The Markowitz Category

Abstract

We give an algebraic definition of a Markowitz market and classify markets up to isomorphism. Given this classification, the theory of portfolio optimization in Markowitz markets without short selling constraints becomes trivial. Conversely, this classification shows that, up to isomorphism, there is little that can be said about a Markowitz market that is not already detected by the theory of portfolio optimization. In particular, if one seeks to develop a simplified low-dimensional model of a large financial market using mean–variance analysis alone, the resulting model can be at most two-dimensional.

Introduction

When developing financial models there is a tension between the desire to capture the complexity of financial markets, and the need to simplify, both for for tractability and to avoid over-fitting. This leads one to consider the question of how best to produce low-dimensional approximations to high-dimensional financial models. As an example of such a dimensional reduction, consider the celebrated one and two mutual fund theorems Merton (\APACyear1972). These build on the work of Markowitz in Markowitz (\APACyear1952) and tell us that, in the Markowitz market model with no restrictions on short selling, an investor who is only interested in the optimal investment problems can safely ignore all but a two-dimensional subspace of the space of portfolios.

This paper considers what can happen if one’s interests are more broad-ranging than just the classical optimal investment problem of Markowitz. Are there other low-dimensional subspaces of the Markowitz market model that may be of particular interest to other market players? We will prove that, in a clearly defined sense, the answer to this question is no. Moreover, in the same clearly defined sense, the two mutual fund theorem says all that there is to say about the market. The key, of course, is to give a rigorous explanation of what we mean by this “clearly defined sense”. This is where we use a little category theory.

Category theory, introduced in Eilenberg \BBA MacLane (\APACyear1945), formalises the common practice of mathematicians to investigate categories of object up to some notion of equivalence or isomorphism. For example, one might attempt to classify vector spaces up to bijective linear transformation or finite groups up to group isomorphism. The advantage of this approach is that spurious details are ignored. For example the specific set underlying the vector space or the group are irrelevant to their classification up to isomorphism.

Following a similar pattern, in Section 1 we will define a class of objects called Markowitz markets and define a notion of a Markowitz isomorphism between markets. Briefly, a Markowitz market is a vector space of possible investment portfolios equipped with: a linear functional that gives the cost of each portfolio; a linear function giving the expected payoff of each portfolio; and a symmetric bilinear form that measures the covariance of two portfolios. An isomoprhism is a map that preserves these structures.

By defining the notion of isomorphism we formally define what we consider to be a financially meaningful feature of a Markowitz market, and what we consider to be spurious information. A financially meaningful property should be preserved by isomorphisms. For example the name of a specific stock is not financially meaningful and our notion of isomorphism reflects this.

We note that this notion of isomorphism presupposes that risk can be measured adequately by standard deviation. As is well known, there are good reasons for considering other risk-measures, in which case one would require more data to define the market and one would have a different notion of isomorphism. Note, while our theory is predicated on the use of standard deviation to measure risk, it is not dependent upon the distribution of returns. In particular the normal distribution will not play a role in our theory.

Having identified the notion of isomorphism, we then classify all arbitrage-free Markowitz markets up to Markowitz isomorphism in Theorem 1.9. This is the central result of this paper. The proof only requires elementary linear algebra and can be given without considering portfolio optimization at all.

In Section 2 we will show how our classification of Markowitz markets can be applied to the study of portfolio optimization. We will see that classical results such as the mutual fund theorems are immediately obvious corollaries of our classification. Moreover, we will observe a close relation between risk-return diagrams and the classification of markets. For example, we will see that two markets of the same dimension and containing no spurious portfolios of zero cost, zero risk and zero expected payoff are isomorphic if and only if they have the same efficient frontier.

As we shall see, the category theory approach to the problem is in many ways more general and more illuminating than the classical approach of Merton (\APACyear1972). The classical approach is based on direct calculation and the theory of Lagrange multipliers, while we geometric arguments based on the Gram–Schmidt process. Readers who wish to compare our presentation with the more standard presentations in terms of returns and portfolio weights should consult Appendix A where we describe in detail there how to translate between the two approaches and give a numerical example.

We will show how our geometric approach can often be generalized to situations where invariance under Markowitz isomorphisms is broken by choosing another appropriate category. For example, when considering the performance of an individual portfolio relative to the market one should only consider isomorphisms that preserve this portfolio. To use the jargon of category theory jargon, one is interested in the “pointed category” of Markowitz markets with a marked portfolio of cost . This category is classified in Theorem 2.6. This theorem explains why risk-return diagrams such as Figure 1 are such an effective tool for understanding this problem. It is interesting to note that when considering optimal hedging, as is done in Sharpe \BBA Tint (\APACyear1990), one again seeks a classification of markets with a marked portfolio (this time the asset to be hedged defines the marked portfolio). A priori, one might imagine that analysing the performance of a portfolio is a very different problem from the analysis of hedging a portfolio, yet both problems can be understood using the same classification theorem.

Another generalization we consider is a market with two marked portfolios. This problem naturally occurs in the Capital Asset Pricing Model (CAPM) (as described in, for example, Jensen \BOthers. (\APACyear1972) and originally developed in Treynor (\APACyear1961); Sharpe (\APACyear1964); Lintner (\APACyear1965); Mossin (\APACyear1966)) . We will show how this theory can be understood via an appropriate classification theorem, in this case Theorem 2.7. The approach can be generalized further to include many classical generalizations of CAPM or to derive new results. For example, if one wishes to study the performance of different hedging portfolios using mean-variance analysis one is naturally lead to the question of classifying markets with yet more marked portfolios. Hence it would be straightforward to generalize the CAPM to obtain a model for evaluating the relative performance of hedging portfolios.

In Section 3 we show that our approach can be used to derive new financially significant results. We formally state and prove a mathematical version of our claim that there are no low-dimensional subspaces of a high dimensional market model that are of special interest to particular market players other than those given by the two mutual fund theorem. Our essential assumption in proving this result is that market players are only interested in markets up to Markowitz isomorphism. Our claim will then follow from our classification theorem together with some very general ideas derived from category theory, which we summarize in Section 3.1.

As a concrete and financially relevant example, consider the practice of applying principal component analysis to the correlation matrix in order to identify interesting subspaces of a market model. This allows one to identify higher dimensional subspaces of a financial model, but at the expense of breaking invariance up to Markowitz isomorphism. Principal component analysis of the correlation matrix can be justified if one believes that the financial properties of a single stock and of a basket of stocks are fundamentally different. For example, if one seeks to find specific stocks reflect the market as accurately as possible, Markowitz invariance is broken and principal component analysis may be a useful tool. On the other hand, if one seeks to choose a small number of individual stocks that represent the market as accurately as possible, one cannot go beyond the two mutual fund theorem.

We give two further examples of how our result can be applied in Section 3. Specifically in Section 3.2 we consider the important problem of estimating the expected return using historic data and the resultant model uncertainty. This problem has been studied extensively (see for example, Black \BBA Litterman (\APACyear1992), Garlappi \BOthers. (\APACyear2006), Jorion (\APACyear1986), Ceria \BBA Stubbs (\APACyear2006)). In Section 3.3 we then consider the problem of designing a mutual fund to attract investors with existing liabilities. In the case where the potential investor’s liability is known this problem has been studied before in Sharpe \BBA Tint (\APACyear1990), but we will consider the case where the potential investor’s liability is unknown. For both the problem of model uncertainty and the problem of investor’s with existing, but unknown, liabilities, our result shows that one cannot identify interesting portfolios beyond those identified by the two mutual fund theorem without supplying additional data.

Finally, we note that although we have chosen to phrase our results in terms of financial markets, we observe in Remark 1.12 that our results also yield a classification for linear stochastic differential equations. Thus one should expect theorems analogous to the two mutual fund theorem to be ubiquitous in the study of linear stochastic differential equations and hence in the study of the short time behaviour of stochastic differential equations in general.

1 The Markowitz Category

We begin with a formal definition of our category of markets. We will then describe how these markets arise in finance. We then prove a classification theorem for these markets.

Definition 1.1.

A Markowitz market consists of a finite dimensional real vector space together with the data:

-

(i)

A symmetric bilinear map satisfying for all ;

-

(ii)

Two linear functionals and .

Definition 1.2.

A Markowitz morphism between two Markowitz markets and is a linear transformation which satisfies:

| (1) |

| (2) |

| (3) |

Two Markowitz markets are said to be isomorphic if there is a bijective Markowitz morphism from one to the other.

Together our definition of markets and their morphisms defines what is called a category. Other examples of categories include: vector spaces and their linear transformations; topological spaces and their continuous maps; groups and their homomorphisms. We will review some essential definitions from category theory, including the definition of a category, in Section 3.1. Until then we will not need to use any category theory explicitly.

Markowitz markets naturally arise in finance.

Consider a trader who buys and sells financial assets. The trader is interested in studying portfolios made up from these assets. A portfolio is defined by knowing the vector in that contains the quantity of each asset held. The abstract vector space in our definition of a Markowitz market represents the space of possible portfolios. A portfolio may contain a negative quantity of a particular asset, this is interpreted financially by saying that a trader may choose to buy assets (a positive quantity) or borrow them (a negative quantity).

In this financial setting, the linear functional computes the initial cost of setting up a portfolio. If we assume the market is infinitely liquid and that unlimited amounts of each asset can be bought and sold it is reasonable to assume that the cost is indeed linear.

The trader models the financial assets as random variables. The linear functional computes the expected payoff of the portfolio at some future time . Infinite liquidity and infinite market depth justify the assumption that is linear. The symmetric bilinear map computes the covariance of the two portfolios at the future time . Note that here we are assuming that all the assets have finite variance.

The quantity , (the standard deviation of ), should be thought of as the risk of a portfolio . There is an extensive literature on risk measurement and numerous statistical quantities have been proposed that can be used to measure the risk of a portfolio. We will not debate the pros and cons of different risk measures here, we simply state that, in the Markowitz framework, risk is measured using standard deviation.

To justify the definition of a Markowitz morphism we assume that the trader is only interested in the portfolios that are available, their costs, payoffs and risk measured using the standard deviation. The trader sees all other market data as extraneous. In particular the trader is unconcerned by the question of how many assets are combined to produce a portfolio.

Our aim now is to classify Markowitz markets up to isomorphism. This is an elementary exercise in linear algebra. To reduce the number of cases in our classification, we will only classify arbitrage-free markets. These are defined as follows.

Definition 1.3.

A Markowitz arbitrage portfolio is a portfolio satisfying , and . A Markowitz market is arbitrage-free if it does not contain any Markowitz arbitrage portfolios.

If we were to choose a probability model for the asset payoffs compatible with and then we would define a classical arbitrage to be a portfolio of zero cost which has an almost surely non-negative payoff and a positive probability of a positive payoff. A Markowitz arbitrage is always a classical arbitrage, but the converse does not hold. Given any values for the expected payoff and for the variance we can always find a probability distribution with mean and variance which takes positive and negative values with positive probabilities (for example a normal distribution). Hence a Markowitz market is arbitrage-free as defined above if and only if it contains no classical arbitrages whatever compatible probability model is chosen for the payoff distribution. This justifies the use of the term arbitrage-free in our definition of an arbitrage-free Markowitz market.

Definition 1.4.

A portfolio is said to be risk-free if . A portfolio is said to be costless if . A portfolio is said to be valueless if , and .

Lemma 1.5.

If is a Markowitz morphism between and ( then

Proof.

This follows immediately from the polarization identity for symmetric bilinear maps:

| (4) |

This shows that the entire covariance structure can be deduced from knowing the standard deviation . ∎

Lemma 1.6.

Define the linear map by then the set of risk-free portfolios, , is equal to .

Proof.

If then . So .

On the other hand, if then the function has a local minimum at . So the derivative of in any direction is equal to zero. This derivative is equal to . So . ∎

Corollary 1.7.

If we have a decomposition for some vector subspace then the value of on is determined by its value on .

Proof.

If a portfolio satisfies , and then either or will be a Markowitz arbitrage portfolio. So a Markowitz market is arbitrage-free if and only if all costless, risk-free portfolios are valueless. This yields the following result:

Lemma 1.8 (Classification of arbitrage-free riskless markets).

In an arbitrage-free Markowitz market, we can write where is zero or one dimensional. If is one dimensional it is spanned by a single portfolio of cost . on .

We are now ready to state and prove our main mathematical result which is to give a canonical form for all arbitrage-free Markowitz markets.

The canonical forms will be expressed in terms of of the vector space . We will write the bilinear map on as an matrix such that

We will write the linear functionals and as co-vectors. We will write the matrices in block diagonal form and will use the notation for the identity matrix and will use for matrices of zeros whose dimensions can be deduced from the context.

Theorem 1.9.

We have the following classification of Markowitz markets.

-

(a)

The case .

Let be given. Given four parameters which do not lie in the set

(5) we can define an isomorphism class of Markowitz markets, , as follows:

-

(i)

If , is the isomorphism class of the market with

-

(ii)

If , is the isomorphism class of the market with

Note that when the parameter is ignored. We have chosen our coordinates and for the isomorphism classes so that these variables will have simple geometric and financial explanations. This justifies the apparently unnecessary complexity of using and in the formulae.

Any arbitrage-free Markowitz market of dimension with belongs to one of these isomorphism classes. The isomorphism classes are distinct except that

(6) -

(i)

-

(b)

The case .

Any arbitrage-free Markowitz market of dimension with identically zero is Markowitz isomorphic to the market with

where is a uniquely determined integer between and . if but otherwise, is a uniquely determined element of .

Proof.

We first assume that . Case (i) and (ii) can be distinguished in an invariant fashion since there is a risk-free portfolio with in case (i) but not in case (ii). Let us show that conversely if there is such a portfolio we can find a basis such that the market takes the form of case (i), and if not, it takes the form in case (ii).

-

(i)

We suppose that a risk-free portfolio with non-zero cost, , exists. Take and take . Take to be a basis for . By Lemma 1.8, is equal to on . Extend to a basis for . Let be the span of . Then restricted to gives an inner product, so by applying the Gram–Schmidt process we can find an orthonormal basis for restricted to . The inner product on gives a duality isomorphism from to . Let denote the vector in that is dual to the functional via this isomorphism. By applying an isometry of the Euclidean space if necessary, we may assume that is a non-negative multiple of . When one writes , and with respect to the basis we see from Corollary 1.7 that they take the desired form.

Given that the market is of this form, can be invariantly defined as the expected payoff of a riskless portfolio of cost . In the same circumstances, can be invariantly defined as the maximum value of among costless portfolios with . It follows that and are uniquely determined.

-

(ii)

We suppose that all risk-free portfolios have cost zero. Take . Let be a basis for . Extend this to get a basis for . Let denote the span of the . It is an inner product space with respect to , so by applying the Gram-Schmidt process we can obtain a basis for with the orthonormal. By applying an isometry of if necessary, we may assume that the vector dual to via the inner product on is a positive multiple of . By applying a further isometry of the space spanned by , we may assume that the vector dual to via the inner product on lies in the span of and . Writing the market with respect to this basis now puts it into the desired form.

Given that the market is of this form, can be defined invariantly as over the maximum cost of any portfolio with . Define invariantly as the payoff of a portfolio with that maximizes the cost. Now can be defined invariantly by . can be defined invariantly as the maximum expected payoff of any costless portfolio with .

The proof for the case when is similar. ∎

To avoid considering financially-uninteresting special cases in the sequel we make the following definition.

Definition 1.10.

A Markowitz market is non-degenerate if:

-

(i)

The market is arbitrage-free;

-

(ii)

There are no valueless portfolios;

-

(iii)

and are linearly independent.

It follows from our theorem that all non-degenerate Markowitz markets of dimension are of the form or with and .

We have identified the set of non-degenerate Markowitz markets up to isomorphism. We now ask what is the topology of this space?

For a fixed underlying vector space, we can choose an isomorphism to . The space of bilinear forms on can then be viewed as a subspace of and so can be given a topology. We can then give the space of Markowitz markets on a topology. This topology doesn’t depend upon the choice of isomorphism from to . Thus the space of Markowitz markets has a natural topology. The moduli space of Markowitz markets is defined to be the quotient of the space of Markowitz markets by the equivalence relation given by Markowitz isomorphisms.

With this terminology established we may now prove the following corollary of Theorem 1.9.

Corollary 1.11.

The moduli space of non-degenerate Markowitz markets of dimension is homeomorphic to the manifold with boundary . In particular, the map given by is a homeomorphism. Here is equal to if and equal to otherwise.

Proof.

It follows from Theorem 1.9 that is a bijection.

Define to be the market given in matrix form by

is continuous. The market is Markowitz isomorphic to . Therefore is continuous.

We can invariantly and continuously associate a non-degenerate bilinear form with a non-degenerate Markowitz market by defining

To any non-degenerate bilinear form on a finite dimensional vector space, there is an associated isomorphism between the vector space and its dual. This isomorphism is associated continuously. Thus we can continuously and invariantly associate a bilinear form acting on with any non-degenerate Markowitz market. We will write for this form.

A short calculation shows that in both cases (i) and (ii) of Theorem 1.9 we have . Therefore

Thus the function defined on the moduli space of non-degenerate markets is continuous. We calculate similarly that and . Thus , and are continuous functions on the moduli space of non-degenerate Markowitz markets. Hence is continuous. ∎

Remark 1.12.

We have called our algebraic structure a Markowitz market to emphasize its financial relevance. However, this same structure occurs naturally in the abstract setting of linear stochastic differential equations. Let be a stochastic process in an -dimensional vector space determined by a linear stochastic differential equation driven by -dimensional Brownian motion with initial condition given by a known value for . In coordinates we may write:

for constants and . We will say that two such processes and are equivalent if there exists an isomorphism of such that in distribution. We may associate a Markowitz market to an SDE by taking the vector space and defining forms , and as follows:

where denotes the quadratic covariation of two processes and . Note that the definitions of and are independent of the choice of . As is clear from our coordinate free definitions for , and , these forms are defined independently of the choice of basis for . It is easy to see that we have established a one-to-one correspondence between Markowitz markets and linear stochastic differential equations. Thus our theorems can be interpreted as giving a partial classification of linear stochastic differential equations up to linear transformation. We say that this is a partial classification since in this more general context, the “arbitrage-free” assumption may no longer be very natural and one should consider additional cases. We do not explore this further in this paper as our focus is on financial applications.

2 Portfolio Optimization

Armed with our classification theorem, the study of portfolio optimization in Markowitz markets becomes entirely trivial.

Definition 2.1.

Given a Markowitz market, a portfolio is said to be risk minimizing if its risk is equal to the minimum risk among all portfolios, , with and .

Theorem 2.2 (Two mutual-fund theorem).

In a non-degenerate Markowitz market with no risk-free portfolios, the set of risk-minimizing portfolios is a vector subspace of of dimension at most . Moreover, for any feasible payoff and cost there is an associated risk-minimizing portfolio. This is called the two mutual-fund theorem because the space of risk-minimizing portfolios can spanned by two portfolios, these are the “mutual-funds”.

Proof.

Since there are no non-zero risk-free portfolios, we are in case (ii) of our classification, Theorem 1.9. In this case, our vector space is Euclidean space with risk measured by distance, making the result geometrically obvious. We give a few formal details for completeness.

Two portfolios and have the same cost and expected payoff if and only if their first two components are equal. The risk is equal to the sum of the squares of the components, and hence is minimized by taking all components other than the first two equal to zero. Hence the space of risk-minimizing portfolios is the vector space spanned by the standard basis vectors . ∎

Theorem 2.3 (One mutual-fund theorem).

In a non-degenerate Markowitz market with a risk-free portfolio the set of risk-minimizing portfolios is a vector subspace of of dimension at most and contains the risk-free portfolio. For any feasible payoff and cost there is an associated risk-minimizing portfolio. This is called the one mutual-fund theorem because the space of risk-minimizing portfolios can spanned by one arbitrary portfolio and a risk-free portfolio.

Proof.

An obvious consequence of case (i) of Theorem 1.9 ∎

We have not yet used the concept of return of a portfolio. In standard treatments of Markowitz’s theory it is usual to rescale investment problems in terms of the initial cost of a portfolio. This rescaling function is non-linear and not even defined for portfolios of zero cost. It often seems to unnecessarily complicate the discussion. For example, we have stated the mutual-fund theorems in terms of vector spaces which we believe makes them much easier to understand than conventional presentations.

However, the idea that one might be able to rescale and transform a market to simplify it is central to our discussion; it is simply that returns are the “wrong” rescaling. We have observed that the covariance structure defines a natural length scale for the problem and have transformed our coordinates ao that this becomes the standard Euclidean metric. This transformation has the advantage of being linear. This observation is generally useful throughout probability theory: covariance matrices define natural length scales.

Definition 2.4.

The expected return of a portfolio, with non-zero cost is given by

| (7) |

The relative risk of such a portfolio is given by

Let map the set to by . The image of is called the feasible set. The image of the set of risk-minimizing portfolios is called the efficient frontier. The shape of the efficient frontier was identified in Merton (\APACyear1972).

Theorem 2.5.

In a non-degenerate Markowitz market, with , the efficient frontier consists of the points with and

| (8) |

When , the feasible set is equal to the efficient frontier. When , the feasible set is the set of all points on, or to the right of, the efficient frontier.

Proof.

We consider first case (ii) of Theorem 1.9 when . Because of the scaling by cost in the definition of and we see that we need only consider the image of portfolios of cost .

An efficient portfolio with cost takes the form for some . It is mapped to:

We can compute from either the -coordinate or -coordinate of . Equating these expressions gives the expression (8). Since we see that the -coordinate of can take any real value, so the efficient frontier is the right arm of the hyperbola satisfying (8).

If all portfolios are efficient. If , the portfolio is mapped by to

So an y point to the right of the efficient frontier is feasible.

The efficient frontier and feasible set are similarly easy to calculate in case (i) of Theorem 1.9. ∎

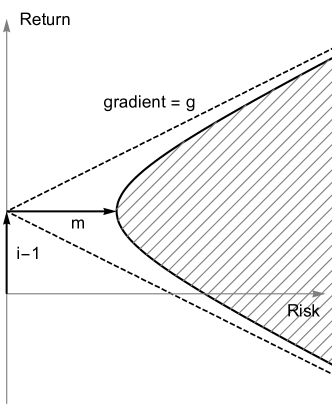

The feasible set and the efficient frontier are iconic images of Markowitz’s theory. They are illustrated in Figure 1.

We now see the justification for our choice of parameter names for the space of Markowitz markets. The parameter measures the minimum risk of a portfolio of cost , the parameter measures the gradient of the asymptotes when or the slope of the lines that the hyperbola degenerates to when. The parameter corresponds to the intercept on the -axis where the asymptotes meet.

From our point of view, the importance of the feasible set and the efficient frontier is explained by the following result.

Theorem 2.6.

Let and be two non-degenerate Markowitz markets of dimension , Let and be portfolios in and repectively, each of cost 1. Then there exists a Markowitz isomorphism of and sending to if and only if the efficient frontiers of and are equal and .

Proof.

By assumption we are in either case (i) or case (ii) of Theorem 1.9. We are in case (ii) if and only if the efficient frontier is one arm of a hyperbola.

In case (ii), our explicit formula for the efficient frontier shows that , and can be recovered from its shape as shown in Figure 1.

After a rotation of the inner product space spanned by , any portfolio in of cost can be written as . The coefficient measures how far the image of under is to the right of the efficient frontier. The term identifies the point on the efficient frontier to the left of .

A similar argument can be applied in case (i). ∎

Theorem 2.6 classifies the pointed category of non-degenerate markets with a marked portfolio of cost . As we discussed in the introduction, this is the natural category to consider when comparing the peformance of a single portfolio to the market as a whole.

As another example of how our approach can be generalized, consider the problem of comparing the performance of two portfolios within a market. The natural category is the category of Markowitz markets with two marked portfolios of cost , which we will label and . We think of as being a market portfolio, perhaps a stock index such as the S&P 500, and being a specific portfolio whose performance we wish to evaluate. This situation can be understood by the following classification theorem.

Theorem 2.7.

Let and be two non-degenerate Markowitz markets of dimension with marked portfolios and in and and in respectively. All the marked portfolios are of cost 1. We also assume that none of these portfolios are risk-free. There exists a Markowitz isomorphism of and sending to and to if and only if the efficient frontiers of and are equal, , and .

Proof.

This is another geometrically obvious corollary of Theorem 1.9. ∎

Thus within any fixed market with a marked market portfolio the properties of a portfolio are determined entirely by and the quantity . Thus this theorem gives a geometric interpretation of the Capital Asset Pricing Model and explains the central role of in this theory.

There is one feature of the market that is missed by risk-return diagrams, namely cost-free portfolios. These portfolios are not uninteresting. In our case (ii) the costless portfolio provides one natural choice of mutual fund to use in the two mutual fund theorem. Adding multiples of this fund to your portfolio allows one to arbitrarily change the risk and return along the efficient frontier without affecting the cost. This fund is a particularly useful and easy to understand financial instrument.

Cost-free portfolios are also likely to be of great interest to rogue traders and fraudsters. They will want to know that arbitrarily large expected returns can be achieved in a Markowitz market at zero cost! Let us classify cost-free portfolios for their benefit. We omit the proof.

Theorem 2.8.

Define by . The image of the cost-free, risk-minimizing portfolios under for the market with is the set with and

We call this set the efficient frontier for costless portfolios. The image of is either equal to the efficient frontier for costless portfolios or to the set of points on or to the right of the efficient frontier for costless portfolios.

There is an automorphism of the market mapping one costless portfolio to another if and only if they have the same image under .

Remark 2.9.

Let us see how our results can be applied beyond familiar portfolio optimization. In Remark 1.12 we noted that we have classified “arbitrage-free” linear stochastic differential equations up to weak equivalence. Thus two-mutual fund theorems should be expected when studying such equations. For example, consider the financial problem of optimizing expected utility when trading stocks that follow a multivariate Bachelier model (i.e. a linear stochastic differential equation). One sees from our invariance arguments that any meaningful solution to this problem will be a dynamic trading strategy in just two mutual funds. We say any “meaningful solution” as it is not entirely straightforward to give a mathematically rigorous formulation of this investment problem. Our point is that however this is done, invariance under Markowitz isomorphisms should be preserved, and this will result in some form of two mutual fund theorem.

3 Dimension reduction of Markowitz markets

Our clssification makes it easy to identify the interesting invariant subsets of the space of portfolios.

Theorem 3.1.

For non-degenerate markets of dimension containing no-valueless portfolios, any invariant submanifold of the market under the automorphism group has dimension less than or equal to or greater than or equal to . If then the invariant submanifolds of dimension less than or equal are all submanifolds of the set of risk-minimizing portfolios. Furthermore in such markets, any invariant portfolio is an element of the set of risk-minimizing portfolios.

Proof.

Any submanifold of the market which is closed under the automorphism group of the market must consist of orbits of the automorphism group acting on . As we have seen, excluding costless portfolios, these orbits consist of the pre-image of points of . The pre-image of the efficient frontier has dimension less than or equal to . The pre-image of any other point in the feasible set is greater than or equal to . We use the map to apply similar reasoning to the case of costless portfolios. It follows that invariant subspaces are of dimensions , , , , or . If , . So in this case all low-dimensional invariant submanifolds are in the pre-image of the efficient frontiers. This implies they lie inside the set of risk-minimizing portfolios.

The final assertion is obvious. ∎

This result can be interepreted as a significant generalization of the classical two mutual fund theorem. However, this interpretation of our result may seem obscure if the reader does not have a background in areas of pure mathematics such as geometry where invariance arguments are commonplace. We will therefore explain this interpretation of our result from a theoretical point of view in Section 3.1. We will then give a number of concrete financial applications: in Section 3.2 we show how our theorem can be applied to the question of optimization under uncertainty; in Section 3.3 we show how our theorem can be applied to the question of choosing optimal hedging portfolios.

3.1 Invariant definitions

There are two commonly used notions of invariance in mathematics. One such notion is invariance under a group action: if a group acts on a set one may ask which elements of the set are left unchanged by the group action. A second notion is independence of presentation where a mathematical property of an object only depends upon the isomorphism class of an object and not on any additional details used to describe the object. In this section we will formalize the latter notion in order to see how the two notions of invariance are related.

We begin by reviewing some fundamental definitions from category theory.

Definition 3.2.

A category consists of the following data:

-

(i)

a class of objects.

-

(ii)

a class of morphisms. To each morphism are associated a source and target . We write . is the class of all morphisms from to .

-

(iii)

for all a binary operation called composition. If , we write or just for the composition.

The composition satisfies

-

(i)

Associativity: If , ,

-

(ii)

Identity: For all there exists a morphism with the property that if , and if , .

For example, we have already defined the category of Markowitz markets whose objects consist of quadruples of Markowitz markets and whose morphisms consist of Markowitz morphisms. The underlying set associated to each market is the set of vectors. We will call this category .

Note that in this case, and indeed the other cases that will interest us, the morphisms can be interpreted as functions and the composition law is given by ordinary function composition.

Another such category is the category of all “small” sets. We must avoid talking about the set of all sets in order to avoid Russell’s paradox. To resolve this problem one chooses a sufficiently large set that will contain all the sets of interest to you and define a small set to be sets contained in this large set. The same technical device can be applied to other categories, so we will henceforth allow ourselves to talk about “all markets” when we should say “all small markets”.

Definition 3.3.

A functor from a category to a category is a mapping which

-

(i)

associates to each object an object in .

-

(ii)

associates to a morphism in a morphism in .

and which satisfies

-

(i)

For all ,

-

(ii)

If and then .

An obvious example of a functor is the identity map .

Another example is the “forgetful functor” which maps to the category of sets by mapping an object to the set of vectors in . This functor acts as the identity on the morphisms of .

As a more interesting example of a functor, consider the category of finite dimensional vector spaces with morphisms given by the invertible linear transformations between these vector spaces. We may then define a functor by , the dual of and for a morphism . We will denote this functor by .

We have now established all the concepts we need in order to define the notion of an “invariantly defined element”.

Definition 3.4.

Let be a category and let be a functor from to . Then an invariantly defined element for is a map

such that and (recall that in set theory the elements of sets are themselves set which is why the codomain of is even though we think of the values of primarily as elements rather than as sets).

If is a functor from category to category and if is a category whose morphisms are in fact transformations of a set, we will say that is an invariantly defined element for if it is an invariantly defined element for where is the forgetful functor.

In particular if an invariantly defined element for the identity functor on will be a map from a market to a portfolio in that market. So we will call this an invariantly defined portfolio. If we think of a morphism between two markets as a relabelling of the elements of the market, we see that an invariantly defined portfolio is a way of selecting a portfolio from any market that behaves correctly under relabellings. Thus our notion of an invariantly defined element captures the idea of “independence of presentation”.

The advantage of our category theory approach is that we can define more than just invariantly defined portfolios. For example an invariantly defined element for the functor will be called an invariantly defined linear functional. It is not hard to check that and are invariantly defined linear functionals.

We are now in a position to explain the relationship between invariance under a group action and independence of presentation.

Lemma 3.5 (Invariance Lemma).

Let be a category where every morphism is invertible. Let be a functor from to .

For each write for the set of morphisms with source and target equal to . forms a group under composition. It acts on the set with the action defined by

for and .

If is an invariantly defined element for then is invariant under .

Conversely, let be the subcategory consisting of objects isomorphic to and their isomorphisms and let be invariant under . The map given by:

| (9) |

for any is well-defined and gives an invariantly defined element for with .

Proof.

The definition of a category ensures that is a semi-group. Our assumption that every morphism in is invertible ensures that is a group.

That the action given is a group action, follows from the definition of a functor. In detail if and then:

and

If is an invariantly defined element of and then

Here we have used in sequence the definition of the group action, the definition of an invariantly defined element and the fact that . Thus is invariant under the action of .

By definition of , an isomorphism exists for any . Suppose too. Then . We see that

The first equality is immediate, we then use the functorality of and then we use the invariance of under . Thus the map defined by (9) is well-defined as claimed. Suppose then so

So is an invariantly defined element as claimed.

Finally note that

as claimed. ∎

A consequence of our invariance Lemma 3.5 when combined with Theorem 3.1 is that any invariantly defined portfolio must lie in the given two dimensional space. Since we believe that any financially interesting statement must be independent of the labelling of stocks and mutual funds in a Markowitz market, this implies that the portfolios that can be identified uniquely by some financially interesting question all lie in a two dimensional space. This gives us our claimed generalization of the two mutual fund theorem, stated in the precise language of invariantly defined elements.

However, this does seem at first to open a new problem, how can we tell if a given is invariantly defined? For example, if we fix constants and , is given by

| (10) |

invariantly defined? We would certainly expect that it is, as this is surely a financially meaningful problem. But how can we prove this without a tedious calculation?

To resolve this problem we note that we can mirror most of the basic constructions of set theory using functors. We will restrict our attention to the case when every morphism in our category is invertible.

For example given two functors and we can define a product category in the obvious way. This allows us to define the notion of an invariantly defined pair of elements.

Similarly if is a functor, since is permutation of we may define an action of on the power set . Hence we can define a power-set functor . This allows us to talk about invariantly defined sets of elements.

Since a function can be defined as a subset of a Cartesian product satisfying certain properties, we see that we can also talk about invariantly defined functions.

It is instructive to compute how we define a functor acting on functions in a little detail. Let and be two functors to categories and which are backed by sets. Write for each of the forgetful functors to . We wish to define a functor called derived from and . It will act on objects by

Given , we can view as a function in which case we write in the usual way. We may also view as a set in which case we have . The recipe above tells us how we should define the action of on morphisms . The quantity should be a new function which we can write explicitly as a subset of the Cartesian product:

We now translate this definition into conventional function notation.

So in conventional function notation

Note that our definition of the dual space functor which we defined earlier is simply a special case. Let us write for the identity functor on vector spaces. Let us write for the trivial functor which maps all vector spaces to and all morphisms to the identity. We see that .

In summary, we have shown that our definition of an invariantly defined element encompasses many of the basic notions of set theory. In particular we have shown how the notion of an invariantly defined function follows directly from the set-theoretic definition of a function.

It is easy to check that all the properties one might expect of invariantly defined sets hold. For example, the union, intersection, product and power set of invariantly defined sets are all invariantly defined. It follows from such basic set theoretic facts as this and the definition of a function as a set that the composition of invariant functions is invariant, the image of an invariant set by an invariant function is invariant and so forth.

There is one set theoretic construction, however, that is not necessarily invariantly defined. This is the act of making a choice. For example, if we simply choose a portfolio in every Markowitz market there is no reason to expect this to be invariantly defined.

We conclude that any mathematical operation applied to invariantly defined inputs will result in an invariantly defined output unless that operation involves making an arbitrary choice. This is a consequence of the fact that mathematics can be modelled using set theory.

As a concrete example, we see that defined in (10) is an invariantly defined portfolio as claimed. This is a consequence of the fact that all the inputs are invariantly defined. For example we have already remarked that and are invariantly defined. Indeed this is an immediate consequence of 3.5, as is the fact that is invariantly defined. The ordering defined on that is used by is also invariantly defined simply because the functor we are using to is trivial. For the same reason and are invariantly defined.

In short, very often quantities are manifestly invariantly defined because their definition does not involve choices.

Having said that, sometimes a quantity is invariantly defined without it being immediately obvious.

For example, consider the measure on a Markowitz market defined as follows: First choose an -orthonormal basis and hence define an inner product space isomorphism from ; define the measure of a subset of to be the Lebesgue measure of . This definition apparently depends upon the choice of the orthonormal basis and so is not manifestly invariantly defined. However, the determinant of an orthogonal transformation is always and so we see that this measure is in fact defined independently of the choice of basis. We have called the measure as it only depends upon .

Once we have established that a quantity is invariantly defined, we may use it to define other invariantly defined quantities. For example we may define the standard Gaussian measure on by

here is the dimension of the vector space which is invariantly defined by undergraduate linear algebra. We conclude that the standard Gaussian measure is invariantly defined. We will use the measure and the standard Gaussian measure to define other more complex invariant objects in Section 3.2 below.

Remark 3.6.

If the reader is already familiar with category theory, they may wonder whether invariantly defined elements can be interpreted as natural transformations (see Eilenberg \BBA MacLane (\APACyear1945) for a definition of a natural transformations). To see how this can be done, let be an invariantly defined element for a functor . Let be the functor mapping every object in to and every morphism in to the identity. For each , define a function by . Then is a natural transformation from to .

3.2 Optimization under uncertainty

We will now show how the the theory of Section 3.1 can be applied to give a concrete financial application of Theorem 3.1.

It has been observed that the portfolios identified by Markowitz’s theory are often badly behaved in practice. For example in Black \BBA Litterman (\APACyear1992), Black and Litterman observe that these “almost always ordain large short positions in many assets” and they cite Green \BBA Hollifield (\APACyear1992) and Best \BBA Grauer (\APACyear1991) as academic references on the types of problems that are experienced.

One source of these problems with Markowitz’s theory is the difficulty of estimating expected returns. One approach to selecting the expected return vector is to use expert knowledge, but in the absence of this specialist knowledge one might estimate expected returns using historical returns. We will refer to the Markowitz market obtained from the historic mean and covariance combined with current prices as the historic Markowitz model. However, as discussed in the references above, it has been found that the historic Markowitz model performs poorly in practice.

One tempting approach to resolving this problem is to consider model uncertainty. Any statistical measure of the historic returns will have some uncertainty and this should be incorporated into the optimization problem. Both the expected returns and the covariance matrix of returns will be difficult to estimate from historic data. There are many approaches to optimization under uncertainty and many of these have been applied to this investment problem. For example, in Jorion (\APACyear1986) a Bayesian approach is used, in Ceria \BBA Stubbs (\APACyear2006) a robust optimization approach is followed, and Garlappi \BOthers. (\APACyear2006) uses an approach based on the multi-prior model of decision making.

For all of these approaches one must make some additional modelling decisions, but in each case there is a natural choice of how to do this based on the data of the historic Markowitz model.

Let us give a concrete example. In a robust optimization approach one needs to choose a set, , of possible probability distributions for asset payoffs. One might decide to choose as the set of Gaussian distributions which are within a certain Hellinger distance, of the standard Gaussian measure arising in the historic Markowitz model (see Ay \BOthers. (\APACyear2015) for a definition of the Hellinger metric). One can think of the Hellinger distance as a measure of the statistical dissimilarity of two distributions.

Let us write for covariance form defined by a probability distribution and for the expected payoff associated with . A typical robust optimization problem would be to find

| (11) |

for a chosen value of a risk-aversion parameter and portfolio cost .

Despite the complexity of this set-up, we see that the problem is invariant under Markowitz isomorphisms. The key step is to note that is invariantly defined. To see this first recall that the Hellinger metric is invariantly defined on the space of measures on a finite dimensional real vector space, even if we forget the extra structure of , and . The Gaussian measure is invariantly defined. The set of measures which are Gaussian can be invariantly defined using only the reference measure . Thus is invariantly defined and hence the set defined by (11) is also invariantly defined.

Hence if this problem does have a unique solution, that solution must be a weighted sum of the portfolios identified by the two mutual fund theorem.

We need not restrict ourselves to using the Hellinger metric to find invariantly defined sets like . There are many metrics and divergences defined on the space of distributions such as the metrics, the Wasserstein metric and the Kullback–Leibler divergence (again see Ay \BOthers. (\APACyear2015) for the necessary definitions). All of these are invariantly defined using only the structure . Thus we may repeat our analysis using any of these methods of defining and we will obtain the same result.

Similarly, as predicted by our theory the invariant multi-prior problem described in Section 2.2.3 of Garlappi \BOthers. (\APACyear2006) and the invariant Bayesian problem described in Section 3.3 of Garlappi \BOthers. (\APACyear2006) also identify linear combinations of the portfolios coming from the two mutual fund theorem.

These examples illustrate the general principle implied by Theorem 3.1 that the observed problems with the historic Markowitz model cannot be fixed by simply using more advanced optimization concepts. One also requires extra data. Indeed the approaches of Black \BBA Litterman (\APACyear1992), Garlappi \BOthers. (\APACyear2006), Jorion (\APACyear1986) and Ceria \BBA Stubbs (\APACyear2006) all suggest additional data that could be incorporated into the optimization problem in order to identify alternative portfolios.

3.3 Optimal hedging

We give a second financial application of Theorem 3.1.

Suppose that a fund manager has already created two investment funds according to the two mutual fund theorem targeting investors who currently have no liabilities. However, an investor with existing liabilities will have different risk preferences as they may be able to take advantage of hedging opportunities in the market. To attract such investors, the fund manager wishes to create one additional fund which can be used for hedging. Due to the overheads of fund management, the fund manager only wishes to create one additional fund. They ask what would be the optimal choice of hedging fund?

In lieu of any data on the existing liabilities of potential investors, they assume that the potential investors have been investing in the stock market previously to build up their liability and were using an optimal investment strategy based on their own estimates the payoff functional . Thus they speculate that the potential investors will have liabilities that are normally distributed around one of the risk-minimizing portfolios found in Theorem 2.2 with covariance given by the bilinear form . As we saw in the previous example, there are many notions of optimality one could now use to define an optimal hedging fund. However, as before any reasonable definition of an optimal hedging fund will be invariant under Markowitz morphisms.

Without loss of generality, the fund manager can also ensure that the fund is independent of their existing funds and is scaled so that purchasing unit of the fund has a cost of . All funds satisfying these last two properties are isomorphic under Markowitz morphisms. Hence whatever notion of optimality the fund manager decides to employ, if it is Markowitz invariant it will fail to identify any optimal hedging fund. Hence it is impossible to identify such an optimal hedging fund without supplying more data.

Acknowledgements

This paper emerged from discussions with Teemu Pennanen and Matthew Glover. It has also benefited from the comments and suggestions of Damiano Brigo and Umut Cetin, and from discussions with James Newton and Ashwin Iyengar.

Appendix A Relationship with the matrix formulation of portfolio optimization

For the reader’s convenience we describe in detail how to translate between standard presentations of Markowitz’s theory and our account. We will use boldface to indicate vectors in and the standard font weight to represent abstract vectors.

Associated to a vector we have its concrete realisation . The -th component of indicates the quantity of asset that is held in the portfolio . We will use boldface and for the row vectors defined by requiring and respectively. We similarly write boldface for the symmetric matrix defined by requiring .

Let be the diagonal matrix with -th entry given by

where is -th component of . We define the porfolio weights, , of a portfolio of non-zero cost by

The sum of the components of is then always equal to . We may write this condition as where boldface is the row vector consisting of ones.

From (7), the expected return can be computed from and satisfies

| (12) |

where is the vector whose -th component is the expected return of asset . The relative risk similarly satisfies

| (13) |

where is the covariance matrix of returns.

Given a non-zero initial cost we can use the mapping to translate between the classical Markowitz optimization problem

and the problem

which we solved in Theorem 2.2. In the classical Markowitz problem with no risk-free asset, one assumes that , and hence , is positive definite. This puts us in case (ii) of Theorem 1.9 with .

To show how our approach compares to the classical approach of Lagrange multipliers we now give a numerical example of the computation of the set of risk-minimizing portfolios and the isomorphism class following a geometric approach. This can be compared with Zivot (\APACyear2013) which performs similar calculations numerically using the Lagrange multiplier approach.

Following Zivot (\APACyear2013), we now suppose that we are given numeric values for the vector of expected returns on each asset and the associated covariance matrix as follows:

In the classical formulation of the Markowitz problem used in Zivot (\APACyear2013), the cost vector is not specified. So we are free to assume that the price of the assets are scaled such that the price of one unit of the asset is equal to . This implies that and so is the identity matrix. Thus from (12) we must take and from (13), .

We begin by identifying the duals and of and with respect to . The dual, of a functional with respect to is defined by the requirement

Hence if denotes the row vector associated with we have

Hence the dual of satisfies

For our concrete example we compute that

We note that it follows immediately from our classification theorem that the space of risk-minimizing portfolios (see Definition 2.1) is spanned by these two vectors. We can also identify the portfolio weights that minimize risk irrespective of the payoff. They are given by

This matches the value obtained using Lagrange multipliers in Zivot (\APACyear2013).

Applying the Gram-Schmidt process to the basis we obtain the -orthonormal vectors

This completely determines an isomorphism of the form given in Theorem 1.9. In practice one would only apply the Gram-Schmidt process to the pair of vectors as that is sufficient to identify the vectors and , and hence the isomorphism class of the market. To identify the isomorphism class we simply solve the equations

In this case we find

As one would expect these values match the ones that can be read off from the plot of the efficient frontier in Figure 1.3 of Zivot (\APACyear2013) using our own Figure 1.

References

- Ay \BOthers. (\APACyear2015) \APACinsertmetastarayJost{APACrefauthors}Ay, N., Jost, J., Vân Lê, H.\BCBL \BBA Schwachhöfer, L. \APACrefYearMonthDay2015. \BBOQ\APACrefatitleInformation geometry and sufficient statistics Information geometry and sufficient statistics.\BBCQ \APACjournalVolNumPagesProbability Theory and Related Fields1621-2327–364. \PrintBackRefs\CurrentBib

- Best \BBA Grauer (\APACyear1991) \APACinsertmetastarbestGrauer{APACrefauthors}Best, M\BPBIJ.\BCBT \BBA Grauer, R\BPBIR. \APACrefYearMonthDay1991. \BBOQ\APACrefatitleOn the sensitivity of mean-variance-efficient portfolios to changes in asset means: some analytical and computational results On the sensitivity of mean-variance-efficient portfolios to changes in asset means: some analytical and computational results.\BBCQ \APACjournalVolNumPagesThe review of financial studies42315–342. \PrintBackRefs\CurrentBib

- Black \BBA Litterman (\APACyear1992) \APACinsertmetastarblackLitterman{APACrefauthors}Black, F.\BCBT \BBA Litterman, R. \APACrefYearMonthDay1992. \BBOQ\APACrefatitleGlobal portfolio optimization Global portfolio optimization.\BBCQ \APACjournalVolNumPagesFinancial Analysts Journal48528–43. \PrintBackRefs\CurrentBib

- Ceria \BBA Stubbs (\APACyear2006) \APACinsertmetastarceriaStubbs{APACrefauthors}Ceria, S.\BCBT \BBA Stubbs, R\BPBIA. \APACrefYearMonthDay2006. \BBOQ\APACrefatitleIncorporating estimation errors into portfolio selection: Robust portfolio construction Incorporating estimation errors into portfolio selection: Robust portfolio construction.\BBCQ \APACjournalVolNumPagesJournal of Asset Management72109–127. \PrintBackRefs\CurrentBib

- Eilenberg \BBA MacLane (\APACyear1945) \APACinsertmetastareilenbergmaclane{APACrefauthors}Eilenberg, S.\BCBT \BBA MacLane, S. \APACrefYearMonthDay1945. \BBOQ\APACrefatitleGeneral theory of natural equivalences General theory of natural equivalences.\BBCQ \APACjournalVolNumPagesTransactions of the American Mathematical Society582231–294. \PrintBackRefs\CurrentBib

- Garlappi \BOthers. (\APACyear2006) \APACinsertmetastargarlappiUppalWang{APACrefauthors}Garlappi, L., Uppal, R.\BCBL \BBA Wang, T. \APACrefYearMonthDay2006. \BBOQ\APACrefatitlePortfolio selection with parameter and model uncertainty: A multi-prior approach Portfolio selection with parameter and model uncertainty: A multi-prior approach.\BBCQ \APACjournalVolNumPagesThe Review of Financial Studies20141–81. \PrintBackRefs\CurrentBib

- Green \BBA Hollifield (\APACyear1992) \APACinsertmetastargreenHollifield{APACrefauthors}Green, R\BPBIC.\BCBT \BBA Hollifield, B. \APACrefYearMonthDay1992. \BBOQ\APACrefatitleWhen Will Mean-Variance Efficient Portfolios Be Well Diversified? When will mean-variance efficient portfolios be well diversified?\BBCQ \APACjournalVolNumPagesThe Journal of Finance4751785–1809. \PrintBackRefs\CurrentBib

- Jensen \BOthers. (\APACyear1972) \APACinsertmetastarjensen{APACrefauthors}Jensen, M\BPBIC., Black, F.\BCBL \BBA Scholes, M\BPBIS. \APACrefYearMonthDay1972. \BBOQ\APACrefatitleThe capital asset pricing model: Some empirical tests The capital asset pricing model: Some empirical tests.\BBCQ \PrintBackRefs\CurrentBib

- Jorion (\APACyear1986) \APACinsertmetastarjorion{APACrefauthors}Jorion, P. \APACrefYearMonthDay1986. \BBOQ\APACrefatitleBayes-Stein estimation for portfolio analysis Bayes-stein estimation for portfolio analysis.\BBCQ \APACjournalVolNumPagesJournal of Financial and Quantitative Analysis213279–292. \PrintBackRefs\CurrentBib

- Lintner (\APACyear1965) \APACinsertmetastarlintner{APACrefauthors}Lintner, J. \APACrefYearMonthDay1965. \BBOQ\APACrefatitleThe valuation of risk assets and the selection of risky investments in stock portfolios and capital budgets The valuation of risk assets and the selection of risky investments in stock portfolios and capital budgets.\BBCQ \APACjournalVolNumPagesThe review of economics and statistics13–37. \PrintBackRefs\CurrentBib

- Markowitz (\APACyear1952) \APACinsertmetastarmarkowitz{APACrefauthors}Markowitz, H. \APACrefYearMonthDay1952. \BBOQ\APACrefatitlePortfolio selection Portfolio selection.\BBCQ \APACjournalVolNumPagesThe Journal of Finance7177–91. \PrintBackRefs\CurrentBib

- Merton (\APACyear1972) \APACinsertmetastarmerton{APACrefauthors}Merton, R\BPBIC. \APACrefYearMonthDay1972. \BBOQ\APACrefatitleAn analytic derivation of the efficient portfolio frontier An analytic derivation of the efficient portfolio frontier.\BBCQ \APACjournalVolNumPagesJournal of Financial and Quantitative Analysis7041851–1872. \PrintBackRefs\CurrentBib

- Mossin (\APACyear1966) \APACinsertmetastarmossin{APACrefauthors}Mossin, J. \APACrefYearMonthDay1966. \BBOQ\APACrefatitleEquilibrium in a capital asset market Equilibrium in a capital asset market.\BBCQ \APACjournalVolNumPagesEconometrica: Journal of the econometric society768–783. \PrintBackRefs\CurrentBib

- Sharpe (\APACyear1964) \APACinsertmetastarsharpeCAPM{APACrefauthors}Sharpe, W\BPBIF. \APACrefYearMonthDay1964. \BBOQ\APACrefatitleCapital asset prices: A theory of market equilibrium under conditions of risk Capital asset prices: A theory of market equilibrium under conditions of risk.\BBCQ \APACjournalVolNumPagesThe journal of finance193425–442. \PrintBackRefs\CurrentBib

- Sharpe \BBA Tint (\APACyear1990) \APACinsertmetastarsharpe{APACrefauthors}Sharpe, W\BPBIF.\BCBT \BBA Tint, L\BPBIG. \APACrefYearMonthDay1990. \BBOQ\APACrefatitleLiabilities-a new approach Liabilities-a new approach.\BBCQ \APACjournalVolNumPagesThe journal of portfolio management1625–10. \PrintBackRefs\CurrentBib

- Treynor (\APACyear1961) \APACinsertmetastartreynor{APACrefauthors}Treynor, J\BPBIL. \APACrefYearMonthDay1961. \BBOQ\APACrefatitleToward a theory of market value of risky assets Toward a theory of market value of risky assets.\BBCQ \APACjournalVolNumPagesUnpublished manuscript6. \PrintBackRefs\CurrentBib

- Zivot (\APACyear2013) \APACinsertmetastarzivot{APACrefauthors}Zivot, E. \APACrefYearMonthDay2013August. \APACrefbtitlePortfolio Theory with Matrix Algebra. In the lecture notes “Computational Finance and Financial Econometrics” \urlhttps://faculty.washington.edu/ezivot/econ424/portfolioTheoryMatrix.pdf. Portfolio Theory with Matrix Algebra. In the lecture notes “Computational finance and financial econometrics” \urlhttps://faculty.washington.edu/ezivot/econ424/portfolioTheoryMatrix.pdf. \PrintBackRefs\CurrentBib