Particles Systems and Numerical Schemes for

Mean Reflected Stochastic Differential Equations

Abstract.

This paper is devoted to the study of reflected Stochastic Differential Equations when the constraint is not on the paths of the solution but acts on the law of the solution. These reflected equations have been introduced recently by Briand, Elie and Hu [BEH16] in the context of risk measures. Our main objective is to provide an approximation of solutions to these reflected SDEs with the help of interacting particles systems. This approximation allows to design a numerical scheme for this kind of equations.

1. Introduction

In this paper, we are concerned with a special type of reflected Stochastic Differentials Equations (SDEs for short in the sequel) in which the constraint is not directly on the paths of the solution to the SDE as in the usual case but on the law of the solution. Typically, the integral of a given function, say , with respect to the law of the solution to the SDE is asked to be nonnegative. We call Mean Reflected Stochastic Differential Equation (MR-SDE) this kind of reflected SDEs which are described by the following system:

| (1.1) |

where , and are given Lipschitz functions from to and where stands for a standard Brownian motion defined on some complete probability space . We will always assume that is nondecreasing and that the law of is such that . The solution to (1.1) is the couple of continuous processes , being needed to ensure that the constraint is satisfied, in a minimal way according to the last condition namely the Skorokhod condition.

Reflected stochastic differential equations have been widely studied in the literature and we refer to the works [Tan79, LS84] for an overview of this theory. As said before, the main particularity comes here from the fact that the constraint acts on the law of the process rather than on its paths. This kind of processes has been introduced by Briand, Elie and Hu in their backward forms in [BEH16]. In that work, they show that mean reflected backward stochastic processes exist and are uniquely defined by the associated system of equations of the form of (1.1) under the same assumptions we use below. The main requirement for uniqueness is to ask the process to be a deterministic function. Our main objective in this paper is to study the convergence of a particles system approximation of (1.1) in order to be able to design numerical schemes for computing solutions to (1.1).

Due to the fact that the reflection process depends on the law of the position, we use for the approximation a particle system interacting through the reflection process. In the terminology of McKean-Vlasov processes (see [BPS91] for an overview), the reflection is hence non-linear. To conclude the analogy with McKean-Vlasov processes let us emphasize that the results obtained in the sequel can be extended to the case where the dynamic of the process (1.1) depends also on its own law.

Our main motivation for studying (1.1) comes from financial problems submitted to risk measure constraints. Given any position , its risk measure can be seen as the amount of own fund needed by the investor to hold the position. Mathematically, a risk measure is a nonincreasing application which is translation invariant in the sense that for any real constant , . Given a risk measure, the acceptance set i.e. the set of all acceptable positions is defined as . A classical example of risk measure is the so called Value at Risk at level : with acceptance set . This means that the probability of loss has to be below the level . Another example of risk measure is the following: where is a utility function (concave and increasing) and is a given threshold. In this case the acceptance set is : a minimal profit is required. We refer the reader to [ADEH99] for coherent risk measures and to [FS02] for convex risk measures.

Suppose now that we are given a portfolio of assets whose dynamic, when there is no constraint, follows the SDE

For instance, in the Black & Scholes model, when the strategy of the agent depends on the wealth of the portfolio. Given a risk measure , one can ask that remains an acceptable position at each time . In the case of the value at risk, this means that the probability of loss is not too great and, in the case of a risk measure defined by a utility function, a minimal profit is guaranteed. In both examples, the constraint rewrites for ( in the case of , in the utility case).

In order to satisfy this constraint, the agent has to add some cash in the portfolio through the time and the dynamic of the wealth of the portfolio becomes

where is the amount of cash added up to time in the portfolio to balance the "risk" associated to . Of course, the agent wants to cover the risk in a minimal way, adding cash only when needed: this leads to the Skorokhod condition .

Putting together all conditions, we end up with a dynamic of the form (1.1) for the portfolio.

The paper is organized as follows. In Section 2, by letting the coefficients satisfy the usual smoothness assumptions (say Lipschitz continuity) and adding a structural assumption on the function (say bi-Lipschitz), we show that the system admits a unique strong solution i.e. there exists a unique pair of process satisfying system (1.1) almost surely, the process being an increasing and deterministic process. Then, we show that, by adding some regularity on the function , the Stieljes measure is absolutely continuous with respect to the Lebesgue measure and we give the explicit expression of its density.

Having in mind the analogy with McKean-Vlasov processes, we also show in Section 3 that system (1.1) can be seen as the limit of an interacting particles system with oblique reflection of mean field type. This could reflect a system of large number of players whose positions are constrained by the mean of the positions of the other players. If all the players have the same dynamic, and if the interaction between the players is on mean field type, we show that there is a propagation of chaos phenomenon so that when the number of players tends to the infinity, the reflection no more depends on the other positions, but only on their statistical distribution. This obviously comes from the law of large number and is what, in fact, exactly happened in the classical McKean-Vlasov setting.

As an application, this result allows to define in Section 4 an algorithm based on this interacting particle system together with a classical Euler scheme which gives a strong approximation of the solution of (1.1). This leads to an approximation error proportional, up to a factor, to the number of points of the discretization grid of the time interval (namely of , where is the number of points of the discretization grid) and on the number of particles (namely when the function is only bi-Lipschitz and when the function is smooth, standing for the number of particles). Finally, we illustrate in Section 5 these results numerically.

2. Existence, uniqueness and properties of the solution

Throughout this paper, we consider the following set of assumptions.

Assumption (A.1).

-

(i)

The functions and are Lipschitz continuous ;

-

(ii)

The random variable is square integrable.

Assumption (A.2).

-

(i)

The function is an increasing function and there exist such that

-

(ii)

The initial condition satisfies: .

Assumption (A.3).

such that belongs to : .

Assumption (A.4).

The mapping is a twice continuously differentiable function with bounded derivatives.

We emphasize that existence and uniqueness results hold only under (A.1) which is the standard assumption for SDEs and (A.2) which is the assumption used in [BEH16]. The convergence of particle systems require only an additional integrability assumption on the initial condition, namely (A.3). We sometimes add the smoothness assumption (A.4) on in order to improve some of the results.

We first recall the existence and uniqueness result of [BEH16] in the case of SDEs.

Definition 2.1.

Given this definition, we have the following result.

Theorem 2.2 (Briand, Elie and Hu, [BEH16]).

Proof.

The proof for the case of backward SDEs is given in [BEH16]. For the ease of the reader, we sketch the proof for the forward case.

Let be a given continuous process such that, for all , . We set

and define the function by setting

| (2.2) |

The function being given, let us define the process by the formula

Let us check that is the solution to (1.1). By definition of , and we have, almost everywhere,

so that -a.e. since is continuous and nondecreasing.

Next, consider the map which associates to the solution of (1.1). Let us show that is a contraction. Let and be given, and define and as above, using the same Brownian motion. We have from Cauchy-Schwartz and Doob inequality

From the representation (2.2) of the process and Lemma 2.5, we have that

Therefore,

Hence, there exists a positive , depending on on , and only, such that for all , the map is a contraction. We first deduce the existence and uniqueness of the solution on and then on by iterating the construction. ∎

Remark 2.3.

Note that from this construction, we deduce that for all positive :

It then follows that the unique solution of (1.1) is a Markov process on the space , where the space of probability measures on .

In the following, we make an intensive use of this representation formula of the process . Define the function

| (2.3) |

We will need also the inverse function in space of evaluated at namely:

| (2.4) |

as well as , the positive part of :

| (2.5) |

With these notations, denoting by the family of marginal laws of we have

| (2.6) |

We start by studying some properties of and .

Lemma 2.4.

Under (A.2) we have:

-

(i)

For all in , the mapping is a bi-Lipschitz function, namely:

(2.7) -

(ii)

For all in , the mapping satisfies the following Lipschitz estimate:

(2.8)

Proof.

The proof is straightforward from the definition of see (2.3). ∎

Note that thanks to Monge-Kantorovitch Theorem, assertion (2.8) implies that for all in , the function is Lipschitz continuous w.r.t. the Wasserstein-1 distance. Indeed, for two probability measures and , the Wasserstein-1 distance between and is defined by:

Therefore

| (2.9) |

Then, we have the following result about the regularity of :

Lemma 2.5.

Under (A.2), the mapping is Lipschitz-continuous in the following sense:

where is the inverse of at point 0. In particular,

| (2.10) |

Proof.

Let and be two probability measures on . From Lipschitz regularity of the positive part, we have

Next, using the bi-Lipschitz in space property of , we get that for any in :

By definitions of and we have, for all in : . Hence, by choosing :

The last assertion immediately follows from (2.9). ∎

We close this section by giving some additional properties of the solution of (1.1).

Let be the linear partial operator of second order defined by

| (2.11) |

for any twice continuously differentiable function .

Proposition 2.6.

Proof.

Let in . Then, thanks to Itô’s Formula we have for all positive :

| (2.13) |

where is given by (2.11).

Suppose, at the one hand, that . Then, by the continuity of and , we get that there exists a positive such that for all , . This implies in particular, from the definition of , that for all in .

At the second hand, suppose that , then two cases arise. Let us first assume that . Hence, we can find a positive such that for all , . We thus deduce from our assumptions and (2.13) that for all in . Therefore, for all in . Suppose next that . By continuity again, there exists a positive such that for all in it holds . Since must be positive on this set, we could have to compensate and is then positive for all in . Moreover, the compensation must be minimal i.e. such that . Equation (2.13) becomes:

on . Dividing both sides by and taking the limit gives (by continuity):

Thus, is absolutely continuous w.r.t. the Lebesgue measure with density:

| (2.14) |

∎

Remark 2.7.

This justifies, at least under the smoothness assumption (A.4) on the constraint function , the non-negative hypothesis imposed on .

Finally, we have the following result concerning the moments of the solution of (1.1).

Proposition 2.8.

Proof.

We have

Let us first consider the last term . From the Lipschitz property of lemma 2.5 of , and the definition of the Wasserstein metric we have

since as and where is defined by (2.1). Therefore

and so

The first part of the result follows from standard computations since and are Lipschitz continuous.

For the second part, the key observation is Remark 2.3:

Therefore, since , and we have

and the result follows from standard computations. ∎

3. Mean reflected SDE as the limit of an interacting reflected particles system

Having in mind the notations defined in the beginning of Section 2 and especially equation (2.6), we can write the unique solution of the SDE (1.1) as:

| (3.1) |

where stands for the law of

We here are interested in the particle approximation of such a system. Our candidates are the particles:

where are independent Brownian motions, are independent copies of and denotes the empirical distribution at time of the particles

It is worth noticing that

Remark 3.1.

Let us emphasize that the previous system of interacting particles can be seen as a multidimensional reflected SDE with oblique reflection. Indeed, if is concave, the set

is convex and the system

is nothing else but the SDE driven by and reflected in the convex with oblique reflexion in the direction . We refer to [LS84].

In order to prove that there is indeed a propagation of chaos effect, we introduce the following independent copies of

and we couple these particles with the previous ones by choosing the same Brownian motion.

In order to do so, we introduce the decoupled particles , :

Note that for instance the particles are i.i.d. and let us denote by the empirical measure associated to this system of particles.

We have the following result concerning the approximation (1.1) by interacting particles system.

Theorem 3.2.

Remark 3.3.

As shown in [FG15], the rate in case (i) is optimal in full generality for the control of the Wasserstein distance of the empirical measure of an i.i.d. sample of random variables towards its own law. It is interesting to note that the supremum over time implies no loss here, as the "propagation of chaos" is mainly herited from the reflection term through .

Proof.

Let . We have, for ,

Taking into account the fact that

we get the inequality

| (3.2) |

where we have set

On the one hand we have, using Doob and Cauchy-Schwartz inequalities

where depends only on and and may change from line to line.

On the other hand, by using (2.10),

and Cauchy-Schwartz inequality gives, since the variables are exchangeable,

Since,

the same computations as we did before lead to

Hence, with the previous estimates we get, coming back to (3.2),

where . Thanks to Gronwall’s Lemma

Proof of (i). Since the function is, at least, a Lipschitz function, we understand that the rate of convergence follows from the convergence of empirical measure of i.i.d. diffusion processes. The crucial point here is that we consider a uniform (in time) convergence, which may possibly damage the usual rate of convergence. We will see that however here, we are able to conserve this optimal rate. Indeed, in full generality (i.e. if we only suppose that (A.2) holds) we get that:

Thanks to the additional assumption (A.3) and to Proposition 2.8, we will adapt and simplify the proof of Theorem 10.2.7 of [RR98] using recent results about the control Wasserstein distance of empirical measures of i.i.d. sample to the true law by [FG15], to obtain

Indeed, let be a positive integer and set , . As in [RR98], denote

Then

Now, using the regularity properties of Proposition 2.8 and proceeding exactly as in [RR98, Th. 10.2.7] we have that there exists such that

We are left to control : first remark that

Use now assumption (A.3) and Theorem 2 (case (3)) in [FG15] to get

from which we deduce that

and optimization procedure on finishes the proof. Let us emphasize that this result does not care of the fact that is an empirical measure associated to i.i.d. copies of a diffusion process.

Proof of (ii). In the case where is a twice continuously differentiable function with bounded derivatives (i.e. under (A.4)), we succeed to take benefit from the fact that is an empirical measure associated to i.i.d. copies of diffusion process, in particular we can get rid of the supremum in time. In view of (3.3), we need a sharp estimate of

Let us first observe that is locally Lipschitz continuous. Indeed, since by definition , if , using (2.7),

We get from Itô’s formula, setting

Since has bounded derivatives and is a square integrable random variable for each (see Corollary 2.8), the result follows easily.

Let us denote by the Radon-Nikodym derivative of . By definition, we have, denoting by the semimartingale , since are independent copies of ,

It follows from Itô’s formula

together with

We deduce immediately that

| where we have set | ||||

As a byproduct,

We get, using Cauchy-Schwartz inequality, since and are i.i.d,

Thus, we get

Since is a martingale with

Doob’s inequality leads to

Finally, using the fact that has bounded derivatives, and are Lipschitz, we get

This gives the result coming back to (3.3).

∎

4. A numerical scheme for MRSDE

We are interested in the numerical approximation of the SDE (1.1) on . Here are the main steps of the scheme. Let be a subdivision of . Given this subdivision, we denote by “” the mapping if , . For simplicity, we consider only the case of regular subdivisions: for a given integer , , .

Let us recall that we proved in the previous section that particles system

| where we have set | ||||

being independent Brownian motions and being independent copies of , converges toward the solution to (1.1). Thus, the numerical approximation is obtained by an Euler scheme applied to this particles system. We introduce the following discrete version of the particles system

| with the notation | ||||

4.1. Scheme

Using the notations given above, the result on the interacting system of mean reflected particles of the MR-SDE of Section 3 and Remark 2.3, we deduce the following algorithm for the numerical approximation of the MR-SDE:

Remark 4.1.

We emphasize that, at each step of the algorithm, we approximate the increment of the reflection process by the increment of the this approximation:

As suggested in Remark 2.3, this increment can be approached by:

Indeed, using the same kind of arguments as in the sketch of the proof of Theorem 2.2, one can show that the increments of the approximated reflection process are equals to the approximation of the increments:

4.2. Scheme error

Proposition 4.2.

Let us admit for the moment the following result that will be useful for our proof.

Lemma 4.3.

There exists a constant such that

We may now proceed to the proof of proposition 4.2

Proof.

Let us fix and . We have, for ,

Hence, using Cauchy-Schwartz and Doob inequality we get:

| (4.1) |

We now deal with the last term in the right hand side: from Lemma 2.5 we have

| and, since the law of the particles is independent by permutations, | ||||

For the first term of the right hand side, let us observe that, since the law of the particles is independent by permutations,

We have for the second term

and obviously

On the other hand,

Proof of Lemma 4.3.

Let us start by observing that

Since the random variables , , as well as the variables , , are independent and have the same law as ,

where , are independent normal gaussian random variables.

Let be the function defined on by ; is convex, increasing with values in . The inverse of is concave on , increasing and . We have, by Jensen inequality,

from which we deduce that

Finally, we have

This concludes the proof of the lemma. ∎

Let us recall that are independent and identically distributed copies of :

where stands for the law of

Theorem 4.4.

5. Numerical illustrations

Throughout this section, we consider, on the following sort of processes:

| (5.1) |

where , , and are bounded adapted processes. This sort of processes allow us to make some explicit computations leading us to illustrate the algorithm. Our results are presented for different diffusion and functions that are summarized below.

Linear constraint

We first consider cases where .

-

Case (i)

Drifted Brownian motion: , , , . We have

-

Case (ii)

Ornstein Uhlenbeck process: , , , , with . We have

-

Case (iii)

Ornstein Uhlenbeck process with stochastic mean parameter: , , , , , , . When

where and .

-

Case (iv)

Black and Sholes process: , , , . Then

Nonlinear constraint

Secondly, we illustrate the case of non-linear function :

and we illustrate this case with an

-

Case (v)

Ornstein Uhlenbeck process: , , , , with . We obtain

where for all in ,

Remark 5.1.

The reader may object that Case (iii) is out of the scope of our theoretical results, which is true. Nevertheless we let it in order to illustrate the robustness of the numerical method.

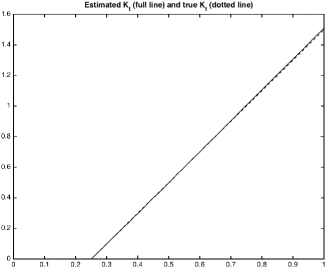

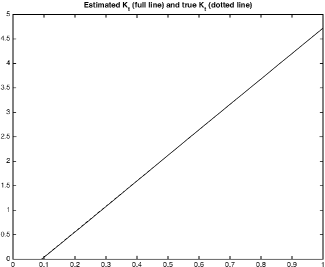

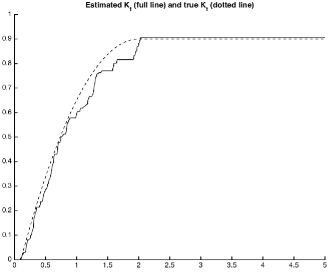

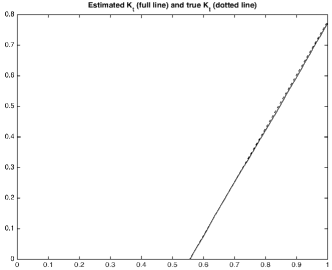

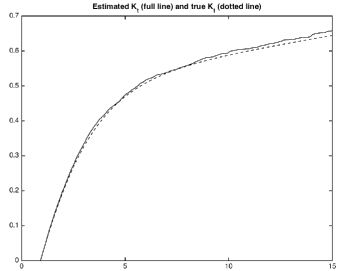

These examples have been chosen in such a way that we are able to give an analytic form of the reflecting process . This enables us to compare numerically the “true” process and its empirical approximation . When an exact simulation of the underlying process is available, we compute the approximation rate of our algorithm.

5.1. Proofs of the numerical illustrations

In order to have closed, or almost closed, expression for the compensator we introduce the process solution to the non-reflected SDE

Letting and applying Itô’s formula on , we get

Hence, the constraint rewrites

| (5.2) |

Proof of assertions (i), (ii) and (iv).

The formula for comes from the expression of its density given in Corollary 2.6 and the fact that in all these cases

∎

Proof of (iii).

Recall that we supposed . In that case, since , the constraint (5.2) becomes

| (5.3) |

so that is nondecreasing with and, for all in ,

| (5.4) |

Note first that since

and using the integration by parts formula we have

Remember that, in this case, we supposed that , and for supposed to be small enough. We here illustrate the dependence of the processes w.r.t. the parameter by adding a superscript on and . Since is a centered gaussian random variable with variance , we have

Therefore, for all ,

It follows that, up to ,

Since , we assume that and we obtain if ,

where . ∎

Proof of assertion (v).

In that case, we have

and

Hence

Since is a centered gaussian random variable with variance ,

we obtain that

Therefore,

∎

5.2. Illustrations

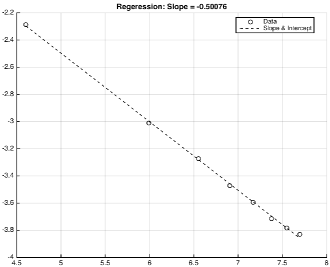

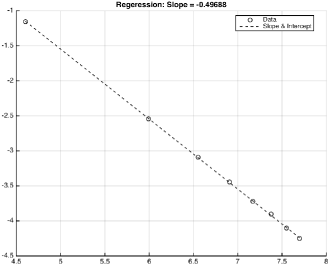

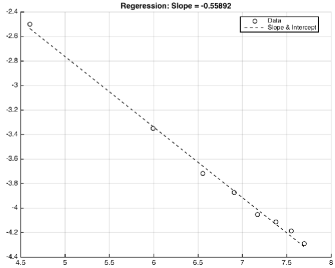

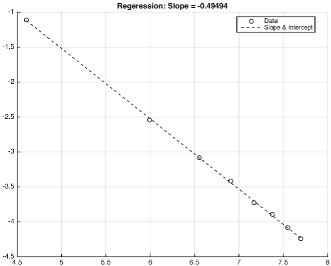

This computation works as follows. Let be a subdivision of of step size , being a positive integer, let be the unique solution of the MRSDE (5.1) and let, for a given , be its numerical approximation given by Algortihm 1. For a given integer , we draw and , independent copies of and . We then approximate the -error of Proposition 4.4 by:

| (5.5) |

References

- [ADEH99] Philippe Artzner, Freddy Delbaen, Jean-Marc Eber, and David Heath. Coherent measures of risk. Math. Finance, 9(3):203–228, 1999.

- [BEH16] Philippe Briand, Romuald Elie, and Ying Hu. BSDEs with mean reflexion. arXiv:1605.06301, 2016. submitted.

- [BPS91] Donald Burkholder, Etienne Pardoux, and Alain-Sol Sznitman. Topics in propagation of chaos. In Ecole d’Eté de Probabilités de Saint-Flour XIX — 1989, volume 1464 of Lecture Notes in Mathematics, pages 165–251. Springer Berlin / Heidelberg, 1991.

- [FG15] Nicolas Fournier and Arnaud Guillin. On the rate of convergence in Wasserstein distance of the empirical measure. Probab. Theory Related Fields, 162(3-4):707–738, 2015.

- [FS02] Hans Föllmer and Alexander Schied. Convex measures of risk and trading constraints. Finance Stoch., 6(4):429–447, 2002.

- [LS84] Pierre-Louis Lions and Alain-Sol Sznitman. Stochastic Differential Equations with Reflecting Boundary Conditions. Comm. Pure Appl. Math., 37(4):511–537, 1984.

- [RR98] Svetlozar T. Rachev and Ludger Rüschendorf. Mass transportation problems. Vol. I. Probability and its Applications (New York). Springer-Verlag, New York, 1998. Theory.

- [Tan79] Hiroshi Tanaka. Stochastic differential equations with reflecting boundary condition in convex regions. Hiroshima Mathematical Journal, 9(1):163–177, 1979.