Explicit expressions for European option pricing under a generalized skew normal distribution

Abstract

Under a generalized skew normal distribution, we consider the problem of European option pricing. Existence of the martingale measure is proved. An explicit expression for a given European option price is presented in terms of the cumulative distribution function of the univariate skew normal and the bivariate standard normal distributions. Some special cases are investigated in a greater detail. To carry out the sensitivity of the option price to the skew parameters, numerical methods are applied. Some concluding remarks and further works are given. The results obtained are extension of the results provided by [4].

Keywords and phrases: Bivariate normal distribution; Complete market; Generalized skew normal distribution; Martingale measure; Option price.

1 Introduction

A call (put) option is the right to buy (sell) a particular asset for a strike price at a specified time in the future. There are various types of option. The most common one is European options (EOs) which can only be exercised on the maturity date. [3] assumed a geometric Brownian motion for the underlying asset and derived a closed form for fair price of a given European option (EO), known as Black-Scholes option pricing formula. It is one of the major successes of modern financial economics. But empirical evidences showed that there are systematic pricing errors when compared to observed option prices. For example, [5] present evidence of systematic mispricing of the Black-Scholes model when the log-returns of the underlying asset are skewed and leptokurtic, typically underpricing options that are deep in-the-money and overpricing options that are out-of-money. To resolve the mispricing problem, Black-Scholes option price has been extended along with several directions. For example, [4] assumed that the underlying stock price process follows a geometric Azzalini skew Brownian motion. More precisely, let

| (1.1) |

where the random variable has a skew normal distribution, denoted by , with probability density function (pdf)

where and are the pdf and the cumulative distribution function (cdf) of the standard normal distribution, respectively, i.e.

EO pricing under the model (1.1) was investigated by

[4]. For a greater detail, see [6]. In this paper, we extend the

results of [4] by assuming a generalized SN distribution for the random variable in (1.1) and call the generalized geometric skew Brownian motion.

There are many extensions for the SN distribution. An extension of the SN distribution was proposed by [2] and discussed by [1] in a more detail. More specifically, the random variable has a generalized SN distribution with parameters , denoted by , if its pdf be

| (1.2) |

In the sequel sections, we assume that the stock price follows the generalized Azzalini skew Brownian motion, i.e.

| (1.3) |

where . Notice that for , the random variable with pdf (1.2) is simplified to the Azzalini’s skew normal and thus the model (1.3) is transformed to the model (1.1). Therefore, the results of this paper are extensions of the results provide by [4]. The rest of this article is organized as follow: In Section 2, the unique martingale measure is derived under the generalized geometric skew Brownian motion (1.3). An explicit expression for the EO price is presented in Section 3. Some special cases are considered in more details in Section 4. In Section 5, the EO price’s sensitivities to the skew parameters is considered. Section 6 concludes. The proofs are given in the appendix.

2 Martingale measure

The first step for obtaining the EO price is to

find an equivalent risk neutral probability measure, denoted by

, under which the discounted stock price process is a martingale, where is the riskless continuous rate of

interest and is the expiry date of the option.

Let denote the moment generating function (MGF) of the random variable . Under the model (1.3) with the objective probability measure , the MGF of the random variable is derived as

| (2.1) | |||||

where is the MGF of the random variable with pdf (1.2) and is the information available to investors at present time . For more details, see [8]. [1] showed that

| (2.2) |

From the identity and (LABEL:h2), under the martingale measure , we have

| (2.4) |

where

and has a generalized SN distribution under the martingale probability measure . Notice that

| (2.5) | |||||

3 European call option price

Assuming a complete market, the equivalent martingale measure will be unique (See, [8]). Therefore, the non-arbitrage (NA) EO price with the strike price and the expiration time , denoted by , is derived as

| (3.1) |

Proposition 3.1

Let . Then

| (3.2) | |||||

where

| (3.3) |

From Equations (3.1) and (3.2), we immediately see that

-

1.

is free of the drift parameter .

-

2.

is an increasing, convex function of .

-

3.

is a decreasing, convex function of .

-

4.

Since the value of an European call option is the same as that of an American call option ([8]), we conclude that is increasing in .

Proposition 3.2

as .

4 Some special cases

In what follows, we obtain simple expressions for given by (3.2) in some special cases.

Case

In this case, Equation (3.3) is reduced to

| (4.1) |

Also,

| (4.2) |

Upon substituting (4.1) and (4.2) into (3.2), we have

| (4.3) |

where is given by (4.1). From (1.2), one can see that for every . Thus, in this case we conclude from (4.3) that

| (4.4) |

which is the well known Black-Scholes option price, denoted by .

Case

In this case, we have from (3.3) that

| (4.5) |

This implies from (3.2) that

where stands for the cdf of the standard Azzalini’s skew normal distribution with parameter , i.e.

The option price (LABEL:option:price:skew:gamma=0), denoted by , was obtained by [4]. One may be noticed that they could not find an explicit expression for (LABEL:option:price:skew:gamma=0) while we could presented EO price in (LABEL:option:price:skew:gamma=0) in terms of the cdf of the univariate skew normal and the bivariate standard normal distributions. Numerical values of these functions are provided by some statistical softwares such as with package .

5 Empirical evidences

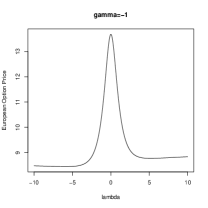

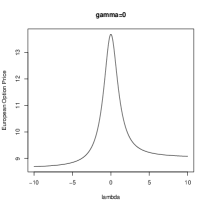

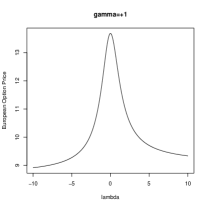

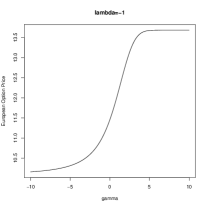

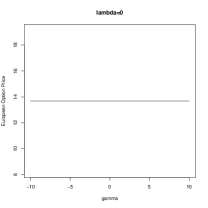

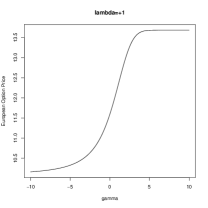

In this section, we consider the option’s sensitiveness to the skew parameters and in (3.2) via a numerical methods because the partial derivatives of the option given by (3.2) have complicated forms. The corresponding plots are given in Figure 1. Following [4], the benchmark case was taken as , , , and . Also, we consider and . Numerical values of for some selected values of the parameters are given in Table 1.

| -2 | -1 | 0 | +1 | +2 | ||

|---|---|---|---|---|---|---|

| -2 | 8.702112 | 10.69672 | 13.68113 | 10.75255 | 8.857459 | |

| -1 | 9.188333 | 10.99278 | 13.68113 | 11.08288 | 9.406439 | |

| 0 | 9.805336 | 11.45179 | 13.68113 | 11.59007 | 10.09846 | |

| +1 | 10.55043 | 12.09882 | 13.68113 | 12.27943 | 10.91346 | |

| +2 | 11.37726 | 12.8264 | 13.68113 | 12.99414 | 11.7723 |

Empirical evidences from Table 1 show that

-

•

the EO price is very sensitive w.r.t. the skew parameters and ;

-

•

the EO price is decreasing in ;

-

•

for , Black-Scholes EO price in Equation (4.4) is obtained;

-

•

for , we have an over estimation by Black-Scholes pricing EO , that is, overpricing by Black-Scholes EO pricing leads to out-of-money;

-

•

for , the option price does not depend on the parameter while for , the option price is increasing in the parameter ;

-

•

for and we have , that is leads to in-the-money (out-of-money).

6 Conclusions

Assuming a generalized SN model, the problem of European option pricing was investigated. Existence and uniqueness of the martingale measure was shown. The explicit expression for EO price was derived in terms of the cdfs of the univariate SN and the bivariate standard normal distributions. Empirically, it was shown that the EO price is sensitive to the skew parameters. The results obtained may be extended for other general SN models. See for example [9]. Another important topic is the problem of the estimating skew parameters on the basis of the observed EO prices [5]. Work in this direction is currently under progress and we hope to report findings in a future paper.

References

- [1] Arnold, B. C., Beaver, R. J. (2002). Skewed multivariate models related to hidden truncation and/or selective reporting. Test, 11, 7–54.

- [2] Azzalini, A. (1985) A class of distributions which includes the normal ones. Scandinavian Journal of Statistics, 12, 171-178.

- [3] Black, F. and Scholes, M. (1973) The pricing of options and corporate liabilities, Journal of Political Economy, 81, 637–659.

- [4] Corns, T. R. A., and Satchell, S. E. (2007) Skew Brownian Motion and Pricing Europuean Options, The European Journal of Finance, 13(6), 523–544.

- [5] Corrado, C. and Su, T. (1997) Implied volatility skews and stock index skewness and kurtosis implied by S&P 500 index option prices, The Journal of Derivatives, 4(4), 8–19.

- [6] Fan, J. and Mancini, L. (2009) Option pricing with model-guided nonparametric methods, Journal of the American Statistical Association, 104(488), 1351–1372.

- [7] Jamalizadeh, A., Pourmousa, R. and Balakrishnan, N. (2009) Truncated and Limited Skew-Normal and Skew- Distributions: Properties and an Illustration, Communications in Statistics-Theory and Methods, 38, 2653–2668.

- [8] Karatzas, I. and Shreve, S. E. (1998) Methods of Mathematical Finance, Springer-Verlag New York, Inc.

- [9] Shafiei, S., Balakrishnan, N., Doostparast, M. (2012). A new parametric family of skewed distributions arising from the symmetric power distribution and associated inference, submitted.

Appendix

Proof of Proposition 3.1

where . Thus,

| (6.1) |

where and and is the indicator function for the set , i.e.

Therefore,

| (6.2) | |||||

where is the truncated skew normal distribution to interval , introduced by Jamalizadeh et al.(2009), and is the corresponding MGF. Jamalizadeh et al.(2009) derived an explicit expression for as

| (6.3) | |||||

where

| (6.4) |

and is the cdf of (the standard bivariate normal distribution with correlation coefficient ). From (6.2), (6.3) and (6.4), one can easily show that

Upon substituting (LABEL:B:expression:2) into (6.1), we have

| (6.6) | |||||

where

After some algebraic manipulations, a simplified version for is derived as

| (6.7) | |||||