Generalized RBF kernel for incomplete data

Abstract

We construct kernel, which generalizes the classical Gaussian RBF kernel to the case of incomplete data. We model the uncertainty contained in missing attributes making use of data distribution and associate every point with a conditional probability density function. This allows to embed incomplete data into the function space and to define a kernel between two missing data points based on scalar product in . Experiments show that introduced kernel applied to SVM classifier gives better results than other state-of-the-art methods, especially in the case when large number of features is missing. Moreover, it is easy to implement and can be used together with any kernel approaches with no additional modifications.

1 Introduction

Incomplete data analysis is an important part of data engineering and machine learning, since it appears naturally in many practical problems. In particular, in medical diagnosis, a doctor may be unable to complete the patient examination due to the deterioration of health status or lack of patient’s compliance (Burke et al., 1997); in object detection, the system has to recognize partially hidden faces (Mahbub et al., 2016) or identify shapes from corrupted images (Berg et al., 2005); in chemistry, the complete analysis of compounds requires high financial costs (Stahura & Bajorath, 2004). In consequence, the understanding and the appropriate representation of such data is of great practical importance.

The choice of the method for analyzing incomplete data depends on the reasons why data are missing (Schafer, 1997). If missing entires are generated completely randomly (MCAR) or at least do not depend on missing values (MAR), then one can reliably estimate the probability distribution of incomplete data by the mixture model applying EM algorithm. Otherwise, we can model the missing data mechanism, which however leads to more complex solutions, or we can completely discard missing features, which drastically reduces available information (NMAR).

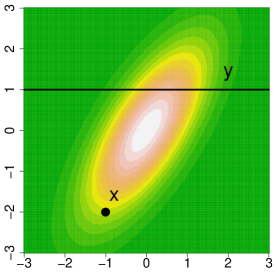

In this paper, we propose , a generalization of RBF (radial basis function) kernel to the case of incomplete data. To briefly explain our approach, let us recall that classical RBF can be constructed by embedding every point into the function space (with regularization by Gaussian kernel) and applying a standard scalar product in . To generalize this process for incomplete data, we model the uncertainty on missing coordinates by restricting data density to absent attributes (for a simplicity, we use a single Gaussian as a density model). In consequence, a missing data point is represented as a regularization of a singular Gaussian density on a respective affine subspace of the data. The illustration of the above process is presented in Figure 1.

Main features of can be summarized as follows:

-

•

is easy to implement and can be used together with any kernel approach,

-

•

it does not perform any direct imputations,

-

•

is effective, resistant to possible perturbations and robust to the number missing entries,

-

•

SVM classifier which uses obtains better results than existing state-of-the-art methods.

2 Related work

The most common approach to learning from incomplete data is known as deterministic imputation (McKnight et al., 2007). In this two-step procedure, the missing features are filled first, and only then a standard classifier is applied to the complete data (Little & Rubin, 2014). Although the imputation-based techniques are easy to use for practitioners, they lead to the loss of information which features were missing and do not take into account the reasons of missingness. To preserve the information of missing attributes, one can use an additional vector of binary flags, indicating which coordinates were missing.

The second popular group of methods aims at building a probabilistic model of incomplete data. If data are missing at random, then it is possible to apply EM algorithm to estimate a density of data by the mixture of parametric models (Ghahramani & Jordan, 1994; Schafer, 1997). Consequently, this allows to generate the most probable values from obtained probability distribution for missing attributes (random imputation) (McKnight et al., 2007) or to learn a decision function directly based on the distributional model. The second option was already investigated in the case of logistic regression (Williams et al., 2005), kernel methods (Smola et al., 2005; Williams & Carin, 2005) or by using second order cone programming (Shivaswamy et al., 2006). One can also estimate the parameters of the probability model and the classifier jointly, which was considered in (Dick et al., 2008; Liao et al., 2007). As it was mentioned above, the limitation of these techniques is the assumption about the process of missing data generation. If missing data depends on the unobserved features then there is no guarantee to get a reasonable estimation of data density.

There is also a group of methods which do not make any assumptions about the missing data mechanism and make a prediction from incomplete data directly. In (Chechik et al., 2008) a modified SVM classifier is trained by scaling the margin according to observed features only. The alternative approaches to learning a linear classifier, which avoid features deletion or imputation, are presented in (Dekel et al., 2010; Globerson & Roweis, 2006). In (Grangier & Melvin, 2010) the embedding mapping of feature-value pairs is constructed together with a classification objective function. Finally, the authors of (Hazan et al., 2015) design an algorithm for kernel classification that performs comparably to the classifier which have an access to complete data, under low-rank assumption (every vector can be reconstructed from the observed attributes).

3 Generalized RBF

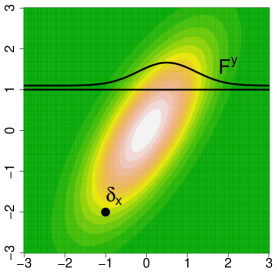

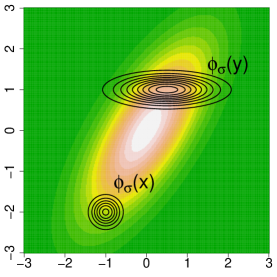

In this section we present the construction of kernel function. We begin with the description of incomplete data by affine subspaces. Next, we show how to use the information contained in data distribution to model the uncertainty on missing coordinates and, in consequence, how to represent incomplete data points by probability measures. This identification allows to apply the reasoning commonly used in classical RBF kernels and to define an analogue formula for a kernel function in the case of incomplete data. The visual representation of the idea behind kernel is given in Figure 2.

3.1 Subspace representation

An incomplete data point in is typically understood as a pair , where and is a set of indices of missing atributes. We can associate a missing data point with an affine subspace , where is the canonical base of . Let us observe that is a set of all -dimensional vectors, which coincide with on the coordinates different from .

In practice, data are often transformed by linear mappings (e.g. whitening) in a preprocessing stage. For this purpose, we generalize the above representation to arbitrary affine subspaces, which do not have to be generated over canonical bases. Therefore, we assume that the set of incomplete data consists of affine subspaces of the form , where is arbitrary and is a linear subspace of .

If is a an affine map, then we can transform a missing data point into another missing data point by the formula:

The linear part of is given by

One can easily compute and represent if the orthonormal base of is given, we simply orthonormalize the sequence .

For example, given the whitening operator:

where denotes the covariance and is the mean vector, a missing data point is transformed to

The linear part is mapped to , which has to be shifted by a vector (classical whitening operator applied to ).

3.2 Missing data point as a probability density

Subspace representation of incomplete data gives no information where the point is localized on the affine subspace. To add this information and to reduce the uncertainty connected with missing attributes we need the knowledge of the distribution of data. It allows to identify a missing data point with a degenerate density with support restricted to the affine subspace.

To realize this goal in practice, we need to perform a density estimation on the incomplete data set. It is well-known that it is possible to apply the EM algorithm to obtain the estimation by a mixture of parametric models if data satisfy missing at random assumption (MAR). Although in more general case the calculated density might be unreliable, we only use it to reduce the uncertainty on absent attributes (for observable attributes this density is not used). Therefore, we assume that some estimation of data density is given.

A complete data point (with no missing coordinates) can be identified with atom Dirac measure (a measure that takes value with probability ), because there is no uncertainty connected with this example. If we have an incomplete data point then the uncertainty is connected with its missing part, which can be modeled by a restriction of density to the affine subspace , which is denoted by (conditional density). Let us recall that if is an orthonormal base of then

This conditional density is defined for points contained in a subspace . Since we work in dimensional space, it is convenient to extend this conditional density to the degenerate density in original space. In other words, we have to form a density from the conditional density by:

We use a density to represent missing data points in .

For a simplicity and clarity of presentation, we restrict our attention to the case of Gaussian densities and assume that , given by

is a Gaussian estimation of the distribution on incomplete data set, where denotes the square of Mahalanobis norm of . Although a single Gaussian density might not be enough to fully reflect a complex structure of data, it is robust to the number of missing attributes, can be easily computed in practice and does not require so strong assumptions on missing data mechanism.

Below, we present how to obtain the conditional density and corresponding density in the original space from a data space distribution .

Observation 3.1.

Let be a density in the affine subspace . If is an orthonormal base of then the corresponding density in the original space equals , where

Proof.

If a random vector has a mean and a covariance , then has the mean and the covariance . We apply this fact to the map , which completes the proof. ∎

Observe that given above is a degenerate density in iff , i.e. the covariance matrix is singular (invertible).

Now, we discuss the inverse problem:

Observation 3.2.

Let be a normal density in . We assume that is an affine subspace of and is an orthonormal base of . Then, the conditional density in the space in the base given by equals , where

Proof.

Let us recall that the formula of normal density can be written as:

where is a normalization factor. Now, restricting the quadratic function to the space by putting we get

Finally, by the canonical form of the quadratic function111Recall the formula , for symmetric , can be rewritten as , for . we get that this mapping equals

where

∎

Taking the above two observations together, we can calculate both densities from the original density . In consequence, we represent a missing data point by a degenerate Gaussian density . As it was mentioned, this identification only influences absent attributes and has no effects on observable features.

3.3 Kernel construction

To define a scalar product (kernel function) on incomplete data, we will adapt the reasoning behind classical RBF kernels to the case of probabilistic representations introduced in previous subsection. Let us observe that the construction of classical RBF kernel for a complete data can be decomposed into the following steps:

-

•

We map every point to Dirac measure .

-

•

Next, we embed it into space by taking the convolution (regularization) with , where is a fixed paramter:

(1) -

•

Then, we apply the normalization

-

•

Finally, we apply the scalar product in space between embeddings to define the kernel function

Due to the normalization, we have .

If not stated otherwise, and will denote classical norm and scalar product in space, respectively.

To perform an analogue procedure in the case of missing data identified with Gaussian densities, let us introduce basic notations. We recall, that the standard scalar product in space is given by

In the case of Gaussian densities, the above scalar product can be easily computed by (Petersen et al., 2008):

| (2) |

where are non-degenerate Gaussians.

We also need the notion of convolution, which for densities is defined by

If is a measure with a mean and a covariance , then the convolution , where is an identity matrix and , is a measure with a mean and a covariance . The convolution of normal densities is a normal density and,

The above formula also holds for degenerate normal densities. In consequence, this operator works as a regularization and allows to transform a degenerate density into a non-degenerate one.

Let us now calculate the normalized embedding of missing data point into space. For a fixed , we have

| (3) |

where follow from Observations 3.1 and 3.2. Since we are interested in normalized embedding, we put:

To define a kernel function on incomplete data, we simply calculate the scalar product in space between embeddings of missing data points. More precisely, for two missing data points and , we put:

| (4) |

where is fixed.

| Data set | #Instances | #Attributes | Classes ratio |

|---|---|---|---|

| Australian | 690 | 14 | 0.56 |

| Bank | 1372 | 5 | 0.56 |

| Breast cancer | 699 | 8 | 0.66 |

| Crashes | 540 | 18 | 0.91 |

| Heart | 270 | 13 | 0.56 |

| Ionosphere | 351 | 34 | 0.64 |

| Liver disorders | 345 | 7 | 0.58 |

| Pima | 768 | 8 | 0.65 |

The following theorem gives a final formula for the kernel function.

Theorem 3.1.

Let be a density on and let be fixed. We assume that and represent missing data points and . Then, the scalar product (4) equals

| (5) |

where and the normalization factor equals:

Let us observe that the above formula generalizes the classical RBF kernel to the case of incomplete data. Indeed, complete data points are represented by Dirac measures, i.e. and . Then and

Taking a parametrization we arrive at the classical formula of RBF kernel. Thus, to be consistent with a typical RBF parametrization, in the experimental section we will use the formula

where

4 Experiments

We evaluated in binary classification experiments using SVM and compared the results with methods that work on incomplete data. We used examples retrieved from UCI repository combined with different strategies for attributes removal.

4.1 Experimental setting

We used eight UCI datasets (Asuncion & Newman, 2007), which are summarized in Table 1. For each one, we considered three strategies for creating missing entries, each one realizing different missing data assumption:

-

•

MCAR. We randomly removed a fixed percentage of features, .

-

•

MAR. We defined a structural process for attributes removal, where the selection of missing entries were fully accounted by visible features. We drawn points of a dataset . Then, for every , where for , we removed its -th attribute with a probability

where is a sample covariance matrix taken from data and is fixed. In other words, -th point determined the removal of -th feature. The value of was fixed so that to remove approximately .

-

•

NMAR. We modified previous scenario in the following way. The set of features was randomly divided into two equally-sized parts: visible features and hidden features . Given randomly selected points of , we removed attribute of with a probability

where denotes the restriction of to coordinates from (as before controlled the number of removed features). After that, data were represented only by features from , while coordinates included in were discarded. In other words, attributes were used to define a removal process, which depends on unobservable features.

The missing entries appeared in both train and test sets.

For a comparison, we used two imputation techniques as baseline, multiple imputation strategy and two state-of-the-art methods developed for SVM:

-

1.

mean: Missing coordinates were filled with average values taken over training set.

-

2.

zero: Absent attributes were set to zeros.

-

3.

mice: Unknown features were filled based on a train set using Multiple Imputation by Chained Equation (Azur et al., 2011) implemented in R package mice222https://cran.r-project.org/web/packages/mice/index.html (Buuren & Groothuis-Oudshoorn, 2011), where several imputations are drawing from the conditional distribution of data by Markov chain Monte Carlo techniques.

-

4.

geom: Geometric margin is a modified SVM classifier proposed by G. Chechik et. al. (Chechik et al., 2008), where no assumption about missing data mechanism is required. In this approach, an objective function is based on the geometric interpretation of the margin and aims to maximize the margin of each sample in its own relevant subspace.

-

5.

karma: It is an algorithm for kernel classification proposed by E. Hazan et. al. (Hazan et al., 2015), where the linear classifier is iteratively tuned.

To estimate a Gaussian density from incomplete data used in , we applied R package norm333https://cran.r-project.org/web/packages/norm/index.html on train set only (estimation stage did not have the access to test/validation set).

Each method was combined with SVM classifier using RBF kernel and tested in double 5-fold cross validation procedure. That is, for every division into train and test sets, the required hyperparameters were tuned using inner 5-fold cross validation applied on train set. The combination of parameters maximizing mean accuracy score (on validation set) was used to learn a final classifier on a entire train set, while the performance was evaluated on a test set that was not used during training. The accuracy was averaged over all 5 trails. Additionally, to reduce the effect from random deletion of attributes, we generated 10 different samples of incomplete data and averaged final accuracy scores.

After normalization of data, a grid search was applied to find optimal values of hyperparameters. We inspected the following ranges for margin parameter and kernel radius . Since karma loss is additionally parametrized by a parameter , we considered444Such a small range was chosen because of relatively high computational complexity of the algorithm. .

4.2 Results

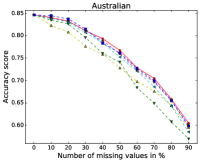

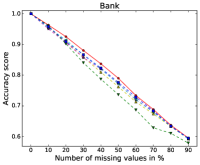

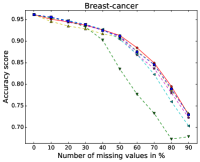

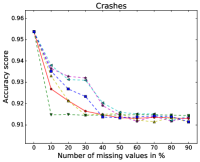

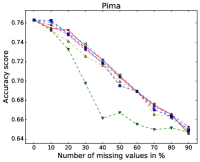

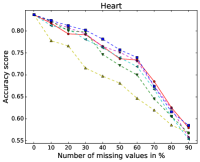

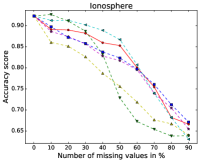

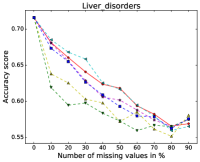

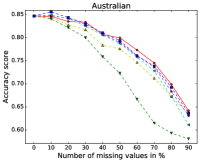

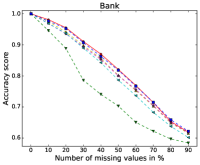

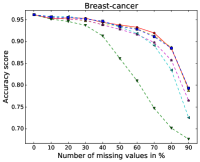

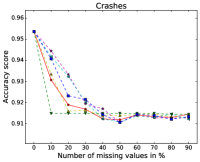

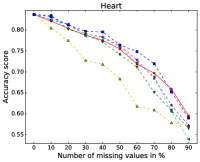

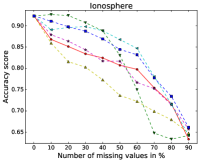

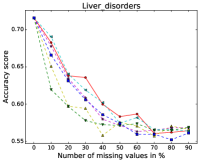

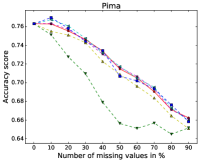

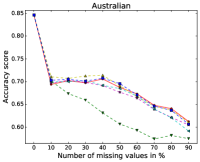

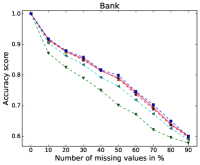

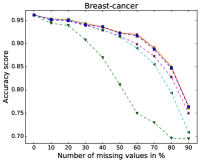

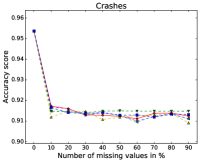

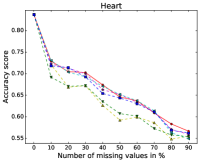

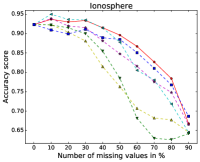

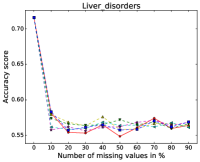

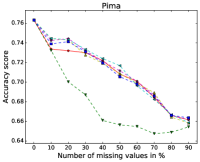

First of all, we noted that the difference between the results in MCAR and MAR scenarios is slight, which might follow from the fact that in both cases the removal process was based on visible features, see Figures 3 and 4. This behavior changed in NMAR situation, Figure 5, where on one hand removing mechanism was more complex, but on the other hand data were represented by lower number of features (half of features were hidden). In consequence, all methods obtained worse prediction rate. In particular, for Liver disorders and Crashes no method was able to produce useful results when at least 20% of attributes were missing (accuracy coincides with the classes ratio).

Visual inspection of the Figures suggests that , karma and mice gave similar results and were in general better than the other methods. It is not surprising that multiple imputation strategy performs better than simpler techniques, like zero or mean imputations. The same holds for karma algorithm, which was recently claimed to obtain state-of-the-art performance. Low quality results produced by geom algorithm might follow from the fact that this method ignores missing attributes and is only based on observed features, which could be beneficial for very complex removal processes.

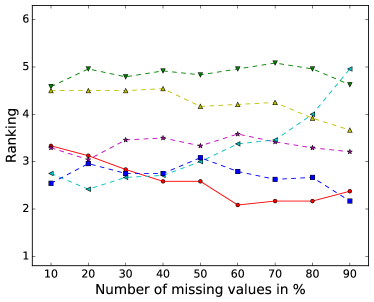

To further analyze the results, we ranked the methods over all data sets and all missing data scenarios; the best performing algorithm got the rank of 1, the second best rank 2 etc. The results presented in Figure 6 show that is best suited to the case when a lot of features are absent. Although the performance of mice is better for 10-30% of missing attributes, its results deteriorate heavily as the number of missing entries increases. It is worth to notice that the rank of karma is very stable. Almost always, it was the second best approach.

We also verified the results applying statistical tests, see (Demšar, 2006), specifically we used the Friedman test with Nemenyi post hoc analysis. Given a ranking of the methods (aggregated additionally over percentage of missing coordinates), the analysis consists of two steps:

-

•

the null hypothesis is made that all methods perform the same and the observed differences are merely random (the hypothesis is tested by the Friedman test, which follows a distribution)

-

•

having rejected the null hypothesis the differences in ranks are analyzed by the Nemenyi test.

Figure 7 visualizes the results for a significance level of . The x-axis shows the mean rank over combinations of data set and percentage of missing values for each method. Groups of methods for which the difference in mean rank is not statistically significant are connected by horizontal bars. As can be observed, the mean rank of is better than the others. This advantage is statistically significant comparing it with all methods except karma. Nevertheless, the use of our method is much simpler, since it relies on applying classical SVM with slightly modified kernel function, whereas karma uses an iterative algorithm to increase the performance of the classifier and requires the selection of one more hyperparameter.

5 Conclusion

We proposed , the generalization of RBF kernel to the case of incomplete data. This method uses the information contained in data distribution to model the uncertainty on absent attributes without performing any direct imputations. The experimental results show that outperforms imputation-based techniques and obtains slightly better results than recent state-of-the-art algorithm. Moreover, it does not require the modification of existing machine learning methods, which makes it easy to use in practice.

References

- Asuncion & Newman (2007) Asuncion, Arthur and Newman, David J. UCI Machine Learning Repository, 2007. URL http://www.ics.uci.edu/$∼$mlearn/{MLR}epository.html.

- Azur et al. (2011) Azur, Melissa J, Stuart, Elizabeth A, Frangakis, Constantine, and Leaf, Philip J. Multiple imputation by chained equations: what is it and how does it work? International journal of methods in psychiatric research, 20(1):40–49, 2011.

- Berg et al. (2005) Berg, Alexander C., Berg, Tamara L., and Malik, Jitendra. Shape matching and object recognition using low distortion correspondences. In Proceedings of the IEEE Computer Society Conference on Computer Vision and Pattern Recognition, pp. 26–33. IEEE, 2005.

- Burke et al. (1997) Burke, Lora E, Dunbar-Jacob, Jacqueline M, and Hill, Martha N. Compliance with cardiovascular disease prevention strategies: a review of the research. Annals of Behavioral Medicine, 19(3):239–263, 1997.

- Buuren & Groothuis-Oudshoorn (2011) Buuren, Stef and Groothuis-Oudshoorn, Karin. mice: Multivariate imputation by chained equations in r. Journal of statistical software, 45(3), 2011.

- Chechik et al. (2008) Chechik, Gal, Heitz, Geremy, Elidan, Gal, Abbeel, Pieter, and Koller, Daphne. Max-margin classification of data with absent features. Journal of Machine Learning Research, 9:1–21, 2008.

- Dekel et al. (2010) Dekel, Ofer, Shamir, Ohad, and Xiao, Lin. Learning to classify with missing and corrupted features. Machine Learning, 81(2):149–178, 2010.

- Demšar (2006) Demšar, Janez. Statistical comparisons of classifiers over multiple data sets. Journal of Machine learning research, 7(Jan):1–30, 2006.

- Dick et al. (2008) Dick, Uwe, Haider, Peter, and Scheffer, Tobias. Learning from incomplete data with infinite imputations. In Proceedings of the International Conference on Machine Learning, pp. 232–239. ACM, 2008.

- Ghahramani & Jordan (1994) Ghahramani, Zoubin and Jordan, Michael I. Supervised learning from incomplete data via an EM approach. In Advances in Neural Information Processing Systems, pp. 120–127. Citeseer, 1994.

- Globerson & Roweis (2006) Globerson, Amir and Roweis, Sam. Nightmare at test time: robust learning by feature deletion. In Proceedings of the International Conference on Machine Learning, pp. 353–360. ACM, 2006.

- Grangier & Melvin (2010) Grangier, David and Melvin, Iain. Feature set embedding for incomplete data. In Advances in Neural Information Processing Systems, pp. 793–801, 2010.

- Hazan et al. (2015) Hazan, Elad, Livni, Roi, and Mansour, Yishay. Classification with low rank and missing data. In Proceedings of The 32nd International Conference on Machine Learning, pp. 257–266, 2015.

- Liao et al. (2007) Liao, Xuejun, Li, Hui, and Carin, Lawrence. Quadratically gated mixture of experts for incomplete data classification. In Proceedings of the International Conference on Machine Learning, pp. 553–560. ACM, 2007.

- Little & Rubin (2014) Little, Roderick J. A. and Rubin, Donald B. Statistical analysis with missing data. John Wiley & Sons, 2014.

- Mahbub et al. (2016) Mahbub, Upal, Patel, Vishal M, Chandra, Deepak, Barbello, Brandon, and Chellappa, Rama. Partial face detection for continuous authentication. In Image Processing (ICIP), 2016 IEEE International Conference on, pp. 2991–2995. IEEE, 2016.

- McKnight et al. (2007) McKnight, Patrick E, McKnight, Katherine M, Sidani, Souraya, and Figueredo, Aurelio Jose. Missing data: A gentle introduction. Guilford Press, 2007.

- Petersen et al. (2008) Petersen, Kaare Brandt, Pedersen, Michael Syskind, et al. The matrix cookbook. Technical University of Denmark, 7:15, 2008.

- Schafer (1997) Schafer, Joseph L. Analysis of incomplete multivariate data. CRC Press, 1997.

- Shivaswamy et al. (2006) Shivaswamy, Pannagadatta K, Bhattacharyya, Chiranjib, and Smola, Alexander J. Second order cone programming approaches for handling missing and uncertain data. Journal of Machine Learning Research, 7:1283–1314, 2006.

- Smola et al. (2005) Smola, Alexander J, Vishwanathan, SVN, and Hofmann, Thomas. Kernel methods for missing variables. In Proceedings of the International Conference on Artificial Intelligence and Statistics. Citeseer, 2005.

- Stahura & Bajorath (2004) Stahura, Florence L and Bajorath, Jurgen. Virtual screening methods that complement HTS. Combinatorial Chemistry & High Throughput Screening, 7(4):259–269, 2004.

- Williams & Carin (2005) Williams, David and Carin, Lawrence. Analytical kernel matrix completion with incomplete multi-view data. In Proceedings of the ICML Workshop on Learning With Multiple Views, 2005.

- Williams et al. (2005) Williams, David, Liao, Xuejun, Xue, Ya, and Carin, Lawrence. Incomplete-data classification using logistic regression. In Proceedings of the International Conference on Machine Learning, pp. 972–979. ACM, 2005.