Tests for the weights of the global minimum variance portfolio in a high-dimensional setting

Abstract

In this study, we construct two tests for the weights of the global minimum variance portfolio (GMVP) in a high-dimensional setting, namely, when the number of assets depends on the sample size such that as tends to infinity. In the case of a singular covariance matrix with rank equal to we assume that as . The considered tests are based on the sample estimator and on the shrinkage estimator of the GMVP weights. We derive the asymptotic distributions of the test statistics under the null and alternative hypotheses. Moreover, we provide a simulation study where the power functions and the receiver operating characteristic curves of the proposed tests are compared with other existing approaches. We observe that the test based on the shrinkage estimator performs well even for values of close to one.

Index Terms:

Finance; Portfolio analysis; Global minimum variance portfolio; Statistical test; Shrinkage estimator; Random matrix theory; Singular covariance matrix.I Introduction

Financial markets have developed rapidly in recent years, and the amount of money invested in risky assets has substantially increased. Due to this, an investor must have knowledge of optimal portfolio proportions in order to receive a large expected return and, at the same time, to reduce the level of the risk associated with the investment decision.

Since Markowitz (1952) presented his mean-variance analysis, many works about optimal portfolio selection have been published. However, investors are faced with some difficulties in the practical implementation of these investing theories since sampling error is present when unknown theoretical quantities are estimated.

In classical asymptotic analysis, it is almost always assumed that the sample size increases while the size of the portfolio, namely the number of included assets , remains constant (e.g., Jobson and Korkie (1981), Okhrin and Schmid (2006)). Nowadays, this case is often called standard asymptotics (see, Cam and Yang (2000)). Here, the traditional plug-in estimator of the optimal portfolio, the so-called sample estimator, is consistent and asymptotically normally distributed. However, in many applications, the number of assets in a portfolio is large in comparison to the sample size (i.e., the portfolio dimension and the sample size tend to infinity simultaneously) such that tends to the concentration ratio . In this case, we are faced with so-called high-dimensional asymptotics or ‘Kolmogorov’ asymptotics (see, Bühlmann and Van De Geer (2011), Bai and Shi (2011), Cai and Shen (2011), Bodnar, Dette and Parolya (2019)). Whenever the dimension of the data is large, the classical limit theorems are no longer suitable because the traditional estimators result in a serious departure from the optimal estimators under high-dimensional asymptotics (Bai and Silverstein (2010)). These methods fail to provide consistent estimators of the unknown parameters of the asset returns, that are, the mean vector and the covariance matrix. Generally, the greater the concentration ratio , the worse the sample estimators are. In these cases, new test statistics must be developed, and completely new asymptotic techniques must be applied for their derivations. Several studies deal with high-dimensional asymptotics in portfolio theory using results from random matrix theory (see, Frahm and Jaekel (2008) and Laloux, Cizeau, Potters and Bouchaud (2000)). Recently, Bodnar, Parolya and Schmid (2018) presented a shrinkage-type estimator for the global minimum variance portfolio (GMVP) weights, and Bodnar, Okhrin and Parolya (2019) derived the optimal shrinkage estimator of the mean-variance portfolio.

Testing the efficiency of a portfolio is a classical problem in finance. What looks good theoretically often suffers from the curse of uncertainty and dimensionality. Nevertheless, some approaches provide effective portfolio choice strategies including the GMVP, which by construction is a mixture of assets that minimizes the portfolio variance/volatility. The success of this strategy violates modern portfolio theory because it takes only the portfolio variance into account. But many empirical studies show that portfolios that focus on minimizing the volatility generate superior out-of-sample results (see, Jagannathan and Ma (2003); Clarke et al. (2011); Ledoit and Wolf (2004); Clarke et al. (2006) among others). That is why it makes sense to provide a statistical test whether the current portfolio composition is different from the conventional GMVP taking into account both the uncertainty of the asset returns and the large dimensionality of the portfolio.

The former literature focuses on the case of standard asymptotics or considers exact tests where both and are fixed. For example, Gibbons, Ross and Shanken (1989) provided an exact -test for the efficiency of a given portfolio, and Britten-Jones (1999) derived inference procedures on the efficient portfolio weights based on the application of linear regression. More recently, Bodnar and Schmid (2008) presented a test for the general linear hypothesis of the portfolio weights in the case of elliptically contoured distributions. The contribution of this study is the derivation of statistical techniques for testing the efficiency of a portfolio under high-dimensional asymptotics. Two statistical tests are considered. Whereas the first approach is based on the asymptotic distribution of the test statistic suggested by Bodnar and Schmid (2008) in a high-dimensional setting, the second test makes use of the shrinkage estimator of the GMVP weights and provides a powerful alternative to the existing methods. To the best of our knowledge, this analysis is the first time that the shrinkage approach has been applied to statistical test theory.

It has to be mentioned that there is a direct link between the subject of the paper and classical methods in statistical signal processing. The equivalent of the GMVP portfolio in signal processing literature is the Capon or minimum variance spatial filter (see, Verdú (1998) and Van Trees (2002)). The estimation risk of the high-dimensional minimum variance beamformer has already been studied in Rubio, Mestre and Palomar (2012) while its constrained versions were discussed in Li, Stoica and Wang (2004). The finite sample size effect on minimum variance filter was investigated by Mestre and Lagunas (2006). An improved calibration of the precision matrix, i.e., the central object for constructing the GMVP portfolio, was discussed in Zhang et al. (2013). For more literature on the applications of the random matrix theory to signal processing and portfolio optimization see, Feng and Palomar (2016) and references therein.

The testing procedure we propose can be used not only for testing on the GMV portfolio but also for the inference on the shrinkage intensity, i.e., the level of shrinkage one needs to decrease the estimation risk of the GMVP. Our test is based on the shrinkage technique for GMVP weights and, thus, setting different shrinkage targets leads to different tests, which could be of independent interest for financial analysts. As an example, one could construct a test whether the GMVP portfolio is stochastically dominating a naive (equally weighted) portfolio, which has attracted much attention of financial scientists during the last decade (see, DeMiguel, Garlappi and Uppal (2009); DeMiguel, Garlappi, Francisco and Uppal (2009)).

The paper is structured as follows. In Section II, we discuss the main results on distributional properties for optimal portfolio weights presented by Okhrin and Schmid (2006). In Section III.A the high-dimensional version of the test based on the test statistics given in Bodnar and Schmid (2008) is proposed, while a new test based on the shrinkage estimator for the GMVP weights is derived in Section III.B. The asymptotic distributions of the test statistics under both the null hypothesis and the alternative hypothesis are obtained, and the corresponding power functions of both tests are presented. In Section III.C, new test procedures for the GMVP weights are proposed under a high-dimensional setting when the covariance matrix is singular. In Section IV, the power functions and the receiver operating characteristic curves of the proposed tests are compared with each other for different values of . In our comparison study, a test of Glombeck (2014) is considered as well. We conclude in Section V. All proofs are given in the Appendix.

II Estimation of Optimal Portfolio Weights

We consider a financial market consisting of risky assets. Let denote the -dimensional vector of the returns on risky assets at time . Suppose that and . The covariance matrix is assumed to be positive definite.

Let us consider a single period investor who invests in the GMVP, one of the most commonly used portfolios (see, for example, Memmel and Kempf (2006), Frahm and Memmel (2010), Okhrin and Schmid (2006), Bodnar and Schmid (2008), Glombeck (2014), and others). This portfolio exhibits the smallest attainable portfolio variance under the constraint , where denotes the -dimensional vector of ones and stands for the vector of portfolio weights. The weights of GMVP are given by

| (1) |

The global minimum variance portfolio is of fundamental interest in applications involving array signal processing. In the array processing literature it is the so-called minimum variance distortionless response (MVDR) spatial filter or beamformer defined as (see, e.g., Van Trees (2002), Chapter 6). The vector is the scalar signature vector associated with some waveform . Thus, the tests for the global minimum variance portfolio developed in this paper could directly be used for minimum variance beamformer just by a simple modification.

The practical implementation of the mean-variance framework in the spirit of Markowitz (1952) relies on estimating the first two moments of the asset returns. Because we do not know the true covariance matrix, it is usually replaced by its sample estimator, which is based on a sample of historical asset returns given by

| (2) |

Replacing in (1) by the sample estimator , we obtain an estimator of the GMVP weights expressed as

| (3) |

Note that the estimator of the GMVP weights is exclusively a function of the estimator of the covariance matrix.

Assuming that the asset returns follow a stationary Gaussian process with mean and covariance matrix , Okhrin and Schmid (2006) proved that the vector of estimated optimal portfolio weights is asymptotically normal. Under the additional assumption of independence, they derived the exact distribution of . Okhrin and Schmid (2006) showed that the distribution of arbitrary components of is a - dimensional -distribution with degrees of freedom and

Consequently, if and are obtained by deleting the last element of and and if and consist of the first elements of and , then has a -variate t-distribution with degrees of freedom and parameters and . This distribution is denoted by , since .

III Test Theory for the GMVP in High Dimensions

At each time point, an investor is interested to know whether the portfolio he is holding coincides with the true GMVP or has to be reconstructed. For that reason, we consider the following testing problem:

| (4) |

where with is a known vector of, for example, the weights of the holding portfolio. Thus, this problem analyses whether the true GMVP weights are equal to some given values.

Bodnar and Schmid (2008) analysed a general linear hypothesis for the GMVP portfolio weights and introduced an exact test assuming that the asset returns are independent and elliptically contoured distributed. Moreover, they derived the exact distribution of the test statistic under the null hypothesis and the alternative hypothesis.

The main focus of this study is high-dimensional portfolios. We want to consider the testing problem (4) in a high-dimensional environment, that is, assuming that as . Note that, in this case, and depend on as well. Thus, it would be more precise to write and . In the following, we will ignore this fact in order to simplify our notation. Moreover, it turns out that the sample covariance matrix is no longer a good estimator of the covariance matrix (see, Bai and Silverstein (2010); Bai and Shi (2011); Yao, Zheng and Bai (2015)). Indeed, the latter references reveal that if and the covariance matrix is then the empirical spectral distribution of the eigenvalues of the sample covariance matrix is supported on . As a result, the larger , the more the eigenvalues spread out. It implies in terms of the norm that is not consistent.

For that reason, it is unclear how well the test of Bodnar and Schmid (2008) behaves in that context. First, we study its behaviour under the high-dimensional asymptotics, and, after that, we propose an alternative test that makes use of the shrinkage estimator for the portfolio weights (cf. Bodnar, Parolya and Schmid (2018)).

In recent years, several studies have dealt with estimators of unknown portfolio parameters under high-dimensional asymptotics with applications to portfolio theory. Glombeck (2014) formulated tests for the portfolio weights, variances of the excess returns, and Sharpe ratios of the GMVP for . Bodnar, Parolya and Schmid (2018) and Bodnar, Okhrin and Parolya (2019) derived the shrinkage estimators for the GMVP and for the mean-variance portfolio, respectively, under the Kolmogorov asymptotics for .

III-A A Test Based on the Mahalanobis Distance

Bodnar and Schmid (2008) proposed a test for a general linear hypothesis of the weights of the global minimum variance portfolio. Here, we are interested in the special case (4). For this case, the test statistic is given by

| (5) |

where consists of the first elements of and the number of assets in the portfolio is fixed. It was shown that has a central -distribution with and degrees of freedom under the null hypothesis, i.e., . Moreover, the density of under the alternative hypothesis is equal to

| (6) | |||||

where

| (7) |

and stands for the hypergeometric function (see, Abramowitz and Stegun (1964), chap. 15), that is,

Thus, the exact power function of the test is given by

| (8) |

where denotes the quantile from the central -distribution with and degrees of freedom. Note that this result is also valid for matrix-variate elliptically contoured distributions (see, Bodnar and Schmid (2008)). On the other hand, several computational difficulties appear when the power function of the test is calculated for large values of and , since doing so involves a hypergeometric function whose computation is very challenging for large values of and . In order to deal with this problem, we derive the asymptotic distribution of in a high-dimensional setting. This result is given in Theorem 1. The proof is in the Appendix. Since depends on (i.e., on ) through , we write in the rest of the paper.

Theorem 1

Let and . Assume that is a sequence of independent and normally distributed -dimensional random vectors with mean and covariance matrix , which is assumed to be positive definite. Let

Then, it holds that

for as . Under the null hypothesis, for as .

The results of Theorem 1 lead to an asymptotic expression of the power function given by

| (9) | |||||

where is the -quantile of the standard normal distribution.

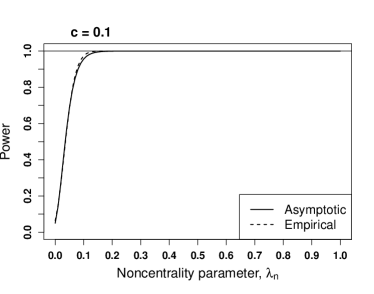

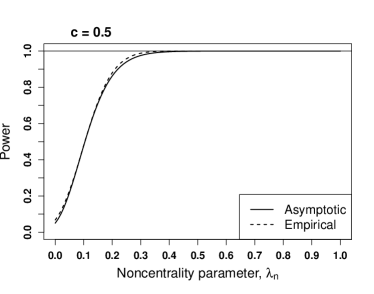

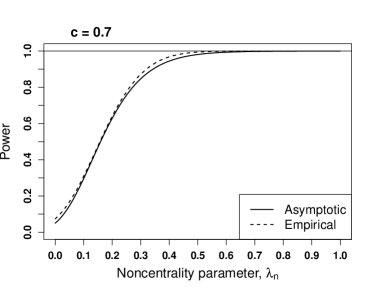

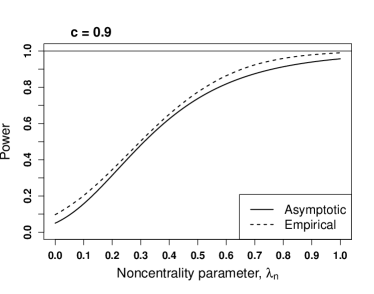

In Figure 1, we plot the power function (9) as a function of for several values of and (solid line). In addition, the empirical power of the test is shown for the same values of and (dashed line) and is equal to the relative number of rejections of the null hypothesis obtained via a simulation study. It is remarkable that, following the proof of Lemma 5, the considered simulation study can be considerably simplified. Instead of generating a random matrix of asset returns in each simulation run, we simulate four independent random variables from standard univariate distributions and then compute the statistic for the given value of following the stochastic representation (33) in the Appendix. Namely, the simulation study is performed in the following way:

-

(i)

Generate four independent random variables , , , and

-

(ii)

For fixed , compute

-

(iii)

Repeat steps (i) and (ii) for , where is the number of independent repetitions and calculate the empirical power by

(10) where is the indicator function of the set .

In Figure 1, we observe a good performance of the asymptotic approximation of the power function. This approximation works almost perfectly for both small and large values of .

|

|

III-B Test Based on a Shrinkage Estimator

In most cases, the unknown parameters of the asset return distribution are replaced by their sample counterparts when an optimal portfolio is constructed. In recent years, however, other types of estimators, such as shrinkage estimators, have been discussed as well (see, Okhrin and Schmid (2007) and Bodnar, Parolya and Schmid (2018)). The shrinkage methodology was introduced by Stein (1956). His results were extended by Efron and Morris (1976) to the case in which the covariance matrix is unknown. The shrinkage methodology can be applied to the expected asset returns (e.g., Jorion (1986)) and the covariance matrix (Bodnar, Gupta and Parolya (2014); Bodnar, Gupta and Parolya (2016)). Both of these applications appear to be very successful in reducing damaging influences on the portfolio selection. A shrinkage estimator was applied directly to the portfolio weights by Golosnoy and Okhrin (2007) and Okhrin and Schmid (2008). They showed that the shrinkage estimators of the portfolio weights lead to a decrease in the variance of the portfolio weights and to an increase in utility.

Bodnar, Parolya and Schmid (2018) proposed a new shrinkage estimator for the weights of the GMVP that turns out to provide better results in the high-dimensional case than the existing estimators do. This estimator is based on a convex combination of the sample estimator of the GMVP weights and an arbitrary constant vector expressed as

| (11) |

Here, the index GSE stands for ‘general shrinkage estimator’. It is assumed that is a vector of constants such that is uniformly bounded. Bodnar, Parolya and Schmid (2018) proposed determining the optimal shrinkage intensity for a given target portfolio such that the out-of-sample risk is minimal, that is,

| (12) |

is minimized with respect to . This result leads to

| (13) |

The authors showed that the optimal shrinkage intensity is almost surely asymptotically equivalent to a non-random quantity when as , which is given by

| (14) |

where

| (15) |

is the relative loss of the target portfolio , is the variance of the target portfolio, and is the variance of the GMVP. This result provides an estimator of the optimal shrinkage intensity given by

| (16) |

Using the estimated shrinkage intensity , the corresponding portfolio weights are given by

| (17) |

Bodnar, Parolya and Schmid (2018) proved that the ratio if as . In Theorem 2, we show that the estimated intensity is asymptotically normally distributed. The proof of Theorem 2 is given in the Appendix.

Theorem 2

Let and . Assume that is a sequence of independent and normally distributed -dimensional random vectors with mean and covariance matrix , which is assumed to be positive definite. Then

| (18) |

where

Next, we introduce a test based on the estimated shrinkage intensity. The motivation is based on the following equivalences (see, (14) and (15)):

This result means that if and only if the variance of the portfolio based on is equal to the variance of the GMVP. This finding in turn means that . Since the GMVP weights are uniquely determined, this result is valid if and only if . Choosing , it holds that

Thus, it is possible to obtain a test for the structure of the GMVP using the shrinkage intensity with the hypothesis given by

| (19) |

Note that . Let . For testing (19), we use the test statistic .

From Theorem 2 we get

where and are given in the statement of Theorem 2. Moreover, under the null hypothesis, and, thus, for as . This result gives us a promising new approach for detecting deviations of the true portfolio weights from the given quantities. Using Theorem 2, we are able to make a statement about the power function of this test. Since and depend on , we only have to replace this quantity with . It holds that

| (20) | |||||

Note that the approximation given in (20) is purely a function of . This property is a main difference from the test discussed in Section III.A, where the power function is a function of . These properties are very useful to analyse the performances of both tests and simplify the power analysis.

|

|

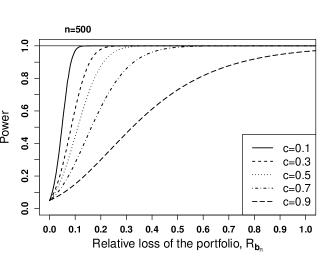

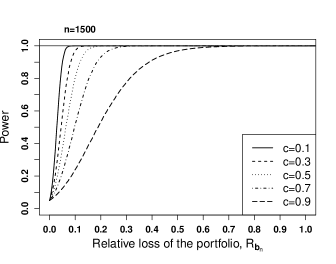

In Figure 2, the power of the test is shown as a function of and . It can be seen that the test performs better for smaller values of . With increasing values of , the power of the test decreases. We determine the power function for two different sample numbers, and . As expected, the test shows a better performance for larger values of , since increases, the numerator of the expression in the cumulative distribution function in (20) becomes negative, and the whole expression tends to one.

III-C Case of a Singular Covariance Matrix

We extend the results of Section III.A and Section III.B to the case of a singular covariance matrix with . Here, we consider two types of singularity: (i) in the population covariance matrix and (ii) in addition, in the sample covariance matrix by allowing the sample size to be smaller than the dimension . Throughout this section, we refer to as the actual dimension of the data generating process and, consequently, derive the results under the high-dimensional asymptotic regime as .

In the case , the sample covariance matrix is singular and its inverse does not exist. As a result, the Moore-Penrose inverse of , which we denote by , is used to estimate the weights of the GMVP expressed as

| (21) |

In a similar way, the true GMVP weights are obtained and they are given by

The Moore-Penrose inverse of the covariance matrix has already been used in portfolio theory by Pappas, Kiriakopoulos and Kaimakamis (2010); Bodnar, Mazur and Podgórski (2016) among others, while Bodnar, Dette and Parolya (2016) derived several distributional properties of the Moore-Penrose inverse of the sample covariance matrix.

Next, we consider linear combinations of both the true GMVP weights and their estimator given by

where is a matrix of constants with and . In particular, if with the -dimensional identity and the zero matrix , then is the vector of the first components of .

In order to verify the structure of the GMVP, we first extend the test based on the Mahalanobis distance to the test problem given by

| (22) |

for some -dimensional vector and the test statistic

| (23) |

where . This test statistic was considered in Bodnar, Mazur and Podgórski (2017), who derived its finite-sample distribution for both small portfolio dimension and sample size.

In Theorem 3, we extend these results by deriving the asymptotic distribution of under the high-dimensional asymptotic regime with and as . To this end, we also note that only a part of the GMVP weights are tested in (22). In order to test the structure of the whole portfolio, we have to repeat the test (22) for several subvectors of and to adjust the significance level of each test by applying, for example, the Bonferroni correction.

Theorem 3

Assume that is a sequence of independent and singular normally distributed -dimensional random vectors with mean and singular covariance matrix with . Let and and let such that . We define

with

Then, it holds that

for and as . Under the null hypothesis, for and as .

The results of Theorem 3 are very useful to derive the power function of the suggested test. Similarly to the case of a non-singular covariance matrix, it is given by

Next, we present the test based on a shrinkage estimator for the singular covariance matrix . Similarly as in the case of a nonsingular covariance matrix we get the shrinkage intensity given by

| (24) |

where are given in (21). The following proposition holds.

Proposition 1

Assume that is a sequence of independent and singular normally distributed -dimensional random vectors with mean and singular covariance matrix with a rank and assume for all . The optimal shrinkage intensity is almost surely asymptotically equivalent to a non-random quantity when as , which is given by

| (25) |

where

| (26) |

Proposition 1 is complementary to Bodnar et al. (2018, Theorem 2.1) and covers additionally the case of a nonsingular matrix . Going carefully through the proof of Proposition 1 we can easily deduce the consistent estimator of given by

| (27) |

with

| (28) |

Now we are ready to state the central limit theorem for , which is a straightforward consequence of the proofs of Proposition 1 and Theorem 2.

Theorem 4

Let and . Assume that is a sequence of independent and singular normally distributed -dimensional random vectors with mean and singular covariance matrix with a rank . Then

| (29) |

where

Next, we are ready to introduce a test based on the estimated shrinkage intensity for testing the hypotheses

| (30) |

which are equivalent to

Similarly as in the case of a nonsingular covariance matrix, we use the test statistic for testing (30). From Theorem 4 we get

where and are given in the statement of Theorem 4. Under the null hypothesis, for as . The power function can be constructed in a similar manner as in the case of a nonsingular matrix .

This result extends our previous findings and suggests that we may still use the test based on the optimal shrinkage intensity in the case of a singular population covariance matrix with the only difference that instead of we demand as and instead of the usual inverse we can safely use the Moore-Penrose inverse of the sample covariance matrix . Moreover, the test based on the shrinkage intensity needs no multiple testing scheme, which indicates its huge advantage over the test based on the Mahalanobis distance.

IV Comparison Study

The aim of this section is to compare several tests for the weights of the GMVP.

In the preceding two subsections, we considered two tests for the weights of the GMVP. For the test based on the empirical portfolio weights, the exact distribution of the test statistic is known. In Section III.A, the asymptotic power function of the test proposed by Bodnar and Schmid (2008) is derived in a high-dimensional setting. In Section III.B, a new test is proposed, and its asymptotic power function, which purely depends on , is determined. The fact that both tests depend on different quantities complicates the comparison of both tests. Note that

Here, both tests are compared with each other via simulations. Additionally, we include the test presented by Glombeck (2014, Theorem 10) in our comparison study as well as tests derived for a singular covariance matrix in Section III.C.

IV-A Design of the Comparison Study

Let be a positive semi-definite covariance matrix of asset returns, the number of samples, and . The structure of the covariance matrix is chosen in the following way: one-ninth of the non-zero eigenvalues are set equal to , four-ninths are set equal to , and the rest are set equal to . A similar structure of the spectrum of the populaion covariance matrix is present in Ledoit and Wolf (2012). In doing so, we can ensure that the eigenvalues are not very dispersed, and if increases, then the spectrum of the covariance matrix does not change its behaviour. Then, the covariance matrix is determined as follows

where is the diagonal matrix whose diagonal elements are the predefined eigenvalues and is the matrix of eigenvectors obtained from the spectral decomposition of a standard Wishart-distributed random matrix.

We consider the following scenario for modelling the changes. Under the alternative hypothesis, the covariance matrix is defined by

| (31) |

where

| (32) |

with and , , when is non-singular and when is singular. The matrix determines the deviations from the null hypothesis due to changes in the eigenvalues of the covariance matrix . Other specifications of the covariance matrix under the alternative hypothesis might be considered as well.

IV-B Comparison of the Tests

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

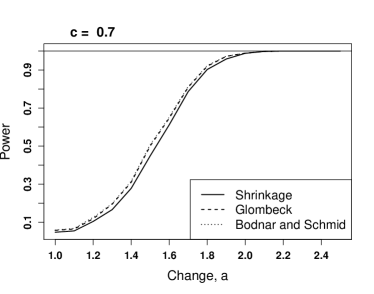

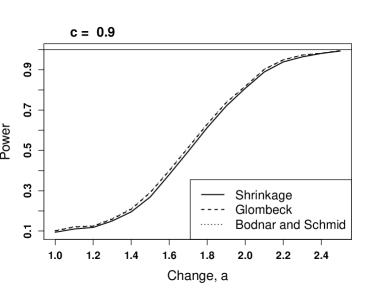

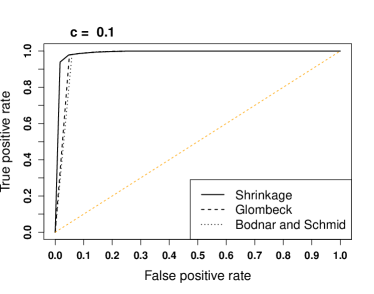

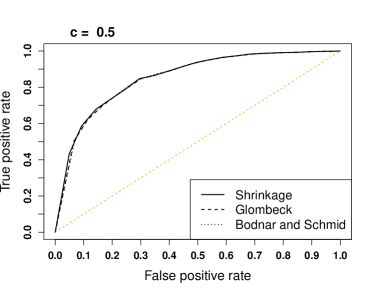

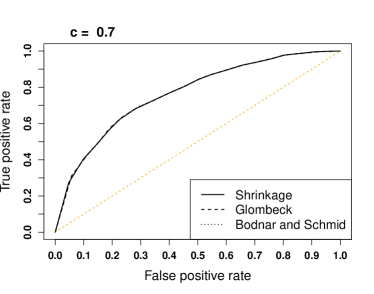

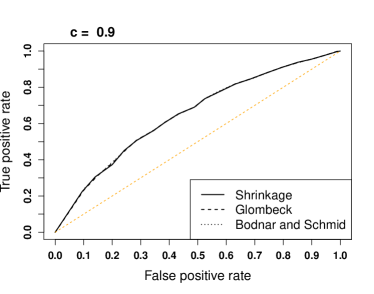

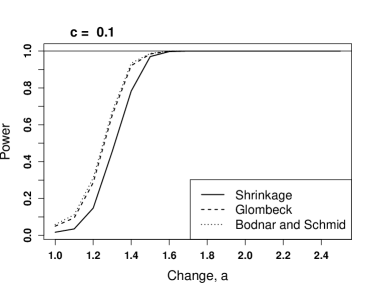

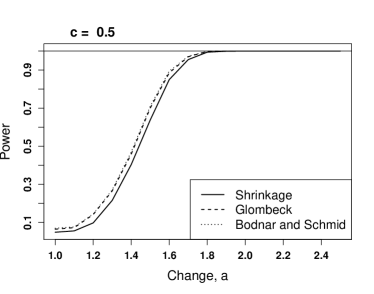

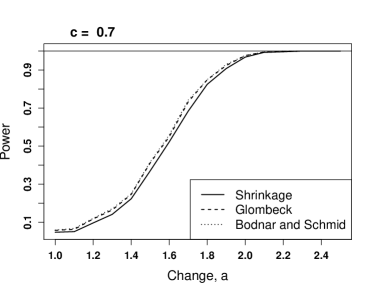

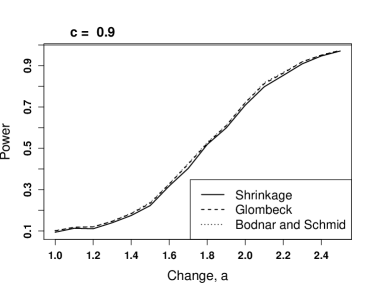

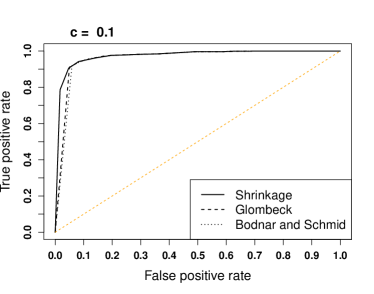

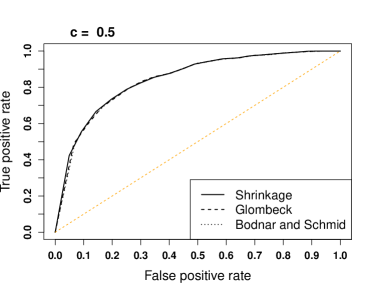

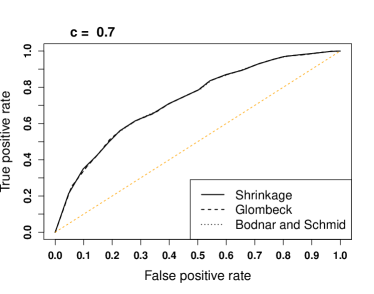

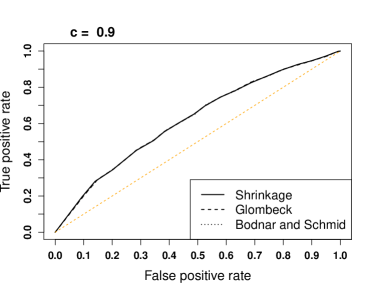

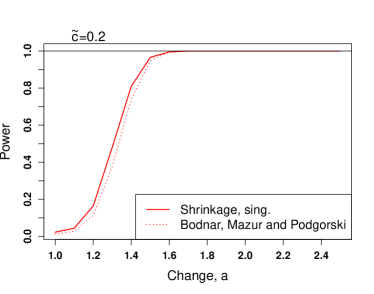

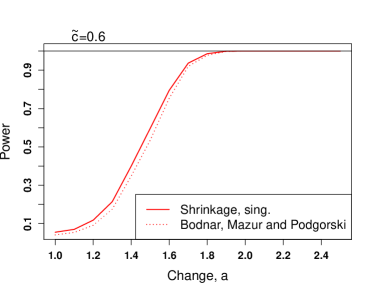

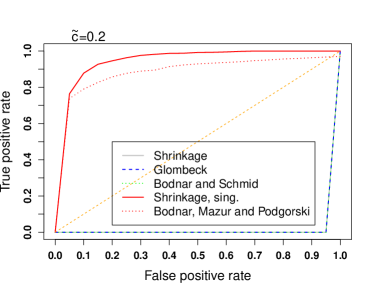

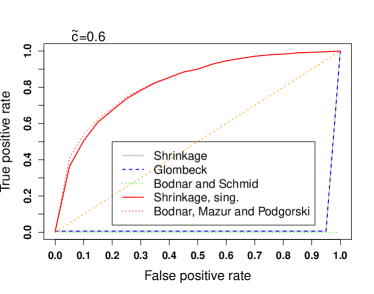

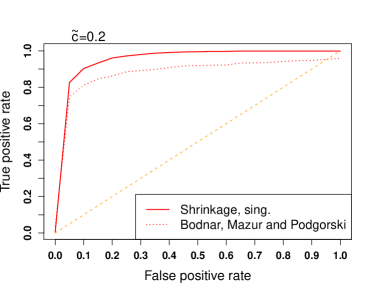

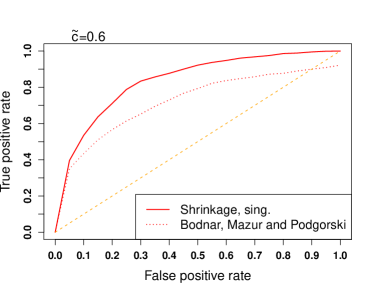

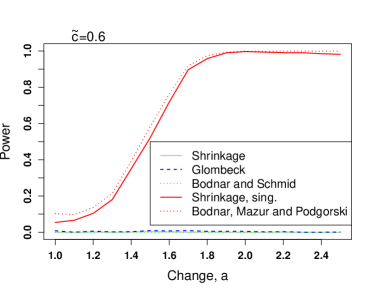

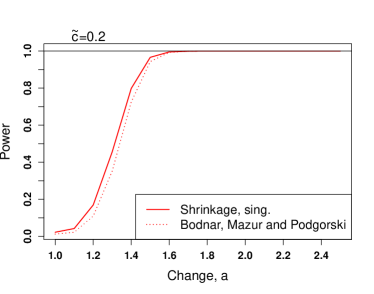

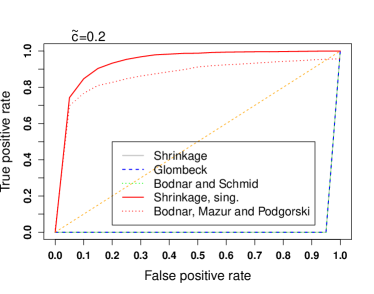

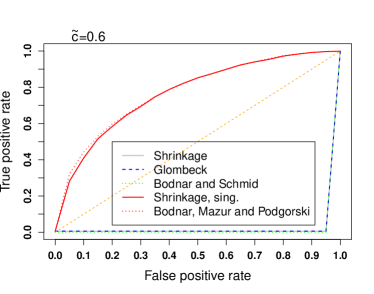

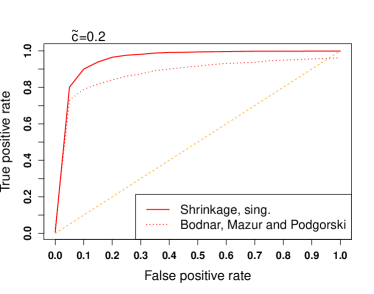

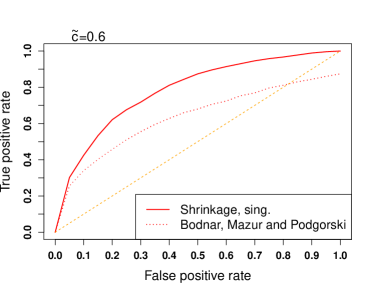

In this section, we present the results of a simulation study to compare the power functions and the ROC (Receiver Operating Characteristic) curves of three tests in the case of a non-singular covariance matrix, of five tests when is singular and , and of two tests when is singular and . Our simulation study is based on independent realizations of . The significance level is chosen to be in the figures showing the power functions and in the figures with the ROC curves. We set , choose when is non-singular, and use in the singular case. Furthermore, we consider in the singular case.

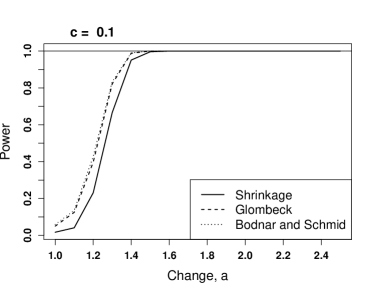

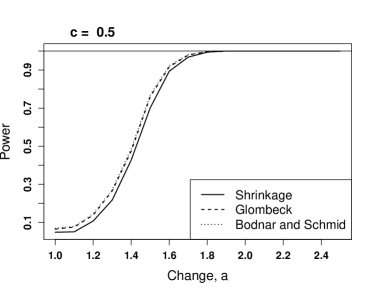

In order to illustrate the performance of the tests based on the shrinkage approach, the test based on the statistic of Bodnar and Schmid (2008), and the test proposed by Glombeck (2014) for the non-singular covariance matrix, the empirical power functions for the general hypothesis are evaluated for (Figure 3) and (Figure 5) while the ROC curves are presented in Figure 4 () and Figure 6 ().

In Figure 3, where of the eigenvalues of the covariance matrix are contaminated, we observe a slow increase of the power functions for and a better behaviour for smaller values of . In the case , there is no significant difference in the performance of the tests. For all considered values of , the power curves of Glombeck’s test and the test of Bodnar and Schmid (2008) are very close to each other and they lie slightly above the power curve of the test based on the shrinkage approach. Some larger deviations are present in the case . While in terms of the power the tests of Glombeck (2014) and of Bodnar and Schmid (2008) outperform the test based on the shrinkage approach, the opposite conclusion is drawn when the tests are compared by using their ROC curves. Here, we observe that the new approach performs better than the other two competitors. These two different performance results can be explained by the observation that the test based on the shrinkage approach tends to be in general undersized for small values of which are not of great importance for the proposed high-dimensional approach. Finally, we observe a similar behavior of the tests in terms of both the power functions and the ROC curves in Figures 5 and 6 for .

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

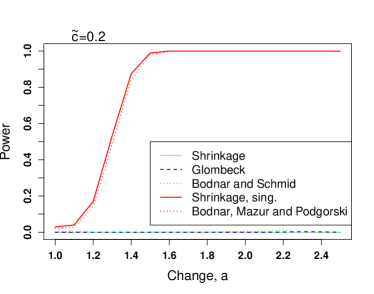

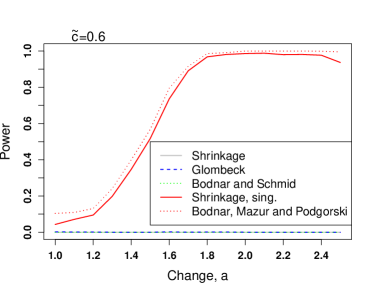

In Figures 7 to 10, we present the results in the case of the singular covariance matrix with two possible values for the ranks, namely which corresponds to . It is remarkable that all three tests, which do not take into account the singularity of the covariance matrix, perform very bad. Both the power functions and the ROC curves are very close to zero in all considered cases. This is due to the fact that under the null hypothesis the computed asymptotic variances for all test statistics are considerably large since the singularity of the covariance matrix was ignored in their derivations. In contrast, the tests of Section III.C, which take into account this singularity in their derivations, provide improvements in both the expressions of the resulting test statistics and in their asymptotic distributions.

Further, we note a very good performance of the test based on the shrinkage approach that takes the singularity of the covariance matrix into account. It outperforms other approaches in almost all considered cases independently of the choice of the performance criterion. Only for and , the test of Bodnar, Mazur and Podgórski (2016) shows a slightly better power function but this is due to the fact that its type I error is larger. Finally, in terms of the ROC curve the test of Bodnar, Mazur and Podgórski (2016) has not a good performance for moderate and large values of the false positive rate. This result is expected since, the test of Bodnar, Mazur and Podgórski (2016) is a multiple test whose critical values are obtained by employing the Bonferroni correction which appears to be very conservative for moderate and large significance values of the test.

V Summary

The main focus of this study is the inference of the GMVP weights. After constructing an optimal portfolio, an investor is interested to know whether or not the weights of the portfolio he is holding are still optimal at a fixed time point. For that reason, we investigate several asymptotic and exact statistical procedures for detecting deviations in the weights of the GMVP. One test is based on the sample estimator of the GMVP weights, whereas another uses its shrinkage estimator. To the best of our knowledge, the shrinkage approach, which is very popular in point estimation, is applied in test theory for the first time. The asymptotic distributions of both test statistics are obtained under the null and alternative hypotheses in a high-dimensional setting. This finding is a great advantage with respect to other approaches that appear in the literature which do not elaborate on the distribution under the alternative hypothesis (e.g., Glombeck (2014)). Finally, we deal with the case of a singular covariance matrix by deriving new testing procedures for the weights of the GMVP that are adopted to the singularity. The distributions of the resulting test statistics are obtained under both the null and alternative hypothesis.

In order to compare the performances of the proposed procedures, the empirical power functions of the derived tests are determined. It is shown that the test based on the shrinkage approach performs uniformly better than the other tests considered in the analysis in terms of both the power function and the ROC curve comparisons when the covariance matrix is singular. The new approach appears to be very promising for testing the portfolio weights in a high-dimensional situation. For a specific scenario, we also have studied a problem how good the power function of the asymptotic test based on the Mahalanobis distance approximates the power of the corresponding test and found good results already for moderate sample size, like with . Surely, these results could not be considered as a general statement to the problem and further investigation in this direction should be done. A similar topic should also be investigated for the test based on a shrinkage estimator, although only asymptotic results are available in the latter case.

Acknowledgement

The authors would like to thank Professor Pier Luigi Dragotti, Professor Byonghyo Shim, Professor Mathini Sellathurai, and anonymous Reviewers for their helpful suggestions. This research was partly supported by the German Science Foundation (DFG) via the projects BO 3521/3-1 and SCHM 859/13-1 ”Bayesian Estimation of the Multi-Period Optimal Portfolio Weights and Risk Measures” and by the Swedish Research Council (VR) via the project ”Bayesian Analysis of Optimal Portfolios and Their Risk Measures”.

References

- (1)

- Abramowitz and Stegun (1964) Abramowitz, M. and Stegun, I. A. (1964). Pocketbook of Mathematical Functions, Verlag Harri Deutsch, Frankfurt(Main).

- Bai and Shi (2011) Bai, J. and Shi, S. (2011). Estimating high dimensional covariance matrices and its applications, Annals of Economics and Finance 12: 199–215.

-

Bai et al. (2011)

Bai, Z. D., Liu, H. X. and Wong, W. K. (2011).

Asymptotic properties of eigenmatrices of a large sample covariance

matrix, Ann. Appl. Probab. 21(5): 1994–2015.

https://doi.org/10.1214/10-AAP748 - Bai and Silverstein (2010) Bai, Z. and Silverstein, J. W. (2010). Spectral Analysis of Large Dimensional Random Matrices, Springer, New York.

- Bodnar, Dette and Parolya (2016) Bodnar, T., Dette, H. and Parolya, N. (2016). Spectral analysis of the Moore–Penrose inverse of a large dimensional sample covariance matrix, Journal of Multivariate Analysis 148: 160–172.

- Bodnar, Dette and Parolya (2019) Bodnar, T., Dette, H. and Parolya, N. (2019). Testing for independence of large dimensional vectors, The Annals of Statistics to appear.

- Bodnar et al. (2014) Bodnar, T., Gupta, A. K. and Parolya, N. (2014). On the strong convergence of the optimal linear shrinkage estimator for large dimensional covariance matrix, Journal of Multivariate Analysis 132: 215–228.

- Bodnar, Gupta and Parolya (2016) Bodnar, T., Gupta, A. K. and Parolya, N. (2016). Direct shrinkage estimation of large dimensional precision matrix, Journal of Multivariate Analysis 146: 223–236.

- Bodnar, Mazur and Podgórski (2016) Bodnar, T., Mazur, S. and Podgórski, K. (2016). Singular inverse Wishart distribution and its application to portfolio theory, Journal of Multivariate Analysis 143: 314–326.

- Bodnar et al. (2017) Bodnar, T., Mazur, S. and Podgórski, K. (2017). A test for the global minimum variance portfolio for small sample and singular covariance, AStA Advances in Statistical Analysis 101(3): 253–265.

- Bodnar and Okhrin (2008) Bodnar, T. and Okhrin, Y. (2008). Properties of the singular, inverse and generalized inverse partitioned Wishart distributions, Journal of Multivariate Analysis 99: 2389– 2405.

-

Bodnar, Okhrin and Parolya (2019)

Bodnar, T., Okhrin, Y. and Parolya, N. (2019).

Optimal shrinkage-based portfolio selection in high dimensions,

arXiv:1611.01958 .

http://adsabs.harvard.edu/abs/2016arXiv161101958B - Bodnar et al. (2018) Bodnar, T., Parolya, N. and Schmid, W. (2018). Estimation of the global minimum variance portfolio in high dimensions, European Journal of Operational Research, in press 266(1): 371–390.

- Bodnar and Schmid (2008) Bodnar, T. and Schmid, W. (2008). A test for the weights of the global minimum variance portfolio in an elliptical model, Metrika 67: 127–143.

- Britten-Jones (1999) Britten-Jones, M. (1999). The sampling error in estimates of mean-variance efficient portfolio weights, The Journal of Finance 54: 655–671.

- Bühlmann and Van De Geer (2011) Bühlmann, P. and Van De Geer, S. (2011). Statistics for High-Dimensional Data: Methods, Theory and Applications, Springer, Berlin, Heidelberg.

- Cai and Shen (2011) Cai, T. and Shen, X. (2011). High-Dimensional Data Analysis, World Scientific, Singapore.

- Cam and Yang (2000) Cam, L. and Yang, G. (2000). Asymptotics in Statistics: Some Basic Concepts, Springer, New York.

-

Clarke et al. (2011)

Clarke, R., de Silva, H. and Thorley, S. (2011).

Minimum-variance portfolio composition, The Journal of Portfolio

Management 37(2): 31–45.

https://jpm.iijournals.com/content/37/2/31 -

Clarke et al. (2006)

Clarke, R. G., de Silva, H. and Thorley, S. (2006).

Minimum-variance portfolios in the U.S. equity market, The

Journal of Portfolio Management 33(1): 10–24.

https://jpm.iijournals.com/content/33/1/10 - DasGupta (2008) DasGupta, A. (2008). Asymptotic Theory of Statistics and Probability, Springer, New York.

- DeMiguel, Garlappi, Francisco and Uppal (2009) DeMiguel, V., Garlappi, L., Francisco, N. and Uppal, R. (2009). A generalized approach to portfolio optimization: Improving performance by constraining portfolio norms, Management Science 55(5): 798– 812.

- DeMiguel, Garlappi and Uppal (2009) DeMiguel, V., Garlappi, L. and Uppal, R. (2009). Optimal versus naive diversification: How inefficient is the portfolio strategy?, The Review of Financial Studies 22(5): 1915– 1953.

- Efron and Morris (1976) Efron, B. and Morris, C. (1976). Families of minimax estimators of the mean of a multivariate normal distribution, Annals of Statistics 4: 11–21.

- Feng and Palomar (2016) Feng, Y. and Palomar, D. P. (2016). A Signal Processing Perspective on Financial Engineering, Vol. 9.

-

Frahm and Jaekel (2008)

Frahm, G. and Jaekel, U. (2008).

Tyler’s M-estimator, random matrix theory, and generalized

elliptical distributions with applications to finance, SSRN Electronic

Journal .

https://ssrn.com/abstract=1287683 - Frahm and Memmel (2010) Frahm, G. and Memmel, C. (2010). Dominating estimators for minimum-variance portfolios, Journal of Econometrics 159: 289–302.

- Gibbons et al. (1989) Gibbons, M. R., Ross, S. A. and Shanken, J. (1989). A test of the efficiency of a given portfolio, Econometrica 57: 1121–1152.

- Glombeck (2014) Glombeck, K. (2014). Statistical inference for high-dimensional global minimum variance portfolios, Scandinavian Journal of Statistics 41: 845–865.

- Golosnoy and Okhrin (2007) Golosnoy, V. and Okhrin, Y. (2007). Multivariate shrinkage for optimal portfolio weights, The European Journal of Finance 13: 441–458.

- Greville (1966) Greville, T. N. E. (1966). Note on the generalized inverse of a product matrix, SIAM Review 8(4): 518–521.

- Gupta and Nagar (2000) Gupta, A. and Nagar, D. (2000). Matrix variate distributions, Chapman and Hall/CRC, Boca Raton.

- Jagannathan and Ma (2003) Jagannathan, R. and Ma, T. (2003). Risk reduction in large portfolios: Why imposing the wrong constraints helps, The Journal of Finance 58(4): 1651– 1683.

- Jobson and Korkie (1981) Jobson, J. and Korkie, B. M. (1981). Performance hypothesis testing with the Sharpe and Treynor measures, The Journal of Finance 36: 889–908.

- Jorion (1986) Jorion, P. (1986). Bayes-Stein estimation for portfolio analysis, Journal of Financial and Quantitative Analysis 21: 279–292.

- Laloux et al. (2000) Laloux, L., Cizeau, P., Potters, M. and Bouchaud, J.-P. (2000). Random matrix theory and financial correlations, International Journal of Theoretical and Applied Finance 3: 391–397.

-

Ledoit and Wolf (2004)

Ledoit, O. and Wolf, M. (2004).

Honey, I shrunk the sample covariance matrix, The Journal of

Portfolio Management 30(4): 110–119.

https://jpm.iijournals.com/content/30/4/110 - Ledoit and Wolf (2012) Ledoit, O. and Wolf, M. (2012). Nonlinear shrinkage estimation of large-dimensional covariance matrices, The Annals of Statistics 40(2): 1024–1060.

- Li et al. (2004) Li, J., Stoica, P. and Wang, Z. (2004). Doubly constrained robust capon beamformer, IEEE Transactions on Signal Processing 52(9): 2407–2423.

- Markowitz (1952) Markowitz, H. (1952). Portfolio selection, The Journal of Finance 7: 77–91.

- Memmel and Kempf (2006) Memmel, C. and Kempf, A. (2006). Estimating the global minimum variance portfolio, Schmalenbach Business Review 58: 332–348.

- Mestre and Lagunas (2006) Mestre, X. and Lagunas, M. (2006). Finite sample size effect on MV beamformers: optimum diagonal loading factor for large arrays, IEEE Transactions on Signal Processing 54(1): 69–82.

- Muirhead (1982) Muirhead, R. J. (1982). Aspects of Multivariate Statistical Theory, Wiley, New York.

- Okhrin and Schmid (2006) Okhrin, Y. and Schmid, W. (2006). Distributional properties of portfolio weights, Journal of Econometrics 134: 235–256.

- Okhrin and Schmid (2007) Okhrin, Y. and Schmid, W. (2007). Comparison of different estimation techniques for portfolio selection, AStA Advances in Statistical Analysis 91: 109–127.

- Okhrin and Schmid (2008) Okhrin, Y. and Schmid, W. (2008). Estimation of optimal portfolio weights, International Journal of Theoretical and Applied Finance 11: 249–276.

- Pappas et al. (2010) Pappas, D., Kiriakopoulos, K. and Kaimakamis, G. (2010). Optimal portfolio selection with singular covariance matrix, International Mathematical Forum 5: 2305–2318.

- Rubio and Mestre (2011) Rubio, F. and Mestre, X. (2011). Spectral convergence for a general class of random matrices, Statistics & Probability Letters 81(5): 592 – 602.

- Rubio et al. (2012) Rubio, F., Mestre, X. and Palomar, D. P. (2012). Performance analysis and optimal selection of large minimum variance portfolios under estimation risk, IEEE Journal of Selected Topics in Signal Processing 6(4): 337–350.

- Stein (1956) Stein, C. (1956). Inadmissibility of the usual estimator for the mean of a multivariate normal distribution, Proceedings of the Third Berkeley Symposium on Mathematical Statistics and Probability, Volume 1: Contributions to the Theory of Statistics, University of California Press, Berkeley, California: 197–206.

- Van Trees (2002) Van Trees, H. L. (2002). Optimum Array Processing, New York: Wiley.

- Verdú (1998) Verdú, S. (1998). Multiuser Detection, New York: Cambridge Univ. Press.

- Yao et al. (2015) Yao, J., Zheng, S. and Bai, Z. (2015). Large Sample Covariance Matrices and High-Dimensional Data Analysis, Cambridge Series in Statistical and Probabilistic Mathematics, Cambridge University Press.

- Zhang et al. (2013) Zhang, M., Rubio, F., Mestre, X. and Palomar, D. (2013). Improved calibration of high-dimensional precision matrices, IEEE Transactions on Signal Processing 61(6): 1509–1519.

Appendix

In this section, the proofs of Theorems are given.

Let the symbol denote equality in distribution. In Lemma 5, we first derive a stochastic representation for .

Lemma 5

Under the conditions of Theorem 1, the stochastic representation of is expressed as

| (33) |

where , , , and ; , , , and are independent.

Proof:

of Lemma 5: Let be a matrix such that , i.e., it transforms the vector of the estimated GMVP weights into the vector of its first components. We define and

with , , , , , and .

Since (-dimensional Wishart distribution with degrees of freedom and covariance matrix ) and we get with Muirhead (1982, Theorem 3.2.11) that

and, consequently (see, Gupta and Nagar (2000, Theorem 3.4.1)),

Recalling the definition of and , we get from Theorem 3 of Bodnar and Okhrin (2008) that

-

1.

is independent of and

-

2.

and, consequently,

(34) -

3.

or, equivalently,

where the conditional distribution does not depend on , i.e., and are independent of . Hence,

(35)

Let

Then, and are independent, and the application of (35) leads to

with

Moreover, in using (cf. Muirhead (1982, Theorems 3.2.10 and 3.2.11)), we obtain

| (36) | |||||

where .

The last equality shows that the conditional distribution of given depends only on over , and, consequently, the conditional distribution coincides with . Using the distributional properties of the non-central -distribution, we obtain the following stochastic representation for given by

and, hence,

where , , , and ; , , , and are independent. ∎

Proof:

In order to stress the dependence on , we use the notation in the proofs of the asymptotic results. For the proof of Theorem 2 we apply Lemma 6. It must be mentioned that Proposition 3 of Glombeck (2014) is not fully correct that is why we can not use this result in proving Lemma 6.

Lemma 6

Let

and denote the unit norm vectors

Proof:

of Lemma 6: Noting that with , the result of Lemma 6 follows by the direct application of Theorem 3 in Bai, Liu and Wong (2011), where it was proven that for as the following result holds

where

with

and the symbol denotes the Hadamard (entrywise) product of matrices. The function denotes the cumulative distribution function of the Marchenko-Pastur law (see, Bai and Silverstein (2010)) for given by

where . The moments of given in the matrix are already calculated in Glombeck (2014, Lemma 14) and, thus, it holds

At last, after elementary calculus the result follows. ∎

Proof:

of Theorem 2: First, the asymptotic distribution of is derived. We rewrite as

with

Then, it follows that

where the last equality follows from Lemma 6.

Since

it follows that

with

Furthermore,

Consequently, if as then

where we have used the equality

Since , it holds that , and, thus, the condition is always fulfilled. Taking into account the relation the proof of Theorem 2 is finished. ∎

In the proof of Theorem 3 we use the following two lemmas. Lemma 7 extends the results of Theorem 1 in Bodnar, Mazur and Podgórski (2016) to the case , while Lemma 8 presents a stochastic representation of similarly to the statement of Lemma 5 in the non-singular case.

Lemma 7

Let with and let be a matrix of constants of rank . Then it holds that

Proof:

of Lemma 7: The stochastic representation of is expressed as

| (38) |

Let be the singular value decomposition of where is the matrix of non-zero eigenvalues and is the semi-orthogonal matrix of the corresponding eigenvectors, i.e., . Then the stochastic representation of is given by

| (39) |

and, hence,

| (40) |

where .

Lemma 8

Under the conditions of Theorem 3, the stochastic representation of is expressed as

| (42) |

where , , , and ; , , , and are independent.

Proof:

Since and , the application of Lemma 7 leads to

and, consequently, has a non-singular Wishart distribution given by

Let

where and are defined in Section III.C.

Since has a non-singular Wishart distribution, following the proof of Lemma 5, we get that and are independent, , and

with

and where and

Hence,

where , , , and ; , , , and are independent. ∎

Proof:

In order to proof Proposition 1 we need the following lemma, which is a special case of Rubio and Mestre (2011, Theorem 1).

Lemma 9

Let a nonrandom -dimensional matrix possesses a uniformly bounded trace norm (sum of singular values) and let . Then it holds that

for as , where

| (43) |

Proof:

of Proposition 1: The proof is similar to the proof of Theorem 2.1 by Bodnar, Parolya and Schmid (2018) with a few important modifications due to the singularity of . Indeed, taking into account the equality (40) we have

where the Wishart matrix is nonsingular. Using now the properties of the Moore-Penrose inverse and (41) we get

| (44) | |||||

Moreover, note the following identities

| (45) |

Recall the optimal shrinkage intensity expressed as

| (46) |

Due to (44) and (45) it holds that for all

| (47) | |||||

| (48) | |||||

| (49) |

with and . The symbol stays for the limit .

Let

where both matrices and possess a bounded trace norm since

Then, for all , we get from Lemma 9

| (51) |

for as , where is given in (43). Using that and combining (Proof:) and (51) with (47) and (48) leads to

| (52) |

| (53) |

for as . Finally, using the equality

we get

for as . As a result,

| (54) |

for as . At last, the application of (52), (53) and (54) to (46) implies the result of Proposition 1. ∎

Proof:

of Theorem 4: Using the proof of Proposition 1 we can immediately deduce that Lemma 6 also holds in the case of singular covariance matrix with the only exception that the usual matrix inverse must be replaced by the Moore-Penrose inverse and must be replaced by , i.e., becomes . That is why the proof of Theorem 2 can be applied step by step again without any further changes. ∎