Convex function approximations for Markov decision processes

Abstract.

This paper studies function approximation for finite horizon discrete time Markov decision processes under certain convexity assumptions. Uniform convergence of these approximations on compact sets is proved under several sampling schemes for the driving random variables. Under some conditions, these approximations form a monotone sequence of lower or upper bounding functions. Numerical experiments involving piecewise linear functions demonstrate that very tight bounding functions for the fair price of a Bermudan put option can be obtained with excellent speed (fractions of a cpu second). Results in this paper can be easily adapted to minimization problems involving concave Bellman functions.

Keywords. Convexity, Dynamic programming, Function approximation, Markov decision processes

1. Introduction

Sequential decision making under uncertainty can often be framed using Markov decision processes (see [10, 7, 17] and the references within). However, due to the tedious nature of deriving analytical solutions, some authors have suggested the use of approximate solutions instead [16] and this view has been readily adopted due to the advent of cheap and powerful computers. Typical numerical methods either use a finite discretization of the state space [15, 6] or using a finite dimensional approximation of the target functions [20]. This paper will focus on the latter approach for Markov decision processes containing only convex functions and a finite number of actions. Convexity assumptions are often used because it affords many theoretical benefits and the literature is well developed [18]. When there are a finite number of actions, there are two main issues facing function approximation methods in practice. The first involves estimating the conditional expectation in the Bellman recursion. The second deals with representing the reward functions and the expected value functions using tractable objects. This paper approaches the expectation operator using either an appropriate discretization of the random variables or via Monte Carlo sampling. The resulting Bellman functions are then approximated using more tractable convex functions. While many approaches have appeared in the literature [2, 16], this paper differs from the usual in the following manner. Typical approaches assume a countable state space or bounded rewards/costs. However, many problems in practice do not satisfy this and so this paper will not take this approach. This paper also directly exploits convexity to extract desirable convergence properties. Given that decisions are often made at selected points in time for many realistic problems, this paper assumes a discrete time setting and this avoids the many technical details associated with continuous time.

Regression based methods [4, 19, 14] have become a popular tool in the function approximation approach. These methods represents the conditional expected value functions as a linear combination of basis functions. However, the choice of an appropriate regression basis is often difficult and there are often unwanted oscillations in the approximations. This paper is related closest to the work done by [9] and [11]. The authors in [9] considered monotone increasing and decreasing bounding function approximations for discrete time stochastic control problems using an appropriate discretization of the random variable. Like this paper, they assumed the functions in the Bellman recursion satisfy certain convexity conditions. However, their functions are assumed to be bounded from below unlike here. In their model, an action is chosen to minimise the value as opposed to maximise in our setting. In addition, this paper considers an extra layer of function approximation to represent the resulting functions in the Bellman recursion. Nonetheless, this paper adapts some of their brilliant insights. In [11], the author exploits convexity to approximate the value functions by using convex piecewise linear functions formed using operations on the tangents from the reward functions. The scheme in [11] results in uniform convergence on compact sets of the approximations and has been successfully applied to many real world applications [13, 12]. Unlike [11], this paper will not impose global Lipschitz continuity on the functions in the Bellman recursion and does not assume linear state dynamics. A much more general class of function approximation is also studied here. Moreover, this paper proves the same type of convergence under random Monte Carlo sampling of the state disturbances as well as deriving bounding functions. In this sense, this paper significantly generalizes the remarkable work done by [11].

This paper is organized as follows. The next section introduces the finite horzion discrete time Markov decision process setting and the convexity assumptions used. The state is assumed to consist of a discrete component and a continuous component. This is a natural assumption since it covers many practical applications. Convexity of the target and approximating functions is assumed on the continuous component of the state. A general convex function approximation scheme is then presented in Section 3. In Section 4, uniform convergence of these approximations to the true value functions on compact sets is proved using straightforward arguments. This convergence holds under various sampling schemes for the random variables driving the state evolution. Under conditions presented in Section 5 and Section 6, these approximations form a non-decreasing sequence of lower bounding or a non-increasing sequence of upper bounding functions for the true value functions, respectively. This approach is then demonstrated in Section 7 using piecewise linear function approximations for a Bermudan put option. The numerical performance is impressive, both in terms of the quality of the results and the computational times. Section 8 concludes this paper. Note that in this paper, global Lipschitz continuity is referred to as simply Lipschitz continuity for shorthand.

2. Markov decision process

Let represent the probability space and denote time by . The state is given by consisting of a discrete component taking values in some finite set and a continuous component taking values in an open convex set . This paper will refer to as the state space. Now at each , an action is chosen by the agent from a finite set . Suppose the starting state is given by with probability one. Assume that evolves as a controlled Markov chain with transition probabilities for and . Here is the probability from moving from to after applying action at time . Assume the Markov process is governed by action via

for some random variable and measurable transition function . At time , is the random disturbance driving the state evolution after action is chosen. The random variables and are assumed to be integrable for , , and .

The decision rule gives a mapping which prescribes an action for a given state . A sequence of decision rules is called a policy. For each starting state and each policy , there exists a probability measure such that and

for each measurable at where denotes our Markov transition kernel after applying action at time . The reward at time is given by . A scrap value is collected at terminal time . Given starting , the controller’s goal is to maximize the expectation

over all possible policies . That is, to find an optimal policy satisfying for any policy . There are only a finite number of possible policies in our setting. Note that this paper focuses only on Markov decision policies since history dependent policies do not improve the above total expected rewards [10, Theorem 18.4].

Let represent the one-step transition operator associated with the transition kernel. For each action , the operator acts on functions by

| (1) |

If an optimal policy exists, it may be found using the following dynamic programming principle. Introduce the Bellman operator

for , , and . The resulting Bellman recursion is given by

| (2) |

for . If it exists, the solution gives the value functions and determines an optimal policy by

| (3) |

for , , and .

2.1. Convex value functions

Since is finite, the existence of the value functions is guaranteed if the functions in the Bellman recursion are well defined. This occurs, for example, when the reward, scrap, and transition operator satisfies the following Lipschitz continuity. Let represent some norm below.

Theorem 1.

If , , and are Lipschitz continuous in for , , and , then the value functions exists.

Proof.

If the functions in the Bellman recursion have an upper bounding function [1, Definition 2.4.1], there will be no integrability issues [1, Proposition 2.4.2]. For , and , Lipschitz continuity yields

for some constant and for . Therefore, and for some constant for and . By assumption on , for , , and ,

for some constant . Therefore, an upper bounding function for our Markov decision process is given by with constant coefficient given by . ∎

Note that on a finite dimensional vector space (), all norms are equivalent and so the choice of is not particularly important. The existence of the value functions and an optimal policy is problem dependent and so the following simplifying assumption is made to avoid any further technical diversions.

Assumption 1.

Bellman functions , , and are well defined and real-valued for all , , , and .

Under the above assumption, value functions and an optimal policy exists. Further, they can be found via the Bellman recursion presented earlier. Since convex functions plays a central role in this paper and to avoid any potential misunderstanding regarding this, the following definition is provided.

Definition 1.

A function is convex in if

for and .

Note that since is open, convexity in automatically implies continuity in . Now impose the following continuity and convexity assumptions.

Assumption 2.

Let be continuous in for and .

Assumption 3.

Let and be convex in for , and . If is convex in , then is also convex in for .

Assumption 2 will be used to apply the continuous mapping theorem in the proofs and Assumption 3 guarantees that all the value functions are convex in for and . Convexity can be preserved by the transition operator (as stated in Assumption 3) due to the interaction between the value function and the transition function. Let us explore just a few examples for :

-

•

If is non-decreasing convex in and is convex in , the composition is convex in .

-

•

Similarly, is convex in if is convex non-increasing in and is concave in .

-

•

If is affine linear in , is also convex in if is convex in . Note this is a consequence of the first two cases since an affine linear function is both convex and concave.

-

•

If the space can be partitioned so that in each component any of the above cases hold, the function composition is also convex in .

3. Approximation

Denote to be a -point grid. This paper adopts the convention that and is dense in . Suppose is a continuous function and introduce some function approximation operator dependent on the grid (this will be clarified shortly) which approximates using another more tractable continuous function. Some examples involving piecewise linear approximations are depicted in Figure 1.

The first step in dealing with the Bellman recursion is to approximate the transition operator (1). For each time and action , choose a suitable -point disturbance sampling with weights . Define the modified transition operator by

| (4) |

and the modified Bellman operator by

| (5) |

where is a function continuous in for . In the above, the approximation scheme is applied to the functions for each and . The resulting backward induction

| (6) |

for gives the modified value functions . From Assumption 2 and the continuity of the modified value functions in for , it is clear that is continuous in for , , and since we have the composition of continuous functions.

The central idea behind this paper is to approximate the original problem in (2) with a more tractable problem given by (6). Therefore, one would like the functions in modified Bellman recursion to resemble their true counterparts. Since Assumption 3 imposes convexity on the functions in the original Bellman recursion and is used to approximate these functions, the following assumption on convexity and pointwise convergence on the dense grid is only natural.

Assumption 4.

For all convex functions , suppose that is convex in for and that for .

The following assumption is now made to hold throughout this paper to guarantee the convexity of the modified value functions.

Assumption 5.

Assume and are convex in for , , and .

Theorem 2.

Proof.

By assumption, is convex in for , , and . The reward functions are convex in (by Assumption 3) for and . Therefore, is convex in by Assumption 4. The sum and pointwise maximum of convex functions is convex. Therefore, is convex in for and due to application of . Proceeding inductively for gives the desired result. ∎

Please note that the grid can be easily made time dependent without affecting the convergence results in the next section. But for notational simplicity, this dependence is omitted. Also note that the modified Bellman operator (5) is not necessarily monotone since the operator is not necessarily monotone. It turns out that the convergence results presented in the next section does not require this property. However, to obtain lower and upper bounding functions in Section 5 and Section 6, this paper will impose Assumption 6 in Section 5 to induce monotonicity in the modified Bellman operator.

4. Convergence

This section proves convergence of the modified value functions. There are two natural choices for the disturbance sampling and weights:

-

•

Use Monte Carlo to sample the disturbances randomly and the realizations are given equal weight or;

-

•

Partition and use some derived value (e.g. the conditional averages) on each of the components for the sampling. The sampling weights are determined by the probability measure of each component.

While the first choice is easier to use and more practical in high dimensional settings, the second selection confers many desirable properties which will be examined later on. First introduce the following useful concepts which will be used extensively.

Lemma 1.

Let be a sequence of real-valued convex functions on i.e. for . If the sequence converges pointwise to on a dense subset of , then the sequence converges uniformly to on all compact subsets of .

Proof.

See [18, Theorem 10.8]. ∎

Definition 2.

A sequence of convex real-valued functions on is called a CCC (convex compactly converging) sequence in if converges uniformly on all compact subsets of .

In the following two subsections, let , , and be arbitrary chosen. The sequence will be used to demonstrate the behaviour of the modified value functions under the modified transition operator. Assume forms a CCC sequence in converging to value functions for all . Note that by Assumption 2, is continuous in since we have a composition of continuous functions.

4.1. Monte Carlo sampling

The below establishes uniform convergence on compact sets under Monte Carlo sampling.

Theorem 3.

Let be idependently and identically distributed copies of and for . Assume these random variables reside on the same probability space as . If is compact, it holds that

If is also convex in for , then forms a CCC sequence in .

Proof.

From the strong law of large numbers,

holds with probability one. The summands can be expressed as

Define . The continuity of in , the uniform convergence on compact sets of to , and the compactness of gives . From Cesaro means,

with probability one and so

with probability one. Therefore,

almost surely and so the first part of the statement then follows. Now observe that the almost sure convergence in the first part of the statement holds for any choice of . There are a countable number of . A countable intersection of almost sure events is also almost sure. Therefore, converges to pointwise on a dense subset of with probability one. The second part of the statement then results from Lemma 1. ∎

The above assumes that is compact. While this compactness assumption may seem problematic for unbounded cases, one can often find a compact subset so obscenely large that it contains the vast majority of the probability mass. Therefore, from at least a numerical work perspective, the drawback from this compactness is not that practically significant especially considering computers typically have a limit on the size of the numbers they can generate and because of machine epsilon. For example, if , one can set where is orders of magnitudes greater than this size limit and is drastically smaller than the machine epsilon. With this, one can then use Monte Carlo sampling in practice as normal without restriction. The above convergence when is not compact will be addresssed in future research.

4.2. Disturbance space partition

This subsection proves the same convergence under partitioning of the disturbance space . Introduce partition and define the diameter of the partition by

if it exists. The case where is compact is considered first.

Theorem 4.

Suppose is compact and let . Choose sampling where and for . It holds that

If is also convex in for , then forms a CCC sequence in .

Proof.

Denote -point random variable

where denotes the indicator function of the set . Now

and so converges to in distribution as . Using this convergence, the fact that is compact, the fact that and are continuous in , and the fact that converges to uniformly on compact sets, it can be seen that

for and . This first part of the statement then follows easily. The second part of the theorem follows from Lemma 1. ∎

The next theorem examines the case when is not necessarily compact. In addition, conditional averages are used for the disturbance sampling and this is perhaps a more sensible choice given that it minimizes the mean square error from the discretization of . In the following, refers to the expectation of conditioned on the event . This paper sometimes refers to this as the local average.

Theorem 5.

Suppose generated sigma-algebras satisfy . Select sampling such that

with for . If is uniformly integrable for and , then:

If is also convex in for all , then forms a CCC sequence in .

Proof.

Denote random variable which takes values in the set of local averages . On the set of paths where the almost sure convergence holds by Levy’s upward theorem [21, Section 14.2], the set is bounded on each sample path since a convergent sequence is bounded and so

with probability one since there is uniform convergence on bounded sets. Using the Vitali convergence theorem [21, Section 13.7],

for . This proves the first part of the statement. The second part of the statement stems from Lemma 1. ∎

The above assumes that is uniformly integrable. This is satisfied when is compact. For not compact, Theorem 6 may be useful.

Lemma 2.

Let random variable be integrable on . The class of random variables is uniformaly integrable.

Proof.

See [21, Section 13.4]. ∎

In the following, the function is said to be convex in component-wise if each component of is convex in .

Theorem 6.

Let and be Lipschitz continuous in with Lipschitz constant . If and for either:

-

•

is Lipschitz continuous in , or

-

•

is convex in , or

-

•

is convex in component-wise,

holds, then is uniformly integrable for .

Proof.

From Lipschitz continuity,

holds for . Since converges to , it is enough to verify that is uniformly integrable to prove the above statement. Now if is Lipschitz continuous in ,

| (7) |

for some constant and . Now suppose instead that is convex in . We know from Jensen’s inequality that

| (8) |

Finally, if is convex in component-wise, Jensen’s gives

holding component-wise. From the above inequality and the fact that convex functions are bounded below by an affine linear function (e.g. tangents), the following holds component-wise for some constants and :

| (9) |

Using Lemma 2 and , Equations (7), (8) or (9) reveals that is uniformly integrable for because it is dominated by a family of uniformly integrable random variables. ∎

The above generalizes the condition used by [11] to ensure uniform integrability his approximation scheme. Before proceeding, note that can be made time dependent without affecting the convergence above.

4.3. Modified value functions

The following establishes the uniform convergence on compact sets of the resulting modified value functions under each of the disturbance sampling methods. Let and be sequences of natural numbers increasing in and , respectively.

Lemma 3.

Suppose and are CCC sequences on converging to and , respectively. Define and . Then:

-

•

is a CCC sequences on converging to ,

-

•

is a CCC sequences on converging to , and

-

•

is a CCC sequences on converging to .

Proof.

Theorem 7.

Proof.

Let us consider the limit as first and prove this via backward induction. At , Lemma 3 reveals that forms a CCC sequence in for and converges to . Now from Assumption 5, is convex in . Therefore, using Assumption 5 and either Theorem 3, Theorem 4 or Theorem 5 reveals that forms a CCC sequence in converging to . From the above and Lemma 3, we know that forms a CCC sequence in and converges to . Since is finite, Lemma 3 implies that forms a CCC sequence in and converges to for . At , it can be shown using the same logic above for and that forms a CCC sequence in and converges to . Following the same lines of argument above eventually leads to forming a CCC sequence in and that it converges to for . Proceeding inductively for gives the desired result. The proof for the case follows the same lines as above. ∎

5. Lower bounds

Observe that the convergence results presented so far does require the modified Bellman operator (5) to be a monotone operator. However, this is needed to obtain lower and upper bounding functions.

Assumption 6.

For all convex functions where for , assume for and .

The modified Bellman operator (5) is now monotone i.e. for , , , and , we have if for . This stems from the monotonicity of (4) and Assumption 6. Under the following conditions, the modified value functions constructed using the disturbance sampling in Theorem 5 leads to a non-decreasing sequence of lower bounding functions. Partition is said to refine if each component in is a subset of a component in .

Lemma 4.

Let and be convex in for all . If refines , then Theorem 5 gives

Proof.

Without loss of generality, assume the last two components of are both subsets of the last component of . With this,

Since is convex in , it holds that

because

and . Therefore, for all

and so as claimed. ∎∎

Theorem 8.

Using Theorem 5 gives for , , , and :

-

•

if is convex in and if for , , , and all convex functions .

-

•

when refines and if and are convex in for , , , and .

-

•

if for , , and all convex functions .

Proof.

The three inequalities are proven separately using backward induction.

1) Recall that for and .. From the tower property, Jensen’s inequality and the monotonicity of (4):

for all and . Therefore, which in turn implies that since . Proceeding inductively for using a similar argument as above gives the first inequality in the statement.

2) Lemma 4 gives which implies . Using the monotonicity of (4) and a similar argument as above, one can show

. Proceeding inductively for proves the desired result.

3) This can be easily proved by backward induction using the monotonicty of (4) and by the fact that and for , , , , and . ∎

It turns out that if the modified value functions are bounded above by the true value functions such as in the first case point of Theorem 8, the uniform integrability assumption in Theorem 5 holds automatically. This is proved in the next subsection.

5.1. Uniform integrability condition

Theorem 9 below differs from Theorem 6 in that Lipschitz continuity in is not assumed for the approximating functions. Instead, the value functions are assumed to bound the approximating functions from above. In the following, the sequence of functions from the previous section is reused. Recall that this sequence converges uniformly to on compact sets.

Lemma 5.

Suppose that for all , , and . For fixed and all , there exists constants such that

for and . It also holds that .

Proof.

The first part follows from the definition of a tangent for a convex function. Now note that if is not bounded for , then there exists and where

since converges to . This yields a contradiction. ∎

Theorem 9.

Suppose for , , and . Assume is convex in and let . If for either:

-

•

is Lipschitz continuous in ,

-

•

is convex in , or

-

•

is convex in component-wise,

holds, then is uniformly intergrable.

Proof.

Jensen’s inequality and gives

Now from Lemma 5, there exists constants such that for all :

for some with probability one. Using the above inequalities:

almost surely. The first term on the right forms a uniformly integrable family of random variables from Lemma 2. Since converges to , . From Lemma 5, . Now can be shown to be uniformly integrable using a similar argument as in the proof of Theorem 6. Therefore, is dominated by a family of uniformly integrable random variables and so is also uniformly integrable. ∎

6. Upper bounds

For the case where is compact, a sequence of upper bounding function approximations can also be constructed using the following setting from [9]. It is well known that a convex function continuous on a compact convex set attains its maximum at an extreme point of that set. The following performs a type of averaging of these extreme points to obtain an upper bound using Jensen’s inequality (see [3, Section 5]). Let us assume that the closures of each of the components in partition are convex and contain a finite number of extreme points. Denote the set of extreme points of the closure of each component by

where is the number of extreme points in . Suppose there exists weighting functions satisfying

for and . Suppose for and define random variables satisfying

and . To grasp the intuition for the upper bound, note that if is a convex and continuous function, then

for (see [9, Corollary 7.2]) and so

| (10) |

For the following theorem, define random variable

Recall that is a CCC sequence in for and that converges to . Also, recall is continuous in .

Lemma 6.

If the diameter of the partition vanishes i.e. , then

If, in addition, is convex in for , then the sequence of functions form a CCC sequence in .

Proof.

By construction, takes values in the extreme points of for and so

Thus, converges to in distribution as . Therefore, the proof for the above statement then follows the same lines as the proof for Theorem 4. ∎

Let us define the following alternative modified transition operator:

| (11) |

The next theorem establishes the uniform convergence on compact sets of the resulting modified value functions when the new modified transition operator (11) is used in place of the original modified transition operator (4). Recall that and are sequences of natural numbers increasing in and , respectively.

Theorem 10.

Under certain conditions, these modified expected value functions also form a non-decreasing sequence of upper bounding functions as shown below. The following gives analogous versions of Lemma 4 and Theorem 8 but for the upper bound case.

Lemma 7.

Suppose refines , that is convex in , and that for , , and . Then

for , , , and .

Theorem 11.

Using (11) gives for , , , and :

-

•

when is convex in and if for , , , and all convex functions .

-

•

if refines of and if and are convex in for , , , and .

-

•

if for , , and all possible convex functions .

Proof.

The three inequalities are proven separately using backward induction.

1) The monotonicity of (11) and Lemma 7 . Proceeding inductively for using a similar argument as above gives the desired result.

2) Lemma 7 . Therefore, . Using the monotonicity of (11) and Lemma 7, it holds that

. Proceeding inductively for proves the second part of the statement.

3) This can be proved via backward induction using the monotonicty of (11) and by the fact that and for , , , and . ∎

7. Numerical demonstration

A natural choice for is to use piecewise linear functions. A piecewise linear function can be represented by a matrix where each row or column captures the relevant information for each linear functional. This is attractive given the availability of fast linear algebra software.

7.1. Bermudan put option

Markov decision processes are common in financial markets. For example, a Bermudan put option represents the right but not the obligation to sell the underlying asset for a predetermined strike price at prespecified time points. This problem is characterized by and . At “unexercised”, applying “exercise” and “don’t exercise” leads to “exercised” and “unexercised”, respectively with probability one. If “exercised”, then = “exercised” almost surely regardless of action . Let be the time step and represent the interest rate per annum by and underlying asset price by . Defining , the reward and scrap for the option are given by

for all and zero for other and . The fair price of the option is

The option is assumed to reside in the Black-Scholes world where the asset price process follows geometric Brownian motion i.e.

where are independent standard normal random variables and vol is the volatility of stock returns. Note that the disturbance is not controlled by action and so the superscript is removed from for notational simplicity in the following subsections. The reward and scrap functions are convex and Lipschitz continuous in . It is not hard to see that under the linear state dynamic for , the resulting expected value functions and value functions are also convex, Lipschitz continuous, and decreasing in . In the following two subsections, two different schemes are used to approximate these functions.

7.2. Approximation using tangents

It is well known that a convex real valued function is differentiable almost everywhere [18, Theorem 25.5] and so can be approximated accurately on any compact set using a sufficient number of its tangents. Suppose that convex function holds tangents on each point in given by and that the approximation scheme takes the maximising tangent to form a convex piecewise linear approximation of i.e.

It is not hard to see that the resulting approximation is convex, piecewise linear, and converges to uniformly on compact sets as . It is also clear that for all . Note that while the choice of a tangent may not be unique at some set of points in , the uniform convergence on compact sets of this scheme is not affected. Assumption 5 holds for any choice of grid and disturbance sampling under the linear state dyanmics in Section 7.1. To see this, note that if is any function convex in then is also convex in for any .

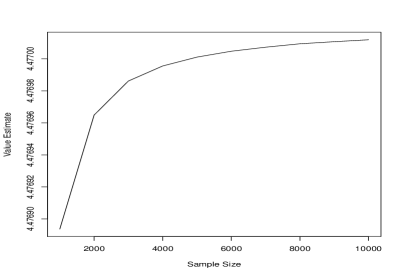

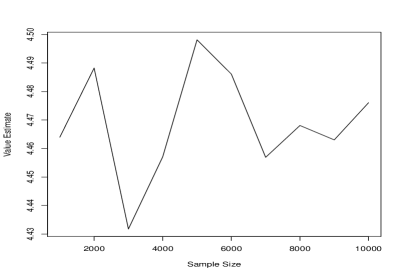

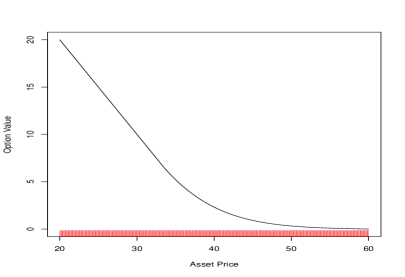

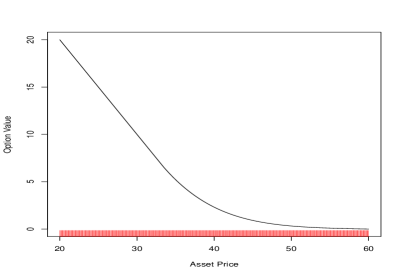

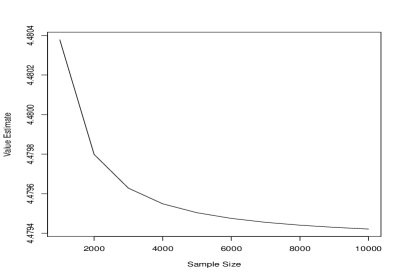

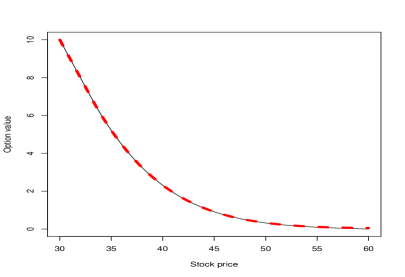

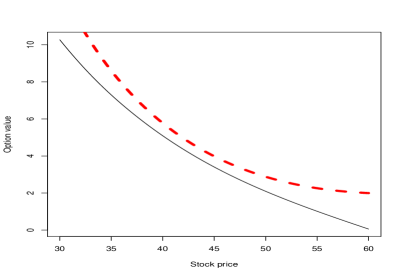

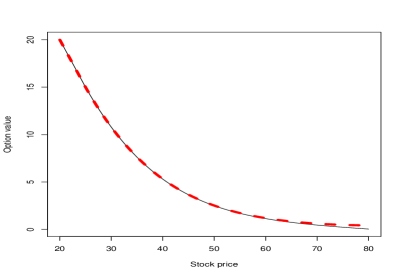

As a demonstration, a Bermudan put option is considered with strike price 40 that expires in 1 year. The put option is exercisable at 51 evenly spaced time points in the year, which includes the start and end of the year. The interest rate and the volatility is set at p.a. and p.a., respectively. Recall that there are two natural choices for the sampling . The first choice involves partitioning the disturbance space and second choice involves obtaining the disturbance sampling randomly via Monte Carlo. Using the first approach, the space is partitioned into sets of equal probability measure and then the conditional averages on each component are used for the sampling. The use of anti-thetic disturbances in Monte Carlo sampling scheme is found to lead to more balanced estimates. While it is clear that the second choice of disturbance sampling is easier to implement, the convergence seems to be slower as demonstrated by Figure 2. In Figure 2, the size of the disturbance sampling is varied from to in steps of under the two different sampling choices. The grid is given by equally spaced grid points from to . In the left plot of Figure 2, the conditions in Theorem 8 are satisfied and so the estimates give a lower bound for the true value. This lower bound increases with the size of the sampling as proved in Thereom 8. Despite the difference in convergence speeds, Figure 3 shows that the two sampling schemes return very similar option value functions for sufficently large disturbance samplings. The ticks on the horizontal axis indicate the location of grid points. The curve in the left plot gives a lower bounding function for the true value function.

7.3. Upper bound via linear interpolation

This subsection constructs upper bounding functions for the option value using the approach presented in Section 6. While the support of the distribution of is unbounded, it can be approximated by a compact set containing of the probability mass i.e. for all . To this end, introduce the truncated distribution defined by for all where is the normalizing constant. In the following results, set and use disturbance space partitions consisting of convex components of equal probability measure. Suppose that the extreme points are ordered for all . For , define points and where denotes the integer part. Defining partial expectations and using

one can determine

for .

Recall that the reward, scrap, and the true value functions are Lipschitz continuous, convex, and non-increasing in . Therefore, there exists a such that these functions are linear in when fro some . In fact, it is well known that when for and some . Let us define our approximation scheme in the following manner. Suppose is a convex function non-increasing in and when . For where and , set

where for . For , forms an approximation of via linear interpolation. It is not hard to see that for all . It is also clear that Assumption 5 will hold for any grid and disturbance sampling due to the linear dynamics of .

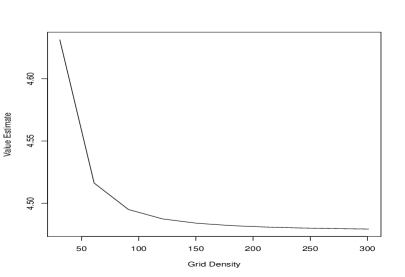

Using the same put option paramters as before and a grid with points equally spaced between and , Figure 4 examines the behaviour of the upper bound for the option with as we increase the size of the partition or the grid density . In the left plot, the size of the partition is increased for fixed . Similarly, the grid density is increased in the right plot for fixed . Observe that the bounds is decreasing in both and as proved by Theorem 10.

7.4. Accuracy and speed

Table 1 gives points on the lower and upper bounding functions for the fair price of the option at different starting asset prices and expiry dates. Columns to give an option with the 1 year expiry. A grid of equally spaced points from to is used. Columns to gives an option expiring in 2 years and is exerciseable at 101 equally spaced time points including the start. A wider grid of equally spaced points from to is used to account for the longer time horizon. For both, a disturbance partition of size is used. The other option parameters (e.g. interest rate) remain the same as before. Tighter bounding functions can be obtained by increasing the grid density or size of the disturbance sampling . This is illustrated by columns where we revisit the 1 year expiry option with equally spaced grid points from to and a disturbance partition of is used.

| Expiry 1 year | Expiry 2 years | Dense, Expiry 1 year | |||||||

|---|---|---|---|---|---|---|---|---|---|

| Lower | Upper | Gap | Lower | Upper | Gap | Lower | Upper | Gap | |

| 32 | 8.00000 | 8.00000 | 0.00000 | 8.00000 | 8.00000 | 0.00000 | 8.00000 | 8.00000 | 0e+00 |

| 34 | 6.05155 | 6.05318 | 0.00163 | 6.22898 | 6.23254 | 0.00356 | 6.05198 | 6.05201 | 2e-05 |

| 36 | 4.47689 | 4.48038 | 0.00348 | 4.83885 | 4.84435 | 0.00550 | 4.47780 | 4.47785 | 5e-05 |

| 38 | 3.24898 | 3.25347 | 0.00450 | 3.74319 | 3.74964 | 0.00645 | 3.25011 | 3.25018 | 7e-05 |

| 40 | 2.31287 | 2.31766 | 0.00479 | 2.88294 | 2.88965 | 0.00670 | 2.31405 | 2.31413 | 8e-05 |

| 42 | 1.61582 | 1.62047 | 0.00465 | 2.21077 | 2.21735 | 0.00658 | 1.61696 | 1.61704 | 8e-05 |

| 44 | 1.10874 | 1.11311 | 0.00437 | 1.68826 | 1.69456 | 0.00630 | 1.10985 | 1.10993 | 8e-05 |

| 46 | 0.74795 | 0.75217 | 0.00423 | 1.28419 | 1.29023 | 0.00604 | 0.74915 | 0.74922 | 7e-05 |

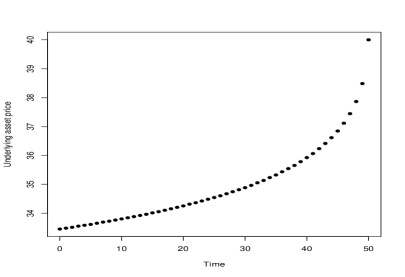

The results in Table 1 were computed using the R script provided in the appendix. On a Linux Ubuntu 16.04 machine with Intel i5-5300U CPU @2.30GHz and 16GB of RAM, it takes roughly 0.15 cpu seconds to generate each of the bounding functions represented by columns and . For expiry 2 years, it takes around 0.20 cpu seconds to generate each bounding function. For columns or , it takes around cpu seconds. Note that the numerical methods used are highly parallelizable. The code uses some multi-threaded code and the times can be reduced to between 0.03 - 0.10 real world seconds to generate columns , and each on four CPU cores. For columns and , the times are reduced to around real world seconds. Please note that faster computational times can be attained by a more strategic placement of the grid points. The reader is invited to replicate these results using the script provided in the appendix. Now given the excellent quality of the value function approximations, the optimal policy can then be obtained via (3). This is demontrated by Figure 5 where the right plot gives the optimal exercise boundary. If at any time the price of the underlying asset is below the cutoff, it is optimal to exercise the option.

For the 1 year expiry option, suppose the volatitilty is doubled to . Using the same grid and disturbance sampling from columns 2 and 3 leads to poor bounding functions as illustrated by the left plot of Figure 6. However, spreading the same number of grid points evenly between and leads to better bounds as shown by the right plot. The computational times remain the same as before. Therefore, the tightness of the bounds can be achieved by the simple modification of either the grid or disturbance sampling and their adjustments can be done independently of each other as shown in Theorem 7 and Theorem 10. This is in contrast to the popular least squares Monte carlo method where the size of the regression basis should not grow independently of the number of simulated paths [5].

8. Conclusion

This paper studies the use of a general class of convex function approximation to estimate the value functions in Markov decision processes. The key idea is that the original problem is approximated with a more tractable problem and under certain conditions, the solutions to this modified problem converge to their original counterparts. More specifically, this paper has shown that these approximations may converge uniformly to their true unknown counterparts on compact sets under different sampling schemes for the driving random variables. Exploiting further conditions leads to approximations that form either a non-decreasing sequence of lower bounding functions or a non-increasing sequence of upper bounding functions. Numerical results then demonstrate the speed and accuracy of a proposed approach involving piecewise linear functions. While the focus of this paper has been numerical work, one can in principle replace the original problem with a more analytically tractable problem and obtain the original solution by considering the limits.

The starting state for the decision problem was assumed to be known with certainity. Suppose this is not true and is distributed with distribution . Then, the value function for this case can be obtained simply via

where is obtained assuming the starting state is known. Now note that the insights presented in this paper can be adapted to problems where the functions in the Bellman recursion are not convex in . For example, it is not hard to see that they can be easily modified for minimization problems involving concave functions. That is, problems of the form

where the scrap and reward functions are concave in and the transition operator preserves concavity. To see this, note that the sum of concave functions is concave and the pointwise minimum of concave functions is also concave. Finally, the methods shown in this paper has been adapted to infinite time horizon contracting Markov decision processes in [22]. Extensions to partially obeservable Markov decision processes will be considered in future research.

Acknowledgements

The author would like to thank Juri Hinz, Onesimo Hernandez-Lerma, and Wolfgang Runggaldier for their help.

Appendix A R Script for Table 1

The script (along with the R package) used to generate columns 2, 3, and 4 in Table 1 can be found at https://github.com/YeeJeremy/ConvexPaper. To generate the others, simply modify the values on Line 6, Line 10, Line 11, and/or Line 14.

References

- [1] N. Bauerle and U. Rieder, Markov decision processes with applications to finance, Springer, Heidelberg, 2011.

- [2] J. Birge, State-of-the-art-survey–stochastic programming: Computation and applications, INFORMS Journal on Computing 9 (1997), no. 2, 111–133.

- [3] J. Birge and R. Wets, Designing approximation schemes for stochastic optimization problems, in particular for stochastic programs with recourse, pp. 54–102, Springer Berlin Heidelberg, 1986.

- [4] J. Carriere, Valuation of the early-exercise price for options using simulations and nonparametric regression, Insurance: Mathematics and Economics 19 (1996), 19–30.

- [5] P. Glasserman and B. Yu, Number of paths versus number of basis functions in american option pricing, Annals of Applied Probability 14 (2004), 2090–2119.

- [6] R. Gray and D. Neuhoff, Quantization, IEEE Trans. Inf. Theor. 44 (2006), no. 6, 2325–2383.

- [7] O. Hernandez-Lerma and J. Lasserre, Discrete-time markov control processes : Basic optimality criteria, Springer, New York, 1996.

- [8] O. Hernandez-Lerma, C. Piovesan, and W. Runggaldier, Numerical aspects of monotone approximations in convex stochastic control problems, Annals of Operations Research 56 (1995), no. 1, 135–156.

- [9] O. Hernandez-Lerma and W. Runggaldier, Monotone approximations for convex stochastic control problems, Journal of Mathematical Systems, Estimation, and Control 4 (1994), no. 1, 99–140.

- [10] K. Hinderer, Foundations of non-stationary dynamic programming with discrete time parameter, Springer-Verlag, Berlin, 1970.

- [11] J. Hinz, Optimal stochastic switching under convexity assumptions, SIAM Journal on Control and Optimization 52 (2014), no. 1, 164–188.

- [12] J. Hinz and J. Yee, Optimal forward trading and battery control under renewable electricity generation, Journal of Banking & Finance InPress (2017).

- [13] by same author, Stochastic switching for partially observable dynamics and optimal asset allocation, International Journal of Control 90 (2017), no. 3, 553–565.

- [14] F. Longstaff and E. Schwartz, Valuing American options by simulation: a simple least-squares approach, Review of Financial Studies 14 (2001), no. 1, 113–147.

- [15] G. Pages, H. Pham, and J. Printems, Optimal quantization methods and applications to numerical problems in finance, pp. 253–297, Birkhäuser Boston, 2004.

- [16] W. Powell, Approximate dynamic programming: Solving the curses of dimensionality, Wiley, Hoboken, New Jersey, 2007.

- [17] M. Puterman, Markov decision processes: Discrete stochastic dynamic programming, Wiley, New York, 1994.

- [18] R. Rockafellar, Convex analysis, Princeton landmarks in mathematics and physics, Princeton University Press, 1970.

- [19] J. Tsitsiklis and B. Van Roy, Optimal stopping of Markov processes: Hilbert space, theory, approximation algorithms, and an application to pricing high-dimensional financial derivatives, IEEE Transactions on Automatic Control 44 (1999), no. 10, 1840–1851.

- [20] by same author, Regression methods for pricing complex American-style options, IEEE Transactions on Neural Networks 12 (2001), no. 4, 694–703.

- [21] D. Williams, Probability with martingales, Cambridge mathematical textbooks, Cambridge University Press, 1991.

- [22] J. Yee, Approximate value iteration for dynamic programming under convexity, Preprint (Preprint).