On the Singular Control of Exchange Rates

Abstract.

Consider the problem of a central bank that wants to manage the exchange rate between its domestic currency and a foreign one. The central bank can purchase and sell the foreign currency, and each intervention on the exchange market leads to a proportional cost whose instantaneous marginal value depends on the current level of the exchange rate. The central bank aims at minimizing the total expected costs of interventions on the exchange market, plus a total expected holding cost. We formulate this problem as an infinite time-horizon stochastic control problem with controls that have paths which are locally of bounded variation. The exchange rate evolves as a general linearly controlled one-dimensional diffusion, and the two nondecreasing processes giving the minimal decomposition of a bounded-variation control model the cumulative amount of foreign currency that has been purchased and sold by the central bank. We provide a complete solution to this problem by finding the explicit expression of the value function and a complete characterization of the optimal control. At each instant of time, the optimally controlled exchange rate is kept within a band whose size is endogenously determined as part of the solution to the problem. We also study the expected exit time from the band, and the sensitivity of the width of the band with respect to the model’s parameters in the case when the exchange rate evolves (in absence of any intervention) as an Ornstein-Uhlenbeck process, and the marginal costs of controls are constant. The techniques employed in the paper are those of the theory of singular stochastic control and of one-dimensional diffusions.

Keywords: singular stochastic control; exchange rates; target zones; central bank; variational inequality; optimal stopping.

MSC2010 subject classification: 93E20, 60J60, 60G40, 91B64, 91G30.

OR/MS subject classification: Dynamic programming/optimal control; Probability: stochastic model/applications; Probability: diffusion.

1. Introduction

One of the main tool that a central bank has at disposal in order to maintain under control the volatility of the exchange rate is to properly purchase or sale foreign currency reserves. As a result of such interventions on the exchange market, in many cases one can observe that the exchange rate between two currencies is either kept below/above a given level, or it is maintained within announced margins on either side of a given value, the so-called central parity (or central rate). Similar regimes of the exchange rate are usually referred to as target zones, and Switzerland, Hong Kong, and Denmark are prominent examples of countries that adopted, or adopt, such a kind of monetary policy.

On the 6th of September 2011, the Swiss National Bank (SNB) stated in a press release [50]:

[…] the current massive overvaluation of the Swiss Franc poses an acute threat to the Swiss economy and carries the risk of deflationary development. The Swiss National Bank is therefore aiming for a substantial and sustained weakening of the Swiss Franc. With immediate effect, it will no longer tolerate a EUR/CHF exchange rate below the minimum rate of CHF 1.20. The SNB will enforce this minimum rate with the utmost determination and is prepared to buy foreign currency in unlimited quantities […]

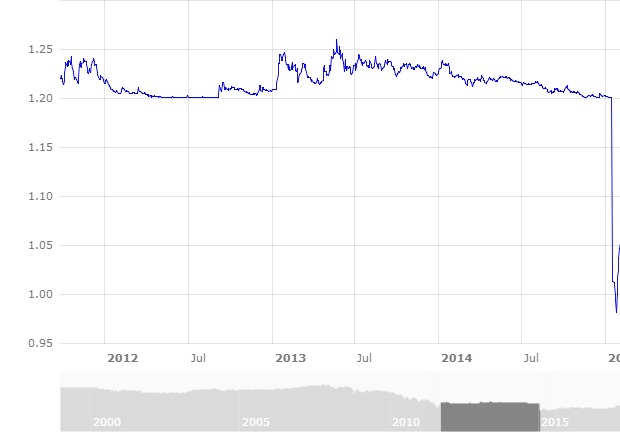

SNB adopted such an aggressive devaluation policy until the 15th of January 2015 [51, 34], when SNB simply dropped its target zone policy with a very evident effect on the CHF/EUR exchange rate (see Figure 1.1).

On the other hand, the 12th of January 2017 marked the 30th anniversary of the Danish central parity [37]. The decision to pursue a fixed exchange rate policy was made in the 1980s when the Danish economy was in a crisis. Since then the Danish Krone (DKK) was anchored to the German Mark, and then, since 1999, to Euro in such a way that the Krone’s central parity has been unchanged since January 12, 1987. The central rate is 7.46038 Krone per Euro, and the Krone is allowed to increase or decrease by 2.25% (even if the fluctuations have been far smaller for many years, see Figure 1.2).

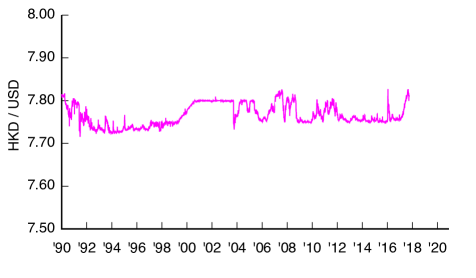

To end with a non-European example, as a response to the Black Saturday crisis in 1983, on October 17, 1983 the Hong Kong Dollar (HKD) has been pegged to the U.S. Dollar (USD), and since then the HKD/USD exchange rate is pegged to a central rate of 7.80 HKD/USD (see Figure 1.3), with a band of HKD/USD [52].

It is not clear (nor of public knowledge) whether the width of the interval where the exchange rate is allowed to fluctuate is chosen according to some optimality criterion (e.g., maximization of social welfare or minimization of expected costs), or it is decided only on the basis of international and political agreements. In the latest years the economic and mathematical literature experienced an intensive research on target zone models. In particular, within the literature we can identify two main streams of research. On one hand, many papers develop stochastic models aiming at explaining the dynamics of exchange rates within a given target zone (see [9, 18, 32, 28, 33, 48], among others). Target zone models have been pioneered in [32] where it is assumed that the “fundamental” (and not observed) exchange rate is a Brownian motion, which is instantaneously reflected at exogenously given upper and lower barriers: this intrinsically defines a singular stochastic control problem, whose value function is the exchange rate really observed in the market. Although in [32] many mathematical details are missing, in that seminal paper the author finds that the observed exchange rate is mean-reverting inside the given target zone. In the subsequent papers (see e.g. [9, 18, 28, 33, 48] and references therein), the authors assume that exchange rates fluctuate stochastically within an exogenously given interval according to a stochastic differential equation parametrized by a set of free parameters, and possibly satisfying reflecting boundary conditions, or with diffusion coefficient vanishing near the boundaries of the interval. The parameters are then calibrated in such a way that the model can fit the data on exchange rates, e.g. in the European monetary system.

On the other hand, several papers in the mathematical literature endogenize the width of the target zone by formulating the exchange rates’ optimal management problem as a stochastic optimal control problem (see [8, 12, 13, 26, 39], and references therein). In these papers, the central bank aims at adjusting the uncertain level of the exchange rate in order to minimize the spread between the instantaneous level of the exchange rate and a given central parity. To accomplish that, the central bank can purchase or sell foreign currency, but whenever the central bank intervenes, a cost for the intervention must be paid. In those papers such a cost has both a proportional and a fixed component, thus leading to a mathematical formulation of the optimization problem as a two-sided stochastic impulsive control problem (possibly also with classical controls modeling the interventions on the domestic interest rate). It is shown that the optimally controlled exchange rate is kept within endogenously determined levels (the so-called free boundaries) and the interventions are of pure-jump type: at optimal times the exchange rate is pushed from a free boundary to another threshold level, which is also found endogenously as a part of the solution to the problem. In essence, it is optimal to follow a two-sided -policy.

However, a closer look at the dynamics of the exchange rate EUR/CHF in the period 2011-2015, or at that of the exchange rate HKD/USD since 2008 reveals no jumps, but a continuous reflection of the exchange rate at the boundaries of the interval where it is allowed to fluctuate (see Figures 1.1 and 1.3). Such an observation suggests that the optimal management problem of exchange rates might be mathematically better formulated as a singular stochastic control problem, rather than as an impulsive one. Indeed, in singular stochastic control problems the optimal control usually prescribes a continuous reflection of the controlled state variable at endogenously determined level(s) (see, e.g., Chapter VIII in [20] and [43] for an introduction to singular stochastic control).

In this paper we thus introduce an infinite time-horizon, one-dimensional bounded variation singular stochastic control problem to model the exchange rates’ optimal management problem. In our model, the (logarithm of the) exchange rate is a one-dimensional Itô-diffusion satisfying a linearly controlled stochastic differential equation with suitable drift and volatility coefficients. Such general dynamics allows us to cover classical models where the exchange rate evolves as a geometric Brownian motion, as well as more realistic mean-reverting behaviors of the exchange rate’s dynamics (see [44, 47] and references therein). The cumulative amount of purchases and sales of the foreign currency (which are the control variables of the central bank) are monotone processes, adapted to the underlying filtration, and satisfying proper integrability conditions. The central bank aims at choosing a (cumulative) purchasing-selling policy in order to minimize a total expected discounted cost functional. This is given by the sum of total expected holding costs and costs of interventions. The instantaneous holding cost of the exchange rate is measured by a general nonnegative convex function. This generalizes the quadratic cost function usually employed in the literature (cf., e.g., [8, 12]). Also, we assume that the instantaneous proportional costs of the interventions on the exchange rate depend on the current level of the exchange rate, and they are sufficiently smooth real-valued functions.

We tackle the problem via a guess-and-verify approach by carefully employing the properties of one-dimensional regular diffusions (see, e.g., [10]), and of their excessive mappings [3]. We find that the optimal purchasing-selling policy of the central bank is triggered by two thresholds (free boundaries), which are the unique solution to a system of two coupled nonlinear algebraic equations. The optimal policy prescribes to purchase and sell the minimal amount of foreign currency that allows to keep the exchange rate within the free boundaries. Mathematically, the optimal control is given by the solution to a two-sided Skorokhod reflection problem.

It is worth noticing that, differently from models involving impulsive controls, where the actual optimality of a candidate value function is usually proved only via numerical methods (see [12, 13]), here we are able to provide a complete analytical study by finding the explicit expression of the value function and of the optimal control process (up to the solution to the algebraic system for the two free boundaries). Moreover, we can provide a detailed comparative statics analysis of the free boundaries when the (log-)exchange rate (in absence of any intervention) evolves through an Ornstein-Uhlenbeck dynamics. The latter allows us to capture the mean-reverting behavior of exchange rates that has been observed in several empirical studies (see [44, 47] and references therein). In particular, by assuming that the instantaneous proportional costs of interventions are constant, we show that the more the exchange market is volatile, the more the central bank is reluctant to intervene. Also, we are able to numerically evaluate the expected exit times and exit probabilities from the target zone, and to relate our findings with the monetary policy adopted by the Danish Central Bank since 1987 [37], and by the SNB in the period 2011–2015 [51, 34].

The contribution of this paper is twofold. On the one hand, we contribute to the literature from the modeling point of view. Indeed, by introducing a singular stochastic control problem to model the exchange rates’ optimal management problem faced by a central bank, we are able to mimick the continuous reflection of the exchange rate at the target zone’s boundaries which seems to happen in reality (see Figures 1.1 and 1.3). From the mathematical point of view, we contribute by providing the explicit solution to a bounded variation singular stochastic control in a very general setting with state variable evolving as a general one-dimensional diffusion, and with instantaneous marginal costs of control that are state-dependent. To the best of our knowledge, the explicit solution to a similar problem is not available in the literature yet.

The work that is perhaps closest to ours is [36], where a one-dimensional, bounded variation singular stochastic control problem over an infinite time-horizon has been studied. However, one can come across several major differences between our paper and [36]. First of all, in [36] the instantaneous marginal costs of control are constant. Second of all, in [36] the state dynamics (in the notation of that paper) is , where is an uncontrolled one-dimensional regular diffusion, and gives the minimal decomposition of a process of bounded variation. In our paper, instead, the dynamics of the state variable is given in differential form (see (2.3)), and, differently to [36], the controlled state process at time cannot be written as the sum of an uncontrolled one and of the cumulative bounded variation control exerted up to time . Finally, in [36] the optimal control is sought within the class of barrier policies, whereas we here obtain optimality in a larger class (see our Definition 2.9 below).

The rest of the paper is organized as follows. In Section 2.1 we set up the probabilistic setting, whereas in Section 2.2 we introduce the exchange rates’ optimal management problem that is the object of our study. In Section 3 we solve the problem by proving first a preliminary verification theorem, and then constructing the value function and the optimal control. In Section 4 we assume that the (log-)exchange rate is an Ornstein-Uhlenbeck process, and we provide the sensitivity of the free boundaries with respect to the model’s parameters and a study of the expected hitting time at the free boundaries. Finally, in the appendix we collect some auxiliary results needed in the paper.

2. Setting and Problem formulation

2.1. The Probabilistic Setting

Let be a complete probability space, a one-dimensional Brownian motion, and denote by a right-continuous filtration to which is adapted. We introduce the nonempty sets

| (2.1) | ||||

| (2.2) |

Then, for any , we denote by the two processes providing the minimal decomposition of ; that is, such that

and the increments and are supported on disjoint subsets of . In the following, we set a.s., without loss of generality, and for frequent future use we notice that any satisfies

Here is the continuous part of , and the jump part is such that , where , .

We then consider on a process satisfying the following stochastic differential equation (SDE)

| (2.3) |

Here , with , and and are suitable drift and diffusion coefficients. The process represents the (log-)exchange rate between two currencies. The drift coefficient measures the trend of the exchange rate, whereas the fluctuations around this trend. The central bank can adjust the level of through the processes and . In particular, and could be an indication of the cumulative amount of the foreign currency which has been bought or sold up to time in order to push the level of the exchange rate up or down, respectively.

The following assumption ensures that, for any , there exists a unique strong solution to (2.3) (see [41], Theorem V.7).

Assumption 2.1.

The coefficients and belong to . Moreover, there exists such that for all ,

From now on, in order to stress its dependence on the initial value and on the two processes and , we refer to the (left-continuous) solution to (2.3) as , where appropriate. Also, in the rest of the paper we use the notation . Here is the expectation under the measure on , and is any Borel-measurable such that is integrable.

We also denote by

the first time when the controlled process leaves .

We also consider a one-dimensional diffusion evolving according to the SDE

| (2.4) |

Notice that, under Assumption 2.1, there exists a weak solution of (2.4) that is unique in law, up to a possible explosion time (see Chapter 5.5 in [30], among others). Indeed, under Assumption 2.1 one has that for any there exists such that

| (2.5) |

We shall consider such a solution fixed for any initial condition throughout this paper. Moreover, (2.5) guarantees that is a regular diffusion. That is, starting from , reaches any other in finite time with positive probability. Finally, to stress the dependence of on its initial value, from now on we write , where needed, and we denote by the expectation under the measure .

Remark 2.2.

Define the new measure through the Radon-Nikodym derivative

| (2.6) |

which is an exponential martingale by the boundedness of . Then by Girsanov theorem the process

| (2.7) |

and it is not hard to verify that .

The infinitesimal generator of the uncontrolled diffusion is denoted by and is defined as

| (2.8) |

whereas the one of is denoted by and is defined as

| (2.9) |

Letting be a fixed constant, we make the following standing assumption.

Assumption 2.3.

for .

In the subsequent optimization problem, the parameter will play the role of the central bank’s discount factor (see (2.28) below).

We introduce and as the fundamental solutions of the ordinary differential equation (ODE) (see Ch. 2, Sec. 10 of [10]),

| (2.10) |

and we recall that they are strictly increasing and decreasing, respectively. For an arbitrary we also denote by

the derivative of the scale function of , and by the constant Wronskian

| (2.11) |

Moreover, under Assumption 2.1, any solution to the ODE

| (2.12) |

can be written as a linear combination of the fundamental solutions and , which again by [10, Chapter 2.10] are strictly increasing and decreasing, respectively. Finally, letting to be arbitrary, we denote by

the derivative of the scale function of , by

| (2.13) |

the density of the speed measure of , and by the Wronskian

| (2.14) |

Remark 2.4.

It is easy to see that the scale functions and speed measures of the two diffusions and are related through and for .

Concerning the boundary behavior of the real-valued Itô-diffusions and , in the rest of this paper we assume that and are natural for those two processes (see [10] for a complete discussion of the boundary behavior of one-dimensional diffusions). This in particular means that they are unattainable in finite time and that

| (2.15) |

| (2.16) |

and

| (2.17) |

| (2.18) |

In the following we also make the next standing assumption.

Assumption 2.5.

One has and .

Under Assumption 2.5 we show in Lemma A.1 in the Appendix that one has and (see also the second part of the proof of Lemma 4.3 in [6]).

Remark 2.6.

It is worth noticing that all the assumptions that we have made regarding the diffusions and (namely, Assumptions 2.1, 2.3 and 2.5) are satisfied in the relevant cases of a (log-)exchange rate given, e.g., by a drifted Brownian motion (i.e. and ), or by a mean-reverting process (i.e. , for some constants , and ), both defined on , i.e. with , .

For future reference, for all we introduce the Green functions associated to the diffusion

| (2.19) |

and to the diffusion

| (2.20) |

Then one has that the resolvents

| (2.21) |

and

| (2.22) |

which are defined for any function such that the previous expectations are finite, admit the representations

| (2.23) |

and

| (2.24) |

for all . Notice that and solve the ODEs

| (2.25) |

for any . Moreover,

| (2.26) |

for any such that and are well defined (a proof of relation (2.26) can be found in the appendix for the sake of completeness).

Finally, the following useful equations hold for any (cf. par. 10, Ch. 2 of [10]):

| (2.27) |

2.2. The Optimal Control Problem

In this section we introduce the optimization problem faced by the central bank. The central bank can adjust the level of the exchange rate by purchasing or selling one of the two currencies (i.e. by properly exerting and ), and we suppose that a policy of currency’s devaluation or evaluation results into proportional costs, and , that depend on the current level of the exchange rate. Also, we assume that, being the level of the (log-)exchange rate at time , the central bank faces an holding cost .

The total expected cost associated to a central bank’s policy is therefore

| (2.28) |

In (2.28) is a suitable discount factor of the central bank,

| (2.29) |

and

| (2.30) |

and and denote the continuous parts of and , respectively. Notice that the definition of the costs of control as in (2.2) and (2.2) has been introduced in [49], and it is now common in the singular stochastic control literature (see [35], among many others).

Regarding the holding cost and the proportional costs , we suppose the following.

Assumption 2.7.

-

(i)

belongs to ;

-

(ii)

For any , belongs to . Moreover, setting , , we have

for some , such that . Furthermore,

and the representation

(2.31) holds true. Finally, there exists and such that

Remark 2.8.

-

(1)

All the results of this paper also hold for a slighly weaker regularity condition on , ; namely, if . The latter is equivalent by Sobolev’s embeddings (see, e.g., Cor. 9.15 in Ch. 9 of [11]) to assuming that, for any , is continuously differentiable with second derivative which is locally bounded in .

-

(2)

It is easy to verify that, for example, , , and for all satisfy Assumption 2.7.

- (3)

The following definition characterizes the class of admissible controls.

Definition 2.9.

For any we say that is an admissible control, and we write , if for all (i.e., -a.s.) and the following hold true:

-

(a)

;

-

(b)

;

-

(c)

(for as in Assumption 2.7-(ii)).

The central bank aims at picking an admissible such that the total expected cost functional (2.28) is minimized; that is, it aims at solving

| (2.32) |

3. Solving the Problem

3.1. A Preliminary Verification Theorem

In this section we prove a verification theorem, which provides a set of sufficient conditions under which a candidate value function and a candidate control process are indeed optimal. To this end, we notice that according to the classical theory of singular stochastic control (see, e.g., Chapter VIII of [20]), we expect to identify with a suitable solution to the Hamilton-Jacobi-Bellman (HJB) equation

| (3.1) |

In fact, the latter takes the form of a variational inequality with state-dependent gradient constraints.

Theorem 3.1 (Verification Theorem).

Suppose that Assumption 2.7 holds true and assume that the Hamilton-Jacobi-Bellman equation (3.1) admits a solution such that

for some , and where is the growth coefficients of , (see Assumption 2.7-(ii)). Then one has that on .

Moreover, given an initial condition , suppose also that there exists such that the processes and providing its minimal decomposition are such that

| (3.2) |

Lebesgue-a.e. -a.s., the process

| (3.3) |

and

| (3.4) |

for all -a.s. Then on and is optimal for (2.32).

Proof.

The proof is organized in two steps. We first prove that on , and then that on , and is optimal for (2.32).

Step 1. Let and . Since we can apply Itô-Meyer’s formula for semimartingales (see [38], pp. 278–301) to the process on an arbitrary time interval , . Then, recalling that and denote the continuous parts of and , respectively, we have

| (3.5) | ||||

where we have set

Since the processes and jump on disjoint subsets of we can write

and because and on by (3.1), we end up from (3.1) with

| (3.6) |

By assumption, for all one has , and therefore we can write for some that

| (3.7) | ||||

From the previous equation we have that, for all ,

so that by admissibility of (cf. Definition (2.9)); hence, is a submartingale. Then, taking expectations in (3.1) we have

Taking limits as , and using the fact that is admissible (cf. Definition 2.9), by the dominated convergence theorem we get . Since the latter holds for any and we conclude that on .

Step 2. Let again be given and fixed, and take the admissible satisfying (3.2), (3.3) and (3.4). Then all the inequalities leading to (3.1) become equalities, and taking expectations we obtain

| (3.8) | ||||

By assumption we have that, for any , , so that we can continue from (3.8) by writing

| (3.9) | ||||

By admissibility of (see Definition 2.9) we can take limits as , invoke the dominated convergence theorem for the second expectation in the right hand-side of (3.9), and finally find that

Hence . Combining this inequality with the fact that on by Step 1, we conclude that on and that is optimal. ∎

3.2. Constructing a Candidate Solution

We here construct a solution to the HJB equation (3.1). In particular, given the structure of our problem, we conjecture that there exist two constant trigger values to be determined, say and , such that

and that

| (3.10) |

Following this conjecture we thus start by solving the ODE

| (3.11) |

in , for some to be found. Recalling (2.25), the general solution to equation (3.11) is given by

| (3.12) |

for some . Also, with regard to (3.10) we set

for any , and

for any . Notice that in this way the function is automatically continuous at and .

In order to determine the four unknown constants , , , and , we assume that , and we then find the nonlinear system of four equations

| (3.13) | ||||

| (3.14) | ||||

| (3.15) | ||||

| (3.16) |

Solving (3.13)–(3.14) with respect to and and using (2.26), simple but tedious algebra and the fact that and (cf. Lemma A.1 in the appendix) give

| (3.17) | ||||

| (3.18) |

We now make the following standing assumption.

Assumption 3.2.

One has that

By (2.15)–(2.18), the latter is essentially a requirement on the growth of and , and of their derivatives. Assumption 3.2 then implies that for any

| (3.19) |

Notice now that for any function , standard differentiation, and the fact that and for , yield

| (3.20) |

and

| (3.21) |

As a consequence, using (3.19) we have that is equivalent to

| (3.22) |

whereas is equivalent to

| (3.23) |

Since we are looking for a solution of (3.22) and (3.23) such that , we can rewrite them in the form

| (3.24) | ||||

| (3.25) |

Proposition 3.3.

Proof.

Step 1. We start by proving existence. Given Assumption 2.7, note that the right-hand sides of (3.24) and (3.25) are strictly negative and strictly positive, respectively. For define the two functionals

For a given and fixed , let and notice that by the integral mean-value theorem there exists such that

| (3.26) | ||||

where in the last step we have used (2.27), the fact that , as well as that by Assumptions 2.1 and 2.3. Because of (2.18), and again since , we obtain from (3.2) that , for any given .

On the other hand, by Assumption 2.7 one has

Also, and for . Hence, for any given , by continuity and strict monotonicity of on , there exists a unique such that (3.25) is satisfied.

Analogously, for fixed , take , and for a suitable one finds

| (3.27) |

We thus conclude that, for any given and fixed , , since is natural for (cf. (2.18)) and . On the other hand, ,

and for . Combining all these facts we find that for any there exists a unique such that (3.24) is satisfied. Since by assumption, we clearly have that if a pair such that and exists, then .

In order to prove that there indeed exists such a couple , let

and notice that because one has by Assumption 2.7

On the other hand, for and for a suitable we have by the integral mean-value theorem

Here we have used that on by Assumption 2.7, equation (2.27), as well as that by Assumptions 2.1 and 2.3. Because of (2.18), and since , we find from the previous equation that . Also, is continuous (since is so by the implicit function theorem), and therefore there exists solving , and this value is such that . Hence, there also exists such that solves system (3.24)–(3.25).

Step 2. We now prove that the couple is indeed unique in the domain . For , , and , , the implicit function theorem gives

Since we already know by Step 1 that there exists a solution belonging to , we can study the sign of the previous derivatives in those intervals. By Assumption 2.7 we have

upon recalling that and . Moreover, at the intersection points and , we have

Since and (by the strict monotonicity of and ), we obtain that , or equivalently

Together with the strict monotonicity of and in and , respectively, the latter shows that the intersection point is indeed unique. ∎

Now, with as above, we define our candidate value function as

| (3.28) |

3.3. The Value Function and the Optimal Control

In this section we prove that the function constructed in Section 3.2 (cf. (3.28) above) coincides with the value function (2.32), and we provide the optimal control .

Theorem 3.4.

Proof.

The proof is organized in several steps.

Step 1. By construction, . Moreover, using the growth requirement on , , of Assumption 2.7-(ii), one obtains from (3.28) that there exists such that for all

Step 2. We here show that for all . This is clearly true with equality by construction for , and we now prove that it also holds for . Analogous arguments might then be employed also to show that for .

First of all we rewrite in a tighter form. Notice that since and by Lemma A.1 in the appendix, and because , we can obtain from (3.17)–(3.18)

Then arranging terms and noticing that , , we find from the previous equation that

| (3.29) | ||||

Then using that , and that for , we obtain from (3.29)

| (3.30) | ||||

Since the resolvent satisfies (cf. (2.25))

and because by (2.31), we conclude by simple algebra from (3.30) that

| (3.31) |

Hence (cf. (3.28))

| (3.32) |

Thanks to (3.32) we can now easily check that on . Indeed, since , we have for any that

However, an integration by parts yields

on , upon recalling (3.32) in the last step. Hence, on .

Step 3. To conclude the proof it remains to show that we have on , since we already know by construction that on and on . We here prove that on . Arguments similar to those employed in the following allow to show that also on .

By construction, the function of (3.28) solves on . Given the regularity of , and of and (cf. Assumption 2.1), we can differentiate the previous equation with respect to inside , and find that solves

together with the boundary conditions and .

Now, take , and define the two stopping times

Then, by the Feynman-Kac formula and the strong Markov property of , we can write

upon recalling (2.22). Because the function , , is strictly positive and strictly increasing (by strict monotonicity of and ), we can apply Lemma 2.3 in [16] to evaluate the last two expectations above, and then to write that

The latter equation immediately implies that

| (3.33) |

We now want to show that on since this is clearly equivalent to proving that on such interval. Clearly , and by standard differentiation one also gets that since . Also, by (3.3) we have that , where the last inequality is due to Assumption 2.7 and the positivity of .

If we now can prove that on , then we have that for any , and therefore that on . Recalling (2.31), we can rewrite (3.3) as

| (3.34) |

Then we can employ (2.24) and (2.20) in (3.3), perform a standard differentiation with respect to , and use the fact that and satisfy (3.22)–(3.23) to find after some algebra

| (3.35) |

The function introduced in (3.35) is such that . Moreover, due to Assumption 2.7 we have that

| (3.36) |

and for any . We now have two cases: either (i) there exists such that (and notice that, if it exists, such a point is unique by strict monotonicity of on ); or (ii) for any .

In case (ii), we immediately conclude from (3.35) that on , and therefore that on .

On the other hand, if we are in case (i), by (3.35) we see that the point is also the unique stationary point of . In fact, it is a maximum of since one can easily derive from (3.35) that , where the last inequality is due to the fact that but . However, since we know that and , we conclude that also in case (ii) one has that on , and therefore that on .

Step 4. Combining the results of the previous steps the proof is completed. ∎

Given , let be such that where is the couple of nondecreasing processes that solves the following double Skorokhod reflection problem

| (3.40) |

Under Assumption 2.1, Problem admits a unique pathwise solution (cf., e.g., Theorem 4.1 in [46]). Moreover, and are continuous, a part possible jumps at time zero of amplitude and , respectively. It also follows that . In the following, we set a.s., and, to simplify notation, , -a.s.

Proposition 3.5.

Let and let solve . Then the process is an admissible control.

Proof.

Clearly . To prove the admissibility of , we have to verify the requirements of Definition 2.9. Since for all , and , we have that -a.s. Moreover, it is easy to see that also (b) and (c) of Definition 2.9 are fulfilled.

It thus remains to show that Definition 2.9-(a) is satisfied as well. By (2.2) and the fact that solves we have

| (3.41) |

where we have used that is the support of the measure on , , induced by the continuous part of . The continuity of yields

| (3.42) |

Also, arguing as in the proof of Lemma 2.1 of [42] (see in particular equations (2.16)–(2.17) therein), we have that

| (3.43) |

Since analogous arguments apply to , by combining (3.42), (3.43) and (3.3), we conclude that the requirement of Definition 2.9-(a) holds true, and therefore that . ∎

Theorem 3.6.

3.4. A Link with an Optimal Stopping Game

The following proposition provides a probabilistic representation of the derivative of the value function. This result plays an important role in the next section where we perform a comparative statics analysis.

Proposition 3.7.

Let be the value function of (2.32). Then for any one has

| (3.44) |

where , are -stopping times, and

| (3.45) |

Moreover, for any , the couple of -stopping times given by

| (3.46) |

form a saddle-point; that is,

for any couple of -stopping times .

Proof.

We only provide a sketch of the proof, since its arguments are quite standard. From Theorem 3.6 we know that on , with as in (3.28). Since , then . Moreover, it is easy to check from (3.28) that is locally bounded on ; that is, . Moreover,

| (3.47) |

| (3.48) |

| (3.49) |

The first equation in (3.47) easily follows by noticing that for any , and by differentiating such an equation with respect to . On the other hand, the inequalities involving in (3.48) and in (3.49) follow from Assumption 2.7-(ii), together with the fact that and .

Given an arbitrary -stopping time , an application of a generalized version of Itô’s lemma (see, e.g., Theorem 10.4.1 in [40]) to the process on the interval yields , upon using (3.47)-(3.49). On the other hand, applying again generalized Itô’s lemma to the process , but now on the interval for an arbitrary -stopping time , and employing (3.47)-(3.49) gives . Finally, by using generalized Itô’s lemma on the process on the interval one finds that by (3.47).

The previous proposition shows that equals the value function of a zero-sum game of optimal stopping (a so-called Dynkin game, cf. [19]). Furthermore, the boundaries that trigger the optimal control, also determine a saddle-point in the game of optimal stopping. Such finding is consistent to the known relation between bounded variation control problems and zero-sum games of optimal stopping (see, e.g., [23], [31], and [45]).

4. A Case Study with a Mean-Reverting (Log-)Exchange Rate

In this section we assume that in (2.3) one has , for some and , and ; that is, for a given , the (log-)exchange rate is a linearly controlled mean-reverting process with dynamics

| (4.1) |

In absence of interventions (i.e. ), this specification is the simplest dynamics which keeps in a given (suitable) region with a high probability, and empirical studies (see, e.g., [9, 47]) have concluded that it well describes several exchange rates among the main world countries.

In this section we also take the instantaneous costs , , such that for all , and we specify a quadratic holding cost function of the form

The parameter represents a so-called reference target, and it can be also viewed as the logarithm of the central parity (introduced in [32] for the first time). The function penalizes any displacement of the (log-)exchange rate from such a value.

We notice that with as in (4.1), we have for all . It thus follows that the process of (2.4) is the unique strong solution to

| (4.2) |

where is a standard Brownian motion. Moreover, because , the characteristic equation (2.12) reads , , and it is known that it admits the two linearly independent, positive solutions (cf. [27], p. 280)

| (4.3) |

and

| (4.4) |

which are strictly decreasing and strictly increasing, respectively. In both (4.3) and (4.4) is the cylinder function of order given by (see, e.g., [7], Chapter VIII, Section 8.3, eq. (3) at page 119)

| (4.5) |

where is the Euler’s Gamma function.

Within this setting, it is easy to see that the two equations for the free boundaries and (cf. (3.24) and (3.25)) read

| (4.6) | ||||

| (4.7) |

where is given by (2.13).

In the next section we study the dependency of the optimal boundaries and with respect to the model’s parameters , , , , and .

4.1. Comparative Statics Results

In the following we will often use the notation , and to stress the dependence of , and with respect to a given parameter. For some of the next results (namely, Propositions 4.1, 4.3, and 4.4) an important role is played by the representation of given in (3.44).

Proposition 4.1.

The optimal intervention boundaries and are decreasing in the long-run equilibrium level ; that is, and are decreasing.

Proof.

Proposition 4.2.

The more the exchange market is volatile, the more the central bank is reluctant to intervene. That is, the optimal intervention boundaries and are such that is decreasing, and is increasing.

Proof.

We borrow arguments from the proof of Theorem 6.1 in [36] (see also Section 3 in [3]). Let , and denote by the solution to (4.1) for and for a volatility coefficient . Let , and for denote by the value function (2.32) when the underlying controlled process solves (4.1) with volatility , by the infinitesimal generator associated to the (uncontrolled) diffusion , and by the infinitesimal generator associated to the solution to (4.2) with volatility . Also, and , , are the optimal control boundaries associated to the value function , .

Then, recall that the value function equals the function given in (3.28) and use that for any (cf. (3.31)),

| (4.8) |

to find

We now prove that all the terms appearing on the right hand-side of the latter equation are nonnegative. On the one hand,

and

where the last inequalities are due to Assumption 2.7 and the fact that .

On the other hand, we notice that since for all , the convexity of and the linearity of the dynamics (4.1) imply that functional is simultaneously convex in , and the set of admissible controls is convex. Therefore,

for all , , , and . Hence is convex on , and this fact in turn yields

since .

It thus follows from the previous considerations that for all . Moreover, since is the value function when , we also have and on , for some , and for as in Assumption 2.7. Therefore, arguing as in Step 1 of the proof of Theorem 3.1 we can show that on .

Thanks to the last inequality we can now prove that . We follow a contradiction scheme, and we suppose that . Then noticing that , and using (4.8) and Assumption 2.7-(ii) we have that (recall that here , )

The latter inequality contradicts that on , and therefore shows that . Analogous arguments can be employed to obtain . ∎

Proposition 4.3.

The optimal intervention boundaries and are such that is decreasing, and is increasing. Also, is decreasing and is increasing.

Proof.

Analogously, taking now we have

i.e., is decreasing and is increasing. ∎

Proposition 4.4.

The optimal intervention boundaries and are such that and are increasing.

Proof.

We notice that is decreasing. It follows from (3.44) that is decreasing as well, and therefore for all we have

Thus, and are both increasing, so that when the target level increases, the no-intervention region is displaced towards higher values. ∎

Remark 4.5.

Notice that the previous monotonicity results can be easily generalized to the case of a more general diffusion. For example, assuming that a comparison principle à la Yamada-Watanabe (see, e.g., Proposition 5.2.18 in [30]) holds true for the diffusion (2.4), that the killing rate is decreasing (i.e. is convex), and that the holding cost function is convex, one can show that the boundaries are monotonically decreasing with respect to the drift coefficient. Also, arguing as in the proof of Theorem 6.1 in [36], one can prove the monotonicity of the boundaries with respect to a general state-dependent volatility coefficient. However, we decided to formulate the study of this section for an Ornstein-Uhlenbeck process because it is perhaps the simplest diffusion that captures the mean-reverting behavior of exchange rates empirically observed in some economies (see [44, 47, 48], and references therein).

4.2. Expected Exit Time from the Target Zone

One of the great advantage of the Ornstein-Uhlenbeck model above is that many quantities about exit times and probabilities are known in closed form. We base our analysis on the results contained in [14, Appendix B]. Recalling the optimally controlled process , define the exit time from as

and notice that for all . Indeed, if then clearly -a.s. On the other hand, if then the optimal control is such that for any , and the (uncontrolled) Ornstein-Uhlenbeck process is positively recurrent. Also, we have that

| (4.9) | |||||

| (4.10) |

Furthermore, we know that the function , , satisfies the boundary value differential problem

whose solution is

| (4.11) |

with the constants and given by

Thanks to the previous results we can numerically compute the mean time until the exchange rate leaves the target zone, i.e. the mean time until the next central bank’s intervention. This will be done in the next section.

4.3. Numerical results

We now present a possible implementation of the previous model, tailored to mimick the DKK/EUR exchange rate. Since it seems that in 30 years there was no need to intervene from the Danish Central Bank, we can safely assume that the long-run mean corresponds to the logarithm of the central parity fixed to 7.46038 DKK/EUR. Remembering that the Ornstein-Uhlenbeck process in equation (4.1) represents the logarithm of the exchange rate, we thus let ; other plausible parameters for the Ornstein-Uhlenbeck dynamics could be and . Given the interest rates in the current economy, a plausible value for could be . The values above are characteristic of the Danish and European economies, and still do not reflect the Danish Central Bank’s policy, which is instead implemented in the three parameters , and . We collect the parameters up to now in Table 1.

| 0.005 | 0.015 | 0.001 | 2.01 | 2.01 |

In order to find the known intervention thresholds of from the central parity, we must implement the following inverse problem: find such that, with the parameters above, the optimal and are

Given the (approximate) symmetry of our problem111since , we search for and such that . From the monotonicity result of Proposition 4.3 we know that, by increasing (decreasing) the common proportional cost , the continuation region will enlarge (shrink): this is a positive sign that our inverse problem can have a unique solution.

With this in mind, we search for such that . We start checking for , and we continue by decreasing the value of until we find our zone: the results are reported in Table 2.

| 1 | 1.93729 | 2.08193 | 0.07232 | 0.07232 |

|---|---|---|---|---|

| 0.5 | 1.95302 | 2.0662 | 0.0565905 | 0.0565905 |

| 0.1 | 1.97703 | 2.04218 | 0.0325786 | 0.0325786 |

| 0.05 | 1.98383 | 2.03539 | 0.0257803 | 0.0257803 |

| 0.04 | 1.98569 | 2.03352 | 0.0239155 | 0.0239155 |

| 0.035 | 1.98674 | 2.03247 | 0.0228658 | 0.0228658 |

| 0.034 | 1.98696 | 2.03225 | 0.0226442 | 0.0226442 |

| 0.0335 | 1.98707 | 2.03214 | 0.0225317 | 0.0225317 |

| 0.033 | 1.98719 | 2.03202 | 0.0224182 | 0.0224182 |

| 0.03 | 1.98789 | 2.03132 | 0.021712 | 0.021712 |

Hence, given the parameters’ values of Table 1, if we let , we find that the optimal and well approximate the boundaries of the target zone that the Central Bank of Denmark is adopting since January 12, 1987 [37].

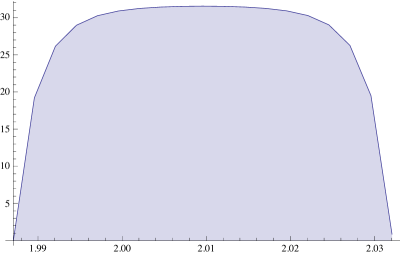

By using the results in Section 4.2, we can also compute the expected exit time of the exchange rate from the target zone. In fact, by taking , equation (4.11) can be plotted as a function of initial (log-)exchange rate . The plot is in Figure 4.1 below.

We can see that the maximal expected time is obtained (as expected) when the deviation from central parity is null, i.e., for , and decreases as the exchange rate nears the target zone’s boundaries. This maximum expected time is around 31.11 years, which is also the expected time before an intervention by the central bank is triggered. This finding is perfectly in line with the observed phenomenon that the Danish Central Bank did not need to intervene to keep the DKK/EUR exchange rate within the target zone since the last 30 years [37].

We now try to reproduce, on this set of parameters, the “pegging” phenomenon which was observed in the CHF/EUR exchange rate in the period 2011–2015 (see Figure 1.1 and [50, 51]). The economic intuition behind it is that the central bank would intervene in pegging the rate above (or below) a certain threshold, even if the rates’ uncontrolled dynamics would push it beyond that threshold. This can be easily implemented in the present framework, by simply changing to be a value different from . Due to the monotonicity results of Proposition 4.4, this would modify the width of the continuation region . If for example, in the previous framework, we let for , then we expect that and are increased. In fact, by keeping all the other parameters fixed, we find the results in Table 3.

| 0 | 1.98707 | 2.03214 | 0.02253 | 0.0225317 |

|---|---|---|---|---|

| 0.01 | 1.99709 | 2.04215 | 0.01251 | 0.0325466 |

| 0.02 | 2.0071 | 2.05217 | 0.00250 | 0.0425615 |

| 0.03 | 2.01712 | 2.06218 | 0.00751 | 0.0525764 |

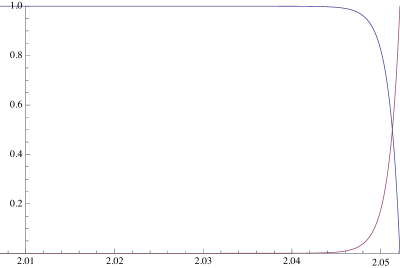

We can observe that, by increasing , also the target zone increases. In particular, it suffices to increase by (remembering that , this would amount to less than 2% of relative increase of the exchange rate) to make that the long-term mean of the exchange rate is outside of the target zone (in fact, in this case we have ). Even in the less severe scenario of , we would have that is still inside the target zone, but very near to the lower threshold. By using again the results in Section 4.2, we can estimate the expected exit time of the exchange rate from the target zone also in this case, and plot the results in Figure 4.2.

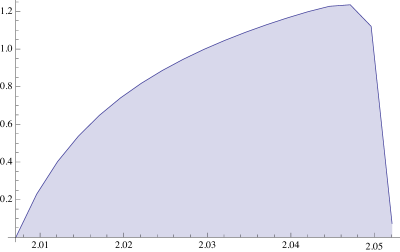

As expected, here we notice a sharp asymmetry: the long-term mean is still , but the target zone is now not symmetric around it. As a consequence, if the (log-)exchange rate starts from , the expected exit time from the target zone (i.e. before the central bank is forced to intervene) is , i.e. about 3 months (instead of the 30+ years of the previous case). However, if we start from , then the process will revert with high probability towards its mean , taking some time in doing that, and then it will spend about other 3 months before hitting one of the boundaries of the target zone. Such an expected time to return to the long-term mean (and thus the expected exit time from the target zone) is an increasing function of the initial level of the (log-)exchange rate for any . Letting the exchange rate process start from a value , it then becomes more probable to exit the target zone from , and the expected exit time starts to decrease. We can also see that at such a critical level we have ; i.e. starting from the expected exit time is maximal, and it is about 1 year and 3 months.

In Figure 4.3, we draw the exit probability from as a function of initial state . We can see that the probability of hitting the “peg” is essentially equal to 1 for any initial value of the (log-)exchange rate . For higher values such a probability then starts to decrease, up to a critical point near to (actually, slightly above 2.05), where it becomes more probable to leave the target zone from than from .

5. Concluding Remarks

In this paper we have studied the optimal management problem of exchange rates faced by a central bank. We have formulated it as an infinite time-horizon singular stochastic control problem for a one-dimensional diffusion that is linearly controlled through a process of bounded variation. We have provided the explicit expression of the value function, as well as the complete characterization of the optimal control. At each instant of time, the optimally controlled exchange rate is kept within an optimal band (continuation region), whose boundaries (the so-called free boundaries) are endogenously determined as part of the solution to the problem.

A detailed comparative statics analyisis of the free boundaries is provided when the (log-)exchange rate (in absence of any intervention) evolves as an Ornstein-Uhlenbeck process. This dynamics captures the mean-reverting behavior of exchange rates that has been observed in several empirical studies (see [44, 47] and references therein). Moreover, it allows the central bank to have aims, both in its cost function as well as in its intervention costs , which possibly contrast with this foreign exchange dynamics. This does not happen if, for example, the minimum of is very near to the long-term mean of the exchange dynamics: in this case, the exchange rate stays naturally with a high probability in the continuation region. This fact can be interpreted as the “target zone” introduced in [32], and it applies, for example, to the Danish and Hong Kong currencies [37, 52]. Instead, if the rate’s long-term mean is far from the minimum of , or worse even outside the continuation region, then it is very probable that the exchange rate hits one boundary of the continuation region much more often than the other one. This phenomenon is usually referred to as “pegging” the exchange rate above or below a given threshold, and it has been observed in the period 2011–2015 in the dynamics of the Swiss Franc versus the Euro [50, 51].

Several comments deserve to be made on our model, and on its possible extensions. First of all, it is worth noting that, given its generality, the control problem studied in this paper might be a reasonable model also in other context, as, e.g., for problems of partially reversible capacity expansion (see [17], [22], among others), for the optimal management of an inventory (see [24] for an early work), for the automotive cruise control of an aircraft under an uncertain wind condition [15], or for the optimal management of stabilization funds [25]. Second of all, there are several possible directions towards our study on exchange rates’ control can be extended. In particular, it would be extremely interesting to develop a mathematical model taking into account the strategic interaction between two (or more) central banks for the management of the exchange rates (see also [1] for a recent contribution in this direction). This would lead to a challenging nonzero-sum stochastic game with singular controls that we leave for future research.

Acknowledgments

Financial support by the German Research Foundation (DFG) through the Collaborative Research Centre 1283 “Taming uncertainty and profiting from randomness and low regularity in analysis, stochastics and their applications” is gratefully acknowledged by the first author. Part of this work has been done while the first author was visiting the Department of Mathematics of the University of Padova thanks to the funding provided by the “ACRI Young Investigator Training Program” (YITP-QFW2017).

Appendix A

Lemma A.1.

Under Assumption 2.5 one has that and , where and are the strictly increasing and strictly decreasing fundamental solutions of the ODE for killed at rate .

Proof.

We simply repeat the arguments in the second part of the proof of Lemma 4.3 in [6] (see also Theorem 9 in [2]). Under Assumption 2.1 standard differentiation reveals that and solve the ODE

| (A-1) |

Also, for any one has , and so any solution to the previous ODE has to be of the form . Furthermore, note that under Assumption 2.1 and 2.3, Corollary 1 of [3] can be applied yielding that and are strictly convex.

We thus find that for all and for all we can write

where , -a.s., and and are the fundamental solutions of (A-1) when is killed at and .

Proof of Equation (2.26)

Assumption 2.1 guarantees that the flow is a.s. continuous, increasing and differentiable for any (see, e.g., [41], Ch. V.7). Defining the process such that , , by ordinary differentiation we find that satisfies

and therefore that

where the exponential martingale has been defined in equation (2.6).

As in Remark 2.2, consider the dynamics of under the measure , and the dynamics of under the measure . Define also a new measure through the Radon-Nikodym derivative and notice that the Girsanov theorem implies that the process

is a standard Brownian motion under .

References

- [1] Aïd, R., Basei, M., Callegaro, G., Campi, L., Vargiolu, T. (2017). Nonzero-sum stochastic differential games with impulse controls: a verification theorem with applications. Preprint. ArXiv: 1605.00039.

- [2] Alvarez, L.H.R. (2001). Singular stochastic control, linear diffusions and optimal stopping: a class of solvable problems. SIAM J. Control Optim. 39(6), pp. 1697–1710.

- [3] Alvarez, L.H.R. (2003). On the properties of a class of -excessive mappings for a class of diffusions. Ann. Appl. Probab. 13(4), pp. 1517–1533.

- [4] Alvarez, L.H.R. (2004). A class of solvable impulse control problems. Appl. Math. Optim. 49, pp. 265–295.

- [5] Alvarez, L.H.R. (2008). A class of solvable stopping games. Appl. Math. Optim. 58, pp. 291–314.

- [6] Alvarez, L.H.R., Matomäki, P. (2015). Expected supremum representation of the value of a singular stochastic control problem. Preprint. ArXiv: 1508.02854.

- [7] Bateman, H. (1981). Higher Trascendental Functions, Volume II. McGraw-Hill Book Company.

- [8] Bertola, G., Runggaldier, W. J., Yasuda, K. (2016). On classical and restricted impulse stochastic control for the exchange rate. Appl. Math. Optim. 74(2), pp. 423–454.

- [9] Bo, L., Li, D., Ren, G. Wang, Y., Yang, X. (2016). Modeling the exchange rates in a target zone by reflected Ornstein-Uhlenbeck process. Preprint. Available at SSRN: https://ssrn.com/abstract=2107686 or http://dx.doi.org/10.2139/ssrn.2107686

- [10] Borodin, W.H., Salminen, P. (2002). Handbook of Brownian Motion-Facts and Formulae. 2nd Edition. Birkhäuser.

- [11] Brezis, H. (2011). Functional Analysis, Sobolev Spaces and Partial Differential Equations. Universitext, Springer.

- [12] Cadenillas, A., Zapatero, F. (1999). Optimal central bank intervention in the foreign exchange market. J. Econ. Theory 87, pp. 218–242.

- [13] Cadenillas, A., Zapatero, F. (2000). Classical and impulse stochastic control of the exchange rate using interest rates and reserves. Math. Finance 10, pp. 141–156.

- [14] Cadenillas, A., Sarkar, S., Zapatero, F. (2007). Optimal dividend policy with mean-reverting cash reservoir. Math. Finance 17(1), pp. 81–109.

- [15] Chow, P.L., Menaldi, J.L., Robin, M. (1985). Additive control of stochastic linear systems with finite horizon, SIAM J. Control Optim. 23(6), pp. 858–899.

- [16] Dayanik, S. (2008). Optimal stopping of linear diffusions with random discounting, Math. Oper. Res. 33(3), pp. 645–661.

- [17] De Angelis, T., Ferrari, G. (2014). A stochastic partially reversible investment problem on a finite-time horizon: free-boundary analysis, Stochastic Process. Appl. 124, pp. 4080–4119.

- [18] De Jong, F., Drost, F.C., Werker, B.J.M. (2001). A jump-diffusion model for exchange rates in a target zone. Statist. Neerlandica 55(3), pp. 270–300.

- [19] Dynkin, E.B. (1969). Game variant of a problem on optimal stopping, Soviet. Math. Dokl. 10, pp. 270–274.

- [20] Fleming, W.H., Soner, H.M. (2005). Controlled Markov processes and viscosity solutions. 2nd Edition. Springer.

- [21] Graczyk, P., Jakubowski, T. (2008). Exit times and Poisson kernels of the Ornstein-Uhlenbeck diffusion, Stoch. Models 24(2), pp. 314–337.

- [22] Guo, X., Pham, H. (2005). Optimal partially reversible investment with entry decision and general production function, Stochastic Process. Appl. 115, pp. 705–736.

- [23] Guo, X., Tomecek, P. (2008). Connections between singular control and optimal switching. SIAM J. Control Optim. 47(1), pp. 421–443.

- [24] Harrison, M., Taksar, M.I. (1983). Instantaneous control of Brownian motion. Math. Oper. Res. 8(3), pp. 439–453.

- [25] Huamán-Aguilar, R. (2015). Stochastic control for optimal government debt management. Ph.D. Thesis, University of Alberta.

- [26] Jeanblanc-Picqué, M. (1993). Impulse control method and exchange rate. Math. Finance 3, pp. 161–177.

- [27] Jeanblanc, M., Yor, M., Chesney, M. . Mathematical Methods for Financial Markets. Springer.

- [28] Jørgensen, B., Mikkelsen, H. O. (1996). An arbitrage free trilateral target zone model. J. Int. Money Finance 15(1), pp. 117–134.

- [29] Karatzas, I., Shreve, S.E. (1985). Connections between optimal stopping and singular stochastic control II. Reflected follower problems. SIAM J. Control Optim. 23(3), pp. 433–451.

- [30] Karatzas, I., Shreve, S.E. (1991). Brownian motion and stochastic calculus (Second Edition). Graduate Texts in Mathematics 113, Springer-Verlag, New York.

- [31] Karatzas, I., Wang, H. (2005). Connections between bounded-variation control and Dynkin games in “Optimal Control and Partial Differential Equations”; Volume in Honor of Professor Alain Bensoussan’s 60th Birthday (J.L. Menaldi, A. Sulem and E. Rofman, eds.), pp. 353–362. IOS Press, Amsterdam.

- [32] Krugman, P.R. (1991). Target zones and exchange rate dynamics. Quart. J. Econ. 106(3), pp. 669–682.

- [33] Larsen, K.S., Sørensen, M. (2007). Diffusion models for exchange rates in a target zone. Math. Finance 17(2), pp. 285–306.

- [34] C. Lloyd (2015). On the end of the EUR CHF peg. SNBCHF.com, February 6, 2015 https://snbchf.com/chf/colin-lloyd-end-eur-chf-peg/

- [35] Lon, P.C., Zervos, M. (2011). A model for optimally advertising and launching a product. Math. Oper. Res. 36, pp. 363–376.

- [36] Matomäki, P. (2012). On solvability of a two-sided singular control problem. Math. Meth. Oper. Res 76, pp. 239–271.

-

[37]

Mikkelsen, O. (2017). Denmark’s fixed exchange rate policy: 30th anniversary of unchanged central rate. News — Danmarks Nationalbank, Jan. 2017 n. 1.

http://www.nationalbanken.dk/en/publications/Pages/2017/01/Denmark’s-fixed-exchange-rate-policy-30th-anniversary-of-unchanged-central-rate.aspx - [38] Meyer, P.A. (1976). Lecture Notes in Mathematics 511. Seminaire de Probailities X, Université de Strasbourg. Springer-Verlag. New York.

- [39] Mundaca, G., Øksendal, B. (1998). Optimal stochastic intervention control with application to the exchange rate. J. Math. Econ. 29, pp. 223–241.

- [40] Øksendal, B. (2003). Stochastic differential equations (Sixth Edition). Springer, Berlin-Heidelberg-New York.

- [41] Protter, P. (1990). Stochastic Integration and Differential Equations. Springer, Berlin.

- [42] Shreve, S.E., Lehoczky, J.P., Gaver, D.P. (1984). Optimal consumption for general diffusions with absorbing and reflecting barriers. SIAM J. Control Optim. 22(1) , pp. 55–75.

- [43] Shreve S.E. (1988). An Introduction to Singular Stochastic Control, in Stochastic Differential Systems, Stochastic Control Theory and Applications, IMA Vol. 10, W. Fleming and P.-L. Lions, ed. Springer-Verlag, New York.

- [44] Sweeney, R. J. (2006). Mean reversion in G-10 nominal exchange rates. J. Finan. Quant. Anal. 41(3), pp. 685–708

- [45] Taksar, M.I. (1985). Average optimal singular control and a related stopping problem. Math. Oper. Res. 10(1), pp. 63–81.

- [46] Tanaka, H. (1979). Stochastic differential equations with reflecting boundary condition in convex regions. Hiroshima Math. J. 9, pp. 163–177.

- [47] Tvedt, J. (2012). Small open economies and mean reverting nominal exchange rates. Australian Econ. Pap. 51(2), pp. 85–95.

- [48] Yang, X., Ren, G., Wang, Y., Bo, L., Li, D. (2016). Modeling the exchange rates in a target zone by reflected Ornstein-Uhlenbeck process. Perprint. Available at SSRN, https://ssrn.com/abstract=2107686 or http://dx.doi.org/10.2139/ssrn.2107686.

- [49] Zhu, H. (1992). Generalized solution in singular stochastic control: The nondegenerate problem. Appl. Math. Optim. 25(3), pp. 225–245.

- [50] Swiss Central Bank Acts to Put a Cap on Franc’s Rise. The New York Times, Sept. 6, 2011. http://www.nytimes.com/2011/09/07/business/global/swiss-franc.html

- [51] The Economist explains: Why the Swiss unpegged the franc. The Economist, Jan. 18, 2015. http://www.economist.com/blogs/economist-explains/2015/01/economist-explains-13

-

[52]

Hong Kong Monetary Authority. Linked exchange rate system. http://www.hkma.gov.hk/eng/key-functions/monetary-stability/linked-exchange-rate-

system.shtml