Dual control Monte Carlo method for tight bounds of value function under Heston stochastic volatility model

Abstract

The aim of this paper is to study the fast computation of the lower and upper bounds on the value function for utility maximization under the Heston stochastic volatility model with general utility functions. It is well known there is a closed form solution of the HJB equation for power utility due to its homothetic property. It is not possible to get closed form solution for general utilities and there is little literature on the numerical scheme to solve the HJB equation for the Heston model. In this paper we propose an efficient dual control Monte Carlo method for computing tight lower and upper bounds of the value function. We identify a particular form of the dual control which leads to the closed form upper bound for a class of utility functions, including power, non-HARA and Yarri utilities. Finally, we perform some numerical tests to see the efficiency, accuracy, and robustness of the method. The numerical results support strongly our proposed scheme.

MSC 2010: 49L20, 90C46

Keywords: Utility maximization, Heston stochastic volatility model, dual control Monte Carlo method, lower and upper bounds, non-HARA and Yarri utilities

1 Introduction

Dynamic portfolio optimization is one of most studied research areas in mathematical finance. Stochastic control and convex duality are two standard methods to solve utility maximization problems. For a complete market such as the Black-Scholes model, the problem has already been solved. One may first find the optimal terminal wealth and then use the martingale representation theorem to find the optimal control, or one may solve the HJB equation to find the optimal value function and optimal control, see many excellent books for expositions, e.g., Karatzas and Shreve (1998), Pham (2009).

For an incomplete market driven by some Markovian processes, one may use the dynamic programming equation to solve the problem. One well-known example is the Heston stochastic volatility model. The HJB equation has two state variables (wealth and variance). For a power utility, one may decompose the solution to reduce the dimensionality of state variables by one and get a simplified nonlinear PDE with one state variable (variance). Thanks to the affine structure of the Heston model, Zariphopoulou (2001) uncovers a clever transformation that simplifies the nonlinear equation further into an equivalent linear PDE and derives a closed-form solution, see Zariphopoulou (2001) and Kraft (2005) for details. Kallsen and Muhle-Karbe (2010) extend the Heston model to general affine stochastic volatility models and Richter (2014) to multi-dimensional affine jump-diffusion stochastic volatility models with the martingale method and matrix Riccati ordinary differential equations.

The success of finding a closed-form solution for utility maximization with the Heston model (or general affine stochastic processes) crucially depends on the underlying utility being a power utility if the wealth process is exponential (or exponential utility if the wealth process is additive). Such combination of utility and wealth process would decouple wealth and variance variables in the optimal value function and the special affine structure of variance would help to give a closed-form solution, whether using the HJB equation or the quadratic backward stochastic differential equation. For general utilities, there is no way one can decouple wealth and variance variables and, consequently, there are no results for the existence of a classical solution to the HJB equation, let alone a closed form solution. Furthermore, due to high nonlinearity of the HJB equation with two state variables, it is also very difficult to find an efficient numerical method to solve it.

For a Black-Scholes market with closed convex cone constraints for controls and general continuous concave utility functions, Bian and Zheng (2015) (see also Bian et al. (2011)) show that there exists a classical solution to the HJB equation and the solution has a representation in terms of a solution to the dual HJB equation. That approach does not work for an incomplete market model such as the Heston model. The reason is that the stochastic volatility is not a traded asset (unless an additional volatility related security is introduced) and the Heston model is not a geometric Brownian motion and the dual HJB equation is an equally difficult nonlinear PDE with two state variables.

Although the dual control method cannot solve general utility maximization problems with incomplete market models, it nevertheless provides the valuable information for the optimal value function. The dual value function supplies a natural upper bound for the original primal value function due to the dual relation and a feasible control which may be used to provide a good lower bound for the primal value function. If one can make the gap between the lower and upper bounds small, then one can at least find an approximate solution to the primal value function, which would be impossible without using the dual control method. This idea has been applied successfully to find the approximate optimal value function for regime switching asset price models with general utility functions, see Ma et al. (2017).

In this paper we adopt this line of attack to utility maximization with the Heston stochastic volatility model. We derive the dual control problem and recover the optimal solution for power utility in Zariphopoulou (2001) and Kraft (2005). For general utilities, we propose a Monte Carlo method to compute the lower and upper bounds for the primal value function. Some upper bounds can be computed efficiently with the closed form formula or the fast Fourier-cosine method thanks to the affine structure of the Heston model. Numerical tests for power, non-HARA and Yarri utilities show that these bounds are tight, which provides a good approximation to the primal value function. To the best of our knowledge, this is the first time an efficient dual control Monte Carlo method is proposed to find the tight lower and upper bounds for the value function with the Heston stochastic volatility model and general utility functions.

The rest of the paper is arranged as follows. Section 2 discusses the dual control method and derives the same closed-form solution for power utility as that in Kraft (2005). Section 3 presents the dual control Monte Carlo method for computing tight lower and upper bounds of the value function. Section 4 provides the closed-form upper bound for a specific form of the dual control and a class of utility functions, including power, non-HARA and Yarri utilities. Section 5 performs numerical tests to see the efficiency, accuracy, and robustness of the method. Section 6 concludes. Appendix A gives the closed form solution of the Riccati equation associated with the Heston model and Appendix B explains the COS method for computing the upper bound with Yarri utility.

2 The Heston model and the dual control method

Assume that is a given probability space with filtration generated by standard Brownian motions and with correlation coefficient and completed with all -null sets. The market is composed of two traded assets, one savings account with riskless interest rate and one risky asset satisfying a stochastic differential equation (SDE) (see Heston (1993)):

where is a constant representing the market price of risk, is an asset variance process satisfying a mean-reverting square-root process:

is the long-run average volatility, the rate that reverts to , the variance of , and all parameters are positive constants and satisfy the Feller condition to ensure that is strictly positive.

Let be the wealth process. At time the investor allocates a proportion of wealth in risky asset and the remaining wealth in savings account . Then the wealth process satisfies the SDE:

| (2.1) |

where is a progressively measurable control process.

The utility maximization problem is defined by

| (2.2) |

where is a utility function that is continuous, increasing and concave (but not necessarily strictly increasing and strictly concave) on , and . To solve (2.2) with the stochastic control method, we define the value function

| (2.3) |

where is the conditional expectation operator given and , and is the set of all admissible control strategies over .

By the dynamic programming principle, satisfies the following HJB equation:

| (2.4) |

with the terminal condition , where is the partial derivative of with respect to and evaluated at , the other derivatives are similarly defined. The maximum in (2.4) is achieved at

| (2.5) |

Inserting (2.5) into (2.4) gives a nonlinear PDE

| (2.6) |

For a power utility , , the solution of (2.6) can be decomposed as

for some function which satisfies

| (2.7) |

with the termianl condition . The optimal control is given by

The equation (2.7) is simpler than the equation (2.6) but is still a nonlinear PDE. Zariphopoulou (2001) suggests a clever transformation

with , which removes the nonlinear terms in (2.7), and satisfies a linear PDE

| (2.8) |

with the terminal condition . The equation (2.8) can be easily solved and the solution has a Feynman-Kac representation. In fact, thanks to the affine structure of the Heston model, the solution of the equation (2.7) has an analytical form as

where and are solutions of some Riccati-type ODEs with terminal conditions and and can be easily solved, and the optimal control is given by , see Kraft (2005) for details.

The success of simplifying the HJB equation (2.6) to a solvable nonlinear PDE (2.7) crucially depends on the assumption that the utility function is a power utility. For general utility functions (e.g., non-HARA and Yarri utilities), it is virtually impossible one can find the analytical solutions.

The dual function of is defined by

| (2.9) |

for . The function is a continuous, decreasing and convex function on and satisfies . Suppose a dual process of the following form

with the initial condition . If is a super-martingale for any control process , then

where is the initial wealth, which leads to

and we have a weak duality relation. To make a super-martingale, we can use Itô’s formula to get

Furthermore, since is a decreasing convex function, we must have . Therefore, the dual process is given by

| (2.10) |

with the initial condition , where is a dual control process and is also a dual control variable. The solution to (2.10) at time , with initial condition , can be written as

where

Define the dual value function as

By the dynamic programming principle, satisfies the following dual HJB equation

| (2.11) |

with the terminal condition . The minimum in (2) is achieved at

| (2.12) |

Inserting (2.12) into (2) gives

| (2.13) |

Theorem 2.1.

Let be the solution of the dual HJB equation (2) and let be strictly convex in and satisfy and . Then the primal value function is given by

where is the solution of the equation

Furthermore, is the solution of the HJB equation (2.6) with the boundary condition and the optimal feedback control is given by

Proof.

Define

Since and is strictly convex in and and , we have

where satisfies . Using the Implicit Function Theorem, we have and therefore . Simple calculus shows that

and

Substituting these relations into (2.13) gives that satisfies the HJB equation (2.6). Moreover it follows from the conjugate equation (2) and that . The verification theorem then gives . The optimal feedback control is derived from (2.5) and the dual relations of the derivatives. ∎

Remark 2.2.

Theorem 2.1 shows there is no duality gap if the dual control takes the form (2.12). This is interesting in theory and is useful if one knows . In general, it is highly unlikely one can find , which requires to solve an equally difficult nonlinear PDE (2.13). However, if one can choose a dual control which gives a good approximation to , then one may follow Theorem 2.1 to get good approximations to the primal value function and the optimal feedback control. This is essentially the idea we use to design a Monte Carlo method for computing tight lower and upper bounds of the primal value function in the next section. For power utility , we can find a closed-form solution of (2.13) and therefore solve the primal problem with the dual method. This is explained in the next result.

Corollary 2.3.

Proof.

The dual function of is given by , where . We may set and substitute it into the equation (2.13) to get a simplified equation for :

| (2.15) |

with the terminal condition . We can solve equation (2.15) by setting and plugging into (2.15) to get two ODEs for and as follows:

and

We can easily find once is known and solve the Riccati equation to get a closed-form solution , see Appendix. Next we solve the equation to get

Using Theorem 2.1, we obtain the primal value function by

∎

3 Monte Carlo lower and upper bounds

For general utility functions, it seems impossible we can solve the primal problem by using Theorem 2.1 as the dual problem is equally difficult. Note that

| (3.1) |

for all dual controls . For every fixed , define

| (3.2) |

Then is an upper bound and can be easily computed with simulation. Note that depends on the choice of dual control . Denote the conjugate function of for fixed and by

| (3.3) |

The following theorem presents the tight lower and upper bounds on the primal value function.

Theorem 3.1.

Let be a set of admissible dual controls and be given by (3.3). Then the optimal value function defined in (2.3) satisfies

| (3.4) |

Furthermore, assume that given by is twice continuously differentiable and strictly convex for with fixed and , is the solution of the equation

| (3.5) |

the feedback control , defined by

| (3.6) |

is admissible, and is the unique strong solution of SDE (2.1) with the feedback control for . Define

| (3.7) |

Then the optimal value function satisfies

| (3.8) |

Proof.

It is obvious from (3.1) and the definitions of and . ∎

Remark 3.2.

Clearly, if , then

| (3.9) |

Using instead of gives a tighter upper bound but is more expensive in computation. The same applies to the lower bound. For numerical tests in Section 5, we choose the set to contain the following dual controls: , where is a piecewise constant function

| (3.10) |

with for and , being arbitrary constants.

Remark 3.3.

If the dual function has the form where for and , then

where . The upper bound is given by

and is the solution of equation (3.5): The feedback control for the lower bound is given by (3.6):

For fixed dual control , , we can use the Monte Carlo method to compute and approximate with the finite difference for sufficiently small . If , we have a closed-form solution . If , we can use the Newton-Raphson method to find .

Remark 3.4.

If the dual function is Lipschitz continuous, then we may use the pathwise differentiation method to compute , that is,

For example, the dual function of Yarri utility (see (4.6)) is given by , we have , where is an indicator which equals 1 if happens and 0 otherwise. We can then approximate and with finite differences and , respectively, for sufficiently small .

The Monte-Carlo methods can be used to find the tight lower and upper bounds, analogously to the algorithm developed by Ma et al. (2017). To implement the method, we need to discretize the dual process in (2.10).

Although under the Feller condition , the stochastic volatility process is strictly positive, the discretization of the SDE will draw below zero. To deal with this situation, we apply the full-truncation Euler method first proposed in Lord et al. (2010), which outperforms many biased schemes in terms of bias and root-mean-squared error. The stochastic volatility can be discretized in the following form

where and is a standard normal variate, the processes and by the Euler method,

where and are two independent standard normal variables. For wealth process driven by , it is possible that an investor loses all his money during the investment period. Thus if , we stop generating the paths, and set for the current path.

Next we describe the Monte-Carlo methods for computing the tight lower and upper bounds at time . The tight lower and upper bounds at other time can be computed similarly. Assume , and the dual utility function in (2.9) are known. The dual control or or , where is a piecewise constant function given by (3.10). Denote by the set of vectors which form the coefficients of the function .

Monte-Carlo method for computing tight lower and upper bounds:

-

Step 1: Fix a vector and a form of dual control .

-

Step 2: Generate sample paths of Brownian motion and , discretize SDE (2.10), compute with and the average derivative:

-

Step 3: Use the bisection method to solve equation (3.5) and get the solution .

-

Step 4: Compute the upper bound

-

Step 6: Compute the lower bound

-

Step 7: Repeat Steps 1 to 6 with different to derive the tight lower bound and the tight upper bound .

Remark 3.5.

It is much more time consuming to compute the tight lower bound than to the tight upper bound. The reason is that one has to generate sample paths of the wealth process and control process , which requires to solve equation (3.5) at all grid points of time, not just at as in the case of computing the tight upper bound. One technique to speed up is to use a four-dimensional matrix to pre-save the values of on a lattice, and then apply linear interpolation to approximate the exact values we need while generating sample paths of .

4 Closed-form upper bounds

For general dual controls , , we have to use the Monte Carlo method to compute the upper bound of (3.2). However, for a class of special dual controls and utility functions, we can find the upper bound in closed-form. Since satisfies a linear SDE (2.10) and is a decreasing and convex function, is a decreasing and convex function for with fixed and . Moreover, the Feynman-Kac theorem implies that satisfies the following linear PDE:

| (4.1) |

with terminal condition . The choice , where is a piecewise constant function, is particularly interesting as we can get the closed-form solution of the equation (4.1) if is a linear combination of power functions. Specifically, if

where is a piecewise constant function defined by (3.10), and

| (4.2) |

where with for . The solution of (4.1) is given by

| (4.3) |

where and satisfy the following ODEs

and

with coefficients given by

Furthermore, is given by

where , , are computed recursively as follows: for ,

with terminal condition and, for ,

with terminal condition . The closed-form solutions of and are given by (6.2) and (6.1) respectively in Appendix A. Comparing in Remark 3.3 and (4.3), we see that

and the upper bound and the feedback control are given by

| (4.4) |

and

| (4.5) |

where is the unique solution of equation .

Since the PDE (4.1) can be solved with a closed form solution, which makes the computation of the upper bound very fast. Even if the dual utility is not in the form of (4.2), but has some simple structure such as call/put option payoff function, one can still compute the upper bound efficiently by using the fast Fourier transform method. We next discuss several examples to illustrate these points.

Example 4.1.

(power utility). For , its dual function is given by , where . Let . This is a special case of (4.2) with and . The dual value function , defined by (3.2), is given by (4.3). For power utility, the upper bound and the feedback control can be written out explicitly as

where and are given by (6.2) and (6.1), respectively, with , and . Note that is a deterministic function of time . We can then use the Monte Carlo method to generate sample paths of the wealth process to compute the lower bound, see Remark 3.3. However, for power utility, there is a fast approximation method to compute the lower bound as shown next. By the Feynman-Kac theorem, the lower bound , defined by (3.7), satisfies the following PDE:

with the terminal condition . Thanks to the power utility, the solution of the above equation is given by

where and satisfy the following ODEs

and

Even though satisfies a Riccati equation, there is no closed form solution for as is a continuous function, not a constant. We can nevertheless approximate with a piecewise constant function and then get a closed-form approximate solution to with a recursive method. Specifically, we may divide interval by grid points and approximate by a piecewise constant function

can be made arbitrarily close to . If we replace by in the Riccati equation for , the solution of the resulting equation can be written as

where , , satisfy Riccati equations (6.1) with constant coefficients on intervals and can be computed recursively in a closed form with terminal conditions . The function is a good approximation of .

Example 4.2.

(non-HARA utility). Assume

for , where

It can be easily checked that is continuously differentiable, strictly increasing and strictly concave, satisfying , , and . Furthermore, the relative risk aversion coefficient of is given by

which shows that is not a HARA utility and represents an investor who will increase the percentage of wealth invested in the risky asset as wealth increases, see Bian and Zheng (2015) for more details. The dual function of is given by

Let . This is a special case of (4.2) with and . The dual value function is given by (4.3), the upper bound by (4.4) and the feedback control by (4.5), in the case here, can be computed explicitly as

where are given by (6.2) and (6.1) respectively with , and , see Appendix B.

Note that, unlike the case for power utility, there is no closed form formula for the lower bound . One has to use the Monte Carlo method to generate sample paths of the wealth process in order to find its value. We can nevertheless find a reasonable lower bound at more expensive computational cost.

Example 4.3.

(Yarri utility). Assume

| (4.6) |

where is a positive constant. is a continuous, increasing and concave function, but not differentiable at and not strictly concave. Also note that , so Inada’s condition is not satisfied. This utility is called Yarri utility and is used in behavioural finance. The dual function is given by

For the dual process (2.10) with , where is an arbitrarily fixed constant, we evaluate the dual value function

This is a European put option pricing problem with the Heston model. Let and . Then

| (4.7) |

with terminal condition . Although the conditional probability density function of is unknown, its conditional characteristic function (namely, the Fourier transform of the density function) can be derived. Therefore, analogous to the well-known Heston method in Heston (1993), function in (4.7) can be written as an integral formula, which can be evaluated by numerical integration rules based on the Fast Fourier Transform (FFT). Fang and Oosterlee (2008) develop Fourier-cosine expansion in the context of numerical integration as a more efficient alternative for the methods based on the FFT, which is named as COS method. For the convenience of the readers, we show the main ideas of COS method in Appendix B.

We now give some details. Define the conditional characteristic function of by

By the Feynman-Kac theorem, satisfies the following PDE

| (4.8) |

Assume that takes the following form

| (4.9) |

with and . Inserting (4.9) into (4.3) gives that and satisfy the Riccati equations in Appendix A with coefficients and

The closed form solutions and are given by (6.2) and (6.1), respectively, with , , , . Define . This is the conditional characteristic function of .

5 Numerical tests

In the following numerical examples we use the dual-control Monte-Carlo method to solve the optimal control problem (2.3) with power, non-HARA and Yarri utilities. We compute the upper bounds using the closed form formulas for power and non-HARA utilities and the Fourier-cosine method for Yarri utility when and everything else (the lower bounds for all and the upper bounds for and ) using the Monte-Carlo method with path number 100,000 and time steps 100 for discretizing SDEs with the Euler method, see Remarks 3.3 and 3.4.

5.1 Power utility

Example 5.1.

This example is aimed to apply the lower and upper bound method to the power utility when following mean-reversion square-root process. The following parameters

| (5.1) |

are taken from Zhang ad Ge (2016). The comparisons are carried out for the cases of sampling control for times uniformly distributed in for both the lower and upper bounds. The benchmark value is the primal value explicitly given by Kraft (2005). The parameter in utility function equals , and other parameters follow values in (5.1). The numerical results are listed in Table LABEL:power-table-1.

| Num | LB | UB | diff | rel-diff (%) | LB time (secs) | UB time (secs) |

|---|---|---|---|---|---|---|

| 1 | 2.074824 | 2.074894 | 7.01e | 3.38e | 2.62e | |

| 5 | 2.074824 | 2.074894 | 7.01e | 3.38e | 2.63e | |

| 20 | 2.074824 | 2.074894 | 7.01e | 3.38e | 2.65e | |

| 80 | 2.074824 | 2.074893 | 6.92e | 3.34e | 2.76e | 2.24e |

| Num | LB | UB | diff | rel-diff (%) | LB time (secs) | UB time (secs) |

| 1 | 2.074823 | 2.074845 | 2.12e | |||

| 5 | 2.074823 | 2.074845 | ||||

| 20 | 2.074823 | 2.074845 | ||||

| 80 | 2.074823 | 2.074842 | ||||

| Num | LB | UB | diff | rel-diff (%) | LB time (secs) | UB time (secs) |

| 1 | 2.074824 | 2.074894 | ||||

| 5 | 2.074824 | 2.074894 | ||||

| 20 | 2.074824 | 2.074894 | ||||

| 80 | 2.074824 | 2.074893 | ||||

Example 5.2.

From Example 5.1, we see outperforms other choices of . In this example we further test the robustness of the dual control Monte-Carlo methods for . The comparisons are carried out for the cases of sampling control for times uniformly distributed in both for the lower and upper bounds. In Table LABEL:power-table-2, we give the mean and standard deviation of the absolute and relative difference between the lower and upper bounds of power utility with randomly sampled parameters-sets: 10 samples of from the uniform distribution on interval , on , on , on , on , on , , , and . It is clear that the gap between the tight lower and upper bounds is very small, especially when the dual control is used. This shows that the algorithm is reliable and accurate. The numerical results are listed in Table LABEL:power-table-2.

| Num | mean diff | std diff | mean rel-diff (%) | std rel-diff (%) | mean time (secs) |

|---|---|---|---|---|---|

| 1 | |||||

| 5 | |||||

| 20 | |||||

| 80 |

Example 5.3.

This example compares performances of with being a constant (, the number of pieces ) and being a two-piecewise constant function (, the number of pieces ). Since is a power utility, we also replace the feasible control for the lower bound by a piecewise constant control ( with and ) to expedite the computation of the lower bound. Table LABEL:power-table-3 lists the numerical results. It is clear that lower and upper bounds are very tight, even for and one sample of constant which is 0 in this case. The lower bound is the same as the optimal value. The upper bound can be improved as the number of samples for is increased. We make the number of samples for each , , the same as that of for to ensure piecewise functions with include all functions with , so the performance should be better. Our numerical results confirm this is indeed the case, even though the rate of improvement is small, possibly because the bounds are already very tight. This implies we can reduce the gap of the bounds by increasing the number at cost of exponentially increased computation. One needs to strike a balance of accuracy and cost. Since gives good estimation of the bounds, we use it from now on for other utilities too, including non-HARA and Yarri utilities.

| Num | LB | UB | diff | rel-diff (%) | LB (secs) | UB (secs) |

|---|---|---|---|---|---|---|

| 1 | 2.074842060 | 2.074844628 | ||||

| 60 | 2.074842060 | 2.074844628 | ||||

| 600 | 2.074842060 | 2.074842126 | ||||

| 6000 | 2.074842060 | 2.074842125 | ||||

| Num | LB | UB | diff | rel-diff (%) | LB (secs) | UB (secs) |

| 1 | 2.074842060 | 2.074844628 | ||||

| 2.074842060 | 2.074842469 | |||||

| 2.074842060 | 2.074842119 | |||||

| 2.074842060 | 2.074842104 | |||||

5.2 Non-HARA utility

Example 5.4.

This example is aimed to check the correctness of the lower and upper bounds when process always constant through the time, in which case there is explicit solution to the primal value function. Let , and the other parameters be the same as (5.1). Denote and . Then the primal value function has the following explicit form (see Bian and Zheng (2015)):

with

The lower and upper bounds are computed by the Monte-Carlo method with path number and time steps . The numerical results are listed in Table LABEL:non-HARA-table-1, in which the numerics show that the benchmark is between the lower and upper bound, and the difference between these is proportional to and relative difference . Therefore, the lower and upper bound methods are reliable and accurate.

| Benchmark | LB | UB | diff | rel-diff (%) |

|---|---|---|---|---|

| 2.307810 | 2.307691 | 2.307843 |

Example 5.5.

This example is aimed to apply the lower and upper bound methods to the non HARA utility when following mean-reversion square-root process. The comparisons are carried out for the cases of sampling control for times uniformly distributed in both for the lower and upper bounds. The other parameters values are the same as in (5.1). The numerical results in Table LABEL:non-HARA-table-2 show that the choice outperforms the others.

| LB | UB | diff | rel-diff(%) | LB time (secs) | UB time (secs) | |

|---|---|---|---|---|---|---|

| 2.327407 | 2.327834 | |||||

| 2.327573 | 2.327858 | |||||

| 2.327411 | 2.327833 |

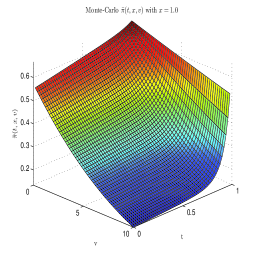

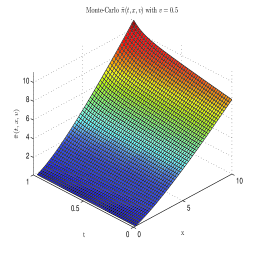

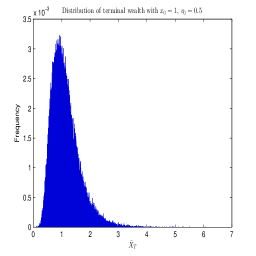

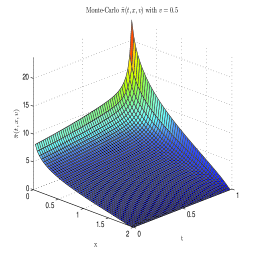

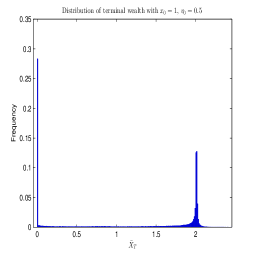

Using the optimal control for computing the tight lower bound for in Table LABEL:non-HARA-table-2, we draw the 3D figures for the optimal strategies and the distribution of the terminal wealth (see Figure 1).

Example 5.6.

In this example, we further examine the robustness of the lower and upper bound methods with . The comparisons are carried out for the cases of sampling control for times uniformly distributed in both for the lower and upper bounds. In Table LABEL:non-HARA-table-3, we give the mean and standard deviation of the absolute and relative difference between the lower and upper bounds for non-HARA utility with randomly sampled parameters-sets: samples of from the uniform distribution on interval , on , on , on , on , on , , , and . It is clear that the difference (and relative difference) between the tight lower and upper bounds is very small, especially when the dual control is used. This shows that the algorithm is reliable and accurate.

| Num | mean diff | std diff | mean rel-diff (%) | std rel-diff (%) | mean time (secs) |

|---|---|---|---|---|---|

| 1 | |||||

| 5 | |||||

| 10 | |||||

| 20 |

5.3 Yarri utility

Example 5.7.

This example is aimed to check the lower and upper bound methods when process always constant through the time. Let , and the other parameters be the same as (5.1). Then the analytical solution to the primal value is given by

The upper bound is computed by the Monte-Carlo methods with path number and time steps , and the lower bound with path number and time steps . The threshold is taken as . The numerical results are listed in Table LABEL:Yarri-table-1, which confirm that the lower and upper bound methods are reliable and accurate.

| Benchmark | LB | UB | diff | rel-diff (%) |

|---|---|---|---|---|

| 1.139790 | 1.136091 | 1.139889 |

Example 5.8.

This example is aimed to apply the lower and upper bound methods to the Yarri utility when following mean-reversion square-root process. The comparisons are carried out for sampling control for times uniformly distributed in both for the lower and upper bounds. The values of other parameters are the same as Example 5.7. For the Fourier-cosine methods, we set the truncation number as . The numerical results are listed in Table LABEL:Yarri-table-2. It is shown that the choice outperforms the others.

| LB | UB | diff | rel-diff (%) | LB time (secs) | UB time (secs) | |

|---|---|---|---|---|---|---|

| 1.113889 | 1.174928 | |||||

| 1.172057 | 1.173366 | |||||

| 1.137594 | 1.174928 |

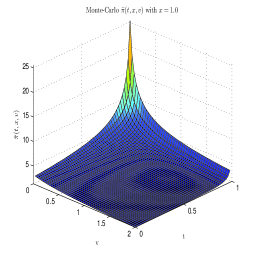

The 3D figures are drawn for the optimal strategy . Also it is plotted that the distribution of the terminal wealth (See Figure 2).

Example 5.9.

In this example, we further test the robustness of the lower and upper bound methods for . The comparisons are carried out for the cases of sampling control for times uniformly distributed in both for the lower and upper bounds. In Table LABEL:Yarri-table-3, we give the mean and standard deviation of the absolute and relative difference between the lower and upper bounds with randomly sampled parameters-sets: samples of from the uniform distribution on interval , on , on , on , on , on , , , and . It is clear that the gap between the tight lower and upper bounds is very small, especially when the dual control is used. This shows that the algorithm is reliable and accurate.

| Num | mean diff | std diff | mean rel-diff (%) | std rel-diff (%) | mean time |

|---|---|---|---|---|---|

| 1 | |||||

| 5 | |||||

| 10 | |||||

| 20 |

6 Conclusions

In this paper we use the weak duality relation to construct the lower and upper bounds on the primal value function for utility maximization under the Heston stochastic volatility model with general utilities. We propose a dual control Monte Carlo method to compute the bounds and suggest some simple forms of the dual control which makes the bounds tighter and computation easier. In particular, if is taken as with being a piecewise constant function, the closed form upper bound can be obtained for a broad class of utilities (including power and non-HARA utilties), and the Fourier-Cosine formula can be used for the Yarri utility. The gap between the lower and upper bounds can be reduced if the number of sampling or the number of time pieces increases. Numerical examples show that the tight bounds can be derived with little computational cost.

References

- Bian et al. (2011) Bian, B., Miao, S. and Zheng, H. (2011). Smooth value functions for a class of nonsmooth utility maximization problems, SIAM Journal of Financial Mathematics, 2, 727–747.

- Bian and Zheng (2015) Bian, B. and Zheng, H. (2015). Turnpike property and convergence rate for an investment model with general utility functions, Journal of Economic Dynamics and Control, 51, 28–49.

- Fang and Oosterlee (2008) Fang, F. and Oosterlee C.W. (2008). A novel pricing method for European options based on Fourier-cosine series expansions, SIAM Journal on Scientific Computing, 31, 826–848.

- Heston (1993) Heston, S.L. (1993). A closed-form solution for options with stochastic volatility with applications to bond and currency options, The Review of Financial Studies, 6, 327–343.

- Kallsen and Muhle-Karbe (2010) Kallsen, J. and Muhle-Karbe, J. (2010). Utility maximization in affine stochastic volatility models, International Journal of Theoretical and Applied Finance, 13, 459–477.

- Karatzas and Shreve (1998) Karatzas, I. and Shreve, S.E. (1998). Methods of Mathematical Finance, Springer.

- Kraft (2005) Kraft, H. (2008). Optimal portfolios and Heston’s stochastic volatility model: an explicit solution for power utility, Quantitative Finance, 5, 303–313.

- Lord et al. (2010) Lord, R., Koekkoek, R. and Dijk, D. (2010). A comparison of biased simulation schemes for stochastic volatility models, Quatitative Finance, 10, 177–194.

- Ma et al. (2017) Ma, J., Li, W. and Zheng, H. (2017). Dual control Monte-Carlo method for tight bounds of value function in regime switching utility maximization, European Journal of Operational Research, 262, 851–862.

- Pham (2009) Pham, H. (2009). Continuous-time Stochastic Control and Optimization with Financial Applications, Springer.

- Richter (2014) Richter, A. (2014). Explicit solutions to quadratic BSDEs and applications to utility maximization in multivariate affine stochastic volatility models, Stochastic Processes and their Applications, 124, 3578–3611.

- Zariphopoulou (2001) Zariphopoulou, T. (2001). A solution approach to valuation with unhedgeable risks, Finance and Stochastics, 5, 61–82.

- Zhang ad Ge (2016) Zhang, Q. and Ge, L. (2016). Optimal strategies for asset allocation and consumption under stochastic volatility, Applied Mathematics Letters, 58, 69–73.

Appendix A

In the paper we need to solve a number of times the following system of equations:

and

with the terminal conditions and , where all coefficients are constants. Assume and , where

The assumption ensures and are distinct real numbers. We can first find by writing the equation as

Using the terminal condition and denote we obtain the solution of (Appendix A) as

| (6.1) |

which leads to a closed-form formula for on interval . As for , we have the following form

| (6.2) |

The assumption is to exclude the case of being hypersingular integral.

Appendix B

This part explains the main idea of COS method in Fang and Oosterlee (2008) and derives the formula for computing the upper bound for Yarri utility.

For a function supported on , the cosine expansion reads

| with |

where indicates that the first term in the summation is weighted by one-half. For functions supported on any other finite interval, say , the Fourier-cosine series expansion can easily be obtained via a change of variables:

It then reads

with

| (6.3) |

Suppose is chosen such that the truncated integral approximates the infinite counterpart well, i.e.,

| (6.4) |

Comparing equation (6.4) with the cosine series coefficients of on in (6.3), we find that

where denotes taking the real part of the argument. It then follows from (6.4) that with

We now replace by in the series expansion of on , i.e.,

and truncate the series summation such that

For an option pricing problem expressed in (4.7), we rewrite it in the following form

| (6.5) |

Since the density rapidly decays to zero as in (6.5), we truncate the infinite integration range without loosing significant accuracy to , and obtain approximation :

In the second step, since is usually unknown whereas the characteristic function is, we replace the density by its cosine expansion in ,

with

which leads to

Interchanging the summation and integration, and inserting the definition

where

we have

Due to the rapid decay rate of these coefficients, we further truncate the series summation to obtain approximation :

Approximating by , we obtain

Define . This is the conditional characteristic function of . Then we can obtain (4.11). To find for the (4.10), we need to solve the following equation

To compute the feedback control (3.6), we need the following derivative

Finally, according to Fang and Oosterlee (2008), we can choose the boundary of integral as

where

and is a constant chosen large enough to guarantee . Cumulant may become negative for sets of Heston parameters that do not satisfy the Feller condition, i.e., . We therefore use the absolute value of .