Nonparametric Hawkes Processes: Online Estimation and Generalization Bounds††thanks: Yingxiang Yang and Negar Kiyavash are affiliated with Department of Electrical and Computer Engineering at University of Illinois at Urbana-Champaign. Negar Kiyavash is also affiliated with Department of Industrial and Enterprise Systems Engineering at University of Illinois at Urbana-Champaign, along with Jalal Etesami and Niao He. Emails: yyang172,etesami2,niaohe,kiyavash@illinois.edu. This work was supported in part by MURI grant ARMY W911NF-15-1-0479 and ONR grant W911NF-15-1-0479. Part of this work was presented at Advances in Neural Information Processing Systems (NIPS 2017) (Yang et al., 2017).

Abstract

In this paper, we design a nonparametric online algorithm for estimating the triggering functions of multivariate Hawkes processes. Unlike parametric estimation, where evolutionary dynamics can be exploited for fast computation of the gradient, and unlike typical function learning, where representer theorem is readily applicable upon proper regularization of the objective function, nonparametric estimation faces the challenges of (i) inefficient evaluation of the gradient, (ii) lack of representer theorem, and (iii) computationally expensive projection necessary to guarantee positivity of the triggering functions. In this paper, we offer solutions to the above challenges, and design an online estimation algorithm named NPOLE-MHP that outputs estimations with a regret, and a stability. Furthermore, we design an algorithm, NPOLE-MMHP, for estimation of multivariate marked Hawkes processes. We test the performance of NPOLE-MHP on various synthetic and real datasets, and demonstrate, under different evaluation metrics, that NPOLE-MHP performs as good as the optimal maximum likelihood estimation (MLE), while having a run time as little as parametric online algorithms.

1 Introduction

Multivariate Hawkes Processes (MHPs) are multivariate counting process where an arrival in one dimension can affect the arrival rates of other dimensions. The origin of MHPs dates back to Hawkes (1971), where it was used to statistically model earthquakes, for the purpose of revealing a temporally self-excitation pattern and a spatially mutual-excitation structure. Because of their ability to capture mutual excitation between different dimensions of a multivariate counting process, MHPs have become a popular model in a plethora of scenarios. In high frequency trading (Bacry et al., 2015b, 2012a; Hardiman et al., 2013), MHPs are commonly used to model the clustered arrival patterns of bullish and bearish orders. In computational biology, MHPs are used to model neural spike train data (Reynaud-Bouret et al., 2010). In social network studies, MHPs have been used to model diffusion networks as an alternative for the contagion model (Yang and Zha, 2013). In computational phenotyping, MHPs are used to extract useful information from Electronic Health Record (EHRs), such as the relationship between the symptoms experienced by patients and the intake of prescribed medicines (Bao et al., 2017). In criminology, MHPs have been applied to analyze the spatially and temporally clustered occurrences of crimes and terrorist activities, enabling more efficient dispatch of the police forces (Mohler et al., 2011; Porter et al., 2012).

The key factor that determines the ability of an MHP for capturing the self- and the mutual-excitation effects lies within the form of its intensity function. For a -dimensional MHP, the intensity function of the -th dimension takes the following form:

| (1) |

where the constant is the base intensity of the -th dimension, counts the number of arrivals in the -th dimension within , and is the triggering function that embeds the underlying causal structure of the model. Heuristically, one arrival in the -th dimension at time will affect the intensity function of the -th dimension at time by the amount for . The cumulative effect of the arrivals from different dimensions, as well as the cumulative effect of the arrivals over a period of time, are embedded within the additive structure of the intensity function.

In many cases, an MHP alone is not enough to capture the dynamics of the underlying counting process, especially in the case where the events arrived at different times are not identical. For example, in a high frequency trading scenario, each order not only has an arrival time, but also has a trading volume, which is an important parameter that influences the trend and momentum of a stock. Likewise, when studying the patterns of earthquakes, one cannot ignore the magnitude of each shock, as it is intuitive that a strong earthquake is more likely to trigger aftershocks than an earthquake with a much smaller magnitude. Such differences are typically distinguished by associating a mark to each event, and a multivariate marked Hawkes process (MMHP) (Fauth and Tudor, 2012) model is used to fit the data. For an MMHP, the intensity function of the -th dimension takes the form

| (2) |

where, compared to (1), the triggering function now depends on both the arrival time and the corresponding mark.

1.1 Motivations

Driven by its wide applicability, there has been extensive studies on the estimation of MHPs and MMHPs from real-time and large volumes of event data (Hall and Willett, 2016; Bacry et al., 2014, 2015a, 2012b). However, most existing Hawkes process models, as well as the methods used for estimating these models, suffer from severe limitations from both the modeling and the computational perspectives.

Firstly, existing works often make strong assumptions and specify a restricted parametric form of the intensity functions that is not expressive enough to capture the temporal dynamics in many applications. For example, exponential triggering functions

| (3) |

are used in most existing works, where s are unknown while s are given a priori. Under this assumption, the estimation of each triggering function is equivalent to the estimation of a real number. However, there are many scenarios where (3) fails to describe the correct mutual influence pattern between dimensions. This is especially true in studies related to neural spike trains, where it is well known that human body takes time to react to the information it receives. For example, Krumin et al. (2010) and Eichler et al. (2017) have reported delayed and bell-shaped triggering functions when applying the MHP model to neural spike train datasets. Moreover, when the triggering functions are not exponential, or when s are inaccurate, formulation in (3) is prone to model mismatch (Hall and Willett, 2016).

Secondly, most existing works perform batched estimation upon observing all the samples. This can be costly when the samples are streaming in nature and are expensive to observe. For example, in criminology. On the other hand, when the amount of samples is huge, evaluating the batch gradient can be computationally expensive, and the scalability of such algorithms is poor (Yang et al., 2017).

The above concerns motivate us to investigate the estimation of MHPs in an online and nonparametric regime.

1.2 Related Works

Earlier works on estimating the triggering functions for MHPs can be largely categorized into three classes: (i) parametric batch estimation, (ii) nonparametric batch estimation, and (iii) parametric online estimation. The contribution on MMHPs is even less, and mostly focuses on parametric batch estimation (Fauth and Tudor, 2012).

Parametric batch estimation. Based on the assumption that the triggering functions have exponential forms specified in (3) with known s, parametric batch estimation uses all the available samples to estimate the coefficient s. Under the exponential form of the triggering functions, the MHPs possesses the Markov property, and the intensity function for each dimension can be evaluated by considering only “recent” events. Therefore it is computationally much less expensive than nonparametric estimation. The most widely used estimators include the maximum likelihood estimator (MLE, Ozaki (1979)), and the minimum mean-square error estimator (MMSE, Bacry et al. (2015a)). These estimation methods can also be generalized to the high dimensional case when the coefficient matrix is sparse and low-rank (Bacry et al., 2015a).

More generally, one can assume that s lie within the span of a pre-determined set of basis functions : where s have a given parametric form (Etesami et al., 2016; Xu et al., 2016). One example of such algorithms is presented in Xu et al. (2016), where the number of bases is adaptively chosen, which sometimes requires a significant portion of the data to determine the optimal set of bases.

Nonparametric batch estimation. A more sophisticated approach towards finding the set of basis functions is explored in Zhou et al. (2013), where the coefficients and the basis functions are iteratively updated and refined. Unlike Xu et al. (2016), where the basis functions take a predetermined form, Zhou et al. (2013) updates the basis functions by solving a set of Euler-Lagrange equations in the nonparametric regime. However, the optimality for Zhou et al. (2013) is not guaranteed as its formulation is nonconvex. Practically, the method also requires more than arrivals for each dimension in order to obtain good results, on networks of less than 5 dimensions.

Another way to estimate s nonparametrically is proposed in Bacry and Muzy (2016), which solves a set of Wiener-Hopf systems with dimensions. The algorithm is guaranteed to converge and achieves excellent visual goodness-of-fit in various numeric examples. However, this method requires inverting a matrix, which is costly, if not at all infeasible, when is large.

Parametric online estimation. To the best of our knowledge, online estimation of the triggering functions seems largely unexplored. Under the assumption that s are exponential, Hall and Willett (2016) proposes an online algorithm using gradient descent, while exploiting the evolutionary dynamics of the intensity function. The time axis is discretized into small intervals, and the updates are performed at the end of each interval. Unfortunately, this method cannot be extended to the nonparametric setting where the triggering functions are not exponential, mainly because the evolutionary dynamics of the intensity functions does not hold in general. Therefore, the nonparametric estimation of the triggering functions remains largely an open problem.

1.3 Challenges and Our Contributions

Designing a nonparametric online estimation algorithm is not without its challenges: (i) It is not clear how to represent the triggering functions. In this work, we relate the triggering functions to a reproducing kernel Hilbert space (RKHS). Upon proper regularization of the objective function, one can apply the representer theorem (Schölkopf et al., 2001) which reduces the estimation of the triggering function to the estimation of a growing set of coefficients. (ii) Although online kernel estimation is a well studied topic in other scenarios (Kivinen et al., 2004), a typical choice of objective function for an MHP usually involves the integral of the triggering functions, which prevents the direct application of the representer theorem. (iii) For the commonly used objective functions, such as the log-likelihood and the MSE loss, the evaluation of the stochastic gradient requires evaluating the intensity function, which is computationally expensive in nonparametric regime due to a lack of Markov property and evolutionary dynamics. (iv) The outputs of the algorithm at each iteration require a projection step to ensure positivity of the intensity function. This requires solving a quadratic programming problem, which can be computationally expensive.

In this paper, we design, to the best of our knowledge, the first nonparametric online estimation algorithm for the triggering functions. In particular, we contribute to the subject of estimating MHPs by providing solutions to the four challenges we mentioned above. (i) For representation, we base our analysis on the assumption that the triggering functions belong to an RKHS. (ii) We choose the negative log-likelihood as the objective function, and, to apply representer theorem, we approximate the objective function by discretization and characterize the approximation error bound. (iii) We achieve fast evaluation of the gradient using a truncated intensity function, and characterize the approximation error bound. (iv) For projection operation, we adopt a transformation to the triggering function, which achieves low estimation error under various simulation settings.

Theoretically, our algorithm achieves a regret bound of , with being the time horizon. Numerical experiments show that our approach outperforms the previous approaches despite the fact that they handle a less general setting. In particular, our algorithm attains a similar performance to the nonparametric batch maximum likelihood estimation method while reducing the run time extensively.

1.4 Organization of This Paper

The rest of this paper is organized as follows. In Section 2, we provide a short introduction on RKHSs, as it is the main tool we will use throughout this paper. In Sections 3-5, we develop the nonparametric online learning algorithm for MHPs, and provide theoretical guarantee to the proposed algorithm. The formulation of the problem is introduced in Section 3; three online algorithms are introduced in Section 4, including the nonparametric online algorithm for MHPs, as well as parametric and nonparametric algorithms for MMHPs; the regret bound and statistical performances are presented in Section 5; numerical simulations are provided in Section 7.

1.5 Notations

Prior to discussing our results, we introduce the basic notations used in the paper. Detailed notations will be introduced along the way. For a -dimensional MHP, we denote the intensity function of the -th dimension by . We use to denote the vector of intensity functions, and we use to denote the matrix of triggering functions. The -th row of is denoted by . The number of arrivals in the -th dimension up to is denoted by the counting process . We set . The estimates of these quantities are denoted by their “hatted” versions. The arrival time of the -th event in the -th dimension is denoted by . Lastly, define . The proofs appear in Appendix.

2 Preliminaries

In this section, we introduce some preliminaries on RKHSs, and review previous approaches to estimating MHPs using maximum likelihood estimation.

2.1 Reproducing Kernel Hilbert Spaces

Consider a Hilbert space that contains functions supported on . The inner product of is denoted by , and recall that is complete under the norm induced by the inner product. This Hilbert space is an RKHS if there exists a bivariate function , such that for any , , and , is a positive definite kernel:

and that for any , the evaluation functional is bounded (or equivalently continuous):

for some constant . We call the reproducing kernel of .

Several commonly used RKHSs include RKHSs associated with (i) Polynomial kernels: for , When , reduces to a linear kernel. (ii) Gaussian kernels with bandwidth : (iii) Laplacian kernels with bandwidth : The concrete expression of the inner product varies by the choice of the reproducing kernel. We skip the detailed discussion since it is irrelevant in our paper. The functional gradient , which is the fastest ascent direction of within , is defined as Since , we have . RKHS and kernel methods are widely used for nonparametric estimation in machine learning, especially for empirical risk minimization. This is largely due to the representer theorem, which allows reducing an infinite-dimensional optimization problem to a finite-dimensional one.

Theorem 1 (Representer theorem (Schölkopf et al., 2001)).

Let be the reproducing kernel of , and let be a strictly monotonically increasing function. Then,

has a representation form of where is the set of coefficients.

2.2 Estimation of Multivariate Hawkes Processes

A common approach for estimating the parameters of an MHP is to perform regularized MLE. The negative of the log-likelihood function of an MHP over the time interval is given by

| (4) |

Since the intensity is linear with respect to the triggering functions , the negative log-likelihood function is convex with respect to for all . In the parametric case (3), each triggering function is a linear function of , and therefore is a convex with respect to for all .

Alternatively, other convex loss functions have also been used for parametric estimation of Hawkes processes in the literature, e.g., square loss Bacry et al. (2015a) and logistic loss Menon and Lee (2018). To promote solutions with desired structures, such as sparsity of the triggering matrix or the smoothness of the triggering functions, one can also add proper penalties to these objectives (see, e.g., Bacry et al. (2015a); Zhou et al. (2013); Xu et al. (2016)). The resulting optimization problems are often processed by Expectation Maximization (EM) algorithm (Xu et al., 2016), batch gradient descent, ADMM (Zhou et al., 2013), and so on.

3 Problem Formulation

In this section, we introduce our assumptions and definitions followed by the formulation of the objective function. We omit the basics on MHPs and instead refer the readers to Liniger (2009) for details.

Assumption 3.1.

We assume that the constant base intensity is bounded between and . We also assume bounded and stationary increments for the MHP in the sense that, for a fixed and any , for all .

Definition 3.1.

Suppose that is an arbitrary time sequence with , and . Let be a continuous and bounded function such that . Then, satisfies the decreasing tail property with tail function if

Assumption 3.2.

Let be an RKHS associated with a kernel that satisfies . Let be the space of functions for which the absolute value is Lebesgue integrable. For any , we assume that and , with both and satisfying the decreasing tail property of Definition 3.1.

Assumption 3.1 is common and has been adopted in existing literature (Liniger, 2009; Hawkes, 1971; Brémaud and Massoulié, 1996). In particular, it ensures that the MHP is not “explosive” by assuming that is bounded. A simple analysis shows that this condition likely holds: for an MHP with stationary increments, we have where denotes the -algebra generated by , counts the number of arrivals for all dimensions, and collects the intensity functions of the dimensions. Taking another expectation and combining the stationary increment assumption, we have

where is a positive constant vector that represents the average growth rates of s. On the other hand, using the second order statistics of Hawkes processes in Bacry et al. (2015a), we know that the covariance matrix of a Hawkes process is given by

where is a matrix in Theorem 1 of Bacry et al. (2012b). This shows that has a fixed mean and a covariance that converges to as . Therefore, asymptotically, for all .

Assumption 3.2 restricts the tail behaviors of both and . Intuitively, it restricts the total impact of the historic events on the intensity function, and hence also guarantees that the MHP under consideration is not “explosive”. As it turns out, corresponds to the set of update time when designing the online algorithm. Complicated as it may seem, functions with exponentially decaying tails satisfy this assumption, as is illustrated by the following examples:

Example 1.

The function with satisfies Assumption 3.2 with as its tail function.

Proof of Example 1.

When , is a monotonically decreasing function. Therefore, for any -update set, we have Hence,

where the inequality is due to the fact that, for and , . Summing up both sides of the above inequality, we have

Similarly, one can obtain the tail functions of that is .

∎

Example 2.

The function satisfies Assumption 3.2 with as its tail function.

Proof or Example 2.

For , we have in which we used the fact that . Hence, a tail function for is

For the derivative of and for , we have This implies the following tail function for :

∎

3.1 A Discretized Objective Function for Online Estimation

A main challenge in nonparametric estimation of MHPs arises from the lack of representer theorem, which is often necessary for reducing the complexity of function estimation. Note that in the case of MHPs, the negative log-likelihood function, given in (4), contains an integral term of , i.e., it depends on for all rather than a discrete set. Thus it does not satisfy the condition required for representer theorem as shown in Theorem 1.

To resolve this issue, several approaches are recently proposed: (i) the discretization approach (Hall and Willett, 2016), which approximates the integral by its Riemann sum; (ii) the adjusted Hilbert space approach (Flaxman et al., 2017; Raskutti et al., 2012), which transforms the integral term together with the RKHS norm defined on into a new RKHS norm defined on . The latter approach, however, only applies to inhomogeneous Poisson process and cannot be easily generalized to the complicated MHPs. Moreover, it requires solving an unfavorable non-convex optimization problem. Due to these considerations, we adopt the first approach and discretize the integral.

Let denote the arrival times of all the events within and let be the end points of a finite partition of the time interval such that and In addition, without loss of generality, we assume . Using this partitioning, it is straightforward to see that the function in (4) can be written as

| (5) |

where . By the definition of , we know that either corresponds to the arrival time of an event, or the end of an interval in which no events arrived, which implies . We now approximate the integral by , and thus obtaining

| (6) |

Intuitively, if is small enough and the triggering functions are bounded, it is reasonable to expect that is close to . Below, in Proposition 1, we characterize the accuracy of the above discretization of the intensity function.

Another challenge in nonparametric estimation of MHPs comes from the expensive computation cost when evaluating the functional gradient of the objective, which requires the evaluations of for . To perform fast evaluation of the intensity function, we introduce the concept of “truncated intensity”, denoted by , by considering the impact of only those events that arrived within a recent window .111Since the probability that an event arrive at is , it does not matter whether the interval is close or open on the left-hand side. Since for , it does not matter whether the interval is open or close on the right-hand side. Similar to discretization, the approximation error caused by the truncation can be well-controlled given Assumptions 3.2 and 3.1. We now formally define the truncated intensity function before characterizing the truncation error together with the discretization error in Proposition 1.

Definition 3.2.

We define the truncated intensity function as follows

| (7) |

Proposition 1.

The first term in the bound characterizes the approximation error when one truncates with . The second term describes the approximation error caused by the discretization. When , , and the approximation error is contributed solely by discretization. In many cases, a small enough truncation error can be obtained by setting a relatively small , which greatly simplifies the evaluation procedure and effectively captures the effect of those important “recent” events. For example, for , setting would result in a truncation error less than . Therefore, in our algorithm, we evaluate the intensity functions with their truncated versions.

Finally, to invoke the representer theorem, we consider the regularized instantaneous risk function with Tikhonov regularization for s and :

| (8) |

and aim at producing a sequence of estimates of with minimal regret:

| (9) |

In (8), and are positive regularization coefficients. Adding the regularization terms in (8) not only allows us to apply the representer theorem, but also accelerates the gradient descent as the regularized instantaneous risk function is now strongly convex. Notice that a tradeoff exists between the optimality of the solution and the algorithmic stability: for large and , the algorithm is more stable but the objective function deviates from the negative log-likelihood of MHP, whereas for small and , the objective function is closer to the negative log-likelihood function but the algorithm becomes less stable due to the lack of regularization.

4 Online Estimation for Multivariate Hawkes Processes

We introduce our NonParametric OnLine Estimation for MHP (NPOLE-MHP) in Algorithm 1. We adopt an online gradient descent (OGD) framework as it achieves the known optimal asymptotic average regret among all online convex optimization algorithms. In particular, NPOLE-MHP updates the estimates of and at each iteration using the corresponding gradient. The most important components of NPOLE-MHP are (i) the computation of the gradients and (ii) the projection operation, in lines 6 and 8, respectively. We now illustrate those procedures in detail.

4.1 Computation of the Gradient

The computation of the gradient include two aspects: derivatives with respect to (i) , and (ii) .

Partial derivative with respect to . Recall the definition of in (8) and in (7). It is easy to see that , and therefore by chain rule, we have

For simplicity, we define the following quantity

| (10) |

which gives us

| (11) |

Upon performing the gradient descent step on , the algorithm checks whether it is below . Since the triggering functions are constrained to be positive at each step of the algorithm, forcing guarantees that and is bounded away from 0 at each step of the algorithm.

Partial derivative with respect to s. We next discuss the update step for in line 8 of the algorithm. By the reproducing property of the kernel, we have

Therefore, by chain rule, we have

| (12) |

Afterward, a projection is necessary to ensure that the estimated triggering functions are positive. According to representer theorem, the optimal positive function is a finite summation, and therefore, we define the projection operation for any , with , to be

| (13) |

It is worth pointing out, however, that MHPs can be generalized so that the triggering functions need not be positive, as long as the intensity function is lower bounded by some constant . For the generalized MHPs, the arrival of the events on one dimension potentially reduces the arrival rates of events in other dimensions, which happens in many applications. For example, the consumption of medication prevents the arrivals of heart attacks. While we restrain our attention to the less general case of positive triggering functions, our algorithm can be generalized to adapt to the more general case by modifying the projection step in line 8 such that for each .

4.2 Projection of the Triggering Functions

In general, the projection step of the triggering function requires solving a constrained quadratic programming (QP) problem: subject to and . For NPOLE-MHP, we have and for some set due to the representer theorem, and the projection operation on reduces to solving a QP on the coefficient vector :

where is the Gramian matrix. As is given, minimizing the distance between and is equivalent to minimizing the above quadratic form with respect to . Notice that the constraint has to hold for every , resulting in infinite number of constraints in general. In order to simplify computation, one can approximate the solution by relaxing the constraints such that holds for only a finite set of s within .

Semidefinite programming (SDP) for polynomial kernels. When the reproducing kernel is a polynomial kernel defined over , we can exploit its unique structure to formulate the projection as an SDP. This is mainly due to the solution of Hilbert’s 17th problem (Bochnak et al., 2013), which states that a -degree polynomial is nonnegative if and only if it can be written as the sum of -degree polynomials. In particular, let and , then is equivalent to where is the feature map of : . With this intuition, the projection step can be formulated as an SDP problem (Vandenberghe and Boyd, 1996) as follows:

Proposition 2.

Let be the set of s. Let and be two polynomial kernels with . Furthermore, let and denote the Gramian matrices where the -th element correspond to and , with and being the -th and -th element in . Suppose that is the coefficient vector such that , and that the projection step returns . Then the coefficient vector can be obtained by

| (14) |

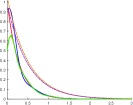

Nonconvex approaches. Alternatively, positivity can be guaranteed by assuming or , where . By minimizing the loss with respect to , one can naturally guarantee that . This method was adopted in Flaxman et al. (2017) for estimating the intensity functions of nonhomogeneous Poisson processes. The drawback of this approach is that the objective function is no longer convex. However, as will be demonstrated in Figure 1, the output of this method converges aligns with the ground truth when the initialization is close to the global minima.

4.3 Computational Complexity

Since s can be estimated in parallel, we restrict our analysis to the case of a fixed in a single iteration. For each iteration, the computational complexity comes from evaluating the intensity function and projection. Since the number of arrivals within the interval is bounded by and , evaluating the intensity costs operations. For the projection in each step, one can truncate the number of kernels used to represent to be with controllable error (Proposition 1 of Kivinen et al. (2004)), and therefore the computation cost is . Hence, the per iteration computation cost of NPOLE-MHP is . By comparison, parametric online algorithms (DMD, OGD of Hall and Willett (2016)) also require operations for each iteration, while the batch estimation algorithms (MLE-SGLP, MLE of Xu et al. (2016)) require operations, which is caused by the update of the EM algorithm.

5 Theoretical Properties

We now discuss the theoretical properties of NPOLE-MHP. We start with defining the regret.

5.1 Regret Bounds

Definition 5.1.

The regret of Algorithm 1 at time is given by

where and denote the estimated base intensity and the triggering functions, respectively.

Theorem 2.

The regret bound of Theorem 2 resembles the regret bound for a typical online learning algorithm with strong convex objective function (see for example, Theorem 3.3 of Hazan et al. (2016)). When , and are fixed, , which is intuitive as one needs to update functions at each iteration. Note that the regret in Definition 5.1, encodes the performance of Algorithm 1 by comparing its loss with the approximated loss. Below, we compare the loss of Algorithm 1 with the original loss in (5).

Corollary 1.

Note that is due to discretization and truncation steps and it can be made arbitrary small for given by setting small and large enough .

5.2 Generalization Error Bounds

Generalization error bounds are useful tools to characterize how well an algorithm perform on unseen data. Consider a general nonparametric estimation setting, in which a function is obtained upon minimizing an objective function determined from a set of samples, denoted by the set . The samples within , denoted by , are generated according to some joint distribution, and under a specific objective function , the generalization error bound refers to an upper bound for the following generalization error:

| (16) |

The bound is typically obtained by first noticing , and then providing an upper bound on . For MHPs, we define the generalization error to be

| (17) |

where the expectation is taken over the distribution of the intensity process. Note that, although is the summation of instantaneous objective functions, we average it by instead of . This design is based on the fact that is an approximation of the negative log-likelihood. It also simplifies the analysis since otherwise one would have to take into concern the randomness of .

It is immediate that (17) is drastically different compared to (16) because the correlation between different arrivals: a slight perturbation in the arrival time of one event could lead to changes in both the arrival times and the number of events consequently. Therefore, we consider the generalization error assuming that the number of arrivals is fixed, namely

| (18) |

This notion of generalization error allows us to characterize the performance of NPOLE-MHP from a stability point of view. For MHPs with stationary increments, , . Therefore, by the law of large numbers,

in probability. Hence, for large , can serve the purpose of . We now state the result of (18) in Theorem 3.

Theorem 3.

See Appendix A for proof.

6 Extensions to Marked and Spatial Point Processes

In this section, we generalize NPOLE-MHP to other point processes. In particular, we consider multivariate marked Hawkes processes, and spatial Hawkes processes.

6.1 Multivariate Marked Hawkes Processes

Multivariate marked Hawkes processes (MMHPs) have received relatively less attention compared to their unmarked version. Statistical properties such as limit theorems and the convergence rate to equilibrium state are studied in Karabash and Zhu (2015); Brémaud et al. (2002), whereas a nonparametric estimation framework was proposed in Bacry and Muzy (2016) based on second order statistics.

In this section, we adapt NPOLE-MHP to online estimation of MMHPs. While it is commonly assumed that the marks and the arrivals have independent effects on the intensity function, i.e.,

for some functions and , we do not require this assumption for NPOLE-MMHP.

The key to generalizing NPOLE-MHP to adapt to the existence of marks is to adopt a two dimensional kernel where and are two dimensional vectors consisting of a time variable and the value of the mark. The nonparametric online estimate of the triggering functions can then be obtained by using the following expression of functional gradient in line 9 of Algorithm 1.

Furthermore, when we can update and separately by substituting the functional gradient in line 9 of Algorithm 1 with separate updates of and , with the functional gradients being

and

respectively. However, while the approach exploits the multiplicative structure of the triggering function, the objective function is no longer convex when estimating and separately.

6.2 Spatial Hawkes Processes

Lastly, we generalize NPOLE-MHP to spatial Hawkes processes. Spatial Hawkes processes are Hawkes processes where the arrivals lie within . The -th arrival consists of a time stamp , and a location , and the intensity at at time can be written as

The spatial Hawkes processes can be viewed as a generalization to MHPs, for the latter of which the arrivals are restricted to distinct directions only. As a concrete example, a spatial Hawkes process can be used to model the crime happening in an entire area on the map, while MHPs can only model crimes that happen at certain locations.

We present the adpated version of NPOLE-MHP to spatial Hawkes processes in the following algorithm, where the subscripts in NPOLE-MHP are now ignored as there’s only one base intensity and triggering function.

Particularly, the functional gradient in line 7 of Algorithm 2 takes the form

where has the same form as (10), except that it now depends on the specific location of . As a consequence, the nonparametric estimation of the spatial Hawkes process requires significantly more time and memory due to the increased complexity in evaluating used in the gradient.

7 Numerical Experiments

We now demonstrate the performances of NPOLE-MHP and its generalizations on both synthetic and real data. On synthetic data, we compare our algorithm’s performance to that of online parametric algorithms (DMD, OGD of Hall and Willett (2016)) and nonparametric batch learning algorithms (MLE-SGLP, MLE of Xu et al. (2016)). Our synthetic data is generated by repeatedly evaluating the intensity function upon each arrival, and generating the next arrival as the first arrival among nonhomogenous Poisson processes. Other simulation schemes exist, such as a clustered Poisson process scheme (Dassios et al., 2013).

We use three types of evaluation metrics. (i) We assess the visual goodness-of-fit of estimating each triggering functions. (ii) We compare the numeric performances of the algorithms by measuring the log-likelihood of their estimates. When multiple trials are averaged over synthetic data, we also use a metric named “average error”, which is defined as the average of over multiple trials. (iii) We compare the scalability of NPOLE-MHP over both the dimension and time horizon .

7.1 Synthetic Data for Testing NPOLE-MHP

Consider a 5-dimensional MHP with for all dimensions. We set the triggering functions as

The design of allows us to test NPOLE-MHP’s ability of detecting (i) exponential triggering functions with various decaying rate; (ii) zero functions; (iii) functions with delayed peaks and tail behaviors different from an exponential function.

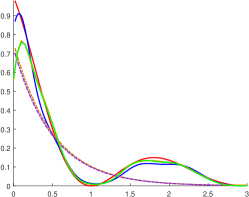

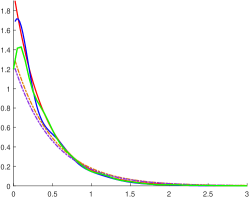

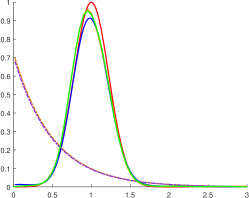

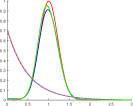

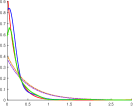

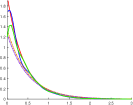

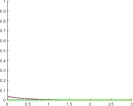

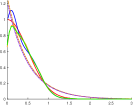

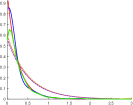

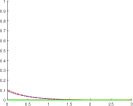

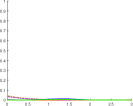

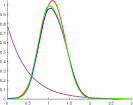

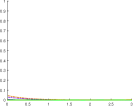

Goodness-of-fit. We run NPOLE-MHP over a set of data with and around events for each dimension. The parameters are chosen by grid search over a small portion of data, and the parameters of the benchmark algorithms are fine-tuned. In particular, we set the discretization level , the window size , the step size , and the regularization coefficient . The performances of NPOLE-MHP and benchmarks are shown in Figure 1. Complete set of results can be found in Appendix E. We see that NPOLE-MHP captures the shape of the function much better than the DMD and OGD algorithms with mismatched forms of the triggering functions. It is especially visible for and . In fact, our algorithm scores a similar performance to the batch learning MLE estimator, which is optimal for any given set of data.

Run time comparison. The simulation of the DMD and OGD algorithms took 2 minutes combined on a Macintosh with two -core Intel Xeon processor at 2.4 GHz, while NPOLE-MHP took 3 minutes. The batch learning algorithms MLE-SGLP and MLE in Xu et al. (2016) each took about 1.5 hours. Therefore, our algorithm achieves the performance similar to batch learning algorithms with a run time close to that of parametric online learning algorithms.

Effects of the hyperparameters: , , and . We investigate the sensitivity of NPOLE-MHP with respect to the hyperparameters, measuring the “averaged error” defined at the beginning of this section. We independently generate 100 sets of data with the same parameters, and a smaller for faster data generation. The result is shown in Table 2. For NPOLE-MHP, we fix . MLE and MLE-SGLP score around 1.949 with 5/5 inner/outer rounds of iterations. NPOLE-MHP’s performance is robust when the regularization coefficient and discretization level are sufficiently small. It surpasses MLE and MLE-SGLP on large datasets, in which case the iterations of MLE and MLE-SGLP are limited due to computational considerations. As increases, the error decreases first before rising drastically, a phenomenon caused by the mismatch between the loss functions. For the step size, the error varies under different choice of , which can be selected via grid-search on a small portion of the data like most other online algorithms.

|

|

|

| (a) | (b) | (c) |

| Regularization | ||||||

| Horizon (days) | ||||

| Dimension | ||||

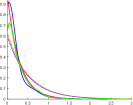

Lastly, we demonstrate the effect of discretization in Figure 3. For , the stepwise loss evaluated with the true s varies very little. When we decrease from 1 to 0.05, however, the performance of NPOLE-MHP improves drastically.

7.2 Inferring Impact Between News Agencies with MHP

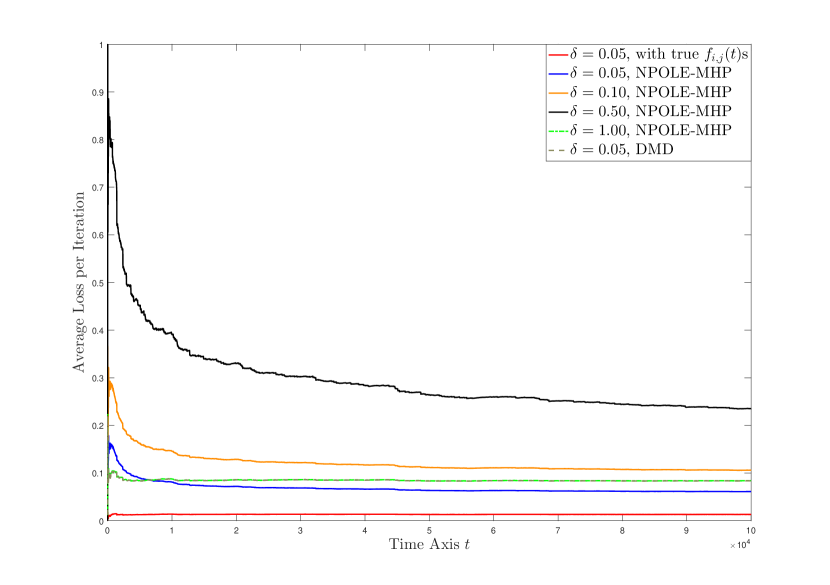

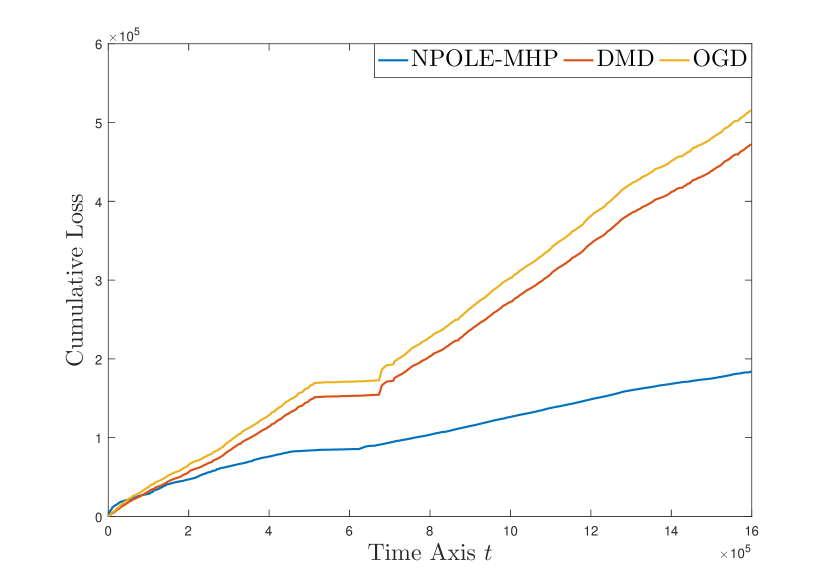

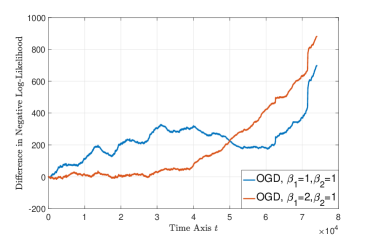

We also tested the performance of our algorithm on the memetracker data (Leskovec et al., 2009). The data collects from the web a set of popular phrases, including their content, the time at which they are published, and the url address of the articles that contributed to these occurrences. We study the relationship between different news agencies, and therefore model the data with a -dimensional MHP where each dimension corresponds to the articles published by a news website. Note that a similar experiment was conducted in Hall and Willett (2016). Unlike Hall and Willett (2016), where all the data is used, we focus on only 20 websites that publish the most number of news articles using 18 days of data. The cumulative objective functions are plotted in Figure 3, where we set the window size to be 3 hours, discretization level second, and step size with for NPOLE-MHP. For DMD and OGD, we set the step size . The result shows that NPOLE-MHP accumulates a smaller loss per step compared to OGD and DMD.

7.3 Inferring Crime Pattern in Chicago with MMHP

|

|

| (a) NPOLE-MMHP | (b)OGD |

|

|

| (c) Mark distribution | (d) Excess regret |

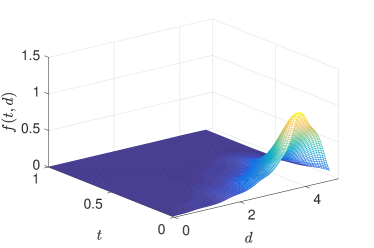

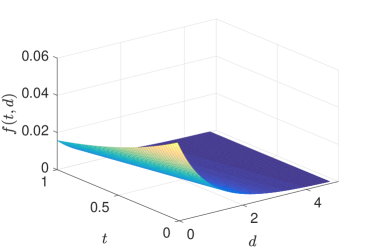

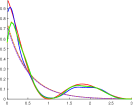

We next demonstrate the performance of NPOLE-MMHP on the Chicago crime data. The dataset collects the time and location information of various types of crimes within a span of 16 years from 2001 to 2017. In this study, we focus on the most common type of crime, thievery, and aim at inferring the impact of each incident on a pre-selected area. In this case, the dimension .

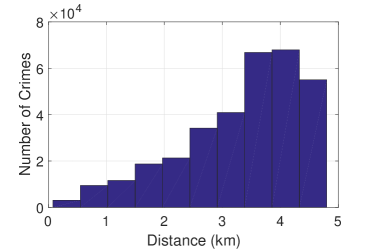

To model the data using an MMHP, we consider the thievery incidents that happen within 3 miles radius of the United Center, located at . Each thievery crime is considered as an event, and the location where it happens serves as its mark. For the sake of reducing computation burden, we simplify the model by assuming that a crime happening at time and location would affect the intensity function by an amount . That is, the location of the crime only matters through its distance towards the selected center of the region. Similar to MHP, we consider only those crimes that happen within a window of , where we set to be 1 hour.

We compare our method with the parametric benchmark: , where is estimated under different choices of pairs using online gradient descent (OGD). We tune the step size on the first 50% of the updates, and use the remaining 50% as test data.

The test results are shown in Figure 4. In Figure 4, we plot the triggering function estimated by NPOLE-MMHP and OGD. As can be seen from Figure 4(c), the majority of the crime happens at around 4km away from the selected area center. Therefore, the result generated by NPOLE-MMHP is a more natural estimation that reflects this piece of information. On the other hand, it can also be seen from Figure 4(d) that the estimation of NPOLE-MMHP generates a slightly lower negative likelihood. Note that for various parameters pairs the performance of OGD varies slightly, indicating that the OGD model is almost merely fitting a Poisson process to the data.

8 Conclusion and Discussions

We developed a nonparametric method for learning the triggering kernels of a multivariate Hawkes process (MHP) given time series observations. To formulate the instantaneous objective function, we adopted the method of discretizing the time axis into small intervals of lengths at most , and we derived the corresponding upper bound for approximation error. From this point, we proposed an online learning algorithm that is based on the framework of online kernel learning and exploits the interarrival time statistics under the MHP setup. Theoretically, we derived the regret bound for our algorithm, which is when the time horizon is known a priori, and we showed that per iteration cost of the proposed algorithm is . Numerically, we compared our algorithm’s performance with parametric online learning algorithms and nonparametric batch learning algorithms. Results o both synthetic and real data showed that we are able to achieve similar performance to that of nonparametric batch learning algorithms with a run time comparable to parametric online learning algorithms.

References

- Bacry et al. (2012a) Bacry, E., Dayri, K. and Muzy, J. F. (2012a). Non-parametric kernel estimation for symmetric hawkes processes. application to high frequency financial data. The European Physical Journal B 85 157.

- Bacry et al. (2012b) Bacry, E., Dayri, K. and Muzy, J.-F. (2012b). Non-parametric kernel estimation for symmetric Hawkes processes. application to high frequency financial data. The European Physical Journal B-Condensed Matter and Complex Systems 85 1–12.

- Bacry et al. (2015a) Bacry, E., Gaïffas, S. and Muzy, J.-F. (2015a). A generalization error bound for sparse and low-rank multivariate Hawkes processes. arXiv preprint arXiv:1501.00725 .

- Bacry et al. (2014) Bacry, E., Jaisson, T. and Muzy, J.-F. (2014). Estimation of slowly decreasing Hawkes kernels: Application to high frequency order book modelling. arXiv preprint arXiv:1412.7096 .

- Bacry et al. (2015b) Bacry, E., Mastromatteo, I. and Muzy, J.-F. (2015b). Hawkes processes in finance. Market Microstructure and Liquidity 1 1550005.

- Bacry and Muzy (2016) Bacry, E. and Muzy, J.-F. (2016). First- and second-order statistics characterization of Hawkes processes and non-parametric estimation. IEEE Transactions on Information Theory 62 2184–2202.

- Bagnell and Farahmand (2015) Bagnell, J. A. and Farahmand, A.-m. (2015). Learning positive functions in a Hilbert space.

- Bao et al. (2017) Bao, Y., Kuang, Z., Peissig, P., Page, D. and Willett, R. (2017). Hawkes process modeling of adverse drug reactions with longitudinal observational data. To appear in Machine Learning and Healthcare .

- Bochnak et al. (2013) Bochnak, J., Coste, M. and Roy, M.-F. (2013). Real algebraic geometry, vol. 36. Springer Science & Business Media.

- Brémaud and Massoulié (1996) Brémaud, P. and Massoulié, L. (1996). Stability of nonlinear Hawkes processes. The Annals of Probability 1563–1588.

- Brémaud et al. (2002) Brémaud, P., Nappo, G. and Torrisi, G. (2002). Rate of convergence to equilibrium of marked hawkes processes. Journal of Applied Probability 39 123–136.

- Dassios et al. (2013) Dassios, A., Zhao, H. et al. (2013). Exact simulation of hawkes process with exponentially decaying intensity. Electronic Communications in Probability 18.

- Eichler et al. (2017) Eichler, M., Dahlhaus, R. and Dueck, J. (2017). Graphical modeling for multivariate Hawkes processes with nonparametric link functions. Journal of Time Series Analysis 38 225–242.

- Etesami et al. (2016) Etesami, J., Kiyavash, N., Zhang, K. and Singhal, K. (2016). Learning network of multivariate Hawkes processes: A time series approach.

- Fauth and Tudor (2012) Fauth, A. and Tudor, C. A. (2012). Modeling first line of an order book with multivariate marked point processes. arXiv preprint arXiv:1211.4157 .

- Flaxman et al. (2017) Flaxman, S., Teh, Y. W. and Sejdinovic, D. (2017). Poisson intensity estimation with reproducing kernels. International Conference on Artificial Intelligence and Statistics .

- Hall and Willett (2016) Hall, E. C. and Willett, R. M. (2016). Tracking dynamic point processes on networks. IEEE Transactions on Information Theory 62 4327–4346.

- Hardiman et al. (2013) Hardiman, S., Bercot, N. and Bouchaud, J.-P. (2013). Critical reflexivity in financial markets: a hawkes process analysis .

- Hawkes (1971) Hawkes, A. G. (1971). Spectra of some self-exciting and mutually exciting point processes. Biometrika 58 83–90.

- Hazan et al. (2016) Hazan, E. et al. (2016). Introduction to online convex optimization. Foundations and Trends® in Optimization 2 157–325.

- Karabash and Zhu (2015) Karabash, D. and Zhu, L. (2015). Limit theorems for marked hawkes processes with application to a risk model. Stochastic Models 31 433–451.

- Kivinen et al. (2004) Kivinen, J., Smola, A. J. and Williamson, R. C. (2004). Online learning with kernels. IEEE Transactions on Signal Processing 52 2165–2176.

- Krumin et al. (2010) Krumin, M., Reutsky, I. and Shoham, S. (2010). Correlation-based analysis and generation of multiple spike trains using Hawkes models with an exogenous input. Frontiers in computational neuroscience 4.

- Leskovec et al. (2009) Leskovec, J., Backstrom, L. and Kleinberg, J. (2009). Meme-tracking and the dynamics of the news cycle. In Proceedings of the 15th ACM SIGKDD International Conference on Knowledge Discovery and Data Mining. ACM.

- Liniger (2009) Liniger, T. J. (2009). Multivariate Hawkes processes. Ph.D. thesis, Eidgenössische Technische Hochschule ETH Zürich.

- McDiarmid (1989) McDiarmid, C. (1989). On the method of bounded differences. Surveys in combinatorics 141 148–188.

- Menon and Lee (2018) Menon, A. K. and Lee, Y. (2018). Proper loss functions for nonlinear hawkes processes .

- Mohler et al. (2011) Mohler, G. O., Short, M. B., Brantingham, P. J., Schoenberg, F. P. and Tita, G. E. (2011). Self-exciting point process modeling of crime. Journal of the American Statistical Association 106 100–108.

- Ozaki (1979) Ozaki, T. (1979). Maximum likelihood estimation of Hawkes’ self-exciting point processes. Annals of the Institute of Statistical Mathematics 31 145–155.

- Porter et al. (2012) Porter, M. D., White, G. et al. (2012). Self-exciting hurdle models for terrorist activity. The Annals of Applied Statistics 6 106–124.

- Raskutti et al. (2012) Raskutti, G., Wainwright, M. J. and Yu, B. (2012). Minimax-optimal rates for sparse additive models over kernel classes via convex programming. Journal of Machine Learning Research 13 389–427.

- Reynaud-Bouret et al. (2010) Reynaud-Bouret, P., Schbath, S. et al. (2010). Adaptive estimation for Hawkes processes; application to genome analysis. The Annals of Statistics 38 2781–2822.

- Schölkopf et al. (2001) Schölkopf, B., Herbrich, R. and Smola, A. J. (2001). A generalized representer theorem. International Conference on Computational Learning Theory 416–426.

- Vandenberghe and Boyd (1996) Vandenberghe, L. and Boyd, S. (1996). Semidefinite programming. SIAM review 38 49–95.

- Xu et al. (2016) Xu, H., Farajtabar, M. and Zha, H. (2016). Learning Granger causality for Hawkes processes. International Conference on Machine Learning 48 1717–1726.

- Yang and Zha (2013) Yang, S.-H. and Zha, H. (2013). Mixture of mutually exciting processes for viral diffusion. International Conference on Machine Learning 28 1–9.

- Yang et al. (2017) Yang, Y., Etesami, J., He, N. and Kiyavash, N. (2017). Online learning for multivariate Hawkes processes. Neural Information Processing Systems .

- Zhou et al. (2013) Zhou, K., Zha, H. and Song, L. (2013). Learning triggering kernels for multi-dimensional Hawkes processes. In International Conference on Machine Learning, vol. 28.

Appendix A Generalization Error Bound

Proof of Theorem 3.

General settings for the proof. Suppose that there are arrivals, and for each , denote the interval within which the -th arrival falls using . We wish to prove the statement by invoking the concentration inequality of bounded difference. Therefore we consider two sets of arrival times: and that differ by only one element: and , and denote the update times of NPOLE-MHP given and as and , respectively.

By the design of the update rule, there exist , such that and . Notice that and need not be the same because the difference in the arrival times could span multiple intervals of length , resulting in multiple updates in between. However, when the underlying MHP has stationary increments, , implying that . Therefore, we can assume without loss of generality.

Suppose that the solution to the optimization problem (9) is when the arrival times is the set , and when the set of arrival times is the set . To avoid confusion, we write when referring to the objective function evaluated at , with the update times coming from the arrival set .

Outline of the proof. The proof can be obtained following the outline below.

-

•

First, we show that the discretized objective function with the truncated is Lipschitz continuous with respect to , with a Lipschitz constant . That is, for any , we have

(19) where

-

•

Second, when the regularization coefficient for is , and when ,

(20) which holds as a property of the RKHS.

-

•

Next, for and learned from and , respectively, we have

(21) -

•

Lastly, we prove the generalization error bound by combining the first three steps and invoking the McDiarmid concentration inequality.

Step 1: Proving the Lipschitz continuity, (19). By the definition of the objective function, we have

| (22) |

where in the last step, we have assumed, without generality, that is much smaller than . In addition, we have also used the fact that is -Lipschitz continuous when .

It is not hard to see that proving (19) now reduces to proving the Lipschitz continuity of for every . Indeed,

| (23) |

Step 2: Proving (20). Equation (20) holds as a property for the RKHS. Since , we have

for any . Therefore (20) holds by taking supremum over on both sides in the above inequality.

Step 3: Proving (21). We now turn to prove (21), which upper bounds the RKHS norm of the difference between and . The upper bound on the right-hand side decays at the speed of . This implies that the more updates used for learning and , the less likely that they will be different when we slightly perturb the arrival epoch of a single event.

To formally show this, fix . In addition, for notational simplicity, we denote by , and define the instantaneous objective function without regularization as

Let be a strictly convex function. Then the Bregman divergence with respect to is defined as

Set , then , and we have which further implies

Adopt the following functional notation, where :

and

Consider two choices of : . Recall from the previous steps that those are the solutions to the optimization problem (9) when the observed sample sets are and , respectively. It is not hard to see that the functional is strictly convex with respect to , and therefore the Bregman divergence can be defined for as well. Hence, by the linearity of the Bregman divergence with respect to , we have

where the second step holds true since and are the minimizers and the gradient of the first order terms in the definition of and become zero. Notice that and only differ in one element, which occurs at the -th update of NPOLE-MHP. As a consequence, this element in question only affects at most two instantaneous objective functions: and . Therefore,

and

From (A), we know that the Lipschitz continuity holds for any instantaneous objective function without regularization. Therefore,

which gives us the desired equation (21), upon noticing that .

Step 4: Invoking McDiarmid concentration inequality. Combining (20) and (21), we have

which implies

Plugging the above result into (19), we have

| (24) |

This gives us the argument that has bounded difference when one slightly perturbs one instance in the training data of . It can also be shown that is bounded, by noticing that

Furthermore, when one fixes , and perturbs , the upper bound given in (A) is independent of the choice of . Therefore, we can invoke the generalized McDiarmid inequality in the form of Corollary 6.10 of McDiarmid (1989), and obtain

∎

The covering number and the -net argument. Suppose that the true lies within the part of the Hilbert space where , and denote this part of the RKHS as . Let be an -net for . Then, for any , there exists such that . Recall that the risk function is -Lipschitz, we have

Therefore,

For different RKHSs, has different forms. For the RKHS associated with a one-dimensional Gaussian kernel,

Therefore, for any with , we can pick , and

Therefore the generalization error bound of the optimization problem (8) is .

Appendix B Proof of Proposition 1

Fix the triggering functions and the constant base intensity . Then,

| (25) |

We bound the first term on the right-hand side that is corresponding to the truncation error as follows:

| (26) |

First, we define . Using the fact that , we obtain

| (27) |

where is a tail function such that for any and , . The above inequality is due to Assumption 3.2. Suppose that the -th arrival of the -th dimension is in . Then,

| (28) |

The last inequality uses Assumption 3.2 and the fact that the number of arrivals in an interval of length one is bounded by . Therefore, by combining (B) with (B) and (B), we get

| (29) |

We now proceed to bound the second term in (25). By the definition, we have

| (30) |

To bound the right-hand side, using the definition of , we have that (30) is bounded above by

where is a tail function such that for any and , . In the above equations, (a) uses the fact that in an interval , arrivals can only happen at the endpoints. Moreover, (b) uses Assumption 3.2. Using the upper bounds of (30) and (29) in (25) will imply the result.

Appendix C Proof of Theorem 2

We prove this regret bound following the proof technique for Theorem 4 of Kivinen et al. (2004) and the proof technique for Theorem 3.3 of Hazan et al. (2016). The outline of this proof is as follows:

-

•

Firstly, we derive the following upper bound:

(31) -

•

Next, we derive the following upper bound:

(32) To do this, we need three separate steps:

-

–

Prove the Lemma 1, which we state below.

-

–

Prove that the instantaneous objective function is strongly convex with respect to and .

- –

-

–

- •

Step 0: Technical assumptions and lemma. Before the main body of the proof, we need to introduce the following technical assumption, as well as a lemma that bounds the -norm of . These result will be frequently referred to throughout the main body of the proof.

Assumption C.1.

We assume that is set small enough such that .

This assumption does not affect the implementation of the algorithm since and are both manually set.

Assumption C.2.

We assume that the initialization of the algorithm is nice enough:

and

Similar to C.1, this assumption does not affect the implementation of the algorithm as we can set to be small.

The following lemma is needed in Step 2, and will be proved in Step 2.

Lemma 1.

We are now ready to prove the main part of the theorem.

Step 1: Proving equation (31). We start the proof of (31) by observing the following fact: given , the objective function is -strongly convex with respect to and the square operator. This implies that

which further indicates that

| (34) |

By the update rule, we have

Since the projection is contractive, we have

Hence,

| (35) |

It is not hard to verify that is bounded: first, notice that

| (36) |

where the last step uses the result , which is a direct consequence from Assumption C.1. By the update rule of , we can see that if , then

Therefore by Assumption C.2 and mathematical induction, for every . Combining this result with (C), we have

| (37) |

With (C), (37) and (34), we have

where in the last step, we have invoked the assumption that when , and for 222we assume since was not involved in the summation., . Furthermore, Hence, plugging this result into the previous equation, we have

completing the proof of Step 1.

Step 2: Proving equation (32). The proof of (32) follows the same procedure as the proof of (31). However, proving the counterpart of (37) is more complicated. We stated it in Lemma 1, and we now formally prove it.

Step 2.1: Proof of Lemma 1.

Recall from equation (12) that, at the -th update epoch, the update rule for can be written as

where, by Assumption 3.2, for all . Since we have used the truncated intensity function , we have, by triangle inequality,

where is the window size that is selected at the beginning of the algorithm. Here, we have used the assumption that the number of arrivals within is upper bounded by , by Assumption 3.1. In addition, by the design of the algorithm, we always have Hence, when ,

| (38) |

where in the last step of (C), we have used the technical assumption C.1. When the algorithm initializes with satisfies Assumption C.2, i.e.,

we can use induction and (C) to show that every satisfies the above bound. In addition, by (12), we have

Similarly, when , the term vanishes because , and hence we reach the desired statement.

Step 2.2: Strong convexity of the objective function. The instantaneous objective function is strongly convex in the following sense:

In particular, the instantaneous objective function is strongly convex with respect to any one of the s and when the remaining are fixed. The proof follows directly from the strong convexity of .

Step 2.3: Proof of (32). We now prove (32). By the strong convexity of the instantaneous objective function proved in Step 2.2, we have

| (39) |

This can be written as follows

| (40) |

For any , since and is contractive, we have

Therefore,

| (41) |

Using Lemma 1, we have

when , and

when .

We now proceed to final step, which sums (40) over and then combines the result with (41) summed over . To obtain stronger intuition, we choose to use the uniform upper bound for , which holds for all values of . We thus obtain

| (42) |

Since , we obtain

Furthermore, . Therefore, substituting the above inequalities into (C), we get

Step 3. The overall regret bound can be obtained by adding (31) and (32).

C.1 Proof of Corollary 1

Appendix D Proof of Proposition 2

Generally speaking, the projection operation is a QP problem:

| (43) |

Recall , where Hence, (43) can be written as

| (44) |

Let be the RKHS with kernel , for some integer . By the solution of Hilbert’s 17th problem (Bochnak et al., 2013), we know that a 1-dimensional and -degree polynomial is nonnegative iff it can be written as the sum of squares of -degree polynomials, i.e., a quadratic form of -degree polynomials. This allows us to substitute the constraint in (44) with , where is the feature map of the kernel function , i.e., .

Appendix E Experiment Details

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

| (a) MLE estimate with 8 outer loops and 8 inner loops. | (b) NPOLE-MHP esitmate with . |

|

|

| (c) NPOLE-MHP esitmate with . | (d) NPOLE-MHP esitmate with . |

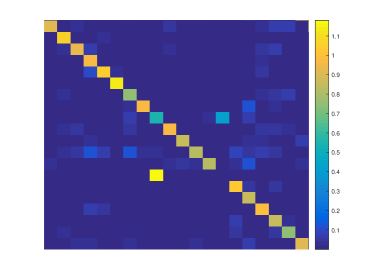

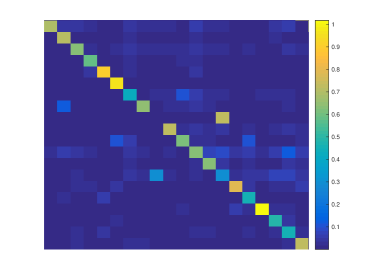

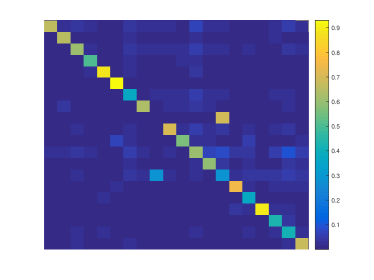

In this section, we show the complete set of estimates for the estimates on synthetic data, in Figure 5, and on real data, in Figure 6.

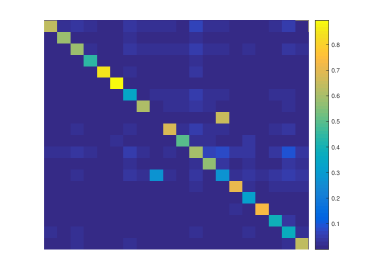

For the real data, we compare the values of by converting them into color maps (Figure 6). Top left corner, is computed using the output of MLE of Xu et al. (2016) with 8 outer loops and 8 inner loops, respectively, using 18 days of the meme-tracking dataset. For the rest of the three plots, we calculate using the output of NPOLE-MHP with different step sizes. It can be seen that NPOLE-MHP generates similar sparsity patterns to that of MLE where the diagonal dominates.