A Network Formation Model Based on Subgraphs

Abstract.

We develop a new class of random graph models for the statistical estimation of network formation—subgraph generated models (SUGMs). Various subgraphs—e.g., links, triangles, cliques, stars—are generated and their union results in a network. We show that SUGMs are identified and establish the consistency and asymptotic distribution of parameter estimates in empirically relevant cases. We show that a simple four-parameter SUGM matches basic patterns in empirical networks more closely than four standard models (with many more dimensions): (i) stochastic block models; (ii) models with node-level unobserved heterogeneity; (iii) latent space models; (iv) exponential random graphs. We illustrate the framework’s value via several applications using networks from rural India. We study whether network structure helps enforce risk-sharing and whether cross-caste interactions are more likely to be private. We also develop a new central limit theorem for correlated random variables, which is required to prove our results and is of independent interest.

JEL Classification Codes: D85, C51, C01, Z13.

Keywords: Subgraphs, Random Networks, Random Graphs, Exponential Random Graph Models, Exponential Family, Social Networks, Network Formation, Consistency, Central Limit Theorem, Sparse Networks, Multiplex, Multigraphs

1. Introduction

Networks of interactions impact many economic behaviors including insuring one’s self (e.g., Cai, deJanvry, and Sadoulet (2015)), participating in microfinance (e.g., Banerjee et al. (2013)), educating one’s self (e.g., Calvo-Armengol, Patacchini, and Zenou (2009); Carrell, Sacerdote, and West (2013)), and engaging in criminal behavior (e.g., Glaeser, Sacerdote, and Scheinkman (1996); Patacchini and Zenou (2008)). Networks of interactions are also essential to understanding financial contagions (e.g., Gai and Kapadia (2010); Elliott, Golub, and Jackson (2014); Acemoglu, Ozdaglar, and Tahbaz-Salehi (2015)), as well as world trade (e.g., Chaney (2016)), inter-state war (e.g., Jackson and Nei (2015); Koenig, Rohner, Thoenig, and Zilibotti (2015)), and a host of other economic phenomena. As such, the structure that a network takes has profound consequences—changing the possibility of contagions, the decisions that people make, and the beliefs that people hold—and so it essential to understand and estimate network formation. Moreover, networks are of interest precisely because there are externalities—one agent’s behavior impacts the welfare and behaviors of others.111For detailed discussions see Jackson, Rogers, and Zenou (2016) and Jackson (2019). This feature means that connections between agents are not independent, and so appropriate models of network formation must admit correlations in connections.

Despite the importance of network formation, general, flexible, and tractable econometric models for the estimation of network formation are lacking. This stems from two challenges: the aforementioned dependence in connections and the fact that many studies involve one (large) network. Thus, one is often confronted with estimating a model of formation by taking advantage of the large number of connections, but having them all be dependent observations. Despite the dependence, it is possible that the many relationships in a network still provide rich enough information to consistently estimate the parameters of a network model and test hypotheses from a single observed network, at least hypothetically. Here we develop a class of models that admit correlations in links and also provide practical techniques of estimating the models, showing that they are estimable, even with just a single network.

Before describing our model, it is useful to discuss some of the alternative approaches.

1.1. Alternative Models of Network Formation

The most basic models are what are known as ‘stochastic block models’, in which links may depend on node characteristics but are (conditionally) independent of each other. That approach requires correlation between links to be well-approximated by observable characteristics, and may not be sufficient for most applications.222A variation on this is community detection where nodes are estimated to belong to certain groups, though this calculation is NP-hard. See Bickel et al. (2011) for a “non-parametric view” of network formation, and Jackson and Storms (2017) for an approach to estimating the blocks even if they are latent. In particular, stochastic block models are not a good option for estimation in applications in which there is substantial clustering (triangles) or other cliques in the network. In fact, in Section 5 we show that our model (even with only four parameters) models the graph structure of real-world data better than a stochastic block model even when the block model admits a rich set of covariates and unobserved node level heterogeneity (fixed effects) (Chatterjee et al., 2010; Graham, 2017).333In fact, correlations can be viewed as driven by unobserved heterogeneity (Chatterjee, Diaconis, and Sly, 2010), which has links be uncorrelated conditional on all (observed and unobserved) characteristics (as extended by Graham (2017)). See also Charbonneau (2017) for related work that is a directed networks version of Graham (2017). Such models have been studied in the mathematics and statistics literatures (e.g., Holland and Leinhardt (1981); Park and Newman (2004); Blitzstein and Diaconis (2011)). Although there are challenges in taking such models to data, they are useful if link correlation is not a concern.

Given the importance of clustering and other local network architectures in many applications, a literature spanning several disciplines (sociology, statistics, economics, and computer science) turned to using exponential random graph models—henceforth “ERGMs”. ERGMs admit link interdependencies and have become the workhorse models for estimating network formation.444These grew from work on what were known as Markov models (e.g., Frank and Strauss (1986)) or models (e.g., Wasserman and Pattison (1996)). An alternative is to work with regression models at the link level, but to allow for dependent error terms, as in the “MRQAP” approach (e.g., Krackhardt (1988)). However, from the onset of the use of ERGMs, researchers realized that the parameter estimates could be unstable on all except excessively small networks. It has been shown that maximum likelihood and Bayesian estimators are not computationally tractable (the required Gibbs sampler will take exponential time to mix) nor consistent for important classes of such models—and in particular for the ERGMs that include many link dependencies of interest (and neither parameter estimates nor standard errors can be trusted). For details see Bhamidi, Bresler, and Sly (2008); Shalizi and Rinaldo (2012); Chandrasekhar and Jackson (2012).555Recent work has made progress on both the speed of convergence of estimation algorithms as well as characterizing the asymptotic distribution of sufficient statistics in some classes of ERGMs that avoid extensive link dependencies (see e.g., Mele (2017, 2022); Mele and Zhu (2023)).

A set of models that allow for link dependencies and are estimable is the class of models based on explicit link formation algorithms (e.g., Barabasi and Albert (1999); Jackson and Watts (2001); Jackson and Rogers (2007); Currarini, Jackson, and Pin (2009, 2010); Christakis, Fowler, Imbens, and Kalyanaraman (2010); Bramoullé, Currarini, Jackson, Pin, and Rogers (2012)). These models can be estimated since the algorithms are particular enough so that one can directly derive how parameters in the model translate into aggregate network statistics, such as the degree distribution or homophily levels. The advantage of such models is that a specific algorithm allows for estimation. The disadvantage is that the specificity of the algorithms also necessarily results in narrow models. Thus, these approaches are useful in some contexts, but they are not designed, nor intended, for general statistical testing of a wide variety of network formation models and hypotheses. For instance, such models cannot generate considerable triadic closure (where links correlated across triples of nodes—so if two people have a friend in common, are they more likely to be friends with each other than if link formation were independent).666The Jackson and Rogers (2007) model does have a parameter that affects triadic closure, but in that model closure cannot be separated from the shape of the degree distribution. So, it is best suited for growing random networks where new nodes are born over time.

Another approach has roots in the spatial statistics literature. Such models organize nodes such that pairs can be evaluated in terms of distance, with linking probabilities decaying in distance. The distance may be latent (unobserved) or in observed characteristic space (such as geography or demographics). Such models have foundations in the mathematics literature on random geometric graphs (Penrose, 2003)—where nodes are distributed in a latent space according to some Poisson point process and linking is much more likely among proximate nodes—and have been analyzed in the statistics literature in work on latent space models such as in Hoff et al. (2002). Links between distant-enough pairs of nodes are asymptotically independent and such models have been developed in more detail in the econometrics literature (e.g., Boucher and Mourifié (2012); Leung (2014)). This approach holds promise for some enormous networks with appropriate spatial structures—in which the graph can almost be decomposed into independent pieces.777McCormick and Zheng (2015) merge the insights from the unobserved heterogeneity and the latent space distance models, and Breza, Chandrasekhar, McCormick, and Pan (2020) evaluate its empirical performance. However, there are many applications for which these latent space (and generally spatial) models and the geometry of the space the nodes overly dictates and limits the structure of link correlation. As a simple example, consider a large tree, which is a structure that is certainly of empirical interest in a number of disciplines including economics, computer science, sociology, and biology. The spatial style models, as typically used, cannot generate large trees. This is because an infinite tree cannot be embedded in a finite dimensional Euclidean (or spherical) space.888In fact, these models need to be altered to have distances defined in hyperbolic space instead. So using these models may in fact require estimating an unobserved manifold, which presents its own challenges.999 Estimating the latent geometry by using the network data to identify the underlying metric signature is the subject of one of the authors’ related work in (Lubold et al., 2023). Our model dispenses with these problems in a straightforward way, allowing correlations across nodes but not forcing correlations generated through distances in unobserved or characteristic space. Therefore, we can easily model large trees.

Finally, there is a large literature on the theory of network formation from a strategic perspective (for references, see Jackson (2005, 2008)). Since the first writing of this paper, researchers have started to derive versions of such models that can be taken to data. One approach builds upon the relationship between certain classes of strategic network formation models and potential games; some of which leverage subgraphs, but in a rather different way from us (Butts (2009); Mele (2017); Badev (2021)). Another derives restrictions on parameters of an observed network under the presumption that it is in equilibrium (pairwise stable) (De Paula, Richards-Shubik, and Tamer (2018); Sheng (2020)). The latter makes the observation that by using pairwise stability restrictions of Jackson and Wolinsky (1996) on subnetworks, one can partially identify preference parameters in the model, whereas doing so on the full graph can be computationally infeasible.101010For a recent overview of the recent literature, see De Paula (2017).,111111In both the potential games and the partial identification literatures, subgraphs play very different roles from their role here. Although the progress to date requires strong restrictions on how links can enter agent’s payoffs, they provide important first steps in deriving implications of the arsenal of strategic network formation models. Below, we also provide ways to incorporate strategic formation in SUGMs, thus in part bridging our approach here and the strategic formation approach.

1.2. Our Subgraph Model Approach

Our approach is distinct from all of the above, both in terms of the approach (working with subgraphs as the basic building blocks) and the technicalities of allowing nontrivial conditional correlations. Our contribution is to develop models of network formation that admit considerable interdependency without spatial restrictions, and still prove consistency and asymptotic Normality of the parameter estimates. As part of this, we develop a new central limit theorem for non-trivially correlated random variables that moves away from relying on spatial-style mixing arguments that force decaying dependence in distance.

The paucity of flexible models that are computable and can be used across many applications for hypothesis testing and inference is what motivates our work here. Although our models are simple conceptually, we provide different applications that illustrate how such models admit strategic network formation, general covariates, and generate rich network features.

In Section 2 we introduce subgraph generated models—henceforth SUGMs. In these models, various subgraphs (e.g., links, triangles, cliques, and stars) are generated directly. For instance, students may form friendships with their roommate(s), members of a study group, teammates, band members, etc.; researchers may form collaborations on writing papers in pairs, or triples, or quadruples, etc; villagers may form specific bilateral or multilateral agreements independently, each to sustain some collection of favors between those individuals involved in the agreement. This results in links and those links are then naturally correlated since they are formed in combinations. The union of all these subgraphs results in a network. In this section, we also introduce three motivating applications to demonstrate how this model could be used: (i) descriptively modeling network structure, (ii) motives for risk-sharing, and (iii) incentives to link across social boundaries.

The statistical challenge is that often only the final network is observed: a survey may ask people to list their friends or acquaintances, or links may be observed on a social platform, or emails or phone calls are observed, etc., but the original formation process is often not observed. Subgraphs may overlap and may incidentally generate new subgraphs: e.g., three links may form and result in a triangle. Thus, the true rate of formation of the subgraphs cannot generally be inferred just by counting their presence in the resulting network.121212The closest work to ours is a Bollobás et al. (2011) piece on random graph theory, which looks at percolation processes, giant component structure, and degree distributions in a model where the observed graph is generated by a set of atoms (subgraphs in our language). That paper focuses on a specific rate of arrival of subgraphs (to maintain a sparsity where a core problem we study is ruled out) and is not interested in statistical estimation.

Despite this, in Section 3 we prove that every subgraph generated model is identified. That is, if we consider a SUGM—a collection of subgraphs that can potentially form together with a set of parameters governing the probabilities of each subgraph forming—then any two distinct set of parameters necessarily has two distinct set of distributions over the set of possible networks. Furthermore, we explore specific cases that are of empirical relevance—for instance, links and triangles models—and demonstrate that not only are the distributions generally distinct, but that simple statistics (such as the share of links or triangles that form) allow us to identify the parameters of interest.

Next we turn to estimation of the underlying parameters describing subgraph formation rates in Section 4. We show that we can consistently estimate the parameters and we derive the asymptotic distribution of the estimates so we can conduct inference. There are two situations that a researcher may face.

In the first case, the researcher has access to “many networks”. This could be because they have collected network data from numerous schools, many villages, or so on. Here we demonstrate (using standard results) that the parameters governing the SUGM can be estimated consistently with maximum likelihood estimators that are asymptotically Normally distributed. For some empirically relevant classes of models, we demonstrate that there are computationally simple, minimum distance estimators which satisfy consistency and asymptotic Normality.

The second case is where the researcher has one (or just a few) “large network”. This could be because they have collected very rich network data with resource constraints in just a few communities, or because they are looking at a single market, or because they are looking at one social media platform, etc. In this case, the asymptotics are more technically challenging for two reasons. First, the network cannot be too sparse, as enough subgraphs must form to make estimation possible, nor too dense because it becomes impossible to distinguish which subgraph likely generated a candidate link. So formally, we have “rate requirements” on the parameters governing the probabilities of subgraphs forming, although these turn out to be quite accomodating. Second, existing central limit theorems from the spatial and time-series econometrics literatures do not apply to our setting, as we need to allow subgraphs to form on arbitrary groups of nodes, which then results in correlation patterns across all links in the network. We overcome this problem by developing a new central limit theorem and use it to characterize when certain classes of SUGMs have estimators that are consistent and asymptotically Normally distributed.131313An interesting consideration for future work is to employ the techniques in Bhattacharyya et al. (2015), who develop a bootstrapping method to estimate the distribution of empirical counts of different subgraphs in enormous networks.

With the statistical properties established, we turn to our empirical applications in Section 5. In each application we use the detailed network data we collected in 75 villages in Karnataka, India (Banerjee et al., 2019). We begin by comparing SUGMs to four archetypical models from the literature in terms of how well they model real-world data. Specifically, we fit each model to the data and then draw from the distribution at the estimated parameters for each model. We are interested in a variety of economically relevant network features (none of which are directly used to estimate any of the models). We find that across the board a four parameter SUGM outperforms a stochastic block model with flexible covariates; a model of unobserved heterogeneity at the node level as well as rich covariates; a latent space model with unobserved locations and heterogeneity as well as observed covariates; and an exponential random graph model with rich covariates. Only the SUGM comes close to capturing the average path length, homophily, maximal eigenvalue, size of the giant component, isolates, and clustering. Having established this, the second example turns to whether the structure of the networks is consistent with the idea that there are stronger incentives to have supported relationships for risk sharing links rather than informational links (Jackson et al., 2012) and we find evidence consistent with this. The third example explores whether linking across social boundaries—here links between upper caste and lower caste (Dalit communities)—is more likely to form in private (bilateral) rather than group (triadic) settings and we find exactly this. Together, these examples demonstrate the utility of our general framework.

In Section 6 we return to state our Central Limit Theorem, which is of independent interest. We provide covariance conditions that are high-level but also straightforward to interpret, check, and micro-found. We use a powerful lemma from Stein (1986) in our proof. Many CLTs build upon Stein’s method141414For instance, Bolthausen (1982) uses a pre-cursor lemma from Stein (1972) to derive CLTs from some mixing conditions. In time-series and spatial econometrics, a non-exhaustive but illustrative list of papers using Bolthausen (1982) include Conley (1999), Jenish and Prucha (2009), Bester, Conley, and Hansen (2011), among others., but we allow for much richer dependence—all random variables can have non-zero correlation—which is necessary in our setting; and we also allow for triangular arrays. We discuss the relationship of our Central Limit Theorem and its proof to precursors in Section 6.

2. A Model of Network Formation via Subgraphs

2.1. Networks

is the number of nodes on which a network is formed. Nodes may have characteristics, such as age, profession, gender, race, caste, etc., that we denote by the vector for a generic . The have finite support.151515This is a limitation since there are network models that do not require discrete covariates. While continuous variables can be discretized, this is a trade-off. As such nodes can be classified by a finite set of observable types.161616We conjecture that our results extend to allow for continuous covariates as well, though that requires specifying parametric functions for the probability of subgraphs as a function of covariates and so remains beyond the scope of this paper.

We denote a network by , the collection of subsets of of size 2 that lists the edges or links that are present in its graph. So, indicates the network that has links between nodes 1 and 3 and between nodes 2 and 5. For notational ease, we simply write , and write to denote that link is present in network . Our model easily accommodates directed graphs, and all of the definitions below extend directly, in which case instead of pairs of nodes, these would be ordered pairs so that and would differ. However, for ease of exposition, most of the examples and discussion refer to the undirected case. denotes the set of all networks on nodes.

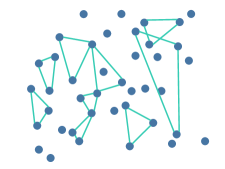

2.2. Subgraphs and SUGMs

In a subgraph generation model, subgraphs are each directly generated, and then the resulting network is the union of all of the links in all of the subgraphs. Degenerate examples of this are Erdos-Renyi random networks, and the generalization of that model, stochastic-block models, in which links are formed with probabilities based on nodes’ attributes. The more interesting classes of SUGMs include richer subgraphs, and hence involve dependencies in link formation. It might be that people of the same caste meet more frequently or are more likely to form a relationship when they do meet, as in a stochastic block model, but it could also be that groups of three (or more) meet and can decide whether to form a triangle, with the meeting probability and decision potentially driven by their castes and/or other characteristics. The model can then be described by a list of probabilities, one for each type of subgraph, where subgraphs can be based on the subgraph shape as well as the nodes’ characteristics.

A SUGM is formally defined as follows.

There are finitely many types of nonempty subgraphs, indexed by , for instance in the links and triangles case .171717This definition does not admit isolates since we define subgraphs to be nonempty and connected, but isolates are easily admitted with notational complications, and are illustrated in some of our examples below as well as the supplementary appendix. The subgraph types are denoted by , where each is a set of possible subgraphs on nodes. For each and pair of subgraphs and there exists a bijection on such that if and only if . For instance if and is the set of triangles, then and it would be the set . Note that it is not required that contain all triangles. In examples in which node characteristics matter, different triangles could be categorized into different s, for example. However, we do require that no subgraph is contained in two different sets: if then implies that .

The definitions of the subgraph types can have restrictions based on node characteristics, for instance, requiring that the characteristics and be the same—e.g., for some could be the set of “triangles that involve one child and two adult nodes”. As an example, the set for some could be all stars with one central node and four other nodes, and another could be all the links that involve people of different castes, and so forth.

A few examples are pictured in Figure 1.

The probability that various subgraphs form is described by a vector of parameters, denoted , where is (unless otherwise noted) a compact subset of .181818We treat vectors as row or columns as is convenient in what follows. For instance, in a links and triangles example.191919In some examples below, we expand this demonstrating how can have entries that are monotone functions of preference parameters (or equilibrium behavior), which allows us to study certain economic questions. Estimating allows us to either recover the parameters or behavior of interest in some cases or conduct loose hypothesis testing using our estimates of .

A network on nodes is randomly formed as follows:

-

(1)

Each of the possible subgraphs forms with probability independently of all other subgraphs (including others in ).

-

(2)

The resulting network, , is the union of all the links that appear in any of the generated subgraphs.

2.3. An Example with Node Characteristics

Suppose that nodes come in two colors: blue and red (for instance different genders, age groups, religions, etc., and clearly this extends directly to more than two colors). In our example of links and triangles, there are now three types of links: (blue, blue), (blue, red), (red, red); and four types of triangles (blue,blue,blue), (blue,blue,red), (blue,red,red), (red,red,red) which comprise the set of subgraphs indexed by .

Thus, in this example the sets of subgraphs are

and

and so forth, as depicted in Figure 2. The parameters

are the probabilities that the corresponding subgraphs form.

One could restrict or enrich the model by having simpler or more complex sets of parameters – for instance requiring that , or by having preference parameters that govern the probabilities of various subgraphs forming, as we discuss below.

2.4. Links and Triangles as Our Leading Example

The bulk of our illustrations and applications are based on link and triangle SUGMs, though other subgraphs can be included and are covered by our general results (e.g., Theorems 1, 2, and 3). Our illustrations focus on links and triangles for two reasons: first, this case is simple to understand and illustrates the main points since it exhibits correlated links and incidental generation; second, the link and triangle model already matches the moments that are of interest in many research projects (larger cliques are rare). In fact, as we show below, simply looking at a links and triangle SUGM tagged with whether the nodes involved are homogenous or heterogeneous in demographics (e.g., just a 4 parameter model), replicates real-world network features better than far-richer models. Still, we leave further specification to the researcher as it will depend on their context and the phenomenon being modeled. If there are other the types of subgraphs that are hypothesized to arise in some particular context, then that model can be constructed and estimated in the ways we outline and are covered by our general results.202020One could also have a list of subgraphs as a possible basis for the SUGM with only a subset of them actually forming the true SUGM; allowing the data to tell the researcher which to include. Some of that can be done here, including the various subgraphs that might be involved and then seeing which have nontrivial parameter estimates. This marries SUGMs with model selection, a topic which could be explored further in future research.

3. Identification

3.1. The Challenge of Identification

The researcher’s goal is to use the observed data—from one or more networks—to recover the parameters of interest, for example, the in a SUGM of links and triangles. If the researcher observed the links and triangles that were formed directly, then estimation would be straightforward. Indeed, in some instances a researcher has direct information on all the various groups a given individual is involved in: for instance in the case of a co-authorship network, the researcher may observe all the papers a researcher has written and thus observes papers with two authors, three authors, and so forth. Instead, for instance, it may be that there are groups of three people who commonly share favors and risks together—who really form a triangle, but the researcher only has information from a survey asking with which alters a given person interacts (as in networks derived from the Add Health data set as in Currarini et al. (2009)), or who borrows from whom and who lends kerosene and rice to whom and other bilateral nominations (as in our Indian village data Banerjee et al. (2013)), or from observing that who are friends on a social platform (as in Facebook network data as in Bailey et al. (2016); Chetty et al. (2022)), or from observing that two people phone each other or remit payments to each other (as in Blumenstock et al. (2011)).

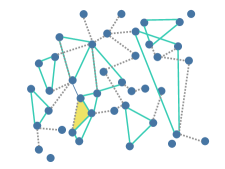

Thus, the general problem is that the formation of the subgraphs is not directly observed, and so must be inferred in order to estimate the parameters of interest. For example, if three links are observed between , , and , is it the case that formed as a triangle, or that , and formed as links, or that and formed as links and formed as part of a different triangle , or some combination of these or other combinations? Figure 3 provides an illustration.

The overlap and incidental generation present a challenge for estimating a parameter related to triangle formation since some of the observed triangles were “directly generated” in the formation process, and others were “incidentally generated;” and similarly, it presents a challenge to estimating a parameter for link formation since some truly generated links end up as parts of triangles.We show that despite this difficulty, the parameters can be recovered by careful study of the observed patterns. In particular, we show that a SUGM is always identified, and also provide techniques for recovering the parameters.

3.2. A General Identification Result

We first show that as the parameters of any SUGM change, so does the distribution over networks, and hence SUGMs are identified models.

Let denote the probability distribution over a network on nodes under a vector of parameters describing the probabilities of subgraph types .

Theorem 1.

Every SUGM is identified. That is, for any finite collection of distinct types of subgraphs on nodes,

Recalling the general definition of the SUGM, this means that for every SUGM (even one comprised of subgraphs that could have nodes with varying (discrete) covariates and allowing for multiplexing, etc.) is identified.

To understand why this holds, for instance in the case of links and triangles, note that as one varies , the relative rates of overall observed links and triangles change, as do the number of triangles that overlap with each other. One can calculate the relative rates at which incidental links and triangles are expected to be generated, and there is an invertible relationship between observed counts of links and triangles, and the underlying rates at which they were expected to be directly formed. Theorem 1 shows that this is true not only for links and triangles, but for any collection of distinct subgraphs.

We emphasize, of course, that identification does not imply that the parameters are easily estimated, especially on a very small number of nodes. We provide results on consistency below, which require observation of a sufficiently large network and/or sufficiently many networks.

3.2.1. Identification from Link and Triangle Counts

Although Theorem 1 shows that SUGMs are always identified—i.e., distinct parameters yield distinct distributions—it is often convenient to use minimum distance based estimators based on simple moments of the network. Thus, it is useful to show that identification can be achieved from simple statistics. We illustrate that this can be done with direct counts of the relative frequency of appearances of the subgraphs. In particular, in Proposition 1 we show that a links and triangles SUGM can be identified directly from the counts of links and triangles: . This does not mean that one can ignore incidental generation, but it does mean that the information one has to use can be simple counts.

Further below, in Theorem 3, we show conditions under which such direct counts not only identify the parameters for general subgraphs, but can also be used to derive consistent and Normally distributed estimators of the parameters.

To understand the identification, consider Figure 4. Each configuration involves two triangles, but the graph in Panel B with only five links is relatively more easily incidentally formed than the one in Panel A. Thus, by looking at the combination of how many triangles and how likely links there are, we can sort out relative rates of the two parameters.

Proposition 1.

A SUGM of links and triangles is identified from moments for any . That is, if then .

Let us outline the basic ideas behind the proof, with the full proof appearing in the appendix. Let denote the probability that any given link forms conditional upon exactly one particular triangle that it could be a part of not forming. For instance, for nodes it is the probability that is formed either as a link or as part of a triangle that is not triangle for some other node . Although this is not an immediately obvious parameter to define, it allows us to write the probability that a given link forms as . This turnd out to be useful to compare to the probability that a given triangle forms. In particular:

| (3.1) |

For instance, note that the term is the probability that a triangle forms, either directly (), or does not form directly but then each of the links then forms on its own .212121Conditional upon the triangle not forming directly, the links are then independent. This is helpful in showing how different parameters lead to different rates of formation of links and triangles since we can isolate the difference via the versus expressions.

4. Asymptotics

We now provide conditions under which various estimators of the parameters are consistent and describe their asymptotic distributions. We consider two asymptotic frames, in which at least one of either the size of the network or the number of networks becomes large enough for consistent estimation. We discuss two different estimators for each frame for a total of four estimators.

4.1. Data and Asymptotic Frames

Suppose that the researcher observes independently, and identically drawn graphs , on at least nodes each, drawn from a SUGM with a list of subgraphs and parameters . Each of the subgraphs involves no more than nodes. For simplicity in notation, we work with each network having exactly nodes, but one can directly extend the results by simply selecting nodes for each network and applying all of our estimation to those subgraphs.

The first asymptotic frame, studied in Section 4.2, covers situations in which the number of different realizations of networks tends to infinity. Here researchers have access to many networks and the empirical moments of interest converge to their expectations via observation of independent networks. This applies when a researcher is studying, for instance a number of schools, classrooms, villages, etc. In this case estimation and inference is straightforward. There are a growing number of independent draws from the distribution and we have already proven identification in Theorem 1. Our Theorem 2 shows that the maximum likelihood estimator from networks—which we denote by —is consistent and asymptotically Normally distributed as grows.

Given the difficulty in calculating the likelihoods for networks, also consider a second computationally-simpler minimum-distance estimator (presented for the case of links and triangles), denoted by . We show in Proposition 2 that this minimum distance estimator is consistent and asymptotically Normally distributed.

The second asymptotic frame is studied in Section 4.3 and it holds the number of networks observed fixed, without loss of generality at , and then lets the number of nodes grow: . Examples include when the researcher has detailed information about a large community, friendships on social media platform, citation networks, etc. Clearly, this extends to cases with large and more than one network, but we consider for ease of notation. This is the more challenging perspective as the observations of various parts of a network are not independent. Also, the identification result from Theorem 1 does not guarantee that the empirical moments converge to their expectations in a single large network.

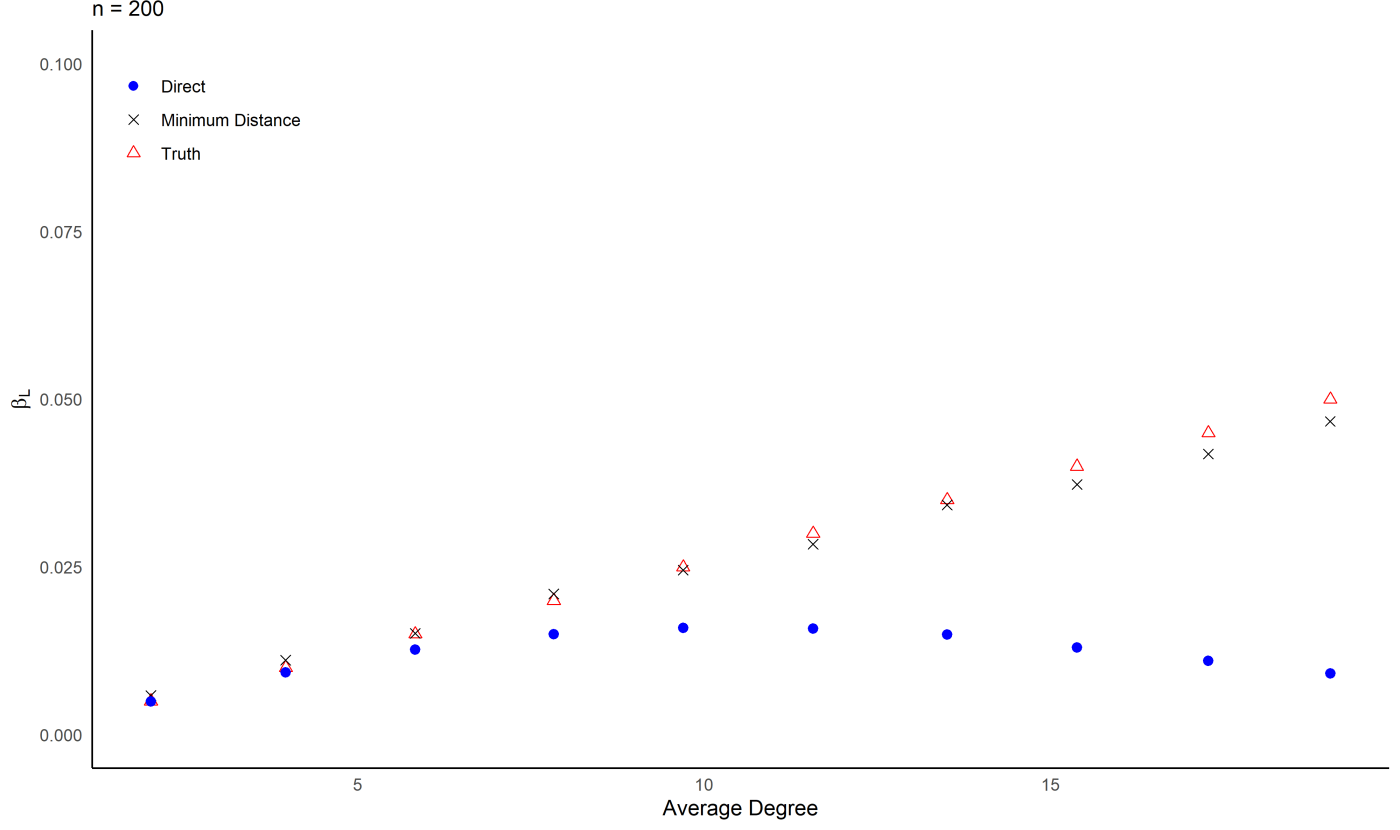

There are two cases of interest with a single large network. The first is what we call the sparse case (which we explicitly characterize), and this is a situation in which certain types of incidental generation of subgraphs become asymptotically negligible. For the sparse case, we prove that identification and asymptotic consistency and Normality is possible from an easy variation on direct counts of observed subgraphs. Namely, one begins with the largest subgraph in the model, count how many of them are present, then remove links associated with them and step down to the next largest and so on. The estimator corresponding to this procedure is what we call a direct count estimator—denoted by —as it is essentially directly calculating the linking rate for each subgraph type. We prove the consistency and asymptotic Normality of the direct count estimator under suitable sparsity conditions in Theorem 3.

It is possible to verify whether a network is sparse enough to permit the direct estimator in the following way. One can take relevant parameter values for the SUGM (which one can find by a first crude estimation from the data) and then generate a network with those parameter values and then check to see if the direct estimators recover these parameters. If there is too much incidental generation, then the parameters will not be recovered and then our fourth estimator is needed, as is our new central limit theorem.

In particular, Theorem 3 requires a level of sparsity that makes certain kinds of incidental generations rare. For denser graphs (which can still be sparse, but permitting nontrivial incidental generation) we work with a minimum distance estimator that matches the moments of the shares of the subgraphs—which we denote by . In Proposition 3, we show the consistency and asymptotic Normality of this minimum distance estimator. We focus on the links and triangles model since the calculations are idiosyncratic based on the specific SUGM the researcher wants to employ, but the logic extends. The proof of asymptotic Normality in this case of potentially dense SUGMs requires using our new central limit theorem for correlated random variables, Theorem 4, which is the focus of Section 6.

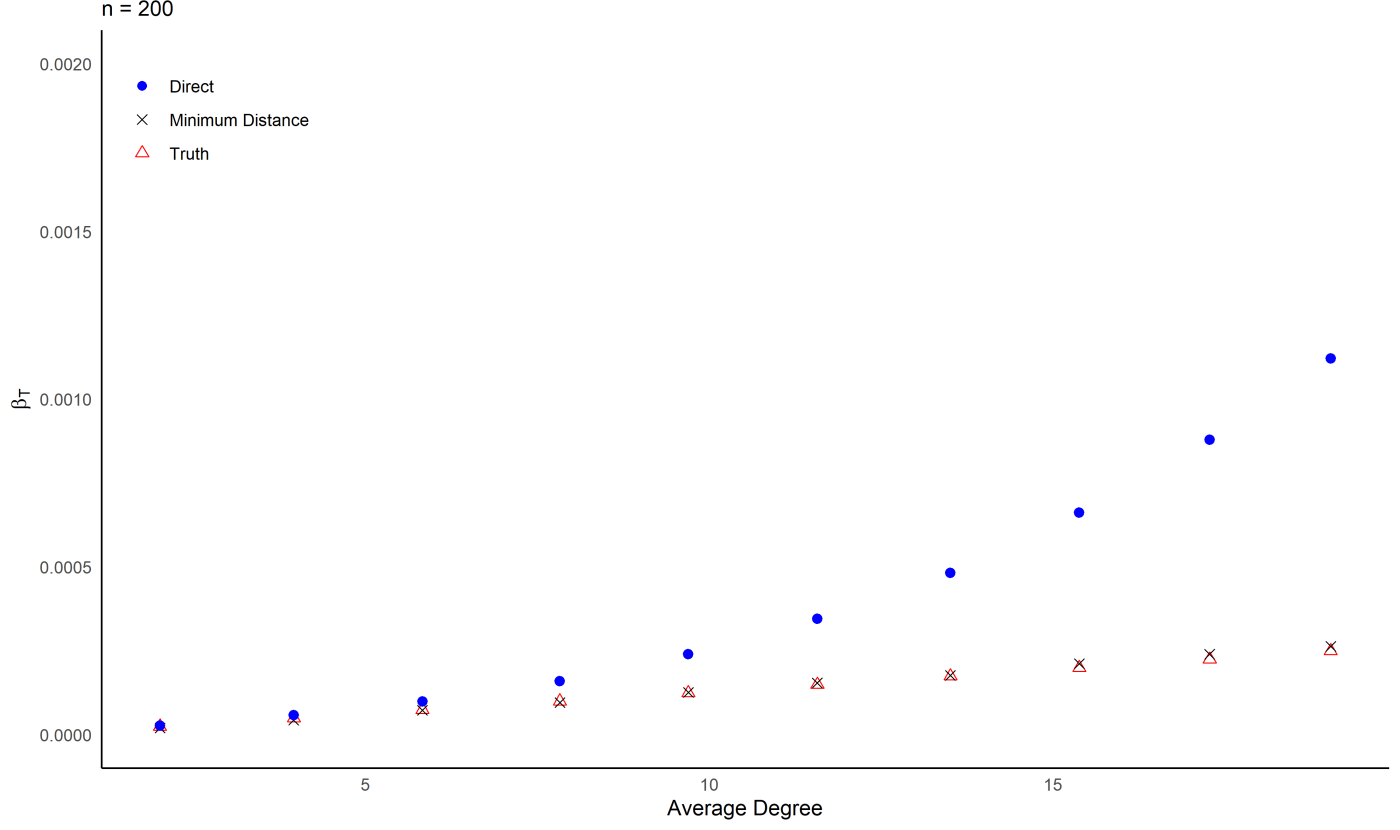

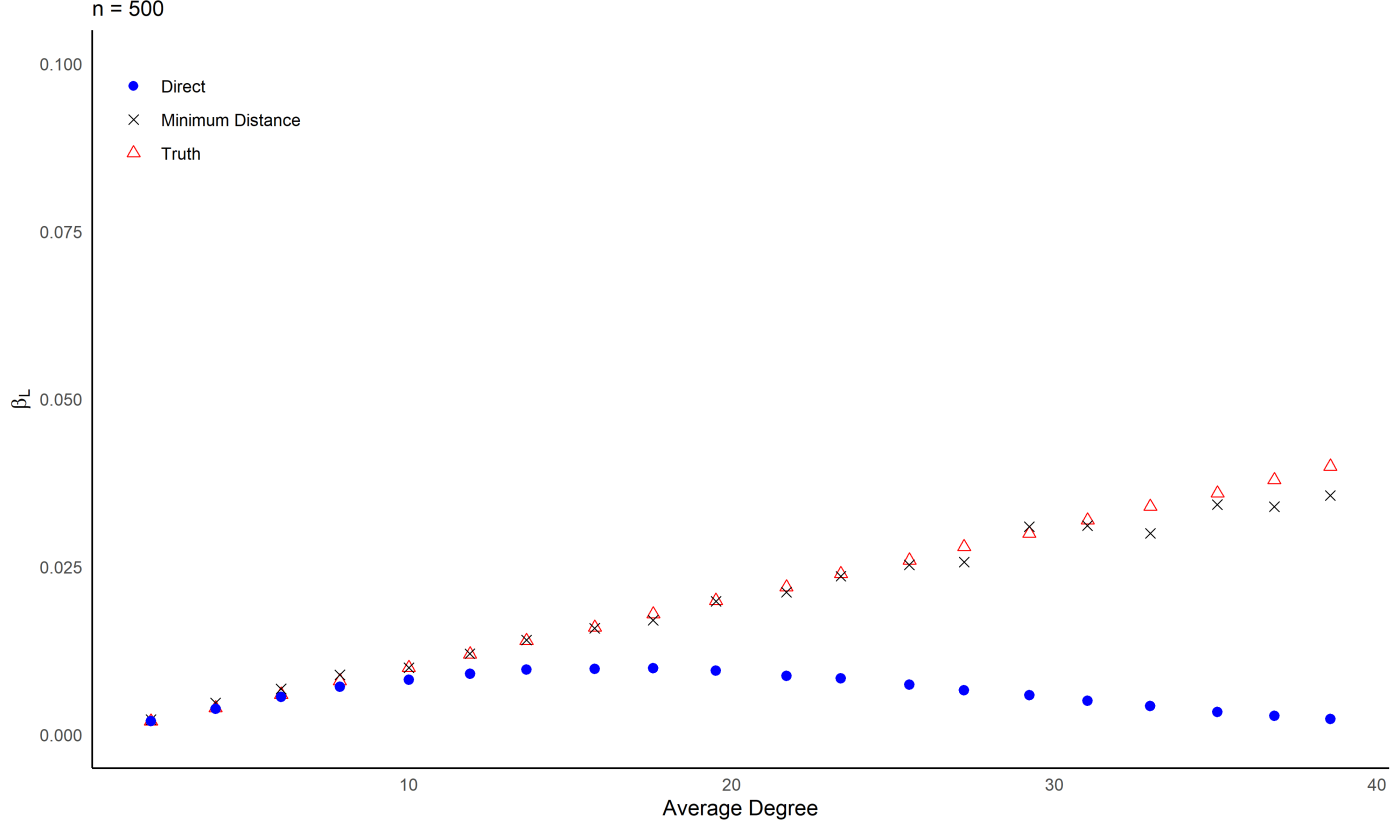

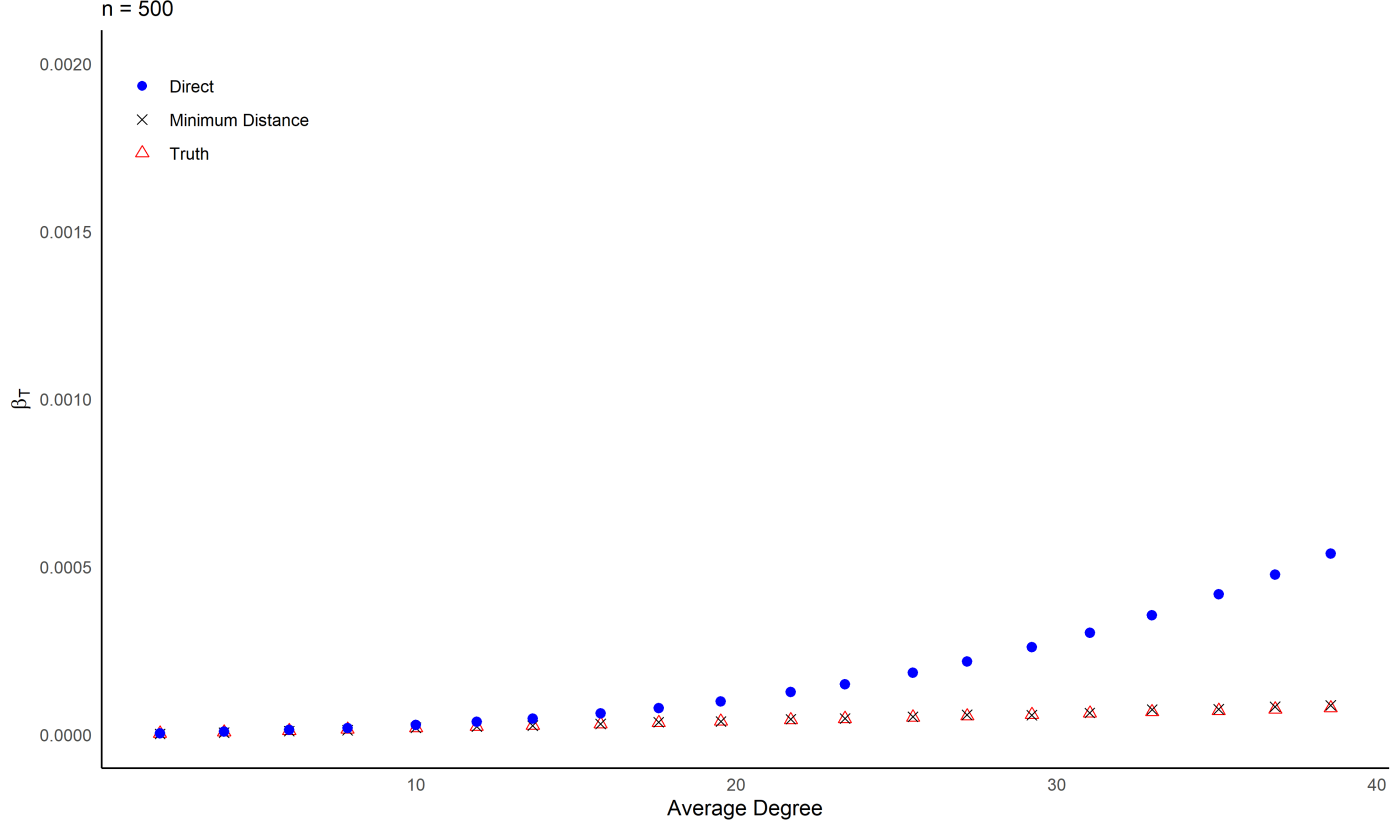

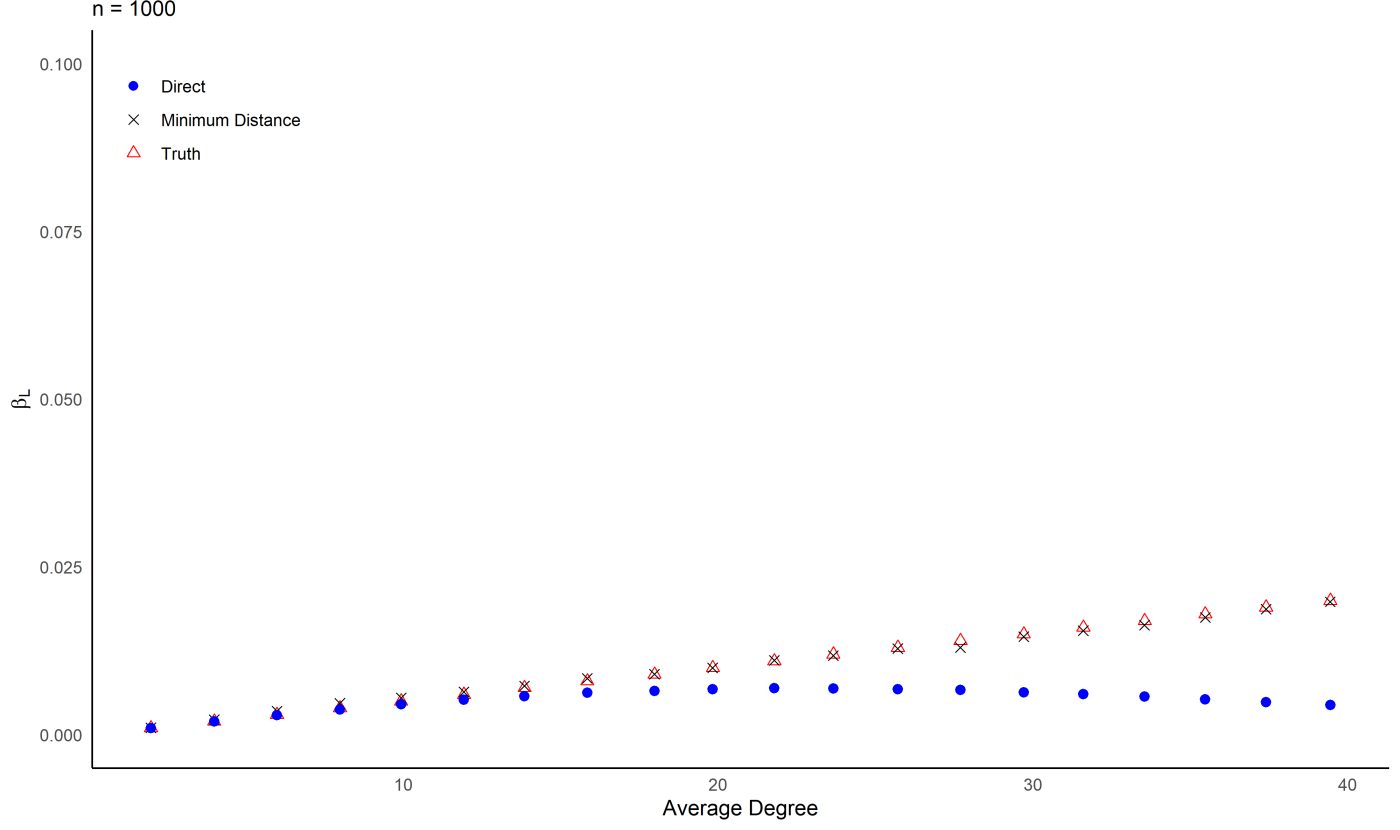

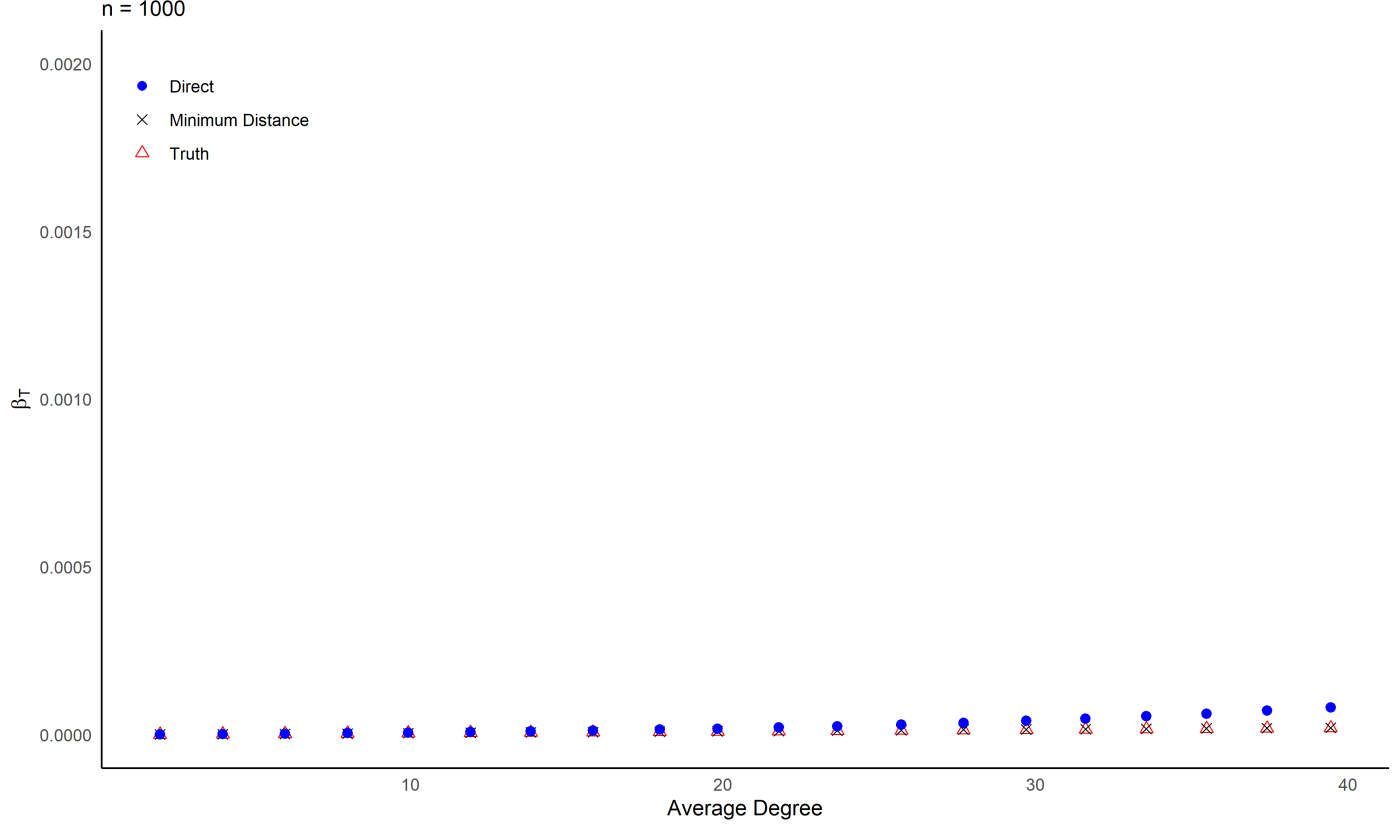

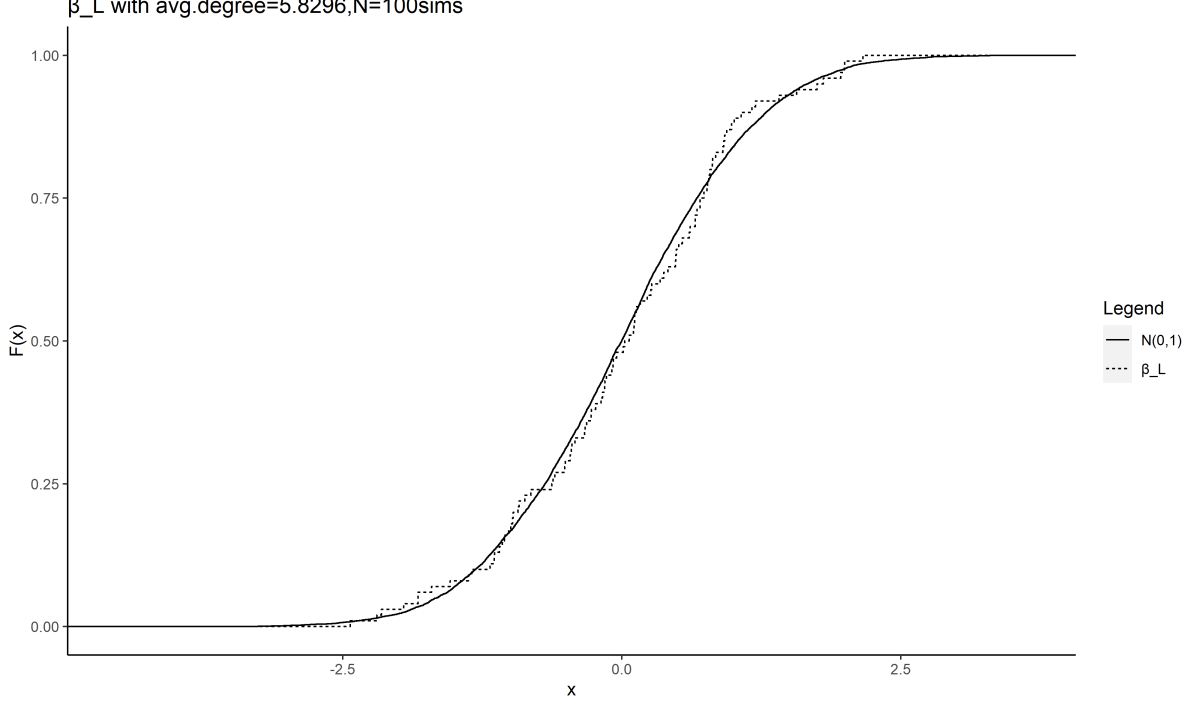

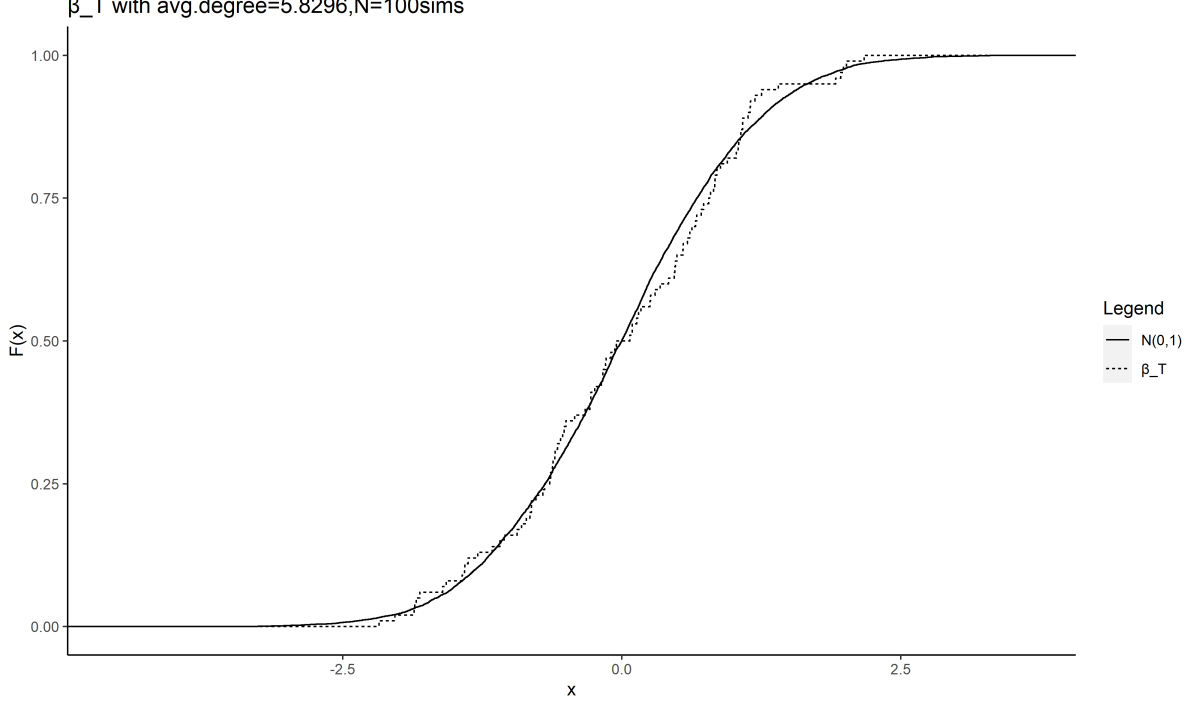

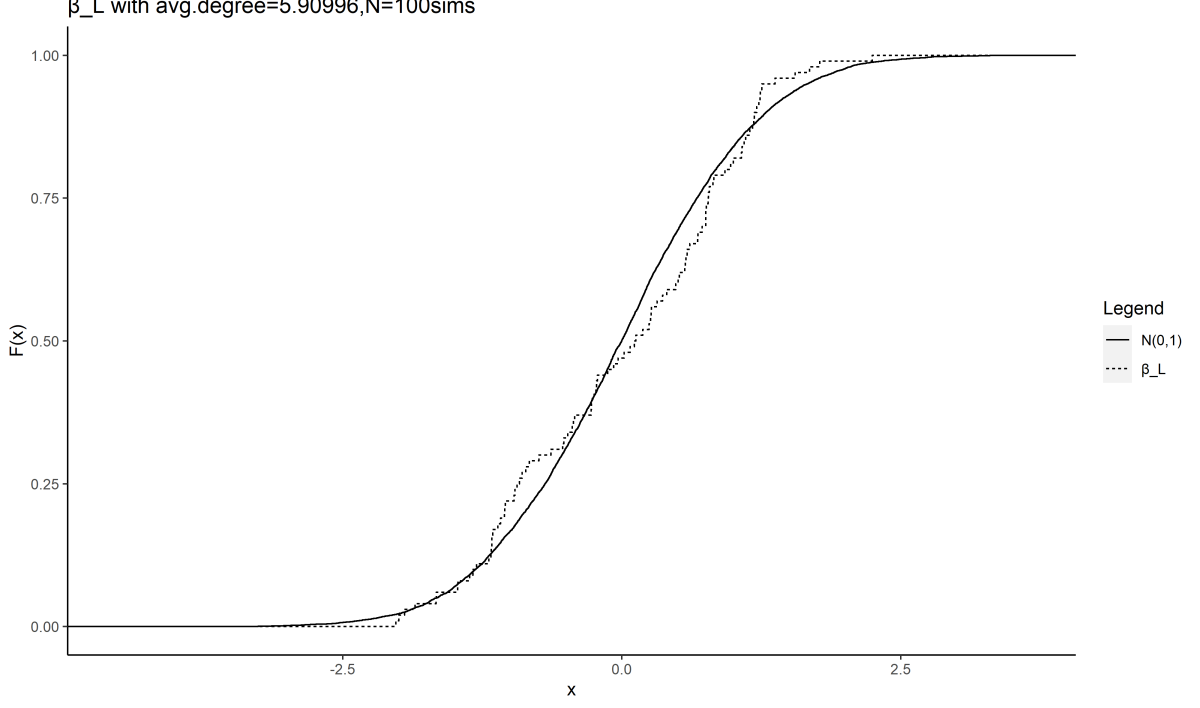

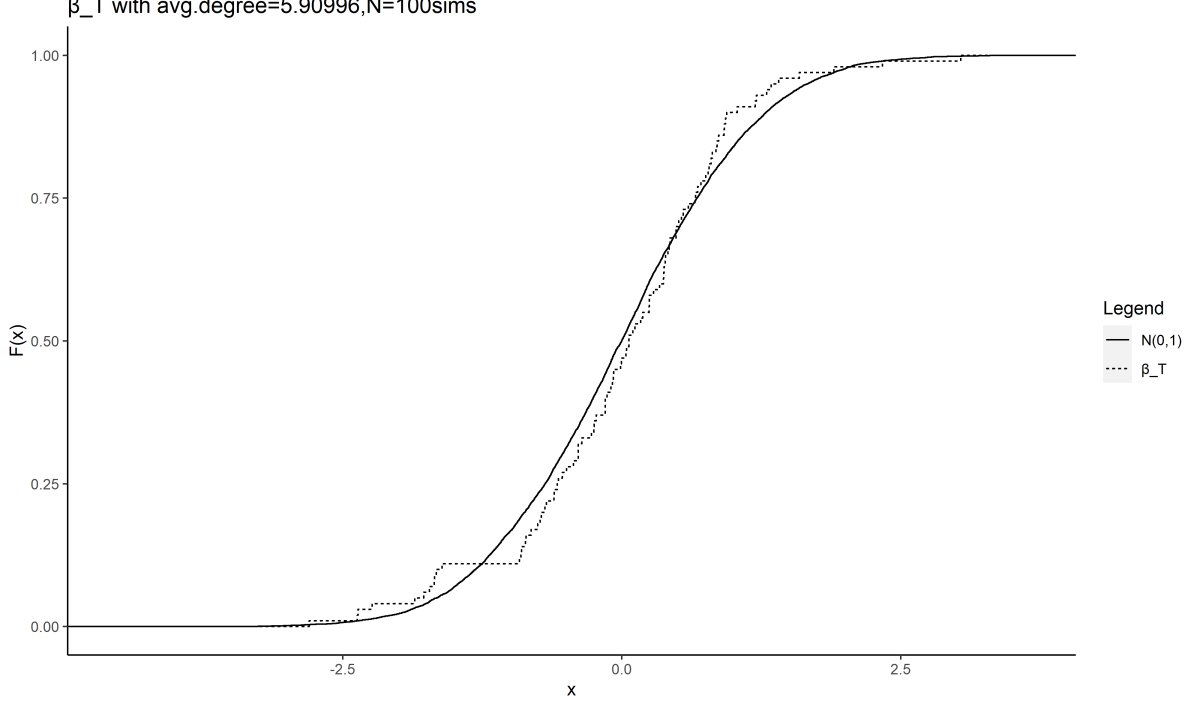

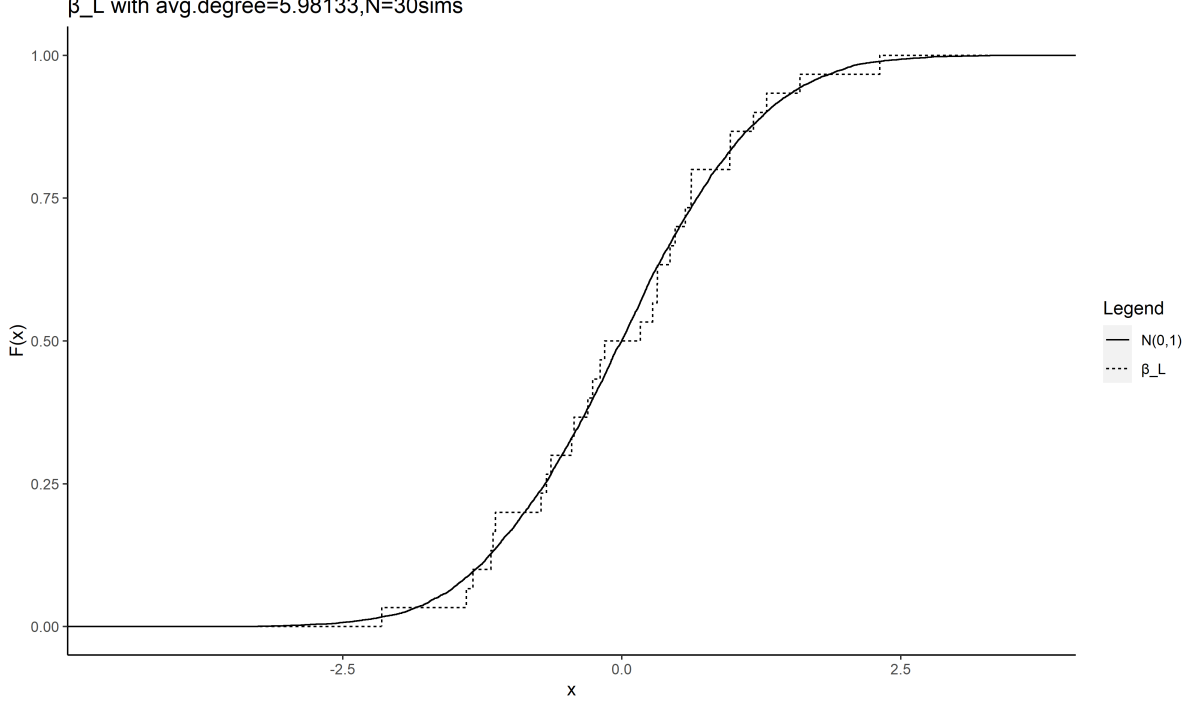

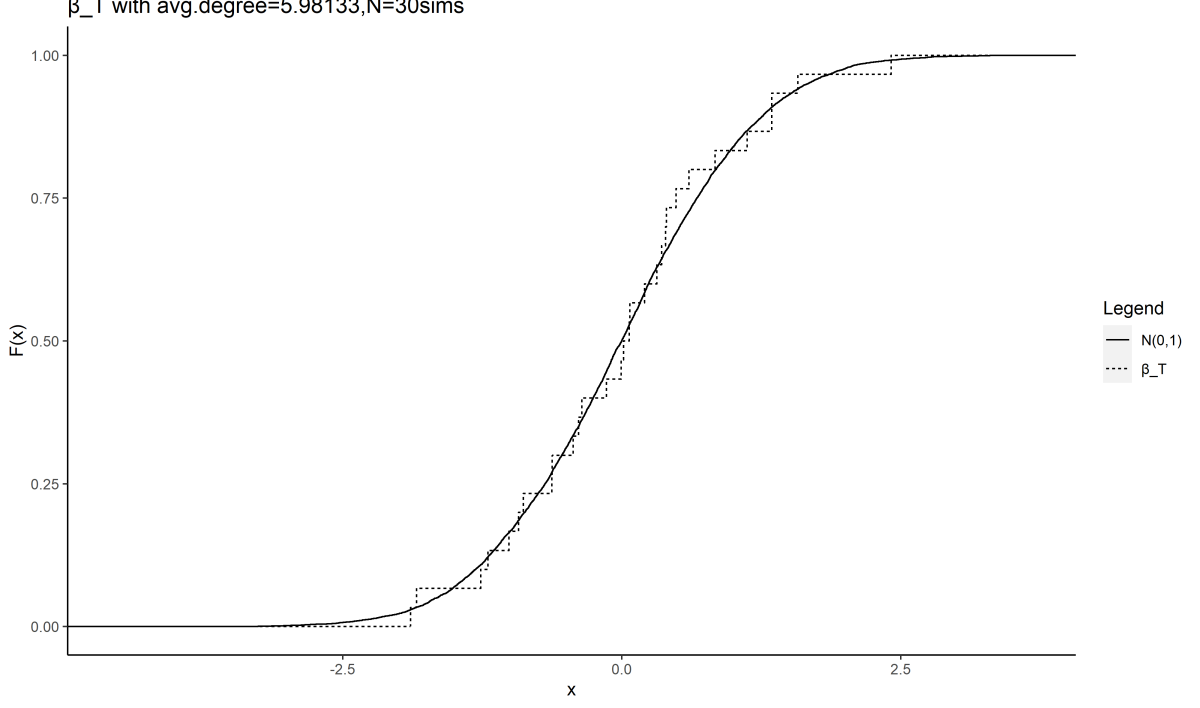

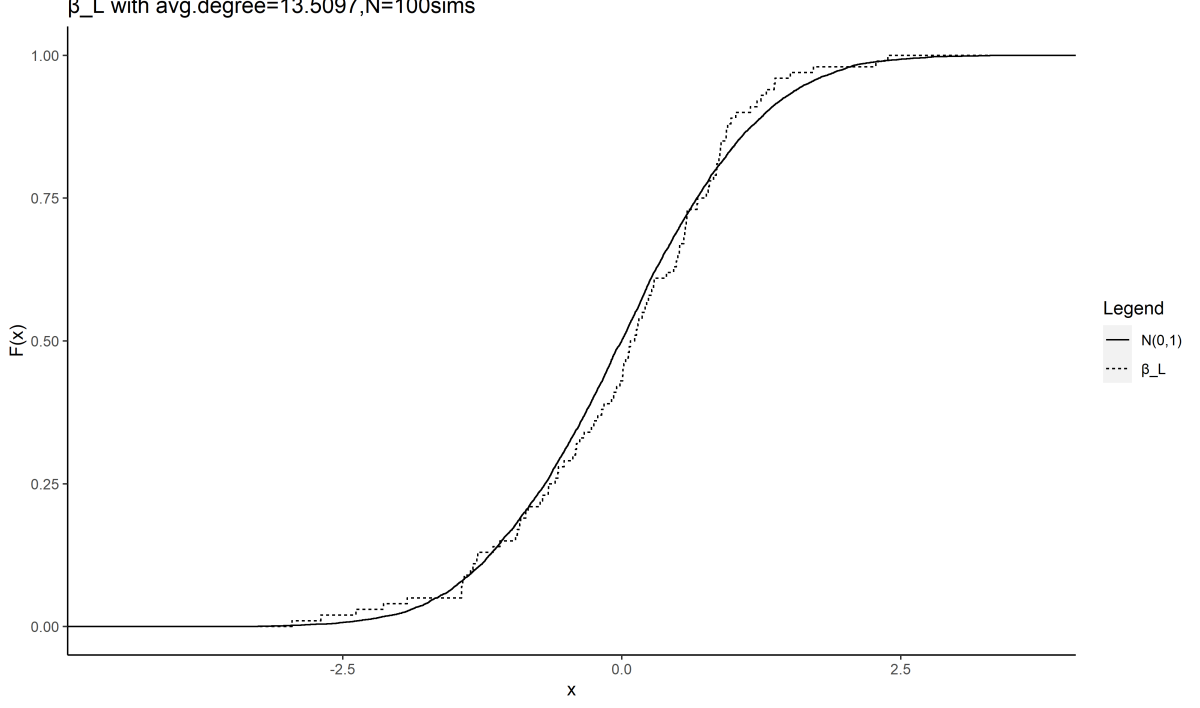

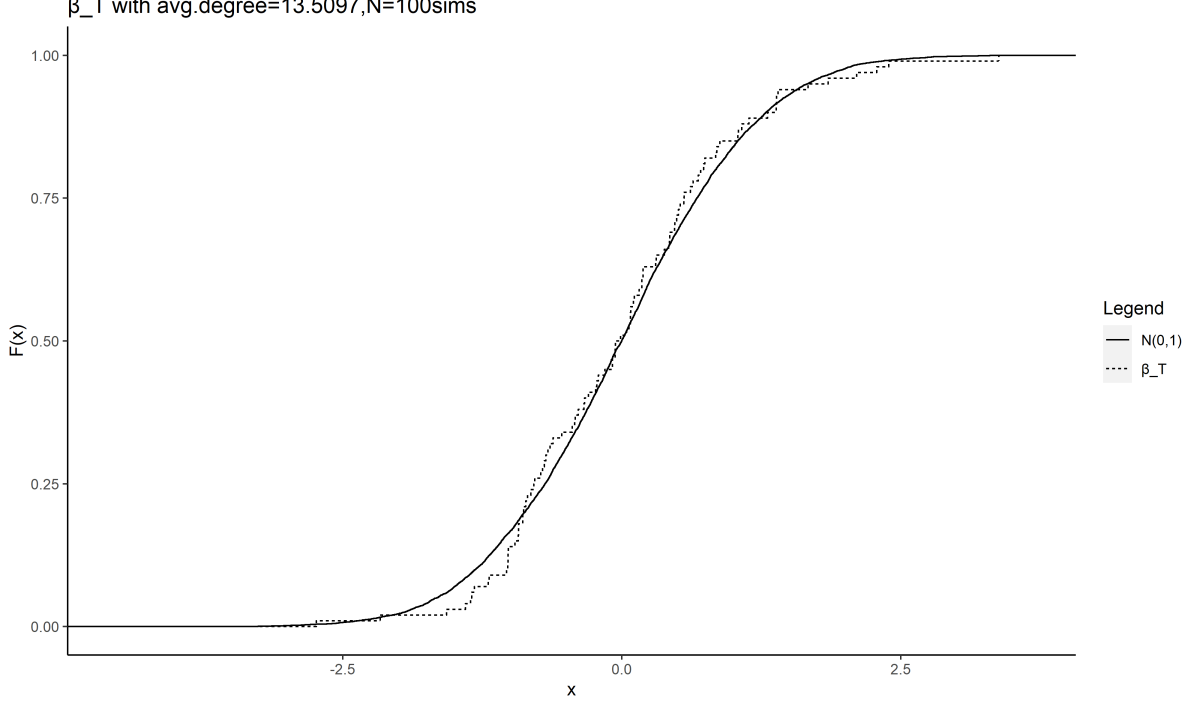

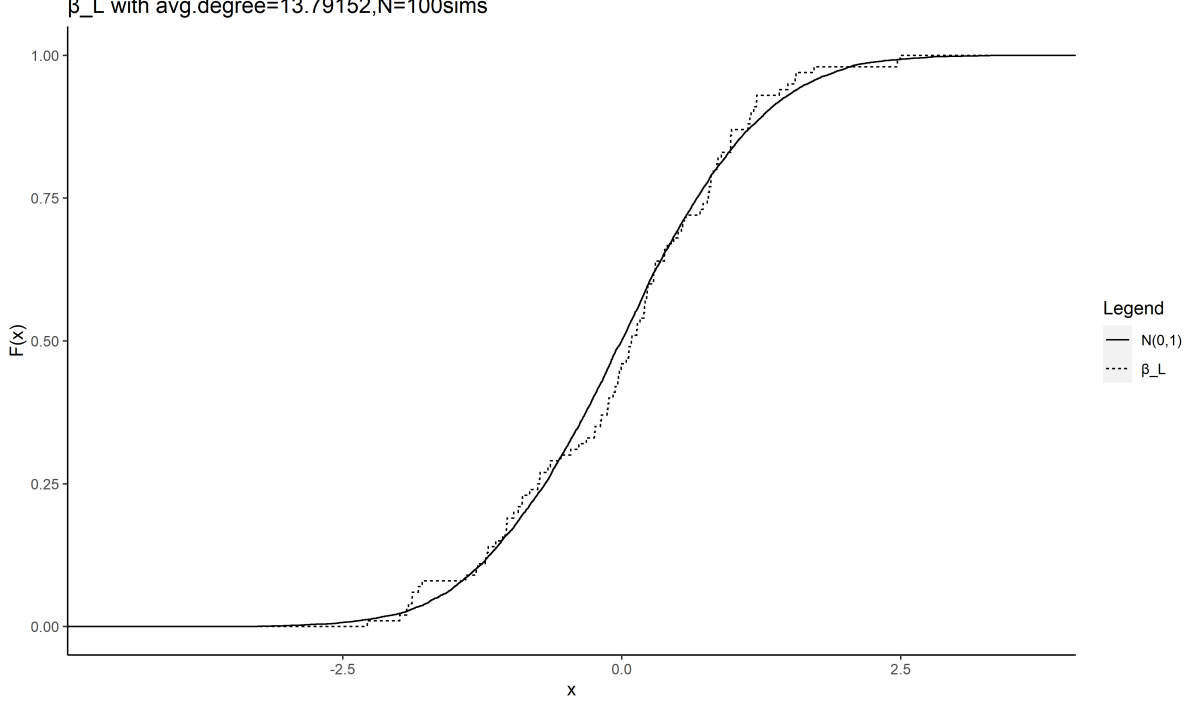

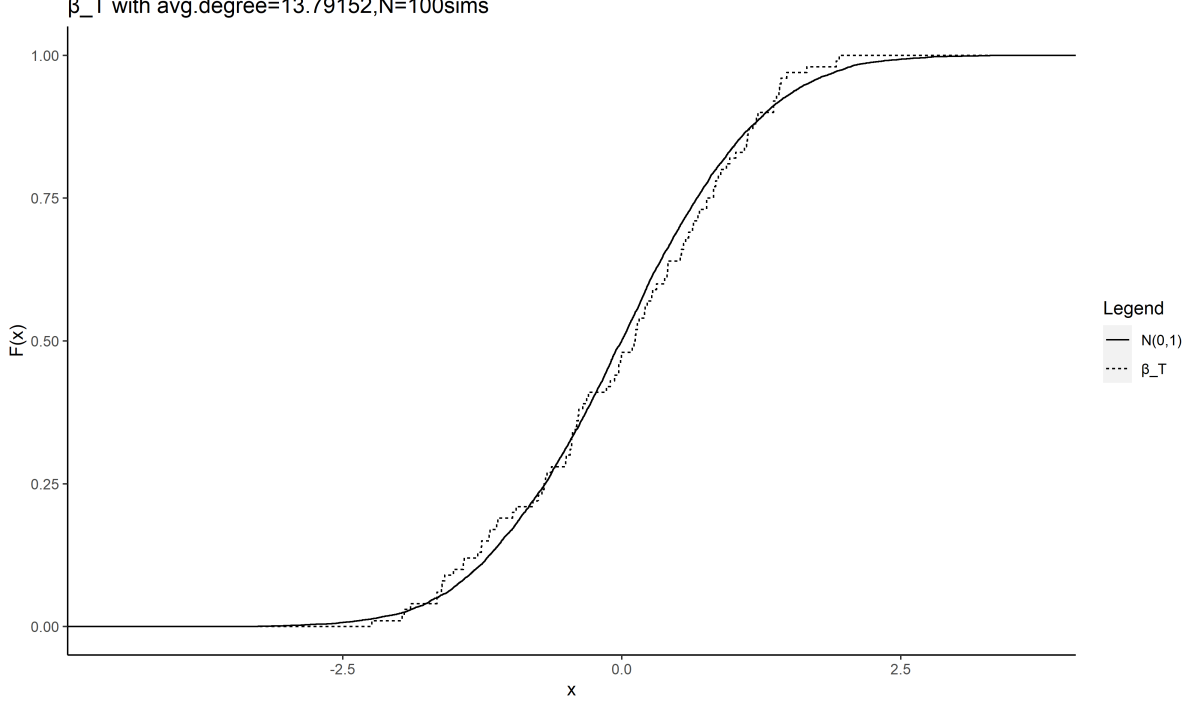

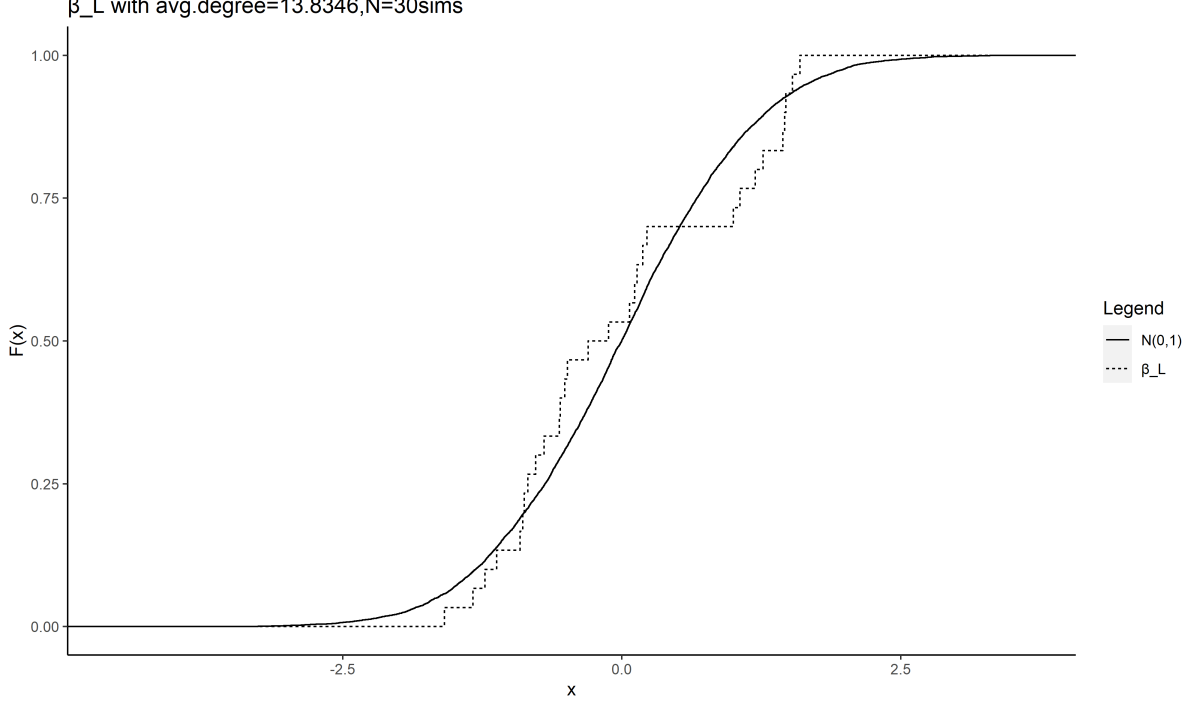

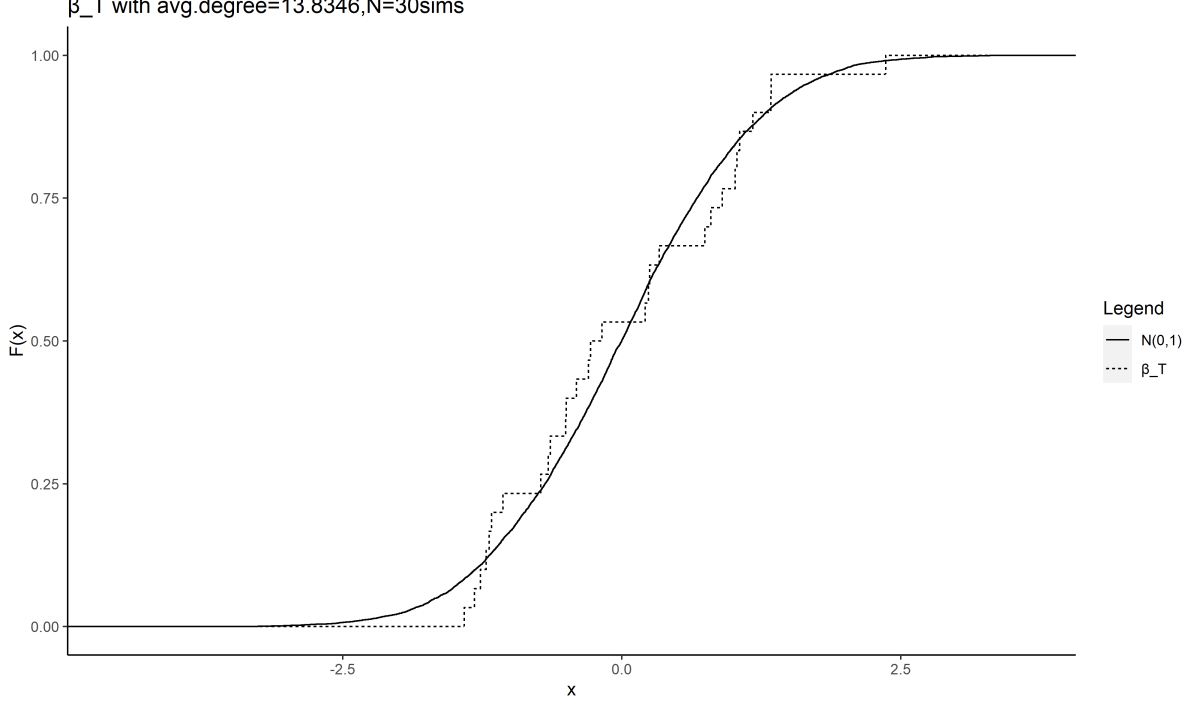

Appendix D provides simulations verifying consistency, asymptotic Normality, and covergence. We also show how and both perform well when incidental generation is sufficiently small but that as the networks become denser is biased while is consistent.

We let possibly depend on and/or as described below. We take the list of the types of subgraphs to be analyzed to be fixed.

4.2. The Many Networks Case

We keep the presentation of this first frame brief since it follows standard statistical arguments (e.g., Newey and McFadden (1994)).

One has a collection of networks, each drawn independently according to a SUGM with the same parameter vector . We hold fixed. Theorem 2 states that a maximum likelihood estimator of the parameters is consistent and asymptotically Normally distributed.

Theorem 2.

Consider a SUGM of distinct types of subgraphs with , for a compact subset of . Let for denote i.i.d. draws from this distribution. Let denote the maximum likelihood estimator Then If in addition is non-singular, then

Although Theorem 2 demonstrates that a consistent and asymptotically Normally distributed estimator exists, calculating the likelihood function of arbitrary networks as a function of the parameters can be computationally intensive for large networks. Thus, we also present a result on a minimum distance estimator which is computationally straightforward since it simply involves calculating frequencies of certain subgraphs. We present it based on links and triangles as the typical case that researchers will need, but the technique extends as a researcher requires. As before, let and denote the fraction of links and triangles in the network , with .

Proposition 2.

Consider a SUGM of links and triangles with parameters , a compact subset of . Let for denote i.i.d. draws from this distribution. Let denote the minimum distance estimator,

Then,

where and .

4.3. The Large Network Case

Next we turn to the case where researchers have access to at least one large network (modeled as ). For the exposition, we let , but clearly this extends directly to having observations of more than one network.

This case is considerably more challenging as it involves correlated observations generated within a network. Network data tend to be sparse, but still have local patterns such as clustering, so that people have relatively few connections compared to the potential number of links, but where a person’s neighbors tend to be linked to each other with much higher than an independent probability (e.g., see the background in Newman (2003); Jackson (2008)). Such clustering is the challenging aspect of the asymptotics since subgraphs are not only directly generated but also incidentally generated. Thus, we need new techniques for our asymptotic results.

4.3.1. Sequences of Large Random Networks

To describe how parameter estimates behave as a function of the number of nodes , it is useful to allow the parameters to also be indexed by . This approach is standard in the random graphs literature (e.g., see the classic book of Bollobas (2001)) as it is needed to accommodate most applications. Specifically, research on social networks has long observed that parameters need to adjust with the number of nodes. For example, friendship networks among a small set of agents (say 50 or 100) and large set of agents (thousands or much more) often have comparable average degrees.222222See Chandrasekhar (2016) for examples networks of varying size ranging from village network data in sub-saharan Africa or India to university dorm friendship network data which all exhibit somewhat comparable number of links per node. As a concrete example, consider friendships among high school students in the U.S. based on the Add Health data set (e.g., see (Currarini, Jackson, and Pin, 2009, 2010)). There are some high schools with only 30 students and others with around 3000 students. The average degree ranges between 6 and 8 over the high schools, but this means that the link probability must shrink dramatically with : average degree corresponds to a link probability of roughly in the small schools, but only in the large schools. Thus, irrespective of the size of their school, students have numbers of friends of the same order of magnitude; and so the true underlying parameters describing friendship formation must decrease with to match the data.

Thus, we consider a sequence of SUGMs with subgraphs that form on nodes that are generated with probabilities . The superscript on the indicates the dependence on to allow for true subgraph formation rates to vary along the sequence.

4.3.2. Direct-Count Estimators for Negligible Incidental Generation

It is convenient to express the s in the form

for some and fixed in . This allows us to encode the rates at which the parameters vary with , and is a general way of encoding the rates that could come from meeting, time budgets, costs, or any other constraints that gives rise to sparse networks.

We consider the case in which (where recall that is the number of nodes in the subgraph of type and is fixed along the sequence), as otherwise the expected number of subgraphs in the whole network could be bounded as grows, precluding estimation.

The researcher can make assumptions on , either its value or the possible range of values that are admissible for their model. In fact, the magnitude may be straightforward to observe with simple subgraph counts. For example, if across networks of varying size, one sees some growing function of links, triangles, and so on, one can infer what values of are needed to be consistent with data. In fact, in most models of network formation, such assumptions are implicitly made, knowingly or not.

We show that even without knowing the or , the parameters can be well-estimated, provided the network model is not so sparse that subgraphs are never observed, nor so dense so that they scale linearly in .

To develop the estimator, first we need some definitions and notation.

Consider a SUGM and order the classes of the subgraphs, , from ‘largest’ to ‘smallest’. In particular, pick an ordering of so that a subgraph in cannot be a subnetwork of the subnetworks in for :

There exists at least one such ordering - for instance, any ordering in which subgraphs with more links are counted before subgraphs with fewer links. In an example with links, 2-stars and triangles: triangles precede 2-stars which precede links. Note that this is a partial order: for instance, a ‘three link line’ is neither a subgraph nor a supergraph of a ‘3-star’ , which is also a three link subgraph on four nodes. It is irrelevant in which order subgraphs with the same number of links are counted.

We count subgraphs in this order after having removed links associated with all of the subgraphs already counted. The resulting counts are denoted :232323Note that counting in order from ‘largest’ to ‘smallest’ subnetworks means that we count things from smallest to largest index since the specification of how we ordered labels moves in the opposite direction of the size of the subgraphs.

The logic of this is that incidental generation is more often in one direction than another: a triangle incidentally generates three links, while it can be much rarer that three links happen to independently form to make a triangle. This manner of counting motivates a simple estimator that we call the direct-count estimator. We then divide by the number of possible subgraphs of that variety.

For the direct count estimator we presume that, for each , includes all subgraphs that are relabellings of each other. Thus, we work without demographics on the subgraphs, but these counts can be adjusted accordingly by normalizing by . Let denote the (finite number) of relabelings to count different subgraphs of type on a given set of nodes.242424For example, note that for a triangle but for a -star it is since each star is different when a different member of the nodes is the center. Then is the number of possible subgraphs of type .

The direct-count estimator is

| (4.1) |

As we prove in Section 4.3.2, under suitable conditions, incidental generation is low and the direct estimators are consistent estimates of the true parameters and are asymptotically Normally distributed.

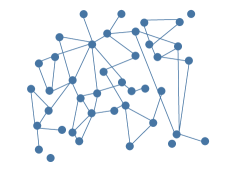

As an illustration, consider Figure 5 in which links and triangles are formed on 41 nodes. There are 9 truly generated triangles, but 10 observed overall. So, the frequency of triangles, , is overestimated by using 10 instead of 9. The true frequency was but is estimated as . With respect to links, there were actually 25 truly directly generated, but one becomes part of an incidentally generated triangle and two others overlap on existing triangles, and so becomes 22 instead. So we estimate while the true frequency was . These errors are already small on a network on just 41 nodes, and as we prove below, the errors disappear completely as grows.

To understand when the direct-count estimator is appropriate, we need to characterize the rate of incidental subgraph formation. To do this we track how many ways a subnetwork could be incidentally generated.

We first provide a precise specification of what it means to be incidentally generated. We say that a subgraph for some can be incidentally generated by the subgraphs , indexed by , if . For instance a triangle 123 can be incidentally generated by links 12, 23, and triangle 134; or by link 12 and triangles 234 and 135, etc. Some of these incidental generations are equivalent to each other (e.g., involve two links and one triangle) and so it is useful to define equivalence classes of generators.

Consider any potential subgraph that can be incidentally generated by a set of subnetworks with associated indices and also by another set . We say that and are equivalent generators of if there exists a bijection from to such that and . So the equivalent generating sets have the same configurations in terms of numbers and types of subgraphs, and in terms of how many nodes each of those subgraphs intersects the given network. For instance a triangle 123 is not only incidentally generated by links 12, 23, and triangle 134; but also by an equivalent generator of links 12, 23, and triangle 135, or links 23, 13; and triangle 128, and so forth.

Given this equivalence relation, we simplify by ignoring the specific labels of subgraphs and defining generating classes for any type of subgraph . We just track the number and type of subgraphs needed, as well as how many nodes each subgraph has intersecting with the given incidentally generated subgraph.

In particular, each generating class of some is a list consisting of a list of types of subgraphs used for the incidental generation and how many nodes each has intersecting with the given incidentally generated subgraph. Thus, is such that there generated by some for which and for each : and . For example, if we consider a triangle, then it can be incidentally generated by two other triangles and a link; and we represent that as , where this indicates that two triangles were involved and each intersected the subgraph in question in two nodes and then indicates that a link was involved intersecting the subgraph in two nodes.

We order generating classes so that the indices are ordered: , and lexicographically whenever . This ensures that we avoid counting the same class twice.252525 However, a generating class of two links and a triangle is a different generating class than one link and two triangles - this numbering just avoids the double counting of two links and a triangle separately from a triangle and two links.

We only need to work with a small set of generating classes, so we restrict attention to the following:

-

•

generating classes that only involve smaller subgraphs: for all , and

-

•

generating classes that are minimal: in the above there cannot be such that .

The first condition states that we can ignore many generating classes because of our counting convention: when counting any given subgraph type, we only have to worry about incidental generation by the remaining (weakly smaller) subgraphs. We do it this way, since we first count the largest subgraphs, and having accounted for them, we worry about the remaining subgraphs, and so forth. The second condition restricts attention to the smallest generators. For instance a triangle could be generated by two links and two triangles. However, in that case either one of the links or one of the triangles can be dropped. The minimal classes for the triangle only involve three subgraphs: three links, two links and one triangle, one link and two triangles, or three triangles. Under the first condition, there are no generating classes for links to worry about, since they cannot be incidentally generated by themselves and we only count them after removing all triangles.

The following conditions ensure that the direct estimation parameters are arbitrarily accurate for large enough networks.

First, for each let

| (4.2) |

This condition ensures that the overall degree of any node grows more slowly than the size of the graph. This comes from the fact that any given node can be a part of subgraphs of type , each of which forms with probability . Expecting over these gives an upper bound on the number of links (up to a proportional constant) that a given node is part of from graphs of type , and the condition is that this be smaller than . The average degree can still grow with , but sublinearly. In particular, this condition ensures that the chance that any given link is part of multiple subgraphs is vanishing.

Next, for each consider any (minimal)262626If the condition is satisfied by minimal classes, it is automatically satisfied by larger classes. generating class with index of subgraphs no larger than . Let

| (4.3) |

and

| (4.4) |

for each .

(4.3) is the requirement that a given subgraph is more likely to form directly than indirectly. governs the direct formation, and governs the rate of incidental generation, and so the exponent on the direction formation must be less than the sum of the exponents of the graphs needed for incidental generation, subtracting off how many variations on each of these there are (captured by the coming from how many nodes are free to be chosen for each incidentally generating subgraph). (4.4) is the requirement that a given subgraph of some type that is part of a generating class of some appear at a fast enough rate to ensure that it is not always becoming part of incidentally generated s, but can be distinguished. This is a similar calculation of rates.

Under these conditions, we prove identification in addition to consistency and asymptotic Normality on a single large network.

Define the variance-covariance matrix

Theorem 3.

Although the conditions may appear hard to understand, they are actually fairly straightforward, and it is easy to see sufficient conditions that ensure them.

For example, suppose that each for some same , so that each node has the same order probability of being a part of different sorts of subgraphs. This is the natural case, as otherwise some subgraphs become infinitely more likely than others.

In that case, all three conditions are automatically satisfied whenever the subgraphs are all cyclic (cliques, or other subgraphs in which all nodes are parts of cycles). If some of the subgraphs are not cyclic (e.g., lines or stars), then all three conditions hold if .

Corollary 1.

Consider a sequence of SUGMs of types of subgraphs with associated true parameters for which . If for each and some and either all subgraphs are cyclic or else , then and .

In both results, although we state them in terms of s, it is also true that the ratio of to , tends to one. Furthermore, as we show in the proof, if we normalize the difference between the estimated probability and the truth by the standard deviation, this is asymptotically Normally distributed. This is an equivalent representation of the above result, but is helpful to note as it does not require knowledge of s but rather just that they satisfy the relevant bounds, which is true of many human networks.

4.3.3. Minimum Distance Estimator for Non-Negligible Incidental Generation

Theorem 3 holds for parameter values for which incidental generation becomes small as a function of the overall counts of the subgraphs, and works for arbitrary subgraph varieties. However, we may want an estimator that works when incidental generation is not ignorable, even in the limit.

For SUGMs with specific subgraph types, we can explicitly calculate all the incidental rates and account for them, and develop an estimator that is more accurate in small samples where there can be nontrivial incidental generation and also works asymptotically even when there is incidental generation. In particular, in this section we consider a links and triangles SUGM based and provide an estimator that fully accounts for incidental generation (with extensive details in Appendix C). We prove identification as well as consistency and asymptotic Normality of a minimum distance estimator.

In order to show the properties of the minimum distance estimator, we show that the following moments converge:

and jointly as well, where and . Since

and and are correlated for any , involves correlated random variables, and since any two triples in that involve a common link are correlated, we need to prove a central limit theorem that shows that such correlation does not cause problems.

Let be the stacked vector of both shares. It is useful to define the variance-covariance matrix of the moments

Finally, let . With this defined we can state our result.

Define the minimum distance estimator for a single large network by

Proposition 3.

Consider a links and triangles SUGM with associated parameters with such that . Then the minimum distance estimator is consistent, , and 272727The expression for is different when , and is given in the proof of the proposition. and asymptotically Normal, .

Proposition 3 covers a wide range of link and triangle densities, ranging from average degree on the order to for any . This covers the order constant and logarithmic growth rates of average degree studied in the literature (Newman et al., 2001; Bollobas, 2001; Jackson, 2008; Graham, 2017), for instance.

In particular, Proposition 3 covers situations in which the rate of incidental generation (e.g., the proportion of triangles that are generated incidentally) does not vanish asymptotically. Not only does the estimator have better small sample properties (see the simulations below), but it also works asymptotically in cases that Theorem 3 does not.

The restrictions are easily interpretable. ensures that triangles are not so numerous that almost all of the links in the network lie in triangles: that does not dwarf . ensures the opposite: that triangles are not always incidentally formed by links and never formed directly: is not dwarfed by . ensures that links and triangles are disentangled by imposing a density cap. Finally, ensure that there is information in the network—enough links and triangles are present to estimate their formation.

Again we note that although the results are stated in terms of , these are equivalent statements to saying that ratio of the estimated () and true () frequencies tend to one. And, that, when self-normalized by the standard deviations, the empirical frequencies estimated are asymptotically Normally distributed. Thus, the result requires no knowledge of s other than that they satisfy the relevant bounds.

4.3.4. Discussion of incidental generation and estimators

It is instructive to summarize the difference in assumptions and performance of and . Again, the first requires more sparsity—less incidental generation specifically—than the latter. Relative to Theorem 3, we can see that Proposition 3 covers cases where incidental generation is not ignorable. Namely, one can check that our result on the requires (which means that the probability of a triangle is going to faster at a rate faster than ). But only requires a rate faster than or . This means that triangles (and therefore links, checking the conditions) can appear at a faster rate and still be estimated under the minimum distance estimator but not through direct-counts. We also see evidence of this in our simulations, in Appendix D, where for very sparse networks both estimators give the same result but the direct-count becomes biased as we increase density whereas the minimum distance estimator remains unbiased.

5. Applications

SUGMs are useful for a number of purposes. First, purely as a statistical modeling tool, SUGMs—even ones with just links and triangles—generate higher-order features of empirically observed social networks that link-based models (even those accounting for characteristics, unobserved characteristics, geography, and latent locations) cannot. This is important for prediction. For example, if one wants to see which networks might form under a hypothetical policy, a model is only useful if it can generate networks that are likely to occur at a variety parameter values. As we demonstrate, our model outperforms stochastic block models, models with node-level fixed effects, latent space models, and ERGMs in generating realistic distributions of networks even with considerably fewer parameters (e.g., 4 parameter SUGMs versus over 200 (or even 400) parameters in some alternatives).

Second, a SUGM can be used to test which incentives underlie link formation. There are many theories (e.g., Coleman (1988); Jackson, Rodriguez-Barraquer, and Tan (2012)) predicting that triangles and other cliques play special roles in maintaining cooperation in favor exchange. In order to test such theories, we need a statistical model that allows us to test whether cliques appear significantly more often than being randomly generated by links, and whether they appear in configurations that would be predicted by the game theory.

Third, SUGMs can be used for structural estimation. There are parsimonious microfoundations—models of mutual consent or search—that give rise to SUGMs. Structural parameters are useful for welfare analyses, and also aid in examining counterfactuals or policy evaluation. Such parameters are recoverable from SUGM parameters.

We provide three examples. Our first example shows that SUGMs model a myriad of network features much better than other standard models. The other two examples build models of network formation to address specific economic questions. In both cases, the equilibrium network is a random draw from a SUGM with interpretable parameters.

5.1. Data

We use the Banerjee, Chandrasekhar, Duflo, and Jackson (2013, 2019) data consisting of a variety of social and economic networks from 75 Indian villages as well as detailed demographic background.282828See Banerjee, Chandrasekhar, Duflo, and Jackson (2013) for more information about the data. Having 75 villages allows us to show not only how the model scales with the number of nodes, but also to cover both of our asymptotic frames.

The networks have households as nodes. There are an average of households per village. We surveyed adults, asking them about a variety of their daily interactions, as well as their demographics (caste, education, profession, religion, family size, wealth variables, voting and ration cards, self-help group participation, savings behavior, etc.). We have network data from 89.14 percent of the 16,476 households based on interviews with 65 percent of all adults between the ages of 18 and 55. We have data concerning twelve types of interactions: (1) whose houses he or she visits, (2) who visits his or her house, (3) his or her relatives in the village, (4) non-relatives who socialize with him or her, (5) who gives him or her medical help, (6) from whom he or she borrows money, (7) to whom he or she lends money, (8) from whom he or she borrows material goods (e.g., kerosene, rice), (9) to whom he or she lends material goods, (10) from whom he or she gets important advice, (11) to whom he or she gives advice, (12) with whom he or she goes to pray (e.g., at a temple, church or mosque).

The answers are aggregated to the household level, but one can also work with the individual-level networks to get similar results to those presented below. How a link is defined varies based on the application. We use undirected,292929Some links are not reciprocated, but that is true at similar rates for the questions regarding relatives as compared to the other questions, and so much of the failure of reciprocation may simply be measurement error rather than true one-way relationships. For our purposes here, which are purely to illustrate the ability of the models to match data, this distinction is inconsequential. unweighted networks that may allow for multiplexing. This also means that we observe 98.8% of the potential links between pairs.303030This is a new wave of data relative to our original microfinance study that includes more surveys. Note that .

For much of what follows, we work with the borrowing and lending of material goods (questions 8 and 9, with any positive answer indicating a link being present) that we call “favor” links, and the exchange of advice (questions 10 and 11, with any positive answer indicating a link being present) that we call “info” links.

5.2. Example 1: Matching Features of Empirical Network Data

A challenge for network formation models has been to capture more than one or two observed features of networks at a time. For instance, many observed social networks are sparse but clustered, which motivates developing models that reflect this (Watts and Strogatz, 1998). They also have a variety of differing degree distributions ((Barabasi and Albert, 1999; Jackson and Rogers, 2007) and exhibit high levels of homophily (McPherson, Smith-Lovin, and Cook, 2001; Currarini, Jackson, and Pin, 2009, 2010), which can lead to poverty traps and inequalities (Calvo-Armengol and Jackson, 2007; Jackson, 2023). There are also features such as the expansion properties of a network that are described by maximal eigenvalue of the adjacency matrix and governs diffusion processes operating on the network (Bollobas (2001)). The depth of the max flow min cut speaks to several things such as consensus time in a social learning process Golub and Jackson (2012) as well as the sustainable degree of cooperation (Karlan, Mobius, Rosenblat, and Szeidl, 2009).

We show that a SUGM fits economically-relevant network features in the data far better than four prominent alternatives. Importantly, these features were not used to fit the model. They are the size of the giant component, average path length, and various spectral properties of the adjacency matrix (e.g., the largest eigenvalue and an eigenvalue measure of homophily). A simple SUGM outperforms the alternative models despite the fact that the alternative models have many more dimensions such as numerous covariates, fixed effects, or even latent space variables, that should give them an advantage in fitting.

Specifically, the alternative models are (a) a standard stochastic block model that includes flexible controls for continuous covariates that influence edge probabilities; (b) an extension of that model that includes parameters to capture node fixed effects (e.g., Graham (2017)); (c) a latent space model (Hoff, Raftery, and Handcock, 2002) in which nodes have unobserved arbitrary locations in to be estimated and the probability of linking declines in their latent positions; and (d) an exponential random graph model with links, triangles, and a rich set of covariates.

Before we proceed, we review the features of the graph structure that we examine and why they are interesting. We look at the first eigenvalue of the adjacency matrix, which is a measure of diffusiveness of a network under a percolation process (e.g., Bollobás, Borgs, Chayes, and Riordan (2010); Jackson (2008)). This is intimately related to the expansiveness of the network—namely, for any subset of nodes the number of links leaving the subset relative to the number of links within the subset. We are also interested in the second eigenvalue of the stochasticized adjacency matrix.313131The stochasticized adjacency matrix is defined as , where either , or for some , as this captures the set of people to whom listens. This is a quantity that is key in local average learning processes and modulates the time to consensus (DeMarzo, Vayanos, and Zwiebel (2003); Golub and Jackson (2012)), but is also closely related to homophily (Golub and Jackson (2012)) and is labeled as such in the table below. Additionally, we look at the fraction of nodes that belong to the giant component of the network, as well as the number of isolates, as empirical networks are often not completely connected. Finally, we also consider average path length (in the largest component).

We present the results for favor and info networks. These networks are reasonably connected (with more than ninety percent of the nodes being in the giant component) and yet also typically sparse.

Our procedure is as follows. For every village, we estimate six network formation models.

One network formation model is a link-based model (stochastic block model) in which the probabilities can depend on geographic distance, caste, the number of rooms households have, number of beds, quality of electricity provision, quality of latrines, household ownership status, and squared differences in non-binary variables. The probabilities are estimated using logistic regression and the model has 12 parameters.

The next is the model of Graham (2017). This is the same formulation of the preceding model, but adds unobserved heterogeneity in the form of node-fixed effects,

where is the logit link function and is the aforementioned vector of demographic characteristics and polynomials therein. This model has +12 parameters per network.323232Consistency of all in addition to has been proven for a dense sequence of graphs (e.g., Chatterjee et al. (2010); Graham (2017)).

The third model is a latent space model,

where now are unobserved positions in .333333We use as Euclidean is commonly used in the literature, though it is not the only choice. The subject of choice of geometry is addressed in Lubold, Chandrasekhar, and McCormick (2023), which shows how to check isometric embedding conditions. In this data we find that 25% of networks are not consistent with any latent space from the family of simply connected, complete Riemannian manifolds of constant curvature, lending evidence to the idea that latent space models may not be a universally appropriate device to model correlation. This has parameters.

The fourth model is a links and triangles ERGM with covariates. Specifically,

Turning to SUGMs, in contrast, we consider only low-dimensional models. One is a the basic SUGM with links and triangles. Pairs of household are categorized as either being “close” or “far,” where “close” refers to pairs of nodes that are of the same caste and “far” to those that differ in caste. Similarly, we categorize triangles as being “close” if all nodes are of the same caste and “far” otherwise. Thus, we allow for four parameters, close and far link parameters and close and far triangle parameters. The other model is a slightly richer SUGM in which we allow some nodes to be isolates, which adds one more parameter.343434With isolates, in a first stage some nodes are randomly chosen to be isolates with a given probability. For the subsequent formation of other subgraphs, those isolates can be considered as removed from the set of nodes and no subgraph that involves them forms in the subsequent subgraph formation. Neither includes any other demographic covariates nor unobserved heterogeneity. We estimate both via the minimum distance estimator of Proposition 3, , since there appears to be enough incidental generation that needs to be accounted for.

To make the strongest point, we compare these stark SUGMs that use only same/different caste variables to account for homophily, to very rich covariate dependent (block) models that can incorporate a large set of covariates – including much richer demographics that are usually available to a researcher as well as node-level fixed effects in the unobserved heterogeneity model and node-level latent locations in the latent space model. We show that even though we have considerably more information on the nodes, such as geographic distance and demographic characteristics, and allow for such unobserved heterogeneities—and we do not make use of this information for the SUGMs—they recreate networks much more accurately than a link-based model that does takes advantage of a rich set of node characteristics. Adding over 12 parameters to the block model to flexibly control for demographic attributes, or even +12 parameters with unobserved heterogeneity or with latent locations, does not come close to doing as well as the simple SUGMs. Moreover, since the specification developed here makes use of considerably richer data than those used in the two candidate SUGM models, it suggests that by decomposing a network into a tapestry of random structures (triangles, links, and even isolates), considerable value is added in modeling higher order features of networks in a parsimonious way.

We estimate parameters village-by-village for each model and then generate random network from each model based on the estimated parameters. We do 100 such simulations for each of the 75 village and for each of the models. We then compare the true network characteristics with those from the simulations.

![[Uncaptioned image]](/html/1611.07658/assets/x5.png)

Table 1 presents the results. Both of the SUGMs match the features of the networks substantially better than the conditional edge independent models (with and without node fixed effects). Including isolates in the SUGM further improves the fits not only for isolates, but also for fraction in the giant component and the maximum eigenvalue. This suggests that there are more isolated households in a village for a reason beyond randomness in network formation.

An obvious thing to note is that the link-based and also latent space models do extremely poorly when it comes to matching clustering while the SUGM does much better, and here adding unobserved dimensions to generate unconditional link correlations (e.g., clustering) does worse than a SUGM that allows correlated link formation directly. The ERGM performs better on clustering but a the cost of generating excessive density, diffusiveness, the spectral cut (homophily), connectedness, and average path length.

Including triangles in the SUGM is enough to deliver better matches on all dimensions, and the difference on homophily is perhaps most interesting, since one would imagine that the block models or even latent space models could get that right given that they include many covariates. This tells us that triangles and correlation between links play a subtle but important role in homophily—something that is better picked up by a SUGM than an independent link model even when that model includes rich demographics and unobserved heterogeneity.

It is important that SUGMs do a much better job at recreating a multitude of features of observed network structures that standard link-based models, especially with rich demographic information, models with unobserved heterogeneity, latent space models, and ERGMs. It suggests that there is a substantial value added of modeling the formation of triangles and isolates. Knowing that our model is better able to capture the realistic correlation of links within observed networks should make us more confident in trusting the results of some other empirical applications. For example, when we look at links across social boundaries, we can be comfortable that to a first order, thinking about a SUGM with links and triangles across and within caste groups can do a good job of matching patterns in the data, and thus tracing them back to model parameters.

5.3. Example 2: Do incentives for risk sharing drive network formation?

5.3.1. A model of mutual consent

Consider a simple model in which individuals get utility from being in bilateral relationships, denoted by , as well as trilateral relationships, denoted by . The value of a partner to in a bilateral relationship is a function of their demographics (given by vector ) is given by :

where is a distance or other function comparing the demographics—for instance to allow for homophily. Similarly, the value of a triangle of relationships to is given by :

where is a function that is symmetric in arguments, and is a function that is symmetric in the last two arguments. The value of the relationships depend on the characteristics of the people involved, as well as some idiosyncratic values to the relationships, and , which may capture personalities, compatibilities, etc., distributed according to some distributions and respectively.

Forming relationships requires mutual consent (e.g., the pairwise stability of Jackson and Wolinsky (1996)), so the net utility must be positive to all agents. The probability that a subgraph forms is

and similarly the probability that subgraph forms is

The products capture that a link requires two consents and a triangle requires three.

By estimating the probabilities of subgraphs forming ( and ), under suitable assumptions described below, one can recover the marginal effects of changes in covariates on preferences for being in various configurations ( and ). Since we have finite support for covariates, we label the subgraph formation probabilities and for pair and node covariate combination and respectively.

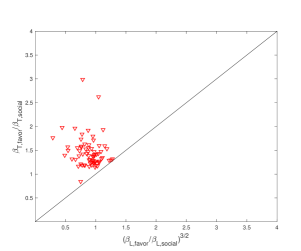

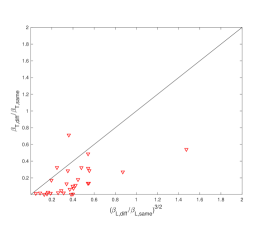

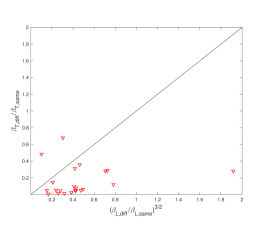

5.3.2. Incentives for Risk-Sharing

Jackson, Rodriguez-Barraquer, and Tan (2012) show that whether or not a link is supported can play an key role in maintaining informal favor exchange when it would not be self-sustaining without social pressure. It characterizes renegotiation-proof and robust pairwise stable networks and shows that (in the homogenous parameter case) all networks that incentivize exchange are quilts (a union of cliques with no cycle involving more than the minimal clique-size number of nodes), and in the inhomogenous parameter case every link must be supported (if are linked then there exists such that ).

Consider a variation on this model wherein now there are multiple link types: favors and information. We can use this to study the question raised by Jackson, Rodriguez-Barraquer, and Tan (2012). To make this simple ignore covariates, so all nodes are identical. Preferences are described by a random utility framework (McFadden, 1973), with the value of a link between and to given by

and the value of a triangle given by