Subdiffusive fractional Brownian motion regime for pricing currency options under transaction costs

Foad Shokrollahi

Department of Mathematics and Statistics, University of Vaasa, P.O. Box 700, FIN-65101 Vaasa, FINLAND

foad.shokrollahi@uva.fi

(Date: March 18, 2024)

Abstract.

A new framework for pricing European currency option is developed in the case where the spot

exchange rate follows a subdiffusive fractional Brownian motion. An analytic formula for pricing European

currency call option is proposed by a mean self-financing delta-hedging argument

in a discrete time setting. The minimal price of a currency option under transaction costs is obtained as time-step

, which can be used as the actual price of an option. In addition, we also show that

time-step and long-range dependence have a significant impact on option pricing.

Key words and phrases:

Tubdiffusion process;

Currency option;

Transaction costs;

Inverse subordinator process

2010 Mathematics Subject Classification:

91G20; 91G80; 60G22

1. Introduction

The classical and still most popular model of option pricing is the Black–Scholes [1]. It is

assumed that the price of risky asset is governed by a geometric Brownian motion, that is

(1.1)

where and are fixed and is the Brownian motion.

Empirical research show that the model cannot capture many of the characteristic features of prices, such as: long-range dependence, heavy-tailed and skewed marginal distributions, the lack of scale invariance, periods of constant values, etc. In 1983, Garman and Kohlhagen [2] presented a modified version of the model for pricing currency option. However, some scholars have argued that

option pricing with utilizing the model based on Brownian motion, cannot satisfactorily model for pricing currency option because currencies differ from stocks in financial markets. Hence, they have proposed some generalization of the model to capture the phenomena from stock markets [2, 3]. To capture these non-normal behaviors, many

researchers have considered other distributions with fat tails such as the

Pareto-stable distribution and the Generalized Hyperbolic Distribution

among others. Moreover, self-similarity and long-range dependence

have become important concepts in analyzing the financial time series.

There is strong evidence that the stock return has little or no

autocorrelation. Since fractional Brownian motion has two important

properties called self-similarity and long-range dependence, it has the

ability to capture the typical tail behavior of stock prices or indexes.

The fractional Brownian motion model is an extension of the model, which displays the long-range dependence observed in empirical data. The model is given by

(1.2)

where is a with Hurst parameter . It has been shown that the model admits arbitrage in a complete and frictionless market [4, 5, 6, 7, 8]. Wang [9] resolved this contradiction by giving up the arbitrage argument and examining option replication in the presence of proportional transaction costs in discrete time setting [10].

Magdziarz [11] applied the subdiffusive mechanism of trapping events

to describe properly financial data exhibiting periods of constant values and introduced the

subdiffusive geometric Brownian motion

(1.3)

as the model of asset prices exhibiting subdiffusive dynamics, where is a subordinated

process (for the notion of subordinated processes please refer to Refs. [12, 13, 14]), in which the

parent process is the geometric Brownian motion defined in (1.1) and is the inverse -stable subordinator

defined in the following way

(1.4)

is the -stable subordinator with Laplace transform: , , where denotes the mathematical expectation. Assuming

that is independent of the Brownian motion . Moreover, he demonstrated that this model is free-arbitrage but is incomplete. In this regard, he presented a new formula for fair prices of European option with the corresponding subdiffusive model. For additional information about more models that describe such characteristic behavior, you can see [15, 16, 17, 18, 19].

In this study, in order to capture the long-range dependence of interest rates and to examine option replication in the presence of proportional transaction costs in a discrete time setting, we consider the problem of pricing currency option, where the spot

exchange rate is governed by a subdiffusive as follows

(1.5)

Making the change of variable, , then we have

(1.6)

When the price of the underlying stock satisfies Eq. (1.6), we derive an explicit option pricing formula for the European

currency call option. This formula is similar to the Black–Scholes option pricing formula, but with the volatility being different.

We denote the subordinated process , where is a and is the inverse -subordinator, which are supposed to be independent. The process called a subdiffusion process. Particularly, when , it is a subdiffusion process presented in [20, 21].

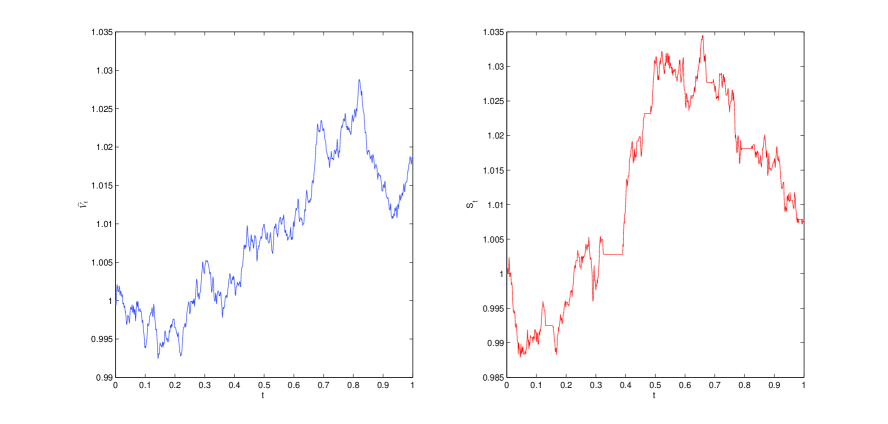

Fig. 1 shows typically the differences and relationships between the sample paths of the spot exchange rate in the model and the subdiffusive model.

Figure 1. Comparison of the spot exchange rate’sample paths in the model (left) and the subdiffusive model (right) for .

The rest of the paper proceeds as follows: In Section 2, we provide an analytic pricing formula for the European currency option in the subdiffusive environment and some Greeks of our pricing model are also obtained. Section 3 is devoted to analyze the impact of scaling and

long-range dependence on currency option pricing. Moreover, the comparison of our subdiffusive model and traditional models is undertaken in this section. Finally, Section 4 draws the concluding remarks.

2. Pricing model for the European call currency option

In this section we derive a pricing formula for the European call currency option of the subdiffusive

model under the following assumptions:

(i)

We consider two possible investments: (1) a stock whose price satisfies the equation:

(2.1)

where , , and and, are the domestic and the foreign interest rates respectively. (2) A money market account:

(2.2)

where shows the domestic interest rate.

(ii)

The stock pays no dividends or other distributions and all securities are perfectly divisible. There are no penalties to

short selling. It is possible to borrow any fraction of the price of a security to buy it or to hold it, at the short-term

interest rate. These are the same valuation policy as in the model.

(iii)

There are transaction costs which are proportional to the value of the transaction in the underlying stock. Let k denote

the round trip transaction cost per unit dollar of transaction. Suppose shares of the underlying stock are bought

or sold at the price , then the transaction cost is given by in either buying or selling. Moreover, trading takes place only at discrete intervals.

(iv)

The option value is replicated by a replicating portfolio with units of stock and riskless bonds with value . The value of the option must equal the value of the replicating portfolio to reduce (but not to avoid) arbitrage opportunities

and be consistent with economic equilibrium.

(v)

The expected return for a hedged portfolio is equal to that from an option. The portfolio is revised every and hedging

takes place at equidistant time points with rebalancing intervals of (equal) length , where is a finite and fixed,

small time-step.

Remark 2.1.

From [20, 22], we have . Then, by using -self-similar and non-decreasing sample paths of , we can obtain that -self-similarand non-decreasing sample paths of ,

(2.3)

and

(2.4)

Let be the price of a European currency option at time with a strike price that matures at time . Then, the pricing formula for currency call option is given by the following theorem

Theorem 2.1.

is the value of the European currency call option on the stock satisfied (1.6) and the trading takes place

discretely with rebalancing intervals of length . Then satisfies the partial differential equation

(2.5)

with boundary condition . The value of the currency call option is

(2.6)

and the value of the put currency option is

(2.7)

where

(2.8)

(2.9)

where is the cumulative normal distribution function.

In what follows, the properties of the subdiffusive model are discussed, such as Greeks, which summarize how option prices change with respect to underlying variables and are critically important to asset pricing and risk management. The model can be used to rebalance a portfolio to achieve the desired exposure to certain risk. More importantly, by knowing the Greeks, particular exposure can be hedged from adverse changes in the market by using appropriate amounts of other related financial instruments. In contrast to option prices that,

can be observed in the market, Greeks can not be observed and must be calculated given a model assumption. The Greeks are typically computed using a partial differentiation of the price formula.

Theorem 2.2.

The Greeks can be written as follows

(2.10)

(2.11)

(2.12)

(2.13)

(2.14)

(2.15)

(2.16)

Remark 2.2.

The modified volatility without transaction costs is given by

The aim of this section is to obtain the minimal price of an option with transaction costs and to show the impact of time scaling , transaction costs , and subordinator parameter on the subdiffusive model. Moreover, in the last part we compute the currency option prices using our model and make comparisons with the results of the and models.

Since often holds (For example: ), from Eq. (2.9) we have

(3.1)

where . Then the minimal volatility is

as .

Thus the minimal price of an option under transaction costs is represented as with in Eq. (2.8).

Moreover, the option rehedging time interval for traders to take is

.

The minimal price can be used as the actual price of an option.

In particular, since and

(3.2)

and , then we have

(3.3)

which displays that an increasing Hurst exponent comes along with a decrease of the option value (See Fig. 2).

On the other hand, if , then

(3.4)

and if , then as

In addition, if

(3.5)

and if , then as

Lux and Marchesi [24] have shown that Hurst exponent in some cases, so the equations (3.4) and (3.5)

have a practical application in option pricing. For example: if and , then , and ; and if and , then , and

In the following, we investigate the impact of scaling and long-range dependence on option pricing. It is well known that Mantegna and Stanley [25] introduced the method of scaling invariance from the complex science into the economic systems for the first time. Since then, a lot of research for scaling laws in finance has begun. If and , from Eq. (2.9) we know that shows that fractal scaling has not any impact on option pricing if a mean self-financing delta-hedging strategy is applied in a discrete time setting, while subordinator parameter has remarkable impact on option pricing in this case. In particular, from Eqs. (3.4) and (3.5), we know that as and as . Therefore is approximately scaling-free with

respect to the parameter , if , but is scaling dependent with respect to subordinator parameter . However, is scaling-dependent with respect to parameters and , if . On the other hand, if and , from Eq. (2.17) we know that , which displays that the fractal

scaling and sabordinator parameter have a significant impact on option pricing. Furthermore, for , from Eq. (2.8) we know that option pricing is scaling-dependent in general.

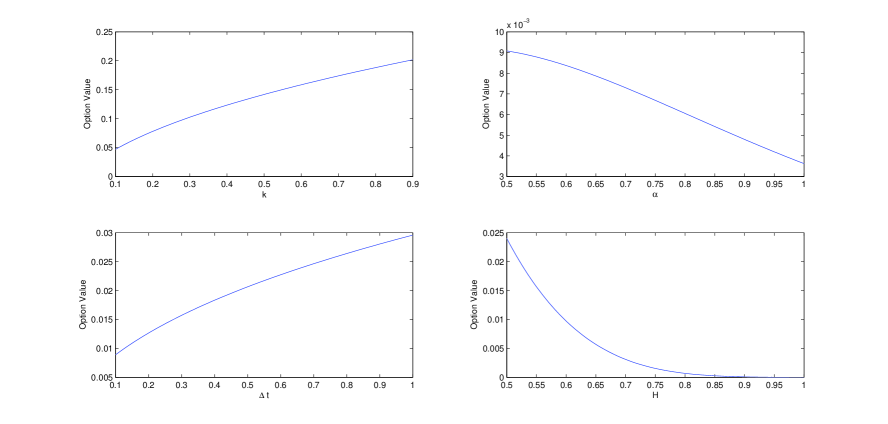

Now, we present the values of currency call option

using subdiffusive model for different parameters. For the sake of simplicity, we will just consider the out-of-the-money case. Indeed, using the same method,

one can also discuss the remaining cases: in-the-money and at-the-money. First, the prices of our subdiffusive model are investigated for some and prices for different exponent parameters. The prices of the call currency option versus its parameters and are revealed in Fig. 2. The selected parameters are . Fig. 2 indicates that, the option price is an increasing function of and , while, it is a decreasing function of and .

Figure 2. Call currency option values

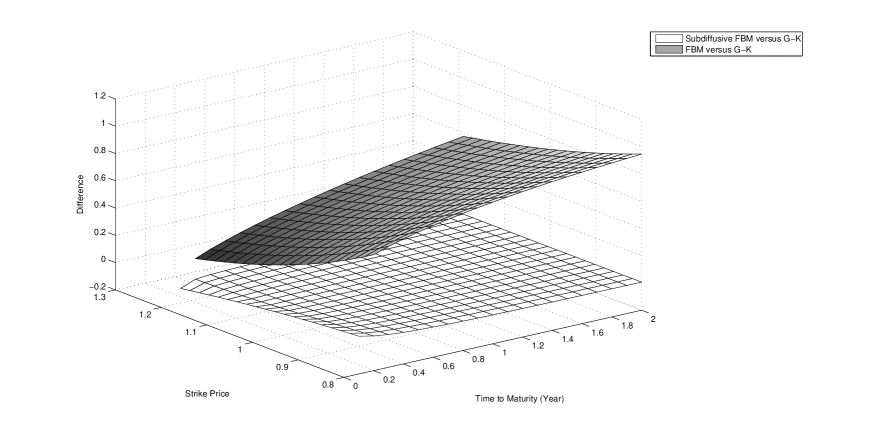

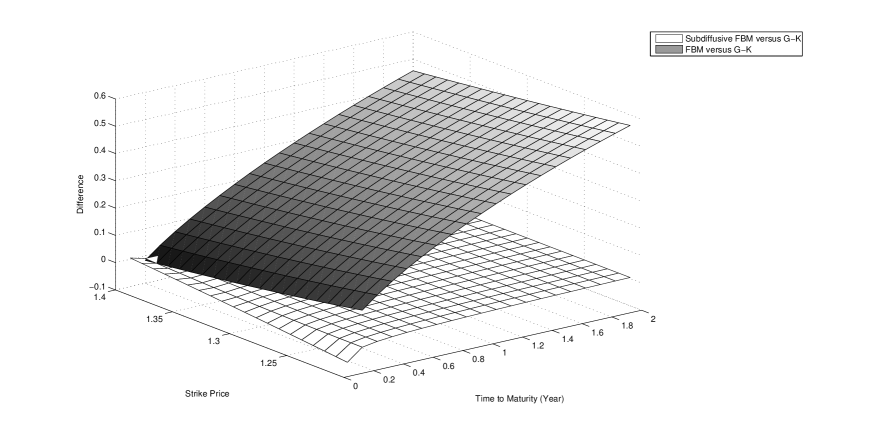

For a detailed analysis of our model, the prices calculated by the , and subdiffusive models are compared for both out-of-the-money and in-the-money cases. The following parameters are chosen: , and , along with time maturity , strike price for the in-the-money case and for the out-of-the-money case. Figs. 3 and 4 show the theoretical values difference by the , , and our subdiffusive models for the in-the-money and out-of-the-money, respectively. As indicated in these figures, the values computed by our subdiffusive model are better fitted to the values than the model for

both in-the-money and out-of-the money cases. Hence, when compared to these figures, our subdiffusive model seems reasonable.

Figure 3. Relative difference between the , , and subdiffusive models for the in-the-money caseFigure 4. Relative difference between the , , and subdiffusive models for the out-of-the-money case

4. Conclusion

Without using the arbitrage argument, in this paper we derive a European

currency option pricing model with transaction costs to capture the

behavior of the spot exchange rate price, where the spot exchange rate follows a subdiffusive with transaction costs.

In discrete time case, we show that the time scaling and the Hurst exponent play

an important role in option pricing with or without transaction costs and option pricing is scaling-dependent. In particular,

the minimal price of an option under transaction costs is obtained.

Appendix

Proof of Theorem 2.1. The movement of on time interval of length is

Moreover, from assumptions (iii) and (iv), it is found that the change in the value of portfolio is

(4.10)

where the number of bonds is constant during time-step . From assumption (v), is replicated by portfolio . Thus, at time points , , we have and . Therefore, according to Eqs. (4.6)-(4.10) we have

(4.11)

Consequently,

(4.12)

The time subscript, has been suppressed. As expected, using Eq. (4.12), (iv), Remark 2.1, and

[27] we infer

where is ever positive for the ordinary European currency call option without transaction costs, if the same conduct of is postulated here and remains fixed during the time-step . Then, from Eqs. (4.14) and (4.15) we obtain

(4.16)

Followed by

(4.17)

and

(4.18)

Proof of Theorem 2.2. First, we derive a general formula. Let be one of the influence factors. Thus

[1]

F. Black, M. Scholes, The pricing of options and corporate liabilities, The

Journal of Political Economy (1973) 637–654.

[2]

M. B. Garman, S. W. Kohlhagen, Foreign currency option values, Journal of

international Money and Finance 2 (3) (1983) 231–237.

[3]

T. S. Ho, R. C. Stapleton, M. G. Subrahmanyam, Correlation risk, cross-market

derivative products and portfolio performance*, European Financial Management

1 (2) (1995) 105–124.

[4]

P. Cheridito, Arbitrage in fractional brownian motion models, Finance and

Stochastics 7 (4) (2003) 533–553.

[5]

X.-T. Wang, E.-H. Zhu, M.-M. Tang, H.-G. Yan, Scaling and long-range dependence

in option pricing II: Pricing european option with transaction costs under

the mixed brownian–fractional brownian model, Physica A: Statistical

Mechanics and its Applications 389 (3) (2010) 445–451.

[6]

T. Sottinen, E. Valkeila, On arbitrage and replication in the fractional

black–scholes pricing model, Statistics & Decisions/International

mathematical Journal for stochastic methods and models 21 (2/2003) (2003)

93–108.

[7]

F. Shokrollahi, A. Kılıçman, Delta-hedging strategy and mixed

fractional brownian motion for pricing currency option, Mathematical Problems

in Engineering 501 (2014) 718768.

[8]

W.-L. Xiao, W.-G. Zhang, X.-L. Zhang, Y.-L. Wang, Pricing currency options in a

fractional brownian motion with jumps, Economic Modelling 27 (5) (2010)

935–942.

[9]

X.-T. Wang, Scaling and long-range dependence in option pricing I: Pricing

european option with transaction costs under the fractional black–scholes

model, Physica A: Statistical Mechanics and its Applications 389 (3) (2010)

438–444.

[10]

M. Mastinšek, Discrete–time delta hedging and the black–scholes model

with transaction costs, Mathematical Methods of Operations Research 64 (2)

(2006) 227–236.

[11]

M. Magdziarz, Black-scholes formula in subdiffusive regime, Journal of

Statistical Physics 136 (3) (2009) 553–564.

[12]

A. Janicki, A. Weron, Simulation and chaotic behavior of alpha-stable

stochastic processes, Vol. 178, CRC Press, 1993.

[13]

A. Janicki, A. Weron, Simulation and chaotic behaviour of a-stable stochastic

processes, Journal of the Royal Statistical Society-Series A Statistics in

Society 158 (2) (1995) 339.

[14]

A. Piryatinska, A. Saichev, W. Woyczynski, Models of anomalous diffusion: the

subdiffusive case, Physica A: Statistical Mechanics and its Applications

349 (3) (2005) 375–420.

[15]

E. Scalas, R. Gorenflo, F. Mainardi, Fractional calculus and continuous-time

finance, Physica A: Statistical Mechanics and its Applications 284 (1) (2000)

376–384.

[16]

J. Janczura, S. Orzeł, A. Wyłomańska, Subordinated -stable

ornstein–uhlenbeck process as a tool for financial data description, Physica

A: Statistical Mechanics and its Applications 390 (23) (2011) 4379–4387.

[17]

H. Gu, J.-R. Liang, Y.-X. Zhang, Time-changed geometric fractional brownian

motion and option pricing with transaction costs, Physica A: Statistical

Mechanics and its Applications 391 (15) (2012) 3971–3977.

[18]

F. Shokrollahi, A. Kılıçman, Pricing currency option in a mixed

fractional brownian motion with jumps environment, Mathematical Problems in

Engineering 2014.

[19]

Z. Guo, Option pricing under the merton model of the short rate in subdiffusive

brownian motion regime, Journal of Statistical Computation and Simulation

87 (3) (2017) 519–529.

[20]

M. Magdziarz, Stochastic representation of subdiffusion processes with

time-dependent drift, Stochastic Processes and their Applications 119 (10)

(2009) 3238–3252.

[21]

M. Magdziarz, Path properties of subdiffusion—a martingale approach,

Stochastic Models 26 (2) (2010) 256–271.

[22]

Z. Guo, H. Yuan, Pricing european option under the time-changed mixed

brownian-fractional brownian model, Physica A: Statistical Mechanics and its

Applications 406 (2014) 73–79.

[23]

C. Necula, Option pricing in a fractional brownian motion environment,

Available at SSRN 1286833.

[24]

T. Lux, M. Marchesi, Scaling and criticality in a stochastic multi-agent model

of a financial market, Nature 397 (6719) (1999) 498–500.

[25]

R. N. Mantegna, H. E. Stanley, et al., Scaling behaviour in the dynamics of an

economic index, Nature 376 (6535) (1995) 46–49.

[26]

S. G. Samko, A. A. Kilbas, O. I. Marichev, Fractional integrals and

derivatives, Theory and Applications, Gordon and Breach, Yverdon 1993.

[27]

H. E. Leland, Option pricing and replication with transactions costs, The

Journal of Finance 40 (5) (1985) 1283–1301.