Hyperbolic Discounting of the Far-Distant Future

Abstract. We prove an analogue of Weitzman’s [7] famous result that an exponential discounter who is uncertain of the appropriate exponential discount rate should discount the far-distant future using the lowest (i.e., most patient) of the possible discount rates. Our analogous result applies to a hyperbolic discounter who is uncertain about the appropriate hyperbolic discount rate. In this case, the far-distant future should be discounted using the probability-weighted harmonic mean of the possible hyperbolic discount rates.

Keywords: Hyperbolic discounting, Uncertainty.

JEL Classification: D71, D90.

1 Introduction

Consider an individiual -- or Social Planner -- who ranks streams of outcomes over a continuous and unbounded time horizon using a discounted utility criterion with discount function . We assume throughout that is differentiable, strictly decreasing and satisfies . For example, might have the exponential form

for some constant discount (or time preference) rate, . Such discounting may be motivated by suitable preference axioms ([4]) or as a survival function with constant hazard rate, ([6]). For an arbitrary (i.e., not necessarily exponential) discount function, Weitzman ([7]) defines the local (or instantaneous) discount rate, , using the relationship:

| (1) |

Note that is constant if (and only if) has the exponential form.

Weitzman ([7]) considers a scenario in which the decision-maker is uncertain about the appropriate discount function to use. She may, for example, be uncertain about the true (constant) hazard rate of her survival function, as in [6]. The decision-maker entertains possible scenarios corresponding to possible discount functions , , with associated local discount rate functions . Suppose that scenario has probability , with , and that the decision-maker discounts according to the expected (or certainty equivalent) discount function

| (2) |

(Such a discount function may also arise if the decision-maker is a utilitarian Social Planner for a population of heterogeneous individuals, as in [5].)

Let be the local discount rate function associated with certainty equivalent discount function (2). Weitzman [7] studies the limit behaviour of as . He proves that if each converges to a limit, then converges to the lowest of these limits. In other words, if

for each , then

| (3) |

Moreover, if each is constant (i.e., each is exponential), then declines monotonically to this limit ([7]).111In fact, this is true more generally – see [7, footnote 6].

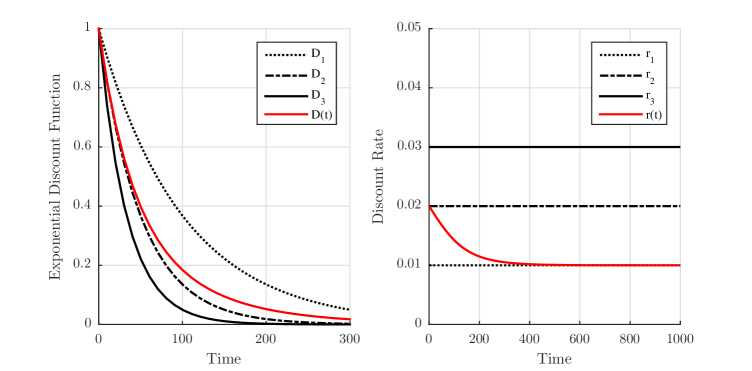

Example 1.

Suppose each is exponential, so that is constant. Then the results in [7] imply that declines monotonically with limit . Figure 1 illustrates for the case , , , and .

Weitzman’s result may be interpreted as saying that the mixed discount function (2) behaves locally as an exponential discount function with discount rate (3) when discounting outcomes in the far distant future. This result is most salient if the the individual functions are themselves exponential, as in Example 1. However, many individuals do not discount exponentially ([2]). If the functions all fall within some non-exponential class, it is natural to characterise the local asymptotic behaviour of (2) using the same class of functions. The next section considers the hyperbolic class.

2 The case of proportional hyperbolic discounting

In this section we assume that each has the (proportional) hyperbolic form

where is the hyperbolic discount rate. We further assume that . In particular, exhibits the most ‘‘patience’’ and the least -- see [1] and Example 2.

Note that

and hence for each . In other words, the limiting local (exponential) discount rate is the same for each discount function, reflecting the fact that hyperbolic functions decline more slowly than exponentials for large . Weitzman’s result is not very informative for this scenario.

Instead, we should like to have a local hyperbolic approximation to the mixed discount function (2), which may not itself have the proportional hyperbolic form. We therefore follow Weitzman’s example and define the local (or instantaneous) hyperbolic discount rate, , as follows:

| (4) |

Note that is constant if (and only if) has the proportional hyperbolic form.

How does behave as ?

The following two results, which are proved in the Appendix, answer this question. In order to state the second result, we remind the reader that the weighted harmonic mean of non-negative values with non-negative weights satisfying is

It is well-known that the weighted harmonic mean is smaller than the corresponding weighted arithmetic mean (i.e., expected value).

Theorem 1.

The local hyperbolic discount rate, , is strictly decreasing.

Theorem 2.

The local hyperbolic discount rate of the certainty equivalent discount function converges to the probability-weighted harmonic mean of the individual hyperbolic discount rates. That is

as .

The following example illustrates both results.

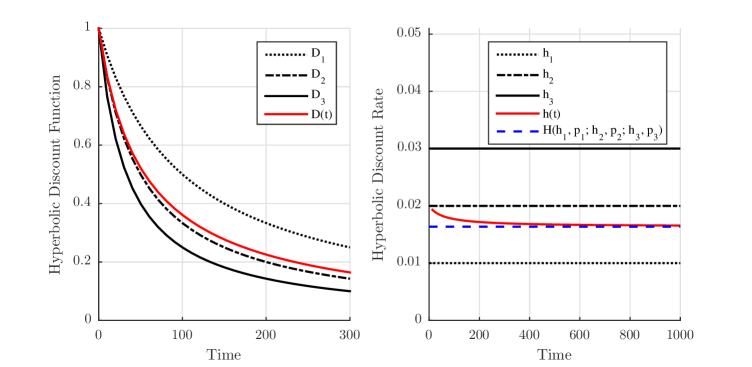

Example 2.

Suppose , , , and . Note that corresponds to the arithmetic mean of , and . Figure 2 displays the monotonic decline of towards the weighted harmonic mean .

3 Discussion

With exponential discounting, uncertainty about the (exponential) discount rate implies that the far-distant future is discounted according to the most ‘‘patient’’ of the possible discount functions.222See, in particular, the important reformulation of Weitzman’s result by Gollier and Weitzman ([3]), which resolves the so-called “Weitzman-Gollier puzzle”. If discounting is hyperbolic, with uncertainty about the (hyperbolic) discount rate, all possible discount functions matter for the discounting of the far-distant future. The asymptotic local hyperbolic discount rate is, however, below the average (i.e., arithmetic mean) of the possible rates.

Acknowledgments

Nina Anchugina gratefully acknowledges financial support from the University of Auckland. Arkadii Slinko was supported by the Royal Society of New Zealand Marsden Fund 3706352.

Appendix A Appendix

A.1 Proof of Theorem 1

We prove this statement by induction on . First we need to prove that the statement holds for . In this case:

for each . Rearranging:

Since we obtain:

By differentiating :

| (5) |

We need to show that . Since the denominator of (5) is positive, the sign of depends on the sign of the numerator. Therefore, we denote the numerator of (5) by and analyse it separately:

By expanding the brackets and using the fact that implies expression can be simplified further:

Therefore, since we have . Hence it follows that and is strictly decreasing.

Suppose that the proposition holds for . We need to show that it also holds for . When we have:

Since

we may write

where

By the induction hypothesis it follows that

where is strictly decreasing. Therefore,

Let , , and . Then we have

Analogously to the case , this expression can be rearranged to give:

However, in contrast to the case , is now a function of . Thus:

| (6) |

where

The denominator of (6) is strictly positive, so the sign of the derivative is the same as that of . Note that

where is defined as above, but with and . Since (with equality if and only if ) and , it suffices to show

| (7) |

Cancelling terms on the left-hand side of (7) leaves us with:

We now use the fact that to get

which is strictly positive. This establishes the required inequality (7) and completes the proof.

A.2 Proof of Theorem 2

We note that

where when . Let . Hence it follows that:

where as . This implies that as .

References

- [1] N. Anchugina, M.J. Ryan, and A. Slinko. Aggregating time preferences with decreasing impatience. arXiv preprint arXiv:1604.01819, April 2016.

- [2] S. Frederick, G. Loewenstein, and T. O’Donoghue. Time discounting and time preference: A critical review. Journal of Economic Literature, 40(2):351--401, 2002.

- [3] C. Gollier and M. L. Weitzman. How should the distant future be discounted when discount rates are uncertain? Economics Letters, 107:350--353, 2010.

- [4] C. M. Harvey. Value functions for infinite-period planning. Management Science, 32(9):1123--1139, 1986.

- [5] M. O. Jackson and L. Yariv. Collective dynamic choice: the necessity of time inconsistency. American Economic Journal: Microeconomics, 7(4):150--178, 2015.

- [6] P. D. Sozou. On hyperbolic discounting and uncertain hazard rates. Proceedings of the Royal Society of London. Series B: Biological Sciences, 265(1409):2015--2020, 1998.

- [7] M. L. Weitzman. Why the far-distant future should be discounted at its lowest possible rate. Journal of Environmental Economics and Management, 36(3):201--208, 1998.