Testing if the market microstructure noise is fully explained by the informational content of some variables from the limit order book111We would like to thank Yingying Li, Xinghua Zheng, Dacheng Xiu, Viktor Todorov, Torben Andersen, Rasmus Varneskov, Rui Da, Yacine Aït-Sahalia (the Editor), two anonymous referees and an anonymous Associate Editor, the participants of ECOSTA 2018, 2018 Asian meeting of the Econometric Society, SoFiE Financial Econometrics Summer School 2017 at Kellogg School of Management and 2017 Asian meeting of the Econometric Society at The Chinese University of Hong Kong for helpful discussions and advice. The research of Yoann Potiron is supported by Japanese Society for the Promotion of Science Grant-in-Aid for Young Scientists (B) No. 60781119 and a special grant from Keio University. The research of Simon Clinet is supported by CREST Japan Science and Technology Agency and a special grant from Keio University.

Abstract

In this paper, we build tests for the presence of residual noise in a model where the market microstructure noise is a known parametric function of some variables from the limit order book. The tests compare two distinct quasi-maximum likelihood estimators of volatility, where the related model includes a residual noise in the market microstructure noise or not. The limit theory is investigated in a general nonparametric framework. In the presence of residual noise, we examine the central limit theory of the related quasi-maximum likelihood estimation approach.

Keywords: efficient price ; estimation ; high frequency data ; information ; limit order book ; market microstructure noise ; integrated volatility ; quasi-maximum likelihood estimator ; realized volatility ; test

1 Introduction

If one can sample directly from the efficient price, the estimation of volatility is a well-studied matter. The realized volatility (RV) estimator, i.e. summing the square of the log-returns, is both consistent and efficient. However, in practice the observed price does not behave as expected. When sampling at high frequency, it can be quite different from the efficient price due to bid-ask bounce mechanism, the spread, the fact that transactions lie on a tick grid, etc. Market microstructure noise (MMN) typically degrades RV to the extent that it is highly biased when performed on tick by tick data.

One approach to overcome the problem consists in sub-sampling, say every 5 minutes, as in the pioneer work from [Andersen et al., 2001] and [Barndorff-Nielsen and Shephard, 2002]. On the contrary, [Aït-Sahalia et al., 2005] recognize the MMN as an inherent part of the data and advice for the use of the Quasi-Maximum Likelihood Estimator (QMLE) which was later shown to be robust to time-varying volatility in [Xiu, 2010]. Concurrent methods include and are not limited to: the Two-Scale Realized Volatility (TSRV) in [Zhang et al., 2005], the Multi-Scale Realized Volatility in [Zhang, 2006], the Pre-averaging approach (PAE) in [Jacod et al., 2009], realized kernels (RK) in [Barndorff-Nielsen et al., 2008] and the spectral approach considered in [Altmeyer and Bibinger, 2015].

Those two approaches have cons in that the sub-sampling technique discards a large proportion of the data and the noise-robust estimators have a slower rate of convergence than RV in the absence of noise. The only exception is the QMLE proposed by [Da and Xiu, 2017], which is automatically adaptive to noise magnitude and always enjoys optimal rate. In this paper, we consider the MMN as a salient part of the financial market, but using the growing limit order book (LOB) big data available to the econometrician we ask a different question. Can we test whether the MMN is fully explained by the informational content of some variables from the limit order book and can we estimate the parameter of the model? If the MMN can be expressed as an observable function, then we can estimate the efficient price and use RV including all the data points. This idea is not new, and actually our work is heavily based on the two very nice papers [Li et al., 2016] and [Chaker, 2017]. We will explain the differences later in the introduction.

In fact it is rather natural to see the MMN as a function of some variables of the LOB as in the pioneer work from [Roll, 1984] where the trade type, i.e. whether the trade was buyer or seller initiated, is used to correct for the bid-ask bounce effect in the observed price. The related observed price is then defined as

| (1.1) |

where can be interpreted as one-half of the effective bid-ask spread, is equal to 1 if the trade at time is buyer-initiated and -1 if seller-initiated. A simple extension where the spread is time-varying is given by

| (1.2) |

Discussion and related leading models can be found in: [Black, 1986], [Hasbrouck, 1993], [O’hara, 1995], [Madhavan et al., 1997], [Madhavan, 2000], [Stoll, 2000] and [Hasbrouck, 2007] among other prominent work.

The question we address is: can we trust models such as (1.1) or (1.2)? To investigate it, we introduce the general set-up as

| (1.3) |

where are observable variables included in the LOB while is known to the econometrician, and we develop tests for the presence of the residual noise at any given sampling frequency. The associated null hypothesis is such that and the alternative , where is known up to the parameter .

Our tests are based on [Hausman, 1978] tests555As far as we know, the use of Hausman tests in high-frequency data can be traced back to the TSRV and [Huang and Tauchen, 2005]. developed in [Aït-Sahalia and Xiu, 2016], which is restricted to the case . The authors consider the difference , where and corresponds to the QMLE in a model where . The Hausman test statistic is of the form , where is an estimator of under the null hypothesis. Under the alternative, RV is not consistent whereas the QMLE stays consistent so that the authors show that explodes in that case.

To test the presence of residual noise in (1.3) in the case where , we consider the Hausman tests comparing two distinct QMLE related to a model including the explicative part, i.e. which is restricted to a null residual noise and including the residual noise. As far as the authors know, is novel in the particular context of high frequency data. They respectively play the role of and , but they are both distinct from the latter related to a model with . Note that [Aït-Sahalia and Xiu, 2016] consider other candidates for testing, including the PAE, that we set aside in this paper.

The estimator corresponds exactly to estimators considered in [Li et al., 2016] (the so-called estimated-price RV in the latter paper) and [Chaker, 2017] (although the latter work is restricted to a linear ). Moreover, the E-QMLE discussed in [Li et al., 2016] (Section 2.2.1), i.e. first estimating the price and then applying the usual QMLE to the estimates, is asymptotically equivalent to . In addition, [Chaker, 2017] actually provides tests from a different nature for the presence of residual noise when is linear. Finally, some extensions are considered in Section 4.4 of [Potiron and Mykland, 2016].

Our first main theoretical contribution includes the investigation of the joint limit theory of , where is an estimator of the residual noise and are estimates of the parameter both obtained via QMLE under small residual noise, i.e. . The marginal limit theory for boils down to Theorem 2 in [Li et al., 2016] as is equal to the estimated-price RV estimator, and to Theorem 4 (i) in [Chaker, 2017] when is linear. In addition, used in conjunction with the toolkit in [Aït-Sahalia and Xiu, 2016], one could easily obtain an asymptotically equivalent joint limit theory of as the E-QMLE is asymptotically equivalent to . However the main difference between our setting and that of [Aït-Sahalia and Xiu, 2016] is that we have stochastic observation times whereas the cited authors only consider regular sampling times. In particular, in case of regular observation times, our contribution boils down to the marginal and joint limits for . We further demonstrate that only is residual noise robust so that we can consider the corresponding Hausman statistic to test the presence of residual noise.

When there is no residual noise in the model, i.e. , a byproduct of our contribution is that the parameter estimators are asymptotically equivalent. Subsequently, following the procedure considered in [Chaker, 2017] and [Li et al., 2016], we can consistently estimate the efficient price directly from the data as

| (1.4) |

This procedure seems to be traced back to the model with uncertainty zones, which was introduced in [Robert and Rosenbaum, 2010] and [Robert and Rosenbaum, 2012]. See also the pioneer work from [Hansen and Lunde, 2006] and the more recent work from [Andersen et al., 2017] for efficient price estimation, although in a slightly different context.

When we assume a residual noise in the model, we examine the measure of goodness of fit introduced in [Li et al., 2016], which corresponds to the proportion of MMN variance explained by the explicative part. Such measure can be estimated using the parameter and the residual noise variance estimates obtained with the QMLE related to the model including the residual noise. Our second main contribution establishes the corresponding central limit theorem in case when the variance of the residual noise stays constant. This goes one step further than Theorem 3 from [Li et al., 2016] in that the noise variance does not shrink to 0 asymptotically, and that we can actually provide a more reliable residual noise variance estimator, along with the asymptotic theory. Also, the convergence rate is smaller than the pre-estimation (1.4)-TSRV approach considered in [Chaker, 2017] (see Theorem 4 (ii)). In particular, volatility estimation is naturally not as fast as when we assume small noise in the model.

We implement the tests over a one month period with tick by tick data, and find out that the linear signed spread model (1.2) consistently stands out from many other alternatives including Roll model (1.1). The tests further reveal that the large majority of stocks can be reasonably considered as free from residual noise with such model. Moreover, we implement the tests from [Aït-Sahalia and Xiu, 2016] regarding the estimated efficient price (1.4) as the given observed price. They largely corroborate the findings.

As far as we know, there are at least another paper in volatility estimation closely related to our work. The impact of on RV is thoroughly discussed in [Diebold and Strasser, 2013]. In that paper, the authors study several leading models from the market microstructure literature. Unfortunately, their assumption of constant volatility is quite strong.

The remainder of the paper is structured as follows. The model is introduced in Section 2. The limit theory of the QMLE under small noise, the Hausman tests and the efficient price estimator are developed in Section 3. We discuss about measure of goodness of fit estimation, central limit theory under large noise and guidance for implementation of volatility estimation in Section 4. Section 5 performs a Monte Carlo experiment to assess finite sample performance of the tests and validation of the sequence to estimate volatility. Section 6 is devoted to an empirical study. We conclude in Section 7. Theoretical details and proofs can be found in the Appendix.

2 Model

For a given horizon time , we make observations666All the considered quantities are implicitly or explicitly indexed by . Consistency and convergence in law refer to the behavior as . A full specification of the model actually involves the stochastic basis , where is a -field and is a filtration. We assume that all the processes are -adapted (either in a continuous or discrete meaning) and that the observation times are -stopping times. Also, when referring to Itô-semimartingale, we automatically mean that the statement is relative to . contaminated by the MMN at (possibly random) times of the efficient log-price , and we assume that we have the additive decomposition

Here the parameter , where is a compact set. The impact function is known, of class in with , and corresponds to the remaining noise. Finally, includes observable information from the LOB such as the trade type , the trading volume ([Glosten and Harris, 1988]), the duration time between two trades ([Almgren and Chriss, 2001]), the quoted depth777The ask (bid) depth specifies the volume available at the best ask (bid) ([Kavajecz, 1999]), the bid-ask spread , the order flow imbalance888It is defined as the imbalance between supply and demand at the best bid and ask prices (including both quotes and cancellations) ([Cont et al., 2014]). The introduced MMN complies with the empirical evidence about autocorrelated noise999Although not with endogenous and/or heteroskedastic noise. (see, e.g., [Kalnina and Linton, 2008] and [Aït-Sahalia et al., 2011]). Some examples of can be consulted on Table 1.

The efficient price

The latent log-price is an Itô-semimartingale of the form

| (2.1) | |||||

| (2.2) |

with which is a 2 dimensional standard Brownian motion, the drift which is componentwise locally bounded, 101010A nice review on the use of stochastic volatility in financial mathematics can be found in [Ghysels et al., 1996]. which is componentwise locally bounded, itself an Itô process and a.s. We also assume that is a 2 dimensional pure jump process111111Jumps in volatility are a salient part of the data (see, e.g., [Todorov and Tauchen, 2011] for empirical evidence.) of finite activity.

The observation times

Crucial to the estimation is the robustness of the procedure when considering tick-time volatility instead of calendar-time volatility. For instance, [Patton, 2011] (see, e.g., p. 299) compares empirically the accuracy of estimators and mentions that using tick-time sampling leads to more accurate volatility estimation, although the considered estimators are a priori not robust to such sampling procedure. Also, [Xiu, 2010] and [Aït-Sahalia and Xiu, 2016] (Section 5, p. 17) compute the likelihood estimators estimating tick-time volatility even though the theory only covers the regular observation times framework.

We introduce the notation . We consider the random discretization scheme used in [Clinet and Potiron, 2018a] (Section 4) and adapted from [Jacod and Protter, 2011] (see Section 14.1). We assume that there exists an Itô-semimartingale which satisfies Assumption 4.4.2 p. 115 in [Jacod and Protter, 2011] and is locally bounded and locally bounded away from , and i.i.d that are independent with each other and from other quantities such that

| (2.3) | |||||

| (2.4) |

We further assume that , and that for any , , is independent of . If we define and the number of observations before as we have that and that121212Actually the convergence is , i.e. uniformly in probability on for any . Equation (2.5) can be shown using Lemma 14.1.5 in [Jacod and Protter, 2011]. The uniformity is obtained as a consequence of the fact that and are increasing processes and Property (2.2.16) in [Jacod and Protter, 2011].

| (2.5) |

When there is no room for confusion, we sometimes drop in the expression, i.e we use .

The information

Given the process , the observed information is assumed to be conditionally stationary, i.e. for any , , , , and for any continuous and bounded function we have

| (2.6) |

We introduce the difference between the explicative part taken in and in as

| (2.7) |

and for any , and for any multi-indices , , where the subcomponents of and are themselves dimensional multi-indices, the following quantities conditioned on the price process

| (2.8) | |||||

| (2.9) | |||||

| (2.10) | |||||

where and are assumed independent of . Note that conditions (2.8)-(2.10) state that conditional moments of the information process (and its derivatives with respect to ) up to the fourth order are independent of the efficient price. This is weaker than assuming the independence of and (and thus it is weaker than the classical QMLE framework of [Xiu, 2010] where the MMN is assumed independent of ). When (respectively ), we refer directly to (respectively ) in place of (respectively ). To ensure the weak dependence of the information over time and the identifiability of , we also assume for any and the following set of conditions:

| (2.11) | |||||

| (2.12) | |||||

| (2.13) | |||||

| (2.14) |

Remark 1.

Conditions (2.11)-(2.12) ensure the weak dependence over time of the information process whereas Condition (2.14) implies the identifiability of for the QMLE. They are needed in order to derive the limit theory of the QMLE estimators related to that are defined in the next section. Note that we consider a setting where the information process is stationary when conditioned on the efficient price process, which was not assumed in [Li et al., 2016]. In particular conditions (2.11)-(2.12) are stronger forms for stationary sequences of Condition (A.xi), while (2.14) replaces the identifiability assumption (A.x) in their paper. The need for stronger assumptions is due to the fact that in this work, in addition to the consistency with rate of convergence , we also prove the central limit theory for the QMLE related to . On the other hand, the moment condition (2.13) is weaker than the quite strong assumption (A.v) requiring that the information process is uniformly stochastically bounded.

The residual noise

The remaining noise is assumed independent of all the other processes, i.i.d with and , and with finite fourth moment.

Remark 2.

Given the assumptions on the information process and on the residual noise , we have ruled out the case of an heteroskedastic MMN. Although empirical evidence indicates time dependence of the MMN (as pointed out in, e.g, [Hansen and Lunde, 2006]), incorporating heteroskedasticity in our model is beyond the scope of this paper. Note also that we only allow for a weak form of endogeneity for the explicative part (its conditional moments of order or less should not depend on ). Again, we set aside stronger forms of endogeneity in this paper. Nevertheless, we have considered an endogenous and heteroskedastic residual noise in our simulation study and shown that the tests seem reasonably robust to such misspecification.

3 Tests for the presence of residual noise

3.1 Small noise alternative case

We first consider the simple semiparametric model where , the observations are regular which implies that , the residual noise is normally distributed with zero-mean and variance . We further define which in this simple model satisfies . The null hypothesis is defined as whereas the alternative is defined as , where and is a constant which does not depend on . The cases of large noise alternative and alternative are respectively delayed to Section 3.2 and Section 3.3. To ensure that our method is robust to general information, our strategy consists in considering two distinct likelihood functions conditioned on the information. We define the observed log returns , . Moreover, the returns of information are denoted by , and we further define . Key to our analysis is that is known to the econometrician.

In the absence of residual noise, the observed returns can be expressed as

| (3.1) |

It is then clear that is i.i.d normally distributed centered with variance and the log-likelihood can be expressed as

| (3.2) |

When the residual noise is present, [Aït-Sahalia et al., 2005] show that in the case where there is no information, i.e.

| (3.3) |

features a MA(1) process so that the log-likelihood process of the model is

| (3.4) |

where is the matrix

| (3.5) | |||

| (3.6) |

When incorporating non-null information, the model for the returns can be written as

| (3.7) |

It is then immediate to see that follows a MA(1) dynamic so that we can substitute the log-likelihood function by

| (3.8) |

To assess the central limit theory, we consider the general framework specified in Section 2 and define the quadratic variation as

where , and we assume that almost surely, where . This assumption is necessary to maximize the quasi likelihood function on a well-defined bounded space. This may seem to be a somewhat restrictive condition on the volatility process, but since can be taken arbitrarily large, it does not affect the implementation of the estimation procedure in practice. Under and assuming null information, [Aït-Sahalia and Xiu, 2016] show that the QMLE associated to (3.4) is optimal with rate of convergence . When incorporating information into the model, both QMLE related to (3.2) and (3.8) also turn out to converge with rate . Formally, we assume that , where . We define and as respectively one solution to the equation on the interior of and one solution to the equation on , where and . This corresponds to an extension of parameter space as can take negative values, as in [Aït-Sahalia and Xiu, 2016] (see the discussion at the bottom of p. 8). Such extension is needed because under and with the non-extended space , the parameter would lie on the boundary of the parameter space, making the above procedure inconsistent. In the following theorem, we give the joint limit distribution of assuming that the noise process is of order . We also specify the limit under , i.e when there is no residual noise.

Theorem 3.1.

(Joint central limit theorem for under the small residual noise framework) Assume that and that for some fixed , , where is the fourth order cumulant of . Then, we have -stably131313The filtration is defined as . in law that

where , , ,

is an additional matrix due to the presence of residual noise of the form

and , are two bias terms due to the presence of jumps in the price process. The exact expression of V, , and can be found in Section 9.

In particular, , and thus, under , we have -stably in law that

Remark 3.2.

(Regular sampling) If observations are regular, , and can be specified as

| (3.9) |

We consider now the problem of testing against . To do that we consider the Hausman statistics of the form

| (3.10) |

where is a consistent estimator of that will be defined in what follows. We aim to show that satisfies the key asymptotic properties

| (3.11) | |||||

| (3.12) |

where is a standard chi-squared distribution. Actually, we can deduce (3.11) from Theorem 3.1 along with the consistency of and (3.12) is relatively easy to obtain. As in [Aït-Sahalia and Xiu, 2016], we consider three distinct scenarios, i.e.

-

(i)

constant volatility

-

(ii)

time-varying volatility and no price jump

-

(iii)

time-varying volatility and price jump

This leads us to define two (one estimator is robust to two scenarios) distinct variance estimators and their affiliated statistics in what follows. Due to the non regularity of arrival times, fourth power returns based estimators such as (defined in Section 8) are inconsistent in general. We therefore consider bipower statistics, inspired by [Barndorff-Nielsen and Shephard, 2004b] and [Barndorff-Nielsen and Shephard, 2004a]. If we assume (i) we have that , which can be estimated by

| (3.13) |

The estimator is also robust to (ii), where . Under (iii), . If we introduce which is random and satisfies and , we can estimate with

We first show the consistency of the proposed estimators.

Proposition 3.3.

For any we have, as ,

if we assume the related framework.

We then deduce asymptotic properties of the statistics.

Corollary 3.4.

Let and the associated -quantile of the standard chi-squared distribution. Under the related framework, the test statistics satisfy

| (3.15) |

When there is no residual noise in the model, following the procedure considered in [Li et al., 2016] and [Chaker, 2017], we can estimate the efficient price as

| (3.16) |

By virtue of Theorem 3.1, we have that is consistent and thus we can show the consistency of . It is also immediate to see that

| (3.17) |

Formally, the volatility estimator (3.17) expressed as a function of the estimated parameter is equal to the volatility estimator (also viewed as a function of the estimated parameter) considered in [Li et al., 2016]. Moreover, given the shape of in (3.2), the QMLE and the least square estimator (9) in the cited paper (p. 35) coincide, implying that both volatility estimators are equal. The need to correct for the price prior to using RV in (3.17) can be understood looking at Table 3 (p. 1324) from [Diebold and Strasser, 2013]. In that table, the first column reports the limit of the naive RV. Accordingly, one can see that depending on the serial autocorrelation of , there will be one or more extra autocorrelation terms in the limit. Subsequently, the use of the price estimation in (3.17) permits to get rid of those additive terms.

The following corollary formally states the consistency of and the efficiency of RV when used on . This corresponds exactly to Theorem 2 in [Li et al., 2016]. This also corresponds to Theorem 4 (i) in [Chaker, 2017] when is linear.

Corollary 3.5.

Under , the estimator is consistent, i.e. for any ,

| (3.18) |

Furthermore, we have -stably in law that

| (3.19) |

In particular, when observations are regular and the efficient price is continuous, this can be written as

| (3.20) |

It is interesting to remark that when , convergence (3.19) shows that RV on the estimated price is efficient in the sense that its AVAR attains the nonparametric efficiency bound derived in [Renault et al., 2017]. Indeed, taking , note that our model of observation times falls under the setting of [Renault et al., 2017] (see Assumption 2 and the short discussion below), where, in view of (2.10) on p. 447 in the aforementioned paper, we easily derive that . Thus, (3.19) can be rewritten as

| (3.21) |

which corresponds precisely to the efficiency bound (3.18) on p. 454 in [Renault et al., 2017] in the case .

3.2 Large noise alternative case

If one can detect small noise, one can a-priori detect large noise. In this section, we consider the large noise alternative , where we recall that and . We show that Proposition 3.3 and Corollary 3.4 remain valid in what follows. We have removed the statements related to which obviously stay true.

Proposition 3.6.

Under the related framework, for any we have, as ,

Corollary 3.7.

Under the related framework, the test statistics satisfy

| (3.22) |

3.3 The alternative case

So far we have assumed that the tests were conditional on a specific parametric model where is non-null, so that the null hypothesis and the alternative were considered under the constraint . In this part, we consider the pure i.i.d MMN alternative , where the noise may be small () or large () with . Note that this is precisely the same alternative as that of [Aït-Sahalia and Xiu, 2016]. We prove in what follows that Proposition 3.3 and Corollary 3.4 remain true up to an innocuous assumption on the fitted model , which is satisfied on all the models considered in this paper. Here again we have removed the statements related to .

Proposition 3.8.

Assume that there exists in the interior of such that . Then, under the related framework, for any we have, as ,

Corollary 3.9.

Assume that there exists in the interior of such that . Then, under the related framework, the test statistics satisfy

| (3.23) |

4 Goodness of fit

The goal of this section is threefold. First, we introduce a measure of goodness of fit which can be used by the high frequency data user prior to testing to compare several models and assess if one or several candidates are worth testing. Second, we provide the central limit theory of the QMLE related to the model including the residual noise when assuming that it is present, and we deduce an estimator of the measure. Finally, we give a practical guidance to estimate volatility -this sequence is illustrated in the finite sample analysis that follows.

4.1 Definition

Prior to looking at the Hausman tests, it is safer to assume a model where the variance of the residual noise is non negligible. We introduce the proportion of variance explained as

| (4.1) |

which is a measure of goodness of fit of the model. This measure is almost identical to from Remark 8 (p. 37) in [Li et al., 2016]. The estimation of (4.1) is based on the QMLE related to the model including the residual noise and given in (4.5).

4.2 Central limit theory

Throughout the rest of this section we assume that the residual noise variance does not depend on . When , this corresponds to a widespread assumption on the residual noise (which in this case corresponds exactly to the MMN). In this setting and further assuming that the volatility is constant, [Aït-Sahalia et al., 2005] show that the MLE related to (3.4) is efficient with convergence rate and obtain the robustness of the MLE in case of departure from the normality of the noise. [Xiu, 2010] shows that the procedure is also robust to time-varying volatility. We further investigate in [Clinet and Potiron, 2018a] the behavior of the estimator when adding jumps to the price process and considering non regular stochastic arrival times. In what follows we show in particular that converges at the same rate . We assume that , where with . Finally, is defined as one solution to the equation on the interior of .

Theorem 4.1.

We have -stably in law that

| (4.2) |

where the term stands for the fourth order cumulant of , and is the Fisher information matrix related to defined as

Remark 4.2.

(Variance gain when estimating the quadratic variation) If we assume that the information process is i.i.d, it is also possible to directly estimate the quadratic variation and the global noise variance using the original QMLE of [Xiu, 2010] and generalized to our setting with jumps and stochastic observation times in [Clinet and Potiron, 2018a]. Denoting such estimator by , we have:

| (4.3) |

where . Therefore, in view of (4.2) and (4.3), accounting for the explicative part of the noise in the estimation process results in an asymptotic variance reduction for the volatility estimation of a factor

In particular, when the residual noise is negligible, i.e. in the limit , we see that the asymptotic gain is infinite which is coherent with the fact that in such case the rate of convergence of switches from to as in Theorem 3.1.

Remark 4.3.

(Connection to the literature) [Li et al., 2016] consider a shrinking noise in their Theorem 3, and thus they obtain a faster rate of convergence for the volatility estimator. On the other hand, [Chaker, 2017] considers the same setting as ours in their Theorem 4, but as they are using a modification of the TSRV, they obtain the slower rate of convergence .

Remark 4.4.

(Regular sampling and continuous price case) When the observation times are regularly spaced and the efficient price is continuous, (4.2) can be specified as

| (4.4) |

Remark 4.5.

(Local QMLE) Using the local QMLE, we could further reduce the AVAR of the volatility obtained in (4.2). In the case of regular sampling and continuous price process, we could be as close as possible from the lower efficiency bound defined in [Reiss, 2011]. The proofs of this paper would straightforwardly adapt. The case is treated in [Clinet and Potiron, 2018a].

Based on Theorem 4.1, we can consistently estimate as

| (4.5) |

In accordance with our empirical findings (see Section 6), we also investigate what happens in the case where approaches , which corresponds to the small noise framework of Section 3, where for some fixed , and where . It turns out that under this framework too converges to . In particular, this also proves the consistency of in the case , that is . More precisely, we have the following result.

Lemma 4.6.

(consistency of ) In the large noise case , we have

In the small noise case , , with , we have

4.3 Practical guidance to estimate volatility

In this section, we provide a sequence -not theoretically validated but which behaves correctly numerically in next section- to estimate volatility based on the introduced tests. As a matter of fact, the sequence may suffer from the so-called post-model selection problem (as in, e.g [Leeb and Pötscher, 2005]). This is due to a possible lack of uniformity when pre-testing the presence of residual noise, and may affect the finite sample performance of the volatility estimator constructed from the sequence hereafter. A solution to that issue would be to prove that the proposed inference is uniformly valid with respect to the residual noise magnitude, in a similar way as in [Da and Xiu, 2017], Section 4.3-4.4. In practice, Section 5 of the present paper suggests that in finite sample, the post-model selection problem does not seem to impact much volatility estimation for the considered models. Moreover, we provide steps -here again completely ad hoc, but implemented in our empirical study- to the empirical researcher to investigate if it is worth considering a specific when implementing the tests. A rigorous statistical approach to choose among a class of competitive models in practice based on Bayesian Information Criterion is beyond the scope of this paper and can be found in [Clinet and Potiron, 2018b].

We suggest the following sequence for volatility estimation:

-

•

If the original Hausman tests from [Aït-Sahalia and Xiu, 2016] are not rejected, it is reasonably safe to use RV on the raw data, even though it does not necessarily mean that there is no MMN -in our simulation study and empirical study, we find that the tests are rejected (almost) all the time when used at the highest frequency on fairly liquid stocks-. We emphasize that although not reported in our numerical study results, the original tests from [Aït-Sahalia and Xiu, 2016] when implemented with estimators not robust to autocorrelated MMN (such as RK, PAE, QMLE) are distorted by the presence of MMN of the form with . Accordingly, in line with our numerical study, we strongly advise the user to implement as volatility estimator to be compared with RV. This requires a priori to know and . Another alternative, which does not need any preestimation, consists in using an estimator robust to autocorrelated MMN such as in [Da and Xiu, 2017]. We did not implement this type of estimator in our numerical study. Finally, we insist on the fact that the theory related to such Hausman tests has not been investigated.

-

•

If the original tests are rejected and the tests considered in this paper are rejected, one should stick to .

-

•

If the original tests are rejected and the tests of this paper are not rejected, then one should use .

Finally, we recommend the empirical researcher the following steps to choose a specific prior to implementing the tests on several models:

-

•

The user may implement the original Hausman tests from [Aït-Sahalia and Xiu, 2016] on the raw data. In agreement with the sequence of volatility estimation, we advise the user to choose a volatility estimator robust to autocorrelated MMN.

-

•

If the results seem to indicate the presence of MMN, the user should estimate the ratio (4.1).

-

•

If the ratio turns out to be close to 100%, then a proper investigation using the tests should be carried out.

To illustrate the method, we follow this procedure in our empirical study.

5 Finite sample performance

We now conduct a Monte Carlo experiment to assess finite sample performance of the tests, and validity of the sequence to estimate volatility described in Section 4.3 -which a priori is subject to multiple testing, model selection and post model selection issues- by comparing it to some leading estimators from the literature. We simulate M=1,000 Monte Carlo days of high-frequency returns where the related horizon time is annualized. One working day corresponds to 6.5 hours of trading activity, i.e. 23,400 seconds.

The efficient price

We introduce the Heston model with U-shape intraday seasonality component and jumps in both price and volatility as

where

with , , , the signs of the jumps are i.i.d symmetric, is a homogeneous Poisson process with parameter so that the contribution of jumps to the total quadratic variation of the price process is around 50%, , , , , , the volatility jump size parameter , the volatility jump time follows a uniform distribution on , , , , is a standard Brownian motion such that , , is sampled from a Gamma distribution of parameters , which corresponds to the stationary distribution of the CIR process. To obtain more information about the model and values, see [Clinet and Potiron, 2018a]. The model is inspired directly from [Andersen et al., 2012] and [Aït-Sahalia and Xiu, 2016].

The observation times

We consider three levels of sampling: tick by tick, 15 seconds, 30 seconds. The observation times are generated regularly except for the tick by tick case. For the latter, we assume that , and that are following an exponential distribution with parameter . We have that the rate of arrival times exhibits a usual U-shape intraday pattern, as pointed out in [Engle and Russell, 1998] (see discussions in Section 5-6 and Figure 2) and [Chen and Hall, 2013] (see Section 5, pp. 1011-1017). We fix , and following the empirical values exhibited in [Clinet and Potiron, 2018c], which implies that the sampling frequency is on average faster than one second.

The information

We implement two models: Roll model and the signed spread model. As in the simulation study from [Li et al., 2016], the trade indicator is simulated featuring a Bernoulli process with parameter and with an autocorrelation chosen equal to 0.3. We fix the parameter in the case of Roll model. For the signed spread model, we further simulate the spread as an AR(1) process with mean , variance and correlation parameter which amounts to . The parameter is chosen equal to . The values of the parameters correspond roughly to the fitted values141414Although not fully reported in the empirical study..

The residual noise

To assess finite sample performance of the tests, we consider two types of (finite sample) alternative. In , we assume that the residual noise is i.i.d normally distributed with zero-mean and variance . In , which in particular does not accommodate with the assumptions of this paper, we assume that the residual noise

where , , and are standard independent normally distributed variables, and . With that specification, the residual noise has also variance approximately equal to (with ), is serially correlated (since is serially correlated), heteroskedastic, endogenous as both correlated with the efficient returns and the explicative part of the MMN.

To validate the sequence to estimate volatility, we consider , where the latter corresponds to a setup where there is no residual noise for half of the days in the sample and a residual noise with variance for the remaining half in the sample.

Remaining tuning parameters

Although the likelihood-based estimators do not require any tuning parameter, we need to select some parameters for the truncation method used when computing and . We choose , , , , and , consistently with [Aït-Sahalia and Xiu, 2016] (except for which was set equal to 3, because this was yielding too many jumps detection in our case).

Concurrent volatility estimators and simulated model considered for comparison

We consider a group of eight concurrent volatility estimators which is a mix of estimators considered in this paper and leading estimators from the literature. corresponds to the sequence introduced in Section 4.3. The QMLEexp is , and is actually equal to estimated-price RV defined in [Li et al., 2016] since both considered are linear. The QMLEerr is defined as . The E-QMLE is the two-step estimator with price estimation first and (regular) QMLE on the price estimates. We also have some popular estimators QMLE, PAE, RK, and RV.151515Details on the choice of tuning parameters for the PAE and the RK can be obtained upon request to the authors. In particular, excluding , no tests are applied prior or post to the estimation methods.

The simulated model considered features time-varying volatility but does not incorporate jumps in the price process as most methods considered are not robust to such environment. Moreover, the sampling times are regular (with high frequency sampling every second) since some methods may be badly affected when they are not.

Results

We first discuss the results to assess finite sample performance of the tests. We compute and when dealing with the tick by tick simulated returns, and , and , which are introduced in the appendix, when looking at sparser observations. We report in Table 2 and in Table 3 the fraction of rejections of at the 0.05 level for different scenarios. The statistics have desired fraction of rejections, and the power is reasonable (it is actually slightly better when the residual noise from the alternative has a general form which actually breaks the theoretical assumptions of this paper). There are two important lessons to take from this part. First, the power is much more satisfactory in the tick by tick case, and thus we insist that the high frequency data user should make inference using all the data available. Second, depending on the simulated scenario, i.e. constant volatility, time-varying volatility including jumps or not, the related statistic behave slightly better than the other statistics. One should confirm accordingly the type of data at hand prior to choosing the related statistic to use. This will heavily depend on data pre-processing, such as controlling for diurnal pattern in volatility (see [Christensen et al., 2018]) and/or removing jumps.

We now discuss about the validity of the sequence given in Section 4.3. Table 4 reports the bias, standard deviation and RMSE of the eight concurrent volatility estimators for the three scenarios, i.e. no residual noise, residual noise and a mix of both aforementioned scenarios. As expected from Theorem 3.1, QMLEexp leads the cohort when there is no residual noise. QMLEerr has approximately a standard deviation times as big as that of QMLEexp, which is in line with the theorem. The sequence using the tests’ RMSE is very close to that of QMLEexp, although slightly bigger, which is due to the fact that the test to assess if the MMN is fully explained by some variables of the limit order book are (falsely) rejected one time over twenty. In case of non-zero residual noise, QMLEerr performs the best which is not surprising since the estimation procedure is residual noise robust. The sequence using the tests’ RMSE is almost the same as that of QMLEerr, which is explained by the fact that the tests from this paper are (rightly) rejected 499 days over 500. On the other hand, QMLEexp suffers since it is not residual noise robust. Overall, the sequence using the tests is leading the group (in terms of RMSE) in the mix scenario (which is the most realistic case). In particular, note that the first step in the sequence using the original tests of [Aït-Sahalia and Xiu, 2016] implemented with QMLEerr as volatility estimator compared with RV has no distortion on the finite sample results since tests are rejected all the time. QMLEerr comes second while being relatively close from the sequence using the tests. E-QMLE is virtually tied with QMLEerr, which can be explained by the fact that they are asymptotically equivalent. The other estimators perform more poorly.

6 Empirical study

Our main dataset consists of one calendar month (April 2011) of trades and quotes for thirty one CAC 40 constituents traded on the Euronext NV. The data for individual stocks were obtained from the TAQ data and the Order book data.161616The data were obtained through Reuters and provided by the Chair of Quantitative Finance of Ecole Centrale Paris. We keep quotes corresponding to best bid/ask price, which are often referred to as Level 1 data. To obtain the information of trade type, we implement Section 3.4 in [Muni Toke, 2016].171717The code is available on our websites. A comparison with the simple and popular Lee-Ready procedure introduced in [Lee and Ready, 1991] can be consulted in Section 5 of the cited paper. The timestamp is rounded to the nearest millisecond.

To prevent from opening and closing effects, we restrict our dataset starting each day at 9:30am and ending at 4pm. We consider the data in tick time, for an average of 3,000 daily trades and a quote/trade ratio bigger than 20. The most active days include more than 10,000 trades, whereas the less liquid days are around 500 trades. Descriptive statistics on the individual stocks are detailed on Table 5. Using the regular QMLE restricted to , we find that the MMN variance lies within and , taking the value on average.

We first implement the tests of [Aït-Sahalia and Xiu, 2016] on the observed price on tick-by-tick data. The results can be found on Table 8. The six tests consistently indicate that we reject those tests almost all the time, indicating that there seems to be MMN at the highest frequency for the stocks and days considered. Accordingly, we report in Table 6 the measure of goodness of fit of several leading models: Roll, Glosten-Harris, signed timestamp, signed spread model, signed quoted depth, the order flow imbalance, a linear combination of all the aforementioned models and a non-linear signed spread. The signed spread model incontestably dominates with an astonishing proportion of variance explained estimated around 99%. This dominance is in fact consistent across sampling frequencies, stocks and over time, although not fully reported. Finally, this measure stagnates when sampling at sparser frequencies, and we argue that this is because there is (almost) no remaining noise.

Among the concurrent models, the goodness of fit of Roll model is very decent with a four fifth proportion of variance explained at the highest frequency and increasing when diminishing the sampling frequency. Yet this feature hints that the model cannot be considered as reasonably free of residual noise when using tick by tick data. The measure related to Glosten-Harris model is slightly bigger, suggesting that the information on the volume helps to improve the fit to a certain extent. Those estimated values are in line with the results discussed in the empirical study of [Li et al., 2016]. The fit is not as good on other models. We have tried many other alternative models (such as linear combinations of the aforementioned models) but have not found any significant improvement in the fit of the signed spread model, as reported in Table 6. In particular adding a Roll component to it was not found to improve the fit much.

We further investigate if the signed spread model can fairly be considered as free from residual noise by implementing the two tick-by-tick-robust Hausman tests. For each individual stock and test, the fraction of rejection at the 0.05 level is reported on Table 7. Although not reported, the results are very similar when using the other three statistics. Over the thirty one stocks, the averaged-across-tests fraction lies within 0.00 and 0.11 for twenty eight constituents (hereafter denoted as the main group, and which features a proportion of variance explained bigger than 99%), whereas picking at 0.11, 0.16 and 0.42 for the three remaining components (henceforth referred as the minor group, which features a proportion of variance explained slightly below 95%). The observed fraction of rejections of the main group constituents can be considered as reasonably close to the theoretical threshold 0.05 hence we can not reject the null hypothesis for them and this indicates that stocks from the main group can be considered as fairly free from residual noise. On the contrary the rejection is clear for the three stocks from the minor group.

An example of estimated efficient price can be seen on Figure 1. To explore the properties of the estimated price, we recognize it as the given observed price to be tested in [Aït-Sahalia and Xiu, 2016]. Although their tests are by nature related to our tests, the estimators they are using differ from the ones considered in our work, and thus their tests can be regarded as a sensibly independent check on the efficiency of the estimated price. The fraction of rejections of their null hypothesis at the 0.05 level can be consulted on Table 8. When restricting to the main group constituents, the six tests range from 0.05 to 0.09 and are equal to 0.06 on average. When considering the minor group stocks, the same tests range from 0.33 to 0.42. This largely corroborates the fact that the main group stocks are most likely free from residual noise whereas the minor group constituents cannot be considered as such. One feature common to the minor group constituents, namely France Telecom, Louis Vuitton and Schneider Electric, is that they are stocks with large ticks and small spread, which is almost always equal to 1 tick. This feature can be seen on Table 5, as the three stocks share the top 3 in terms of smallest spread, and part of the top 5 when looking at the smallest ratio of price over tick size. Even for those stocks, our findings strongly indicate that the estimated price is much closer from efficiency than the observed price on which the tests are rejected 100% of the time.

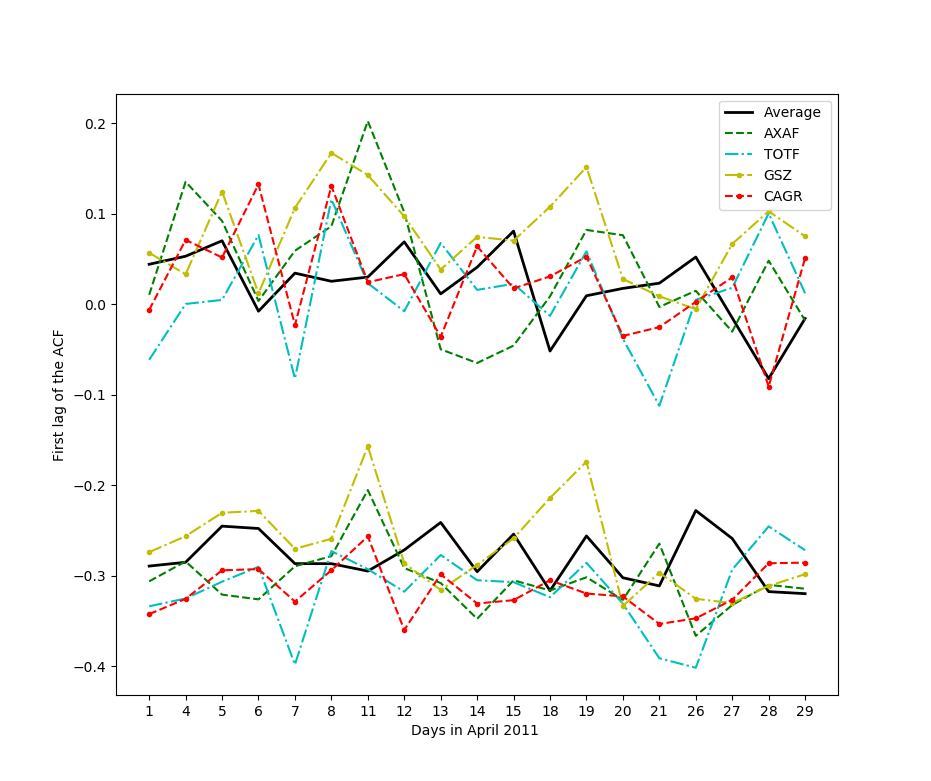

Another way to question the efficiency of the estimated price consists in inspecting the first lag of the autocorrelation function and the visual "signature plot" procedure of [Andersen et al., 2000] (see also [Patton, 2011]). This can be seen on Figure 2-3. A satisfactory amelioration of the first lag of the autocorrelation function is noticeable, as it averages 0.02 when looking at the estimated price whereas -0.28 when taking the observed price. The signature plot is also acceptable as it is relatively flat.

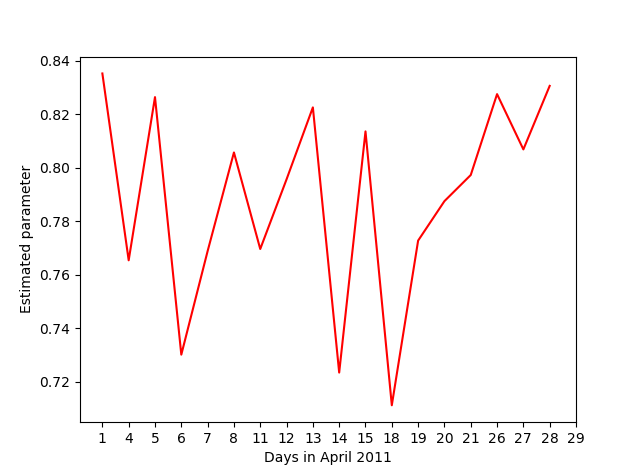

Finally, the maximum likelihood estimation in both settings delivers very similar (the difference is at most equal to even when considering the three stocks from the minor group) and stable estimates of the parameter which lies systematically between 0.60 and 0.90 with an average around 0.79 and a standard deviation slightly above 0.03 when sampling at the highest frequency. The estimation is also stable across sampling frequencies as the average values are and when considering the 15-second and 30-second frequency, respectively. Moreover, Figure 4 documents that the daily estimates averaged across stocks are also relatively stable over time.

Note that we can also consider as in [Chaker, 2017] (p. 15) the finite sample correction by instrumental variables. This slightly shifts estimation of the parameter towards the origin, with a decrease of magnitude one quarter of its value in the estimates. As it can improve finite sample properties, we implemented and chose to work with such finite sample correction, including in our implemented tests. Finally, we have considered variance estimators based on raw returns instead of estimated price returns for stability reason.

7 Conclusion

The paper introduces tests to assess if the market microstructure noise can be fully explained by the informational content of some variables from the limit order book. Two novel quasi-maximum likelihood estimators are extensively studied in the development. Subsequently, based on a common procedure the paper proposes an efficient price estimator.

We emphasize that the method can be easily implemented to assist anyone who is working with high frequency data. The empirical study should be taken as a reference for repeating the exercise, i.e. first testing among a class of candidates and then choosing one specific model based on the measure of goodness of fit. We hope this provides an alternative and reliable solution to the common dilemma between sparsing and using sophisticated noise-robust estimators.

We also call attention to the fact that when the market microstructure noise is fully explained by the limit order book, other quantities beyond quadratic variation, such as pure integrated volatility (by truncation), integrated powers of volatility, high-frequency covariance or even volatility of volatility can be estimated following the same procedure as investigated in our recent work [Clinet and Potiron, 2017].

Finally, although we have checked that there is no major distortion of our tests in finite sample and that they can be useful to improve the precision of volatility estimation, challenging and interesting avenues for future research include a possible improvement of the method checking whether, or not, the testing procedure suffers from the classical post-model selection issue as presented in [Leeb and Pötscher, 2005].

APPENDIX

8 Definition of supplementary variance estimators when observations are regular

In this section, we provide supplementary variance estimators in the case of regular observations. We consider the three aforementioned scenarios, i.e.

-

(i)

constant volatility

-

(ii)

time-varying volatility and no price jump

-

(iii)

time-varying volatility and price jump

In the case (i), we have from Theorem 3.1 that . This can be simply estimated by

| (8.1) |

Under (ii), we have which can be estimated by:

| (8.2) |

where was previously defined in (1.4). When assuming (iii), we have . If we introduce such that and with , and , the asymptotic variance can be estimated via

| (8.3) | |||||

The estimator is based on the truncation method considered in [Mancini, 2009]. The three variances estimators for are identical to the ones introduced in [Aït-Sahalia and Xiu, 2016], up to a scaling factor . It is due to the fact that the authors scale their Hausman test statistics by whereas we used instead. Those three estimators satisfy the conditions of Proposition 3.3 and Corollary 3.4. In the corresponding proofs, we also show for the case .

9 Expression of the asymptotic variance terms defined in Theorem 3.1

We recall that

| , | ||||

Moreover, we also have

| (9.1) | |||||

| (9.2) |

so that and . The components of V are expressed as

Remark 3.

When the volatility is constant, the observation times are regular and there are no jumps in the price process, we have , , and thus replacing and using (9.1) and (9.2), we have that the variance matrix for () is of the form

equal to

which corresponds to the limit variance of Theorem 2 p.371 of [Aït-Sahalia et al., 2005] in the abovementioned framework.

For the information part, we define for any the quantity

along with the matrices

Then, the asymptotic variance and covariance terms can be expressed as

Finally, introducing , and is the only index such that the bias terms are expressed as

In particular, under , and so that

10 Proofs

10.1 Simplification of the problem

We give an additional assumption which is harmless (see e.g. the discussion in [Clinet and Potiron, 2018a], Section A.1). Note that we can apply Girsanov theorem as all the assumptions on the information also hold on the risk-neutral probability.

(H) We have . Moreover , , , , , , , are bounded. Given an a priori number , we also have .

From now on, to avoid confusion as much as possible, we explicitly write the exponent in the expressions , , etc. Note also that, by virtue of Lemma 14.1.5 in [Jacod and Protter, 2011], recalling the definition , and we have

| (10.1) |

We sometimes refer to the continuous part of defined as

| (10.2) |

We define the -field that generates the observation times and which is independent of and . We will often have to use the conditional expectation , that we hereafter denote for convenience by . We also define the discrete filtration , and the continuous version . Note that by independence from , admits the same Itô semi-martingale dynamics in the extension .

Finally, all along the proofs, we recall that we write in place of , we define , for some to be adjusted, and we let be a positive constant that may vary from one line to the next.

10.2 Estimates for

We start this appendix by giving some useful estimates for the matrix which was defined in (3.6). Let us define . Note that , and . In all this section, the expression means a (possibly random) function , where , which is bounded uniformly in all its arguments and in under the constraint , and which is on the compact , such that its partial derivatives are also bounded. In particular, for any multi-index we have the useful property . Finally, we define for the function . Note that is always dominated by .

Lemma 10.1.

(expansions for ) There exists , such that uniformly in ,

Proof.

From the relation , it is sufficient to show the result with . Under the change of variable

we recall the expression of

| (10.3) |

taken from [Xiu, 2010], eq. (28) p 245. By a short calculation we also have the expansions

| (10.4) |

and

| (10.5) |

Now, for the first term in the numerator, we can write

Moreover, as , similar calculations lead to the estimates

and finally

We also have the expansion

by direct calculation. Overall we thus get

up to the terms related to and , which we gather in .

∎

For a matrix , we associate the matrix and whose components respectively satisfy

| (10.6) |

and

| (10.7) |

with the convention when or . We recall the following lemma taken from [Clinet and Potiron, 2018c].

Lemma 10.2.

Let , with , , and define

and the same way. Then we have the by-part summation identities

We define accordingly , and . In the next lemmas we derive some estimates for such matrices.

Lemma 10.3.

(expansions for ) We have the approximation, uniform in ,

where .

Proof.

Once again we assume without loss of generality that . From Lemma 10.1 and the definition of , some calculation gives, up to the term ,

and expanding the terms in parenthesis we get the result.

∎

From the previous lemma we deduce by similar computations an expansion for .

Lemma 10.4.

(expansions for ) If , we have the approximation, uniform in

| (10.8) |

Moreover, uniformly in ,

| (10.9) |

10.3 Estimates for the efficient price

Hereafter, we adopt the same notation convention as in [Clinet and Potiron, 2018a], Section A.3. For a process , and we write . We also write . Finally, for interpolation purpose we sometimes write the continuous version . Let us define

| (10.10) |

We recall the following standard estimates.

Lemma 10.5.

We have, for some constant independent of ,

| (10.11) |

| (10.12) |

| (10.13) |

| (10.14) |

10.4 Estimates for the information part

In this section we derive some asymptotic results for the information part. We define for

| (10.15) |

along with the asymptotic fields

| (10.16) |

and

| (10.17) |

By Lemma 10.4, we have the following matrix decomposition for . Let

| (10.18) |

Then we have

| (10.19) |

where are respectively the identity matrix and the matrix whose components are all equal to .

Lemma 10.6.

Let be a multi-index such that . if , then we have

| (10.20) |

Moreover, if , then we have

| (10.21) |

Proof.

First note that by Lemma 10.2, has the representation

| (10.22) |

and thus by (10.19) admits the decomposition

Consider now some multi-index such that , and first assume that . Let us denote

| (10.23) |

and a similar definition for . We show (10.20). First note that in that case since and does not depend on . Moreover, it is immediate to see that the term in is negligible given the factor . Let us show now that we have

| (10.24) |

which after some straightforward calculation is equivalent to showing that

| (10.25) |

By the classical variance-bias decomposition, (10.25) will be proved if we can show uniformly in that we have

| (10.26) |

on the one hand, and

| (10.27) |

on the other hand. We start by (10.26). Recall that for some . From the definition of in (10.18), it is straightforward to see that as soon as , and otherwise. Therefore, we have

| (10.28) |

From the symmetry we split the sum as

and first we have

where the estimates uniformly in is a consequence of Assumption (2.11). Now we also have

by the same argument. Thus we have proved (10.26). Now, using a similar formula as for [McCullagh, 1987], Section 3.3 p. 61, (10.27) can be expressed as the sum

| (10.29) |

where by the Leibniz rule,

| (10.30) |

with , , where and are dimensional multi-indices such that , and

| (10.31) |

First, we have

Now, since we can swap the elements of without loss of generality we can assume that is symmetric in so that we have up to a multiplicative constant

by Assumption (2.12). On the other hand, following a similar path as for the bias case, we can reduce up to negligible terms the elementary terms of to

where the last estimate is obtained by application of Assumption (2.11). Similar reasoning also shows the negligibility of the terms in . Thus we have proved (10.27), so that (10.24) holds true. To complete the proof of (10.20), it remains to show

| (10.32) |

which can be expressed as

| (10.33) |

We adopt the same bias-variance approach as before, and first compute using the symmetry ,

| (10.34) |

Now, we have immediately , so that

| (10.35) |

uniformly in . Thus, by (10.34) and (10.35) we have

and noticing that , we easily conclude as before by the dominated convergence theorem along with Assumption (2.11) that

| (10.36) |

Moreover, the variance term is treated as previously.

Finally, for (10.21), similar computations yield the result. Note that when , the diagonal terms of predominate, hence there is absence of higher order correlations , , in the limit. ∎

To deal with the cross terms, we define in the same fashion as before

| (10.37) |

Lemma 10.7.

Let be a multi-index such that . Then, if , we have

| (10.38) |

If , we have

| (10.39) |

Proof.

Let us first show (10.38). By Lemma 10.2, we have the representation

| (10.40) |

Accordingly, we start by showing that

| (10.41) |

In the case where is continuous, that is , we have

Now, using , and that by Assumption (H) where can be taken arbitrary small, we get

and summing first over and using Assumption (2.11), we get

uniformly in by direct calculation for the last estimate. Now, when for sufficiently large, using the finite activity property of the jump process it is easy to see that an additional term appears in the quadratic expression,

| (10.42) |

where is the finite number of jumps of on , the related jump times, and is the only index such that . Given the estimate of of the previous section and the definition of , we immediately see that the coefficients for some , and thus (10.42) is negligible so that we have (10.41). Now we show that we have

| (10.43) |

By independence, we immediately have

| (10.44) |

and from here using that when on the one hand, then summing over and applying Assumption (2.11) and finally computing the explicit sum of exponential terms leads to

| (10.45) |

uniformly in . Thus we have proved (10.38). Finally, (10.39) is proved similarly. ∎

10.5 Proof of Theorem 4.1

We derive the limit theory for (hereafter denoted by ) when . In our terminology, we recall that we have for any and up to an additive constant term

| (10.46) |

with , where we also recall that the definition of can be found in (10.3). Moreover, note that does not depend on and corresponds precisely to the quasi log-likelihood with no information as studied in [Xiu, 2010] and extended to a more general setting in [Clinet and Potiron, 2018a]. On the other hand, is the additional part incorporating and depends on the whole vector . Following a similar procedure as in [Xiu, 2010] and [Clinet and Potiron, 2018a], we introduce the approximate log-likelihood random field as

| (10.47) |

with

and

Consider the diagonal scaling matrix

| (10.48) |

Define also for the scaled scores , , and . Accordingly, the approximate scores , , and admit the same definition replacing by . We start by a technical lemma to ensure the uniform convergence of some random fields.

Lemma 10.8.

Let be a sequence of random variables of class in , each convex compact, such that , and a sub -field of the general -field. For any multi-index such that , we assume that

Then we have the uniform convergence

| (10.49) |

Proof.

By Theorem 4.12 Part I case A (taking , ) from [Adams and Fournier, 2003], we apply Sobolev’s inequality and define some constant such that we have

∎

Lemma 10.9.

(Asymptotic score) For any , let

We have

| (10.50) |

Proof.

Since , the lemma will be proved if we can show that

| (10.51) |

and

| (10.52) |

uniformly in . Note that (10.51) is a consequence of Lemma A.3 in [Clinet and Potiron, 2018a]. For (10.52), by Lemma 10.7 combined with Lemma 10.8, we have uniformly in that . Thus it is sufficient to show that we have the convergence (10.52) for . Combining Lemma 10.6 and Lemma 10.8, we obtain

| (10.53) |

∎

Theorem 10.10.

(consistency). If is the QMLE, we have

| (10.56) |

Proof.

We extend the proof of Lemma A.4 in [Clinet and Potiron, 2018a], that is, since we already have

| (10.57) |

by Lemma 10.9, we show that for any

| (10.58) |

Given the form of , the equality is immediate. Note also that the left hand side inequality of (10.58) will be automatically satisfied if we show that as soon as by a continuity argument since is compact. Let us then take such that , and assume first that . In that case, we have

by (2.14), which leads to a contradiction. We thus get and in a similar way, we also have

that implies . Finally, the first component of leads to the domination

so that we can conclude .

∎

Let be the scaled Hessian matrix of the likelihood field, defined as

| (10.59) |

and similarly , , , , .

Lemma 10.11.

(Fisher information) For , let be the matrix

| (10.60) |

We have, for any ball , centered on and shrinking to ,

| (10.61) |

Proof.

As for the proof of Lemma 10.9, we have

| (10.62) |

uniformly in by Lemma A.5 in [Clinet and Potiron, 2018a], so that by the identity the lemma will be proved if we can show

| (10.63) |

uniformly in . Since , an immediate application of Lemma 10.7 and Lemma 10.8 yields . Moreover, by Lemma 10.6 and Lemma 10.8, we have

| (10.64) |

with

| (10.65) |

Thus, by continuity of , we deduce

| (10.66) |

and moreover it is immediate to check that

| (10.67) |

in view of of definitions (2.7), (2.9), (10.16) and (10.17). ∎

We now extend the notations of [Clinet and Potiron, 2018a] (A.27)-(A.30) p. 128, and we define a few processes involved in the derivation of the central limit theorem. For , and ,

| (10.68) | |||||

| (10.69) | |||||

| (10.70) | |||||

| (10.71) | |||||

| (10.72) |

We also define the three-dimensional vectors for . In all the definitions (10.68)-(10.72), the terms involving the parameters such as , , … are evaluated at point , for some . For , when properly scaled, the processes admit limit distributions whose expressions can be found in Lemma A.6, A.7, A.9 and A.10 of [Clinet and Potiron, 2018a]. We complete these results and show that tends in distribution conditioned on to a normal distribution. Before stating the results, we recall that for a -field , a random vector and a sequence of random vectors in , is said to converge in law towards conditioned on if we have for any

| (10.73) |

Lemma 10.12.

We have, conditionally on , the convergence in distribution

| (10.74) |

Proof.

Since , it is sufficient to prove the marginal CLT for . The proof is conducted in two steps.

Step 1. We introduce

| (10.75) |

We show that . We decompose

| (10.76) |

where

| (10.77) |

| (10.78) |

and

| (10.79) |

Now, by a similar proof as in Lemma 10.7, we have easily . Moreover, by application of Lemma 10.4, Assumption 2.11 and the independence of and , we easily get that . Finally, by Lemma 10.4 we have so that we obtain directly by independence of and and for each component of , ,

and thus .

Step 2. Now we show that conditionally on (and so conditionally on ). To do so, we will apply a conditional version of Theorem 5.12 from [Kallenberg, 2006](p. 92) with respect to . Accordingly, we first remark that we have the representation where are rowwise conditionally independent and centered given . To get the desired convergence in distribution, it is thus sufficient to show that

| (10.80) |

and Lindeberg’s condition, for some ,

For (10.80), we immediately note that

| (10.81) |

where we have used the independence of and , and where the final step is a straightforward consequence of conditions (2.11) and (2.12). Moreover Lindeberg’s condition (10.81) for is also easily verified using moment conditions and stationarity of the information process.

∎

Lemma 10.13.

We have for any , taking , stably in , the convergence in distribution

where .

Proof.

Note that we have the decomposition

First we show that converges in distribution conditioned on . By Lemma A.9 and A.10 in [Clinet and Potiron, 2018a], and both tend in distribution conditioned on to mixed normal distributions of respective asymptotic variances

| (10.82) |

and

| (10.83) |

Moreover, by independence of with the other processes and the fact that and are uncorrelated, we deduce that the conditional covariance terms between any pair , , are null, so that along with the marginal convergence obtained in Lemma 10.12 this automatically yields the convergence in law conditioned on

By Slutsky’s lemma and Lemma A.6 and A.7 from [Clinet and Potiron, 2018a], we also have the -stable convergence in distribution of towards a mixed normal distribution of random variance

| (10.84) |

Finally, by application of Proposition A.8 from [Clinet and Potiron, 2018a], we deduce the joint -stable convergence of , hence the convergence of the global term , and we are done.

∎

We are now ready to prove the central limit theorem.

Proof of Theorem 4.1.

The proof follows exactly the proof of Theorem A.12 in [Clinet and Potiron, 2018a] in the case , and replacing by , and the score function along with the Fisher information by their three dimensional counterparts.

∎

10.6 Proof of Theorem 3.1

In the case , that is in the small residual noise framework, we are interested in deriving the joint law of two estimators, which are and , which is obtained under the no-residual noise constraint in the quasi-likelihood function. For the former estimator, the limit theory is fairly different from the case of a fixed non-zero noise. Indeed, we are going to show that the rate of convergence is changed to . Moreover, the noise and price increments being of the same order, complex interaction terms now appear in the limit variance of the estimators. To derive a CLT for , let us reformulate a bit the problem and, introducing , , and , we are now interested in showing that

| (10.85) |

admits a CLT with rate . We note that is the QMLE related to the new log-likelihood

| (10.86) |

where now is replaced by with

| (10.87) |

and is one maximizer in the variables of

| (10.88) |

that is (10.86) with , where is the identity matrix. We now adopt somewhat similar notations to [Aït-Sahalia and Xiu, 2016], proof of Theorem 1, and we simplify the problem introducing the change of variables

and when . We have

| (10.89) |

with the convention . We are thus going to derive the asymptotic properties of

obtained by maximization of the log-likelihood functions seen respectively as functions of and . Given the form of and , we see that there exists and such that the optimizations are respectively conducted on the sets , and . Then, we will get back to by the delta method.

We keep similar notations as in the previous part and we write the score function for the first experiment, and similarly . Sometimes we will consider the joint process . We also naturally adapt the notations (10.15) and (10.37) to the small noise context

| (10.90) |

and

| (10.91) |

We first give the limit of both estimators when .

Theorem 10.14.

(consistency) Assume that . Define . Let , and . Let

We have

In particular, under the null hypothesis , both estimators are consistent as we have

Proof.

We show separately the consistency of and . Let us start with . The methodology for the proof is the same as those of Lemma 10.9 and Theorem 10.10. First, let us define

| (10.92) |

| (10.93) |

for any multi-index such that , and with

with , and

| (10.94) |

Therefore, adapting the reasoning from [Aït-Sahalia and Xiu, 2016] (p. 45) to our setting (by (10.1) we have that the step size of the observation grid ) and combining them with (10.93), (10.94) and Lemma 10.8, we get the convergence

| (10.95) |

where

Now, by a classical statistical argument (see e.g [Van der Vaart, 2000], Theorem 5.9) along with (10.95), the consistency of will be proved if for any , where , and where , and if . The second assertion is immediate. To prove the former, let us take an arbitrary number and consider . We are going to show that on the one hand, and on the other hand. In the first case, by hypothesis , and writing , we automatically have that is a symmetric positive matrix for any as a simple consequence of the Cauchy-Schwarz inequality and the stationarity of the information process. Thus, writing the minimal eigenvalue of and , we get that in the first case

In the second case, since is a compact space a continuity argument shows that it is sufficient to prove that if and only if . Let thus such that the score at point is null. Given the shape of and the positivity of for any , yields . Then

yields the second order equation , which in turn implies (the other root being non-admissible). Finally

gives replacing by its expression, and thus . In particular, when , this gives and .

We now derive the limit of . By the relation (10.88) we also immediately deduce that

where

and

From there, a similar reasoning to the case applied to yields the convergence in probability of towards . In particular, the volatility component is consistent under the null hypothesis and inconsistent otherwise whereas the information estimator is consistent in both situations. ∎

We now introduce, as in the previous section,

| (10.96) |

and

| (10.97) |

Lemma 10.15.

(Fisher information) Let and be the matrices

| (10.98) |

and

| (10.99) |

where . We have, for any balls and respectively centered on and and shrinking to and ,

| (10.100) |

and

| (10.101) |

Proof.

Adapting the reasoning to get the third and fourth equations (p. 45) in [Aït-Sahalia and Xiu, 2016] (replacing by ), taking the first derivatives of the score functions, and using (10.93) and (10.94) for the information part, we directly obtain the convergence for any

| (10.102) |

where

By continuity of , we immediately deduce that

| (10.103) |

and moreover from the definition of we have

| (10.104) |

since

and using the relations and . Convergence (10.101) is proved in the same way. ∎

and note that, up to exponentially negligible terms, we have the representation

Lemma 10.16.

Let . We have, -stably in law, that

Proof.

Note that . Since , standard calculations involving Burkholder-Davis-Gundy inequalities, assumption (H) and the finite activity property of the jumps easily yield

where

Now, by a straightforward adaptation of Lemma 1 (in the case ) in the proof of Theorem 2 Appendix A.3 p.40 in [Aït-Sahalia and Xiu, 2016] in the case of an irregular grid of the form (2.4), and following the same line of reasoning as the proof of Lemma A.7 in [Clinet and Potiron, 2018a], we conclude that -stably in law,

and we are done. ∎

Lemma 10.17.

Let and define . We have, -stably in law, that

Proof.

Again, given the shapes of and , by standard calculations on martingale increments, introducing and , we easily have

where

and a similar statement for . Proving a central limit theorem for now boils down to following exactly the same calculations as for in the large noise case (see the proof of Lemma A.7 in [Clinet and Potiron, 2018a]) but replacing by and . In particular, a careful inspection of the proof shows that all the calculations remain valid replacing the scalar in the expression of the asymptotic variance, by the matrix

which yields the -stable convergence in distribution

∎

Lemma 10.18.

Let and define . We have, conditioned on the convergence in distribution

Proof.

As in the previous lemma, we introduce the coefficients and . Note that for and for . Moreover, if , and if , . Given the exponential shape of the coefficients, we easily show as for the previous lemma that

where

and a similar definition for . Now, as for , we adapt the proof of from the large noise case (proof of Lemma A.9 in [Clinet and Potiron, 2018a]). Again, all the calculations remain valid except that now should be replaced by and , and accordingly, in the limiting variance the scalar is replaced by the matrix

where the last step is obtained by direct calculation on the coefficients, and because by definition of . ∎

Lemma 10.19.