Multi-objective risk-averse two-stage

stochastic programming problems

Abstract

We consider a multi-objective risk-averse two-stage stochastic programming problem with a multivariate convex risk measure. We suggest a convex vector optimization formulation with set-valued constraints and propose an extended version of Benson’s algorithm to solve this problem. Using Lagrangian duality, we develop scenario-wise decomposition methods to solve the two scalarization problems appearing in Benson’s algorithm. Then, we propose a procedure to recover the primal solutions of these scalarization problems from the solutions of their Lagrangian dual problems. Finally, we test our algorithms on a multi-asset portfolio optimization problem under transaction costs.

Keywords and phrases: multivariate risk measure, multi-objective risk-averse two-stage stochastic programming, risk-averse scalarization problems, convex Benson algorithm, nonsmooth optimization, bundle method, scenario-wise decomposition

Mathematics Subject Classification (2010): 49M27, 90C15, 90C25, 90C29, 91B30.

1 Introduction

We consider a multi-objective risk-averse two-stage stochastic programming problem of the general form

In this formulation, is the first-stage decision variable, is the second-stage decision variable and is a compact finite-dimensional set defined by linear constraints. are cost parameters which are matrices of appropriate dimension. We assume that is deterministic and is random. is a multivariate convex risk measure, which is a set-valued mapping from the space of -dimensional random vectors into the power set of (see Hamel and Heyde (2010)). In other words, is the set of deterministic cost vectors for which becomes acceptable in a certain sense.

The above problem is a vector optimization problem and solving it is understood as computing the upper image of the problem defined by

whose boundary is the so-called efficient frontier. Here, denotes the closure operator. One would be interested in finding a set of weakly efficient solutions with for some such that there is no with and . Here, denotes the componentwise strict order in . The components of these solutions are on the efficient frontier. In addition, the set is supposed to construct in the sense that

where denotes the convex hull operator. Our aim is to compute approximately using a finite set of weakly efficient solutions.

Algorithms for computing upper images of vector optimization problems are extensively studied in the literature. A seminal contribution in this field is the algorithm for linear vector optimization problems by Benson (1998), which computes the set of all weakly efficient solutions of the problem and works on the outer approximation of the upper image rather than the feasible region itself. Benson’s algorithm has been generalized recently in Ehrgott et al. (2011) and Löhne et al. (2014) for (ordinary) convex vector optimization problems, namely, optimization problems with a vector-valued objective function and a vector-valued constraint that are convex with respect to certain underlying cones, e.g., the positive orthants in the respective dimensions. While the algorithm in Ehrgott et al. (2011) relies on the differentiability of the involved functions, Löhne et al. (2014) makes no assumption on differentiability and obtains finer approximations of the upper image by making use of the so-called geometric dual problem.

In the literature, there is a limited number of studies on multi-objective two-stage stochastic optimization problems. Some examples of these studies are Abbas and Bellahcene (2000), Cardona et al. (2011), where the decision maker is risk-neutral, that is, one takes . In principle, multi-objective risk-neutral two-stage stochastic optimization problems with linear constraints and continuous variables can be formulated as linear vector optimization problems and they can be solved using the algorithm in Benson (1998). If the number of scenarios is not too large, then the problem can be solved in reasonable computation time. Otherwise, one should look for an efficient method, generally, based on scenario decompositions.

To the best of our knowledge, for the risk-averse case, there is no study on multi-objective two-stage stochastic programming problems. However, single-objective mean-risk type problems can be seen as scalarizations of two-objective stochastic programming problems (see, for instance, Ahmed (2006), Miller and Ruszczyński (2011)). On the other hand, Dentcheva and Wolfhagen (2016), Noyan et al. (2017) work on single-objective problems with multivariate stochastic ordering constraints. As pointed out in the recent survey Gutjahr and Pichler (2016), there is a need for a general methodology for the formulation and solution of multi-objective risk-averse stochastic problems.

The main contributions of the present study can be summarized as follows:

-

1.

To the best of our knowledge, this is the first study focusing on multi-objective risk-averse two-stage stochastic programming problems in a general setting.

-

2.

We propose a vector optimization formulation for our problem using multivariate convex risk measures. Such risk measures include, but are not limited to, multivariate coherent risk measures and multivariate utility-based risk measures.

-

3.

To solve our problem, we suggest an extended version of the convex Benson algorithm in Löhne et al. (2014) that is developed for a convex vector optimization problem with a vector-valued constraint. Different from Löhne et al. (2014), we deal with set-valued risk constraints and dualize them using the dual representation of multivariate convex risk measures (see Hamel and Heyde (2010)) and the Lagrange duality for set-valued constraints (see Borwein (1981)).

-

4.

The convex Benson algorithm in Löhne et al. (2014) cannot be used for some multivariate risk measures, specifically, for higher-order nonsmooth risk measures. On the other hand, our method is general and can be used for any risk measures for which subgradients can be calculated. An example of such risk measures is higher-order mean semideviation (see Shapiro et al. (2009) and the references therein).

-

5.

Two risk-averse two-stage stochastic scalarization problems, namely, the problem of weighted sum scalarization and the problem of scalarization by a reference variable, have to be solved during the procedure of the convex Benson algorithm. As the number of scenarios gets larger, these problems cannot be solved in reasonable computation time. Therefore, based on Lagrangian duality, we propose scenario-wise decomposable dual problems for these scalarization problems and suggest a solution procedure based on the bundle algorithm (see Lemaréchal (1978), Ruszczyński (2006) and the references therein).

-

6.

Our scenario-wise decomposition algorithms for the scalarization problems can be embedded into other algorithms using the same type of scalarization problems. See (Jahn, 2004, Chapter 12) for examples of such algorithms.

-

7.

We propose a procedure to recover the primal solutions of the scalarization problems from the solutions of their Lagrangian dual problems.

The rest of the paper is organized as follows: In Section 2, we provide some preliminary definitions and results for multivariate convex risk measures. In Section 3, we provide the problem formulation and recall the related notions of optimality. Section 4 is devoted to the convex Benson algorithm. The two scalarization problems in this algorithm are treated separately in Section 5. In particular, we propose scenario-wise decomposition algorithms and procedures to recover primal solutions. Computational results are provided in Section 6. Some proofs related to Section 5 are collected in the appendix.

2 Multivariate convex risk measures

We work on a finite probability space with . For each , let be the probability of the elementary event so that .

Let us introduce the notation for (random) vectors and matrices. Let be a given integer and . and denote the set of all elements of the Euclidean space whose components are nonnegative and positive, respectively. For , their scalar product and Hadamard product are defined as

respectively. For a set , its associated indicator function (in the sense of convex analysis) is defined by

for each . We denote by the set of all -dimensional random cost vectors , which is clearly isomorphic to the space of -dimensional real matrices. We write for . For , we denote by its realization at , and define the expected value of as

Similarly, given another integer , we denote by the set of all -dimensional random matrices with realizations .

The elements of will be used to denote random cost vectors; hence, lower values are preferable. To that end, we introduce , the set of all elements in whose components are nonnegative random variables. Given , we write if and only if for every and , that is, . We call a set-valued function a multivariate convex risk measure if it satisfies the following axioms (see Hamel and Heyde (2010)):

-

(A1)

Monotonicity: implies for every .

-

(A2)

Translativity: for every and .

-

(A3)

Finiteness: for every .

-

(A4)

Convexity: for every , .

-

(A5)

Closedness: The acceptance set of is a closed set.

A multivariate convex risk measure is called coherent if it also satisfies the following axiom:

-

(A6)

Positive homogeneity: for every , .

Remark 2.1.

It is easy to check that the values of a multivariate convex risk measure are in the collection of all closed convex upper subsets of , that is,

where and denote the closure and convex hull operators, respectively. In other words, for every , the set is a closed convex set with the property . The collection , when equipped with the superset relation , is a complete lattice in the sense that every nonempty subset of has an infimum (and also a supremum) which is uniquely given by as an element of (see Example 2.13 in Hamel et al. (2016)). The complete lattice property of makes it possible to study optimization problems with -valued objective functions and constraints, as will also be crucial in the approach of the present paper.

A multivariate convex risk measure can be represented in terms of vectors of probability measures and weight vectors in the cone , which is called its dual representation. To state this representation, we provide the following definitions and notation.

Let be the set of all -dimensional vectors of probability measures on , that is, for each , the probability measure assigns the probability to the elementary event for . For and , we also write . Finally, for and , we define the expectation of under by

A multivariate convex risk measure has the following dual representation (see Theorem 6.1 in Hamel and Heyde (2010)): for every ,

where is the minimal penalty function of defined by

| (2.1) |

for each , . Note that and are convex functions as they are suprema of linear functions.

The scalarization of by a weight vector is defined as the function

| (2.2) |

on . As an immediate consequence of the dual representation of , we also obtain a dual representation for its scalarization:

| (2.3) |

Some examples of multivariate coherent and convex risk measures are the multivariate conditional value-at-risk (multivariate CVaR) and the multivariate entropic risk measure, respectively.

Example 2.2 (Multivariate CVaR).

Let be a polyhedral closed convex cone with . The multivariate conditional value-at-risk is defined by

| (2.4) |

where

for each and (see Definition 2.1 and Remark 2.3 in Hamel et al. (2013)). Here, is a risk-aversion parameter and for . The minimal penalty function of is given by

where is the positive dual cone of defined by

Note that (2.4) is the multivariate extension of the well-known conditional value-at-risk (see Rockafellar and Uryasev (2000), Rockafellar and Uryasev (2002)).

Example 2.3 (Multivariate entropic risk measure).

Consider the vector-valued exponential utility function defined by

where

for each and . Here, is a risk-aversion parameter. Note that is a concave decreasing function. Let be a polyhedral closed convex cone with . The multivariate entropic risk measure is defined as

| (2.5) |

for each (see Section 4.1 in Ararat et al. (2017)). Since , larger values of the expected utility are prefered. Moreover, as each is a decreasing function, implies for every .

3 Problem formulation

We consider a multi-objective risk-averse two-stage stochastic programming problem. The decision variables and the parameters of the problem consist of deterministic and random vectors and matrices of different dimensions. To that end, let us fix some integers and deterministic parameters and . At the first stage, the decision-maker chooses a deterministic vector with associated cost , where . At the second stage, the decision-maker chooses a random vector based on the first-stage decision as well as the random parameters . The random cost associated with is , where .

Given feasible choices of the decision variables and , the risk associated with the second-stage cost vector is quantified via a multivariate convex risk measure . The set consists of the deterministic cost vectors in that can make acceptable in the following sense:

where is the acceptance set of the risk measure. Hence, collects the deterministic cost reductions from that would yield an acceptable level of risk for the resulting random cost. Together with the deterministic cost vector , the overall risk associated with and is given by the set

where the last equality holds thanks to the translativity property (A2).

Our aim is to calculate the “minimal” vectors over all feasible choices of and . Using vector optimization, we formulate our problem as follows:

| () | |||

Let

We assume that is a compact set. Let us denote by the image of the feasible region of under the objective function, that is,

The upper image of is defined as the set

| (3.1) |

In particular, we have , that is, is a closed convex upper set; see Remark 2.1.

Finding the “minimal” vectors of is understood as computing the boundary of the set . For completeness, we recall the minimality notions for .

Definition 3.1.

A point is called a weak minimizer (weakly efficient solution) of if and is a weakly minimal element of , that is, there exists no such that .

Definition 3.2.

(Definition 3.2 in Löhne et al. (2014)) A set is called a weak solution of if the following conditions are satisfied:

-

1.

Infimality: it holds ,

-

2.

Minimality: each is a weak minimizer of .

Ideally, one would be interested in computing a weak solution of . However, except for some special cases (e.g. when the values of and the upper image are polyhedral sets), such consists of infinitely many feasible points, that is, it is impossible to recover using only finitely many values of . Therefore, our aim is to propose algorithms to compute approximately through finitely many feasible points.

Definition 3.3.

(Definition 3.3 in Löhne et al. (2014)) Let . A nonempty finite set is called a finite weak -solution of if the following conditions are satisfied:

-

1.

-Infimality: it holds ,

-

2.

Minimality: each is a weak minimizer of .

As noted in Löhne et al. (2014), a finite weak -solution provides an outer and an inner approximation of in the sense that

| (3.2) |

Let us also introduce the weighted sum scalarization problem with weight vector :

| () |

Define as the optimal value of . For the remainder of this section, we provide a discussion on the existence of optimal solutions of as well as the relationship between and .

Proposition 3.4.

Let . Then, there exists an optimal solution of .

- Proof.

Remark 3.5.

Note that the feasible region of is not compact in general due to the multivariate risk measure , which has unbounded values. However, in Löhne et al. (2014), the feasible region of a vector optimization problem is assumed to be compact. Therefore, by assuming only to be compact, Proposition 3.4 generalizes the analogous result in Löhne et al. (2014).

The following proposition is stated in Löhne et al. (2014) without a proof. It can be shown as a direct application of Theorem 5.28 in Jahn (2004).

Proposition 3.6.

(Proposition 3.4 in Löhne et al. (2014)) Let . Every optimal solution of is a weak minimizer of .

Proposition 3.6 implies that, in the weak sense, solving is understood as solving the family of weighted sum scalarizations.

4 Convex Benson algorithms for

The convex Benson algorithms have a primal and a dual variant. While the primal approximation algorithm computes a sequence of outer approximations for the upper image in the sense of (3.2), the dual approximation algorithm works on an associated vector maximization problem, called the geometric dual problem. To explain the details of these algorithms, we should define the concept of geometric duality as well as a new scalarization problem , called the problem of scalarization by a reference variable .

4.1 The problem of scalarization by a reference variable

The problem is required to find the minimum step-length to enter the upper image from a point along the direction . It is formulated as

| () |

Note that is a scalar convex optimization problem with a set-valued constraint. We denote by the optimal value of . We relax the set-valued constraint in a Lagrangian fashion and obtain the following dual problem using the results of Section 3.2 in Borwein (1981):

| () |

Note that is constructed by rewriting the risk constraint of as and calculating the support function of the set by the dual variable . The next proposition states the strong duality relationship between and .

Proposition 4.1.

(Theorem 19 and Equation (3.23) in Borwein (1981)) Let . Then, there exist optimal solutions of and of , and the optimal values of the two problems coincide.

Finally, we recall the relationship between and . The next proposition is provided without a proof since the proof in Löhne et al. (2014) can be directly applied to our case.

Proposition 4.2.

(Proposition 4.5 in Löhne et al. (2014)) Let . If is an optimal solution of , then is a weak minimizer of .

4.2 Geometric duality

Let be the unit simplex in , that is,

For each , let be the unit vector in , that is, the entry of is one and all other entries are zero.

The geometric dual of problem is defined as the vector maximization problem

| () | |||

where is the so-called ordering cone defined as . Similar to the upper image of , we can define the lower image of as

Remark 4.3.

In analogy with Remark 2.1, the lower image is a closed convex -lower set, that is, .

Next, we state the relationship between and the optimal solutions of , , .

Proposition 4.4.

(Proposition 3.5 in Löhne et al. (2014)) Let . If has a finite optimal value , then is a boundary point of and it is also a -maximal element of , that is, there is no such that .

Proposition 4.5.

(Propositions 4.6, 4.7 in Löhne et al. (2014)) Let . If is an optimal solution of and is an optimal solution of , then is a maximizer of , that is, is a -maximal element of the lower image . Moreover, is a supporting halfspace of at the point .

Proposition 4.6.

Let . If is an optimal solution of , then is a supporting halfspace of at the point .

-

Proof.

From Proposition 4.4, is a boundary point of . Moreover, it follows that

since . Hence, the assertion of the proposition follows. ∎

Proposition 4.7.

(Proposition 3.10 in Löhne et al. (2014)) Let .

-

(a)

Let be a finite weak -solution of . Then,

is an inner approximation of the upper image , that is, . Moreover,

is an outer approximation of the lower image , that is, .

-

(b)

Let be a finite -solution of . Then,

is an inner approximation of , that is, . Moreover,

is an outer approximation of , that is, .

The problems , and the above propositions form a basis for the primal and dual convex Benson algorithms. These algorithms are explained briefly in the following sections.

4.3 Primal algorithm

The primal algorithm starts with an initial outer approximation for the upper image . To construct , for each , the algorithm computes the supporting halfspace of with direction vector by solving the weighted-sum scalarization problem . If is an optimal solution of , then this halfspace supports the upper image at the point . Then, is defined as the intersection of these supporting halfspaces.

The algorithm iteratively obtains a sequence of finer outer approximations, it updates a set and of weak minimizers and maximizers for and , respectively. At iteration , the algorithm first computes , that is the set of all vertices of . For each vertex , an optimal solution to is computed. The optimal is the minimum step-length required to find a boundary point of . Since the triplet is a weak minimizer of by Proposition 4.2, it is added to the set . Then, an optimal solution of the dual problem is computed, which is a maximizer for (see Proposition 4.5) and is added to the set . This procedure is continued until a vertex with a step-length greater than an error parameter is detected. For such , using Proposition 4.5, a supporting halfspace of at point is obtained. The outer approximation is updated as by intersecting with this supporting halfspace. The algorithm terminates when all the vertices are in -distance to the upper image .

At the termination, the algorithm computes inner and outer approximations for the upper image and for the lower image using Proposition 4.7. Note that both and are outer approximations for . However, is a finer outer approximation than . The reason is that when is updated, only the vertices in more than -distance to are used. On the other hand, all the vertices are considered when calculating . Furthermore, the algorithm returns a finite weak -solution to and a finite -solution to (see Theorem 4.9 in Löhne et al. (2014)).

The steps of the primal algorithm are provided as Algorithm 1.

4.4 Dual algorithm

The steps of the dual algorithm follow in a way that is similar to the primal algorithm; however, as a major difference, at each iteration, an outer approximation for the dual image is obtained. Moreover, the dual algorithm does not require solving ; only is solved for different weights in the initialization step as well as in the iterations. An optimal solution of is used to update the outer approximation of as in Proposition 4.6.

At the termination, the algorithm computes inner and outer approximations for the upper image and lower image using Proposition 4.7. Furthermore, the algorithm returns a finite weak -solution to and a finite -solution to (see Theorem 4.14 in Löhne et al. (2014)).

The steps of the dual algorithm are provided as Algorithm 2.

5 Scenario decomposition for scalar problems

In this section, we are interested in solving the scalarization problems and . Note that these problems are single-objective multivariate risk-averse two-stage stochastic programming problems. For such problems, the problem size increases as the number of scenarios, , gets larger. An efficient solution procedure is possible by scenario-wise decompositions. In the univariate case, for risk-neutral two-stage stochastic programming problems, see Birge and Louveaux (1997), Birge and Louveaux (1988), Kall and Mayer (2005), Ruszczyński (2003), Van Slyke and Wets (1969) for solution methodologies by scenario-wise decomposition. For scenario decompositions in two-stage risk-averse stochastic programming problems, the reader is refered to Ahmed (2006), Miller and Ruszczyński (2011), Fábián (2008), Kristoffersen (2005) for problems with a single coherent risk-averse objective function and to Liu et al. (2016) for chance-constrained problems. Scenario-wise decomposition solution methodology is also possible for multi-stage stochastic programming problems with dynamic coherent risk measure as suggested in Collado et al. (2012). Different from these studies, the scalarization problems we solve are two-stage risk-averse stochastic programming problems with multivariate convex risk measures; therefore, these problems require different solutions techniques than the existing ones.

5.1 The problem of weighted sum scalarization

Let . The weighted sum scalarization problem defined in Section 3 can be rewritten more explicitly as:

| () | |||

We propose a Lagrangian dual reformulation of whose objective function is scenario-wise decomposable. The details are provided in Section 5.1.1. Based on this dual reformulation, in Section 5.1.2, we propose a dual cutting-plane algorithm for , called the dual bundle method, which provides an optimal dual solution. As the Benson algorithms in Section 4 require an optimal primal solution in addition to an optimal dual solution, in Section 5.1.3, we show that such a primal solution can be obtained from the dual of the so-called master problem in the dual bundle method.

5.1.1 Scenario decomposition

To derive a decomposition algorithm for , we randomize the first stage variable and treat it as an element with realizations . To ensure the equivalence of the new formulation with the previous one, we add the so-called nonanticipativity constraints

which are equivalent to .

Let us introduce

| (5.1) |

where, for each ,

With this notation and using the nonanticipativity constraints, we may rewrite as follows:

| () | |||

Note that the optimal value of is .

The following theorem provides a dual formulation of by relaxing the nonanticipativity constraints in a Lagrangian fashion. We call this dual formulation as .

Theorem 5.1.

-

Proof.

We may write

(5.3) (5.4) (5.5) where the passage to the last line is by (2.3). Using the minimax theorem of Sion (1958), we may interchange the infimum and the supremum in the last line. This yields

(5.6) where, for each ,

(5.7) Let us fix . Note that is the optimal value of a large-scale linear program where the only coupling constraints between the decision variables for different scenarios are the nonanticipativity constraints. To obtain a formulation of this problem that can be decomposed into a subproblem for each scenario, we dualize the nonanticipativity constraints. The reader is referred to Section 2.4.2 of Shapiro et al. (2009) for the details on the dualization of nonanticipativity constraints. To that end, let us assign Lagrange multipliers for the non-anticipativity constraints. Note that we may consider them as the realizations of a random Lagrange multiplier . By strong duality for linear programming,

where the Lagrangian is defined by

for each . Given such , note that

if we set . In this case, . Therefore, we obtain

(5.8) where , defined by (5.2), is the optimal value of the subproblem for scenario . The assertion of the theorem follows from (5.6) and (5.8). ∎

5.1.2 The dual bundle method

To solve given in Theorem 5.1, we propose a dual bundle method which constructs affine upper approximations for , , and . The upper approximations are based on the subgradients of these functions at points that are generated iteratively by solving the so-called master problem. The reader is referred to Ruszczyński (2006) for the details of the bundle method.

For , we denote by the subdifferential of the concave function at the point , that is, is the set of all vectors such that

| (5.9) |

for all . Note that the right hand side of (5.9) provides an affine upper approximation for . For this reason, (5.9) is called as a cut.

Similarly, we denote by the subdifferential of the concave function at a point , which is the set of all vectors such that

| (5.10) |

for all . We call (5.10) a cut for .

In the next proposition, we show how to compute the subdifferential of the function at a point .

Proposition 5.2.

For , let

Then,

-

Proof.

Let . The function is affine for all . The function is also affine and continuous for all . Finally, the set is compact by assumption. By Theorem 2.87 in Ruszczyński (2006), the assertion of the proposition follows. ∎

Next, we show how to compute a subgradient of the function at a point .

Proposition 5.3.

Recall that the set is the acceptance set of . For , let

and assume that . Then,

-

Proof.

Let . The function is affine for all . The function is also affine and continuous for all . By Theorem 2.87 in Ruszczyński (2006), the assertion of the proposition follows. ∎

Remark 5.4.

For practical risk measures, such as the multivariate entropic risk measure (see Example 2.3), the function is differentiable and the subdifferential is a singleton. For coherent multivariate risk measures, such as the multivariate CVaR (see Example 2.2), there exists a convex cone such that if and otherwise. For multivariate CVaR with risk-aversion parameter ,

For a coherent multivariate risk measure, is the set of all normal directions of at . It follows that the cut (5.10) is always satisfied; therefore, it can be ignored.

At each iteration of the bundle method, we solve the master problem

| () | |||

| (5.11) | |||

| (5.12) | |||

| (5.13) | |||

| (5.14) | |||

| (5.15) | |||

| (5.16) |

with , . Here, denotes the Euclidean norm on an appropriate dimension. Note that constraints (5.14) and (5.15) for are equivalent to having , and constraint (5.13) for is equivalent to having . with are parameters of the problem, called the centers, that are initialized and updated within the bundle method. The quadratic terms in the objective function are Moreau-Yosida regularization terms and they make the overall objective function strictly convex. These regularization terms enforce an optimal solution of to be close to the centers.

Let be an optimal solution for . Computing the subgradients

at this optimal solution and using (5.9) and (5.10), a cut for each of the functions and are added to at the next iteration in order to improve the upper approximations for these functions.

The centers are updated in the following fashion. At iteration , one checks if the difference between the objective value of evaluated at the point , that is, , and the objective value evaluated at the centers , that is, , is larger than a threshold. If so, this means that an optimal solution of is close to . Therefore, the new centers are set to , respectively. This is called a descent step. Otherwise, the centers remain unchanged, that is, are set to , respectively.

The steps of our dual bundle method are provided as Algorithm 3. By (Ruszczyński, 2006, Theorem 7.16), the bundle method generates a sequence that converges to an optimal solution of as . In practice, the stopping condition in line 22 of Algorithm 3 is not satisfied. Therefore, it is a general practice to stop the algorithm when

| (5.17) |

for some small constant .

Remark 5.5.

Note that the objective function of can be replaced with

and constraint (5.11) can be replaced with

This way one would obtain an upper approximation for the sum . Compared to the multiple cuts in (5.11), this provides a looser upper approximation for . However, while one adds cuts at each iteration in the multiple cuts version, this approach adds a single cut.

5.1.3 Recovery of primal solution

Both the primal and the dual Benson algorithms require an optimal solution of the problem . Therefore, in Theorem 5.6, we suggest a procedure to recover an optimal primal solution from the solution of the master problem .

Theorem 5.6.

Let be the index set at the last iteration of the dual bundle method with the approximate stopping condition (5.17) for some . Let be the first descent iteration after the approximate stopping condition is satisfied and let . For with centers and index set , let be the Lagrangian dual variables assigned to the constraints (5.11), (5.12), (5.13), (5.14), (5.15), respectively, with for each . Let be an optimal solution of the subproblem in line 6 of Algorithm 3 for each and . Let

be a dual optimal solution for . Let be defined by

Moreover, let be a minimizer of the problem

Then, is an approximately optimal solution of in the following sense:

-

(a)

for each .

-

(b)

.

-

(c)

As , it holds for each .

-

(d)

As , it holds .

5.2 The problem of scalarization by a reference variable

Let . The problem defined in Section 4.1 is formulated to find the minimum step-length to enter from along the direction and it can be rewritten more explicitly as

| () | |||

We propose a scenario-wise decomposition solution methodology for . Even the steps we follow are similar to the ones for , the decomposition is more complicated because the weights are not parameters but instead they are decision variables in the dual problem of (see Theorem 5.11 below). Therefore, following the same steps as in results in a nonconvex optimization problem. In order to resolve this convexity issue, we propose a new formulation for by introducing finite measures to the dual representation of .

The flow of this section is as follows: in Sections 5.2.1 and 5.2.2, we propose a scenario-wise decomposition solution methodology for . Section 5.2.3 is devoted to the recovery of a primal solution.

5.2.1 Scenario decomposition

To derive a decomposition algorithm for , we randomize the first stage variable as in and add the nonanticipativity constraints

Using the feasible region defined by (5.1), we may rewrite as follows:

| () | |||

Note that the optimal value of is .

Different from the approach for , in order to obtain a convex dual problem for , we use finite measures instead of probability measures in the dual representation of . To that end, let be the set of all -dimensional vectors of finite measures on , that is, for each , the finite measure assigns to the elementary event for . For and , we also write .

The following lemma provides the relationship between and .

Lemma 5.7.

For every and , there exists such that

| (5.18) |

for every . Conversely, for every , there exist and such that (5.18) holds for every .

- Proof.

Recall that is the minimal penalty function of as defined in (2.1). For , let us define

| (5.19) |

Similarly, recall the function defined in (5.2). For and , let us define

| (5.20) |

Therefore, if and are related as in Lemma 5.7 and , then it is clear that

Example 5.8.

Recall Example 2.3 on the multivariate entropic risk measure. The function takes the form

where and is the relative entropy of with respect to defined by

Example 5.9.

Remark 5.10.

Note that, in general, is not a convex function since is not a convex function. On the other hand, is a convex function. Indeed, for each and , is a linear function so that is a convex function since it is the supremum of linear functions indexed by . Similarly, is not a concave function in general. However, is the infimum of linear functions indexed by ; therefore, it is a concave function.

Theorem 5.11.

It holds

| () |

In view of Remark 5.10, while the first reformulation of provided in Theorem 5.11 is not a convex optimization problem, the second reformulation, that is , is a convex optimization problem.

Lemma 5.12.

For every ,

-

Proof.

Let . Note that

is the optimal value of a single-objective optimization problem with a set-valued constraint function . Using the Lagrange duality in Borwein (1981) for such problems, in particular, Theorem 19, we have

(5.21) To be able to use this result, we check the following constraint qualification: is open at in the sense that for every with and for every , there exists an open ball around such that

(5.22) To that end, let with , that is, . Let . Since is an interior point of and due to the monotonicity and translativity of , it follows that is an interior point of . On the other hand, note that

thanks to the monotonicity and translativity of . Hence, is an interior point of the above union. Therefore, (5.22) holds for some open ball around and (5.21) follows.

-

Proof of Theorem 5.11.

Using Lemma 5.12, we may write

Using the minimax theorem of Sion (1958), we may interchange the infimum and the supremum, and obtain

where, for each , , is defined by (5.7). Hence, using (5.8), we obtain

where is defined by (5.2). Hence, the first reformulation follows. The second reformulation follows from the first reformulation and Lemma 5.7. ∎

5.2.2 The dual bundle method

To solve provided in Theorem 5.11, we propose a dual bundle method similar to the one in Section 5.1.2.

At each iteration of the dual bundle method, we solve the master problem given below. Here, denotes a subgradient of the concave function at the point . Similarly, denotes a subgradient of the concave function at the point . We call (5.23) and (5.24) a cut for and , respectively.

| () | |||

| (5.23) | |||

| (5.24) | |||

| (5.25) | |||

| (5.26) | |||

| (5.27) | |||

| (5.28) |

Here, , .

The steps of the dual bundle method are provided in Algorithm 4. Similar to (5.17), the algorithm stops in practice when

| (5.29) |

for some . Since the construction of this algorithm is similar to the construction of Algorithm 3, the details are omitted for brevity.

Next, we provide a recipe for computing the subgradients . Let us denote by the subdifferential of the function at a point , and by the subdifferential of the function at a point . In the next proposition, we show how to compute and a subgradient of the function .

Proposition 5.13.

-

(a)

For , let

Then,

-

(b)

Recall that the set is the acceptance set of . For , let

and assume that . Then,

5.2.3 Recovery of primal solution

The primal Benson algorithm requires an optimal solution of the problem . Therefore, in Theorem 5.14, we suggest a procedure to recover an optimal primal solution from the solution of the master problem .

Theorem 5.14.

Let be the index set at the last iteration of the dual bundle method with the approximate stopping condition (5.29) for some . Let be the first descent iteration after the appriximate stopping condition is satisfied and let . For with centers and index set , let be the Lagrangian dual variables assigned to the constraints (5.23), (5.24), (5.25), (5.26), (5.27), respectively, with for each . Let be an optimal solution of the subproblem in line 6 of Algorithm 4 for each and . Let

be a dual optimal solution for . Let be defined by

Let

Then, is an approximately optimal solution of in the following sense:

-

(a)

for each .

-

(b)

.

-

(c)

As , it holds for each .

-

(d)

As , it holds .

5.2.4 Recovery of a solution to ()

In addition to a primal optimal solution , the primal Benson algorithm also requires an optimal solution of the dual problem (see Section 4.1). Therefore, in Theorem 5.15, we suggest a procedure to recover this solution from the solution of the master problem .

Theorem 5.15.

In the setting of Theorem 5.14, let

| (5.30) |

Then, is an approximately optimal solution of () in the following sense: as , it holds

| (5.31) |

6 Computational Study

In order to test our methods, we solve a multi-objective risk-averse portfolio optimization problem under transaction costs. We consider a one-period market with risky assets. Each asset has a random return . At the beginning of the period, it costs units of asset for an agent to buy one unit of asset . At the end of the period, the random transaction cost of buying one unit of asset is units of asset .

The risk-averse agent has a capital units of asset to be invested in the assets. Let denote the number of physical units of asset purchased by the agent; hence, she spends units of asset for this purchase. At the end of the period, the agent observes the random return of each asset as well as the random transaction costs between the assets. The value of each asset is and it is transacted to purchase the assets with a transaction cost of for asset . Let denote the number of physical units of asset purchased by selling some units of asset . Let denote the total number of physical units of asset purchased by the agent so that . The objective is to minimize the risk of the random cost vector using a multivariate convex risk measure . This problem can be formulated as follows:

Note that is the first-stage, are the second-stage decision variables.

All computational experiments are conducted on a PC with 8.00 GB of RAM and an Intel(R) Core(TM) i7-4790 CPU@3.60 GHz processor. We use Matlab implementations of Algorithms 3 and 4 where CVX 1.22 is used to solve master problems and CPLEX 12.6 is used to solve subproblems.

We generate two classes of instances where the number of assets is either 2 or 3. In both cases, we assume . We set , . The return of asset 1 is uniformly distributed between and , denoted by . Similarly, we assume and . The random transaction costs among the assets are assumed to have the following distributions: , , , , , , and .

First of all, in Example 6.1, we compare our dual bundle method with CVX on the problem of weighted sum scalarization. Our dual bundle method takes the advantage of scenario-wise decompositions while CVX solves the problem as a standard convex optimization problem without decompositions.

Example 6.1.

We compare the CPU times (in seconds) of the dual bundle method and the CVX solver on instances with two- and three-dimensional multivariate entropic risk measure and different numbers of scenarios (). In each instance, we use a fixed weight vector .

| Dual Bundle Method | CVX | |

|---|---|---|

| 1000 | 869.22 | 75.98 |

| 2500 | 2130.85 | 588.85 |

| 5000 | 4170.55 | 3091.44 |

| 10000 | 8452.47 | ** |

| Dual Bundle Method | CVX | |

|---|---|---|

| 50 | 56.39 | 35.22 |

| 100 | 252.73 | 98.73 |

| 250 | 1838.38 | 346.87 |

| 500 | 6309.39 | ** |

As observed in Table 1 and Table 2, the CVX solver overperforms the dual bundle method for smaller numbers of scenarios. However, as the number of scenarios increases, the dual bundle method overperforms the CVX solver. For instance, for in Table 1, the CVX solver cannot solve the problem due to a memory error. The same situation is observed for in Table 2.

For the remainder of this section, we use the multivariate CVaR (see Example 2.2) and the multivariate entropic risk measure (see Example 2.3) for the choice of . For each risk measure, we consider the biobjective ( assets) and the three-objective ( assets) cases. We run the primal and dual Benson algorithms with different error parameters () and report the total number of scalar optimization problems solved (opt.), the number of vertices in the final outer approximation (vert.) and the CPU time in seconds (time).

Example 6.2.

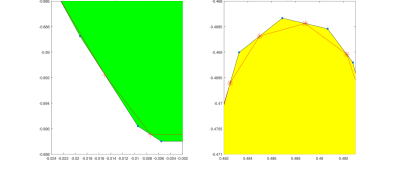

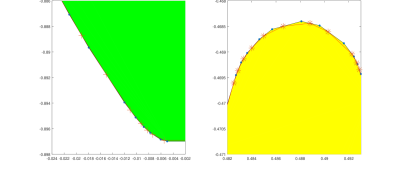

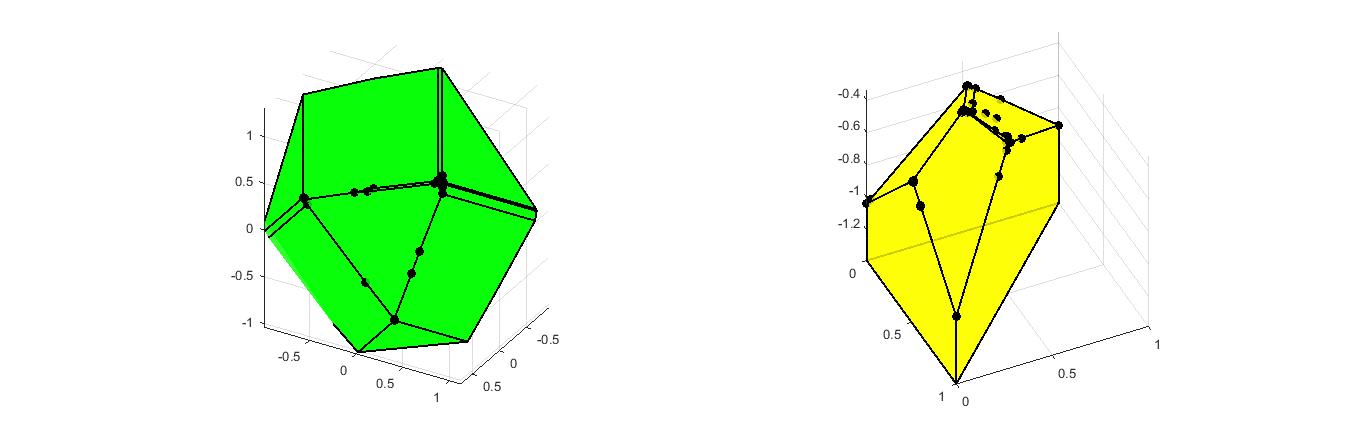

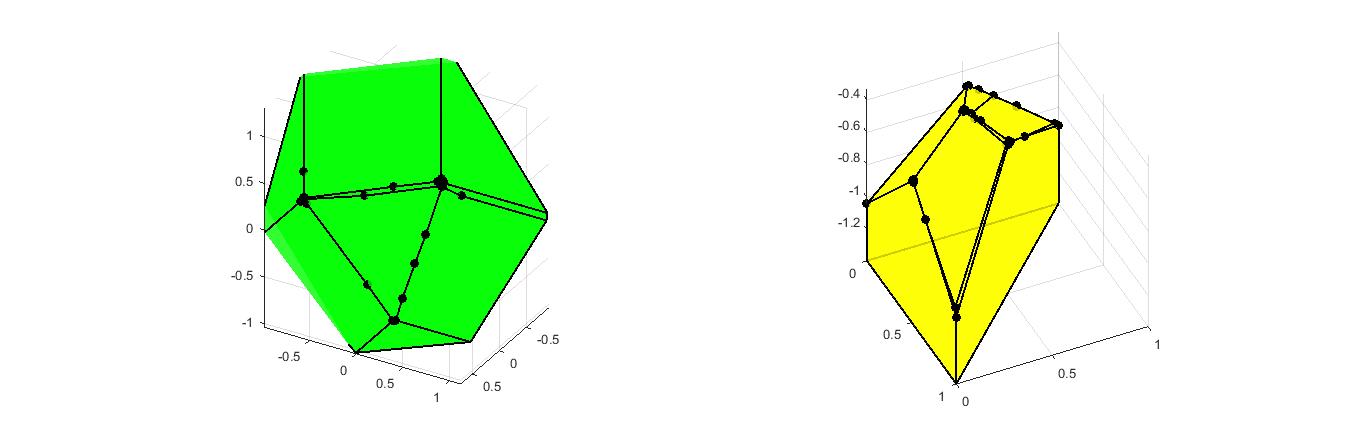

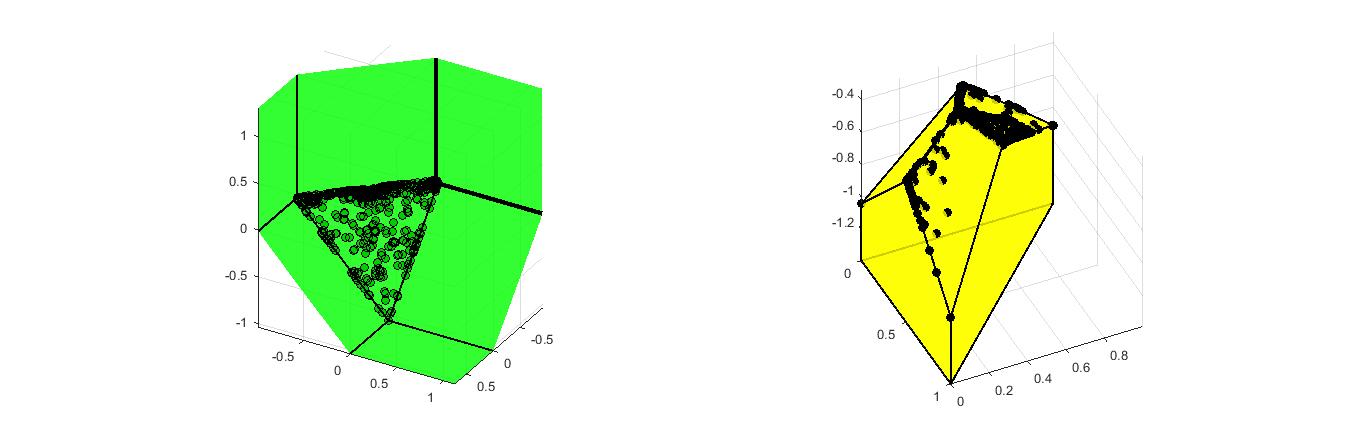

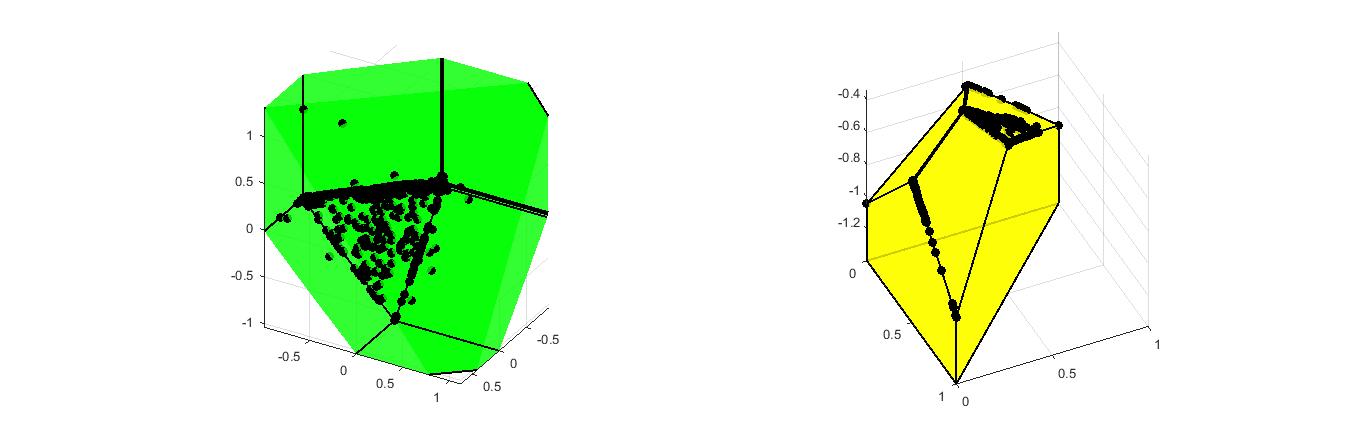

(Two-dimensional multivariate CVaR) We consider assets under scenarios. The parameters of the multivariate CVaR are chosen as . We use error parameter values . The computational results are reported in Table 3. It can be seen that the performances of the primal and dual algorithms are close to each other.

The inner (red lines) and outer (blue lines) approximations of the upper image and the lower image are given in Figures 1 and 2. These figures are obtained by the primal algorithm. Since the corresponding figures for the dual algorithm are similar, they are omitted. Clearly, the algorithm provides finer approximations for the upper and lower images when is reduced from to .

| opt. | vert. | time | ||

|---|---|---|---|---|

| Primal Algorithm | 5 | 3 | 2675.69 | |

| 11 | 6 | 10513.06 | ||

| 23 | 13 | 11391.12 | ||

| Dual Algorithm | 5 | 4 | 2819.92 | |

| 13 | 8 | 7021.55 | ||

| 25 | 15 | 10007.75 |

Example 6.3.

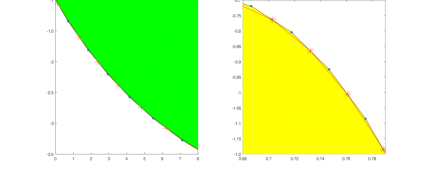

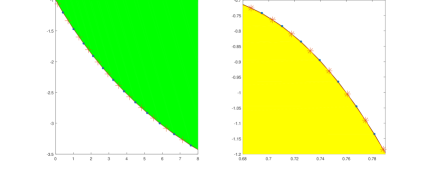

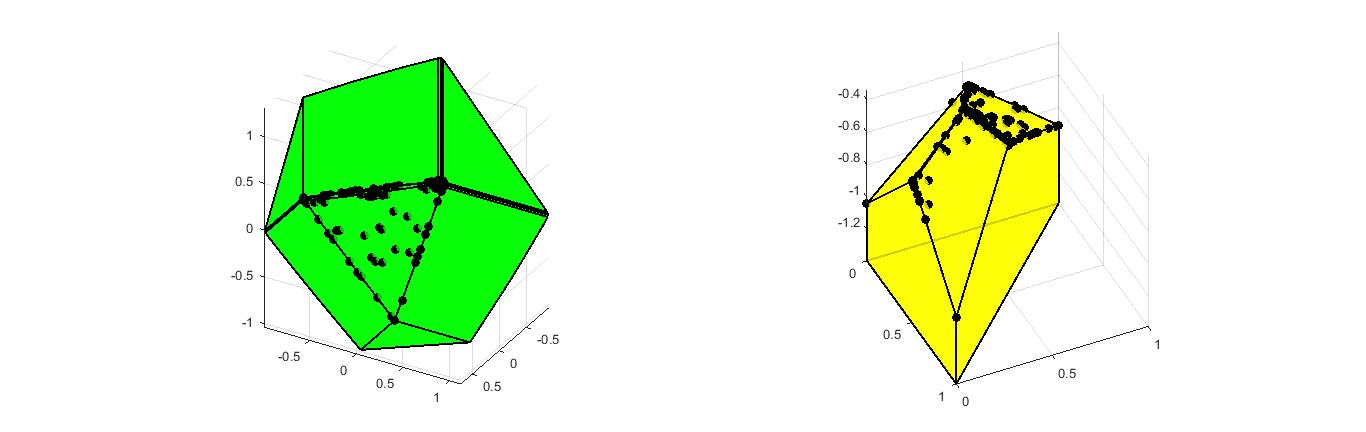

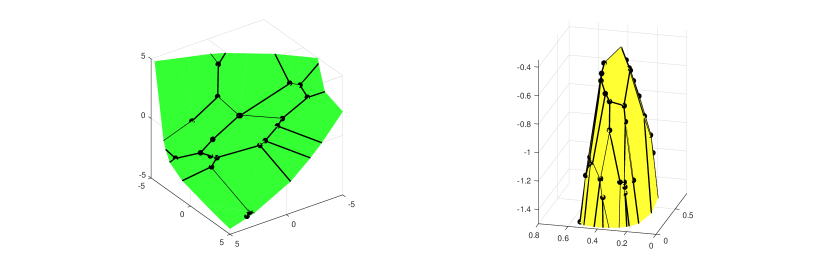

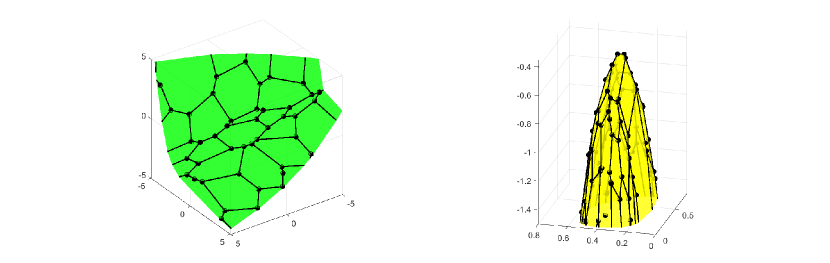

(Two-dimensional multivariate entropic risk measure) We consider assets under scenarios. The parameters of the multivariate entropic risk measure are chosen as and the cone is generated by the vectors and . We use error parameter values .

The computational results are reported in Table 4. In this example, the dual algorithm solves more optimization problems and enumerates more vertices than the primal algorithm in significantly shorter time. The inner and outer approximations of the upper image and the lower image obtained by the primal algorithm are given in Figures 3 and 4. Since the corresponding figures for the dual algorithm are similar, they are omitted.

| opt. | vert. | time | ||

|---|---|---|---|---|

| Primal Algorithm | 0.1 | 25 | 13 | 37706.90 |

| 0.05 | 37 | 19 | 84730.81 | |

| 0.01 | 83 | 42 | 144848.62 | |

| Dual Algorithm | 0.1 | 31 | 17 | 13955.43 |

| 0.05 | 47 | 25 | 14088.08 | |

| 0.01 | 85 | 44 | 17121.26 |

Example 6.4.

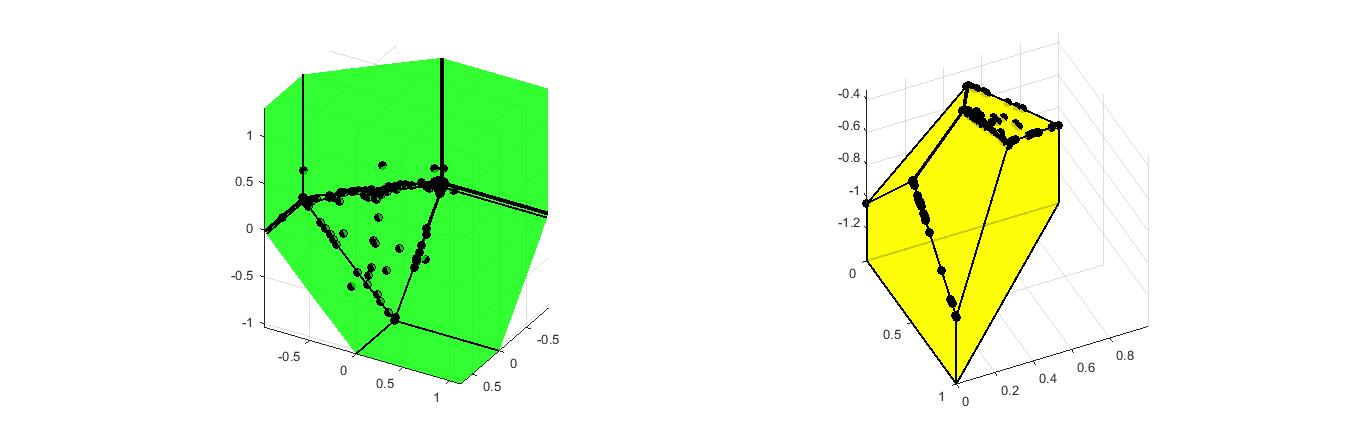

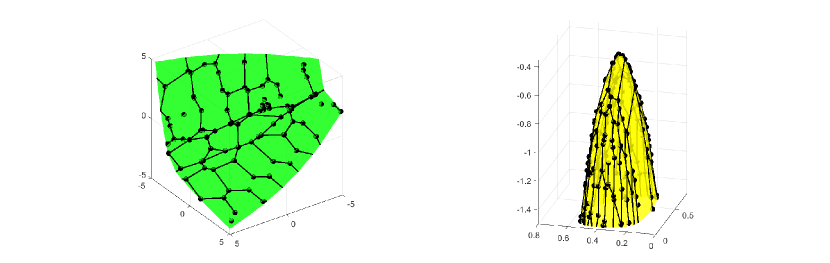

(Three-dimensional multivariate CVaR) We consider assets under scenarios. The parameters of the multivariate CVaR are chosen as . We use error parameter values .

The computational results are reported in Table 5. For and , the primal algorithm terminates in shorter time while, for , the dual algorithm is faster.

The outer approximations of the upper image and the lower image obtained by the primal and dual algorithms are given in Figures 5-7. Note that the dots represent the vertices of some polyhedra even if they are not connected by line segments.

As observed in these figures, the primal algorithm provides a better approximation of the lower image compared to the dual algorithm. However, the approximation of the upper image provided by the dual algorithm is better than the one by the primal algorithm.

The multivariate CVaR is defined in terms of the positive part function , which is piecewise linear. As a result, the upper and lower images of the problem are polyhedral sets and the vertices of their outer approximations in Figures 5-7 are generally dense around certain line segments.

| opt. | vert. | time | ||

|---|---|---|---|---|

| Primal Algorithm | 21 | 9 | 16856.84 | |

| 82 | 32 | 67555.09 | ||

| 468 | 162 | 319862.68 | ||

| Dual Algorithm | 24 | 11 | 20303.43 | |

| 98 | 36 | 79397.49 | ||

| 448 | 152 | 249081.86 |

Example 6.5.

(Three-dimensional multivariate entropic risk measure) We consider assets under scenarios. The parameters of the multivariate entropic risk measure are chosen as and the cone is generated by the vectors . We use error parameter values .

The computational results are reported in Table 4. We are not able to solve this problem using the primal algorithm as the dual bundle method for does not converge for some vertices . This is in line with what is reported in (Löhne et al., 2014, Example 5.4) for a four-objective problem with multivariate entropic risk measure. The results of the dual algorithm are provided in Table 6 and Figure 8.

As the multivariate entropic risk measure is defined in terms of the exponential utility function, which is strictly convex, the upper and lower images are non-polyhedral sets. For this reason, the polyhedral outer approximations of these sets have a more uniform density of vertices over their surfaces compared to the outer approximations for the multivariate CVaR.

| opt. | vert. | time | ||

|---|---|---|---|---|

| Dual Algorithm | 0.1 | 196 | 61 | 48742.57 |

| 0.05 | 319 | 99 | 82237.89 | |

| 0.01 | 670 | 211 | 168460.45 |

References

- Abbas and Bellahcene (2000) M. Abbas, F. Bellahcene, Cutting plane method for multiple objective stochastic integer linear programming, European Journal of Operational Research, 168(3), 967–984 (2006)

- Ahmed (2006) S. Ahmed, Convexity and decomposition of mean-risk stochastic programs, Mathematical Programming, 106(3), 433–446 (2006)

- Aliprantis and Border (2006) C. D. Aliprantis, K. C. Border, Infinite dimensional analysis: a hitchhiker’s guide. Springer, Heidelberg, Germany (2006)

- Ararat et al. (2017) Ç. Ararat, A. H. Hamel, B. Rudloff, Set-valued shortfall and divergence risk measures, International Journal of Theoretical and Applied Finance, doi: 10.1142/S0219024917500261 (2017)

- Benson (1998) H. P. Benson, An outer approximation algorithm for generating all efficient extreme points in the outcome set of a multiple objective linear programming problem, Journal of Global Optimization, 13(1), 1–24 (1998)

- Birge and Louveaux (1988) J. R. Birge, F. V. Louveaux. A multicut algorithm for two-stage stochastic linear programs, European Journal of Operational Research, 34(3), 384–392 (1988)

- Birge and Louveaux (1997) J. R. Birge, F. V. Louveaux, Introduction to Stochastic Programming. Springer, New York, USA (1997)

- Borwein (1981) J. M. Borwein, Convex relations in analysis and optimization, in: S. Schaible, W. T. Ziemba (eds.) Generalized Concavity in Optimization and Economics, Academic Press Inc., New York, 335–377 (1981)

- Cardona et al. (2011) Y. Cardona-Valdés, A. Álvarez, D. Özdemir, A bi-objective supply chain design problem with uncertainty, Transportation Research Part C: Emerging Technologies, 19(5), 821–832 (2011)

- Collado et al. (2012) R. A. Collado, D. Papp, A. Ruszczyński, Scenario decomposition of risk-averse multistage stochastic programming problems, Annals of Operations Research, 200(1), 147–170 (2012)

- Dentcheva and Ruszczyński (2009) D. Dentcheva, A. Ruszczyński, Optimization with multivariate stochastic dominance constraints, Mathematical Programming, 117(1), 111–127 (2009)

- Dentcheva and Wolfhagen (2016) D. Dentcheva, E. Wolfhagen, Two-stage optimization problems with multivariate stochastic order constraints, Mathematics of Operations Research, 41(1), 1–22 (2016)

- Ehrgott et al. (2011) M. Ehrgott, L. Shao, A. Schöbel, An approximation algorithm for convex multi-objective programming problems, Journal of Global Optimization, 50(3), 397–416 (2011)

- Fábián (2008) C. I. Fábián, Handling CVaR objectives and constraints in two-stage stochastic models, European Journal of Operational Research, 191(3), 888–911 (2008)

- Föllmer and Schied (2002) H. Föllmer, A. Schied, Convex measures of risk and trading constraints, Finance and Stochastics, 6(4), 429–447 (2002)

- Gutjahr and Pichler (2016) W. J. Gutjahr, A. Pichler, Stochastic multi-objective optimization: a survey on non-scalarizing methods, Annals of Operations Research, 236(2) 475–499 (2016)

- Hamel and Heyde (2010) A. H. Hamel, F. Heyde, Duality for set-valued measures of risk, SIAM Journal on Financial Mathematics, 1(1), 66–95 (2010)

- Hamel et al. (2016) A. H. Hamel, F. Heyde, A. Löhne, B. Rudloff and C. Schrage, Set optimization - a rather short introduction, In: (ed.) A. Hamel, F. Heyde, A. Löhne, B. Rudloff and C. Schrage, Set optimization and applications in finance - the state of the art, Proceedings in Mathematics & Statistics, Springer, 65–141 (2016)

- Hamel et al. (2013) A. H. Hamel, B. Rudloff, M. Yankova, Set-valued average value at risk and its computation, Mathematics and Financial Economics, 7(2), 229–246 (2013)

- Jahn (2004) J. Jahn, Vector Optimization - Theory, Applications, and Extensions. Springer, Berlin Heidelberg, Germany (2004)

- Kall and Mayer (2005) P. Kall, J. Mayer, Stochastic Linear Programming. Springer, New York, USA (2005)

- Kristoffersen (2005) T. K. Kristoffersen, Deviation measures in linear two-stage stochastic programming, Mathematical Methods of Operations Research, 62(2), 255–274 (2005)

- Lemaréchal (1978) C. Lemaréchal, Nonsmooth optimization and descent methods, Research Report 78-2, International Institute for Applied Systems Analysis, Laxenburg (1978)

- Liu et al. (2016) X. Liu, S. Küçükyavuz, J. Luedtke, Decomposition algorithms for two-stage chance-constrained programs, Mathematical Programming, 157(1), 219–243 (2016)

- Löhne et al. (2014) A. Löhne, B. Rudloff, F. Ulus, Primal and dual approximation algorithms for convex vector optimization problems, Journal of Global Optimization, 60(4), 713-–736 (2014)

- Löhne and Schrage (2013) A. Löhne, C. Schrage, An algorithm to solve polyhedral convex set optimization problems, Optimization, 62(1), 131–141 (2013)

- Miller and Ruszczyński (2011) N. Miller, A. Ruszczyński, Risk-averse two-stage stochastic linear programming: modeling and decomposition, Operations Research, 59(1), 125–132 (2011)

- Noyan et al. (2017) N. Noyan, M. Meraklı, S. Küçükyavuz, Two-stage stochastic programming under multivariate risk constraints with an application to humanitarian relief network design, preprint, (2017)

- Rockafellar and Uryasev (2000) R. T. Rockafellar, S. Uryasev, Optimization of conditional value-at-risk, Journal of Risk, 2(3), 21–41 (2000)

- Rockafellar and Uryasev (2002) R. T. Rockafellar, S. Uryasev, Conditional value-at-risk for general loss distributions, Journal of Banking & Finance, 26(7), 1443–1471 (2002)

- Ruszczyński (2003) A. Ruszczyński, Decomposition methods in A. Ruszczyński, A. Shapiro, eds. Stochastic Programming. Elsevier, Amsterdam, the Netherlands (2003)

- Ruszczyński (2006) A. Ruszczyński, Nonlinear optimization. Princeton University Press, Princeton, New Jersey, USA (2006)

- Shapiro et al. (2009) A. Shapiro, D. Dentcheva, A. Ruszczyński, Lectures on Stochastic Programming: Modeling and Theory. MPS-SIAM Series on Optimization, No. 9, MPS-SIAM, Philadelphia, Pennsylvania, USA (2009)

- Sion (1958) M. Sion, On general minimax theorems, Pacific Journal of Mathematics, 8(1), 171–176 (1958)

- Van Slyke and Wets (1969) R. Van Slyke, R. J.-B. Wets, L-shaped linear programs with applications to optimal control and stochastic programming, SIAM Journal on Applied Mathematics, 17(4), 638–-663 (1969)

Appendix A Proof of Theorem 5.6

In the setting of Theorem 5.6, let be an optimal solution for with index set . Recall that

Let us define

Furthermore, let be defined as

| (A.1) |

for every .

Lemma A.1.

The following relationships hold for , , , , , , , , :

| (A.2) | |||

| (A.3) | |||

| (A.4) | |||

| (A.5) |

-

Proof.

The Lagrangian for with centers and index set is

(A.6) The dual objective function is defined by

and the dual problem is

() Note that is an optimal solution for with centers and index set , and

is the corresponding optimal solution for . The maximization of the Lagrangian over and gives (A.2) and (A.3), respectively, as constraints for the dual problem. The maximization of the Lagrangian over gives the first-order condition (A.4). Finally, the maximization of the Lagrangian over gives the first-order condition (A.5). ∎

Lemma A.2.

The following statements hold for every :

-

(a)

As , .

-

(b)

.

-

(c)

will be an element of the set as in the sense that and for every as .

-

Proof.

- (a)

-

(b)

By line 6 of Algorithm 3, we have for every and . Since is convex, and , we have for every .

-

(c)

Note that for every . Since is a closed set, the limit of this point as is also an element of . On the other hand, for every , as by part (a). Hence, as . Therefore, for every ,

as .

∎

Recall that is a subgradient of at , for each . From (2.1), there exists some , , such that

| (A.9) |

for all . Since is convex, and , it follows that

| (A.10) |

Lemma A.3.

The followings hold:

-

(a)

For each ,

(A.11) -

(b)

For each ,

(A.12) Moreover,

(A.13) -

(c)

(A.14) -

(d)

is an -subgradient of at in the sense that, for every ,

(A.15)

-

Proof.

Consider with centers and index set .

- (a)

-

(b)

Note that

Here, the first inequality follows since for each and , the second inequality follows since

due to the center update rule in line 14 of Algorithm 3, the third inequality follows since the master problem with index set and center has a smaller optimal value than the master problem with index set and center . Finally, the last inequality is by the approximate stopping condition (5.17). Hence, (A.12) and (A.13) follow.

-

(c)

Similar to part (b), we can show that (A.14) holds.

-

(d)

Note that constraint (5.12) can be rewritten as

since by the definition of subgradient. From the complementary slackness conditions,

(A.16) From (A.9), (A.10), (A.16), it follows that

(A.17) For every ,

where the first inequality follows from (2.1), and the last inequality follows from (A.14) and (A.17). Hence, the claim follows.

∎

Lemma A.4.

The followings hold:

-

(a)

As ,

-

(b)

Let be a minimizer of the problem

Then, as .

-

Proof.

-

(a)

Note that

(A.18) where the first equality follows from (A.11). We may rewrite as

(A.19) since is deterministic and . Note that

(A.20) where for . By the proof of Theorem 7.16 in Ruszczyński (2006), we have for every , where is some constant. Using (A.19) and (A.20), we get

(A.21) Therefore, by Lemma A.2(a), (a) and (A.21),

(A.22) as . On the other hand, by (A.13) and using the fact that , are upper approximations for , , respectively, we get

(A.23) By (A.8), as . By Lemma 7.17 in Ruszczyński (2006), as , converges to the optimal value of , which is . Hence, also converges to as . Finally, by triangle inequality, (A.22) and (A.23) yield

From (A.22), the right hand side converges to zero as . We conclude that also converges to as .

-

(b)

By (2.3), we have

The corresponding Lagrangian dual problem is given by

The optimization over gives the first-order condition

(A.24) for some . We argue that satisfies (A.24) in an approximate sense. Note that we may rewrite (A.5) as

(A.25) As shown in (A.15), is an -subgradient of at . Hence, there exists a subgradient of at for each such that as . On the other hand, by (A.8), as . Therefore, from (b), (A.24) is satisfied by and approximately in the sense that

and in the limit as .

∎

-

(a)

Appendix B Proof of Theorem 5.14

In the setting of Theorem 5.14, let be an optimal solution for with index set . Recall that

Let us re-define

Furthermore, let be defined as

| (B.1) |

for every .

Lemma B.1.

The following relationships hold for , , , , , , , , :

| (B.2) | |||

| (B.3) | |||

| (B.4) | |||

| (B.5) |

-

Proof.

The Lagrangian for with centers and index set is

(B.6) The dual objective function is defined by

and the dual problem is

() Note that is an optimal solution for with centers and index set , and

is the corresponding optimal solution for . The maximization of the Lagrangian over and gives (B.2) and (B.3), respectively, as constraints for the dual problem. The maximization of the Lagrangian over gives the first-order condition (B.4). Finally, the maximization of the Lagrangian over gives the first-order condition (B.5). ∎

Lemma B.2.

The following statements hold for every :

-

(a)

As , .

-

(b)

.

-

(c)

will eventually be an element of the set as in the sense that and for every as .

-

Proof.

The proof of this lemma is similar to the proof of Lemma A.2. Therefore, it is omitted. ∎

Recall that is a subgradient of at , for each . From (5.19), there exists some , , such that

| (B.7) |

for all . Since is convex, and , it follows that

| (B.8) |

Lemma B.3.

The followings hold:

-

(a)

For each ,

(B.9) -

(b)

For each ,

(B.10) Moreover,

(B.11) -

(c)

(B.12) -

(d)

is an -subgradient of at in the sense that, for every ,

(B.13)

-

Proof.

Consider with centers and index set .

- (a)

-

(b)

Note that

Here, the first inequality follows since for each and , the second inequality follows since

due to the center update rule in line 14 of Algorithm 4, the third inequality follows since the master problem with index set and center has a smaller optimal value than the master problem with index set and center . Finally, the last inequality is by the approximate stopping condition (5.29). Hence, (B.10) and (B.11) follow.

-

(c)

Similar to part (b), we can show that (B.12) holds.

-

(d)

Note that constraint (5.24) can be rewritten as

since by the definition of subgradient. From the complementary slackness conditions,

(B.14) From (B.7), (B.8), (B.14), it follows that

(B.15) For every ,

where the first inequality follows from (5.19), and the last inequality follows from (B.12) and (B.15). Hence, the claim follows.

∎

Lemma B.4.

The followings hold:

-

(a)

As ,

-

(b)

Let

(B.16) Then, as .

-

Proof.

-

(a)

By (B.9),

(B.17) Using Lemma B.2(a), (B.17) and (A.21), we obtain

(B.18) as . On the other hand, by (B.11) and using the fact that are upper approximations for , respectively, we get

(B.19) By an analog of (A.8), as . By Lemma 7.17 in Ruszczyński (2006), as , converges to the optimal value of , which is . Hence, also converges to as . Finally, by triangle inequality, (B.18) and (B.19) yield

From (B.18), the right hand side of the above inequality converges to zero as . We conclude that also converges to as .

-

(b)

By Lemma 5.7 and Lemma 5.12, we have

The corresponding Lagrangian dual problem is given by

The optimization over gives the first-order condition

(B.20) for some . We argue that satisfies (B.20) in an approximate sense. Note that we may rewrite (B.5) as

(B.21) As shown in (B.13), is an -subgradient of at . Hence, there exists a subgradient of at for each such that as . On the other hand, by an analog of (A.8), as . Therefore, from (b), (B.20) is satisfied by and approximately in the sense that

and

(B.22) in the limit as .

∎

-

(a)

Appendix C Proof of Theorem 5.15

- Proof of Theorem 5.15.

For the objective function of evaluated at , we have

| (C.1) | |||

| (C.2) | |||

where the first equality is obvious, the second equality follows by (2.3), (5.26) and Lemma 5.7, the third and fourth equalities follow by the dualization of the nonanticipativity constraints as in the proof of Theorem 5.1, the fifth equality is by the interchange of infimum and supremum using Sion (1958), the sixth equality follows by the definition of in (5.20). The inequality in (C.2) follows since the feasible region of the problem in (C.1) is a subset of the feasible region of the problem in (C.2). The last equality is by Theorem 5.11.

Since is a feasible solution for the maximization problem in (C.1), we have

As , by Lemma B.4(a), the first expression converges to , and so does the second by sandwich theorem. This finishes the proof of (5.31).

∎