A Monte Carlo method for estimating sensitivities of reflected diffusions in convex polyhedral domains

Abstract.

In this work we develop an effective Monte Carlo method for estimating sensitivities, or gradients of expectations of sufficiently smooth functionals, of a reflected diffusion in a convex polyhedral domain with respect to its defining parameters — namely, its initial condition, drift and diffusion coefficients, and directions of reflection. Our method, which falls into the class of infinitesimal perturbation analysis (IPA) methods, uses a probabilistic representation for such sensitivities as the expectation of a functional of the reflected diffusion and its associated derivative process. The latter process is the unique solution to a constrained linear stochastic differential equation with jumps whose coefficients, domain and directions of reflection are modulated by the reflected diffusion. We propose an asymptotically unbiased estimator for such sensitivities using an Euler approximation of the reflected diffusion and its associated derivative process. Proving that the Euler approximation converges is challenging because the derivative process jumps whenever the reflected diffusion hits the boundary (of the domain). A key step in the proof is establishing a continuity property of the related derivative map, which is of independent interest. We compare the performance of our IPA estimator to a standard likelihood ratio estimator (whenever the latter is applicable), and provide numerical evidence that the variance of the former is substantially smaller than that of the latter. We illustrate our method with an example of a rank-based interacting diffusion model of equity markets. Interestingly, we show that estimating certain sensitivities of the rank-based interacting diffusion model using our method for a reflected Brownian motion description of the model outperforms a finite difference method for a stochastic differential equation description of the model.

Key words and phrases:

reflected diffusion, Monte Carlo method, sensitivity analysis, infinitesimal perturbation analysis, pathwise differentiability, derivative process, derivative map, boundary jitter property, rank-based interacting diffusions, Atlas model2010 Mathematics Subject Classification:

Primary: 65C05, 65C30, 90C31. Secondary: 60G17, 60H101. Introduction

1.1. Overview

Reflected diffusions in convex polyhedral domains arise in numerous applications. For instance, they arise in the study of rank-based interacting diffusion models in mathematical finance [2, 12] and as diffusion approximations in queueing theory [6, 18, 19, 23, 24, 25]. For use in uncertainty qualification, stochastic optimization and other areas (see [1, Chapter VII] for a list of the numerous applications), it is of interest to estimate the gradient of the expectation of a functional of a reflected diffusion with respect to its defining parameters — namely, its initial condition, drift and diffusion coefficients, and directions of reflection along the boundary of its domain. (Henceforth, we simply write “sensitivities” to mean “gradients of expectations of functionals”.) The main contribution of this work is to develop a broadly applicable asymptotically unbiased estimator of a large class of sensitivities of reflected diffusions, which can be used to approximate sensitivities of reflected diffusions via a Monte Carlo method.

Our estimator is based on a probabilistic representation for sensitivities of reflected diffusions that was obtained in [15, Corollary 3.15]. This representation expresses the sensitivity as the expectation of a functional of a reflected diffusion and its associated derivative process. The derivative process satisfies a constrained linear stochastic differential equations with jumps whose coefficients, domain and directions of reflection are modulated by the reflected diffusion, and it was shown in [15, Theorem 3.13] that the pathwise derivatives of a reflected diffusion can be described via the derivative process. While this representation provides an unbiased estimator for sensitivities of a reflected diffusion, computation of sensitivities via this representation would entail simulation of the reflected diffusion and its associated derivative process, which typically involves discrete-time approximations. There is a large literature devoted to approximating reflected diffusions in convex polyhedral domains (see, e.g., [4, 5, 10, 17, 20, 21, 27, 28]); however, there is no method for approximating the derivative process. In this work we propose an Euler scheme for the approximation of a reflected diffusion and its derivative process, and prove that the associated estimators of sensitivities of the reflected diffusion are asymptotically unbiased, as the discretization parameter goes to zero. The proof that the Euler scheme for the reflected diffusion is asymptotically unbiased follows an argument analogous to the one used in the proof of [28, Theorem 3.2], which established the result in the case of normal reflection. The proof that the Euler scheme for the derivative process is asymptotically unbiased is much more challenging because the derivative process jumps whenever the reflected diffusion hits the boundary of the polyhedral domain. Establishing convergence of the approximation is quite subtle and relies on a continuity property of a certain map, called the derivative map. This continuity property is of independent interest; for example, it is used in [16] to prove that a reflected Brownian motion (RBM) in a convex polyhedral cone and its derivatives process are jointly Feller continuous.

Our method, which relies on pathwise derivatives of a reflected diffusion, falls into the class of infinitesimal perturbation analysis (IPA) methods used in sensitivity analysis (see, e.g., [1, Chapter VII.2]). We compare the performance of our IPA method to a standard likelihood ratio (LR) method and provide numerical evidence that the variance of the former is substantially smaller than that of the latter. It is also worth mentioning here that the LR method only applies to perturbations of the drift and in many applications it is of interest to study perturbations with respect to all of the parameters (e.g., when estimating sensitivities of diffusion approximations of queueing networks, which we plan to investigate in future work). We also apply our method to study a particular rank-based interacting diffusion model called the Atlas model, originally proposed by Fernholz [8, Example 5.3.3] to model equity markets, and subsequently generalized by Banner, Fernholz and Karatzas [2] and Ichiba et. al. [12]. This model is described by a stochastic differential equation (SDE) with discontinuous drift coefficients, and its sensitivities can be estimated using a standard finite difference (FD) method (although this method remains biased as the time-discretization vanishes). On the other hand, the dynamics of this model can also be expressed in terms of an RBM in a convex polyhedral domain (see, e.g., [8] and Section 5.2 below). We estimate sensitivities by applying our method to this RBM representation, and provide numerical evidence to show that it performs much better than the FD method applied to the SDE description of the model.

In summary, the main contributions of this work are as follows:

-

•

An IPA method for estimating sensitivities of a reflected diffusion (Algorithm 1).

- •

-

•

Comparison of our method with the LR method, with numerical evidence that our method performs better, especially over long time horizons (Section 4).

-

•

Application of our method to estimate certain sensitivities of the Atlas model, and numerical evidence that our method applied to the RBM representation of the model performs better than the FD method applied to an SDE description of the model (Section 5.2).

-

•

A continuity property of the derivative map (Theorem 6.15).

1.2. Outline

The remainder of this paper is organized as follows. In Section 2 we give precise definitions of a reflected diffusion and its associated derivative process, and we recall the probabilistic representation of sensitivities of reflected diffusions from [15]. In Section 3 we define an Euler approximation for a reflected diffusion and its derivative process, state our main convergence result and describe a numerical algorithm for estimating sensitivities. In Section 4 we compare our algorithm with an LR algorithm for gradient estimation in cases when the latter applies. In Section 5 we present numerical results from applying our method to a one-dimensional RBM and to the Atlas model. In Section 6, we define and state properties of the Skorokhod problem (SP) and the derivative problem, which are used to characterize a reflected diffusion and its derivative process, respectively. These are used in the proofs of our main results, which are presented in Sections 7–9.

1.3. Notation

Let denote the set of positive integers, and . Given , we use to denote the closed nonnegative orthant in -dimensional Euclidean space . When , we suppress and write for and for . For let , and . For a subset , let and denote the infimum and supremum, respectively, of , with the convention that the infimum and supremum of the empty set are respectively defined to be and . For a column vector , let denote the th component of , for , and let denote the usual Euclidean norm of . We let denote the standard normal basis in , where is the column vector in whose th component is one and whose other components are zero, for . We let denote the unit sphere in . For , let denote the set of real-valued matrices with rows and columns. We write for the transpose of a matrix . Let denote the identity matrix. Let denote the operator norm on .

Given we let denote the convex cone generated by ; that is,

and let denote the set of all possible finite linear combinations of vectors in , with the convention that and are equal to . Given or let denote the set of functions mapping to that are right-continuous with finite left limits (RCLL). Let denote the subset of continuous functions in . For a subset , let and . We endow and its subsets with the -topology and recall that the -topology relativized to coincides with the topology of uniform convergence on compact subsets of . Given and , we let denote the left limit of at . Given a function , we say that as if as , and we say that as if is bounded as .

Throughout this paper we fix a filtered probability space satisfying the usual conditions; that is, is a complete probability space, contains all -null sets in and the filtration is right-continuous. We write to denote expectation under . We abbreviate “almost surely” as “a.s.” By a -dimensional -Brownian motion on , we mean that are independent and for each , is a continuous martingale with and quadratic variation for . We let , for , denote the universal constants in the Burkholder-Davis-Gundy (BDG) inequalities (see, e.g., [26, Chapter IV, Theorem 42.1]).

2. Background on reflected diffusions and their sensitivities

2.1. A parameterized family of reflected diffusions

Let be a closed polyhedron in equal to the intersection of finitely many closed half spaces in ; that is,

| (2.1) |

for a positive integer , unit vectors and constants , for . Let . For , we let denote the th face of . For , we write to denote the (possibly empty) set of indices associated with the faces that intersect at .

Let and be an open parameter set in . For each , fix a continuously differentiable function that satisfies for all . For , will denote the (constant) direction of reflection along the face associated with the parameter . Since the direction of reflection can be renormalized, our assumption for all is without loss of generality. We let

denote the continuous differentiable function defined by for , and let denote the Jacobian of at . We refer to as the reflection matrix associated with . Fix continuously differentiable functions

For , , and will respectively be the initial condition, drift and dispersion coefficients for the reflected diffusion associated with . We refer to as the diffusion coefficient associated with . For and , we let denote the Jacobian of at , denote the Jacobian of at , denote the Jacobian of at , and similarly define and .

Definition 2.1.

Given and a -dimensional -Brownian motion on , a reflected diffusion associated with and driving Brownian motion is a -dimensional continuous -adapted process such that a.s. for all , and satisfies

| (2.2) |

where is an -dimensional continuous -adapted process such that a.s. and for every , the th component of , denoted , is nondecreasing and can only increase when lies in face ; that is,

We say that pathwise uniqueness holds if given and a -dimensional -Brownian motion on , any two reflected diffusions associated with and driving Brownian motion are indistinguishable.

Remark 2.2.

In [15, Definition 2.1] the authors define a family of reflected diffusions in which the drift and dispersion coefficients and directions of reflection are parameterized by , but the initial condition is parameterized by . In [15], this allowed for a characterization of pathwise derivatives of flows of reflected diffusions and was a convenient representation in the proofs. In contrast, here we will find it more convenient to assume that the initial condition is a continuously differentiable function on taking values in .

Remark 2.3.

Given and a reflected diffusion with satisfying the conditions in Definition 2.1, define the -dimensional -adapted constraining process by . It follows from the definition of and the conditions on in Definition 2.1 that satisfies, for all ,

| (2.3) |

where

| (2.4) |

In particular, we see that satisfies [15, Definition 2.1] for a reflected diffusion (with initial condition there). The more general condition (2.3) allows for reflected diffusions that are not semimartingles. In this work we impose a mild linear independence condition on the directions of reflection (see Assumption 2.4 below) under which satisfies Definition 2.1 if and only if satisfies [15, Definition 2.1].

Let lie in , the space of real-valued functions on that are continuously differentiable with bounded first partial derivatives. Suppose that for each there exists a unique reflected diffusion associated with . Then for , define to be the mapping from to defined by

| (2.5) |

In the next two sections we state our main assumptions, introduce the derivative process along and characterize the Jacobian of in terms of and the derivative process along .

2.2. Main assumptions

The assumptions stated in this section are assumed to hold, without restatement, throughout this work.

The first three assumptions on the data ensure the associated SP is well defined and the associated Skorokhod map (SM) is Lipschitz continuous (see Proposition 6.5 below), which is useful for proving strong existence of reflected diffusions and establishing pathwise uniqueness.

Assumption 2.4.

For each and , is a set of linearly independent vectors.

Given a convex set , let denote the set of inward normal vectors to the set at .

Assumption 2.5.

For each there exists and a compact, convex, symmetric set in with such that for ,

| (2.6) |

Recall the definition of given in (2.4).

Assumption 2.6.

For each there is a map satisfying for all and for all .

Remark 2.7.

Remark 2.8.

Along with the last three assumptions, the final two assumptions on the coefficients , and ensure existence and pathwise uniqueness of the reflected diffusion and the derivative process, as well as the characterization of sensitivities of reflected diffusions in terms of the derivative process (see Theorem 2.13 below).

Assumption 2.9.

There exists such that for all and ,

In addition, there exist and such that for all and ,

Assumption 2.10.

For each there exists such that for all ,

| (2.7) |

2.3. Sensitivities of reflected diffusions in terms of the derivative process

We first define the derivative process, which was introduced in [15, Definition 3.5] to characterize pathwise derivatives of a reflected diffusion. Given , define

| (2.8) |

Recall the definition of in (2.4).

Definition 2.11.

Let , be a -dimensional -Brownian motion on and be a reflected diffusion associated with and driving Brownian motion . A derivative process along is an RCLL -adapted process taking values in such that a.s. for all , for and satisfies

| (2.9) | ||||

where is an RCLL -adapted process taking values in such that a.s. and for each and all ,

| (2.10) |

We say that pathwise uniqueness holds if for each , -dimensional -Brownian motion and reflected diffusion associated with with driving Brownian motion , any two derivative processes along are indistinguishable.

The equation 2.9 for the derivative process can be viewed as a linearized version of the equation (2.2) for the reflected diffusion , with the key feature, established in [15], that serves as the appropriate linearization of the constraining process .

Remark 2.12.

Definition 2.11 for the derivative process is slightly different from the definition given in [15, Definition 3.5] due to the fact that the initial condition here is a function of . To clarify the relation, suppose satisfies Definition 2.11 and satisfies [15, Definition 3.5]. Then, for , the th column vector of satisfies for all (where the right-hand side of the equality is written in the notation of [15]).

In the following theorem we state the probabilistic representation of sensitivities of reflected diffusions that was obtained in [15] and serves as the starting point for the method for sensitivity estimation that we introduce in this work. Recall that the assumptions stated in Section 2.2 hold.

Theorem 2.13.

For each and -dimensional -Brownian motion on , the following hold:

-

(i)

There exists a pathwise unique reflected diffusion associated with and driving Brownian motion , and it is a strong Markov process.

-

(ii)

There exists a pathwise unique derivative process along .

-

(iii)

Given , a.s. is continuous at , and a.s. is continuous at almost every .

-

(iv)

Given , the function defined in (2.5) is differentiable at and its Jacobian satisfies

(2.11)

Proof of Theorem 2.13.

Part (i) follows from [15, Proposition 2.16] (see also, [22, Theorem 4.3]) and the equivalence between solutions of Definition 2.1 and [15, Definition 2.1] stated in Remark 2.3. Parts (ii) and (iii) follow from [15, Corollary 3.15] and Remark 2.12. Part (iv) follows from [15, Corollary 3.16] and the chain rule. ∎

While (2.11) provides an unbiased estimator for , exact sampling of functionals of is complicated by the discontinuous dynamics when reaches the boundary . As is often the case when simulating diffusion processes, we sample from a discrete-time Euler approximation of . Our main result (see Corollary 3.7 below) states that the Euler approximation can be used to construct an asymptotically unbiased estimator for .

3. Main results

Recall that the assumptions stated in Section 2.2 hold. Fix and a -dimensional -Brownian motion on . Let denote the pathwise unique reflected diffusion associated with and driving Brownian motion , and let denote the pathwise unique derivative process along . Throughout this section, given a time step , define the sequence by

| (3.1) |

and let be the sequence of i.i.d. -dimensional Gaussian random variables with mean zero and diagonal covariance matrix given by

| (3.2) |

In addition, let denote the discrete filtration defined by

| (3.3) |

3.1. Euler scheme for the reflected diffusion

In this section we present an Euler scheme for approximating just the reflected diffusion . This is an extension of a result obtained in [28] to allow for reflected diffusions with oblique reflection. We also prove a convergence result for an Euler approximation of the process that will be needed in the next section. Let denote the unique mapping satisfying the conditions in Assumption 2.6. In order to define the Euler scheme, we need the following lemma.

Lemma 3.1.

There exists a unique map such that for each , and the th component of satisfies only if , for .

Remark 3.2.

In the case of a simple polyhedral cone with vertex at the origin (i.e., and for ), Assumption 2.9 implies is invertible for each and so for each and .

Proof.

For let denote the pair of piecewise constant RCLL -adapted processes taking values in defined as follows: Set

| (3.4) |

and, for , set

| (3.5) |

and recursively define

| (3.6) |

where is the random -dimensional vector defined by

| (3.7) |

We have the following result on the convergence of the Euler approximations.

Theorem 3.3.

For each , as ,

| (3.8) | ||||

| (3.9) |

The proof of Theorem 3.3 is given in Section 7. The proof is a straightforward adaptation of the proof of [28, Theorem 3.2(i)], which proves (3.8) in the case of normal reflection along the boundary. The main difference between the two results is that we allow for oblique reflection along the boundary and also prove convergence of the constraining process in (3.9).

3.2. Euler scheme for the derivative process

We now construct an Euler scheme for the derivative process. We start with a lemma that introduces a linear projection map that can be interpreted as a linearization of . Recall the definition of the linear subspace , for , given in (2.8).

Lemma 3.4.

For each , there is a unique map that satisfies for all . Furthermore, is linear.

Proof.

Remark 3.5.

For each , since is a linear map from to , we can write as a matrix whose column vectors lie in . Throughout this work we view as this matrix and refer to as the derivative projection matrix.

For recall the sequence , the random vectors , , the discrete filtration and the pair of processes defined in the last section. Let denote the piecewise constant RCLL -adapted process taking values in defined as follows: Set

| (3.10) |

and, for , set

| (3.11) |

and recursively define

| (3.12) |

where is the random element taking values in defined by

| (3.13) | ||||

The following establishes convergence of the Euler scheme for the derivative process.

Theorem 3.6.

A.s. converges to in as . In addition, given any , the family is a uniformly integrable family of random variables.

The proof of Theorem 3.6, which is given in Section 8, relies on continuity properties of the related derivative map, which are established in Theorem 6.15.

Corollary 3.7.

For all ,

| (3.14) |

Corollary 3.7 suggests an asymptotically unbiased estimator for . In the next section we describe an algorithm for estimating based on the Euler discretization. It is also of interest to investigate whether there is an exact sampling algorithm for the joint process , which would avoid the bias introduced by the Euler discretization. Even in the setting of an RBM, where an exact sampling method has been proposed in [4] for RBMs in the nonnegative orthant with reflection matrices that are so-called -matrices, it is a challenging problem to exactly sample the associated derivative process due to the fact that the derivative process jumps whenever the RBM reaches the boundary of the domain. We leave this as an interesting open problem for future work.

3.3. Numerical algorithm

Fix . Since is typically much smaller than , for simplicity we can assume is a positive integer. Since and are constant on intervals of the form , , we have

| (3.15) | ||||

Algorithm 1.

In the next section we compare our algorithm with other methods for sensitivity analysis. In Section 5 below, we illustrate our algorithm with an example of a one-dimensional RBM and an example of an RBM that arises in the study of a rank-based interacting diffusion model of equity markets.

4. Comparison with existing methods

The main existing (asymptotically unbiased) estimator for estimating sensitivities of reflected diffusions is the LR method. The LR method is applicable only when the law of the perturbed process is absolutely continuous with the law of the original process. In the context of multidimensional (reflected) diffusions, this only holds for perturbations to the drift. In this case, the LR method uses a change of measure argument to recast expectations of functionals of the perturbed process as the expectation, under the law of the original process, of the functional multiplied by the likelihood ratio or the Radon-Nikodym derivative. The LR method for sensitivities of diffusions with respect to drift was introduced in [32] and the authors describe an extension of their method to reflected diffusions (see [32, Section 9]). Here we provide a brief summary of the method in the context of reflected diffusions in convex polyhedral domains and refer the reader to [32] for the details.

Since we can only consider perturbations to the drift in this section, in addition to the assumptions stated in Section 2.2, we also assume that the initial condition, dispersion coefficient and directions of reflection are constant in ; that is, , and . Fix and . For , by a standard argument using the Lipschitz continuity of and Girsanov’s transformation (see, e.g., [26, Chapter IV.38]), there is a family of probability measures on the measurable space that are mutually absolutely continuous with respect to the underlying measure with Radon-Nikodym derivative

| (4.1) |

where is given by

such that under is equal in distribution to under . Let denote the -dimensional random variable whose th component, denoted for , is defined by

where denotes the partial derivative of at with respect to the th component of . According to [32, Theorem 3.1],

As described in Section 3.1, we have an Euler approximation for , which yields the approximation for , for , given by

| (4.2) |

According to [32, Theorem 4.1],

| (4.3) |

We now propose a numerical algorithm for estimating based on (4.2) and (4.3). Fix so that is a positive integer. Then we have

| (4.4) |

Algorithm 2.

We briefly mention some of the advantages and drawbacks of the LR method. When applicable, the main advantage of the LR method is that it applies to a broad class of functionals of reflected diffusions, requiring only that and be measurable (and integrable) without imposing additional smoothness conditions that are required for our IPA method (Algorithm 1). In addition, since there are exact sampling methods for reflected diffusions (see [4]), they can potentially be adopted to obtain an unbiased estimator of . On the other hand, as mentioned above, the main drawback of the LR method is that it is only applicable to perturbations of the drift. This is quite restrictive as it is often of interest to compute sensitivities with respect to parameters other than the drift (e.g., in diffusion approximations of queueing networks, which we plan to study in future work). In [32, Section 8] the authors show that in the one-dimensional setting, the approach can be adapted to allow for perturbations of the diffusion coefficient, but those methods do not extend to higher dimensions. Furthermore, even when considering perturbations to the drift, numerical evidence suggests that the variance of an LR estimator performs worse than the our method, especially over large time intervals (see Figure 2 below). This supports the observation made in [1, Chapter VII.5] that IPA estimators usually outperform LR estimators when both methods are applicable.

Remark 4.1.

It is worthwhile to compare our IPA algorithm with the class of FD methods, which can be used to estimate sensitivities. These are based on approximating the derivative by a finite difference and include forward, backward and central difference approximations (see, e.g., [1, Chapter VII.1]). For example, the forward difference estimator associated with fixed (and assuming once again that is a positive integer) for , for , is given by

| (4.5) | ||||

with defined as in (3.1). The appeal of an FD method is that it is simple to implement and can be used to approximate sensitivities with respect to all of the parameters. The main drawback is that it introduces an extra source of bias from the derivative approximation. Our IPA method can be viewed as a limiting version of the FD method that eliminates the bias from the derivative approximation, without any increase in the computational complexity of implementation. Since there is no computational advantage to using the FD method and in general there do not appear to be any other advantages to using an FD method over an IPA method when both are applicable (see, e.g., the first paragraph at the the top of [1, page 219]), we do not provide a numerical comparison of our method and an FD method.

5. Examples

We illustrate the value of our method (Algorithm 1) with two examples: a one-dimensional RBM and a three-dimensional RBM that arises in the study of rank-based interacting diffusion models of equity markets. We used the program R for all computations, which were performed on an Apple machine with a 2.26 GHz Intel Core 2 Duo processor.

5.1. One-dimensional RBM

Let , and be a one-dimensional -Brownian motion on . For each , let be a one-dimensional RBM in with initial condition , constant drift and variance , and driving Brownian motion . It is well known (see, e.g., [1, Chapter X.8]) that satisfies

where is given by

It is readily verified that the assumptions in Section 2.2 hold. For , define by

| (5.1) |

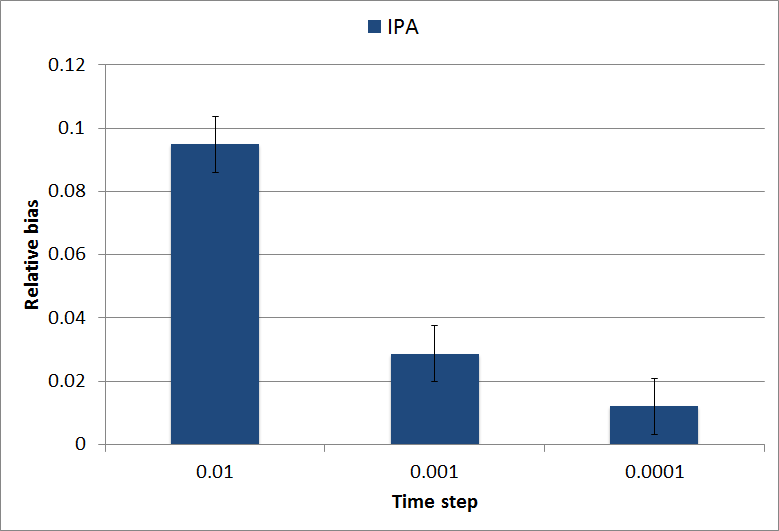

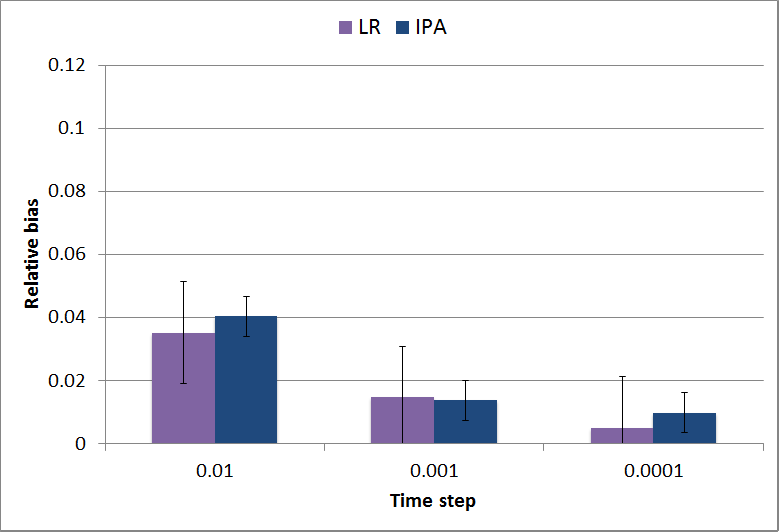

We use our algorithm (Algorithm 1) to estimate the first partial derivatives , and . In the case of , we compare our method IPA with the LR method. In Table 1 we compare the estimates with the analytic values obtained using the formula for the cumulative distribution function of a one-dimensional RBM given on [11, page 49], and, in the case of perturbations to the drift, with the estimates obtained using the LR method (Algorithm 2). In Figure 1 we plot confidence intervals for the magnitude of the relative biases of the LR estimator and our IPA estimator for different time steps , which, as expected, decrease with . (The “relative bias” of an estimator is equal to the difference between the mean of the estimator and the analytic value divided by the magnitude of the analytic value.) In Figure 2 we compare the empirical variance of our estimator of with the empirical variance of the LR estimator of over the time interval . Our estimator performs substantially better than the LR estimator, especially as increases.

| Method |

| Analytic | N/A |

| LR | N/A | N/A | ||

| IPA |

| LR | N/A | N/A | ||

| IPA |

| LR | N/A | N/A | ||

| IPA | . |

5.2. Rank-based interacting diffusion model of equity markets

We consider a rank-based interacting diffusion model, referred to as the Atlas model, which was first introduced by Fernholz in [8, Example 5.3.3] to study equity markets, and subsequently generalized by Banner, Fernholz and Karatzas [2] and Ichiba et. al. [12]. In the usual model of an equity market, the growth and volatility of each stock are fixed and depend on the identity of the stock, whereas in the class of Atlas models, the growth and volatility of each stock are determined by its relative rank within the market and thus are time-varying (and discontinuous). We consider the simplest version of the Atlas model (with stocks) in which the stocks have equal volatility, and the smallest stock, referred to as the Atlas stock, has positive growth rate, whereas all other stocks have zero growth. More precisely, let , and be a -dimensional Brownian motion. Let denote the -dimensional process whose th component at time , denoted , is equal to the value of the th stock at time . Then evolves according to the stochastic differential equation (with discontinuous drift)

| (5.2) |

where is equal to if for all and equal to zero otherwise, for . Weak existence and uniqueness of solutions to (5.2) follows from their relation to martingale problems, and existence and uniqueness results for martingale problems established in Stroock and Varadhan [29] and Bass and Pardoux [3]. Let be the rank-ordered process, where is obtained by permuting the components of (the logarithm is applied componentwise) so that they are in descending order, for . Then according to [2] (see the paragraph following the proof of Proposition 2.3 on page 2303) is a -dimensional RBM in the Weyl chamber with drift vector , diagonal covariance matrix , and normal reflection along each of the faces , for .

In many applications in mathematical finance, it is of interest to compute sensitivities of functionals of the stocks in a market with respect to the underlying parameters of the market. For example, sensitivities of derivative prices with respect to the underlying market parameters, commonly referred to as the “Greeks”, play an important role in risk management and hedging strategies (see, e.g., [9, Chapter 7]). Here, we study sensitivities related to the Atlas model, which have not yet received much attention. A performance measure of interest in this context is the so-called diversity of the equity market, which is expressed in terms of the -dimensional process of relative market capitalizations defined by for , where is defined by

| (5.3) |

Fix and define by

| (5.4) |

Then is the th power of the diversity function and is a measure of the diversity of the market (see [8, Example 3.4.4]). Since is invariant under permutations of the components of and is obtained by permuting the components of , it follows from (5.3) and (9.56) that , where is the continuously differentiable function defined by

A straightforward computation shows that the gradient of is bounded and continuous. Here, we first use a FD method based on the stochastic differential equation representation (5.2) and then our IPA method for the reflected diffusion representation to estimate the sensitivity of to an underlying parameter of the market.

Fix and set . For each set the growth rate to be , let be the -dimensional process satisfying (5.2) with , let be the process of relative market capitalizations defined by for and define

Let and . Assuming that is differentiable, it follows that, as ,

In [31] Yan proposed an Euler scheme for approximating solutions to stochastic differential equations with discontinuous drift and proved convergence properties of the Euler scheme. Using the algorithm described in [31, Section 4] one can obtain estimators and (using “common random numbers”, see [1, Chapter VII.1]) for and , respectively, and use the (forward-difference) approximation

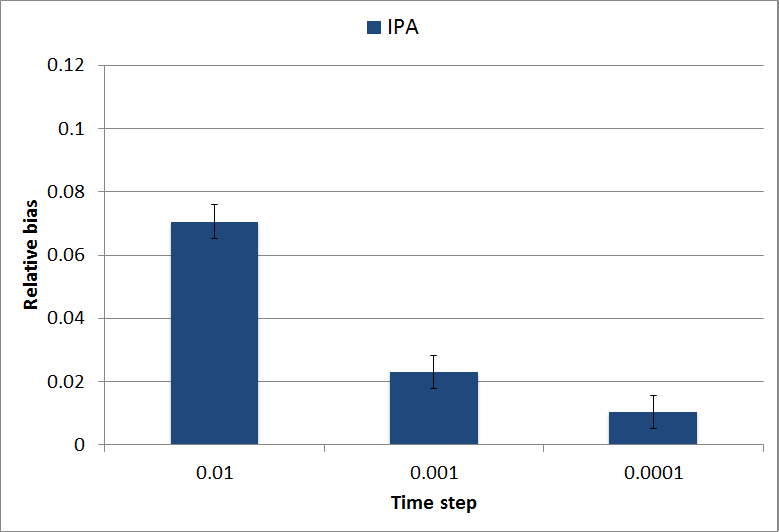

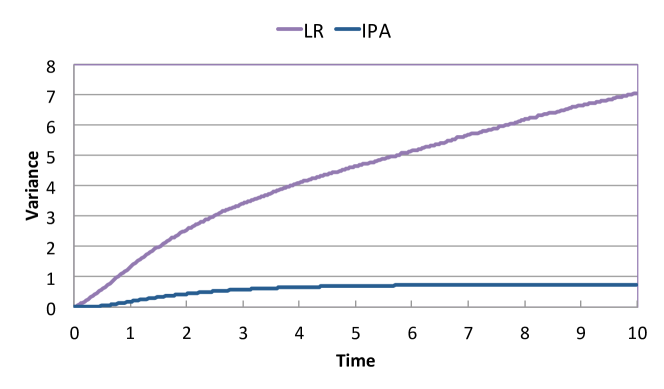

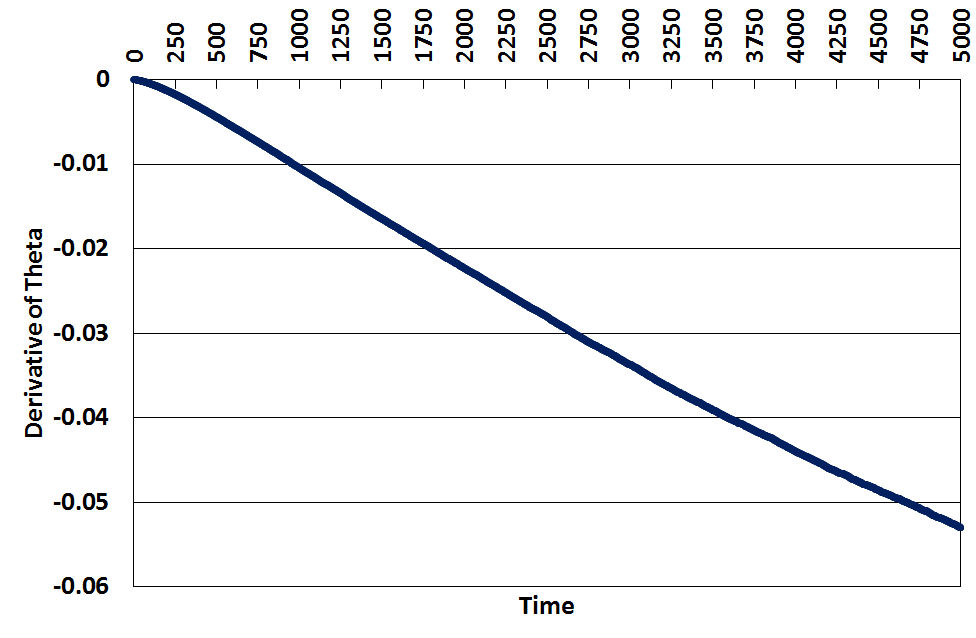

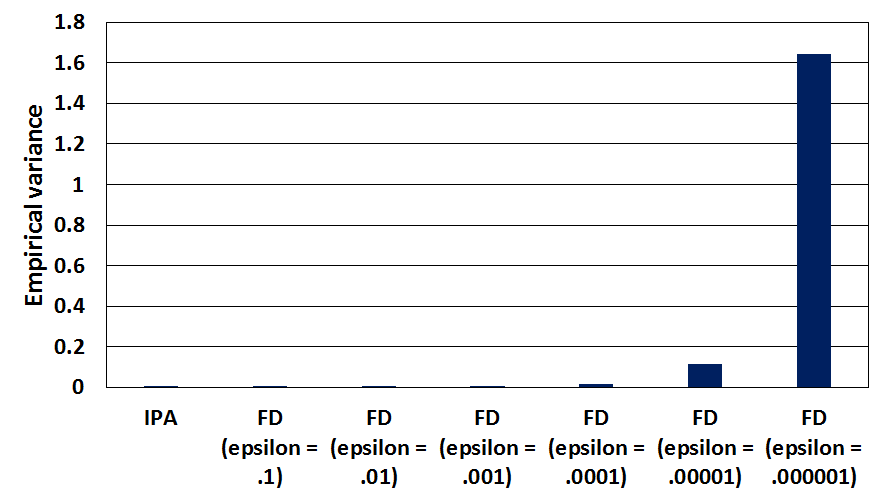

Alternatively, let denote the associated rank-ordered process so that . Then we can use our method to estimate . Let , , and . In Figure 3, we plot estimates of over the time interval obtained using Algorithm 1. In Figure 4 we plot the empirical variance of our IPA estimator (Algorithm 1) and the FD estimator (described in [31]) for . As seen in Figure 4, the empirical variance of the FD estimators appears to diverge as goes to zero.

6. The Skorokhod problem and the derivative problem

In this section we recall the deterministic SP, extended Skorokhod problem (ESP) and derivative problem. We state some useful properties and also state a new continuity result for the derivative problem (see Theorem 6.15 below) that is needed in the proof of Theorem 3.6 and whose proof is deferred to Section 9. Throughout this section we fix . Recall that Assumptions 2.4, 2.5 and 2.6 hold.

6.1. The Skorokhod problem and extended Skorokhod problem

Definition 6.1.

Given , a pair is a solution to the SP for if

where and for each , the th component of , denoted , is nondecreasing and can only increase when lies in face ; that is,

If there exists a unique solution to the SP for , we write and refer to as the associated SM.

In the following we state the ESP, which is an extension of the SP that allows for a constraining term with unbounded variation. We introduce the ESP formulation because it will be more convenient to work with in subsequent proofs.

Definition 6.2.

Given , a pair is a solution to the ESP for if and the following conditions hold:

-

1.

for all ;

-

2.

for all ;

-

3.

for all ,

-

4.

for all , .

If there exists a unique solution to the ESP for , we write and refer to as the associated ESM.

Remark 6.3.

Given a reflected diffusion with satisfying the conditions in Definition 2.1 define the -adapted -dimensional continuous process by

| (6.1) |

Then by the properties of stated in Definition 2.1, is a solution to the SP for . Define the constraining process by . Then by the properties of stated in Remark 2.3, is a solution to the ESP for .

The following is a time-shift property to the ESP. A similar property holds for the SP; however, it is not needed in this work.

Lemma 6.4 ([22, Lemma 2.3]).

Suppose is a solution to the ESP for . Let and define , and by

| (6.2) |

Then is a solution to the ESP for .

The following proposition ensures the SP and ESP are well defined and the associated SM and ESM are Lipschitz continuous.

Proposition 6.5.

Let .

-

(i)

There exists such that if, for , and is the solution to the SP for , then for all ,

(6.3) -

(ii)

There exists such that if, for , and is the solution to the ESP for , then for all ,

(6.4) -

(iii)

Given there exists a unique solution to the SP for .

-

(iv)

Given , there exists a unique solution to the ESP for .

Proof.

We close this section by stating a version of the boundary jitter property that was introduced in [14, Definition 3.1]. The boundary jitter property will be important for establishing continuity properties of the so-called derivative map.

Definition 6.6.

A pair satisfies the boundary jitter property if the following hold:

-

1.

If for some , then is nonconstant on .

-

2.’

does not spend positive Lebesgue time in the boundary ; that is,

-

3.

If for some , then for each and all there exists such that .

-

4.

If , then for each and all , there exists such that .

Remark 6.7.

Condition 2’ of the boundary jitter property is slightly stronger than condition 2 of [15, Definition 3.1], which only requires that does not spend positive Lebesgue time in the nonsmooth part of the boundary (i.e., where two or more faces intersect). The stronger version of condition 2 stated in Definition 6.6 is used in the proof of Theorem 6.15 below.

For the following, given and the associated reflected diffusion , let denote the constraining process introduced in Remark 2.3.

Proposition 6.8.

Let . Then a.s. satisfies the boundary jitter property.

6.2. The derivative problem

The derivative problem was first introduced in [14] as an axiomatic framework for studying directional derivatives of the ESM. The formulation of the derivative problem can be thought of as a linearization to the ESP (note the similarities between Definition 6.2 and Definition 6.9).

Definition 6.9.

Given , suppose is a solution to the ESP for . Let . Then is a solution to the derivative problem along for if and the following conditions hold:

-

1.

for all ;

-

2.

for all ;

-

3.

for all ,

-

4.

for all , .

If there exists a unique solution to the derivative problem along for , we write and refer to as the derivative map associated with .

Remark 6.10.

Remark 6.11.

Given a derivative process along a reflected diffusion , define the continuous -adapted process taking values in , for , by

| (6.5) | ||||

For each , it follows from the properties of stated in Definition 2.11 that a.s. is a solution to the derivative problem along for . In other words, a.s. .

In the following we state some important properties of the derivative problem and its associated derivative map. The first lemma states a time-shift property of the derivative problem.

Lemma 6.12.

Let be a solution to the ESP for . Suppose is a solution to the derivative problem along for . Let and define as in (6.2), and define by

| (6.6) |

Then is a solution to the derivative problem along for .

Proof.

This was shown for in [14, Lemma 5.2]. A similar argument can be used to prove the lemma in the case that . The only difference is that condition 4 must also be verified. To see that condition 4 holds, fix and let . By the definition of , condition 4 to the DP and the definition of ,

This proves condition 4 of the DP holds. ∎

Proposition 6.13.

Let . There exists such that if is the solution to the ESP for , and, for , is a solution to the derivative problem along for , then for all ,

| (6.7) |

Proof.

When , the proposition follows from [14, Theorem 5.4]. When is not continuous, the proof follows exactly analogously to the proof of [14, Theorem 5.4] except that [14, equation (3.5)] does not follow from condition 3 of the derivative problem, but rather is due to condition 4 of the derivative problem. ∎

For the following, let denote the nonsmooth part of the boundary; that is,

| (6.8) |

Proposition 6.14.

Let . Given suppose the solution to the ESP for satisfies the boundary jitter property (Definition 6.6). Then given there exists a unique solution to the derivative problem along for . Furthermore, is continuous at times that .

Proof.

We close this section with the following continuity property of the derivative map that will be instrumental in the proof of our main result. In addition to its use in this work, it is also used in [16] to show that the joint reflected diffusion and derivative process is Feller continuous. In contrast to the other results in this section, we explicitly state exactly which assumptions are required for the following theorem. Recall that we have equipped with the Skorokhod -topology.

Theorem 6.15.

Suppose Assumptions 2.5 and 2.6 hold. Given suppose the solution to the ESP for satisfies the boundary jitter property (Definition 6.6). Let be a sequence in such that converges to in as and for each , let denote the solution to the ESP for . Suppose satisfies and is a sequence in such that converges to in as . Then converges to in as .

7. Convergence of the Euler scheme for reflected diffusions

For recall the sequence in defined in (3.1), define the RCLL step function by

| (7.1) |

recall the definition of the discrete filtration given in (3.3), and define the piecewise constant RCLL -adapted process on by

| (7.2) |

Observe that and are constant on the interval for each and

| (7.3) | ||||

| (7.4) |

for each , where is defined as in (3.2). Recall the piecewise constant RCLL -adapted processes taking values in defined in (3.4)–(3.7). By (3.4)–(3.7) and (3.1), we have, for each ,

where the third equality uses the fact that, by Lemma 3.1, for each . Since , , and are constant on intervals of the form for , it follows from (3.4), (7.3), (7.4) and the last display that, for all ,

| (7.5) |

In addition, by (3.4)–(3.6) and Lemma 3.1, we see that a.s. and for each , the th component of is nondecreasing and can only increase when lies in .

Remark 7.1.

Define the -dimensional piecewise constant RCLL -adapted process by

| (7.6) |

Then by the properties of stated above and Definition 6.1, we see that is a solution to the SP for .

We now prove the convergence of the Euler scheme for the reflected diffusion. The argument is analogous to the one given in [28] for reflected diffusions in convex polyhedral domains with normal reflection. Given a function and , define

| (7.7) |

Lemma 7.2 ([28, Lemma A.4]).

For each , and ,

Proposition 7.3.

For each , and ,

Proof.

Fix and . The proof is analogous to the proof of [28, Theorem 3.2], which assumes normal reflection along the boundary. In particular, following [28, equations (3.3)–(3.4)], there exists a constant such that, for all ,

| (7.8) |

Due to the facts that and by Remarks 6.3 and 7.1, and the Lipschitz continuity of the SM shown in Proposition 6.5(i), we have, for ,

Substituting the last inequality into the integrand on the right hand side of (7.8) and applying Gronwall’s inequality yields

which completes the proof of the lemma. ∎

8. Convergence of the Euler scheme for the derivative process

For recall the sequence in defined in (3.1), the RCLL step function defined in (7.1), the discrete filtration defined in (3.3), the piecewise constant RCLL -adapted process defined in (7.2), the piecewise constant RCLL -adapted processes taking values in defined in (3.4)–(3.7), and the piecewise constant RCLL -adapted process taking values in defined in (3.10)–(3.12).

8.1. Relation between the discretized derivative process and the derivative map

Recall the definition of given in (2.8) for . Suppose for some . Then, for all and sufficiently small so that , we have

where the final inequality is due to the fact that takes values in . Since the last display holds for all , by considering limits as from the left and right, this implies that the column vectors of take values in . In particular, it follows that given , the column vectors of take values in . Thus, by (3.1), (3.10) and (3.4),

| (8.1) |

Here denotes the th column vector of . By (3.10)–(3.13) and (3.4), we have, for each ,

| (8.2) |

and

| (8.3) | ||||

where is the piecewise constant RCLL -adapted process taking values in defined by and, for each , for all and

| (8.4) |

Since , , , , and are constant on intervals fo the form for , it follows from (8.1), (8.2), (8.3), (3.10), (7.1) and (7.2) that, for all ,

| (8.5) |

and

| (8.6) | ||||

By (8.4) and Lemma 3.4, we see that for each and ,

Here denotes the th column vector of the matrix . Since and are piecewise constant, it follows that, for all and

| (8.7) |

and for all and ,

| (8.8) |

8.2. Proof of Theorem 3.6

In preparation for proving Theorem 3.6, we first state some preliminary results.

Lemma 8.2.

Given , and there exists such that for all ,

| (8.11) |

Proof.

Fix , and . The fact that

| (8.12) |

follows from a standard argument using (7.6), Hölder’s inequality, the BDG inequalities, Tonelli’s theorem, Assumption 2.9, the facts thats by Remark 7.1 and where , the Lipschitz continuity of the SM (Proposition 6.5(i)) and Gronwall’s inequality. Then, using the fact that is the solution to the SP for by Remark 7.1, the fact that is the solution to the SP for , (8.12) and the Lipschitz continuity of the SM, we obtain (8.11). ∎

Lemma 8.3.

For each , and , there exists such that for all ,

| (8.13) |

Proof.

Fix , and . Let . For brevity, let . By (8.9), Hölder’s inequality, the BDG inequalities, Tonelli’s theorem and bounds on the coefficients stated in Assumption 2.9,

By (8.10), the Lipschitz continuity of the derivative map (Proposition 6.13), and Lemma 8.2, we have

An application of Gronwall’s inequality yields (8.13) with

∎

Proposition 8.4.

For each , and ,

| (8.14) |

We first show how Theorem 3.6 and Corollary 3.7 can be deduced from Proposition 8.4. The proof of Proposition 8.4 is given in Section 8.4, with preliminary results established in Section 8.3.

Proof of Theorem 3.6.

Let . By Theorem 3.3 and Proposition 8.4, a.s. converges to uniformly on compact time intervals as . By Proposition 6.8, a.s. satisfies the boundary jitter property. Then by the facts that and for , and the continuity of the derivative map shown in Theorem 6.15, a.s. converges to in the -topology as . Since this holds for each , the proof is complete. ∎

Proof of Corollary 3.7.

By part (iii) of Theorem 2.13, Proposition 6.8, condition 2’ of the boundary jitter property and [15, Lemma 4.13], a.s. is continuous at and at almost every . Thus, by Theorem 3.6, a.s. converges to at and at almost every . Along with the uniform integrability of stated in Theorem 3.6, this implies that (3.14) holds. ∎

The remainder of this section is devoted to the proof Proposition 8.4.

8.3. Some useful lemmas

Recall the derivative processes introduced in Definition 2.11 and the associated process introduced in Remark 6.11. We first recall a basic estimate.

Lemma 8.5 ([15, Lemma 5.7]).

For each , and ,

We now prove an estimate that relates the derivative map along the reflected diffusion with the derivative map along the Euler discretization of the reflected diffusion.

Lemma 8.6.

For each , , and ,

| (8.15) |

Proof.

Fix , , and . Recall the constraining process introduced in Remark 2.3 and the process defined in (6.1). By Remark 6.3 and Proposition 6.8, a.s.

-

(a)

is the solution to the ESP for , and

-

(b)

satisfies the boundary jitter property.

For , recall the process defined in (7.6). Then by Remark 7.1 and Proposition 7.3, a.s.

-

(c)

, and

-

(d)

converges to in as .

Since (a)–(d) hold a.s., it follows from Theorem 6.15 that a.s. converges to in as . Thus, a.s.

| (8.16) |

By the Lipschitz continuity of the derivative map (Proposition 6.13),

Therefore, by Lemma 8.5, the dominated convergence theorem and (8.16), (8.15) holds. ∎

8.4. Proof of Proposition 8.4

Fix . For brevity, throughout this section we let

where and denote the constants in Assumption 2.9, denotes the constant in Proposition 6.5 and denotes the constant in Proposition 6.13.

Proof of Proposition 8.4.

Let and . By (8.9) and (6.5), for each ,

| (8.17) | ||||

| (8.18) | ||||

| (8.19) | ||||

| (8.20) | ||||

| (8.21) | ||||

| (8.22) | ||||

| (8.23) | ||||

| (8.24) | ||||

| (8.25) | ||||

| (8.26) | ||||

| (8.27) | ||||

| (8.28) |

We treat each of the eleven terms on the right-hand side of the last display separately.

(8.18): Since and are constant on intervals of form for , it follows that for ,

Therefore, by Assumption 2.9 and the fact that ,

| (8.29) |

(8.20): Since and are constant on intervals of form for , it follows that for ,

Therefore, using Hölder’s inequality and Assumption 2.9,

| (8.31) | ||||

(8.23): Since and are constant on intervals of form for , it follows that for ,

Therefore, by Assumption 2.9, (7.7) and the fact that ,

| (8.34) | ||||

(8.25): Since , and are constant on intervals of form for , it follows that for ,

Therefore, by Assumption 2.9, the Cauchy-Schwarz inequality, (7.7) and the fact that ,

| (8.36) | ||||

(8.28): By Assumption 2.9, the facts that solves the SP for and solves the SP for and the Lipschitz continuity of the SM (Proposition 6.5(i)),

| (8.39) |

Before combining the terms, we observe that because and for each , it follows from the Lipschitz continuity of the derivative map that

Thus,

| (8.40) | ||||

Now combining (8.17)–(8.40) and applying Gronwall’s inequality, we obtain

where

By Lemma 8.3, Lemma 7.2, Theorem 3.3, Proposition 7.3 and Lemma 8.6, as , thus completing the proof. ∎

9. Continuity of the derivative map

Throughout this section we fix . For brevity, we drop the notation and write , and for , and , respectively.

9.1. Proof of Theorem 6.15

In this section we first prove Theorem 6.15 when for all and lies in a class of simple functions (see Lemma 9.2 below). With that in mind, let denote the set of simple functions in ; that is,

For let

denote the times in that lies in the boundary , and for let

denote the jump or discontinuity points of in . Recall the definition of , , given in (2.8). For , define

| (9.1) |

Lemma 9.1.

Given , suppose has zero Lebesgue measure. Then for with , there is a sequence in such that converges to uniformly on compact intervals as .

Proof.

Fix with . Let and be arbitrary. It suffices to show that there exists such that . Since is dense in under the topology of uniform convergence on compact intervals (see, e.g., [30, Theorem 6.2.2]), we can choose such that and . By the definition of and the fact that , there exist , and such that and

Without loss of generality, we can assume . Since is uniformly continuous on , we can choose sufficiently small so that , for each , and

Set . For each , let , which is nonempty because has zero Lebesgue measure. Define by

Then . Let and be such that . Then there exists such that and so and

Since was arbitrary, this completes the proof. ∎

We now state a key convergence lemma, Lemma 9.2, and show how it, together with Lemma 9.1, can be used to prove Theorem 6.15. The proof of Lemma 9.2 is deferred to Section 9.3, after first establishing some preliminary results in Section 9.2.

Lemma 9.2.

For , given suppose that the solution to the ESP for satisfies the boundary jitter property. Let be a sequence in such that converges to in as and for each , let denote the solution to the ESP for . Then for all , converges to in as .

Proof of Theorem 6.15.

Fix and, for any , denote just by . Fix and a sequence in such that converges to in as . Let denote the solution to the ESP for and for each , let denote the solution to the ESP for . Fix and a sequence in such that converges to in as . Let denote a metric on that is compatible with the Skorokhod -topology. Let denote a metric on that is compatible with the topology of uniform convergence on compact intervals. Since the topology of uniform convergence on compact intervals is a stronger topology than the Skorokhod -topology, we can assume the metrics are chosen such that . Then by the triangle inequality and Lipschitz continuity of the derivative map (Proposition 6.13),

Since and the Skorokhod -topology relativized to coincides with the topology of uniform convergence on compact intervals there, converges to uniformly on compact intervals as . Therefore, converges to zero as . We are left to show converges to zero as . According to Lemma 9.1, there is a sequence in such that converges to in as . For each , by the Lipschitz continuity of the derivative map,

By Lemma 9.2, converges to zero as . Then letting , converges to zero. This completes the proof. ∎

9.2. Characterization of solutions to the derivative problem

In this section we characterize solutions to the DP along when the input is simple up until the first time hits the intersection of two or more faces. As a preliminary result, in Lemma 9.4, we first characterize solutions to the DP when the input is constant.

In order to characterize the solutions to the DP, we first need some definitions. Recall that denotes the th face of , for ; and for . The following is an upper semicontinuity property of the set-valued function .

Lemma 9.3 ([13, Lemma 2.1]).

For each , there is an open neighborhood of in such that for all .

Suppose is the solution to the ESP for and . Define and for such that , define

| (9.2) |

to be the first time after that lies on a boundary face that is distinct from the faces on which lies. Also, define

| (9.3) |

We claim that for some , at which point we set and end the sequence. To see that the claim holds, suppose for a proof by contradiction that for all . Since is increasing and bounded from above, there exists such that as . By the upper semicontinuity of shown in Lemma 9.3 and the continuity of , this implies there exists such that for all . Since , this implies

| (9.4) |

However, (9.3) and (9.4) imply , which yields a contradiction. With this contradiction thus obtained, we see that for some .

We now characterize solutions to the DP when the input is constant. In this case is constant while is in the interior of and jumps whenever hits the boundary and the jump can be expressed in terms of a derivative projection matrix. (Recall the derivative projection matrices , , introduced in Lemma 3.4.)

Lemma 9.4.

Proof.

We will prove the relation

| (9.6) |

We can then iterate (9.6) and use the fact that to obtain (9.7). Let . We first claim that is constant on . Due to the uniqueness that follows from Lipschitz continuity of the derivative map stated in Proposition 6.13, in order to prove the claim it suffices to show that if satisfies conditions 1–4 of the derivative problem for and is constant on , then satisfies conditions 1–4 of the derivative problem for . Let . Since satisfies condition 1 of the derivative problem at and are constant on , we have , so condition 1 of the derivative problem holds at . Next, since satisfies condition 2 of the derivative problem at , is constant on and by the definition of in (9.2), we have , where the last inclusion holds by (2.8). Thus, condition 2 of the derivative problem holds at . Lastly, since is constant on , conditions 3 and 4 of the derivative problem are straightforward to verify, so we omit the details. This concludes the proof that is constant on .

Next, by the definition of in (9.3), the upper semicontinuity of shown in Lemma 9.3 and the continuity of , there exists such that for all . Along with the fact that is constant on , conditions 1–4 of the derivative problem, the fact that is constant on , and the definition of in (2.4), this implies that and

The unique characterization of stated in Lemma 3.4 then implies (9.6) holds. ∎

We have the following corollary of Lemma 9.4.

Corollary 9.5.

Given and , suppose is the solution to the ESP for and is the solution to the derivative problem along for . Let and suppose is constant on . Then there exists and such that

| (9.7) |

In Lemma 9.6 below, we characterize solutions to the DP along for simple up until the first time hits the intersection of two or more faces. In the next section we use an inductive argument (on the first time hits or more faces) to prove continuity properties of the derivative map. With that in mind, given a solution to the ESP for , define

| (9.8) |

and set . Suppose is of the form

| (9.9) |

for some , such that for , and with . For each , define and the sequence in as follows: set and for such that , recursively define

| (9.10) |

If for some , then set and end the sequence so that

| (9.11) |

On the other hand, if for all , then set . In the case that , since is increasing and bounded above by , there exists such that as . If , then we must have , and hence, . Alternatively, if , then the definition of given in (9.10) and the continuity of imply that , which along with the fact that for all implies . In either case, we see that if , then as . Hence, due to the fact that , we have only if . In this case,

| (9.12) |

Lemma 9.6.

Proof.

In order to prove the lemma, it suffices to show that , where is defined as in (9.13), satisfies conditions 1–3 of the derivative problem along for on the interval (since condition 4 follows from condition 3 when is continuous). Condition 1 holds automatically. We next show that condition 2 holds. Given let and be such that . By (9.10), . Therefore, due to the fact that maps into , it follows that

Therefore, condition 2 of the derivative problem holds. We are left to show that condition 3 of the derivative problem holds. First observe that for and , (9.9) and (9.13) imply that and are constant on , and hence is constant there as well. Therefore, it suffices to show that

| (9.14) |

for each and . Suppose and . Then by definition, so the facts that , by (9.13), by (9.9) and by Lemma 3.4, together imply

Next, suppose and . Then the facts that , by (9.13), is continuous at by (9.9) and together imply

This verifies (9.14), and thus proves the lemma. ∎

9.3. Proof of Lemma 9.2

We use the principle of mathematical induction to prove the following statement holds for . Since by definition, this will complete the proof of Lemma 9.2. Given , we say that a function is a time-change if is nondecreasing and onto.

Statement 1.

Given , suppose that the solution to the ESP for satisfies the boundary jitter property (Definition 6.6). Let be a sequence in such that converges to in as and for each , let denote the solution to the ESP for . Then given , there is a sequence of time-changes mapping to such that for all ,

| (9.15) |

and for all ,

| (9.16) |

We first prove the base case .

Lemma 9.7.

Statement 1 holds with .

Since the proof of the base case is lengthy, we first provide a brief outline of the argument. First, we show that because satisfies the boundary jitter property and converges to as , it follows that, roughly speaking, on a compact interval contained in and for sufficiently large, hits the same boundary faces that hits, and hits those boundary faces in the same order that does. The time-change is then constructed so that, again roughly speaking, on , jumps at the same time that jumps, and hits the same boundary faces that hits, and both paths, and , hit those boundary faces in the same order and at the same times. The paths and will then be equal on since the jumps of both paths depend only on the jump times and jump sizes of and , respectively, and on the times that and , respectively, hit the boundary faces.

Proof of Lemma 9.7.

Let , , , and be as in Statement 1. Define as in (9.8). If , then (9.15) and (9.16) hold trivially. For the remainder of the proof we assume that . Since converges to in as , and the Skorokhod -topology relativized to coincides with the topology of uniform convergence on compact intervals, the Lipschitz continuity of the ESM stated in Proposition 6.5(ii) implies the following:

-

(a)

converges to uniformly on compact intervals as .

Since we are only concerned with the interval in this proof and , we can assume without loss of generality that is of the form (9.9) for some , , such that for , and with . For each , define and the sequence in as in (9.10) and the subsequent two sentences. As noted following (9.10), for each and

| (9.17) | |||||

| (9.18) |

By the definition of in (9.10), the definition of in (9.8) and condition 1 of the boundary jitter property, for each and , there is a unique index such that

-

(b)

and is nonconstant on every neighborhood of .

By the upper semicontinuity of shown in Lemma 9.3, the continuity of , the definition of in (9.10) and (b), for each and , there exists , which is not necessarily unique, such that

| (9.19) | ||||||

| (9.20) | ||||||

| (9.21) | ||||||

| (9.22) |

Set . By (9.19)–(9.22), the upper semicontinuity of , (b) and (a), for each , we can choose such that for all ,

| (9.23) | ||||||

| (9.24) | ||||||

| (9.25) | ||||||

| (9.26) |

and

-

(c)

is nonconstant on for and ,

-

(d)

is nonconstant on for .

By (9.24), (9.26), (c), (d) and the fact that can only increase when lies in , we have

-

(e)

for each and , for some ,

-

(f)

for each , for some .

Given define and for each , define and the sequence in as follows: set and, for such that , define

| (9.27) |

If for some , then set . Alternatively, if for all , then set . Let and suppose . Then (9.27), the definition of for , (9.23)–(9.26), (e) and (f) imply that

-

(g)

for ,

-

(h)

and for and ,

-

(i)

and for .

Now fix and . We show that

| (9.28) |

Since , we can choose sufficiently small so that . Let be such that (e.g., if , choose ; and if , choose ). By (a), (9.20), (b), (c) and (d), there exists a positive integer sufficiently large such that if , then for and is nonconstant on . This, along with (e) and (f), implies that for all . Since was arbitrary, (9.28) holds.

We now define the time-changes . Let be such that for each and all , (9.23)–(9.26) hold. Fix . If , then set for all . Now suppose . Let be such that . For and , and for and , define

| (9.29) |

and, if , define

| (9.30) |

whereas if , define

| (9.31) |

It is readily verified from (9.29), (9.30) and (9.31) that for each , is a nondecreasing, continuous, piecewise linear function mapping onto such that for each ,

| (9.32) | |||||

| (9.33) |

We begin with the proof of (9.15). Let . We first treat the case that . By (9.17) and (9.18), we can choose such that . Then by (9.29), (9.30) and (9.31), for all ,

| (9.34) |

Letting , it follows from (9.28) that (9.15) holds. Next, consider the case that . Let be arbitrary. Since and (9.15) holds whenever , we have

| (9.35) |

Therefore, it suffices to show that

| (9.36) |

By the triangle inequality and the fact that is nondecreasing, we have, for all and ,

| (9.37) | ||||

By (9.35) and the continuity of , as , which along with (9.37) yields (9.36). This establishes (9.15).

We now turn to the proof of (9.16), which will complete the proof that Statement 1 holds with . Let . By (9.17) and (9.18), we can choose such that . We show that for each ,

| (9.38) |

which will complete the proof of (9.16). Fix . By Lemma 9.6, for each and , satisfies

| (9.39) |

for all , where . Similarly, by Lemma 9.6, for each and (by (g)), satisfies

| (9.40) | ||||

for , where and we have used (h) and (i) in the second equality and properties of the derivative projection matrix in Lemma 3.4. By (9.32), (9.33), for and , or for and ,

| (9.41) |

Then since , by (9.39), (9.41) and a simple recursion argument, we see that (9.38) holds. ∎

Before proving the induction step, we need the following helpful lemma.

Lemma 9.8 ([14, Lemma 8.3]).

There is a norm on , denoted , such that under the derivative projection matrix is a contraction for all ; that is, for all and . Furthermore, since norms on are equivalent, there exists such that for all .

Proof.

Let , , , and be as in Statement 1. If then (9.15) and (9.16) hold by assumption. For the remainder of the proof we assume that . We split the proof into four parts (whose titles are indicated using italic font). The first two parts are devoted to defining the time-changes and the latter two parts are devoted to proving convergence results for the time-changes and the time-changed paths.

Partition of the interval into subintervals : Set , and for such that , define to be the first time after that hits a face that does not lie in the subset of faces that lies in; that is,

| (9.42) |

and let be the first time after that lies at the intersection of or more faces; that is,

| (9.43) |

If for some , then set and end the sequence. Alternatively, if for all , define . In this case, we claim that as . The claim clearly holds if as ; and on the other hand, if is uniformly bounded for all , then there must be an accumulation point and it follows from (9.42)–(9.43) that the accumulation point must be . In either case, the following holds:

| (9.44) | Given , there exists such that . |

Definition of the time-changes : We use the induction hypothesis and time-shift properties of the ESP (Lemma 6.4) and derivative problem to define the time-changes on intervals of the form for . We begin with the interval . Since by definition and Statement 1 holds by the induction hypothesis, there is a sequence of time-changes mapping to such that for all ,

| (9.45) |

and for all ,

| (9.46) |

For each , define on the interval by

| (9.47) |

Now suppose . Since spends zero Lebesgue measure on the boundary due to condition 2 of the boundary jitter property (Definition 6.6), it follows from the definition of in (9.42) and the upper semicontinuity of shown in Lemma 9.3 that there exists

| (9.48) |

such that

| (9.49) |

Since by (9.42), the definition of in (9.1) implies that is constant in a neighborhood of . In particular, by choosing possibly larger, we can assume that

| (9.50) |

Define

| (9.51) |

By the time-shift property of the ESP, is a solution to the ESP for . In addition, since satisfies the boundary jitter property and by (9.49), it follows from (6.2) that

| (9.52) |

Finally, by (6.2), (9.49) and (9.43),

| (9.53) | ||||

For each , define , and

| (9.54) |

Again, by the time-shift property of the ESP, is a solution to the ESP for . Since converges to in uniformly on compact intervals as , it follows that

| (9.55) |

Therefore, by the Lipschitz continuity of the ESM (Proposition 6.5(ii)),

| (9.56) |

Define

| (9.57) |

By the time-shift property of the derivative problem (Lemma 6.12),

| (9.58) |

The definitions of and , the fact that so , the fact that and (9.1) imply that

| (9.59) |

By (9.52), (9.55), (9.59) and the fact that Statement 1 holds by assumption (with , , , , , , and in place of , , , , , , and , respectively), there is a sequence of time-changes mapping to such that for all ,

| (9.60) |

and for all ,

| (9.61) |

For each , define on the interval (due to (9.53)) by

| (9.62) |

Convergence of the time-changed paths on intervals of the form : We use the principle of mathematical induction to show that for each and for all ,

| (9.63) |

and for all ,

| (9.64) |

The base case follows immediately from (9.45) and (9.46). Now suppose and (9.63) holds for all and (9.64) holds for all . We first prove (9.63) holds for all with in place of . Let . We have

| (9.65) |

| (9.66) |

By (9.65), our assumption that (9.63) holds, (9.66) and (9.60), we see that (9.63) holds with in place of .

Next, we prove (9.64) holds for all . If , then (9.64) follows by assumption. Let . We have

| (9.67) | ||||

We first show that

| (9.68) |

Since by (9.43), Proposition 6.14 implies that is continuous at . Let . By (9.48) and the continuity of at , we can choose sufficiently small such that

| (9.69) |

and

| (9.70) |

Due to the upper semicontinuity of shown in Lemma 9.3 and the definition of in (9.42), we can choose possibly smaller to ensure that

| (9.71) |

It follows from (9.64) (which holds for by assumption) that

| (9.72) |

Then by (9.72) and (9.70), we can choose sufficiently large such that for all ,

| (9.73) | ||||

By (9.56), the fact that (9.63) holds with in place of and the relation , we see that

Then by the last display, (9.71) and the upper semicontinuity of , we can choose possibly larger such that for all ,

| (9.74) |

Let be arbitrary. Since is constant on , according to Corollary 9.5, there exists and a sequence such that for all ,

| (9.75) |

In addition, since (by condition 2 of Definition 6.9) and (9.74) holds, it follows from the uniqueness of the derivative projection matrices stated in Lemma 3.4 that

By (9.75), the last display and the fact that are linear operators, we have, for all ,

Let be the norm on introduced in Lemma 9.8. Then by the last display, Lemma 9.8, (9.70) and (9.73), for all ,

Since was arbitrary, for all ,

Since norms on are equivalent and was arbitrary, we have

| (9.76) |

Next, we show that

| (9.77) |

Define , , and in (9.51), , and as in (9.54) and as in (9.57). For each , define by

| (9.78) |

Then by the time-shift property of the derivative problem (Lemma 6.12),

| (9.79) |

Thus, by (9.79), (9.58) and the triangle inequality,

| (9.80) | ||||

By the Lipschitz continuity of the derivative map (Proposition 6.13), the definition of in (9.78), the definition of in (9.57), we have

Then by (9.68) and the fact that due to (9.62), letting yields

| (9.81) |

Since , it follows from (9.61) that

| (9.82) |

Together, (9.80), (9.81) and (9.82) imply (9.77) holds. Since (9.68) and (9.77) both hold, we see that (9.64) holds with in place of . With the induction step established, the principle of mathematical induction implies that for each , (9.63) holds for all and (9.64) holds for all .

Convergence of the time-changed paths on : We first prove (9.15) holds for all with in place of . Let . Suppose . Then there exists such that , so by (9.63),

| (9.83) |

Now suppose . Let be arbitrary. Since (9.83) holds for all , we have

| (9.84) |

Thus, we are left to show that

| (9.85) |

By the triangle inequality and the fact that is nondecreasing, for all and ,

| (9.86) |

By (9.84) and the continuity of , as . Thus, (9.85) holds, which implies (9.15) holds with in place of . We are left with the final step of proving (9.16) holds for all . Let . By (9.44) there exists such that . It then follows from (9.64) that (9.16) holds. ∎

Proof of Lemma 9.2.

Acknowledgments. We thank Mike Giles for useful feedback on a preliminary draft of this paper.

References

- [1] S. Asmussen and P. W. Glynn. Stochastic Simulation: Algorithms and Analysis. Springer, 2007.

- [2] A. D. Banner, R. Fernholz, and I. Karatzas. Atlas models of equity markets. Ann. Appl. Probab., 15(4):2296–2330, nov 2005.

- [3] R. F. Bass and E. Pardoux. Uniqueness for diffusions with piecewise constant coefficients. Probab. Theory Related Fields, pages 557–572, 1987.

- [4] J. Blanchet and K. R. A. Murthy. Exact simulation of multidimensional reflected Brownian motion. arXiv preprint arXiv:1405.6469, 2014.

- [5] M. Bossy, E. Gobet, and D. Talay. Symmetrized Euler scheme for an efficient approximation of reflected diffusions. Journal of Applied Probability, 4(3):877–889, 2004.

- [6] H. Chen and A. Mandelbaum. Leontief systems, RBVs and RBMs. In M.H.A. Davis and R.J. Elliott, editors, Appl. Stoch. Anal. (London, 1989), pages 1–43. Gordon and Breach, New York, 1991.

- [7] P. Dupuis and K. Ramanan. Convex duality and the Skorokhod problem. I. Probab. Theory Relat. Fields, 115:153–195, 1999.

- [8] E. R. Fernholz. Stochastic Portfolio Theorey. Springer, New York, 2002.

- [9] P. Glasserman. Monte Carlo Methods in Financial Engineering. Springer, New York, 2003.

- [10] E. Gobet. Efficient schemes for the weak approximation of reflected diffusions. Monte Carlo Methods and Applications, 7:193–202, 2001.

- [11] J. M. Harrison. Brownian Motion and Stochastic Flow Systems. Wiley, New York, 1985.

- [12] T. Ichiba, V. Papathanakos, A. Banner, I. Karatzas, and R. Fernholz. Hybrid atlas models. Ann. Appl. Probab., 21(2):609–644, 2011.

- [13] W. Kang and R. J. Williams. An invariance principle for semimartingale reflecting Brownian motions in domains with piecewise smooth boundaries. Ann. Appl. Probab., 17(2):741–779, 2007.

- [14] D. Lipshutz and K. Ramanan. On directional derivatives of Skorokhod maps in convex polyhedral domains. To appear in Ann. Appl. Probab., 2016.

- [15] D. Lipshutz and K. Ramanan. Pathwise differentiability of reflected diffusions in convex polyhedral domains. arXiv preprint arXiv:1705.02278v1, 2017.

- [16] D. Lipshutz and K. Ramanan. Sensitivity analysis of the stationary distribution of reflected Brownian motion in a convex polyhedral cone. Preprint, 2017.

- [17] Y. Liu. Numerical approches to stochastic differential equations with boundary conditions. PhD thesis, Purdue University, 1993.

- [18] A. Mandelbaum and G. Pats. State-dependent stochastic networks. Part I. Approximations and applications with continuous diffusion limits. Ann. Appl. Probab., 8(2):569–646, 1998.

- [19] W. P. Peterson. A heavy traffic limit theorem for networks of queues with multiple customer types. Math. Oper. Res., 16(1):90–118, 1991.

- [20] R. Pettersson. Approximations for stochastic differential equations with reflecting convex boundaries. Stoch. Process. Appl., 59:295–308, 1995.

- [21] R. Pettersson. Penalization schemes for reflecting stochastic differential equations. Bernoulli, 3:403–414, 1997.

- [22] K. Ramanan. Reflected diffusions defined via the extended Skorokhod map. Electron. J. Probab., 11(36):934–992, 2006.

- [23] K. Ramanan and M. I. Reiman. Fluid and heavy traffic diffusion limits for a generalized processor sharing model. Ann. Appl. Probab., 13(1):100–139, 2003.

- [24] K. Ramanan and M. I. Reiman. The heavy traffic limit of an unbalanced generalized processor sharing model. Ann. Appl. Probab., 18(1):22–58, 2008.

- [25] M. I. Reiman. Open queueing networks in heavy traffic. Math. Oper. Res., 9(3):441–458, 1984.

- [26] L. C. G. Rogers and D. Williams. Diffusions, Markov Processes and Martingales. Volume 2: Itô Calculus. Cambridge University Press, Cambridge, UK, second edition, 2000.

- [27] L. Słomiński. On approximation of solutions of multidimensional SDE’s with reflecting boundary conditions. Stoch. Process. Appl., 50:197–219, 1994.

- [28] L. Słomiński. Euler’s approximations of solutions of SDEs with reflecting boundary. Stoch. Process. Appl., 94:317–337, 2001.

- [29] Stroock and S. R. S. Varadhan. Multidimensional diffusion processes. Springer, Berlin, 2006.

- [30] W. Whitt. An Introduction to Stochastic-Process Limits and Their Applications to Queues. Internet Supplement, 2002. http://www.columbia.edu/~ww2040/supplement.html.

- [31] L. Yan. The Euler scheme with irregular coefficients. Ann. Probab., 30(3):1172–1194, 2002.

- [32] J. Yang and H. J. Kushner. A Monte Carlo method for sensitivity analysis and parametric optimization of nonlinear stochastic systems. SIAM Journal on Control and Optimization, 29(5):1216–1249, 1991.