A continuous selection for optimal portfolios

under convex risk measures does not always exist

Abstract

One of the crucial problems in mathematical finance is to mitigate the risk of a financial position by setting up hedging positions of eligible financial securities. This leads to focusing on set-valued maps associating to any financial position the set of those eligible payoffs that reduce the risk of the position to a target acceptable level at the lowest possible cost. Among other properties of such maps, the ability to ensure lower semicontinuity and continuous selections is key from an operational perspective. It is known that lower semicontinuity generally fails in an infinite-dimensional setting. In this note we show that neither lower semicontinuity nor, more surprisingly, the existence of continuous selections can be a priori guaranteed even in a finite-dimensional setting. In particular, this failure is possible under arbitrage-free markets and convex risk measures.

Keywords: risk measures, portfolio selection, perturbation analysis, continuous selections.

Mathematics Subject Classification: 91B30, 91B32

1 Introduction

This note deals with the existence of continuous selections for a class of optimal set mappings that play an important role in several areas of mathematical finance, including capital adequacy, pricing, hedging, and capital allocation. In that context, one if often confronted with the problem of mitigating the risk of a given financial position by setting up a suitable capital buffer whose function is to absorb future larger-than-expected losses. This capital reserve is usually held in the form of a portfolio of some financial securities called the eligible assets. The optimal set mappings under consideration associate to each financial position precisely the set of all payoffs of eligible assets that allow to confine risk within an acceptable level of security at the lowest possible cost.

A thorough analysis of qualitative robustness for such set-valued maps has been recently provided in [4]. Among the various stability properties, lower semicontinuity proves to be of cardinal importance in that it ensures that any optimal payoff of eligible assets remains close to being optimal after a slight misestimation of misspecification of the underlying financial position. However, one of the key findings of [4] was that lower semicontinuity is typically not satisfied. The counterexamples to lower semicontinuity provided there exploited in an essential way the infinite-dimensional structure of the underlying model space. At the same time, the lower semicontinuity results established there suggest that, under appropriate convexity assumptions, lower semicontinuity might not be too difficult to ensure in a finite-dimensional setting. It is therefore natural to ask whether, by restricting the attention to finite-dimensional model spaces and by working in a suitable convex environment, one may always guarantee lower semicontinuity.

From an operational perspective, the existence of continuous selections constitutes another key property of the above optimal set mappings that allows to associate to each financial position a unique portfolio of eligible assets in such a way that a slight perturbation of the underlying financial position does not engender a dramatic change in the structure of the corresponding optimal portfolio. Recall that, for convex-valued maps, the existence of continuous selections is automatically implied by lower semicontinuity by virtue of Michael’s Theorem ([1, Theorem 17.66]). Hence, one may hope to always have continuous selections in a finite-dimensional setting, at least under convexity, even in the case that lower semicontinuity failed. This question was not addressed in [4].

In this note we provide concrete examples of optimal set mappings of the above type in a finite-dimensional model space that (1) fail to be lower semicontinuous but admit a continuous selection (2) fail to admit a continuous selection. Besides their intrinsic mathematical interest, our examples raise a serious warning in the above-mentioned fields of application: a cost or risk minimization problem under a convex risk measure in a finite-dimensional space need not allow for a robust way to select optimal portfolios of eligible assets. Hence, a case-by-case analysis is required to establish whether a special choice of a (convex) risk measure leads to robust optimal selections or not.

This note is structured as follows. In Section 2 we introduce our mathematical setting and define the relevant class of optimal set mappings. In Section 3 we show that an optimal set mapping in a finite-dimensional setting may fail to be lower semicontinuous but still admit continuous selections. Section 4, which builds on the example discussed in the previous section, establishes that an optimal set mapping in a finite-dimensional setting may even fail to admit continuous selections.

2 The optimal set mapping

We introduce our optimal set mapping by adopting the same notation of [4], to which we refer for more details about the non-mathematical aspects of our problem.

Consider a one-period economy with dates (the initial date) and (the terminal date). Financial positions at the terminal date are represented by the elements of a (real) Hausdorff topological vector space , which we assume to be partially ordered by a convex cone . Within the space of position one identifies a set of acceptable (from the point of view of financial regulators) or desirable (from the point of view of risk or portfolio managers) positions. We denote by a finite-dimensional linear subspace of , whose elements represent the payoffs of a finite number of financial assets that are used to push unacceptable positions into the target set . The space is endowed with the relative topology induced by . Each payoff in carries a certain price that is represented by a linear functional .

From a capital management perspective it is important to know at which cost a certain financial position can be made acceptable. This leads to studying the optimal value function defined by

In the financial literature the above function is usually referred to as a risk measure. The interested reader can consult [2], [3], [6], [7], [8] for a variety of results on risk measures and discussions on their financial relevance in different areas of mathematical finance.

The optimal set mapping associated to the above parametric optimization problem is the set-valued map given by

Any element of is referred to an an optimal payoff for . We refer to [4] for a comprehensive study of qualitative robustness for the above mappings. As mentioned in the introduction, one of the main findings of that paper was to show that, in many relevant cases, the map fails to be lower semicontinuous. This is true even if the acceptance set is assumed to be convex. Recall that is lower semicontinuous at some whenever for any open set satisfying there exists a neighborhood of such that

Intuitively speaking, this means that any optimal payoff for remains close to being optimal after a slight perturbation of .

However, all the counterexamples to lower semicontinuity exhibited in [4] use in a critical way the infinite dimensionality of the underlying ambient space. In fact, none of them can be reproduced in a finite-dimensional setting due to the general results from the same paper. More precisely, the acceptance sets used in the counterexamples become polyhedral sets once restricted to finite dimension and lower semicontinuity is always ensured under polyhedrality by virtue of [4, Theorem 5.12]. It remained thus open whether, especially for convex acceptance sets, one can still find counterexamples to lower semicontinuity and, more generally, to the existence of continuous selections for in a finite-dimensional setting.

We aim to enrich the results of [4] by showing that not only might lower semicontinuity fail for a convex acceptance set in a finite-dimensional model space, but we might even fail to find continuous selections for the optimal set mapping. This is also true if we impose the following requirements:

-

(R1)

is closed, convex, contains zero and satisfies the monotonicity property

-

(R2)

admits no arbitrage opportunity, i.e.

-

(R3)

is finite and continuous.

In this case, we will say that is admissible. The assumptions on are standard in the risk measure literature. In particular, by stipulating that any aggregation of acceptable positions remains acceptable, the property of convexity is often viewed to provide the mathematical translation of the economics principle of diversification, according to which aggregation should always improve security. The monotonicity property requires that any position dominating some acceptable position should also be deemed acceptable. The absence of arbitrage opportunities, which corresponds to the strict positivity of the pricing functional , is universally encountered in the mathematical finance literature. Finally, assuming that be finite and continuous makes the question of lower semicontinuity meaningful and our search for a counterexample more challenging.

3 Convexity does not ensure lower semicontinuity

Throughout this section we assume that . Our aim is to construct an admissible triple and exhibit a vector such that fails to be lower semicontinuous at . We split our construction in several steps.

The basic set

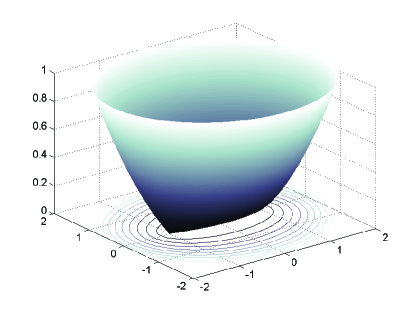

The acceptance set will be obtained by a suitable extension and rotation applied to the following basic set. Fix and define a subset of by setting

The lower boundary of this set has the boat-like shape depicted in Figure 1 with the projection of some level sets. For every the slice is an ellipsoid centered in with axes parallel to the canonical vectors and and of lengths and , respectively. In particular, the slice is a degenerated ellipsoid whereas the slice contains a circle of radius .

The set is clearly closed and is easily seen to be convex. Indeed, since the function defined by is convex, it follows that for every with and and . The same conclusion holds for every by closedness.

For every given radius consider the ice-cream cone

We claim that satisfies

| (1) |

To prove this, consider the convex function given by

| (2) |

After some elementary manipulations, one can show that is nothing but a section of the epigraph of , namely

For every with one can easily verify that

Since and , we infer that

The rotation

Consider the isometry defined by

| (3) |

It can be easily verified that is the composition of a clockwise rotation of an angle around the unit vector with a clockwise rotation of an angle such that and around the unit vector .

The acceptance set

Let and consider the set defined by

Recall that is a compact and convex set containing zero. As a result, we immediately see that is closed, convex, and contains zero. Moreover, satisfies the monotonicity property by definition. Hence, requirement (R1) is fulfilled.

The payoff space

The space of payoffs is the linear subspace of given by

where . It is immediate to see that is spanned by and . In addition, the pricing functional is the linear functional given by

In particular, we have and . To show that admits no arbitrage, take any nonzero and note that

for a suitable . Since is positive but nonzero, we must have and therefore . This shows that (R2) holds.

To show finiteness and continuity of , note first that

Set so that . Since , it follows from (1) that

As a result, we see that . Now, take any and note that

where . Then, it is not difficult to verify that

This shows that is finitely valued and (globally Lipschitz) continuous. Hence, requirement (R3) is also satisfied and the triple is admissible.

The failure of lower semicontinuity

First of all, note that for every we can write

Consider now the sequence in with general term

Note that and for every we have and

At the same time, recalling that , it clearly holds

This shows that fails to be lower semicontinuous at . In fact, a slight perturbation of may cause the corresponding set of optimal payoffs to shrink from an infinite set to just a singleton!

4 Convexity does not ensure continuous selections

Albeit not lower semicontinuous, the optimal set mapping in the preceding example is easily seen to admit a continuous selection. In this section we show that, by properly modifying the above acceptance set, we may be unable to ensure the existence of continuous selections as well. This is also possible under the constraint that be an admissible triple.

To this effect, we follow the general construction of the preceding example. The only difference is that we will “twist” the set in a suitable way. This modification will require some technical preliminary work to ensure convexity, which was automatic in the above example. In the sequel, for any and any subset we will consider sets of the form

The auxiliary set

Fix . In this section we focus on sets where

for given and . Note that we can always write

where is specified by setting

| (4) |

with .

Now, assume that so that . In this case, is infinitely differentiable and satisfies

| (5) |

whenever with . Indeed, if we found for some with we would produce the contradiction

where we used that in the second-to-last inequality and in the last inequality. As a result, (5) holds. Then, by the Implicit Function Theorem, there exists an open set and a continuously differentiable function for which

Of course, it is not difficult to see that we can extend this function continuously to obtain

| (6) |

Convexity of . We claim that is convex whenever . To show this, we shall use the following result by [5].

Theorem 4.1.

Let be a lower semicontinuous quasiconvex function. Then, is convex if and only if the function defined by

is concave for every .

Note first that is lower semicontinuous and quasiconvex by construction. We use Theorem 4.1 to prove its convexity. For every the sublevel set is easily seen to satisfy

This set is an ellipsoid and its support function can be computed explicitly. For we indeed have

As a function of , we have a sum of two square roots of affine functions. If , these two terms are concave. Assume, then, that . The second derivative of the first term is

which can be seen to become more and more negative as increases. So, to establish the concavity of , it suffices to consider . In this case, we get

which is concave as . This proves that is convex and, hence, that is also convex.

The convexity of holds even if . To see this, define

for any , where under the assumption that none of the ellipsoids is empty. Now, let . Then, there exists a sequence such that for every . This result is trivial when . Otherwise, setting so that , we simply take

and construct the corresponding point of . Conversely, if defines a sequence converging to with , then by continuity of the functions and . This property is also immediately verified when . As a result, if we let , then we see that is convex due to the convexity of each of the sets .

Curvature of . Finally, for our later construction, we need to provide some estimates on the norm of the gradient of . For any with it follows from the Implicit Function Theorem that

Now, assume that and and take . We claim that

| (7) |

and, under the assumption ,

| (8) |

Note that we can restrict the above optimization domains to those such that by convexity. After a few elementary rearrangements, we get

where, for notational convenience, we have set

with , , , , and . Note that are all nonnegative while the sign of depends on . We show that implies

| (9) |

To show this, assume first that . In this case, we easily see that so that (9) holds. Then, assume that and note that

Since and , the numerator is strictly decreasing in and, hence, it is negative due to . Similarly, since , the denominator is strictly increasing in and, hence, it is strictly positive due to . This establishes (9) also when . As a result, we get

whenever , thus proving (7).

To prove (8), assume that belongs to the interval . In this case, the numerator of is easily seen to be maximized by if and by otherwise. At the same time, the denominator of has its global minimum at , which is larger or equal than since and . Hence, the denominator is minimized by . Now, if we infer that

The last inequality is due to the fact that, by assumption, and . On the other side, if , then we have

The second inequality follows from , which holds since , and the last inequality is, as above, due to the fact that, by assumption, and . This finally establishes the bound in (8).

The basic set

Consider the set defined as the union of the following four quarters of ellipsoids:

Let be fixed and consider the set . This set has the same structure as the set considered above once we note that for a suitable circle . The set is clearly closed but its convexity is not a priori obvious.

Convexity of . We prove that is convex. By symmetry, this will imply that is also convex. Note that the half ellipsoid

is contained in the half ellipsoid

so that . It follows from our previous paragraph that is convex. Now, take and note that any convex combination of and belongs to . Since the equation

has at most two solutions , the segment with extremes and is divided in at most three subsegments where has a constant sign. Positive subsegments are contained in and, hence, belong to . Negative subsegments are contained in

which is also contained in . This establishes the convexity of .

The boundary of is smooth. Let and be the functions associated to and as in (4) and note that they coincide on the set . Moreover, for every we have

and

Observe that whenever . Finally, take an arbitrary with and . In this case, it is easy to see that so that, in fact, . In addition, we have as well as

As a result, we can use the above gradient formula to obtain

This shows that the boundary of is smooth when .

“Monotonicity” of . For any consider the ice-cream cone

We claim that

| (10) |

To show this, let be the function associated to as in (6) and note that . As a result of the bound established in (7), it follows that

for every with . The same bound holds, by symmetry, if we replace by . Similarly, if is the function associated to as in (6), then implies that

for every with by (8). The same bound holds, by symmetry, if we replace by . Then, one can easily establish (10) following the lines of the proof of (1).

The acceptance set

Let and consider the convex acceptance set defined by

where is the rotation defined in (3). Since is a compact and convex set containing zero, we see that is closed, convex, and contains zero. In addition, satisfies by definition the monotonicity property. Hence, requirement (R1) is fulfilled.

The space of payoffs

As above, the space of payoffs is the linear subspace of given by

where . The pricing functional is defined by setting

In line with what established above, (R2) holds.

Set so that . Since , it follows from (10) that

Hence, we can reproduce the above argument to establish that is finite and (Lipschitz) continuous, so that (R3) holds as well. In other words, is an admissible triple.

The failure of continuous selections

First of all, note that for every we can write

Now, consider the sequence defined by

Then, we easily see that

and similarly

for every . Since but we clearly have

it follows that no selection of can be continuous at .

References

- [1] Aliprantis, Ch.D., Border, K.C.: Infinite Dimensional Analysis: A Hitchhiker’s Guide, Springer (2006)

- [2] Artzner, Ph., Delbaen, F., Eber, J.-M., Heath, D.: Coherent measures of risk, Mathematical Finance, 9, 203-228 (1999)

- [3] Artzner, Ph., Delbaen, F., Koch-Medina, P.: Risk measures and efficient use of capital, ASTIN Bulletin, 39, 101-116 (2009)

- [4] Baes, M., Koch-Medina, P., Munari, C.: Existence, uniqueness and stability of optimal portfolios of eligible assets, ArXiv:1702.01936 (2017)

- [5] Crouzeix, J.-P.: Conditions for quasiconvexity of convex functions, Mathematics of Operations Research, 5(1), 120-125 (1980)

- [6] Farkas, W., Koch-Medina, P., Munari, C.: Beyond cash-additive risk measures: when changing the numéraire fails, Finance and Stochastics, 18, 145-173 (2014)

- [7] Farkas, W., Koch-Medina, P., Munari, C.: Measuring risk with multiple eligible assets, Mathematics and Financial Economics, 9, 3-27 (2015)

- [8] Föllmer, H., Schied, A.: Stochastic Finance: An Introduction in Discrete Time, 3rd edition, de Gruyter (2011)