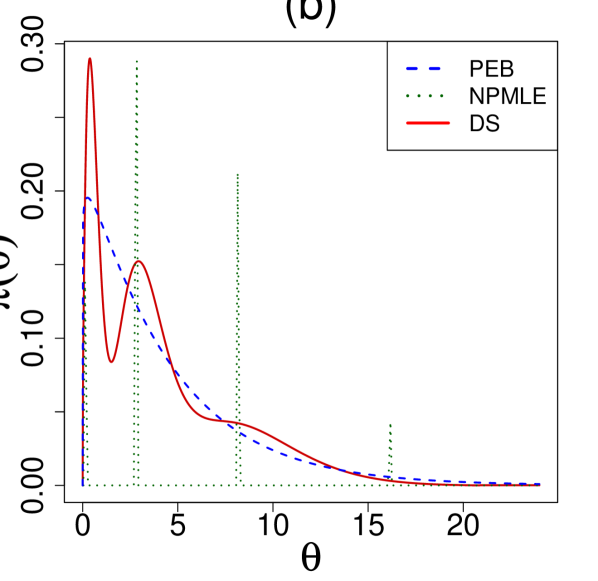

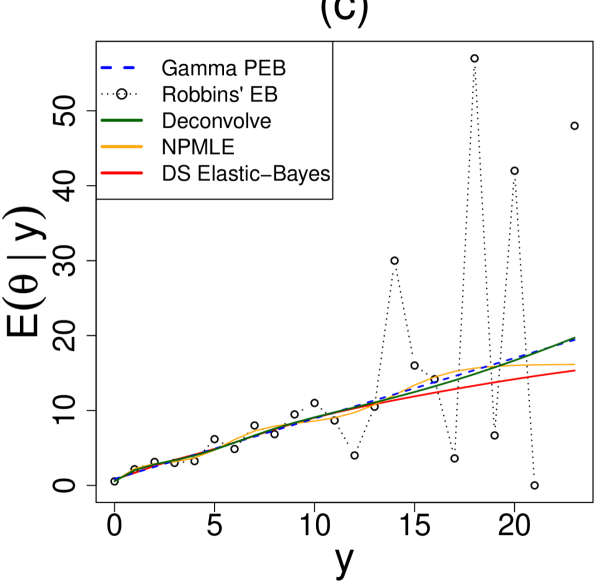

The insurance data. Table 4 reports the Bayes estimates for the insurance data. We compare five methods: parametric Gamma, classical Robbins’ EB, Efron’s Deconvolve, Koenker’s NPMLE, and our procedure. The raw-nonparametric Robbins’ estimator is clearly erratic at the tail due to data-sparsity. The PEB estimate overcomes this limitation and produces a stable estimate; but is it dependable? Should we stop here and report this as our final result? Our exploratory U-diagnostic tells that (consult Sec 3.3) the PEB estimate needs a second-order correction to resolve the discrepancy between the Gamma prior and data. The improved LP-Stein estimates are shown in the last row of Table 4.

The butterfly data. The next example is Corbet’s Butterfly data [fisher1943]– one of the earliest examples of empirical Bayes. Alexander Corbet, a British naturalist, spent two years in Malaysia trapping butterflies in the 1940s. The data consist of the number of species trapped exactly times in those two years for . Figure 8(b) plots different Bayes estimates. The Robbins’ procedure suffers from similar ‘jumpiness.’ The blue dotted line represents the linear PEB estimate with and (same as of Efron and Hastie [efron2016computer, Eq. 6.24]) estimated from the zero-truncated negative binomial marginals. Our DS-estimate is almost sandwiched between the PEB and Deconvolve answer. The NPMLE method (the orange curve) yields some strange looking sinusoidal pattern, probably due to overfitting. In conclusion, we must say that the triumph of our procedure as compared to the other Bayes estimators lies in its automatic adaptability that Robbins alluded in his 1980 article [robbins1980].

5 Discussions

We laid out a new mechanics of data modeling that effectively consolidates Bayes and frequentist, parametric and nonparametric, subjective and objective, quantile and information-theoretic philosophies. However, at a practical level, the main attractions of our “Bayes via goodness-of-fit” framework lie in its (i) ability to quantify and protect against prior-data conflict using exploratory graphical diagnostics; (ii) theoretical simplicity that lends itself to analytic closed-form solutions, avoiding computationally intensive techniques such as MCMC or variational methods.

We have developed the concepts and principles progressively through a range of examples, spanning application areas such as clinical trials, metrology, insurance, medicine, and ecology, highlighting the core of our approach that gracefully combines Bayesian way of thinking (parameter probability where prior knowledge can be encoded) with a frequentist way of computing via goodness-of-fit (evaluation and synthesis of the prior distribution). If our efforts can help to make Bayesian modeling more attractive and transparent for practicing statisticians (especially non-Bayesians) by even a tiny fraction, we will consider it a success.

Data availability

All datasets and the computing codes are available via free and open source R-software package BayesGOF. The online link: https://CRAN.R-project.org/package=BayesGOF

References

Additional information

Supplementary information: It includes (i) connection with other major Bayesian modeling cultures, (ii) Details of BayesGOF R-Software together with additional numerical illustrations, (iii) important extensions to examples with covariates and (iv) Maximum-entropy modeling. Competing Interests: The authors declare no competing interests.

Supplementary Material for “Bayesian Modeling via Goodness-of-fit”

Subhadeep Mukhopadhyay∗, Douglas Fletcher

Temple University, Department of Statistical Science

Philadelphia, Pennsylvania, 19122, U.S.A.

∗ To whom correspondence should be addressed; E-mail: deep@temple.edu

This supplementary document contains nine Appendices, organized as follows:

-

•

Appendix A: Connections with other Bayesian modeling cultures.

-

•

Appendix B: More insights into the LP-basis functions.

-

•

Appendix C: The DS sampler.

-

•

Appendix D: Other practical considerations.

-

•

Appendix E: Software.

-

•

Appendix F: Data Catalogue.

-

•

Appendix G: The Robbins’ puzzle.

-

•

Appendix H: Example with covariates.

-

•

Appendix I: Maximum-Entropy enhancement.

A. CONNECTIONS WITH OTHER BAYESIAN MODELING CULTURES

In this section, we explore the relationship of our approach with other existing Bayesian data modeling cultures from philosophical and computational perspective. We will show that our formulation can be interpreted from surprisingly diverse perspectives.

A1. Robust Bayesian Methods

Our view of going from a unique prior assumption to a class of priors for robust Bayesian modeling was shaped by the Jim Berger’s outstanding article [Berger1994robust]. In the same spirit of the -contamination class [berger1986robust], our U-function can be thought of as an automatic robustifier for standard (conjugate) priors. Thus, our approach may attain similar goals in a more computationally friendly way. Finally, we completely agree with Berger [Berger1994robust] that ‘The major objection of non-Bayesians to Bayesian analysis is uncertainty in the prior, so eliminating this concern can make Bayesian methods considerably more appealing.’

A2. Empirical Bayes Methods

Empirical Bayes approaches use data to determine the prior. While parametric empirical Bayes [PEB] [morris1983parametric] fixes the hyperparameters based on the data, nonparametric empirical Bayes [NEB] [efron2003robbins] makes no assumptions on the prior’s form and develops it based solely on the data. In particular, Brad Efron [efron1996empirical, efron2014bayes] advocate a smooth nonparametric exponential family model: for the prior distribution where is estimated by maximizing the marginal log-likelihood function.

Example 1. The dotted line in Figure 9(a) denotes the non-parametrically estimated Efron’s based on two-dimensional sufficient vector for the ulcer data [efron1996empirical]. At a first glance, it appears strikingly close to the conjugate normal prior , marked as the bold red line. Perhaps the reader may be curious to know whether ‘ PEB Normal’ here? This is indeed the case, as already shown in Figure 1(b) of the main paper. Our generalized empirical Bayes (gEB) framework automatically reduces to PEB when the data is consistent with the assumed parametric prior and modifies it non-parametrically otherwise. The output of the combined inference from clinical trials is shown as a green triangle , which is quite close222The slight gain in accuracy for our method lies in the style of estimation that proceeds via goodness-of-fit. Constructing prior by validating its credibility (using frequentist criterion) may also strengthen the Bayesian objectivity that Brad Efron [efron1986isn] alluded to his article “Why isn’t everyone a Bayesian?” to the Efron’s nonparametric answer [efron1996empirical] . The negative macro-estimate of the log-odds ratio parameters suggests that the new surgical treatment for stomach ulcers is overall more effective than the existing one. Another attractive NEB technique is based on non-parametric maximum likelihood estimate (NPMLE): maximize the log-likelihood over the set of all on , which is known to be a notoriously difficult problem. Thanks to Gu and Koenker [koenker2016], an approximate NPMLE can be estimated via convex optimization technique (interior point method) instead of classical EM (Expectation-Maximization) algorithm [laird1978], thereby making it a computationally feasible alternative.

Example 2. NPMLE imposes no structural constraint and produces an estimated prior as discrete measure supported on at most points within the data range. Figure 9(b) shows its application to the child illness data [wang2007fast], which comes from a study that followed pre-school children in north-east Thailand from June 1982 through September 1985. Researchers recorded the number of times () a child became sick during every 2-week period. Using the DS-Bayes method, we have where is a gamma distribution with and as

| (5.1) |

Our method produces a smooth, grid-free that accurately captures the overall shape. Figure 9(c) plots the Bayes estimates for all competing methods. For Efron’s Deconvolve we have used c0 = 2 and pDegree = 25, which seems to produce a reasonable prior density estimate for this example. A careful look at the plot reveals an ‘oscillating’ NPMLE Bayes estimates (orange curve), which many not be particularly desirable.

| Data Set | # Studies () | DS | DP | Ratio | BDP | Ratio |

|---|---|---|---|---|---|---|

| Time | Time | DP to DS | Time | BDP to DS | ||

| Rat Tumor | 70 | 1.83 | 10.42 | 5.69 | 3457.75 | 1889.5 |

| Surgical Node | 844 | 30.95 | 189.3 | 6.12 | 45292.15 | 1463.4 |

| Terbinafine | 41 | 1.7 | 5.46 | 3.2 | 1883.18 | 1107.8 |

| Rolling Tacks | 320 | 8.27 | 59.16 | 7.15 | 16569.78 | 2003.6 |

| Arsenic | 28 | 0.47 | 13.09 | 27.8 | 433.29 | 254.9 |

A3. Dirichlet-Process-based Approaches

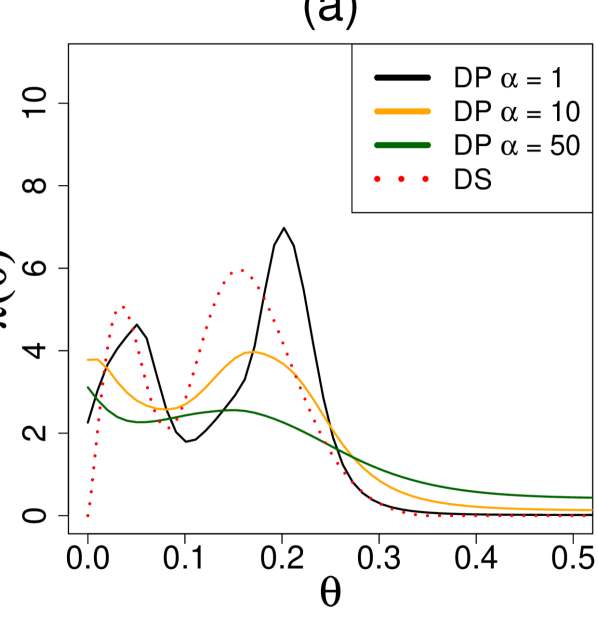

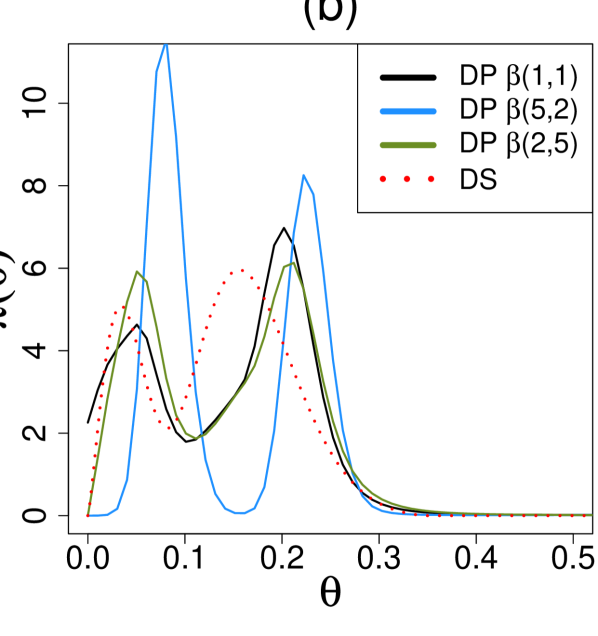

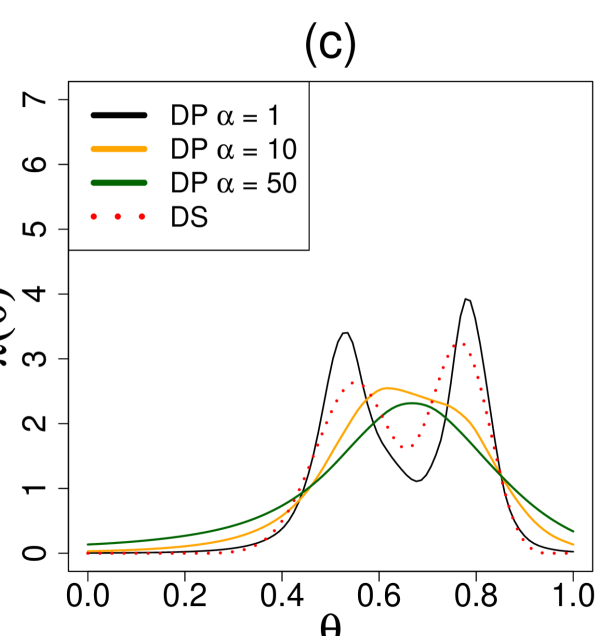

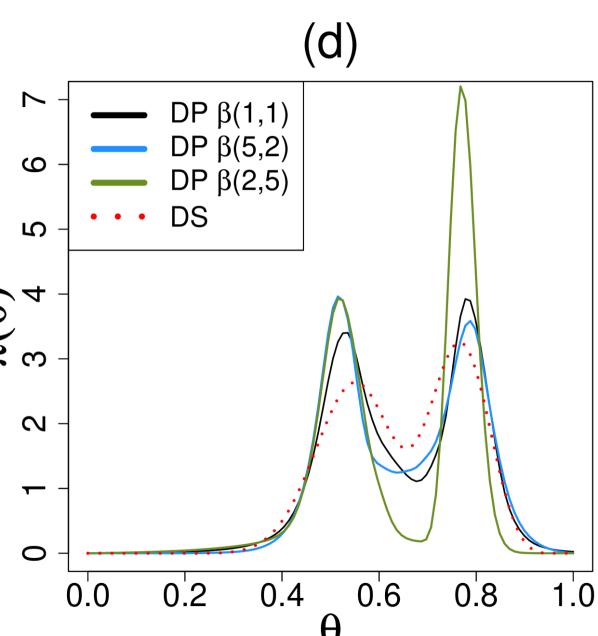

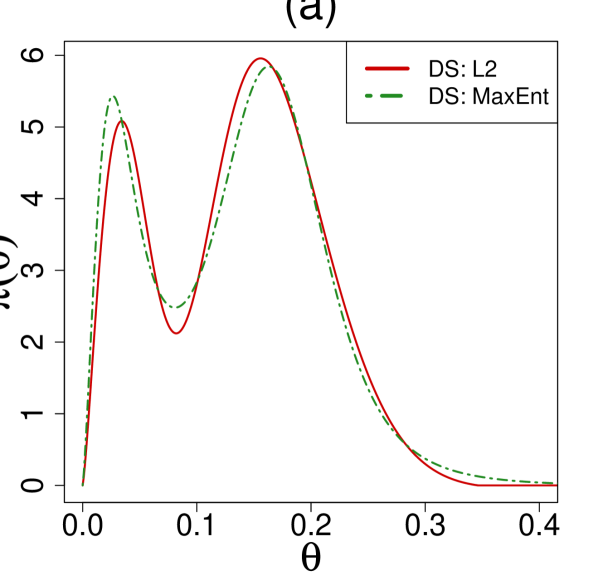

Bayesian nonparametric [BNP] technique assigns prior distribution on infinite-dimensional spaces of probability models. The majority of work on Bayesian nonparametrics utilizes a Dirichlet process prior [ferguson1973]. The computational cost of BNP is severe and produces prior on a set of discrete probability measures that demands an additional layer of smoothing. Figure 10 contrasts Dirichlet-process based Beta-Binomial models [liu1996nonparametric] with our DS-Bayes model. There are few remarks warranted here:

-

•

BNP method requires careful tuning of several hyper-priors values, which from our experience can be quite sensitive (see Figure 10). Without practical guidance, this “fishing expedition” can potentially overwhelm one who seeks to confidently use it in practice. On the contrary, our method finds practically the same answer without adjusting multiple hyper-prior values.

-

•

The posterior inferences of BNP are highly complex and require computationally expensive MCMC. In contrast, the beauty of our approach is that it provides compact analytical expressions that make the computation much more amicable.

-

•

The flexibility of BNP comes with the heavy task of estimating a massive number of parameters–“massively parametric Bayes.” Contrast this with model, which provides a reduced-dimensional characterization of the prior distribution with a closed form solution that is computationally efficient (see Table 5) and produces smooth estimates in one-shot. For additional comments see the ‘Critical Appraisal’ section.

A4. Weakly Informative Priors

A weakly informative prior [WIP] is a proper prior that intentionally provides less information than available prior knowledge. This lies somewhere between a fully subjective and a fully objective prior [gelman2008weakly, gelman2013bayesian].

One can also view our approach from a WIP-angle where acts as a “spreading/weakening function” of the subjective prior , which we learn from the data. In the language: is the radius of spread; the larger the , the greater possibility you allow for changing the shape (the process of weakening) of the presumed scientific prior distribution . These analogies suggest that our concepts and notations might provide a systematic way to formulate the WIP philosophy by addressing the debates around “WIP is a subjective prior with ad hoc large but bounded support.” This reformulation can also bring some tangible computational gain.

A Critical Appraisal

We close this section by highlighting some of the unique aspects and practical advantages of our technique:

-

•

Clarifying the Motivation: Let’s start by reminding ourselves that the core motivation behind the ‘Bayes via goodness-of-fit’ is more than just another recipe for estimating the prior from data. To understand the mysterious prior in a transparent and definitive way, it is critical to ask: How can we provide automatic protection from unqualified specifications of prior distribution? How do we assess the prior-uncertainty using exploratory graphical tools? How can we prescribe a revised statistical-prior starting from the user-specified scientific-prior? As it stands, these fundamental questions are usually left unanswered in traditional Bayes framework and create a major obstacle for non-Bayesian practitioners to confidently use Bayesian tools. Consequently, there is a need to address these issues in a formal manner to bring much-needed transparency. This paper has taken some solid steps toward this goal with a methodology that is readily usable for wide-range of applied problems. We believe that our technology can become an integral part of applied Bayesian modeling.

-

•

Theoretical Novelty: Our proposed theory, which is general enough to include almost all commonly-used models, yields analytic closed-form solutions for posterior modeling. This is noteworthy for the simple reason that none of the nonparametric methods mentioned above can stand by this claim.

-

•

Theoretical Simplicity: The whole ‘Bayes via Goodness-of-fit’ framework can be developed starting from a few basic principles, without requiring any exotic theoretical treatment. This could add invaluable transparency to the theory and practice of (empirical) Bayesian statistics.

-

•

Exploratory Side: Our approach brings a distinct exploratory flavor into the empirical-Bayes modeling. It encourages interactive data analysis rather than blindly ‘turning the crank.’ Through numerous examples, we demonstrated how this mode of operation often leads to more insights into the data that are typically infeasible under a business-as-usual Bayesian modus operandi.

-

•

Computational Side: Simplicity of implementation and computational ease are the two hallmarks of our method. No expensive MCMC or even sophisticated optimization routines are required! We made a sincere effort to design a practical Bayesian data analysis tool that is both simpler to comprehend and easy to implement.

-

•

A Third Empirical Bayes Culture. Our empirical Bayes approach is neither parametric nor nonparametric. As argued in Section 4.4 (of the main paper), our algorithmic approach blends conventional PEB and Robbins-style full-fledged NEB. Our goal is to combine the best of both worlds, in the sense that the prior reduces to PEB (ulcer data example) when in fact the default parametric is appropriate, while in the event of prior-data conflict (rat tumor or child illness data), it automatically produces reliable nonparametric procedures. And in this whole story, the U-function acts as the “connector” between these two extreme philosophies. Overall, we are hopeful that our Generalized EB (gEB) modeling framework might expedites the development of a new genre of ‘unified’ Bayesian algorithms [berger2000bayesian] by leveraging the rich interplay between two extreme EB philosophies.

B. MORE INSIGHTS INTO THE LP-BASIS FUNCTIONS

Here we will show the shapes of the LP-polynomials, focusing only the Binomial case. It works similarly for other families. The denotes the class of orthonormal polynomials of the beta distribution with parameters and . Let and . Figure 11 displays the shapes of top four LP polynomials for three different sets of parameters. We generate these polynomials with the following R code:

C. THE SAMPLER

The following algorithm generates samples from the model via accept/reject scheme. Sampling Algorithm Step 1. Generate from ; independent of , generate from . Step 2. Accept and set if

otherwise, discard and return to Step 1.

Step 3. Repeat until simulated sample of size , .

Note that when then the automatically samples from parametric .

D. OTHER PRACTICAL CONSIDERATIONS

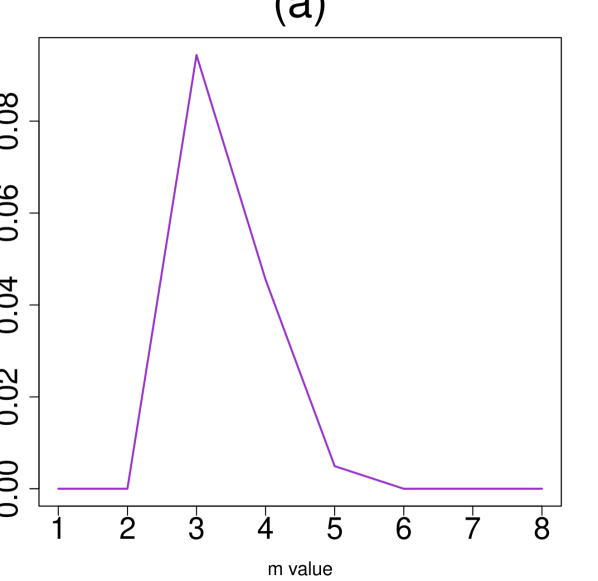

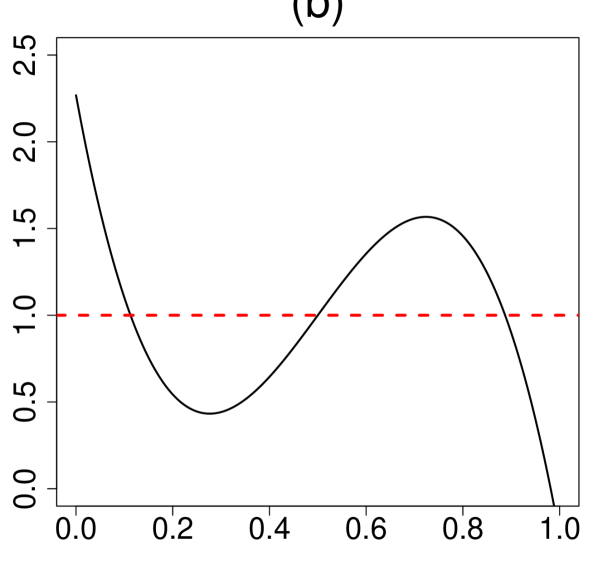

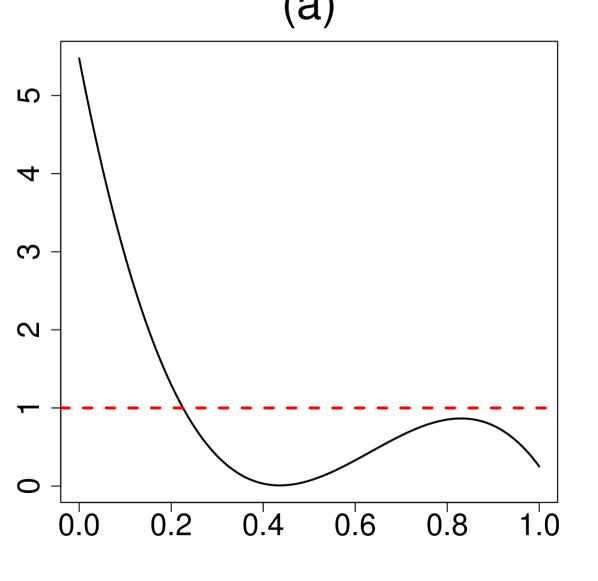

In the event that no prior knowledge is available, selecting the parametric conjugate prior with empirically estimated in conjunction with our Type-II Method of Moments algorithm (sec. 3.2) will provide a quick estimate of the oracle . The algorithm finds the ‘best’ approximating prior model given m.max: the maximum complexity that the subject-matter experts want to entertain. From our experience with model, we found works satisfactorily well in practice (in fact in all our examples was our default choice), which encompasses the space of reasonable priors around . Given this maximum radius, our method generates a deviance plot, where the “elbow” shape (see Figure 12 (a)) denotes the most likely model dimension. This procedure is fully incorporated into our algorithm so that practitioners can use it in a completely automatic manner.

Illustration. Consider the model: with and the true prior distribution . Our goal is to see how well we can approximate the unknown without any prior knowledge of its shape. The following R code can be used to reproduce our findings reported in Figure 12.

The sim.start object holds the MLE estimate for the initial parameters for . From the sim.LP.par object, we generate diagnostic and analysis plots for appropriate , U-function, and the estimate, as shown in Figure 12.

E. SOFTWARE

We provide an R package, BayesGOF [bayesgofR] to perform all the tasks outlined in the paper. We now summarize the main functions and their usage for the Rat binomial data example:

The package also provide functionalities for Macro and MicroInference:

We hope this software will encourage applied data scientists to apply our method for their real problems.

F. DATA CATALOGUE

| Dataset | # Studies () | Family | Sources |

|---|---|---|---|

| Surgical Node | 844 | Binomial | Efron (2016) [efron2014bayes] |

| Rolling Tacks | 320 | Binomial | Beckett and Diaconis (1994) [beckett1994spectral] |

| Rat Tumor | 70 | Binomial | Gelman et al. (2013, Ch. 5) [gelman2013bayesian] |

| Terbinafine | 41 | Binomial | Young-Xu and Chan (2008) [young2008pooling] |

| Naval Shipyard | 5 | Binomial | Martz et al. (1974) [martz1974empirical] |

| \hdashlineGalaxy | 324 | Gaussian | De Blok et al.(2001) [de2001high] |

| Ulcer | 40 | Gaussian | Sacks et al.(1990) [sacks1990endoscopic] |

| Arsenic | 28 | Gaussian | Willie and Berman (1995) [willie1995ninth] |

| \hdashlineInsurance | 9461 | Poisson | Efron and Hastie (2016) [efron2016computer] |

| Child Illness | 602 | Poisson | Wang (2007) [wang2007fast] |

| Butterfly | 501 | Poisson | Fisher et al. (1943) [fisher1943] |

| Norberg | 72 | Poisson | Norberg(1989) [norberg1989experience] |

G. THE ROBBINS’ PUZZLE

In Section 4.3 of the main paper, we presented a simulated scenario ( Pharma-example) that demonstrated the power of the DS Elastic-Bayes estimate when there is significant prior-data conflict. Here we include further comparisons with two recent methods: Efron’s Bayesian deconvolution (implemented in the deconvolveR package), and Koenker’s NPMLE (implemented in the REBayes package).

Example 1. Here we will operate under the exact settings presented in Section 4.3. Figure 13(a) shows that as increases, DS tends to outperform the other two methods, although Deconvolve performs superbly for smaller than . Two specially interesting extreme cases are and . The first scenario describes the situation when the underlying parametric distribution is the right choice for the prior where, as expected, the Stein’s parametric shrinkage estimator dominates other nonparametric approaches. On the other hand, the is a complicated situation where , and consequently, the parametric EB [PEB] is less efficient compared to the nonparametric ones. The most interesting and surprising result, however, comes from DS Elastic-Bayes, which acts like the Stein prediction formula when underlying parametric assumption is correct (the null case) but adapts itself non-parametrically in a completely automated manner when the true deviates from the assumed , thereby elegantly addressing the robustness-efficiency puzzle of Robbins [robbins1980].

Example 2. Next, we investigate the prediction problem originally introduced by Robbins [robbins1985asymptotically] and discussed in Gu and Koenker [koenker2016]. We observe , , where , and with probability and respectively. Our goal is to estimate the -vector under the loss . For comparison purpose, we computed the ratio of PEB empirical risk222Mean loss is computed over replications. to the the DS method (EB/DS) and to the NPMLE estimator (EB/KW) for . Figure 13(b) shows a very interesting result: Kiefer-Wolfowitz NPMLE method performs significantly better than the DS-elastic Bayes when . While for other values of , including equals to zero point, our micro-estimation procedure demonstrates tremendous promise. This further validates the flexibility and adaptability of our technique even in the discrete settings.

H. EXAMPLE WITH COVARIATES

The ‘Bayes via goodness-of-fit’ methodology can easily accommodate additional covariates. We demonstrate this capability using the following example.

The Norberg Example. The Norberg insurance dataset [norberg1989experience] consists of Norwegian occupational categories, where denotes the number of claims made against a policy. Additionally, we have the total number of years each group was exposed to risk ; when normalized by a factor of 344, gives the expected number of claims during a contract period. Similar to Norberg [norberg1989experience], we assume . Given the normalized , we interpret as the occupational-specific rate of risk. DS-Bayes analysis yields the following estimated prior, where is the conjugate gamma prior with MLE and :

| (5.2) |

In Figure 14(a), the U-function clearly indicates potential prior-data conflict when using . Figure 14(b) displays the DS prior (red) along with the parametric EB (blue) and the Kiefer-Wolfowitz NPMLE estimate (green). We see a definite bimodality for , indicating that there are two distinct groups of risk profiles. The macroinference plot in Figure 14(c) reinforces the structured heterogeneity of the data. In terms of risk-profile, we consider the mode at as occupational categories with comparatively lower risk; these are occupations less likely to make a claim based on their risk exposure. The mode at represents those occupations at a higher risk, thus more likely to make a claim based on their exposure.

Of particular interest are panels (d), (e), and (f). These panels show the microinference for three specific occupational groups: group 13 (, ), group 22 (, ), and group 53 (, ). In Figure 14(d), we have an occupational category that identifies as higher risk with a small lower risk component. The unimodality in Figure 14(e) clearly indicates that category is a higher risk of claim based on exposure. Finally, the occupational category in Figure 14(f) is tricky. Here, we have bimodality with an almost equal probability of being a high or low-risk occupation. While the other two groups provide clear alternatives for an insurance company, the occupational group needs the company’s judgment in assigning the policy.

I. MAXIMUM-ENTROPY ENHANCEMENT

For more enhanced result, we offer an extension to maximum entropy model, which assumes the following representation of the prior distribution:

| (5.3) |

where is some normalizing constant and the ’s are the LP-maximum entropy coefficients. The following algorithm outlines the process to solve for the unknown ’s starting from the estimate.

Orthogonal Series to Maximum Entropy Estimator Step 0. Input: BIC-smoothed LP-Fourier () coefficients , . Step 1. Define the set , collection of ’s for which we have significant non-zero orthogonal coefficients. Step 2. To estimate the maximum entropy coefficients in of (5.3), solve the following sets of moment equality constraints:

| (5.4) |

Step 3. Output: ; accordingly the estimated maximum entropy and .

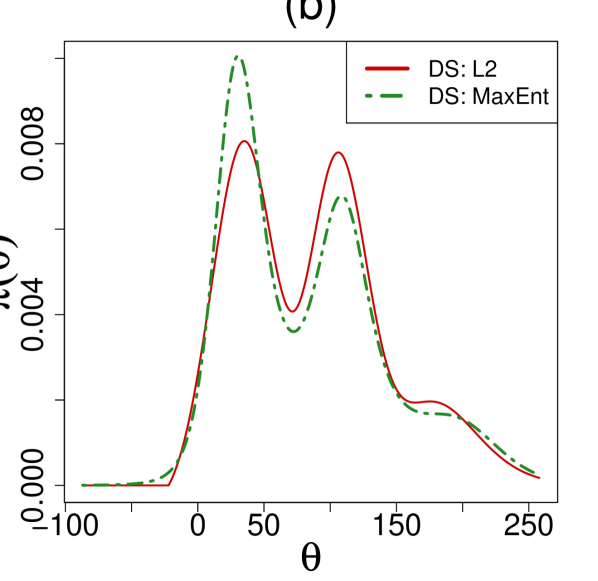

Two Data Examples. Here we carry out the maximum entropy analysis for rat (binomial variate) and galaxy data (normal variate). The galaxy data consists of observed rotation velocities and their uncertainties of Low Surface Brightness (LSB) galaxies [de2001high].

-

(a)

Rat Tumor data, is beta distribution with MLE , :

(5.5) -

(b)

Galaxy data, is normal distribution with MLE , :

(5.6)

The resulting LP-maximum-entropy priors are shown in Figure 15. In both examples, we see the maximum entropy estimates (green dashed lines) are very similar to the with some adjustments to the modal shapes.

The BayesGOF package in R implements this algorithm as an option for the DS.prior function. The following code demonstrates how to generate both the and maximum entropy representations of the LP coefficients for both the rat tumor and galaxy data sets.