Asymptotics for the expected shortfall

Abstract

We derive the joint asymptotic distribution of empirical quantiles and expected shortfalls under general conditions on the distribution of the underlying observations. In particular, we do not assume that the distribution function is differentiable at the quantile with strictly positive derivative. Hence the rate of convergence and the asymptotic distribution for the quantile can be non-standard, but our results show that the expected shortfall remains asymptotically normal with a -rate, and we even give the joint distribution in such non-standard cases. In the derivation we use the bivariate scoring functions for quantile and expected shortfall as recently introduced by fisszieg2015elicitability. The main technical issue is to deal with the distinct rates for quantile and expected shortfall when applying the argmax-continuity theorem. We also consider spectral risk measures with finitely-supported spectral measures, and illustrate our results in a simulation study.

Abstract

We provide additional details to the paper zwingHolz2016.

1 Introduction

Value-at-risk (VaR) and expected shortfall (ES) are two popular measures of the risk of a financial position (mcneil2010quantitative). While the VaR is simply a quantile of the profit-and-loss-distribution, the ES is defined as the average below a certain quantile. Thus, the ES is deemed to be more informative, and indeed fulfills the desirable property of subadditivity which the VaR lacks in general (artzner1999). On the other hand, the VaR is elicitable (gneiting2011) in the sense that it can be represented as a minimizer of an expected loss, which is, however, not possible for the ES.

Statistical estimation of a given -quantile, , is a very-well developed problem. Precise asymptotic expansions, called Bahardur expansions, for the empirical quantile have been developed if the underlying distribution function has a density which is positive and sufficiently regular at the -quantile (bahadur; kiefer). This expansion in particular implies the asymptotic normality. In this regular case, an alternative quantile estimator based on a smoothed empirical distribution function has been proposed by chenTang2005 to improve finite-sample mean-square-error properties. The general case in which the distribution function is not differentiable at the -quantile or in which its derivative vanishes was studied in smirnov1952limit and Knight2002LimDistr. Here, non-normal limit distributions and slower rates of convergence than occur.

The ES at level can be estimated as the empirical average below the empirical -quantile. scaillet2004 proposed instead to use a smoothed version of this estimator. chen2008 proved asymptotic normality of these estimators and further showed that no improvement in terms of mean-square-error properties can be expected for the smoothed estimator. Further work on the asymptotic properties of ES estiamtors are linton2013 and hill2013 for heavy-tailed distributions, and peracchi2008, taylor2008, cai2008 and kato2012 in a nonparametric regression framework.

All these papers require that the distribution function is quite regular at its -quantile, having a smooth and positive density as required for asymptotic normality when estimating the quantile.

Here we show that this assumptions is not required for the expected shortfall, and that the simple estimator of the ES remains normal under the weak assumption that the distribution function is continuous and strictly increasing at its -quantile. We even determine the joint asymptotic distribution of the estimators for -quantile and expected shortfall in this general case. Our approach is based on the argmax-continuity theorem, e.g. vdv2000asympstat, by using the scoring functions for the bivariate parameter, quantile and ES, as recently introduced by fisszieg2015elicitability. Because of the different rates of convergence for quantile and ES, application of the argmax-continuity theorem is not straightforward and requires substantial technical effort.

The paper is organised as follows. In Section 2 we introduce the expected shortfall and the bivariate scoring function for quantile and expected shortfall, and discuss the resulting minimum-contrast estimators. Section 3 presents our results on the joint asymptotic distribution of quantile and expected shortfall, also in the multivariate case for various levels. We further discuss asymptotic properties of estimators of spectral risk measures with finitely supported spectral measures. Section 4 contains simulations in two scenarios, once for a kink in the distribution function, and once for a density with a zero of order two. In Section 5 we indicate properties of the bootstrap, and also extensions to dependent data. Proofs of the major steps are deferred to Section 6, while some details are relegated to the technical supplement zwingHolzm2016.

In the rest of the paper, we use the following notation. For i.i.d. observations distributed according to the distribution function , we use the notation

where . Note that is the empirical expectation w.r.t. . Further, we let denote the order statistics of a sample . We denote by convergence in distribution.

2 Estimating quantile and expected shortfall

Suppose that the random variable has distribution function and satisfies . Given the lower tail expected shortfall of at level is defined by

For the specific value of under consideration, we shall always impose the following.

Assumption. For the given , the distribution function is continuous and strictly increasing at its -quantile .

Then has a unique -quantile, and the empirical quantile

is a consistent estimator for . Further, for the expected shortfall we have that

| (1) |

Consider the class of strictly consistent scoring functions for the bivariate parameter as introduced by fisszieg2015elicitability,

| (2) | ||||

where is a three-times continuously differentiable function, and it is required that . From the proof of Corollary 5.5 in fisszieg2015elicitability, one may choose so that . Denote the asymptotic contrast function by

then has a unique minimum in .

Let be i.i.d., distributed according to with . Consider the minimum contrast estimator for the bivariate parameter defined by

As the proposition below shows, this is, at least approximately, simply another way of representing standard estimators for quantile and expected shortfall.

Proposition 1.

The estimator can be chosen equal to the empirical quantile. Further, the estimator is given by

| (3) | ||||

and we have that

The empirical expected shortfall may be defined to be

As the proposition shows, the estimator is, up to a term of order , equal to this empirical expected shortfall. Thus, its asymptotic properties will be identical to those of .

3 Joint asymptotic theory for quantile and expected shortfall

We start the asymptotic analysis by providing a general consistency result.

Proposition 2.

Let be a consistent estimator of . Then the estimators

are consistent for . In particular, is consistent.

Now we turn to the joint asymptotic distribution of quantile and expected shortfall.

One major issue is to include the case of low regularity of at its -quantile . In particular, we do not impose the standard assumption that has a positive derivative at . In such more general situations, the limit distribution for the empirical quantile has been analyzed in smirnov1952limit and Knight2002LimDistr.

Consider the following assumption, taken from smirnov1952limit and Knight2002LimDistr.

Assumption [A]: There exists a function with

such that for some deterministic, positive sequence with it holds that

The following proposition, which is mainly taken from smirnov1952limit, recalls the classification of the functions which may occur in Assumption [A] and further shows that, if the empirical -quantile is a consistent estimator for , then Assumption [A] can always be satisfied with a degenerate choice for the function .

Proposition 3.

a. The function in Assumption [A] is necessarily of one of the forms

where and . Moreover, except for the last case with , i.e. with , the sequence is uniquely determined up to asymptotic equivalence.

b. If the empirical -quantile is consistent, so that , then there exists a sequence for which Assumption [A] is satisfied for the limit function .

Here, sequences of positive numbers and are asymptotically equivalent if , . Part b. of the proposition implies that Assumption [A] imposes no additional general restrictions if is strictly increasing and continuous at its -quantile.

Example 1.

Assume that there exists an and functions , which are continuous in with and fulfill

for some . For example, if has a density with a root of order in its -quantile, these assertions are met; see Sections 4.1 and 4.2.

Since we assume strict monotonicity of in , we must have for and hence as well (it is by assumption), and similarly for . Then for , setting we have that for big enough, hence

| (4) |

Similarly for and we have that

| (5) |

Now if , we can choose and

Then the sequence together with the function fulfill Assumption [A].

If , for choosing we have for big enough that

| (6) |

Thus, Assumption [A] is then satisfied for and

The case is treated similarly.

The second assumption will guarantee the existence of a limit variance for the estimator .

Assumption [B]: It holds that .

Now we may state our main result.

Theorem 4.

Under Assumptions [A] and [B], we have that

where are jointly normally distributed,

and

| (7) |

Remark.

The theorem implies that the marginal asymptotic distribution of the estimator is not effected by low regularity of the distribution function at , although rate of convergence and asymptotic distribution of become non-standard. This is not unsurprising, for the following reason. For a known value of the -quantile, one could consider the oracle estimator

which has asymptotic variance . Now

If , which is plausible in applications since we consider the lower-tail expected shortfall, then since the difference will be negative, so that estimating the quantile actually may reduce the asymptotic variance of the expected shortfall. This effect persists even it is quite hard – as in situations with low regularity of at – to estimate the quantile.

Remark.

Chen and Tang (2005) proposed a smoothed estimator of the quantile and showed that higher-order correction of the MSE is possible for appropriate choice of the bandwidth. Scaillet (2004) proposed a smoothed estimator of the expected shortfall, but the asymptotic analysis in Chen (2008) showed that no asymptotic improvement can be expected, thus, Chen (2008) recommends the use of the simple empirical expected shortfall. What is more, the favourable analysis of Chen and Tang (2005) for the smoothed estimator of the quantile depends on regularity of and , roughly a twice-continuously differentiable density. We shall investigate behaviour of the smoothed estimator of the expected shortfall in our less regular situations in the simulation study.

Remark.

The proof of Theorem 4 relies on the argmax-continuity theorem as presented e.g. in vdv2000asympstat, Corollary 5.58. However, this cannot be applied directly since the contrast process does not properly converge when normalized with a single rate, and the proof becomes quite involved.

Example 2 (Example 1 continued).

Next let us extend Theorem 4 to a multivariate version.

For given choose distinct , , and assume as before that is strictly monotone and continuous at each quantile .

Assumption [Ak]: For each and corresponding and , Assumption [A] is satisfied with associated sequence and function .

Theorem 5.

Let [Ak] and [B] hold. Then as ,

where for , and , with as in (7) and the vector distributed according to with determined by

for .

The extension of the proof of Theorem 4 to the multivariate case in Theorem 5 is relegated to the technical supplement.

As an application of the above theorem, consider estimation of spectral risk measures with finite support. For a probability measure on , called the spectral measure, define

as the spectral risk measure associated to . Here, the boundary cases are given by and essinf. If is finitely supported in , is a finite convex combination of expected shortfalls for different levels,

fisszieg2015elicitability show that strictly consistent scoring functions for in this case are given by

where the functions and are as above. If we define the corresponding M-estimator

then we have the following result.

Theorem 6.

We have that

| (8) |

Consequently, under Assumptions [Ak] and [B] it follows that

where the are as in Theorem 5.

4 Simulations

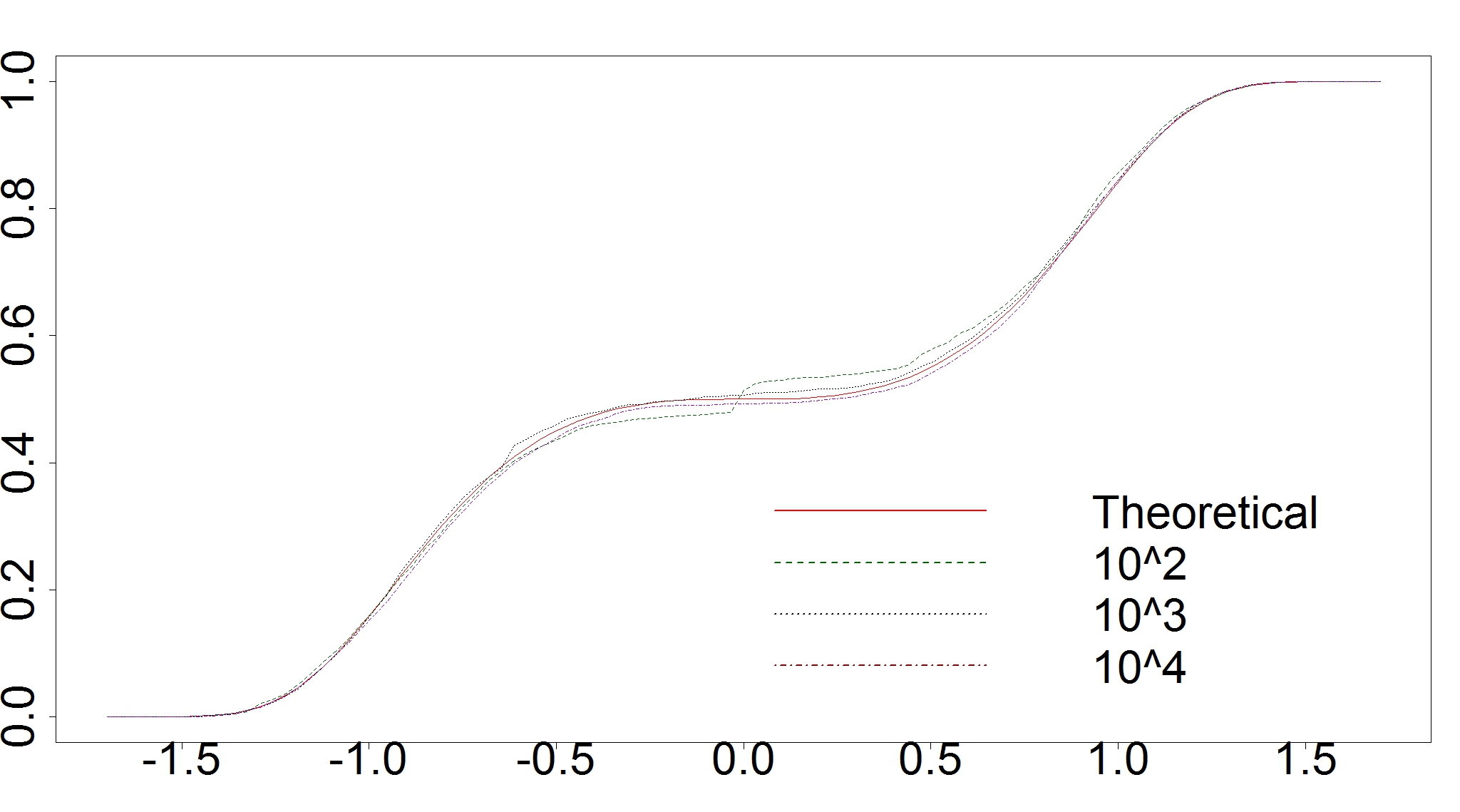

4.1 Distribution function with kink in the -quantile

We let be given by

Then , and the expected shortfall at level is . Further, and , where denote the left- and right-sided derivatives in .

Taylor expansion shows that Example 1 applies with , and

so that

It follows that

where

The limit distribution function of is calculated as

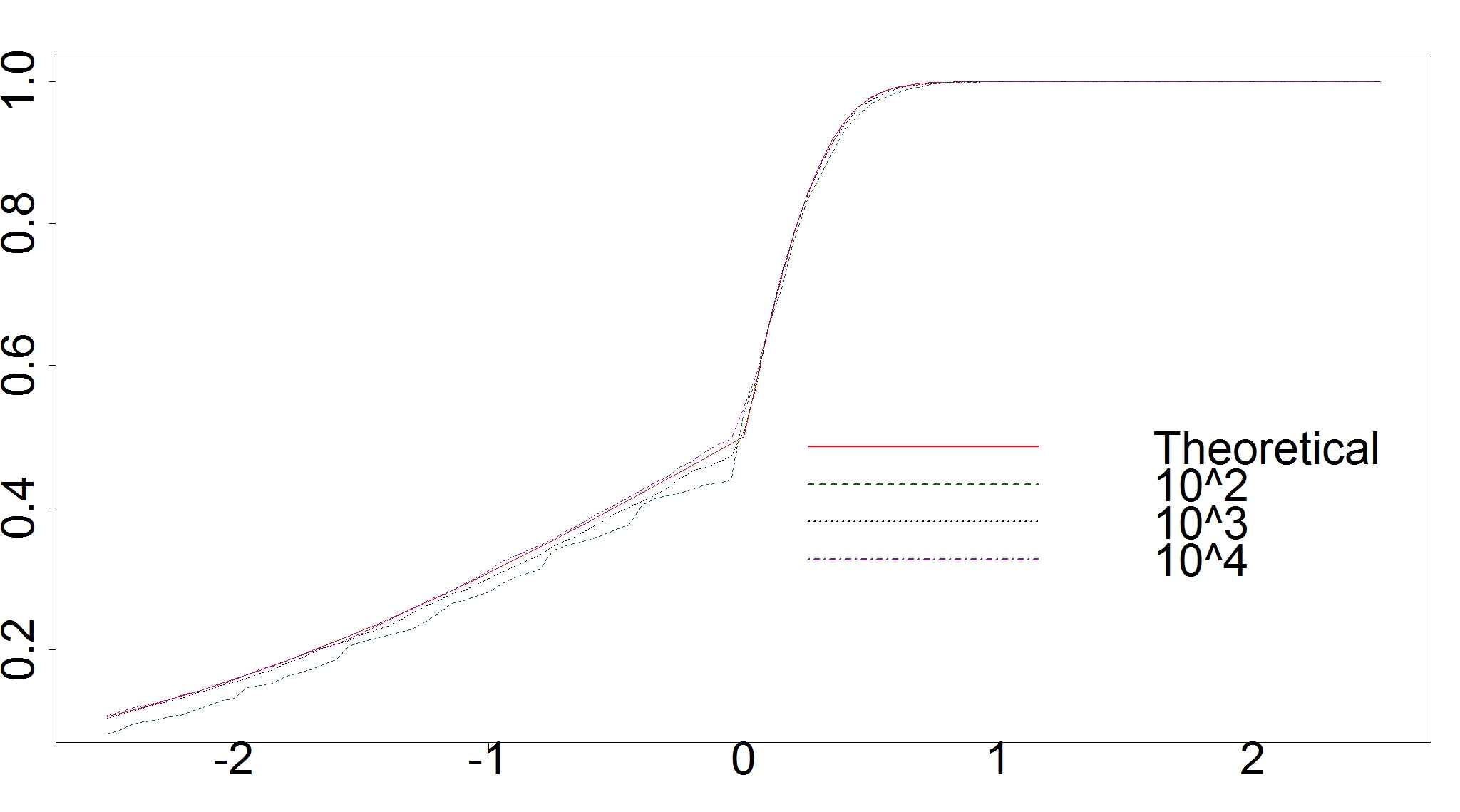

We compute the estimators for simulated samples of sizes , each for iterations, using the using R programming language. Figure 2 shows estimated and asymptotic distribution functions of

for samples of sizes . The approximation is reasonable in both cases also for small sample sizes.

The right picture (b) accordingly shows the estimated and the limit (solid red) distribution function of for (green dashed), (black dotted) and (purple dot-dashed).

Here was chosen for both estimations.

From the same data we in addition computed the smoothed quantile estimator and the estimator for the expected shortfall as proposed in chenTang2005 and chen2008, respectively. Here we used fixed bandwidths chosen as the median normal reference bandwidth of additional training samples.

Table 1 shows the mean and the standard deviation of the centered and rescaled estimators for the quantile and the expected shortfall, as well as their correlation. We observe that the limit distribution of does not have mean , while the mean of seems to diverge. Smoothing the expected shortfall also seems to introduce a small bias, without substantially reducing the standard deviation.

| Samplesize | |||||||

| Mean | |||||||

| Standard | |||||||

| deviation | |||||||

| Correlation | and |

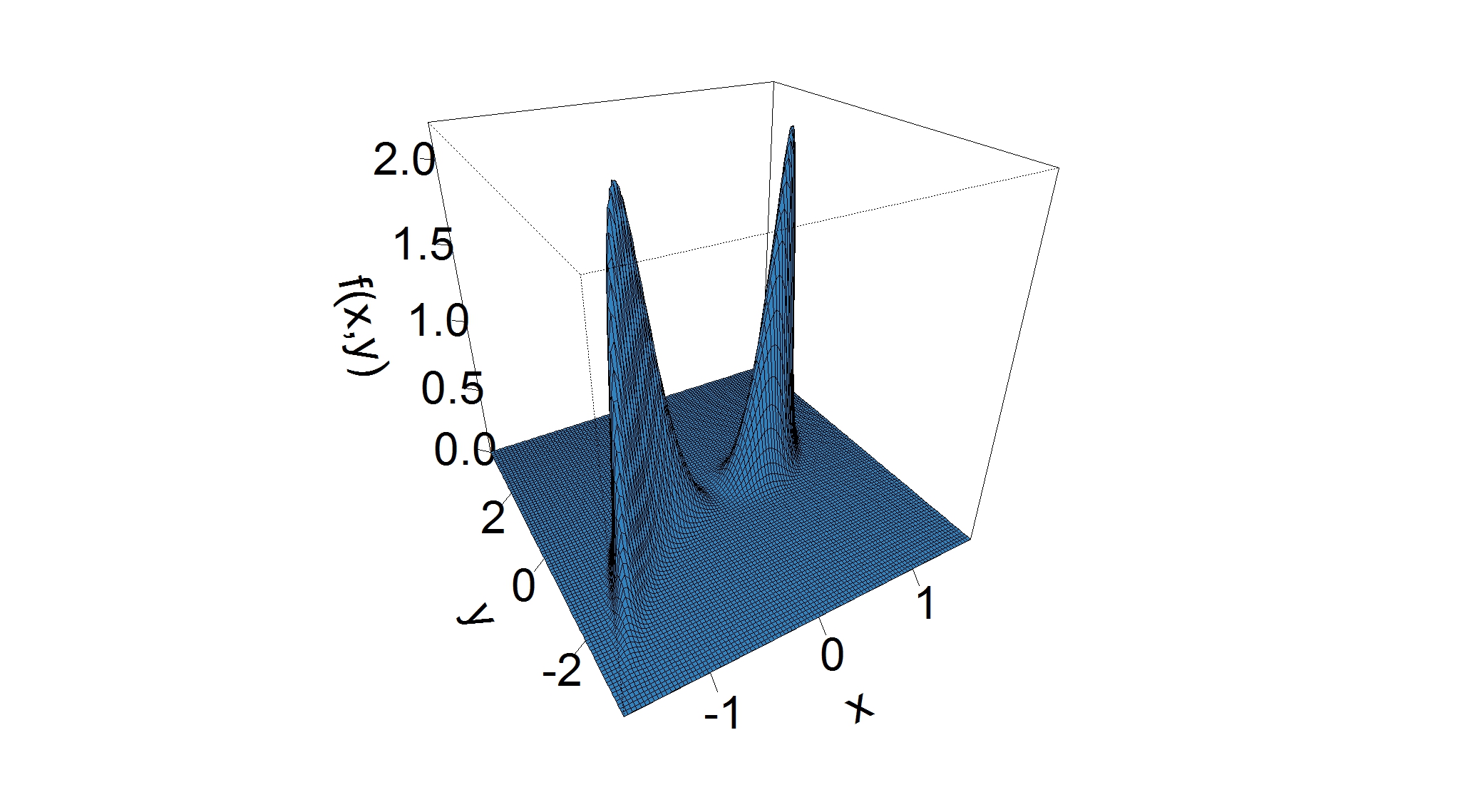

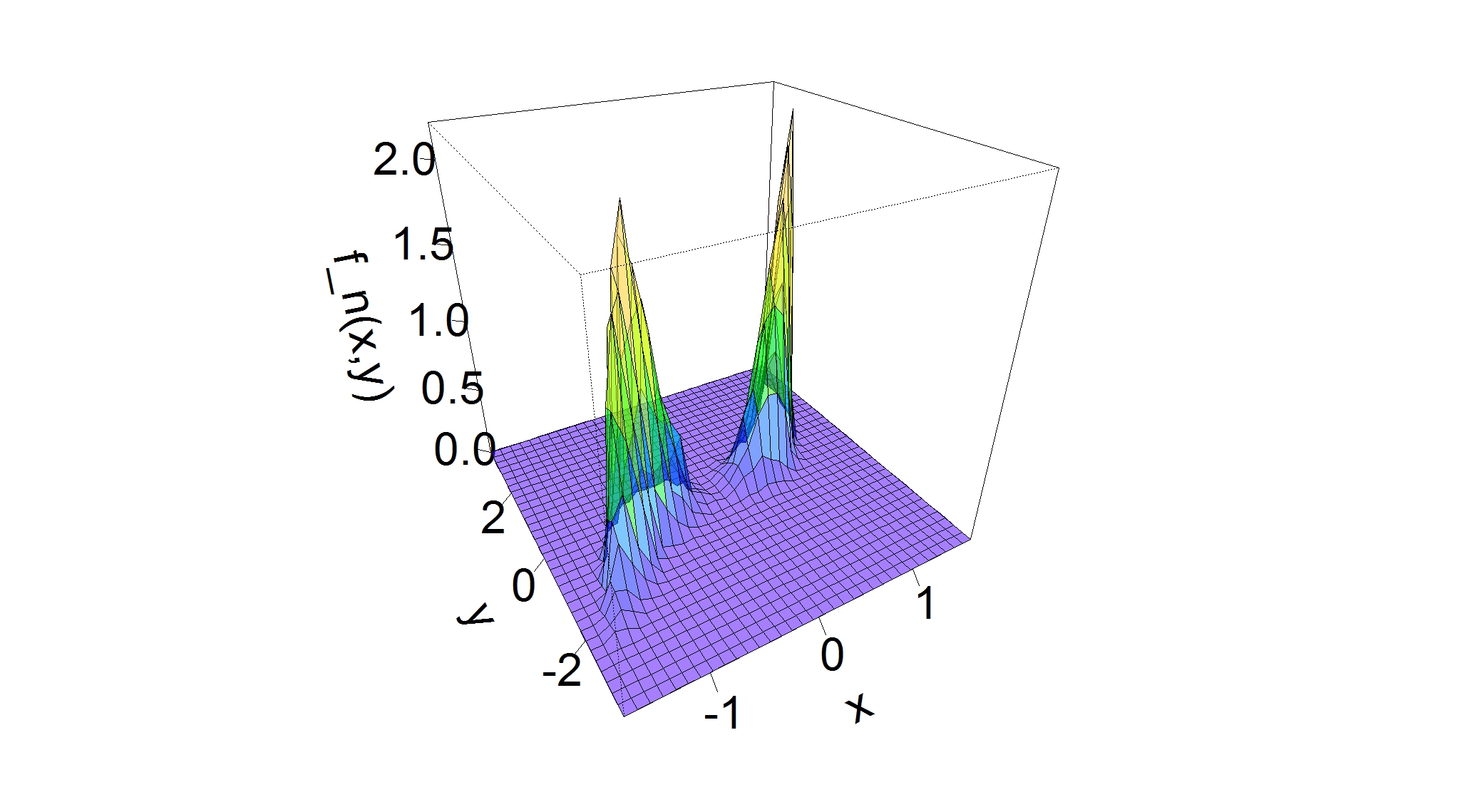

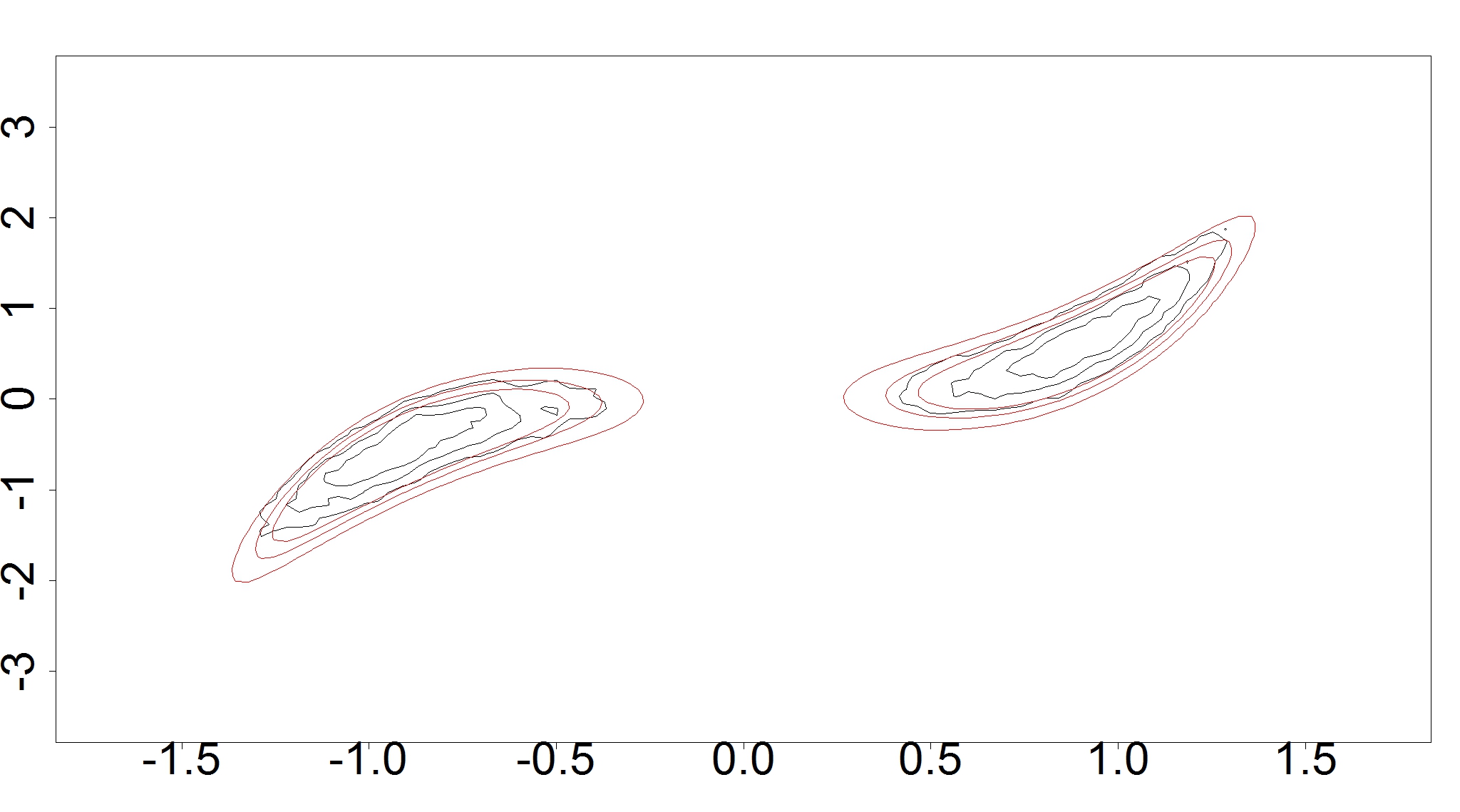

4.2 Density with root of order

Let and

Then , so that and . Example 1 applies with , and , hence and satisfy Assumption [A]. The map is invertible with . Assumption [B] is fulfilled as well with . Using Theorem 4 we obtain

where

The distribution function of is and the joint density of is given by

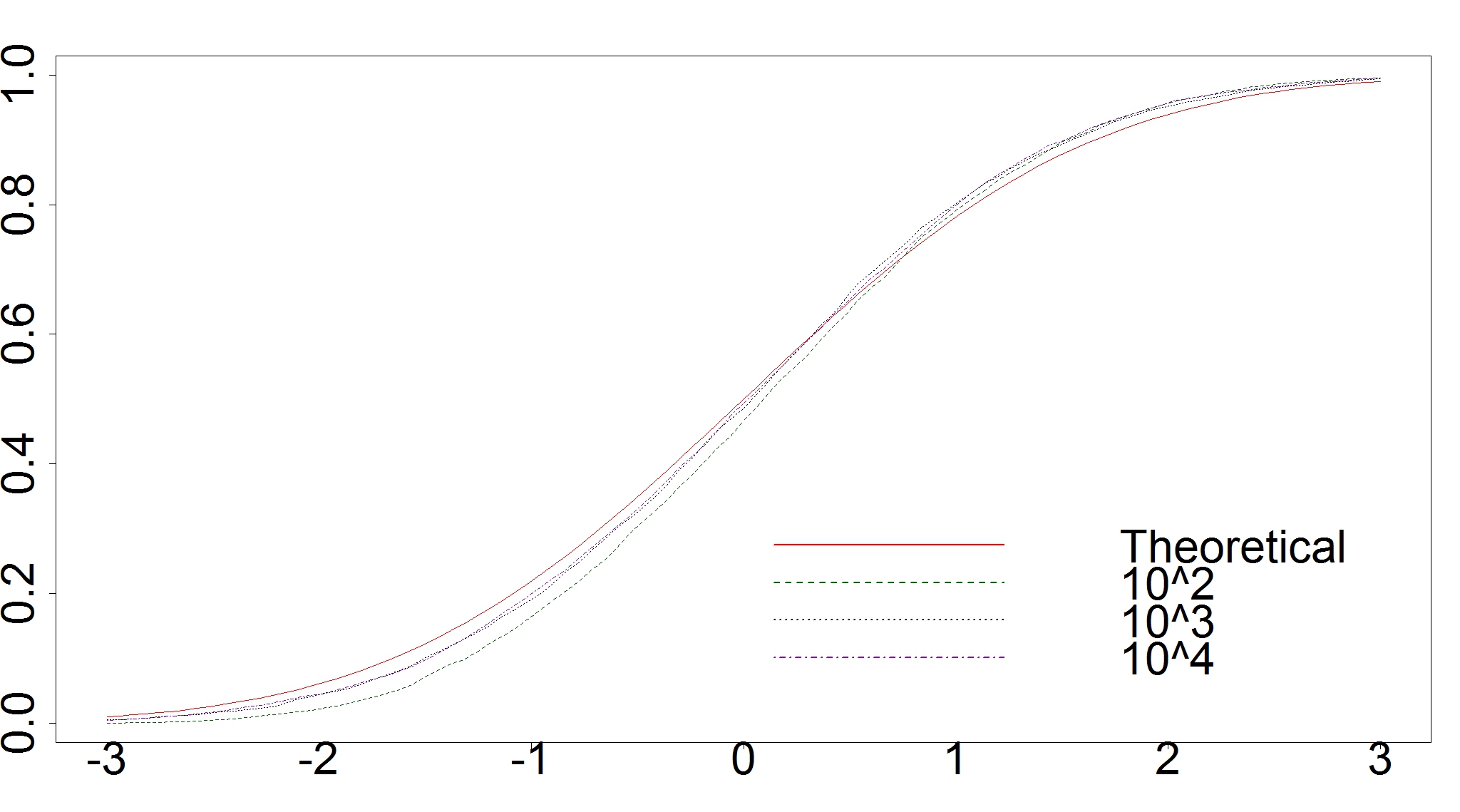

We compute the estimators for simulated samples of sizes , each for iterations.

Figure 2 shows estimated and asymptotic distribution functions of

where Figure 2 contains the results for for the quantile estimator as well as for the expected shortfall estimator, and Table 2 shows the means and the standard deviations as well as the correlations of the centred and rescaled estimators.

| Samplesize | |||||||

| Mean | |||||||

| Standard | |||||||

| deviation | |||||||

| Correlation | and |

Overall, the asymptotic approximation is reasonable for the quantile already for moderate sample sizes, but the expected shortfall requires quite large sample sizes for the asymptotic approximation to become valid.

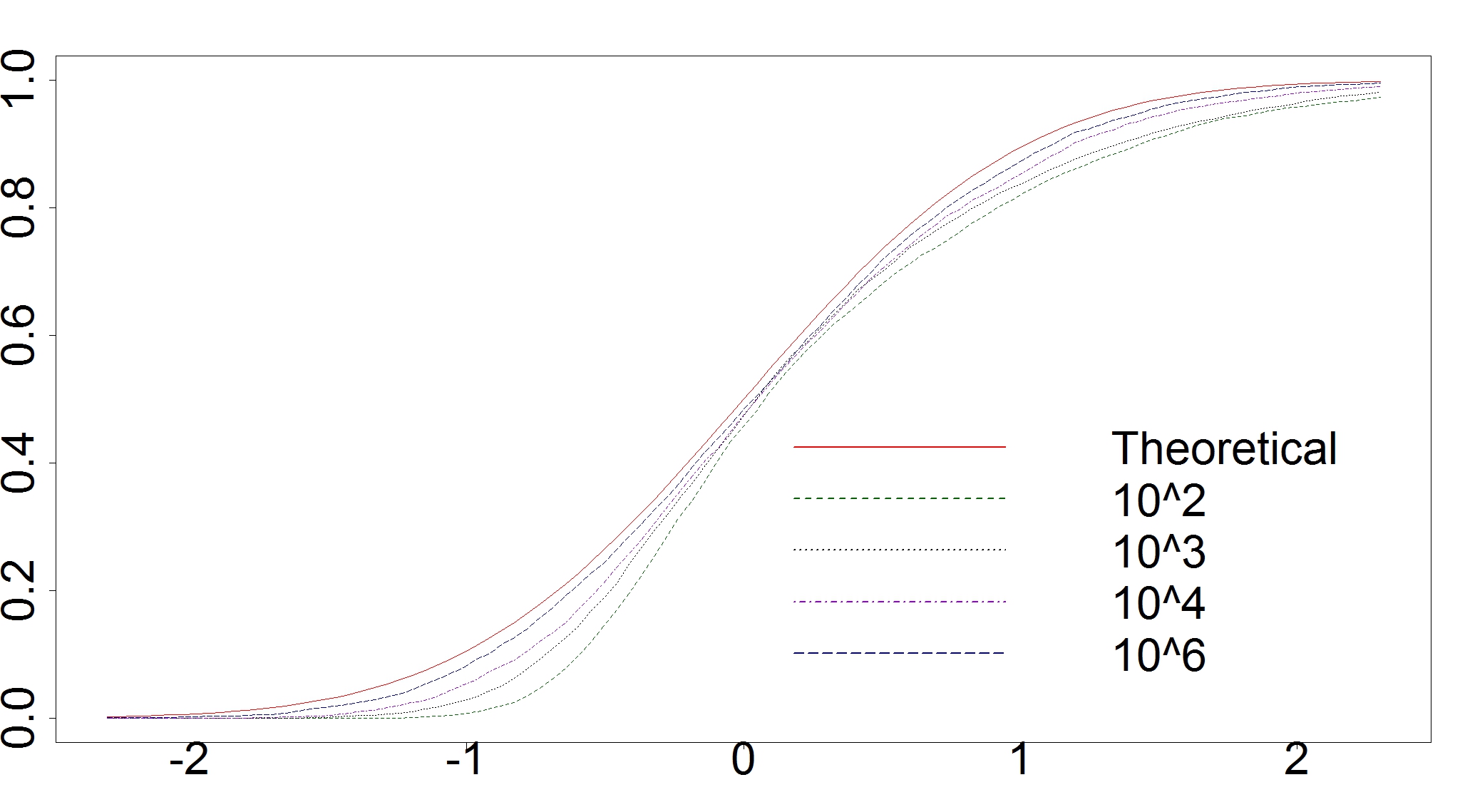

In Figure 3 we used and increased the number of iterations to in order to nonparametrically estimate the joint density function of , using the R-package ks, and compared this estimate to the density of the asymptotic distribution.

5 Conclusions and discussion

We show that the assumption of having a positive density at the -quantile, required for the quantile estimate to be asymptotically normal at -rate, are not required for asymptotic normality of the expected shortfall.

The asymptotic variance of the ES can be estimated by forming a sample-counterpart expression. Alternatively, one may use the bootstrap. For the quantile in non-standard situations, knightboot shows that the simple -out-of- bootstrap is not consistent, but subsampling works. For the marginal asymptotic distribution of the expected shortfall, however, additional simulations indicate that the -out-of- bootstrap is consistent, even without regularity of the density at the quantile.

In this paper we only considered i.i.d. data. Quantile and expectile estimation is often applied to financial time series, and therefore extensions of the results to dependent data would be useful. These should be possible but the details, in particular general M-estimation theory based on dependent data by using the argmax-continuity theorem, still need to be developed.

Finally, the analysis of the expected shortfall as a process in the level would be of some interest, in particular to study general spectral risk measures when not assuming a finitely-supported spectral measure.

Acknowledgements

Tobias Zwingmann acknowledges financial support from of the Cusanuswerk for providing a dissertation scholarship.

6 Proofs

6.1 Proofs of Propositions 1, 2 and 3

We may write (2) equivalently as

| (9) | ||||

Proof of Proposition 1.

Define the functions

so that

see (9), hence

holds. The minimal value equals

| (10) |

so that the minimizer in the first coordinate does not depend on the choice of and it follows that

which includes the empirical quantile .

From (10), minimizes

The partial derivatives of the functions are given by

Thus

As by assumption, setting the above derivative equal to zero is equivalent to

By multiplying this with and reorganising the resulting equation the claim follows.

For the final estimate, we observe that by the above,

So it remains to discuss : As we know that and thus we obtain

which implies the assertion. ∎

Proof of Proposition 2.

By the law of large numbers and the definition (1) of ,

This implies that

and it remains to show that

| (11) |

Recall that since the quantile is finite, hence . Now let and choose such that – this is possible since is continuous in . On the set the integral above is smaller than (or equal to)

Next note that converges in probability to . Thus it follows that

The last two probabilities can be made small by choosing big enough ( and ).

For the statement concerning , as in the proof of Proposition 1 we obtain the generalization of (3),

Since from the first part of the proof, the last term above converges to in probability, it remains to show . For this it suffices to show , as is tight by assumption. The argument for this part is same as for (11). This concludes the proof of the proposition. ∎

Proof of Proposition 3.

a. The classification of is shown in smirnov1952limit. Uniqueness of up to asymptotic equivalence follows from the convergence of types theorem and the distributional convergence of to a non-degenerate limit distribution under Assumption [A], see Knight2002LimDistr or the proof of Theorem 4.

b. If , then one can find a sequence for which is still true.

By Theorem 4, smirnov1952limit, this holds if and only if

| (12) |

Here, is a non-decreasing function uniquely determined by

further

With these definitions note that

holds. Thus the convergence in (12) is equivalent to

which then yields the convergence assumed in [A] with and as chosen above.

∎

6.2 General auxillary results

The rates of convergence will be proved using the next theorem, which is a generalization of Theorem 5.52, vdv2000asympstat, and similar to his Theorem 5.23. We will provide a proof for convenience. Assume that are metric spaces and that for all , , the map is measurable. To unify notation, we will use and in the formulation of the theorem, but note that here could also have a more general form (not needing a finite first moment or to be real).

Theorem 7.

Assume that for fixed and , every and all sufficiently small it holds that

| (13) |

and

| (14) |

Additionally suppose that converges to in (outer) probability and converges to in (outer) probability and fulfils

Then .

For convenience, a proof of Theorem 7 is provided in the technical supplement.

The next result is essential for obtaining the joint asymptotic distribution by use of the argmax-theorem when having different rates for the processes to be optimized.

Lemma 8.

Let and be real valued processes, where admits the representation

| (15) |

for , where is a sequence of random variables not depending on . Assume that

| (16) |

and that holds in for every compact set and some process . Choose () as minimizer of and assume in addition that and (as variables in ), where is the unique minimizer of (assuming all of these variables exist). Then

Remark.

The sequence of processes need not converge and hence the argmax-continuity theorem cannot be applied directly to the minimizers . The approximating processes converge apart from a sequence of random variables not depending on .

Proof of Lemma 8..

Let

For set

and similarly for as well as for .

We shall show , so that from the continuous mapping theorem we deduce that converges to weakly and thus in probability.

For the weak convergence of we utilize the Portmanteau Theorem. Let be closed and let . Since and by assumption we can find a compact set for which and . From (16) and the representation of we have that

and similarly for . Now if , then holds, and by the above this implies , thus

| (17) |

The process is asymptotically tight by assumption, hence is asymptotically tight by Lemma 1.4.3, vdvwellner1996weak. The convergence of the finite dimensional distributions is fulfilled as and thus Theorem 1.5.4 of vdvwellner1996weak yields . Therefore, by the continuous mapping theorem the weak convergence in for any compact follows. Hence – again due to the continuous mapping theorem – the convergence holds. Then Slutsky’s lemma and the portmanteau lemma imply

| (18) |

Since is the unique minimizer of by assumption, on the event the inequality is fulfilled. If we additionally are on the event we can deduce that must hold, hence . This means

| (19) |

Combining (17), (18) and (19) gives

| (20) |

Now by the choice of we have and

so it follows that

Since was arbitrary the portmanteau lemma yields . ∎

6.3 Proof of Theorem 4

In this subsection we give the main steps of the proof of Theorem 4. Proofs of intermediate lemmas are either given in the following subsection, or deferred to the technical supplement.

Step 1 Increments of the scoring function

We start with a technical lemma on increments of the scoring function.

Lemma 9.

a. We have that

| (21) | |||

| (22) |

b. Setting we have that

| (23) |

c. Generally, we have that

| (24) |

The proof of Lemma 9 is relegated to the technical supplement.

Step 2 -rate of convergence of or, more generally, .

The following lemma is proved by checking the assumptions of Theorem 7.

Lemma 10.

Assume to be a consistent estimator of and [B] to hold, then the sequence is tight, where is the minimizer of the function

In particular, if [A] and [B] hold, then is a tight sequence.

Step 3 Convergence of processes to be minimized

Using (24) with , , and , where , we may write

| (25) | ||||

where

| (26) |

and

| (27) | ||||

| (28) |

Here we used (23) and (22) and made a substitution in the integrals.

Under the Assumptions [A] and [B] the processes and the rescaled processes converge in distribution.

Lemma 11.

If [A] holds, then

| (29) |

in for every compact set , where .

If [B] holds we have the convergence

| (30) |

in for every compact set and .

Moreover, if both [A] and [B] hold we have that

| (31) |

in for compact , where in the definition of are jointly normal with covariance .

Step 4 Approximation of by minimizer of .

Lemma 12.

The processes and in Lemma 11 have unique minimizers and , and . Moreover, we have that

| (32) |

Step 5 Application of the argmax continuity theorem.

From Lemma 12, we have that

Now, is by construction a sequence of minimizers of the processes , but since the variables are separated, also of the processes

which, by Lemma 11, (31), and the continuous mapping theorem, converge in for compact to the process

To conclude, the minimizer of , we apply the argmax-continuity theorem, e.g. Corollary 5.58, vdv2000asympstat, and need to check the remaining assumptions.

The process apparently has a unique minimizer, and is a tight sequence by Lemma 10.

The process also has a unique minimum almost surely. Indeed, the form of the functions as given in Proposition 3, in particular that , as well as the form of in (29) imply that and that for the closed interval for which the derivative has at most one zero; if it has no zero the minimizer is on the boundary of this interval. Moreover, in the proof of Lemma 12 we already observed that is a tight sequence. This concludes the proof of Theorem 4.

6.3.1 Proofs of intermediate results

Proof of Lemma 10.

The proof proceeds by checking the assumptions of Theorem 7 with , , the Euclidean distance in and the criterion function . We give an outline here, full details are provided in the technical supplement.

Consistency has been taken care of in Theorem 2.

To this end, using (21) in Lemma 9, we get by convexity of that

for . Since holds by assumption on we can find and with for every . This proves (33).

Proving (21) reduces to showing that

| (35) |

for some constant not depending on , which may be accomplished by using a maximal inequality involving the bracketing integral (Definition in Chapter 19.2, vdv2000asympstat). ∎

Proof of Lemma 11..

Assume [A]. In fact, the convergence (29) was shown in Knight2002LimDistr. For convenience, we give a (different) proof here. First we observe that

| (36) |

Indeed, if , then is satisfied. Else, if , then

is valid. In the last case where it holds that . All three cases together prove (36).

Using the Lipschitz continuity (36), from Lemma 19.31 in vdv2000asympstat we obtain that

Therefore, from the definition of in (26),

| (37) |

The first term converges by the central limit theorem to for as stated. For the second, note that under Assumption [A] we also have

Indeed, using the monotonicity of , this follow from the dominated convergence theorem if , and the fact that and are open intervals (see Proposition 3, a.) if .

Now assume [B]. Below we show that for every compact set with there exists a function such that for every ,

| (38) |

where fulfills .

To deduce (29) we again apply Lemma 19.31, in vdv2000asympstat. From (38) and since

we thus obtain that

converges to zero in probability in . Using (23) this implies

| (39) |

The first term converges weakly by the central limit theorem to for the stated , as is a sequence of i.i.d. random variables. The second term converges to , thus the limit process of has the asserted form. To conclude the proof of (29), it remains to show (38). Using (21) we compute

It follows from the mean value theorem, that we can find a for which . The right hand side of this is smaller than , as is continuous and hence bounded on (). This ends the discussion of the first addend above as we therefore obtain

For the other addend we utilize the (second) mean value theorem to get

where the inequality holds because is continuous and thus bounded on . All in all we end up with

Now under [B] it holds that , so in this case is true.

Proof of Lemma 12.

The process is quadratic and has the unique minimizer . Further, from the form (28) of and the argument leading to (3) it follows that the unique minimizer of is given by

which, by the central limit theorem, converges in distribution to .

To show (32) we apply Lemma 8 to the processes

which is minimzed by , see (3), and

so that will play the role of in Lemma 8, which converges on compact sets to by Lemma 30. Now, in Lemma 10 we showed that is a tight sequence, and in the beginning of this proof we already showed that for the minimizers, .

It thus remains to show that (16) holds true for the above choices of and ,

| (40) |

To this end, assume . Then

since is monotonically non-decreasing. The first two factors are constant, the last factor is since the fraction converges to , and it remains to show that , which is implied by

| (41) |

To see this, we first remark that is a tight sequence. This follows from the results in Knight2002LimDistr, but is directly implied by (29), convexity of the and , and uniqueness of the minimizer of with the aid of Lemma 2.2 in davis1992mestimation. Thus given there exists a compact set with . Since for fixed compact the map is continuous for (w.r.t. the sup-norm), (29) implies that , in particular is a tight sequence. To conclude note that

which implies (41), and finishes the proof of the lemma.

∎

Asymptotics for the expected shortfall: Technical Supplement

1 Notation and results from the main paper

For i.i.d. observations distributed according to the distribution function , we use the notation

where . Note that is the empirical expectation w.r.t. . Further, we let denote the order statistics of a sample . We denote by convergence in distribution.

Suppose that the random variable has distribution function and satisfies . Given the lower tail expected shortfall of at level is defined by

For the specific value of under consideration, we shall always impose the following.

Assumption. For the given , the distribution function is continuous and strictly increasing at its -quantile . Under this assumption, has a unique -quantile.

Further, for the expected shortfall we have that

| (1) |

Consider the class of strictly consistent scoring functions for the bivariate parameter as introduced by fisszieg2015elicitability,

| (2) | ||||

where is a three-times continuously differentiable function, and it is required that . Further, from the proof of Corollary 5.5 in fisszieg2015elicitability it follows that one may choose so that . We may write

| (3) | ||||

Denote the asymptotic contrast function by

Let be i.i.d., distributed according to with . Consider the minimum contrast estimator for the bivariate parameter defined by

Assumption [A]: There exists a function with

such that for some deterministic, positive sequence with it holds that

Assumption [B]: It holds that .

Theorem 3.

Under Assumptions [A] and [B], we have that

where

and

| (4) |

Assumption [Ak]: For each and corresponding and , Assumption [A] is satisfied with associated sequence and function .

Theorem 4.

Let [Ak] and [B] hold. Then

where for , and , with as in (4) and the vector distributed according to with determined by

for .

For a probability measure on , called the spectral measure,

is called the spectral risk measure associated to . Here, the boundary cases are given by and essinf. If is finitely supported in , is a finite convex combination of expected shortfalls for different levels,

fisszieg2015elicitability show that strictly consistent scoring functions for in this case are given by

where the functions and are as above. If we define the corresponding M estimator

then we have the following result.

Theorem 5.

We have that

| (5) |

Consequently, under Assumptions [Ak] and [B] we have that

where the are as in Theorem 4.

2 Missing details in the proof of Theorem 3

Lemma 9.

a. We have that

| (6) | |||

| (7) |

b. Setting we have that

| (8) |

c. Generally, we have that

| (9) |

Proof of Lemma 9.

Observe that for and hence

| (11) |

In the terms and cancel out. Rearranging gives

By a partial integration

which together with (11) implies (6). A further partial integration gives (7).

To prove (8), note that by a partial integration,

where in the last equality we added and subtracted the term .

∎

Lemma 10.

Assume to be a consistent estimator of and [B] to hold, then the sequence is tight, where is the minimizer of the function

In particular, if [A] and [B] hold, then is a tight sequence.

Proof of Lemma 10.

We shall check the assumptions of Theorem 13 with , , the Euclidean distance in and the criterion function . Consistency has been taken care of in Theorem 2 in the main paper.

To this end, using (6) in Lemma 9, we get that

The function is convex, so that is convex as well, where the (unique) minimum is attained in (score function of ). But and thus the expression above is greater than (or equal to)

The remaining integral is monotonically increasing (decreasing) for (), whence the infimum is attained in . A partial integration then gives

for . Since holds by assumption on we can find and with for every . This proves (12).

For (24) we require

| (13) |

for some . To see this inequality we use (6) again and the fact that equals to obtain

(only the stochastic term remains). Since , the former expression does not exceed

Because the first integral fulfils

for some by the mean value theorem, and , it is enough to show

| (14) |

for some constant not depending on .

To this end we will use a maximal inequality involving the bracketing integral (Definition in Chapter 19.2, vdv2000asympstat). Observe for any the inequality

Thus is an envelope function for the (measurable) class of functions . Using Corollary 19.35, vdv2000asympstat, we obtain

for some constant and , where denotes the bracketing number with respect to the norm (see the beginning of Chapter 19.2, vdv2000asympstat; note by [B]). Next observe that the class fulfills a Lipschitz-condition, namely for any it holds that

As seen in Example 19.7, vdv2000asympstat, there is a constant only depending on , such that the bracketing number satisfies

for any . Hence by partitioning the bracketing integral we are left with

Putting things together we have shown

what is (14). ∎

2.1 Proofs of Theorems 4 and 5

Write

| (15) | ||||

where

| (16) |

and

| (17) | ||||

| (18) |

In Lemma 11 we showed that

| (19) |

and that

| (20) |

Lemma 12.

The processes and have unique minimizers and , and . Moreover, we have that

| (21) |

Proof of Theorem 4.

We define the processes and as in (16) and (18) for each , . Then the expansions (19) and (20) are valid for each , and the covariance matrix in the joint normal distribution of the vector in the limit processes and , which are given by

see Lemma 11 in the main paper, is determined by

and

where . Further, Lemma 12 also holds true for each . As in step 5 of the proof of Theorem 3 in the main paper, we may then consider the sequence of minimizers of the processes

which converge to the process

and apply the argmax-continuity theorem to obtain the result. ∎

Proof of Theorem 5.

The formula (5) together with Theorem 4 immediately imply the second statement of the theorem. Concerning (5), setting

we have that

For the minimal value we have

so the minimizer in does not depend on , and is actually given by . It remains to find the minimizer of the function

Differentiation of the maps and gives

so that minimizing the above function is equivalent to solving

for , which results in

The formula

| (22) | ||||

for the expected shortfall then implies (5). ∎

3 A general result on rates of convergence

The rates of convergence will be proved using the next theorem, which is a generalization of Theorem 5.52, vdv2000asympstat, and similar to his Theorem 5.23. We will provide a proof for convenience. Assume that are metric spaces and that for all , , the map is measurable. To unify notation, we will use and in the formulation of the theorem, but note that here could also have a more general form (not needing a finite first moment or to be real).

Theorem 13.

Assume that for fixed and , every and all sufficiently small it holds that

| (23) |

and

| (24) |

Additionally suppose that converges to in (outer) probability and converges to in (outer) probability and fulfils

Then .

Proof of Theorem 13.

We set and suppose, that minimises the map up to a random variable .

For each the set can be partitioned into the sets

If for some , then must be in one of the for . Further, if and then for . This gives

Assume for a involved in the above union. Then by assumption on the infimum of the map over is at most . If we suppose in addition that holds, then the infimum of over is smaller than as well. Hence if for some , this infimum is smaller than . Thus

| (25) |

Observe that the last three summands can be made small for any by choosing and big enough (, in (outer) probability, ).

Now choose small enough to ensure that the conditions of the theorem hold for all . Every involved in the above sum does fulfils , whence from the first assumption (23)

| (26) |

Hence

where the last inequality uses (26). Choose large enough to guarantee , so that

holds for . This means that the former sum does not exceed

By taking absolute values and multiplying with this expression is smaller than

Due to Markov’s inequality and the second assumption (24) this term is finally not bigger than

The last series can be made small by taking big enough since . Hence every summand in (25) can be made small and thus the theorem is proven. ∎