Markov cubature rules for polynomial processes111The authors would like to thank the anonymous referees for their careful reading of the manuscript and suggestions. Martin Larsson gratefully acknowledges support from SNF Grant 205121_163425. The research of Sergio Pulido benefited from the support of the Chair Markets in Transition (Fédération Bancaire Française) and the project ANR 11-LABX-0019. The research leading to these results has received funding from the European Research Council under the European Union’s Seventh Framework Programme (FP/2007-2013) / ERC Grant Agreement n. 307465-POLYTE

forthcoming in Stochastic Processes and their Applications)

Abstract

We study discretizations of polynomial processes using finite state Markov processes satisfying suitable moment matching conditions. The states of these Markov processes together with their transition probabilities can be interpreted as Markov cubature rules. The polynomial property allows us to study such rules using algebraic techniques. Markov cubature rules aid the tractability of path-dependent tasks such as American option pricing in models where the underlying factors are polynomial processes.

Keywords: Polynomial process; cubature rule; asymptotic moments; transition rate matrix; transition probabilities; American options.

MSC2010 subject classifications: 60G07, 60J25, 60J27, 60J28, 60J10, 91G60, 65C20, 65C30, 60H35, 60F99, 60J60, 60J75, 60H10, 60H20, 60H30.

1 Introduction

Polynomial processes have recently gained popularity thanks to their tractability and flexibility. For instance, they have been applied in financial market models for interest rates (Delbaen and Shirakawa, 2002; Zhou, 2003; Filipović et al., 2017), credit risk (Ackerer and Filipović, 2016), variance swaps (Filipović et al., 2016), stochastic volatility (Ackerer et al., 2018), stochastic portfolio theory (Cuchiero, 2019), life insurance liabilities (Biagini and Zhang, 2016), energy prices (Filipović et al., 2018), and foreign exchange rates (De Jong et al., 2001; Larsen and Sørensen, 2007). Polynomial processes, as considered by Cuchiero et al. (2012) and Filipović and Larsson (2016, 2017), are stochastic processes with the property that the conditional expectation of a polynomial is a polynomial of the same or lower degree. This implies that conditional moments can be computed efficiently and accurately, which can be exploited to construct tractable models. Despite these advantages, the tractability of polynomial processes deteriorates as one faces path-dependent tasks such as American option pricing or computation of path-dependent functionals.

In this paper, we develop a method for tackling such problems. We approximate a given polynomial process by a finite state Markov process that matches moments up to a given order. We call such a finite state process a Markov cubature rule because the states of the process together with their transition probabilities can be interpreted as cubature rules for the law of the original process at different times. Markov cubature rules facilitate the implementation of polynomial models by simplifying costly computational tasks such as Monte-Carlo simulation and pricing of path-dependent and American options.

The polynomial property allows us to study the existence of Markov cubature rules using algebraic techniques. Contrary to the classical cubature problem, we look for cubature rules that use the same set of cubature points at all times, as this is desirable for numerical applications like the calculation of American option prices in finance. Additionally, the moments to be matched depend on the cubature points chosen. In continuous time, the exact moment matching condition turns out to be too stringent as we explain in Section 2.1. Instead, we find approximate Markov cubature rules by solving a quadratic programming problem. This quadratic programming problem arises naturally from our first main result, Theorem 3.2, which gives an algebraic and geometric characterization of continuous time Markov cubature rules. While a systematic analysis of computational cost, accuracy, and convergence falls outside the scope of the present paper, we provide numerical examples which indicate that the approximate Markov cubature rules work well in practice. In discrete time, our second main result, Theorem 5.2, yields existence of Markov cubature rules on an appropriately chosen time grid, under suitable assumptions involving the asymptotic moments of the given polynomial process. The existence of asymptotic moments is a crucial hypothesis and lies at the core of the proof of this theorem.

Approximations by discretization of stochastic models using finite state Markov processes appear regularly in the numerical methods literature. In finance, these techniques have been used in order to price and hedge exotic and American options via finite state Markov chain and binomial tree approximations; see e.g. Gruber and Schweizer (2006); Kifer (2006); Bayraktar et al. (2018). As explained by Kushner (1984) and Kushner and Dupuis (2013), these approximations are linked to numerical analysis techniques such as the finite difference method. It is also relevant to mention quantization methods that address the optimal choice of the approximation grid on a finite time domain and in higher dimensional state spaces. Quantization has been employed to price American options by Bally et al. (2005), and in the context of polynomial processes by Callegaro et al. (2017). In all these cases, discretization happens at two levels: the discretization of the time domain, as it is performed in simulation algorithms, and the discretization of the space domain. We add to this literature by developing a cubature based discretization of stochastic models.

Cubature methods play a crucial role in numerous numerical algorithms. For instance, classical cubature techniques have been applied within the context of filtering in Arasaratnam and Haykin (2009). Additionally, the cubature formulas on Wiener space, developed by Lyons and Victoir (2004), have been used in multiple applications: in filtering problems by Lee and Lyons (2015), to calculate greeks of financial options by Teichmann (2006), and to numerically approximate solutions of Stochastic Differential Equations by Bayer and Teichmann (2008) and Doersek et al. (2013), Backward Stochastic Differential Equations (BSDEs) by Crisan and Manolarakis (2012, 2014), and Forward-Backward Stochastic Differential Equations (FBSDEs) by Chaudru de Raynal and Garcia Trillos (2015). Cubature methods ease the calculation of conditional expectations, which are at the core of the above mentioned numerical problems. Contrary to the techniques mentioned in the previous paragraph where discretization is performed in the time and space domains, cubature on Wiener space discretizes path space directly. These cubature rules extend Tchakaloff’s cubature theorem, as studied by Putinar (1997) and Bayer and Teichmann (2006), to the Wiener space of continuous paths. Our Markov cubature of polynomial processes provides a practically feasible variant of cubature of stochastic processes, as it is based on elementary matrix exponential calculus.

Our paper is organized as follows. In Section 2 we define Markov cubature rules and provide some basic facts about polynomial processes. In particular, in Section 2.1 we explain why the notion of Markov cubature rule is too stringent in continuous time. In Section 3, we give algebraic and geometric characterizations of continuous time Markov cubature rules for polynomial processes; see Theorem 3.2. Motivated by this result we introduce, in Section 4, a notion of approximate continuous time Markov cubature rule, and describe the quadratic programming problem through which it is obtained. The performance of these approximate Markov cubature rules is illustrated through numerical examples. Specifically, in Sections 4.1 and 4.2 we use them to price American options in the Black–Scholes model and in a Jacobi model of exchange rates. In Section 5, we study existence of discrete time Markov cubature rules; see Theorem 5.2. In Section 6 we discuss another possible relaxation of the Markov cubature problem by allowing negative weights. However, as we then illustrate, these negative weights are not suitable for numerical computations. The conclusions of our study are summarized in Section 7. Appendix A presents results on asymptotic moments of polynomial processes needed throughout the paper, and Appendix B contains the proofs of all results in the main text.

We adopt the following notation: We write for the set of nonnegative real numbers, for the set of positive real numbers, and for the set of positive natural numbers. For , denotes the vector space of matrices, and by convention consists of column vectors. Given and a set , we say that is a polynomial on if there exists a polynomial on such that . Its degree is defined by . We let and denote the algebra of polynomials on and the vector space of polynomials on of degree less than or equal to , respectively. For and a set we write for the convex hull of .

2 Setup and overview

Fix a state space . We consider a càdlàg adapted process defined on a filtered measurable space , along with a family of probability measures , , such that is an -valued Markov processes under each , starting at . We assume that admits an extended generator , whose domain contains all polynomials. That is, we assume

for every and every . This implies in particular that is a semimartingale under each . Moreover, the positive maximum principle holds, in the sense that for any ,

| if for some , then . | (2.1) |

In particular, on whenever on , which implies that is well-defined as an operator on .666Indeed, if is a representative of , we define , which is independent of the choice of representative .

2.1 Markov cubature rules

Our goal is to construct a time-homogeneous Markov process with finite state space that approximates the process . We base our approximation on moment conditions across initial states and times. With this goal is mind we make the following definition.

Definition 2.1.

We say that a time-homogeneous Markov process with finite state space defines an -Markov cubature rule for on if

| (2.2) |

holds for all , , and .

Remark 2.2.

In condition (2.2), denotes the expectation with respect to the probability measure while denotes the expectation with respect to the probability measure associated to the finite state Markov process . We adopt this convention throughout the paper.

Suppose that is a -Markov cubature rule for on . The moment-matching condition (2.2) can be rewritten as

| (2.3) |

for all , , and . Hence, for any and , the points together with the transition probabilities define an -cubature rule for the law of with respect to . We highlight that for Markov cubature rules, contrary to classical cubature rules, the matched moments depend on the cubature points, and the same points are used for all times . In addition, as stated in Theorem 2.7 below, the properties of the weights inherited by the Markov property of Y guarantee time-consistency features of these cubature rules for polynomial processes. This time-consistency is desirable to conduct path-dependent computations as the ones presented in the numerical examples in Section 4.

We will also consider relaxed versions of -Markov cubature rules. Indeed, it turns out that the notion of an -Markov cubature rule is too stringent in general. To see why, suppose is given as the solution of an SDE of the form

Under linear growth conditions on the coefficients, one has the estimate

for all , where is a constant that only depends on and ; see Problem 5.3.15 in Karatzas and Shreve (1991). If is a -Markov cubature rule for on , this estimate carries over to , which in conjunction with the time-homogeneous Markov property yields

for any and any with . By Kolmogorov’s continuity lemma, then has a version with continuous paths, which forces it to be constant. Consequently, in the generic case, the diffusion will not admit any non-trivial -Markov cubature rule on , unless . Moreover, by a similar argument, unless exhibits jumps, it is impossible to construct a non-trivial Markov process with countable state space such that (2.2), with , holds for all initial conditions. This is a rather severe restriction.

One way to avoid this obstruction is to relax the exact moment matching condition (2.2) and allow a process whose moments approximate the moments of the original process . This approach is explained in Section 4. Another possibility is to replace with a discrete time set , in which case one remains within the framework of Definition 2.1. This approach is pursued in Section 5. A different relaxation is obtained if negative weights in the cubature rule are allowed. This approach is explained in Section 6.

We will study these relaxations of the Markov cubature problem for polynomial processes. This will allow us to employ algebraic considerations in our study. We give the basic properties of polynomial processes in the next subsection.

2.2 Polynomial processes

Definition 2.3.

The operator is called polynomial if for all . In this case is called a polynomial process.

Remark 2.4.

In the present paper, is assumed to be the extended generator of some given Markov process . We are not concerned with the question of existence of such a process given a candidate operator . This issue is discussed in Filipović and Larsson (2016) for polynomial diffusions.

If is a polynomial process, then all mixed moments of are polynomial functions of the initial state. More precisely, fix and denote by the dimension of . Let be a basis for and define

| (2.4) |

If is polynomial, one has

| (2.5) |

for some matrix , where acts componentwise on . From this one obtains the following lemma.

Lemma 2.5.

Assume is a polynomial process. Then for any polynomial with coordinate representation , that is, , one has

| (2.6) |

Thus the left-hand side is a polynomial in with coordinate representation .

Remark 2.6.

As a consequence of Lemma 2.5, Markov cubature rules for polynomial processes are polynomial processes as well when contains an interval around zero.

We say that the time set is stable under differences, if for all such that . This property turns out to be useful for path-dependent computations involving polynomial processes, as we illustrate numerically in Section 4. The reason is that stability under differences leads to the following time consistency result, which states that not only the one-dimensional marginals satisfy moment matching, but higher dimensional marginals do as well.

Theorem 2.7.

Suppose that is a polynomial process and that is stable under differences. Let be a time-homogeneous Markov process with state space . Then the process is an -Markov cubature rule for on if and only if given such that and polynomials with , we have

| (2.7) |

for all .

Remark 2.8.

Assume that is an -Markov cubature rule for a polynomial process on . Set . The time set is the smallest subset of that is stable under sums and contains . The argument in the proof of Theorem 2.7 shows that is also an -Markov cubature rule for on .

3 Continuous time Markov cubature for polynomial processes

We assume hereafter that is a polynomial process, and fix . We will study characterizations of continuous time -Markov cubatures rules for , namely -Markov cubature rules on . Even though, as explained in Section 2.1, these cubature rules turn out to be too stringent in general, the results of this section motivate and facilitate the study of relaxed notions of Markov cubature in Sections 4, 5 and 6.

We adopt the notation of Section 2 but for simplicity we often omit the index . Given points we denote by the -matrix whose elements are

| (3.1) |

for all and . Notice that the -th row of the matrix is equal to as defined in (2.4).

| (3.2) | ||||

| (3.3) |

for all and . Equations (3.2)-(3.3) establish a relationship between the analytical calculation of the generator and semigroup acting on the function space of polynomials, and an algebraic calculation involving matrix multiplication.

Theorem 3.2 below is the main characterization theorem for the existence of a continuous time -Markov rule. Before stating the theorem we recall that a transition rate matrix is a matrix whose rows add up to zero and off-diagonal elements are nonnegative. We also need the following definition.

Definition 3.1.

We say that a vector points into at if there exist such that

Theorem 3.2.

Given a set of points the following statements are equivalent.

-

(i)

There exists a continuous time -Markov cubature rule with state space ; see Definition 2.1.

-

(ii)

Given as in (3.1), for some transition rate matrix .

-

(iii)

Given as in (3.1), for some matrix with nonnegative off-diagonal elements.

-

(iv)

For each the vector points into at the point ; see Definition 3.1.

If in addition and the matrix is invertible, there exists a Lagrange basis of , , i.e. a basis with , and the above statements are equivalent to:

-

(v)

for .

Moreover, when condition (ii) is satisfied, can be taken as the transition rate matrix of the -Markov cubature rule .

For the proof of Theorem 3.2 we will need the following lemma.

Lemma 3.3.

Suppose that is a matrix such that . Then the rows of add up to zero.

As the proof shows, the conditions in Theorem 3.2 imply that if is an -Markov cubature rule then, for each , the flow never leaves the convex set . Indeed, notice that is a transition semigroup and for all we have

The points lie on the moment curve and correspond to the rows of . Their convex hull represents all the possible initial distributions of a Markov chain with state space .

4 Approximate Markov cubature

According to Theorem 3.2, in order to find a continuous -Markov cubature rule for a polynomial process one has to find points and a transition rate matrix such that

where is the matrix defined by (3.1) and is the matrix of the generator of restricted to with respect to the basis ; see (2.5). As explained in Section 2.1, it is actually impossible to solve this problem for polynomial diffusions if . In view of this restriction we instead consider the optimization problem

| (4.1) |

where the Frobenius norm is used, and where we have fixed the generator matrix and the points , hence the matrix .777Recall that the Frobenius norm of a matrix is . The constraint that be a transition rate matrix can be written

| (4.2) | |||

| (4.3) |

where is a vector of ones. Through vectorization we can write this optimization problem as a quadratic programming problem. Indeed, we have

where is the vectorization operator, the Kronecker product, and the -dimensional identity matrix. In addition, the constrains (4.2)-(4.3) on correspond to

| (4.4) | |||||

| (4.5) |

where and the ’s are the canonical basis vectors in . Therefore the minimization problem (4.1) can be translated into the quadratic programming problem

| (4.6) |

We will illustrate the performance of this type of finite state Markov approximation through numerical examples.

4.1 American option pricing in the Black–Scholes model

We consider a Black–Scholes model where the financial asset’s return process is a Brownian motion with drift. More precisely, is supposed to have risk-neutral dynamics of the form

where is the spot interest rate, is the volatility of the returns and is a one-dimensional Brownian motion. In this model, the price at time of an American put option with maturity , strike price , and initial log-price is

| (4.7) |

To approximate the value we proceed as follows. We fix equidistant points on the truncated support of the process given by

We further fix and the standard monomial basis of . Let be the solution of the quadratic programming problem (4.6) and define as the finite state process on with transition rate matrix . For let be a uniform partition of the time horizon . We define by

for . Since is a finite state Markov process and we are only considering finitely many exercise times in , the vector can be computed through a very simple backward induction algorithm. This computation resembles the calculation of an American option price in a binomial tree approximation of the Black–Scholes model; see Cox et al. (1979). Explicitly, we have where

| (4.8) |

with and . Observe that this computation gives simultaneously all the values for . For any initial value we can simply perform an interpolation in order to approximate . Moreover, we have that is the price of an American put option with strike and initial underlying log-price . Hence, the same approximate cubature rule can be used to price American options for several initial values of the log-price and for different strikes. This observation remains valid in any stochastic volatility model framework as long as the dynamics of the volatility process are independent of the initial value of the spot price.

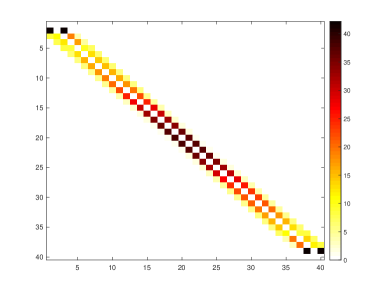

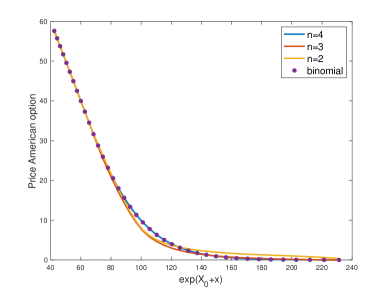

To illustrate the performance of our method we consider the parameters , , and . We compute the approximate American put option prices with cubature points, moments and time steps. We compare these prices with the benchmark prices obtained with a 1000–time step binomial tree approximation of the Black–Scholes model. The results are reported in Table 1. We find that with these parameters our approximate Markov cubature method has a mean relative difference with respect to the benchmark binomial tree prices of the order . The choice of and is made to achieve this level of accuracy in a comparable amount of time with as few cubature points and moments as possible. The colormap in Figure 1 shows the off-diagonal values of the transition rate matrix . We observe in particular that the majority of nonzero transition rates in the approximate Markov cubature rule occur around the diagonal, hence the process has a multinomial tree structure. Also the transition rates decrease as we approach the limits of the interval . The high transition rates close to the limit points of the interval are a boundary effect as a consequence of the truncation of the domain of . The running time to find the transition rate matrix by solving the optimization problem (4.1) in Matlab on a 2.3 GHz Intel Core i5 CPU, is approximately 0.75 seconds. Once the transition rate matrix is obtained, the computation of the American option prices using the recursive algorithm (4.8), for a given maturity, a given strike, and all initial prices, is almost instantaneous and takes only about 0.004 seconds. To illustrate the influence of the moments, we plot in Figure 2 the American put option prices for and different values of . These prices are compared with the benchmark values obtained with a 1000 time step binomial approximation of the Black–Scholes model on the 40 points of the log-price grid.

4.2 American option pricing in a Jacobi exchange rate model

Suppose that represents the exchange rate between two currencies at time . Inspired by De Jong et al. (2001) and Larsen and Sørensen (2007), we model with a Jacobi diffusion of the form

| (4.9) |

for given parameters , , . We assume that the domestic interest rate is constant and the foreign interest rate is such that (4.9) describes the risk neutral dynamics of the log exchange rate (for details see De Jong et al. (2001); Larsen and Sørensen (2007)). In this model the exchange rate between the currencies stays bounded between and . As in the previous example, we consider an American exchange option with payoff of the form and maturity . We fix equidistant points on the support of given by and proceed precisely as in the previous example. Namely, we approximate , as in (4.7), using the vector . To compute we use the recursive algorithm in (4.8).

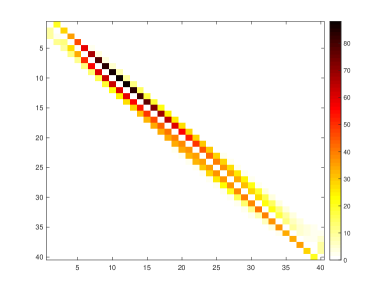

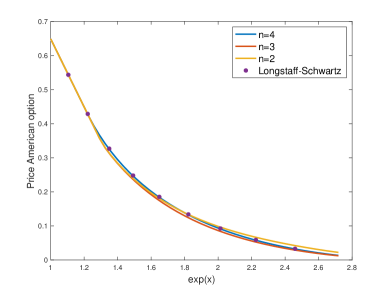

For our numerical illustration we consider the following parameters: , , , , , , and . We compute the approximate American put option prices with cubature points, moments and time steps. We compare these prices with the benchmark prices obtained with a 1000–time step Longstaff–Schwartz algorithm; see Longstaff and Schwartz (2001). The results are reported in Table 2. Our experiments suggest that the approximate Markov cubature method can lead to significant speed-up compared to the simulation based Longstaff–Schwartz approach. The colormap in Figure 3 shows the off-diagonal values of the transition rate matrix . In particular we verify a multinomial nature of our approximate Markov cubature. The running times to find the transition rate matrix and to compute American option prices are comparable to those reported in Section 4.1. To illustrate the influence of the moments, we plot in Figure 4 the American put option prices for and different values of and compare them with the benchmark values obtained with the Longstaff–Schwartz method for the values of in Table 2.

5 Discrete time Markov cubature

The construction of a discrete time -Markov cubature rule for (see Theorem 5.2 below) will use cubature methods over the asymptotic moments. According to Theorem A.1, all the asymptotic moments of order less than or equal to exist if and only if the following condition holds.

-

(H1)

For all nonzero eigenvalues of , we have that and the eigenvalue 0 is a semisimple eigenvalue, i.e. its algebraic and geometric multiplicities coincide.

In this case, we denote these asymptotic moments by

| (5.1) |

To use classical cubature rules, we would like the asymptotic moments (5.1) to be independent of . According to Corollary A.3, this is the case under the following assumption, which is a stronger condition than (H1).

-

(H2)

For all nonzero eigenvalues of , we have that and the eigenvalue 0 is a simple eigenvalue, i.e. its algebraic (and hence geometric) multiplicity is 1.

In this case we write the asymptotic moments (5.1) simply as . In conjunction with (H2), we will make the following assumption throughout this section.

-

(H3)

There exist points and such that

(5.2) for all .

Remark 5.1.

As a consequence of condition (H3) the weights add up to one. Indeed, suppose that the constant polynomial can be written as . Then by (5.1) and (5.2) we deduce

Hence, condition (H3) states that the asymptotic moments (5.1) belong to . As belongs to for all , and (see Putinar (1997), Bayer and Teichmann (2006)), this would be the case if for instance is closed. It would also hold if the asymptotic moments are the moments of a probability distribution; see Proposition A.6. Additionally, as the weights in (H3) are strictly positive, there does not exist a strict subset such that contains all the asymtotic moments (5.1).

Theorem 5.2 below is the main theorem of this section.

Theorem 5.2.

To prove Theorem 5.2 we need the following lemma.

Lemma 5.3.

Suppose the hypotheses of Theorem 5.2 hold. Then, for sufficiently large, there exists a probability matrix with positive entries such that .

The proofs of Theorem 5.2 and Lemma 5.3 suggest a possible procedure for finding discrete cubature rules. In practice, denoting the pseudo-inverse matrix of , one searches for large times so that the matrix has positive entries. One then takes to be the first time such that the entries of are nonnegative, in which case is the transition probability matrix of a discrete cubature rule with time lag .

The following remark shows that the existence of discrete time Markov cubature rules is true under more general hypotheses.

Remark 5.4.

Example 5.5.

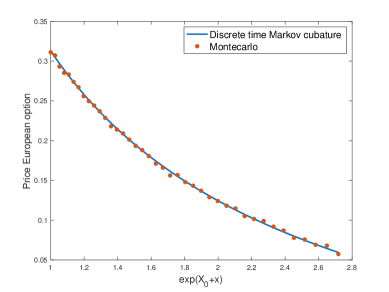

Discrete cubature rules can be useful to perform computations in longer time periods, for example the calculation of prices of European options. To illustrate this we consider the exchange rate model and parameters described in Section 4.2. To approximate the price of a European put option with maturity , strike , and initial log rate equal to , we proceed as follows. We fix a regular partition of the support of . In this case the conditions of Theorem 5.2 are satisfied. The asymptotic moments are

We observe that for there is transition rate matrix such that . We approximate the price of the European put options for the points on the partition using the vector

where and . Figure 5 shows these approximate prices along with the prices obtained using Monte-Carlo simulation.

6 Markov cubature with negative weights

In this section we explore yet another possible relaxation of the Markov cubature problem. We first recall the definition of the mapping in (2.4). In the spirit of Bayer and Teichmann (2006), observe that -Markov cubatures rules for the process correspond naturally to 1-Markov cubature rules for the process , and that the state space of is , which lies on the moment curve . It can be shown that is a polynomial process on ; see Filipović and Larsson (2017, Theorem 4.2). Hence, the study of -Markov cubatures rules for polynomial processes can be reduced to the study of 1-Markov cubature rules by increasing the complexity of the state space.

These observations suggest the following alternative way to relax the notion of Markov cubature in continuous time. For each , consider the process . Due to Lemma 2.5, the process solves the ODE

| (6.1) |

While is only well-defined for initial conditions , whose geometry is highly complex in general, the solution of (6.1) admits any point as initial condition. Therefore, one could seek continuous 1-cubature rules for the deterministic process on instead of on . In view of Theorem 3.2 this amounts to finding points and a transition rate matrix such that

| (6.2) |

where is a matrix whose rows are . Suppose we can find such a matrix of the form , with a matrix of rank . Then there also exists such that the -dimensional identity matrix, and we can rewrite (6.2) as

| (6.3) |

where . The matrix is not necessarily a transition rate matrix. Nevertheless, due to Lemma 2.5 and (6.3) we have

| (6.4) |

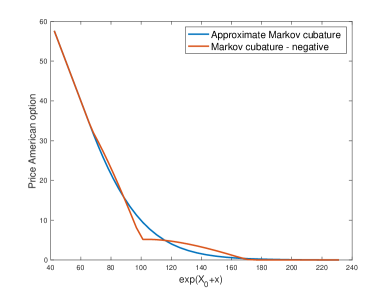

Hence, the pseudo transition rate matrix , defines a pseudo Markov cubature rule with weights that might be negative. These possibly negative weights can be interpreted as the negative “probabilities” appearing in the pseudo transition probability matrix . Therefore, the limitation posed by Kolmogorov’s continuity lemma disappears in a framework with negative “probabilities”. As we will illustrate below, however, negative weights are not compatible with fundamental results such as the dynamic programming principle underlying the pricing of American options. For this reason, we do not pursue this relaxation of the Markov cubature problem.

Example 6.1.

To illustrate why negative weights are not compatible with the dynamic programming principle, we consider the setup of Section 4.1 and the same Black–Scholes model parameters. In particular, we employ cubature points, moments and to approximate the American put option prices. We compare in Figure 6 the results obtained by using the solution of the quadratic programming method described in Section 4 with those obtained with a matrix that solves equation (6.3). This figure clearly demonstrates that the relaxation with negative “probabilities” is not useful for probabilistic applications.

7 Conclusions

In this paper we study discretizations of polynomial processes, via moment conditions, using finite state Markov processes. We call these discretizations Markov cubature rules. The polynomial property allows us to conduct our analysis using algebraic techniques; see Theorems 3.2 and 5.2. Due to Kolmogorov’s continuity lemma the moment matching conditions in continuous time for polynomial diffusions are too stringent. We study instead relaxed versions of Markov cubature rules. A possible relaxation allowing negative transition “probabilities” shows not to be useful for probabilistic applications; see Section 6. We instead retain two other relaxations of the Markov cubature problem that are more useful. In Section 4 we show how to find approximate Markov cubature rules by means of a quadratic programming problem. We then illustrate with examples how to employ this approximation to solve time-dependent problems, like the valuation of American options. In these examples the method performs well. Then, in Section 5 we discuss conditions on the asymptotic moments that allow the construction of discrete time Markov cubature rules; see Theorem 5.2. We also illustrate through a numerical example the use of these discrete rules on longer time grids. A systematic analysis of computational cost, accuracy, and convergence falls outside the scope of the present paper, but is an interesting topic for future research.

Appendix A Asymptotic moments of polynomial processes

Suppose that is a polynomial process with extended generator and state space . Fix and let be the matrix of restricted to with respect to a basis of .

The following theorem shows that Hypothesis (H1) is equivalent to the existence of asymptotic moments of order .

Theorem A.1.

The following are equivalent:

-

(i)

Hypothesis (H1) holds.

-

(ii)

The sequence of matrices converges as .

-

(iii)

converges as for all and .

-

(iv)

converges as for all and .

Proof.

(i)(ii) Suppose that where is the (complex) Jordan normal form of . We have that converges as if and only if converges as . Additionally, converges as if and only if converges for all , where the ’s are the Jordan blocks of the matrix .

Each is of the form where is an eigenvalue of , is the identity matrix and is a nilpotent matrix. Therefore, with a polynomial. We remark that if and only if , and is not a constant polynomial in if .

Hypothesis (H1) holds if and only if for all such that and if , . These observations imply the equivalence between (i) and (ii).

(ii)(iii) Suppose that the matrices converge to a matrix as . By (2.6), we have that

for all and . Hence (iii) holds.

We claim that there exists points, , such that for all

| (A.1) |

Assume for the sake of contradiction that there are no points such that (A.1) holds. Let be a polynomial on and such that By assumption, we can find and such that and Recursively, we would be able to construct points , and polynomials such that

| (A.2) |

These polynomials would be linearly independent and hence a basis of .

Assume that satisfies As is a linear combination of the polynomials we would conclude by (A.2) that all the coefficients of the linear combination are equal to zero and is zero everywhere, a contradiction.

Hence we can always find such that (A.1) holds. These points allow us to define a norm on the space by

Another norm is given by

where . As these norms are equivalent, convergence of a sequence of polynomials on implies convergence of the coefficients. The coefficients of the polynomials of the form are entries of the matrix . Hence (ii) holds. ∎

In general, these asymptotic moments might depend on . In fact we have the following proposition.

Proposition A.2.

Proof.

An immediate corollary of these results characterizes the case when the asymptotic moments are independent of .

Corollary A.3.

Proof.

We already have the equivalence between Hypothesis (H1) and the existence of the asymptotic moments by Theorem A.1. Moreover, observe that (A.4) in the previous proposition implies that for all

where the eigen-polynomials (corresponding to the eigenvalue 0 of ) are given by

for all . These polynomials are linearly independent, as polynomials in . This linear independence implies that is constant on for all if and only if . ∎

Example A.4.

Suppose that is a polynomial martingale. This holds when , where is the matrix of the generator restricted to the space . A particular example is geometric Brownian motion. In this case we have that for all and , and hence,

In this example, , as an eigenvalue of , has algebraic multiplicity 2.

Example A.5.

Suppose that and . Then

In this example, has multiplicity 1 as an eigenvalue of (the matrix of the generator restricted to .) However, 0 has algebraic multiplicity 2 as an eigenvalue of (the matrix of the generator restricted to ). The operator is the infinitesimal generator of the process , where is a Brownian motion. In this case, is a supermartingale converging to zero in expectation while is a martingale starting at .

The following proposition gives sufficient conditions under which the limiting moments are moments of a positive Borel measure.

Proposition A.6.

Let be the matrix of the generator restricted to the space with respect to an extended basis of . Assume that (H1) holds for . Then for all there exists a positive Borel measure such that

| (A.5) |

for all .

Proof.

Let and be fixed. We have by Theorem A.1 that converges as for any polynomial . Define De La Vallée-Poussin’s theorem implies that is uniformly integrable. Additionally, we have that the sequence of Borel probability measures on given by is tight.

Let be an accumulation Borel probability measure of this sequence. We conclude that (A.5) holds. Indeed, assume with out loss of generality that converges in distribution to . By Fatou’s lemma

Therefore, given and , there exist constants such that for all , and for

Hence, for

Since was arbitrary we obtain (A.5); see also Theorem 3.5 in Billingsley (1995). ∎

Remark A.7.

In the proof of Proposition A.6, the existence of the asymptotic moments up to order is simply used in order to apply De La Vallée-Poussin’s theorem and to deduce uniform integrability.

In some cases the measure of the proposition above is not necessarily an invariant measure. The following example illustrates this.

Example A.8.

Suppose that is an exponential Brownian motion. In particular is a martingale and for all . Hence, , where is the asymptotic mean. In this case which is not an invariant measure for .

Appendix B Proofs

Proof of Lemma 2.5.

In view of (2.5) we obtain the vector equation

| (B.1) |

for some local martingale with components. We claim that the expectation is locally bounded in . This follows from the inequality

which holds for some constant that depends on but not on or . This inequality is proved using the argument in the proof of Theorem 2.10 in Cuchiero et al. (2012). Furthermore, in conjunction with Lemma B.1 below, this also implies that is a true martingale. Taking expectations on both sides of (B.1) thus yields the integral equation

whose solution is . This yields (2.6). ∎

Lemma B.1.

Let . The local martingale admits a predictable quadratic variation process, given by .

Proof.

Squaring the expression for and rearranging yields

where the last equality follows from the identity with . Therefore, since is also a polynomial and hence in the domain of , we obtain

This implies the assertion of the lemma. ∎

Proof of Theorem 2.7.

Clearly if (2.7) holds then is an -Markov cubature rule for on . Conversely, suppose that is an -Markov cubature rule for on . By an induction argument it is enough to show (2.7) with . To this end, fix with and let be such that . Define the function

Since is a polynomial process, by Lemma 2.5 the function is a polynomial and . On the other hand, by the definition of a Markov cubature rule and the stability under differences of we have

for all . Therefore, as and are Markov processes, we conclude that

for all . ∎

Proof of Lemma 3.3.

Denote by the coordinates of the constant polynomial with respect to the basis . We have that

the vector of 1’s in . Additionally by (3.2),

Hence

∎

Proof of Theorem 3.2.

Let be the transition rate matrix of the -Markov cubature rule . Equations (3.3) and (2.2) imply that for all , and

Hence, for all . Differentiating with respect to and evaluating at we obtain (ii).

This follows directly from Lemma 3.3.

By (3.2)

for all . On the other hand, the -th row of can be written as a cone combination of the form

| (B.2) |

where the coefficients are nonnegative. Since we conclude (iv).

Condition (iv) implies the existence of coefficients for such that (B.2) is equal to the -th row of for all . Hence, we can find a transition rate matrix such that . This implies, by an induction argument, that

This in turn implies that

| (B.3) |

Since defines a transition semigroup, we can define a Markov process with state space by

Equations (3.3) and (B.3) imply that for all and , i.e. defines a continuous time -Markov cubature rule.

Suppose now that and the matrix is invertible. For all define as the polynomial whose coordinates with respect to the basis are the -th column of . We have that is a basis that satisfies .

Proof of Lemma 5.3.

Equations (3.3), (5.1) and (5.2) imply that

where is the matrix with all columns equal to . Since has rank the set

is an open set in . Then, for large enough and defining , we have

| (B.4) |

The argument to show that the rows of add up to 1 is similar to that of Lemma 3.3. Suppose that are the coordinates of the constant polynomial with respect to the basis . We have that where is the vector of 1’s. Since is an eigenvalue of with corresponding eigenvalue 0, is an eigenvector of with eigenvalue 1. Hence, This observation together with (B.4) implies that and the rows of add up to 1, i.e. is a probability matrix. ∎

References

- Ackerer and Filipović (2016) D. Ackerer and D. Filipović. Linear credit risk models. Swiss Finance Institute Research Paper No. 16-34., 2016. Available at SSRN: http://ssrn.com/abstract=2782455.

- Ackerer et al. (2018) D. Ackerer, D. Filipović, and S. Pulido. The Jacobi stochastic volatility model. Finance and Stochastics, 22(3):667–700, 2018.

- Arasaratnam and Haykin (2009) I. Arasaratnam and S. Haykin. Cubature Kalman filters. IEEE Transactions on automatic control, 54(6):1254–1269, 2009.

- Bally et al. (2005) V. Bally, G. Pagès, and J. Printems. A quantization tree method for pricing and hedging multidimensional american options. Mathematical Finance, 15(1):119–168, 2005.

- Bayer and Teichmann (2006) C. Bayer and J. Teichmann. The proof of Tchakaloff’s theorem. Proceedings of the American Mathematical Society, 134(10):3035–3040, 2006.

- Bayer and Teichmann (2008) C. Bayer and J. Teichmann. Cubature on Wiener space in infinite dimension. Proceedings of The Royal Society of London. Series A. Mathematical, Physical and Engineering Sciences, 464(2097):2493–2516, 2008.

- Bayraktar et al. (2018) E. Bayraktar, Y. Dolinsky, and J. Guo. Recombining tree approximations for optimal stopping for diffusions. SIAM Journal on Financial Mathematics, 9(2):602–633, 2018.

- Biagini and Zhang (2016) S. Biagini and Y. Zhang. Polynomial diffusion models for life insurance liabilities. Insurance Mathematics and Economics, 71:114–129, 2016.

- Billingsley (1995) P. Billingsley. Probability and Measure. Wiley Series in Probability and Statistics. Wiley, 1995.

- Callegaro et al. (2017) G. Callegaro, L. Fiorin, and A. Pallavicini. Quantization goes polynomial. arXiv:1710.11435, 2017.

- Chaudru de Raynal and Garcia Trillos (2015) P.E. Chaudru de Raynal and C.A. Garcia Trillos. A cubature based algorithm to solve decoupled McKean–Vlasov forward–backward stochastic differential equations. Stochastic Processes and their Applications, 125(6):2206–2255, 2015.

- Cox et al. (1979) John C. Cox, Stephen A. Ross, and Mark Rubinstein. Option pricing: A simplified approach. Journal of Financial Economics, 7(3):229 – 263, 1979. ISSN 0304-405X. doi: https://doi.org/10.1016/0304-405X(79)90015-1. URL http://www.sciencedirect.com/science/article/pii/0304405X79900151.

- Crisan and Manolarakis (2012) D. Crisan and K. Manolarakis. Solving backward stochastic differential equations using the cubature method: application to nonlinear pricing. SIAM Journal on Financial Mathematics, 3(1):534–571, 2012.

- Crisan and Manolarakis (2014) D. Crisan and K. Manolarakis. Second order discretization of backward SDEs and simulation with the cubature method. The Annals of Applied Probability, 24(2):652–678, 2014.

- Cuchiero (2019) C. Cuchiero. Polynomial processes in stochastic portfolio theory. Stochastic Processes and their Applications, 129(5):1829–1872, 2019.

- Cuchiero et al. (2012) C. Cuchiero, M. Keller-Ressel, and J. Teichmann. Polynomial processes and their applications to mathematical finance. Finance and Stochastics, 16:711–740, 2012.

- De Jong et al. (2001) F. De Jong, F. C. Drost, and B. J. M. Werker. A jump-diffusion model for exchange rates in a target zone. Statistica Neerlandica, 55(3):270–300, 2001.

- Delbaen and Shirakawa (2002) F. Delbaen and H. Shirakawa. An interest rate model with upper and lower bounds. Asia-Pacific Financial Markets, 9:191–209, 2002.

- Doersek et al. (2013) P. Doersek, J. Teichmann, and D. Velušček. Cubature methods for stochastic (partial) differential equations in weighted spaces. Stochastic Partial Differential Equations: Analysis and Computations, 1(4):634–663, 2013.

- Filipović and Larsson (2016) D. Filipović and M. Larsson. Polynomial diffusions and applications in finance. Finance and Stochastics, 20(4):931–972, 2016.

- Filipović and Larsson (2017) D. Filipović and M. Larsson. Polynomial jump-diffusion models. arXiv:1711.08043, 2017.

- Filipović et al. (2016) D. Filipović, E. Gourier, and L. Mancini. Quadratic variance swap models. Journal of Financial Economics, 119(1):44–68, 2016.

- Filipović et al. (2017) D. Filipović, M. Larsson, and A. Trolle. Linear-rational term structure models. Journal of Finance, 72(2):655–704, 2017.

- Filipović et al. (2018) D. Filipović, M. Larsson, and T. Ware. Polynomial processes for power prices. arXiv:1710.10293, 2018.

- Gruber and Schweizer (2006) U. Gruber and M. Schweizer. A diffusion limit for generalized correlated random walks. Journal of applied probability, 43(1):60–73, 2006.

- Karatzas and Shreve (1991) I. Karatzas and S.E. Shreve. Brownian Motion and Stochastic Calculus. Graduate Texts in Mathematics. Springer New York, 1991.

- Kifer (2006) Y. Kifer. Error estimates for binomial approximations of game options. The Annals of Applied Probability, 16(2):984–1033, 2006.

- Kushner and Dupuis (2013) H. Kushner and P.G. Dupuis. Numerical Methods for Stochastic Control Problems in Continuous Time. Stochastic Modelling and Applied Probability. Springer New York, 2013.

- Kushner (1984) H.J. Kushner. Approximation and Weak Convergence Methods for Random Processes With Applications to Stochastic Systems Theory. Signal Processing, Optimization, and Control. MIT Press, 1984.

- Larsen and Sørensen (2007) K. S. Larsen and M. Sørensen. Diffusion models for exchange rates in a target zone. Mathematical Finance, 17(2):285–306, 2007.

- Lee and Lyons (2015) W. Lee and T. Lyons. The adaptive patched particle filter and its implementation. arXiv:1509.04239, 2015.

- Longstaff and Schwartz (2001) F. A. Longstaff and E. S. Schwartz. Valuing american options by simulation: A simple least-squares approach. Review of Financial Studies, pages 113–147, 2001.

- Lyons and Victoir (2004) T. Lyons and N. Victoir. Cubature on Wiener space. Proceedings: Mathematical, Physical and Engineering Sciences, 460(2041):169–198, 2004.

- Putinar (1997) M. Putinar. A note on Tchakaloff’s theorem. Proceedings of the American Mathematical Society, 125(8):2409–2414, 1997.

- Teichmann (2006) J. Teichmann. Calculating the Greeks by cubature formulae. Proceedings of The Royal Society of London. Series A. Mathematical, Physical and Engineering Sciences, 462(2066):647–670, 2006.

- Zhou (2003) H. Zhou. Itô conditional moment generator and the estimation of short-rate processes. Journal of Financial Econometrics, 1:250–271, 2003.

| Rel. diff. | |||

|---|---|---|---|

| 80 | 21.6180 | 21.6059 | 0.0006 |

| 85 | 18.0206 | 18.0374 | 0.0009 |

| 90 | 14.9271 | 14.9187 | 0.0006 |

| 95 | 12.2445 | 12.2314 | 0.0011 |

| 100 | 9.9539 | 9.9458 | 0.0008 |

| 105 | 8.0282 | 8.0281 | 0.0000 |

| 110 | 6.4324 | 6.4352 | 0.0004 |

| 115 | 5.1267 | 5.1265 | 0.0000 |

| 120 | 4.0697 | 4.0611 | 0.0021 |

| Rel. diff. | |||

|---|---|---|---|

| 0.1 | 0.5436 | 0.5434 | 0.0003 |

| 0.2 | 0.4273 | 0.4286 | 0.0030 |

| 0.3 | 0.3251 | 0.3265 | 0.0043 |

| 0.4 | 0.2468 | 0.2478 | 0.0041 |

| 0.5 | 0.1839 | 0.1852 | 0.0069 |

| 0.6 | 0.1327 | 0.1339 | 0.0087 |

| 0.7 | 0.0912 | 0.0924 | 0.0132 |

| 0.8 | 0.0580 | 0.0590 | 0.0172 |

| 0.9 | 0.0323 | 0.0329 | 0.0196 |