Wavelet eigenvalue regression for -variate operator fractional Brownian motion ††thanks: The first author was partially supported by grant ANR-16-CE33-0020 MultiFracs. The second author was partially supported by the prime award no. W911NF-14-1-0475 from the Biomathematics subdivision of the Army Research Office, USA. The second author’s long term visits to ENS de Lyon were supported by the school. The authors would like to thank Mark M. Meerschaert for his comments on this work. The second author would also like to thank Tewodros Amdeberhan for the enlightening mathematical discussions. ††thanks: AMS Subject classification. Primary: 62M10, 60G18, 42C40. ††thanks: Keywords and phrases: operator fractional Brownian motion, operator self-similarity, wavelets, eigenvalues.

Abstract

In this contribution, we extend the methodology proposed in Abry and Didier (?) to obtain the first joint estimator of the real parts of the Hurst eigenvalues of -variate OFBM. The procedure consists of a wavelet regression on the log-eigenvalues of the sample wavelet spectrum. The estimator is shown to be consistent for any time reversible OFBM and, under stronger assumptions, also asymptotically normal starting from either continuous or discrete time measurements. Simulation studies establish the finite sample effectiveness of the methodology and illustrate its benefits compared to univariate-like (entrywise) analysis. As an application, we revisit the well-known self-similar character of Internet traffic by applying the proposed methodology to 4-variate time series of modern, high quality Internet traffic data. The analysis reveals the presence of a rich multivariate self-similarity structure.

1 Introduction

An operator fractional Brownian motion (OFBM) is a -valued Gaussian stochastic process with stationary increments that satisfies the operator self-similarity relation

| (1.1) |

where stands for the equality of finite-dimensional distributions. In relation (1.1), which generalizes the univariate concept of self-similarity, is a matrix called the Hurst matrix, and , where is the usual matrix exponential. If the Jordan form

| (1.2) |

is diagonalizable with real (Hurst) eigenvalues for a nonsingular , then the eigenvectors form a coordinate system in which the -th marginal of , , is a fractional Brownian motion (FBM) with Hurst scaling index (namely, a Gaussian, self-similar, stationary increment stochastic process – see Embrechts and Maejima (?), Taqqu (?)). These coordinate processes need not be independent. It is generally assumed that OFBM is stochastically continuous, i.e., whenever , and proper, namely, its variance matrix has full rank for .

OFBM is a multivariate fractional process. Univariate fractional processes have been used with great success in the modeling of data sets from many fields of science, technology and engineering (e.g., Mandelbrot (?), Taqqu et al. (?), Ivanov et al. (?), Ciuciu et al. (?), Foufoula-Georgiou and Kumar (?)). The literature on the probability theory and statistical methodology for univariate fractional processes is now voluminous (e.g., Mandelbrot and Van Ness (?), Taqqu (?, ?), Dobrushin and Major (?), Granger and Joyeux (?), Hosking (?), Fox and Taqqu (?), Dahlhaus (?), Beran (?), Robinson (?, ?), Abry et al. (?), Stoev et al. (?), Moulines et al. (?, ?, ?), Beran et al. (?), Bardet and Tudor (?), Clausel et al. (?), Pipiras and Taqqu (?), to cite a few).

In modern applications, however, data sets are often multivariate, since several natural and artificial systems are monitored by a large number of sensors. Accordingly, the literature on multivariate fractional processes has been expanding at a fast pace. The contributions include Hosoya (?, ?), Lobato (?), Marinucci and Robinson (?), Becker-Kern and Pap (?), Robinson (?), Hualde and Robinson (?), Sela and Hurvich (?), Kristoufek (?, ?) and Kechagias and Pipiras (?, ?), in the time and Fourier domains, and Wendt et al. (?), Amblard et al. (?), Coeurjolly et al. (?), Achard and Gannaz (?), Frecon et al. (?), in the wavelet domain (see also Marinucci and Robinson (?), Robinson and Yajima (?), Hualde and Robinson (?), Nielsen and Frederiksen (?), Shimotsu (?) on the related fractional cointegration literature in econometrics).

The framework of operator self-similar (o.s.s.) random processes and fields was originally conceived by Laha and Rohatgi (?), Hudson and Mason (?), and has attracted much attention recently (e.g., Maejima and Mason (?), Mason and Xiao (?), Biermé et al. (?), Xiao (?), Guo et al. (?), Didier and Pipiras (?, ?), Clausel and Vedel (?, ?), Li and Xiao (?), Dogan et al. (?), Puplinskaitė and Surgailis (?), Didier et al. (?, ?)). If and in (1.1), then the latter relation breaks down into simultaneous entrywise expressions

| (1.3) |

Relation (1.3) is henceforth called entrywise scaling. Several estimators have been developed by building upon the univariate-like, entrywise scaling laws, e.g., the Fourier-based multivariate local Whittle (e.g., Shimotsu (?), Nielsen (?)) and the multivariate wavelet regression (Wendt et al. (?), Amblard and Coeurjolly (?)). However, if is non-diagonal, then the matrix mixes together the several entries of . In this case, the univariate-like statistical analysis of each entry of will often generate estimates that are undetermined convex combinations of Hurst eigenvalues or, at large scales, estimates of the largest Hurst eigenvalue (see, for instance, Chan and Tsai (?), Didier et al. (?), Tsai et al. (?), Abry et al. (?)).

In Abry and Didier (?), the use of the eigenstructure of wavelet variance matrices is proposed for the estimation of the Hurst parameters of OFBM. The main results are obtained in the bivariate context, in which it is shown that wavelet log-eigenvalues – and also wavelet eigenvectors, under assumptions – are consistent and asymptotically normal estimators of the eigenstructure of the Hurst matrix .

In this paper, we extend this approach by proposing a wavelet eigenvalue regression estimator of the Hurst eigenvalues of -variate OFBM. The estimator is shown to be consistent for the real parts of the eigenvalues of for (essentially) any time reversible OFBM. Under the stronger assumption that Hurst eigenvalues are real and simple (pairwise distinct), we further show that the wavelet eigenvalue regression estimator is asymptotically normal. Establishing the latter properties involves showing that the wavelet log-eigenvalues themselves are a consistent and asymptotically normal estimator of (the real parts of) the eigenvalues of the Hurst matrix. Under the additional assumption that the matrix of Hurst eigenvectors (mixing matrix) in (1.2) is orthogonal, a consistent sequence of wavelet eigenvectors is also shown to exist. With a view toward hypothesis testing, we also investigate conditions for asymptotic normality when all Hurst eigenvalues are equal. The mathematical framework is much more general than that in Abry and Didier (?), which builds upon closed form expressions for eigenvalues and eigenvectors in dimension 2.

In the context of scaling properties, the use of eigenanalysis was first proposed in Meerschaert and Scheffler (?, ?) for operator stable laws, and later in Becker-Kern and Pap (?) for o.s.s. processes in the time domain. It has also been used in the cointegration literature (e.g., Phillips and Ouliaris (?), Harris and Poskitt (?), Li et al. (?), Zhang et al. (?)). The wavelet framework has the benefit of computational efficiency (Daubechies (?), Mallat (?)), which is especially important in a multivariate setting (see Abry et al. (?), Section 5.2, for a computational comparison between maximum likelihood and a wavelet-based estimation methodology). In addition, for a large enough number of vanishing moments , wavelet coefficients are stationary in the shift parameter at every octave , and the sample wavelet variance matrix is asymptotically normal at a fixed octave . These properties are in part a consequence of the quasi-decorrelation property of the wavelet transform (Flandrin (?), Wornell and Oppenheim (?), Masry (?), Bardet and Tudor (?), Clausel et al. (?)). To the best of our knowledge, we are proposing the first eigenanalysis-based asymptotically normal estimator of Hurst eigenvalues in general dimension , under assumptions. The most general case of multiple blocks of Hurst eigenvalues with algebraic multiplicity greater than 1 (see Section 2 on terminology) calls for special efforts and remains a topic for future research, since asymptotic distributions may be normal or nonnormal (see Remark 3.2 on the difficulties involved).

We conducted broad Monte Carlo experiments which illustrate the appropriate use of the estimator and demonstrate its finite sample size effectiveness. In addition, we apply the proposed methodology in the modeling of 4-variate Internet traffic time series from the so-named MAWI archive. The latter comprises Internet traffic traces captured on a high-speed, high-capacity backbone that mostly connects academic institutions in Japan and the USA. Our study reveals, for the first time, the presence of multivariate scaling properties in Internet traffic.

This paper is organized as follows. Section 2 contains the notation, theoretical background, assumptions and definitions. The main mathematical results can be found in Section 3, namely, the consistency and asymptotic normality of wavelet log-eigenvalues for Hurst eigenvalues, as well as the corresponding results for the wavelet eigenvalue regression estimator. In Section 4, we extend the results from Section 3 to the more realistic context where measurements are made in discrete time. Section 5 contains Monte Carlo studies. Section 6 contains the wavelet eigenvalue analysis of Internet traffic data. All proofs can be found in the Appendix, together with auxiliary results.

2 Preliminaries

2.1 Notation and background

Hereinafter, , , , , and denote, respectively, the space of symmetric matrices and the cones of symmetric positive semidefinite, symmetric positive definite, Hermitian positive semidefinite and Hermitian positive definite matrices, and the space of matrices. The real and complex spheres are represented by and , respectively. For , denotes a Jordan block of size (see (LABEL:e:Jordan_block) for an explicit expression). For a matrix , recall that the multiplicity of an eigenvalue is its multiplicity as a zero of the characteristic polynomial of . An eigenvalue is called simple when its algebraic multiplicity is 1 (Horn and Johnson (?), p. 76). The operator vectorizes the upper triangular entries of a symmetric matrix .

Let be an OFBM with Hurst matrix . Following the results in Didier and Pipiras (?), if the eigenvalues of satisfy

| (2.1) |

then the OFBM admits the harmonizable representation

| (2.2) |

where denotes the equality of finite dimensional distributions, , and is a -valued, Gaussian random measure satisfying the constraints , . Conversely, if

| (2.3) |

then the process defined by the expression on the right-hand side of (2.2) is proper; hence, it defines an OFBM . If

| (2.4) |

then the OFBM is time reversible, i.e., .

2.2 Assumptions and definitions

Throughout the paper, we assume that the underlying stochastic process is a -valued OFBM under the following conditions.

Assumption (OFBM1): condition (2.3) holds.

Assumption (OFBM2): condition (2.4) holds.

In Sections 3 and 4, we will make use of assumptions (OFBM 1–2) combined with one of the following two assumptions.

The first one, called (OFBM3), is the more general and will be applied in consistency statements. In fact, it simply recasts (2.1) based on Jordan blocks.

Assumption (OFBM3):

where each is a Jordan block of length ,

| (2.5) |

and denotes a column vector of .

The second one, named (OFBM3′), is more stringent and will be used in (most) asymptotic normality statements (n.b.: the latter should not to be confused with Theorem 2.1, which holds under great generality for fixed scales).

Assumption (OFBM3′):

| (2.6) |

In particular, condition (2.6) implies that every eigenvalue of the Hurst matrix is real and simple.

Throughout the paper, we will make the following assumptions on the underlying wavelet basis. For this reason, such assumptions will be omitted in statements.

Assumption : is a wavelet function, namely,

| (2.7) |

Assumption :

| (2.8) |

Assumption : there is such that

| (2.9) |

Under (2.7), (2.8) and (2.9), is continuous, is everywhere differentiable and its first derivatives are zero at (see Mallat (?), Theorem 6.1 and the proof of Theorem 7.4).

Example 2.1

If is a Daubechies wavelet with vanishing moments, (see Mallat (?), Proposition 7.4).

Next, we define the wavelet transform and sample wavelet variance (spectrum) of OFBM.

Definition 2.1

Let be an OFBM satisfying the assumptions (OFBM 1–3). Its (normalized) wavelet transform at octave and shift is given by

| (2.10) |

For a (wavelet) sample size , the sample wavelet variance is defined by the random matrix

| (2.11) |

The following theorem shows that is asymptotically normal (see Section 2 on the definition of the operator ).

Theorem 2.1

(Abry and Didier (?), Theorem 3.1) Let be an OFBM under the assumptions (OFBM1–3) and consider

| (2.12) |

Let be the asymptotic covariance matrix described in Proposition 3.3 in Abry and Didier (?). Then,

| (2.13) |

as .

When with real eigenvalues and a scalar matrix – i.e., it has the form for some constant –, the sample wavelet variance satisfies the so-named entrywise scaling relation

(c.f. Introduction). In this case, the (Hurst) eigenvalues can be estimated by means of an entrywise log-regression procedure (Amblard and Coeurjolly (?), Coeurjolly et al. (?)). However, for a general matrix , entrywise analysis is highly biased, since there is no simple relation between Hurst eigenvalues and the entrywise behavior of the wavelet variance matrix.

Likewise, wavelet eigenvalues do not satisfy a simple scaling relation based on Hurst eigenvalues. However, as it turns out, an approximate scaling relation appears in the coarse scale limit. So, rewrite the sample wavelet variance at scale as

| (2.14) |

The dyadic, slow-growth scaling factor in (2.14) satisfies the relation

| (2.15) |

where is the regularity parameter

Then, by the operator self-similarity property (see Abry and Didier (?), Proposition 3.1),

| (2.16) |

where

| (2.17) |

In particular, if is diagonalizable, the latter matrices satisfy entrywise scaling relations

| (2.18) |

We are now in a position to define the wavelet eigenstructure estimator of the real parts of the Hurst eigenvalues (2.1) by means of a weighted regression procedure on wavelet log-eigenvalues.

Definition 2.2

Let be an OFBM satisfying the assumptions (OFBM 1–3), and let be its sample wavelet variance matrices corresponding to scales . The wavelet eigenstructure estimator of the Hurst eigenvalues is given by the regression system

| (2.19) |

In (2.19), , , are weights satisfying the relations

| (2.20) |

Since a.s., then expression (2.19) is well-defined a.s. If, in addition, for some , we will simply write instead of .

3 Asymptotic theory: continuous time

In this section, assuming measurements in continuous time, we establish the asymptotic properties of wavelet log-eigenvalues, as well as the corresponding results for the wavelet eigenvalue regression estimator described in Definition 2.2.

In Theorem 3.1, ordered wavelet log-eigenvalues are shown to be consistent for their respective (real parts of) Hurst eigenvalues for any time reversible OFBM. Consistency appears as a consequence of the operator self-similarity property (2.16) of wavelet variance matrices by applying the Courant-Fischer principle (see (A.1)).

Theorem 3.1

Let be an OFBM under the assumptions (OFBM 1–2). Fix . If, in addition, satisfies (OFBM3), then

| (3.1) |

as , where is such that

| (3.2) |

In particular, if , then

| (3.3) |

Theorem 3.2, which requires the stronger assumption (OFBM3′), establishes the asymptotic normality of wavelet log-eigenvalues. Proving it requires establishing Proposition 3.1 first, which contains some properties of interest of wavelet variance matrices. For sample wavelet variance matrices, these properties can be summed up as follows. First, the ratio between the -th wavelet eigenvalue and the power law converges to a limiting function that satisfies a scaling relation. Second, for each eigenvalue , , there is a convergent sequence of associated eigenvectors . Therefore, we can assume that the eigenvectors converge (in probability) in the space (see (2.5) on the definition of the vectors ). In particular, .

Proposition 3.1

Let be an OFBM under the assumptions (OFBM 1,2,3′). Let be the sample wavelet variance matrix (2.14). Fix and an octave . Then, as ,

-

there is a function such that

(3.4) -

for some sequence of unit eigenvectors associated with the -th eigenvalue of , there is a unit vector such that

(3.6) where

(3.7) In particular,

-

the sequence satisfies

(3.8) for some limiting vector function (see (LABEL:e:x*_sol_determ)).

All claims above hold with the matrix as in (2.14) replacing , and with deterministic convergence in expressions (3.4), (3.6) and (3.8).

Corollary 3.1

Remark 3.1

Example 3.1

We are now in a position to prove the asymptotic normality of wavelet log-eigenvalues. Apart from Proposition 3.1, the latter is mainly a consequence of the operator self-similarity property (2.16), Theorem 2.1, and the fact that all eigenvalues of become simple for large enough by virtue of condition (2.6).

Theorem 3.2

Let be an OFBM under the assumptions (OFBM 1–2). Consider the range of octaves (2.12). If, in addition, satisfies (OFBM3′), then

| (3.9) |

as . If we write the asymptotic covariance matrix in block form , then its main diagonal entries satisfy , .

The asymptotic properties of the wavelet eigenvalue regression estimator (2.19) are a consequence of those of wavelet log-eigenvalues, as established in Theorems 3.1 and 3.2.

Corollary 3.2

Let be an OFBM under the assumptions (OFBM 1–2) and consider the estimator described in Definition 2.2.

As discussed before the statement of Theorem 3.2, assumption (2.6) of simple Hurst eigenvalues plays an important role in (3.9) and (3.11). Proposition 3.2, stated next, provides a basic framework for testing the hypothesis that there is a single Hurst eigenvalue with multiplicity . To establish it, we make the following assumption.

Assumption (OFBM3′′):

| (3.12) |

and

| (3.13) |

Proposition 3.2

Remark 3.2

A convergent sequence of wavelet eigenvectors (see Proposition 3.1) is required in the proof of Theorem 3.2. However, the existence of such a sequence is in general not guaranteed. For instance, without (3.13), eigenvectors do not necessarily converge under (3.12). Under the latter condition, the asymptotic distribution of

| (3.14) |

depends on whether or not has simple eigenvalues. In particular, (3.14) may not be asymptotically normal (c.f. Abry et al. (?), Proposition F.1). Tackling the most general case of multiple blocks of Hurst eigenvalues with algebraic multiplicity greater than 1 requires addressing all these issues.

4 Asymptotic theory: discrete time

In this section, instead of a continuous time OFBM path , we assume that only a discrete OFBM sample

| (4.1) |

is available. Starting from the so-called discretized wavelet coefficients (as defined in (4.2) below), we develop the asymptotic properties of wavelet log-eigenvalues, as well as of the redefined wavelet eigenvalue regression estimator.

We suppose the wavelet approximation coefficients stem from Mallat’s pyramidal algorithm, under a multiresolution analysis of (MRA; see Mallat (?), chapter 7, and Stoev et al. (?), Proposition 2.4 and Theorem 3.2). Accordingly, we need to replace () with the following more restrictive condition.

Assumption ():

| the functions (a bounded scaling function) and correspond to a MRA of , | ||

| and and are compact intervals. |

Throughout this section, we assume that (), () and () hold. Given (4.1), we initialize the algorithm with the vector-valued sequence

also called the approximation coefficients at scale . At coarser scales , Mallat’s algorithm is characterized by the iterative procedure

where the filter sequences , are called low- and high-pass MRA filters, respectively. Due to (), only a finite number of filter terms is nonzero, which is convenient for computational purposes (see Daubechies (?), chapter 6).

Definition 4.1

The normalized discretized wavelet coefficients are defined by

| (4.2) |

Let , and let be the discretized wavelet coefficient (4.2) at scale and shift . We define the associated sample wavelet variance by

Likewise, the discrete time wavelet eigenvalue regression estimator is defined by the relation

| (4.3) |

where the weights , , satisfy (2.20).

The following theorem contains the discrete time version of the main results in Section 3.

Theorem 4.1

Let be an OFBM under the assumptions (OFBM 1–2) and the condition

| (4.4) |

on its Hurst eigenvalues. Consider the estimator described in Definition 4.1 and the following three different settings.

- ()

- ()

Remark 4.1

5 Monte Carlo studies

Numerical experiment setting. To study the performance of the estimator (2.19), broad Monte Carlo experiments were conducted for sample sizes in the range , with 1,000 independent OFBM sample paths for each of the latter. The synthesis of OFBM was performed using the multivariate toolbox devised in Helgason et al. (?, ?) and available at www.hermir.org. We opted for showing results in dimension as representative of the general multivariate situation , while keeping the number of plots reasonable. Results are reported for a single representative instance of OFBM with Hurst eigenvalues

| (5.1) |

and Hurst eigenvector matrix

| (5.2) |

since similar conclusions can be drawn from several other instances.

The analysis was conducted using orthogonal least asymmetric Daubechies wavelets, with vanishing moments. It has been checked that varying or using other regular enough wavelets yields qualitatively identical conclusions. The log-linear regressions (2.19) were performed across scales using weights

which satisfy (2.20). The scalars can be freely chosen and reflect the degree of confidence in each term . Following Abry et al. (?), we picked . We compare the estimation performance to that of the univariate-like analysis of each component separately, i.e., of the log-linear regressions

based on the main diagonal entries of (see, for instance, Veitch and Abry (?) and Ciuciu et al. (?)).

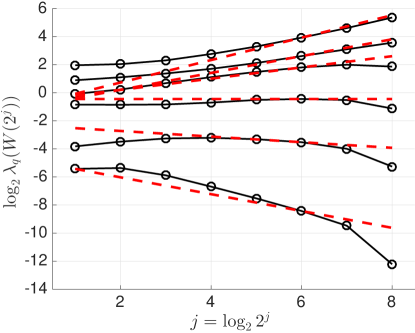

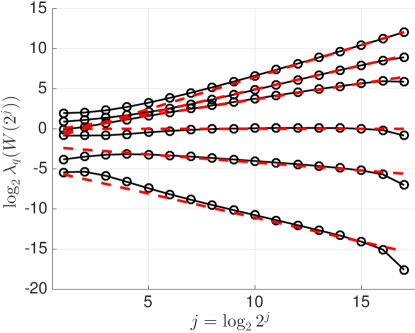

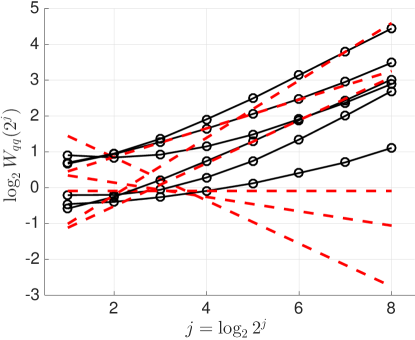

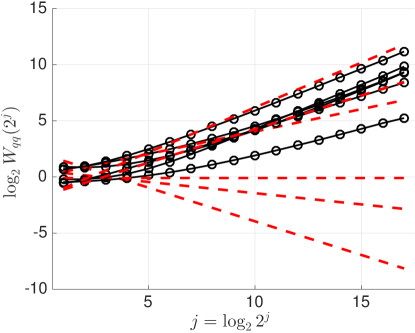

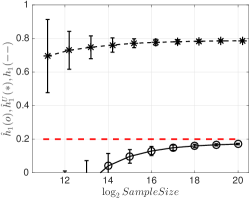

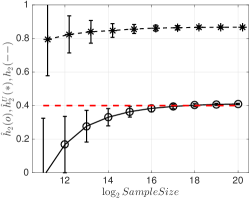

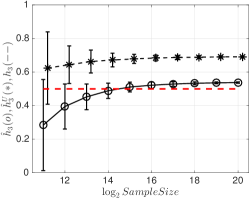

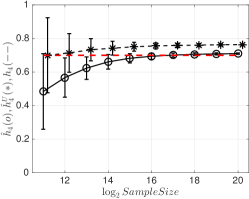

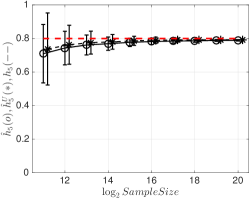

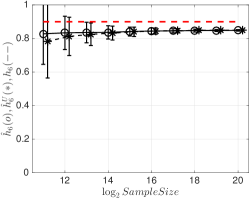

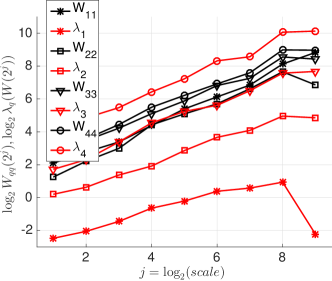

Estimation principle. To illustrate the estimation procedure, for each and for the smallest and largest sample sizes, Figure 1 compares the multivariate and univariate-like wavelet analysis functions (top plots) and , respectively. The symbol denotes the Monte Carlo average, used as a numeric surrogate for the ensemble average .

Figure 1 clearly shows that, for each , the Monte Carlo averaged univariate-like analysis functions fail to reproduce the theoretical asymptotic behavior (dashed red lines) and essentially follow the dominant asymptotic behavior . This leads to the incorrect conclusion that the 6 components have the same Hurst eigenvalue . By contrast, Figure 1 shows that the Monte Carlo averaged multivariate analysis functions , , closely follow the theoretical asymptotic behavior . This provides evidence of the existence of different Hurst eigenvalues in the multivariate data.

Interestingly, the agreement of observed and theoretical scaling remains very satisfactory even for small sample sizes (in this case, !).

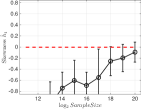

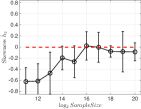

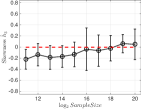

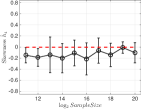

Bias and standard deviation. To further assess the estimation performance, in Figure 2 biases for and , , are compared as functions of (the of) the sample size. The results confirm that the univariate-like estimates (dashed black lines with ) are strongly biased, barely departing from the largest Hurst eigenvalue . In other words, under an OFBM model, univariate-like data analysis leads practitioners to incorrectly conclude that all components have the same Hurst eigenvalue, i.e., , .

Moreover, biases for the wavelet eigenstructure estimators decrease with sample size for all , as predicted by Theorem 3.2. Unsurprisingly, the simulations further show that the accurate estimation of the smaller Hurst eigenvalues is more demanding in terms of data by comparison to larger Hurst eigenvalues. While the estimation of shows negligible bias for a sample size as small as , equally accurate estimation of requires .

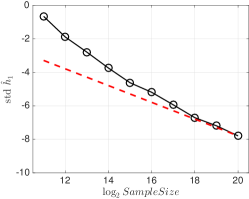

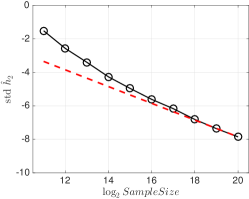

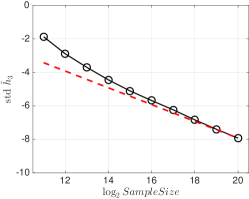

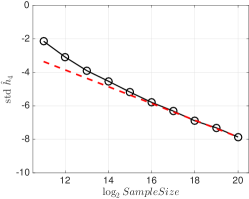

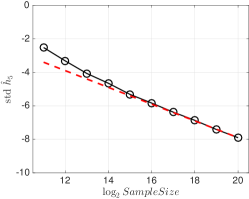

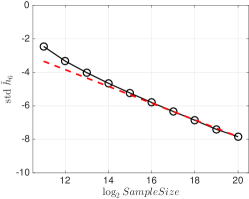

Figure 3 further shows that Monte Carlo standard deviations for decay as . Interestingly, the amplitude of standard deviations depends neither on each individual value nor, globally, on the ensemble of parameters (5.1). These results constitute two very remarkable features of the proposed estimation procedure, which is strongly reminiscent of what was observed in univariate estimation for FBM (see Veitch and Abry (?)).

In addition, Monte Carlo experiments not reported indicate that, surprisingly, biases and standard deviations neither depend (significantly) on the off-diagonal entries of the instantaneous covariance (i.e., on correlations among pre-mixed components), nor on the choice of the Hurst eigenvector matrix . This is another striking feature of the performance of the estimators (2.19).

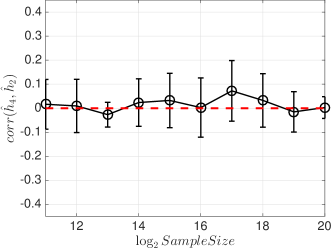

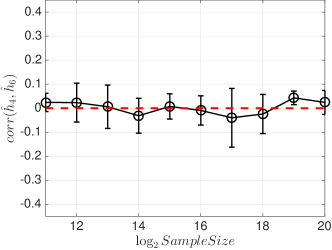

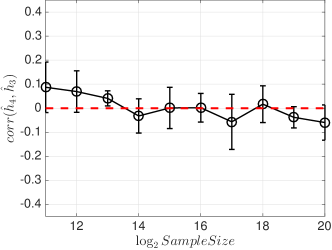

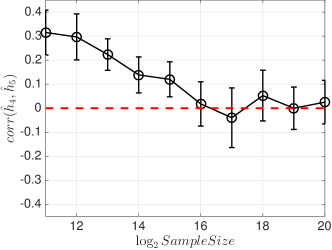

Covariance amongst estimates . Figure 4 indicates that, asymptotically, the covariances of and , , tend to .

Monte Carlo experiments also consistently showed that is generally correlated with and (Figure 4, bottom plots), with decreasing covariances, while the covariances between and with are remarkably close to even for small sample sizes (e.g., Figure 4, top plots). These are important facts to be accounted for in practice.

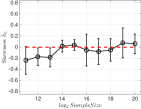

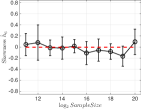

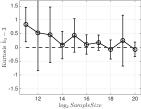

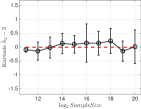

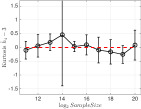

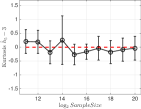

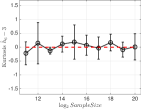

Asymptotic normality of . Figure 5 displays the skewness and (excess) kurtosis of the finite sample distribution of the Hurst eigenvalue estimators . Both measures decrease as the sample size increases. Moreover, the plots provide a measure of the sample sizes needed for an accurate Gaussian approximation to the distribution of each estimator . In particular, Figure 5 indicates that normality is reached much faster (i.e., for much smaller sample sizes) for the larger Hurst eigenvalue than for the smaller ones.

Scaling range selection for estimation. In our Monte Carlo studies, the log-regression octave range () was set a priori. The choice of octaves involved in the estimation of Hurst eigenvalues is a way of balancing the bias-variance trade-off. On one hand, a large leads to a small bias. However, given the small number of sum terms in the sample wavelet variances (2.11), it also results in a large estimation variance. On the other hand, a small reduces the variance at the price of increased bias. Monte Carlo studies not reported show that small values of lead to an overall better performance in terms of mean squared error, hence the choice in the experiments reported above. The choice of optimal scaling ranges (which may depend on the rank of the Hurst eigenvalue) is a topic for future investigation.

6 Internet traffic modeling

The statistical modeling of Internet traffic is a central task in traffic engineering for the purposes of network design, management, control, security and pricing. Nevertheless, the data has always been modeled as a collection of univariate time series. In this section, we carry out the first study of multivariate self-similarity in Internet traffic data. We use OFBM as a baseline model for (second order) multivariate scaling properties, in the same way that FBM has been applied in the univariate context.

Empirical computer network traffic analysis started in the 1990s and hence can be considered a relatively new scientific field. Yet, the striking properties of Internet traffic data were revealed from the beginning. Standard models of traffic include a Poisson process with independent inter-arrival times or short range (exponentially decaying) autocorrelation structures. Instead, collected data was found to be characterized by significant burstiness (strong irregularity over time) as well as slow, power law correlation decay (see Leland et al. (?), Paxson and Floyd (?), Erramilli et al. (?), Willinger et al. (?), Abry and Veitch (?), Park and Willinger (?), Erramilli et al. (?)). It was soon recognized that the latter phenomenon, referred to as asymptotic self-similarity or long range dependence (LRD; Beran (?)), had strong implications for network management due to its dramatic impact on queuing performance (see Norros (?), Boxma and Dumas (?), Boxma and Cohen (?)). This lead to substantial research efforts in the last 20 years (see Willinger et al. (?), Willinger et al. (?) and Fontugne et al. (?) for reviews and references therein for details).

Self-similarity in Internet traffic has been widely investigated, but it remains controversial and a number of issues are still open. The data is often modeled in terms of aggregate time series. The latter consist of either IP (Internet Protocol) packet or byte counts on a given link, at a given time resolution . It has long been debated whether self-similarity is rather a property of the packet or byte count time series. Another question is whether traffic should be analyzed globally, with traffic traveling in both directions of the link, or if it should be split into directional traffic. In Dewaele et al. (?) and Borgnat et al. (?), these issues are analyzed and commented on in light of self-similarity. In this section, we consider a 4-variate setting, obtained as byte and packet counts, for each direction of the link.

The MAWI archive (Cho et al. (?)) is an ongoing collection of Internet traffic traces, captured on a high-speed, high-capacity backbone that mostly connects Japanese academic institutions to the USA. Anonymized traces are made publicly available at http://mawi.wide.ad.jp/mawi/ and http://mawi.wide.ad.jp/, and several of them were kindly prepared for analysis and made available by the authors of Mazel et al. (?). The data consists of 15 minute recordings, collected everyday at 2pm Japanese time.

It is well known in the field of Internet analysis that traffic is constantly affected by the emergence of anomalies. The latter pose significant hurdles to robust and meaningful statistical modeling of traffic. To tackle this issue, the technique of random projections was developed. It consists of splitting each traffic series into a collection of subtraces. It has been reported that the median applied to the independent analysis of these subtraces is a robust statistical description of background (anomaly-free) traffic. This is thoroughly documented in Dewaele et al. (?), Borgnat et al. (?) and Fontugne et al. (?).

In this work, the random projection procedure yields 16 different subtraces. For each subtrace, the 4 time series consist of byte and packet counts in each direction (Japan to USA and USA to Japan), aggregated at the reference scale s.

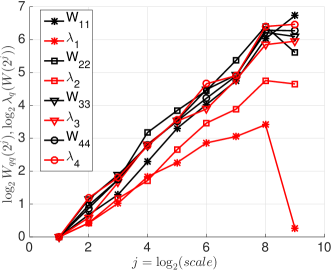

We analyze the data both by means of univariate-like and multivariate methodologies, based upon, respectively, the main diagonal entries and the log-eigenvalue functions . The median of each function and , , is taken across subtraces to generate a characterization of self-similarity in Internet traces.

Examples of such functions are shown in Figure 6, left panel. The functions clearly display linear behavior, hence indicating self-similarity. They are, however, nearly identical, with similar slopes. Incorrectly, this leads to the conclusion that the 4 times series are characterized by the same Hurst exponent (cf. Table 1, top row).

Multivariate analysis also confirms self-similarity by means of the linear behavior of the functions . However, the slopes clearly differ, which is evidence for the presence of different Hurst eigenvalues for the 4-variate data (cf. Table 1, bottom row). This reveals the rich character of multivariate self-similarity in Internet traffic.

This finding is important in several ways. First, it complements 20 years of self-similarity analysis in Internet traffic and significantly enhances and renews it. Second, multivariate self-similarity modeling may permit revisiting several traffic engineering issues. Notably, it may underpin the construction of new anomaly detection schemes that will fruitfully complement those already available (see Mazel et al. (?)).

Results are reported here for one day traces, but equivalent conclusions can be drawn from numerous other traces in the MAWI repository. A longitudinal large-scale study is currently being conducted in collaboration with the teams managing the MAWI repository, aiming both at multivariate self-similarity characterization and at exploring its potential interest in anomaly detection.

| univariate-like | 0.85 | 0.86 | 0.86 | 0.90 |

|---|---|---|---|---|

| multivariate | 0.51 | 0.69 | 0.82 | 0.86 |

7 Conclusion

In this paper, we construct the first joint estimator of the real parts of the Hurst eigenvalues of -variate OFBM. The procedure consists of a wavelet regression on the log-eigenvalues of the sample wavelet spectrum. The estimator is shown to be consistent for any time reversible OFBM and, under stronger assumptions, also asymptotically normal starting from either continuous or discrete time measurements. Simulation studies establish the finite sample effectiveness of the methodology in terms of bias, mean squared error and asymptotic normality, and illustrate its benefits compared to univariate-like (entrywise) analysis. An application to 4-variate time series of Internet traffic data from the MAWI archive turned up evidence of multivariate self-similarity. Future work includes the quantification of confidence intervals and optimal regression procedures in practice; the construction of methodology for instances where Hurst eigenvalues display multiplicity strictly between 1 and ; applications in anomaly detection in Internet traffic. In the near future, a Matlab toolbox for the estimators proposed in this paper will be made publicly available.

Appendix A Proofs

In the proofs, whenever convenient we write instead of .

A.1 Consistency of wavelet log-eigenvalues

To show Theorem 3.2, recall that the Courant-Fischer principle provides a variational characterization of the eigenvalues of a matrix . In other words, it states that, for ,

| (A.1) |

where is an -dimensional subspace of (e.g., Horn and Johnson (?), chapter 4).

Proof of Theorem 3.1: The limits (3.3) are a direct consequence of (3.1). We will only show the first limit in (3.1), since the second one can be proved by a similar and slightly simpler argument.

We first lay out a few facts that will be used throughout the proof. Note that the nonsingularity of (see (2.5)) implies that

| (A.2) |

Under conditions (2.1), (2.3) and (2.4), by operator self-similarity the sample wavelet spectrum satisfies the operator scaling relation

| (A.3) |

for as in (2.14) (c.f. (2.16)). Now define the set , . Note that, by Theorem 2.1, , , for some pair . So, for any small ,

| (A.4) |

for some . For any , by Lemma LABEL:l:S_1=<S_2 applied to , and , ,

| (A.5) |

for . Recall that

and set , . Now consider Lemma LABEL:l:S_1=<S_2 applied to

and

We obtain the double bound

| (A.6) |

However, in view of (A.2), we can write

| (A.7) |

By expressions (A.7) and (LABEL:e:z^Jlambda),

| (A.8) |

for . In the first inequality in (A.8), we use the fact that , i.e., is a strictly positive constant. The second equality in (A.8) holds because no logarithmic term appears in one of the main diagonal blocks with power greater than . By (A.6), (A.8) and taking logs in (A.5), in view of (A.4) we arrive at the consistency relation in (3.1).

A.2 Asymptotic normality of wavelet log-eigenvalues

Recall that, throughout this section, we work under the stronger assumption (2.6). For notational simplicity, we write

| (A.9) |

Proof of Proposition 3.1: In this proof, we will use the Courant-Fischer principle (A.1) as applied to real spaces.

We start off with the eigenvalue , whose behavior is the easiest to characterize. From expression (LABEL:e:W_a,2j), note that

| (A.10) |

Recall that denotes an eigenvector of associated with . For every , a.s., and the largest eigenvalue of is the only one not converging to zero. Therefore, (3.6) holds, and so does (3.4) for and

Turning to the remaining eigenvalues, in regard to , statement (3.6) is a consequence of (LABEL:e:|<p3,u2>|a^(h3-h2)=O_P(1)) by considering , sequentially. To show , fix and rewrite

| (A.11) |

In (A.11), each entry is generally not identically zero and can be obtained by symmetry, and in both matrices on the right-hand side of (A.11), entry appears in boldface for ease of visualization. By Weyl’s inequality,

| (A.12) |

(Horn and Johnson (?), Theorem 4.3.1, p. 239). Since , then

| (A.13) |

Now consider the second term on the right-hand side of (A.12). Define the matrix

| (A.14) |

Let

| and | (A.15) |

be unit eigenvectors associated with and , respectively. As a consequence of (LABEL:e:|<p3,u2>|a^(h3-h2)=O_P(1)) in Lemma LABEL:l:<p3,u2>a(nu)^(h_3-h_2)=OP(1) applied to and , for any there exists such that

| (A.16) |

where

| (A.17) |

Moreover,

Therefore, for some constant , with probability going to 1,

Hence, in the set ,

| (A.18) |

where the inequality holds for large enough and the last equality is a consequence of (A.17).

Turning to the matrix , it is clear that

is the real -dimensional eigenspace associated with the zero eigenvalues of , i.e., with , . Therefore,

| (A.19) |

Let

be the global minima of the functions and as in (LABEL:e:x*_sol) and (LABEL:e:x*_sol_determ), respectively. Consider a sequence of vectors

| (A.20) |

such that

which is possible for large enough . In particular, the distance between and the subspace goes to zero. This implies that, without loss of generality, we can choose the sequence so that

| (A.21) |

where is given by (3.6). Let be a sequence of eigenvectors (of ) as in (3.6). Then, by (A.19) and (A.20),

| (A.22) |

On the other hand, since is the global minimum of the function ,

| (A.23) |

From (A.12), (A.13), (A.18), (A.22) and (A.23),

| (A.24) |

in the set , where

Consequently, for any and large enough ,

| (A.25) |

Since is arbitrary,

| (A.26) |

This establishes (3.4) for with

| (A.27) |

To show , consider any subsequence of

We will show that there is a further subsequence such that

| (A.28) |

where is given by (LABEL:e:x*_sol_determ). This, in turn, implies (3.8).

In fact, (3.4) and (A.27) imply that there is a further subsequence such that

| (A.29) |

Let be a sequence of eigenvectors (of ) satisfying (3.6). The subsequence is bounded a.s., which can be shown by an adaptation of the proof of Lemma LABEL:l:<p3,u2>a(nu)^(h_3-h_2)=OP(1). Therefore, we may assume without loss of generality that there is some such that

Consequently,

In view of (A.29), . Since is the unique global minimum of ,

It only remains to show (). First recall that the limiting matrix satisfies the entrywise scaling relation (2.18). Therefore, the function in (A.32) can be rewritten as

where

| (A.30) |

Since the relation (A.30) is isomorphic, minimizing the function over is equivalent to minimizing the function again over , where the latter function does not depend on . Since and correspond to the values attained by the functions and at their minima, respectively, relation (3.5) holds.

Lemma A.1

Fix and let , be, respectively, a sequence of eigenvectors associated with and its limit in probability as in (3.6). Let be the random and deterministic functions, respectively, defined by

| (A.31) |

and

| (A.32) |

where the residual function in (A.31) is given by

Then, each function and has a unique global minimum.