Risk Apportionment: The Dual Story††thanks: With great sadness, we lost our friend and co-author Harris Schlesinger, who passed away while we were in the process of writing this paper. We are very grateful for detailed comments from Sebastian Ebert, Johanna Etner, Christian Gollier, Glenn Harrison, Mike Hoy, Liqun Liu (discussant), Lisa Posey (discussant), Nicolas Treich, Michel Vellekoop, and Claudio Zoli. We are also grateful to conference and seminar participants at the EGRIE Meeting, the Risk Theory Society Meeting, the World Risk and Insurance Economics Congress, the Tinbergen Institute, and the KAFEE seminar at the University of Amsterdam for helpful comments. This paper was circulated earlier under the title “Prudence, temperance (and other virtues): The dual story”. This research was funded in part by the Netherlands Organization for Scientific Research (Laeven) under grant NWO VIDI.

Abstract

By specifying model free preferences towards simple nested classes of lottery pairs,

we develop the dual story to stand on equal footing with that of

(primal) risk apportionment.

The dual story provides an intuitive interpretation, and full characterization,

of dual counterparts of such concepts as prudence and temperance.

The direction of preference between these nested classes of lottery pairs

is equivalent to signing the successive derivatives of the probability weighting function

within Yaari’s (1987) dual theory.

We explore implications of our results for optimal portfolio choice

and show that the sign of the third derivative of the probability weighting function

may be naturally linked to a self-protection problem.

Keywords: Higher Order Risk Attitudes; Prudence; Temperance;

Risk Apportionment; Dual Theory; Portfolio Choice; Self-Protection.

JEL Classification: D81, G11, G22.

1 Introduction

Although first received with some skepticism, the notions of prudence and temperance have now been widely accepted almost on par with the fundamental concept of risk aversion, at least in an expected utility (EU) framework.

The expanding use of these notions, sometimes termed “higher order risk attitudes”, can be explained by the fact that they were progressively given a more general interpretation. Consider prudence, for instance. This term was coined by Kimball (1990) in an influential paper in which he showed that precautionary savings as an optimizing type of behavior is characterized in an EU framework by a positive third derivative of the utility function (i.e., “” or “prudence”). However, it is by now well-known that this positive sign of can be justified more generally outside the specific decision problem of saving. This more primitive justification of prudence was initiated by Menezes, Geiss and Tressler (1980), who used the term “downside risk aversion”, and it was further pursued in Eeckhoudt and Schlesinger (2006), who also showed how to proceed from prudence to higher order risk attitudes. These authors first state a “model free” preference, namely that decision makers (DM’s) like to “combine good with bad” instead of having to face either everything good or everything bad. Next, this model free preference is shown to be translated into prudence () within the EU model, and from prudence—by defining a sequence of nested lotteries and always asserting the preference for combining good with bad—the higher order risk attitudes may be obtained similarly, starting with temperance () at the fourth order.

It turns out besides that the simple primitive interpretation of prudence and higher order risk attitudes found in Eeckhoudt and Schlesinger (2006) lends itself easily to experimental verification. As a result, there is now an intensive experimental research activity around the concepts of prudence and temperance in an EU framework (e.g., Ebert and Wiesen (2011, 2014), Deck and Schlesinger (2010, 2014), and Noussair, Trautmann and van de Kuilen (2014), to name a few).

The preference for “combining good with bad” has appeared under different names in the literature. It was called “risk apportionment” in Eeckhoudt and Schlesinger (2006). A little earlier, Chiu (2005) referred to a “precedence relation”, in which one stochastic dominant change precedes another. The phrase “combining good with bad” as a primitive trait first appeared in Eeckhoudt, Schlesinger and Tsetlin (2009).

While prudence, temperance, and higher order risk attitudes can be presented initially as natural properties in a model free environment, their interpretation and implementation have been developed so far exclusively within an EU framework.111In very recent work, Baillon (2017) generalizes these interpretations of prudence and higher order risk attitudes to a setting featuring ambiguity. In this paper, by specifying new model free preferences towards simple nested classes of lottery pairs, we develop the dual story to stand on equal footing with that of (primal) risk apportionment. The dual story provides an intuitive interpretation, and full characterization, of dual counterparts of such concepts as prudence, temperance, and other virtues. We show that the direction of preference between the nested classes of lottery pairs that we construct is equivalent to signing the derivative of the probability weighting (or distortion) function within Yaari’s (1979) dual theory (DT), with an arbitrary positive integer.222One may therefore say that this paper constitutes the genuine appropriate dual counterpart of (primal) risk apportionment (Eeckhoudt and Schlesinger (2006)). Indeed, from a technical perspective, the contribution of the present paper to the extant literature on (dual or inverse) stochastic ordering in DT (e.g., Muliere and Scarsini (1989), Wang and Young (1998) and Chateauneuf, Gajdos and Wilthien (2002)) is similar to the contribution of Eeckhoudt and Schlesinger (2006) to the literature on (primal) stochastic ordering in EU (e.g., Whitmore (1970), Ekern (1980) and Menezes, Geiss and Tressler (1980)). It turns out that this development requires a fundamental departure from the approach of Eeckhoudt and Schlesinger (2006), which, as we will show, is unable to deliver the desired implications within the DT framework. The dual story we develop retains generic features of the primal story—e.g., a precedence relation—but crucially departs from it in its construction and implementation—e.g., by reference to what we will refer to as “squeezing” and “anti-squeezing” and to the “dual moments”.

This paper thus represents a first step towards a more general interpretation of higher order risk attitudes within alternative non-EU decision models, such as rank-dependent utility and prospect theory (Kahneman and Tversky (1979), Quiggin (1982), Schmeidler (1986, 1989), Tversky and Kahneman (1992)), for which DT is a building block. Indeed, because DT is “orthogonal” to EU, our analysis not only reveals the differences with the primal story under EU, but it is also a prerequisite for a development of higher order risk attitudes as primitive traits of behavior compatible with the more general models of choice under risk provided by rank-dependent utility and prospect theory.

A positive sign of the third derivative of the probability weighting function is consistent with an “inverse S-shape”, exhibited by the popular probability weighting functions proposed by Tversky and Kahneman (1992) (see also Wu and Gonzalez (1996, 1998)) and Prelec (1998) under typical parameter sets implied by experiments.333The inverse S-shape reflects the psychological notion of diminishing sensitivity (in the domain of probabilities), which stipulates that DM’s become less (more) sensitive to changes in the objective probabilities when they move away from (towards) the reference points 0 and 1. These inverse S-shaped probability weighting functions typically feature a positive sign for the odd derivatives and an alternating sign (first negative at low wealth levels, then positive at high wealth levels) for the even derivatives. Provided that the probability weighting function is first concave and then convex with second derivative equal to zero at the inflection point, a positive sign of the third derivative of the probability weighting function implies that the function becomes more concave when moving to the left of the inflection point and becomes more convex when moving to the right of the inflection point.

As is well-known, primal and dual stochastic dominance coincide up to the second order and may diverge from the third order onwards. As a by-product, which is of interest in its own right, the model free story appropriate for DT will nicely make apparent the fundamental reason behind this divergence.

Our results about the shape of the probability weighting function are relevant for the analysis of well-known problems in the economics of risk, such as portfolio choice and the level of self-protection in the presence of background risk. We first illustrate our results by deriving their implications for optimal portfolio choice with a risky asset, a risk-free asset and access to zero-mean financial derivative products on the risky asset. We show that, contrary to under EU (Gollier (1995)), an order improvement of the risky asset’s return, achieved by supplementing (hence, squeezing) the risky asset with an appropriate selection of derivative products (e.g., a straddle at the third order or a volatility spread at the fourth order), never reduces the demand for the risky asset under the DT model. Furthermore, we show that the third derivative of the probability weighting function naturally appears in a self-protection problem that trades off the risk of a loss and the effort of protecting against the loss, in the presence of an independent background risk. In particular, if the third derivative of the probability weighting function is positive (“dual prudence”), the background risk stimulates self-protection.

This paper is organized as follows. In Section 2, we fix the notation and setting, introduce some preliminaries for the DT decision model, and provide some basic intuition behind our results. In Section 3, we introduce dual higher order risk attitudes by developing new model free preferences. Section 4 illustrates implications of our results for optimal portfolio choice. Section 5 shows that the sign of the third derivative of the probability weighting function is naturally linked to a self-protection problem. Section 6 contains the formal presentation of our general results. We conclude in Section 7 with a summary of the results and an indication of potential extensions. Proofs are relegated to the Appendix.444Some supplementary material, including two illustrations and some technical details to supplement Section 2.2, some further details to supplement Section 5, and some technical details to supplement the Appendix, suppressed in this version to save space, is contained in the extended online version of this paper that is available from the authors’ webpages (see http://www.rogerlaeven.com).

2 Preliminaries

2.1 Notation and Setting

We represent an -state lottery , assigning probabilities to final wealth outcomes , , by . We always assume that states are ordered according to their associated outcomes, from the lowest outcome state to the highest outcome state. Outcomes are assumed to be non-negative. That is, . With each lottery, generating a probability distribution over outcomes, one can associate a random variable. Henceforth, the lottery and its associated random variable are often identified. We write , with and the cumulative and decumulative distribution functions of , respectively. Furthermore, we denote by a (weak) preference relation over lotteries.

Under Yaari’s (1987) dual theory (DT), the evaluation of the -state lottery is given by

| (2.1) |

with and by convention, and with satisfying , , and , a probability weighting (or distortion) function, henceforth assumed to be differentiable for all degrees of differentiation on .555In the literature, following Yaari (1987), the evaluation under DT is often carried out by distorting the decumulative distribution function instead of the cumulative distribution function as in (2.1). Notice, however, that with , mapping the unit interval onto itself and satisfying , , and , and that positive signs of the higher order derivatives of are equivalent to alternating signs of the higher order derivatives of . In particular, concavity of translates to convexity of . To be consistent with the alternating signs of the derivatives of the utility function in the EU model, we define the evaluation under DT by distorting the cumulative distribution function rather than the decumulative distribution function . Thus, in our setting a concave probability weighting function is equivalent to “strong” risk aversion in the sense of aversion to mean preserving spreads (Chew, Karni and Safra (1987) and Roëll (1987)), and, more generally, the higher order derivatives of the probability weighting function will naturally alternate in sign, just like that of . We sometimes denote by the derivative of .666We use the notations , and , interchangeably.

We say that a lottery dominates a lottery in third-degree dual (or inverse) stochastic dominance order if

Here, () and () are two independent draws from lottery (). Furthermore, , , , with , and inequalities between functions are understood pointwise. We refer to as the “dual moment” of .777In statistics, these moments are sometimes referred to as mean (first) order statistics. They measure the expected worst outcome in an experiment with repeated independent draws; see also David (1981). Primal moments occur under EU when considering power functions as utility functions. Similarly, dual moments occur under DT when considering power functions as probability weighting functions: with and , . Observe that the power probability weighting function satisfies , hence . In full generality, we say that lottery dominates lottery in -degree dual stochastic dominance order () if

Preferences for order dual stochastic dominance, with first dual moments equal, are well-known to be linked to the sign of the derivative of the probability weighting function within DT (Muliere and Scarsini (1989)), just like primal stochastic dominance orders are connected to the successive derivatives of the utility function under EU (Ekern (1980)). For further details on dual (inverse) stochastic dominance, we refer e.g., to De La Cal and Cárcamo (2010) and the references therein.

Under EU the sign of the derivative of the utility function can be interpreted by comparing simple nested pairs of lotteries with equal primal moments, obtained via the apportionment of harms (Eeckhoudt and Schlesinger (2006)). To interpret the sign of the derivative of the probability weighting function under DT, we develop simple nested lottery pairs that have equal dual moments.

2.2 Illustration and Intuition

Since it is well-known that EU and DT agree at the first and second orders in their evaluation of a sure reduction in wealth and a mean preserving spread (see Yaari (1986), Chew, Karni and Safra (1987), Roëll (1987) and Muliere and Scarsini (1989)) we develop here a numerical example to illustrate that they may diverge at the third order. This example builds the intuition behind the reason why EU and DT may diverge at the third order and motivates the adjustments that have to be made to the story of “combining good with bad” used to interpret the signs of the successive derivatives of the utility function under EU. While it is known that third order primal and dual stochastic dominance do not in general coincide (see Muliere and Scarsini (1989) and its references), we illustrate their potential divergence here in the context of (primal) risk apportionment (Eeckhoudt and Schlesinger (2006)).888In this context, similarly, EU and DT may agree at the third order, such as in their evaluation of the specific case of Mao’s (1970) lotteries considered also by Menezes, Geiss and Tressler (1980) (see the extended online version), or may not agree, such as in the example presented in this section.

We start from an initial lottery given by

and, invoking (primal) risk apportionment, “add” the independent zero-mean risk given by

to one of the states of . If is added to the first state of (which is the bad one) we generate a lottery given by

while if it is added to the second state (which is the good one) we generate a lottery given by

From Eeckhoudt and Schlesinger (2006), we know that under EU, implies .999Lottery is obtained from lottery by adding the bad risk (bad since is second order stochastically dominated by ) to the good state of while the converse is true for . One might alternatively say that in the bad () precedes the good (). Conversely, in the good () precedes the bad (). If the DM has a quadratic utility (hence, “” or “zero prudence”) he is indifferent between and .

Now consider a DM under the DT model with a quadratic probability weighting function:

with and so that , and is non-decreasing and concave.101010Note that by definition. Furthermore, to have , should hold. Hence, , so that . To have (hence whenever ), should hold. Finally, so if . In sum, and . This DM has “zero dual prudence” (“”). Simple computations reveal that for this DM, with strict inequality whenever (hence, ). Thus, there is a difference of opinions between the EU DM, who is indifferent between and under zero primal prudence, and the DT DM, who prefers over under zero dual prudence.

The divergence of opinions between these two DM’s can be related to a difference between the primal and dual moments of and . Clearly, and have the first two primal moments (mean and variance) in common. Their second dual moments are, however, different.111111Indeed, while .

It thus appears that the model free prescription that favors “combining good with bad” in the particular way as suggested by Eeckhoudt and Schlesinger (2006) leads to an interpretation of the signs of the successive derivatives of within the EU model; however, this model free principle does not always generate a similar interpretation for the signs of the successive derivatives of the probability weighting function under the DT framework. Thus, if one desires to obtain for DT and the signs of the successive derivatives of the probability weighting function a development that parallels that within EU, one has to modify the initial model free preferences. This is the purpose of the next section.

3 Model Free Preferences

To provide an intuitive interpretation to the signs of the successive derivatives of the probability weighting function beyond the second order121212As is well-known, both and correspond to strong risk aversion (i.e., aversion to mean preserving spreads); see the references in Section 2.2. we now develop the appropriate model free preferences. We will continue to assert that DM’s want to combine good with bad. In Chiu’s (2005) equivalent terminology, the DM still satisfies a precedence relation. He favors that the good precedes the bad. However, our definition of good and bad will be based on the concepts of “squeezing” and “anti-squeezing” a distribution instead of adding zero-mean risks and zero with certainty as in Eeckhoudt and Schlesinger (2006). Squeezing and anti-squeezing will serve as the main building blocks in our approach. The sequence of squeezes and anti-squeezes that we develop will preserve dual rather than primal moments.

Squeezing occurs when we transform an initial lottery

with (where equality to zero is explicitly permitted), , and , into a lottery given by

with . Anti-squeezing occurs when is replaced by , that is, when is transformed into a lottery given by

Clearly, both squeezing and anti-squeezing preserve the mean. Note the generality of these transformations. Depending on the specification of and , a squeeze and an anti-squeeze can be interpreted both as a shift in outcomes and as a shift in probabilities.

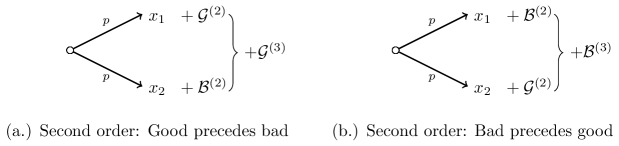

In this section, we explicate the dual story in examples. Section 6 contains the general approach. We first return to the second order and consider an initial lottery given by131313The superscript (2) refers to “second order” and more generally the superscript (m) refers to “ order”.

Now we transform the lottery into a lottery by squeezing. Specifically, we “attach” (state-wise with the state probabilities matched)

to , where in this case we let , , and where , .141414The condition on guarantees that the squeeze does not change the initial ranking of outcomes. We assume the good () precedes the bad (). This squeeze yields the new lottery given by

Of course, an anti-squeeze of that is same-sized but opposite to the squeeze, achieved by attaching and state-wise with the bad now preceding the good, would generate given by

See the illustration in Figure 1.

Clearly, under strong risk aversion, .151515For reasons that become apparent in Section 6 we don’t compare the changed lotteries and to the initial lottery they are generated from, although this comparison is straightforward in this particular case, in which . In fact, throughout this section, , , for DT DM’s having probability weighting functions with higher order derivatives that alternate in sign. For brevity, we sometimes directly construct from in the following sections. These preferences correspond to under DT and to under the EU model. Indeed, squeezing and anti-squeezing are special cases of a mean preserving contraction and a mean preserving spread in the sense of Rothschild and Stiglitz (1970), and DT and EU are known to agree in their evaluation of a mean preserving contraction and a mean preserving spread.

This figure plots the transformation from to (left panel) and from to (right panel), with , , and . and will be used to develop the dual story at the third order.

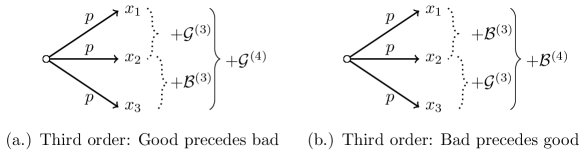

Turning now to the third order, the agreement between DT and EU may collapse, as already anticipated in Section 2.2. The model free preferences based on the precedence relation towards good and bad coupled with the notions of squeezing and anti-squeezing are deployed as follows.161616This is again an illustration. The general treatment is contained in Section 6. We start from an initial lottery given by

Then we generate as

with . To obtain from , we first transform the worst two states of by applying a squeeze, attaching

where we take in this case , , and , . Then on the best two states of we perform an anti-squeeze, achieved by attaching

with , , and , . In the transformation from to , the good () precedes the bad (). To keep the required number of states as small as possible, for ease and parsimony of exposition, we consider in this illustration a lottery with only 3 states, having moreover equal probabilities of occurrence, and we squeeze and anti-squeeze at an overlapping state (that with outcome 2) and by the same amount. These restrictions are, however, not required for our general approach; see Section 6 for further details.

Similarly, we generate a lottery given by

obtained from the initial lottery by letting the bad, , precede the good, . See the illustration in Figure 2.

As shown in Section 6, to which a precise statement of this result is deferred—see Theorems 6.1 and 6.2—, “dual prudence” (or “”) corresponds to “”. Both the well-known probability weighting function of Tversky and Kahneman (1992) and that of Prelec (1998) exhibit under the typical parameter sets implied by experiments.

This figure plots the transformation from to (left panel) and from to (right panel), with , , , and . and will be used to develop the dual story at the fourth order.

It is very important to realize that there is no unanimity among EU maximizers with on the comparison between and . This is essentially so because these two lotteries with the same mean have different variances and skewnesses. Indeed, and . As a result, EU DM’s who are relatively more (less) risk averse than prudent prefer (). While our story of squeezing and anti-squeezing may yield different primal moments (variances in particular) for the lotteries that are compared, it preserves equality of the second dual moments. Indeed, one may verify that

This is the fundamental reason why EU and DT may diverge from the third order onwards.

We note that if we would have started from an initial lottery given by

equality of the variances would have been preserved in the transformation to the corresponding and . In this case both EU DM’s with and DT DM’s with would have preferred over . That is, EU and DT may, but need not, diverge at the third order.

In order to interpret the sign of the fourth derivative of we start from an expanded lottery given by

Now on the worst three states of we conduct the beneficial transformation described at the third order (i.e., that with preceding ), attaching

with in this case , , and , . Next, on the best three states of we conduct exactly the opposite transformation, by attaching

so that we obtain a lottery given by

Conversely, by letting the bad precede the good we generate

In Section 6, we show that is unanimously preferred over by DT DM’s with “dual temperance” (or “”)—see Theorems 6.3 and 6.4.

To see the implications of the dual story within the EU model, it is convenient to compare to when . While in this case and have the same mean and variance, one easily verifies that has both a smaller skewness and a smaller kurtosis than . Hence, there cannot be unanimity among the prudent and temperate EU DM’s about the appreciation of the two lotteries: some will prefer while others will prefer , depending upon their relative degrees of prudence and temperance. This observation makes explicit the reason why at the fourth order EU and DT may (continue to) diverge: while the sequence of squeezing and anti-squeezing at the fourth order may produce different third primal moments for and , it preserves the equality of the third dual moments, corroborating again their relevance for the dual story.

We finally note that the lotteries at the third and fourth orders are generated by simple iterations of the transformations relevant at the second and third orders, respectively. Hence, this analysis can be pursued up to arbitrary order to interpret the signs of the successive derivatives of the probability weighting function. We thus obtain, as in the Eeckhoudt and Schlesinger (2006) approach, a sequence of simple nested lotteries that yield now the appropriate interpretation of the signs of .

4 Portfolio Choice with Derivatives

Consider a DT investor with initial sure wealth . Suppose that he allocates an amount to a risky asset (the “stock”) and an amount to a risk-free asset (the “bond”). The bond (stock) earns a sure (risky) return of () per unit invested. Assume that and are independent of the amounts invested. The investor aims to determine the optimal amount . Because and the DT evaluation is translation invariant and positively homogeneous, his problem reads:

| (4.1) |

We add the constraint . It readily follows that the optimal solution is a corner solution.

Suppose . Then the optimal solution is . In this case, the investor fully invests in the bond. Now imagine that the investor is offered an improvement to the distribution of the risky return. In particular, he is offered the possibility of supplementing the stock with derivative products on the stock that have zero expected value at zero cost. The derivative products are selected by applying the dual story such that they induce, through squeezing and anti-squeezing, an order improvement of , with . The return of the risky portfolio of stock and derivatives jointly is denoted by . (We provide details on the derivative products shortly.)

Then two cases are possible: (i) If , full investment in the bond remains optimal. (ii) If the improvement is sufficiently large so that , the DT investor will shift from one corner solution (full investment in the bond, i.e., ) to the other corner solution (full investment in the risky portfolio, i.e., ).

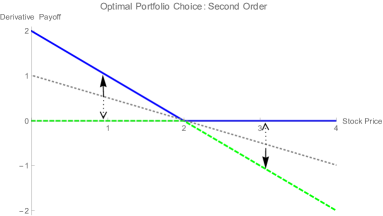

To illustrate these order improvements, suppose for ease of exposition that . Consider the second order first. Assume that the stock price takes the values 1 and 3 each with probability 1/2. Invoking the dual story, we find that a long position in a put option combined with a short position in a call option, each with a strike price of 2 such that the joint expected value is zero, improves the attractiveness of the risky portfolio ( versus ) whenever . Indeed, the difference between and can in this case be seen as the result of squeezing and anti-squeezing.171717Throughout this section the risky stock price , with the initial stock price, plays the role of the lotteries encountered in the dual story, while the stock-and-derivatives portfolio price plays the role of the lotteries . The derivative supplements directly generate the improvement from . Specifically, and . At the second order, Of course, and may be generated from a common initial lottery by squeezing and anti-squeezing, that is, by attaching to . If the good (bad) precedes the bad (good), () is generated. As visualized in the top left panel of Figure 3, this combination of long put and short call provides a hedge against adverse stock scenarios, which is financed by giving up upward potential.

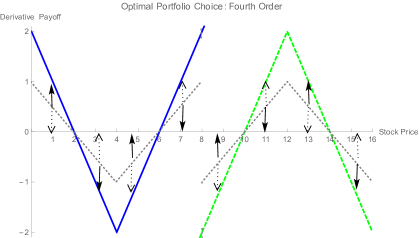

This figure plots the payoff functions of the derivative products to supplement the stock inducing an order improvement, . At each order, the derivative products have zero (joint) expected value. At the second order (top left panel), we supplement the stock with a long position in a put option (blue, solid) and a short position in a call option (green, dashed), both with a strike price of 2. At the third order (top right panel), we enter into a straddle option (blue) at stock price 4. Finally, at the fourth order (bottom panel), we add a long straddle at stock price 4 (blue) and a short straddle at stock price 12 (green, dashed). Both the stock price itself and the stock-and-derivatives portfolio price can at each order be generated from a common initial lottery (in the form of a stock-and-derivatives portfolio) represented by the grey dotted lines through (a sequence of) squeezes and anti-squeezes represented by the solid and dashed arrows, respectively, according to the dual story; see also footnotes 17 and 18.

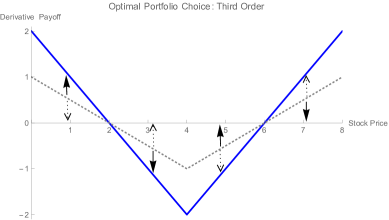

Next, consider the third order. Assume now that the stock price takes the values each with probability 1/4. Then, deploying the dual story, one may readily verify that a so-called “straddle” option at stock price 4 such that the expected value is zero, improves the attractiveness of the risky portfolio ( versus ) whenever . As visualized in the top right panel of Figure 3, the straddle pays off in bad stock scenarios and in good stock scenarios, but generates losses in intermediate stock scenarios.181818At the third order, and , where They can be generated from an initial lottery by attaching at non-overlapping states. Because the straddle increases not only the skewness but also the variance of the risky portfolio, there would be no unanimity for the straddle supplement under EU, contrary to under DT.

Finally, at the fourth order, assume that the stock price takes the values each with probability 1/8. Then, the dual story implies that a long straddle at stock price 4 combined with a short straddle at stock price 12, with joint expected value equal zero, improves the attractiveness of the risky portfolio provided . This combination of a long and short straddle, visualized in the last panel of Figure 3, is a popular and simple case of a so-called “volatility spread”.191919The payoffs of the long and short straddle are digitally set to 0 at stock price 8 for simplicity.

We thus find that an order (dual) improvement of the risky asset’s return distribution never reduces the demand for the risky asset when the successive derivatives of the probability weighting function alternate in sign. This stands in sharp contrast to the familiar results under EU, where an order (primal) improvement of has ambiguous demand effects, even for . Indeed, to obtain the natural result that such improvements induce a higher demand for the risky asset under EU, additional non-trivial conditions need to be imposed (see Section 9.3 of Eeckhoudt and Gollier (1995) and Gollier (1995) for details).202020See also the analysis of Dittmar (2002) in the EU model.

5 Self-Protection with Background Risk

In this section, we consider a DT DM with initial sure wealth who faces the risk of losing the monetary amount . The probability of occurrence of the loss, , depends on the self-protection212121Adopting the terminology of Ehrlich and Becker (1972). effort, , exerted by the DM. In particular, is decreasing in . Effort is measured in monetary equivalents. The DM aims to determine the optimal level of effort that maximizes his DT evaluation.

We analyze this problem in the presence of an independent background risk. This background risk may e.g., be due to the risk of holding risky financial assets or to uncertain labor income. The sign of appears to play an essential role in this self-protection problem with background risk. Hence, while under EU the a priori validity of is connected to a savings decision (Kimball (1990)), we show that under DT the a priori validity of may be linked to a self-protection problem.

With an independent binary background risk taking the value , , each with probability , the self-protection problem can be represented by the following 4-state lottery :

assuming . If , the middle two states of change places. The DT DM solves:

| (5.1) |

We assume throughout that is concave in .

If , the first-order condition for optimality reads

After obvious simplifications, we obtain

| (5.2) |

We note that in the absence of any background risk, i.e., when , the first-order condition reduces to

| (5.3) |

Now assume first, like in Eeckhoudt and Gollier (2005) for EU, that when . This means that the DT DM optimally selects an effort level such that the probability of the occurrence of a loss is , in the absence of background risk. Under this assumption, we find from (5.2) that the impact of the background risk is linked to the sign of

| (5.4) |

If the sign of is positive, then (5.4) is negative, and note that is negative, too. Therefore, and in view of the concavity of with respect to , the introduction of a background risk in this setting stimulates self-protection provided the DT DM is dual prudent.

Next, consider the case . In this case, the first-order condition is

which, after obvious simplifications, reduces to

| (5.5) |

Recall that in the absence of any background risk, the first-order condition equals (5.3). Hence, noting that the difference between the left-hand side of (5.5) and the left-hand side of (5.3) equals

| (5.6) |

and maintaining the assumption that when , we find that the impact of the background risk is again linked to the sign of (5.4) which, in turn, depends on the sign of .

Thus, under the maintained assumption that when , guarantees that the marginal benefit of self-protection increases upon the introduction of an independent background risk. Therefore, the background risk stimulates self-protection under dual prudence.222222There is a difference between the two cases. When , the convexity of adds a marginal benefit that depends on the size of compared to the situation of no background risk; cf. (5.2). When , the convexity of adds a marginal benefit that is independent of but depends on the size of compared to the situation of no background risk; cf. (5.6).

By a similar analysis, we can extend the results to a larger set of possible cases.232323See the extended online version for further details. If when , we find that dual imprudent DM’s (i.e., ) exert less effort with background risk than without. If when , we obtain that dual prudent DM’s (i.e., ) exert more effort with background risk than without.

6 Dual Risk Apportionment

In this section, we develop the dual story as illustrated in Section 3 in full generality. Throughout this section we consider -state lotteries and assume all states to have equal probability of occurrence , . We permit that the increments in the outcomes when moving to an adjacent state are equal to zero. This can be interpreted to yield lotteries with unequal state probabilities.

6.1 The Third Order: Dual Prudence

We start by providing a simple class of lottery pairs such that the direction of preference between these lottery pairs is equivalent to signing the third derivative of the probability weighting function under DT. Consider

with . The acronyms “” and “” refer to “good” and “bad”. Upon “attaching” and state-wise to an arbitrarily given initial lottery that has at least three states such that the state-wise addition is feasible, we generate if state-wise precedes and we generate if state-wise precedes . Attaching the good, , induces a squeeze, while attaching the bad, , induces an anti-squeeze.

To emphasize the generality of these transformations, we note that: (i) and may differ; (ii) the number of states that “” denotes in and in may differ; (iii) the number of states that “” denotes in and in may be equal to zero; (iv) the spacing (i.e., the number of states) between and on the one hand and and on the other hand when attaching them to the initial lottery may differ; (v) this spacing may be negative, so that the good and the bad partially overlap, but strictly precedes by at least one state for and strictly precedes by at least one state for . All these generalities are permitted as long as the ranking of outcomes remains unaffected by the squeezes and anti-squeezes and the outcomes of the resulting lotteries remain non-negative. These generalities are in part thanks to the fact that we don’t compare the changed lotteries to the initial lottery they are generated from. Rather we compare two altered lotteries: one has the good precede the bad, the other the reverse.

We say that an individual is “dual prudent” if, for any such lottery pair , he prefers to . The following theorem shows that within DT this is guaranteed by a positive sign of . The individual’s type of behavior corresponding to these lottery preferences, and their higher-order generalizations that we develop below, may be termed “dual risk apportionment”. Much like under primal risk apportionment, the apportionment of harms within a lottery mitigates the detrimental effects for such an individual.

Theorem 6.1

If and are generated by the transformations described above, then is preferred (dispreferred) to by any DT DM with ().

In the remainder of this subsection, we consider a parsimonious subclass of lottery pairs and that turns out to be already sufficient for the purpose of signing . Let and consider

The three states in bold need to be present for any given , the remaining states are added arbitrarily until the state probabilities sum up to 1. The increments in the outcomes when moving to an adjacent higher state of are allowed to be arbitrarily non-negative and state-dependent, as long as the squeezes and anti-squeezes performed below do not change the ranking of outcomes.242424This is accomplished by restricting in the squeezes and anti-squeezes explicated below accordingly.

Then, we (directly) construct from by attaching to the three states in bold

This yields given by

Clearly, and occur as a subclass of and . To see this, consider an initial lottery given by

and generate () by attaching the good (bad), (), given by

to the first two bold states of , and attaching the bad (good), (), to the last two bold states of . To keep the required number of states as small as possible and enhance parsimony, sufficient for our purpose of signing , we squeeze and anti-squeeze at an overlapping state, just like in Section 3.

The following theorem shows that within DT the preference towards the class of lottery pairs and signs :

Theorem 6.2

If, for any , a DT DM prefers (disprefers) to , then ().

6.2 The Fourth Order: Dual Temperance

Next, we provide a simple class of lottery pairs such that the direction of preference between these lottery pairs is equivalent to signing the fourth derivative of the probability weighting function under DT. Consider

with . Upon attaching and to an arbitrarily given initial lottery that has at least four states such that the state-wise addition is feasible, we generate if state-wise precedes and we generate if state-wise precedes . We note that and can each be interpreted as simple concatenations of same-sized but exactly opposite and . Thus, we define the fourth order transformations by simple iterations of the third order ones.

To emphasize the generality of these transformations, we note that: (i) and may differ; (ii) the number of states that “” denotes may differ within and between and , but both and need to be symmetrical in the sense that the first and third “” within denote the same number of states and similarly for (which is compatible with and each being concatenations of same-sized but exactly opposite and ); (iii) the number of states that the first and third “” denote in and is non-negative and may be equal to zero, while the number of states that the middle (second) “” denotes is larger than or equal to minus one;252525If the number of states that “” represents is -1, the middle two adjacent states overlap, thus attaching for and for to a state with probability . (iv) the spacing (i.e., the number of states) between and on the one hand and and on the other hand when attaching them to the initial lottery may differ; (v) this spacing may be negative, so that the good and the bad partially overlap, but strictly precedes by at least one state for and strictly precedes by at least one state for . All these generalities are permitted as long as the ranking of outcomes remains unaffected and the outcomes of the resulting lotteries remain non-negative.

We say that an individual is “dual temperate” if, for any such lottery pair , he prefers to . The following theorem shows that within DT this is guaranteed by a negative sign of .

Theorem 6.3

If and are generated by the transformations described above, then is preferred (dispreferred) to by any DT DM with ().

As in Section 6.1, let us in the remainder of this subsection consider a parsimonious subclass of lottery pairs and , already sufficient for our purpose of signing . Let and consider

The four states in bold need to be present for any given , the remaining states are added arbitrarily until the state probabilities sum up to 1. The increments in the outcomes when moving to an adjacent higher state of are again allowed to be arbitrarily non-negative and state-dependent, as long as the transformations conducted below do not change the ranking of outcomes.262626This is accomplished by restricting in the transformations explicated below accordingly.

Then, we (directly) construct from by attaching to the four states in bold

This yields given by

Clearly, and occur as a subclass of and . To see this, consider an initial lottery given by

and generate () by attaching the good (bad), (), given by

to the first three bold states of , and attaching the bad (good), (), to the last three bold states of . To keep the required number of states as small as possible and enhance parsimony, sufficient for our purpose of signing , we again conduct transformations at overlapping states, just like in Section 6.1 and Section 3.

The following theorem shows that within DT the preference towards the class of lottery pairs and signs :

Theorem 6.4

If, for any , a DT DM prefers (disprefers) to , then ().

6.3 The Order

In this section, we systematically construct simple nested classes of lottery pairs such that the direction of preference between these lottery pairs is equivalent to signing the derivative of the probability weighting function under DT. We start at the second order and proceed to construct all higher orders of dual risk apportionment by simple iteration, as follows. Consider

with . Taking the order as a starting point, we construct the class of lottery pairs for the order in two steps. Let . Then:

-

(i)

Concatenate a same-sized but exactly opposite and , with state-wise preceding by at least one state. This generates . Similarly, concatenate another same-sized but exactly opposite and , with state-wise preceding by at least one state. This generates .

-

(ii)

Attach and to an arbitrarily given -state initial lottery. We generate if state-wise precedes and we generate if state-wise precedes .

In the transformations to and we require that the ranking of outcomes remains unaffected and the outcomes of the resulting lotteries remain non-negative.

Then, we state the following theorem:

Theorem 6.5

Let . If and are generated by the transformations described above, then is preferred (dispreferred) to by any DT DM with ().

Just like in Sections 6.1 and 6.2 we consider henceforth parsimonious subclasses of lottery pairs and that are already sufficient for signing . We start at the second order and proceed by simple iteration. Let and consider

The states in bold need to be present for any , the remaining states are added arbitrarily until the state probabilities sum up to 1. The increments in the outcomes when moving to an adjacent higher state of are allowed to be arbitrarily non-negative and state-dependent, as long as the transformations conducted below do not change the ranking of outcomes. Taking the order as a starting point, we construct the class of lottery pairs for the order in two steps:

-

(i)

Concatenate a same-sized but exactly opposite and , with state-wise preceding by exactly one state. This generates . Next, concatenate the same and with state-wise preceding by exactly one state. This generates . (For , we set and , .)

-

(ii)

Generate by attaching to the first bold states of and attaching to the last bold states of .

In the transformations from to we require that the ranking of outcomes remains unaffected and the outcomes of the resulting lotteries remain non-negative. For , we perform our sequences of squeezes and anti-squeezes at overlapping states to keep the required number of states minimal. This yields a parsimonious approach already sufficient for signing .

Finally, the following theorem shows that within DT the preference towards the class of lottery pairs and signs :

Theorem 6.6

Let . If, for any , a DT DM prefers (disprefers) to , then ().

7 Conclusion

Starting with Menezes, Geiss and Tressler (1980), many papers have been devoted to an interpretation of the signs of the successive derivatives of the utility function within the EU model.

In this paper we have developed a model free story of preferences towards particular nested classes of lottery pairs that is appropriate to satisfy the specific requirements of the DT model. The story yields an intuitive interpretation, and full characterization, of the dual counterparts of such concepts as prudence and temperance. The direction of preference between the nested lottery pairs that are provided by the story is equivalent to signing the derivative of the probability weighting function within DT.

We have analyzed implications of our results for portfolio choice, which appear to stand in sharp contrast to familiar implications under the EU model. We have also shown that, where the sign of the third derivative of the utility function is connected to a savings problem, the sign of the third derivative of the probability weighting function may be naturally linked to a self-protection problem.

Because the primal and dual stories have several aspects in common, some of the implications of the primal story can potentially be extended to a dual world. For instance, because it is also simple, the dual story should be as amenable to experimentation as the primal story. Another promising route for future research is that the dual story can serve as a building block on the basis of which it should be possible to obtain related interpretations for more general models of choice under risk (and ambiguity). Indeed, now that the dual story has been told, future research can develop an interpretation to the signs of the successive derivatives of both the utility function and the probability weighting function in the rank-dependent utility (RDU) model of Quiggin (1982) and in prospect theory of Tversky and Kahneman (1992). For example, one may verify that the direction of preference between the intersection of lottery pairs generated by primal and dual risk apportionment signs the successive derivatives of the utility and probability weighting functions jointly under RDU. This would provide a test for the null hypothesis that both and in the RDU environment, as is often assumed in parametric specifications of the utility and probability weighting functions. Furthermore, subsets of lottery pairs generated by dual risk apportionment that share the same final wealth outcomes can be used to test the null hypothesis that (only) in the RDU setting.

As such, this paper represents a first step, and paves new ways, towards the development of higher order risk attitudes in non-EU theories, as explicitly desired by Deck and Schlesinger (2010).

Appendix: Proofs

Proof of Theorem 6.1. We first note that the probabilities of generating the minimal outcome in a two-shot experiment (i.e., in two independent draws) for the states of an arbitrarily given -state lottery with equal state probabilities are

respectively. Thus, the second dual moment of is given by

Hence, one readily verifies that

Indeed, attaching and with state-wise preceding versus attaching and with state-wise preceding has the same (incremental) impact on the dual moments up to the second order. Furthermore, surpasses before crossing twice, so that dominates in third-degree dual stochastic dominance; see e.g., Proposition 4.9 of Wang and Young (1998).

It then follows from a Taylor expansion of the “dual utility premium”,

(see Theorem 4.4 of Wang and Young (1998)) that when the dual moments are equal up to the second order, () implies that the dual utility premium above is non-negative (non-positive). This proves the stated result.

Proof of Theorem 6.2. Since is differentiable on , the third derivative of being non-negative is equivalent to requiring that

for any four equidistant probabilities . We will show that this condition is satisfied whenever is preferred to for any within DT. (The implication follows similarly.)

We note that the DT evaluation of a lottery with outcomes is given by

with . Observe that with , , ; and that is equivalent to . Here, by convention, so . Hence,

with corresponding to the state preceding the three states in bold that are always present in , and similarly for . Notice that

Furthermore,

and

suppressing the indices and for convenience. Define, for given , the probability , , such that

Then,

and

Upon defining such that

it then follows from the arbitrariness of , hence the arbitrariness of , that

for any four equidistant probabilities , whenever is preferred to for any . We note that is the DT analog of the utility premium in the EU model. Finally, observe that is equivalent to . This proves the stated result.

Proof of Theorem 6.3. By analogy to the proof of Theorem 6.1, we first note that the probabilities of generating the minimal outcome in a three-shot experiment (that is, in three independent draws) for the states of an arbitrarily given -state lottery with equal state probabilities are

respectively. Thus, the third dual moment of is given by

Hence, one may verify that not only the first two dual moments of and are equal, but also the third:

Indeed, attaching and with state-wise preceding versus attaching and with state-wise preceding has the same (incremental) impact on the dual moments up to the third order. The proof then follows by similar arguments as the proof of Theorem 6.1. The details are suppressed to save space. They are contained in the extended online version.

References

- [1] Baillon, A. (2017). Prudence (and more) with respect to uncertainty and ambiguity. Economic Journal, forthcoming.

- [2] Chateauneuf, A., T. Gajdos and P.-H. Wilthien (2002). The principle of strong diminishing transfer. Journal of Economic Theory 103, 311-333.

- [3] Chew, S.H., E. Karni and Z. Safra (1987). Risk aversion in the theory of expected utility with rank dependent probabilities. Journal of Economic Theory 42, 370-381.

- [4] Chiu, H. (2005). Skewness preference, risk aversion, and the precedence relations on stochastic changes. Management Science 51, 1816-1828.

- [5] David, H.A. (1981). Order Statistics. 2nd Ed., Wiley, New York.

- [6] De La Cal, J. and J. Cárcamo (2010). Inverse stochastic dominance, majorization and mean order statistics. Journal of Applied Probability 47, 277-292.

- [7] Deck, C. and H. Schlesinger (2010). Exploring higher order risk effects. Review of Economic Studies 77, 1403-1420.

- [8] Deck, C. and H. Schlesinger (2014). Consistency of higher order risk preferences. Econometrica 82, 1913-1943.

- [9] Dittmar, R.F. (2002). Nonlinear pricing kernels, kurtosis preference, and evidence from the cross section of equity returns. Journal of Finance 57, 369-403.

- [10] Ebert, S. and D. Wiesen (2011). Testing for prudence and skewness seeking. Management Science 57, 1334-1349.

- [11] Ebert, S. and D. Wiesen (2014). Joint measurement of risk aversion, prudence, and temperance. Journal of Risk and Uncertainty 48, 231-252.

- [12] Eeckhoudt, L.R. and C. Gollier (1995). Risk: evaluation, management and sharing. Harvester Wheatsheaf, Hertfordshire.

- [13] Eeckhoudt, L.R. and C. Gollier (2005). The impact of prudence on optimal prevention. Economic Theory 26, 989-994.

- [14] Eeckhoudt, L.R. and H. Schlesinger (2006). Putting risk in its proper place. American Economic Review 96, 280-289.

- [15] Eeckhoudt L.R., H. Schlesinger and I. Tsetlin (2009). Apportioning of risks via stochastic dominance. Journal of Economic Theory 144, 994-1003.

- [16] Ehrlich, I. and G. Becker (1972). Market insurance, self insurance and self protection. Journal of Political Economy 80, 623-648.

- [17] Ekern, S. (1980). Increasing th degree risk. Economics Letters 6, 329-333.

- [18] Gollier, C. (1995). The comparative statics of changes in risk revisited. Journal of Economic Theory 66, 522-536.

- [19] Kahneman, D. and A. Tversky (1979). Prospect theory: An analysis of decision under risk. Econometrica 47, 263-292.

- [20] Kimball, M.S. (1990). Precautionary saving in the small and in the large. Econometrica 58, 53-73.

- [21] Mao, J.C.T. (1970). Survey of capital budgeting: Theory and practice. Journal of Finance 25, 349-369.

- [22] Menezes, C.F., C. Geiss and J. Tressler (1980). Increasing downside risk. American Economic Review 70, 921-932.

- [23] Muliere, P. and M. Scarsini (1989). A note on stochastic dominance and inequality measures. Journal of Economic Theory 49, 314-323.

- [24] Noussair, C.N., S.T. Trautmann and G. van de Kuilen (2014). Higher order risk attitudes, demographics, and financial decisions. Review of Economic Studies 81, 325-355.

- [25] Prelec, D. (1998). The probability weighting function. Econometrica 66, 497-527.

- [26] Quiggin, J. (1982). A theory of anticipated utility. Journal of Economic Behaviour and Organization 3, 323-343.

- [27] Roëll, A. (1987). Risk aversion in Quiggin and Yaari’s rank-order model of choice under uncertainty. The Economic Journal 97, 143-159.

- [28] Rothschild, M. and J.E. Stiglitz (1970). Increasing risk: I. A definition. Journal of Economic Theory 2, 225-243.

- [29] Schmeidler, D. (1986). Integral representation without additivity. Proceedings of the American Mathematical Society 97, 253-261.

- [30] Schmeidler, D. (1989). Subjective probability and expected utility without additivity. Econometrica 57, 571-587.

- [31] Tversky, A. and D. Kahneman (1992). Advances in prospect theory: Cumulative representation of uncertainty. Journal of Risk and Uncertainty 5, 297-323.

- [32] Wang, S.S. and V.R. Young (1998). Ordering risks: Expected utility theory versus Yaari’s dual theory of risk. Insurance: Mathematics and Economics 22, 145-161.

- [33] Whitmore, G. (1970). Third order stochastic dominance. American Economic Review 50, 457-459.

- [34] Wu, G. and R. Gonzalez (1996). Curvature of the probability weighting function. Management Science 42, 1676-1690.

- [35] Wu, G. and R. Gonzalez (1998). Common consequence effects in decision making under risk. Journal of Risk and Uncertainty 16, 115-139.

- [36] Yaari, M.E. (1986). Univariate and multivariate comparisons of risk aversion: a new approach. In: Heller, W.P., R.M. Starr and D.A. Starrett (Eds.). Uncertainty, Information, and Communication. Essays in honor of Kenneth J. Arrow, Volume III, pp. 173-188, 1st Ed., Cambridge University Press, Cambridge.

- [37] Yaari, M.E. (1987). The dual theory of choice under risk. Econometrica 55, 95-115.