Regression of exchangeable relational arrays

fmarrs3@lanl.gov

2Department of Statistics, Colorado State University

3Departments of Statistics and Sociology, University of Washington

)

Abstract

Relational arrays represent

measures of association between pairs of actors, often in varied contexts or over time. Trade flows between countries, financial transactions between individuals, contact frequencies between school children in classrooms, and dynamic protein-protein interactions are all examples of relational arrays.

Elements of a relational array are often modeled as a linear function of observable covariates.

Uncertainty estimates for regression coefficient estimators – and ideally the coefficient estimators themselves – must account for dependence between elements of the array (e.g. relations involving the same actor) and existing estimators of standard errors that recognize such relational dependence rely on estimating extremely complex, heterogeneous structure across actors.

This paper develops

a new class of parsimonious coefficient and standard error estimators for regressions of relational arrays.

We leverage an exchangeability assumption to derive standard error estimators that pool information across actors and are substantially more accurate than existing estimators in a variety of settings.

This exchangeability assumption is pervasive in network and array models in the statistics literature, but not previously considered when adjusting for dependence in a regression setting with relational data.

We demonstrate improvements in inference theoretically, via a simulation study, and by analysis of a data set involving international trade.

Keywords: array data; weighted network; dependent data; generalized least squares.

1 Introduction

Entries in relational arrays quantify pairwise interactions between actors that may be of multiple types or observed over time. Examples include annual flows of migrants between countries (Aleskerov et al.,, 2017) and interactions between students over the course of a semester (Han et al.,, 2016). In economics, relational arrays are used to describe monetary transfers between individuals as part of informal insurance markets (see Bardham,, 1984; Fafchamps,, 2006; Foster and Rosenzweig,, 2001; Attanasio et al.,, 2012; Banerjee et al.,, 2013)). Other examples of data that are naturally represented as relational arrays include gene expressions (Zhang and Horvath,, 2005) and international relations (Fagiolo et al.,, 2008).

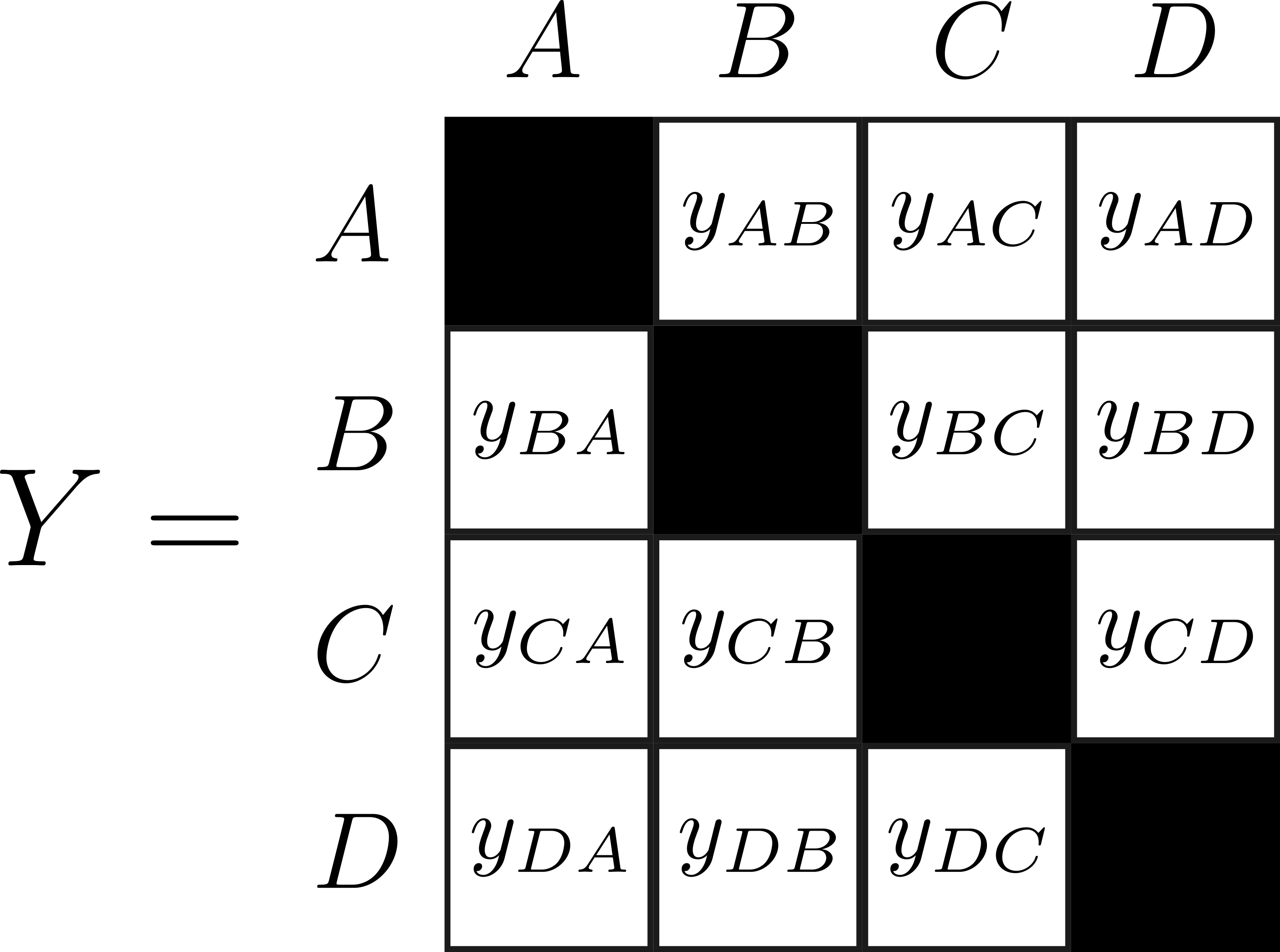

A relational array where , is composed of a series of matrices of size , each of which describes the directed pairwise relationships among actors of type , e.g. time period or relation context . The diagonal elements of each matrix, for example , are assumed to be undefined, as we do not consider, e.g., international relations of a country with itself. The relationship from actor to actor may differ than that from to , , however, the methods we propose extend to the symmetric relation case (see Section S3).

The primary goal in our setting is inference for linear regressions exploring the effects of exogenous covariates on the values in the relational array, expressed as

| (1) |

where is a continuous directed measure of the th relation from actor to actor , is a vector of covariates, and is an unobserved, scalar random error. For example, considering informal insurance markets, fafchamps2007formation examine how covariates such as geographical proximity and kinship relate to risk sharing relations after economic shocks.

A core challenge in making inference on arises from the innate dependencies among error relations involving the same actor. For example, dependence often exists between trade relations involving the same country or between economic transfers originating from the same individual. This dependence may arise due to variation unaccounted for in the covariates, for example, from differences in production levels between nations or from individual differences in risk aversion. Standard regression techniques may lead to poor estimates of and/or incorrect conclusions regarding the significance of the estimate of . Approaches to account for error dependence in relational arrays have appeared in the statistics, biostatistics, and econometrics literatures and can be characterized into two broad classes.

The first set of approaches impose a parametric model on the errors. Specifically, they either use latent variables to model the array measurements as conditionally independent given the latent structure (see holland1983stochastic; wang1987stochastic; hoff2002latent; li2002unified; hoff2005bilinear) or model the error covariance structure directly subject to a set of simplifying assumptions (see hoff2011separable; fosdick2014separable; hoff2015multilinear). While these methods allow for (possibly) improved estimation of and appropriate standard error estimators in the presence of relational dependence, the accuracy of inference on depends on the extent to which the true error structure is consistent with the specified parametric model. In addition, many of these models are estimated in a Bayesian paradigm using Markov chain Monte Carlo approaches, which are commonly computationally expensive to estimate.

The second set of approaches to accounting for relational dependence relies heavily on empirical estimates of the error structure based on the regression residuals, first proposed by fafchamps2007formation and based on the spatial dependence work of conley1999gmm. This framework is model agnostic, making as few assumptions as possible about the data generating process. One empirical approach estimates the regression coefficients using ordinary least squares, and then utilizes a sandwich covariance estimator – which is robust to a wide array of error structures – for the standard errors of the regression coefficients (fafchamps2007formation; aronow2015cluster). In finite samples, this estimator is hindered by the need to estimate a large number of covariance parameters with limited observations (king2014robust for a discussion in other contexts), and is the reason why wakefield2013bayesian suggests such estimators be labeled empirical rather than robust. We observe that standard errors from this empirical framework are often highly variable and are anticonservative.

In this work, we introduce an empirical estimation approach for relational arrays that incorporates an exchangeability assumption. This assumption is implicit in many of the model-based approaches discussed previously and is a hallmark of Bayesian hierarchical models within, and outside, the relational context (orbanz2015bayesian). Our key contribution is to define the covariance matrix (and a corresponding estimator) of the relational error array under exchangeability. Use of our parsimonious estimator produces superior estimates of and its standard errors relative to existing approaches, and our estimator is easier to compute than existing Bayesian model-based and exchangeable bootstrapping (menzel2017bootstrap; green2017bootstrapping) approaches. Reproduction code is available at https://github.com/fmarrs3/netreg_public and methods are implemented in R package netregR.

2 Inference in relational regression

2.1 Estimation of regression coefficients

We employ a least squares framework to perform inference on in the relational regression model in (1) aitkin1935least. An unbiased estimator for is the ordinary least squares estimator, , where is an matrix of covariate vectors and is a vectorized representation of . The least squares estimator is the best linear unbiased estimator for when the covariance matrix is proportional to the identity matrix. Dependence is expected in relational data, e.g. between relations and which share actor . If were known, the best linear unbiased estimator for is the generalized least squares estimator of aitkin1935least,

| (2) |

In practice, is unknown and must be estimated. Given estimator , alternating estimation of with (2) (replacing with at each iteration) is termed feasible generalized least squares. When is consistent, feasible generalized least squares is asymptotically efficient for (greene2003econometric; hansen2015econometrics).

Regardless of whether the ordinary least squares estimator or (2) is used to estimate , uncertainty estimates are required for inference. A common approach is to approximate the distribution of the estimate as a multivariate normal random variable and construct confidence intervals using an estimator of its variance: in the ordinary least squares setting,

| (3) |

and in the generalized least squares setting,

| (4) |

where is the final estimate of from the generalized least squares procedure. Variance estimators are often constructed by substituting an estimator for in (3) and (4), and are commonly termed sandwich estimators (huber1967behavior; white1980heteroskedasticity). Thus, inference for requires an estimator for , regardless of how is estimated, and properties of the estimator of depend strongly on the estimator of .

2.2 Dyadic clustering estimator

fafchamps2007formation, cameron2011robust, aronow2015cluster, and tabord2017inference propose and describe the properties of a flexible standard error estimator for relational regression which makes the sole assumption that two relations and are independent if and do not share an actor. This assumption implies that for non-overlapping relation pairs, but places no restrictions on the covariance elements for pairs of relations that share an actor. Let denote the covariance matrix of , subject to this non-overlapping pair independence assumption. fafchamps2007formation propose estimating each nonzero entry of with a product of residuals, i.e. using to estimate , where . The estimator can be seen as that which takes the empirical covariance of the residuals defined by , where is a vector of the set of residuals , and introduces zeros to enforce the non-overlapping pair independence assumption. fafchamps2007formation propose a sandwich variance estimator for in (3) based on ,

| (5) |

We refer to as the dyadic clustering estimator as it owes its derivation to the extensive literature on cluster-robust standard error estimators.

The dyadic clustering estimator in (5) has the attractive properties that it is asymptotically consistent under wide range of error dependence structures and is fast to compute. However, estimates nonzero covariance elements separately based on dependent observations, and thus, is inherently quite variable. Only when there is extreme heterogeneity in the true covariance structure is the dyadic clustering method optimal and it will suffer a loss of efficiency otherwise.

3 Standard errors under exchangeability

3.1 Exchangeability in relational models

A common modeling assumption for relational and array structured errors is exchangeability. Defined by de Finetti for a univariate sequence of random variables, exchangeability was generalized to array data by hoover1979relations and aldous1981representations. The errors in a relational data model are jointly exchangeable if the probability distribution of the error array is invariant under any simultaneous permutation of the rows and columns, and secondary permutation of the third dimension. Mathematically, this means where is the error array with its indices reordered according to permutation operators and . Intuitively, exchangeability in the regression context means the observed covariates are sufficiently informative such that the labels of the rows and columns in the error array are uninformative. Similarly the ordering of the third dimension of the error array is uninformative to its distribution. This assumption may be appropriate when the third dimension of the array represents different contexts of observations (such as economic trade sectors) that have no inherent ordering, or when the third dimension represents time periods, but the bulk of the temporal variation is accounted for in the covariates. Many of the conditionally independent parametric latent variable models cited in the Introduction have this joint exchangeability property (hoff2008modeling; bickel2009nonparametric).

|

|

3.2 Impact of exchangeability on covariance structure

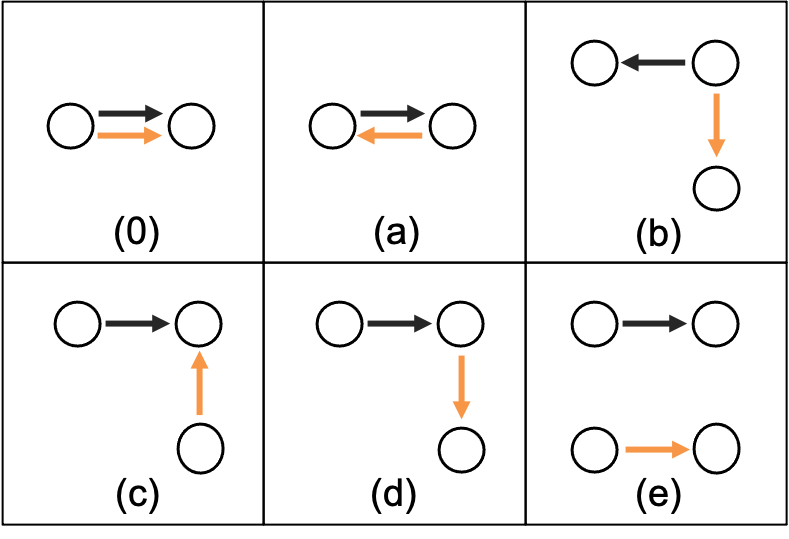

li2002unified and hoff2005bilinear describe several particular random effects models for . The corresponding error covariance matrices have different entries depending on the model, yet all covariance matrices have at most six unique entries. A key contribution of this paper is to formalize and extend this observation, showing that any jointly exchangeable model for relational array results in an of the same form, with at most six unique terms when and at most twelve unique terms when .

Proposition 1.

If a probability model for a directed relational array is jointly exchangeable and has finite second moments, then the covariance matrix of contains at most twelve unique values.

The twelve (possibly) unique entries in correspond to the twelve distinguishable configurations of relation pairs and with unlabeled actors. The twelve configurations can be separated into two sets of six identical configurations of relations and with unlabeled actors, as depicted in Figure 1, where each set corresponds to and . A proof is provided in Section S4.

3.3 Covariance matrices of exchangeable relational arrays

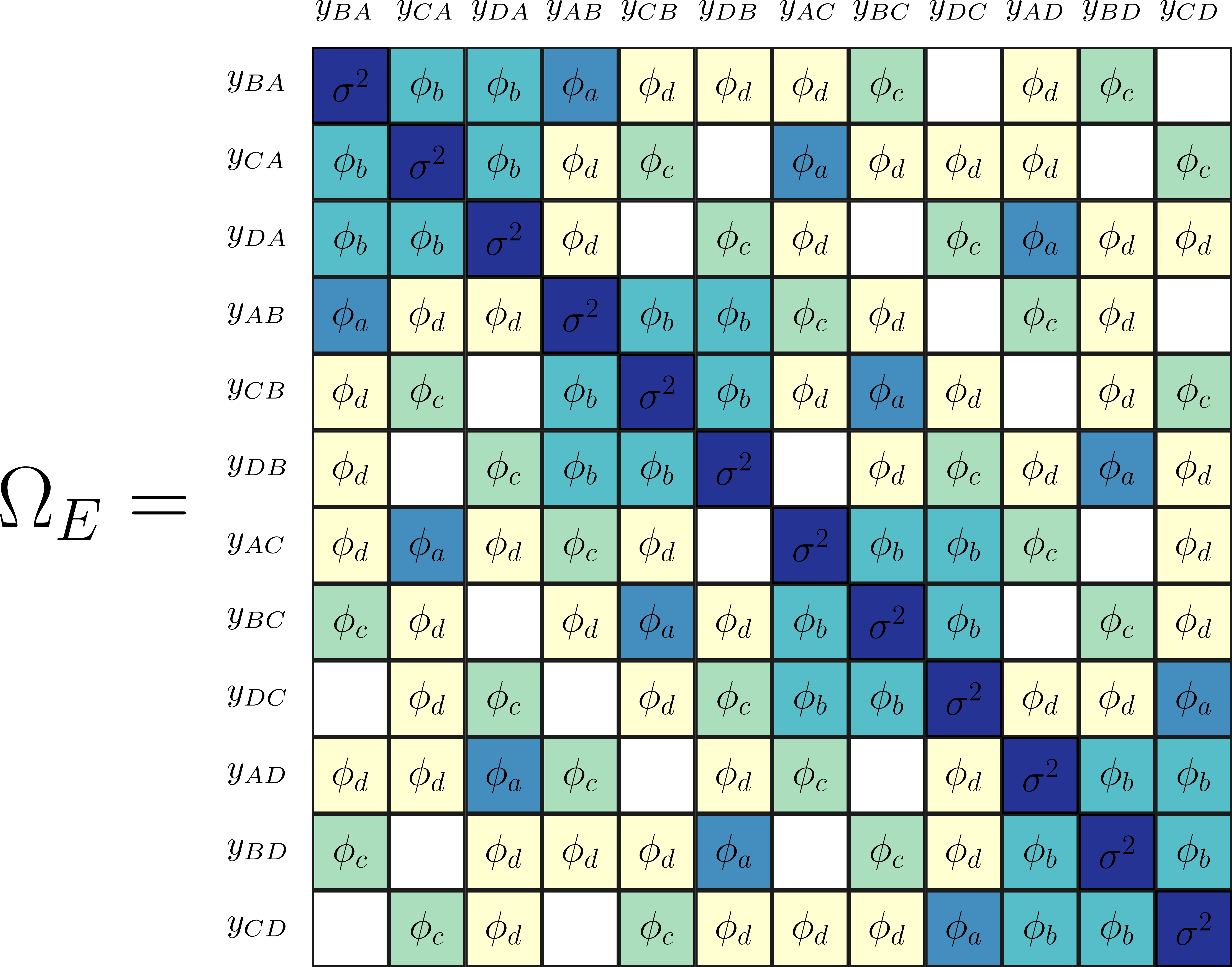

Similar to the dyadic clustering estimator, we assume non-overlapping relation pairs are independent, such that , for any and when are distinct. This assumption sets two of the twelve parameters in to zero. We introduce a new class of covariance matrices which contain ten possibly nonzero entries, , associated with the left panel in Figure 1. The separation of covariances by and implies that consists of blocks of and , each consisting of five nonzero terms for () and (), respectively (Figure 1, right panel). We define an exchangeable covariance matrix as any covariance matrix of this form and denote it .

4 Exchangeable estimator definition and evaluation

4.1 Exchangeable covariance estimator

Consider relational regression models with of the exchangeable form . The proposed exchangeable estimator of is then

| (6) |

where denotes the binary matrix with ’s in the entries corresponding to relation pairs of type as defined in Figure 1. We propose estimating the ten parameters in by averaging the residual products that share the same index configurations, corresponding to (0)-(d) in Figure 1. For example, the estimate of , corresponding to and , is

| (7) |

The remaining nine estimators for , are defined analogously, and may be interpreted as the projection of into the vector space over symmetric matrices of the form of . We provide theoretical details for the proposed exchangeable estimator, including asymtotic normality of least squares under exchangeability and consistency of in Sections S7- S9.

4.2 Comparison of exchangeable estimator with dyadic clustering

It is intuitive that the moment-based exchangeable estimator is consistent, and more efficient than the dyadic clustering estimator whenever the exchangeability assumption is satisfied. One might expect the highly parametrized dyadic clustering estimator to trade off high variance for reduced bias. However, we derive the result that the dyadic clustering estimator is biased downwards, and that this bias is larger than twice the bias of the exchangeable estimator. One concludes that one tradeoff for the robustness of the dyadic clustering estimator is anticonservatism. The proof of Theorem 2 is provided in Section S6. We provide additional theoretical details for the proposed exchangeable estimator (comparison of mean-square error with dyadic clustering) in Section S10.

Theorem 2.

Consider error vector and normally distributed covariate vector with mean zero, exchangeable covariance matrix, and bounded fourth moments, where

Then, the dyadic clustering estimator for is biased downwards,

noting that both and are .

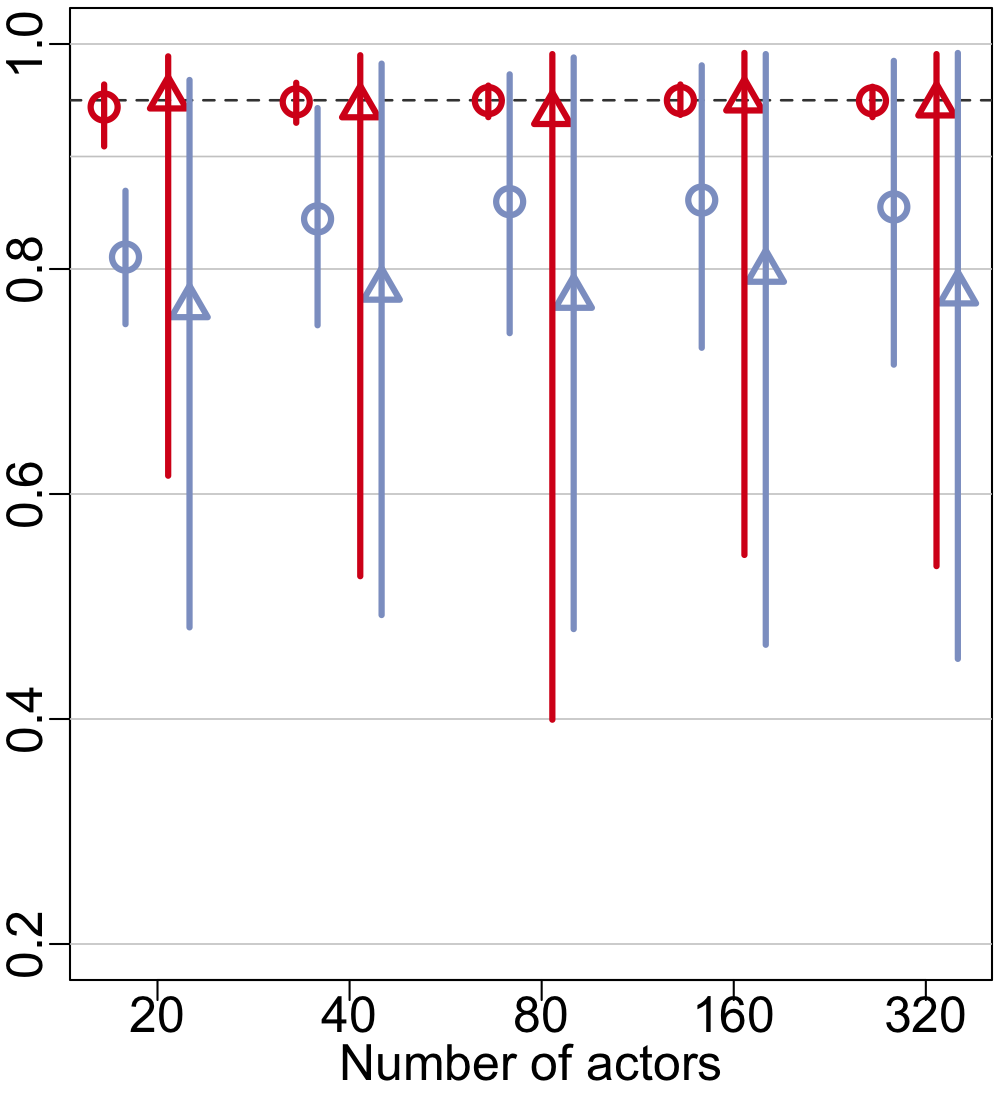

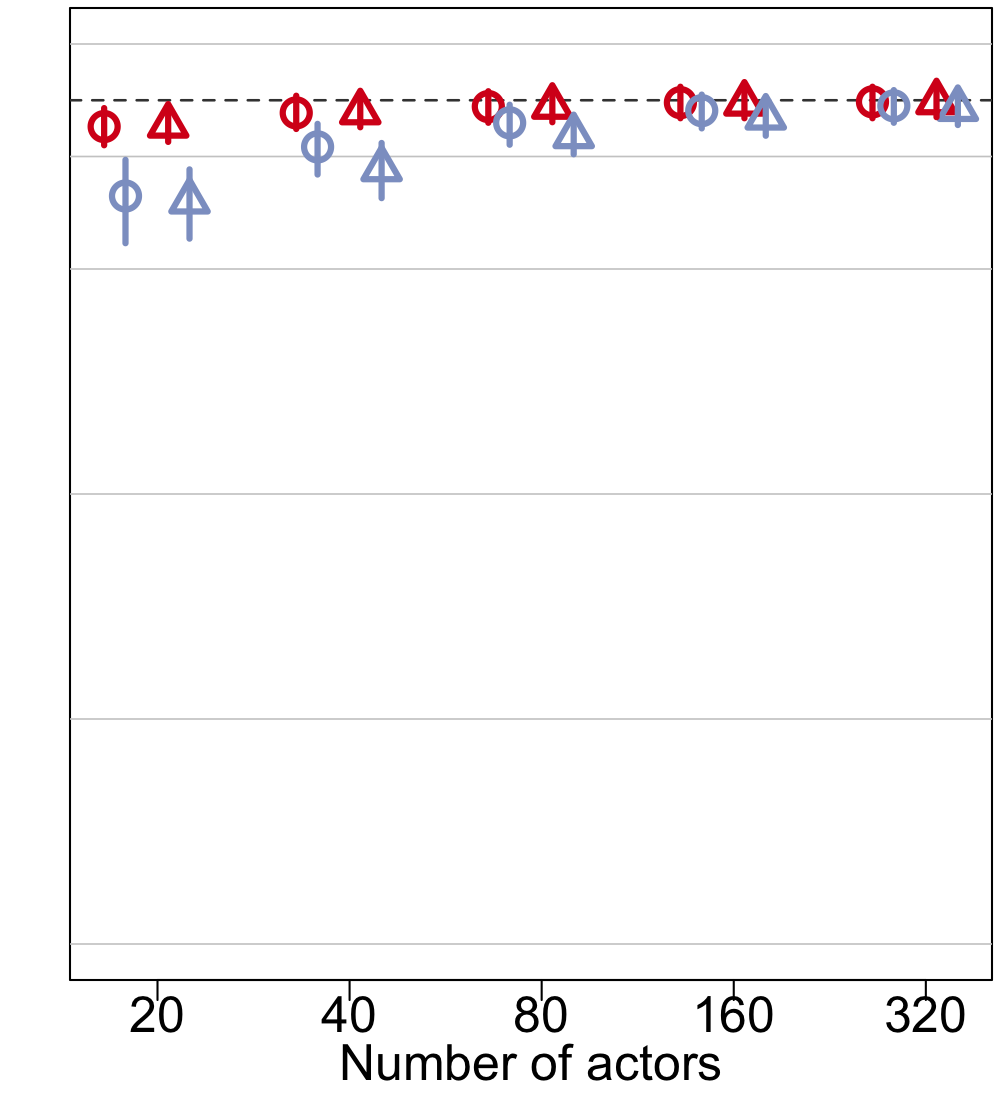

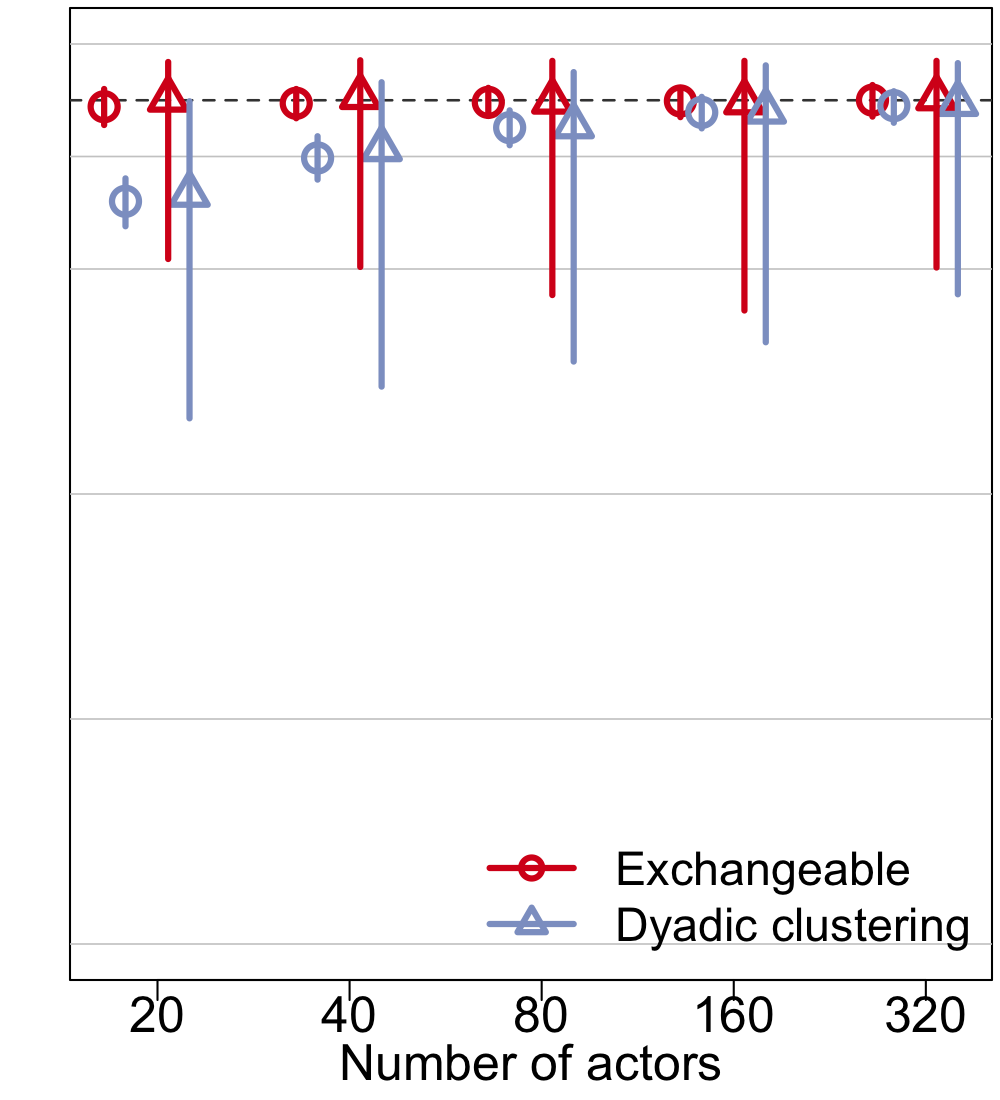

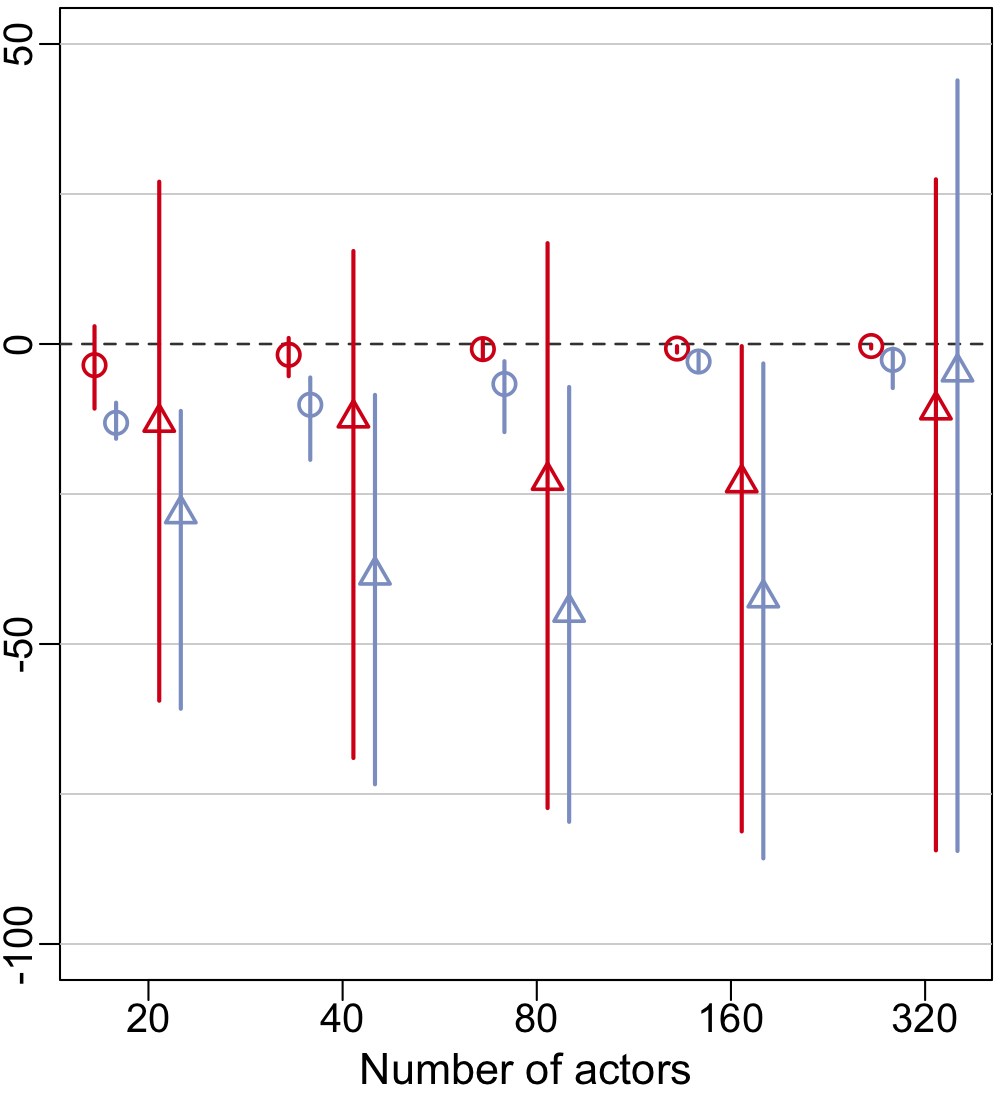

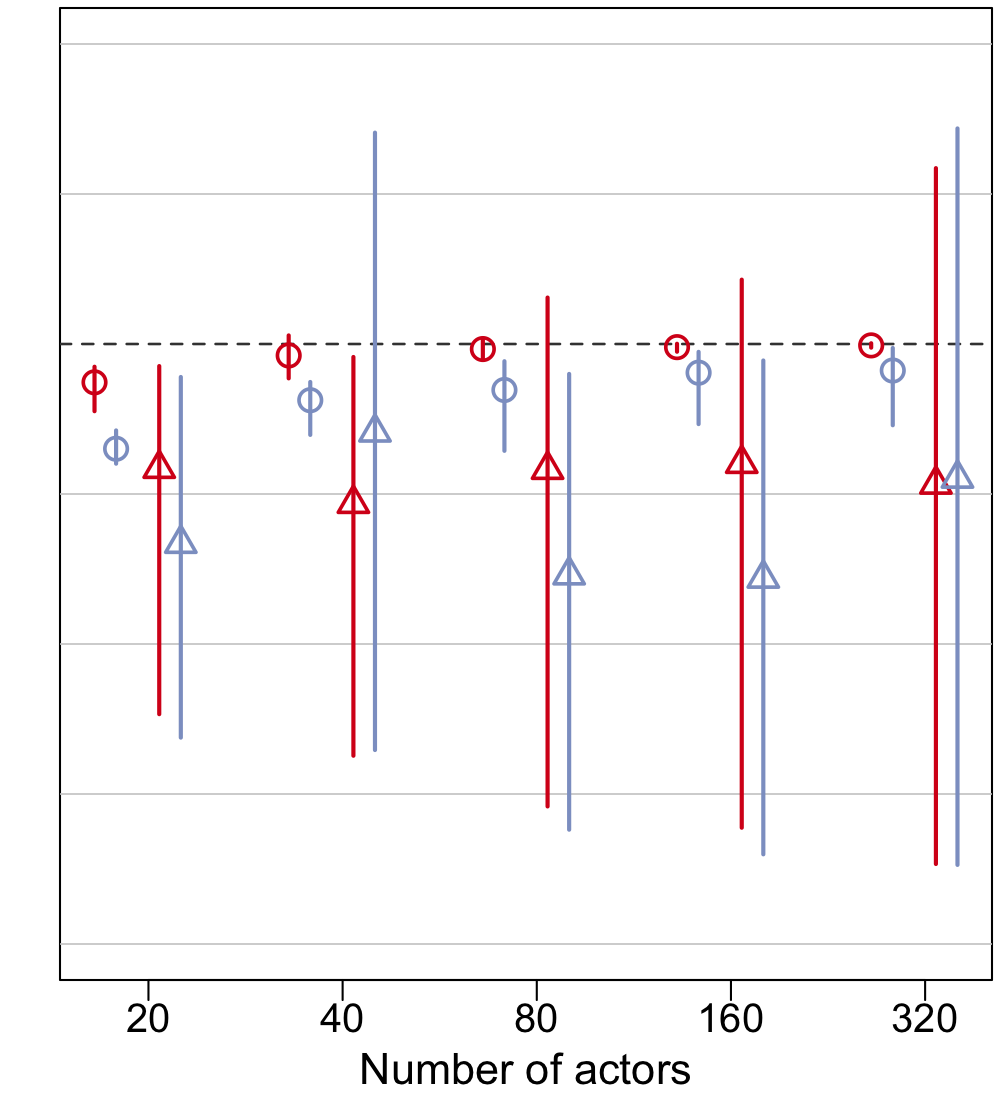

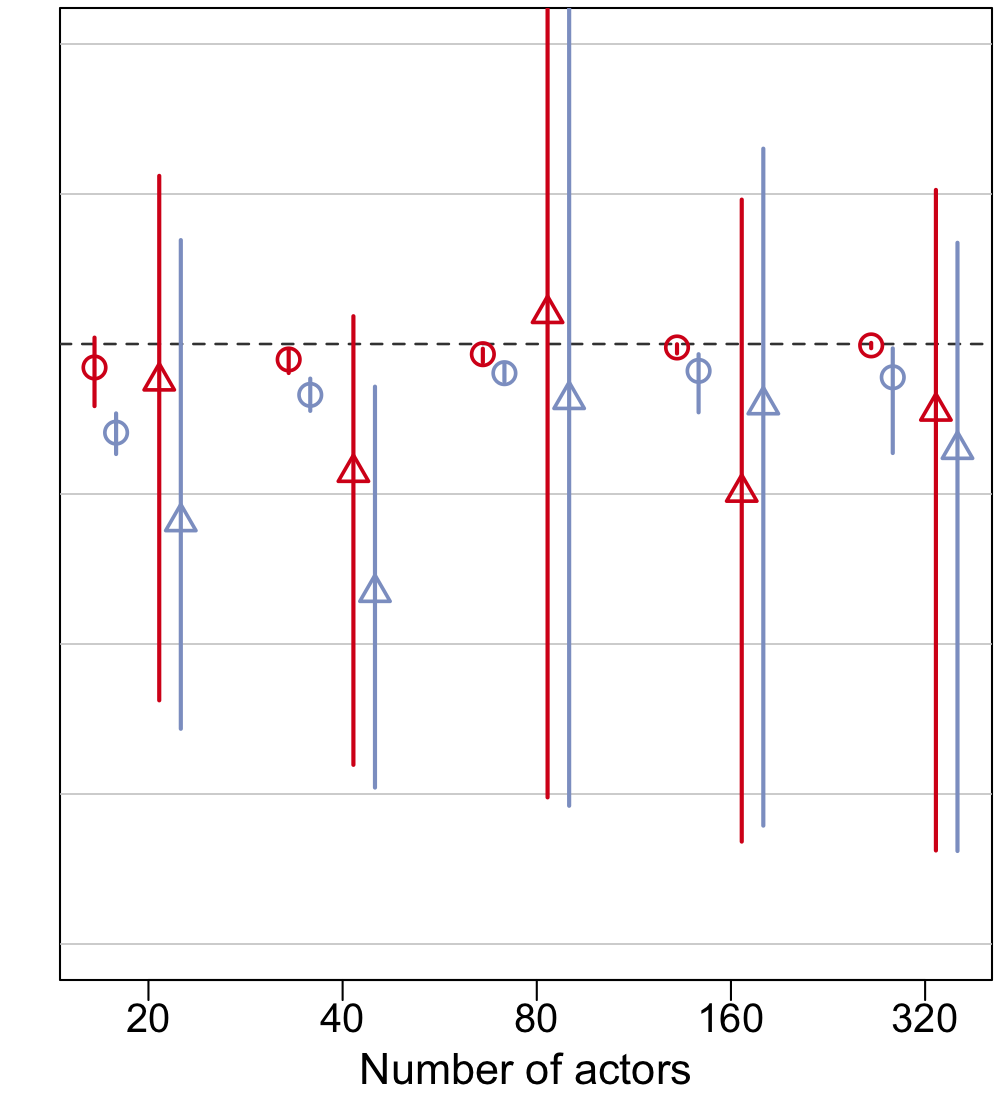

We conducted a simulation study to compare the bias and 95% confidence interval coverage when using the exchangeable and dyadic clustering estimators. We simulated from a model with three covariates (one each of binary, positive real, and real-valued) with exchangeable and non-exchangeable error models, for and (see Section S11 for details). Figure 2 shows the estimated mean coverage and middle 95% of coverages across various realizations. In all settings, the estimated mean coverage of the exchangeable estimator is closer to the nominal level than the dyadic clustering estimator. This difference is most pronounced for the binary covariate, where there is reduced signal-to-noise relative to the other covariates. The average bias of the dyadic clustering estimator is typically more than four times that of the exchangeable estimator under the exchangeable error model, confirming Theorem 2 and driving the poorer coverage performance (see Section S11.2 for details).

| binary | positive real | real-valued | |

|---|---|---|---|

|

Estimated coverage |

|

|

|

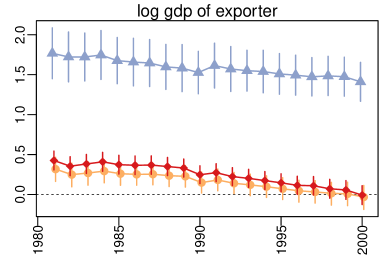

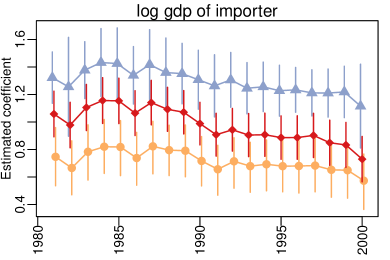

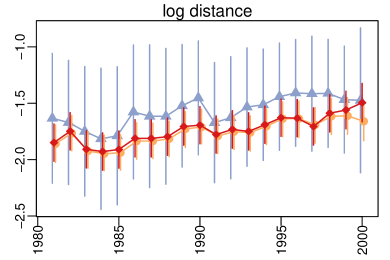

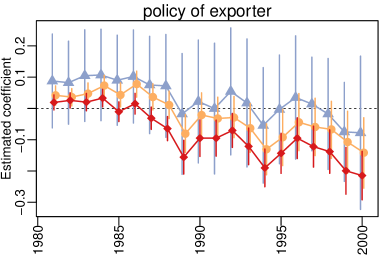

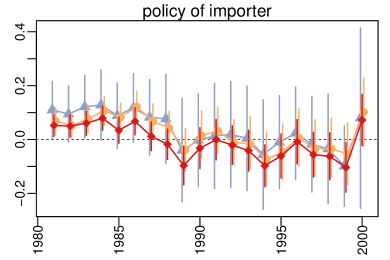

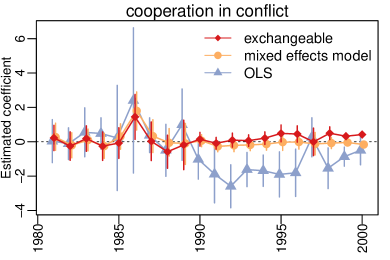

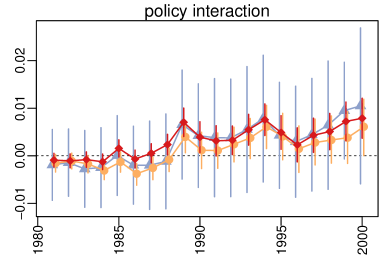

5 Patterns in international trade

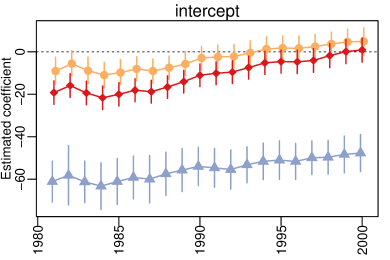

We demonstrate the implications of using our exchangeable estimator in a study of international trade among countries over years. These data were previously analyzed and made available by westveld2011mixed. Following westveld2011mixed, ward2007persistent, and tinbergen1962shaping, we use a modified gravity mean model to represent log yearly trade between each pair of countries as linear function of seven covariates in years 1981-2000. westveld2011mixed propose a model – which we refer to as the mixed effects model – which explicitly decomposes the regression error term for each time period and pair of actors into time-dependent sender and receiver effects, resulting in 13 error covariance parameters which are estimated using a latent variable representation and Bayesian Markov chain Monte Carlo methodology. We propose estimating the gravity mean model using feasible generalized least squares, assuming the errors are jointly exchangeable. As noted in Section 4.1, the proposed approach estimates ten error covariance parameters. We provide a method for efficient inversion of in this setting in Section S13.

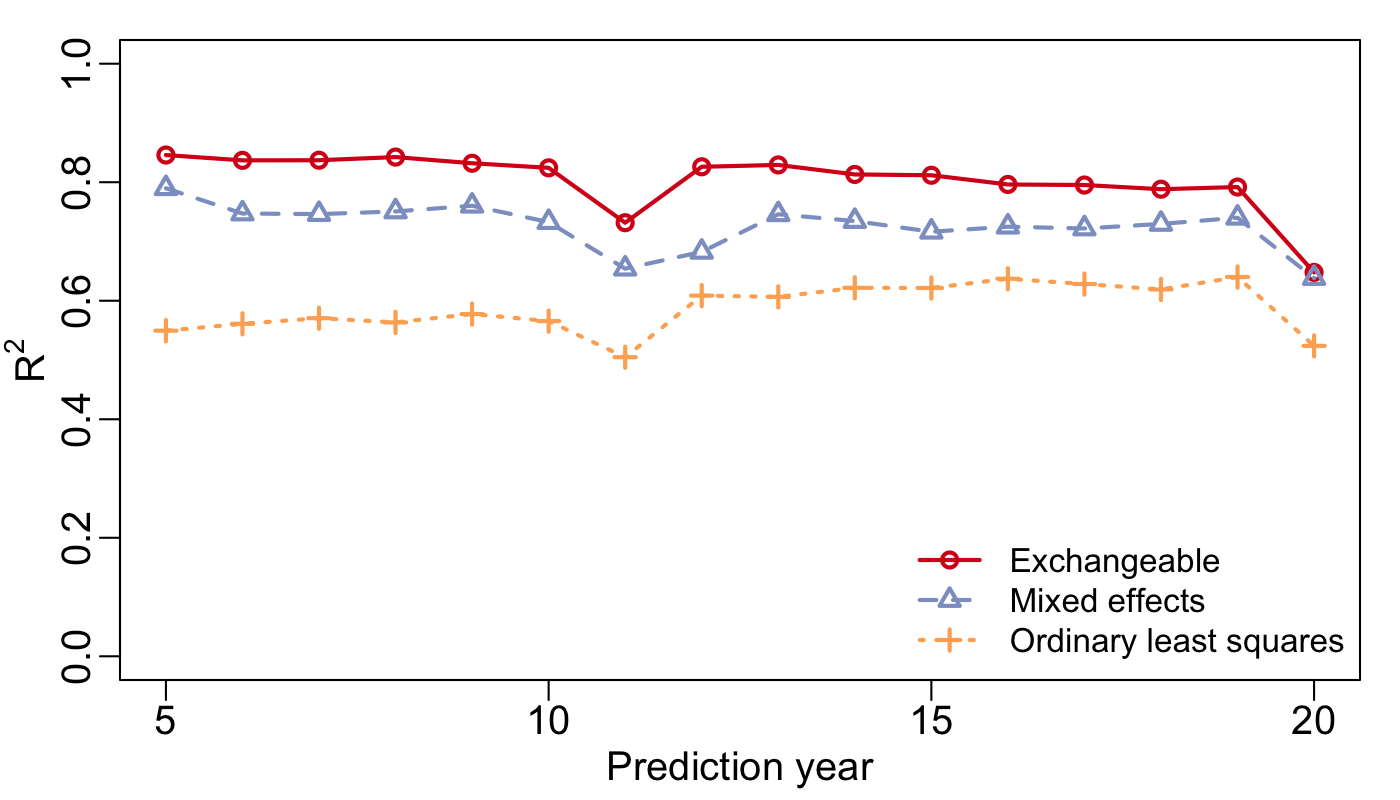

We compared the exchangeable and mixed effects approaches (and ordinary least squares as a baseline) in an out-of-sample prediction study. Here we estimated the regression coefficients using the first years of trade data for and used the estimates to predict trade values in the following year. Figure 3 provides the coefficient of determination, , for the three procedures when predicting trade flows in years 5 through 20. There is a median increase in of about 10% (30%) when using the proposed exchangeable approach relative to the mixed effects approach (and ordinary least squares, respectively). The proposed approach performs better than the other approaches for all time periods, although the gap in performance decreases as increases. These results suggest the more parsimonious exchangeable approach represents the data better than the mixed effects model, and yet, the exchangeable approach runs in a small fraction of the time of the mixed effects approach. See Section S14 for additional details.

We compared the coefficients of the ordinary least squares, mixed effects, and exchangeable approaches. The between the ordinary least squares and mixed effects coefficients is about , while the exchangeable and mixed effects coefficients have an of . About of the ordinary least squares coefficients (using dyadic clustering standard errors) were significantly different from the mixed effects coefficients, while only of the exchangeable coefficients were significantly different from the the mixed effects coefficients. Finally, the ordinary least squares coefficients have standard errors that are, on average, over times the standard errors of the exchangeable coefficients (with exchangeable standard errors). See Section S14.3 for more details. Together with the one-year-ahead prediction results, the coefficient and standard error comparisons suggest that the proposed approach can revise ordinary least squares coefficients in the direction of a higher fidelity model, giving more precise estimates of the coefficients, while requiring few modeling decisions and with limited runtime penalty. Based on the success of the exchangeable approach in the trade data analysis and simulation study, we recommend that researchers use the feasible generalized least squares estimator of the coefficient vector as demonstrated here (unless an unbiased estimator of the coefficient vector is specifically desired).

6 Discussion

The proposed exchangeable estimator leverages exchangeability for maximal symmetry (and thus maximal parsimony) in the covariance matrix of relational array . The exchangeability assumption may not be appropriate when the true error covariances are substantially heterogeneous. We propose using a permutation test based on the dyadic clustering estimator for testing the hypothesis of exchangeable errors. The procedure consists of generating a null distribution of in (5) by randomly permuting the residual array in a manner consistent with exchangeability. If the observed estimator is extreme relative to the null distribution, this suggests the errors are non-exchangeable. Details and simulations are available in Section S15.

Supplementary material

The supplementary material contains details about the estimator and analyses, proofs, further theoretical details, and a proposed test for exchangeability.

References

- Aitkin, (1935) Aitkin, A. (1935). On least squares and linear combination of observations. Proc. R. Soc. Edinb., 55:42–48.

- Aldous, (1981) Aldous, D. J. (1981). Representations for partially exchangeable arrays of random variables. J. Multivariate Anal., 11(4):581–598.

- Aleskerov et al., (2017) Aleskerov, F., Meshcheryakova, N., Rezyapova, A., and Shvydun, S. (2017). Network analysis of international migration. In Kalyagin, V. A., Nikolaev, A. I., Pardalos, P. M., and Prokopyev, O. A., editors, Models, Algorithms, and Technologies for Network Analysis, pages 177–185, Cham. Springer International Publishing.

- Aronow et al., (2015) Aronow, P. M., Samii, C., and Assenova, V. A. (2015). Cluster–robust variance estimation for dyadic data. Political Anal., 23(4):564–577.

- Attanasio et al., (2012) Attanasio, O., Barr, A., Cardenas, J. C., Genicot, G., and Meghir, C. (2012). Risk pooling, risk preferences, and social networks. Am. Econ. J., 4(2):134–167.

- Austern and Orbanz, (2018) Austern, M. and Orbanz, P. (2018). Limit theorems for invariant distributions. arXiv:1806.10661.

- Banerjee et al., (2013) Banerjee, A., Chandrasekhar, A. G., Duflo, E., and Jackson, M. O. (2013). The diffusion of microfinance. Science, 341:363–373.

- Bardham, (1984) Bardham, P. (1984). Land, labor and rural poverty. Oxford University Press.

- Bickel and Chen, (2009) Bickel, P. J. and Chen, A. (2009). A nonparametric view of network models and Newman–Girvan and other modularities. Proc. Natl. Acad. Sci. USA, 106(50):21068–21073.

- Bolthausen, (1982) Bolthausen, E. (1982). On the central limit theorem for stationary mixing random fields. Ann. Probab., 10(4):1047–1050.

- Cameron et al., (2011) Cameron, A. C., Gelbach, J. B., and Miller, D. L. (2011). Robust inference with multiway clustering. J. Bus. Econom. Statist., 29(2).

- Cameron and Miller, (2014) Cameron, A. C. and Miller, D. L. (2014). Robust inference for dyadic data. Working paper, University of California-Davis.

- Conley, (1999) Conley, T. G. (1999). GMM estimation with cross sectional dependence. J. Econometrics, 92(1):1–45.

- Cramér and Wold, (1936) Cramér, H. and Wold, H. (1936). Some theorems on distribution functions. J. Lond. Math. Soc., 1(4):290–294.

- Fafchamps, (2006) Fafchamps, M. (2006). Development and social capital. J. Develop. Studies, 42(7):1180–1198.

- Fafchamps and Gubert, (2007) Fafchamps, M. and Gubert, F. (2007). The formation of risk sharing networks. J. Dev. Econ., 83(2):326–350.

- Fagiolo et al., (2008) Fagiolo, G., Reyes, J., and Schiavo, S. (2008). On the topological properties of the world trade web: A weighted network analysis. Phys. A, 387(15):3868–3873.

- Fortini et al., (2012) Fortini, S., Ladelli, L., and Regazzini, E. (2012). Central limit theorem with exchangeable summands and mixtures of stable laws as limits. arXiv:1204.4357.

- Fosdick and Hoff, (2014) Fosdick, B. K. and Hoff, P. D. (2014). Separable factor analysis with applications to mortality data. Ann. Appl. Stat., 8(1):120–147.

- Foster and Rosenzweig, (2001) Foster, A. D. and Rosenzweig, M. R. (2001). Imperfect commitment, altruism, and the family: Evidence from transfer behavior in low-income rural areas. Rev. Econ. Stat., 83(3):389–407.

- Green and Shalizi, (2017) Green, A. and Shalizi, C. R. (2017). Bootstrapping exchangeable random graphs. arXiv:1711.00813.

- Greene, (2003) Greene, W. H. (2003). Econometric analysis. Prentice Hall, 5 edition.

- Guyon, (1995) Guyon, X. (1995). Random fields on a network: Modeling, statistics, and applications. Springer Science & Business Media.

- Han et al., (2016) Han, G., McCubbins, O., and Paulsen, T. (2016). Using social network analysis to measure student collaboration in an undergraduate capstone course. NACTA Journal, 60(2):176.

- Hansen, (2015) Hansen, B. E. (2015). Econometrics. Online at http://www.ssc.wisc.edu/~bhansen/econometrics/.

- Hoff, (2005) Hoff, P. D. (2005). Bilinear mixed-effects models for dyadic data. J. Amer. Statist. Assoc., 100(469):286–295.

- Hoff, (2008) Hoff, P. D. (2008). Modeling homophily and stochastic equivalence in symmetric relational data. In Adv. Neural Inf. Process Syst., pages 657–664.

- Hoff, (2011) Hoff, P. D. (2011). Separable covariance arrays via the Tucker product, with applications to multivariate relational data. Bayesian Anal., 6(2):179–196.

- Hoff, (2015) Hoff, P. D. (2015). Multilinear tensor regression for longitudinal relational data. Ann. Appl. Stat., 9(3):1169–1193.

- Hoff et al., (2002) Hoff, P. D., Raftery, A. E., and Handcock, M. S. (2002). Latent space approaches to social network analysis. J. Amer. Statist. Assoc., 97(460):1090–1098.

- Holland et al., (1983) Holland, P. W., Laskey, K. B., and Leinhardt, S. (1983). Stochastic blockmodels: First steps. Soc. Networks, 5(2):109–137.

- Hoover, (1979) Hoover, D. N. (1979). Relations on probability spaces and arrays of random variables. Preprint, Inst. for Adv. Study, Princeton, NJ, 2.

- Huber, (1967) Huber, P. J. (1967). The behavior of maximum likelihood estimates under nonstandard conditions. In Proc. Fifth Berkeley Symp. on Math. Statist. and Prob., volume 1, pages 221–233.

- Kallenberg, (2006) Kallenberg, O. (2006). Probabilistic Symmetries and Invariance Principles. Springer Science & Business Media.

- King and Roberts, (2015) King, G. and Roberts, M. E. (2015). How robust standard errors expose methodological problems they do not fix, and what to do about it. Polit. Anal., 23(2):159–179.

- Li and Loken, (2002) Li, H. and Loken, E. (2002). A unified theory of statistical analysis and inference for variance component models for dyadic data. Statist. Sinica, pages 519–535.

- Lumley and Hamblett, (2003) Lumley, T. and Hamblett, N. M. (2003). Asymptotics for marginal generalized linear models with sparse correlations. UW Biostatistics Working Paper Series.

- Menzel, (2017) Menzel, K. (2017). Bootstrap with clustering in two or more dimensions. arXiv:1703.03043.

- Orbanz and Roy, (2015) Orbanz, P. and Roy, D. M. (2015). Bayesian models of graphs, arrays and other exchangeable random structures. IEEE Trans. Pattern Anal. Mach. Intell., 37(2):437–461.

- Tabord-Meehan, (2018) Tabord-Meehan, M. (2018). Inference with dyadic data: Asymptotic behavior of the dyadic-robust t-statistic. Journal of Business & Economic Statistics, pages 1–10.

- Tinbergen, (1962) Tinbergen, J. (1962). Shaping the world economy: Suggestions for an international economic policy. Twentieth Century Fund, New York.

- Wakefield, (2013) Wakefield, J. (2013). Bayesian and frequentist regression methods. Springer Science & Business Media.

- Wang and Wong, (1987) Wang, Y. J. and Wong, G. Y. (1987). Stochastic blockmodels for directed graphs. J. Amer. Statist. Assoc., 82(397):8–19.

- Ward and Hoff, (2007) Ward, M. D. and Hoff, P. D. (2007). Persistent patterns of international commerce. J. Peace Res., 44(2):157–175.

- Westveld and Hoff, (2011) Westveld, A. H. and Hoff, P. D. (2011). A mixed effects model for longitudinal relational and network data, with applications to international trade and conflict. Ann. Appl. Stat., pages 843–872.

- White, (1980) White, H. (1980). A heteroskedasticity-consistent covariance matrix estimator and a direct test for heteroskedasticity. Econometrica, pages 817–838.

- Zhang and Horvath, (2005) Zhang, B. and Horvath, S. (2005). A general framework for weighted gene co-expression network analysis. Stat. Appl. Genet. Mol. Biol., 4(1).

Supplementary material for “Regression of exchangeable relational arrays”

.

Contents Page No.

S1 Patterns of exchangeable covariance matrices

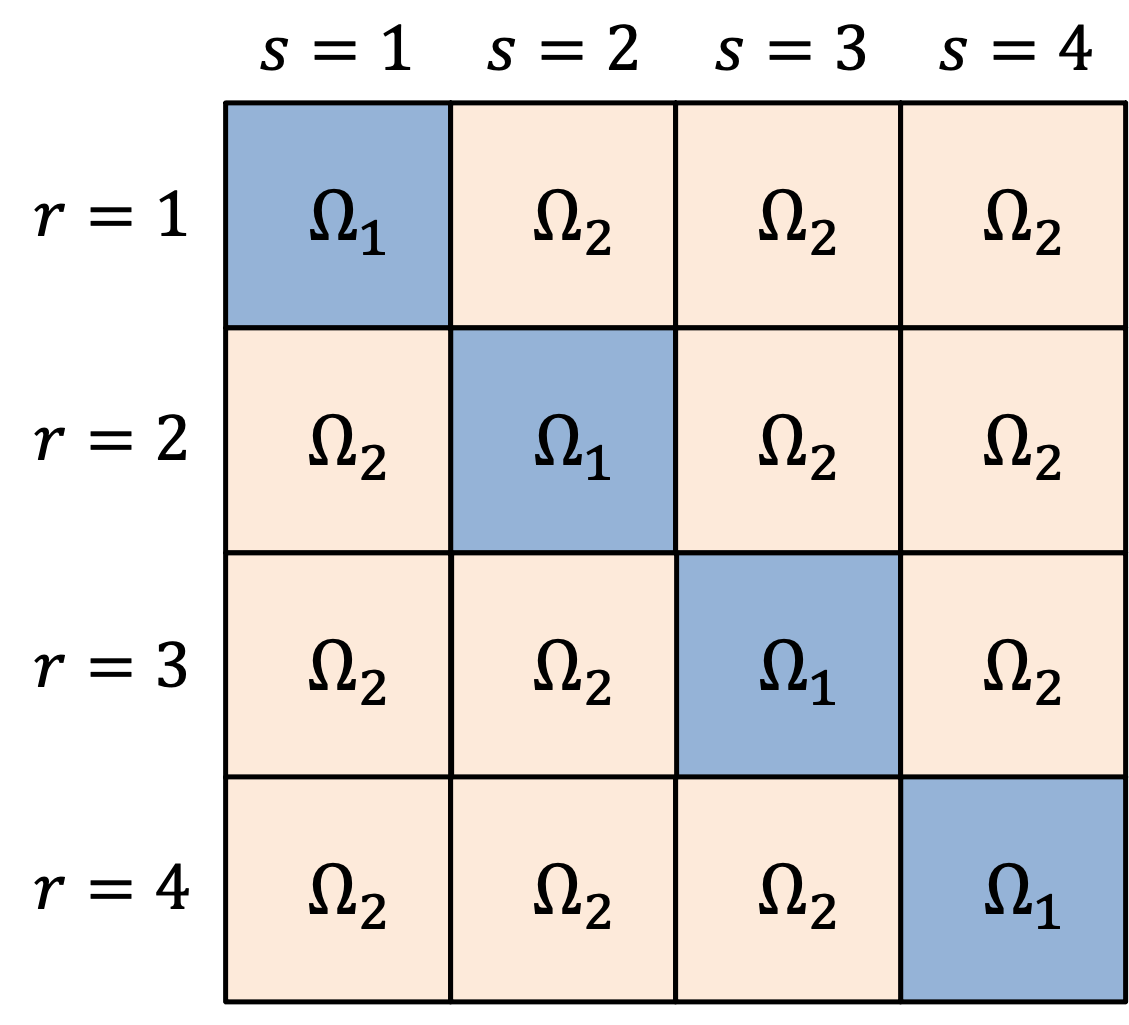

Figure S1 shows the structure of for a relational matrix with four actors and .

|

|

S2 Exchangeable estimator details

The text gives an example for the estimator of . We explicitly define the empirical mean estimates used in the exchangeable estimator in (6) below:

Recall from the text that is an estimator of , is an estimator of , is an estimator of , is an estimator of , and is an estimator of (and equivalently an estimator of ). The estimator , for , is the analogous estimator to , only when .

S3 Undirected arrays

This section specializes the results presented in the manuscript to undirected relational data. Consider the case when and suppose the relational data contains the relations among actors. The covariance of the errors contains six possibly unique elements

As in the directed case, we assume covariances corresponding to relations which share no common actor are zero. We again propose estimating the remaining nonzero covariances using the corresponding means of residuals.

S4 Proof of Proposition 1

Proof.

Consider a probability model for a directed relational array that satisfies the joint exchangeability and second moment criteria defined in the proposition. Now consider arbitrary permutations of the actor set and of the actor set . Exchangeability implies the that the probability distribution of is the same as . Thus, every entry in is marginally identically distributed, and

This is one of the entries in , the covariance matrix of .

We now move onto the covariances in ; it remains to show that there are 11 unique entries beyond the variance. This result follows from two facts. The first fact is that exchangeability implies that the bivariate distribution of the pair must be the same as bivariate distribution of , and thus,

The second fact is that permutations preserve equality and inequality, meaning that if , then , and if , then , for any permutation . We will enumerate the 11 patterns of indices that have the same bivariate distributions, as implied by the equality-inequality preservation of permutations, being mindful of the fact that the first two indices in refer to the same index set .

First take the case when and . When , we have the variance previously discussed. When , we obtain the second set of equivalent bivariate distributions (after the variance):

where it is understood that due to the network setting. Moving on, consider the case when and , noting that, by assumption, and . Then, we obtain two sets with equivalent bivariate distributions, pertaining to and :

Thus far, we have enumerated four sets of equivalent bivariate distributions under exchangeability. The remaining eight may be determined by cycling through combinations of indices in equal to, and not equal to, indices in , for both and . Table S1 summarizes the twelve index patterns that result; the first and third row in the table have already been discussed. The second row, first column, states that pairs of entries in with the index pattern form a set with the same bivariate distribution.

| (0) | ||

|---|---|---|

| (a) | ||

| (b) | ||

| (c) | ||

| (d) | ||

| (e) |

Finally, one might at first think that we have missed the bivariate distribution of . However, we note that the bivariate distribution of random variables is equal to that of , and thus, the bivariate distribution of is captured in the first column of row of Table S1. Since we have enumerated all entries in , and there are twelve possibly unique sets with equivalent covariances (or variances), the result is shown for . When , it is sufficient to consider only the first column of Table S1, which establishes that there are at most six unique entries in for . ∎

S5 Eigenvalues of exchangeable covariance matrix

S5.1 Positive definite

Since the entries in the exchangeable covariance matrix estimator are empirical averages, it is possible the estimate is not positive definite. Here we briefly investigate the constraints on the parameters that guarantee the resulting covariance matrix is positive definite when . Note that for computing the sandwich estimator variance of and making inference on , positive definiteness of is not necessary. However, if generalized least squares is employed to estimate , the inverse of the covariance matrix estimator is required, and hence it is desirable that be positive definite.

S5.2 Undirected relational data

We first focus on the undirected case, where the exchangeable covariance matrix contains two distinct nonzero entries: a variance and a parameter in the off-diagonal representing the correlation between any pairs of relations that share an actor. Below we consider the correlation matrix, rather than the covariance matrix, which contains only a single nonzero correlation value. We denote this value by .

Based on a thorough empirical investigation, we conjecture that the exchangeable correlation matrix corresponding to an undirected set of relations among actors, which has nonzero value in select off-diagonal entries, has exactly three eigenvalues as given below.

| Eigenvalue | Multiplicity |

|---|---|

The correlation matrix is positive definite if and only if all eigenvalues are positive. Thus, if , the correlation matrix is positive definite. Notice that the upper bound on does not vary with . Using the relation between and , this constraint can be re-expressed as a constraint on the covariance parameters.

S5.3 Directed relational data

Since matrices of the form of form a five-dimensional linear subspace over square symmetric matrices, it is intuitive that the eigenspace of such matrices is limited. We find empirically that square symmetric matrices of the form of have five unique eigenvalues (when ). As in the undirected case, we again focus on the exchangeable correlation matrix which contains four nonzero off-diagonal elements corresponding, respectively, in placement to in the exchange covariance matrix . Note , , and so on. Based on empirical studies, we conjecture the eigenvalues for the exchangeable correlation matrix associated with a directed set of relations among actors has exactly five eigenvalues as given below.

| Eigenvalue(s) | Multiplicity |

|---|---|

| 1 | |

where and . As in the undirected case, these constraints can be re-expressed as constraints on the original five covariance parameters.

S6 Proof of Theorem 2: bias of the exchangeable estimator

S6.1 Notation and proof preliminaries

In this section we prove that the dyadic clustering estimator is biased downwards, and that this bias is greater in absolute value than the bias of the exchangeable estimator, in the case when .

First, we make some definitions. Recall that the dyadic clustering estimator is based on the outer product of residuals, with entries corresponding to pair of relations that do not share an actor set to zero. This operation may be viewed as a projection onto a vector space of square, symmetric matrices of dimension with zeros in the appropriate entries. The dimension of this vector space is . We define the vector space below:

Definition S3.

Vector space : Let be the square matrix of dimension with a ‘1’ in the entry corresponding to relations and , and zeros elsewhere. Then,

We define the orthogonal projection of matrix onto as .

A similar definition to Definition S3 may be made concerning the space of covariance matrices corresponding to jointly exchangeable random variables, as defined below.

Definition S4.

Vector space : Let be an indicator matrix of entries in square, symmetric matrices of dimension corresponding to pairs of relations that share an actor in the manner, for . Then,

We define the orthogonal projection of matrix onto as .

It will be useful to write the dyadic clustering and exchangeable estimators as functions of the projections in Definitions S3 and S4, supposing that is orthogonal, that is, , where is a function of the number of actors . The dyadic clustering estimator of is then

| (S1) | ||||

where is column of covariate matrix . The second equality in (S1) results from the application of a property of inner products, which we apply to the inner product over matrices, where, for any projection operator , we have that . An analogous definition to (S1) holds for the exchangeable estimator of when replacing the projections onto in (S1) with projections onto .

Finally, to prove Theorem 2, we need some relationships between the error covariance parameters when is positive definite. We summarize these relationships in the inequalities in the following proposition. We drop the superscript ‘’ to lighten notation.

Proposition S5.

Let be an exchangeable correlation matrix, with . Then,

Proof.

The inequalities result from the requirement that eigenvalues of are positive for all . Taking arbitrarily large, the eigenvalues of are

The second and third eigenvalues give that . The fourth and fifth eigenvalues imply .

Using the fourth and fifth eigenvalue and rearranging,

| (S2) | ||||

Then, we have that

| (S3) | ||||

which establishes the second result. The third result follows from an analogous argument to (S3) for . The final result follows from summing the previous two, such that

∎

S6.2 Proof of Theorem 2

In this proof, we start by establishing the expression for the true variance of . Then, we write the bias of the dyadic clustering and exchangeable estimators as a function of the variance parameters of and . Then, we write the bias of the dyadic clustering estimator as a function of the bias of the exchangeable estimator, and then bound the absolute value of the bias of the exchangeable estimator, which gives the result. Throughout, we assume that the bias of the exchangeable and dyadic clustering estimators, scaled by , are . We verify this assumption at the end of the proof. Without loss of generality, we prove for the scaled problem where with .

We begin by expressing the true variance of . We require that converges in distribution to a normal random variable with finite variance, which may be expected from Proposition 3.2 in tabord2017inference. By assumption, . The true variance of is then

where we use that by assumption. Using (S1), it will be useful to rewrite the true variance

where we use the fact that is a member of both spaces and by assumption.

We now write the expectation of the dyadic clustering estimator, taking only the leading terms. First, the expectation

where is the projection onto the column space of the covariate matrix . By assumption, we have that

where is a vector of 1’s of appropriate length (in this case, length ). Using the expression of the dyadic clustering estimator in (S1), its expectation is

| (S4) | ||||

The second term in (S4) is zero in probability, as the row sums of are all the same, and are . Thus,

Then, the second term is

| (S5) |

since by assumption, which implies that the second term vanishes relative to the rest.

The third term in (S4) may be written

where is the row sum of , which again is the same for all rows. Further, using the Cauchy-Scharz inequality,

Substituting, the third term is

We now bound the order of . By assumption, , and thus

Using this bound, the third term is

| (S6) |

and the third term vanishes relative to the other terms in (S4). Further, the sixth term in (S4) is of the same order,

| (S7) |

and may also be neglected.

Using (S5), (S6), and (S7), the expression for the bias of the dyadic clustering estimator based on (S4) becomes

| (S8) |

Since, by the properties of projections, since , we may write the bias of the exchangeable estimator by analogy:

| (S9) |

We now explicitly determine the value of the exchangeable bias in (S9). By assumption,

recalling that . Then, the projection of onto the exchangeable space is

| (S10) |

and the scaled true variance is

| (S11) |

Using (S10) and (S11), the first term in the exchangeable bias in (S9) is

The second term in the exchangeable bias in (S9) is

Now we must determine for each and . Recalling that is a matrix that indicates pairs of relations and that share an actor in the manner,

| (S12) |

Then, the sums (S12) may be determined by examining the relationships between the actors in relations and . First, for any and , must share at least one actor with , as the expectation is zero otherwise. This result implies that every sum in (S12) is at most . As an example, we consider and . In this case, is of the form and is of the form . Whenever , the expectation . When , the expectation , although there are an order of magnitude fewer of these terms. Finally, similar to the expectation argument, the variance of the sums in (S12) consists of at most finite terms, and thus tends to zero. Then, the sum tends to the limit of its expectation. Summarizing, we have that

Similar counting operations give the following result, for ,

Substituting, we have the following expression for the bias of the exchangeable estimator

| (S13) | ||||

We now return to the bias of the dyadic clustering estimator in (S8). The first term in the bias of the dyadic clustering estimator is

| (S14) |

As with the exchangeable estimator, the sum in (S14) converges to the limit of its expectation, as the variance tends to zero. Then, using Iserlis’ theorem,

using the assumption that . Then, the first term in the bias of the dyadic clustering estimator in (S8) is

We now turn to the second term in the bias of the dyadic clustering estimator in (S8).

| (S15) |

where ‘’ represents element-wise multiplication. As with the exchangeable estimator, the sum in (S15) has variance that tends to zero, and converges to its expectation. Writing in sum form and using Isserlis’ theorem,

Substituting into (S15), the second term in the bias of the dyadic clustering estimator is

| (S16) |

Then, combining (S14) and (S16), we obtain the following expression for the bias of the dyadic clustering estimator,

wherein we recognize the bias of the exchangeable estimator, and

| (S17) |

Since we have positive definite and

Thus, we have shown that the bias of the dyadic clustering estimator is less than twice the bias of the exchangeable estimator. To establish that this same property holds for the absolute values of the biases, it remains to show that , that is, that the right hand side of (S17) is negative and bounded away from zero. Combining terms in (S13), the bias of the exchangeable estimator is

Now, using Proposition S5, we have that

| (S18) | |||

and thus,

| (S19) |

To establish a lower bound on the bias of the exchangeable estimator, using (S2) and (S3) in Proposition S5,

| (S20) |

and a similar argument holds for . Then, recalling from Proposition S5 that

and combining with (S20), we obtain the following bound on the key expressions in (S18),

| (S21) | ||||

To obtain the final inequality in (S21), we use the fact that to find that

and that

A similar argument to that in (S21) can be obtained starting with . Then, combining (S21) with the complete expression for the bias in (S18) and the upper bound in (S19),

| (S22) |

S6.3 A corollary to Theorem 2

In the following corollary we expand the conditions of the bias theorem slightly, such that the error array is not strictly in the exchangeable, similar to Corollary S12.

Corollary S6.

Theorem 2 holds under the relaxation exchangeability of , where the first two entries in the covariance matrix of are allowed to be heterogenous, that is, and , where . Similarly, the conditions hold when and , where the entries in matrices and are bounded.

The result follows directly from noting that the proof of Theorem 2 depends only on the values of and for for , at least up to a vanishing constant. Thus, so long as the expectations and for for are bounded, Theorem 2 holds. Corollary S6 states that even under heteroskedasticity in the covariance matrix of the error vector , the exchangeable estimator still outperforms the dyadic clustering estimator in bias. Only when the entries in corresponding to configurations (b), (c), and (d) are heterogeneous does the theory fail to hold.

S7 Theoretical properties of the exchangeable estimator

In this section, we provide additional theoretical results for the proposed exchangeable estimator. Namely, we show that the proposed exchangeable estimator is consistent and provides an improvement in mean-square error over the dyadic clustering estimator, when the assumed model is correct. First, we provide conditions under which the theory holds, and prove asymptotic normality of ordinary least squares (which is necessary for the results that follow). For brevity, we focus on the ordinary least squares coefficient estimator and the case of a singe time period or array observation, where .

S7.1 Conditions for theory

We define the conditions under which we establish the theory, starting with a formal definition of the class of exchangeable covariance matrices.

Definition S7.

An exchangeable covariance matrix is defined as arising from mean-zero random vector , where is a jointly exchangeable random matrix with entries independent whenever .

For the theoretical assessment of the exchangeable estimator, we take random, but still evaluate , , and conditional on . We assume the rows of the matrix are jointly exchangeable, meaning that a reordering of the rows to leaves the distribution of matrix invariant for any permutation . As with the dependence in the errors, we assume that two rows of that correspond to relations which do not share an actor are independent, that is row is independent row whenever . This dependence in the rows of matrix (along with some assumptions on the finiteness of its moments) implies the following:

| (S24) |

where is the set of pairs of relations that share a member in the th manner and ‘’ refers to self-relation (i.e. variance).

The theoretical setting is as follows:

Condition S8.

Define the following data generating process:

-

(A1)

The true data generating model is , where the errors are mean-zero with exchangeable covariance matrix as in Definition S7.

-

(A2)

At least one of is nonzero.

In addition, consider the following regularity conditions:

-

(B1)

The covariate matrix has rows that are jointly exchangeable with at least one of in (S24) nonzero, and where row is independent row whenever .

-

(B2)

The fourth moments of the errors and the eight moments of the covariates are bounded: and where .

-

(B3)

The errors and covariates are independent.

-

(B4)

is full rank.

S7.2 Additional theoretical results

The following theorem establishes asymptotic normality of , and supports the normal approximation to to produce confidence intervals.

Theorem S9.

Theorem S9 is similar to Proposition 3.2 in tabord2017inference, although with unbounded errors. It may be seen as an extension of central limit theorems for sums over infinitely exchangeable arrays (fortini2012central) to regression scenarios, and belongs to a broader literature on distributions of random processes that satisfy a symmetry property (kallenberg2006probabilistic; austern2018limit).

We establish consistency of the proposed estimator, and its improvement in performance over the dyadic clustering estimator, in the following three theorems.

Theorem S10.

Under Conditions S8, the exchangeable covariance estimator is consistent in the sense that

where ‘’ denotes convergence in probability.

Theorem S11.

Under Conditions S8, the mean-square error of the exchangeable estimator is less than that of the dyadic clustering estimator with probability approaching 1, that is

S7.3 Corollary to theory

S8 Proof of asymptotic normality of ordinary least squares

S8.1 Notation and outline of proof

For this proof, and throughout the remainder of the supplementary material, we adopt slightly different notation to simplify the representation of the exchangeable covariance estimator. Recall that the exchangeable covariance estimator for the OLS estimating equations is

where is the exchangeable estimate of the error covariance matrix, consisting of five averages of residual products. Here we express as

| (S25) |

This amounts to mapping , , …, , and re-indexing the and matrices accordingly. Additionally, when we consider sequences of jointly exchangeable random variables , it is understood that the sequence arises from a relational array such that entries with are undefined. Thus, sums over the sequence are of terms and we define .

We work in the asymptotic regime where actors are added incrementally to the relational data set, i.e. is continually increasing. To establish asymptotic normality of , we wish to show

where are as in (S24) and ‘’ denotes element-wise convergence in distribution.

The motivation for the proof argument follows from the expression

| (S26) |

We state that converges in probability to , and then show asymptotic normality of the second multiplicative term in (S26).

In analyzing , by condition (B1), the joint exchangeability and independence of non-overlapping pairs of the sequence extends to the component sequences in the vectors . Thus, to prove asymptotic normality of , we first prove a theorem stating that the average of a mean-zero sequence of jointly exchangeable random variables is asymptotically normal. Specifically, for mean zero and jointly exchangeable, we show

| (S27) |

for some normalizing constant and fixed sequence as .

To prove (S27), we rely on a result from bolthausen1982central, as well as a supporting lemma which we present here. Below we outline the significance of these results in the proof.

-

•

Lemma S13 (bolthausen1982central): Provides a sufficient condition for asymptotic normality of a sequence of measures based on the standard normal characteristic function.

- •

From (S27), we immediately have the marginal asymptotic normality of the sample mean of each of the vector components in the sequence . To establish joint asymptotic normality, we employ the Cramér-Wold device (cramer1936some), where asymptotic normality of , for all with , establishes joint normality. To achieve the asymptotic normality of this inner product, we simply recognize that this inner product is itself the mean of an exchangeable sequence of random variables. Joint asymptotic normality of the mean of the sequence of vectors establishes joint asymptotic normality of via (S26).

S8.2 Lemmas and theorem in support of Theorem S9

The following is Lemma 2 in bolthausen1982central and provides a sufficient condition for asymptotic normality. We abuse notation slightly, letting be the imaginary unit where appropriate.

Lemma S13 (bolthausen1982central).

Let be a sequence of probability distributions over which satisfies

-

1.

, and

-

2.

for all ,

Then,

To provide intuition for Lemma S13, the integral in condition (2) is identically zero when is the standard normal distribution.

The next lemma provides a sufficient condition on the dependence structure in necessary for the proof of asymptotic normality in (S27). Reecall that terms in with are undefined.

Lemma S14.

Let be a sequence of jointly exchangeable random variables as in Definition S7 with , where for . Then,

for some , where is the set of ordered pairs that share an index with .

Proof.

By definition we write

| (S28) |

Each covariance of (S28) is bounded by . To bound the variance, we will show the number of nonzero entries in the sum is . For , there must be overlap between the index sets and . Further, the sum in (S28) is taken over index sets that themselves contain overlap, i.e. and . For example, the index sets and have nonzero covariance in (S28). Since there are 5 unique indices in the union of the sets and , there are such index set pairs of this form in total. There are 96 pairs of index sets that result in nonzero covariance . For example, another such pair of index sets is and . Each of these 96 pairs of index sets is . Thus, the sum of covariances in (S28) is over bounded elements. ∎

It is worth noting that we repeat the counting argument in the proof of Lemma S14 in many of the following proofs, including those in later sections. Now that we have Lemma S13 and S14, we prove that a general sequence of mean-zero exchangeable random variables is asymptotically normal.

Theorem S15.

Let be a mean-zero sequence of jointly exchangeable random variables with at least one of nonzero. If , then

| (S29) |

Proof.

We first show that is the correct limiting variance. Writing the variance of the expression on the left hand side of (S29) explicitly and recalling that entries such that are undefined, we see

by the properties of joint exchangeability of as described in Section 3.3. This variance is finite and nonzero by assumption. To prove (S29), it is sufficient to show

| (S30) |

Define the limiting variance as and the sum .

To establish (S30), we employ Lemma S13, where is the probability measure corresponding to for all . The first condition of Lemma S13 is satisfied since

for and all . Thus, to prove (S30), it is sufficient to show the second condition of Lemma S13: for all , as ,

| (S31) |

We decompose the term in the expectation as in guyon1995random and lumley2003asymptotics:

where . To satisfy (S31) it remains to be shown that for each .

Beginning with , . Using this fact and Lemma S14,

for all real-valued . limiting to zero implies limits to zero, and hence limits to zero.

Now, for , by Taylor expansion of , we can write

for some and all . Using this bound and the fact that , we evaluate directly below:

for all real . As limits to zero, so does .

Finally, for , the expression sums all terms in the sequence that depend upon , including itself. Thus, and are independent. It follows immediately that

since for all ordered pairs .

S8.3 Proof of Theorem S9

We begin by writing

| (S32) |

again emphasizing that entries in the sum with are undefined and omitted. Addressing the first multiplicative term in (S32), we recall that the inverse map is continuous. Then, by (S24) and the continuous mapping theorem, we have

| (S33) |

We now analyze the second multiplicative term in (S32). Showing asymptotic normality of this term is sufficient to show asymptotic normality of the expression on the left hand side of (S32). Recall . We wish to show that the sum of vectors

| (S34) |

for some limiting variance . By the Cramér-Wold device (cramer1936some), is asymptotically normal with asymptotic variance if and only if is asymptotically normal with asymptotic variance for every vector such that . Clearly,

where we define . We wish to apply Theorem S15 to the sequence . First, the condition of finite moments in (B2) of Theorem S9 and implies that for some finite . Secondly, by the independence of and in (B3) of Theorem S9, the sequence is a mean-zero exchangeable sequence of scalar random variables. Taking the variance directly,

| (S35) |

Then, we apply Theorem S15 with in (S35), which gives that

Thus, by the Cramér-Wold device, we get the desired joint asymptotic normality

| (S36) |

Combining the convergence in probability in (S33) and the asymptotic normality of (S36), we obtain the desired result. ∎

S9 Proof of consistency of the exchangeable estimator

S9.1 Notation and outline of proof

For the proof of the consistency of the exchangeable estimator , we adopt the same change in notation as in Section S8, defined in (S25). We deviate slightly in that we denote to denote dyadic pairs and that share a member in the th manner. For example, for we must have and . We use the same assumptions as in Theorem S9.

This proof is outlined as follows. We initially prove that the exchangeable estimator is consistent if the exchangeable parameter estimates are consistent for the true parameters. We then prove consistency of in two steps: (a) we show parameter estimates based on the unobserved true errors are consistent and then (b) we show that the parameter estimates are asymptotically equivalent to . We require the consistency of result (implied by Theorem S9) for this last step.

S9.2 Proof of Theorem S10: consistency of the exchangeable estimator

First, from Theorem S9, the order of convergence of is . Thus, we choose the rate as our asymptotic regime for consistency of . We wish to show that

| (S37) |

First we show that to prove consistency of , it is sufficient to prove the consistency of the parameter estimates for the true parameters. We begin by writing the difference of variances in (S37), as

| (S38) |

where and contains the remaining terms which are functions of . By the counting argument used to show Lemma S14, each is at most , so each for some finite constant . Namely, for , when , and for . To obtain the result in (S37), it is sufficient then to show and converges in probability to some constant for all . The latter comes easily, that is, by assumption and Slutsky’s theorem,

The continuous mapping theorem allows us to take the probability limit of before inversion, as the inversion map is continuous.

We now consider consistency of the parameter estimates . First, define error averages analogous to the parameter estimates, such that for each ,

We will show converges in probability to zero, and then do the same for . This is sufficient for showing as .

To show convergence in probability of to zero, we use the argument that the bias and variance both tend to zero. By assumption (A1), for every relation pair . Thus, for all and . We now turn to the variance:

We again make a counting argument similar to that in Lemma (S14). By condition (B2), each of the covariances in the sum above are bounded. The covariance between and is nonzero only if there is overlap between their two index sets. This reduces the number of nonzero covariances from the maximum possible by a factor of at least . Again, consider the case of where . Each pair of relations in must be of the form , and thus the second set of indices must be of the form , for example, for the covariance to be nonzero. The set of indices is of order . There are other forms of relation pairs in the second sum that give rise to nonzero covariance, such as and so on. However, there are nine such forms, each of which is . Thus, the number of nonzero covariances is , and hence, we have

| (S39) |

This same argument holds for all , and thus, we have the desired consistency: for .

We now show that converges in probability to zero. We first write the expression in terms of the estimated coefficients :

| (S40) |

By Theorem S9, converges to zero in probability. By Slutsky’s theorem, if the terms in (S40) involving elements of and converge in probability to any constant, then converges in probability to zero. By (B1) and (S24) we have the convergence in probability of the term involving . Furthermore, by condition (B3), we have that . It remains to be shown that the variance of the error-covariate averages tend to zero. Consider the variance of the first error-covariate averages:

| (S41) |

In writing (S41), we use condition (B3) and simplify by conditioning on and using the law of total variance. By the same counting arguments used to establish (S39), there are nonzero bounded covariances in (S41). Thus, we have

Since the expectation and variance both tend to zero, we have

The same argument applies to the second error-covariate term in (S40). Thus, we have shown that consistency of implies

∎

S10 Proof of Theorem S11: mean-square error of the exchangeable and dyadic clustering estimators

In this section, we prove that the mean-square error of the estimator of , conditional on , is lower when using the exchangeable estimator than that when using the dyadic clustering estimator with high probability in , assuming that the error structure is exchangeable. Before proving the theorem, we provide a lemma that states that the mean-square error of the each estimator is asymptotically equivalent to the mean-square error of each estimator based on the true errors, which vastly simplifies the proof of the mean-square error theorem. Even so, we must consider higher order moments of than the covariances . So, we also provide a lemma in which we define the covariance of any pair of product of error relations and define the limiting values of the covariance of the error averages, , for every pair .

In this Section, we use the notation and , for some , to denote the convergence a sequence of numbers to a constant (possibly zero) and a nonzero constant, respectively, as grows to infinity. In other words, means that the sequence converges to a constant that may be zero. The notation means that the sequence converges to a nonzero constant. Lastly, it follows that means that the sequence converges to zero.

We use similar notation for convergence of sequences of random variables. The notation for some means that the sequence converges in distribution to a random variable (possibly a constant). The notation for some means that the sequence converges in probability to zero. Finally, we define to mean that converges in distribution to a random variable with distribution that is not a point mass at zero, and thus possibly a nonzero constant (as will always be the case in this section).

S10.1 Lemmas in support of Theorem S11

The first lemma describes the covariances of parameter estimates based on the errors, which arise in the proof of the mean-square error theorem. Of interest are the covariances for , as there are times as many of these covariances in as those covariances where at least one of or is in . However, we provide limiting values of all covariances for completeness. The proof of this lemma follows from recognizing that is a sample average and from defining all possible covariances that make up and their multiplicities.

Lemma S16.

If is a mean zero random vector with positive definite covariance matrix in the exchangeable class, , and , then the covariance for converges to

| (S42) | ||||

| where | ||||

and , , and are unknown finite constants equal to for various configurations of the sets and .

Proof.

By definition,

| (S43) |

The sum is over terms. Whenever , the covariance is zero. This removes a power of from the sum in (S43), such that the sum is over possibly nonzero covariances. The scaled sum in (S43) converges – provided that the number of values that can take is finite – as each covariance is finite by assumption and the sequence of covariances is homogeneous as grows by exchangeability. In the remainder of the proof, we enumerate and define the covariances in (S43) for particular pairs , showing that the number of values that can take is finite. This is sufficient to establish convergence.

We begin by analyzing the case of interest, that is when both and are members of . As an example, we focus on and , where the first product of error relations corresponds to the same-sender covariance (b) in Figure 1 and the second corresponds to the same-receiver covariance (c) in Figure 1. In this case, both . When and , the covariance in (S43) becomes

| (S44) |

where ‘’ denotes equality in the limit as grows to infinity.

Only pairs of relation products that share a single actor will remain in the limit, as there are an order of fewer covariances resulting from pairs of relation products that share two actors. One such pair of relation products that share a single actor correspond to the case when , i.e. , of which there are in the sum in (S44). There are covariances corresponding to the case when and , i.e. . The values of all covariances in (S44) are finite by assumption and not equal in general. However, by exchangeability, covariances resulting from pairs of relations that share an actor in the same way are equal. For example, the covariance corresponding to is the same regardless of the node labeling, that is for any set with .

There are nine ways that we may have in (S44), i.e. there are nine ways that exactly one of equals exactly one of . However, these reduce into four unique covariance values for each pair . As an example, when the covariance is the same as that when , that is . Now we define these four covariance values and their multiplicities out of the nine possible ways that exactly one of equals exactly one of :

-

•

When , we define the covariance , of which there is one out of nine possible;

-

•

When , the covariance is the same as when (multiplicity two), and we define this covariance ;

-

•

When , the covariance is the same as when (multiplicity two), and we define this covariance ;

-

•

We define the covariance when to be , of which there are four, the remaining terms of which correspond to , , and .

Now, noting that there are covariances in the sum (S44) corresponding to each of the nine possible ways that exactly one of equals exactly one of , we see that

| (S45) | ||||

where ‘’ denotes convergence in the limit as goes to infinity. Under appropriate definition of for , the same argument applies when both and are one of . When (relation products of the form and ) and , however, we then must consider covariances and from , which doubles the coefficients in (S45). This accounts for when and otherwise in (S42). The same argument applies when .

We now analyze both and in , corresponding to variance and the reciprocal covariance (a) in Figure 1. In this case, both . Taking and as an example, in the limit, the covariance in (S43) is

| (S46) |

Again, we only consider covariances corresponding to pairs of relation products that share a single actor as only these covariances survive in the limit. There are four possible ways that shares exactly one actor with . We define the three unique covariances and their multiplicities corresponding to the four ways that shares exactly one actor with as follows:

-

•

When , we define the covariance , of which there is one out of the four possibilities;

-

•

When , we define the covariance , of which there is one;

-

•

When , we define the covariance , which is the same as when , accounting for the remaining two possibilities.

Now, the fact that there are covariances in the sum (S46) corresponding to each of the four possible ways that shares exactly one actor with gives that

Of course, the same argument applies to any and both in . In the case where and , by symmetry, . Similarly, for , all .

Similar counting arguments to those in the previous paragraphs apply when one of is in and the other is in . As an example, consider and . Once again, only pairs of relations that share a single actor will remain in the limit. Then, in the limit, the covariance in (S43) becomes

| (S47) |

Now, there are six ways in which the first pair of relations share an actor with the second pair, i.e. all sets with exactly one actor from equal to exactly one other from . We define the covariances corresponding to the six possibilities below:

-

•

When , we define the covariance , of which there is one out of the six possibilities;

-

•

When , we define the covariance , of which there is one;

-

•

The overlaps where and result in the same covariance (multiplicity two), which we define ;

-

•

The overlaps where and result in the same covariance (multiplicity two), which we define .

Then, noting that there are covariances in the sum (S47) corresponding to each of the six possible ways that exactly one actor from is equal to exactly one other from , we have that converges to

| (S48) | |||

When for is appropriately defined, the same argument applies for all settings where one of is in and the other is in . When (relation products of the form and ), however, we then must consider covariances in (S47) and , which doubles the coefficients in (S48). This accounts for when and otherwise in (S42). When , for example, we have the simplification that and . ∎

The expressions for the estimators based on the errors are simpler to analyze than those based on the residuals. For example, when comparing the mean-square errors of the exchangeable and dyadic clustering estimators, it is desirable to analyze instead of . The following lemma allows us to do just this. This lemma states that mean-square errors of the estimators based on the errors are asymptotically equivalent to the mean-square error of those based on the residuals. The proof consists of first evaluating the mean-square error conditional on . We then show that converges in -probability to a nonzero constant in general and that converges in -probability to zero, implying that the difference between and is asymptotically negligible. We repeat the procedure for and .

Lemma S17.

Assuming for all and under the assumptions of Theorem S9, the mean-square error for both the exchangeable and dyadic clustering estimators based on the residuals is asymptotically equivalent to the mean-square error of each respective estimator based on the errors. That is,

| (S49) |

and analogously for dyadic clustering.

Proof.

We will focus on the exchangeable estimator first, and then the dyadic clustering estimator. Throughout, we drop the conditioning on in the mean-square error as it is understood, for example .

We begin with the exchangeable estimator. By definition, the mean-square error of the exchangeable estimator is

| (S50) |

where , the true variance of . By the Cauchy-Schwarz inequality,

| (S51) |

If we show that converges in -probability to a constant, i.e. , and that , then (S51) implies that the third additive term of (S50) is . This is sufficient to establish (S49). We begin with showing . By definition, the scaled mean-square error is , which is equal to

| (S52) |

By Lemma S16, converges to a finite constant for every . The convergence in probability of each multiplicative term in (S52) containing is defined by assumption (B1); only those with both and in survive in the limit as these have whereas for . Thus, we have that

| (S53) |

which is finite., and where ‘’ denotes convergence in -probability.

It remains to show that . To establish this fact, it is sufficient to show that , and then, by the continuous mapping theorem, , which implies the desired result. Writing directly,

| (S54) |

By assumption (B1), the multiplicative terms involving converge in probability to constants. To establish , it is sufficient show that for all . Writing this expression directly, the difference is

| (S55) |

By Theorem S9, . Also, by assumption (B1), the sum involving in the second term converges in probability to a constant; thus, the second additive term in (S55) is . Turning to the first additive term, we notice its expectation is zero, that is for all relations and . The variance is

where we use the fact that is only nonzero when relation shares an actor with relation since whenever and is independent by assumption (B3). This fact removes at least a factor of from the sum. Thus, we have that , which gives that and

which establishes (S49) for the exchangeable estimator.

The same argument following (S50) applies to the dyadic clustering estimator. To establish (S49) for the dyadic clustering estimator, it is thus sufficient to show that converges in -probability to a constant and that . We begin with the former. By definition, is

| (S56) |

where is the set of relation pairs that share an actor in any manner. Then, substituting the asymptotic values for from Lemma S16 and separating the sum by the five ways that two relations may share an actor,

| (S57) |

where ‘’ denotes equality in the limit and is the set of relations such that and and such that the pairs of relations and share a single actor as appropriate for in Lemma S16. In (S57), we substitute the limit of from assumption (B1). Also in (S57), only terms with and both in survive in the limit as the set (as detailed in Lemma S16), while the order is less for either or in , so these terms vanish in the limit. Evaluating the vector products, the expression on the right hand side of (S57) equal to

| (S58) |

where is the entry in e.g., and is the entry in pertaining to column and relation . Further, the variance is

| (S59) | |||

where and indexes the first sum and indexes the second sum. The convergence is the result of the independence portion of assumption in (B1) and the bounded moment assumption on . The variance in (S59) converges to zero for every set of covariates , every relation type and both in , and every covariance type . Thus, provided that the expectation of converges to a constant, this expression converges in probability to that same constant. This expectation is

| (S60) |

where is the entry in and we use the symmetry of for all . Unlike , for a given , the covariances in (S60) may not be the same for two relation sets in . However, by assumption (B1) and taking , , and for example, we still have that

| (S61) |

for . That is, covariances that share an actor in the same way are still equal. So, for fixed and pair of and both in , we may collect the possible covariances and average them to attain the convergent value. We thus define the limit

| (S62) | ||||

| (S63) |

where is the set of ways that correspond to . For example, when , , and , contains four index sets corresponding to the four multiplicities of as defined in Lemma (3). The convergence of (S62) results from (S61). As the average over is over a finite number of terms since each is bounded, there is no possibility of divergence. The covariances in (S62) are finite by assumption (B2) and arises from the asymptotic limit of . Taking (S62) together with (S60), we have the convergence of the expectation of . Along with (S59), convergence of the expectation of establishes the convergence of to the same limit.

Now, for a particular and both in and , we collect the set of for every and in from (S63) into a matrix defined . Substituting this definition into (S58) while noting each is symmetric, the convergent value for the dyadic clustering estimator is

| (S64) | |||

Since the convergent value in (S64) is a finite constant, it remains to show that

As with the exchangeable estimator, it is sufficient to show that . Using the residual definition , the expression for is

| (S65) | |||

where we substitute the convergence of to and have used the exchangeability property to get the factor of two on the second additive term in the center of (S65). Analyzing the first additive term in the center of (S65),

| (S66) | |||

recalling the notation that is the set of all relations that share an actor with relation and that . We attain the convergence rate by noting that the -terms in (S66) converge in probability to constants by assumption (B1) and by Theorem S9. The convergences in (S66) are for matrices; these convergences are element-wise.

We now analyze the convergence rate of the second additive term in the center of (S65),

Again, the convergence of the first multiplicative term is a result of assumption (B1) and by Theorem S9. The mean is expectation zero and by previous arguments, for example in (S34). Thus, we have , and the dyadic clustering estimator satisfies the relation in (S49). ∎

S10.2 Proof of Theorem S11

We now establish that the mean-square error of the exchangeable estimator is less than that of the dyadic clustering estimator with high probability. To do so, we show that the value to which the difference in mean-square errors converges is nonnegative. Throughout the proof, we drop the conditioning on in the mean-square error as it is understood, for example .

The asymptotic difference in mean-square errorss is as follows, where we substitute the expressions for the estimators based on the errors in (S53) and (S64), as justified by Lemma S17:

| (S67) |

It remains to show that this is a nonnegative constant. To do so, we show that the matrix in the quadratic form in (S67) is the limit of a variance matrix, and thus positive semi-definite. We will show that the scaled variance

| (S68) |