On parameter estimation with the Wasserstein distance

Abstract

Statistical inference can be performed by minimizing, over the parameter space, the Wasserstein distance between model distributions and the empirical distribution of the data. We study asymptotic properties of such minimum Wasserstein distance estimators, complementing results derived by Bassetti, Bodini and Regazzini in 2006. In particular, our results cover the misspecified setting, in which the data-generating process is not assumed to be part of the family of distributions described by the model. Our results are motivated by recent applications of minimum Wasserstein estimators to complex generative models. We discuss some difficulties arising in the approximation of these estimators and illustrate their behavior in several numerical experiments. Two of our examples are taken from the literature on approximate Bayesian computation and have likelihood functions that are not analytically tractable. Two other examples involve misspecified models. Keywords: Wasserstein distance, optimal transport, parameter inference, generative models, minimum distance estimation

1 Introduction

We consider a statistical estimation approach for parametric models that is based on minimizing the Wasserstein distance between the empirical distribution of the data and the model distributions (Belili et al.,, 1999; Bassetti et al.,, 2006). We study two different point estimators, where the first, called the minimum Wasserstein estimator (MWE), arises as the most important special case of the estimator introduced by Bassetti et al., (2006). The second, which we term the minimum expected Wasserstein estimator (MEWE), is better suited to numerical approximations.

We derive theoretical properties of the estimators, such as existence, measurability, and consistency, in the misspecified setting. That is, we do not assume that the observations are generated from the working model. For one-dimensional data, we also study the convergence rate and asymptotic distribution of the minimum Wasserstein estimator of order 1, extending the work of Bassetti and Regazzini, (2006) on location-scale models. Our proofs are based on epi-convergence (Rockafellar and Wets,, 2009) and general results on minimum distance estimation (Pollard,, 1980), and are as such different from those presented by Bassetti and coauthors.

There are two main motivations for developing these results. Firstly, recent advances in computational optimal transport have led to the application of minimum Wasserstein distance estimators in increasingly complicated settings, where the models are likely to be misspecified. For instance, Genevay et al., (2018) apply the MEWE in the tuning of image generation models, and Genevay et al., (2017) show that a version of the MEWE also appears in the popular Wasserstein GAN method (Arjovsky et al.,, 2017). This development has been driven by the advent of efficient numerical algorithms to approximate the Wasserstein distance (see e.g. Peyré et al.,, 2019; Cuturi,, 2013; Benamou et al.,, 2015; Genevay et al.,, 2016; Li et al.,, 2018; Altschuler et al.,, 2018).

Secondly, minimum Wasserstein distance estimators, which are particular instances of minimum distance estimators (Basu et al.,, 2011), appear to be practical and robust alternatives to likelihood-based estimation in the setting of generative models. In these models, synthetic observations can be generated given a parameter, but the likelihood function and associated maximum likelihood estimators might be intractable (Gouriéroux et al.,, 1993; Marin et al.,, 2012; Bernton et al.,, 2019). Some comments on the comparison between the Wasserstein distance and other distances commonly used in minimum distance estimation are provided.

The rest of this article is organized as follows: we review the definitions of minimum distance estimation, of the Wasserstein distance, and of the estimators of interest in the rest of this section. Theoretical results, whose proofs can be found in the Appendix, and some open questions are stated in Section 2. We briefly review computational strategies to compute the Wasserstein distance and the estimators in Section 3, before illustrating their behavior on various examples in Section 4. We conclude in Section 5. Code to reproduce the numerical results can be found at github.com/pierrejacob/winference.

1.1 Notation

Throughout this article we consider a probability space , with associated expectation operator , on which all the random variables are defined. The set of probability measures on a space is denoted by . The data take values in , a subset of for some , and is endowed with the Borel -algebra. We observe data points, , that are distributed according to . Let , where is the Dirac distribution with mass on . We refer to as the empirical distribution of , even in settings where the observations are not i.i.d.

A model refers to a collection of distributions on , denoted by

where is the parameter space, endowed with a distance and of dimension . However, we will often assume that the sequence of models is such that, for every , the sequence of random probability measures on converges (in some sense) to a distribution , where with . Similarly, we will often assume that converges to some distribution as . Whenever the notation and is used, it is implicitly assumed that these objects exist. In such cases, we instead refer to as the model. We say that it is well-specified if there exists such that ; otherwise it is misspecified. Parameters are identifiable if is implied by . The weak convergence of a sequence of measures to is denoted by . The Kullback-Leibler (KL) divergence between and is defined as

if is absolutely continuous with respect to , and otherwise.

1.2 Minimum distance estimation

Minimum distance estimation refers to the minimization, over the parameter , of a distance between the empirical distribution and the model distribution (Wolfowitz,, 1957; Basu et al.,, 2011). More formally, denoting by a distance or divergence on , the associated minimum distance estimator (MDE) can be defined as

| (1) |

In broad terms, the minimum distance estimation principle captures the idea of many statistical paradigms. For instance, the generalized method of moments (Hansen,, 1982) consists in minimizing a discrepancy defined as the weighted Euclidean distance between moments of and . In the empirical likelihood method (Owen,, 2001), is taken to be the KL divergence, and the model is supported strictly on the set of observed data and subject to moment conditions. The maximum likelihood estimator minimizes the KL divergence between and in the limit of the number of observations going to infinity.

However, it is worth noting that the definition in (1) precludes the naive application of some discrepancy measures. For instance, one could not directly choose to be the KL divergence or the total variation distance, since for any model distribution not supported solely on the observed data, they would evaluate to and respectively. To apply discrepancies of this kind, one would first need to build sample-based estimators of the underlying population quantity , assuming it is well-defined. Many such approaches have been studied in detail by Basu et al., (2011).

The computation of the minimum distance estimator might be intractable, especially in settings where it is assumed that one can simulate data from the model distribution but not evaluate its density. For such generative models, the following minimum expected distance estimator might be more computationally convenient:

| (2) |

where the expectation is taken over the distribution of the sample giving rise to . When is fixed and is large, or when and is large, one might hope that the expectation is close to , and that the estimators and have similar properties. Inference techniques such as the method of simulated moments (McFadden,, 1989) and indirect inference (Gouriéroux et al.,, 1993) often (implicitly) use estimators of this form, in which defined as the weighted Euclidean distance between sample moments or summary statistics of and , and the expectation in (2) is replaced with a Monte Carlo approximation.

1.3 Minimum Wasserstein estimation

In this work, we focus on minimum distance estimation with the Wasserstein distance. Let be a distance on the observation space , and let with (e.g. or ) be the set of distributions with finite -th moment, i.e. there exists such that . The -Wasserstein distance, also called the Monge-Kantorovich, Mallows, or Gini distance, is a finite metric on , defined by the optimal transport problem

| (3) |

where is the set of probability measures on with marginals and respectively; see Chapter 6 of Villani, (2008) for a brief history of this distance and its central role in optimal transport.

A useful property of the Wasserstein distance is that it is well-defined for distributions with non-overlapping supports. This allows us to define the minimum Wasserstein estimator (MWE) of order , denoted , by simply plugging into (1) in place of . Some properties of the MWE have been studied in Bassetti et al., (2006), for well-specified models and i.i.d. data; we derive new results in Section 2.1 under weaker assumptions. We also propose the minimum expected Wasserstein estimator (MEWE), obtained by replacing with in (2) and denoted . We describe some of its theoretical properties in Section 2.2.

Variations of these estimators have recently been applied by for instance Arjovsky et al., (2017) and Genevay et al., (2018). In the settings they consider, the models are likely to be misspecified, and are supported on low-dimensional manifolds that might not overlap with the support of the data-generating mechanism. While the Wasserstein distance is well-defined in that case, the KL divergence or the total variation are not. This motivates the study of minimum Wasserstein estimators for these settings.

2 Theoretical results

We prove the existence, measurability, and consistency of the MWE and MEWE under weak assumptions, allowing the model to be misspecified and to produce data with certain types of dependencies. Under stronger assumptions, we study the rate of convergence and the asymptotic distribution of the MWE when and . Throughout, we compare our results to those of Bassetti et al., (2006) and Bassetti and Regazzini, (2006).

Informally, the consistency of the MWE and MEWE can be understood as follows. Under some conditions, we expect to converge to , in the sense that as . Consequently, the minimum of might converge to the minimum of , denoted by , assuming its existence and unicity. The same can be said for the minimum of , provided also. The parameter is thus the limiting object of interest, also termed the estimand. Beyond its interpretation as the minimizer of , this parameter would coincide to the data-generating parameter if we assume that the data are generated from the model. In the misspecified case, note that is not necessarily the parameter that minimizes , which is the limit of the maximum likelihood estimator under standard regularity conditions.

2.1 Minimum Wasserstein estimator

2.1.1 Existence, measurability, and consistency

We first list assumptions on the data-generating process and on the model that are sufficient for the existence, measurability, and consistency for the MWE.

Assumption 2.1.

The data-generating process is such that , -almost surely as .

Assumption 2.2.

The map is continuous in the sense that implies as .

Assumption 2.3.

For some , the set is bounded, where .

Theorem 2.1 (Existence and consistency of the MWE).

For a generic function , let . Theorem 2.1 also holds if one replaces with , for any sequence converging to zero. If is unique, the result can be rephrased as -almost surely.

The following theorem derives from a general result by Brown and Purves, (1973) on the measurability of estimators defined as minimizers.

Theorem 2.2 (Measurability of the MWE).

Suppose that is a -compact Borel measurable subset of . Under Assumption 2.2, for any and , there exists a Borel measurable function that satisfies

Theorem 2.1 generalizes the results of Bassetti et al., (2006), where the model is assumed to be well-specified in the sense that . Moreover, Theorem 2.1 allows for data-generating processes which do not produce independent data points. For instance, if the data form a stationary and ergodic time series whose marginal distribution has finite -th moments, then Assumption 2.1 still holds. These and other sufficient conditions for Assumption 2.1 to be satisfied are elaborated upon in the Appendix. Theorem 2.2 is only a minor generalization of the result in Bassetti et al., (2006), where it is assumed that for each , is non-empty for almost every . In the next section, this small modification also enables the direct application of results by Pollard, (1980).

2.1.2 Rate of convergence and asymptotic distribution

Under conditions guaranteeing the consistency of the minimum Wasserstein estimator, we study its rate of convergence and asymptotic distribution in the case where , , . Under this setup, it can be shown that where and denote the cumulative distribution functions (CDFs) of and respectively (see e.g. Ambrosio et al.,, 2005, Theorem 6.0.2). Additionally, assume that is endowed with a norm: . We also require that is “well-separated”:

Assumption 2.4.

For all , there exists such that

This assumption is commonly made in the asymptotic study of M-estimators; see e.g. Chapter 5 of Van der Vaart, (2000) and the Appendix. We focus on the setting in which the model is well-specified, but also discuss some extensions to the misspecified setting in Section 2.1.3.

Our approach to derive asymptotic distributions follows Pollard, (1980). Let , and denote the CDFs of , and respectively. Informally speaking, we show that can be approximated by

near , for some , with . Results by del Barrio et al., (1999) and Dede, (2009) give conditions under which converges to a zero mean Gaussian process with known covariance structure, for both independent and certain classes of dependent data. Heuristically, the distribution of is then close to that of . The required form of is given in the following assumption:

Assumption 2.5.

There exists a non-singular such that

as

To provide some intuition into the nature of the “derivative” , we consider the following simple example. Let for , and for some . By Taylor expanding around (for fixed ), Assumption 2.5 can be shown to hold with , where and denote the CDF and density of a standard Gaussian variable, respectively. Next, we state a result that holds for a well-specified model producing i.i.d. data, and analogous results for misspecified models and certain types of dependent processes can be found in the Appendix.

Theorem 2.3.

A similar statement for can potentially be derived by considering the results of del Barrio et al., (2005). The condition implies the existence of second moments, and is itself implied by the existence of moments of order for some (see e.g. Section 2.9 in Wellner and van der Vaart,, 1996). The uniqueness assumption on the argmin in the limit can be relaxed by considering convergence to the entire set of minimizing values, as in the Appendix and Section 7 of Pollard, (1980). Still, uniqueness can sometimes be established, using e.g. the results of Cheney and Wulbert, (1969). This approach is taken by Bassetti and Regazzini, (2006), who directly show that Theorem 2.3 holds when is a location-scale family supported on a bounded open interval. The existence and form of can in many cases be derived if the model is differentiable in quadratic mean (Le Cam,, 1970), which is elaborated upon in the Appendix. There, one can also find results to verify Assumptions 2.1 and 2.4. It can in some cases potentially be easier to verify the assumptions for a reparameterization of , say . Provided that the theorem holds for and that the inverse map is differentiable, the limiting distribution of can be derived using a delta method argument.

Computing confidence intervals using the asymptotic distribution provided by Theorem 2.3 is hard, due in part to its dependence on unknown quantities. However, the existence of the limiting distribution is in itself sufficient to guarantee the asymptotic validity of appropriately constructed subsampling confidence intervals (Politis et al.,, 1999, Theorem 2.2.1). This also generalizes to settings with certain kinds of dependent data. Under slightly stronger assumptions, the closely related out of bootstrap produces asymptotically valid confidence intervals as well; see Bickel and Sakov, (2008) and references therein. In the numerical experiments of Section 4, we find that the standard bootstrap (Efron and Tibshirani,, 1994) works well in practice.

2.1.3 Extensions

Under slightly stronger assumptions, Theorem 2.3 can be extended to the misspecified setting. In particular, suppose that there exists a neighborhood of and a constant such that for any ,

In the well-specified case, this property is implied by Assumption 2.5. Then, as elaborated upon in the Appendix, the minimum of is attained on the set with probability going to one. Since the conditions of Theorem 2.3 imply that , this in turn implies that also. In other words, the minimum Wasserstein estimator retains its rate of convergence in the misspecified case.

To find its asymptotic distribution, one can observe that with probability going to one, the map can be approximated uniformly well over by the map which similarly achieves its minimum on . Therefore, as gets large, behaves like a minimum of

Under the conditions of Theorem 2.3, converges to in the sense of del Barrio et al., (1999). In turn, should be distributed as the minimizer(s) of as grows. A technical complication arises since this function converges pointwise to infinity, and we therefore leave formal statements for the Appendix.

Extensions to cases with multivariate data are left for future research. It is unclear whether convergence to will occur at the same rate in higher dimensions. This is because is on the order of whenever is absolutely continuous with respect to the Lebesgue measure and (see e.g. Weed and Bach,, 2019, and references therein). On the other hand, Del Barrio et al., (2019) show, under some assumptions, that the 2-Wasserstein distance satisfies the following CLT:

where has a known form and the expectation is taken with respect to the observations Similar results are expected to hold for other also. It therefore seems likely that the distance(s) between the MWE and the minimizer(s) of converges to zero at the standard rate. If these speculations hold true, one could interpret them in terms of a bias-variance trade-off: the bias would appear to be on the order of , whereas the variance is on the order of . However, note that the function depends only on population properties of . As such, it is a reasonable alternative to the objective function , and might still yield reasonable identification of the parameters. For instance, if the model is well-specified and Gaussian with being a location parameter, it seems likely that is minimized at for any . It is therefore unclear whether the slow convergence rate of the bias would always be of practical concern.

2.2 Minimum expected Wasserstein estimator

2.2.1 Existence, measurability, and consistency

In order to show similar results for the MEWE as for the MWE, we introduce the following additional assumptions.

Assumption 2.6.

For any , if , then as .

Assumption 2.7.

If , then as .

Assumption 2.6 is slightly stronger than Assumption 2.2, stating that we not only need weak convergence of the “model” distributions , but also of the sample distributions for any . Assumption 2.7 is implied by , which in turn might hold when is compact and the inequalities in Fournier and Guillin, (2015) hold.

In the next result, we prove an analogous version of Theorem 2.1 for the MEWE as . For simplicity, we write as a function of and require that as .

Theorem 2.4 (Existence and consistency of the MEWE).

Theorem 2.5 (Measurability of the MEWE).

Suppose that is a -compact Borel measurable subset of . Under Assumption 2.6, for any and and , there exists a Borel measurable function that satisfies

The results above appear to be the first of their kind for the MEWE.

2.2.2 Convergence to the MWE

The next result considers the case where the data are fixed, while . It shows that the MEWE converges to the MWE, assuming the latter exists. Using the results of Del Barrio et al., (2019) and references therein, one could potentially derive the rate of this convergence, which we leave for future work. We formulate the following additional assumption, in which the observed empirical distribution is kept fixed and .

Assumption 2.8.

For some , the set is bounded.

3 Computational aspects

3.1 Computing the Wasserstein distance

We recall some strategies to calculate or approximate the Wasserstein distance between empirical distributions. In the case where , the exact computation is cheap, as the main computational task reduces to sorting the samples. However, in dimensions , the cost is in general expensive, which has motivated a rich literature on fast approximations (Peyré et al.,, 2019). We will write for , where and stand for the empirical distributions and . The Wasserstein distance then takes the form

| (4) |

where is the set of matrices with non-negative entries, columns and rows resp. summing to and .

3.1.1 Exact computation

The formulation in (4) is a linear program, and can be solved with generic linear program solvers. However, specialized approaches can be more efficient. In the univariate case with , the optimal transport coupling can be found by sorting the vectors and to get the collections of order statistics and . Suppose that for some . Then, the -Wasserstein distance in (4) can be expressed as

| (5) |

which can be seen from the representation (see e.g. Ambrosio et al.,, 2005, Theorem 6.0.2). The cost of the Wasserstein distance computation is thus of order in the univariate setting. Note that, in some cases, the generation of sorted observations can be done directly for a cost of order , for instance by generating already-sorted uniforms and applying a quantile function (Devroye,, 1985). It should also be noted that the expression in combination with a numerical integrator, could be used whenever the quantile functions of and are known (as in the g-and-k example of Section 4.1). In that case one can directly target the MWE with a numerical optimizer, as an alternative to computing the MEWE. The same is true if the CDFs are available, using the expression given in Section 2.1.2.

In multivariate settings, one can solve the problem in (4) using dual ascent methods (see e.g. Bertsimas and Tsitsiklis,, 1997). This includes the Hungarian algorithm, applicable in the setting where , at a cost of order . Other algorithms have a cost of order , with , and can therefore be more efficient when is small (Burkard et al.,, 2009, Section 4.1.3). A practical alternative is the short-list method, derived from the network simplex algorithm, presented by Gottschlich and Schuhmacher, (2014) and implemented in the transport R package (Schuhmacher et al.,, 2017). In general, simplex algorithms come without guarantees of polynomial running times, but Gottschlich and Schuhmacher, (2014) show empirically that their method tends to have sub-cubic cost. When the cost of computing the Wasserstein distance exactly gets prohibitively large, we can resort to various approximations.

3.1.2 Approximations

In parallel with its increasing popularity as an inferential tool in statistics and machine learning, there has been fast growth in the number of algorithms that approximate the Wasserstein distance at reduced computational costs. The book of Peyré et al., (2019) provides an overview of many such methods. In particular, they provide a thorough discussion of the method introduced by Cuturi, (2013), which regularizes the optimization problem in (4) using an entropic constraint. Specifically, the regularized version of (4) reads:

| (6) |

which includes a penalty on the entropy of . The regularized problem can be solved iteratively by Sinkhorn’s algorithm (Cuturi,, 2013) or iterative Bregman projections (Benamou et al.,, 2015) for a total cost of order . Define the dual-Sinkhorn divergence . If goes to zero, the dual-Sinkhorn divergence goes to the Wasserstein distance. If goes to infinity, it converges to the energy distance (Ramdas et al.,, 2017). Other fast approximations of the Wasserstein distance include Ye et al., (2017); Altschuler et al., (2017, 2018); Li et al., (2018).

In the case where , computing the Wasserstein distance can be viewed as an assignment problem, which leads to other specialized approaches. For instance, Puccetti, (2017) proposes a greedy algorithm based on swaps in the assignment, for a cost of per iteration. When a cost of order or is too large, Bernton et al., (2019) propose a new distance generalizing the idea of sorting when . It consists in sorting samples according to their projection via the Hilbert space-filling curve and computing a distance analogous to the one in (5), for a computational cost of the order of . A similar idea underlies the sliced Wasserstein distance (Rabin et al.,, 2011; Bonneel et al.,, 2015), which can be estimated by projecting the data onto random lines, and by averaging the Wasserstein distances computed in the associated one-dimensional spaces, for a total cost on the order of .

3.2 Computing the estimators

The exact computation of the MWE and MEWE is in general intractable. This is also true when is substituted for any of its approximations mentioned above. However, we can envision various schemes to numerically approximate the estimators.

The calculation of the MEWE can be based on Monte Carlo approximation of the function using synthetic samples generated given . Assume that a data set can be sampled from by setting , where is a deterministic function of the parameter and a random variable independent of . Then, the mean , where the are i.i.d., is a natural estimate of . By the law of large numbers, we know that almost surely as . Since this estimator is an average of i.i.d. random variables, the central limit theorem indicates that the rate of convergence is . Moreover, this approximation is a deterministic function of , which can be optimized with standard methods. In turn, this optimization step can be placed within a Monte Carlo Expectation-Maximization (MCEM) algorithm (Wei and Tanner,, 1990), which would alternate between optimization of and resampling of . Convergence results for such algorithms, as both the number of iterations and go to infinity, are reviewed in Neath et al., (2013).

In practice, we are naturally constrained to finite values of and . The incremental cost of increasing is typically lower than that of increasing , due in part to the potential for parallelization when calculating the distances for a given , and in part to the algorithmic complexity in , which is super-linear as described in the previous section. In the numerical experiments of Section 4, we found that and within a single iteration of MCEM yielded accurate estimators. That is, we draw for once and for all, and optimize over . We illustrate the effect of choosing different and in Section 4.3.

Several alternatives to the MCEM approach exist. An approach to computing the MEWE was proposed in Genevay et al., (2018) based on the Sinkhorn divergence approximation to the Wasserstein distance. They derive gradients of with respect to while is fixed, allowing for the application of stochastic gradient descent. In practice, the gradients can be computed with auto-differentiation. A method for computing the MWE was proposed by Chen and Li, (2018), in which they pull back the -Wasserstein metric tensor in to , under which becomes a Riemannian manifold. In turn, this structure allows them to derive a novel gradient descent algorithm. Alternatively, in the spirit of Monte Carlo optimization, one can modify the sampling algorithms used for the approximate Bayesian computation (ABC) approach described by Bernton et al., (2019) to approximate the MEWE. This has the benefit of not requiring the synthetic data to be generated via a deterministic function with fixed-dimensional arguments. Related discussions can be found in Wood, (2010); Rubio et al., (2013).

4 Illustrations

In Sections 4.1 and 4.2, we compute the MEWE in two well-specified models with intractable likelihoods that produce i.i.d. data, taken from the ABC literature. We empirically estimate the coverage of bootstrap confidence intervals for the data-generating parameter. In Section 4.1, we also compute the MEWE in a setting where the data-generating process produces a time series. In Section 4.3, we compare the distribution of the MEWE with that of the maximum likelihood estimator (MLE) in a simple misspecified setting. We also investigate the effect of and on the distribution of the approximate MEWE. In Section 4.4, we highlight the robustness of this choice by considering a heavy-tailed data-generating process for which the MLE is not consistent. Throughout the numerical experiments, we have chosen , as this imposes minimal assumptions on the existence of moments of both the data-generating process and the model.

4.1 Quantile “g-and-” distribution

4.1.1 Independent data

The g-and- distribution (Tukey,, 1977; Jorge and Boris,, 1984) is defined in terms of its quantile function:

| (7) |

where refers to the -th quantile of the standard Normal distribution. The model is indexed by the parameter , and we take with . The probability density function, and therefore the likelihood of the model, is analytically intractable; thus the model has become a standard benchmark for ABC methods (Sisson et al.,, 2018). Though, the likelihood can be estimated by numerically inverting and then differentiating the quantile function, as described in Rayner and MacGillivray, (2002); Bernton et al., (2019).

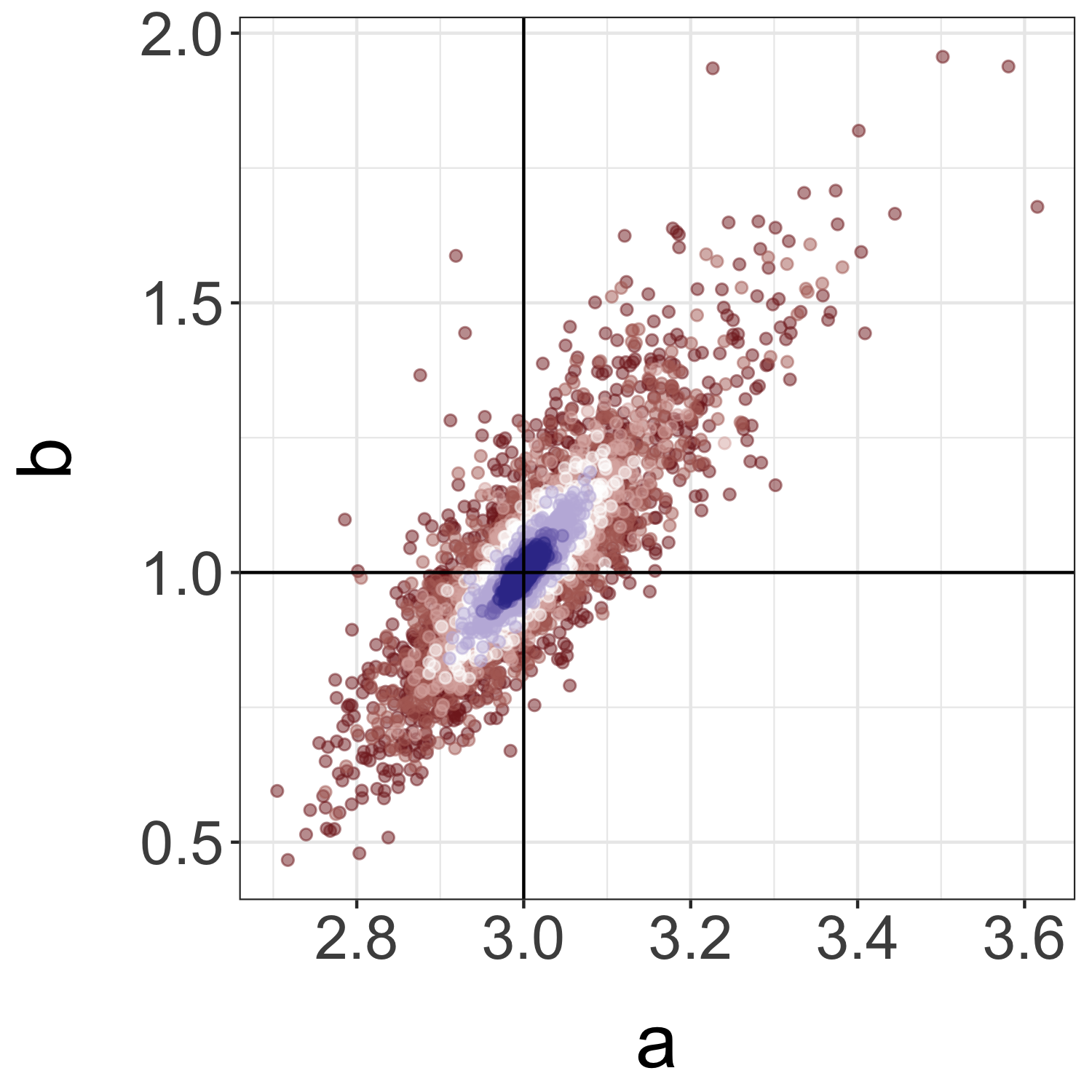

Sampling i.i.d. variables from the g-and- distribution can be achieved straightforwardly by plugging independent standard Normals into (7) in place of . Therefore, the MEWE with large can be computed to high precision. In Figure 1, we show the behavior of the MEWE with and for different numbers of observed data, and illustrate its concentration around the data-generating parameter . In computing the MEWE, we used and only one iteration of MCEM. That is, we approximate the MEWE by sampling independent random variables and minimize to form the estimator, using the optim function in R (R Core Team,, 2015).

We check the coverage of bootstrap confidence intervals calculated for . We use the percentile bootstrap (Efron and Tibshirani,, 1994) for data sets of size and synthetic data sets of size , and calculate the MEWE with . We draw data sets from the data-generating process, and bootstrap data sets for each of these. The observed coverage rates of the resulting confidence intervals were for , for , for , and for . The coverage rates should approach as , , and within the MCEM algorithm. After a Bonferroni correction, the observed coverage of the confidence sets for was .

As mentioned in Section 3.1.1, since the g-and- distribution has an explicit quantile function (insofar as the Normal quantile function can be considered explicit), one could instead directly estimate the Wasserstein distance between the g-and-k distribution and some empirical distribution using a representation of the distance in terms of an integral of the difference of quantile functions, combined with a numerical integrator.

4.1.2 Dependent data

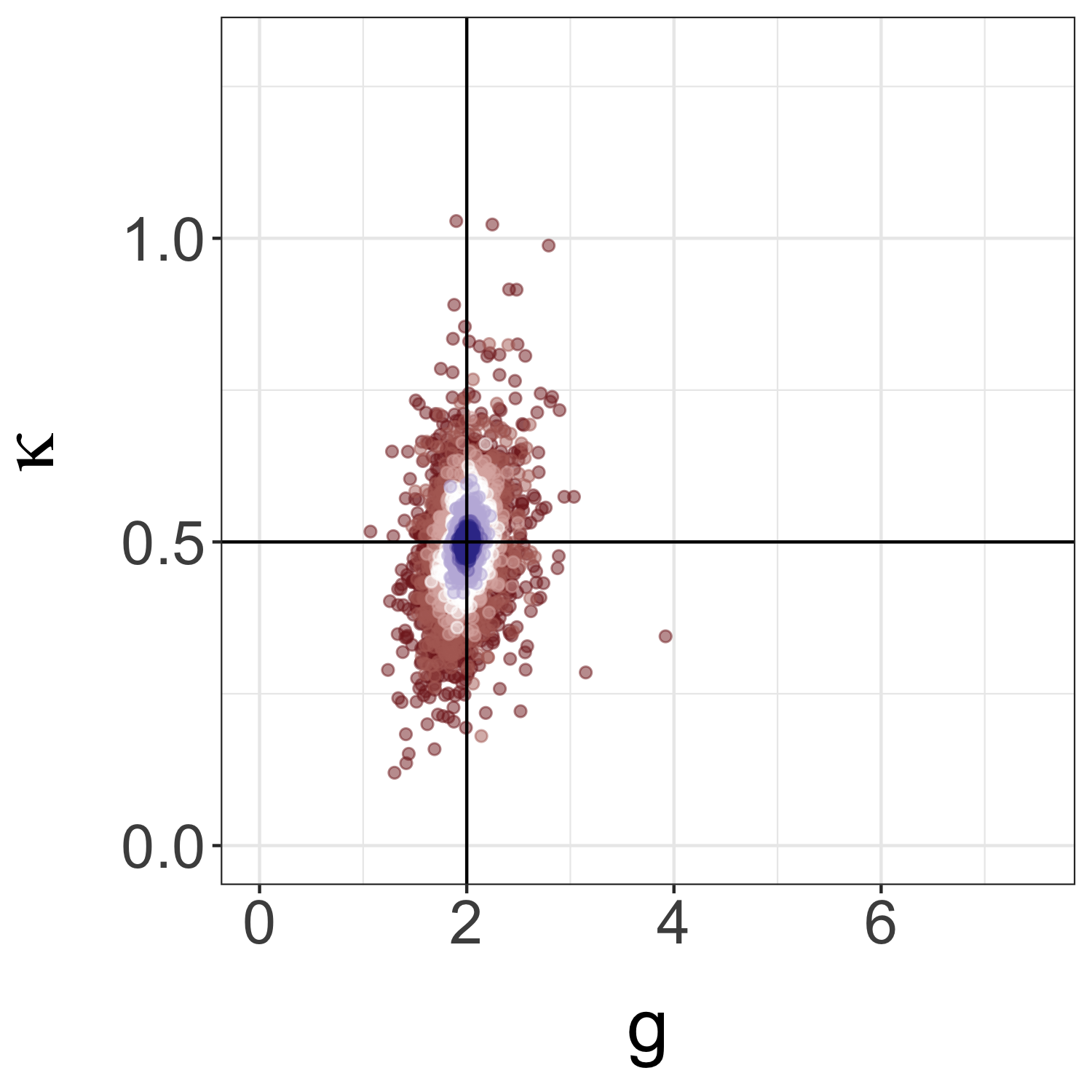

To illustrate the behavior of the estimator when the data-generating process produces dependent data, we also generated g-and- variables using Normals from an AR(1) process. Specifically, we let and for , where independently, and . Hence, these variables are marginally distributed as , but are positively correlated. To produce the observation for each , we plugged into (7) in place of , using the same as in the independent setting. The marginal distribution of the data are therefore the same as before, but the sequence of observations now forms a stationary and ergodic time series. This setting is covered by the theoretical results of Section 2; Assumption 2.1 holds with . The model, as before, is taken to generate i.i.d. data.

To approximate the MEWE, we used the same computational approach as in the i.i.d. setting, with , , and . In Figure 2, we show that the MEWE appears to concentrate around at the same rate as in the i.i.d. setting, but that its asymptotic distribution has higher variance. Note that in Figure 2, the data sizes are times larger than in the plots for the i.i.d. setting (Figure 1), as the correlation between the samples effectively reduces the sample size and makes the estimators poorly behaved when is small.

4.2 Sum of log-Normal random variables

The distribution of the sum of log-Normal random variables appears in various settings (Fenton,, 1960; Rodrigues et al.,, 2018), but no analytical formula is available for its probability density function, and thus the associated likelihood function is intractable. For a given positive integer , and , the model generates an observation by sampling independently, and defining . Thus, sampling synthetic observations from the model is simple. We consider the task of estimating from data, fixing to , and using the MEWE. We generate observations independently using .

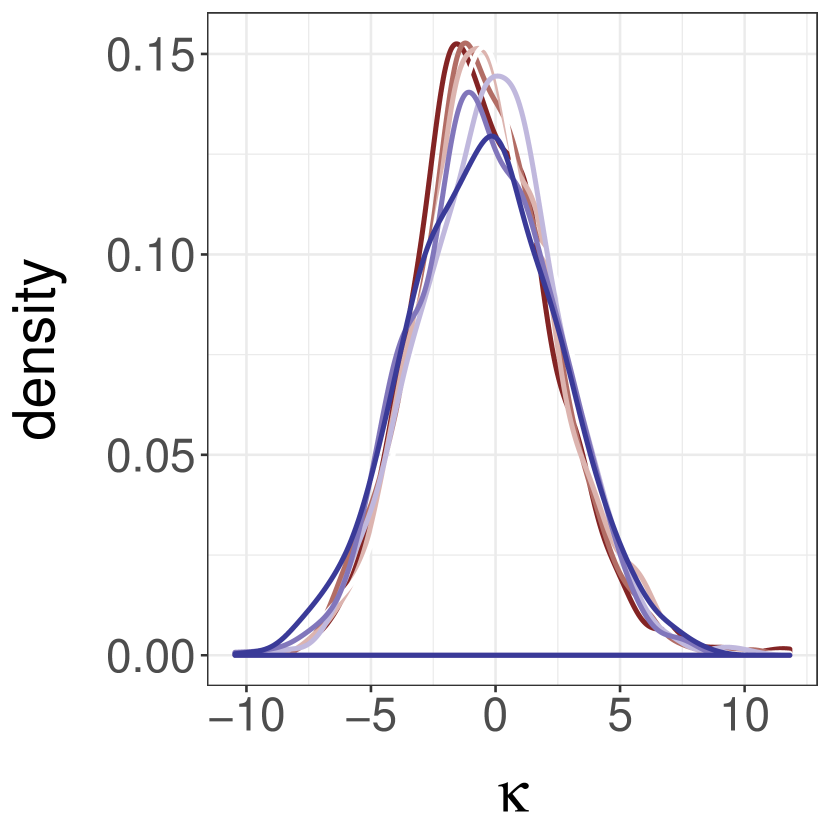

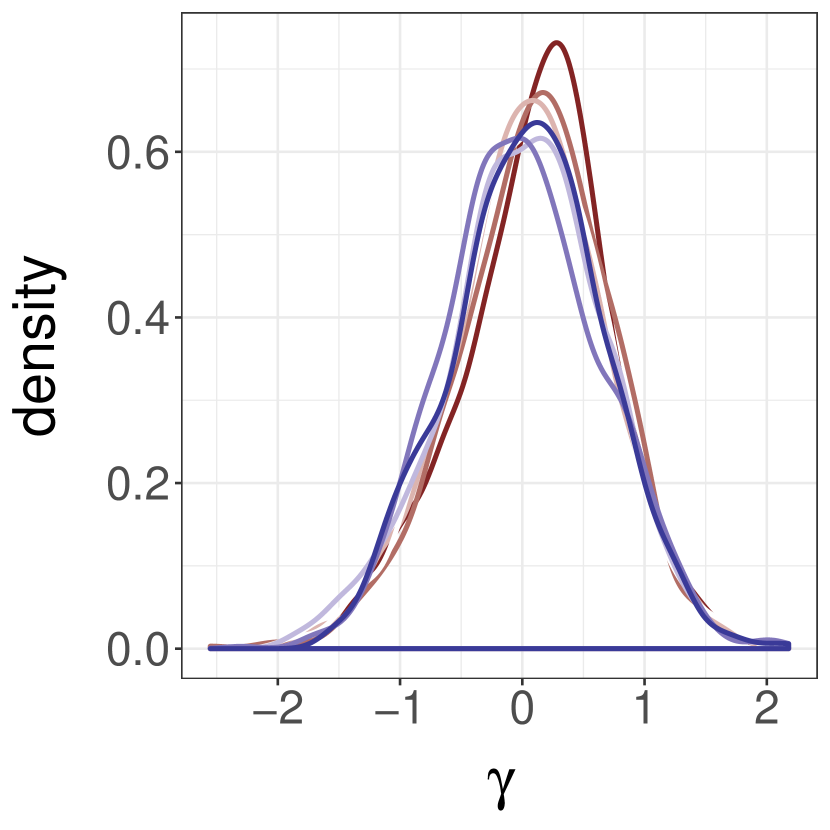

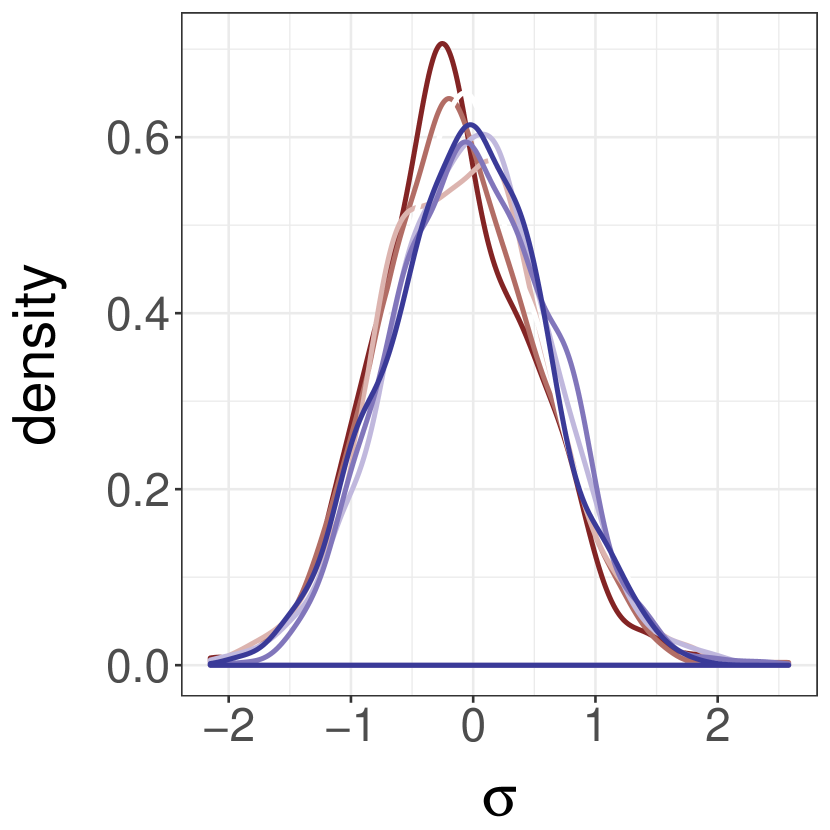

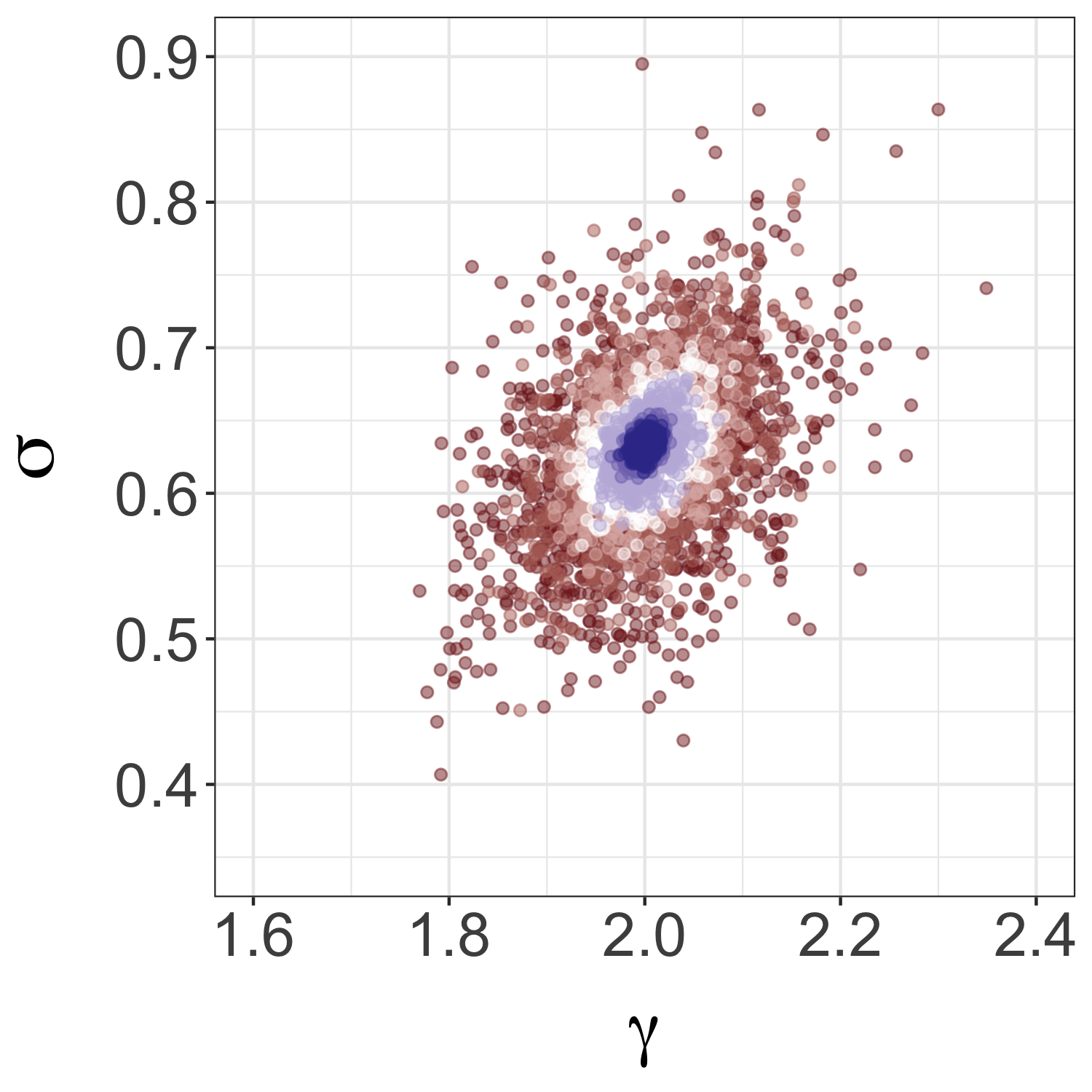

In Figure 3, we illustrate the behavior of the MEWE with and for different sizes of observed data . The sampling distribution of the MEWE appears to concentrate around the data-generating parameter at the rate as increases. In computing the MEWE, we used and one iteration of MCEM as in the previous section.

We estimate the coverage of bootstrap confidence intervals calculated for . As before, we use the percentile bootstrap (Efron and Tibshirani,, 1994) for data sets of size and synthetic data sets of size , and calculate the MEWE with . We draw data sets from the data-generating process, and bootstrap data sets for each. The observed coverage rates were and for and respectively, which are close to the limiting coverage rates. After a Bonferroni correction, the observed coverage of the confidence sets for was .

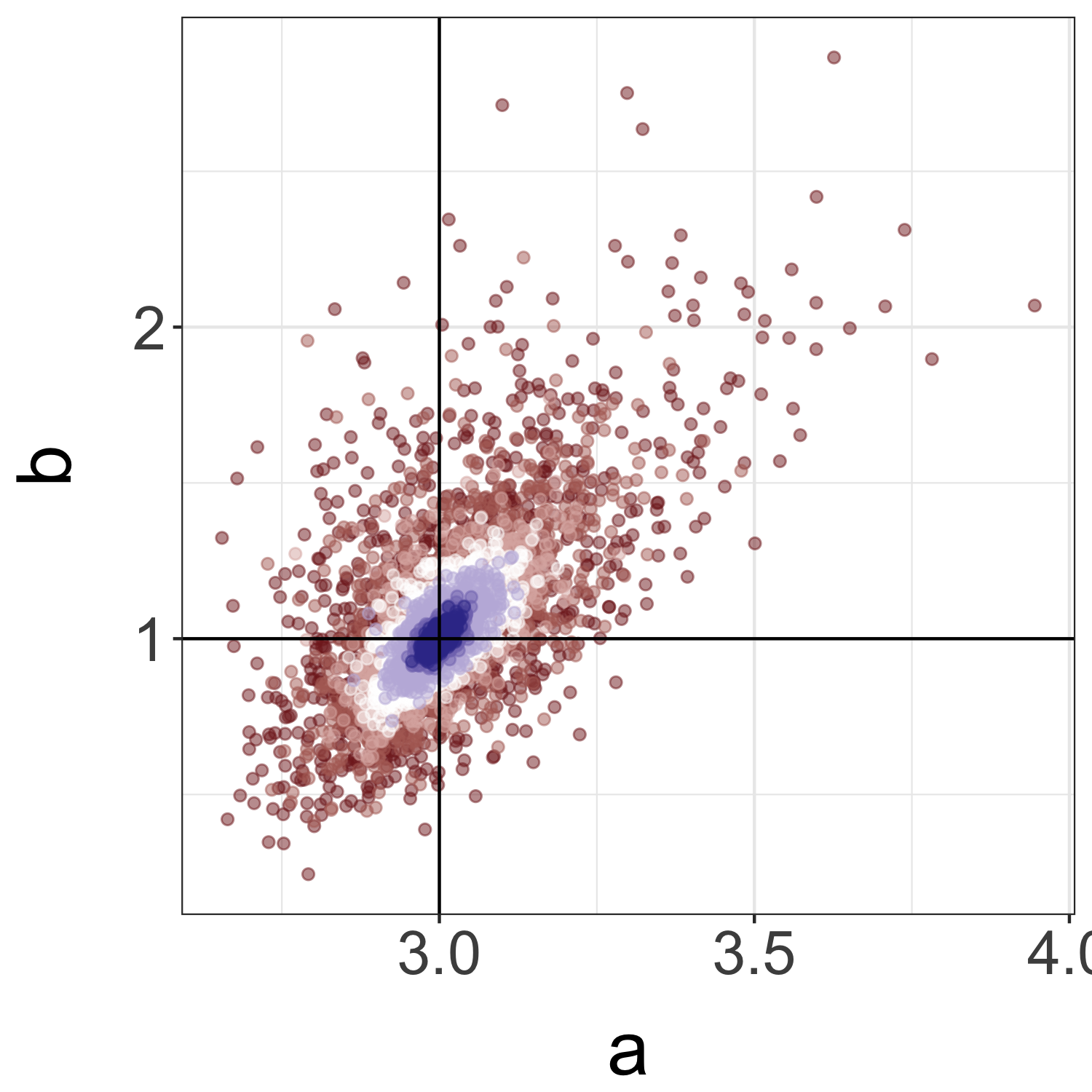

4.3 Gamma data fitted with a Normal model

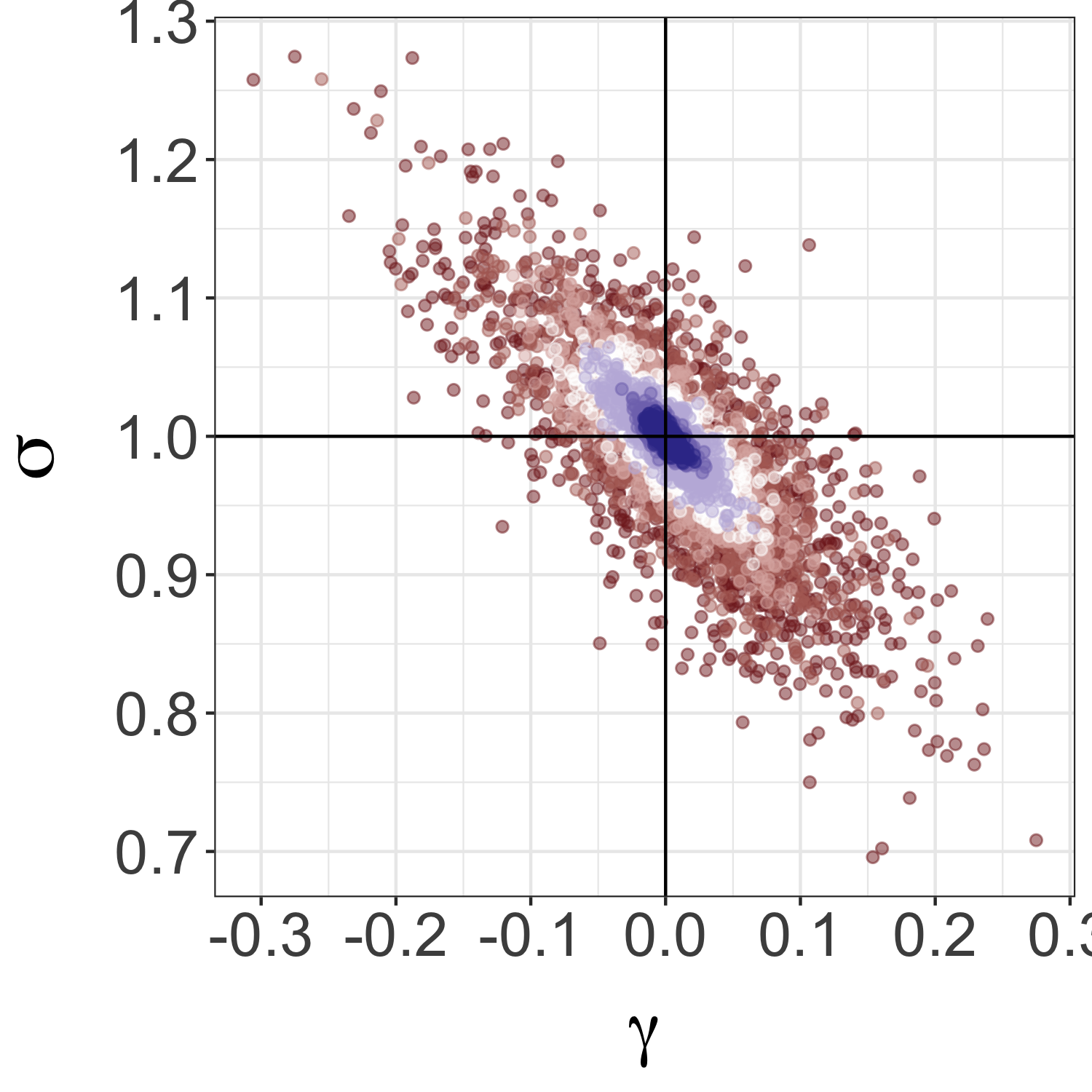

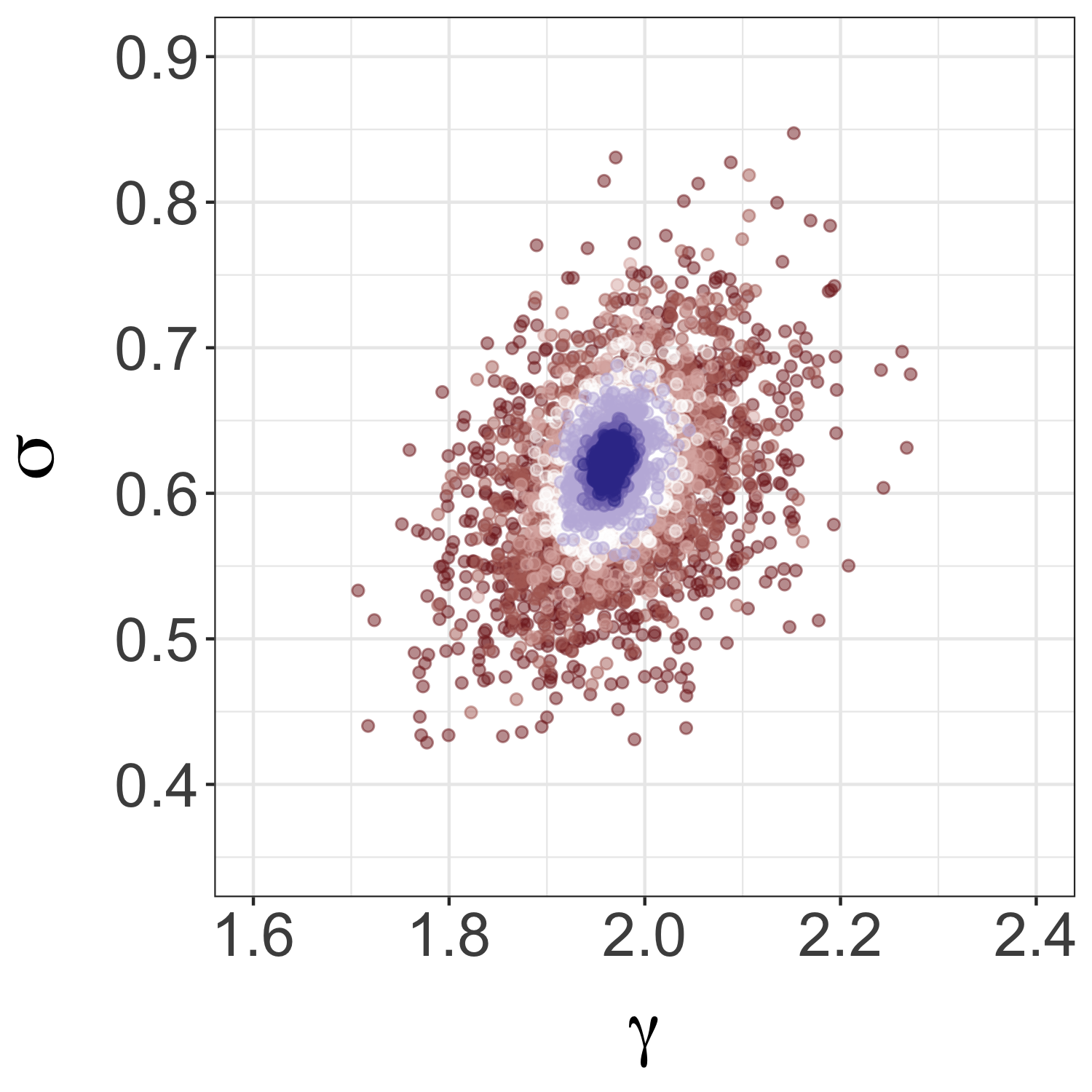

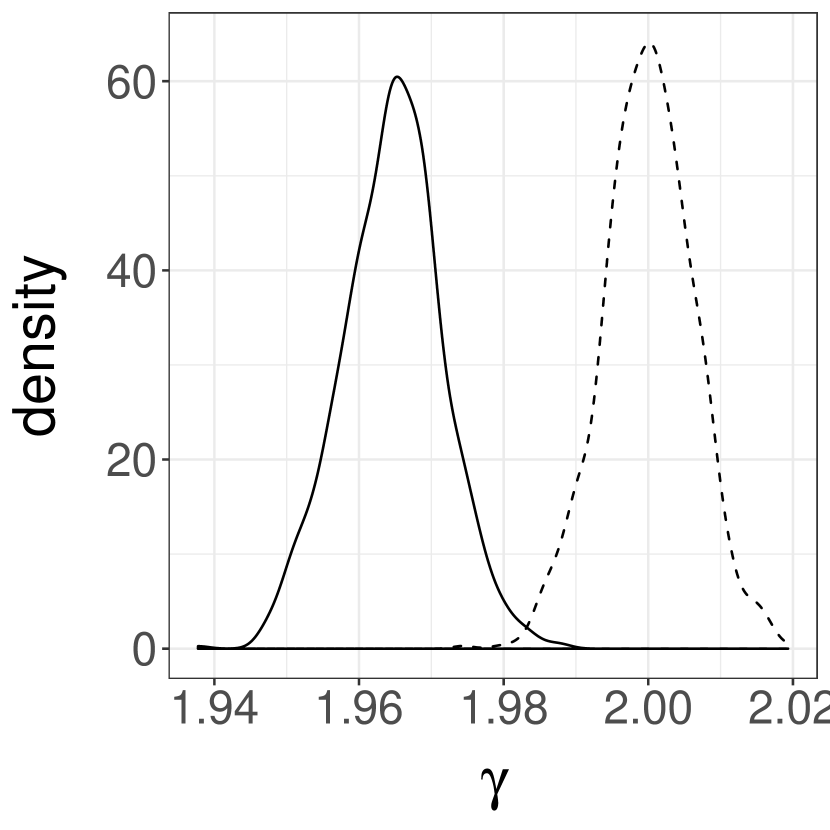

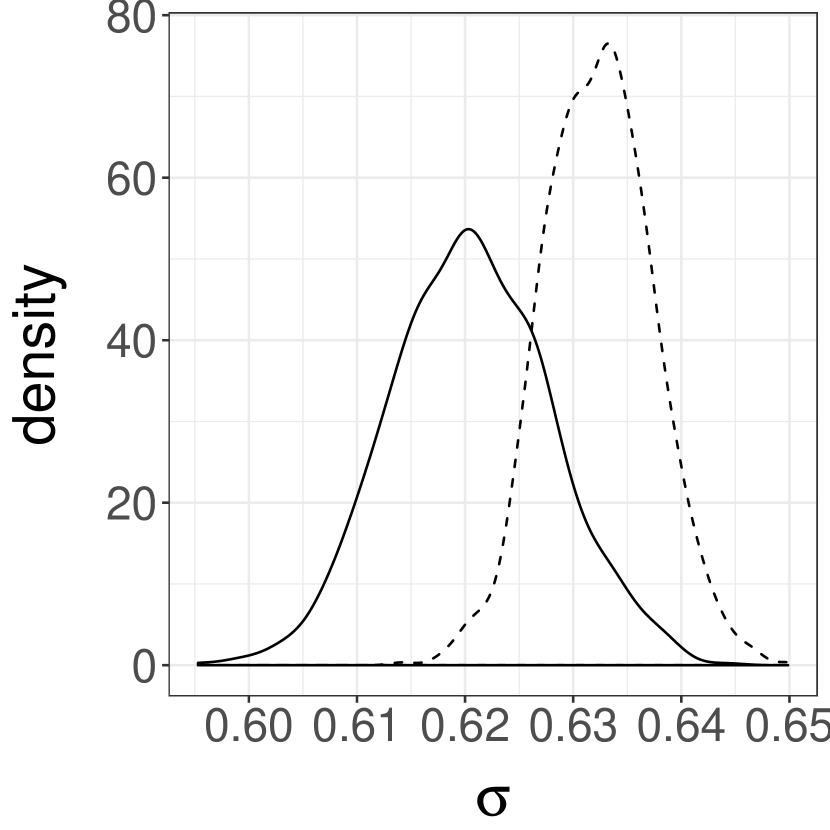

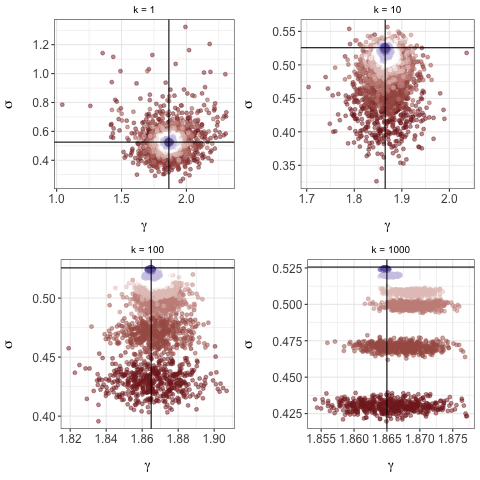

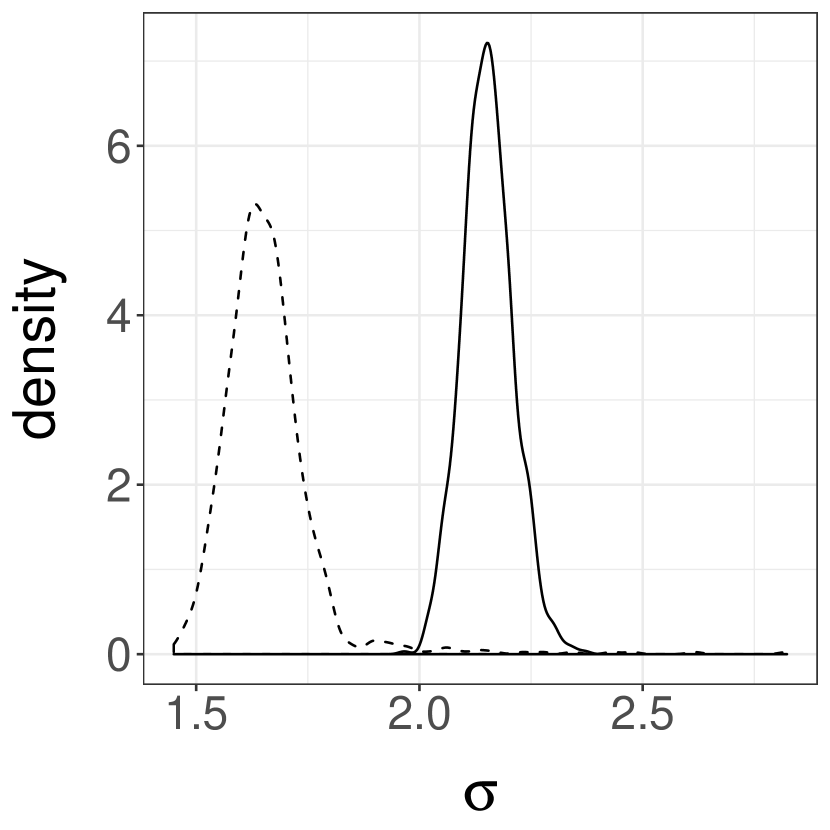

We now consider a misspecified setting. Let be a distribution (parametrized by shape and rate) and . The Normal location-scale model is very simple, yet it is widely used in practice in the form of regression models. Figure 4 compares the sampling distributions of the maximum likelihood estimator and approximations of the MEWE of order 1, over experiments, for different values of . The MEWE converges at the same rate as the MLE, albeit to a distribution that is centered at a different location. Therefore, despite both estimation techniques leading to similar values for and , the distributions of the estimators have very little overlap for large , as observed in Figures 4(c) and 4(d). For the MEWE, we have again used , , and one iteration of MCEM.

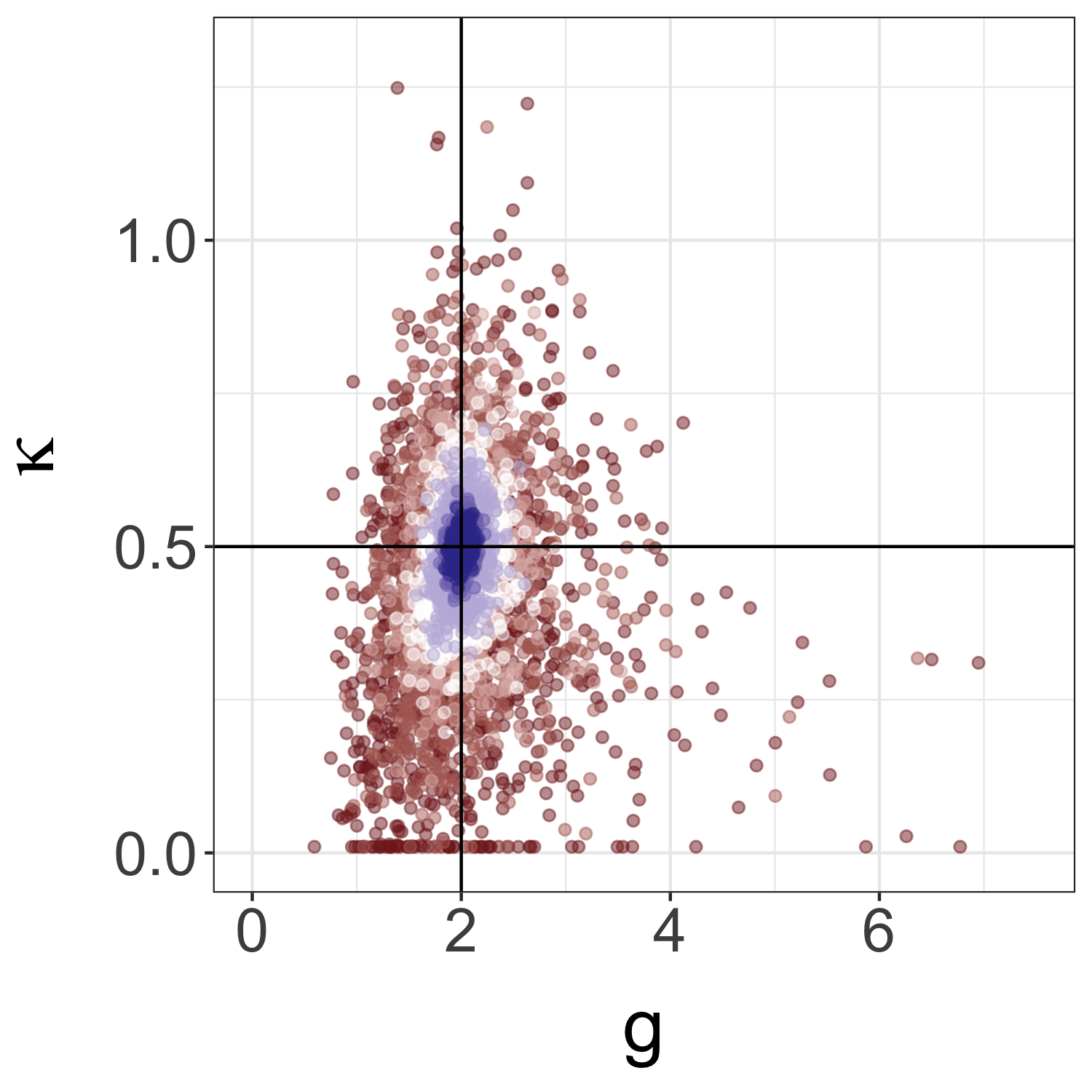

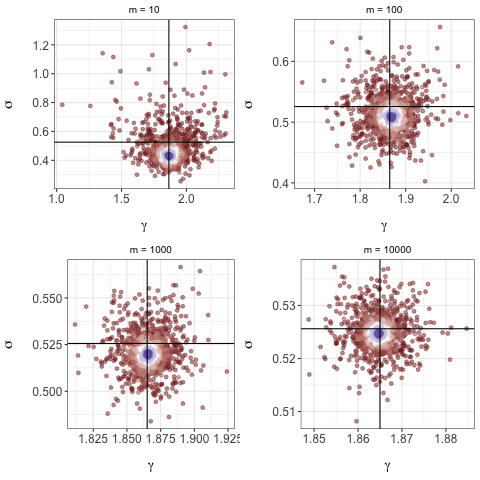

In Figure 5, we fix an observed data set of size , and compute instances of the approximate MEWE for 8 different values of and , ranging from to and to respectively. In Figure 5(a), we plot the estimators obtained for all the levels of , given 4 different values of . In Figure 5(b), we plot the estimators obtained for all the levels of , given 4 different values of . The axis scales are different for each subplot. In both figures, black points correspond to the “true” MWE, calculated using a very large value of (). For low values of , the estimators might be significantly different from the MWE, as can be seen from the lower-right sub-plots of Figure 5(b). When increases, the estimators converge to the MWE. Increasing reduces variation in the estimator. The changes in and had no significant impact on the number of evaluations of the objective required to locate the maximum using the optim function in R (R Core Team,, 2015), which uses the Nelder–Mead simplex method (Nelder and Mead,, 1965).

We check the coverage of bootstrap confidence intervals calculated for (itself calculated using and ). As before, we use the percentile bootstrap (Efron and Tibshirani,, 1994) for data sets of size and synthetic data sets of size , and calculate the MEWE with . We draw data sets from the data-generating process, and bootstrap data sets for each of these. The observed coverage rates of the resulting confidence intervals were and for and respectively. After a Bonferroni correction, the observed coverage rate of the confidence sets for was .

4.4 Cauchy data fitted with a Normal model

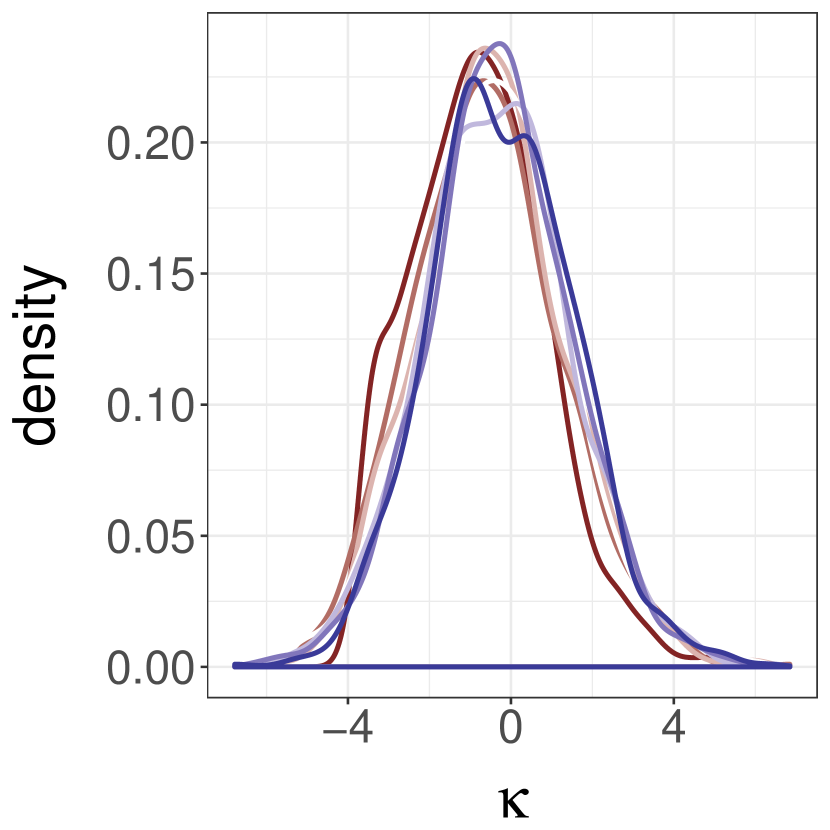

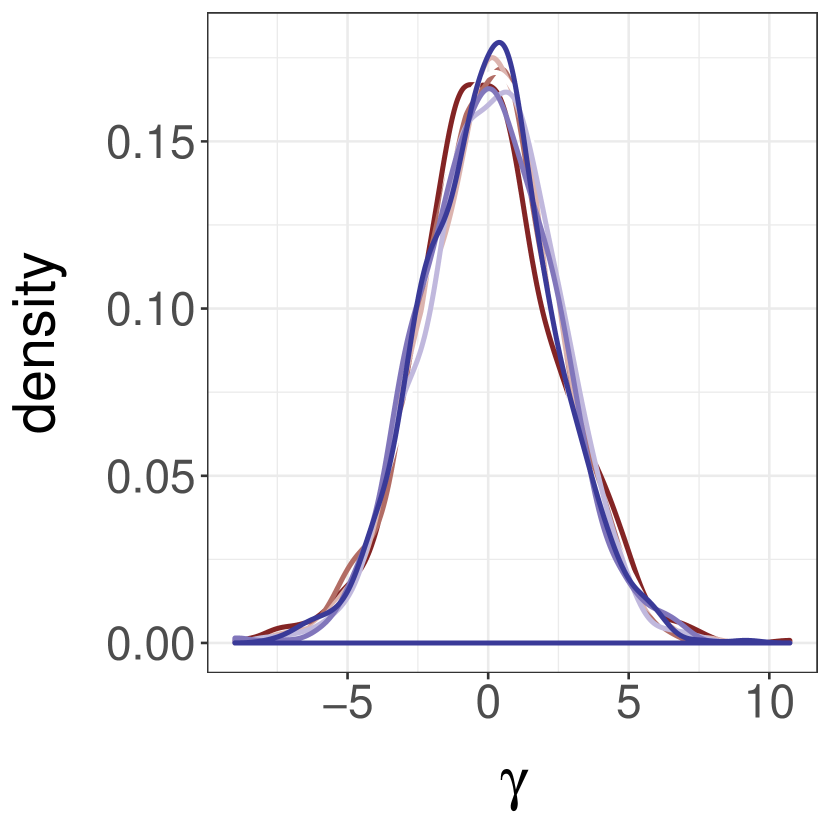

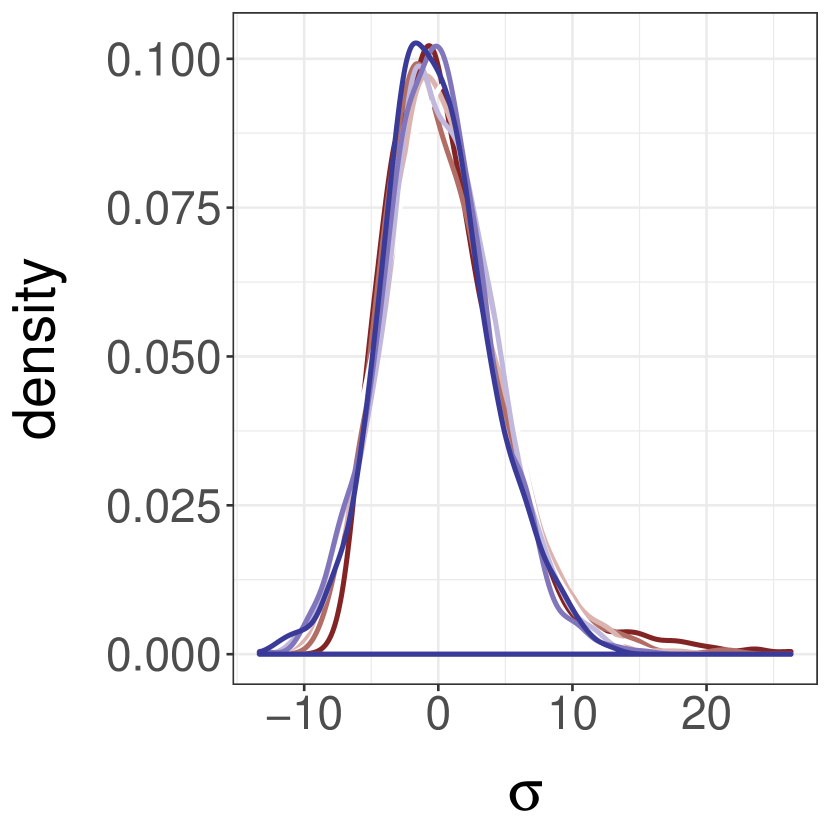

Let be Cauchy with median zero and scale one, and consider the model . We explore the behavior of the MEWE of order 1, over repeated experiments. Figure 6 shows its sampling distributions, for ranging from to . The marginal distribution of the estimator of concentrates around , the median of . The marginal distribution of the estimator of also concentrates to a value close to . The concentration appears to occur at rate , as shown by the marginal densities of the rescaled estimators of and in Figures 6(a) and 6(b).

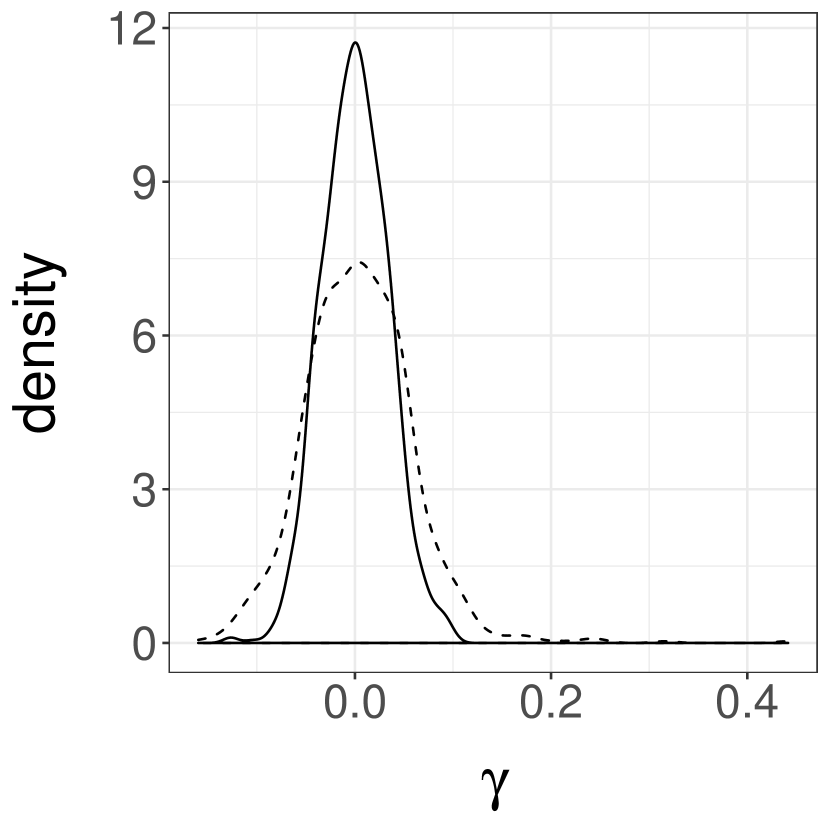

In this setting the maximum likelihood estimator would not converge as , as the maximum likelihood estimator for is the sample average, and the sample average of independent Cauchy variables is also Cauchy, with the same location and scale. As an alternative, we consider an estimator defined by minimizing a sample based estimator of the Kullback-Leibler divergence between and . For the KL approximation we use the function KL.divergence in the FNN package (Beygelzimer et al.,, 2013), which approximates the KL divergence using -nearest neighbor estimates described in Boltz et al., (2009) (and using the default parameter ). The resulting estimator is termed the minimum KL estimator (MKLE), and is a variation of the MDEs discussed by Basu et al., (2011). We compute it using the same approach as for the MEWE, using , , and one iteration of MCEM. For the distributions of MEWEs and MKLEs are plotted in Figures 6(c) and 6(d). Both estimators appear to be robust in the sense that they converge to well-defined limits, unlike the MLE approach. The estimators of are concentrated around , but the estimators of are concentrated around two different values: the MEWEs seem to concentrate around and the MKLEs around . The marginal distributions of the MEWE appear to have slightly smaller variance than those of the MKLE.

Note that this example is not covered by the theoretical results of Section 2 since the Cauchy distribution does not have a finite first moment. Robustness properties of general minimum distance estimators are discussed in Parr and Schucany, (1980), and of the MWE in location models in Bassetti and Regazzini, (2006). In the location-scale model considered here, if the approximation of the MEWE is computed with and for some , it can be written

As such, the approximate MEWE can be seen as the coefficients in a median regression (Koenker and Hallock,, 2001) of a vector on a vector , where for each , and contains the order statistics of an -sample of random variables. Quantile regression is often presented as a robust alternative to linear regression in the presence of outliers, and further connections might explain the observed robustness of the MEWE with in this example.

5 Discussion

The minimum Wasserstein (or Kantorovich) estimation approach (Bassetti et al.,, 2006) has received a renewed attention, due to recent advances in the field of computational optimal transport (Peyré et al.,, 2019), along with various applications in machine learning. In the broad context of generative models, these estimators present various appeals compared to maximum likelihood estimators. For instance, in Sections 4.1 and 4.2, we have observed the satisfactory behavior of minimum expected Wasserstein estimators in models where the likelihood function is not analytically available. In Sections 4.3 and 4.4 we have observed similarities and differences between MEWE and MLE in misspecified settings, illustrating some robustness properties of minimum Wasserstein estimation.

Minimum distance estimators were originally developed for obtaining almost surely convergent estimators (Wolfowitz,, 1957), and we have showed that both the MWE and MEWE have this strong consistency property under mild conditions. We have also proved that the MWE converges to at the optimal convergence rate when the observations are univariate, and have derived its asymptotic distribution. The generalization of this result to multivariate data is left for future research. Interestingly, given the known convergence properties of the Wasserstein distance, it seems reasonable to conjecture that the rate of the MWE depends (negatively) on the dimension of the observation space rather than that of the parameter space. Other topics for future research include a more general derivation of the limiting distributions of the estimators, whose existence is needed to justify the asymptotic coverage of subsampling confidence intervals, as well as the development of a better understanding of their robustness properties.

Acknowledgements

The bootstrap experiments were in part performed on the Odyssey cluster supported by the FAS Division of Science, Research Computing Group at Harvard University. Pierre E. Jacob acknowledges support from the National Science Foundation through grant DMS-1712872.

References

- Altschuler et al., (2018) Altschuler, J., Bach, F., Rudi, A., and Weed, J. (2018). Massively scalable Sinkhorn distances via the Nyström method. Preprint arXiv:1812.05189, Massachusetts Institute of Technology.

- Altschuler et al., (2017) Altschuler, J., Weed, J., and Rigollet, P. (2017). Near-linear time approximation algorithms for optimal transport via Sinkhorn iteration. In Guyon, I., Luxburg, U. V., Bengio, S., Wallach, H., Fergus, R., Vishwanathan, S., and Garnett, R., editors, Advances in Neural Information Processing Systems 30, pages 1964–1974. Curran Associates, Inc.

- Ambrosio et al., (2005) Ambrosio, L., Gigli, N., and Savaré, G. (2005). Gradient Flows in Metric Spaces and in the Space of Probability Measures. Birkhäuser Verlag AG, Basel, second edition.

- Arjovsky et al., (2017) Arjovsky, M., Chintala, S., and Bottou, L. (2017). Wasserstein generative adversarial networks. In Precup, D. and Teh, Y. W., editors, Proceedings of the 34th International Conference on Machine Learning, volume 70 of Proceedings of Machine Learning Research, pages 214–223, International Convention Centre, Sydney, Australia. PMLR.

- Bassetti et al., (2006) Bassetti, F., Bodini, A., and Regazzini, E. (2006). On minimum Kantorovich distance estimators. Statistics & probability letters, 76(12):1298–1302.

- Bassetti and Regazzini, (2006) Bassetti, F. and Regazzini, E. (2006). Asymptotic properties and robustness of minimum dissimilarity estimators of location-scale parameters. Theory of Probability and its Applications, 50(2):171–186.

- Basu et al., (2011) Basu, A., Shioya, H., and Park, C. (2011). Statistical Inference: the Minimum Distance Approach. CRC Press, Boca Raton, Florida.

- Belili et al., (1999) Belili, N., Bensaï, A., and Heinich, H. (1999). Estimation based on the Kantorovich functional and the Lévy distance. Comptes Rendus de l’Academie des Sciences Series I Mathematics, 5(328):423–426.

- Benamou et al., (2015) Benamou, J.-D., Carlier, G., Cuturi, M., Nenna, L., and Peyré, G. (2015). Iterative Bregman projections for regularized transportation problems. SIAM Journal on Scientific Computing, 37(2):A1111–A1138.

- Bernton et al., (2019) Bernton, E., Jacob, P. E., Gerber, M., and Robert, C. P. (2019). Approximate Bayesian computation with the Wasserstein distance. Journal of the Royal Statistical Society: Series B, 81(2):235–269.

- Bertsimas and Tsitsiklis, (1997) Bertsimas, D. and Tsitsiklis, J. N. (1997). Introduction to Linear Optimization. Athena Scientific, Belmont, Massachusetts.

- Beygelzimer et al., (2013) Beygelzimer, A., Kakadet, S., Langford, J., Arya, S., Mount, D., and Li, S. (2013). FNN: fast nearest neighbor search algorithms and applications. R package version, 1.

- Bickel and Sakov, (2008) Bickel, P. J. and Sakov, A. (2008). On the choice of m in the m out of n bootstrap and confidence bounds for extrema. Statistica Sinica, 18(3):967–985.

- Boltz et al., (2009) Boltz, S., Debreuve, E., and Barlaud, M. (2009). High-dimensional statistical measure for region-of-interest tracking. IEEE Transactions on Image Processing, 18(6):1266–1283.

- Bonneel et al., (2015) Bonneel, N., Rabin, J., Peyré, G., and Pfister, H. (2015). Sliced and radon Wasserstein barycenters of measures. Journal of Mathematical Imaging and Vision, 51(1):22–45.

- Brown and Purves, (1973) Brown, L. D. and Purves, R. (1973). Measurable selections of extrema. Annals of Statistics, 1(5):902–912.

- Burkard et al., (2009) Burkard, R., Dell’Amico, M., and Martello, S. (2009). Assignment Problems. Society for Industrial and Applied Mathematics (SIAM), Philadelphia, Pennsylvania.

- Chen and Li, (2018) Chen, Y. and Li, W. (2018). Natural gradient in Wasserstein statistical manifold. Preprint arXiv:1805.08380, California Institute of Technology.

- Cheney and Wulbert, (1969) Cheney, E. W. and Wulbert, D. E. (1969). The existence and unicity of best approximations. Mathematica Scandinavica, 24:113–140.

- Cuturi, (2013) Cuturi, M. (2013). Sinkhorn distances: Lightspeed computation of optimal transport. In Burges, C. J. C., Bottou, L., Welling, M., Ghahramani, Z., and Weinberger, K. Q., editors, Advances in Neural Information Processing Systems 26, pages 2292–2300. Curran Associates, Inc.

- Dede, (2009) Dede, S. (2009). An empirical central limit theorem in for stationary sequences. Stochastic Processes and their Applications, 119:3494 – 3515.

- del Barrio et al., (1999) del Barrio, E., Giné, E., and Matrán, C. (1999). Central limit theorems for the Wasserstein distance between the empirical and the true distributions. Annals of Probability, 27(2):1009–1071.

- del Barrio et al., (2005) del Barrio, E., Giné, E., and Utzet, F. (2005). Asymptotics for functionals of the empirical quantile process, with applications to tests of fit based on weighted Wasserstein distances. Bernoulli, 11(1):131–189.

- Del Barrio et al., (2019) Del Barrio, E., Loubes, J.-M., et al. (2019). Central limit theorems for empirical transportation cost in general dimension. The Annals of Probability, 47(2):926–951.

- Devroye, (1985) Devroye, L. (1985). Non-uniform random variate generation. Springer-Verlag, New York.

- Efron and Tibshirani, (1994) Efron, B. and Tibshirani, R. J. (1994). An Introduction to the Bootstrap. CRC press, Boca Raton, Florida.

- Fenton, (1960) Fenton, L. (1960). The sum of log-Normal probability distributions in scatter transmission systems. IRE Transactions on Communications Systems, 8(1):57–67.

- Fournier and Guillin, (2015) Fournier, N. and Guillin, A. (2015). On the rate of convergence in Wasserstein distance of the empirical measure. Probability Theory and Related Fields, 162:707–738.

- Genevay et al., (2016) Genevay, A., Cuturi, M., Peyré, G., and Bach, F. (2016). Stochastic optimization for large-scale optimal transport. In Lee, D. D., Sugiyama, M., Luxburg, U. V., Guyon, I., and Garnett, R., editors, Advances in Neural Information Processing Systems 29, pages 3440–3448. Curran Associates, Inc.

- Genevay et al., (2017) Genevay, A., Peyré, G., and Cuturi, M. (2017). GAN and VAE from an optimal transport point of view. Preprint arXiv:1706.01807, Université Paris Dauphine.

- Genevay et al., (2018) Genevay, A., Peyre, G., and Cuturi, M. (2018). Learning generative models with Sinkhorn divergences. In Storkey, A. and Perez-Cruz, F., editors, Proceedings of the Twenty-First International Conference on Artificial Intelligence and Statistics, volume 84 of Proceedings of Machine Learning Research, pages 1608–1617.

- Gottschlich and Schuhmacher, (2014) Gottschlich, C. and Schuhmacher, D. (2014). The shortlist method for fast computation of the earth mover’s distance and finding optimal solutions to transportation problems. PloS one, 9(10):e110214.

- Gouriéroux et al., (1993) Gouriéroux, C., Monfort, A., and Renault, E. (1993). Indirect inference. Journal of Applied Econometrics, 8:85–118.

- Hansen, (1991) Hansen, B. E. (1991). Strong laws for dependent heterogeneous processes. Econometric Theory, 7(2):213 – 221.

- Hansen, (1982) Hansen, L. P. (1982). Large sample properties of generalized method of moments estimators. Econometrica: Journal of the Econometric Society, 50(4):1029–1054.

- Jorge and Boris, (1984) Jorge, M. and Boris, I. (1984). Some properties of the Tukey g and h family of distributions. Communications in Statistics-Theory and Methods, 13(3):353–369.

- Koenker and Hallock, (2001) Koenker, R. and Hallock, K. F. (2001). Quantile regression. Journal of Economic Perspectives, 15(4):143–156.

- Le Cam, (1970) Le Cam, L. (1970). On the assumptions used to prove asymptotic normality of maximum likelihood estimators. Annals of Mathematical Statistics, 41:802–828.

- Lehmann and Romano, (2005) Lehmann, E. L. and Romano, J. P. (2005). Testing Statistical Hypotheses. Springer, third edition.

- Li et al., (2018) Li, W., Ryu, E. K., Osher, S., Yin, W., and Gangbo, W. (2018). A parallel method for Earth Mover s distance. Journal of Scientific Computing, 75(1):182–197.

- Marin et al., (2012) Marin, J.-M., Pudlo, P., Robert, C. P., and Ryder, R. J. (2012). Approximate Bayesian computational methods. Statistics and Computing, 22(6):1167–1180.

- McFadden, (1989) McFadden, D. (1989). A method of simulated moments for estimation of discrete response models without numerical integration. Econometrica, 57(5):995–1026.

- Neath et al., (2013) Neath, R. C. et al. (2013). On convergence properties of the Monte Carlo EM algorithm. In Advances in Modern Statistical Theory and Applications: A Festschrift in Honor of Morris L. Eaton, pages 43–62. Institute of Mathematical Statistics, Bethesda, Maryland.

- Nelder and Mead, (1965) Nelder, J. A. and Mead, R. (1965). A simplex method for function minimization. The Computer Journal, 7(4):308–313.

- Owen, (2001) Owen, A. B. (2001). Empirical likelihood. CRC press, Boca Raton, Florida.

- Parr and Schucany, (1980) Parr, W. C. and Schucany, W. R. (1980). Minimum distance and robust estimation. Journal of the American Statistical Association, 75(371):616–624.

- Peyré et al., (2019) Peyré, G., Cuturi, M., et al. (2019). Computational optimal transport. Foundations and Trends® in Machine Learning, 11(5-6):355–607.

- Politis et al., (1999) Politis, D. N., Romano, J. P., and Wolf, M. (1999). Subsampling. Springer-Verlag New York.

- Pollard, (1980) Pollard, D. (1980). The minimum distance method of testing. Metrika, 27:43–70.

- Puccetti, (2017) Puccetti, G. (2017). An algorithm to approximate the optimal expected inner product of two vectors with given marginals. Journal of Mathematical Analysis and Applications, 451(1):132–145.

- R Core Team, (2015) R Core Team (2015). R: A Language and Environment for Statistical Computing. R Foundation for Statistical Computing, Vienna, Austria.

- Rabin et al., (2011) Rabin, J., Peyré, G., Delon, J., and Bernot, M. (2011). Wasserstein barycenter and its application to texture mixing. In International Conference on Scale Space and Variational Methods in Computer Vision, pages 435–446, Ein-Gedi, Israel. Springer.

- Ramdas et al., (2017) Ramdas, A., Trillos, N. G., and Cuturi, M. (2017). On Wasserstein two-sample testing and related families of nonparametric tests. Entropy, 19(2):47.

- Rayner and MacGillivray, (2002) Rayner, G. D. and MacGillivray, H. L. (2002). Numerical maximum likelihood estimation for the g-and-k and generalized g-and-h distributions. Statistics and Computing, 12(1):57–75.

- Rockafellar and Wets, (2009) Rockafellar, R. T. and Wets, R. J.-B. (2009). Variational Analysis, volume 317. Springer Science & Business Media, New York, New York.

- Rodrigues et al., (2018) Rodrigues, G., Prangle, D., and Sisson, S. (2018). Recalibration: A post-processing method for approximate Bayesian computation. Computational Statistics & Data Analysis, 126:53–66.

- Rubio et al., (2013) Rubio, F. J., Johansen, A. M., et al. (2013). A simple approach to maximum intractable likelihood estimation. Electronic Journal of Statistics, 7:1632–1654.

- Schuhmacher et al., (2017) Schuhmacher, D., Bähre, B., Gottschlich, C., and Heinemann, F. (2017). transport: Optimal Transport in Various Forms. R package version 0.8-2.

- Sisson et al., (2018) Sisson, S. A., Fan, Y., and Beaumont, M. (2018). Handbook of Approximate Bayesian Computation. CRC Press, Boca Raton, Florida.

- Tukey, (1977) Tukey, J. W. (1977). Modern techniques in data analysis. In Proceedings of the NSF-Sponsored Regional Research Conference, volume 7, Dartmouth, Massachusetts. Southern Massachusetts University.

- Van der Vaart, (2000) Van der Vaart, A. W. (2000). Asymptotic Statistics. Cambridge University Press, Cambridge, UK.

- (62) Varadarajan, V. S. (1958a). On the convergence of sample probability distributions. Sankhyā: The Indian Journal of Statistics, 19(1):23–26.

- (63) Varadarajan, V. S. (1958b). Weak convergence of measures in separable metric spaces. Sankhyā: The Indian Journal of Statistics, 19(1):15–22.

- Villani, (2008) Villani, C. (2008). Optimal Transport, Old and New. Springer-Verlag New York.

- Weed and Bach, (2019) Weed, J. and Bach, F. (2019). Sharp asymptotic and finite-sample rates of convergence of empirical measures in Wasserstein distance. To appear, Bernoulli.

- Wei and Tanner, (1990) Wei, G. C. and Tanner, M. A. (1990). A Monte Carlo implementation of the EM algorithm and the poor man’s data augmentation algorithms. Journal of the American Statistical Association, 85(411):699–704.

- Wellner and van der Vaart, (1996) Wellner, J. A. and van der Vaart, A. W. (1996). Weak Convergence and Empirical Processes. Springer-Verlag New York.

- Wolfowitz, (1957) Wolfowitz, J. (1957). The minimum distance method. The Annals of Mathematical Statistics, 28(1):75–88.

- Wood, (2010) Wood, S. N. (2010). Statistical inference for noisy nonlinear ecological dynamic systems. Nature, 466(7310):1102–1104.

- Ye et al., (2017) Ye, J., Wang, J. Z., and Li, J. (2017). A simulated annealing based inexact oracle for Wasserstein loss minimization. In Proceedings of the 34th International Conference on Machine Learning, volume 70 of Proceedings of Machine Learning Research, pages 3940–3948, International Convention Centre, Sydney, Australia. PMLR.

Appendix A Preliminary results

Before proving the results stated in the main text, we first provide some preliminary results.

A sequence of probability measures is said to converge weakly in to as if , i.e. converges weakly in the usual sense, and such that . Recall that is a subset of for .

Theorem A.1.

The -Wasserstein distance metrizes weak convergence in : a sequence converges weakly to in if and only if .

For a proof, see Villani, (2008, Theorem 6.9). From this result one can deduce the continuity of the -Wasserstein distance. If and converge weakly in to and , then . On the other hand, if and converge weakly in the usual sense, the Wasserstein distance is only lower semicontinuous:

The following lemma is extended from Bassetti et al., (2006). Its second condition corresponds to Assumption B.2, and is implied by the first condition. All limits in the lemma are understood to be as .

Lemma A.1.

Let be a sequence in and . Suppose that either of the following conditions holds.

-

1.

implies that .

-

2.

implies that .

Then, respectively,

-

1.

is continuous.

-

2.

is lower semicontinuous.

Proof.

This follows directly from the two assumptions and the continuity/lower semicontinuity derived from Theorem A.1. ∎

Lemma A.2.

The function is lower semicontinuous with respect to weak convergence. Furthermore, if implies that , then the map is lower semicontinuous.

Proof.

Let and . Then there exist versions of the corresponding empirical measures such that almost surely.

Indeed, by Skorokhod’s representation theorem, there exists a probability space and random variables and such that -almost surely. Let and be the empirical distributions of these samples. By Varadarajan, 1958b and since is separable, there exists a fixed countable subset of continuous and bounded functions on , such that for any sequence of measures , converges weakly to if and only if for all . Fix one such . Then,

on a set of -probability one, by the continuous mapping theorem. Taking the countable intersection of these sets over , we get that -almost surely.

By the lower semicontinuity of the -Wasserstein distance and Fatou’s lemma,

The lower semicontinuity of is proved analogously to Lemma A.1. ∎

Appendix B Proofs: MWE

B.1 Existence, measurability, and consistency

For ease of presentation, we recall the assumptions made in the main text.

Assumption B.1.

The data-generating process is such that , -almost surely as .

Assumption B.2.

The map is continuous in the sense that implies as .

For the next assumption, define ; we will use this definition throughout.

Assumption B.3.

For some , the set is bounded.

Theorem B.1 (Existence and consistency of the MWE).

Before giving the proof, we recall a definition and a proposition.

Definition B.1.

A sequence of functions is said to epi-converge to if for all ,

A useful equivalent formulation of epi-convergence can be found in Proposition 7.29 of Rockafellar and Wets, (2009), paraphrased here.

Proposition B.1 (Proposition 7.29 of Rockafellar and Wets, (2009)).

The sequence epi-converges to if and only if

In an colloquial sense, epi-convergence is a weak notion of convergence for which the minimizer of converges to the minimizer of . Showing that the function epi-converges to almost surely is the key step in the proof of Theorem B.1.

Proof of Theorem B.1.

First note that, for any , the lower semicontinuity of the map follows from Lemma A.1, via Assumption B.2. Next, since , the set with the of Assumption B.3 is non-empty, by definition of the infimum. Moreover, since is lower semicontinuous, the set is closed. By Assumption B.3, is therefore compact. In other words, again by lower semicontinuity, the set is non-empty.

We now show that epi-converges to -almost surely. Let denote the set of probability one from Assumption B.1 and let . Fix compact. By lower semicontinuity of , we know that

for some sequence . Hence,

Fix open. By definition of the infimum, there exists a sequence such that . Now, . Hence,

Using Proposition B.1, the sequence of functions epi-converges to .

Theorem 7.29b) of Rockafellar and Wets, (2009) implies that

So, for all , there exists , such that for , . Let . The set

is non-empty for , by definition of the infimum. Let belong to this set. Then, by the triangle inequality,

By Assumption B.1, there exists an such that for , . So, if , we have that . This means that

As a consequence, we know that for ,

By Theorem 7.31a) of Rockafellar and Wets, (2009), this implies

For and by the same reasoning as for the map , the sets are non-empty. By Theorem 7.31b) of Rockafellar and Wets, (2009), the result follows. The same argument holds for with , since eventually.

∎

Theorem B.2 (Measurability of the MWE).

Suppose that is a -compact Borel measurable subset of . Under Assumption B.2, for any and , there exists a Borel measurable function that satisfies

Before the proof, we first recall a useful result from Brown and Purves, (1973), also used in Bassetti et al., (2006).

Theorem B.3 (Corollary 1 in Brown and Purves, (1973)).

Let be Polish, be Borel, and be Borel measurable. Suppose that for all , the section is -compact and that is lower semicontinuous with respect to the relative topology on . Then

-

1.

The sets and are Borel.

-

2.

For each , there exists a Borel measurable function such that for ,

Proof of Theorem B.2.

First note that endowed with the product topology is Polish since is Polish. Also, depends on only through , where . We can therefore write , where , and consider the empirical measure a function on . The map is measurable with respect to the Borel -algebra on with respect to weak convergence. Recall also that is Polish since is Polish by Theorem 6.18 of Villani, (2008).

Let . By Lemma A.1 and Assumption B.2, the map is lower semicontinuous (and therefore measurable). Hence the map is also lower semicontinuous on for any . Being the composition of measurable functions, is measurable on . In light of this, the result follows by a direct application of Theorem B.3.

∎

B.2 Asymptotic distribution

Let , , and . In this case we have

where and denote the cumulative distribution functions (CDFs) of and respectively (see e.g. Ambrosio et al.,, 2005, Theorem 6.0.2). For this reason, we will occasionally use the notation . Assume also that is endowed with a norm: . We recall results from del Barrio et al., (1999) and Dede, (2009), after a few definitions.

Definition B.2.

Suppose that the sequence for all , and , are stochastic processes with almost all their sample paths in . Then is said to converge weakly to in if as for all bounded continuous functions .

Definition B.3.

The stochastic process is a -Brownian bridge if it is a zero mean Gaussian process with covariance function

Theorem B.4 (Theorem 2.1a in del Barrio et al., (1999)).

Suppose that , and define and . The stochastic process converges weakly in to a -Brownian bridge , if and only if the condition is satisfied.

For a stationary sequence, let . Note that for stationary sequences, -mixing is weaker than -mixing, as defined later in Section D.

Theorem B.5 (Proposition 3.5 in Dede, (2009)).

Suppose that is ergodic and stationary, and that

Then converges weakly in to a zero mean Gaussian process with sample paths in and covariance satisfying: for every ,

where

Dede, (2009) also provides other conditions, e.g. on -mixing coefficients, for which the convergence above holds. We first consider the well-specified setting, in which our results follow directly from Pollard, (1980).

B.2.1 Well-specified setting

Suppose that for some in the interior of , and consider the following assumptions:

Assumption B.4.

For all , there exists such that

Assumption B.5.

There exists a non-singular such that

as

The following results contain Theorem 2.3 of the main text as a special case.

Theorem B.6.

Theorem B.7.

Proof.

The proofs of these two results follow the steps outlined in Pollard, (1980)’s Theorems 4.2 and 7.2 respectively, which also generalize to the setting where the map does not necessarily have a unique minimum (see also Section B.2.2 below). The delta methods employed therein hold for the 1-Wasserstein distance due to the representation . Moreover, the well-separation of provided by Assumption B.4, the consistency and measurability of the MWE proved earlier, and Theorems B.4 and B.5 proved in del Barrio et al., (1999) and Dede, (2009) respectively, guarantee that Pollard’s conditions are satisfied. Note that the measurability concerns outlined in his Section 3 do not apply to here, as is separable.

∎

B.2.2 Misspecified setting

To study the asymptotic distribution of the MWE in the misspecified setting, we adapt the arguments outlined in Section 7 of Pollard, (1980). Define and . Let be the class of all compact, convex, non-empty subsets of a set equipped with its canonical distance. The corresponding Hausdorff metric on is defined by , where . Let . The function maps into and, by Pollard, (1980, Lemma 7.1), is measurable. Let also

and . Let

where is any sequence such that and is non-empty. That is, is a set of approximate MWEs.

Consider the following assumption:

Assumption B.6.

There exists a neighborhood of and a constant such that for any ,

In the well-specified setting, this condition follows from Assumption B.5. The next result concerns the distribution of the set as becomes large.

Theorem B.8.

Suppose Assumptions B.1-B.6 hold for some in the interior of , and that the conditions of either Theorem B.4 or Theorem B.5 are satisfied. Then, there exist positive real numbers such that

-

1.

as , where denotes inner probability, and

-

2.

if and are versions of the processes such that in almost surely, then

Since one can interpret this result as saying that the limit of the set of approximate MWEs behaves distributionally like the limit of the sets in the Hausdorff metric sense. Note that the latter sequence does not depend on the data. Since the assumptions guarantee that weakly in , there exist versions of these variables that converge almost surely. For simplicity, we assume without loss of generality that these are the variable we work with. As noted by Pollard, (1980), establishing the measurability of the sets is hard, which is why the result is stated in terms of inner probability. See also Pollard, (1980, pp. 67) for further comments on the sequence .

Proof of Theorem B.8.

Let , where is the set from Assumption B.6. By Assumption B.4 and Pollard, (1980, Lemma 4.1) or the proof of Theorem B.1, we know that the minimizers of will be attained in with probability going to one. For , we have that

Let and . Then, by the assumptions on and , we know that . If , then by the inequality derived above, . Thus, with inner probability going to one, it has to be that .

Next, we approximate with the convex map over the set . First, note that Assumption B.5 implies that the remainder satisfies

where is an increasing function such that as . Define

We then have that

Hence, we have uniform control over the difference between and its convex approximation over . Moreover, the map also attains its minimum on with probability going to one, since for such that ,

Hence, if and , then

In other words, with probability going to one, where we have used the reparameterization , or equivalently .

Now, since , we can find a sequence of positive real numbers such that . Similarly, we can find and such that and . Define . Let be such that and , and suppose that and . By combining the approximations developed above, we have that

Since , we have that . This proves the first part of the theorem, as the events considered above all hold with (inner) probability going to one.

By the triangle inequality, implies that . Hence, with probability going to one, . Similarly, implies that . Recall that almost surely. Let denote the set on which this occurs. Then, for every every , there exists such that for , . By the definition of the Hausdorff metric, these set inclusions imply that

∎

B.2.3 Differentiability condition

The condition in Assumption B.5 can sometimes be established from more familiar concepts of differentiability, such as differentiability in quadratic mean (Le Cam,, 1970). The following proposition gives such a result. Suppose that the model family is absolutely continuous with respect to the Lebesgue measure on , and denote the density of by . Let for all . Le Cam, (1970) introduced the concept of differentiability in quadratic mean, which we define below.

Definition B.4.

The model is differentiable in quadratic mean at if there exists and such that where as .

Differentiability in quadratic mean holds for many classical models, such as exponential families and many location-scale families (see e.g. Section 12.2 in Lehmann and Romano,, 2005).

Proposition B.2.

Suppose that the model family is supported on a set of bounded Lebesgue measure, and that it is differentiable in quadratic mean at . Let

for and zero elsewhere. Then, as ,

Proof.

Consider

where is some constant and the last equality follows by applying the Cauchy-Schwarz inequality to the two last terms of the integrand. ∎

Appendix C Proofs: MEWE

C.1 Existence, measurability, and consistency

In order to show similar results for the MEWE, we introduce the following assumptions.

Assumption C.1.

For any , if , then as .

Assumption C.2.

If , then as .

Assumption C.1 is a slightly stronger version of Assumption B.2, stating that we not only need weak convergence of the “model” distributions , but also of the sample distributions for any . Assumption C.2 is implied by , which in turn might hold when is compact and the inequalities in Fournier and Guillin, (2015) hold. In the next result, we prove an analogous version of Theorem B.1 for the MEWE as . For simplicity, we write as a function of and require that as .

Theorem C.1.

Proof of Theorem C.1.

For any , lower semicontinuity of the map follows from Lemma A.1, via Assumption B.2. Since , with the of Assumption B.3 is non-empty, by definition of the infimum. Moreover, since is lower semicontinuous, the set is closed. By Assumption B.3, is therefore compact. In other words, again by lower semicontinuity, the set is non-empty.

We show that epi-converges to -almost surely. Let denote the set of probability one from Assumption B.1 and let . Fix compact. By lower semicontinuity of , ensured by Lemma A.2 and Assumption C.1, we know that

for some sequence . Hence,

Fix open. By definition of the infimum, there exists a sequence such that . Now,

Hence,

Theorem 7.29b) of Rockafellar and Wets, (2009) implies that

Hence, for all , there exists , such that implies that

Let . The set is non-empty for , by definition of the infimum. Let belong to this set. Then, by the triangle inequality,

By Assumption B.1, there exists an such that for , . By Assumption C.2, there exists an such that for any , we have . So, if , we have . This means that

As a consequence, for ,

By Theorem 7.31a) of Rockafellar and Wets, (2009), we have

Also, for and by the same reasoning as for the map , the sets are non-empty. By Theorem 7.31b) of Rockafellar and Wets, (2009), the result follows. The same argument holds for the sets

with , since eventually.

∎

C.2 Convergence to the MWE

The next result considers the case where the data and is fixed, while . It shows that the MEWE converges to the MWE, assuming the latter exists. We summarize this condition in the following assumption, in which the observed empirical distribution is kept fixed and .

Assumption C.3.

For some , the set is bounded.

Theorem C.2.

Proof of Theorem C.2.

Lower semicontinuity of the map follows from Lemma A.1, via Assumption B.2. Since , with the of Assumption B.3 is non-empty, by definition of the infimum. Moreover, since is lower semicontinuous, the set is closed. By Assumption C.3, is therefore compact. In other words, by lower semicontinuity, the set is non-empty.

We show that epi-converges to as . Fix compact. By lower semicontinuity of , ensured by Lemma A.2 and Assumption C.1, we know that

for some sequence . Hence,

Fix open. By definition of the inf, there exists a sequence such that . Now, . Hence,

Theorem 7.29b) of Rockafellar and Wets, (2009) implies that

Hence, for all , there exists , such that for , . Let . The set

is non-empty for , by definition of the infimum. Let belong to this set. Then, by the triangle inequality,

By Assumption C.2, there exists an such that for , . So, if , we have that . This means that

Hence, for , .

Theorem C.3 (Measurability of the MEWE).

Suppose that is a -compact Borel measurable subset of . Under Assumption C.1, for any and and , there exists a Borel measurable function that satisfies

Appendix D Checking the assumptions

The following proposition gives three data-generating mechanisms for which -almost surely, which is Assumption B.1. The three conditions below are mainly chosen for illustrative purposes, and are by no means exhaustive. We first give definitions that are used in the conditions. We denote by the measurable sets of .

Definition D.1.

The stochastic process is stationary if for any and we have that and have the same distribution.

Definition D.2.

The map is -measure preserving if for all .

Definition D.3.

The map is -ergodic if it is -measure preserving, and such that for all with we have that or . The stochastic process is ergodic if it can be represented by for some ergodic and some random variable .

Definition D.4.

The stochastic process is -mixing with mixing coefficients

if as , where and .

Proposition D.1.

Suppose that is a stochastic process such that either

-

1.

, for some , i.e. the observations are i.i.d, or

-

2.

is ergodic and stationary, represented by , where and is an ergodic, measure preserving map, or

-

3.

is mixing with mixing coefficients such that , with such that converges weakly to in and satisfies for some (where it is assumed for simplicity).

Then there exists a set with such that, for all , .

Proof.

Under condition 1., Theorem 3 in Varadarajan, 1958a establishes that there exists a set with such that for all , converges weakly to . By the strong law of large numbers, there exist a set with and an such that for all . Then, in light of Theorem A.1, the claim holds on .

Consider condition 2. By Varadarajan, 1958b , there exists a fixed countable set of continuous and bounded functions on , such that for any sequence of measures on , converges weakly to if and only if for all . Fix . We know that is measurable and that since is bounded, so by Birkhoff’s ergodic theorem there exists a set such that and

for all . Moreover, since we know and that there exists a set with such that

for all . Since is countable we know that . In other words, this means that for all .

Under condition 3., we first note that since is mixing, then so is for any measurable , with mixing coefficients bounded above by since . Also, since converges weakly to in we have that for all ,

and

By Hansen, (1991) Corollary 4, we know that for all we have that the zero-mean, -mixing sequence satisfies

Similarly,

Together this gives us that

and

Then, again by the countability of , we can conclude that for all in a set defined analogously to the one for the second set of conditions. ∎

The following proposition can be used to verify Assumption B.4.

Proposition D.2.

Suppose that either of the conditions of Lemma A.1 holds. Suppose that there exists a proper, connected and compact subset with positive Lebesgue measure such that Then there exists a attaining the infimum of . If is unique, then it is well-separated.

Proof.

Since is continuous/lower semicontinuous, it attains a minimum on . This is also the global minimum by the assumption on . If is unique, it is well-separated in the sense of Assumption B.4, for all , there exists such that

Indeed, let , and consider . Either the set is contained in , and thus well-separation follows, or, is not empty. Then we show that it is compact. Since is compact, there exists such that . Therefore,

Now is compact. An intersection of compact sets is compact. Therefore, being continuous/lower semicontinuous, an infimum is attained on , and by uniqueness of , well-separation follows. ∎