Online Convex Optimization with Stochastic Constraints

Hao Yu, Michael J. Neely, Xiaohan Wei

Department of Electrical Engineering

University of Southern California

Abstract

This paper considers online convex optimization (OCO) with stochastic constraints, which generalizes Zinkevich’s OCO over a known simple fixed set by introducing multiple stochastic functional constraints that are i.i.d. generated at each round and are disclosed to the decision maker only after the decision is made. This formulation arises naturally when decisions are restricted by stochastic environments or deterministic environments with noisy observations. It also includes many important problems as special cases, such as OCO with long term constraints, stochastic constrained convex optimization, and deterministic constrained convex optimization. To solve this problem, this paper proposes a new algorithm that achieves expected regret and constraint violations and high probability regret and constraint violations. Experiments on a real-world data center scheduling problem further verify the performance of the new algorithm.

I Introduction

Online convex optimization (OCO) is a multi-round learning process with arbitrarily-varying convex loss functions where the decision maker has to choose decision before observing the corresponding loss function . For a fixed time horizon , define the regret of a learning algorithm with respect to the best fixed decision in hindsight (with full knowledge of all loss functions) as

The goal of OCO is to develop dynamic learning algorithms such that regret grows sub-linearly with respect to . The setting of OCO is introduced in a series of work [1, 2, 3, 4] and is formalized in [4]. OCO has gained considerable amount of research interest recently with various applications such as online regression, prediction with expert advice, online ranking, online shortest paths and portfolio selection. See [5, 6] for more applications and backgrounds.

In [4], Zinkevich shows that using an online gradient descent (OGD) update given by

(1)

where is a subgradient of and is the projection onto set can achieve regret. Hazan et al. in [7] show that better regret is possible under the assumption that each loss function is strongly convex but is the best possible if no additional assumption is imposed.

It is obvious that Zinkevich’s OGD in (1) requires the full knowledge of set and low complexity of the projection . However, in practice, the constraint set , which is often described by many functional inequality constraints, can be time varying and may not be fully disclosed to the decision maker. In [8], Mannor et al. extend OCO by considering time-varying constraint functions which can arbitrarily vary and are only disclosed to us after each is chosen. In this setting, Mannor et al. in [8] explore the possibility of designing learning algorithms such that regret grows sub-linearly and , i.e., the (cumulative) constraint violation also grows sub-linearly. Unfortunately, Mannor et al. in [8] prove that this is impossible even when both and are simple linear functions.

Given the impossibility results shown by Mannor et al. in [8], this paper considers OCO where constraint functions are not arbitrarily varying but independently and identically distributed (i.i.d.) generated from an unknown probability model. More specifically, this paper considers online convex optimization (OCO) with stochastic constraint where is a known fixed set; the expressions of stochastic constraints (involving expectations with respect to from an unknown distribution) are unknown; and subscripts indicate the possibility of multiple functional constraints. In OCO with stochastic constraints, the decision maker receives loss function and i.i.d. constraint function realizations at each round . However, the expressions of and are disclosed to the decision maker only after decision is chosen. This setting arises naturally when decisions are restricted by stochastic environments or deterministic environments with noisy observations. For example, if we consider online routing (with link capacity constraints) in wireless networks [8], each link capacity is not a fixed constant (as in wireline networks) but an i.i.d. random variable since wireless channels are stochastically time-varying by nature [9]. OCO with stochastic constraints also covers important special cases such as OCO with long term constraints [10, 11, 12], stochastic constrained convex optimization [13] and deterministic constrained convex optimization [14].

Let be the best fixed decision in hindsight (knowing all loss functions and the distribution of stochastic constraint functions ). Thus, minimizes the -round cumulative loss and satisfies all stochastic constraints in expectation, which also implies almost surely by the strong law of large numbers. Our goal is to develop dynamic learning algorithms that guarantee both regret and constraint violations grow sub-linearly.

Note that Zinkevich’s algorithm in (1) is not applicable to OCO with stochastic constraints since is unknown and it can happen that for certain realizations , such that projections or required in (1) are not even well-defined.

Our Contributions: This paper solves online convex optimization with stochastic constraints. In particular, we propose a new learning algorithm that is proven to achieve expected regret and constraint violations and high probability regret and constraint violations. Along the way, we developed new techniques for stochastic analysis, e.g., Lemma 5, and improve upon state-of-the-art results in the following special cases.

•

OCO with long term constraints: This is a special case where each is known and does not depend on time. Note that can be complicated while might be a simple hypercube. To avoid high complexity involved in the projection onto as in Zinkevich’s algorithm, work in [10, 11, 12] develops low complexity algorithms that use projections onto a simpler set by allowing for certain rounds but ensuring . The best existing performance is regret and constraint violations where is an algorithm parameter [12]. This gives regret with worse constraint violations or constraint violations with worse regret. In contrast, our algorithm, which only uses projections onto as shown in Lemma 1, can achieve regret and constraint violations simultaneously.111By adapting the methodology presented in this paper, our other report [15] developed a different algorithm that can only solve the special case problem “OCO with long term constraints” but can achieve regret and constraint violations. The current paper also relaxes a deterministic Slater condition assumption required in our other technical report [16] for OCO with time-varying constraints, which requires the existence of constant and fixed point such that for all . By relaxing the deterministic Slater condition assumption to the stochastic Slater condition in Assumption 2, the current paper even allows the possibility that is infeasible for certain . However, under the deterministic Slater condition assumption, our technical report [16] shows that if the regret is defined as the cumulative loss difference between our algorithm and the best fixed point from set , which is called a common subset in [16], then our algorithm can achieve regret and constraint violations simultaneously even if the constraint functions are arbitrarily time-varying (not necessarily i.i.d.). That is, by imposing the additional deterministic Slater condition and restricting the regret to be defined over the common subset , our algorithm can escape the impossibility shown by Mannor et al. in [8]. To the best of our knowledge, this is the first time that specific conditions are proposed to enable sublinear regret and constraints violations simultaneously for OCO with arbitrarily time-varying constraint functions. Since the current paper focuses on OCO with stochastic constraints, we refer interested readers to Section IV in [16] for results on OCO with arbitrarily time-varying constraints.

•

Stochastic constrained convex optimization: This is a special case where each is i.i.d. generated from an unknown distribution. This problem has many applications in operation research and machine learning such as Neyman-Pearson classification and risk-mean portfolio. The work [13] develops a (batch) offline algorithm that produces a solution with high probability performance guarantees only after sampling the problems for sufficiently many times. That is, during the process of sampling, there are no performance guarantees. The work [17] proposes a stochastic approximation based (batch) offline algorithm for stochastic convex optimization with one single stochastic functional inequality constraint. In contrast, our algorithm is an online algorithm with online performance guarantees. 222While the analysis of this paper assumes a Slater-type condition, note that our other work [16] shows that the Slater condition is not needed in the special case when both the objective and constraint functions vary i.i.d. over time. (This also includes the case of deterministic constrained convex optimization, since processes that do not vary with time are indeed i.i.d. processes.) In such scenarios, Section VI in our work [16] shows that our algorithm works more generally whenever a Lagrange multiplier vector attaining the strong duality exists.

•

Deterministic constrained convex optimization: This is a special case where each and are known and do not depend on time. In this case, the goal is to develop a fast algorithm that converges to a good solution (with a small error) with a few number of iterations; and our algorithm with regret and constraint violations is equivalent to an iterative numerical algorithm with convergence rate. Our algorithm is subgradient based and does not require the smoothness or differentiability of the convex program. Recall that Nesterov in [14] shows that is the best possible convergence rate of any subgradient/gradient based algorithm for non-smooth convex programs. Thus, our algorithm is optimal. The primal-dual subgradient method considered in [18] has the same convergence rate but requires an upper bound of optimal Lagrange multipliers, which is typically unknown in practice.

Our algorithm does not require such bounds to be known.

II Formulation and New Algorithm

Let be a known fixed compact convex set. Let be sequences of functions that are i.i.d. realizations of stochastic constraint functions with random variable from an unknown distribution. That is, are i.i.d. samples of . Let be a sequence of convex functions that can arbitrarily vary as long as each is independent of all with so that we are unable to predict future constraint functions based on the knowledge of the current loss function. For example, each can even be chosen adversarially based on and actions . For each , we assume are convex with respect to . At the beginning of each round , neither the loss function nor the constraint function realizations are known to the decision maker. However, the decision maker still needs to make a decision for round ; and after that and are disclosed to the decision maker at the end of round .

For convenience, we often suppress the dependence of each on and write . Recall where the expectation is with respect to . Define . We further define the stacked vector of multiple functions as and define . We use to denote the Euclidean norm for a vector. Throughout this paper, we have the following assumptions:

Assumption 1(Basic Assumptions).

•

Loss functions and constraint functions have bounded subgradients on . That is, there exists and such that for all and all and for all , all and all .333We use to denote a subgradient of a convex function

at the point .

If the gradient exists, then is the gradient. Nothing in this paper requires gradients to exist: We only need the basic subgradient inequality for all .

•

There exists constant such that for all and all .

•

There exists constant such that for all .

Assumption 2(The Slater Condition).

There exists and such that for all .

II-ANew Algorithm

Now consider the following algorithm described in Algorithm 1. This algorithm chooses as the decision for round based on and without requiring or .

Algorithm 1

Let be constant algorithm parameters. Choose arbitrarily and let . At the end of each round , observe and and do the following:

•

Choose that solves

(2)

as the decision for the next round , where is a subgradient of at point and is a subgradient of at point .

•

Update each virtual queue via

(3)

where takes the larger one between two elements.

For each stochastic constraint function , we introduce and call it a virtual queue since its dynamic is similar to a queue dynamic. The next lemma summarizes that update in (2) can be implemented via a simple projection onto .

Lemma 1.

The update in (2) is given by ,

where and is the projection onto convex set .

Proof.

The projection by definition is and is equivalent to (2).

∎

Note that if there are no stochastic constraints , i.e., , then Algorithm 1 has and becomes Zinkevich’s algorithm with in (1) since

(4)

where (a) follows from (2); and (b) follows from Lemma 1 by noting that . Call the term marked by an underbrace in (4) the penalty. Thus, Zinkevich’s algorithm is to minimize the penalty term and is a special case of Algorithm 1 used to solve OCO over .

Let be the vector of virtual queue backlogs. Let be a Lyapunov function and define Lyapunov drift

(5)

The intuition behind Algorithm 1 is to choose to minimize an upper bound of the expression

(6)

The intention to minimize penalty is natural since Zinkevich’s algorithm (for OCO without stochastic constraints) minimizes penalty, while the intention to minimize drift is motivated by observing that is accumulated into queue introduced in (3) such that we intend to have small queue backlogs. The drift can be complicated and is in general non-convex. The next lemma provides a simple upper bound of and follows directly from (3).

where is the number of constraint functions; and and are defined in Assumption 1.

Proof.

Recall that for any , if then . Fix . The virtual queue update equation implies that

(8)

where (a) follows by defining .

Define , where ; and . Then,

(9)

where (a) follows from the triangle inequality; and (b) follows from the definition of Euclidean norm, the Cauchy-Schwartz inequality and Assumption 1.

where (b) follows from (9). Rearranging the terms yields the desired result.

∎

At the end of round , is a given constant that is not affected by decision . The algorithm decision in (2) is now transparent: is chosen to minimize the drift-plus-penalty expression (6), where is approximated by the bound in (7).

II-CPreliminary Analysis and More Intuitions of Algorithm 1

The next lemma relates constraint violations and virtual queue values and follows directly from (3).

Lemma 3.

For any , Algorithm 1 guarantees , where is defined in Assumption 1.

where (a) follows from the Cauchy-Schwartz inequality and (b) follows from Assumption 1. Rearranging terms yields

Summing over yields

where (a) follows from the fact .

∎

Recall that function is said to be

-strongly convex if is convex over . By the definition of strongly convex functions, it is easy to see that if

is a convex function, then for any constant and any constant vector , the function is -strongly convex. Further, it is known that if is a -strongly convex function and is minimized at point , then (see, for example, Corollary 1 in [19]):

(10)

Note that the expression involved in minimization (2) in Algorithm 1 is strongly convex with modulus and is chosen to minimize it. Thus, the next lemma follows.

Lemma 4.

Let be arbitrary. For all , Algorithm 1 guarantees

Rearranging terms and cancelling common terms yields

where (a) follows by the Cauchy-Schwarz inequality (note that the second term on the right side applies the Cauchy-Schwarz inequality twice); and (b) follows from Assumption 1.

Thus, we have

∎

The next corollary follows directly from Lemma 3 and Corollary 1 and shows that constraint violations are ultimately bounded by sequence .

This corollary further justifies why Algorithm 1 intends to minimize drift . Recall that controlled drift can often lead to boundedness of a stochastic process as illustrated in the next section. Thus, the intuition of minimizing drift is to yield small bounds.

This section shows that if we choose and in Algorithm 1, then both expected regret and expected constraint violations are .

III-AA Drift Lemma for Stochastic Processes

Let be a discrete time stochastic process adapted444Random variable is said to be adapted to -algebra if is -measurable. In this case, we often write . Similarly, random process is adapted to filtration if . See e.g. [20]. to a filtration . For example, can be a random walk, a Markov chain or a martingale. Drift analysis is the method of deducing properties, e.g., recurrence, ergodicity, or boundedness, about from its drift . See [21, 22] for more discussions or applications on drift analysis. This paper proposes a new drift analysis lemma for stochastic processes as follows:

Lemma 5.

Let be a discrete time stochastic process adapted to a filtration . Suppose there exists an integer , real constants , , and such that

The above lemma provides both expected and high probability bounds for stochastic processes based on a drift condition. It will be used to establish upper bounds of virtual queues , which further leads to expected and high probability constraint performance bounds of our algorithm. For a given stochastic process , it is possible to show the drift condition (14) holds for multiple with different and . In fact, we will show in Lemma 7 that yielded by Algorithm 1 satisfies (14) for any integer by selecting and according to . One-step drift conditions, corresponding to the special case of Lemma 5, have been previously considered in [22, 23]. However, Lemma 5 (with general ) allows us to choose the best in performance analysis such that sublinear regret and constraint violation bounds are possible.

III-BExpected Constraint Violation Analysis

Define filtration with and being the -algebra generated by random samples up to round . From the update rule in Algorithm 1, we observe that is a deterministic function of and where is further a deterministic function of , and . By inductions, it is easy to show that and for all where denotes the -algebra generated by random variable . For fixed , since is fully determined by and are i.i.d., we know is independent of . This is formally summarized in the next lemma.

Fix and . Since is independent of , which is determined by , it follows that , where (a) follows from the fact that and .

∎

To establish a bound on constraint violations, by Corollary 2, it suffices to derive upper bounds for . In this subsection, we derive upper bounds for by applying the drift lemma (Lemma 5) developed at the beginning of this section. The next lemma shows that random process satisfies the conditions in Lemma 5.

Lemma 7.

Let be an arbitrary integer. At each round in Algorithm 1, the following holds

where , is the number of constraint functions; and are defined in Assumption 1; and is defined in Assumption 2. (Note that by the definition of .)

Lemma 7 allows us to apply Lemma 5 to random process and obtain by taking , and , where represents the smallest integer no less than . By Corollary 2, this further implies the expected constraint violation bound as summarized in the next theorem.

where the expectation is taken with respect to all .

Proof.

Define random process and filtration . Note that is adapted to . By Lemma 7, satisfies the conditions in Lemma 5 with , and . Thus, by part (1) of Lemma 5, for all , we have

where is an absolute constant irrelevant to algorithm parameters. Taking , and , for all , we have

Summing (18) and (19), cancelling common terms and rearranging terms yields

(20)

Note that

(21)

where (a) follows from the Cauchy-Schwartz inequality; and (b) follows from Assumption 1.

Substituting (21) into (20) yields

Summing over yields

where (a) follows by recalling that ; and (b) follows because by Assumption 1, and .

Dividing both sides by yields the desired result.

∎

Note that if we take and , then term (I) in (17) is . Recall that the expectation of term (II) in (17) with is non-positive by Lemma 6. The expected regret bound of Algorithm 1 follows by taking expectations on both sides of (17) and is summarized in the next theorem.

Theorem 2(Expected Regret Bound).

Let be any fixed solution that satisfies , e.g., . If and in Algorithm 1, then for all ,

where the expectation is taken with respect to all .

Taking expectations on both sides and using (15) yields

Taking and yields

∎

III-DSpecial Case Performance Guarantees

Theorems 1 and 2 provide expected performance guarantees of Algorithm 1 for OCO with stochastic constraints. The results further imply the performance guarantees in the following special cases:

•

OCO with long term constraints: In this case, and there is no randomness. Thus, the expectations in Theorems 1 and 2 disappear. For this problem, Algorithm 1 can achieve (deterministic) regret and (deterministic) constraint violations.

•

Stochastic constrained convex optimization: Note that i.i.d. time-varying is a special case of arbitrarily-varying as considered in our OCO setting. Thus, Theorems 1 and 2 still hold when Algorithm 1 is applied to stochastic constrained convex optimization. That is, and . This online performance guarantee also implies Algorithm 1 can be used a (batch) offline algorithm with convergence for stochastic constrained convex optimization. That is, after running Algorithm 1 for slots, if we use as a fixed solution, then and with by the i.i.d. property of each and and Jensen’s inequality. If we use Algorithm 1 as a (batch) offline algorithm, its performance ties with the algorithm developed in [17], which is by design a (batch) offline algorithm and can only solve stochastic optimization with a single constraint function.

•

Deterministic constrained convex optimization: Similarly to OCO with long term constraints, the expectations in Theorems 1 and 2 disappear in this case since and . If we use as the solution, then and , which follows by dividing inequalities in Theorems 1 and 2 by on both sides and applying Jensen’s inequality. Thus, Algorithm 1 solves deterministic constrained convex optimization with convergence.

IV High Probability Performance Analysis

This section shows that if we choose and in Algorithm 1, then for any , with probability at least , regret is and constraint violations are .

IV-AHigh Probability Constraint Violation Analysis

Similarly to the expected constraint violation analysis, we can use part (2) of the new drift lemma (Lemma 5) to obtain a high probability bound of , which together with Corollary 2 leads to a high probability constraint violation bound summarized in Theorem 3.

Theorem 3(High Probability Constraint Violation Bound).

Let be arbitrary. If and in Algorithm 1, then for all and all , we have

Proof.

Define random process . By Lemma 7, satisfies the conditions in Lemma 5 with , and

To obtain a high probability regret bound from Lemma 8, it remains to derive a high probability bound of term (II) in (17) with . The main challenge is that term (II) is a supermartingale with unbounded differences (due to the possibly unbounded virtual queues ). Most concentration inequalities, e.g., the Hoeffding-Azuma inequality, used in high probability performance analysis of online algorithms are restricted to martingales/supermartingales with bounded differences. See for example [24, 25, 10]. The following lemma considers supermartingales with unbounded differences. Its proof uses the truncation method to construct an auxiliary well-behaved supermargingale. Similar proof techniques are previously used in [26, 27] to prove different concentration inequalities for supermartingales/martingales with unbounded differences.

Lemma 9.

Let be a supermartingale adapted to a filtration with and , i.e., . If there exits constant such that , where each is adapted to and . Then, for all , we have

Note that if , then is a supermartingale with differences bounded by and . In this case, Lemma 9 reduces to the conventional Hoeffding-Azuma inequality.

The next theorem summarizes the high probability regret performance of Algorithm 1 and follows from Lemmas 5-9 .

Theorem 4(High Probability Regret Bound).

Let satisfy , e.g., . Let be arbitrary. If and in Algorithm 1, then for all , we have

V Experiment: Online Job Scheduling in Distributed Data Centers

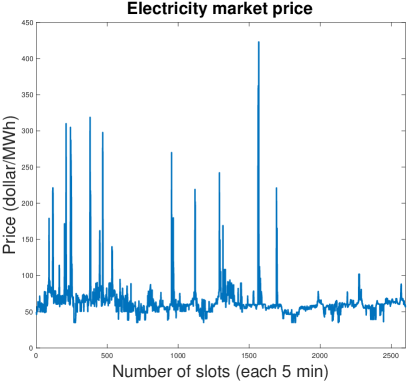

Consider a geo-distributed data center infrastructure consisting of one front-end job router and geographically distributed servers, which are located at different zones to form clusters ( servers in each cluster). See Fig. 1(a) for an illustration. The front-end job router receives job tasks and schedules them to different servers to fulfill the service. To serve the assigned jobs, each server purchases power (within its capacity) from its zone market. Electricity market prices can vary significantly across time and zones. For example, see Fig. 1(b) for a -minute average electricity price trace (between and ) at New York zone CENTRL [28]. This problem is to schedule jobs and control power levels at each server in real time such that all incoming jobs are served and electricity cost is minimized. In our experiment, each server power is adjusted every minutes, which is called a slot. (In practice, server power can not be adjusted too frequently due to hardware restrictions and configuration delay.) Let be the power vector at slot , where each must be chosen from an interval restricted by the hardware, and service rate at each server satisfy , where is an increasing concave function. At each slot , the job router schedules amount of jobs to server . The electricity cost at slot is where is the electricity price at server ’s zone. Use from real-world -minute average electricity price data at different zones in New York city between and obtained from NYISO [28]. At each slot , the incoming job is given by and satisfies a Poisson distribution. Note that the amount of incoming jobs and electricity price are unknown to us at the beginning of each slot but can be observed at the end of each slot. This is an example of OCO with stochastic constraints, where we aim to minimize the electricity cost subject to the constraint that incoming jobs must be served in time. In particular, at each round , we receive loss function and constraint function .

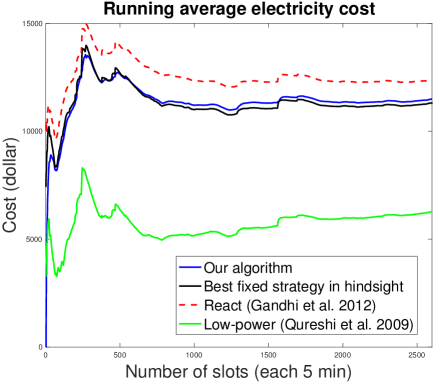

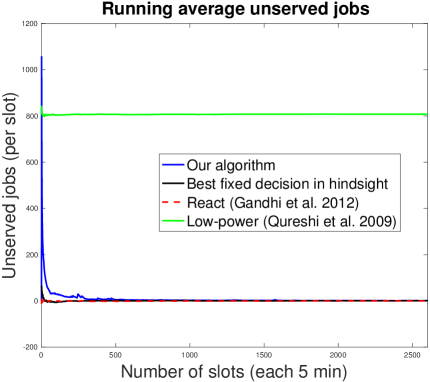

We compare our proposed algorithm with baselines: (1) best fixed decision in hindsight; (2) react [29] and (3) low-power [30]. Both “react” and “low-power” are popular power control strategies used in distributed data centers. See Supplement E for more details of these baselines and our experiment. Fig. 1(c)(d) plot the performance of algorithms, where the running average is the time average up to the current slot. Fig. 1(c) compares electricity cost while Fig. 1(d) compares unserved jobs. (Unserved jobs accumulated if the service rate provided by an algorithm is less than the job arrival rate, i.e., the stochastic constraint is violated.) Fig. 1(c)(d) show that our proposed algorithm performs closely to the best fixed decision in hindsight over time, both in electricity cost and constraint violations. ‘React” performs well in serving job arrivals but yields larger electricity cost, while “low-power” has low electricity cost but fails to serve job arrivals.

(a)

(b)

(c)

(d)

Figure 1: (a) Geo-distributed data center infrastructure; (b) Electricity market prices at zone CENTRAL New York; (c) Running average electricity cost; (d) Running average unserved jobs.

VI Conclusion

This paper studies OCO with stochastic constraints and proposes a novel learning algorithm that guarantees expected regret and constraint violations and high probability regret and constraint violations.

In this proof, we first establish an upper bound of for some constant . Part (1) of this lemma follows by applying Jensen’s inequality since is convex with respect to when . Part (2) of this lemma follows directly from Markov’s inequality.

The following fact is useful in the proof.

Fact 1.

for any .

Proof.

By Taylor’s expansion, we known for any , there exists a point in between and such that . (Note that the value of depends on and if , then ; if , then ; and if , then . ) Since , we have . Thus, for any .

∎

The next lemma provides an upper bound of with constant .

Lemma 10.

where , and where denotes the smallest integer that is no less than .

Proof.

Since , we have . Define . Note that and . Then,

(25)

(26)

where (a) follows from Fact 1 by noting that and ; and (b) follows by substituting into a single of the term .

Next, consider the cases and , separately.

•

Case : Taking conditional expectations on both sides of (26) yields:

where (a) follows from the fact that when ; and (b) follows from the fact that .

•

Case : Taking conditional expectations on both sides of (25) yields:

where (a) follows from the fact that .

Putting two cases together yields:

(27)

where (a) follows by the definition of expectations; (b) follows from the results in the above two cases; (c) follows from the fact that ; and (d) follow from the fact that .

Now, we prove , where denotes the smallest integer that is no less than , by inductions. Since , it follows that , where the last inequality follows because and .

Fix . Assume holds. Note that the base case is just proven above. Consider . By (27), we have

Thus, this lemma follows by inductions.

∎

By this lemma, for all , we have

(28)

where (a) follows from the fact that ; and (b) follows from the facts that and .

Proof of Part (1): Note that is convex with respect to when . By Jensen’s inequality,

To prove this lemma, we first show that . Fix . Note that and is independent of . Further, if , then . Thus, we have

where (a) follows from iterated expectations; (b) follows because is independent of and ; (c) follows by extracting the constant and (d) follows from the assumption that is a Slater point, are i.i.d. across and the fact that .

Now, summing over yields

where (a) follows from the basic fact that when .

∎

The bounded difference of follows directly from the virtual queue update equation (3) and is summarized in the next Lemma.

Lemma 12.

Let be the sequence generated by Algorithm 1. Then,

Proof.

•

Proof of :

Fix and . The virtual queue update equation implies that

where (a) follows from the convexity of .

Note that and recall the fact that if , then for all . Then, we have .

Summing over yields

Thus, where the last inequality follows from Assumption 1.

•

Proof of :

Since , it follows that . (This can be shown by considering and separately.) Thus, we have , which further implies by the triangle inequality of norms.

∎

Now, we are ready to present the main proof of Lemma 7. Note that Lemma 12 gives , which further implies that when . It remains to prove when . Note that .

Fix and consider that . Let and be defined in Assumption 2. Note that since are i.i.d. from the distribution of . Since , by Lemma 4, for all , we have

Adding on both sides and noting that by convexity yields

Rearranging terms yields

(31)

where (a) follows from the Cauchy-Schwarz inequality and (b) follows from Assumption 1.

Intuitively, the second term on the right side in the lemma bounds the probability that for any , while the first term on the right side comes from the conventional Hoeffding-Azuma inequality. However, it is unclear that whether is still a supermartigale conditional on the event that for any .That’s why it is important to have and , which means the boundedness of can be inferred from another random variable that belongs to . The proof of Lemma 9 uses the truncation method to construct an auxiliary supermargingale.

Recall the definition of stoping time given as follows:

Let be a filtration. A discrete random variable is a stoping time (also known as an option time) if for any integer ,

i.e. the event that the stopping time occurs at time is contained in the information up to time .

The next theorem summarizes that a supermartingale truncated at a stoping time is still a supermartingale.

Theorem 5.

(Theorem 5.2.6 in [20]) If random variable is a stopping time and is a supermartingale, then is also a supermartingale, where .

To prove this lemma, we first construct a new supermartingale by truncating the original supermartingale at a carefully chosen stopping time such that the new supermartingale has bounded differences.

Define integer random variable . That is, is the first time when happens. Now, we show that is a stoping time and if we define , then and is a supermartingale with differences bounded by .

1.

To show is a stoping time: Note that . Fix integer , we have

where (a) follows because for all and . It follows that is a stoping time.

2.

To show : Fix . Note that

where (a) follows by noting that if then .

3.

To show is a supermartingale with differences bounded by : Since random variable is proven to be a stoping time, is a supermartingale by Theorem 5. It remains to show . Fix integer . Note that

Now consider and separately.

•

In the case when , it is straightforward that .

•

Consider the case when . By the definition of , we know that , where the last inclusion follows from the fact that . That is, when , we must have for all , which further implies that . Thus, when , .

Combining two cases together proves .

Since is a supermartingale with bounded differences and , by the conventional Hoeffding-Azuma inequality, for any , we have

(32)

Finally, we have

where (a) follows from equation (32) and the second bullet in the above; and (b) follows from the union bound and the hypothesis that .

Define . Recall . The next lemma shows that satisfies Lemma 9 with and .

Lemma 13.

Let be any fixed solution that satisfies , e.g., . Under Algorithm 1, if we define and , then is a supermartingale adapted to filtration such that where is a random variable adapted to .

Proof.

It is easy to say is adapted . It remains to show is a supermartingale. Note that and

where (a) follows from the fact that , and is independent of ; and (b) follows from which further follows from are i.i.d. samples. Thus, is a supermartingale.

We further note that

where (a) follows from the Cauchy-Schwarz inequality and the assumption that .

This implies that if , then . Thus, . Since is adapted to , it follows that is a random variable adapted to .

∎

By Lemma 13, satisfies Lemma 9. Fix , Lemma 9 implies that

(33)

Fix . In the following, we shall choose and such that both term (I) and term (II) in (33) are no larger than .

Recall that by Lemma 7, random process satisfies the conditions in Lemma 5. To guarantee term (II) is no lareger than , it suffices to choose such that

By part (2) of Lemma 5 (with ), the above inequality holds if we choose where

is an absolute constant irrelevant the algorithm parameters and is an arbitrary integer.

Once is chosen, we further need to choose such that term (I) in (33) is . It follows that if , then

In the experiment, we assume the job arrivals are Poisson distributed with mean jobs/slot. For simplicity, assume each server is restricted to choose power at each round and the service rate satisfies . (Note that our algorithm can easily deal with general concave functions and each server in general can have different functions.) The simulation duration is slots (corresponding to days).

The three baselines are further elaborated as below:

•

Best fixed decision in hindsight: Assume all the electricity price traces and the job arrival distribution are known beforehand. The decision maker chooses a fixed power decision vector that is optimal based on data in slots.

•

React algorithm: This algorithm is developed in [29]. The algorithm reacts to the current traffic and splits the load evenly among each server to support the arrivals. Since instantaneous job arrivals is unknown at the current slot, we use the average of job arrivals over the most recent slots as an estimate. Since this algorithm is designed to meet the time varying job arrivals but is unaware of electricity variations, its electricity cost is high as observed in our simulation results.

•

Low-power algorithm: This algorithm is adapted from [30] and always schedule jobs to servers in the zones with the lowest electricity price. Since instantaneous electricity prices are unknown at the current slot, we use the average of electricity prices over the most recent slots at each server as an estimate. Recall that each server has a finite service capacity (), this algorithm is not guaranteed serve all job arrivals. Thus, the number of unserved jobs can eventually pile up.

References

[1]

N. Cesa-Bianchi, P. M. Long, and M. K. Warmuth, “Worst-case quadratic loss

bounds for prediction using linear functions and gradient descent,”

IEEE Transactions on Neural Networks, vol. 7, no. 3, pp. 604–619,

1996.

[2]

J. Kivinen and M. K. Warmuth, “Exponentiated gradient versus gradient descent

for linear predictors,” Information and Computation, vol. 132, no. 1,

pp. 1–63, 1997.

[3]

G. J. Gordon, “Regret bounds for prediction problems,” in Proceeding of

Conference on Learning Theory (COLT), 1999.

[4]

M. Zinkevich, “Online convex programming and generalized infinitesimal

gradient ascent,” in Proceedings of International Conference on

Machine Learning (ICML), 2003.

[5]

S. Shalev-Shwartz, “Online learning and online convex optimization,”

Foundations and Trends in Machine Learning, vol. 4, no. 2, pp.

107–194, 2011.

[6]

E. Hazan, “Introduction to online convex optimization,” Foundations and

Trends in Optimization, vol. 2, no. 3–4, pp. 157–325, 2016.

[7]

E. Hazan, A. Agarwal, and S. Kale, “Logarithmic regret algorithms for online

convex optimization,” Machine Learning, vol. 69, pp. 169–192, 2007.

[8]

S. Mannor, J. N. Tsitsiklis, and J. Y. Yu, “Online learning with sample path

constraints,” Journal of Machine Learning Research, vol. 10, pp.

569–590, March 2009.

[9]

D. Tse and P. Viswanath, Fundamentals of Wireless Communication. Cambridge University Press, 2005.

[10]

M. Mahdavi, R. Jin, and T. Yang, “Trading regret for efficiency: online convex

optimization with long term constraints,” Journal of Machine Learning

Research, vol. 13, no. 1, pp. 2503–2528, 2012.

[11]

A. Cotter, M. Gupta, and J. Pfeifer, “A light touch for heavily constrained

sgd,” in Proceedings of Conference on Learning Theory (COLT), 2015.

[12]

R. Jenatton, J. Huang, and C. Archambeau, “Adaptive algorithms for online

convex optimization with long-term constraints,” in Proceedings of

International Conference on Machine Learning (ICML), 2016.

[13]

M. Mahdavi, T. Yang, and R. Jin, “Stochastic convex optimization with multiple

objectives,” in Advances in Neural Information Processing Systems

(NIPS), 2013.

[14]

Y. Nesterov, Introductory Lectures on Convex Optimization: A Basic

Course. Springer Science & Business

Media, 2004.

[15]

H. Yu and M. J. Neely, “A low complexity algorithm with regret

and finite constraint violations for online convex optimization with long

term constraints,” arXiv:1604.02218, 2016.

[16]

M. J. Neely and H. Yu, “Online convex optimization with time-varying

constraints,” arXiv::1702.04783, 2017.

[17]

G. Lan and Z. Zhou, “Algorithms for stochastic optimization with expectation

constraints,” arXiv:1604.03887, 2016.

[18]

A. Nedić and A. Ozdaglar, “Subgradient methods for saddle-point

problems,” Journal of Optimization Theory and Applications, vol. 142,

no. 1, pp. 205–228, 2009.

[19]

H. Yu and M. J. Neely, “A simple parallel algorithm with an

convergence rate for general convex programs,” SIAM Journal on

Optimization, vol. 27, no. 2, pp. 759–783, 2017.

[20]

R. Durrett, Probability: Theory and Examples. Cambridge University Press, 2010.

[21]

J. L. Doob, Stochastic processes. Wiley New York, 1953.

[22]

B. Hajek, “Hitting-time and occupation-time bounds implied by drift analysis

with applications,” Advances in Applied Probability, vol. 14, no. 3,

pp. 502–525, 1982.

[23]

M. J. Neely, “Energy-aware wireless scheduling with near optimal backlog and

convergence time tradeoffs,” in Proceedings of IEEE International

Conference on Computer Communications (INFOCOM), 2015.

[24]

N. Cesa-Bianchi and G. Lugosi, Prediction, Learning, and Games. Cambridge University Press, 2006.

[25]

P. L. Bartlett, V. Dani, T. Hayes, S. Kakade, A. Rakhlin, and A. Tewari,

“High-probability regret bounds for bandit online linear optimization,” in

Proceedings of Conference on Learning Theory (COLT), 2008.

[26]

V. Vu, “Concentration of non-lipschitz functions and applications,”

Random Structures & Algorithms, vol. 20, no. 3, pp. 262–316, 2002.

[27]

T. Tao and V. Vu, “Random matrices: universality of local spectral statistics

of non-hermitian matrices,” The Annals of Probability, vol. 43,

no. 2, pp. 782–874, 2015.

[28]

“New York ISO open access pricing data. http://www.nyiso.com/.”

[29]

A. Gandhi, M. Harchol-Balter, and M. A. Kozuch, “Are sleep states effective in

data centers?” in International Green Computing Conference (IGCC),

2012.

[30]

A. Qureshi, R. Weber, H. Balakrishnan, J. Guttag, and B. Maggs, “Cutting the

electric bill for internet-scale systems,” in ACM SIGCOMM, 2009.