Learning Vector Autoregressive Models with Latent Processes

Abstract

We study the problem of learning the support of transition matrix between random processes in a Vector Autoregressive (VAR) model from samples when a subset of the processes are latent. It is well known that ignoring the effect of the latent processes may lead to very different estimates of the influences among observed processes, and we are concerned with identifying the influences among the observed processes, those between the latent ones, and those from the latent to the observed ones. We show that the support of transition matrix among the observed processes and lengths of all latent paths between any two observed processes can be identified successfully under some conditions on the VAR model. From the lengths of latent paths, we reconstruct the latent subgraph (representing the influences among the latent processes) with a minimum number of variables uniquely if its topology is a directed tree. Furthermore, we propose an algorithm that finds all possible minimal latent graphs under some conditions on the lengths of latent paths. Our results apply to both non-Gaussian and Gaussian cases, and experimental results on various synthetic and real-world datasets validate our theoretical results.

Introduction

Identifying causal influences among time series is a problem of interest in many fields. In macroeconomics, for instance, researchers seek to understand what factors contribute to economic fluctuations and how they interact with each other (?). In neuroscience, many researchers focus on learning the interactions between different regions of brain by analyzing neural spike trains (?; ?; ?).

Granger causality (?), transfer entropy (?), and directed information (?; ?) are some of the most commonly used measures in the literature to calculate time-delayed dependence structures in time series. Measuring the reduction of uncertainty in one variable after observing another variable is the key concept behind such measures. Under certain assumptions, these measures may represent causal relations among the variables (?; ?). In (?), an overview of various definitions of causation is given for time series.

In this work, we study the causal identification problem in VAR models when only a subset of times series is observed. More precisely, we assume that the available measurements are a set of random processes which, together with another set of latent random processes , where form a first order VAR model as follows:

| (1) |

Here we assume that observed data were measured at the right causal frequency of the VAR process; otherwise one may need to consider the effect of the sampling procedure such as subsampling or temporal aggregation (?; ?; ?). Under certain assumptions (e.g., causal sufficiency), the support of the transition matrix corresponds to the causal structure between these processes (?; ?; ?). If we ignore the influence of latent processes and just regress on , we may get a wrong estimate of the transition matrix between observed processes (see the example in (?)). Hence, it is crucial to consider the presence of latent processes and their influences on the observed processes.

Contributions: The contributions of this paper are as follows: we propose a learning approach that recovers the observed sub-network (support of ) by regressing the observed vector on a set of its past observations (not just ) as long as the graph representation of latent sub-network (support of ) is a directed acyclic graph (DAG). We also derive a set of sufficient conditions under which we can uniquely recover the influences from latent to observed processes, (support of ) and also the influences among the latent variables, (support of ). Additionally, we propose a sufficient condition under which the support of the complete transition matrix can be recovered uniquely.

More specifically, we show that under an assumption on the observed to latent noise power ratio, if neither of the sub-matrices and are zero, it is possible to determine the length of all directed latent paths111A directed path is a latent path if it connects two observed variables and all the intermediate variables on that path are latent.. We refer to this information as linear measurements222This is because it can be inferred from the observational data using linear regression.. This information reveals important properties of the causal structure among the latent and observed processes, i.e., support of . We call this sub-network of a VAR model unobserved network. We show that in the case that the unobserved network is a directed tree and each latent variable has at least two parents and two children, a straightforward application of (?) can recover the unobserved network uniquely. Furthermore, we propose Algorithm 1 that recovers the support of and given the linear measurements when only the latent sub-network is a directed tree plus some extra structural assumptions (see Assumption 2). Lastly, we study the causal structures of VAR models in a more general case in which there exists at most one directed latent path of length between any two observed processes (see Assumption 3). For such VAR models, we propose Algorithm 2 that can recover all possible unobserved networks with minimum number of latent processes. Our results apply to both non-Gaussian and Gaussian cases, and experimental results on various synthetic and real-world datasets validate our theoretical results. All proofs can be found in supplemental material.

Related works: The problem of recovering latent causal structure for time series has been studied in the literature. Assuming that connections between observed variables are sparse and each latent variable interacts with many observed variables, it has been shown that the transition matrix between observed variables can be identified in a VAR model (?). However, their approach focuses on learning only the observed sub-network. (?) applied a method based on expectation maximization (EM) to infer properties of partially observed Markov processes, without providing theoretical analysis for identifiability. (?) showed that if the exogenous noises are independent non-Gaussian and additional so-called genericity assumptions hold, then the sub-networks and a part of are uniquely identifiable. However, these assumptions may not hold true in a real-world dataset even with three variables (?). They also presented a result in which they allowed Gaussian noises in their VAR model and obtained a set of conditions under which they can recover up to candidate matrices for . Their learning approach is also based on EM and approximately maximizes the likelihood of a parametric VAR model with a mixture of Gaussians as noise distribution. Recently, (?) studied a network of processes (not necessary a VAR model) whose underlying structure is a polytree and introduced an algorithm that can learn the entire casual structure (observed and unobserved networks) using a particular discrepancy measure.

Compared to related works, we improve the state of the art for latent recovery by showing the identifiability of a much larger class of structures. Unlike (?), we do not assume the non-Gaussian distribution of the exogenous noises or those genericity assumptions. Moreover, our results do not rely on the assumption that connections between observed variables are sparse or each latent variables interacts with many observed variables as in (?). Furthermore, these works (?; ?) can uniquely identify at most a part of transition matrix ( or a part of ).

Problem Definition

In this part, we review some basic definitions and our notation. Throughout this paper, we use an arrow over the letters to denote vectors. We assume that the time series are stationary and denote the autocorrelation of by . We denote the support of a matrix by and use to indicate whenever . We also denote the Fourier transform of by and it is given by .

In a directed graph with the node set and the edge set , we denote the set of parents of a node by and the set of its children by . The skeleton of a directed graph is the undirected graph obtained by removing all the directions in .

System Model

Consider the VAR model in (1). Let and be i.i.d random vectors with mean zero. For simplicity, we denote the matrix by . Our goal is to recover from observational data, i.e., . Rewrite 1 as follows

| (2) |

where , for , and .

Assumption 1.

We assume that the is acyclic, i.e., , such that .

Based on the above assumption, for , Equation (System Model) becomes333Note that the limits of summations in (3) are changed.

| (3) |

We are interested in recovering the set because it captures important information about the structure of the VAR model. Specifically, ; so it represents the direct causal influences between the observed variables and for determines whether at least one directed path of length exists between any two observed nodes which goes through the latent sub-network.444Herein, we exclude degenerate cases where there is a direct path from an observed node to another one with length but the corresponding entry in matrix is zero. In fact, such special cases can be resolved by small perturbation of nonzero entries in matrix . In the causal discovery literature, this assumption is known as faithfulness (?). We will make use of this information in our recovery algorithm. We call the set of matrices , linear measurements. In Section 4, we present a set of sufficient conditions under which given the linear measurements, we can recover the entire or most parts of the unobserved network uniquely. Learning the Unobserved Network

Note that in general, the linear measurements cannot uniquely specify the unobserved network. For example, Figure 1 illustrates two different unobserved networks that both share the same set of linear measurements, for and the only nonzero entries of and are and , respectively.

Identifiability of the Linear Measurements

As we need the linear measurements for our structure learning, in this section, we study a sufficient condition under which we can recover the linear measurements from the observed processes . To do so, we start off by rewriting Equation (3) as follows,

| (4) |

where , and By projecting onto the vector space spanned by the observed processes, i.e., , we obtain

| (5) |

where denote the residual terms and are the corresponding coefficient matrices. Substituting (5) into (4) implies

| (6) |

where , and Note that by this representation, is orthogonal to . Hence, Equation (6) shows that the minimum mean square error (MMSE) estimator can learn the coeffiecient matrix given the observed processes. More precisely, let , then we have

| (7) |

This result implies that we can asymptotically recover the support of as long as the absolute values of non-zero entries of are bounded away from zero by . Please note that if . In Appendix (the second section), we explained how these bounds can be estimated from observational data.

Proposition 2.

Let and be the autocovariance matrices of and , respectively. Then, the ratio strictly increases by decreasing .

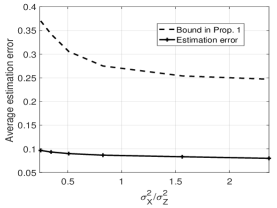

Proposition 2 implies that when the increases, will decrease, and based on the bound in Proposition 1, the estimation error will decrease (it goes to zero as tends to infinity). This shows that recovering the linear measurements is much easier in high regime as illustrated in Figure 3b. Note that Proposition 1 stresses a suffiecient condition for recovering the linear measurements. As shown in Figure 3b, in practice, the actual estimation error is much smaller than the bound in Proposition 1. In the next section, we will make use of to recover the unobserved network. We assume that the correct linear measurements can be obtained from matrix .

In order to estimate the support of matrix from a finite number of samples drawn from the observed processes, say , first we obtain the lag length in (6) by AIC or FPE criterion (see Chapter 4 in (?)). Afterwards, we can estimate the coefficient matrix , using an empirical estimator for , , and then applying (7). Denote the result of this estimation by . It can be shown that (?), where denotes convergence in distribution, and is the autocovariance matrix of . transforms a matrix to a vector by stacking its columns and is the Kronecker product. Having the estimates of and , we can test whether the entries of matrix are greater than the bounds in Proposition 1 (see Chapter 3 in (?)).

Learning the Unobserved Network

Recall that we refer to as the unobserved network and as the latent sub-network. We present three algorithms that take the linear measurements as their input. The first algorithm recovers the entire unobserved network uniquely as long as it is a directed tree and each latent node has at least two parents and two children. The output of the second algorithm is , where . This is guaranteed whenever the latent sub-network is a directed tree and some extra conditions are satisfied on how the latent and observed nodes are connected. The third algorithm finds the set of all possible networks with minimum number of latent nodes that are consistent with the measurements. This algorithm is able to do so when there exists at most one directed latent path of any arbitrarily length between two observed nodes. A directed path is latent if all the intermediate variables on that path are latent.

Unobserved Network is a Directed Tree

Authors in (?) introduced a necessary and sufficient condition for recovering a weighted directed tree uniquely from a valid distance matrix defined on the observed nodes,555The skeleton of the recovered tree is the same as the original one but not necessary the weights. and also proposed a recovery algorithm. The condition is as follows: every latent node must have at least two parents and two children. A matrix , in (?), is a valid distance matrix, when equals the sum of all the weights of those edges that belong to the directed path from to , and , if there is no directed path.

The algorithm in (?) has two phases. In the first phase, it creates a directed graph among the observed nodes with the adjacency matrix . In the second phase, it recursively finds and removes the circuits by introducing latent nodes for each circuit.666In a directed graph, a circuit is a cycle after removing all the directions. For more details, see (?).

In order to adopt (?)’s algorithm for learning the unobserved network, we introduce a valid distance matrix using our linear measurements as follows, if and 0, otherwise. Recall that indicates whether there exists a directed latent path from to of length in the unobserved network. From theorem 8 in (?), it is easy to show that the unobserved network can be recovered uniquely from above distance matrix if its topology is a directed tree and every latent node has at least two parents and two children.

Latent Sub-network Is a Directed Tree

Definition 1.

We denote the subset of observed nodes that are parents of a latent node by and denote the subset of observed nodes for which is a parent, by . We further denote the set of all leaves in the latent sub-network by .

We consider learning an unobserved network that satisfies the following assumptions.

Assumption 2.

Assume that the latent sub-network of is a directed tree. Furthermore, for any latent node in , (i) and, (ii) if is a leaf of the latent sub-network, then .

This assumption states that the latent sub-network of must be a directed tree such that each latent node in has at least one unique parent in the set of observed nodes. That is, a parent who is not shared with any other latent node. Furthermore, each latent leaf has at least one unique child among the observed nodes. For instance, when represents a directed tree and both and contain identity matrices, Assumption 2 holds. As we will see later in Experimental Results (Figure 3c), a large portion of randomly generated graphs satisfy Assumption 2.

Figure 2e illustrates a simple network that satisfies Assumption 2 in which the unique parents of latent nodes , and are , , , and , respectively. The unique children of latent leaves and are and , respectively.

Theorem 1.

Note that if Assumption 2 is violated, one can find many unobserved networks that are consistent with the linear measurements but are not minimum (in terms of the number of latent nodes). For example, the network in Figure 2a satisfies Assumption 2 (ii) but not (i). Figure 2b depicts an alternative network with the same linear measurements as the network in Figure 2a but it has fewer number of latent nodes. Similarly, the graph in Figure 2c satisfies Assumption 2 (i) but not (ii). Figure 2d shows an alternative graph with one less latent node.

Theorem 2.

Consider an unobserved network with adjacency matrix . If satisfies Assumption 2, then its corresponding linear measurements uniquely identify upto , where .

Figure 2e gives an example of a network satisfying Assumption 2 and an alternative network, Figure 2f, with the same linear measurements which departs from the Figure 2e in the component.

Next, we propose the directed tree recovery (DTR) algorithm that takes the linear measurements of an unobserved network satisfying Assumption 2 and recovers upto the limitation in Theorem 2. This algorithm consists of three main loops. Recall that Assumption 2 implies that each latent node has at least one unique observed parent. The first loop finds all the unique observed parents for each latent node (lines: 4-11). The second loop reconstructs and (lines: 12-17). And finally, the third loop constructs such that (lines: 18-22).

The following lemma shows that the first loop of Algorithm 1 can find all the unique observed parents from each latent node. To present the lemma, we need the following definitions.

Definition 2.

For an observed node , we define

| (8) | ||||

| (9) |

In the above equations, denotes the length of longest directed latent path that connects node to any observed node. is the set of all observed nodes that can be reached by with a directed latent path of length and set consists of all pairs such that there exists a directed latent path from to with length .

Lemma 1.

Under Assumption 2, an observed node is the unique parent of a latent node if and only if for any other observed node s.t. , we have

In the first loop, if there exist multiple unique parents of a latent node (for instance, node 2 and node 3 in Figure 2b), we pick the one with a minimum index (lines: 7-9).

The second loop recovers based on the following observation. If a latent node is the parent of latent node , then can reach all the observed nodes in , i.e., and (line: 13). Furthermore, can be recovered using the fact that an observed node is a children of a latent node , if a unique parent of , e.g., , can reach by a directed latent path of length 2 (line: 16). Finally, the third loop reconstructs by adding an observed node to the parent set of latent node , if can reach all the observed nodes that a unique parent of , e.g., , reaches (lines: 18-22).

Learning More General Unobserved Networks with Minimum Number of Latent Nodes

In general, the latent sub-network may not be a tree or there may not be a unique minimal unobserved network consistent with the linear measurements (see Figure 1). Hence, we try to find an efficient approach to recovering all possible minimal unobserved networks under some conditions. In fact, without any extra conditions, finding a minimal unobserved network is NP-hard.

Theorem 3.

Finding an unobserved network that is both consistent with a given linear measurements and has a minimum number of latent nodes is NP-hard.

Below, after some definitions, we propose the Node-Merging (NM) algorithm that returns all possible unobserved networks with minimum number of latent nodes under the following assumption.

Assumption 3.

Assume that there exists at most one directed latent path of each length between any two observed nodes.

|

|

For example, the graph in Figure 2f satisfies this assumption but not the one in Figure 2e. This is because there are two directed latent paths of length 2 from node 5 to node 4.

Definition 3.

(Merging) We define merging two nodes and in graph as follows: remove node and the edges between and , and then give all the parents and children of to . We denote the resulting graph after merging and by . We say that two nodes and are mergeable if is consistent with the linear measurements of .

Definition 4.

(Connectedness) Consider an undirected graph over the observed nodes which is constructed as follows: there is an edge between two nodes and in , if there exists s.t. or ; We say that two observed nodes and are “connected” if there exist a path between them in .

It can be seen that if pairs and are connected then node are also connected. We then define a connected class as a subset of observed nodes in which any two nodes are connected.

Initialization:

We first find the set of all connected classes, say .

For each class , we create a directed graph that is consistent with the linear measurements.

To do so, for any two observed nodes , if , we construct a directed path with length from node to node by adding new latent nodes to .

Merger:

In this phase, for any from the initialization phase, we merge its latent nodes iteratively until no further latent pairs can be merged.

Since the order of mergers leads to different networks with minimum number of latent nodes, the output of this phase will be the set of all such networks.

Algorithm 2 summarizes the steps of NM algorithm.

In this algorithm, subroutine checks whether two nodes and are mergeable.

Experimental Results

Synthetic Data:

We considered a directed random graph, denoted by DRG, such that there exists a directed link between an observed and latent node with probability , independently across all pairs, and there is a directed link between two latent nodes with probability . If there is a link between two nodes, we set the weight of that link uniformly from .

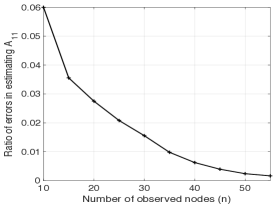

We utilize the method described in Section 3 to estimate linear measurements with a significance level of . In order to evaluate how well we can estimate the linear measurements, we generated 1000 instances of DRG with , , and . The length of the time series was set to . Let be the estimate of support of . In Figure 3a, the expected estimation error, i.e. , is computed, where is the Frobenius norm. One can see that the estimation error decreases as the number of observed variables increases.

|

|

We also studied the effect of the observed to latent noise power ratio (OLNR), , on , and compared it with the bound given in Proposition 1. We generated instances of DRG with , , and . As it can be seen in Figure 3b, the average estimation error decreases as OLNR increases, as expected from Proposition 2.

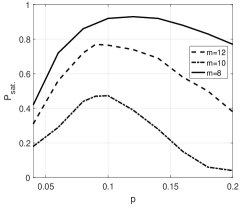

We investigated what percentage of instances of the random graphs satisfy Assumption 2. We generated instances of DRG with , and . In Figure 3c, the probability of satisfying Assumption 2, , is depicted versus for different numbers of latent variables in the VAR model. For larger , it is less likely to see a unique observed parent for each latent node and thus decreases. For a fixed , the same phenomenon will occur if we increase when is relatively large. Furthermore, for small , there might exist some latent nodes that have no observed parent or no observed children.

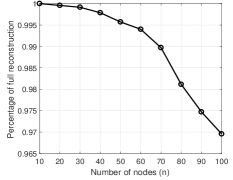

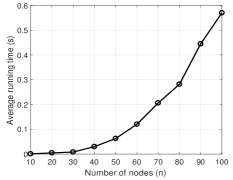

We also evaluated the performance of the NM algorithm in random graphs. We generated instances of DRG with and , and computed the linear measurements. To save time, if for a class of connected nodes the number of latent nodes generated in the initial phase exceeds , we supposed that the corresponding instance cannot be recovered efficiently in time and did not proceed to the merging phase. Figures 4a and 4b depict the percentage of instances in which the algorithm can recover all possible minimal unobserved networks and the average run time (in seconds) of the algorithm, respectively.777We performed the experiment on a Mac with GHz 6-Core Intel Xeon processor and 32 GB of RAM. This plot shows that we can recover all possible minimal unobserved networks for a large portion of instances efficiently even in relatively large networks.

|

|

US Macroeconomic Data:

We considered the following set of time series from the quarterly US macroeconomic data for the period from 31-Mar-1947 to 31-Mar-2009 collected from the St. Louis Federal Reserve Economic Database (FRED) (?): GDP, GDPDEF, COE, HOANBS, TB3MS, PCEC, GPDI.

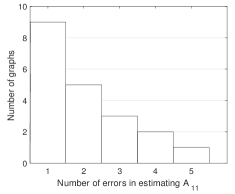

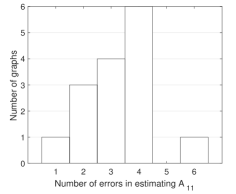

Assuming that the underlying dynamics is linear (Eq. (1)), we considered the estimated VAR model over all variables as the ground truth. Then, we selected four arbitrary times series as observed processes and computed . We divided the possible selections into two classes: 1) high power, where tr for a fixed threshold ; 2) low power: where tr. In this experiment, we set . In Figure 5, we plotted the histograms of for these two classes. As it can be seen, in the high power regime, most of the possible selections have small estimation errors.

We also considered the following six time series of US macroeconomic data during 1-Jun-2009 to 31-Dec-2016 from the same database: GDP, GPDI, PCEC, TBSMS, FEDFUND, and GS10. We obtained the causal structure among these six time series by fitting a VAR model on all of them and considered the result as our ground truth (see Figure 6). Then, we removed GPDI from the dataset and considered the remaining five time series as observe processes and checked whether the influences from the “latent” process (GPDI) can be corrected estimated.

Dairy Prices:

A collection of three US dairy prices has been observed monthly from January 1986 to December 2016 (?): milk, butter, and cheese prices.

We estimated the VAR model on all the time series with lag length and considered the resulting graph as our ground truth (see Figure 7). Next, we omitted the butter prices from the dataset and considered the milk and cheese prices as observed processes. The estimated linear measurements were: and . Algorithm 1 correctly recovered the true causal graph using this linear measurements. Note that the genericity assumptions in (?) do not hold true for this data set (see Experiments section).

West German Macroeconomic Data:

We considered the quarterly West German consumption expenditures , fixed investment , and disposable income , during 1960-1982 (?).

Similar to the previous experiment with dairy prices, we first obtained the entire transition matrix among all the process. Figure 8 depicts the resulting graph. Next, we considered to be latent and used to estimate the linear measurements and . Using this linear measurements, Algorithm 1 recovered the true network in Figure 8 correctly.

Conclusion and Future work

We considered the problem of estimating time-delayed influence structure from partially observed time series data. Our approach consisted of two parts: First, we studied sufficient conditions under which certain aspects of the influence structure of the underlying system are identifiable. Second, we proposed two algorithms that recover the influence structures satisfying the sufficient conditions given in the first part. The proposed algorithms can construct the observed sub-network (support of ), the causal influences from latent to observed processes (support of ), and also the causal influences among the latent variables (support of ), uniquely under a set of sufficient conditions. As a future direction, we plan to extend our results to the case that might have cycles. In the paper, we have seen examples showing that unique recovery is not possible if any conditions of Assumption 2 are violated. These conditions are a good starting point for the case that we have cycles in .

References

- [Besserve et al. 2010] Besserve, M.; Schölkopf, B.; Logothetis, N. K.; and Panzeri, S. 2010. Causal relationships between frequency bands of extracellular signals in visual cortex revealed by an information theoretic analysis. Journal of computational neuroscience 29(3):547–566.

- [Boyen, Friedman, and Koller 1999] Boyen, X.; Friedman, N.; and Koller, D. 1999. Discovering the hidden structure of complex dynamic systems. In Proceedings of the Fifteenth conference on Uncertainty in artificial intelligence, 91–100. Morgan Kaufmann Publishers Inc.

- [Dai ] (DAI) Dairy prices, dairy marketing and risk management program, University of Wisconsin. http://future.aae.wisc.edu/tab/prices.html.

- [Danks and Plis 2013] Danks, D., and Plis, S. 2013. Learning causal structure from undersampled time series. In JMLR: Workshop and Conference Proceedings.

- [Eichler 2012] Eichler, M. 2012. Causal inference in time series analysis. Causality: statistical perspectives and applications 327–354.

- [Etesami, Kiyavash, and Coleman 2016] Etesami, J.; Kiyavash, N.; and Coleman, T. 2016. Learning minimal latent directed information polytrees. Neural Computation.

- [FRE ] (FRE) St. Louis Federal Reserve Economic Database. http://research.stlouisfed.org/fred2/.

- [Geiger et al. 2015] Geiger, P.; Zhang, K.; Gong, M.; Janzing, D.; and Schölkopf, B. 2015. Causal inference by identification of vector autoregressive processes with hidden components. In Proceedings of 32th International Conference on Machine Learning (ICML 2015).

- [Gong et al. 2015] Gong, M.; Zhang, K.; Schölkopf, B.; Tao, D.; and Geiger, P. 2015. Discovering temporal causal relations from subsampled data. In ICML, 1898–1906.

- [Gong et al. 2017] Gong, M.; Zhang, K.; Schölkopf, B.; Glymour, C.; and Tao, D. 2017. Causal discovery from temporally aggregated time series. In Proc. Conference on Uncertainty in Artificial Intelligence (UAI 17).

- [Granger 1969] Granger, C. W. 1969. Investigating causal relations by econometric models and cross-spectral methods. Econometrica: Journal of the Econometric Society 424–438.

- [Hoyer et al. 2008] Hoyer, P. O.; Shimizu, S.; Kerminen, A. J.; and Palviainen, M. 2008. Estimation of causal effects using linear non-gaussian causal models with hidden variables. International Journal of Approximate Reasoning 49(2):362–378.

- [Jalali and Sanghavi 2012] Jalali, A., and Sanghavi, S. 2012. Learning the dependence graph of time series with latent factors. ICML.

- [Johnson 1985] Johnson, D. S. 1985. The np-completeness column: an ongoing guide. Journal of Algorithms 6(3):434–451.

- [Kim et al. 2011] Kim, S.; Putrino, D.; Ghosh, S.; and Brown, E. N. 2011. A granger causality measure for point process models of ensemble neural spiking activity. PLoS computational biology 7(3):e1001110.

- [Lütkepohl and Krätzig 2004] Lütkepohl, H., and Krätzig, M. 2004. Applied time series econometrics. Cambridge university press.

- [Lütkepohl 2005] Lütkepohl, H. 2005. New introduction to multiple time series analysis. Springer Science & Business Media.

- [Marko 1973] Marko, H. 1973. The bidirectional communication theory–a generalization of information theory. Communications, IEEE Transactions on 21(12):1345–1351.

- [Massey 1990] Massey, J. 1990. Causality, feedback and directed information. In Proc. Int. Symp. Inf. Theory Applic.(ISITA-90), 303–305. Citeseer.

- [Patrinos and Hakimi 1972] Patrinos, A. N., and Hakimi, S. L. 1972. The distance matrix of a graph and its tree realization. Quarterly of applied mathematics 255–269.

- [Pearl 2009] Pearl, J. 2009. Causality. Cambridge university press.

- [Roebroeck, Formisano, and Goebel 2005] Roebroeck, A.; Formisano, E.; and Goebel, R. 2005. Mapping directed influence over the brain using granger causality and fmri. Neuroimage 25(1):230–242.

- [Schreiber 2000] Schreiber, T. 2000. Measuring information transfer. Physical review letters 85(2):461.

- [Spirtes, Glymour, and Scheines 2000] Spirtes, P.; Glymour, C. N.; and Scheines, R. 2000. Causation, prediction, and search. MIT press.

- [WG ] (WG) West German fixed investment, disposable income, consumption expenditures in billions of DM, 1960Q1-1982Q4. http://www.jmulti.de/data_imtsa.html.

Appendix A Proof of Proposition 1

We project the vector onto as follows:

| (10) |

where , and is a block matrix with as its th block for . Please note that is orthogonal to for . Since and are orthogonal, we can see

| (11) |

Using (11) and the relationship between and norms of a matrix, we obtain

| (12) |

where and denote the minimum and maximum eigenvalues of a given matrix, respectively. Please note that is white noise and thus we have: . Using the fact that is diagonal and , we obtain

| (13) |

where and .

Appendix B Estimating the Bounds in Proposition 1

The bound can be estimated as follows:

-

•

The lag length in (6) can be obtained from AIC or FPE criterion (see chapter 4 in (?)).

-

•

We can estimate by observation vector . We also consider a bound on the maximum variance of exogenous noises in latent part.

-

•

We assume a bound on and .

In summary, an upper bound would be: . Suppose that absolute values of nonzero entries of are greater than . We can recover the support of matrix successfully if

| (14) |

Appendix C Proof of Proposition 2

The spectral density of matrix can be computed as follows:

| (15) |

where , , and denotes Hermitian of a matrix. Thus, we have:

| (16) |

where and .

We define the function where is a unit vector. Suppose that minimizes the function . By the definition of and , the ratio is equal to . Now if we decrease to , then we have: . Moreover, for the optimal solution of , we know that: . Thus, we can conclude that: .

Appendix D Proof of Theorem 1

First, we show such has a minimum number of latent nodes. We do this by means of contradiction. But first observe that since the latent subnetwork of is a directed tree, we can assign a non-negative number to latent node that represents the length of longest directed path from to its latent descendants. Clearly, all such descendants are leaves which we denote them by . For instance, if the latent subnetwork of is , then and .

Suppose that contains latent nodes and there exists another network (not necessary with tree-structure induced latent subgraph), with number of latent nodes that it is also consistent with the same linear measurements as . Due to assumption (i), there is at least distinct observed nodes that have out-going edges to the latent subnetwork. More precisely, each has at least a unique observed node as its parent. We denote a unique observed parent of node by .

Because , there exists at least one observed node in that has shared its latent children with some other latent nodes in . Among all such observed nodes, let to be the one whose corresponding latent node in , (), has maximum .888If there are several such observed node, let to be one of them. Furthermore, let to be the index-set of those observed nodes that has shared a latent child with them in .

By the choice of , we know that for all and if for some , , then has not shared its latent child in with any other observed nodes in . Moreover, there should be at least a latent node where such that . Otherwise, will not be consistent with the linear measurements of . Let . Because shares its latent children with in and both and consistent with the same linear measurements, the following holds in graph ,

where indicates the set of observed children of the set . This indeed contradicts assumption (ii).

Appendix E Proof of Theorem 2

First, we require the following definition. For a network with corresponding latent sub-network that is a tree, we define . To prove the equivalency, suppose there exists another network such that its latent sub-network is a tree and has a minimum number of latent nodes. Let to denote the latent nodes in . Since satisfies Assumption (i), for every latent node there exists a unique observed node such that and for all .

Since both and are consistent with the same linear measurement, it is easy to observe that if , then must have at least a latent child in , say , such that . Note that is computed in and in . Moreover, we must have:

where denotes the set of latent nodes in that have as their observed parent.

In other words, observed nodes that can be reached by a directed path of length from should be the same in both graph and .

This results plus the fact that satisfies Assumption (ii), imply:

I) For every , there exists a unique latent node , such that and for all , and

Using I) and knowing that both and have the same number of latent nodes, we obtain:

II) , for all .

Using I) and II), we can define a bijection between the latent subnetworks of and as follows .

Using this bijection and Assumption (ii) of conclude that if is the common parent of , then should be the common parent of and the proof is complete.

Appendix F Proof of Lemma 1

Suppose that is the unique observed node of a latent node . Then, for any such that , if is not a child of , then from assumption ii we have . If is a child of , then since we know that , and .

Now, suppose that the observed node satisfies conditions but it is not unique parent of any latent node. Let and be children of . At least one of them, say node , can reach an observed node by a path of length . If has the same property, then consider the unique observed parent of , say node . Based on Assumption (ii), we have , which is in contradiction with the assumption that node satisfies conditions of Lemma. Moreover, if does not have a path to observed node with a length of , then for any observed parent of , one of the conditions in the Lemma is not satisfied. Thus, the proof is complete.

Appendix G Proof of Proposition 3

Notice that the first loop in Algorithm 1 uses the result of Lemma 1 and finds all the latent nodes and their corresponding unique observed parents. The next loop uses the fact that the latent sub-network is a tree and also it satisfies Assumption 2. Hence, if there exist two latent nodes and , one with depth and the other one with depth , such that , then must be the parent of in the latent sub-network.

Moreover, since each latent node has a unique observed parent, using , Algorithm 1 can identify all the observed children of a latent node. Finally, the last loop in this algorithm locates the rest of observed nodes as the input of the right latent nodes. The algorithm does it by using the fact that if an observed node shares a latent child with another observed node , then . Clearly, if the true unobserved network satisfies Assumption 2, the output of this algorithm will have a latent sub-network that is a tree and consistent with the linear measurement. Thus, by the result of Theorem 1, it will be the same as the true unobserved network up to some permutations in .

Appendix H Proof of Theorem 3

Consider the instance of the problem where . Without loss of generality, we can assume that entries of and are just zero or one. Thus, we need to find and such that and is minimum. We will show that the set basis problem (?) can be reduced to the decision version of finding the minimal unobserved network which we call it the latent recovery problem. But before that, we define the set basis problem:

The Set Basis Problem (?): given a collection of subsets of a finite set and an integer , decide whether or not there is a collection of at most sets such that for every set , there exists a collection where .

Any instance of the basis problem can be reduced to an instance of latent recovery problem. To do so, we encode any set in collection to a row of where -th entry is equal to one if , and otherwise zero. It is easy to verify that the rows of matrix correspond to sets in collection if there exist a solution for the basis problem. Since the basis problem is NP-complete, we can conclude that finding the minimal unobserved network is NP-hard.

Appendix I Proof of Theorem 4

Consider a minimal unobserved network . Pick any latent node which its in-degree or out-degree is greater than one. Let and be the sets of nodes that are going to and incoming from node , respectively. We omit the node and create latent nodes . We also add a direct link from node to and from to in order to be consistent with measurements. We continue this process until there is no latent node with in-degree or out-degree greater than one. Since there exists at most one path with length from any observed node to another observed node, the resulted graph is exactly equal to graph . Hence we can construct the minimal graph just by reversing the process of generating latent nodes from to merging latent nodes from . But the NM algorithm consider all the sequence of merging operations. Thus, would be in the set and the proof is complete.