On Game-Theoretic Risk Management (Part Three)

Abstract

Abstract

The game-theoretic risk management framework put forth in the precursor reports “Towards a Theory of Games with Payoffs that are Probability-Distributions” (arXiv:1506.07368 [q-fin.EC]) and “Algorithms to Compute Nash-Equilibria in Games with Distributions as Payoffs” (arXiv:1511.08591v1 [q-fin.EC]) is herein concluded by discussing how to integrate the previously developed theory into risk management processes. To this end, we discuss how loss models (primarily but not exclusively non-parametric) can be constructed from data. Furthermore, hints are given on how a meaningful game theoretic model can be set up, and how it can be used in various stages of the ISO 27000 risk management process. Examples related to advanced persistent threats and social engineering are given. We conclude by a discussion on the meaning and practical use of (mixed) Nash equilibria equilibria for risk management.

1 Introduction

With algorithmic matters of game-theoretic risk management being covered in [37], it remains to discuss a few (among more existing) possibilities of how game models can be used in risk management.

First, observe that matrix games directly cover plain optimization as the special case of an either or game. Both have applications in risk management, such as helping with the following common subtasks:

-

•

If the current security configuration is to be assessed against a number of (new) threats, we can think of the defender having only 1 strategy (the current state). The equilibrium in terms of the -ordering is then the most severe threat (since the attacker maximizes).

-

•

Likewise, if several options for mitigating a particular threat are available, then the equilibrium being the -minimum determined by the defender, is the action leaving the -least damage when being mounted.

-

•

The general case of and strategies for both, the defender and attacker, is discussed in the remainder of this article.

Unique Selling Points:

The method described in the following offers a variety of advantages relative to the “conventional” approach to managing risks, which is usually tied to intensive discussion (meetings), and also up to difficult consensus finding. On the contrary, we propose a method that is based on questioning experts individually, separately, asynchronously and anonymously, which entails the following features, among well known improvement of the so-obtained data quality [31]:

-

1.

Distributed expert interviews that do not require to be at a certain room at a certain time (no meetings), and thus allow provide input in between the normal workflow (asynchronously to the input of other experts).

-

2.

Since the questioning is done individually, it can be done anonymized. This avoids social or cultural effects that may change a person’s statement spoken out loud in presence of certain other people (superiors, subordinates, etc.)

-

3.

Exploitation of matrix organization: it may well be the case that experts are well informed about certain aspects of a problem, but have no reliable clue on some other aspects. Polling people by online questionnaires in the privacy of their own office allows them to answer only those parts of the survey that they can offer input for, while leaving them a safe way of refraining from answering other questions. Since our method works on probability distributions, the resulting dataset from which these are compiled may be richer or sparser, depending on how many informed opinions are available. In any case, however, asking people face-to-face in a meeting can bring up an uninformed guess just to have said something, so that the overall data quality is not necessarily as good as in a distributed and individual interview.

-

4.

Enlargement of the opinion pool: without the need for a personal (and confidential) meeting, people even outside the company can be included in the risk assessment. For example, matters of reputation can more reliably be assessed by customers (which are typically not invited to internal management meetings).

-

5.

The use of distributions also avoids problems of consensus finding or opinion pooling (see, e.g., [20, 5] to mention only two out of many publications in this area) towards a representative number. It is in that sense preserving all information, since all opinions (all available data) goes into the decision process with equal weight.

As a final pro that a game theoretic risk assessment allows, it is even possible to offer the game solution algorithms as a webservice, where the modeling and threat assessment can be left to the customer enterprise. For example, if the client has identified a set of threats and countermeasures, it will prefer to not disclose this information to a subcontractor in charge of risk management. Since the game model and solution can be formulated using abstract names only, it is possible to anonymize the data by letting the threats be only named “T1”, “T2”, …, “Tn”, as well as the countermeasures be called “C1”, “C2”, …, “Cm”. The real meaning of threats and countermeasures can then remain private information of the company, whereas the game model being given in terms of these abstract identifiers remains solvable by any third party contractor. This allows the method to be offered as a (web-)service, without running into troubles of unwanted information disclose (even the number of threats and countermeasures can be disguised, if a company adds dummy copies of actions to the list to make it longer than it actually is).

2 Game-Theory based Risk Management

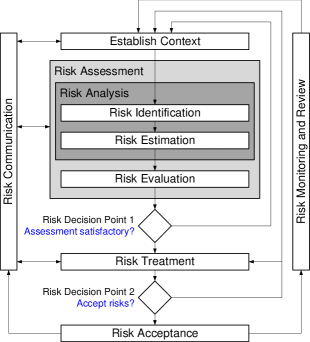

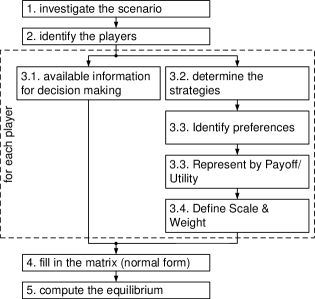

An eloquent and detailed comparison of how game theory fits into and aids the classical risk management process has been given by [34]. We follow their presentation hereafter, while instantiating and adapting the specific steps to the concrete setting outlined in the precursor parts to this work [35, 37].To get started, consider the classical ISO risk management process as depicted in Figure 1, and compare it to the workflow to be completed when a game-theoretic model is to be set up; shown in Figure 2.

The workflow in Figure 2 needs some explanation, in order to establish a mapping to the risk management process. Perhaps the most important difference between risk management and game theory is the former being about minimization of losses caused by a not necessarily rational opponent (nature, but possibly also a hostile party that has explicit intentions). Contrary to this, game theory in any case assumes a rational opponent, whose goal is maximizing the own revenue. A conflict/competition arises if the revenues for both players are negatively correlated, in the extreme case culminating in the well-known zero-sum competition, meaning “my gain is your loss” (and vice versa). This is the scenario that we also assume for risk management based on distribution-valued game theory, although bearing in mind that the incidents that the risk management refers to may not always follow a hidden rationale or agenda. Nevertheless, the zero-sum assumption (even though perhaps unrealistic) provides us with a valid worst-case assessment, and reality can only look better than predicted for the risk manager. The players engaging in the risk management process may be diverse and many, depending on the variety of threats to be considered. In mapping this to a game-theoretic model, we collect all physically existing opponents into a single adversary acting as “player 2”, against the risk manager, which is player 1. As for the adversary, “player 1” is here an abbreviation and means the entirety of people engaged in the practicalities (“do”-phase of the ISO PDCA-cycle) of the risk management. We will hereafter call this player the “defender”, to ease our wording. Specifically the “do” phase is the one where game theory can help, since it requires:

-

•

The selection of controls: this is an action undertaken in the final “risk treatment” phase in Figure 1, and the point where game theory is applied.

- •

-

•

The definition of measures to check their effectiveness: the measures per goal are the assurances defined in [35, Def.4.1].

So, all these actions can be supported by game theory. To make this precise, let us look at the steps numbered in Figure 2, and to be completed for each player:

- 3.1:

-

each player has some a-priori or current knowledge when a decision is made. In classical game theory, the next action depends only on the current state of the game (in a generalization to stochastic or sequential games, a dependency on past game iterations is included; we discuss one such example in Section 5.1). In the reality of risk management, external need to be considered, and the player’s action is hardly dependent on the current state of the system only (at least because the system state may not even be known precisely at all times). For this reason, the theory developed in [35],unlike classical game theory, allows uncertainty to be explicitly modeled at this stage, and incarnate through the payoffs of an action that we describe below.

- 3.2:

-

strategies for a player refer to everything that can be done in the current position. In fact, if the game play covers several stages until the payoff is received, then the strategy is an exact prescription of what is to be done at each step. In that sense, it is comparable to a “recipe” that the player can follow to accomplish the desired goal. Mapping this to a practical setting, the strategy may be named “patch machine X”, whereas its details relate to all the steps taken from the current state of machine X until the point where the patch has been installed and the machine is put back to work. Likewise, a strategy for the opponent (player 2, adversary) may be high-level named “hack machine X”, where the details of this strategy may include a sequence of steps such as “sending a phishing mail” “connect to the malware” …

- 3.3:

-

Identify the interests of a player and define measures of “fulfilment” of these needs. In our case, this process refers to the identification of goals that are object of the risk management. Examples include (but are not limited to): economic, reputation, people, information, capability, etc. (see [45]). The degree of achievement in each of these goals must be measured on a scale that makes the different goals comparable, and – for technical reasons – also arithmetically compatible. The easiest way of assuring this is to define a common set of discrete risk categories, with individually specific meanings per security goal. This has several advantages beyond pure theoretical reasons, as it “equalizes” the understanding of risk valuations and the taxonomies in which risk and outcome of actions is expressed. This is the fundament to the next step 3.4.

- 3.4:

-

Preferences of the players are found by asking how the players valuate an outcome. For general games, this has to be done for each player. In our case (and every zero sum game), it suffices to ask only player 1 (the defender) for this valuation, in each scenario. By construction, we specifically allow an outcome of a specific scenario of strategies for the defender and the attacker to be rated in various respects, i.e., in terms of each security goal. Having a common vocabulary (set of risk categories) in which the risk in each goal is expressed, the underlying theory of multi-criteria optimization meaningfully applies and helps optimizing the actions towards maximizing the security goal fulfilment (equivalently, minimize the residual risk).

- 3.5:

-

the representation of preferences by a utility function is –in classical game theory – done by specifying a function for the -th player, so that each scenario of defense (action from the list of available options) and attack (action from , i.e., possible exploits) is rated in some real-valued score. The construction in [35]deviates from this definition in allowing the outcome to be not crisp but a random probability distribution, thus the function takes the form , where is the set of all probability distributions (more precisely their density functions) that satisfy the regularity conditions (lower bounded by 1, absolute continuity w.r.t. Lebesgue or counting measure; see [35]). The crux of this modification is that:

-

•

Letting be valued in terms of probability distributions offers a powerful model to capture uncertainty (cf. our remarks in step 3.1 above).

-

•

The specific definition of can be made based on empirical statistics; that is, we can simply collect many domain expert opinions on a specific scenario from , and define the value as the empirical histogram of this expert survey (we expand this approach below in section 3.3). This has a neat effect, since it:

-

–

Preserves all information provided by the experts

-

–

Avoids a consensus problem that would normally arise from the need to agree on a single representative opinion about the risk. In practice, people may be unsure and disagreeing to the opinion of others, so that conflicts and aggregation of opinions may be required. In letting the risk valuation be an entire histogram, each input goes into the assessment with the same weight, so that no domain expert is “overruled” or has less influence than any other.

If the system response dynamics is known, on the other hand side, then there may not even be a need to poll experts, and a simulation of the outcomes under the specific scenario could be imaginable. Percolation theory [22] offers one way to do this (among other possibilities).

-

–

-

•

In assuming a zero-sum competition and a two-player game, the risk management process outlined here is asset-centric. This is an important core philosophy of the entire process, since the overall goal is not about preventing all possible threats, but about making an attack non-economic for the attacker. This is the main point of applying optimization (i.e., game theory) here, since we seek to minimize our own losses (measured in terms of the values of our assets), against whatever an attacker may do.

| ISO/IEC Process/Terminology | Game theoretic step/terminology | |

| Context establishment | Setting the basic criteria Defining the scope and boundaries Organization of an information security risk management (ISRM) | Scenario investigation (scope definition and asset identification) Player identification (mostly assigning the role of the defender). |

| Risk identification | Identification of assets | Included in the scenario investigation |

| Identification of existing controls | Identify implemented controls, i.e. “do nothing” option for the defender. | |

| Identification of vulnerabilities | Options that can be exploited by threats. Included while determining the strategies of the attacker (player 2). We denote this list as . | |

| Identification of consequences | Identify how players value multiple aspects of outcomes. Identify preferences (i.e., priorities among different security goals) | |

| Risk estimation | Assessment of consequences | Define a common scale and ranking scheme for all relevant outcomes. |

| Assessment of incident likelihoods | Computed likelihoods for each strategy for both players. | |

| Level of risk estimation (list of risks with value levels assigned) | Expected outcome for each scenario. This expected value (a real number) is in HyRiM replaced by an entire distribution function (thus avoiding information loss due to a “representative” centrality measure like the average). | |

| Risk evaluation | List of risks prioritized | Prioritize the expected outcome for both of the players |

| Risk treatment | Risk treatment options are risk reduction, retention, avoidance and transfer | Strategies (control measures) for the defender can be categorized into “static” (changes applied to the system that have a permanent effect, e.g., installation of intrusion detection systems) and “dynamic” (actions that need to be repeated in order to retain their effect on security, e.g., security awareness trainings). The entirety of controls available is denoted as . |

| Residual risks | Expected outcome of the game. In HyRiM, this is the equilibrium value distribution, from which all statistically meaningful quantities can be computed. For example, the mean of this outcome distribution would correspond to the classical quantitative understanding of risk as the product of likelihood and impact. Since HyRiM admits multiple goals to be optimized at the same time, the residual risk is returned per security goal. The theory coined this output artefact “assurance”, and it is one probability distribution for the losses in each relevant security goal. | |

| Risk acceptance | List of accepted risks based on the organization criteria | Strategies of the defender (based on the organization criteria) |

| Risk communication | Continual understanding of the organization’s ISRM process and results | Strategies of the defender |

| Risk monitoring and review | Monitoring and review of risk factors Risk management monitoring, reviewing and improving | The process is repeated as the player’s options and their outcome valuation may change |

| not included | Information gained by the opponent | |

| not included | Beliefs and incentives of the opponent | |

| not included | Optimization of the strategies | |

The mapping sketched in Table 1 has been adapted from [34], but needs a bit of tailoring towards defining an analogous process based on distribution-valued games (and the theory thereabout). Specifically, the risk assessment phase (Figure 1), comprising risk identification, risk estimation and risk evaluation, refers to the current state of the system, whose valuation may trigger further action (implementation of controls) in later phases of the process (namely the risk treatment).

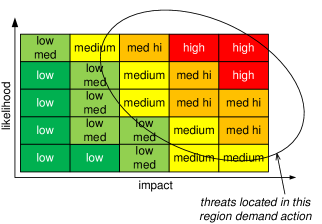

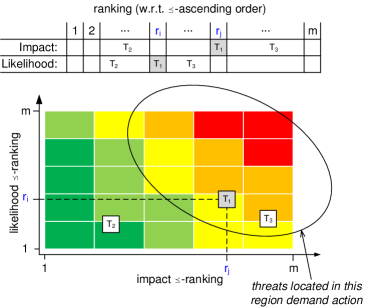

In Table 1, the process of determining the current state is only briefly mentioned as adding a strategy “do nothing” to the game, which merely models the possibility of the situation at hand being satisfying already. Here, we will resemble the classical process of risk management to a wide extent using only the idea of an outcome valuation in terms of probability distributions, which is made possible by the -ordering on these objects that was invented in earlier stages of the project. This extends up to the point where risks are evaluated, which is normally done using a 2-dimensional risk matrix, typically with colored entries like shown in Figure 3. The (specification of the) elliptic region displayed on the upper right corner is the main output of the risk evaluation, which establishes a priority list of risks and divides the threats into those that demand action (i.e., which are put into the critical region based on their impact and likelihood) and those who do not demand immediate actions (i.e., which lie outside the critical region).

In the original ISO/IEC process, the risk value is computed as the product . It is popular to define a categorical scale for both, the likelihood and the impact (in tabular form explaining what exactly is meant by a “medium likelihood” or a “medium impact”; section 3.8 gives examples). Multiplying the ranks (i.e., category numbers111it is advisable to avoid using the number zero as a category number or rank, as it would cancel out any rating in the other aspect. Indeed, we have adopted such an assumption quite explicitly already by declaring loss random variables (or categories) to be in any case; see [36].) then gives the risk score and delivers the coloring of the risk matrix as exemplified in Figure 3. Note that loss valuations based on crowd sourcing (expert surveys, detailed in section 3.3) in fact embody both, the impact (as is directly asked for), and the likelihood (as the relative frequency of answers provided by the set of experts polled) in one object. That is, the classical two-dimensional matrix depicted in Figure 3 would boil down to a 1-dimensional list of threats, which can plainly be sorted in -ascending order. Thus, the risk evaluation is even simplified in our setting here. It may nonetheless be advisable to resemble the classical process of risk management a little closer by asking for both, the impact and the likelihood, and construct empirical distributions for both. This may be useful in letting the expert express his beliefs more detailed than just asking for a possibility (and not for a probability too). We revisit this issue later in section 4, after having established the basics of this process first.

In generalizing this classical approach to risk management to a more sophisticated technique based on games and distributions as risk representing objects, our main target in the next section will be modeling the losses as probability distributions, and how to prepare the game theoretic models for the risk treatment phase, when the games are to be solved and “played” in practice. We will exemplify the modeling based on two examples, which are advanced persistent threats (APTs), covered in section 5.1, and social engineering, discussed in section 5.2. Once the cycle in Figure 1 has been completed for once, any repetition entailing another round of risk estimation and risk evaluation can be supported by exactly the same kind of game-theoretic models that were used in the previous risk treatment phase (in fact, the equilibrium strategy enforced as result of the last risk treatment phase is the “do nothing” strategy in the next risk assessment; cf. Table 1). Examples of potentially suitable models are described in the sections to follow. Section 6.3 discusses how to use the game analysis results for effective improvements and control selection.

3 Modelling Losses

The proposed method of risk modeling is here based on non-parametric loss models, for their conservation of information and absence of perhaps difficult to verify assumptions. Nonetheless, actuarial science knows important applications of parametric loss models, which we briefly discuss in the next section.

3.1 Parametric Loss Models

The weight of a distribution’s tails is what makes it (in)appropriate for risk management, where distributions with heavy, fat or long tails are common choices. In the continuous case, extreme value distributions (Gumbel, Frechet or Weibull) are suitable choices, as well as stable distributions. The latter, despite not having analytically expressible densities except for special cases, can nevertheless be ordered upon using sequences of truncations or moment sequences (if they exist) [37].

In the discrete case, the or class of distributions may be considered, with a density in the former class being defined recursively as for . The class is – roughly speaking – the truncated version of an -density excluding the possibility of the event . It can be shown that the former class includes exactly three families of distributions, which are Poisson, Binomial and the Negative Binomial distribution.

A general issue with parametric losses is their representation of an arbitrary amount of information by a fixed number of parameters. This inevitably incurs a loss of information, and calls for partly sophisticated methods of parameter fitting or similar. On the contrary, nonparametric losses like (the previously proposed) kernel densities come with the appeal of preserving all information upon which they are constructed, as well as offering the flexibility of allowing for adjustments to model uncertainty in the expert’s answers more explicitly. An example of this will be sketched in section 3.7.

Nonetheless, if a parametric model should be used, then one should bear in mind that risk is intrinsically a latent variable, and the best we can do is relate it to some observable variables. Unfortunately, the usual assumptions on the latent variable being dependent on the hidden variable, so that an inference towards risk is possible, may not directly apply to a risk assessment process. Risk is a property of some general entity, action, intention, or similar. As such, subjective assessments of it are made by humans whose risk perception may be correlated (to a degree that depends on the skill level of the person in the respective regard) but not directly influenced by the true underlying objective value of the risk variable. Still, algorithms like expectation-maximization [27] could (and should) be assessed for the extent to which they can deliver a useful risk model. Indeed, the result of an EM-algorithm being a distribution model over latent variables together with a point estimate on its parameters is a perfectly suitable input for the decision models put forth in the precursor parts of this report.

3.2 Nonparametric Loss Models

Parametric models come at the cost of information loss due to representing the entire data by a (preferably small) set of parameters to the distribution. This is the price for analytic elegance and the ease of many matters related to working with such models practically.

In light of the scarceness and inconsistencies in the data to be expected in a risk management application, we may thus look at nonparametric loss models as a potentially interesting alternative. The method of choice here will follow the proposals made in [37].Specifically, we will start from an empirical distribution compiled from expert interview data, and use a kernel density estimator for our loss model. Moreover, we will focus on discrete risk assessment scales, which lead to discrete (in fact categorical) empirical distributions. For a kernel density estimator in this context, it is somewhat surprising that the literature is unexpectedly thin on discrete kernel density estimates. Besides only a few proposals found in [33, 24, 6], the problem of “good” kernel density estimation seems to be as much of an art (on top of science) as it is in the continuous case. Hence, we will continue defining our own discrete kernel proposal based on Gaussian densities, but postpone the details until later, when we have specified the process of data collection, which obviously goes first.

3.3 Collecting Data from Experts

As for every empirical study, the first step is fixing the details of the scenario about which experts are to be interviewed. In our context, this may entail the identification of a particular threat and related countermeasures. The high level description of a threat, say “unauthorized access to server ”, must here be followed by a sequence of possible detailed suggestions on how the respective attack could be mounted. For the aforementioned example, possibilities include the exploitation of (known) vulnerabilities (up to zero-day exploits) in the server itself, social engineering, theft of access credentials, or similar. Normally, each of these possibilities is matched with a respective countermeasure. Risk management standards like ISO 27000 [17, 15] or related ones [4] provide an indispensable source of threats and countermeasures, which can be used in this step.

Abstractly, let us think of this process having brought up a list of countermeasures, opposing a list of possible threat scenarios (the acronym means “pure strategy”, as a reminder that we are approaching a game-theoretic model here).

The lists and can be assumed to be quite short (though they must be comprehensive; ideally exhaustive) in practice, and each scenario of “defense ()-vs-attack ()” can be put to its own individual review (not necessarily independent of other scenarios, but the design of questionnaires and the amount of context specification in there is a different and nontrivial story of empirical science not subject of this report).

Remark 3.1 (Simultaneous Occurrences of Multiple Scenarios)

Note that the modeling so far implicitly prescribes the assessment to be done relative to a specific single threat. This restriction can be dropped in presenting the expert a set of threats and explicitly allowing for several of them to occur at the same time. At first glance, this would exponentially enlarge the list , this combinatorial explosion can be avoided by allowing the expert to name multiple possible loss categories with different likelihoods. That is, the expert may center the thoughts around a specific threat, but may take further considerations of coincidental other incidents into account in saying that, for example,

-

•

losses of category are most likely,

-

•

while losses of the larger category remain possible if two or more incidents occur at roughly the same time.

If several such possibilities are uttered, they are most conveniently described by a distribution supported on (at least) the anticipated loss categories and .

To set up the empirical game theoretic model, let us therefore assume that one scenario has been specified in detail, say (for illustration)

| : | perform periodic updates |

| : | exploit some software vulnerability |

It goes without saying that this specific (example) scenario appears (if at all) in the middle of a real-life APT, as the earlier stages are usually matters of social engineering to make an initial contact and infection. We will go into details of this in section 5.1, and keep our example abstract here only for the sake of illustration.

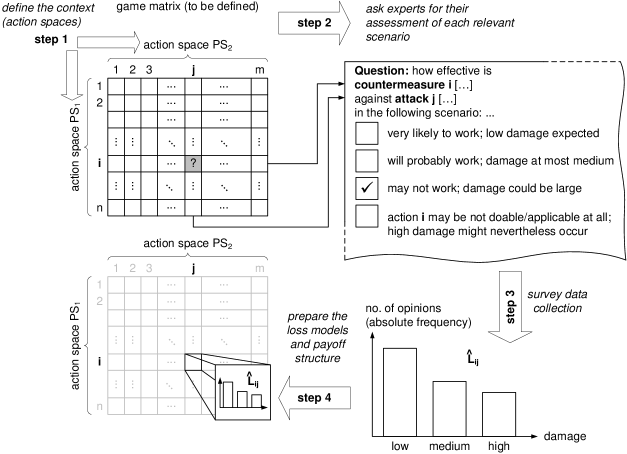

The goal of data collection is getting a payoff matrix composed from loss distributions that can be used with the game theoretic framework defined in the preceding reports [36, 37].Figure 4 displays the workflow to fill in one cell in the payoff matrix, which is basically done along four steps:

-

1.

Selection and specification of a scenario as a questionnaire presentable to experts (the wording and style of the questions is itself a highly nontrivial matter, and should be done w.r.t. the subsequent implementation strategy for the optimal defense. We will revisit this issue later in section 6.5),

-

2.

Doing an expert survey on the effectiveness of countermeasure against attack . It is crucial for this survey to clearly define at least the following items:

-

•

the context of the risk assessment (that is, the aspects that are relevant and those that are irrelevant for the risk assessment)

- •

-

•

-

3.

Collecting as much expert input as possible to define an empirical loss distribution over the categories as specified in the survey.

-

4.

Preparing the loss distribution for a subsequent game-theoretic analysis.

The details of step 1 are individually dependent on the application context, i.e., are specific for the system or infrastructure under investigation. This step is recommended to be done according to established standard procedures as described by ISO 27000 or its relatives. Step 2 is a matter of empirical research and questionnaire design. The literature on this is rich, and this task should be left with experienced staff educated in empirical research and statistics. On the technical level, collecting the data is relatively simple, since it is an easy task to set up an online survey, displaying a sequence of questions asking the expert to give her/his risk rating on each described scenario. Things may be even made more efficient by showing the expert the entire matrix, asking to enter a risk assessment in each cell (showing yet another combination of defense and attack), and to leave all fields blank for which there is a lack of domain knowledge or no justified opinion can be expressed.

Step 3 deserves some attention, as this involves an a-priori agreement on the loss categories to be used in the survey. We give details on this in section 3.8.

The final preparation of loss distributions in step 4 is a matter of kernel smoothing, and described in section 3.10.

3.4 Refining the Expert Survey

Note that the expert survey – in the form described – only asks for possibilities and not for probabilities. That is, the expert is only questioned to state an expectation of outcome, rather than telling how likely s/he feels it to be. If the survey is refined to ask for a likelihood in addition (as is prescribed in the conventional ISO/IEC risk management standards), then we end up with two probability distributions, one for the impact, the other for the likelihood. A “multiplication” of these two objects, to resemble the usual formula “risk impact likelihood” underlying quantitative risk management, is theoretically possible (as a multiplication of the hyperreal representatives), but not practically meaningful. If the two distributions are available, then a lexicographic comparison of or may be the more reasonable way to go. However, an explicit advantage of the expert surveys and using distributions as representative objects is them embodying both, impact and likelihoods within the same loss distribution object, thus the expert interviews are greatly simplified over the standard risk management process.

3.5 Outlier Elimination

It is important to note that any survey data should be cleaned from outliers, and there has to be a consensus on the treatment of missing values. Either is up to a variety of statistical methods and the particular method should be chosen in light of the given application.

The discussion here is only meant to bring this point to the attention of the reader, and will not go into details of how this could be done.

3.6 Harmonizing Risk Attitudes

After having cleaned outliers, it remains to “harmonize” different kinds of answers depending on the individual personalities and risk attitudes. Persons known to be risk averse will tend to overestimate the risk, while risk seekers will tend to underestimate. It is beyond the scope of this report to discuss concrete methods to correct risk estimates based on a respective classification of the individual, but it is important to bear in mind methods of statistical classification as a potential toolbox to help in this regard.

3.7 Using the Bandwidth Parameter to Model Answer Uncertainty

In some occasions, it may happen that an expert is unsure about whether or not certain circumstances enable certain damages. For example, if the question of whether an incident at one point in the system can cause damage at another point in the system can be answered with “generally no, except for some rare cases”, then the risk assessment related to the incident will have its modal value at a low category, but – due to the possibility of the incident being nonetheless severe – extends the distribution up to the full range of loss categories. The bandwidth parameter of the kernel density estimate can be increased to let the density put more weight on far away categories, or be chosen smaller when the certainty about the assessment (rareness of the incident), is better. In any case, the choice of bandwidth for the kernel density estimates gains another dimension of importance as being a parameter to control/describe the expert’s certainty in the data.

3.8 Defining Risk Assessment Categories

It is crucial (not only for technical reasons) that all loss distributions for all goals in a multi-goal security game must be defined on the same categories. This can be justified by technical but also interpretative reasons:

- Technical reason:

-

the procedure to numerically compute multi-goal security strategies (MGSS) relies on casting the multi-criteria objective function (vector-valued) into a scalar that is a weighted sum. This transformation requires “compatible” objects to be weighted and added (see [37]), which calls for the same underlying scale in all goals.

- Interpretation:

-

comparing the severity of damages in two security goals is only meaningful if the goals are quantified in the same terms. That is, the understanding of, say “high” damage has to be fixed for all goals, and must not be left to a subjective idea that is individual for each expert (otherwise, the outcome of any such assessment is useless). This is especially relevant for non-numeric goals like the reputation of an enterprise, customer trust, or similar.

Especially to address the latter, it appears advisable to underpin the survey/questionnaire by an a priori fixed definition of categories in which the risk assessment shall be made. This can be done in tabular form where each goal is assigned a column, with rows corresponding to the categories, and cell entries describe the meaning of a risk category specifically for each goal. Table 2 shows an example, whereas it must be stressed that the concrete content of the table must be adapted/tailored to the practical situation at hand.

| risk category (numerical representative) | loss category | |||

|---|---|---|---|---|

| loss of intellectual property | damage to reputation | harm to customers | … | |

| negligible (1) | € | not noticeable | none | … |

| noticeable (2) |

between 500 €

and 10.000 € |

noticeable loss of customers (product substituted) | inconvenience experienced but no physical damage caused | … |

| low (3) | € and 50.000 € | significant loss of customers | damages to customers’ property, but nobody injured | … |

| medium (4) | € and 200.000 € | noticeable loss of market share (loss of share value at stock market) | reported and confirmed incidents involving light injuries | … |

| high (5) |

€

and 1 Mio. € |

potential loss of marked (lead) | reported incidents involving at least one severe injury but with chances of total recovery | … |

| critical (6) | Mio. € | chances of bankrupt | unrecoverable harm caused to at least one customer | … |

Such a table should be displayed together with the survey, to equalize the expert’s individual understandings of the risk categories, and to harmonize the resulting data. The loss categories actually used with the model are simply the integers , noting that the number 0 is precluded as a category (in order not to violate the assumptions made in [36]).

3.9 Using Continuous Scales

If the loss is measured in continuous terms, then a common categorization like outlined above must be replaced by a “meaningful” common (continuous) risk range. The exact definition of “meaningful” must herein be made dependent on the context of the problem, so that all security goals (losses) homogeneously cover the range without being concentrated in disjoint regions. We illustrate the issue with two examples, one showing how it should be done, the other illustrating the problem:

Example 3.2 (well chosen loss range)

Consider two loss variables, with are monetary loss due to theft of intellectual property, and (monetary) investments to protect these assets. Since security is primarily not about making an attack impossible but only about making it non-economic, it can be expected that both losses range in roughly the same numeric region. Formally, let be the two random loss variables, and let be a small value for which we truncate both distributions at their respective -quantiles, denoted as for . Call the so-obtained loss ranges and . If (i.e., ), then we may take the convex hull of as the common loss range, and be sure that the comparativeness of the two loss variables is retained and reasonable.

Example 3.3 (badly chosen loss range)

Let be two random losses with Gaussian distributions. As before, if the modeler chooses the range as the (convex hull) of the union of both (truncated) ranges at some -quantile, the game may be defined over losses within the common range (for , the range covers of the cases for the Gaussian distribution ; our cut off here is at , and thus covers more than ). Since , however, assigns most of its mass in the region , it will always (at least up to reasonable numerical precision) be -larger than , so the optimization is pointless.

To avoid situations like sketched in Example 3.3, (at least) two options are available:

-

1.

Rescaling of all loss ranges to a common region. Continuing example 3.3, this would mean replacing by .

-

2.

Defining a common continuous scale with the same intended usage as the discrete categories. That is, if a continuous loss rating is permitted, we may define it within a common interval from , allowing any value to be picked by the modeler, as long as it is within the range. This may be the method of choice if the modeling interface displays a “slider” where a user can drag the gauge at any position on a continuous scale to express the (subjective) belief about the loss.

3.10 Preparing the Loss Model

In [37], the theoretical possibility of convergence issues in the game’s analysis (by fictitious play) was anticipated, occurring when the loss distributions do not share the same support (this adds to the technical justification stated in the previous section 3.8). Practically, this is highly likely to occur due to missing data. If some categories are simply not being used (either because of an unsuitable definition or because the scale is fine-grained so that not all levels are being used by the experts), then the loss model may be empirically correct, but not useful with a subsequent numeric analysis.

The solution in the continuous case was a kernel smoothing, technically a convolution with a Gaussian density, to extend all loss distributions until a common end of their support (previously called the cutoff point) is reached. We will do the same thing in the discrete case, using a kernel obtained from discretizing the Gaussian distribution. To this end, define as the density of a standard normal distribution, and for every , define the kernel function as

where is the bandwidth parameter (as familiar from continuous kernel density estimates). Obviously, and , so defines a discrete probability mass function on . Moreover, it is easy to see that for every , the function resembles a discrete version of a Gaussian density, so that by letting , degenerates into a discrete Dirac mass,

| (1) |

If we call a general empirical distribution function (defined on any subset of ) obtained from data points (answers in the expert survey). The convolution is another distribution function supported on all , i.e., for all . Moreover, in letting , we have the pointwise convergence for all , so the estimate is asymptotically correct (note that in contrast to Nadaraja’s theorem, we do not even need to assume a specific speed of decay when letting ). This convergence easily follows from (1). The same result equivalently holds if we replace by a truncated version thereof (being supported on for some integer ), leading by disretization to the truncated kernel . In the following, we thus consider the smoothed empirical distribution , noting that this also pointwise converges to and that the support (strictly) covers the full interval . However now, we can make a stronger convergence statement: let be the (unknown) distribution of the loss assessment, which is approximated by the expert data222We somewhat sloppily assume here that the experts provide us with “observations” about the real random loss having the distribution function . This assumption is clearly not correct, but still the best that can be done, given that we cannot simply wait for losses to occur, as this would probably kill the enterprise much before a decent lot of data about the true loss distribution could have been obtained. Thus, we have to live with overly trusted experts providing us with “objective” samples of the unobservable loss variable distributed like ., which is . We can write

| (2) |

To the first term, we can apply a uniform bound thanks to the supports of and being all finite, which is

as is an easy consequence of the equivalence of all norms on . The other term in (2), we can apply Glivenko-Cantelli’s theorem to conclude the convergence

so that in the limit and . Note that this argument is only good for plausibility of our approach, but cannot be taken as a proof of correctness, since practically, it still relies on an infinitude of data, which – more crucially – must be objectively sampled from the real loss variable (having the distribution ).

On the bright side, however, the proposed smoothing enjoys a nice intuitive justification as accounting for uncertainty in the assessment.

Example 3.4

Suppose an expert utters the opinion that, on a scale from 1 to 5, the risk is 3. Despite that a middle assessment is an implicit statement of uncertainty already333This is usually avoided by choosing a risk scale with an even number of categories to avoid having the median on the scale., there statement “the risk score is 3” is not equivalent to the statement that the risk cannot be anything else. In other words, there may be admitted chances of the damage being higher or lower than the average told by the expert. To express such uncertainty more detailed, the expert may admit possible outcomes on the entire range , with the initial assessment being just the most confident outcome.

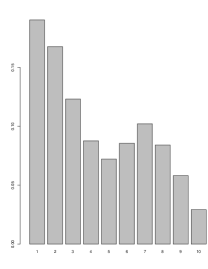

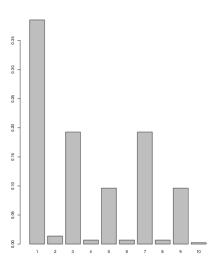

Of course, it will not be feasible to ask experts to provide entire probability distributions over a scoring scale, but the smoothing of the empirical distribution by convolution with achieves the same thing. Viewing as a set of weights associated with all possibilities around the mean value , the expert assessment receives the maximal weight (as being the modal value of ), whereas all other possibilities receive a nonzero weight that decays with the distance to the value . Graphically, this process thus “fills” all empty bins in the empirical histogram (say, if a category has never been assigned during the expert survey), and additionally extends the distribution up to the full and identical support for all loss distributions. Hence, besides satisfying the technical constraints imposed, the smoothing naturally accounts for the uncertainty in the assessment; the lower the parameter is, the more confident we are in the assessment (i.e., the closer the smoothed approximation approaches ). Figure 5 displays an example of the original empirical histogram (Figure 5c), and its smoothed version with , having its gaps filled in by the superposition of smoothing kernels (expressing the uncertainty around the modal values given in Figure 5c), and another smoothed version of the histogram with a much smaller bandwidth parameter . This plot visually illustrates (confirms) the formal claim of convergence as stated previously.

The quality of the kernel density estimation, as in general with this nonparameteric method, is the art of choosing the bandwidth parameter . Various rules of thumb (e.g., Silverman’s rule [43]) or cross-validation techniques may be applied. Since there is no generally “best” way to choose this parameter depending on the information at hand, we refer to the literature on nonparametric statistics for concrete methods [49, 47, 8].

4 Risk Prioritization

Let us assume that a total of m threats has been identified. If, say , experts provide their input on the impact and likelihoods (both artefacts obtained by surveys as outlined in section 3.3), then it is a simple matter to compile an empirical histogram (a distribution ) for the impact and another empirical histogram (a distribution ) for the likelihood. In doing so for every threat , we end up with such distributions, which we denote here as for the -th threat in the list. To resemble the risk matrix familiar from the standard process of risk management, we can use the -ordering on the distributions (remember that it is a total order), to separately sort the threats in ascending -order according to their impact and likelihood. This gives two lists, in which each threat gets a rank assigned among the total of threats, say the -th threat has rank on the impact ranking and position on the likelihood ranking. The risk matrix familiar from the ISO processes (cf. Figure 3) is then re-established by placing each threat into a 2D-coordinate system with the -coordinate being the rank on the impact scale and the -coordinate being the rank on the likelihood scale. This puts each threat to a particular position on the grid, and we may then proceed “as usual” by coloring the area as we would do for a normal risk matrix. Likewise, the “critical region” can be defined as the area inside which threats fall that need to be addressed by the subsequent risk management process. Figure 6 displays an example.

The main difference to the standard risk matrix is herein twofold:

-

1.

While a standard risk matrix has axes scaled in categories, the so adapted risk matrix has axes scaled in ranks that go from 1 to the total number of threats.

-

2.

The consensus problem of assigning a threat a single quantification in terms of likelihood and impact is avoided. Since many experts can utter disagreeing opinions, all of which go into the impact- and likelihood-distributions and with equal importance. The total ordering then assures somewhat like a “base-democratic” ranking, since one threat outranks the other in the -ordering, if more people classify the impact, respectively the likelihood, as high (see [37] for the full detailed effect of this ordering).

If the assessment considers multiple criteria, say, if the impact is not only measured in money but also in reputation, then the respective assessments are made separately (not necessarily independently) from one another. For the example of budget-impact and reputation impact, we could think of the one distribution as being replaced by two new distributions and (for budget and reputation). Likewise, if two threats have assessments in these terms, given as and , then we ought to rank the two in terms of two criteria. A canonical way of doing that is offered by defining a game with two goals (“budget” and “impact”), and using one (dummy) strategy for player 1, and letting the two threats being the strategies for the opponent (player 2). It is, however, important to stress that we cannot directly go ahead and set up a multi-criteria -game to get the most severe threat via an equilibrium, since the gameplay is defined to be among players, where each opponent (corresponding to a goal) plays independently of all others. The equilibrium would then return a worst-case threat identified per goal, which is possibly not what we seek here for a multi-criteria risk optimization. The theory, however, remains applicable when the game is reduced to a two-player game with scalar(ized) payoffs per player. In that case, the equilibrium is necessarily pure and indicates the worst case threat for player 1. The R package implements this method in a designated procedure preference:

# ranking if there is only one goal (say, FBI1, vs. FBI2) > preference(FBI1, FBI2) 2 # this means that the second parameter (FBI1) is preferable # ranking, if there are multiple goals (of equal importance) > preference(list(FBI1, FRI1), list(FBI2, FRI2)) # Let us assign twice as high priority to the "reputation" # goal by supplying the parameter weight=c(1,2), i.e. "goal" has # priority 1, and "reputation" has the (double) priority 2. > preference(list(FBI1, FRI1), list(FBI2, FRI2), weights=c(1,2))

The results directly gives the desired ranking by telling that either the first (output “1”) or second (output “2”) threat is less severe; if the function returns zero, then the distributions are identical and the decision is indifferent. For three or more threats, the procedure can be repeated pairwise to rank a whole set of threats in the way as described above.

5 Examples of Game-Theoretic Modeling

5.1 Modeling APTs

The investigation of many examples of advanced persistent threats (APTs) reported in the past reveal a common structure underlying an APT, even though the details thereof may be highly different. Quoting the taxonomy of [7], an APT roughly proceeds along the following steps:

-

1.

Initial infection:

-

(a)

reconnaissance: information gathering,

-

(b)

development: design of a made to measure malware,

-

(c)

weaponization: preparing the trojan and droppers,

-

(d)

delivery: transmission into the victim infrastructure, e.g., by a phishing email, or similar.

-

(a)

-

2.

Learning and propagation: repeated sequence of

-

(a)

exploitation: to get deeper into the system

-

(b)

installation: to leave artifacts and backdoors for an easy return later, and destroy footprints of the attack

-

(a)

-

3.

Damage:

-

(a)

command and control: interaction with the victim system’s compromised resources via previously left artifacts

-

(b)

actions on the target: causing the actual damage

-

(a)

The specific actions taken in each of these phases depend on the target infrastructure and no general description is possible due to the diversity of such infrastructures. However, specific examples can be “read off” reported prominent incidents, such as including Stuxnet [10], Duqu [2], Flame [28], and Aurora [23]. A common element in all these appears to be the human factor, which we discuss separately in section 5.2.

Game theory has been applied in various ways to model attacks and cyber risks [25, 9, 50] and proposals (independent of game theory) include moving target defenses [19, 18], trust mechanisms [48], and defense-in-depth techniques [30]. Here, we will review a recent proposal to model APTs as a sequence of games, each of which is tailored to the specific nature and details of the respective phase.

That is, an APT usually begins with a harmlessly looking email or “lost” USB stick, on which malware enters the system. Alas, nowadays attackers have joint forces into an entire illegal business sector covering the entire supply chain of cyber crime in a spectrum of independently offered services (often referred to as “cybercrime as a service” in alignment to cloud computing terminology). This means that the person identifying a weakness is not necessarily the same who is writing the exploit for it. Likewise, the author of the exploit kit is not necessarily applying it anywhere, but merely sells it to the actual attacker. Similarly, infections with malware are not automatically intended to cause immediate damage. The term “botnet-as-a-service” describes the business model of infecting a large number of machines and offering to deploy malware on these zombies upon request and for a (smaller or larger) fee. In this way, the attacker can simply “buy” access to a potentially large number of infected machines instantly. For the victim, this has the unpleasant effect of the infection remaining stealthy and inactive, until some time later, when the outbreaks causes noticeable damage. At this time, however, it is most likely that no connection between a past email and the current incident is recognized. The exact time window between an infection and its activity is also dependent on the technical countermeasures adopted in the specific company. For example, signature-based malware recognition (like classical anti-virus software used to work) may take a couple of days until the malware is recognized as such and the respective signature is shipped with the next update. On the contrary, cloud based malware detection that is based on recognizing a huge lot of “identical” email (attachments) suddenly flowing through the internet can have a much shorter time (even a few hours) until a malware is suspected and classified. So, the time window between the infection and the exploit may, in some cases, be closed quite fast (by a good malware recognition system).

To model a so-structured APT in terms of games, the first step is listing all potential ways into the system, such as include (but are not limited to):

-

•

(spear) phishing, whaling,

-

•

waterholing,

-

•

tailgating,

-

•

etc.

The entirety of these possibilities makes up the set of strategies for the attacker. Typically, an entry in is thus not constrained to have a specific form or structure (in particular, an element is not a purely mathematical object but rather a description of how an attack would be launched according to this particular strategy ).

In a different view, can be considered as a list of threats, to which corresponding countermeasures can be defined (appealing to catalogues found in standards like ISO 27000, etc.). The list of countermeasures is .

Note that and should be defined bearing in mind the steps and structure of the first phase of the APT, which comprises information gathering, development, weaponization and delivery. Consequently, example defense measures in may relate to periodic (and random) re-configurations of the system in order to thwart the attacker’s respective next steps, either by invalidating so-far collected information or by removing malware by coincidence, say if a computer is reinstalled or privileges of the victim user have changed (were revoked).

In any case, let the game describing the initial infection be a matrix game (where the subscript is a reminder of this being the first phase of the APT). It appears fair to let this be a matrix game (static and repeated), since if the game is expectedly repeated either in case of an attack failed, or to infect further parts of the system, if an attack was successful.

Let the equilibrium computed for the infection game be the pair of distributions ), where the optimal defense against the initial infection is the distribution (the distribution , more specifically, its probability mass function can be taken as a non-unique indicator set of neuralgic points in the infrastructure).

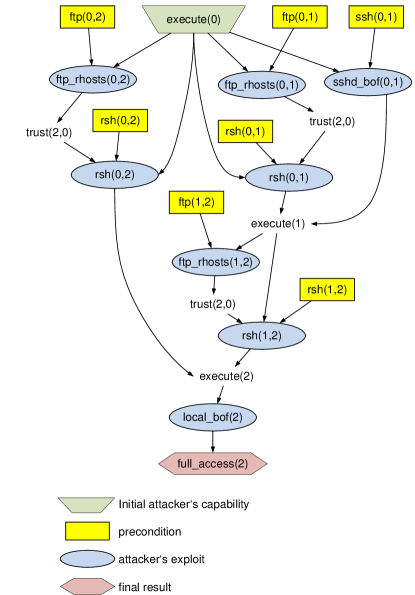

To model the next phase of learning and propagation, we divide the (physical) infrastructure in stages that the adversary needs to reach one by one in order to get to the inner target asset. If the infrastructure is a network graph , then the target asset may be a(ny) fixed node , and the -th stage can (but does not need to) be defined as the set of nodes at distance to the node . That is, the stages are “concentric circles” around the asset, and on each stage, the adversary plays a (different) game to get to the next stage. A single such stage is penetrated by the aforementioned steps of exploitation and installation, continuing with exploitation again on the next stage (only in a different setting there). This modeling is practically supported by topological vulnerability analysis (TVA), which can cook up an attack graph for an infrastructure. In the following, we will illustrate our thoughts based on Example 5.1.

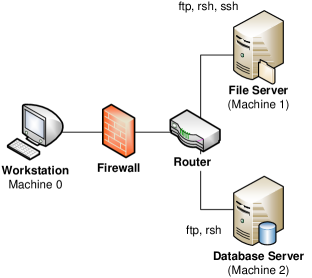

Example 5.1 (based on [44]; see also [40])

Consider a system as shown in Figure 7b, composed from three devices, with various ports opened and services enabled.

Based on this information, the attacker can consider several exploits, such as:

-

•

FTP- or RSH-connections from a node x to a remote host y, hereafter denoted as ftp_rhosts(x,y), and rsh(x,y), respectively.

-

•

a secure shell buffer overflow at node y, remotely initiated from node x, hereafter denoted as sshd_bof(x,y).

-

•

local buffer overflows in node x, hereafter denoted as local_bof(x).

Each of these may establish a trust relation between two nodes x and y, which we denote as trust(x,y). The list of attack strategies to penetrate all the stages until full_access to machine 2 is a matter of plain path enumeration in the attack graph, whose results are shown in table 4.

| 1 | execute(0) ftp_rhosts(0,1) rsh(0,1) ftp_rhosts(1,2) sshd_bof(0,1) rsh(1,2) local_bof(2) full_access(2) |

|---|---|

| 2 | execute(0) ftp_rhosts(0,1) rsh(0,1) rsh(1,2) local_bof(2) full_access(2) |

| 3 | execute(0) ftp_rhosts(0,2) rsh(0,2) local_bof(2) full_access(2) |

| 4 | execute(0) rsh(0,1) ftp_rhosts(1,2) sshd_bof(0,1) rsh(1,2) local_bof(2) full_access(2) |

| 5 | execute(0) rsh(0,1) rsh(1,2) local_bof(2) full_access(2) |

| 6 | execute(0) rsh(0,2) local_bof(2) full_access(2) |

| 7 | execute(0) sshd_bof(0,1) ftp_rhosts(1,2) rsh(0,1) rsh(1,2) local_bof(2) full_access(2) |

| 8 | execute(0) sshd_bof(0,1) rsh(1,2) local_bof(2) full_access(2) |

A selection of respective countermeasures is given in table 4.

| countermeasure | comment |

|---|---|

| deactivation of services (FTP, RSH, SSH) | these may not be permanently disabled, but could be temporarily turned off or be requested on demand (provided that either is feasible in the organizational structure and its workflows) |

| software patches | this may catch known vulnerabilities (but not necessarily all of them), but can be done only if a patch is currently available |

| reinstalling entire machines | this surely removes all unknown malware but comes at the cost of a temporary outage of a machine (thus, causing potential trouble with the overall system services) |

| organizational precautions | for example, repeated security training for the employees. These may also have only a temporary effect, since the security awareness is raised during the training, but the effect decays over time, which makes a repetition of the training necessary to have a permanent effect. |

The game to model the penetration can then be defined per stage by defining the machines 0, 1 and 2 as stages, where machine 2 is the inner assert (node in our previous wording), and a stage is the game played to establish a trust relation between a machine at distance and one at distance to machine 2.

In the (quite simple) infrastructure of Figure 7a, the stages would thus be:

-

•

stage 1 (distance 1 to machine 2): {router}

-

•

stage 2 (distance 2 to machine 2): {file server (machine 1), firewall}

-

•

stage 3 (distance 3 to machine 2): {workstation (machine 0)}

The game played at stage 3, accordingly, has strategies equal to all exploits that can be mounted on the workstation (machine 0), which can be read off the TVA attack tree (Figure 7b) as ftp_rhosts(0,1), ftp_rhosts(0,1), sshd_bot(0,1)}. The corresponding set comprises all countermeasures that can be implemented (such as virus checks, temporary disabling of services, but also non-technical ones like repeated security training, etc.). The strategy spaces and identified in this way then define the shape of the respective 3rd stage game , whose payoff structure is to be defined following the procedure outlined in section 3.3; Figure 4.

The games for the other stages are constructed analogously.

Given a game for each stage, we can connect them into an overall model for phase two of the APT by adopting a high level perspective. In each stage, the adversary has basically two options, which are:

-

1.

penetrate: this means launching an attack as identified based on previously gathered information (cf. example 5.1), or

-

2.

stay, to collect more information while remaining stealthy learning.

Both options can be modeled using their own (distinct) game models, and the connection between the games over all stages is established by considering that in the -th stage game (whether we go for penetrating or staying), the outcome is one of the following:

-

•

if the attacker decides to penetrate, then

-

–

it may succeed, in which case it enters game , or

-

–

it may fail, in which case it has to repeat game once more.

-

–

-

•

if the attacker decides to stay, then

-

–

it may succeed and gain further information, but this leaves the attacker in this stage ,

-

–

it may fail, in which case the overall game terminates, and the entire investment of the attacker is lost (we model this as a negative gain for the attacker).

-

–

Likewise, the defender has the option of defending (without any guarantee of the defense being successful), or not defending. The latter strategy is implicitly played whenever the defender “pauses” in its defense, say, if the security guard is being sent elsewhere and misses the attack by this unfortunate coincidence. In any case, “do not defend” is never a dominating strategy and occurs only due to resource limitations and the inability to defend everywhere at all times against everything.

Writing for the payoff (to the adversary) in the -th stage, the above modeling yields a zero-sum matrix game structured as shown in Figure 8 (cf. [41]). In this model, we have additional quantities and that depend on the current stage, and quantify the likelihood for each action to be successful. These values can be either defined directly, or themselves be derived as saddle point values of classical 0-1-valued matrix games in each stage (in this case, the risk assessment is done in binary terms only asking the expert for whether or not the attack will be successful).

| penetrate | stay | |

|---|---|---|

| defend | ||

| do not defend |

It is reasonable to assume a circular structure in this game (cf. also [1]), which amounts to a single unique equilibrium, for the following reasons:

-

•

if “defend” is a dominating (row) strategy, then either “stay” or “penetrate” will complete this into an equilibrium, and there is nothing to be optimized by game theory here on this (higher) level.

-

•

if “do not defend” is a dominating (row) strategy, then there is no need to do any active security here, as the infrastructure is already secure anyway.

-

•

if “penetrate” is a dominating (column) strategy, then the obvious best choice is to defend, which again degenerates the game into a trivial matter.

-

•

if “stay” would be a dominating (column) strategy, then there is no need to defend anything, since the attacker is not trying to get to the asset anyway.

In any case, it is a simple (yet laborious) matter of working out the game matrix for each stage, and determine an equilibrium for it (say, using fictitious play as described in [37]). The particular equilibrium obtained for the -th stage is the distribution , telling us the distribution of damage in that stage, accompanied by optimal defenses in this stage (obtained from the game and the inner sub-games played for penetration and to collect information during a stay).

Concluding the idea, the decomposition of the learning-and-penetration phase in the APT life cycle into stages and corresponding games played therein delivers an in-depth defense action plan (individual randomized defense actions being taken on each part in the infrastructure), as well as a higher-level risk assessment that refers to each stage. The distribution for the -th such stage then indicates the likelihood of damage suffered at the -th “protective layer” around the asset of interest.

The final game modeling the Damage-phase of the APT can then be defined similar to the initial infection game , as the attacker may simply try and retry causing damage. The process and steps to identify possible actions and countermeasures must again be supported by special purpose (and application specific) tools and expertise, but the game theoretic treatment and computation of risk metrics remains the same. Thus, we will not repeat the details here.

A Static Game Model for the Penetration Phase

In a more simplified view towards a substitute of the sequential phase two game, a static game model can be considered as an alternative (being easier to model and more efficient to analyze computationally). This simplification is bought at the cost of getting a more coarse-grained model, since the attack and defense strategies are defined more “high-level” and not specific for each stage in the graph representation (of the infrastructure or the attack tree).

As before, we can think of the attacker working its way through the stages, while occasionally being sent back or kicked out if a security officer (perhaps unknowingly) closes some of the backdoors established previously. The pure strategy set for the defender is thus the set of all nodes/components in the system on which spot checks (e.g., malware scans, configuration changes, updates, patches, etc.) can be done. Different to the per-stage game modeling from before, the defenses now correspond to high-level attack strategies that describe only techniques but are not specifically tailored to a particular machine. That is, would be composed from a more generic set of threats like

-

•

buffer overflow exploits,

-

•

cross-site scripting,

-

•

code injections,

-

•

etc.,

but unlike in Example 5.1, these attacks would not be considered on specific machines. Rather, the attack scenario is described as a general code injection that may be tried on any machine in the network (if possible). The description of the attack/defense scenario, as well as the possibilities to consider for a risk assessment may be more complex in this kind of modeling, as Example 5.2 shall illustrate.

Example 5.2

The expert survey would ask something like:

What is the expected damage if an attacker attempts a code injection attack in our infrastructure, while machine 1 (see Figure 7a) is being re-installed at roughly the same time.

To answer this question towards a loss estimate, the expert may consider the following aspects:

-

•

Which machines could be vulnerable to such an attack (say, which of them are accessible by a web interface or maybe have an insufficient patch level, etc.)

-

•

Depending on which machine is attacked, the damage may be more or less (thus allowing the expert to utter multiple possibilities; substantiating the construction of a categorial loss distribution once again).

-

•

Depending on where the spot check is done (say, on machine 1 in Example 5.1), three cases are possible:

-

–

Machine 1 has so far not been reached by the attacker (more precisely the attack path), so the reinstallation has no effect on the APT at this stage.

-

–

Machine 1 is exactly the one currently targeted by the attacker. This may render the results of the APT learning phase on this machine useless, since the configuration has changed. Consequently, the attacker is sent back one stage and has to restart learning from here.

-

–

Machine 1 has already been infected with malware, so that the adversary’s backdoor path goes through it. In that case, the attacker’s secret backdoor may be closed by the reinstallment and the attacker is again sent back to a previous stage.

-

–

Since there is uncertainty on where the attack may be mounted, and also on the current position of the adversary, the expert may utter several possibilities in one of two ways:

-

•

Tell about a set of possibilities, expressing the likelihood for each of them individually. For example, the expert may say something about the most likely outcome, but in addition also say that more or less extreme results are possible with certain other likelihoods.

-

•

Give a most likely outcome , and express the uncertainty about it: this in fact corresponds to the aforementioned kernel density smoothing, since the uncertain variation around the most likely value (as expressed by the expert) may be well expressed by a bell-shaped curve centered around the value . This is nothing else than a kernel density, where the uncertainty is “quantified” by the parameter .

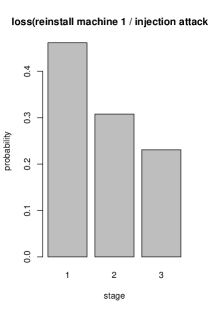

In repeating the procedure exemplified in Example 5.2 for each (high-level) defense/attack scenario , we end up with a standard matrix game defined with probability-distribution valued payoffs, which are now defined not on the risk categories, but on the graph theoretic distances, or more specifically, the stages between the initial infection and the inner asset. Picking up Example 5.1, there are three stages which the attacker has to proceed through, and the loss distribution defined per defense/attack assigns likelihoods to each of these stages; Figure 9 displays an example. The game-theoretic optimization then goes for pushing the probability mass towards “more remote” nodes in the network (or attack graph). That is, we will try maximizing the distance between the attacker and the asset, measured as the number of hops ( stages in our wording) that need to be taken to reach the goal. The stage numbering should, for consistency with the minimization, be increasing from 1 up to the stage where the asset is, i.e., stage 1 should comprise the outermost perimeter, followed by the adjacent inner nodes, until stage being the set of final nodes adjacent to the target asset.

5.2 Modeling Social Engineering

Social engineering is a good example of a case where the distribution-valued game-theoretic framework perfectly fits. Since there is hardly any technical countermeasure against such attacks, and the exploits are based on psychological principles of human behavior, there is also an element of “forgetting” that makes security awareness decay over time. For this reason, security training, information campaigns and similar must be repeated from time to time, and there is never a guarantee that any of these precautions has any or even durable effect. Both of these reasons render matrix games with distribution-valued payoffs into a nice model, since:

-

•

the necessity of repeating social engineering awareness training corresponds with the modeling assumption on the matrix game to be repeated.

-

•

the finiteness of matrix games corresponds to the limited set of possible countermeasures known against such attacks. That is, we cannot ask an employee just to become “creative” in how social engineering may be detected, and the best we can hope for is a feasibly small set of recommendations that a person can remember to avoid falling victim to social engineering.

-

•

the inevitable element of human error renders the outcome of a social engineering scenario in any case up to randomness. Hence, our specification as a distribution-valued matrix game appears as a good fit, as it allows us to classify social engineering countermeasures as being “variably effective” (taking into account the differences in people’s personality, daily mood, current workload, technical skills, time since the last security awareness training, and many more).

For a pure model of social engineering attack/defense scenarios, the questionnaire outlined in section 3.3 may be adapted to poll people about their awareness against social engineering, describing the particular attack scenario in the description of the question, and asking the employee on how he/she would behave in this scenario. The results then equally well compile into the sought loss distributions, if each answer in the multiple-choice survey has a background association with a predefined loss category (cf. section 3.8).

A different approach to account for social engineering when it comes to loss distributions is considering these attacks as methods to establish the initial infection in an APT model as outlined in section 5.1. Here, we would include social engineering techniques in the attacker’s strategy space , and the specification of the respective success rates can be done using the same kind of survey as before. The resulting game then already models the first phase of an APT infection, in giving the probability for a social engineering attack to succeed under the given security awareness campaign (which is a mixed strategy over in the sense of repeated randomly selected trainings, information broadcast, etc.).

The second phase of the APT, the penetration, can as well use social engineering techniques to overcome barriers within the system. Suppose that a subnetwork, for security reasons, does not have any physical or logical connection to the outside or any other intranet within the company. Then a malware can jump over this physical separation by a bring-your-own-device incident. That is, if the malware gets into the system by someone connecting a virulent USB stick to the inner separated network, the infection has effectively overcome the logical separation. Even more, this scenario may start from within the company’s perimeter, since the infection of the USB stick may indeed happen on an employees’ computer, which has a connection to the internet and got infected in the first phase.

The respective loss distributions associated with such an infection outbreak can effectively be constructed by simulation, as is eloquently outlined in [22]. We leave the details aside here.

6 Working with Game-Theoretic Risk Measures

The description in the following is based on the previous explanations about the model, and therefore only discusses practical matters of choosing the parameters and hints on how to interpret the results. A description on how to do the calculations with aid of the R statistical software suite is given in section 6.4.

6.1 Choosing the Cutoff Point

So far, we mentioned the necessity of truncating distributions only as a technical matter of assuring convergence. As such, the point at which the payoff distributions are truncated (for a compact support) also influences the outcome of the game, since the equilibria depend on it. Indeed, the practical choice of can be made in light of how determines the -relation among the payoffs. Informally, Lemma 4.4 in [37] tells that is decided based on how the payoff densities behave in a right neighborhood of . That is, the setting of the value controls the range in which damages are considered as relevant for , whereas damages far lower than become less and less relevant for the -relation. This means that the choice of can be made to implement a risk prioritization in the model in a sense that is perhaps best illustrated by an example (cf. also [38] for a related yet different illustration):

Example 6.1

Suppose an enterprise has backup capacities to bear losses less than . Then, we may set the truncation point , so that the entire probability mass assigned to damages is “squeezed” underneath the distribution on the interval . Consequently, if a loss model admits highly likely losses (i.e., has in that sense a fat tail) will result in a higher value of than maybe the alternative loss distribution , assigning smaller likelihood to such incidents (and in turn coming out with a smaller density ). Thus, will make -preferable over [37].