Evaluating Probabilistic Forecasts with \pkgscoringRules

Alexander Jordan, Fabian Krüger, Sebastian Lerch

\PlaintitleEvaluating Probabilistic Forecasts with scoringRules

\ShorttitleEvaluating Probabilistic Forecasts

\Abstract

Probabilistic forecasts in the form of probability distributions over future events have become popular in several fields including meteorology, hydrology, economics, and demography. In typical applications, many alternative statistical models and data sources can be used to produce probabilistic forecasts. Hence, evaluating and selecting among competing methods is an important task. The \pkgscoringRules package for \proglangR provides functionality for comparative evaluation of probabilistic models based on proper scoring rules, covering a wide range of situations in applied work. This paper discusses implementation and usage details, presents case studies from meteorology and economics, and points to the relevant background literature.

\Keywordscomparative evaluation, ensemble forecasts, out-of-sample evaluation, predictive distributions, proper scoring rules, score computation, \proglangR

\Plainkeywordscomparative evaluation, ensemble forecasts, out-of-sample evaluation, predictive distributions, proper scoring rules, score computation, R

\Address

Alexander Jordan

University of Bern

Institute of Mathematical Statistics and Actuarial Science

Alpeneggstrasse 22

3012 Bern, Switzerland

E-Mail:

Fabian Krüger

Alfred-Weber-Institute for Economics

Heidelberg University

Bergheimer Str. 58

69115 Heidelberg, Germany

E-Mail:

URL: https://sites.google.com/site/fk83research/home

Sebastian Lerch

Heidelberg Institute for Theoretical Studies

HITS gGmbH

Schloss-Wolfsbrunnenweg 35

69118 Heidelberg, Germany

E-Mail:

URL: https://sites.google.com/site/sebastianlerch/

and

Institute for Stochastics

Karlsruhe Institute of Technology

Preface

This vignette corresponds to an article of the same name which has been conditionally accepted for publication at the Journal of Statistical Software. While the two articles are close to identical at the time of this writing (July 27, 2018), the vignette may be updated to reflect future changes in the package. To cite the package, please use Jordan et al. (2018a).

1 Introduction: Forecast evaluation

Forecasts are generally surrounded by uncertainty, and being able to quantify this uncertainty is key to good decision making. Accordingly, probabilistic forecasts in the form of predictive probability distributions over future quantities or events have become popular over the last decades in various fields including meteorology, climate science, hydrology, seismology, economics, finance, demography and political science. Important examples include the United Nation’s probabilistic population forecasts (Raftery et al., 2014), inflation projections issued by the Bank of England (e.g., Clements, 2004), or the now widespread use of probabilistic ensemble methods in meteorology (Gneiting and Raftery, 2005; Leutbecher and Palmer, 2008). For recent reviews see Gneiting and Katzfuss (2014) and Raftery (2016).

With the proliferation of probabilistic models arises the need for tools to evaluate the appropriateness of models and forecasts in a principled way. Various measures of forecast performance have been developed over the past decades to address this demand. Scoring rules are functions that evaluate the accuracy of a forecast distribution , given that an outcome was observed. As such, they allow to compare alternative models, a crucial ability given the variety of theories, data sources and statistical specifications available in many situations. Conceptually, scoring rules can be thought of as error measures for distribution functions: While the squared error measures the performance of a point forecast , a scoring rule measures the performance of a distribution forecast .

This paper introduces the \proglangR (\proglangR Core Team, 2017) software package \pkgscoringRules (Jordan et al., 2018b), which provides functions to compute scoring rules for a variety of distributions that come up in applied work, and popular choices of . Two main classes of probabilistic forecasts are parametric distributions and distributions that are not known analytically, but are indirectly described through a sample of simulation draws. For example, Bayesian forecasts produced via Markov chain Monte Carlo (MCMC) methods take the latter form. Hence, the \pkgscoringRules package provides a general framework for model evaluation that covers both classical (frequentist) and Bayesian forecasting methods.

The \pkgscoringRules package aims to be a comprehensive library for computing scoring rules. We offer implementations of several known (but not routinely applied) formulas, and implement some closed-form expressions that were previously unavailable. Whenever more than one implementation variant exists, we offer statistically principled default choices. The package contains the continuous ranked probability score () and the logarithmic score, as well as the multivariate energy score and variogram score. All of these scoring rules are proper, which means that forecasters have an incentive to state their true belief, see Section 2.

It is worth emphasizing that scoring rules are designed for comparative forecast evaluation. That is, one wants to know whether model A or model B provides better forecasts, in terms of a proper scoring rule. Comparative forecast evaluation is of interest either for choosing a specification for future use, or for comparing various scientific approaches. A distinct, complementary issue is to check the suitability of a given model via tools for absolute forecast evaluation. Here, the focus typically lies in diagnostics, e.g., whether the predictive distributions match the observations statistically (see probability integral transform histogram, e.g., in Gneiting and Katzfuss, 2014). To retain focus, the \pkgscoringRules package does not cover absolute forecast evaluation.

Comparative forecast evaluation shares key aspects with out-of-sample model comparison. In that sense, \pkgscoringRules is broadly related to all software packages which help users determine an appropriate model for the data at hand. Perhaps most fundamentally, the \pkgstats (\proglangR Core Team, 2017) package provides the traditional Akaike and Bayes information criteria to select among linear models in in-sample evaluation. The packages \pkgcaret (Kuhn et al., 2018) and \pkgforecast (Hyndman and Khandakar, 2008) provide cross-validation tools suitable for cross-sectional and time series data, respectively. The \pkgloo (Vehtari et al., 2018) package implements recent proposals to select among Bayesian models. In contrast to existing software, a key novelty of the \pkgscoringRules package is its extensive coverage of the . This scoring rule is attractive for both practical and theoretical reasons (Gneiting and Raftery, 2007; Krüger et al., 2016), yet more widespread use has been hampered by computational challenges. In providing analytical formulas and efficient numerical implementations, we hope to enable convenient use of the in applied work.

To the best of our knowledge, \pkgscoringRules is the first \proglangR package designed as a library for computing proper scoring rules for many types of forecast distributions. However, a number of existing \proglangR packages include scoring rule computations for more specific empirical situations: The \pkgensembleBMA (Fraley et al., 2018) and \pkgensembleMOS (Yuen et al., 2018) packages contain formulas for the CRPS of a small subset of the distributions listed in Table 1 which are relevant for post-processing ensemble weather forecasts (Fraley et al., 2011), and can only be applied to specific data structures utilized in the packages. The \pkgsurveillance (Meyer et al., 2017) package provides functions to compute the logarithmic score and other scoring rules for count data models in epidemiology. By contrast, the distributions contained in \pkgscoringRules are relevant in applications across disciplines and the score functions are generally applicable. The \pkgscoring (Merkle and Steyvers, 2013) package focuses on discrete (categorical) outcomes, for which it offers a large number of proper scoring rules. It is thus complementary to \pkgscoringRules which supports a wide range of forecast distributions while focusing on a smaller number of scoring rules. Furthermore, the \pkgverification (NCAR - Research Applications Laboratory, 2015) and \pkgSpecsVerification (Siegert, 2017) packages contain implementations of the CRPS for simulated forecast distributions. Our contribution in that domain is twofold: First, we offer efficient implementations to deal with predictive distributions given as large samples. MCMC methods are popular across the disciplines, and many sophisticated \proglangR implementations are available (e.g., Kastner, 2016; Carpenter et al., 2017). Second, we include various implementation options, and propose principled default settings based on recent research (Krüger et al., 2016).

For programming languages other than \proglangR, implementations of proper scoring rules are sparse, and generally cover a much narrower score computation functionality than the \pkgscoringRules package. The \pkgproperscoring (The Climate Corporation, 2015) package for the \proglangPython (\proglangPython Software Foundation, 2017) language provides implementations of the CRPS for Gaussian distributions and for forecast distributions given by a discrete sample. Several institutionally supported software packages include tools to compute scoring rules, but typically require input in specific data formats and are tailored towards operational use at meteorological institutions. The \proglangModel Evaluation Tools (Developmental Testbed Center, 2018) software provides code to compute the CRPS based on a sample from the forecast distribution. However, note that a Gaussian approximation is applied which can be problematic if the underlying distribution is not Gaussian, see Krüger et al. (2016). The \proglangEnsemble Verification System (Brown et al., 2010) also provides an implementation of the CRPS for discrete samples. For a general overview of software for forecast evaluation in meteorology, see Pocernich (2012).

The remainder of this paper is organized as follows. Section 2 provides some theoretical background on scoring rules, and introduces the logarithmic score and the continuous ranked probability score. Section 3 gives an overview of the score computation functionality in the \pkgscoringRules package and presents the implementation of univariate proper scoring rules. In Section 4, we give usage examples by application in case studies. In a meteorological example of accumulated precipitation forecasts, we compare ensemble system output from numerical weather prediction models to parametric forecast distributions from statistical post-processing models. A second case study shows how using analytical information of a Bayesian time series model for the growth rate of the US economy’s gross domestic product (GDP) can help in evaluating the model’s simulation output. Definitions and details on the use of multivariate scoring rules are provided in Section 5. The paper closes with a discussion in Section 6. Two appendices contain various closed-form expressions for the CRPS, as well as details on evaluating multivariate forecast distributions.

2 Theoretical background

Probabilistic forecasts usually fit one of two categories, parametric distributions or simulated samples. The former type is represented by its cumulative distribution function (CDF) or its probability density function (PDF), whereas the latter is often used if the predictive distribution is not available analytically. Here, we give a brief overview of the theoretical background for comparative forecast evaluation in both cases.

2.1 Proper scoring rules

Let denote the set of possible values of the quantity of interest, , and let denote a convex class of probability distributions on . A scoring rule is a function

that assigns numerical values to pairs of forecasts and observations . For now, we restrict our attention to univariate observations and set or subsets thereof, and identify probabilistic forecasts with the associated CDF or PDF . In Section 5, we will consider multivariate scoring rules for which .

We consider scoring rules to be negatively oriented, such that a lower score indicates a better forecast. For a proper scoring rule, the expected score is optimized if the true distribution of the observation is issued as a forecast, i.e., if

for all . A scoring rule is further called strictly proper if equality holds only if . Using a proper scoring rule is critical for comparative evaluation, i.e., the ranking of forecasts. In practice, the lowest average score over multiple forecast cases among competing forecasters indicates the best predictive performance, and in this setup, proper scoring rules compel forecasters to truthfully report what they think is the true distribution. See Gneiting and Raftery (2007) for a more detailed review of the mathematical properties.

| Distribution | Family arg. | CRPS | LogS | Additional parameters |

|---|---|---|---|---|

| Distributions for variables on the real line | ||||

| Laplace | \code"lapl" | ✓ | ✓ | |

| logistic | \code"logis" | ✓ | ✓ | |

| normal | \code"norm" | ✓ | ✓ | |

| mixture of normals | \code"mixnorm" | ✓ | ✓ | |

| Student’s | \code"t" | ✓ | ✓ | |

| two-piece exponential | \code"2pexp" | ✓ | ✓ | |

| two-piece normal | \code"2pnorm" | ✓ | ✓ | |

| Distributions for non-negative variables | ||||

| exponential | \code"exp" | ✓ | ✓ | |

| gamma | \code"gamma" | ✓ | ✓ | |

| log-Laplace | \code"llapl" | ✓ | ✓ | |

| log-logistic | \code"llogis" | ✓ | ✓ | |

| log-normal | \code"lnorm" | ✓ | ✓ | |

| Distributions with flexible support and/or point masses | ||||

| beta | \code"beta" | ✓ | ✓ | limits |

| uniform | \code"unif" | ✓ | ✓ | limits, point masses |

| exponential | \code"exp2" | ✓ | location, scale | |

| \code"expM" | ✓ | location, scale, point mass | ||

| gen. extreme value | \code"gev" | ✓ | ✓ | |

| gen. Pareto | \code"gpd" | ✓ | ✓ | point mass (CRPS only) |

| logistic | \code"tlogis" | ✓ | ✓ | limits (truncation) |

| \code"clogis" | ✓ | limits (censoring) | ||

| \code"gtclogis" | ✓ | limits, point masses | ||

| normal | \code"tnorm" | ✓ | ✓ | limits (truncation) |

| \code"cnorm" | ✓ | limits (censoring) | ||

| \code"gtcnorm" | ✓ | limits, point masses | ||

| Student’s | \code"tt" | ✓ | ✓ | limits (truncation) |

| \code"ct" | ✓ | limits (censoring) | ||

| \code"gtct" | ✓ | limits, point masses | ||

| Distributions for discrete variables | ||||

| binomial | \code"binom" | ✓ | ✓ | |

| hypergeometric | \code"hyper" | ✓ | ✓ | |

| negative binomial | \code"nbinom" | ✓ | ✓ | |

| Poisson | \code"pois" | ✓ | ✓ | |

Popular examples of proper scoring rules for include the logarithmic score and the continuous ranked probability score. The logarithmic score (LogS; Good, 1952) is defined as

where admits a PDF , and is a strictly proper scoring rule relative to the class of probability distributions with densities. The continuous ranked probability score (Matheson and Winkler, 1976) is defined in terms of the predictive CDF and is given by

| (1) |

where denotes the indicator function which is one if and zero otherwise. If the first moment of is finite, the CRPS can be written as

where and are independent random variables with distribution , see Gneiting and Raftery (2007). The CRPS is a strictly proper scoring rule for the class of probability distributions with finite first moment. Closed-form expressions of the integral in Equation 1 can be obtained for many parametric distributions and allow for exact and efficient computation of the CRPS. They are implemented in the \pkgscoringRules package for a range of parametric families, see Table 1 for an overview, and are provided in Appendix A.

2.2 Model assessment based on simulated forecast distributions

In various applications, the forecast distribution of interest is not available in an analytic form, but only through a simulated sample . Examples include Bayesian forecasting applications where the sample is generated by a MCMC algorithm, or ensemble weather forecasting applications where the different sample values are generated by numerical weather prediction models with different model physics and/or initial conditions. In order to compute the value of a proper scoring rule, the simulated sample needs to be converted into an estimated distribution (say, ) that can be evaluated at any point . The implementation choices and default settings in the \pkgscoringRules package follow the findings of Krüger et al. (2016) who provide a systematic analysis of probabilistic forecasting based on MCMC output.

For the CRPS, the empirical CDF

is a natural approximation of the predictive CDF. In this case, the CRPS reduces to

| (2) |

which allows one to compute the CRPS directly from the simulated sample, see Grimit et al. (2006). Implementations of Equation 2 are rather inefficient with computational complexity , and can be improved upon with representations using the order statistics , i.e., the sorted simulated sample, thus achieving an average performance. In the \pkgscoringRules package, we use an algebraically equivalent representation of the CRPS based on the generalized quantile function (Laio and Tamea, 2007), leading to

| (3) |

which Murphy (1970) reported in the context of the precursory, discrete version of the CRPS. We refer to Jordan (2016) for details.

In contrast to the CRPS, the computation of LogS requires a predictive density. An estimator can be obtained with classical nonparametric kernel density estimation (KDE, e.g. Silverman, 1986). However, this estimator is valid only under stringent theoretical assumptions and can be fragile in practice: If the outcome falls into the tails of the simulated forecast distribution, the estimated score may be highly sensitive to the choice of the bandwidth tuning parameter. In an MCMC context, a mixture-of-parameters estimator that utilizes a simulated sample of parameter draws rather than draws from the posterior predictive distribution is a better and often much more efficient choice, see Krüger et al. (2016). This mixture-of-parameters estimator is specific to the model being used, in that one needs to know the analytic form of the forecast distribution conditional on the parameter draws. If such knowledge is available, the mixture-of-parameters estimator can be implemented using functionality for parametric forecast distributions. We provide an example in Section 4.2. This example features a conditionally Gaussian forecast distribution, a typical case in applications.

3 Package design and functionality

The main functionality of \pkgscoringRules is the computation of scores. The essential functions for this purpose follow the naming convention \code[score]_[suffix](), where the two maturest choices for \code[score] are \codecrps and \codelogs. Regarding the \code[suffix], we aim for analogy to the usual d/p/q/r functions for parametric families of distributions, both in terms of naming convention and usage details, e.g., {Code} crps_norm(y, mean = 0, sd = 1, location = mean, scale = sd) Based on these computation functions, package developers may write S3 methods that hook into the respective S3 generic functions, currently limited to {Code} crps(y, …) logs(y, …) As the implementation of additional scoring rules matures, this list will be extended. We reserve methods for the class ‘\codenumeric’, e.g., {Code} crps.numeric(y, family, …) which are pedantic wrappers for the corresponding \code[score]_[family]() functions, but with meaningful error messages, making the ‘\codenumeric’ class methods more suitable for interactive use as opposed to numerical score optimization or package integration. Table 1 gives a list of the implemented parametric families, as does the ‘\codenumeric’ class method documentation for the respective score, e.g., see \code?crps.numeric.

Echoing the distinction in Section 2 between parametric and empirical predictive distributions, we note that computation functions following the naming scheme \code[score]_sample(), see Sections 3.2 and 5, have a special status and cannot be called via the ‘\codenumeric’ class method.

3.1 Parametric predictive distributions

When the predictive distribution comes from a parametric family, we have two options to perform the score computation and get the resulting vector of score values, i.e., via the score generics or the computation function. For a Gaussian distribution:

R> library("scoringRules")R> obs <- rnorm(10)R> crps(obs, "norm", mean = c(1:10), sd = c(1:10))

[1] 0.288 1.625 1.570 2.003 2.744 3.688 3.270 4.884 4.162 6.067

R> crps_norm(obs, mean = c(1:10), sd = c(1:10))

[1] 0.288 1.625 1.570 2.003 2.744 3.688 3.270 4.884 4.162 6.067 The results are identical, except when the much stricter input checks of the ‘\codenumeric’ class method are violated. This helps in detecting manual errors during interactive use, or in debugging automated model fitting and evaluation. Other restrictions in the ‘\codenumeric’ class method include the necessity to pass input to all arguments, i.e., default values in the computation functions are ignored, and that all numerical arguments should be vectors of the same length, with the exception that vectors of length one will be recycled. In contrast, the computation functions aim to closely obey standard \proglangR conventions.

In package development, we expect predominant use of the computation functions, where developers will handle regularity checks themselves. As a trivial example, we define functions that only depend on the argument \codey and compute scores for a fixed predictive gamma distribution:

R> crps_y <- function(y) crps_gamma(y, shape = 2, scale = 1.5)R> logs_y <- function(y) logs_gamma(y, shape = 2, scale = 1.5)

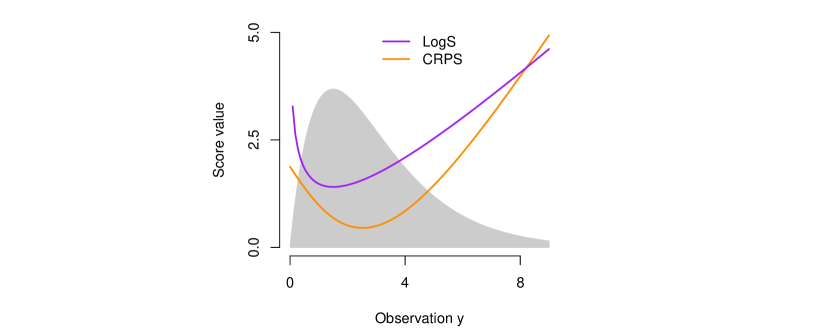

In Figure 1 these functions are used to illustrate the dependence between the score value and the observation in an example of a gamma distribution as forecast. The logarithmic score rapidly increases at the right-sided limit of zero, and the minimum score value is attained if the observation equals the predictive distribution’s mode. By contrast, the CRPS is more symmetric around the minimum that is attained at the median value of the forecast distribution, particularly, it increases more slowly as the observation approaches zero.

3.2 Simulated predictive distributions

Often forecast distributions can only be given as simulated samples, e.g., ensemble systems in weather prediction (Section 4.1) or MCMC output in econometrics (Section 4.2). We provide functions for both univariate and multivariate samples. The latter are discussed in Section 5, whereas the former are presented here: {Code} crps_sample(y, dat, method = "edf", w = NULL, bw = NULL, num_int = FALSE, show_messages = TRUE) logs_sample(y, dat, bw = NULL, show_messages = FALSE) The input for \codey is a vector of observations, and the input for \codedat is a matrix with the number of rows matching the length of \codey and each row comprising one simulated sample, e.g., for a Gaussian predictive distribution:

R> obs_n <- c(0, 1, 2)R> sample_nm <- matrix(rnorm(3e4, mean = 2, sd = 3), nrow = 3)R> crps_sample(obs_n, dat = sample_nm)

[1] 1.216 0.833 0.710

R> logs_sample(obs_n, dat = sample_nm)

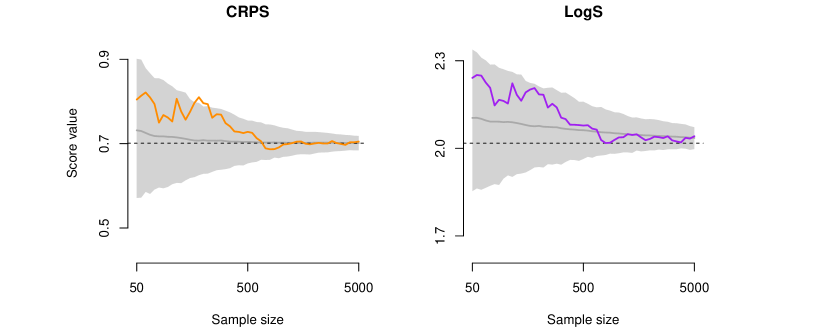

[1] 2.29 2.10 2.04 When \codey has length one then \codedat may also be a vector. Random sampling from the forecast distribution can be seen as an option to approximate the values of the proper scoring rules. To empirically assess the quality of this approximation and to illustrate the use of the score functions, consider the following Gaussian toy example, where we examine the performance of forecasts given as samples of size up to . The approximation experiment is independently repeated times:

R> R <- 500R> M <- 5e3R> mgrid <- exp(seq(log(50), log(M), length.out = 51))R> crps_approx <- matrix(NA, nrow = R, ncol = length(mgrid))R> logs_approx <- matrix(NA, nrow = R, ncol = length(mgrid))R> obs_1 <- 2R> for (r in 1:R) {+ sample_M <- rnorm(M, mean = 2, sd = 3)+ for (i in seq_along(mgrid)) {+ m <- mgrid[i]+ crps_approx[r, i] <- crps_sample(obs_1, dat = sample_M[1:m])+ logs_approx[r, i] <- logs_sample(obs_1, dat = sample_M[1:m])+ }+ }

In this case, the true CRPS and LogS values can be computed using the \codecrps() and \codelogs() functions. Figure 2 graphically illustrates how the scores based on sampling approximations become more accurate as the sample size increases.

The \codemethod argument controls which approximation method is used in \codecrps_sample(), with possible choices given by \code"edf" (empirical distribution function) and \code"kde" (kernel density estimation). The default choice \code"edf" corresponds to computing the approximation from Equation 2, implemented as in Equation 3. A vector or matrix of weights, matching the input for \codedat, can be passed to the argument \codew to compute the CRPS, for any distribution with a finite number of outcomes.

For kernel density estimation, i.e., the default in \codelogs_sample() and the corresponding \codemethod in \codecrps_sample(), we use a Gaussian kernel to estimate the predictive distribution. Kernel density estimation is an unusual choice in the case of the CRPS, but it is the only implemented option for evaluating the LogS of a simulated sample. In particular, the empirical distribution function is not applicable to LogS because an estimated density is required. The \codebw argument allows one to manually select a bandwidth parameter for kernel density estimation; by default, the \codebw.nrd() function from the \pkgstats (\proglangR Core Team, 2017) package is employed.

4 Usage examples

4.1 Probabilistic weather forecasting via ensemble post-processing

In numerical weather prediction (NWP), physical processes in the atmosphere are modeled through systems of partial differential equations that are solved numerically on three-dimensional grids. To account for major sources of uncertainty, weather forecasts are typically obtained from multiple runs of NWP models with varying initial conditions and model physics resulting in a set of deterministic predictions, called the forecast ensemble. While ensemble predictions are an important step from deterministic to probabilistic forecasts, they tend to be biased and underdispersive (such that, empirically, the actual observation falls outside the range of the ensemble too frequently). Hence, ensembles require some form of statistical post-processing. Over the past decade, a variety of approaches to statistical post-processing has been proposed, including non-homogeneous regression (Gneiting et al., 2005) and Bayesian model averaging (Raftery et al., 2005).

Here we illustrate how to evaluate post-processed ensemble forecasts of precipitation, based on data and methods from the \pkgcrch (Messner et al., 2016) package for \proglangR. We model the conditional distribution of precipitation accumulation, , given the ensemble forecasts using censored non-homogeneous regression models of the form

| (4) | |||||

| (5) |

where is the CDF of a continuous parametric distribution with parameters . Equations 4 and 5 specify a mixed discrete-continuous forecast distribution for precipitation: There is a positive probability of observing no precipitation at all (), however, if , it can take many possible values . In order to incorporate information from the raw forecast ensemble, we let be a function of , i.e., we use features of the raw ensemble to determine the parameters of the forecast distribution. Specifically, we consider different location-scale families and model the location parameter as a linear function of the ensemble mean ,

and the scale parameter as a linear function of the logarithm of the standard deviation of the ensemble,

A logarithmic link function is used to ensure positivity of the scale parameter. The coefficients can be estimated using maximum likelihood approaches implemented in the \pkgcrch package. The choice of a suitable parametric family is not obvious. Following Messner et al. (2016), we thus consider three alternative choices: the logistic, Gaussian, and Student’s distributions. For details and further alternatives, see, e.g., Messner et al. (2014); Scheuerer (2014) and Scheuerer and Hamill (2015a).

The \pkgcrch package contains a data set \codeRainIbk of precipitation for Innsbruck, Austria. It comprises ensemble forecasts \coderainfc.1, …, \coderainfc.11 and observations \coderain for 4971 cases from January 2000 to September 2013. The precipitation amounts are accumulated over three days, and the corresponding 11 member ensemble consists of accumulated precipitation amount forecasts between five and eight days ahead. Following Messner et al. (2016) we model the square root of precipitation amounts, and omit forecast cases where the ensemble has a standard deviation of zero. From Messner et al. (2016):

R> library("crch")R> data("RainIbk", package = "crch")R> RainIbk <- sqrt(RainIbk)R> ensfc <- RainIbk[, grep(’^rainfc’, names(RainIbk))]R> RainIbk$ensmean <- apply(ensfc, 1, mean)R> RainIbk$enssd <- apply(ensfc, 1, sd)R> RainIbk <- subset(RainIbk, enssd > 0) We split the data into a training set until November 2004, and an out-of-sample evaluation period (or test sample) from January 2005.

R> data_train <- subset(RainIbk, as.Date(rownames(RainIbk)) <= "2004-11-30")R> data_eval <- subset(RainIbk, as.Date(rownames(RainIbk)) >= "2005-01-01") Then, we estimate the censored regression models that are based on the logistic, Student’s , and Gaussian distributions, and produce the parameters of the forecast distributions for the evaluation period using built-in functionality of the \pkgcrch package. We only show the code for the Gaussian model since it can be adapted straightforwardly for the logistic and Student’s models.

R> CRCHgauss <- crch(rain ~ ensmean | log(enssd), data_train,+ dist = "gaussian", left = 0)R> gauss_mu <- predict(CRCHgauss, data_eval, type = "location")R> gauss_sc <- predict(CRCHgauss, data_eval, type = "scale")

The raw ensemble of forecasts is a natural benchmark for comparison since interest commonly lies in quantifying the gains in forecast accuracy that result from post-processing:

R> ens_fc <- data_eval[, grep(’^rainfc’, names(RainIbk))]

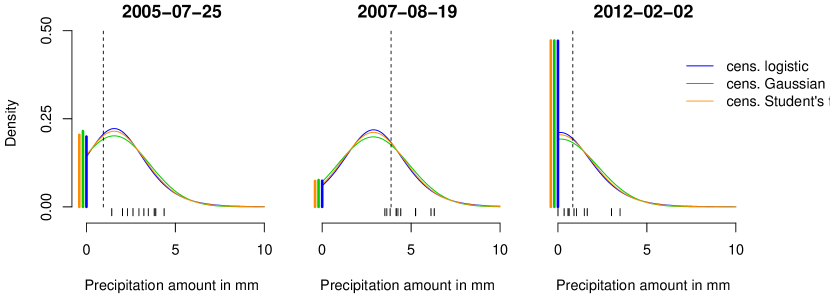

Figure 3 shows the models’ forecast distributions in three illustrative cases. To evaluate forecast performance in the entire out of sample period, we use the function \codecrps() for the model outputs and the function \codecrps_sample() to compute the CRPS of the raw ensemble. Note that we have to turn \codeens_fc into an object of class ‘\codematrix’ manually.

R> obs <- data_eval$rainR> gauss_crps <- crps(obs, family = "cnorm", location = gauss_mu,+ scale = gauss_sc, lower = 0, upper = Inf)R> ens_crps <- crps_sample(obs, dat = as.matrix(ens_fc))

The mean CRPS values indicate that all post-processing models substantially improve upon the raw ensemble forecasts. There are only small differences between the censored regression models, with the models based on the logistic and Student’s distributions slightly outperforming the model based on a normal distribution.

R> scores <- data.frame(CRCHlogis = logis_crps, CRCHgauss = gauss_crps,+ CRCHstud = stud_crps, Ensemble = ens_crps)R> sapply(scores, mean)

CRCHlogis CRCHgauss CRCHstud Ensemble 0.875 0.876 0.875 1.321

4.2 Bayesian forecasts of US GDP growth rate

We next present a representative example from economics, where the predictive distribution is given as a simulated sample. Hamilton (1989) first proposed the Markov switching autoregressive model to allow regime-dependent modeling, i.e., to capture different recurring time-series characteristics. We consider the following simple variant of the model:

where is the observed GDP growth rate of quarter , and is a latent state variable that represents two regimes in the residual variance . Since evolves according to a first-order Markov chain, the specification allows for the possibility that periods of high (or low) volatility cluster over time. The latter is a salient feature of the US GDP growth rate: For example, the series was much more volatile in the 1970s than in the 1990s. The model is estimated using Bayesian Markov chain Monte Carlo methods (Frühwirth-Schnatter, 2006, e.g.,). Our implementation closely follows Krüger et al. (2016, Section 5), and uses the \codear_ms() function, and the data set \codegdp, included in the \pkgscoringRules package.

The data set \codegdp comprises US GDP growth observations \codeval, and the corresponding quarters \codedt and vintages \codevint. Measuring economic variables is challenging, hence records tend to be revised and each quarter has its own time-series, or vintage, of past observations. As a result, the data set for 271 quarters from 1947 to 2014 contains 33616 records.

We split the data into a training sample of observations containing the data before 2014’s first quarter, and an evaluation period containing only the four quarters of 2014, using the most recent vintage in both cases:

R> data("gdp", package = "scoringRules")R> data_train <- subset(gdp, vint == "2014Q1")R> data_eval <- subset(gdp, vint == "2015Q1" & grepl("2014", dt)) As is typical for MCMC-based analysis, the model’s forecast distribution is not available as an analytical formula, but must be approximated in some way. Following Krüger et al. (2016), a generic MCMC algorithm to generate samples of the parameter vector and sample from the posterior predictive distribution proceeds as follows:

-

•

fix

-

•

for ,

-

–

draw , where is a transition kernel that is specific to the model under use

-

–

draw , where denotes the conditional distribution given the parameter values.

-

–

We use the function \codear_ms() to fit the model and produce forecasts for the four quarters of 2014 based on the information available at the end of year 2013, i.e., a single prediction case where the forecast horizon extends from one to four quarters ahead. Here, the conditional distribution is Gaussian, and we run the chain for 20 000 iterations.

R> h <- 4R> m <- 20000R> fc_params <- ar_ms(data_train$val, forecast_periods = h, n_rep = m) This function call yields a simulated sample corresponding to , where we obtain matrices of parameters for the mean and standard deviation. We transpose these matrices to have the rows correspond to the observations, and columns represent the position in the Markov chain:

R> mu <- t(fc_params$fcMeans)R> Sd <- t(fc_params$fcSds) Next, we draw the sample of possible observations corresponding to conditional on the Gaussian assumption and the available parameter information:

R> X <- matrix(rnorm(h * m, mean = mu, sd = Sd), nrow = h, ncol = m) We consider two competing estimators of the posterior predictive distribution . The mixture-of-parameters estimator (MPE)

| (6) |

builds on the simulated parameter values by mixing a series of Gaussian distributions uniformly, whereas the empirical CDF based approximation

utilizes the simulated sample from the conditional distribution given the parameter values, instead of building on the simulated parameter values directly. A standard choice for a smoother approximation is to replace the indicator function with a Gaussian kernel, as in the \codelogs_sample() function.

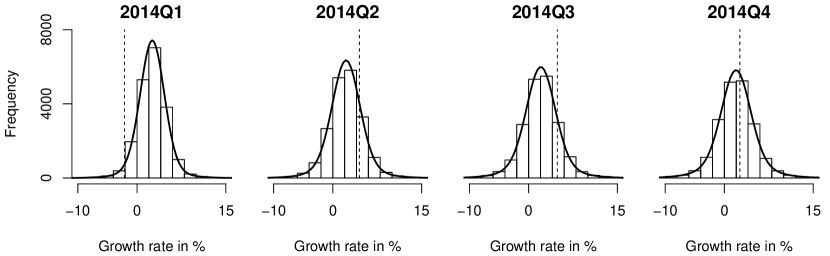

The two alternative estimators are illustrated in Figure 4: For each date, the histogram represents a simulated sample from the model’s forecast distribution, and the black line indicates the mixture-of-parameters estimator. We can observe a distinct decrease in the forecast’s certainty as the forecast horizon increases from one to four quarters ahead.

Finally, we evaluate CRPS and LogS for the approximated forecast distributions described above. The mixture-of-parameters estimator can be evaluated with the functions \codecrps() and \codelogs(), and can be evaluated with the functions \codecrps_sample() and \codelogs_sample():

R> obs <- data_eval$valR> names(obs) <- data_eval$dtR> w <- matrix(1/m, nrow = h, ncol = m)R> crps_mpe <- crps(obs, "normal-mixture", m = mu, s = Sd, w = w)R> logs_mpe <- logs(obs, "normal-mixture", m = mu, s = Sd, w = w)R> crps_ecdf <- crps_sample(obs, X)R> logs_kde <- logs_sample(obs, X)R> print(cbind(crps_mpe, crps_ecdf, logs_mpe, logs_kde))

crps_mpe crps_ecdf logs_mpe logs_kde2014Q1 3.457 3.468 4.01 3.972014Q2 1.358 1.362 2.29 2.282014Q3 1.700 1.690 2.52 2.542014Q4 0.724 0.729 1.96 1.98 The score values are quite similar for both estimators, which seems natural given the large number of MCMC draws. For the logarithmic score in particular, the MPE should be preferred over the KDE based estimator on theoretical grounds, see Krüger et al. (2016).

The algorithm and approximation methods just sketched are not idiosyncratic to our example, but arise whenever a Bayesian model is used for forecasting. For illustrative \proglangR implementations of other Bayesian models, see, e.g., the packages \pkgbayesgarch (Ardia and Hoogerheide, 2010) and \pkgstochvol (Kastner, 2016).

4.3 Parameter estimation with scoring rules

Apart from comparative forecast evaluation, proper scoring rules also provide useful tools for parameter estimation. In the optimum score estimation framework of Gneiting and Raftery (2007, Section 9.1), the parameters of a model’s forecast distribution are determined by optimizing the value of a proper scoring rule, on average over a training sample. Optimum score estimation based on the LogS corresponds to classical maximum likelihood estimation. The score functions to compute and for parametric forecast distributions included in \pkgscoringRules (see Table 1) thus offer tools for the straightforward implementation of such optimum score estimation approaches. Specifically, the worker functions of the form \code[crps]_[family]() and \code[logs]_[family]() entail little overhead in terms of input checks and are thus well suited for use in numerical optimization procedures such as \codeoptim(). Furthermore, functions to compute gradients and Hessian matrices of the have been implemented for a subset of parametric families, and can be supplied to assist numerical optimizers. Such functions are available for the \code"logis", "norm" and \code"t" families and truncated and censored versions thereof (\code"clogis", "tlogis", "cnorm", "tnorm", "ct", "tt"). The corresponding computation functions follow the naming scheme \code[gradcrps]_[family]() and \code[hesscrps]_[family](). However, we emphasize that implementing minimum CRPS or estimation approaches is possible for all parametric families listed in Table 1, even if analytical gradient and Hessian functions are not supplied but are instead approximated numerically by \codeoptim().

Gebetsberger et al. (2017) provide a detailed comparison of maximum likelihood and minimum CRPS estimation in the context of non-homogeneous regression models for post-processing ensemble weather forecasts. Here we illustrate the use for minimum CRPS estimation in a simple simulation example. Consider an independent sample from a normal distribution with mean and standard deviation . The analytical maximum likelihood estimates and are given by

To determine the corresponding estimates by numerically minimizing the CRPS define wrapper functions which compute the mean CRPS and corresponding gradient for a vector of training data \codey_train and distribution parameters \codeparam.

R> meancrps <- function(y_train, param) mean(crps_norm(y = y_train,+ mean = param[1], sd = param[2]))R> grad_meancrps <- function(y_train, param) apply(gradcrps_norm(y_train,+ param[1], param[2]), 2, mean) These functions can then be passed to \codeoptim(), for example, mean and standard deviation of a normal distribution with true values and can be estimated as illustrated in the following. The estimation with sample size 500 is repeated times.

R> R <- 1000R> n <- 500R> mu_true <- -1R> sigma_true <- 2R> estimates_ml <- matrix(NA, nrow = R, ncol = 2)R> estimates_crps <- matrix(NA, nrow = R, ncol = 2)R> for (r in 1:R) {+ dat <- rnorm(n, mu_true, sigma_true)+ estimates_crps[r, ] <- optim(par = c(1, 1), fn = meancrps,+ gr = grad_meancrps, method = "BFGS", y_train = dat)$par+ estimates_ml[r, ] <- c(mean(dat), sd(dat) * sqrt((n - 1) / n))+ }

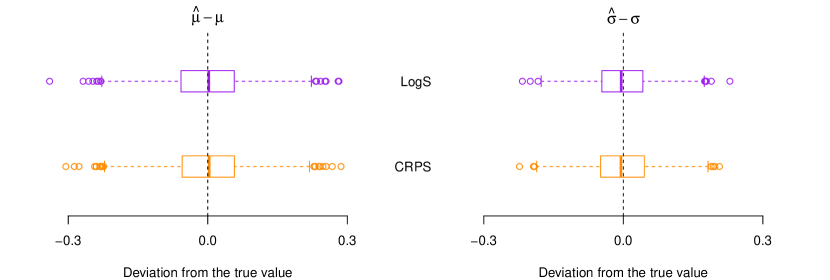

Figure 5 compares minimum CRPS and minimum LogS (i.e., maximum likelihood) parameter estimates. The differences to the true values show very similar distributions and illustrate the consistency of general optimum score estimates (Gneiting and Raftery, 2007, Equation 59). For the standard deviation parameter , the difference between estimate and true value exhibits slightly less variability for the maximum likelihood method.

5 Multivariate scoring rules

The basic concept of proper scoring rules can be extended to multivariate forecast distributions for which the support is given by . A variety of multivariate proper scoring rules has been proposed in the literature. For example, the univariate LogS allows for a straightforward generalization towards multivariate forecast distributions. However, parametric modeling and forecasting of multivariate observations is challenging, and when sampling is a feasible alternative we encounter the same, even exacerbated, problems in kernel density estimation as for univariate samples. As another example, the univariate CRPS can also be generalized to multivariate forecast distributions, and one such generalization is discussed in this chapter, the energy score. Finding closed form expressions for parametric distributions is even more involved than for the univariate CRPS, but the robustness in the evaluation of sample forecasts is retained. We refer to Gneiting et al. (2008) and Scheuerer and Hamill (2015b) for a detailed discussion of multivariate proper scoring rules and limit our attention to the case where probabilistic forecasts are given as samples from the forecast distributions.

Let , and let denote a forecast distribution on given through discrete samples from with . The \pkgscoringRules package provides implementations of the energy score (ES; Gneiting et al., 2008),

where denotes the Euclidean norm on , and the variogram score of order (VSp; Scheuerer and Hamill, 2015b),

In the definition of VSp, is a non-negative weight that allows one to emphasize or down-weight pairs of component combinations based on subjective expert decisions, and is the order of the variogram score. Typical choices of include and .

ES and VSp are implemented for multivariate forecast distributions given through simulated samples as functions {Code} es_sample(y, dat) vs_sample(y, dat, w = NULL, p = 0.5) These functions can only evaluate a single multivariate forecast case and always return a single number to simplify use and documentation, see Appendix B for an example on how to use \codeapply() functions or \codefor loops to sequentially apply them to multiple forecast cases. The observation input for \codey is required to be a vector of length , and the corresponding forecast input for \codedat has to be given as a matrix, the columns of which are the simulated samples from the multivariate forecast distribution. In \codevs_sample() it is possible to specify a matrix for \codew of non-negative weights as described in the text. The entry in the -th row and -th column of \codew corresponds to the weight assigned to the combination of the -th and -th component. If no weights are specified, constant weights with for all are used. For details and examples on choosing appropriate weights, see Scheuerer and Hamill (2015b).

In the following, we give a usage example of the multivariate scoring rules using the results from the economic case study in Section 4.2. Instead of evaluating the forecasts separately for each horizon (as we did before), we now jointly evaluate the forecast performance over the four forecast horizons based on the four-variate simulated sample.

R> names(obs) <- NULLR> es_sample(obs, dat = X)

[1] 4.13

R> vs_sample(obs, dat = X)

[1] 7.05 While this simple example refers to a single forecast case and a single model, a typical empirical analysis would consider the average scores (across several forecast cases) of two or more models.

6 Summary and discussion

The \pkgscoringRules package enables computing proper scoring rules for parametric and simulated forecast distributions. The package covers a wide range of situations prevalent in work on modeling and forecasting, and provides generally applicable and numerically efficient implementations based on recent theoretical considerations.

The main functions of the package – \codecrps() and \codelogs() – are S3 generics, for which we provide methods \codecrps.numeric() and \codelogs.numeric(). The package can be extended naturally by defining S3 methods for classes other than ‘\codenumeric’. For example, consider a fitted model object of class ‘\codecrch’, obtained by the \proglangR package of the same name (Messner et al., 2016). An object of this class contains a detailed specification of the fitted model’s forecast distribution (such as the parametric family of distributions and the values of the fitted parameters). This information could be utilized to write a specific method that computes the of a fitted model object.

The choice of an appropriate proper scoring rule for model evaluation or parameter estimation is a non-trivial task. We have implemented the widely used LogS and along with the multivariate and . Possible future extension of the \pkgscoringRules package include the addition of novel proper scoring rules such as the Dawid-Sebastiani score (Dawid and Sebastiani, 1999) which has been partially implemented. Further, given the availability of appropriate analytical expressions, the list of covered parametric families can be extended as demand arises and time allows.

Acknowledgments

The work of Alexander Jordan and Fabian Krüger has been funded by the European Union Seventh Framework Programme under grant agreement 290976. Sebastian Lerch gratefully acknowledges support by Deutsche Forschungsgemeinschaft (DFG) through project C7 (“Statistical postprocessing and stochastic physics for ensemble predictions”) within SFB/TRR 165 “Waves to Weather”. The authors thank the Klaus Tschira Foundation for infrastructural support at the Heidelberg Institute for Theoretical Studies. Helpful comments by Tilmann Gneiting, Stephan Hemri, Jakob Messner and Achim Zeileis are gratefully acknowledged. We further thank Maximiliane Graeter for contributions to the implementation of the multivariate scoring rules, and two referees for constructive comments on an earlier version of the manuscript.

References

- Ardia and Hoogerheide (2010) Ardia D, Hoogerheide LF (2010). “Bayesian Estimation of the GARCH(1,1) Model with Student-t Innovations.” The \proglangR Journal, 2(2), 41–47.

- Baran and Lerch (2015) Baran S, Lerch S (2015). “Log-Normal Distribution Based Ensemble Model Output Statistics Models for Probabilistic Wind-Speed Forecasting.” Quarterly Journal of the Royal Meteorological Society, 141(691), 2289–2299. 10.1002/qj.2521.

- Brown et al. (2010) Brown JD, Demargne J, Seo DJ, Liu Y (2010). “The \proglangEnsemble Verification System (\proglangEVS): A Software Tool for Verifying Ensemble Forecasts of Hydrometeorological and Hydrologic Variables at Discrete Locations.” Environmental Modelling & Software, 25(7), 854–872. 10.1016/j.envsoft.2010.01.009.

- Carpenter et al. (2017) Carpenter B, Gelman A, Hoffman M, Lee D, Goodrich B, Betancourt M, Brubaker M, Guo J, Li P, Riddell A (2017). “\proglangStan: A Probabilistic Programming Language.” Journal of Statistical Software, 76(1), 1–37. 10.18637/jss.v076.i01.

- Clements (2004) Clements MP (2004). “Evaluating the Bank of England Density Forecasts of Inflation.” The Economic Journal, 114(498), 844–866. 10.1111/j.1468-0297.2004.00246.x.

- Dawid and Sebastiani (1999) Dawid AP, Sebastiani P (1999). “Coherent Dispersion Criteria for Optimal Experimental Design.” The Annals of Statistics, 27(1), 65–81. 10.1214/aos/1018031101.

- Developmental Testbed Center (2018) Developmental Testbed Center (2018). \proglangMET: Version 7.0 \proglangModel Evaluation Tools Users Guide. Available at http://www.dtcenter.org/met/users/docs/overview.php.

- Fraley et al. (2011) Fraley C, Raftery AE, Gneiting T, Sloughter JM, Berrocal VJ (2011). “Probabilistic Weather Forecasting in \proglangR.” The \proglangR Journal, 3(1), 55–63.

- Fraley et al. (2018) Fraley C, Raftery AE, Sloughter JM, Gneiting T, University of Washington (2018). \pkgensembleBMA: Probabilistic Forecasting Using Ensembles and Bayesian Model Averaging. \proglangR package version 5.1.5, URL https://CRAN.R-project.org/package=ensembleBMA.

- Friederichs and Thorarinsdottir (2012) Friederichs P, Thorarinsdottir TL (2012). “Forecast Verification for Extreme Value Distributions with an Application to Probabilistic Peak Wind Prediction.” Environmetrics, 23(7), 579–594. 10.1002/env.2176.

- Frühwirth-Schnatter (2006) Frühwirth-Schnatter S (2006). Finite Mixture and Markov Switching Models. Springer-Verlag, New York. 10.1007/978-0-387-35768-3.

- Gebetsberger et al. (2017) Gebetsberger M, Messner JW, Mayr GJ, Zeileis A (2017). “Estimation Methods for Non-Homogeneous Regression Models: Minimum Continuous Ranked Probability Score vs. Maximum Likelihood.” Working paper. Preprint available at http://EconPapers.RePEc.org/RePEc:inn:wpaper:2017-23.

- Gneiting and Katzfuss (2014) Gneiting T, Katzfuss M (2014). “Probabilistic Forecasting.” Annual Review of Statistics and Its Application, 1, 125–151. 10.1146/annurev-statistics-062713-085831.

- Gneiting et al. (2006) Gneiting T, Larson K, Westrick K, Genton MG, Aldrich E (2006). “Calibrated Probabilistic Forecasting at the Stateline Wind Energy Center.” Journal of the American Statistical Association, 101(475), 968–979. 10.1198/016214506000000456.

- Gneiting and Raftery (2005) Gneiting T, Raftery AE (2005). “Weather Forecasting with Ensemble Methods.” Science, 310(5746), 248–249. 10.1126/science.1115255.

- Gneiting and Raftery (2007) Gneiting T, Raftery AE (2007). “Strictly Proper Scoring Rules, Prediction, and Estimation.” Journal of the American Statistical Association, 102(477), 359–378. 10.1198/016214506000001437.

- Gneiting et al. (2005) Gneiting T, Raftery AE, Westveld III AH, Goldman T (2005). “Calibrated Probabilistic Forecasting Using Ensemble Model Output Statistics and Minimum CRPS Estimation.” Monthly Weather Review, 133(5), 1098–1118. 10.1175/MWR2904.1.

- Gneiting et al. (2008) Gneiting T, Stanberry LI, Grimit EP, Held L, Johnson NA (2008). “Assessing Probabilistic Forecasts of Multivariate Quantities, with an Application to Ensemble Predictions of Surface Winds.” Test, 17(2), 211–235. doi.org/10.1007/s11749-008-0114-x.

- Gneiting and Thorarinsdottir (2010) Gneiting T, Thorarinsdottir TL (2010). “Predicting Inflation: Professional Experts Versus No-Change Forecasts.” Working paper. Preprint available at https://arxiv.org/abs/1010.2318.

- Good (1952) Good IJ (1952). “Rational Decisions.” Journal of the Royal Statistical Society B, 14(1), 107–114. URL https://www.jstor.org/stable/2984087.

- Grimit et al. (2006) Grimit EP, Gneiting T, Berrocal VJ, Johnson NA (2006). “The Continuous Ranked Probability Score for Circular Variables and its Application to Mesoscale Forecast Ensemble Verification.” Quarterly Journal of the Royal Meteorological Society, 132(621C), 2925–2942. 10.1256/qj.05.235.

- Hamilton (1989) Hamilton JD (1989). “A New Approach to the Economic Analysis of Nonstationary Time Series and the Business Cycle.” Econometrica, 57(2), 357–384. 10.2307/1912559.

- Hyndman and Khandakar (2008) Hyndman RJ, Khandakar Y (2008). “Automatic Time Series Forecasting: The \pkgforecast Package for \proglangR.” Journal of Statistical Software, 26(3), 1–22. 10.18637/jss.v027.i03.

- Jordan (2016) Jordan A (2016). “Facets of Forecast Evaluation.” 10.5445/IR/1000063629. Ph.D. thesis, Karlsruhe Institute of Technology, available at https://publikationen.bibliothek.kit.edu/1000063629.

- Jordan et al. (2018a) Jordan A, Krüger F, Lerch S (2018a). “Evaluating Probabilistic Forecasts with \pkgscoringRules.” Journal of Statistical Software. Forthcoming.

- Jordan et al. (2018b) Jordan A, Krüger F, Lerch S (2018b). \pkgscoringRules: Scoring Rules for Parametric and Simulated Distribution Forecasts. \proglangR package version 0.9.5, URL https://CRAN.R-project.org/package=scoringRules.

- Kastner (2016) Kastner G (2016). “Dealing with Stochastic Volatility in Time Series Using the \proglangR Package \pkgstochvol.” Journal of Statistical Software, 69(5), 1–30. 10.18637/jss.v069.i05.

- Krüger et al. (2016) Krüger F, Lerch S, Thorarinsdottir TL, Gneiting T (2016). “Probabilistic Forecasting and Comparative Model Assessment Based on Markov Chain Monte Carlo Output.” Working paper. Preprint available at https://arxiv.org/abs/1608.06802.

- Kuhn et al. (2018) Kuhn M, Contributions from Wing J, Weston S, Williams A, Keefer C, Engelhardt A, Cooper T, Mayer Z, Kenkel B, the \proglangR Core Team, Benesty M, Lescarbeau R, Ziem A, Scrucca L, Tang Y, Candan C, Hunt T (2018). \pkgcaret: Classification and Regression Training. \proglangR package version 6.0-80, URL https://CRAN.R-project.org/package=caret.

- Laio and Tamea (2007) Laio F, Tamea S (2007). “Verification Tools for Probabilistic Forecasts of Continuous Hydrological Variables.” Hydrology and Earth System Sciences Discussions, 11(4), 1267–1277. 10.5194/hess-11-1267-2007.

- Leutbecher and Palmer (2008) Leutbecher M, Palmer TN (2008). “Ensemble Forecasting.” Journal of Computational Physics, 227(7), 3515–3539. 10.1016/j.jcp.2007.02.014.

- Matheson and Winkler (1976) Matheson JE, Winkler RL (1976). “Scoring Rules for Continuous Probability Distributions.” Management Science, 22(10), 1087–1096. 10.1287/mnsc.22.10.1087.

- Merkle and Steyvers (2013) Merkle EC, Steyvers M (2013). “Choosing a Strictly Proper Scoring Rule.” Decision Analysis, 10(4), 292–304.

- Messner et al. (2014) Messner JW, Mayr GJ, Wilks DS, Zeileis A (2014). “Extending Extended Logistic Regression: Extended Versus Separate Versus Ordered Versus Censored.” Monthly Weather Review, 142(8), 3003–3014. 10.1175/MWR-D-13-00355.1.

- Messner et al. (2016) Messner JW, Mayr GJ, Zeileis A (2016). “Heteroscedastic Censored and Truncated Regression with \pkgcrch.” The \proglangR Journal, 17(11), 173–181.

- Meyer et al. (2017) Meyer S, Held L, Höhle M (2017). “Spatio-Temporal Analysis of Epidemic Phenomena Using the \proglangR Package \pkgsurveillance.” Journal of Statistical Software, 77(11), 1–55. 10.18637/jss.v077.i11.

- Möller and Scheuerer (2015) Möller D, Scheuerer M (2015). “Probabilistic Wind Speed Forecasting on a Grid Based on Ensemble Model Output Statistics.” Annals of Applied Statistics, 9(3), 1328–1349. doi:10.1214/15-AOAS843.

- Murphy (1970) Murphy AH (1970). “The Ranked Probability Score and the Probability Score: A Comparison.” Monthly Weather Review, 98(12), 917–924. 10.1175/1520-0493(1970)098<0917:TRPSAT>2.3.CO;2.

- NCAR - Research Applications Laboratory (2015) NCAR - Research Applications Laboratory (2015). \pkgverification: Weather Forecast Verification Utilities. \proglangR package version 1.42, URL https://CRAN.R-project.org/package=verification.

- Pocernich (2012) Pocernich M (2012). “Appendix: Verification Software.” In IT Jolliffe, DB Stephenson (eds.), Forecast Verification: A Practitioner’s Guide in Atmospheric Science, 2nd edition, pp. 231–240. John Wiley & Sons, Chichester. 10.1002/9781119960003.app1.

- \proglangPython Software Foundation (2017) \proglangPython Software Foundation (2017). \proglangPython Software, Version 3.6.4. Beaverton, OR. URL https://www.python.org/.

- Raftery (2016) Raftery AE (2016). “Use and Communication of Probabilistic Forecasts.” Statistical Analysis and Data Mining: The ASA Data Science Journal, 9(6), 397–410. 10.1002/sam.11302.

- Raftery et al. (2014) Raftery AE, Alkema L, Gerland P (2014). “Bayesian Population Projections for the United Nations.” Statistical Science, 29(1), 58–68. 10.1214/13-STS419.

- Raftery et al. (2005) Raftery AE, Gneiting T, Balabdaoui F, Polakowski M (2005). “Using Bayesian Model Averaging to Calibrate Forecast Ensembles.” Monthly Weather Review, 133(5), 1155–1174. 10.1175/MWR2906.1.

- \proglangR Core Team (2017) \proglangR Core Team (2017). \proglangR: A Language and Environment for Statistical Computing. \proglangR Foundation for Statistical Computing, Vienna, Austria. URL https://www.R-project.org/.

- Scheuerer (2014) Scheuerer M (2014). “Probabilistic Quantitative Precipitation Forecasting Using Ensemble Model Output Statistics.” Quarterly Journal of the Royal Meteorological Society, 140(680), 1086–1096. 10.1002/qj.2183.

- Scheuerer and Hamill (2015a) Scheuerer M, Hamill TM (2015a). “Statistical Postprocessing of Ensemble Precipitation Forecasts by Fitting Censored, Shifted Gamma Distributions.” Monthly Weather Review, 143(11), 4578–4596. 10.1175/MWR-D-15-0061.1.

- Scheuerer and Hamill (2015b) Scheuerer M, Hamill TM (2015b). “Variogram-Based Proper Scoring Rules for Probabilistic Forecasts of Multivariate Quantities.” Monthly Weather Review, 143(4), 1321–1334. 10.1175/MWR-D-14-00269.1.

- Siegert (2017) Siegert S (2017). \pkgSpecsVerification: Forecast Verification Routines for the SPECS FP7 Project. \proglangR package version 0.5-2, URL https://CRAN.R-project.org/package=SpecsVerification.

- Silverman (1986) Silverman BW (1986). Density Estimation for Statistics and Data Analysis. Chapman and Hall, London.

- Taillardat et al. (2016) Taillardat M, Mestre O, Zamo M, Naveau P (2016). “Calibrated Ensemble Forecasts Using Quantile Regression Forests and Ensemble Model Output Statistics.” Monthly Weather Review, 144(6), 2375–2393. 10.1175/MWR-D-15-0260.1.

- The Climate Corporation (2015) The Climate Corporation (2015). \pkgproperscoring: Proper Scoring Rules in \proglangPython. \proglangPython package version 0.1, URL https://pypi.python.org/pypi/properscoring.

- Thorarinsdottir and Gneiting (2010) Thorarinsdottir TL, Gneiting T (2010). “Probabilistic Forecasts of Wind Speed: Ensemble Model Output Statistics by Using Heteroscedastic Censored Regression.” Journal of the Royal Statistical Society A, 173(2), 371–388. 10.1111/j.1467-985X.2009.00616.x.

- Vehtari et al. (2018) Vehtari A, Gelman A, Gabry J (2018). \pkgloo: Efficient Leave-One-Out Cross-Validation and WAIC for Bayesian Models. \proglangR package version 2.0.0, URL https://CRAN.R-project.org/package=loo.

- Wei and Held (2014) Wei W, Held L (2014). “Calibration Tests for Count Data.” TEST, 23(4), 787–805. 10.1007/s11749-014-0380-8.

- Yuen et al. (2018) Yuen RA, Baran S, Fraley C, Gneiting T, Lerch S, Scheuerer M, Thorarinsdottir TL (2018). \pkgensembleMOS: Ensemble Model Output Statistics. \proglangR package version 0.8.2, URL https://CRAN.R-project.org/package=ensembleMOS.

Appendix A Formulas for the CRPS

A.1 Notation

| Symbol | Name |

|---|---|

| Euler-Mascheroni constant | |

| floor function | |

| sign function | |

| exponential integral | |

| standard Gaussian density function | |

| standard Gaussian distribution function | |

| gamma function | |

| lower incomplete gamma function | |

| upper incomplete gamma function | |

| beta function | |

| regularized incomplete beta function | |

| modified Bessel function of the first kind | |

| hypergeometric function |

A.2 Distributions for variables on the real line

A.2.1 Laplace distribution

The function \codecrps_lapl() computes the CRPS for the standard distribution, and generalizes via \codelocation parameter and \codescale parameter ,

The CDFs are given by and

A.2.2 Logistic distribution

The function \codecrps_logis() computes the CRPS for the standard distribution, and generalizes via \codelocation parameter and \codescale parameter ,

The CDFs are given by and .

A.2.3 Normal distribution

The function \codecrps_norm() computes the CRPS for the standard distribution, and generalizes via \codemean parameter and \codesd parameter , or alternatively, \codelocation and \codescale,

The CDFs are given by and . Derived by Gneiting et al. (2005).

A.2.4 Mixture of normal distributions

The function \codecrps_mixnorm() computes the CRPS for a mixture of normal distributions with mean parameters comprising \codem, scale parameters comprising \codes, and (automatically rescaled) weight parameters comprising \codew,

The CDF is , and . Derived by Grimit et al. (2006).

A.2.5 Student’s distribution

The function \codecrps_t() computes the CRPS for Student’s distribution with \codedf parameter , and generalizes via \codelocation parameter and \codescale parameter ,

The CDFs and PDF are given by and

A.2.6 Two-piece exponential distribution

The function \codecrps_2pexp() computes the CRPS for the two-piece exponential distribution with \codescale1 and \codescale2 parameters , and generalizes via \codelocation parameter ,

The CDFs are given by and

A.2.7 Two-piece normal distribution

The function \codecrps_2pnorm() computes the CRPS for the two-piece exponential distribution with \codescale1 and \codescale2 parameters , and generalizes via \codelocation parameter ,

where is the CDF of the generalized truncated/censored normal distribution as in Section A.4.7. The CDFs for the two-piece normal distribution are given by

Gneiting and Thorarinsdottir (2010) give an explicit CRPS formula.

A.3 Distributions for non-negative variables

A.3.1 Exponential distribution

The function \codecrps_exp() computes the CRPS for the exponential distribution with \coderate parameter ,

The CDF is given by

A.3.2 Gamma distribution

The function \codecrps_gamma() computes the CRPS for the gamma distribution with \codeshape parameter and \coderate parameter , or alternatively \codescale = 1/rate,

The CDF is given by

Derived by Möller and Scheuerer (2015).

A.3.3 Log-Laplace distribution

The function \codecrps_llapl() computes the CRPS for the log-Laplace distribution with \codelocationlog parameter and \codescalelog parameter ,

The CDF and otherwise required functions are given by

A.3.4 Log-logistic distribution

The function \codecrps_llogis() computes the CRPS for the log-logistic distribution with \codelocationlog parameter and \codescalelog parameter ,

The CDF is given by

Taillardat et al. (2016) give an alternative CRPS formula.

A.3.5 Log-normal distribution

The function \codecrps_lnorm() computes the CRPS for the log-logistic distribution with \codelocationlog parameter and \codescalelog parameter ,

The CDF is given by

Derived by Baran and Lerch (2015).

A.4 Distribution with flexible support and/or point masses

A.4.1 Beta distribution

The function \codecrps_beta() computes the CRPS for the beta distribution with \codeshape1 and \codeshape2 parameters , and generalizes via \codelower and \codeupper parameters , ,

The CDFs are given by and

Taillardat et al. (2016) give an equivalent expression.

A.4.2 Continuous uniform distribution

The function \codecrps_unif() computes the CRPS for the continuous uniform distribution on the unit interval, and generalizes via \codemin and \codemax parameters , , and by allowing point masses in the boundaries, i.e., \codelmass and \codeumass parameters , ,

The CDFs are given by and

A.4.3 Exponential distribution with point mass

The function \codecrps_expM() computes the CRPS for the standard exponential distribution, and generalizes via \codelocation parameter and \codescale parameter , and by allowing a point mass in the boundary, i.e., a \codemass parameter ,

The CDFs are given by and

A.4.4 Generalized extreme value distribution

The function \codecrps_gev() computes the CRPS for the generalized extreme value distribution with \codeshape parameter , and generalizes via \codelocation parameter and \codescale parameter ,

The CDFs and otherwise required functions are given by and

Friederichs and Thorarinsdottir (2012) give an equivalent expression.

A.4.5 Generalized Pareto distribution with point mass

The function \codecrps_gpd() computes the CRPS for the generalized extreme value distribution with \codeshape parameter , and generalizes via \codelocation parameter and \codescale parameter , and by allowing a point mass in the lower boundary, i.e., a \codemass parameter ,

The CDFs are given by and

Friederichs and Thorarinsdottir (2012) give a CRPS formula for the generalized Pareto distribution without a point mass.

A.4.6 Generalized truncated/censored logistic distribution

The function \codecrps_gtclogis() computes the CRPS for the generalized truncated/censored logistic distribution with \codelocation parameter , \codescale parameter , \codelower and \codeupper boundary parameters , , and by allowing point masses in the boundaries, i.e., \codelmass and \codeumass parameters , ,

The CDFs are given by and

Otherwise required functions are given by and

The function \codecrps_clogis() computes the CRPS for the special case when the tail probabilities collapse into the respective boundary,

where the CDF is given by

The function \codecrps_tlogis() computes the CRPS for the special case when , where the CDF is given by

Taillardat et al. (2016) give a formula for left-censoring at zero. Möller and Scheuerer (2015) give a formula for left-truncating at zero.

A.4.7 Generalized truncated/censored normal distribution

The function \codecrps_gtcnorm() computes the CRPS for the generalized truncated/censored normal distribution with \codelocation parameter , \codescale parameter , \codelower and \codeupper boundary parameters , , and by allowing point masses in the boundaries, i.e., \codelmass and \codeumass parameters , ,

The CDFs and otherwise required functions are given by

The function \codecrps_cnorm() computes the CRPS for the special case when the tail probabilities collapse into the respective boundary, where the CDF is given by

The function \codecrps_tnorm() computes the CRPS for the special case when , where the CDF is given by

Thorarinsdottir and Gneiting (2010) give a formula for left-censoring at zero. Gneiting et al. (2006) give a formula for left-truncating at zero.

A.4.8 Generalized truncated/censored Student’s distribution

The function \codecrps_gtct() computes the CRPS for the generalized truncated/censored Student’s distribution with \codedf parameter , \codelocation parameter , \codescale parameter , \codelower and \codeupper boundary parameters , , and by allowing point masses in the boundaries, i.e., \codelmass and \codeumass parameters , ,

The CDFs are given by

Otherwise required functions are given by

The function \codecrps_ct() computes the CRPS for the special case when the tail probabilities collapse into the respective boundary, where the CDF is given by

The function \codecrps_tt() computes the CRPS for the special case when , where the CDF is given by

A.5 Distribution for discrete variables

A.5.1 Binomial distribution

The function \codecrps_binom() computes the CRPS for the binomial distribution with \codesize parameter , and \codeprob parameter ,

The CDF and probability mass function are given by

A.5.2 Hypergeometric distribution

The function \codecrps_hyper() computes the CRPS for the hypergeometric distribution with two population parameters, the number of entities with the relevant feature and the number of entities without that feature, and a parameter for the size of the sample to be drawn,

The CDF and probability mass function are given by

A.5.3 Negative binomial distribution

The function \codecrps_nbinom() computes the CRPS for the negative binomial distribution with \codesize parameter , and \codeprob parameter or alternatively a non-negative mean parameter given to \codemu,

The CDF and probability mass function are given by

Derived by Wei and Held (2014).

A.5.4 Poisson distribution

The function \codecrps_pois() computes the CRPS for the Poisson distribution with mean parameter given to \codelambda,

The CDF and probability mass function are given by

Derived by Wei and Held (2014).

Appendix B Computation of multivariate scores for multiple forecast cases

As noted in Section 5 the computation functions for multivariate scoring rules are defined for single forecast cases only. Here, we demonstrate how \codeapply functions can be used to compute ES and VSp for multiple forecast cases. The simulation example is based on the function documentation of \codees_sample() and \codevs_sample().

The observation is generated as a sample from a multivariate normal distribution in with mean vector and covariance matrix with if and if for all .

R> d <- 10R> mu <- rep(0, d)R> Sigma <- diag(d)R> Sigma[!diag(d)] <- 0.2 The multivariate forecasts are given by 50 random samples from a corresponding multivariate normal distribution with mean vector and covariance matrix which is defined as , but with .

R> m <- 50R> mu_f <- rep(1, d)R> Sigma_f <- diag(d)R> Sigma_f[!diag(d)] <- 0.1 The simulation process is independently repeated 1 000 times. To illustrate two potential data structures, observations and forecasts are saved as list elements in an outer list where the index corresponds to the forecast case, and as 2- and 3-dimensional arrays where the last dimension indicates the forecast case.

R> n <- 1000R> fc_obs_list <- vector("list", n)R> obs_array <- matrix(NA, nrow = d, ncol = n)R> fc_array <- array(NA, dim = c(d, m, n))R> for (fc_case in 1:n) {+ obs_tmp <- drop(mu + rnorm(d) %*% chol(Sigma))+ fc_tmp <- replicate(m, drop(mu_f + rnorm(d) %*% chol(Sigma_f)))+ fc_obs_list[[fc_case]] <- list(obs = obs_tmp, fc_sample = fc_tmp)+ obs_array[, fc_case] <- obs_tmp+ fc_array[, , fc_case] <- fc_tmp+ } Given the data structures of forecasts and observations, all 1 000 forecast cases can be evaluated sequentially using the \codesapply() function (or, alternatively, a \codefor loop) along the list elements or along the last array dimension.

R> es_vec_list <- sapply(fc_obs_list, function(x) es_sample(y = x$obs,+ dat = x$fc_sample))R> es_vec_array <- sapply(1:n, function(i) es_sample(y = obs_array[, i],+ dat = fc_array[, , i]))R> head(cbind(es_vec_list, es_vec_array))

es_vec_list es_vec_array[1,] 2.44 2.44[2,] 2.68 2.68[3,] 2.56 2.56[4,] 1.85 1.85[5,] 3.83 3.83[6,] 3.04 3.04