Targeted Learning Ensembles for Optimal Individualized Treatment Rules with Time-to-Event Outcomes

Abstract

We consider estimation of an optimal individualized treatment rule from observational and randomized studies when a high-dimensional vector of baseline variables is available. Our optimality criterion is with respect to delaying expected time to occurrence of an event of interest (e.g., death or relapse of cancer). We leverage semiparametric efficiency theory to construct estimators with desirable properties such as double robustness. We propose two estimators of the optimal rule, which arise from considering two loss functions aimed at (i) directly estimating the conditional treatment effect (also know as the blip function), and (ii) recasting the problem as a weighted classification problem that uses the 0-1 loss function. Our estimated rules are super learning ensembles that minimize the cross-validated risk of a linear combination in a user-supplied library of candidate estimators. We prove oracle inequalities bounding the finite sample excess risk of the estimator. The bounds depend on the excess risk of the oracle selector and a doubly robust term related to estimation of the nuisance parameters. We discuss some important implications of these oracle inequalities such as the convergence rates of the value of our estimator to that of the oracle selector. We illustrate our methods in the analysis of a phase III randomized study testing the efficacy of a new therapy for the treatment of breast cancer.

1 Introduction

Individualized treatment rules play a fundamental role in the precision medicine model for healthcare, whereby medical decisions are targeted to the individual based on their expected clinical response, instead of the traditional one-size-fits-all approach. Mathematically, a treatment rule is a function that maps an individual’s pre-treatment covariates into an optimal treatment choice. In this paper, we are concerned with learning the optimal rules from data collected as part of an observational or randomized study, where optimality is defined as the maximum delay in the expected time of occurrence of an undesirable event (e.g., death or relapse).

Recent advances in biomedical imaging and gene expression technology produce large amounts of data that can be used to tailor treatment to very specific patient characteristics. Methods to estimate the optimal rule when it is defined with respect to a single time-point outcome include the work of Qian and Murphy (2011); Zhao et al. (2012); Song et al. (2015); Rubin et al. (2012); McKeague and Qian (2014), among others. Methods to solve the problem using survival outcomes subject to informative censoring have been proposed by Zhao et al. (2011); Goldberg and Kosorok (2012). The latter methods use Q-learning, relying on sequential support vector regressions, to estimate the optimal sequential treatment rule that optimizes a survival outcome under right-censoring. Geng et al. (2015) also tackle estimation of the optimal rule in a survival setting using regularization for the outcome regression under the strong assumption that censoring is independent of covariates and the outcome, but their decision functions are restricted to linear functions. Zhao et al. (2015) generalize the weighted classification approach of Zhao et al. (2012) to allow for informative censoring and doubly robust loss functions, but their decision functions are restricted to support vector machines. Bai et al. (2016) present methods for estimating optimal rules with a survival outcome subject to informative censoring. They consider two strategies based on estimation of the blip function and based on a classification perspective. Their methods are restricted to decision functions that can be indexed by a Euclidean vector and parametric nuisance estimators, and are therefore of limited applicability to high-dimensional data. All the above methods are potential candidates in the library of estimators that constitute our ensembles.

In this article, we propose two methods to construct an ensemble of decision functions for the optimal rule. Our ensembles are linear combinations of estimators in a user-supplied library, where the coefficients in the linear combination are chosen to minimize the cross-validated risk. We propose to use a doubly robust loss function with roots in efficient estimation theory for marginal causal effects (Moore and van der Laan, 2009; Díaz et al., 2015). In our context, double robustness means that the estimated rules will have certain optimality properties under consistent estimation of at least one of two nuisance parameters: (a) the hazard of the outcome at each time point conditional on covariates and treatment, and (b) the hazard of censoring and the treatment mechanism.

The library of candidate estimators may contain any of the algorithms discussed in the previous paragraphs. In light of the no free lunch theorems of Wolpert (2002) for supervised learning, for any given dataset, our ensembles are expected to have better or equal generalization error than any of the individual candidates in the library. We provide a formal proof of this claim in the form of an oracle inequality, which bounds the excess risk of our estimator in terms of the excess risk of the oracle estimator, defined as the combination of estimators that would be chosen in a hypothetical world in which an infinite validation sample is available and at least one of the nuisance parameters is known. Our methods are developed under the assumption that censoring is at random (Rubin, 1987), which means that censoring is random within strata of treatment and baseline variables. We also assume that treatment is randomized within strata of the covariates, either by nature or by experimentation.

The finite sample bounds we present are inspired by developments in the targeted learning literature, which establish the optimality of cross-validation in estimator selection for high-dimensional parameters (van der Laan and Dudoit, 2003). Related to our work, Luedtke and van der Laan (2016) consider super learning ensembles for estimation of optimal DTRs in two time points. They present oracle inequalities for super learning of the optimal rule using a loss function indexed by the treatment mechanism, which is assumed known. We generalize their results in the following ways: (i) we provide oracle inequalities under a doubly robust loss function indexed by two nuisance parameters, when neither of the nuisance parameters is known, (ii) we show that the oracle inequalities inherit the double robustness property of the loss function, and (iii) we present comparable oracle inequalities for the 0-1 loss function. In addition, we discuss how these oracle inequalities are related to the convergence of the value of the rule under a margin assumption describing the behavior of the blip function in the boundary of the decision threshold.

2 Data and Notation

Assume individuals are monitored at time points . Let denote a time-to-event outcome taking values in , where represents no event occurring in the follow-up period. Let denote the censoring time defined as the time at which the individual is last observed in the study, and let , represent administrative censoring. Let denote study arm assignment, and let denote a vector of baseline variables, which may include gene expression as well as demographic, comorbidity, and other clinical data. Denote the indicator variable taking value if the argument is true and otherwise. The observed data vector for each participant is , where , and is the indicator that the participant’s event time is observed (uncensored). For a random variable , we let take values on a set .

We assume the observed data vector for each participant , denoted , is an independent, identically distributed draw from the unknown joint distribution on . The empirical distribution of is denoted with . We assume , where is the nonparametric model defined as all continuous densities on with respect to a dominating measure . We use to denote a generic distribution , and to denote expectation with respect to , and is used to denote expectation over draws of . For a function , we denote , and . We use to denote that is smaller or equal than up to a universal constant.

We can equivalently encode a single participant’s data vector using the following longitudinal data structure:

| (1) |

where and , for . For a random variable , we denote its history through time as . For a given scalar , the expression denotes element-wise equality.

Define the following indicator variables for each : , The variable is the indicator based on the data through time that a participant is at risk of the event being observed at time . Analogously, is the indicator based on the outcome data through time and censoring data before time that a participant is at risk of censoring at time . We define .

Define the discrete hazard function for survival at time :

among the population at risk at time within strata of study arm and baseline variables. Similarly, for the censoring variable , define the censoring hazard at time :

We use the notation , , and . Let denote the marginal distribution of the baseline variables . We add the subscript to to denote the corresponding quantities under .

3 Treatment Effect, Identification, and Optimal Individualized Treatment Rules

3.1 Potential Outcomes and Causal Parameter

Define the potential outcomes as the event times that would have been observed had study arm assignment and censoring time been externally set with probability one. For a restriction time of interest, we define the restricted survival time under treatment arm as . For a transformation of , the treatment effect within strata of the covariates may be defined in terms of the so-called full-data blip function (see e.g., Robins, 1997) of the restricted mean survival time:

The transformation may represent a subset of covariates (e.g., gene expression), or the whole vector . We define the marginal treatment effect as .

The subscript denotes a causal parameter, that is, a parameter of the distribution of the potential outcomes and . It can be shown (see Díaz et al., 2015) that where is the survival probability corresponding to the potential outcome under assignment to arm within strata . As a result, may be expressed as

| (2) |

since for and for all .

An individualized treatment rule is a function that maps the covariate values of a given participant to a personalized treatment decision in . The potential time to event under a rule is defined as . Accordingly, the restricted mean survival time under a treatment rule that assigns treatment according to is equal to

Because the last term does not depend on , we define the value of the rule as

The above equation provides the basis for the definition of an optimal rule as

where is the space of functions that map the range of into a treatment decision in . We define optimality of an rule with respect to the restricted mean survival time, though other effect measures could also be used.

3.2 Identification of Parameters in Terms of Observed Data Generating Distribution

In this section we show how the blip function , the value function , and the optimal rule , which are defined above in terms of the distribution of potential outcomes, can be equivalently expressed as functions , , and of the observed data distribution , under the assumptions C.1-C.4 below. This is useful since the potential outcomes are not always observed, in contrast to the observed data vector for each participant, whose distribution we can make direct statistical inferences about.

Define the following assumptions:

C.1Consistency.

C.2Randomization.

is independent of conditional on , for each

C.3Random censoring.

is independent of conditional on , for each

C.4Strong positivity.

and for each and and some .

We make assumptions C.1-C.4 throughout the manuscript. Denote the survival and censoring function for at time conditioned on study arm and baseline variables by

Under assumptions C.1-C.4, we have and therefore and have the following product formula representations:

| (3) |

The potential outcome survival function can be equivalently represented in terms of the observed data distribution as . It follows from (2) that the causal parameter is equal to the following observed-data blip function:

| (4) |

Thus, the value of a rule is equal to , and a corresponding optimal treatment rule is equal to , where we denote the corresponding true quantities (i.e., quantities computed w.r.t. ) as , , and .

In addition to assumptions C.1-C.4 above, we sometimes make the following margin assumption, which is common in the classification literature for plug-in estimators:

C.5Margin assumption.

There exists a constant such that for all .

The case is trivial and implies no assumption, whereas corresponds to the strongest assumption since it implies that is bounded away from zero. This assumption characterizes the behavior of the decision function in the boundary, and has been shown crucial to establish the convergence of certain classifiers (e.g., Audibert et al., 2007; Luedtke and Chambaz, 2017).

4 Plug-in Estimation of the Blip Function and the Optimal Rule

In this section we discuss various estimators for , which can be mapped to a plug-in estimators through . Our general strategy relies on the concept of censoring unbiased transformation, given in Definition 1 below. This concept was first introduced by Fan and Gijbels (1994) and is further discussed in Rubin and van der Laan (2007), among others.

Definition 1 (Unbiased transformation).

is referred to as an unbiased transformation for if .

The above definition motivates the construction of estimators of by regressing the transformation on the covariates . A common complication in this step is that most unbiased transformations typically depend on unknown nuisance parameters which must be estimated prior to carrying out the analysis. In this work, we focus on the doubly robust censoring unbiased transformation defined in Lemma 1 below. In addition to being a doubly robust unbiased transformation for (i.e., providing robustness to inconsistent estimation of one out of two nuisance parameters), is an efficient estimating function in the non-parametric model in the sense that it may be used to construct efficient estimators of the marginal treatment effect (see e.g., Díaz et al., 2015).

Lemma 1 (Doubly robust censoring unbiased transformation).

Define

| (5) |

where , and

| (6) |

Assume is such that or . Then is an unbiased transformation for , that is, .

As a consequence of the previous lemma, the expected value of the quadratic loss function is minimized at if is such that either or .

For a loss function , we denote its expected value as and refer to it as the risk. We now discuss the construction of super learning ensembles of candidate estimators for that target minimization of the quadratic risk. Consider a collection of estimation algorithms for estimating , hereby called a library, . For an estimator of , in light of the discussion of the previous section, this library may be constructed by considering any predictive algorithm that minimizes the quadratic risk for prediction of the doubly robust unbiased transformation . The literature in machine and statistical learning provides us with a wealth of algorithms that may be used in this step. Examples include algorithms based on regression trees (e.g., random forests, Bayesian regression trees), algorithms based on smoothing (e.g., generalized additive models, local polynomial regression, multivariate adaptive regression splines), and others (e.g., support vector machines, neural networks).

Consider the following cross-validation set up. Let denote a random partition of the index set into validation sets of approximately the same size. That is, ; ; and . In addition, for each , the associated training sample is . Denote the estimator of trained only using data in . Likewise, denote by the estimator of obtained by training the -th predictive algorithm in using only data in the sample (e.g., regressing on for ). We use to denote the index of the validation set that contains observation . The cross-validated prediction risk of is defined as

In this paper we consider an ensemble learner given by a convex combination

The weights are chosen to minimize the cross-validated risk of the above combination, that is:

The above expression is a weighted ordinary least squares problem with constraints on the coefficients, and may therefore be solved using standard off-the-shelf regression or optimization software. We denote this super learner with .

The optimality of general cross-validation selection procedures is discussed in van der Laan & S. Dudoit & A.W. van der Vaart (2006); van der Vaart et al. (2006). Optimality here is defined in terms of asymptotic equivalence with the oracle risk, which we define as the risk computed when (i) one of the components of the nuisance parameter is known, and (ii) a validation sample of infinite size is available to assess the performance of the estimator. Specifically,

Definition 2 (Oracle risk and oracle selector).

Let , where either , or . The oracle risk of a candidate is defined as

The oracle selector is equal to

and the corresponding oracle blip function is denoted with .

The risk is the optimal risk (with respect to the loss function , which in light of Lemma 1 is a valid loss function) achieved by the true . The following theorem provides a bound on the excess risk of the estimator and the excess risk of . The excess risk for a selector is defined as the difference between the oracle risk of the selector and the optimal risk, i.e.,

where we remind the reader that the expectation is taken over draws of . We denote this excess risk as , below we refer to its square root as . We show that the above excess risk is bounded by two terms: one depending on the excess risk of the oracle selector , and another one depending on doubly robust terms associated to estimation of .

Theorem 1 (Oracle inequality for the super learner of the blip function).

Let denote the element-wise limit of as , and assume that either or . Define

Then, for

| (7) |

for constants , , and .

Note that the terms and converge to zero if either or converge to or , respectively, in norm. This implies that the doubly robust property of is transferred to the oracle inequality. To the best of our knowledge this result had not been previously shown in the literature.

The super learner may be used to construct a plug-in estimator of the optimal rule as . The following remark discusses the convergence rates of the value of the selected rule to the value of the oracle rule .

Remark 1 (Convergence rates to the oracle value).

Assume

Lemma 5.3 of Audibert et al. (2007), along with Jensen’s inequality, show that under assumption C.5, we have

where is the oracle rule. This yields the following convergence rate:

An example of a case yielding the above rate is a randomized study () with no censoring (.) In this case, a logistic regression fit of on containing at least an intercept would yield an estimator satisfying . Plugging in the true value for , and assuming is inconsistently estimated yields and . Under no margin assumption () we get a convergence rate of . Under a strong margin assumption in which is bounded away from zero () we get a rate of .

The above convergence result establishes the convergence of the value of our estimator to the value of the oracle . This is different from the typical result in the classification literature, which establishes convergence to the optimal value . The latter result often involves fast learning rates (sometimes faster than ) and requires restricting the class of blip functions considered to Hölder (Audibert et al., 2007) or Donsker (Luedtke and Chambaz, 2017) classes, a restriction we do not impose.

5 Super Learner Ensembles for the Optimal Rule from a Classification Perspective

5.1 Estimators Using the 0-1 Loss Function

In this section we discuss a classification approach that aims at directly estimating the optimal rule . Our approach here differs from the previous section in that we do not attempt to estimate the blip function. Instead, we introduce the concept of a decision function, defined as , and which yields a treatment rule . In a slight abuse of notation we use to refer to the value of the rule . Any function such that has optimal value . This provides intuition on the benefits of directly optimizing the value of the loss function instead of the risk of the blip function: an inconsistent estimator of the blip function may provide an optimal rule, as long as its sign is correct. For a given rule , in light of Lemma 1, we have that if is such that either , or . Thus, a decision function that optimizes the value of the rule may be found as

For a binary value and any we have . Thus, the optimization problem may be recast as , where and

| (8) |

Expression (8) is a weighted classification loss function in which we aim to classify the binary outcome based on data , using the 0-1 loss function with weights given by . The objective is to classify an individual who benefits from treatment arm (i.e., an individual with ) as requiring treatment (i.e., ), while penalizing for the loss incurred if the individual were misclassified.

In what follows we consider a library of algorithms for estimation of the decision function . In light of the discussion of the previous sections, the most natural choice for a decision function is the blip function . However, we do not restrict our setup to functions with a blip interpretation. In addition to estimators of the blip function , the library may contain other decision functions such as the support vector machines proposed by Zhao et al. (2015) and the parametric decision functions of Bai et al. (2016).

We construct an ensemble of the decision functions as

| (9) |

In this way, we generate an ensemble optimal rule as . As in the previous section, we define the super learner selector as

where represents (9) with replaced by : the -th decision function estimated using the training sample . The super learner of the decision function is defined as , and the corresponding optimal rule is defined as .

For such that either or , the oracle risk of the decision function is defined as

The oracle selector of is thus defined as , and we denote . The excess risk of an estimator is equal to

In Theorem 2 below, we provide bounds on in terms of the excess risk of the oracle selector and the bias terms and defined in Theorem 1.

Theorem 2 (Oracle inequality for the super learner of the optimal rule).

Remark 2.

Assume converges as in Remark 1. An immediate consequence of the above result is that under no margin assumption, we have . Under the strong margin assumption C.5 with we have . These rates are identical to the rates obtained in Remark 1 for the plug-in estimator. The question of whether analogous convergence rates may be obtained for other values of under condition C.5 remains an open problem.

In comparison to Theorem 1, Theorem 2 has the additional assumption that the optimization of the loss function is carried out in a grid polynomial size in . Inspection of the proofs of the theorems in the Supplementary Material reveals the reason for the additional assumption: the 0-1 loss function is non-smooth and the Lipschitz condition used in the proof of Theorem 1 does not apply. As demonstrated in our data application, this assumption is likely to have little practical consequences, but it is unclear to us whether it can be removed.

5.2 Using a Surrogate Loss Function for the 0-1 Loss

It is well known in the statistical learning literature that minimizing (8) is generally difficult due to the discontinuity and non-convexity of the 0-1 loss. A common approach to mitigate the issues arising from the discontinuity and non-convexity of the 0-1 loss function is to use surrogates loss functions, such as the logistic loss or the hinge loss . We have the following result, which teaches us that any decision function based on a decision function has the same performance as the optimal rule .

Lemma 2.

Assume is such that either , or . Define

| (10) |

where the surrogate loss is defined as

Then we have , where .

6 Estimating the Optimal Treatment for Breast Cancer Patients in our Motivating Application

Different types of human breast cancer tumors have been shown to have heterogeneous response to treatments (Perou et al., 2000; Sotiriou and Pusztai, 2009). Amplification of ERBB2 gene and associated overexpression of human epidermal growth factor receptor (HER2) encoded by this gene occur in 25-30 of breast cancers (Slamon et al., 2001). HER2-positive breast cancer is an aggressive form of the disease and the prognosis for such patients is generally poor (Slamon, 1987; Seshadri et al., 1993). The clinical efficacy of adjuvant trastuzumab, a recombinant monoclonal antibody, in early stage HER2-positive patients was demonstrated by several large clinical trials (Perez et al., 2011; Romond et al., 2005). Despite significant improvement in disease-free and overall survival of patients treated with trastuzumab, about 20-25 patients relapse within 3-5 years (Perez et al., 2011). In this paper we use data from the North Central Cancer Treatment Group N9831 study, a phase III randomized clinical trial testing the addition of trastuzumab to chemotherapy in stage I-III HER2-positive breast cancer.

The total number of patients enrolled in the NCCTG N9831 trial was 3,505. Samples from 1,390 patients, for whom there was available tissue, were used to quantify mRNA from a custom codeset of 730 genes created by experts. The available baseline variables may be thus be categorized in three classes: demographic (e.g, race, age, ethnicity), clinical (e.g., tumor grade, tumors size, nodal status, hormone receptor status), and gene expression. Among the 1,390 patients, 483 received chemotherapy alone (control arm) and 907 patients received chemotherapy plus trastuzumab (treatment arm).

The clinical challenge is to identify genetic and demographic profiles for patients with HER2-positive breast cancer who are unlikely to benefit from adjuvant trastuzumab.

In order to estimate and assess the performance of the estimated rule using different datasets, we split our data into training and validation datasets, of sizes 1000 and 390, respectively.

6.1 Estimators of and

According to our theoretical results, the optimality of the estimated treatment rules hinges upon consistent estimation of at least one of the nuisance parameters and . As a result, it is crucial to employ flexible methods capable of unveiling complex patterns which are not visible to the human eye. As demonstrated below in Section 6.3, simple parsimonious models such as the Cox proportional hazards or logistic regression fail to detect these complex relations in the data.

In order to accurately estimate the nuisance parameters, we use an ensemble learner known as the super learner for prediction (van der Laan et al., 2007). We train the ensemble separately using data from each treatment arm, in order to fully account for treatment-covariate interactions. Like our rule ensembles, super learning predictors build a combination of candidate predictors that minimize a cross-validated user-supplied risk function. Since and are conditional probabilities, we focus on logistic regression ensembles and the negative log-likelihood loss function, using the R implementation in the SuperLearner package (Polley et al., 2016). The candidate estimators included in the ensembles are listed in Table 1, along with the coefficients of each predictor in the ensemble, when trained in the complete dataset using 5-fold cross-validation.

| RF | XGB | MLP | GLM | MARS | LASSO | ||

|---|---|---|---|---|---|---|---|

| 0.100 | 0.056 | 0.000 | 0.000 | 0.312 | 0.532 | ||

| 0.000 | 0.301 | 0.000 | 0.000 | 0.294 | 0.405 | ||

| 0.023 | 0.050 | 0.000 | 0.000 | 0.237 | 0.691 | ||

| 0.154 | 0.086 | 0.098 | 0.060 | 0.123 | 0.480 |

For random forests, extreme gradient boosting, and multilayer perceptron, the tuning parameters are tuned using data splitting with the aid of the R caret package (Kuhn et al., 2016). To avoid , logistic regression and multivariate adaptive splies are estimated with a variable screening algorithm which computes univariate t-statistics and keeps only the 50 variables with a larger value.

6.2 Candidate Estimators for the Optimal Treatment Rule

According to our discussion in Sections 4 and 5, there are at least three types of estimators for the optimal rule . The first type is a simple substitution estimator, obtained through inspection of equation (4), which consists in regressing the blip function on , where is the estimator of the survival function corresponding to the estimator described in Section 6.1. The second type is obtained through regression of the unbiased transformation on . The third type of estimation methods is obtained based on equation (8), and is obtained by classifying the binary outcome as a function of , with weights given by . Here, , where the components of are as described in Section 6.1. Any regression or supervised classification technique available in the statistical learning literature may be used as a candidate for solving these problems.

In our application, we focus on the following candidates for estimating :

| B-Reg | Regression of the blip function using super learning with candidate learners as described in Table 1. |

|---|---|

| D-Reg | Regression of the doubly robust transformation using super learning with candidate learners as described in Table 1. |

| D-Class-RF | Weighted classification of using random forests. |

| D-Class-XGB | Weighted classification of using extreme gradient boosting. |

| D-Class-GLM | Weighted classification of using logistic regression. |

According to our discussion in Sections 4 and 5, we also train four super learning ensembles of the above candidate estimators, using different loss functions:

| SL-Reg | Regression ensemble minimizing the expected quadratic loss function. |

|---|---|

| SL-Class-01 | Classification ensemble minimizing the expected 0-1 loss function. |

| SL-Class-Hinge | Classification ensemble with surrogate hinge loss function. |

| SL-Class-Log | Classification ensemble with surrogate log loss function. |

The coefficients of each candidate estimator in each ensemble are presented in Table 2. These coefficients were computed using the Subplex (Rowan, 1990) routine implemented in the NLopt nonlinear-optimization R package. For improved robustness, the 0-1 loss was optimized using 1000 different random starting values.

| SL-Reg | SL-Class-0-1 | SL-Class-Hinge | SL-Class-Log | |

|---|---|---|---|---|

| D-Class-RF | 0.000 | 0.005 | 0.000 | 0.000 |

| D-Class-XGB | 0.792 | 0.001 | 0.945 | 0.869 |

| D-Class-GLM | 0.000 | 0.031 | 0.000 | 0.000 |

| D-Reg | 0.007 | 0.017 | 0.001 | 0.006 |

| B-Reg | 0.201 | 0.947 | 0.054 | 0.125 |

6.3 Assessing the Performance of The Estimated Treatment Rule

Once each rule is estimated using only data in the training dataset, its value is estimated on the validation dataset. To that effect, we use the targeted minimum loss based estimator of the restricted mean survival time proposed by Díaz et al. (2015) (See also Moore and van der Laan, 2011).

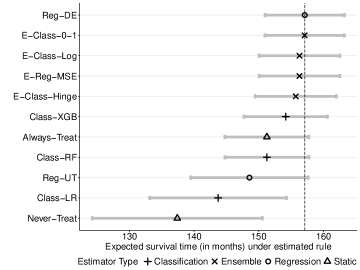

Figure 1 presents the estimated restricted mean survival time obtained with each estimated rule, along with 95% confidence intervals. For comparison, we also present the value of two static rules of interest: never treat and always treat. As is clear from the figure, the best algorithm in our application is regression of the blip function. All super learning ensembles yield a similar value, demonstrating the oracle property of the super learner. Treating patients according to the optimal rule yields a restricted mean survival of 157.1 (s.d. 3.1) months. In comparison with the always treat rule, which yields 151.2 (s.d., 3.3) months, the optimal rule improves mean patient survival by 6 months.

According to Table 2, only the super learning ensemble based on the 0-1 loss assigns a large weight to the best algorithm. In fact, its restricted mean survival time (see Figure 1) is identical to that of the optimal rule. The other ensembles assign more weight to the second best algorithm, weighted classification using extreme gradient boosting, and have slightly smaller restricted mean survival time. This is in agreement with our theoretical findings that the best performance is obtained using the 0-1 loss function.

It is also worth noting that three of the estimated rules (weighted classification using random forests and logistic regression, and regression of the function ) yield a restricted mean survival time smaller or equal than the restricted mean survival time of the static rule always treat.

Table 3 in the Supplementary Materials shows the p-value for the pair-wise comparisons of the value of each estimated rule. A few interesting points to note are:

-

(i)

The ensemble using the 0-1 loss function outperforms the other ensembles, the difference in values is small but significant at 5% level.

-

(ii)

The value of the optimal rule, which is obtained through regression of the blip function (see Figure 1), is significantly different from all other rules, except the ensemble using the 0-1 loss function. This illustrates the theoretical property of super-learning stating that the risk of the ensemble converges to the risk of the best candidate in the library.

-

(iii)

Weighted classification using logistic regression, which is often advocated because it yields parsimonious rules (e.g., Zhang et al., 2015), has a value significantly lower than the static rule always treat.

In our application, we have decided to use data splitting to train and assess the performance of the estimated rules. Though correct, this approach may be unnecessary, since the value of the rule may be assessed using the training dataset, under certain conditions derived by Luedtke et al. (2016).

7 Discussion

We present two methods for constructing an ensemble individualized treatment rule. The methods are based on a plug-in estimator optimizing the prediction error of the blip function, and a weighted classification approach which directly estimates the decision function. Though we found no theoretical differences between the two approaches in terms of their asymptotic properties, the classification ensemble using the 0-1 loss function yielded better treatment rules than the other approaches in our illustrative application. The superiority of the classification approach has been recognized before (e.g., Zhao et al., 2012), and is a consequence of the fact that it emphasizes optimizing the decision rule rather than prediction accuracy emphasized by the blip approach.

We consider a survival time measured in a discrete time scale. Most clinical research studies measure time to event in a discrete scale. In our motivating application, time to relapse of cancer or death was measured in days. We foresee no technical difficulties in extending our approach to consider a continuous time to event. This can be achieved by replacing discrete time hazards by their continuous counterpart, as well as replacing certain sums over time by the appropriate martingale integrals (see Bai et al., 2016) in the definition of the censoring unbiased transformation . A potential practical limitation is that the software and literature for data-adaptive machine learning estimation of continuous time hazards (required for the nuisance parameters) is scarce in comparison to that of binary classification, which may be used for estimation of discrete time hazards. Among the few methods that can be used for this problem are (semi)-parametric models such as Cox regression and accelerated failure time models. Available data adaptive approaches include survival random forests and regularized Cox regression. If time is measured on a continuous scale, implementation of our methods requires discretization. The specific choice of the discretization intervals may be guided by what is clinically relevant. For example, in cancer research, the clinically relevant scale would typically be a week or a month. In the absence of clinical criteria to guide the choice of discretization level, a concern is that too coarse of a discretization may lead to relevant information loss. A question for future research is how to optimally set the level of discretization in order to trade off information loss versus estimator precision. Another area for future research is to consider discretization levels that get finer with sample size.

We present doubly robust oracle inequalities and convergence rates assuming (i) an exposure of interest that occurs at baseline, and (ii) censoring which is confounded with the time to event only by baseline variables. We conjecture that our general results apply to the more general case of a dynamic treatment regime with a time-varying treatment and time-varying confounders. Such results will be the subject of future research.

In our definition of oracle risk and oracle selector we have used a nuisance parameter satisfying either , or . Therefore these oracle quantities change depending on which of the two nuisance parameters is correctly specified. According to efficient estimation theory in semi-parametric models, we expect the case to yield oracle quantities with minimal variability. In the single misspecification case in which or but not both, it is unclear to us whether misspecification of one of the models yields better results than the other. Lastly, our setup includes as particular case the inverse probability weighted loss function, which may be obtained by using a constant estimator , as well as the g-computation loss function, which is obtained by using and .

References

- Audibert et al. (2007) Jean-Yves Audibert, Alexandre B Tsybakov, et al. Fast learning rates for plug-in classifiers. The Annals of statistics, 35(2):608–633, 2007.

- Bai et al. (2016) Xiaofei Bai, Anastasios A Tsiatis, Wenbin Lu, and Rui Song. Optimal treatment regimes for survival endpoints using a locally-efficient doubly-robust estimator from a classification perspective. Lifetime Data Analysis, pages 1–20, 2016.

- Bartlett et al. (2006) Peter L Bartlett, Michael I Jordan, and Jon D McAuliffe. Convexity, classification, and risk bounds. Journal of the American Statistical Association, 101(473):138–156, 2006.

- Díaz et al. (2015) Iván Díaz, Elizabeth Colantuoni, and Michael Rosenblum. Improved efficiency in the analysis of randomized trials with survival outcomes. arXiv preprint arXiv:1511.08404, 2015.

- Dudoit and van der Laan (2005) S. Dudoit and M.J. van der Laan. Asymptotics of cross-validated risk estimation in estimator selection and performance assessment. Statistical Methodology, 2(2):131–154, 2005.

- Fan and Gijbels (1994) Jianqing Fan and Irène Gijbels. Censored regression: local linear approximations and their applications. Journal of the American Statistical Association, 89(426):560–570, 1994.

- Geng et al. (2015) Yuan Geng, Hao Helen Zhang, and Wenbin Lu. On optimal treatment regimes selection for mean survival time. Statistics in medicine, 34(7):1169–1184, 2015.

- Goldberg and Kosorok (2012) Yair Goldberg and Michael R Kosorok. Q-learning with censored data. Annals of statistics, 40(1):529, 2012.

- Kuhn et al. (2016) Max Kuhn, Contributions from Jed Wing, Steve Weston, Andre Williams, Chris Keefer, Allan Engelhardt, Tony Cooper, Zachary Mayer, Brenton Kenkel, the R Core Team, Michael Benesty, Reynald Lescarbeau, Andrew Ziem, Luca Scrucca, Yuan Tang, Can Candan, and Tyler Hunt. caret: Classification and Regression Training, 2016. URL https://CRAN.R-project.org/package=caret. R package version 6.0-73.

- Luedtke and Chambaz (2017) Alexander Luedtke and Antoine Chambaz. Faster rates for policy learning. arXiv preprint arXiv:1704.06431, 2017.

- Luedtke and van der Laan (2016) Alexander R Luedtke and Mark J van der Laan. Super-learning of an optimal dynamic treatment rule. The international journal of biostatistics, 12(1):305–332, 2016.

- Luedtke et al. (2016) Alexander R Luedtke, Mark J Van Der Laan, et al. Statistical inference for the mean outcome under a possibly non-unique optimal treatment strategy. The Annals of Statistics, 44(2):713–742, 2016.

- McKeague and Qian (2014) Ian W McKeague and Min Qian. Estimation of treatment policies based on functional predictors. Statistica Sinica, 24(3):1461, 2014.

- Moore and van der Laan (2011) KellyL. Moore and MarkJ. van der Laan. Rcts with time-to-event outcomes. In Targeted Learning, Springer Series in Statistics, pages 259–269. Springer New York, 2011. ISBN 978-1-4419-9781-4.

- Moore and van der Laan (2009) KL Moore and MJ van der Laan. Increasing power in randomized trials with right censored outcomes through covariate adjustment. Journal of biopharmaceutical statistics, 19(6):1099–1131, 2009.

- Perez et al. (2011) Edith A Perez, Edward H Romond, Vera J Suman, Jong-Hyeon Jeong, Nancy E Davidson, Charles E Geyer Jr, Silvana Martino, Eleftherios P Mamounas, Peter A Kaufman, and Norman Wolmark. Four-year follow-up of trastuzumab plus adjuvant chemotherapy for operable human epidermal growth factor receptor 2–positive breast cancer: Joint analysis of data from ncctg n9831 and nsabp b-31. Journal of Clinical Oncology, 29(25):3366–3373, 2011.

- Perou et al. (2000) Charles M Perou, Therese Sørlie, Michael B Eisen, Matt van de Rijn, Stefanie S Jeffrey, Christian A Rees, Jonathan R Pollack, Douglas T Ross, Hilde Johnsen, Lars A Akslen, et al. Molecular portraits of human breast tumours. Nature, 406(6797):747–752, 2000.

- Polley et al. (2016) Eric Polley, Erin LeDell, and Mark van der Laan. SuperLearner: Super Learner Prediction, 2016. URL https://CRAN.R-project.org/package=SuperLearner. R package version 2.0-19.

- Qian and Murphy (2011) Min Qian and Susan A Murphy. Performance guarantees for individualized treatment rules. Annals of statistics, 39(2):1180, 2011.

- Robins (1997) James M Robins. Causal inference from complex longitudinal data. In Latent variable modeling and applications to causality, pages 69–117. Springer, 1997.

- Romond et al. (2005) Edward H Romond, Edith A Perez, John Bryant, Vera J Suman, Charles E Geyer Jr, Nancy E Davidson, Elizabeth Tan-Chiu, Silvana Martino, Soonmyung Paik, Peter A Kaufman, et al. Trastuzumab plus adjuvant chemotherapy for operable her2-positive breast cancer. New England Journal of Medicine, 353(16):1673–1684, 2005.

- Rowan (1990) Thomas Harvey Rowan. Functional Stability Analysis of Numerical Algorithms. PhD thesis, Austin, TX, USA, 1990. UMI Order No. GAX90-31702.

- Rubin and van der Laan (2007) Daniel Rubin and Mark J van der Laan. A doubly robust censoring unbiased transformation. The international journal of biostatistics, 3(1), 2007.

- Rubin et al. (2012) Daniel B Rubin, Mark J van der Laan, et al. Statistical issues and limitations in personalized medicine research with clinical trials. The international journal of biostatistics, 8(1):1–20, 2012.

- Rubin (1987) Donald B Rubin. Multiple Imputation for Nonresponse in Surveys. John Wiley & Sons, 1987.

- Seshadri et al. (1993) Ram Seshadri, FA Firgaira, DJ Horsfall, K McCaul, V Setlur, and P Kitchen. Clinical significance of her-2/neu oncogene amplification in primary breast cancer. the south australian breast cancer study group. Journal of Clinical Oncology, 11(10):1936–1942, 1993.

- Slamon et al. (2001) Dennis J Slamon, Brian Leyland-Jones, Steven Shak, Hank Fuchs, Virginia Paton, Alex Bajamonde, Thomas Fleming, Wolfgang Eiermann, Janet Wolter, Mark Pegram, et al. Use of chemotherapy plus a monoclonal antibody against her2 for metastatic breast cancer that overexpresses her2. New England Journal of Medicine, 344(11):783–792, 2001.

- Slamon (1987) DJ Slamon. Human breast cancer: correlation of relapse and. Science, 3798106(177):235, 1987.

- Song et al. (2015) Rui Song, Michael Kosorok, Donglin Zeng, Yingqi Zhao, Eric Laber, and Ming Yuan. On sparse representation for optimal individualized treatment selection with penalized outcome weighted learning. Stat, 4(1):59–68, 2015.

- Sotiriou and Pusztai (2009) Christos Sotiriou and Lajos Pusztai. Gene-expression signatures in breast cancer. New England Journal of Medicine, 360(8):790–800, 2009.

- van der Laan and Dudoit (2003) M.J. van der Laan and S. Dudoit. Unified cross-validation methodology for selection among estimators and a general cross-validated adaptive epsilon-net estimator: Finite sample oracle inequalities and examples. Technical report, Division of Biostatistics, University of California, Berkeley, November 2003.

- van der Laan et al. (2007) M.J. van der Laan, E. Polley, and A. Hubbard. Super learner. Statistical Applications in Genetics & Molecular Biology, 6(25):Article 25, 2007.

- van der Laan & S. Dudoit & A.W. van der Vaart (2006) M.J. van der Laan & S. Dudoit & A.W. van der Vaart. The cross-validated adaptive epsilon-net estimator. Statistics & Decisions, 24(3):373–395, 2006.

- van der Vaart (1998) A. W. van der Vaart. Asymptotic Statistics. Cambridge University Press, 1998.

- van der Vaart et al. (2006) A.W. van der Vaart, S. Dudoit, and M.J. van der Laan. Oracle inequalities for multi-fold cross-validation. Statistics & Decisions, 24(3):351–371, 2006.

- Wolpert (2002) David H. Wolpert. The Supervised Learning No-Free-Lunch Theorems, pages 25–42. Springer London, London, 2002. ISBN 978-1-4471-0123-9.

- Zhang et al. (2015) Yichi Zhang, Eric B Laber, Anastasios Tsiatis, and Marie Davidian. Using decision lists to construct interpretable and parsimonious treatment regimes. Biometrics, 71(4):895–904, 2015.

- Zhao et al. (2015) Ying-Qi Zhao, Donglin Zeng, Eric B Laber, Rui Song, Ming Yuan, and Michael Rene Kosorok. Doubly robust learning for estimating individualized treatment with censored data. Biometrika, 102(1):151–168, 2015.

- Zhao et al. (2012) Yingqi Zhao, Donglin Zeng, A John Rush, and Michael R Kosorok. Estimating individualized treatment rules using outcome weighted learning. Journal of the American Statistical Association, 107(499):1106–1118, 2012.

- Zhao et al. (2011) Yufan Zhao, Donglin Zeng, Mark A Socinski, and Michael R Kosorok. Reinforcement learning strategies for clinical trials in nonsmall cell lung cancer. Biometrics, 67(4):1422–1433, 2011.

8 Supplementary Material

8.1 Motivating application

| SL-Class-Log | 0.026 | |||||||||

| SL-Class-Hinge | 0.026 | 0.159 | ||||||||

| SL-Reg | 0.025 | 0.160 | 0.443 | |||||||

| D-Class-RF | 0.001 | 0.001 | 0.001 | 0.001 | ||||||

| D-Class-XGB | 0.001 | 0.009 | 0.007 | 0.007 | 0.003 | |||||

| D-Class-GLM | 0.001 | 0.001 | 0.001 | 0.001 | 0.011 | 0.001 | ||||

| D-Reg | 0.001 | 0.004 | 0.002 | 0.002 | 0.158 | 0.021 | 0.056 | |||

| B-Reg | 0.120 | 0.025 | 0.023 | 0.023 | 0.001 | 0.001 | 0.001 | 0.001 | ||

| Always-Treat | 0.001 | 0.001 | 0.001 | 0.001 | 0.003 | 0.011 | 0.158 | 0.001 | ||

| Never-Treat | 0.001 | 0.001 | 0.001 | 0.001 | 0.001 | 0.001 | 0.036 | 0.002 | 0.001 | 0.001 |

| SL-Class-0-1 | SL-Class-Log | SL-Class-Hinge | SL-Reg | D-Class-RF | D-Class-XGB | D-Class-GLM | D-Reg | B-Reg | Always-Treat |

8.2 Proofs of Theorems and Lemmas

8.2.1 Lemma 1

Proof For simplicity, consider the treatment-time-specific function

and note that . For a function we denote . Conditioning first on in the above display yields

Thus, we have

Plugging in or yields the result.

∎

8.2.2 Theorem 1

Proof We start by assuming the minimization of the risk in the definition of and is carried out in a grid of polynomial size in (that is ) for some , but do away with this assumption at the end of the proof. Let ad denote the cross-validated and oracle selectors when the risk minimization is performed in rather than . We use to denote the empirical distribution corresponding to the validation set , as well as to denote an average across validation splits. We denote . Let

Define the centered loss function

In this proof we denote with the corresponding centered risks, i.e., denote

the corresponding cross-validated and oracle risks. For notational convenience we denote . Note that . For we have

| (11) | ||||

| (12) | ||||

| (13) | ||||

where the second inequality is a consequence of the definition of as the minimizer of , and the last equality is the result of adding and subtracting some terms. Denote (11) with , (12) with , and (13) with .

Note that the assumptions of the theorem imply that for some constant . This, together with Lemma 5 below, allow the application of Lemma 3 in van der Laan and Dudoit (2003) (see also pages 143-145 of Dudoit and van der Laan, 2005) to show that

It remains to analyze and . First, we write , where

For , note that . This yields, for ,

Conditioning on first, from the definition of , Lemma 1 shows that the second term in the right hand side is zero. Conditioning on first along with the proof of Lemma 1 and the Cauchy-Schwartz inequality also yields

where the last inequality follows from Lemma 5 in Appendix 8.2.5 and the definition of as the minimizer of , and the second to last inequality follows from Cauchy-Schwartz applied to the norm defined by the inner product . For , note that is an empirical processes with index set , where the latter set is finite. We will apply the following inequality for empirical processes with finite index set:

| (14) |

where is an envelope of . This result is a direct consequence of Lemma 19.38 of van der Vaart (1998). Note that the all functions in satisfy

where the second inequality follows from Lemma 5. Thus, the envelope of is bounded by the same quantity. This, together with (14) shows

This proves

which is equivalent to for

The quadratic formula implies , which yields

| (15) |

From our definitions and assumptions, the function satisfies the Lipschitz condition

where denotes the supremum norm and the

Euclidean norm. Thus and

are both bounded by , which

allows us to replace by in (15),

completing the proof of the theorem.

∎

8.2.3 Theorem 2

Proof

For convenience in the calculations we use the loss function

which is equivalent to the one used in the Theorem. Let , , , and be defined as in the proof of Theorem 1. We have

Define

Since, by definition, , we have

van der Laan and Dudoit (2003), page 26, show that

In the proof of Theorem 2, we show that

completing the proof of first claim of the theorem.

Assume now condition C.5 holds with such that The proof in this case has the same steps as the proof of Theorem 1 and we will only provide a sketch. The conditions of the Theorem allow application of Lemma 4 below to obtain

For and we get

For , note that is an empirical processes with index set , where the latter set is the finite set with points in which is computed. We will apply inequality (14). Note that the all functions in satisfy

where the second inequality follows from Lemma 5. Thus, the envelope of is bounded by the same quantity. This, together with (14) shows

This completes the proof.

∎

8.2.4 Lemma 2

8.2.5 Lemmas

Lemma 3.

Consider the assumptions of Theorem 1. Let . We have

Proof First, note that

In light of Lemma 1 we have

Note that . Thus

which completes the proof of the lemma.

∎

Lemma 4.

Proof We have

∎

Lemma 5.

Proof First let and . Then and straightforward algebra shows

Analogously, for and we have

Now, for and we get

Putting these results together proves the lemma.

∎

Lemma 6.

For two sequences and we have

Proof

Replace by in the right hand

side and expand the sum to notice it is a telescoping sum.

∎