A semi-parametric estimation for max-mixture spatial processes

Abstract.

We propose a semi-parametric estimation procedure in order to estimate the parameters of a max-mixture model as an alternative to composite likelihood estimation. This procedure uses

the F-madogram. We propose to minimize the square difference between the theoretical F-madogram and an empirical one. We evaluate the performance of this estimator through a

simulation study and we compare our method to composite likelihood estimation. We apply our estimation procedure to daily rainfall data from East Australia.

Key words and phrases:

Spatial dependence measures, asymptotic dependence/independence, max-stable process, max-mixture, madogram1. Introduction

One of the main characteristic of environmental or climatic data is their spatial dependence. The dependencies may be strong even for large distances as observed for heat waves or

they may be strong at short distances and weak at larger distances, as observed for cevenol rainfall events. Many dependence structures may arise, for example, asymptotic

dependence, asymptotic independence, or both. Max-mixture models as defined in [wadsworth2012dependence] are a mixture between a max-stable process and an Asymptotic Independent (AI)

process. These kind of models may be useful to fit e.g. rainfall data (see [bacro2016flexible]).

The estimation of the parameters of these processes remains challenging. The usual way to estimate parameters in spatial contexts is to maximize the composite likelihood. For

example, in [padoan2010likelihood], [davison2012geostatistics] and many others, the composite likelihood maximization is used to estimate the parameters of max-stable processes. In

[bacro2016flexible] and [wadsworth2012dependence], it is used to estimate the parameters of max-mixture processes. Nevertheless, the estimation remains unsatisfactory in some

cases as it seems to have difficulties estimating the AI part. So that, an alternative should be welcomed.

We propose a semi-parametric estimation procedure as an alternative to composite likelihood maximization for max-mixture processes. Our procedure is a least square method on the -madogram. That

is, we minimize the squared difference between the theoretical -madogram and the empirical one. Some of literature deals with semi-parametric estimation in modeling spatial extremes. For

example, [northrop2015efficient] and [aghakouchak2010semi] provided semi-parametric estimators of extremal indexes. In [buhl2016Semiparametric], another semi-parametric procedure to

estimate model parameters is introduced. It is based a non linear least square method based on the extremogram for isotropic space-time Browen-Resnick max-stable processes. The

semi-parametric procedure that we propose in this study is close to that article.

Section 2 is dedicated to the main tools used in this study; it contains definitions of some spatial dependence measures and of different dependence structures (asymptotic

dependence/independence and mixture of them). In Section 3, we calculate an expression for the -madogram of max-mixture models. Section 4 is

devoted to estimation procedures of the parameters of max-mixture processes. We prove that our least square-madogram estimation is consistent, provided that the parameters

are identified by the -madogram.

In Section 5, simulation study is conducted, it allows us to evaluatere the performance of the estimation procedure. Section 6 is devoted to an application on rainfall

real data from East Australia. Finally, concluding remarks are discussed in Section 7.

2. Main tools used in the study

Throughout this study, the spatial process is assumed to be strongly stationary and isotopic. We recall some basic facts and definitions related to spatial extreme theory.

2.1. Dependence measures

The extremal dependence behavior of spatial processes may be described by several coefficient / measures.

The upper tail dependence coefficient (see[bacro2013measuring, sibuya1959bivariate]) is defined for a stationary spatial process on with margin

by:

| (2.1) |

The process is said AI (resp. AD) if for all (resp. ).

For any the coefficient can alternatively be expressed as the limit when of the function defined on into , by

| (2.2) |

Such that, .

For AI processes, cannot reveal the strength of the dependence. This is why the authors in [coles1999dependence], introduced an alternative dependance coefficient called

lower tail dependence coefficient . Consider for any

| (2.3) |

and .

If for all , the spatial process is asymptotically dependent. Otherwise, the process is asymptotically independent. Furthermore, if ( resp. ) the locations and (for any ) are asymptotically positively associated (resp. asymptotically negatively associated).

Another important measure of dependence is the extremal coefficient which was introduced by [buishand1984bivariate, schlather2003dependence].For any and and , let

is related with the upper tail dependence parameter; indeed if exists, we have the following relation (see [bacro2013measuring]):

where . In that case, may be approximated by for large.

This coefficient is particularly useful when dealing with asymptotic dependence, but useless in case of asymptotic independence. To overcome this problem, [ledford1996statistics] proposed a model allowing to gather all the different dependence behaviors. This model has Fréchet marginal laws and for all the pairwise survivor function is given by:

| (2.4) |

where is a slowly varying function and is the tail dependence coefficient. This coefficient determines the decay rate of the bivariate tail

probability for large . The interest of this simple modelization, which appears to be quite general, is that the coefficient provides a measure of the extremal dependence between

and .

(resp. and ), corresponds to asymptotic dependence (resp. asymptotic independence); see [bacro2013measuring, ledford1996statistics]. Finally, it is important to see the relation between and . If equation (2.4) is satisfied, then

.

Another classical tool often used in geostatistics is the variogram. But for spatial processes with Fréchet marginal laws, the variogram does not exist. We shall use the -madogram introduced in [cooley2006variograms] which is defined for any spatial process with univariate margin and for all

| (2.5) |

2.2. Spatial extreme models

For completeness, we recall definitions on max-stable, inverse max-stable and max-mixture processes.

2.3. Max-stable model

Max-stable processes are the extension of the multivariate extreme value theory to the infinite dimensional setting [buhl2016Semiparametric]. If there exist two sequences of continuous functions and such that for all and i.i.d. and a process, such that

| (2.6) |

then is a max-stable process [de2006spatial]. When for all , and , the margin distribution of the process is unit Fréchet, that is for any and ,

in that case, we say that is a simple max-stable porcess.

In [de1984spectral] it is proved that a max-stable process can be constructed by using a random process and a Poisson process. This representation is named the spectral

representation. Let be a max-stable process on . Then there exists i.i.d Poisson point process on , with intensity and a sequence

of i.i.d. copies of a positive process , such that for all such that

| (2.7) |

The c.d.f. of a simple max-stable process satisfies: (see [beirlant2006statistics], Section 8.2.2.)

| (2.8) |

where the function

| (2.9) |

is homogenous of order and is named the exponent measure. One of the interests of the exponent measure is its interpretation in terms of dependence. In fact, the homogeneity of the exponent measure implies

| (2.10) |

In Inequalities (2.10), the lower (resp. upper) bound corresponds to complete dependence (resp. independence).

For simple max-stable process, the extremal coefficient function , for any pairs of sites is the function defined on (or in in isotropic case) with values in by

| (2.11) |

We have

| (2.12) |

If for any , (resp. ), then we have complete dependence (resp. complete independence). The case , for all corresponds to asymptotic dependence. Remark that, for a simple max-stable process, the coefficients and coincide.

Furthermore, it is easy to see the relationship between and ; see [wadsworth2012dependence] for any

| (2.13) |

In the max-stable case, [cooley2006variograms] gives the relation for all ,

| (2.14) |

which appears to be helpful to estimate the extremal coefficient from the empirical madogram. The max-stable process with pairwise distribution function is given by the following equation, for all ,

| (2.15) |

We provide below three examples of well-known max-stable models represented by different exponent measures .

Smith Model (Gaussian extreme value model) [smith1990max] with unit Fréchet margin and exponent measure

| (2.16) |

and the standard normal cumulative distribution function. For isotropic case .

The pairwise extremal coefficient equals

Brown-Resnik Model [kabluchko2009stationary] with unit Fréchet margin and exponent measure

is a variogram and the standard normal cumulative distribution function. The pairwise extremal coefficient given by

Truncated extremal Gaussian Model (TEG) [schlather2002models] with unit Fréchet margin and exponent measure

| (2.17) |

The extremal coefficient is given by

| (2.18) |

where and is a random set which can consider it a disk with fixed radius . In such a case, (see [davison2013geostatistics]) and .

2.4. Inverse Max-stable processes

Max-stable processes are either asymptotically Dependent (AS) or independent. This means that they are not useful to model non trivial AI processes. In,[wadsworth2012dependence] a class of asymptotically independent processes is obtained by inverting max-stable processes. These processes are called inverse max-stable processes; their survivor function satisfy Equation (2.4). Let be a simple max-stable process with exponent measure . Let be defined by and . Then, is an asymptotic independent spatial process with unit Fréchet margin. The -dimensional joint survivor function satisfies

| (2.19) |

The tail dependent coefficient is given by , where is the extremal coefficient of the max-stable process . Moreover, we have . With a slight abuse of notations, we shall say that is the exponent measure of .

2.5. Max-mixture model

In spatial contexts, specifically in an environmental domain, many scenarios of dependence could arise and AD and AI might cohabite. The work by [wadsworth2012dependence] provides a flexible model called max-mixture.

Let be a simple max-stable process with extremal coefficient and bivariate distribution function , and let be an inverse max-stable process whose

tail dependence coefficient is . Its bivariate distribution function is denoted . Assume that and

are independent. Let and define

| (2.20) |

then unit Fréchet marginals and its pairwise survivor function satisfies

| (2.21) |

The process is called a max-mixture process. Assume there exists finite ; then,

| (2.22) |

and

| (2.23) |

Remark 2.1.

If there exists finite , then is asymptotically dependent up to distance and asymptotically independent for larger distances.

Of course, if then is AI and if then is a simple max-stable process.

In [bacro2016flexible] max-mixture processes are studied. The authors emphasize the fact that these models allow asymptotic dependence and independence to be present at a short and intermediate distances. Furthermore, the process may be independent at long distances (using e.g. TEG processes).

3. -madogram for max-mixture spatial process

In extreme value theory and therefore for spatial extremes, one of the main concerns is to find a dependence measure that can quantify the dependences between locations.

The and dependence measures are designed to quantify asymptotic dependence and asymptotic independence respectively (see equations (2.22) and

(2.23)). Max-mixture processes have been introduced in order to

provide both behaviors. We are then faced with the question of finding an adapted tool which would give information on more than one dependence structure.

In [cooley2006variograms], the -madogram has been introduced for max-stable processes. There exists several definitions of madograms. For example, in [naveau2009modelling], the

-madogram is considered in order to take into account the dependence information from the exponent measure when . This -madogram has been extended in

[fonseca2011generalized] to evaluate the dependence between two observations located in two disjoint regions in . [guillou2014madogram] adopted a -madogram suitable for

asymptotic independence instead of asymptotic dependence only. Finally, [bacro2010testing] used F-madogram as a test statistic for asymptotic independence bivariate maxima.

Below, we calculate for a max-mixture process. It appears that contrary to and , it combines the parameters coming from the AD and the AI parts.

Proposition 3.1.

Let be a max-mixture process, with mixing coefficient . Let be its max-stable part with extremal coefficient . Let be its inverse max-stable part with tail dependence coefficient . Then, the -madogram of is given by

| (3.1) |

where is beta function.

Proof.

We have

| (3.2) |

The equality leads to

| (3.3) |

Let , we have:

| (3.4) |

From definition of the max-mixture spatial process , we have

| (3.5) |

where (resp.) corresponding to the exponent measures of (resp. ) and . That leads to

We deduce that

| (3.6) |

where is the density of . Recall that because and return to equation (3.3) to get equation (3.1). ∎

In the particular cases where or , Proposition 3.1 reduces to known results for max-stable processes (see [cooley2006variograms]) and inverse max-stable processes (see [guillou2014madogram]). That is, the -madogram for a max-stable spatial process is given by

| (3.7) |

and the -madogram of an asymptotically independent spatial process is given by

| (3.8) |

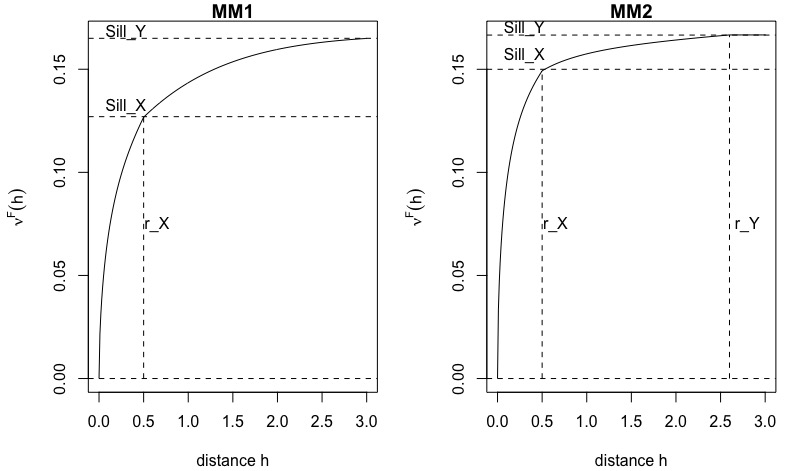

In order to have a comprehensive view of the behavior of , we have plotted in Figure 1 below . We have considered two max-mixture models MM1 and MM2 described as follows:

-

•

MM1 max-mixture between a TEG max-stable process and an inverse Smith max-stable process ;

-

•

MM2 max-mixture between as in MM1 and an inverse TEG max-stable process .

In this Figure and for the two models MM1 and MM2, has two sill one corresponding to and the second corresponding to . This is completely in accordance with the nested variogram concept as presented in [wackernagel1998multivariate]. In data analysis, these two levels of the sill gives the researcher a hint about whether there is more than one spatial dependence structure in the data.

Since the -madogram expresses with all the model parameters it should be useful for the parameter estimation.

4. Model inference

This section is devoted to the parametric inference for max-mixture processes. We begin with the presentation of the maximum composite likelihood estimation, then we present the least squares madogram estimation.

4.1. Parametric Estimation using Composite Likelihood

Consider , , be independent copies of a spatial process , observed at locations . Composite

likelihood inference is an appropriate approach in estimating the parameter models of a spatial process ([lindsay1888composite, varin2011overview]). Asymptotic properties of

this estimator has been proved in [davis2011comments]. This approach has been applied successfully to spatial max-stable processes by [davison2012geostatistics] and

[padoan2010likelihood] and is also used to identify the parameters of data exceedances over a large threshold, for example, [bacro2014estimation] and [thibaud2013threshold].

In this article, we focus on max-mixture models. Composite likelihood inference for max-mixture processes has been studied in [bacro2016flexible] and [wadsworth2012dependence].

We will compare our madogram based estimation to the composite likelihood estimation described in [bacro2016flexible].

If the pairwise density of can be computed and its parameter is identifiable, then it is possible to estimate by maximizing the pairwise weighted log likelihood. For simplicity, we denote for . Let

where

| (4.1) |

where is the likelihood of the pair and is the weight that specifies the contribution for each pair. In [padoan2010likelihood], it is suggested to

In [coles2001introduction], it is suggested to consider a censor approach of the likelihood, taking into account a threshold. This approach has been adopted in this study. Let be a pairwise distribution function and consider the thresholds and ; the likelihood contribution is

In [wadsworth2012dependence], the censored likelihood is used in order to improve the estimation of the parameters related to asymptotic independence. This censored approach was also applied by [bacro2016flexible] for the estimation of parameters of max-mixture processes. In that paper, the replications of are assumed to be -mixing rather than independent. We denote generically by the parameters of the model. In [bacro2016flexible], it is proved, under some smoothness assumptions on the composite likelihood, that the composite maximum likelihood estimator for max-mixture processes is asymptotically normal as goes to infinity with asymptotic variance

where , . The matrix is called the Godambe information matrix (see

[bacro2016flexible] and Theorem 3.4.7 in [guyon1995random]).

An estimator of is obtained from the Hessian matrix computed in the optimization algorithm. The variability matrix has to be

estimated too. In our context, we have independent replications of and is large compared with respect to the dimension of . Then, we can use the outer product of the estimation of

. Let

or by Monte Carlo simulation with explicit formula of (see section 5. in [varin2011overview]). In the case of samples of satisfying the -mixing property, the estimation of can be done using a subsampling technique introduced by [carlstein1986use]; this was used in [bacro2016flexible]. Finally, model selection can be done by using the composite likelihood information criterion [varin2005note]:

Considering several max-stable models, the one that has the smallest CLIC will be chosen. In [thibaud2013threshold], the criterion is proposed. It is close to Akaike information criterion (AIC).

4.2. Semi-parametric estimation using NLS of F-madogram

In this section, we shall define the non-linear least square estimation procedure of the parameters set corresponding to the max-mixture model using the -madogram. This procedure can be considered as an alternative method to the composite likelihood method.

Consider , copies of an isotropic max-mixture process with unit Fréchet marginal laws ( denotes the distribution function of a unit Fréchet law). It may be

independent copies for example, if the data is recorded yearly (see [naveau2009modelling]) or we shall consider that satisfies a -mixing property

([bacro2016flexible]). Let be a finite subset of , and , and . Therefore, for

, the vectors have the same law and are considered either independent or -mixing (in ). The main motivation for using the F-madogram in

estimation is that it contains the dependence structure information for a fixed of (see Section 3.2 in [bacro2010testing]).

In what follows, we make the assumption that the vectors are i.i.d. Note that from the definition of the -madogram, we have where

is the -madogram of with parameters defined in (3.1). If has an unknown true parameter on a compact set , we rewrite

| (4.2) |

The vectors are i.i.d errors with and is finite and unknown.

Let

| (4.3) |

Any vector in which minimizes will be called a least square estimate of :

| (4.4) |

Theorem 4.1.

Assume that is compact and that is continuous for all . We assume that the vectors are i.i.d. Let be least square estimators of . Then, any limit point (as goes to infinity) of satisfies for all .

Remark 4.1.

Of course, if is injective, then Theorem 4.1 implies that the least square estimation is consistent, i.e. a.s. as goes to infinity. In the examples considered below, it seems that the injectivity is satisfied provided , but we were unable to prove it.

Proof.

We follow the proof of Theorem II.5.1 in [antoniadis1992regression]. From (4.2), we have, for all

From the law of large numbers, we have

and for any ,

Therefore,

Take a sequence of least square estimators, taking if necessary a subsequence, we may assume that it converges to some . Using the continuity of , we have

Since is a least square estimator, . It follows that

and thus for all . ∎

The asymptotic normality of the least square estimators should also be obtained by following, e.g., [buhl2016Semiparametric] and using the asymptotic normality of the -madogram obtained in [cooley2006variograms]. Nevertheless, the calculation of the asymptotic variance will require to calculate the covariances between and , which is not straightforward.

5. Simulation study

This section is devoted to some simulations in order to evaluate the performance of the least square estimator and to compare it with the maximum composite likelihood estimator. Recall that denotes the least square estimator of the parameter vector and denotes the composite likelihood estimator.

5.1. Outline the simulation experiment

In order to evaluate the performance of the non-linear least square estimator as defined in (3.1), we have generated data from the model MM1 above.

The least square madogram estimator has been compared with true one and also with parameters estimated by maximum composite likelihood

proposed in [bacro2016flexible, wadsworth2012dependence], on the same simulated data. We considered sites randomly and uniformly distributed in the square .

We have generated i.i.d observations for each site and replicated this experiment times. We have considered several mixing parameters:

. For the composite likelihood estimator , we used the censored procedure with the empirical quantile of data at each site as threshold .

The fitting of was done using the code which was used in [bacro2016flexible] with some appropriated modifications.

5.2. Results on the parameters estimate

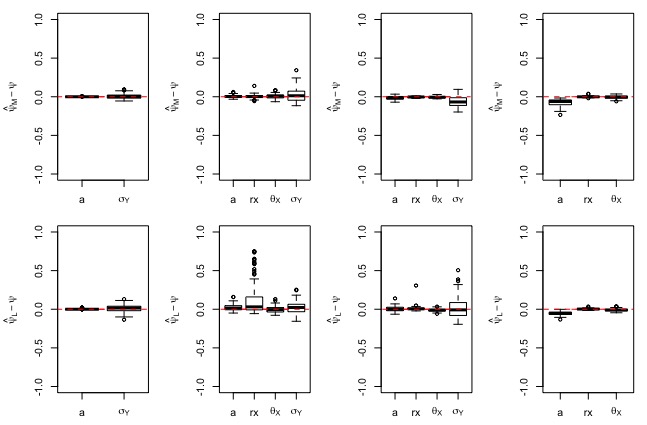

In Figure 3, we represented the boxplots of the errors, that is and for model

MM1. Generally, the estimators above worked well, although the variability in some estimates were relatively large, especially for the asymptotic independence parameters. It also shows some bias in

the estimation of the asymptotic independence model parameters.

It is well known that asymptotic independence is difficult to estimate (see [davison2013geostatistics]). Therefore, the estimation accuracy of the parameters is very sensitive. On one other

hand, the fitting of which appears in TEG models in (2.17), is delicate and might lead to quite different estimates with different data

[davison2012geostatistics].

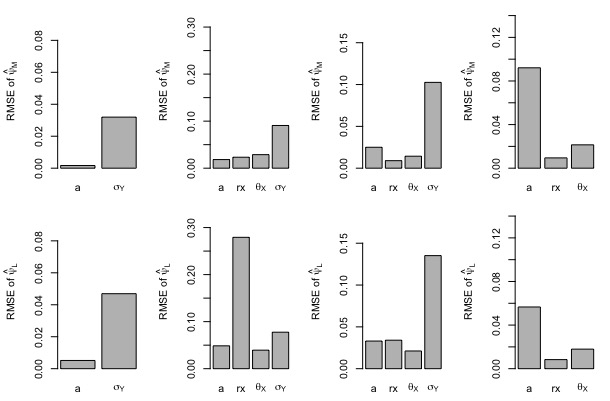

Another comparison indicator is the root mean square error (RMSE) ([zheng2015assessing, zheng2014modeling]): let denote the th estimation (either least square or composite likelihood estimation),

| (5.1) |

The barplot in Figure 3 displays the RMSE for each parameter of MM1 model. We see on these barplots that when is close to (), the estimator over-performs the estimator and vice versa when . For the performance of the two estimators seem equivalent.

5.3. Asymptotic normality

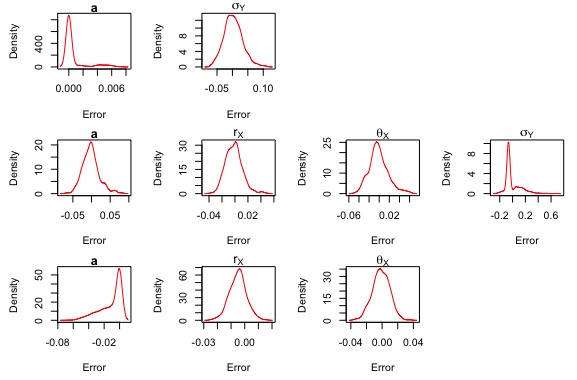

We may figure out whether the least square estimator is asymptotically normal through the graphe of the errors . In Figure 4, the graphs

represent the

distributions of the errors of each estimated parameters of MM1 model for . We did simulation experiments.

We can see on Figure 4 that the densities of the errors of the parameters seem close to the shape of centered normal distribution.

6. Real data example

In this section, we analyze a real data and fit it to some models considered in this study by composite likelihood and LS-madogram procedures.

6.1. Data analysis

We analyzed daily rainfall along the east coast of Australia. We selected 39 locations randomly from this region. The data is daily measured in the period from April to

September for 35 years from 1982-2016. The data is available from the Australian Bureau of Meteorology (http://www.bom.gov.au/climate/data/).

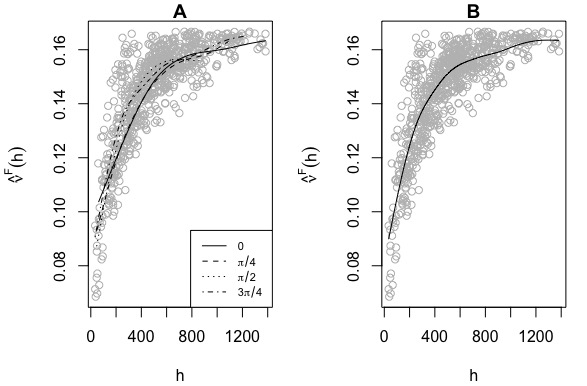

In order to explore the possibility of anisotropy of the spatial dependence, we used the same test as in [bacro2016flexible]. We divided all data set according to directional

sectors , , and , where indicate to north direction. We use the empirical F-madogram

. The directional loss smoothing of such empirical measure in the Figure 5. (A), shows no evidence of anisotropy.

In Figure 5. (B), the empirical F-madogram is plotted for the whose data set. It seems that asymptotic dependence between the locations is present up to

distance 500 km and asymptotic independence could be present at the remaining distance.

6.2. Data fitting

Our interest in this section is to chose a reasonable model for the data. We considered models described below, for each model, the parameters are estimated by LS-madogram and maximum composite likelihood. The selection criteria for LS-madogram estimator is computed as the following:

where is the number of parameters in the model and is the number of the observations, that is: , where is the number of observed pairs. With

respect to censored composite likelihood estimators we adopted the CLIC selection criteria. The two criteria selected the model MM1 as the best model.

We consider the following models:

- MM1:

-

max-mixture between asymptotic dependence process represented by TEG max-stable process with exponential correlation function and is a disk of fixed and unknown radius . The asymptotic independence is represented by an inverse Brown-Resnik max-stable process with variogram , ; is the sill of the variogram.

- MM2:

-

max-mixture between as in MM1 and an inverse inverse Smith max-stable process with .

- M1:

-

A TEG max-stable process specified in MM1.

- M2:

-

A Brown-Resnik max-stable process as specified in MM1.

- M3:

-

An inverse Brown-Resnik max-stable process as specified in MM1.

- M4:

-

A Smith max-stable process as specified in M2.

- M5:

-

A inverse Smith max-stable process as specified in M2.

For all the considered models, the margin distribution are assumed to be unit Fréchet. Therefore it requires to transform the data set to Fréchet. Most of papers (see for example [bacro2016flexible] and [wadsworth2012dependence]) use parametric transformations: they fit GEV parameters for each location separately and then transform the data to Fréchet. In this study, we adopted a non-parametric transformation by using the empirical c.d.f.. For censored composite likelihood procedures, we set and .

| Model | a | SC | |||||

|---|---|---|---|---|---|---|---|

| MM1 | CL | 0.262 | 1217.3 | 1364.5 | 3102.4 | 3.457 | 6807406 |

| LS | 0.259 | 1285.7 | 1390.0 | 5794.8 | 2.013 | 1.917034 | |

| MM2 | CL | 0.248 | 31.16 | 70.15 | 998.84 | 7924609 | |

| LS | 0.185 | 35.51 | 48.14 | 871.19 | 1.917234 | ||

| M1 | CL | 931 | 307.86 | 7926261 | |||

| LS | 1270 | 255.64 | 1.945177 | ||||

| M2 | CL | 931.02 | 3.078663 | 7926261 | |||

| LS | 361.36 | 1.90816 | 1.96165 | ||||

| M3 | CL | 1644.76 | 2.702282 | 7918643 | |||

| LS | 1383.08 | 1.394928 | 1.924574 | ||||

| M4 | CL | 85.34 | 8016633 | ||||

| LS | 193.43 | 1.988753 | |||||

| M5 | CL | 256.39 | 7988838 | ||||

| LS | 334.60 | 1.929235 |

We remark that the two Decision Criteria (CLIC and MIC) choose the same model. We would like to emphasize that CLIC and MIC are not comparable, one is related to the composite likelihood while the other one is related to the least squared madogram difference. For the tested models, we would keep the model with the smallest CLIC or the smallest MIC, depending on the used estimation method. Also, the least squared madogram estimation is involves less computations, indeed, the maximum composite likelihood estimation requires to estimate the Godambe matrix in order to compute the CLIC.

7. Conclusions

The calculation of the F-madogram for max-mixture processes show that it writes with both the AD and the AI parameters. This leads us to propose a semi-parametric estimation procedure using

F-madogram as an alternative to composite likelihood. The simulation study showed that the estimation procedure based on performs better than the composite likelihood

procedure when the model is near to asymptotic independence. We applied these estimator procedures to real data example. On the considered example, the results obtained by composite likelihood

maximization and least squared madogram difference are similar.

Acknowledgements: This work was supported by the LABEX MILYON (ANR-10-LABX-0070) of Université de Lyon, within the program “Investissements d’Avenir” (ANR-11-IDEX-0007) operated by

the French National Research Agency (ANR). We also acknowledge the projet LEFE CERISE.