Testing Forecast Accuracy of Expectiles and Quantiles with the Extremal Consistent Loss Functions††thanks: We thank seminar participants in 2016 macroeconometric modelling workshop (Academia Sinica), the 1st International Conference on Econometrics and Statistics (HKUST), 2017 European meeting of the Econometric society (University of Lisbon), 10th Annual Meeting of Taiwan Econometric Society, 2018 IAAE Annual Conference (UQAM), CRETA workshop (National Taiwan University) and National Chengchi University for helpful comments.

Abstract

Forecast evaluations aim to choose an accurate forecast for making decisions by using loss functions. However, different loss functions often generate different ranking results for forecasts, which complicates the task of comparisons. In this paper, we develop statistical tests for comparing performances of forecasting expectiles and quantiles of a random variable under consistent loss functions. The test statistics are constructed with the extremal consistent loss functions of Ehm

et al. (2016). The null hypothesis of the tests is that a benchmark forecast at least performs equally well as a competing one under all extremal consistent loss functions. It can be shown that if such a null holds, the benchmark will also perform at least equally well as the competitor under all consistent loss functions. Thus under the null, when different consistent loss functions are used, the result that the competitor does not outperform the benchmark will not be altered. We establish asymptotic properties of the proposed test statistics and propose to use the re-centered bootstrap to construct their empirical distributions. Through simulations, we show the proposed test statistics perform reasonably well. We then apply the proposed method on (1) re-examining abilities of some often-used predictors on forecasting risk premium of the S&P500 index; (2) comparing performances of experts’ forecasts on annual growth of U.S. real gross domestic product; (3) evaluating performances of estimated daily value at risk of the S&P500 index.

KEYWORDS: Consistent loss function, Expectile, Extremal consistent loss function, Quantile

JEL codes: C12, C53, E17.

AMS 2010 Classifications: 62G10, 62M20, 62P20.

1 Introduction

When evaluating performances of a benchmark and a competing forecasts for a target functional of a random variable (e.g., conditional expectation), typically we can compare expected values of a loss function (e.g., the squared error loss) evaluated with the two forecasts and the random variable. We say that the competitor outperforms the benchmark under a loss function if the expected value of the loss function for the former is lower than that for the latter. There are many loss functions can be chosen for comparing forecast performances. Such choices may reflect forecast users’ concerns on cost of wrong forecasts in the future (Granger, 1969; Granger and Newbold, 1986). For example, when controlling downside risk of purchasing an asset, one may focus on negative forecast errors111We follow the convention to define a forecast error as realization of the random variable minus the forecast. of the asset’s conditional expected return rather than their positive counterparts. In this situation, it would be suitable to choose a loss function that penalizes more on the negative forecast errors.

An important guideline for choosing a loss function for evaluating forecasts is that the loss function should be consistent (Gneiting, 2011; Patton, 2015). If the target functional can be obtained by minimizing expectation of a certain loss function, then we say the loss function is a consistent loss function for the target functional. If a target functional is the only one minimizer of the expectation of a consistent loss function, then this target functional is called an elicitable target functional and the loss function is called strictly consistent (for the elicitable target functional).

The criterion of consistency reduces the set of loss functions for comparing forecast performances. However, for an elicitable target functional, there may still exist infinitely many corresponding consistent loss functions. Patton (2015) shows that using different consistent loss functions may yield different ranking results for two forecasts, unless (1) they are issued by using correctly specified models, and (2) the information used for generating one forecast is a subset of that used for generating the other. However, conditions (1), (2) or both often do not hold in practice. If either condition (1) or (2) is violated, or estimated forecast models have estimation errors, then using different consistent loss functions may yield different ranking results, which complicates the task of evaluating forecast performances.

In this paper we develop statistical tests for comparing performances of forecasting expectiles and quantiles of a random variable under consistent loss functions. The proposed tests can alleviate the aforementioned difficulty when different consistent loss functions are used on evaluating forecast performances. The test statistics are constructed by using the extremal consistent loss functions of Ehm et al. (2016). The null hypothesis of the tests is that a benchmark forecast at least performs equally well as a competing one under all extremal consistent loss functions. It can be shown that if such a null holds, the benchmark will also at least performs equally well as the competitor under all consistent loss functions, regardless whether the aforementioned conditions (1) or (2) holds or not. Thus under the null hypothesis, using different consistent loss functions will not alter the result that the competitor does not outperform the benchmark. On contrary, if this null hypothesis is rejected, we may see that the competitor outperforms the benchmark under certain consistent loss functions.

The proposed tests may be suitable as a first-step check when the consistent loss function used to generate the competing forecast is unknown, such as that from a survey. In this situation, sometimes it is hard to fairly judge whether one forecast outperforms the other under a chosen consistent loss function. With the proposed test, the forecasts will have a fair chance to demonstrate their ability regardless which consistent loss function is used, since the proposed test verifies whether one forecast outperforms the other over all possible consistent loss functions.

Ehm et al. (2016) use the extremal consistent loss functions to graphically compare performances of two forecasts for the expectiles and quantiles. They term such a graph as a Murphy diagram. While the Murphy diagram is a useful tool, it only provides graphical evidence of the performance differences but gives no formal statistical justification. Our proposed tests can be viewed as formal statistical tests for testing such performance differences uniformly. In addition, our proposed tests are not like traditional forecast accuracy tests, such as the Diebold-Marino test (Diebold and Mariano, 1995), which use only one consistent loss function at a time. Rather our proposed tests seek to detect the performance differences between two forecasts over infinitely many possible consistent loss functions, which may be particularly important when the loss function used to generate the competing forecast is unknown.

We establish theoretical properties of the proposed test statistics under some mild conditions. West (1996) shows that if a loss function has some regular properties, it can be consistently estimated and the estimate is asymptotically normally distributed. However, the extremal consistent loss functions do not possess all the regular properties mentioned in West (1996). In addition, the proposed test statistics have a form of Kolmogorov-Smirnov type. Thus analyzing theoretical properties of our proposed test statistics relies on using non-traditional techniques. We show that the test statistics have a non-degenerate asymptotic distribution related to a mean zero Gaussian process. To efficiently conduct the tests, we propose to use the re-centered bootstrap to construct empirical distributions of the test statistics. We then show validity of the bootstrap scheme by proving empirical distributions of the re-centered bootstrap test statistics converge to distributions of the re-centered sample test statistics.

We next conduct intensive simulations to understand how the proposed test statistics perform with finite samples. In the first simulation, we design a situation in which two forecasts for a conditional expectation perform equally well under the square error loss but differently under the exponential Bregman loss. In this situation, if we use the Diebold Marino test statistic with the squared error loss, we have a low probability to reject the null and it is unlikely to identify which forecast performs better than the other under the exponential Bregman loss. However, our proposed test statistic has a high probability to correctly detect such performance differences in this case. We further show that the proposed test statistics with the re-centered bootstrap work well in more realistic situations.

We apply the proposed tests on three empirical studies. We first re-examine abilities of some often-used predictors on forecasting risk premium of the S&P500 index. We find that evidence for these predictors outperforming historical average of excess returns is weak. We also compare performances of experts’ forecasts on annual growth of U.S. real gross domestic product (RGDP) and find that the mean forecast of experts performs better than or at least equally well as an individual forecast. Finally, we evaluate different models’ performances of forecasting daily value at risk (VaR) of the S&P500 index and find that the CAViaR type models (Engle and Manganelli, 2004) performs better than or at least equally well as the other two simple methods. All these empirical results are robust to choices of different consistent loss functions.

Loss functions can be functions of forecast errors and other parameters. Such loss functions, together with some mild restrictions, are called the generalized loss functions (Granger, 1969, 1999) and some relevant important results were derived, see Elliott et al. (2005), Diebold and Shin (2015) and Jin et al. (2016). The class of the generalized loss functions nests some (but not all) consistent loss functions of forecasting the expectiles and quantiles as special cases, for example, the squared error loss and lin-lin (tick) loss. But some loss functions belonging to the class are not consistent loss functions for the expectiles and quantiles forecasts, for example, linex loss function of Varian (1975) and double exponential loss function of Granger (1999). Thus our proposed tests may be a complementary to forecast accuracy tests based on such a class of loss functions.

Recently Ehm and Krüger (2017) also propose tests to compare forecasts on the expectiles and quantiles based on the extremal consistent loss functions of Ehm et al. (2016). Our proposed method has several differences from theirs. First, empirical p-values of their test statistics are constructed by sign randomization and consequently have different theoretical and empirical properties than those of ours. More importantly, they test hypotheses of conditional performances of the forecasts, but our hypotheses focus on the unconditional performances.

The rest of the paper is organized as follows. In Section 2 we review concepts of consistent loss functions and the extremal consistent loss functions of Ehm et al. (2016). In Section 3 we introduce the proposed tests and establish their theoretical properties, and illustrate how to use the re-centered bootstrap to construct their empirical distributions for statistical inferences. In Section 4 we conduct simulation studies for examining performances of the test statistics in various situations. In Section 5 we use the proposed tests on the three empirical applications. Section 6 is for conclusions.

2 Consistent loss functions for point forecasts

Let denote a loss function for evaluating a forecast for a target functional of a random variable. Following convention, we let the first argument of be the forecast and the second argument be the random variable. For all pairs , assume and if , . Let denote a class of probability functions on a closed subset and be an element in . Let denote a statistical functional which maps to . The loss function is consistent for a statistical functional if for all , and a random variable and . The loss function is strictly consistent for the functional if

| (1) |

and implies . If is a strictly consistent loss function and satisfies (1), then is called elicitable.

2.1 Consistent loss functions for expectiles and quantiles

The functionals we are interested in this paper are conditional expectiles and conditional quantiles.222We use the term “conditional” here since in forecast, the amount of information we can use is only up to current period and is not unlimited. Thus is a distribution conditioning on a limited amount of information and is a conditional statistical functional.The expectile of a random variable at level , called the expectile of , can be obtained by solving in the following equation

When , it is easy to see that is expectation of under the distribution function , . Savage (1971) shows that a consistent loss function for an expectation of a random variable, denoted by , can be expressed as the following Bregman type function

| (2) |

where is a convex function and is its subgradient. The consistent loss function in (2) nests some frequently used loss functions as special cases. With different specifications of in (2), we list examples of in Table 1, which include the squared error loss and the QLIKE loss (Patton, 2011). Another interesting case in Table 1 is when for , and this kind of consistent loss function is associated with the negative log likelihood for the logistic regression estimation.

For the expectile of a random variable, Gneiting (2011) shows that the corresponding consistent loss function, denoted by , can be expressed as

| (3) | |||||

Combining with different forms of in Table 1, we can obtain various loss functions for the expectile forecasts. For example, if we set , becomes the asymmetric squared error loss for estimating the expectile regression of Newey and Powell (1987). The expectile regression can be applied to forecast the expectile-based Value at Risk (EVaR), which measures the relative cost of the expected margin shortfall. Kuan et al. (2009) show that the EVaR is a useful alternative risk measurement for extreme loss to the quantile based VaR.

The quantile of a random variable , denoted by , is defined as

| (4) |

where is the probability of . If the distribution function is strictly monotonically increasing and continuous, then . Quantile forecasts are important in risk managements. For example, the value at risk (VaR) are often constructed by using conditional quantile forecasts of an asset’s return.

Let , where is a nondecreasing function. Thomson (1979) and Saerens (2000) show that a consistent loss function for the quantile of a random variable, denoted by , can be expressed as

| (5) | |||||

The right hand side of (5) is the generalized piecewise linear (GPL) function of order . Several examples of are listed in Table 2. When , is the lin-lin or asymmetric piecewise linear loss function, which can be used to estimate the quantile regression (Koenker and Bassett, 1978). Another interesting case of is the scaled lin-lin loss by setting (Holzmann and Eulert, 2014). When is a continuous random variable, Holzmann and Eulert (2014) show that under distribution , the expected scaled lin-lin loss with is

| (6) |

The second term of right hand side of (6) is the expected shortfall of . Thus equation (6) provides a way to estimate the expected shortfall by subtracting the minimized expected scaled lin-lin loss from the expectation of .

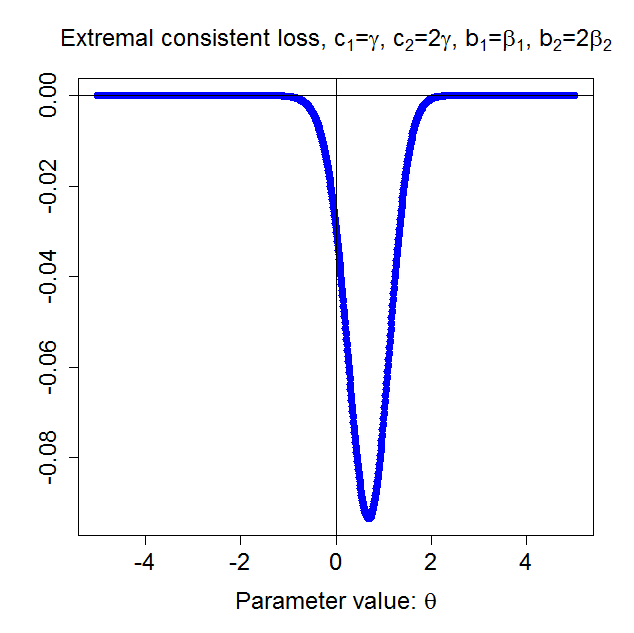

2.2 Extremal consistent loss functions

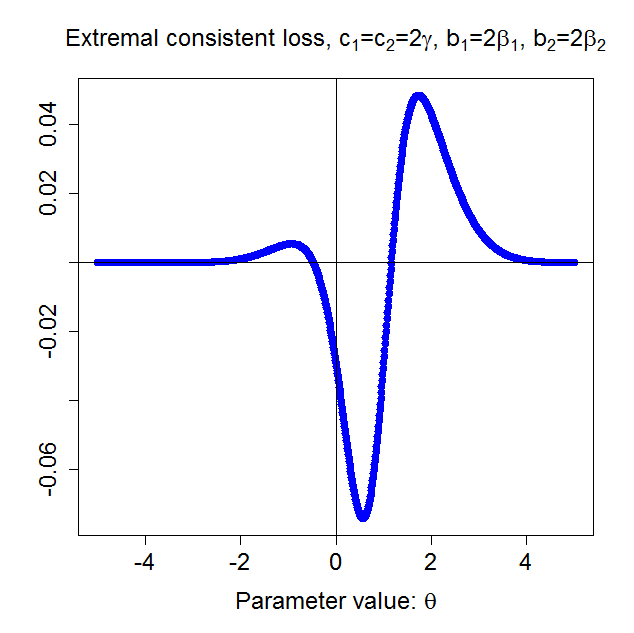

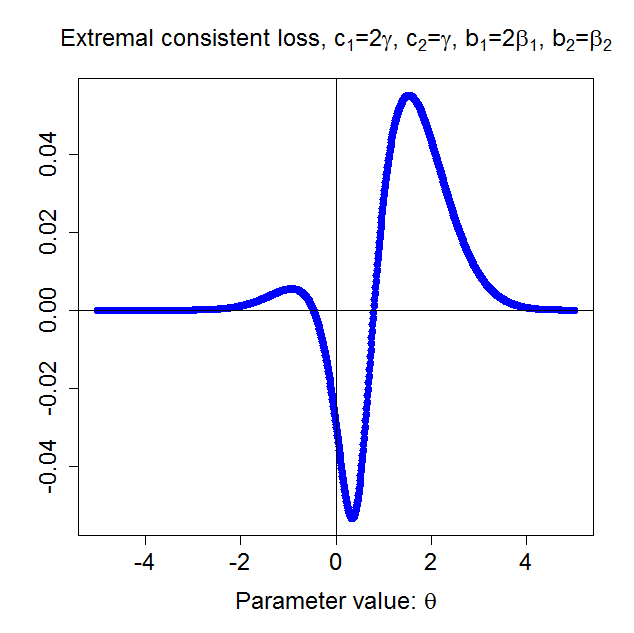

In this subsection we introduce the extremal consistent loss functions of Ehm et al. (2016) for the expectile and quantile of a random variable. Let denote the class of consistent loss functions for the expectile which admits the form of (3). Ehm et al. (2016) show that every consistent loss function can be represented as

| (7) |

where is the extremal consistent loss function for the expectile, which is given by

| (8) |

It can be shown that . It is also easy to see that if we set in (3). The representation of (7) states that every consistent loss function for the expectile is a weighted sum of the extremal consistent loss function . The representation of (7) is a Choquet-type mixture representation in functional analysis (Ehm et al., 2016), in which is a unique non-negative mixing measure which satisfies for , where is the left-hand derivative of the convex function in (3) and is a bounded subset of . Also for , where denotes the left-hand derivative with respect to .

For the quantile, let denote the class of consistent loss functions for the quantile which admits the form of (5). Like the case of , Ehm et al. (2016) show that every consistent loss function also has a Choquet-type mixture representation

| (9) |

where is the extremal consistent loss function for the quantile, which is given by

| (10) |

It can be shown that . It also easy to see that since it is the consistent loss function when in (5). In (9), is a unique non-negative mixing measure which satisfies for , where is the nondecreasing function in (5) and is a bounded subset of . Also for .

2.3 Accuracy of the representations

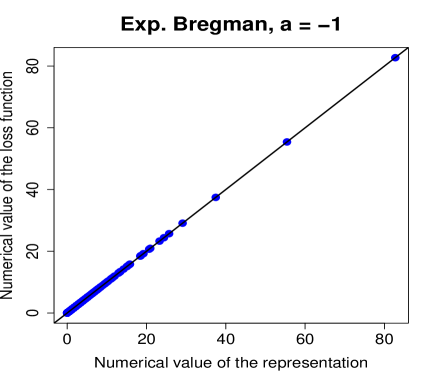

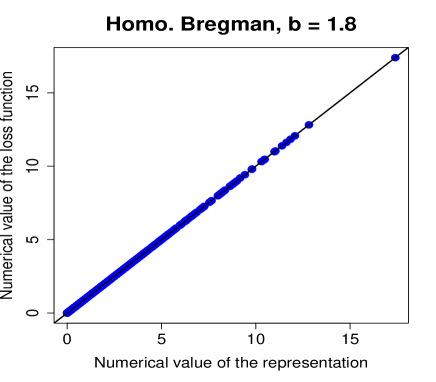

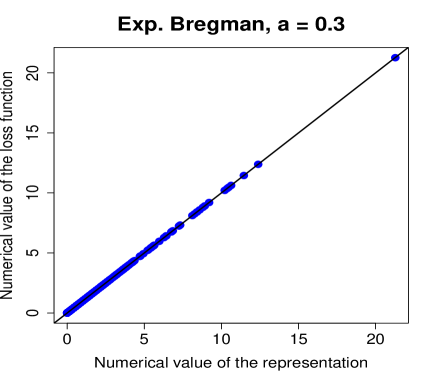

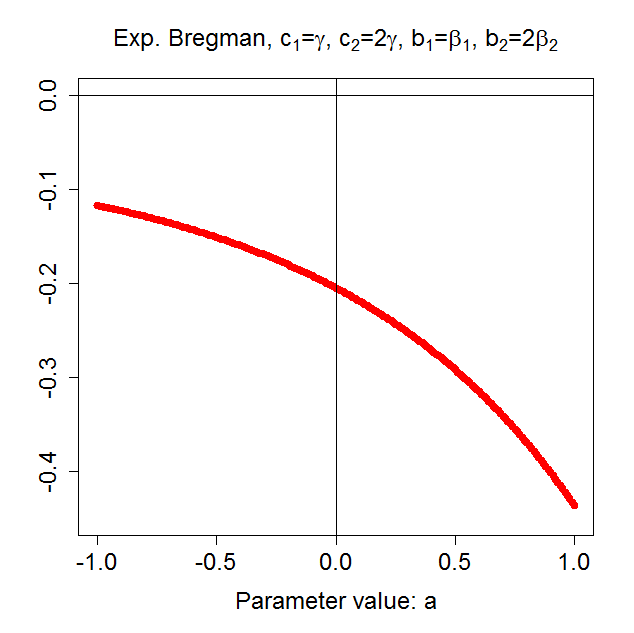

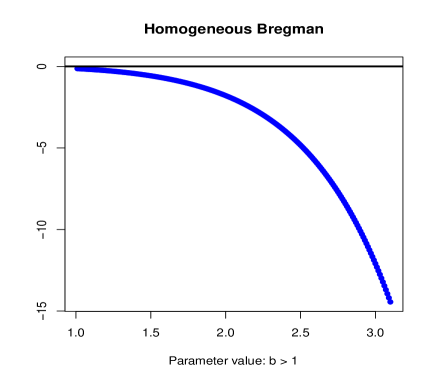

The representations (7) and (9) can be used to numerically approximate the consistent loss functions for the expectile and quantile forecasts. An accurate approximation from the representation is crucial for constructing the proposed test statistic. In this subsection we compare numerical values of several consistent loss functions with those obtained from using the representations of (7) and (9). For the expectile, we choose the exponential (non-homogeneous) Bregman loss and the homogeneous Bregman loss for the comparisons. For the former, and for the latter, , where is the Dirac function. For the quantile, we choose the lin-lin loss and the homogeneous (power) loss with order for the comparisons. For the former, and for the latter, .

Let denote the normal distribution with mean and variance and denote the chi-square distribution with degree of freedom . For the expectile, the simulated data for each comparison are 1000 pairs of and . For the quantile, in the case of the lin-lin loss, the simulated data for each comparison are 1000 pairs of and . In the case of the homogeneous loss with order , the data for each comparison are 1000 pairs of and .

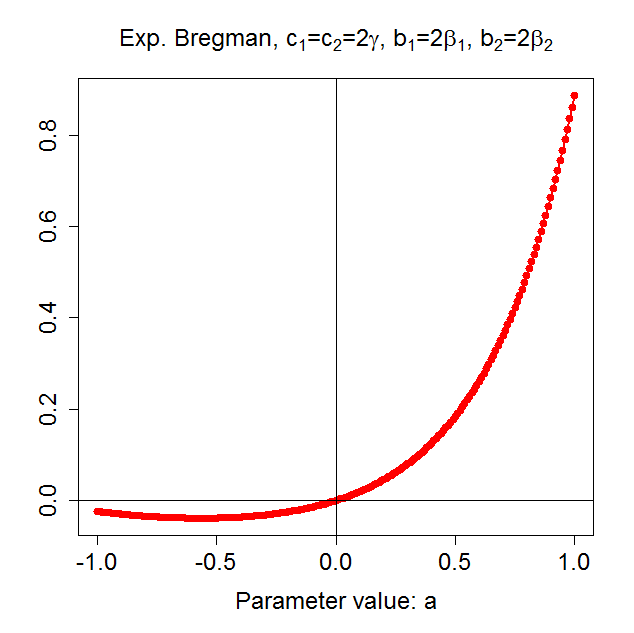

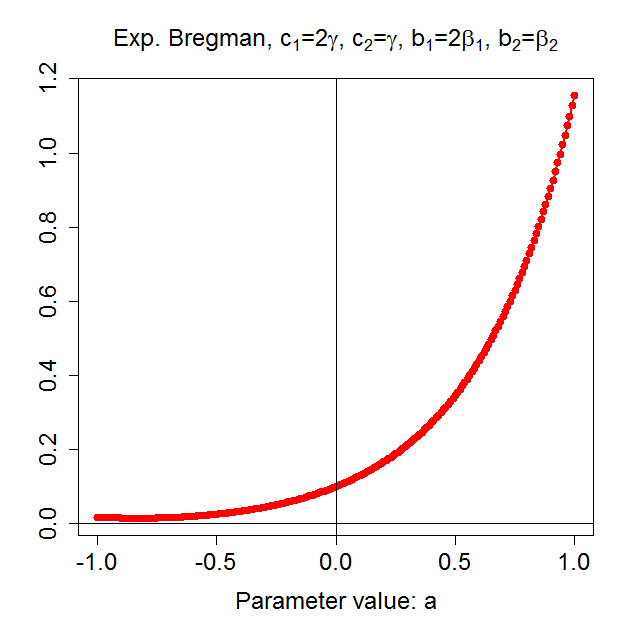

With pairs , we numerically evaluate integrals of (7) and (9) with the Trapezoid method. We then compare the numerical integrals with the corresponding consistent loss functions directly calculated with pairs . In Figure 1, left panel shows comparison results for the exponential Bregman loss with , , 0.3 and 1. Right panel shows those for the homogeneous Bregman loss with , , 2 and 3. In Figure 2, left panel shows the comparison results for the lin-lin loss and right panel shows those for the homogeneous loss with , 0.05 and 0.5. The solid line in each plot is a 45 degree line. From each figure, it can be seen that all pairs of value of the consistent loss function and that obtained from using the representation of (7) (or (9)) almost lie on the 45 degree line, which suggests that the two are virtually identical and the representation of (7) (or (9)) works well on approximating the corresponding consistent loss function.

3 Forecast accuracy tests with the extremal consistent loss functions

In this section we introduce the proposed tests and test statistics for comparing forecast accuracy of the expectile or quantile under all consistent loss functions. Let be a benchmark and be a competing forecasts for the expectile or the quantile of a random variable . For forecasting the expetile, under a consistent loss function , we say that at least performs equally well as if

| (11) |

With the representation of (7), (11) can be expressed as

| (12) |

Since for every , is nonnegative for all and the functional form of the extremal consistent loss is independent of , a sufficient condition for at least performing equally well as as the expectile forecast under all is that holds for all . Thus given , to see whether such a sufficient condition holds, we may test the following null hypothesis

| (13) |

If the null of (13) is rejected, it indicates that for forecasting the expectile, there is evidence that is not outperformed by under all , or may outperform at least when a certain is used in the forecast evaluation.333To see this, let . If , the null of (13) is violated. In this case, outperforms under the extremal consistent loss where . Note that itself is also a consistent loss function for forecasting the expectile. The same argument can be applied to the case of evaluating the quantile forecasts. On contrary, if the null is not rejected, there is evidence that for forecasting the expectile, performs equally well as or better than under all .

Similarly, for comparing forecasts for the quantile under all consistent loss functions, by using the representation of (9) and the arguments that is nonnegative for all and the functional form of the extremal consistent loss is independent of , we may formulate the following null hypothesis

| (14) |

If the null of (14) is rejected, there is evidence that may outperform for forecasting the quantile, at least when a certain is used in the forecast evaluation. If the null is not rejected, there is evidence that for forecasting the quantile, at least can perform no worse than over a class of consistent loss functions belonging to .

3.1 The test statistics

In the following we introduce procedures for testing the nulls of (13) and (14). We consider -period ahead out-of sample (OoS) forecasts of the expectile or quantile of a random variable at each period . Suppose total length of samples available for the forecast evaluation is . Let denote the length of samples used to generate the forecasts (such as length of samples used in estimating a model). Let denote the number of generated forecasts and so . Let and denote the benchmark and competing forecasts for the expectile or the quantile of at period , . To ease the notations, we let and . Let , where . The null hypotheses of (13) or (14) is equivalent to

| (15) |

if we replace with . Let . We can calculate a sample analogue of as

| (16) |

If with some assumptions, , then we may use the following test statistic

| (17) |

to test the null of (15). Here is the union of supports of , and . To find the suprema in , we may take the maxima over a grid of points in the joint supports of , and , for example, all sample points of , and . In practice, to save time of computations, we may calculate approximations to the suprema based on a smaller subset of the points. As the evaluation points increase in the joint supports, the theoretical properties for the test statistics will not be affected by using such approximations (Linton et al., 2005).

3.2 Properties of the test statistics

In the following, we provide asymptotic results for the proposed test statistics of (17). We consider a more general version of the null of (15) in which is replaced by , , . In the more generalized situation, we have generated forecasts and the th forecast is the benchmark and the other forecasts are the competitors. Let

| (18) |

where is for the expectile and quantile forecasts and is non-empty. By assuming that is strictly stationary, it can be shown that

where

| (19) |

for , and . With these notations, we may rewrite a more generalized version of the nulls of (15) as

| (20) |

for .

If the null of (20) is not true, the term as for some . If the null of (20) is true, there exists at least a pair such that for all . Now suppose that under the null of (20), with the pair , for all but for some . This implies that . Let . Under some suitable conditions, with the central limit theorem of an empirical process, it can be shown that the centered process will converge weakly to a mean zero Gaussian process indexed by , say . Since for , but for , as and as . But will approximately equal to . Thus the asymptotic distribution of is determined by , which will weakly converge to under some suitable conditions. On contrary, if with the pair , for all , which implies that is empty, then

as .

We now state relevant assumptions and a formal theorem for the properties of the test statistic as follows. Let and and denote weak convergence of stochastic processes.

Assumption 1

For , is strictly stationary and satisfies strong mixing condition. The mixing coefficients satisfy , where , , and are some constants.

Assumption 2

The forecast error should satisfy

where is the constant satisfying the conditions in Assumption 1.

Assumption 3

For and , the marginal density functions of and , denoted by and , are bounded with respect to Lebesgue measure a.s.

Assumption 1 requires that the generated forecasts and random variable should satisfy a mixing condition. This kind of requirement for time series data is commonly seen in proving consistency results which rely on using property of stochastic equicontinuity of an empirical process (e.g., Hansen (1996a), Jin et al. (2016), Linton et al. (2005), Linton et al. (2016)). Assumption 2 requires the forecast error should satisfy a certain moment condition and Assumption 3 states density functions of the generated forecasts and random variable should be bounded from above. There is a trade-off between the moment condition of Assumption 2 and restriction on the constant in Assumption 1. In our case, we need all the three assumptions to construct the stochastic equicontinuity of the empirical process for in (19), which is indexed by the parameter . With the results of the stochastic equicontinuity, some other useful statistical convergence results can be established. Please see Lemma 1 to 3 and their proofs in Appendix 7.1.

Theorem 1

Suppose Assumptions 1 to 3 hold. Then under the null of (20), the test statistic

for , where is a mean zero Gaussian process with covariance defined in Lemma 3, and and

A detailed proof of Theorem 1 can be found in Appendix 7.1. The theorem says that the sample test statistic of (18) has a non-degenerate asymptotic distribution associated with , which can be used to construct empirical -values. In next subsection we will introduce the method for empirically constructing the distribution of the sample test statistic .

3.3 Constructing empirical distributions of the test statistics

We use the re-centered bootstrap (Linton et al., 2005) to construct the empirical distribution of the sample test statistic , where is for the expectile or quantile forecast. In the following we briefly describe procedures for implementing the re-centered bootstrap. We focus on the case of comparing two forecasts and . Let

where and is the bootstrap sample randomly drawn with replacement from the empirical (joint) distribution of by using a bootstrap re-sampling scheme, e.g., the stationary bootstrap of Politis and Romano (1994). Let which is an analogue of in (16) calculated with the bootstrap sample. Let . Here denotes the expectation relative to the distribution of bootstrap sample conditional on the original sample Practically, we may replace with , the test statistic calculated with the full sample. Let denote the re-centered bootstrap sample test statistic. We then compute the bootstrap distribution of as and use it to construct the critical value and empirical p-value for the test. Here is the size of the bootstrap sample. Let denote ()th sample quantile of : which is the re-centered bootstrap critical value of significance level . We reject the null hypothesis at the significance level if , .

Let , . Let be the reciprocal of mean block length for the stationary bootstrap of Politis and Romano (1994), which is a function of . With the notations used in Subsection 3.2, the theoretical result for validation of using the re-centered bootstrap method with the stationary bootstrap scheme are stated as follows.

Theorem 2

Suppose Assumptions 1 and 2 hold and and as . Then for , we have

as . Furthermore, as and ,

-

1.

if

(21) holds, we have and .

-

2.

if , we have .

As pointed out by Linton et al. (2005), to suitably approximate the distribution of the test statistic under the null, using the re-centered bootstrap method (or other re-centered re-sampling methods) requires (21) holds. The implicit constraint of (21) is a least favorable configuration for the test, which is a special case of and the null . But note that does not imply the favorable configuration. When (21) holds, using the re-centered bootstrap method would yield an exact asymptotic size of the test statistic. But when it fails to hold, in general the exact asymptotic size of the test statistic would not be obtained by using the re-centered bootstrap method. To sum, the re-centered bootstrap sample test statistic is not asymptotically similar on the boundary of the null. When an alternative is too close to the null, in general, a non-asymptotic similar test statistic may be less powerful for it than an asymptotic similar test statistic. However, previous studies show that the re-centered bootstrap method performs at least equally well as other re-sampling methods, either in simulations or empirical applications, see Linton et al. (2005) and Jin et al. (2016). This is the main reason why we suggest to use the re-centered bootstrap method to conduct the proposed tests.444In an early work, we also used subsampling method suggested by Linton et al. (2005) to conduct the proposed tests but found in most situations it performs worse than the re-centered bootstrap method. The relevant results of using the subsampling scheme can be requested. We will use the re-centered bootstrap method in the following simulations and empirical analyses.

4 Simulations

In this section, we conduct simulations to understand how the proposed test statistics perform. In the first simulation in Section 4.1.1, we investigate how the proposed test statistic works when different consistent loss functions provide different ranking results for two forecasts on the conditional expectation. In the rest simulations, models E1 to E3 are for the conditional expectile forecasts and models Q1 and Q2 are for the conditional quantile forecasts. We use these models to examine how the proposed test statistics perform under different data generating processes.

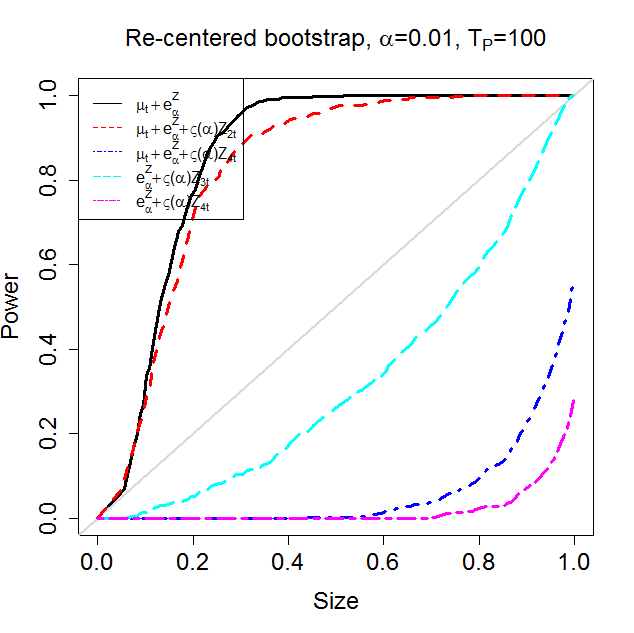

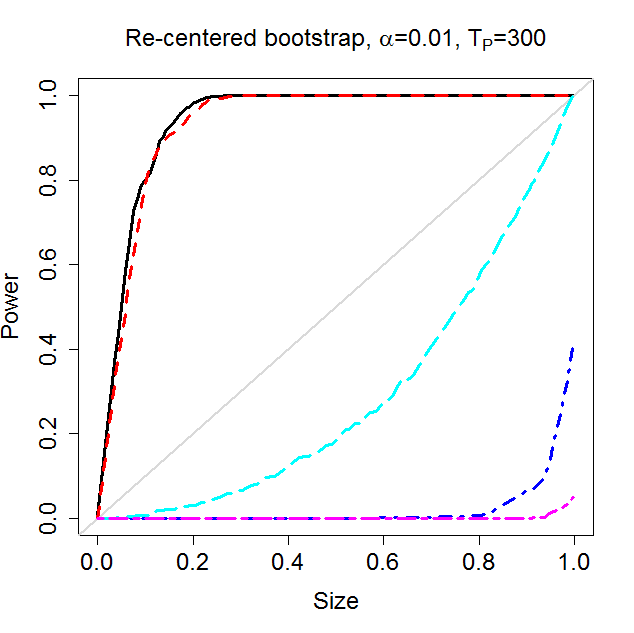

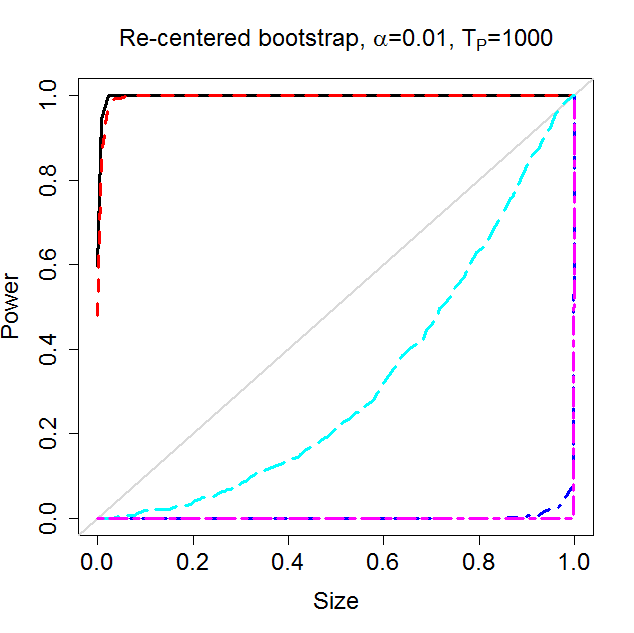

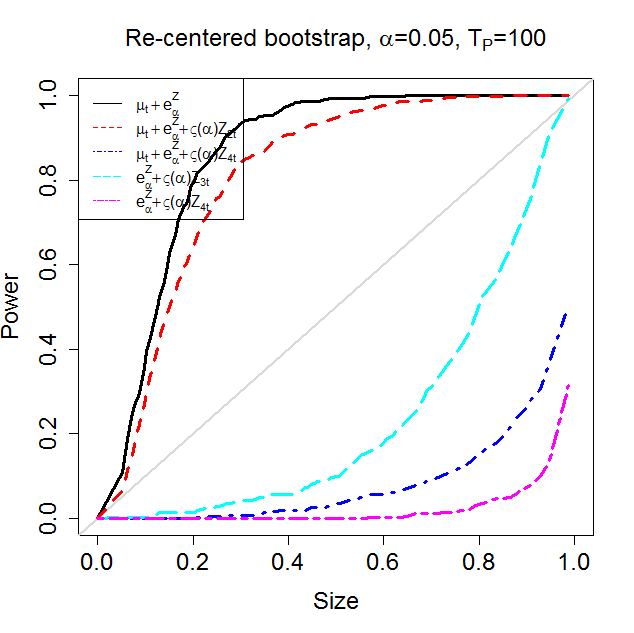

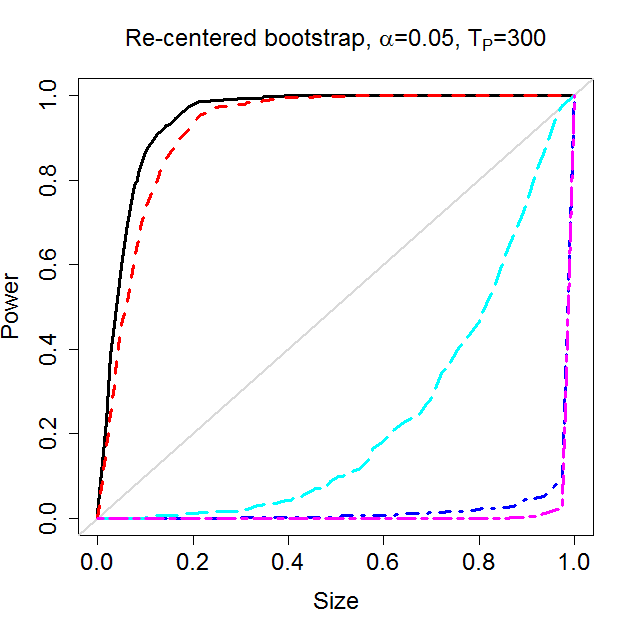

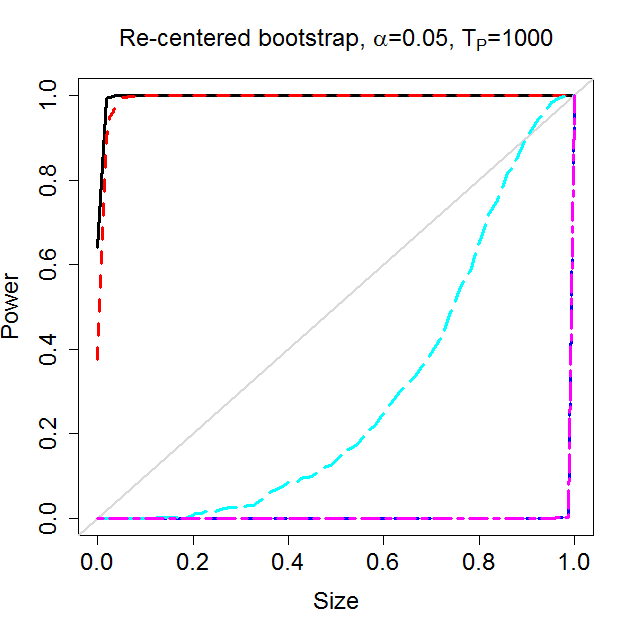

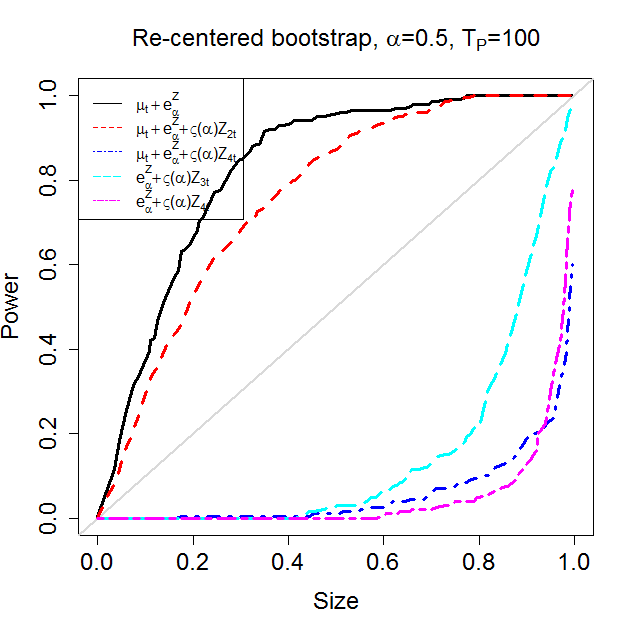

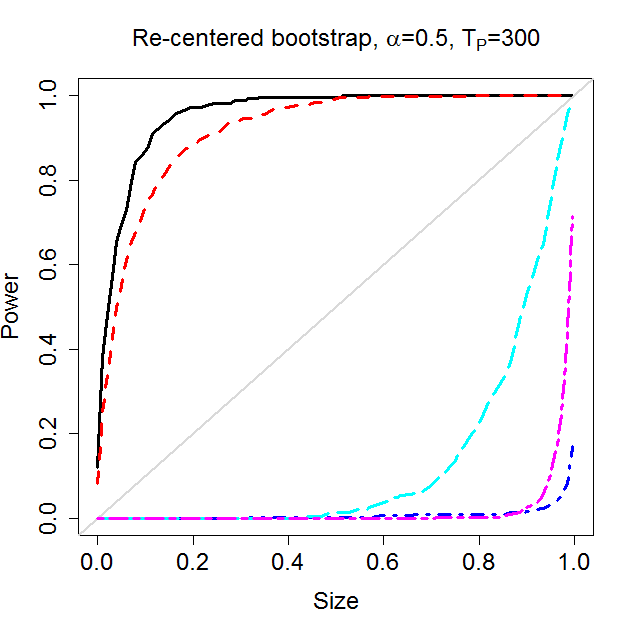

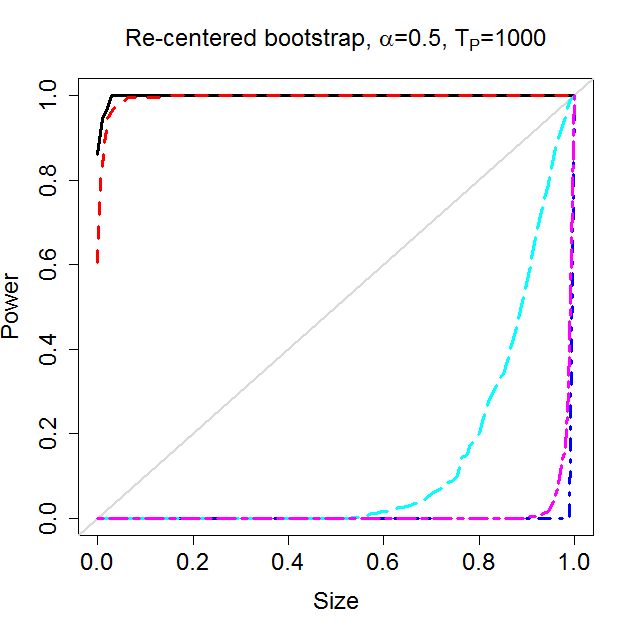

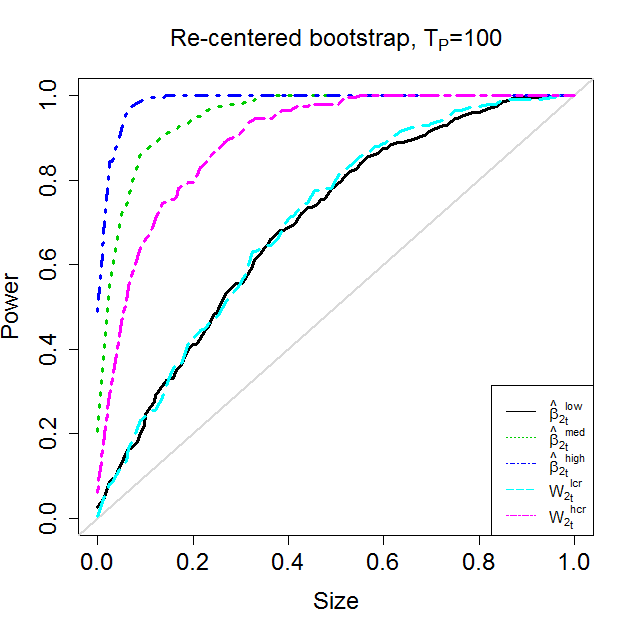

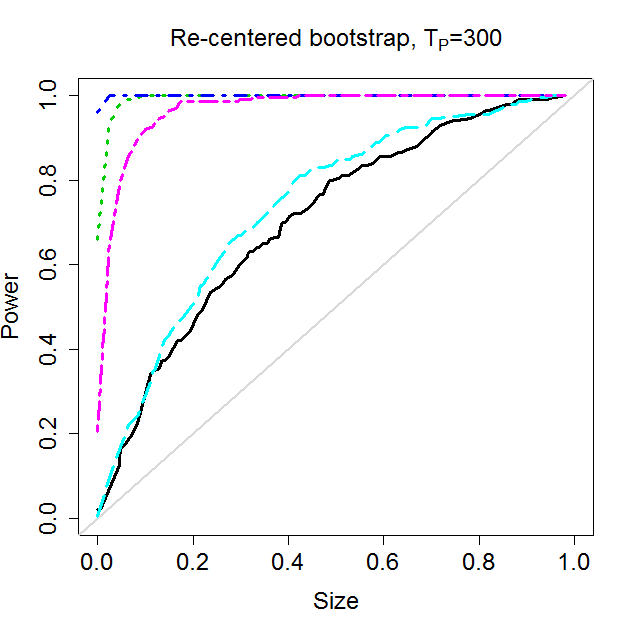

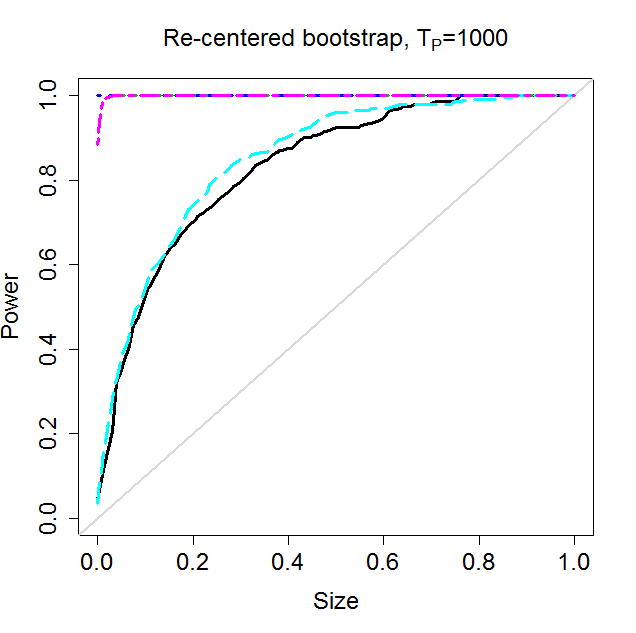

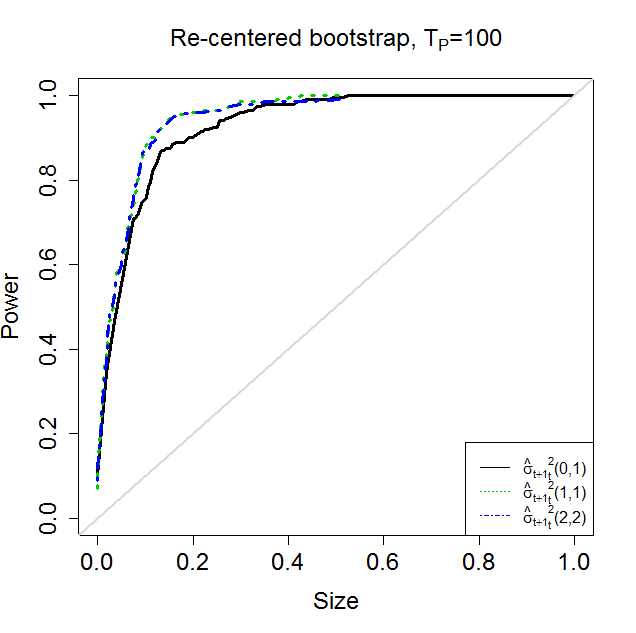

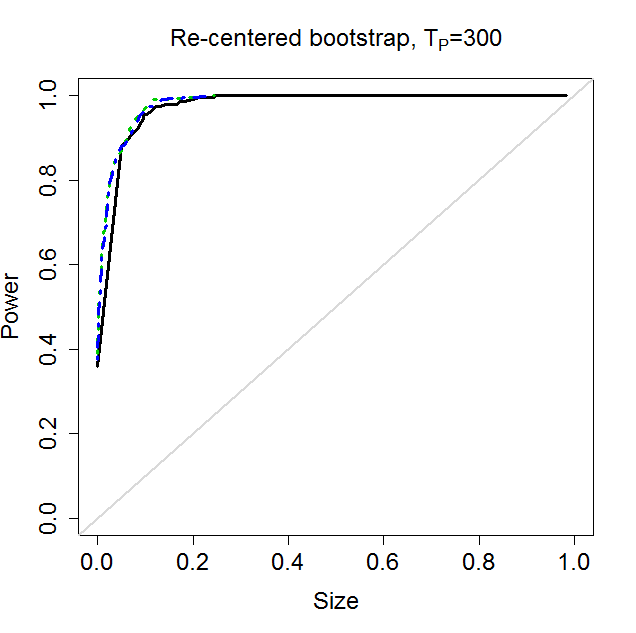

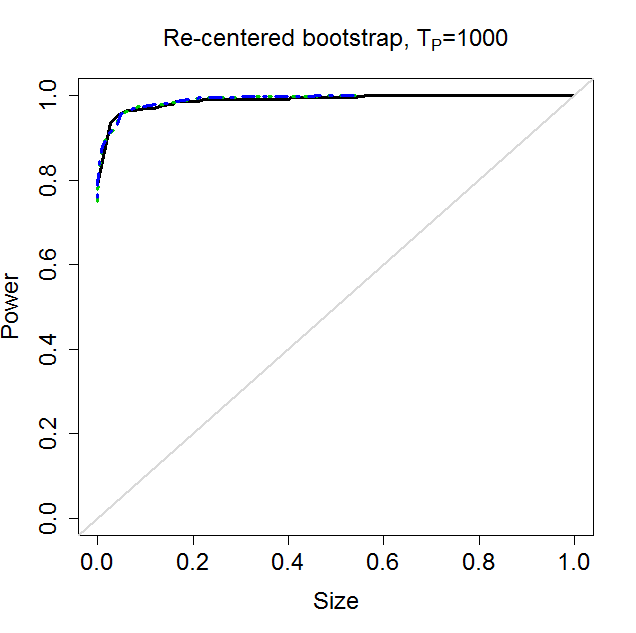

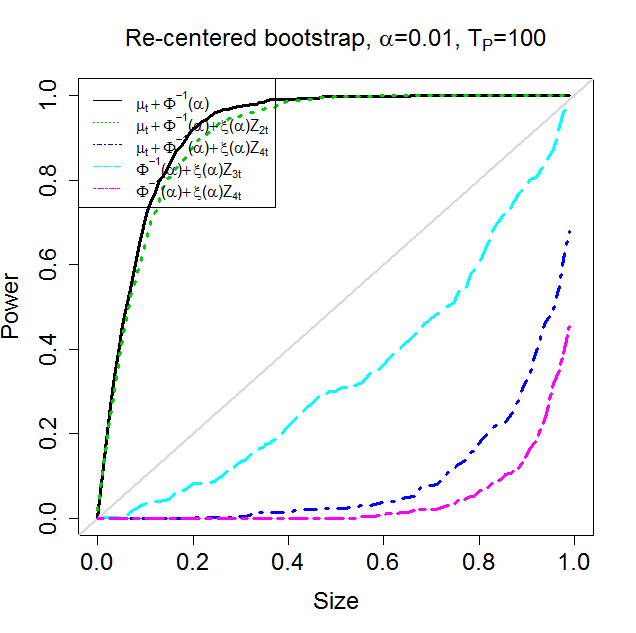

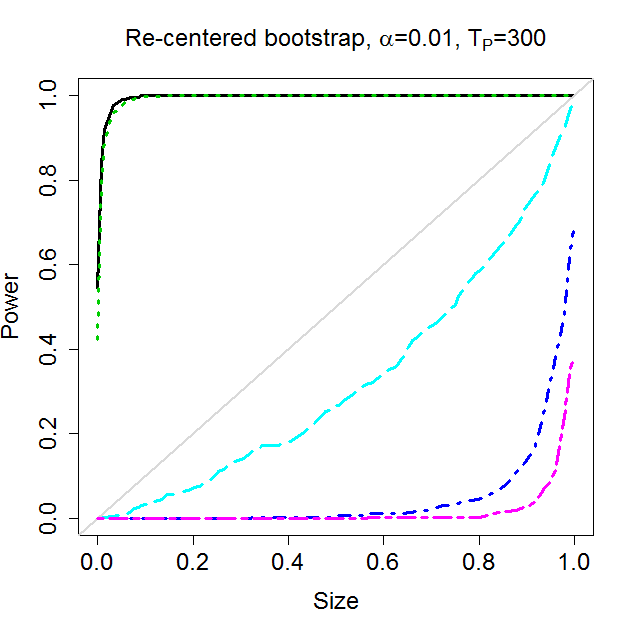

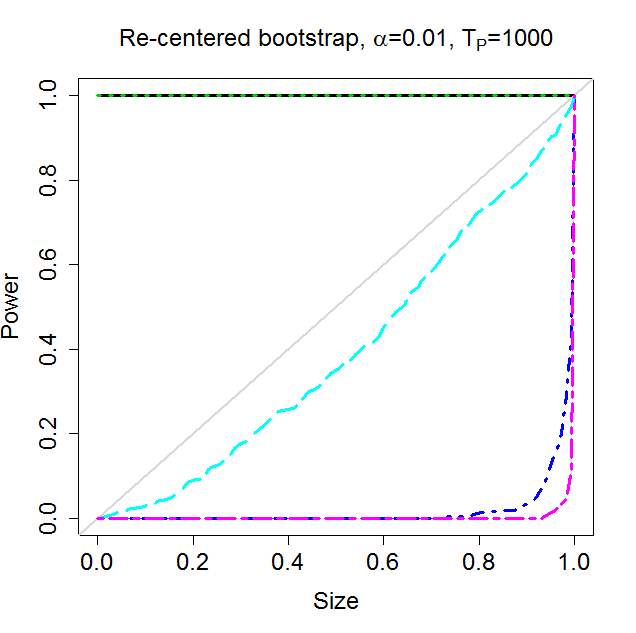

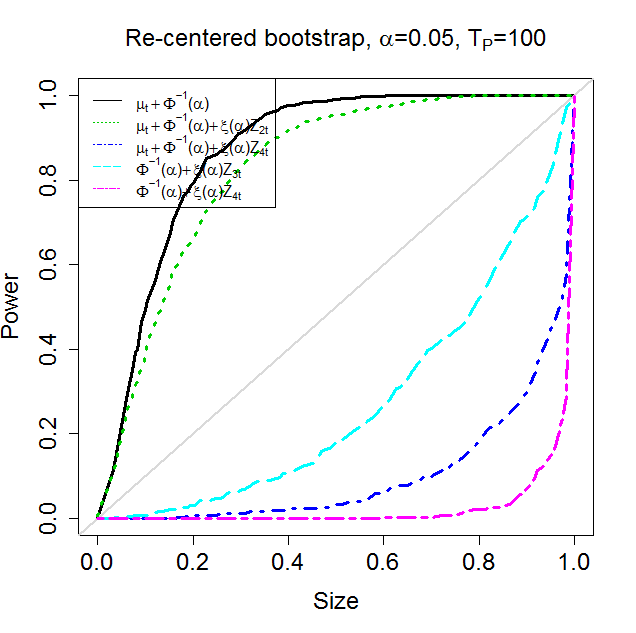

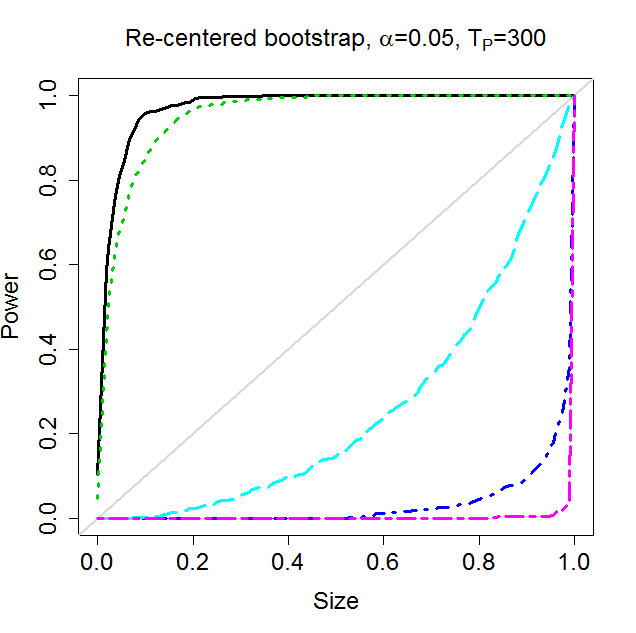

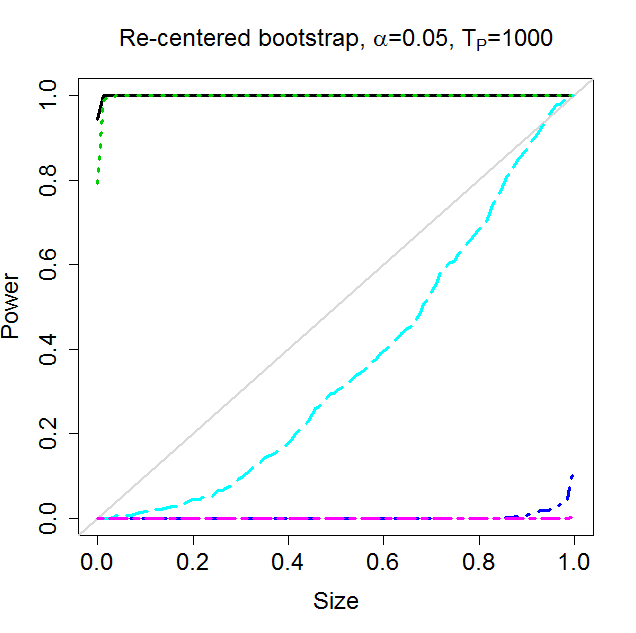

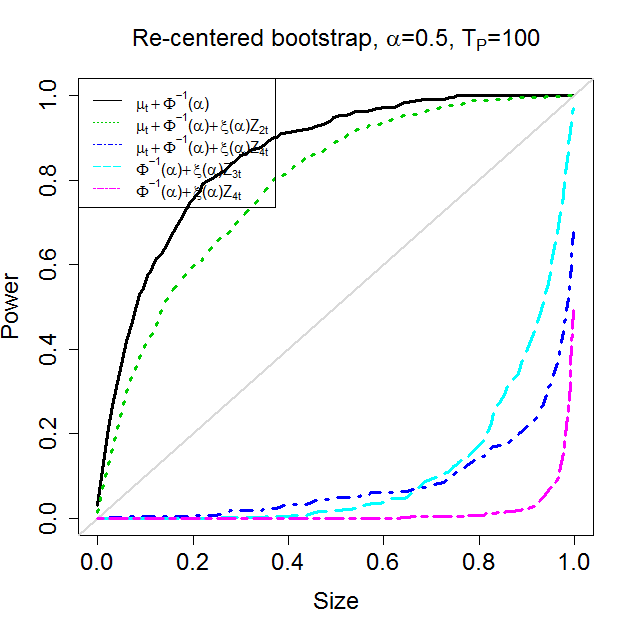

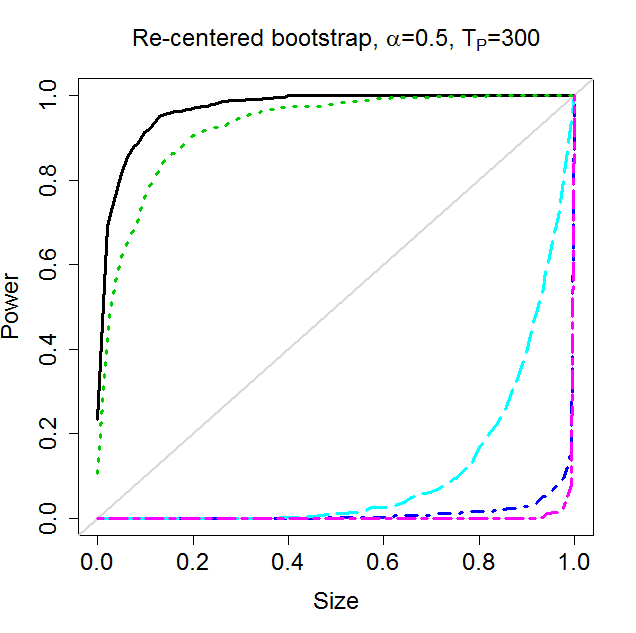

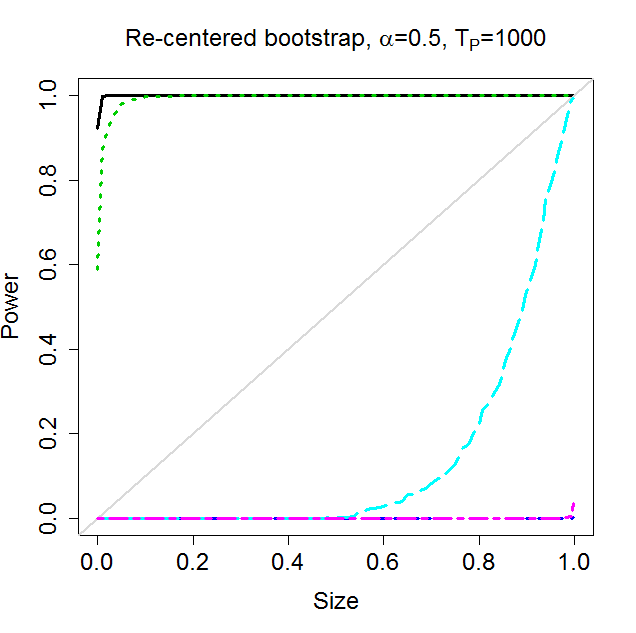

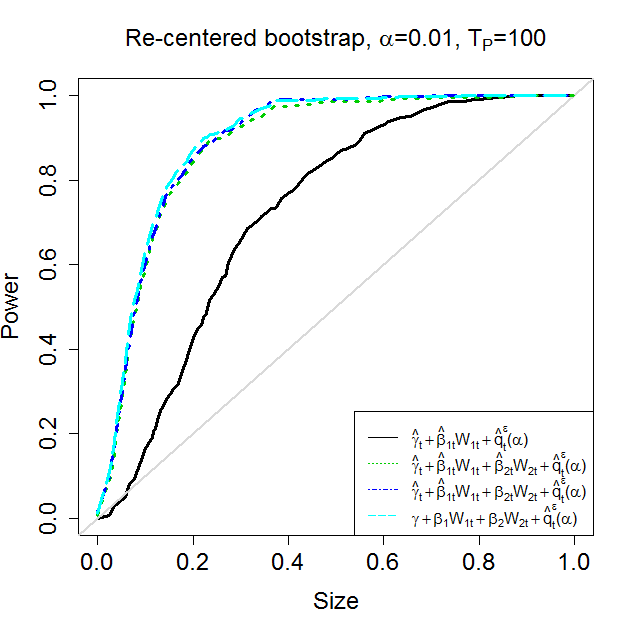

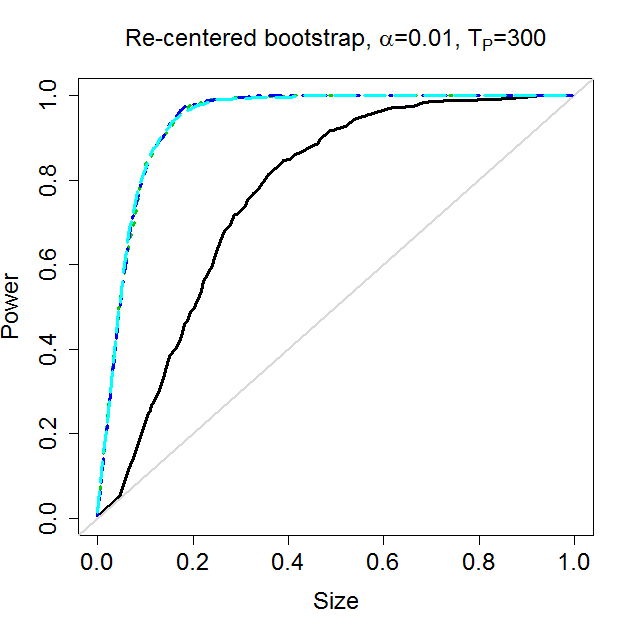

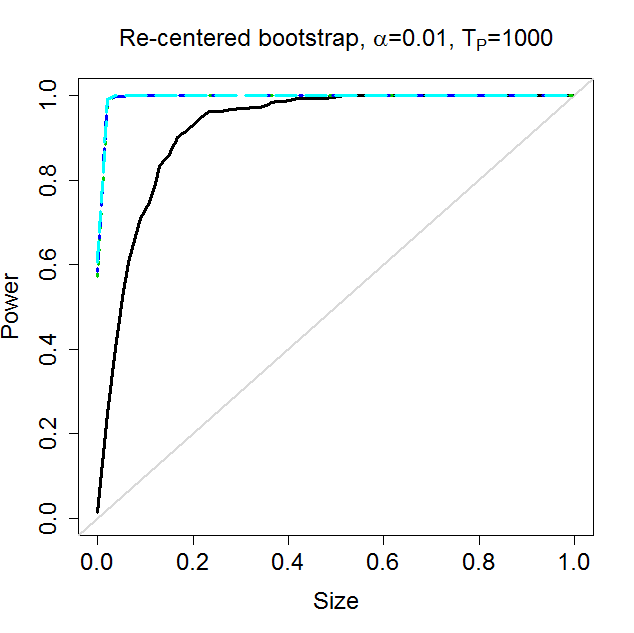

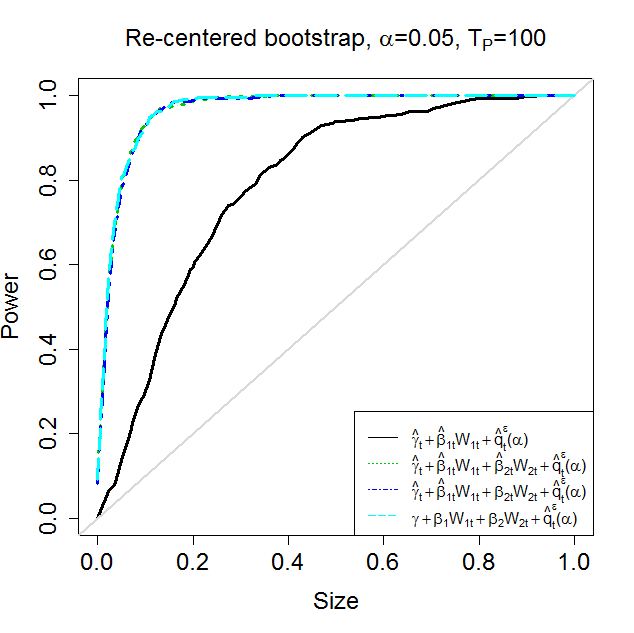

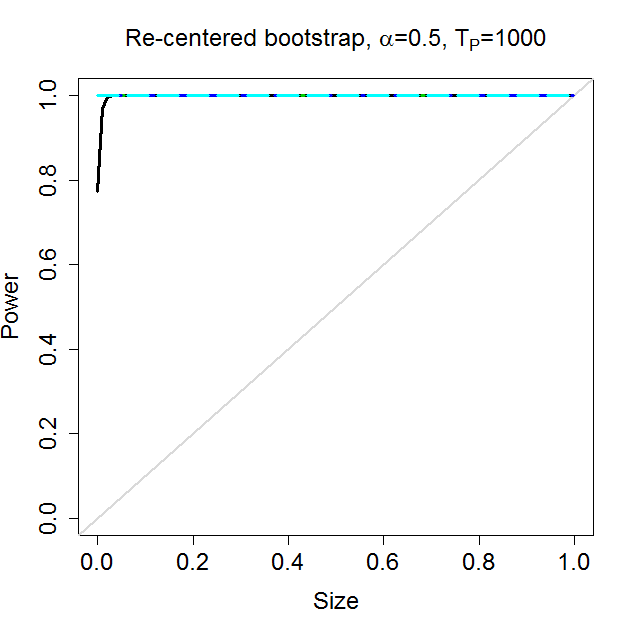

For each simulation, we set the number of generated forecasts , 300 and 1000, and the number of bootstrap . Each scenario is simulated 1000 times. For the simulation in Section 4.1.1 and model E1 and Q1, the forecasts are not generated from any estimated model. For models E2, E3 and Q2, the forecasts are generated by using rolling window scheme with window length , and for each model, length of a generated sample path , where is the sample size for initial estimations of the model parameters. In the main context, for each simulation, we show rejection frequencies of the proposed test statistics used for the simulations from the 1000 iterations. As for a more completed description for properties of size and power of the proposed test statistics, we show their size-power curves (Davidson and MacKinnon, 1998) in Appendix 7.3.

4.1 Conditional expectile forecasts

In this subsection, we present simulation results for forecasting the conditional expectile of a random variable at each period : , where satisfies

and is the conditional expectation operator at period and is the information set up to period . Again we let be the benchmark and be the competing forecasts.

4.1.1 A comparison of consistent loss functions and the proposed test

We first consider a simulation when different consistent loss functions provide different ranking results for two competing forecasts on the conditional expectation of : . The consistent loss functions we consider here are the squared error loss and the exponential Bregman loss. The random variable has the following data generating process

| (22) |

where , and . , and are mutually independent. We set , , and . The benchmark forecast is and the competitor is . We consider three scenarios for parameter settings: (1) , and ; (2) , , and ; (3) , , and . The three scenarios result in different forecast rankings when the squared error loss is used. Let denote the expected squared error loss of the random variable and forecast . As shown in Appendix 7.5, scenario (1) implies ; scenario (2) implies and scenario (3) implies .

In the left panel of Figure 3, we plot differences of the expected exponential Bregman loss for the two forecasts under the three scenarios with parameter . The right panel of Figure 3 shows differences of the expected extremal consistent loss for the two forecasts with parameter .

In scenario (1), the two forecasts have the same expected squared error loss, but as can be seen from Figure 3, they have different expected exponential Bregman loss for .555Note that for , the exponential Bregman loss becomes the squared error loss (scaled by 0.5). The difference is positive for and negative for . In this scenario, if we use an accuracy test with the squared error loss, say the Diebold and Marino (DM) test, we will have a low rejection frequency since it is the least favorable configuration (l.f.c.) of the test. On contrary if the exponential Bregman loss with is used in the accuracy test, we may have a very high rejection frequency. As for the extremal consistent loss, the difference of their expected values has a positive maximum. It suggests that the null of (13) should be rejected.

In scenario (2), the competitor outperforms the benchmark under both the squared error loss and exponential Bregman loss, as can be seen from Figure 3. For the expected extremal consistent loss, again the difference has a positive maximum, which suggests that the null of (13) should be rejected. But it is interesting to note that the difference also has a negative minimum, which suggests that the competitor may perform worse than the benchmark under a certain consistent loss function other than the squared error loss and exponential Bregman loss.

In scenario (3), the benchmark outperforms the competitor under the squared error loss and exponential Bregman loss. Furthermore, the difference of the expected extremal consistent loss is nonpositive for all considered here. It suggests that no matter which consistent loss function is used, the benchmark will still perform no worse than the competitor and the null of (13) should not be rejected.

In the upper panel of Table 3, we show rejection frequencies of the proposed test and the DM test with the squared error loss for scenarios (1) to (3). The significant levels we choose are 0.01, 0.05 and 0.1. The simulation results confirm what Figure 3 shows. For scenario (1), rejection frequencies of the DM test are close to the corresponding significant levels, which is expected, since scenario (1) is the least favorable configuration for the DM test when the squared error loss is used. But in this scenario, rejection frequencies of the proposed test are much higher than the corresponding significant levels and increase with the number of generated forecasts . For scenario (2), rejection frequencies of the proposed test and the DM test both increase with . For scenario (3), the proposed test and the DM test both obtain no rejection, which again confirm what Figure 3 shows.

In the bottom panel of Table 3, we show simulation results for a “reverse situation” in which is the competitor and is the benchmark. In this situation, results for scenarios (1) and (3) are expected. The proposed test statistic and the DM test statistic behave as before in scenario (1). While in scenario (3), now the test statistics both have a high probability to reject the null. In scenario (2), as mentioned, the difference of the expected extremal consistent loss functions has a negative minimum, which implies that may perform worse than under a certain consistent loss function other than the squared error loss and exponential Bregman loss. Our proposed test statistic thus has a high probability to reject the null in this case. However, using the DM test statistic has a very low probability to reject the null since performs better than under the squared error loss.

4.1.2 Model E1

For this simulation, , where the conditional expectation . Let denote the expectile of a standard normal random variable . The conditional expectile of at period is . We set the benchmark forecast for as , where and

The benchmark forecast can be viewed as a noisy forecast for the conditional expectile . For the noise , we scale it with to reflect the fact that accuracy of forecasting conditional expectiles generally depends on .666Note that is the asymptotic variance of the empirical expectile for i.i.d. normal samples, see Newey and Powell (1987). We use the following settings to generate the competing forecast : (1) ; (2) , and 0.25 and 1 for , 3, 4; (3) , , where and 1 for , 4.

In setting (1), is the true conditional expectile. In setting (2), like , can be viewed as a noisy forecast for the conditional expectile. In particular, and shall be equivalent since their noisy terms both follow , and this case is the least favorable configuration for the test. When (), is on average a more accurate (less accurate) forecast than , since the noise () has a smaller (larger) variance than does. In setting (3), can be viewed as a noisy forecast when the conditional expectation is replaced with the unconditional expectation (zero). Also the noise has the same or a larger variance than does. Thus in this case, is expected to perform worse than .

4.1.3 Model E2

For this simulation, we generate data from a VAR(1) model:

where

and denotes a multivariate normal distribution with mean vector and covariance matrix . Here we focus on evaluating forecasts of the conditional expectation of at each period . The parameter controls the importance of for the forecast. For , it does not directly affect and may not be helpful on the forecast. However, if its correlation with (measured by ) is high and is not available, can be a suitable alternative predictor. In the simulation, we will vary and and see how such variations affect performances of the proposed test statistic. The forecasts are all generated with estimated models in which the estimated coefficients at period are obtained from using the OLS and rolling window scheme with window length .

The benchmark forecast is , where , , and and are the estimated coefficients at period . The benchmark is from a misspecified model in which the coefficients are the OLS estimates plus noises. We use the following six settings to generate the competing forecast : (1) , , , . and . For settings (2) to (4), we set , , 0.45 and 0.75, and , where is the estimated coefficient at period and and correspond to , 0.45 and 0.75. For settings (5) and (6), we set and 0.8, , and , where is the estimated coefficient at period and and correspond to and 0.8.

In setting (1), similar as the benchmark , is also from a misspecified model in which the estimated coefficients are perturbed by noises. Since the noises in the benchmark and this setting follow the same distribution, and shall be equivalent forecasts. Hence setting (1) is the least favorable configuration (l.f.c.) for the test. In settings (2) to (4), we vary the coefficient at three different levels and keep and uncorrelated. The model used here is correctly specified. Comparing to the benchmark forecast , it is expected that as magnitude of becomes strong, will become more important in the forecast, and will outperform . Finally, in settings (5) and (6), we vary correlation between and at two different levels but keep constant. Although the model used in settings (5) and (6) is not correctly specified, it is expected that as the correlation between and increases, may become more useful on the forecast. Hence may perform better than in this case.

4.1.4 Model E3

For this simulation, we generate data by using a GARCH(1,1) model. We focus on evaluating forecasts of the conditional expectation of at each period , where and . Note that . The benchmark forecast is , where . Note that and the benchmark forecast is an unbiased forecast. Let denote a one-period ahead forecast for , in which , and are the estimated coefficients at period obtained from using the maximized likelihood (ML). We use the following settings to generate the competing forecast : (1) , ; (2) ; (3) ; (4) .

In setting (1), similar as the benchmark forecast, is a random walk forecast scaled by a log-normal noise multiplying . Since the noises in the benchmark and this setting follow the same distribution, and shall be equivalent forecasts and setting (1) is the least favorable configuration (l.f.c.) for the test. In setting (3), is a forecast from the correctly specified GARCH(1,1) model and it is expected to outperform the benchmark forecast . In setting (2) and (4), is a forecast from misspecified models ARCH(1) and GARCH(2,2), respectively.

4.1.5 Simulation results

Table 4 shows rejection frequencies of the test statistic for using model E1. We can see that when the competing forecast is either or , rejection frequency of the test statistic increases as the length of forecast generated increases. The results are expected, since is the true conditional expectation and has a smaller noisy perturbation than the benchmark . In the least favorable configuration (), when is low, rejection frequency is slightly lower than the corresponding nominal size. But when increases, size of the test statistic is improved, as can be seen that the rejection frequency approaches to the corresponding significant level. For the other three settings, the results are very similar: over different and significant levels, the rejection frequency is at zero or a very low level. The results are also expected, since these competing forecasts are worse forecasts than the benchmark forecast.

Table 5 shows rejection frequencies of the test statistic for using model E2. In the least favorable configuration, the rejection frequency behaves well. For the other five cases, the rejection frequency increases with the length of generated forecast . As the magnitude of increases, on average the rejection frequency increases. When becomes more correlated with , on average the rejection frequency also increases. To sum, these results suggest that statistical power of the proposed test statistic increases when becomes more important for or correlation between and rises. Table 6 show rejection frequencies of the test statistic for using model E3. As can be seen from the table, in the least favorable configuration, the rejection frequency is slightly lower than the corresponding significant level, which suggests that some size distortions occur here. For the other three cases, the rejection frequencies increase with .

4.2 Conditional quantile forecasts

In this subsection, we conduct simulations to understand how the proposed test statistic performs on evaluating forecasts of the conditional quantile of the random variable at each period . The conditional quantile of at period is defined as , where is the conditional probability of at period .

4.2.1 Model Q1

The data generating process for used here is the same as in Subsection 4.1.2. Let and denote density and cumulative distribution functions of a standard normal random variable. The conditional quantile of is , where is the quantile of the standard normal random variable. We set the benchmark forecast , where

and . The benchmark is a noisy forecast for the true conditional quantile. For the noise , we scale it with to reflect the fact that accuracy of forecasting conditional quantiles generally depends on .777Note that is the asymptotic variance of the empirical quantile for i.i.d. normal samples. We use the following settings to generate competitors : (1) ; (2) , and , 0.25 and 1 for , 3, and 4; (3) , , and 1 for and 4.

In setting (1), is the true conditional quantile. In setting (2), like , can be viewed as a noisy forecast for the true conditional quantile. In particular, and shall be equivalent forecasts since their noisy terms both follow , and this case is the least favorable configuration for the test. When (), on average is a more accurate (less accurate) forecast than , since the noise () has a smaller (larger) variance than does. In setting (3), can be viewed as a noisy forecast when the conditional expectation is replaced with the unconditional one (zero). Also the noise has the same or a larger variance than does. Thus in this case, is expected to perform worse than .

4.2.2 Model Q2

For this simulation, we set , where , and . We estimate the conditional quantile of at period with . Here is a forecast for at period from a predictive regression. The predictive regression has different specifications and is estimated with the OLS with the rolling window scheme. is the sample quantile of residuals , , of the predictive regression and is the rolling window length. The benchmark forecast is given by , where and and are the estimated coefficients at period . In this case, is a conditional expectation forecast from a misspecified predictive regression. The benchmark thus can be viewed as a conditional quantile forecast from a misspecified model plus a noise . We use the following settings to generate the competitors : (1) , ; (2) ; (3) ; (4) ; (5) .

In setting (1), an equivalent forecast of , since they have the same and the two noises and have the same distribution. Hence setting (1) is the least favorable configuration for the test. In setting (2), is the same as the benchmark but without the noise term. In setting (3), is estimated from the correctly specified predictive regression. In setting (4), is a combination of two components: and . The former is the same as the conditional expectation forecast in setting (1) and the latter is with its true coefficient. In setting (5), is the true conditional expectation of . From above, it can be seen that in settings (2) to (5) are expected to outperform in forecasting the conditional quantile of .

4.2.3 Simulation results

We report rejection frequencies of the proposed test statistic for using model Q1 in Table 7. From the table, we can see that when the competing forecast is either or , rejection frequency of the test statistic increases as the length of generated forecast increases. The results are expected, since the two are more accurate forecasts than the benchmark . For the least favorable configuration ( ), the sizes are overall controlled well as increases. As for the other three settings, which are considered as worse forecasts than the benchmark, the results are very similar: over different and significant levels, the rejection frequency is at zero or a very low level.

Table 8 shows rejection frequencies of the proposed test statistic for using model Q2. From the table, we can see that for the least favorable configuration, overall the sizes are well controlled. We also can see that for settings (2) to (5), when is low, the rejection frequencies for the low quantiles ( and 0.05) are lower than those for the high quantile (). But as increases, the rejection frequencies increase. For settings (3) to (5), which use the correct model specification, the rejection frequencies for different quantiles approach to a satisfied level as increases. But for setting (2), which uses an incorrect model specification, the rejection frequencies for different quantiles still have some differences as increases. Overall the results suggest that as the competing forecast becomes more accurate than the benchmark, the proposed test statistic has more statistical power to detect the performance difference.

5 Empirical applications

5.1 Forecasting equity risk premium of the S&P500 Index

In this subsection, we use the proposed test to evaluate abilities of some predictors on forecasting risk premium of the S&P500 index. Goyal and Welch (2008) claim that some predictors which were suggested by academic research often perform worse than the historical average excess return on forecasting risk premium of the S&P500 index, either in-sample or out-of-sample. Here we re-examine the claim and focus on the out-of-sample performances of the predictors. The main statistics used in Goyal and Welch (2008) for evaluating the out-of-sample forecasts are the out-of-sample R-square and difference of the root mean squared errors (dRMSE), which are based on the squared error loss function or its variant. We use the proposed test statistic to see whether the predictors can possibly outperform the historical average excess return under other consistent loss functions.

We consider sixteen predictors: (1) the default yield spread (dfy); (2) inflation (infl); (3) stock variance (svar); (4) log dividend payout ratio (de); (5) long term yield (lty); (6) the term spread (tms); (7) treasury-bill rates (tbl); (8) default return spread (dfr); (9) log dividend price ratio (dp); (10) log dividend yield (dy); (11) long term return (ltr); (12) log earnings price ratio (ep); (13) the book-to-market ratio (bm); (14) net equity expansion (ntis); (15) investment to capital ratio (ik); (16) percent equity issuing (eqis). For detailed explanations on the predictors, please see Goyal and Welch (2008). The data have three frequencies: annual (from 1927 to 2015), quarterly (from Q1-1927 to Q4-2015) and monthly (from January-1927 to December-2015).888For some predictors, their quarterly and/or monthly data are not available. Quarterly data are not available for percent equity issuing (eqis). Monthly data are not available for eqis and investment to capital ratio (ik). In addition, yearly and quarterly data for ik are only available after 1947. The data set can be downloaded from Amit Goyal’s website: http://www.hec.unil.ch/agoyal/.

5.1.1 Single-variable predictive regressions

The variable to be forecasted is the one-period-ahead risk premium (expected excess return) of the S&P500 index. To calculate the excess return, we use the simple return (including the dividend) of the index and then subtract the U.S. treasury bill rate from it. We use the historical average excess return of the S&P500 index as the benchmark forecast. The competing forecast is constructed by using a single-variable linear regression (including the intercept term), which is estimated with the OLS. The forecasts may be viewed as the ones that are generated from misspecified models. Thus using different consistent loss functions may yield different ranking results (Patton, 2015).

We use a rolling window scheme to generate the forecasts. The window length for the annual data is 20 years; for the quarterly data, it is 80 quarters and for the monthly data, it is 240 months. Accordingly, the forecasting period for the annual data is from 1947 to 2015 (69 years); for the quarterly data, it is from Q1-1947 to Q4-2015 (276 quarters)999For investment to capital ratio (ik), the forecasting period for the quarterly data is from Q1-1967 to Q4-2015 (196 quarters). and for the monthly data, it is from January-1947 to December-2015 (828 months).

In Table 9, we show values of the proposed test statistic for forecasting the conditional expectation (50%-expectile) and the corresponding empirical p-values. For comparisons, we also show p-values of the Diebold and Marino (DM) test statistic with the squared error loss and the difference of the root mean squared error loss (dRMSE) scaled by 100. The DM test statistic is obtained with the Newey-West standard error of the difference of the squared error loss.

From the table, it can be seen that the proposed test statistic is not statistically significant at 5% level, except in three cases of forecasting the annual risk premium (dp, ik and eqis). For the DM test statistic, it is also not statistically significant 5% level for all cases. These results suggest that there is still weak evidence to say that these predictors can effectively outperform the historical average excess return on forecasting the risk premium of the S&P500 index, even a much larger class of consistent loss functions are considered for the forecast evaluations.

5.1.2 Multivariate predictive regressions

While the results of the single-variable predictive regressions are overall not positive for the considered predictors, different combinations of them might provide improved outcomes. We next apply the proposed test on a completed list of predictive regressions generated from combinations of the predictors.

Some filtrations are conducted before the empirical analysis. First, we only focus on the cases of quarterly and monthly data since they can provide enough samples for the rolling window estimations when the predictive regressions are multivariate. We also exclude investment to capital ratio (ik) from the predictors since its sample length is shorter than others. Thus for each of the quarterly and monthly data used here, we have fourteen predictors. Ideally we can have predictive regressions generated from combinations of these predictors. However, among the predictors, some of them are a linear combination of others. For example, term spread (tms) equals long term yield (lty) minus treasury-bill rates (tbl), and log earnings price ratio (ep) equals log dividend price ratio (dp) minus log dividend payout ratio (de). When these variables are simultaneously included in a predictive regression, it will result in the problem of muticollineraity in the estimation. Thus we exclude the predictive regressions in which all (lty, tms, tbl) or all (de, dp, ep) are included.

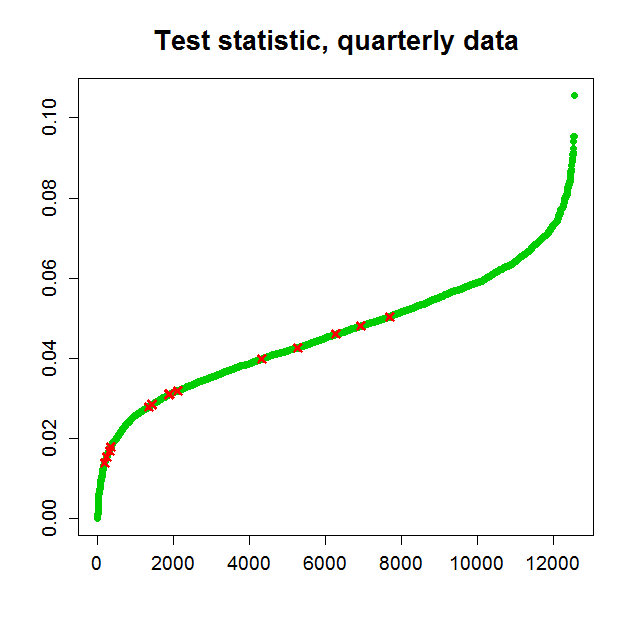

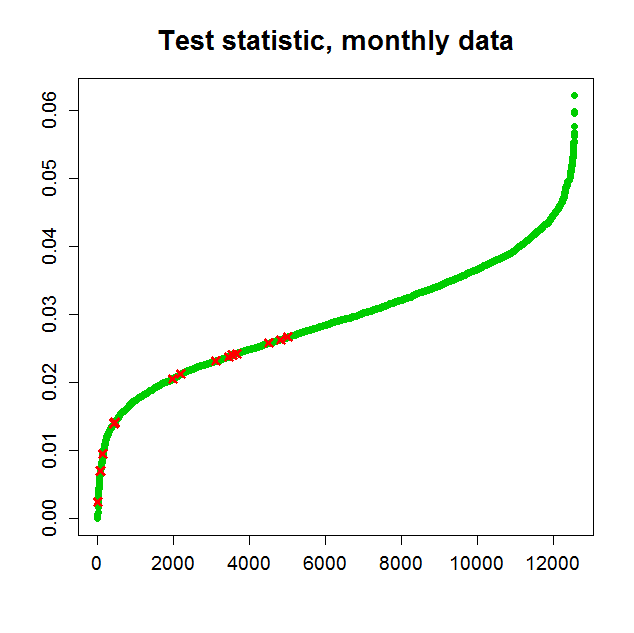

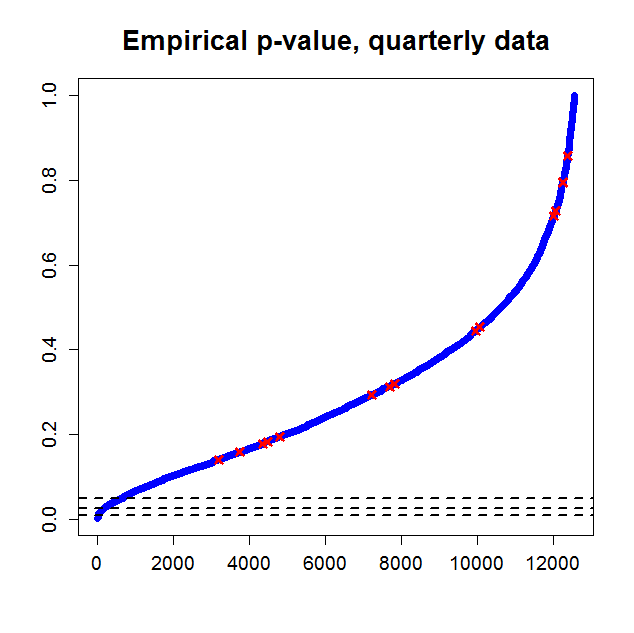

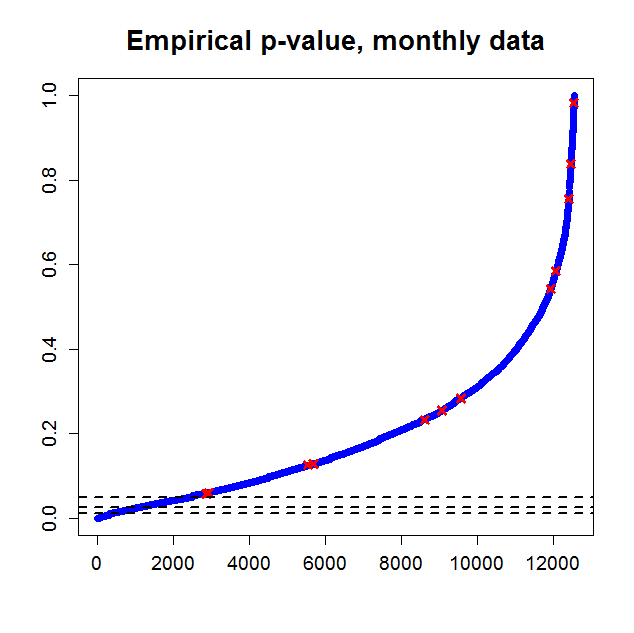

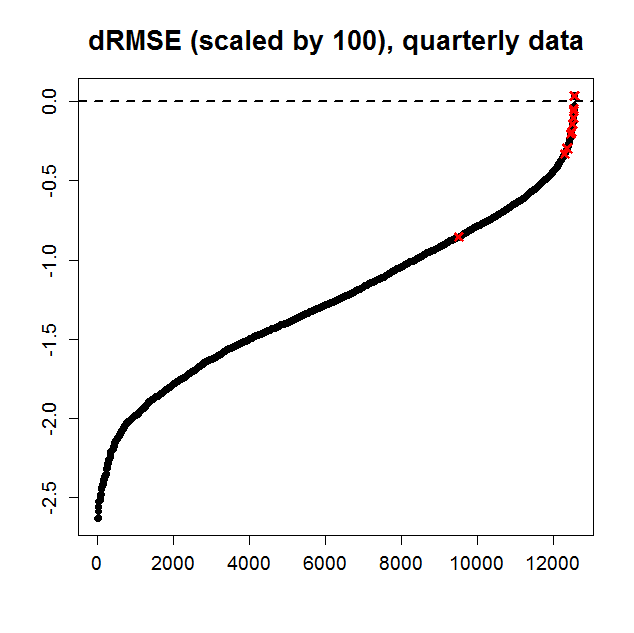

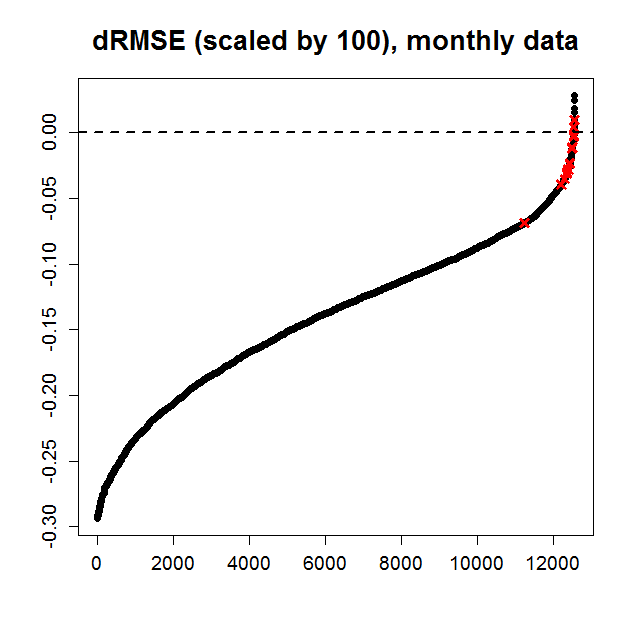

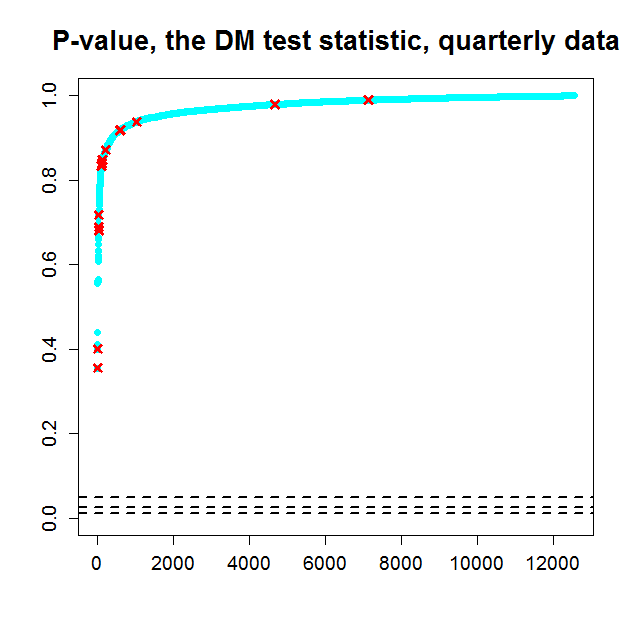

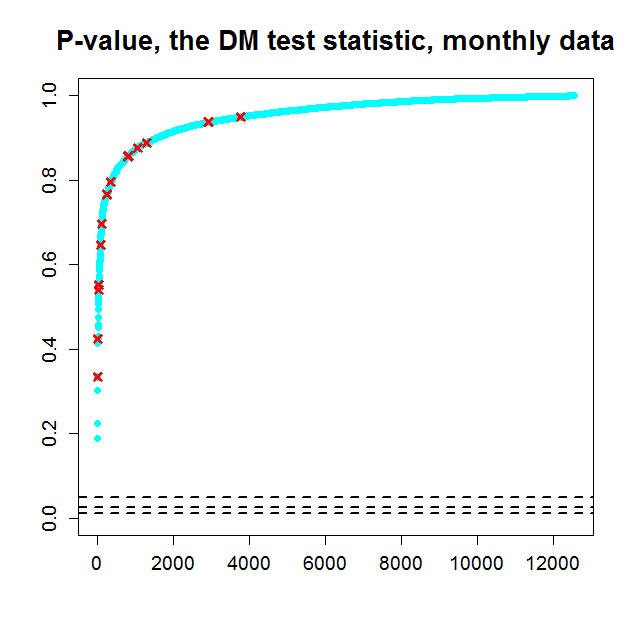

In Figure 4 we show ordered values (from small to large) of the relevant four quantities for forecasts obtained from using the multivariate predictive regressions. The red crosses in each plot are values of the quantities for the single-variable predictive regressions shown in Table 9. As can be seen from the second row of the figure, among these forecasts, only a small proportion of them have a very small p-value. For the quarterly data, only six forecasts generate empirical p-values less than 0.0025;101010Since here we have a large number of candidate predictive regressions, to avoid data snooping and take multiplicity into account, we use a much more restricted criterion for the p-value than the conventional levels 0.05 and 0.01 used in the single-variable predictive regressions. for the monthly data, the same number is 99. As shown in the third row of the figure, there are also only a few number of forecasts generating a positive dRMSE: for the quarterly data, the number is 4 (two of them are from using the single-variable regressions), and for the monthly data, the number is 13 (two of them are from using the single-variable regressions). For the DM test statistic, the p-values are all above 0.35 (0.18) for the quarterly (monthly) data.

Finally, in Table 10 we show frequency that a predictor is included in the predictive regressions whose forecasts have the empirical p-values less than 0.0025, 0.005 and 0.01. Some predictors seem to be more often included in such predictive regressions than others (e.g., dfy and infl for the quarterly data, and dfy and ntis for the monthly data), which suggests that under certain non squared-error loss functions, using these predictors might be helpful on outperforming the historical average excess return on forecasting the risk premium of the S&P500 index.

5.2 Forecasting annual growth of U.S. real gross domestic product (RGDP)

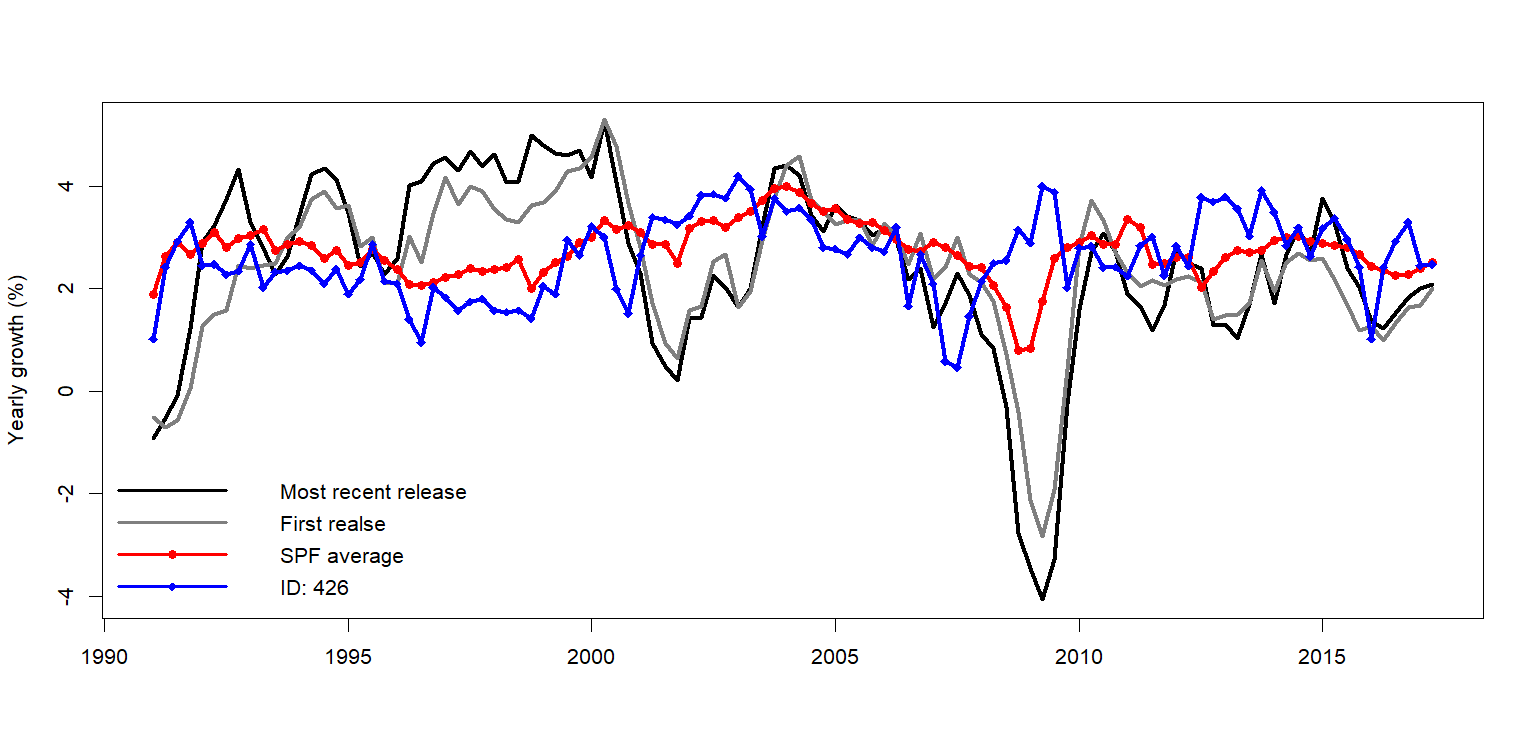

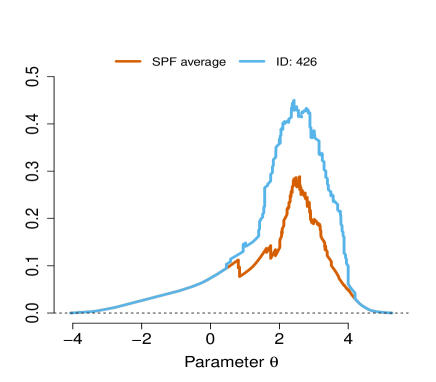

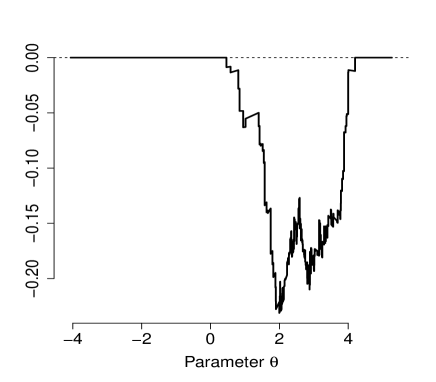

In this subsection, we use the proposed test to compare performances of experts’ forecasts on annual growth of U.S. real gross domestic product (RGDP). The extremal consistent loss function used here is for the conditional expectation forecast. The data are from Survey of Professional Forecasters (SPF) conducted by Federal Reserve Bank of Philadelphia. We focus on comparing mean forecast from all experts (SPF average) and an expert’s (with ID: 426) individual forecast. We use forecasts for next four quarter-to-quarter growth of U.S. RGDP to calculate forecast for the annual growth. We use both Q3-2017 vintage and the first release data of U.S. RGDP level data to calculate the realized annual growth. The sample period for the comparison is from Q1-1991 to Q2-2017 (106 quarters) and all the data used are in quarterly frequency. Figure 5 shows time series plots of the Q3-2017 vintage and the first release data for annual growth of U.S. RGDP and the two forecasts.

Upper panel of Table 11 shows summary statistics for the four time series. The mean forecast can be viewed as an average of opinions of the experts who were in the survey. It is known that such “wisdom of crowds” on average has a superior performance than an individual forecast. Results of our proposed test confirm this. As can be seen in bottom panel of Table 11, when the mean forecast is either the benchmark or the competitor, empirical p-values of the proposed test suggest that the mean forecast should at least perform equally well or better than the individual forecast, no matter whether the Q3-2017 vintage or first release data are used as the realized target random variable. Furthermore, when the mean forecast is the benchmark, the test result suggests that underperformance of the individual forecast is insensitive to the choice of consistent loss function for the conditional expectation forecast.

In upper panel of Figure 6, with the Q3-2017 vintage data, we plot empirical differences of consistent loss functions (SPF average minus ID: 426): exponential and homogeneous Bregman with , over a range of parameter values.111111The plots for the case of using the first release data are very similar, so they are not shown here. As can be seen from the plots, the consistent loss functions chosen here all show non-positive empirical differences, which are in line with the test results.

5.3 Estimating Value at Risk of the daily S&P500 index

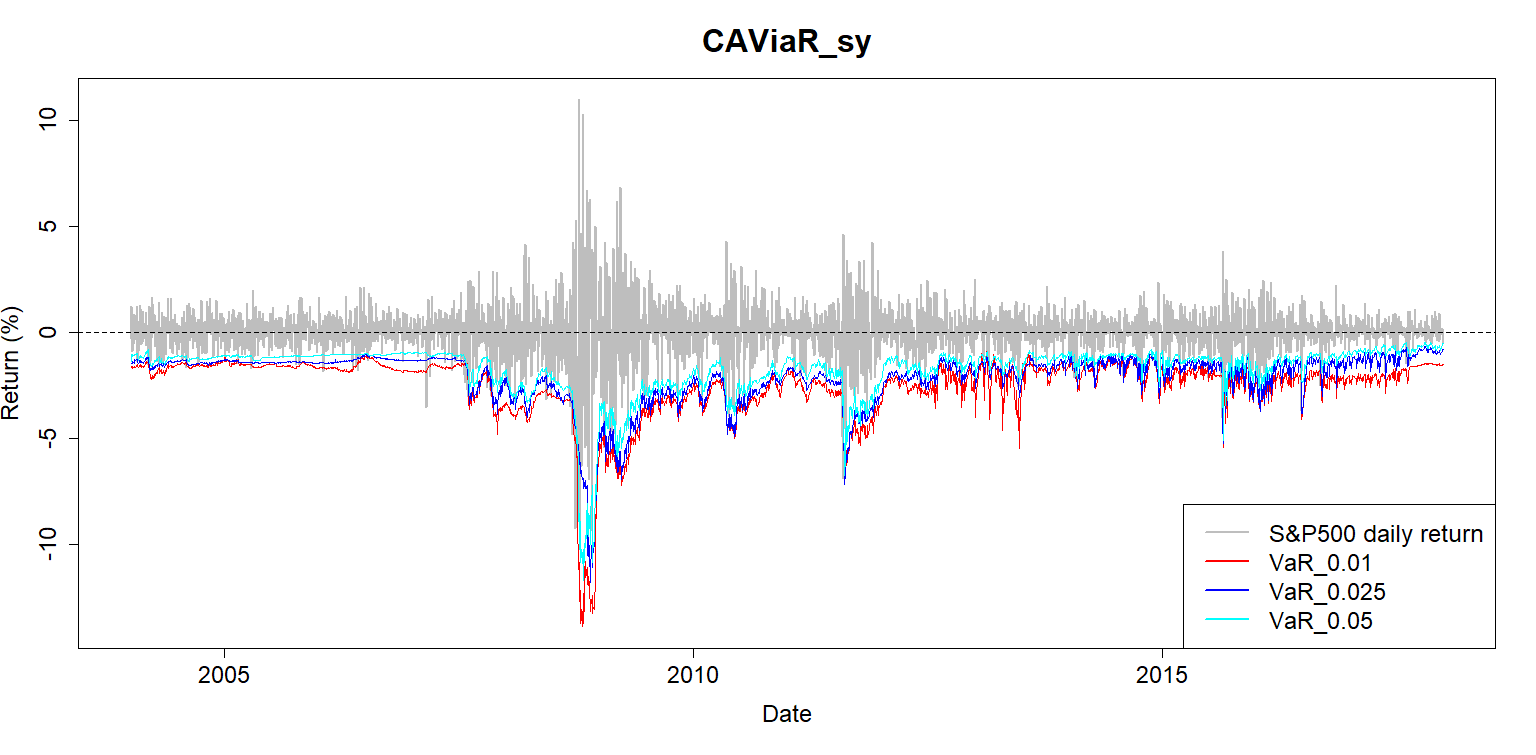

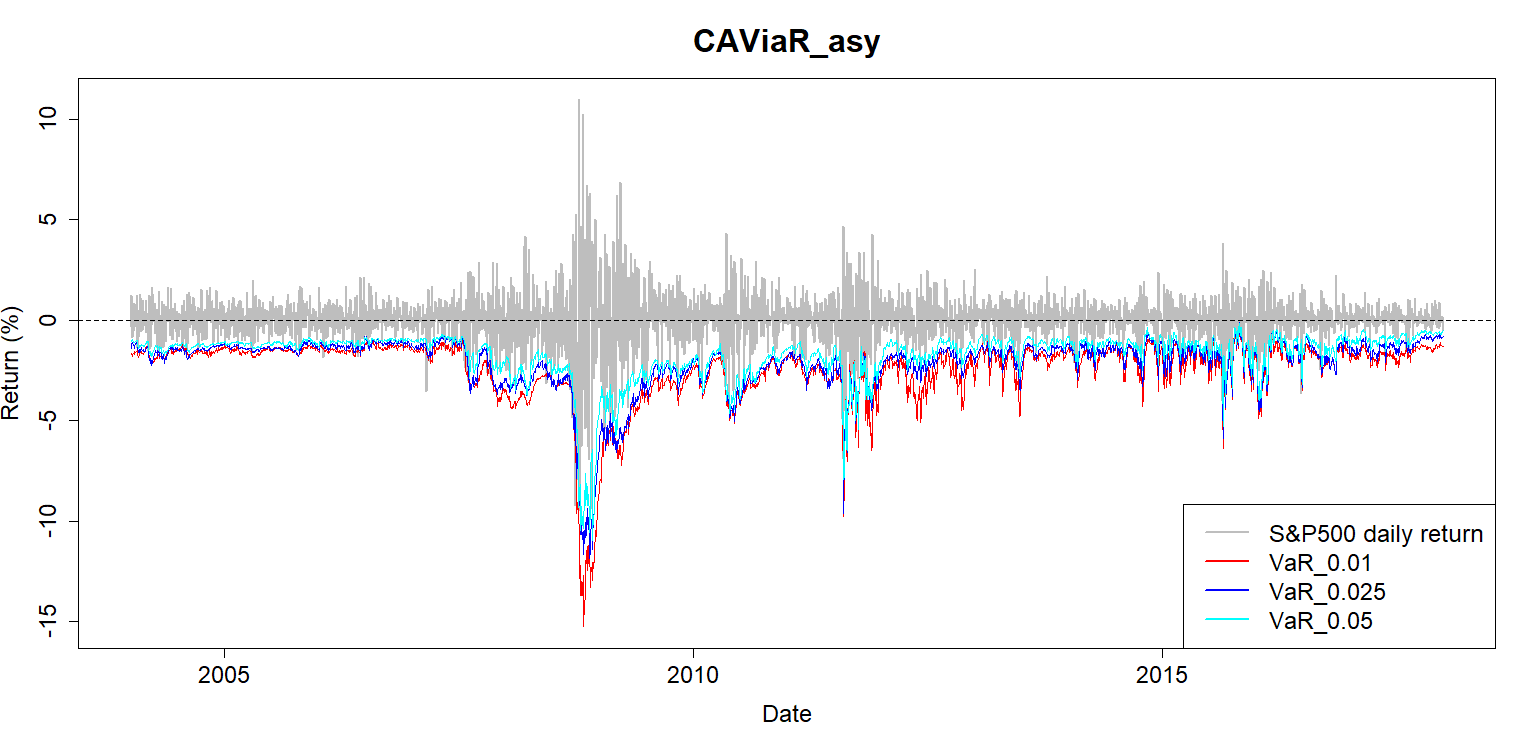

Value at risk (VaR) is an estimated amount of possible investment loss during a certain period. In risk management, the VaR is one of the most important measures used by regulators for quantifying banks’ and financial institutions’ exposures to risk. Suppose the amount of investment at the end of period is and log return of the investment at period is . At period , the VaR at level for period : can be formally defined as the conditional quantile of . For simplicity, we assume for all and thus is equivalent to the conditional quantile of . In this subsection, we use the proposed test for conditional quantile forecasts to compare performances of four methods on estimating daily of the S&P500 index.

The first method is to use sample quantile of an asset’s daily log return. The second one is to assume that the asset’s daily log return follows a normal distribution and the VaR is calculated with the estimated mean and variance. The two methods are simple and can be viewed as benchmarks on estimating the daily VaR. The third and fourth methods are based on the conditional autoregressive value at risk (CAViaR) models of Engle and Manganelli (2004). In the CAViaR models, follows an AR process augmented with a function of a finite number of lagged observable variables. Here we consider the following two specifications for the CAViaR models:

| (25) | |||||

| (26) |

The CAViaR models of (25) and (26) are termed “symmetric absolute value” and “asymmetric slope” in Engle and Manganelli (2004), and thus we use CAViaR-sy and CAViaR-asy to denote them. Coefficients of the two CAViaR models are estimated with minimizing an average of (empirical) tick loss. We solve the minimization problem with the Nelder and Mead simplex algorithm.

We consider 0.025 and 0.05, which are the most often used VaR levels in practice. All of the four methods are conducted with a rolling window scheme with window length equal to 500. The estimated daily is generated as an out-of-sample forecast of the conditional quantiles of the daily S&P500 log return. The sample period of the daily S&P500 index data is from Jan-08-2002 to Dec-29-2017 (4,024 days) and the forecasting period is from Jan-02-2004 to Dec-29-2017 (3,524 days). Figure 7 shows time-series plots of the daily S&P500 log return and the estimated daily generated with CAViaR-sy and CAViaR-asy. Table 12 presents summary statistics, hit proportion and value of averaged tick loss of the estimated daily generated with the four methods and summary statistics of the daily S&P500 log return. The hit proportion is an average of number of days when the daily S&P500 log return is no greater than the estimated daily , which estimates the unconditional probability of an exceedance event. From the table, it can be seen that the two CAViaR models on average generate a lower value of tick loss than the two simple methods.

We report values of the proposed test statistic, the corresponding empirical p-values and p-values of the Diebold-Marino test statistic in Table 13. The loss function used for calculating the DM test statistic is the tick loss. The performances are compared pairwisely. In the table, methods shown in rows are benchmarks and those shown in columns are competitors in the tests. It can be seen that when the two simple methods are the benchmarks and the two CAViaR models are the competitors, under the conventional significant level 0.05, the null hypotheses are all rejected for the proposed test. But when the two CAViaR models are the benchmarks and the two simple methods are the competitors, all the null hypotheses are not rejected under the conventional significant level 0.05 (the smallest corresponding p-value is 0.610). The results suggest that the two CAViaR models perform at least equally well as or better than the two simple methods on estimating the daily of the S&P500 index under all consistent loss functions for forecasting the conditional quantiles when , 0.025 and 0.05. Using the DM test also show similar results. Finally, turning to a comparison of the two CAViaR models themselves, the test results suggest that CAViaR-asy seems to be more adequate than CAViaR-sy on estimating the daily when 0.025 and 0.05.

6 Conclusions

In this paper, we develop statistical tests for evaluating performances of expectile and quantile forecasts of a random variable. Based on the extremal consistent loss functions proposed by Ehm et al. (2016), we construct test statistics for the tests. If the null hypothesis holds, the benchmark forecast will at least perform equally well as the competing one regardless which consistent loss function is used. For implementing the tests, we propose to use the re-centered bootstrap to obtain empirical p-values of the test statistics. We derive asymptotic results for the proposed test statistics and for using the stationary bootstrap to construct the empirical p-values. In the simulation study, we show the proposed test statistics work reasonably well under various situations.

We apply the proposed test on re-examining abilities of some predictors on forecasting risk premiums of the S&P500 index. When the predictors are used individually, we find that they seldom can outperform the historical average of excess return, no matter which consistent loss functions for forecasting conditional expectation is used for evaluating the forecast performances. When we consider possible combinations of the predictors, for forecasting the quarterly and monthly risk premiums, we find a few number of them might outperform the historical average of excess return under certain consistent loss functions. With the proposed test, we also demonstrate that for forecasting U.S. RGDP annual growth, mean forecasts from all experts has a superior performance than an individual forecast, and the result is insensitive to which consistent loss function for forecasting conditional expectation is chosen. As for comparisons of estimated daily value at risk of the S&P500 index, results from the proposed test suggest that the CAViaR type models perform better than the two benchmark methods, no matter which consistent loss function for the conditional quantile forecasts is used for the performance evaluations.

References

- Andrews and Pollard (1994) Andrews, D. W. K. and D. Pollard (1994): “An Introduction to Functional Central Limit Theorems for Dependent Stochastic Processes,” International Statistical Review / Revue Internationale de Statistique, 62, 119–132.

- Davidson and MacKinnon (1998) Davidson, R. and J. G. MacKinnon (1998): “Graphical Methods for Investigating the Size and Power of Hypothesis Tests,” The Manchester School, 66, 1–26.

- Diebold and Mariano (1995) Diebold, F. X. and R. S. Mariano (1995): “Comparing Predictive Accuracy,” Journal of Business and Economic Statistics, 13, 253–263.

- Diebold and Shin (2015) Diebold, F. X. and M. Shin (2015): “Assessing point forecast accuracy by stochastic loss distance,” Economics Letters, 130, 37–38.

- Ehm et al. (2016) Ehm, W., T. Gneiting, A. Jordan, and F. Krüger (2016): “Of quantiles and expectiles: consistent scoring functions, Choquet representations and forecast rankings,” Journal of the Royal Statistical Society: Series B (Statistical Methodology), 78, 505–562.

- Ehm and Krüger (2017) Ehm, W. and F. Krüger (2017): “Forecast dominance testing via sign randomization,” arXiv preprint arXiv:1707.03035.

- Elliott et al. (2005) Elliott, G., I. Komunjer, and A. Timmermann (2005): “Estimation and Testing of Forecast Rationality under Flexible Loss,” The Review of Economic Studies, 72, 1107–1125.

- Engle and Manganelli (2004) Engle, R. F. and S. Manganelli (2004): “CAViaR: Conditional Autoregressive Value at Risk by Regression Quantiles,” Journal of Business & Economic Statistics, 22, 367–381.

- Gneiting (2011) Gneiting, T. (2011): “Making and Evaluating Point Forecasts,” Journal of the American Statistical Association, 106, 746–762.

- Goyal and Welch (2008) Goyal, A. and I. Welch (2008): “A Comprehensive Look at The Empirical Performance of Equity Premium Prediction,” Review of Financial Studies, 21, 1455–1508.

- Granger and Newbold (1986) Granger, C. and P. Newbold (1986): Forecasting Economic Time Series, Elsevier, 2 ed.

- Granger (1999) Granger, C. W. (1999): “Outline of forecast theory using generalized cost functions,” Spanish Economic Review, 1, 161–173.

- Granger (1969) Granger, C. W. J. (1969): “Prediction with a Generalized Cost of Error Function,” Operational Research Quarterly, 20, 199–207.

- Hall and Heyde (1980) Hall, P. and C. Heyde (1980): Martingale Limit Theory and its Application, Academic Press.

- Hansen (1996a) Hansen, B. E. (1996a): “Inference When a Nuisance Parameter Is Not Identified Under the Null Hypothesis,” Econometrica, 64, 413–430.

- Hansen (1996b) ——— (1996b): “Stochastic Equicontinuity for Unbounded Dependent Heterogeneous Arrays,” Econometric Theory, 12, 347–359.

- Holzmann and Eulert (2014) Holzmann, H. and M. Eulert (2014): “The role of the information set for forecasting—with applications to risk management,” The Annals of Applied Statistics, 8, 595–621.

- Jin et al. (2016) Jin, S., V. Corradi, and N. Swanson (2016): “Robust Forecast Comparison,” Ssrn working papers.

- Koenker and Bassett (1978) Koenker, R. and G. Bassett (1978): “Regression Quantiles,” Econometrica, 46, 33–50.

- Kuan et al. (2009) Kuan, C.-M., J.-H. Yeh, and Y.-C. Hsu (2009): “Assessing value at risk with CARE, the Conditional Autoregressive Expectile models,” Journal of Econometrics, 150, 261 – 270.

- Linton et al. (2005) Linton, O., E. Maasoumi, and Y.-J. Whang (2005): “Consistent Testing for Stochastic Dominance under General Sampling Schemes,” The Review of Economic Studies, 72, 735–765.

- Linton et al. (2016) Linton, O., Y.-J. Whang, and Y.-M. Yen (2016): “A nonparametric test of a strong leverage hypothesis,” Journal of Econometrics, 194, 153–186.

- Newey and Powell (1987) Newey, W. K. and J. L. Powell (1987): “Asymmetric Least Squares Estimation and Testing,” Econometrica, 55, 819–47.

- Patton (2011) Patton, A. (2011): “Volatility forecast comparison using imperfect volatility proxies,” Journal of Econometrics, 160, 246–256.

- Patton (2015) ——— (2015): “Evaluating and Comparing Possibly Misspecified Forecasts,” working papers, Duke University.

- Politis and Romano (1994) Politis, D. N. and J. P. Romano (1994): “The Stationary Bootstrap,” Journal of the American Statistical Association, 89, 1303–1313.

- Pollard (1990) Pollard, D. (1990): “Empirical Processes: Theory and Applications,” NSF-CBMS Regional Conference Series in Probability and Statistics, 2.

- Saerens (2000) Saerens, M. (2000): “Building cost functions minimizing to some summary statistics,” IEEE Transactions on Neural Networks, 11, 1263–1271.

- Savage (1971) Savage, L. J. (1971): “Elicitation of Personal Probabilities and Expectations,” Journal of the American Statistical Association, 66, 783–801.

- Thomson (1979) Thomson, W. (1979): “Eliciting production possibilities from a well-informed manager,” Journal of Economic Theory, 20, 360 – 380.

- Varian (1975) Varian, H. R. (1975): “A Bayesian Approach to Real Estate Assessment,” in Studies in Bayesian Econometrics and Statistics, ed. by S. E. Feinberge and A. Zellner, Amsterdam North Holland, 195–208.

- West (1996) West, K. D. (1996): “Asymptotic Inference about Predictive Ability,” Econometrica, 64, 1067–84.

| Domain of | Name for , | Reference | ||

|---|---|---|---|---|

| Squared error loss | - | |||

| if , if | Negative log likelihood for | - | ||

| , | Homogeneous Bregman loss | Gneiting (2011) | ||

| , | Exponential (non-homogeneous) | Patton (2015) | ||

| Bregman loss | ||||

| QLIKE loss (homogeneous loss | Patton (2011) | |||

| with order ) | ||||

| Homogeneous loss with order | Patton (2011) | |||

| , | Homogeneous loss with order | Patton (2011) | ||

| , | Extremal consistent loss (for expectile) | Ehm et al. (2016) |

| Domain of | Name for , | Reference | ||

|---|---|---|---|---|

| Lin-lin (tick) loss | - | |||

| , | Homogeneous (power) loss | Gneiting (2011) | ||

| with order | ||||

| Homogeneous (power) loss | Gneiting (2011) | |||

| with order | ||||

| Scaled lin-lin loss | Holzmann and | |||

| Eulert (2013) | ||||

| , | Extremal consistent loss (for quantile) | Ehm et al. (2016) |

| Benchmark: , Competitor: | ||||||||

| The proposed test | DM | |||||||

| 0.01 | 0.05 | 0.1 | 0.01 | 0.05 | 0.1 | |||

| 100 | 0.047 | 0.207 | 0.347 | 0.011 | 0.052 | 0.120 | ||

| Scenario (1) | 300 | 0.237 | 0.519 | 0.716 | 0.015 | 0.052 | 0.092 | |

| 1000 | 0.968 | 1.000 | 1.000 | 0.007 | 0.048 | 0.102 | ||

| 100 | 0.120 | 0.317 | 0.511 | 0.097 | 0.272 | 0.397 | ||

| Scenario (2) | 300 | 0.419 | 0.721 | 0.875 | 0.237 | 0.479 | 0.608 | |

| 1000 | 0.998 | 1.000 | 1.000 | 0.736 | 0.888 | 0.953 | ||

| 100 | 0.000 | 0.000 | 0.000 | 0.000 | 0.000 | 0.000 | ||

| Scenario (3) | 300 | 0.000 | 0.000 | 0.000 | 0.000 | 0.000 | 0.000 | |

| 1000 | 0.000 | 0.000 | 0.000 | 0.000 | 0.000 | 0.000 | ||

| Benchmark: , Competitor: | ||||||||

| The proposed test | DM | |||||||

| 0.01 | 0.05 | 0.1 | 0.01 | 0.05 | 0.1 | |||

| 100 | 0.362 | 0.611 | 0.721 | 0.015 | 0.045 | 0.095 | ||

| Scenario (1) | 300 | 0.828 | 0.958 | 0.983 | 0.007 | 0.057 | 0.122 | |

| 1000 | 1.000 | 1.000 | 1.000 | 0.012 | 0.057 | 0.105 | ||

| 100 | 0.217 | 0.479 | 0.599 | 0.000 | 0.000 | 0.001 | ||

| Scenario (2) | 300 | 0.559 | 0.791 | 0.888 | 0.000 | 0.000 | 0.001 | |

| 1000 | 0.980 | 1.000 | 1.000 | 0.000 | 0.000 | 0.000 | ||

| 100 | 0.611 | 0.845 | 0.908 | 0.648 | 0.863 | 0.925 | ||

| Scenario (3) | 300 | 0.988 | 0.998 | 1.000 | 0.993 | 1.000 | 1.000 | |

| 1000 | 1.000 | 1.000 | 1.000 | 1.000 | 1.000 | 1.000 | ||

| 0.01 | 0.05 | 0.1 | 0.01 | 0.05 | 0.1 | 0.01 | 0.05 | 0.1 | ||||||

|---|---|---|---|---|---|---|---|---|---|---|---|---|---|---|

| 0.01 | 0.002 | 0.062 | 0.314 | 0.080 | 0.519 | 0.800 | 0.963 | 1.000 | 1.000 | |||||

| 0.05 | 0.005 | 0.100 | 0.374 | 0.147 | 0.596 | 0.868 | 0.980 | 1.000 | 1.000 | |||||

| 0.5 | 0.036 | 0.226 | 0.386 | 0.380 | 0.709 | 0.877 | 0.971 | 1.000 | 1.000 | |||||

| 0.01 | 0.000 | 0.082 | 0.282 | 0.065 | 0.454 | 0.788 | 0.900 | 0.998 | 1.000 | |||||

| 0.05 | 0.000 | 0.050 | 0.282 | 0.085 | 0.459 | 0.731 | 0.828 | 0.995 | 1.000 | |||||

| 0.5 | 0.031 | 0.121 | 0.295 | 0.240 | 0.555 | 0.736 | 0.876 | 0.985 | 0.995 | |||||

| 0.01 | 0.000 | 0.012 | 0.070 | 0.002 | 0.025 | 0.087 | 0.015 | 0.052 | 0.102 | |||||

| (l.f.c.) | 0.05 | 0.000 | 0.010 | 0.077 | 0.002 | 0.052 | 0.112 | 0.007 | 0.062 | 0.107 | ||||

| 0.5 | 0.011 | 0.026 | 0.061 | 0.014 | 0.053 | 0.100 | 0.015 | 0.066 | 0.105 | |||||

| 0.01 | 0.000 | 0.000 | 0.000 | 0.000 | 0.000 | 0.000 | 0.000 | 0.000 | 0.000 | |||||

| 0.05 | 0.000 | 0.000 | 0.000 | 0.000 | 0.000 | 0.000 | 0.000 | 0.000 | 0.000 | |||||

| 0.5 | 0.000 | 0.000 | 0.000 | 0.000 | 0.000 | 0.000 | 0.000 | 0.000 | 0.000 | |||||

| 0.01 | 0.000 | 0.002 | 0.012 | 0.000 | 0.002 | 0.007 | 0.000 | 0.001 | 0.002 | |||||

| 0.05 | 0.000 | 0.002 | 0.002 | 0.000 | 0.000 | 0.000 | 0.000 | 0.000 | 0.000 | |||||

| 0.5 | 0.000 | 0.000 | 0.000 | 0.000 | 0.000 | 0.000 | 0.000 | 0.000 | 0.000 | |||||

| 0.01 | 0.000 | 0.000 | 0.000 | 0.000 | 0.000 | 0.000 | 0.000 | 0.000 | 0.000 | |||||

| 0.05 | 0.000 | 0.000 | 0.000 | 0.000 | 0.000 | 0.000 | 0.000 | 0.000 | 0.000 | |||||

| 0.5 | 0.000 | 0.000 | 0.000 | 0.000 | 0.000 | 0.000 | 0.000 | 0.000 | 0.000 | |||||

| 0.01 | 0.05 | 0.1 | 0.01 | 0.05 | 0.1 | 0.01 | 0.05 | 0.1 | ||||

|---|---|---|---|---|---|---|---|---|---|---|---|---|

| (l.f.c.) | 0.011 | 0.051 | 0.125 | 0.015 | 0.049 | 0.086 | 0.011 | 0.054 | 0.101 | |||

| 0.051 | 0.146 | 0.245 | 0.066 | 0.177 | 0.297 | 0.124 | 0.352 | 0.543 | ||||

| 0.413 | 0.721 | 0.869 | 0.881 | 0.985 | 1.000 | 1.000 | 1.000 | 1.000 | ||||

| 0.705 | 0.918 | 0.989 | 0.997 | 1.000 | 1.000 | 1.000 | 1.000 | 1.000 | ||||

| 0.025 | 0.126 | 0.241 | 0.025 | 0.176 | 0.292 | 0.134 | 0.383 | 0.525 | ||||

| 0.192 | 0.465 | 0.662 | 0.503 | 0.805 | 0.922 | 0.991 | 1.000 | 1.000 | ||||

| 0.01 | 0.05 | 0.1 | 0.01 | 0.05 | 0.1 | 0.01 | 0.05 | 0.1 | ||||

|---|---|---|---|---|---|---|---|---|---|---|---|---|

| (l.f.c.) | 0.005 | 0.031 | 0.082 | 0.000 | 0.016 | 0.051 | 0.010 | 0.027 | 0.054 | |||

| 0.267 | 0.564 | 0.758 | 0.645 | 0.891 | 0.953 | 0.903 | 0.960 | 0.971 | ||||

| 0.281 | 0.601 | 0.881 | 0.645 | 0.870 | 0.965 | 0.883 | 0.956 | 0.977 | ||||

| 0.273 | 0.602 | 0.875 | 0.633 | 0.881 | 0.965 | 0.878 | 0.954 | 0.975 | ||||

| 0.01 | 0.05 | 0.1 | 0.01 | 0.05 | 0.1 | 0.01 | 0.05 | 0.1 | ||||||

|---|---|---|---|---|---|---|---|---|---|---|---|---|---|---|

| 0.01 | 0.065 | 0.441 | 0.713 | 0.865 | 0.988 | 1.000 | 1.000 | 1.000 | 1.000 | |||||

| 0.05 | 0.027 | 0.209 | 0.491 | 0.446 | 0.825 | 0.958 | 1.000 | 1.000 | 1.000 | |||||

| 0.5 | 0.115 | 0.382 | 0.566 | 0.554 | 0.815 | 0.915 | 0.998 | 1.000 | 1.000 | |||||

| 0.01 | 0.085 | 0.411 | 0.643 | 0.830 | 0.973 | 0.998 | 1.000 | 1.000 | 1.000 | |||||

| 0.05 | 0.025 | 0.190 | 0.387 | 0.297 | 0.706 | 0.853 | 0.978 | 1.000 | 1.000 | |||||

| 0.5 | 0.070 | 0.264 | 0.411 | 0.299 | 0.618 | 0.768 | 0.875 | 0.983 | 0.998 | |||||

| 0.01 | 0.002 | 0.042 | 0.077 | 0.020 | 0.050 | 0.107 | 0.007 | 0.055 | 0.102 | |||||

| (l.f.c.) | 0.05 | 0.000 | 0.022 | 0.092 | 0.002 | 0.047 | 0.095 | 0.007 | 0.050 | 0.087 | ||||

| 0.5 | 0.010 | 0.027 | 0.062 | 0.005 | 0.047 | 0.097 | 0.012 | 0.042 | 0.085 | |||||

| 0.01 | 0.000 | 0.000 | 0.000 | 0.000 | 0.000 | 0.000 | 0.000 | 0.000 | 0.000 | |||||

| 0.05 | 0.000 | 0.000 | 0.000 | 0.000 | 0.000 | 0.000 | 0.000 | 0.000 | 0.000 | |||||

| 0.5 | 0.002 | 0.002 | 0.005 | 0.000 | 0.000 | 0.000 | 0.000 | 0.000 | 0.000 | |||||

| 0.01 | 0.000 | 0.002 | 0.030 | 0.000 | 0.007 | 0.030 | 0.002 | 0.017 | 0.027 | |||||

| 0.05 | 0.000 | 0.005 | 0.007 | 0.000 | 0.000 | 0.002 | 0.000 | 0.007 | 0.015 | |||||

| 0.5 | 0.000 | 0.000 | 0.000 | 0.000 | 0.000 | 0.000 | 0.000 | 0.000 | 0.000 | |||||

| 0.01 | 0.000 | 0.000 | 0.000 | 0.000 | 0.000 | 0.000 | 0.000 | 0.000 | 0.000 | |||||

| 0.05 | 0.000 | 0.000 | 0.000 | 0.000 | 0.000 | 0.000 | 0.000 | 0.000 | 0.000 | |||||

| 0.5 | 0.000 | 0.000 | 0.000 | 0.000 | 0.000 | 0.000 | 0.000 | 0.000 | 0.000 | |||||

| 0.01 | 0.05 | 0.1 | 0.01 | 0.05 | 0.1 | 0.01 | 0.05 | 0.1 | ||||||

|---|---|---|---|---|---|---|---|---|---|---|---|---|---|---|

| 0.01 | 0.002 | 0.037 | 0.142 | 0.000 | 0.012 | 0.055 | 0.010 | 0.040 | 0.077 | |||||

| (l.f.c.) | 0.05 | 0.000 | 0.042 | 0.140 | 0.000 | 0.047 | 0.107 | 0.010 | 0.042 | 0.102 | ||||

| 0.5 | 0.020 | 0.060 | 0.120 | 0.015 | 0.060 | 0.100 | 0.017 | 0.047 | 0.092 | |||||

| 0.01 | 0.002 | 0.042 | 0.165 | 0.007 | 0.070 | 0.224 | 0.135 | 0.516 | 0.733 | |||||

| 0.05 | 0.017 | 0.137 | 0.302 | 0.060 | 0.287 | 0.526 | 0.524 | 0.873 | 0.958 | |||||

| 0.5 | 0.127 | 0.414 | 0.594 | 0.429 | 0.713 | 0.853 | 0.970 | 1.000 | 1.000 | |||||

| 0.01 | 0.022 | 0.269 | 0.591 | 0.137 | 0.541 | 0.826 | 0.960 | 1.000 | 1.000 | |||||

| 0.05 | 0.354 | 0.788 | 0.925 | 0.955 | 1.000 | 1.000 | 1.000 | 1.000 | 1.000 | |||||

| 0.5 | 0.991 | 1.000 | 1.000 | 1.000 | 1.000 | 1.000 | 1.000 | 1.000 | 1.000 | |||||

| 0.01 | 0.025 | 0.289 | 0.606 | 0.165 | 0.531 | 0.820 | 0.945 | 0.998 | 1.000 | |||||

| 0.05 | 0.327 | 0.781 | 0.933 | 0.963 | 0.998 | 1.000 | 1.000 | 1.000 | 1.000 | |||||

| 0.5 | 0.988 | 1.000 | 1.000 | 1.000 | 1.000 | 1.000 | 1.000 | 1.000 | 1.000 | |||||

| 0.01 | 0.025 | 0.307 | 0.631 | 0.160 | 0.554 | 0.828 | 0.965 | 1.000 | 1.000 | |||||

| 0.05 | 0.357 | 0.805 | 0.928 | 0.968 | 1.000 | 1.000 | 1.000 | 1.000 | 1.000 | |||||