Factor-Adjusted Regularized Model Selection

Abstract

This paper studies model selection consistency for high dimensional sparse regression when data exhibits both cross-sectional and serial dependency. Most commonly-used model selection methods fail to consistently recover the true model when the covariates are highly correlated. Motivated by econometric studies, we consider the case where covariate dependence can be reduced through factor model, and propose a consistent strategy named Factor-Adjusted Regularized Model Selection (FarmSelect). By separating the latent factors from idiosyncratic components, we transform the problem from model selection with highly correlated covariates to that with weakly correlated variables. Model selection consistency as well as optimal rates of convergence are obtained under mild conditions. Numerical studies demonstrate the nice finite sample performance in terms of both model selection and out-of-sample prediction. Moreover, our method is flexible in a sense that it pays no price for weakly correlated and uncorrelated cases. Our method is applicable to a wide range of high dimensional sparse regression problems. An R-package FarmSelect is also provided for implementation.

Key words: High dimension; Model selection consistency; Correlated covariates; Factor model; Regularized -estimator; Time series.

1 Introduction

Specifying an appropriate yet parsimonious model is a key topic in economics and statistics studies. Parsimonious models are preferable due to their simplicity and interpretability. In addition, removing redundent coefficients can improve the prediction accuracy. In classic econometric studies, extensive efforts have been made to identify the correct orders of time series models, see Akaike (1973), Schwarz (1978), Tsay and Tiao (1985), Choi (1992) and Tiao and Tsay (1989) among others. With the development of data collection and storage technologies, high dimensional time series characterize many contemporary research problems in economics, finance, statistics, machine learning and so on. Therefore, over the past two decades, many model selection methods have been developed. A major part of them are based on the regularized -estimation approach including the LASSO (Tibshirani, 1996), the SCAD (Fan and Li, 2001), the elastic net (Zou and Hastie, 2005), and the Dantzig selector (Candes and Tao, 2007), among others. These methods have attracted a large amount of theoretical and algorithmic studies. See Donoho and Elad (2003), Fan and Peng (2004), Efron et al. (2004), Meinshausen and Bühlmann (2006), Zhao and Yu (2006), Fan and Lv (2008), Zou and Li (2008), Bickel et al. (2009), Wainwright (2009), Zhang (2010), and references therein. However, most existing model selection schemes are not tailored for economic and finance applications as they assume covariates are cross-sectionally weakly correlated and serially independent. These conditions are easily violated in economic and financial datasets. For example, economics studies (e.g. Stock and Watson, 2002; Bai and Ng, 2002) show that there exist strong co-movements among a large pool of macroeconomic variables. A stylized feature of the stock return data is cross-sectionally correlated among the stock returns. Furthermore, even if the weakly correlated assumption holds, one may still observe strong spurious correlations in a high dimensional sample.

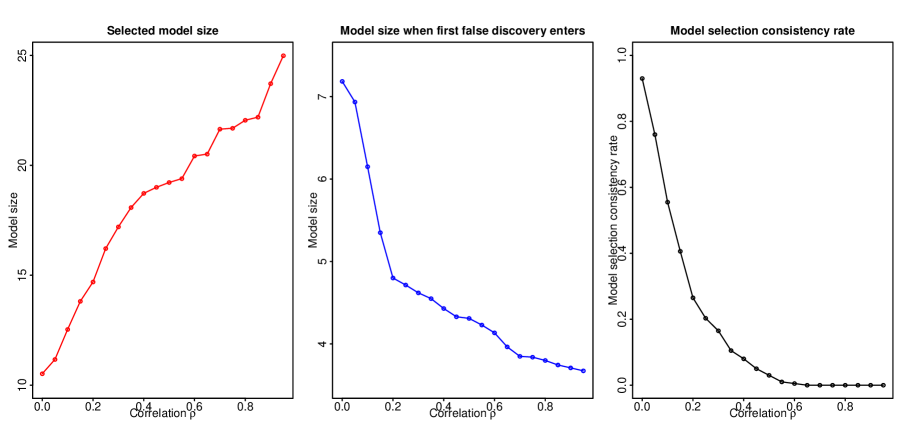

To illustrate how cross-sectional correlations influence the model selection result, we consider a toy example of LASSO with an equally correlated design. Consider a sparse linear model with no intercept. We choose sample size , dimensionality , , and . The nonzero coefficients are drawn from i.i.d. Uniform . The covariates are drawn from the normal distribution where is a correlation matrix with all off-diagonal elements for some . Let increase from 0 to by a step size . For each given , we simulate 200 replications and calculate the average model size selected by LASSO, the average model size when the first false discovery (, ) enters the solution path and the model selection consistency rate. As is shown in Figure 1, the correlation influences the model selection results in the following three aspects: (i) selected model size, (ii) early selection of false variables, (iii) model selection consistency rates. Therefore, when the covariates are highly correlated, there is little hope to exactly recover the active set from the solution path of LASSO. As to be shown later, the correlation has similar adverse impacts on other model selection methods (e.g. SCAD and elastic net).

To overcome the the aforementioned problems caused by the cross-sectional correlation, this paper proposes a consistent strategy named Factor-Adjusted Regularized Model Selection (FarmSelect) for the case where covariates can be decorrelated via a few pervasive latent factors. More precisely, let be the th () observation of the th () covariate, and assume that follows an approximate factor model

| (1.1) |

where is a vector of latent factors, is a matrix of factor loadings, and is a vector of idiosyncratic components that are uncorrelated with . The strategy of FarmSelect is to first learn the parameters in approximate factor model (1.1) for the covariates . Denote by and the obtained estimators of the factors and loadings respectively. Then by identifying the highly correlated low rank part by , we transform the problem from model selection with highly correlated covariates in to that with weakly correlated or uncorrelated idiosyncratic components and . The second step amounts to solving a regularized profile likelihood problem. We study FarmSelect in details by providing theoretical guarantees that FarmSelect can achieve model selection consistency as well as estimation consistency under mild conditions. Unlike traditional studies in model selection where the samples are assumed to be i.i.d., serial dependency is allowed and thus our theories apply to time series data. Moreover, both theoretical and numerical studies show the flexibility of FarmSelect in a sense that it pays no price for weakly correlated cases. This property makes FarmSelect very powerful when the underlying correlations between active and inactive covariates are unknown.

FarmSelect is applicable to a wide range of high dimensional sparse regression related problems that include but are not limited to linear model, generalized linear model, Gaussian graphic model, robust linear model and group LASSO. For the sparse linear regression, the proposed approach is equivalent to projecting the response variable and covariates onto the linear space orthogonal to the one spanned by the estimated factors. Existing algorithms that yield solution paths of LASSO can be directly applied in the second step. To demonstrate the finite sample performance of FarmSelect, we study two simulated and one empirical examples. The numerical results show FarmSelect can consistently select the true model even when the covariates are highly correlated while existing methods like LASSO, SCAD and elastic net fail to do so. An R-package FarmSelect ( https://cran.r-project.org/web/packages/FarmSelect ) is also provided to facilitate the implemention our method.

Various methods have been studied to estimate the approximate factor model. Principal components analysis (PCA, Stock and Watson, 2002) is among one of the most popular ones. Data-driven estimation methods of the number of factors have been studied in extensive literature, such as Bai and Ng (2002), Luo et al. (2009), Hallin and Liška (2007), Lam and Yao (2012), and Ahn and Horenstein (2013) among others. Recently, a large amount of literature contributed to the asymptotic analysis of PCA under the ultra-high dimensional regime including Johnstone and Lu (2009), Fan et al. (2013), Shen et al. (2016) and Wang and Fan (2017), among others.

The rest of the paper is organized as follows. Section 2 overviews the problem setup including regularized -estimator of sparse regression, the irrepresentable condition and approximate factor models. Section 3 introduces the model selection methodology of FarmSelect and studies the sparse generalized linear model as a showcase example. Some issues related to the estimation of approximate factor models will be discussed in Section 3 as well. Section 4 presents the general theoretical results. Section 5 provides simulation studies and Section 6 studies the forecast of U.S. bond risk premia. The appendix contains the technical proofs.

Here are some notations that will be used throughout the paper. denotes the identity matrix; refers to the zero matrix; and represent the all-zero and all-one vectors in , respectively. For a matrix , we denote its matrix entry-wise max norm as and denote by and its Frobenius and induced -norms, respectively. denotes the minimum eigenvalue of if it is symmetric. For , and , define , and . For a vector and , define to be its subvector. Let and be the gradient and Hessian operators. For and , define and . refers to the normal distribution with mean and covariance matrix .

2 Problem Setup

2.1 Regularized -estimator

Let us begin with a family of high dimensional sparse regression problems in the following settings. From now on we suppose that are -dimensional random vectors of covariates with zero mean111We use instead of to denote the number of covariates so that there are coefficients including the intercept. In addition, we center the covariates if they could have non-zero means. Whether this step is done or not will not affect the estimation of , but affect the intercept ., and are responses with each sampled from some probability distribution parametrized by . Here is a sparse vector with non-zero elements. Let and be the design matrix and response vector, respectively. Define , where the subscript refers to the all-one column added to the original design matrix .

Let be some convex and differentiable loss function assigning a cost to any parameter . Suppose that is the unique minimizer of the population risk . Under the high-dimensional regime, it is natural to estimate via a regularized -estimator as follows:

| (2.1) |

where is a norm that penalizes the use of a nonsparse vector and is a tuning parameter.

A special case of this problem is the penalized likelihood estimation of generalized linear models. Suppose the conditional density function of given covariates is a member of the exponential family, i.e.

| (2.2) |

where , and are known functions, and is an unknown coefficient vector of interest. It is commonly assumed that is strictly convex. Taking the loss function to be the negative log-likelihood function and the penality function to be the norm, the regularized -estimator of admits the form

| (2.3) |

2.2 Irrepresentable condition

We expect a good estimator of (2.1) to achieve estimation consistency as well as selection consistency. The former one requires for some norm as ; while the latter one requires as . In general, the estimation consistency does not imply the selection consistency and vice versa. To study the selection consistency, we consider a stronger condition named general sign consistency as follows.

Definition 2.1 (Sign consistency).

An estimate is sign consistent with respect to if such that .

Zhao and Yu (2006) studied the LASSO estimator and showed there exists an irrepresentable condition which is sufficient and almost necessary for both sign and estimation consistencies for sparse linear model. Without loss of generality, we assume . Denote and as the submatrices of defined by its first columns and the rest columns, respectively. Then the irrepresentable condition requires some , such that

| (2.4) |

For general regularized -estimator (2.1) to achieve both sign and estimation consistencies, Lee et al. (2015) proposed a generalized irrepresentable condition. When applied to the regularizer, it becomes

| (2.5) |

for some , where . It is easy to check (2.5) is equivalent to (2.4) under the LASSO case. The generalized irrepresentable condition will easily get violated when there exists strong correlations between active and inactive variables. Even if it holds, the key parameter can be very close to zero, making it hard to select the correct model and obtain small estimation errors simultaneously.

2.3 Approximate factor model

To go beyond the assumption on weakly correlation, a natural extension is conditional weak correlation. Suppose covariates are dependent through latent common factors. Given these common factors, the idiosyncratic components are weakly correlated. Factor model has been well studied in econometrics and statistics literature, we refer to Lawley and Maxwell (1971); Stock and Watson (2002); Bai and Ng (2002); Forni et al. (2013); Fan et al. (2013), among others.

We assume that follows the approximate factor model

| (2.6) |

where are latent factors, is a loading matrix, and are idiosyncratic components. Note that is the only observable quantity. Throughout the paper, is assumed to be independent of , which is a standard assumption in the literature of factor model Fan et al. (2013). We assume that comes from a time series . Denote and . Then (2.6) can be written in a more compact form:

| (2.7) |

We impose the following identifiability assumption (Fan et al., 2013). Here we only put the most basic assumption for factor model, and more can be found in Section 3.3 where estimation of factor model is discussed.

Assumption 2.1.

Assume that , is diagonal, and all the eigenvalues of are bounded away from 0 and as .

3 Factor-adjusted regularized model selection

3.1 Methodology

To illustrate the main idea, we temporarily assume and to be observable. Define and . By the approximate factor model (2.7), we have decompositions and

where . The regularized -estimator (2.1) can be rewritten as

Instead of using to estimate , we regard as nuisance parameters, drop the constraint , and consider a new estimator

| (3.1) |

namely are now regarded as new covariates. In other words, by lifting the covariate space from to , the highly dependent covariates are replaced by weakly dependent ones.

The theoretical for us to ignore the constraint is given by the following lemma, whose proof is given by Appendix A.

Lemma 3.1.

Consider the generalized linear model (2.2), let , and . If , then

It is worth pointing out that the assumption is very mild and natural. We just assume the residual and augmented covariates to be uncorrelated, which is almost as weak as the standard condition for the generalized linear model. For example, in the linear model where and , we just strengthen the condition from to and . In particular, the assumptions hold if is independent of and .

By construction, has now much weaker cross-sectional correlation than . Thus, the penalized profile likelihood (3.1) removes the effect of strong correlations caused by the latent factors. It can be implemented as follows:

Step 1: Initial estimation. Let be the design matrix. Fit the approximate factor model (2.7) and denote , and the obtained estimators of , and respectively by using the principal component analysis (Bai, 2003; Fan et al., 2013). More specifically, the columns of are the eigenvectors of corresponding to the top eigenvalues, . This is the same as and , where and are top eigenvalues in descending order and their associated eigenvectors of the sample covariance matrix.

Step 2: Augmented -estimation. Define and . Then is obtained from the first entries of the solution to the augmented problem

| (3.2) |

We call the above two-step method as the factor-adjust regularized model selection (FarmSelect). If is independent of and the variables in the idiosyncratic component are weakly correlated, then the columns in are weakly correlated as long as and are well estimated. Hence, we successfully transform the problem from model selection with highly correlated covariates in (2.1) to model selection with weakly correlated or uncorrelated ones by lifting the space to higher dimension. The augmented problem (3.2) is a convex optimization problem which can be minimized via many existing convex optimization algorithms, for example coordinate descent (e.g. Friedman et al., 2010) and ADMM.

3.2 Example: sparse linear model

Now we illustrate the FarmSelect procedure using sparse linear regression, where . By defining and , we have and

| (3.3) |

The augmented -estimator (3.2) for the sparse linear model is of the following form:

Solving the least-squares problem with respect to , we have the penalized profile least-squares solution

| (3.4) |

where is the projection matrix onto the column space of . As the decorrelation step does not depend on the choice of the regularizer , FarmSelect can be applied to a wide range of penalized least squares problems such as SCAD, group LASSO, elastic net, fused LASSO, folded concave penalty such as SCAD, and so on.

There is another way to understand this method. By left multiplying the projection matrix to both sides of (3.3), we have

| (3.5) |

where can be treated as the decorrelated design matrix and is the corresponding response variable. From (3.5) we see that the method in Kneip and Sarda (2011) coincides with FarmSelect in the linear case. However, the projection-based representation only makes sense in sparse linear regression. In contrast, our idea of profile likelihood directly generalizes to more general problems.

3.3 Estimating factor models

Principal component analysis (PCA) is frequently used to estimate latent factors for model (2.7). The estimated matrix of latent factors is times the eigenvectors corresponding to the largest eigenvalues of the matrix . Using the normalization yields . Now we introduce the asymptotic properties of estimated factors and idiosyncratic components. We adopt the regularity assumptions in Fan et al. (2013), which are similar to the ones in Bai (2003) and other literature on high-dimensional factor analysis.

Assumption 3.1.

-

1.

is strictly stationary and in addition, for all , and ;

-

2.

There exist constants such that , and

; -

3.

There exist and such that for any , and , and .

Assumption 3.2.

Let and denote the -algebras generated by and respectively. Assume the existence of such that and for all ,

Assumption 3.3.

There exists such that for all , we have , and .

We summarize useful properties of and in Lemma 3.2, which directly follows from Lemmas 10-12 in Fan et al. (2013).

Lemma 3.2.

A practical issue arises on how to choose the number of factors. We adapt the ratio method for the numerical studies in this paper, as it involves only one tuning parameter. Let be the th largest eigenvalue of and be a prescribed upper bound. The number of factors can be consistently estimated by (Luo et al., 2009; Lam and Yao, 2012; Ahn and Horenstein, 2013)

| (3.6) |

Other viable method includes the information criteria in Bai and Ng (2002).

3.4 Decorrelated variable screening

Screening methods (e.g. Fan and Lv, 2008; Fan and Song, 2009; Wang and Leng, 2016) are computationally attractive and thus popular for ultra-high dimensional data analysis. However, the screening methods tend to include too many variables when there exist strong correlations among covariates (Fan and Lv, 2008; Wang and Leng, 2016). As an extension of FarmSelect, we propose the following conditional variable screening method to tackle this problem.

- Step 1:

-

Initial estimation. We fit the approximate factor model (2.7) to obtain , , and .

- Step 2:

-

Augmented marginal regression. For , let be the -th column of and

(3.7) - Step 3

-

Screening. Sort the in terms of their absolute values, and take the largest ones.

For sparse linear regression, our screening method reduces to the factor-profiled screening proposed by Wang (2012).

4 Theoretical results

4.1 General results

We first present general model selection results for the FarmSelect estimator (3.2). Without loss of generality, we assume the last variables are not penalized. Let be a convex loss function, and be the sparse sub-vector of interest. Then and are estimated via

respectively. Further, denote , and .

Assumption 4.1 (Smoothness).

and there exist , such that whenever and .

Assumption 4.2 (Restricted strong convexity).

There exist such that and .

Assumption 4.3 (Irrepresentable condition).

for some .

Assumptions 4.1 – 4.3 are standard in the studies of high-dimensional regularized estimators (e.g. Negahban et al., 2012; Lee et al., 2015). Based on them, we introduce the following theorem of () error bounds and sign consistency for the FarmSelect estimator.

Theorem 4.1.

Remark 4.1.

Theorem 4.1 shows how the correlated covariates affect the sign consistency as well as error bounds. To achieve the sign consistency, the tuning parameter should scale with . Therefore, the and errors will scale with and , respectively. When the covariates are highly correlated, the irrepresentable condition will get violated or the parameter is very small. As a result, the model selection procedures will fail to achieve the sign consistency and the error bounds will be suboptimal. On the other hand, the optimal error bounds require a small , which typically leads to an overfitted model. One can see a trade-off between model selection and parameter estimation due to the existence of dependency.

Remark 4.2.

The and error bounds in Theorem 4.1 depend on , the number of active variables. They stem from the bias induced by the penalty. To reduce the bias, it is desirable to penalize as few active variables as possible. This phenomena motivates FarmSelect to adopt a penalized profile likelihood form by not imposing penalty on the nuisance parameter .

As discussed in Remark 4.1, when the covariates are highly correlated, the irrepresentable condition may not hold, or has a very small . This makes the model selection consistency either very hard to achieve or incompatible with low estimation error bounds. Therefore, the FarmSelect strategy can improve the model selection consistency and reduce the estimation error bounds if can be decomposed into such that is well-behaved. This is due to the fact that the irrepresentable condition is easier to hold with positive bounded away from zero after the decorrelation step. To this end, any effective decorrelation procedure can be incorporated into this frame work.

4.2 FarmSelect with approximate factor model

Now we study the FarmSelect estimator when the covariates admits the approximate factor model (2.7). The oracle procedure uses true augmented covariates for and solves

where . However, is not observable in practice. Hence we need to use its estimator and solve

Below the error induced by the factor estimation will be studied carefully. To deliver a clear discussion on the conditions and results, we focus on the FarmSelect estimator for the generalized linear model (2.3), and assume that the covariates are generated from the approximate factor model (2.7).

Assumption 4.4 (Smoothness).

. For some constants and , we have and , .

Assumption 4.5 (Restricted strong convexity and irrepresentable condition).

Let . Assume the existence of and such that

| (4.3) |

Assumption 4.6 (Estimation of factor model).

for some constant . In addition, there exist nonsingular matrix , and such that for , we have and .

Remark 4.3.

(i) Assumption 4.4 holds for a large family of generalized linear models. For example, linear model has , and ; logistic model has and finite , . (ii) Note that the first inequality in (4.3) involves only a small matrix and holds easily, and the second inequality there is related to the generalized irrespresentable condition. Standard concentration inequalities (e.g. the Bernstein inequality for weakly dependent variables in Merlevède et al. (2011)) yield that Assumption 4.5 holds with high probability as long as satisfies similar conditions. (iii) Under the conditions of Lemma 3.2, we have and , where , and some proper . Hence can guarantee Assumption 4.6 to hold with high probability.

Theorem 4.2.

By taking , one can achieve the sign consistency and , and . Hence is a key quantity characterizing the error rate of our FarmSelect estimator, whose size is controlled using the following lemma.

Lemma 4.1.

Let and . Assume that is strictly stationary and satisfies the following conditions

-

1.

;

-

2.

There exist constants such that for all and ;

-

3.

There existconstants such that for all ,

where and denote the -algebras generated by and respectively;

In addition, suppose that the assumptions in Lemma 3.2 hold. Then we have

Recall that the assumption has been used in Lemma 3.1 as a cornerstone of our FarmSelect methodology. The rest in the list are standard conditions similar to Assumptions 3.1-3.3. All of them are mild and interpretable.

Lemma 4.1 asserts that . The first term corresponds to the optimal rate of convergence for high-dimensional -estimator (e.g. Bickel et al., 2009). The second term is the price we pay for factor estimation, which is negligible if . In that high-dimensional regime, all the error bounds for () match the optimal ones in the literature.

5 Simulation study

5.1 Example 1: Linear regression

We study a simulated example for high dimensional sparse linear regression with correlated covariates. The correlation structure is calibrated from S&P 500 monthly excess returns between 1980 and 2012. Throughout the numerical studies of this paper, the tuning parameter is selected by the 10-fold cross validation. The model selection performance is measured by the model selection consistency rate and the sure screening rate. The former is the proportion of simulations that the selected model is identical to the true one and the latter is the proportion of simulations that the selected model contains all important variables.

Calibration and data generation process

We calculate the centered monthly excess returns for the stocks in S&P 500 index that have complete records from January 1980 to December 2012. The data, collected from CRSP222Center for Research in Security Prices Database, see http://www.crsp.com/ for more details. , contains the returns of 202 stocks with a time span of 396 months. Denote the centred monthly excess returns as , . The calibration and data generation procedure are outlined as follows.

-

(1)

Fit with a three factor model. We apply PCA on the sample covariance of and denote and , , as the top three eigenvalues and corresponding eigenvectors. We estimate loadings and .

-

(2)

Calculate as the sample covariance of the rows of , which is . Generate loading matrix whose rows are draws from i.i.d. .

-

(3)

Fit VAR(1) model . Denote the estimate of and calculate . Generate from the VAR(1) model with , where is generated from i.i.d. .

-

(4)

Calculate the residual and the sample covariance matrix of . Denote the average of the diagonal entries of . Generate covariates from a factor model where the entries in are drawn from i.i.d. .

-

(5)

Generate the response from a sparse linear model . The true coefficients are , and the nonzero coefficients are drawn from i.i.d. Uniform(2,5). We draw from an AR(1) model with .

The results of the calibrated parameters are presented in Table 1.

| 0.5237 | 0 | 0 | 0.1897 | -0.0375 | -0.0223 | 0.9621 | -0.0056 | 0.0182 | |

| 0 | 0.2884 | 0 | 0.0630 | 0.1553 | 0.0206 | -0.0056 | 0.9715 | -0.0078 | 0.0146 |

| 0 | 0 | 0.2372 | -0.0432 | 0.0102 | 0.4343 | 0.0182 | -0.0078 | 0.8094 | |

Impacts of Irrepresentable Condition

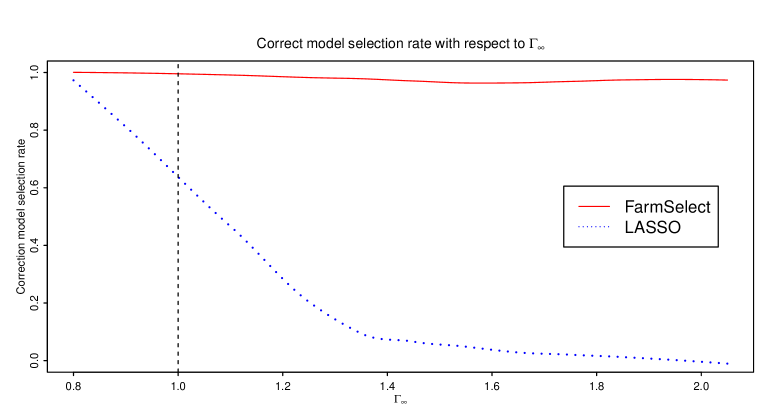

First, we show LASSO performs poorly in terms of model selection consistency rate when the irrepresentable condition is violated, while FarmSelect can consistently select the correct model. Let and . Denote by . When the irrepresentable condition holds and otherwise it is violated. We simulate 10,000 replications. For each replication, we calculate and apply both LASSO and FarmSelect for model selection. Then we calculate the model selection consistency rate within each small interval around (a nonparametric smoothing). The results are presented in Figure 2. According to Figure 2, both FarmSelect and LASSO have high model selection consistency rate when . This shows FarmSelect does not pay any price under the weak correlation scenario. As grows beyond 1, the correct model selection rate of LASSO drops quickly. When the irrepresentable condition is strongly violated (e.g. ), the correct model selection rate of LASSO is close to zero. On the contrary, FarmSelect has high selection consistency rates regardless of .

Impacts of sample size

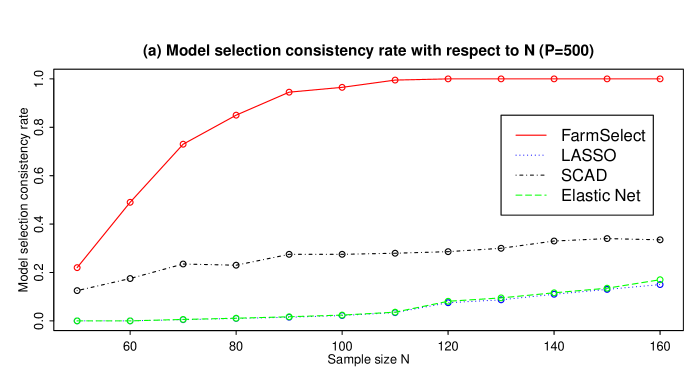

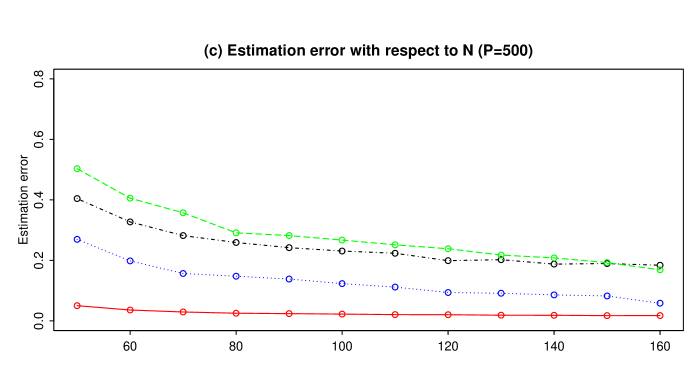

Second, we examine the model selection consistency with a fixed dimensionality and an increasing sample size. We fix and let increase from 50 to 150. For each given sample size, we simulate 200 replications and calculate the model selection consistency rates and the sure screening rates for LASSO, SCAD, elastic net and FarmSelect, respectively. For the elastic net, we set . The results are presented in Figure 3 (a) and Figure 3 (b). Figure 3 (a) shows that model selection consistency rates of LASSO, SCAD and elastic net do not enjoy fast convergence to 1 when the sample size increases, while the one of FarmSelect equals to one as long as the sample size exceeds 100. Similar phenomena are observed from sure screening rates. To demonstrate the prediction performance, we report the mean estimation error for each method, which is a good indicator of the prediction error. The estimation errors are reported in Figure 3 (c). When the sample size is small, LASSO, SCAD and elastic net have large estimation errors since they tend to select overfitted models.

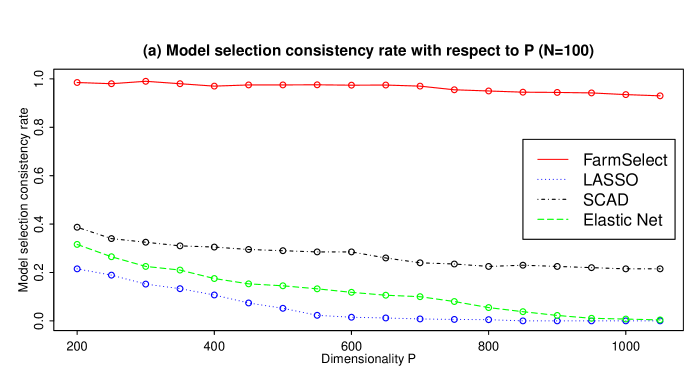

Impacts of dimensionality

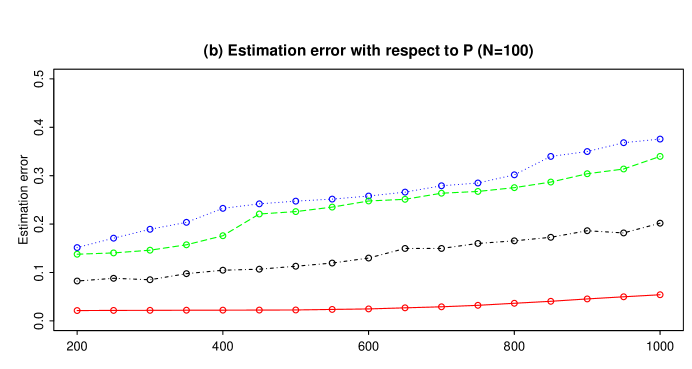

Third, we assess the model selection performance when the dimensionality is growing beyond and diverging. We fix and let grow from 200 to 1000. For each given , we simulate 200 replications and calculate the model selection consistency rate of LASSO, SCAD, elastic net and FarmSelect respectively. The model selection consistency rates are presented in Figure 4(a). According to Figure 4(a), the model selection consistency rate of FarmSelect stays close to 1 even as increases, whereas the rates for the other three methods drop quickly. Again, we report the estimation errors in Figure 4(b). As the dimensionality grows, FarmSelect has the least increase of estimation error.

5.2 Example 2: Logistic regression

We consider the following logistic regression model whose conditional probability function is:

| (5.1) |

We set sample size and dimensionality . The true coefficients are set to be with . Hence the true model size is 3.

The covariates are generated from one of the following three models:

-

(1)

Factor model with . Factors are generated from a stationary VAR(1) model with . The th entry of is set to be 0.5 when and when . We draw , and from the i.i.d. standard Normal distribution.

-

(2)

Equal correlated case. We draw from i.i.d. , where has diagonal elements 1 and off-diagonal elements 0.8.

-

(3)

Uncorrelated case. We draw from i.i.d.

We compare the model selection performance of FarmSelect with LASSO and simulate 100 replications for each scenario. The model selection performance is measured by selection consistency rate, sure screening rate and the average size of selected model. The results are presented in Table 2 below. According to Table 2, FarmSelect pays no price for the uncorrelated case and outperforms LASSO for highly correlated cases.

| Factor model with | ||||||

|---|---|---|---|---|---|---|

| FarmSelect | LASSO | |||||

| Selection rate | Screening rate | Average model size | Selection rate | Screening rate | Average model size | |

| 0.94 | 1.00 | 3.07 | 0.07 | 0.98 | 12.61 | |

| 0.90 | 0.99 | 3.12 | 0.05 | 0.95 | 12.94 | |

| 0.83 | 0.98 | 3.18 | 0.03 | 0.93 | 15.07 | |

| Equal correlated case | ||||||

| FarmSelect | LASSO | |||||

| Selection rate | Screening rate | Average model size | Selection rate | Screening rate | Average model size | |

| 0.93 | 1.00 | 3.09 | 0.07 | 0.85 | 9.90 | |

| 0.89 | 1.00 | 3.14 | 0.05 | 0.80 | 10.82 | |

| 0.85 | 0.99 | 3.19 | 0.02 | 0.69 | 11.79 | |

| Uncorrelated case | ||||||

| FarmSelect | LASSO | |||||

| Selection rate | Screening rate | Average model size | Selection rate | Screening rate | Average model size | |

| 0.97 | 1.00 | 3.03 | 0.95 | 1.00 | 3.14 | |

| 0.93 | 1.00 | 3.07 | 0.91 | 1.00 | 3.34 | |

| 0.91 | 1.00 | 3.10 | 0.89 | 1.00 | 3.42 | |

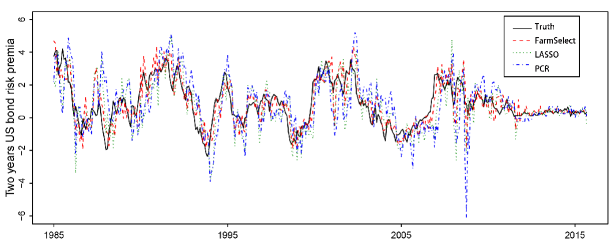

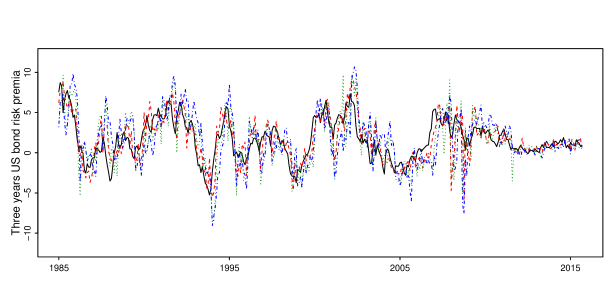

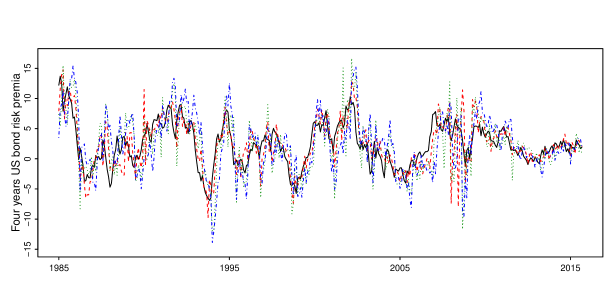

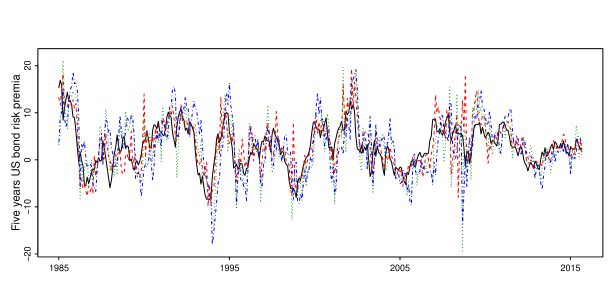

6 Prediction of U.S. bond risk premia

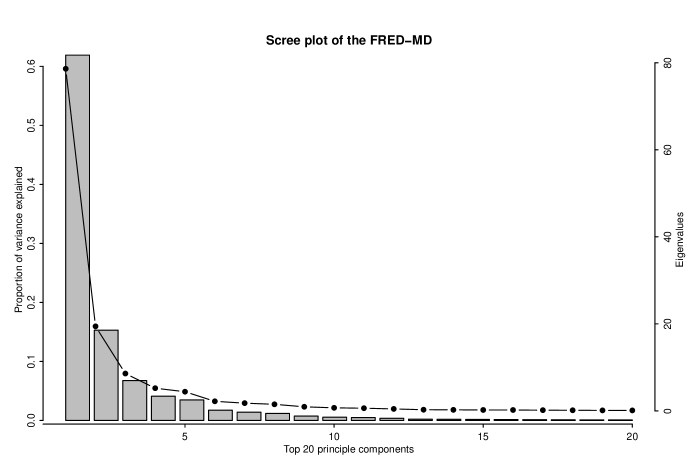

In this section, we predict U.S. bond risk premia with a large panel of macroecnomic variables. The response variable is the monthly data of U.S. bond risk premia with maturity of 2 to 5 years between January 1980 and December 2015 containing 432 data points. The bond risk premia is calculated as the one year return of an years maturity bond excessing the one year maturity bond yield as the risk-free rate. The covariates are 134 monthly U.S. macroeconomic variables in the FRED-MD database333The FRED-MD is a monthly economic database updated by the Federal Reserve Bank of St. Louis which is public available at http://research.stlouisfed.org/econ/mccracken/sel/. (McCracken and Ng, 2016). The covariates in the FRED-MD dataset are strongly correlated and can be well explained by a few principal components. To see this, we apply principal component analysis to the covariates and draw the scree plot of the top 20 principal components in Figure 5. The scree plot shows the first principal component solely explains more than 60% of the total variance. In addition, the first 5 principal components together explain more than 90% of the total variance.

We apply one month ahead rolling window prediction with a window size of 120 months. Within each window, we predict the U.S. bond risk premia by a high dimensonal linear regression model of dimensionality 134. We compare the proposed FarmSelect method with LASSO in terms of model selection and prediction. In addition, we include the principal component regression (PCR) in the competition of prediction. The FarmSelect is implemented by the FarmSelect R package with default settings. To be specific, the loss function is , the number of factors is estimated by the eigen-ratio method and the regularized parameter is selected by multi-fold cross validation. The LASSO method is implemented by the glmnet R package. The PCR method is implemented by the pls package in R. The number of principal components is chosen as 8 which is suggested in Ludvigson and Ng (2009).

The prediction performance is evaluated by the out-of-sample which is defined as

where is the response variable realized at time , is the predicted by one of the three methods above using the previous 120 months data, and is the sample mean of the previous 120 months responses , which represents a naive predictor. For FarmSelect and LASSO, we also report the average selected model size for prediction at time . The out-of-sample and average selected model size are reported in Table 3. The detailed prediction performances can be viewed in Figure 6. The results in Table 3 show that FarmSelect selects parsimonious models and achieves the highest ’s in all scenarios. On the contrary, LASSO may select redundant models as it ignores the correlations among covariates. To see this, we rank the covariates according to the selection frequency. The top 10 selected covariates and their frequencies are listed in Table 4. According to Table 4, LASSO tends to select some highly correlated covariates simultaneously. For instance, LASSO includes both Housing Starts Northeast and New Private Housing Permits, Northeast (SAAR) due to strong correlation between them. In addition, both Switzerland/U.S. and Japan/U.S. exchange rates enter the solution path of LASSO early, which can be another evidence of overfitting.

| Maturity of Bond | Out of sample | Average model size | |||

|---|---|---|---|---|---|

| FarmSelect | LASSO | PCR | FarmSelect | Lasso | |

| 2 Years | 0.2586 | 0.2295 | 0.2012 | 8.80 | 22.72 |

| 3 Years | 0.2295 | 0.2166 | 0.1854 | 8.92 | 21.40 |

| 4 Years | 0.2137 | 0.1801 | 0.1639 | 9.03 | 20.74 |

| 5 Years | 0.2004 | 0.1723 | 0.1463 | 9.21 | 20.21 |

| FarmSelect | ||

|---|---|---|

| Rank | Name | Frequency |

| 1 | Switzerland / U.S. Foreign Exchange Rate | 75 |

| 2 | Civilians Unemployed - Less Than 5 Weeks | 73 |

| 3 | Moody’s Baa Corporate Bond Minus FEDFUNDS | 72 |

| 4 | Housing Starts, Northeast | 71 |

| 5 | Industrial Production: Durable Consumer Goods | 69 |

| 6 | CBOE S&P 100 Volatility Index | 65 |

| 7 | Real M2 Money Stock | 64 |

| 8 | 10-Year Treasury Rate | 63 |

| 9 | CPI : Commodities | 61 |

| 10 | Commercial and Industrial Loans | 58 |

| LASSO | ||

| Rank | Name | Frequency |

| 1 | CBOE S&P 100 Volatility Index | 134 |

| 2 | Industrial Production: Residential Utilities | 130 |

| 3 | Housing Starts, Northeast | 127 |

| 4 | Switzerland / U.S. Foreign Exchange Rate | 126 |

| 5 | Industrial Production: Fuels | 124 |

| 6 | New Private Housing Permits, South | 122 |

| 7 | Canada / U.S. Foreign Exchange Rate | 117 |

| 8 | 10-Year Treasury Rate | 114 |

| 9 | Japan / U.S. Foreign Exchange Rate | 110 |

| 10 | CPI : Commodities | 106 |

References

- Akaike (1973) Akaike, H. (1973). Information theory and an extension of the maximum likelihood principle. In Second International Symposium in Informa- tion Theory, (B.N. Petroc and F. Caski, eds.). Akademiai Kiado, Bu- dapest, 276–281.

- Ahn and Horenstein (2013) Ahn, S. C. and Horenstein, A. R. (2013). Eigenvalue ratio test for the number of factors. Econometrica, 81, 1203–1227.

- Bai (2003) Bai, J. (2003). Inferential theory for factor models of large dimensions. Econometrica, 71, 135–171.

- Bai and Ng (2002) Bai, J. and Ng, S. (2002). Determining the number of factors in approximate factor models. Econometrica, 70, 191–221.

- Bickel et al. (2009) Bickel, P. J., Ritov, Y. A., and Tsybakov, A. B. (2009). Simultaneous analysis of Lasso and Dantzig selector. The Annals of statistics, 37, 1705–1732.

- Candes and Tao (2007) Candes, E. and Tao, T. (2007). The Dantzig selector: Statistical estimation when is much larger than . The Annals of Statistics, 35, 2313–2351.

- Choi (1992) Choi, B.S. (1992). ARMA Model Identification., Springer-Verlag, New York.

- Donoho and Elad (2003) Donoho, D. L. and Elad, M. (2003). Optimally sparse representation in general (nonorthogonal) dictionaries via minimization. Proceedings of the National Academy of Sciences, 100, 2197–2202.

- Efron et al. (2004) Efron, B., Hastie, T., Johnstone, I. and Tibshirani, R. (2004). Least angle regression. The Annals of statistics, 32, 407–499.

- Fan and Li (2001) Fan, J., and Li, R. (2001). Variable selection via nonconcave penalized likelihood and its oracle properties. Journal of the American statistical Association, 96, 1348-1360.

- Fan et al. (2013) Fan, J., Liao, Y. and Mincheva, M. (2013). Large covariance estimation by thresholding principal orthogonal complements (with discussion). Journal of the Royal Statistical Society, Series B, 75, 603–680.

- Fan and Lv (2008) Fan, J. and Lv, J. (2008). Sure independence screening for ultrahigh dimensional feature space. Journal of the Royal Statistical Society, Series B, 70, 849–911.

- Fan and Peng (2004) Fan, J. and Peng, H. (2004). On non-concave penalized likelihood with diverging number of parameters. Annals of Statistics, 32, 928-961.

- Fan and Song (2009) Fan, J. and Song, R. (2009). Sure Independence Screening in Generalized Linear Models with NP-Dimensionality. Annals of Statistics, 38,3567–3604.

- Forni et al. (2013) Forni, M., Hallin, M., Lippi, M.and Reichlin, L. (2005). The generalized dynamic factor model: one-sided estimation and forecasting. ournal of the American Statistical Association, 100, 830–840.

- Friedman et al. (2010) Friedman, J., Hastie, T. and Tibshirani, R. (2010). Regularization paths for generalized linear models via coordinate descent. Journal of statistical software, 33, 1–22.

- Hallin and Liška (2007) Hallin, M. and Liška, R. (2007). Determining the number of factors in the general dynamic factor model. Journal of the American Statistical Association, 102, 603–617.

- Johnstone and Lu (2009) Johnstone, I. M. and Lu, A. Y. (2009). On consistency and sparsity for principal components analysis in high dimensions. Journal of the American Statistical Association, 104, 682–693.

- Kneip and Sarda (2011) Kneip, A. and Sarda, P. (2011). Factor models and variable selection in high-dimensional regression analysis. The Annals of Statistics, 39, 2410–2447.

- Lam and Yao (2012) Lam, C. and Yao, Q. (2012). Factor modeling for high dimensional time-series: inference for the number of factors. Annals of Statistics, 40, 694–726.

- Lawley and Maxwell (1971) Lawley, D. and Maxwell, A. (1971). Factor analysis as a statistical method., Butterworths, London.

- Lee et al. (2015) Lee, J. D., Sun, Y. and Taylor, J. E. (2015). On model selection consistency of regularized M-estimators. Electronic Journal of Statistics, 9, 608–642.

- Luo et al. (2009) Luo, R., Wang, H. and Tsai, C. L. (2009). Contour projected dimension reduction. Ann. Statist., 37, 3743-3778.

- Ludvigson and Ng (2009) Ludvigson, S. and Ng, S. (2009). Macro factors in bond risk premia. Review of Financial Studies, 22, 5027–5067.

- McCracken and Ng (2016) McCracken, M. and Ng, S. (2016). FRED-MD: A Monthly Database for Macroeconomic Research. Journal of Business & Economic Statistics, 34, 574–589.

- Meinshausen and Bühlmann (2006) Meinshausen, N. and Bühlmann, P. (2006). High-dimensional graphs and variable selection with the lasso. The annals of statistics, 34, 1436–1462.

- Merlevède et al. (2011) Merlevède, Florence and Peligrad, Magda and Rio, Emmanuel (2011). A Bernstein type inequality and moderate deviations for weakly dependent sequences. Probability Theory and Related Fields, 151, 435–474.

- Negahban et al. (2012) Negahban, S., Ravikumar, P. K., Wainwright, M. J. and Yu, B. (2012). A unified framework for high-dimensional analysis of -estimators with decomposable regularizers. Statistical Science, 27, 1348–1356.

- Oberthuer et al. (2006) Oberthuer, A., Berthold, F., Warnat, P., Hero, B., Kahlert, Y., Spitz, R., Ernestus, K., Knig, R., Haas, S.,, Eils, R., and Schwab, M. (2006). Customized oligonucleotide microarray gene expression-based classification of neuroblastoma patients outperforms current clinical risk stratification. Journal of clinical oncology, 24, 5070–5078.

- Schwarz (1978) Schwarz, G.E. (1978). Estimating the dimension of a model. The Annals of statistics, 6, 461–464.

- Shen et al. (2016) Shen, D., Shen, H., Zhu, H. and Marron, J. S. (2016). The statistics and mathematics of high dimension low sample size asymptotics. Statistica Sinica, 26, 1747–1770.

- Stock and Watson (2002) Stock, J. and Watson, M. (2002). Forecasting using principal components from a large number of predictors. Journal of the American Statistical Association, 97, 1167–1179.

- Tiao and Tsay (1989) Tiao, G. C., and Tsay, R. S. (1989). Model specification in multivariate time series. Journal of the Royal Statistical Society. Series B, 51, 157–213.

- Tsay and Tiao (1985) Tsay, R. S., and Tiao, G. C. (1985). Use of canonical analysis in time series model identification. Biometrika, 72, 299–315.

- Tibshirani (1996) Tibshirani, R. (1996). Regression shrinkage and selection via the Lasso. Journal of the Royal Statistical Society: Series B, 58, 267–288.

- Van De Geer (2008) Van De Geer, S. A. (2008). High-dimensional generalized linear models and the lasso. The Annals of Statistics, 36, 614–645.

- Wainwright (2009) Wainwright, M. J. (2009). Sharp thresholds for high-dimensional and noisy sparsity recovery using-constrained quadratic programming (lasso). quadratic programming (Lasso) IEEE transactions on information theory, 55, 2183–2202.

- Wang (2012) Wang, H (2012). Factor profiled sure independence screening. Biometrika, 99, 15–28.

- Wang and Fan (2017) Wang, W. and Fan, J. (2017). Asymptotics of Empirical Eigen-structure for Ultra-high Dimensional Spiked Covariance Model. Annals of Statistics, 45, 1342–1374.

- Wang and Leng (2016) Wang, X. and Leng, C. (2016). High dimensional ordinary least squares projection for screening variables. Journal of the Royal Statistical Society: Series B (Statistical Methodology), 78, 589–611.

- Zhang (2010) Zhang, C. H. (2010). Nearly unbiased variable selection under minimax concave penalty. The Annals of Statistics, 38, 894–942.

- Zhao and Yu (2006) Zhao, P. and Yu, B. (2006). On model selection consistency of Lasso. Journal of Machine Learning Research, 7, 2541–2563.

- Zou and Hastie (2005) Zou, H. and Hastie, T. (2005). Regularization and variable selection via the elastic net. Journal of the Royal Statistical Society: Series B (Statistical Methodology), 67, 301–320.

- Zou and Li (2008) Zou, H. and Li, R. (2008). One-step sparse estimates in nonconcave penalized likelihood models. The Annals of statistics, 36, 1509–1533.

- Lawley and Maxwell (1971) Lawley, D. and Maxwell, A. (1971). Factor analysis as a statistical method., Butterworths, London.

Appendix A Some preliminary results

In the first appendix, we introduce some useful results in convex analysis and inverse problems. Under mild conditions, the tools we developed connect the unique global optimum of the regularized loss function with the solution of a constrained problem .

Lemma A.1.

Suppose and is convex. is convex and for and , where is a linear subspace of and is its orthonormal complement. In addition, there exists such that for and . Let where , and .

If and for all , then is the unique global minimizer of .

Proof.

For any we use , to denote its orthonormal projections on and , respectively. On the one hand, by convexity and orthogonality we have

Since , there exists such that implies . Together with , we know as long as , and the inequality strictly holds when .

On the other hand, . Hence forces and the inequality strictly holds when .

Now suppose . If , then the facts and , implies that . In addition, our assumptions yield for , leading to over . If , then and . Therefore is a strict local optimum of , which is convex over . This finishes the proof.

∎

Lemma A.2.

Let be convex over a Euclidean space . If , , and over the sphere , then any minimizer of is within the ball .

Proof.

For any , there exists and such that . Then , yielding . Hence there is no minimizer outside . ∎

Lemma A.3.

Suppose is a Euclidean space, and is convex over . In addition, there exist such that as long as and . If , then any minimizer of is within the ball .

Proof.

If and , then

Taking and such that . This forces over the sphere . Let be one of the minimizers of . Lemma A.2 implies that . Then . The result is proved by taking the infimum over . ∎

Corollary A.1.

Suppose , is a Euclidean space, , and is convex, and is convex. In addition, there exist such that as long as . If , then has unique minimizer and .

Proof.

Note that . There exists such that and . Applying Lemma A.3 to and , we obtain that any minimizer of satisfies . Then and , proving both the bound and uniqueness. ∎

Proof of Lemma 3.1

Let and . Note that and . The claim is proved by

Proof of Lemma 3.2

Appendix B Proofs of Section 4

B.1 Proof of Theorem 4.1

Define for . We first introduce two useful lemmas.

Lemma B.1.

Suppose and and , where is an induced norm. Then .

Proof.

By the sub-multiplicity of induced norms,

∎

Proof.

Define for and . Note that for any symmetric matrix , we have and . Hence by the Assumptions we obtain that when and ,

Now we are ready to prove Theorem 4.1.

Proof of Theorem 4.1.

First we study the restricted problem . Take and . Let and hence . Lemma B.2 shows that and over .

Second, we study the bound. On the one hand, the optimality condition yields and hence . On the other hand, by letting () we have

Hence

By Assumptions 4.1 and 4.2, we obtain that

By we have

Therefore,

| (B.1) |

Third we study the bound. The bound on can be obtained in a similar way. Using the fact that for symmetric matrices,

Hence . Since , we also have

This gives another bound.

By Lemma A.1, to derive it remains to show that . Using the Taylor expansion we have

| (B.2) |

On the one hand, the first term in (B.2) follows,

By the Taylor expansion, triangle’s inequality, Assumption 4.1 and the fact that ,

On the other hand, we bound the second term in (B.2). Note that for all . Assumption 4.1 yields

As a result,

Recall that the bound in (B.1). By plugging in this estimate, and using the assumptions and , we derive that

This implies and translates all the bounds for to the ones for . The proposition on sign consistency follows from elementary computation, thus we omit its proof. ∎

B.2 Proof of Theorem 4.2

Proof of Theorem 4.2.

Recall that . Also, Assumption 4.6 tells us is nonsingular and so is . Define , , , and . We easily see that and . Then it follows that and for any norm .

Consequently, Theorem 4.2 is reduced to studying and the loss function . The Lemma B.3 below implies that all the regularity conditions (with ) in Theorem 4.1 are satisfied.

Let and be the -th element of and , respectively. Observe that , and . Hence and consequently, , and . In addition, . Based on these estimates, all the results follow from Theorem 4.1 and some simple algebra. ∎

Here we present the Lemma B.3 used above and its proof.

Lemma B.3.

Proof.

(i) Based on the fact that , we have and . For any and ,

| (B.3) |

By the Cauchy-Schwarz inequality and , we obtain that for , . Plugging this result back to (B.3), we get

(ii) Now we come to the second claim. For any ,

Also, by and we have

Define . By the Jensen’s inequality, ,

As a result,

| (B.4) |

Let . Then

| (B.5) |

(iii) The third argument follows (B.6) easily. Since holds for any symmetric matrix , we have and thus .

(iv) Finally we prove the last inequality. On the one hand,

From claim (ii) and (B.4) it is easy to see that

On the other hand, we can take , and . By Assumption 4.5, . Lemma B.1 forces that

We have shown above in (B.5) that . As a result,

By combining these estimates, we have

Therefore . ∎

B.3 Proof of Lemma 4.1

Let for . Observe that and . By Cauchy-Schwarz inequality,

As a result,

| (B.7) |