Pricing Variance Swaps on Time-Changed Markov Processes

Abstract

We prove that the variance swap rate (fair strike) equals the price of a co-terminal European-style contract when the underlying is an exponential Markov process, time-changed by an arbitrary continuous stochastic clock, which has arbitrary correlation with the driving Markov process, provided that the payoff function of the European contract satisfies an ordinary integro-differential equation, which depends only on the dynamics of the Markov process, not on the clock. We present examples of Markov processes where the function that prices the variance swap can be computed explicitly. In general, the solutions are not contained in the logarithmic family previously obtained in the special case where the Markov process is a Lévy process.

Keywords: Variance swap, Time change, Markov process

1 Introduction

Consider a forward price that evolves in continuous time. Let time zero be the valuation time for a derivative security written on the path of , with a fixed maturity date . Assume that is a known constant, and that the process is strictly positive over a time interval . As a result, the price process is well-defined, and derivative securities expiring at can also be written on the path of . In particular, we focus on a continuously-monitored variance swap, which pays the difference between the terminal quadratic variation of the price process and a constant determined at inception. For brevity, we will refer to a continuously monitored variance swap as a VS in the sequel. As with any swap, the constant that is determined at inception is chosen so that there is no initial cost of entering into the VS. The objective of this paper is to give additional conditions on the dynamics of under which this constant can be determined from an initial observation of the -maturity implied volatility smile.

Earlier papers by Neuberger (1990) and Dupire (1993) show that continuity of suffices for pricing a VS relative to the co-terminal smile. Carr et al. (2012) weakens the continuity hypothesis by showing that the price can be specified as a Lévy process running on an unspecified continuous clock. When the Lévy process is specified as Brownian motion with drift , the earlier results of Neuberger (1990) and Dupire (1993) arise as a special case. The more general formulation of Carr et al. (2012) allows for the variance and jump-intensity to depend on the level of through a local time-change (see Remark 4.3). However, the local variance and Lévy kernel must have the same functional dependence on (up to a scaling constant). Additionally, while the arrival rate of each jump size in is allowed to depend on the level of , the ratio of the arrival rates at any two jump sizes is constant in that previous paper.

This paper weakens the stationary independent increments property of the Lévy process used by Carr et al. (2012). We allow that could be specified as a time-homogeneous Markov process running on an unspecified continuous clock. As a result (i) the variance and jump-intensity may have distinct -dependence and (ii) the ratio of the arrival rates at any two jump sizes of can depend on the current level of .

In effect, we allow the background process to have nearly the full generality of general Markov processes whose jump times are not predictable, as discussed in Remark 2.1. We allow that general background Markov process to undergo a time-change by an unspecified continuous stochastic clock which may have arbitrary correlation or dependence on the background process. In this setting, we prove that European-style payoff functions price the variance swap, in the sense that the variance swap rate (fair strike) equals the price of a contract paying , provided that satisfies an ordinary integro-differential equation that depends only on the dynamics of the Markov driver, not on the clock.

Our results are related to the semiparametric approach taken by Lorig et al. (2016), who consider the pricing of a VS when the underlying forward price is modeled as Feller diffusion time-changed by an unspecified Lévy subordinator. For fully parametric approaches to VS pricing in models with jumps and stochastic volatility we refer the reader to Itkin and Carr (2010); Wendong and Kuen (2014); Filipović et al. (2016); Cui et al. (2017). For model-independent bounds on (discrete and continuous) VS prices see Hobson and Klimmek (2012), Nabil (2014), and Henry-Labordère and Touzi (2016, Example 5.7).

The rest of this paper proceeds as follows. Section 2 specifies dynamics for the forward price process and verifies that these dynamics can arise from time-changing the solution of a stochastic differential equation. Section 3 states and proves our main result (Theorem 3.5), which establishes that the VS has the same value as a European-style claim whose payoff function solves an ordinary integro-differential equation (OIDE). Section 4 provides examples of price dynamics for which we can solve the OIDE explicitly. Section 5 concludes.

2 Time-changed Markov dynamics

2.1 Assumptions

With respect to a (“calendar-time”) filtration on a probability space , assume that is a semimartingale with predictable characteristics , relative to a truncation function (to be definite, let ), which satisfy

| (2.1) |

where is a real-valued continuous increasing adapted process that is null at zero, is a Borel function, and for each fixed the is a Lévy measure, and

| (2.2) |

with

| (2.3) |

The intuition of the Lévy kernel or transition kernel is that it assigns, to each point in the state space, a “local” Lévy measure . Jumps of size in any interval arrive with intensity when is at .

2.2 Time-change of an SDE solution

This section verifies that the assumptions of Section 2.1 hold in the case that comes from time-changing the solution of a stochastic differential equation (SDE) driven by a Brownian motion and a Poisson random measure. With respect to a filtration (the “business time” filtration), consider a Brownian motion , and a Poisson random measure with intensity measure for some Lévy measure . Assume that is a semimartingale that satisfies

| (2.5) |

where is a bounded Borel function, is given by

| (2.6) |

and is a Borel function such that , defined for each Borel set by

| (2.7) |

satisfies

| (2.8) |

Then by Jacod and Shiryaev (1987, Prop. III.2.29), the semimartingale characteristics of are , where

| (2.9) |

with defined in (2.3).

Now let be a continuous increasing family of finite -stopping times (which are not assumed to be independent of ). Let the “calendar-time” filtration be defined by , and let

| (2.10) |

By Kallsen and Shiryaev (2002b, Lemma 5), the -characteristics of are where , and is determined by

| (2.11) |

for general Borel sets and . By the first two equalities in (2.9) we have

| (2.12) |

and, by substituting the last equality in (2.9) into (2.11) and changing variables to , we have

| (2.13) |

Therefore satisfy (2.1). This verifies the hypotheses of Section 2.1, as claimed.

Remark 2.1.

Time-changes of SDE solutions are nearly as general as time-changes of general Markov processes whose jump times are not predictable.

To be precise, Çinlar and Jacod (1981) show that every strong Markov quasi-left-continuous semimartingale (which includes every Feller semimartingale) is a continuous time change of an SDE solution driven by Brownian motion and a Poisson random measure (on an enlarged probability space if needed). Thus, if is a continuous time-change of a general Feller semimartingale , then by Çinlar-Jacod, is a continuous time change of an SDE solution , and therefore is a continuous time change of an SDE solution .

2.3 Notations

Let denote the class of -times continuously differentiable functions, and define the integro-differential operator by

| (2.14) | ||||

| (2.15) |

for all such that for all .

In more concise notation,

| (2.16) |

where is the shift operator defined by . This use of to express translations in the jump part of the generator follows Itkin and Carr (2012).

Let denote the union of and the following set: all functions whose derivative is everywhere absolutely continuous, and whose second derivative (which therefore exists a.e.) is equal (a.e.) to a bounded function, which we will still denote by or .

Thus the definition of extends, by relaxing the condition to , which still defines uniquely, up to sets of measure zero, via (2.15).

3 Variance swap pricing

In what follows, each will denote a constant (non-random and non-time-varying). Different instances of , even in the same expression, may have different values.

Lemma 3.1.

Suppose that and there exists such that

| and | (3.1) |

Then is a special semimartingale.

Proof.

By the form of Itô’s rule in, for instance Protter (2004, Theorem IV.70), is a semimartingale.

By Kallsen and Shiryaev (2002a, Lemma 2.8), it suffices to check that the predictable process

| (3.2) |

is finite (hence of finite variation, as it is increasing in ).

In the case , we have . In the case , we have

| (3.3) |

In this case, for each , let be such that for all , and let because is càdlàg. Then

| (3.4) |

is bounded in case by , and in case by times

| (3.5) | |||

| (3.6) |

These upper bounds do not depend on , which verifies that (3.2) is finite. ∎

Lemma 3.2.

If then .

Proof.

Let . We have due to (2.2) and .

Defining by

| (3.7) |

we have, by Jacod and Shiryaev (1987, Proposition II.2.29), that is a local martingale satisfying

| (3.8) |

because . By Burkholder-Davis-Gundy, , which implies the result. ∎

Lemma 3.3.

Suppose is bounded and satisfies

| (3.9) |

Let

| (3.10) | ||||

| (3.11) |

Then is a martingale, and

| (3.12) |

Proof.

Let be the integer-valued random measure associated with the jumps of . Let .

By Kallsen and Shiryaev (2002a, Theorem 2.19), the process is the stochastic exponential of the local martingale

| (3.13) |

where is the continuous martingale part of . By the boundedness of and assumptions (2.2) and (3.9), it follows that

| (3.14) |

is bounded. So by Lepingle and Mémin (1978), the process is a martingale and , which implies (3.12) because is bounded. ∎

Let us define two conditions that may be satisfied by where . The first is

| (3.15) |

and the second is

| (3.16) |

Lemma 3.4.

Proof.

We prove for the case that the satisfies (3.15) or (3.16). The case that is the sum of such functions follows immediately by linearity.

To show that is a local martingale, note that Jacod and Shiryaev (1987, Theorem II.2.42c) extends as follows. They assume bounded, only to show that is a special semimartingale, but the conditions in Lemma 3.1 suffice for that conclusion. Moreover they assume , only to use Itô’s lemma, but suffices here, by Protter (2004, Theorem IV.70) and its first corollary.

To show that is a true martingale, it suffices, by Protter (2004, Theorem I.51), to show that . In case (3.15), let . In both cases, by (2.2), we have

| (3.18) |

and by Taylor’s theorem and for , we have

| (3.19) |

and by (2.2),

| (3.20) |

where each does not depend on . Combining (3.18), (3.19), (3.20), and the bounds on and , we have

| (3.21) |

which is integrable in case (3.15) because , and in case (3.16) by Lemma 3.3. The remaining component of has magnitude

| (3.22) |

In conclusion, we relate to the value of a European-style contract:

Theorem 3.5.

Assume that the forward price , the log-price , and the clock satisfy the assumptions of Section 2.1. Assume that is a sum of finitely many functions, each of which satisfies (3.15) or (3.16), and that satisfies (for a.e. )

| (3.23) |

Then prices the variance swap, meaning that

| (3.24) |

Thus, if is a martingale measure for VS and contracts, then the fair strike of the VS (equivalently: the forward price of the floating leg of the VS) is (3.24).

Remark 3.6.

The sum of finitely many functions is more general than a single function; for instance, may be the sum of two functions, one satisfying (3.16) for some , and the other for some .

Remark 3.7.

Functions that satisfy the conditions of Theorem 3.5, and therefore price the VS, are not unique. Indeed, if does, then so does , where are any constants. Adding the latter two terms does not affect the valuation , because .

Proof of Theorem 3.5.

Theorem 3.5 allows us to value a VS relative to the -maturity implied volatility smile as follows:

| (3.29) |

A the amount agreed upon at time to pay at time when taking the long side of a variance swap.

B the value of a European contract with payoff .

C the value of zero-coupon bonds.

As shown in Carr and

Madan (1998), if is a difference of convex functions, then for any we have

| (3.30) |

Here, is the left-derivative of , and is the second derivative, which exists as a generalized function. Taking expectations,

| (3.31) |

where and are, respectively, the prices of put and call options on with strike and expiry . Knowledge of and the -expiry smile implies knowledge of the initial prices of -expiry European options at all strikes . Thus the quantity B in (3.29) is uniquely determined from the -expiry volatility smile by applying (3.31) to , assuming one can determine the function . Therefore, to price a VS relative to co-terminal calls and puts, what remains is to find a solution of the OIDE (3.23).

4 Examples

In this section we provide examples, in the setting of Section 2.2, of local variance and Lévy kernel pairs , such that solutions of OIDE (3.23) can be obtained explicitly. In one of the examples, moreover, we investigate the ratio between the values of the VS and the log contract.

4.1 Constant relative jump intensity

Theorem 4.1.

Assume the local variance and Lévy kernel are of the form

| (4.1) |

where is a constant, is a Lévy measure, and is a positive bounded Borel function. Assume . Then

| (4.2) |

prices the variance swap, where

| (4.3) |

Remark 4.2.

In particular, the constant in two extreme cases is as follows

| (4.4) | |||||

| (4.5) |

Remark 4.3.

Dynamics of this form arise by time-changing a Lévy process using the clock

| (4.6) |

See, for instance, Küchler and Sørensen (1997, Proposition 11.6.1). Thus the payoff function (4.2) in this case should, and indeed does, match the payoff function obtained by Carr et al. (2012) for time-changed Lévy processes.

4.2 Fractional linear relative jump intensity

Let satisfy

| and | (4.7) |

Let

| (4.8) |

Let and satisfy .

Let be a positive, bounded, Borel function, and let

| (4.10) |

Lemma 4.4.

The function is positive and bounded.

Proof.

To show that the denominator from (4.10) has a positive lower bound, first note that

| (4.11) |

where the first two expressions are the denominator for and respectively.

For , the denominator is bounded below by , so just subtract from (4.11). For the denominator is bounded below by

| (4.12) |

Next, to show that the numerator from (4.10) is positive and bounded, we verify in three intervals. For , the numerator is , and is moreover bounded above. In the other two intervals, the result follows from

| (4.13) |

where the first two expressions are the numerator for and respectively. ∎

Theorem 4.5.

Remark 4.6.

We describe these dynamics as “fractional linear relative jump intensity” because, for , the relative jump intensity

| (4.15) |

is a ratio of polynomials linear in the underlying log-price.

4.3 Lévy mixture with state-dependent weights

Assume the local variance and Lévy kernel are of the form

| (4.16) |

where and are Lévy measures with

| (4.17) |

Let us first derive a candidate solution to (3.23) from an ansatz and then verify the validity of the solution.

Inserting the expressions for and from (4.16) into (3.23) and dividing by , we have

| (4.18) |

where and are constants defined by

| (4.19) |

and, using the notation of (2.16), the operators and are given by

| (4.20) | ||||

| (4.21) |

Assume a solution of (4.18) has a power series expansion in :

| (4.22) |

where the functions are, at this point, unknown. Inserting the expansion (4.22) into OIDE (4.18) and collecting terms of like order in results in the following sequence of nested OIDEs:

| (4.23) | |||||||

| (4.24) | |||||||

| (4.25) | |||||||

Noting that

| (4.26) | ||||||||

| (4.27) |

one can easily verify, by direct substitution into (4.24), a solution given by

| (4.28) |

and solutions given, for , by

| (4.29) |

Thus we have a formal series expansion, defined by (4.22), (4.28) and (4.29), for a function that solves OIDE (3.23). The following conditions suffice for validity of this expansion.

Theorem 4.7.

Proof.

The summation in (4.22) can be written as

| (4.31) |

The infinite sum is a power series in , with coefficients satisfying, by (4.30),

| (4.32) |

which implies that the sum in (4.31) has infinite radius of convergence, and is well-defined on by (4.22), with (4.28) and (4.29). As every power series can be differentiated and integrated term-by-term within its radius of convergence, solves OIDE (3.23). ∎

Remark 4.8.

If , , , and (respectively, ), then any Lévy measure with support on the positive (resp. negative) axis will satisfy (4.30).

Remark 4.9.

If , , , and (respectively, ), then a Lévy measure will satisfy (4.30) only if the support of lies strictly within the negative (resp. positive) axis.

Remark 4.10.

In the particular case where the forward price is a time-change of an exponential Lévy process with variance and Lévy measure , the function prices the VS. In the more general class of models in (4.16), which can be seen as a regular -perturbation around the time-changed exponential Lévy case, the candidate function for pricing the VS by Theorem 3.5 becomes, by (4.31), a -perturbation around .

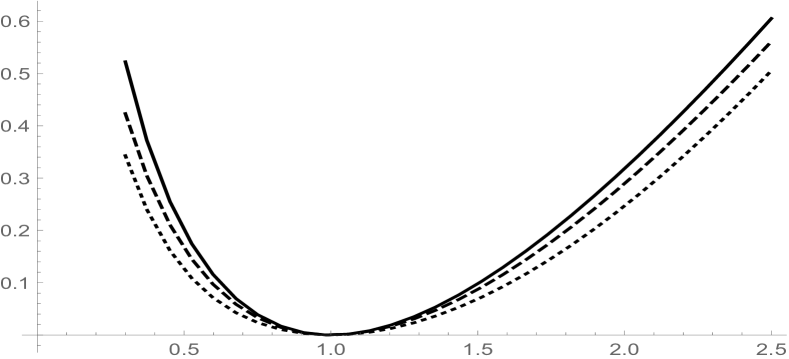

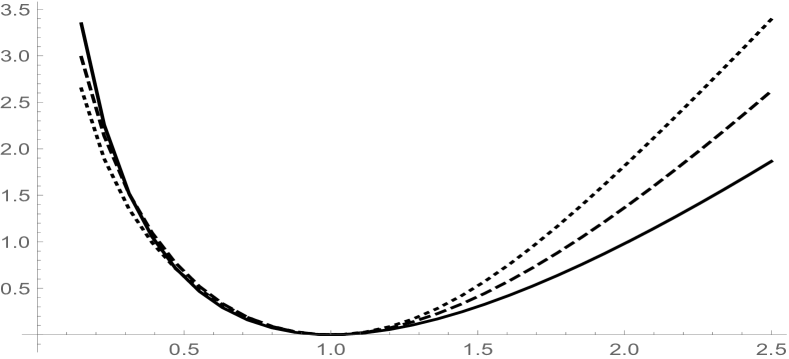

In Figures 1 and 2, using a variety of different model parameters, we plot

| (4.33) |

as a function of , where is defined by (4.22), (4.28) and (4.29). Note that, if prices the VS, then prices the VS for any constant . The particular value of in (4.33) ensures that .

4.3.1 Ratio of the VS value to the contract value

Although the purpose of this paper is to compute the value of a VS relative to the contract (and to solve for ), it is interesting to compute the ratio of the value of the VS to the value of a European contract. To this end, for a function that prices a VS, let

| (4.34) |

In Carr et al. (2012) the authors find that if where is a Lévy process, then the ratio is a constant which is independent of the initial value of the underlying and the time to maturity (see Theorem 4.1 and Remark 4.3 of Section 4.1). This is in contrast to empirical results from the same paper, which show in a study of S&P500 data that the ratio is not constant. In the more general time-changed Markov setting considered in the present paper, the ratio can (in general) depend on the current value of the underlying and the time to maturity . Below, we derive a formal approximation for the ratio for one specific example of which is of the form (4.16).

Assumption 4.11.

Throughout this section, we assume where is a continuous time change independent of and the Laplace transform is known. Let the Markov process have local variance and Lévy kernel of the form (4.16) with

| (4.35) |

where . Assume moreover that the Lévy measure satisfies the conditions of Theorem 4.7. Thus, the function , defined by (4.22), (4.28) and (4.29), solves (3.23) . In accordance with Remark 4.9, jumps must be downward, i.e., .

We compute an approximation for in three Steps, described below.

Step 1.

Derive an approximation for .

Formally, the function satisfies the Kolmogorov backward equation

| (4.36) |

where , the generator of , is given by

| (4.37) |

Now, suppose that the function has a power series expansion in

| (4.38) |

where the functions are unknown. Inserting expressions (4.37) and (4.38) into (4.36) and collecting terms of like powers of , we obtain a sequence of nested partial integro-differential equations (PIDEs) for the unknown functions

| (4.39) | |||||||||

| (4.40) | |||||||||

The solution to this nested sequence of PIDEs is given in Jacquier and Lorig (2013, Equation (5.2)). We have

| (4.41) |

where an empty product is defined to equal one and denotes the distributional generalization of the Fourier transform defined for integrable functions by

| (4.42) |

Inserting expression (4.41) into the sum (4.38) and truncating at order yields , our order approximation of . Explicitly,

| (4.43) | ||||

| (4.44) |

Step 2.

Step 3.

Derive an approximation for .

With as given in Theorem 4.7, we have

| (4.48) | ||||

| (4.49) | ||||

| (4.50) | ||||

| (4.51) | ||||

| (4.52) |

where Id is the identity function . Replacing the function wherever it appears in (4.51) by and truncating the infinite sum at terms produces , our order approximation of . Explicitly,

| (4.53) |

The Fourier transforms of the complex exponential () and the identity function Id, as needed to compute and in (4.53), are given by

| (4.54) |

where and denote the Dirac delta function and its derivative, understood in the sense of distributions. Inserting (4.54) into (4.47) and integrating produces closed-form expressions for both and .

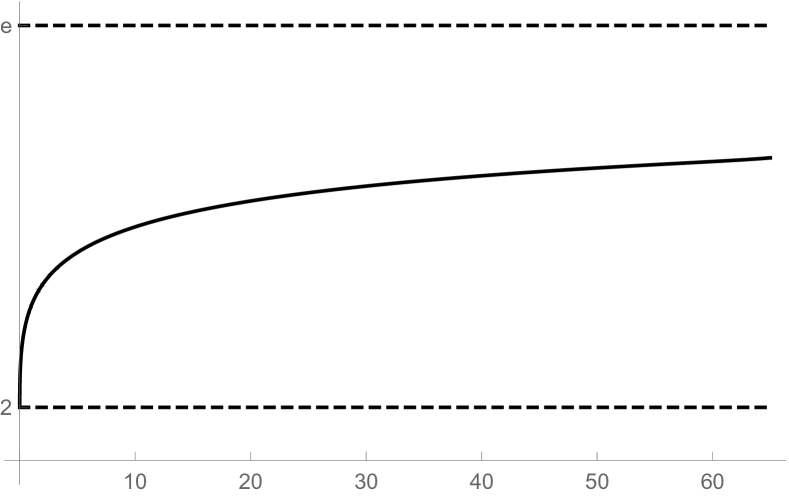

Figure 3 plots as a function of .

5 Conclusion

In Carr et al. (2012), the authors model the forward price as the exponential of a Lévy process time-changed by a continuous increasing stochastic clock. In this setting, they show that a variance swap has the same value as a fixed number of European contracts. The exact number of contracts that price the variance swap depends only on the dynamics of the driving Lévy process, irrespective of the time-change.

This paper generalizes the underlying forward price dynamics to time-changed exponential Markov processes, where the background process may have a state-dependent (i.e., local) volatility and Lévy kernel, and where the stochastic time-change may have arbitrary dependence or correlation with the Markov process. In the time-changed Markov setting, we prove that the variance swap is priced by a European-style contract whose payoff depends only on the dynamics of the Markov process, not on the time-change. We explicitly compute the payoff function that prices the variance swap for various driving Markov processes. When the Markov process is a Lévy process we recover the results of Carr et al. (2012).

For certain Markov processes, we also compute directly from model parameters an approximation for valuation of European-style contracts, showing the variation in the ratio of the VS value to the contract value as a function of the current level of the underlying. This is in contrast to Carr et al. (2012), who show in the more restrictive time-changed Lévy process setting that this ratio is constant.

Thanks

The authors are grateful to Feng Zhang and Stephan Sturm for their helpful comments.

References

- Carr et al. (2012) Carr, P., R. Lee, and L. Wu (2012, 4). Variance swaps on time-changed Lévy processes. Finance and Stochastics 16(2), 335–355.

- Carr and Madan (1998) Carr, P. and D. Madan (1998). Towards a theory of volatility trading. In Volatility: new estimation techniques for pricing derivatives, pp. 417–427. Risk Books.

- Çinlar and Jacod (1981) Çinlar, E. and J. Jacod (1981). Representation of semimartingale Markov processes in terms of Wiener processes and Poisson random measures. In Seminar on Stochastic Processes, 1981, Volume 1 of Progress in Probability and Statistics, pp. 159–242. Birkhäuser Boston.

- Cui et al. (2017) Cui, Z., J. L. Kirkby, and D. Nguyen (2017). A general framework for discretely sampled realized variance derivatives in stochastic volatility models with jumps. European Journal of Operational Research 262(1), 381 – 400.

- Dupire (1993) Dupire, B. (1993). Model art. Risk 6(9), 118–124.

- Filipović et al. (2016) Filipović, D., E. Gourier, and L. Mancini (2016). Quadratic variance swap models. Journal of Financial Economics 119(1), 44 – 68.

- Henry-Labordère and Touzi (2016) Henry-Labordère, P. and N. Touzi (2016, 7). An explicit martingale version of the one-dimensional Brenier theorem. Finance and Stochastics 20(3), 635–668.

- Hobson and Klimmek (2012) Hobson, D. and M. Klimmek (2012, 10). Model-independent hedging strategies for variance swaps. Finance and Stochastics 16(4), 611–649.

- Itkin and Carr (2010) Itkin, A. and P. Carr (2010). Pricing swaps and options on quadratic variation under stochastic time change models – discrete observations case. Review of Derivatives Research 13(2), 141–176.

- Itkin and Carr (2012) Itkin, A. and P. Carr (2012). Using pseudo-parabolic and fractional equations for option pricing in jump diffusion models. Computational Economics 40(1), 63–104.

- Jacod and Shiryaev (1987) Jacod, J. and A. N. Shiryaev (1987). Limit theorems for stochastic processes, Volume 288. Springer-Verlag Berlin.

- Jacquier and Lorig (2013) Jacquier, A. and M. Lorig (2013). The smile of certain Lévy-type models. SIAM Journal on Financial Mathematics 4(1), 804–830.

- Kallsen and Shiryaev (2002a) Kallsen, J. and A. Shiryaev (2002a). The cumulant process and esscher’s change of measure. Finance and Stochastics 6(4), 397–428.

- Kallsen and Shiryaev (2002b) Kallsen, J. and A. Shiryaev (2002b). Time change representation of stochastic integrals. Theory of Probability & Its Applications 46(3), 522–528.

- Küchler and Sørensen (1997) Küchler, U. and M. Sørensen (1997). Exponential families of stochastic processes, Volume 3. Springer Science & Business Media.

- Lepingle and Mémin (1978) Lepingle, D. and J. Mémin (1978). Sur l’intégrabilité uniforme des martingales exponentielles. Probability Theory and Related Fields 42(3), 175–203.

- Lorig et al. (2016) Lorig, M., O. Lozano-Carbassé, and R. Mendoza-Arriaga (2016). Variance swaps on defaultable assets and market implied time-changes. SIAM Journal on Financial Mathematics 7(1), 273–307.

- Nabil (2014) Nabil, K. (2014). Model-independent lower bound on variance swaps. Mathematical Finance 26(4), 939–961.

- Neuberger (1990) Neuberger, A. (1990). Volatility trading. Working paper: London Business School.

- Protter (2004) Protter, P. (2004). Stochastic integration and differential equations, Volume 21. Springer Verlag.

- Wendong and Kuen (2014) Wendong, Z. and K. Y. Kuen (2014). Closed form pricing formulas for discretely sampled generalized variance swaps. Mathematical Finance 24(4), 855–881.