An optimal transportation approach for assessing almost stochastic order.111Research partially supported by the

Spanish Ministerio de Economía y Competitividad y fondos FEDER, grants

MTM2014-56235-C2-1-P and MTM2014-56235-C2-2.

E. del Barrio1, J.A. Cuesta-Albertos2 and C. Matrán1 1Departamento de Estadística e Investigación Operativa and IMUVA,

Universidad de Valladolid 2Departamento de

Matemáticas, Estadística y Computación,

Universidad de Cantabria

Abstract

When stochastic dominance does not hold, we can improve agreement

to stochastic order by suitably trimming both distributions.

In this work we consider the Wasserstein distance, , to stochastic order of

these trimmed versions. Our characterization for that distance

naturally leads to consider a -based index of disagreement with

stochastic order, . We provide asymptotic

results allowing to test vs

, that, under rejection,

would give statistical guarantee of almost stochastic dominance.

We include a simulation study showing a good performance of the index under the normal model.

1 Introduction

Let be probability distributions on the real line

with distribution functions (d.f.’s in the sequel) , respectively.

Stochastic dominance of over , denoted is defined in terms

of the d.f.’s by for every

(throughout we will also use the alternative notation ).

The meaning of this relation is that random outcomes produced by the second law tend to be

larger than those produce by the first one. We gain a

better understanding of this stochastic order by considering a quantile representation. For a d.f. ,

the quantile function associated to , that we will denote by , is defined by

The following well-known statements (see e.g. [15]) are equivalent to :

a)

There exist random variables defined on some probability space ,

with respective laws and (), satisfying .

b)

for every .

Quantile functions (also called ‘monotone rearrangements’ in other contexts)

are characterized by if and only if . Therefore it

is straightforward that, when considered as random variables defined on the unit

interval with the Lebesgue measure , they satisfy

. This representation shows that a)

and b) are equivalent and, more importantly in the present setting, allows

us to relate characteristics and measure agreement or disagreements with the stochastic

order.

From the previous considerations it becomes clear that guaranteeing stochastic dominance,

, should be the goal when comparing treatments or production schemes.

However, the rejection of

on the basis of two data samples is an ill posed statistical problem:

As showed in [8] and noted in [17], [13],

or [5], the ‘non-data test’, namely the test which rejects with probability , regardless the data,

is uniformly most powerful for testing the nonparametric hypotheses vs .

This fact motivates recent research looking for suitable indices measuring ‘almost’ or ‘approximate’ versions of

stochastic dominance. Here, suitability of an index must be understood in terms of computability and interpretability,

but also in terms of statistical performance.

Usually, as already suggested in

a general context in [14], such measures of nearness involve the use of some kind of distance to the null.

This will also be the approach here, with the choice of the -Wasserstein distance between probabilities.

For in the set of Borel probabilities on with finite second order moments,

this distance is defined as

In the univariate case, equals the -distance between quantile functions, namely,

(1)

Statistical applications based on optimal transportation, and particularly on the version, are receiving considerable

attention in recent times (see e.g. [9], [10], [11], [18] or [6]).

We should mention here our papers [2] and [3], dealing with similarity of

distributions (as a relaxation of homogeneity) through this distance,

and also [5] (and [4]) which introduced

an index of disagreement from stochastic dominance based on the idea of similarity.

The key to this index is the existence,

for a given (small enough) of mixture decompositions

(2)

If model (2) holds then it means that stochastic order holds after removing

contaminating -fractions from each population.

The minimum compatible with (2),

denoted by , can then be taken as a measure of deviation from stochastic order,

see [5] for details.

We would like to emphasize here that the analysis in [5] is based on the connection between

contamination models and trimmed probabilities. We recall that an -trimming of a

probability, , is any other probability, say , such that

for some function taking values in . Like the trimming methods,

commonly used in Robust Statistics, consisting of removing disturbing observations,

the function allows to discard or downplay the influence of some regions on the sample space.

On the real line, writing for the set of trimmings of , it turns out (see [5]) that

(3)

The contaminated stochastic order model (2) can also be recast

in terms of trimmings. If we denote

or, equivalently (this follows from compactness of with

respect to ; we omit details), if and only if

(5)

where denotes the metric on the set given by

and, for , .

For fixed ,

can be used as a measure of deviation from the contaminated stochastic order model

(2). In this work we obtain a simple explicit

characterization of this measure (see Theorem 2.3 below)

that could be used for statistical purposes. Later, we use this characterization

to introduce a new index, , see (8), to evaluate disagreement

with respect to the (non-contaminated) stochastic order.

We also provide asymptotic theory (Theorem 2.4) about the behavior of this index, that allows addressing the goal of statistical assessment

of -almost stochastic dominance. This index has some similarity

with that proposed in [17] for which,

in contrast, asymptotics are not available.

The remaining sections of this work are organized as follows. Section 2 presents the announced results, introduces

the new index and discusses its application in the statistical assessment of almost stochastic order.

This includes an illustration of the meaning of the index in the case of normal distributions and a small simulation study. Finally,

the more technical proof of Theorem 2.4 is given in an Appendix.

2 Main results

A fortunate fact that eases the use of trimming in the stochastic dominance setting is that the set has a minimum and a maximum for the stochastic order. Moreover both can be easily characterized as follows (see Proposition 2.3 in [5]).

Proposition 2.1

Consider a distribution function and . Define the d.f.’s

Then and any other

satisfies

.

Recalling the characterization of the stochastic order in terms of quantile functions,

a simple computation shows that the associated quantile functions are

(6)

so we can restate this proposition in the following new way.

Proposition 2.2

If , then its quantile function

satisfies

(7)

We can use equation (7) for proving our next result, the announced

characterization for , a quantity that measures

deviation from the contaminated stochastic order model (2).

We keep the notation in (6) and

define

Theorem 2.3

With the above notation, if and are distribution functions with finite second moment the

, are the quantile functions of a pair .

Furthermore, if we denote ,

Proof. To see that is a quantile function we note that

This shows that is nondecreasing and left continuous, hence a quantile function.

That has finite second moment follows from the elementary

bounds

A similar argument works for . Obviously and, therefore,

. Now, for any

and we have , ,

.

We define . Then

where the last lower bound is just the trivial fact that if , then the minimum value , for is just attained at , , . To complete

the proof we note that

Particularizing for , Theorem 2.3 shows that the distance between the

pair and the set is attained at the pair associated to

the quantile functions and .

Moreover, .

Avoiding the factor , this is just the part of due to the violation of stochastic dominance.

Therefore, for distinct d.f.’s , according to the notation , the quotient

(8)

can be considered as a normalized index of such violation.

It satisfies with the extreme values 0 and 1

corresponding, respectively, to perfect stochastic dominance of over and vice-versa.

We notice that [17], following a very different motivation, introduced a related index

consisting in the quotient where is the norm with respect to the Lebesgue measure on the line.

The index can be estimated by its sample counterpart , when and are the sample d.f.’s associated to independent samples respectively obtained from and . The following theorem gives the mathematical background for such task.

Theorem 2.4

Let be distinct d.f.’s in and assume with

. If and are the sample d.f.’s based on

independent samples of and , then a.s.. If, additionally, and have bounded

convex supports, then

(9)

where

, and

and are independent r.v.’s with d.f.’s and , respectively.

A critical analysis of the problem of assessing improvement in a treatment comparison setup

from the perspective of stochastic dominance is given in [7].

It is argued there that under, say, normality assumptions, improvement with the new treatment

is often assessed through a one sided test for the mean, while the really interesting test would be

that of vs . Since, as argued in the Introduction, this is

not a feasible statistical task, we emphasized there

on the alternative, feasible goal of testing that slightly relaxed versions of stochastic

dominance hold. In the present setting, such a strategy leads to consider the problem of testing, at a given

confidence level, vs , where is a small enough prefixed

amount of disagreement with the stochastic order.

Following the scheme in [5] and [7], from the asymptotic normality obtained

in Theorem 2.4 we propose to reject if

(10)

where is an estimator of (for example a bootstrap estimator).

This rejection rule provides a consistent test of asymptotic level .

Also,

(11)

provides an upper confidence bound for with asymptotic level .

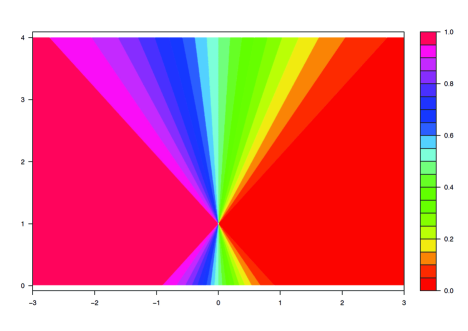

Let us take now a closer look at the index for distributions in

a location-scale family. For simplicity, we focus on normal laws. It is an elementary fact that

is invariant to changes in location and scale and we can, consequently, resctrict ourselves to the analysis of

Therefore we can obtain the values of , .

Moreover, it is easy to see that is constant when moves

along directed rays from . This fact is showed in figure 1. We see that corresponds to

, with ,

but the index can be made arbitrarily close to by taking large enough.

Finally, we present in Table 1 some simulations showing

the performance of the proposed nonparametric procedure. We see the observed

rejection rates for the test (10). In our simulations we have taken and

for several choices of . We show also the rejection rates

based on a natural competitor, the parametric maximum likelihood estimator

.

This estimator is, of course, highly nonrobust and useless in practice without the a priori knowledge that and are

normal, but we use it here as a benchmark. We see a reasonable amount of agreement of the rejection frequencies to the

nominal level of the test, even if it is slightly liberal for close to one and small , but the nonparamentric

procedure does not perform worse than the parametric benchmark. We also see that it is possible to get statistical evidence

that almost stochastic order does hold. For instance, for , (true )

sizes suffice to conclude that with probability close to .

Figure 1: Contour-plot of as in (8) for

different values of (X-axis) and (Y-axis)

Table 1: Rejection rates for

at level along 1,000 simulations. Upper

(resp. lower) rows show results for nonparametric (resp. parametric)

comparisons. For each , is chosen to make

0.01, 0.05 and 0.10 (first, second and third columns, resp.).

Sample

size

.01

100

.000

.000

.000

.053

.007

.000

.180

.009

.004

.000

.000

.000

.062

.006

.000

.112

.003

.000

1000

.004

.000

.000

.086

.000

.000

.116

.000

.000

.036

.002

.000

.086

.000

.000

.086

.000

.000

5000

.014

.000

.000

.084

.000

.000

.077

.000

.000

.078

.003

.000

.086

.000

.000

.060

.000

.000

.05

100

.013

.004

.004

.321

.060

.019

.677

.138

.028

.017

.007

.004

.382

.064

.027

.690

.086

.017

1000

.101

.017

.004

.929

.088

.003

.999

.101

.000

.219

.041

.015

.982

.087

.002

1.000

.085

.000

5000

.488

.056

.009

1.000

.067

.000

1.000

.070

.000

.704

.099

.009

1.000

.069

.000

1.000

.057

.000

.10

100

.034

.017

.006

.608

.210

.092

.930

.402

.148

.040

.022

.009

.658

.205

.073

.941

.364

.109

1000

.267

.082

.020

1.000

.545

.076

1.000

.861

.096

.431

.132

.047

1.000

.642

.076

1.000

.928

.084

5000

.867

.246

.058

1.000

.970

.056

1.000

1.000

.078

.960

.356

.087

1.000

.994

.058

1.000

1.000

.069

3 Appendix

We prove here central limit theorems for the index in (8).

We will assume that are i.i.d. random variables,

uniformly distributed on . We consider independent samples i.i.d. and

such that the d.f. of the and the are and , respectively.

We note that, without loss of generality, we can assume that the and are generated

from the and the through , .

We write , , and for the empirical d.f.’s on the , the , and the , respectively.

Note that, in particular, , . Finally, and

will denote the empirical processes associated to the and the , namely, , ,

and similarly for and we will write instead of .

We introduce the statistics , ,

, and write , , for the corresponding population counterparts.

Note that, to ensure that is finite, and should have, at least, finite

second moments. However, to simplify the arguments our proof will require bounded supports. We set

, , and define

(12)

and similarly and replacing with and , respectively. Observe that .

We this notation we have the following result.

Theorem 3.1

If and have bounded support and is continuous on then

Proof. We assume that , for

all and some .

The continuity and boundedness assumption on allows us to assume that is a continuous

function on , hence, uniformly coutinuous and its modulus of continuity,

satisfies as .

It is convenient at this point to note that is a function of the and also of and we stress this fact

writing instead of in this proof, and the same for and . Similarly, we set

, , .

We claim now that

(13)

where . To check this, let us assume first that is finitely supported,

say on with , This means that if (we set for convenience)

and we have

A similar expression holds for replacing with and we see that

We can argue analogously to check that

Hence, we see that

and (13) follows. For general take finitely supported such that , supported in .

Then, for fixed , and as . As a consequence, we conclude that

(13) holds also in this case.

Now, by the Dvoretzky-Kiefer-Wolfowitz inequality (see [16]) we have

, . This entails that is uniformly

integrable and also that vanishes in probability. Since, on the other hand,

we conclude that

(14)

as and this proves the first claim in the Theorem. For the others, we can argue as above to see

that (13) also holds if we replace and with the corresponding pairs and

or and . This completes the proof.

From Theorem 3.1 we obtain a CLT for the one-sample empirical version of .

Corollary 3.2

If and have bounded support and is continuous, then

Proof. Observe that . From Theorem 3.1, , while a.s.

Remark 3.2.1

For the two-sample analogue of Corollary 3.2 it is important to observe that the conclusion of Theorem 3.1

remains true if we replace by and .

In fact, in the finitely supported case, keeping the notation in the proof of Theorem 3.1, we have

from which we see that

in probability, since is continuous and in probability.

Similar statements are true for and .

Proof of Theorem 2.4.

Convergence in the Wasserstein distance sense is characterized through weak convergence plus convergence of second order moments. Therefore the a.s. consistency essentially follows from the strong law of large numbers (see [12] for details and more general results).

For the asymptotic law, we write . By Theorem 3.1 and Remark 3.2.1 arguing as in the proof of Corollary 3.2

we see that .

A minor modification of the proof of Corollary 3.2 yields that

with as in (12) and a U(0,1) law,

and also that and

are asymptotically independent. The result follows.

References

[1]

[2]

Álvarez-Esteban, P.C.; del Barrio, E.; Cuesta-Albertos, J.A. and Matrán, C. (2011).

Uniqueness and approximate computation of optimal incomplete transportation plans.

Ann. Inst. Henri Poincaré - Probabilités et Statistiques, 47, No. 2, 358–375.

[3]

Álvarez-Esteban, P.C.; del Barrio, E.; Cuesta-Albertos, J.A. and Matrán, C. (2012).

Similarity of samples and trimming. Bernoulli, 18, 606–634.

[4]

Álvarez-Esteban, P.C.; del Barrio, E.; Cuesta-Albertos, J.A. and Matrán, C. (2014). A contamination model for approximate stochastic order: extended version. http://arxiv.org/abs/1412.1920

[5]

Álvarez-Esteban, P.C.; del Barrio, E.; Cuesta-Albertos, J.A. and Matrán, C. (2016). A contamination model for stochastic order. Test. DOI 10.1007/s11749-016-0494-2

[6]

Álvarez-Esteban, P.C.; del Barrio, E.; Cuesta-Albertos, J.A. and Matrán, C. (2017).Wide Consensus aggregation in the Wasserstein Space. Application to location-scatter families. http://arxiv.org/abs/1511.05350

[7]

Álvarez-Esteban, P. C., del Barrio, E., Cuesta-Albertos, J. A., and Matrán, C. (2017). Models for the assessment of treatment improvement: the ideal and the feasible, 1–27. http://arxiv.org/abs/1612.01291

[8]

Berger, R.L. (1988). A Nonparametric, Intersection-Union Test for Stochastic Order. In Statistical Decision Theory and Related Topics IV. Volume 2. (eds. Gupta, S. S., and Berger, J. O.). Springer-Verlag, New York.

[9]

Boissard, E., Le Gouic, T. and Loubes, J.M. (2015). Distribution s template estimate with Wasserstein metrics. Bernoulli, 21(2), 740–759.

[10]

Carlier, G., Chernozhukov, V., and Galichon, A. (2016). Vector quantile regression: An optimal transport approach. Ann. Stat., 44(3), 1165–1192.

[11]

Chernozhukov, V., Galichon, A., Hallin, M., and Henry, M. (2014).

Monge-Kantorovich Depth, Quantiles, Ranks, and Signs. Ann. Statist., to appear.

[12]

Cuesta, J. A., and Matrán, C. (1992). A review on strong convergence of weighted sums of random elements based on Wasserstein metrics. Jour. Stat. Planning and Inference,30(3), 359–370.

[13]

Davidson, R., and Duclos, J.-Y. (2007). Testing for Restricted Stochastic Dominance, working paper, Department of Economics, McGill University.

[14]

Hodges, J.L. and Lehmann, E.L. (1954). Testing the approximate validity of statistical

hypotheses. J. R. Statist. Soc. B16, 261–268.

[15]

Lehmann, E. L. (1955). Ordered families of distributions. Ann. Math. Stat.26, 399–419.

[16] Massart, P. (1990). The tight constant in the Dvoretzky-Kiefer-Wolfowitz inequality.

Ann. Probab., 18, 1269–1283.

[17]

Leshno, M., and Levy, H. (2002). Preferred by All and Preferred by Most Decision Makers: Almost Stochastic Dominance. Management Science, 48(8), 1074 1085.

[18]

Rippl, T., Munk, A., and Sturm, A. (2016).

Limit laws of the empirical Wasserstein distance: Gaussian distributions. J. Multiv. Anal. 151, 90–109.