Predictive, finite-sample model choice for time series

under stationarity and non-stationarity

Abstract

In statistical research there usually exists a choice between structurally simpler or more complex models. We argue that, even if a more complex, locally stationary time series model were true, then a simple, stationary time series model may be advantageous to work with under parameter uncertainty. We present a new model choice methodology, where one of two competing approaches is chosen based on its empirical, finite-sample performance with respect to prediction, in a manner that ensures interpretability. A rigorous, theoretical analysis of the procedure is provided. As an important side result we prove, for possibly diverging model order, that the localised Yule-Walker estimator is strongly, uniformly consistent under local stationarity. An R package, forecastSNSTS, is provided and used to apply the methodology to financial and meteorological data in empirical examples. We further provide an extensive simulation study and discuss when it is preferable to base forecasts on the more volatile time-varying estimates and when it is advantageous to forecast as if the data were from a stationary process, even though they might not be.

Key words and phrases.

forecasting,

Yule-Walker estimate,

local stationarity,

covariance stationarity.

MSC2010 subject classifications: Primary 62M20; secondary 62M10.

1 Introduction

A well-trodden path in applied statistical research is to propose a model believed to be a good approximation to the data-generating process, and then to estimate the model parameters with a view to performing a specific task, for example, prediction. However, even if the analyst were ‘lucky’ and chose the right model family, thereby reducing modelling bias, the resulting parameter estimators could be so variable that the selected model might well be sub-optimal from the point of view of the task in question. Choosing a slightly wrong model but with less variable parameter estimates may well lead to superior performance in, for example, prediction. This effect is usually referred to as the bias-variance trade-off and it has frequently been discussed in the literature. In this paper we explore how this unsurprising but interesting phenomenon could and should affect model choice in the analysis of non-stationary time series.

Choosing between stationary and non-stationary modelling is, typically, an important step in the analysis of time series data. Stationarity, which assumes that certain probabilistic properties of the time series model do not evolve over time, is a key assumption in time series analysis, and several excellent monographs focus on stationary modelling; see, e. g., Brillinger, (1975), Brockwell and Davis, (1991) or Priestley, (1981). However, in practice, many time series are deemed to be better-suited for non-stationary modelling; this judgement can be based on diverse factors, such as, for example, visual inspection, formal tests against stationarity, or the observation that the data have been collected in a time-evolving environment and therefore are unlikely to have come from a stationary model.

Early contributions to the literature of non-stationary time series are Subba Rao, (1970), where the tvAR model was introduced, and Hallin, (1978), who defined the tvARMA model. A general non-stationary time series framework was provided by Priestley, (1965), who defined the evolutionary spectrum. A now particularly popular framework for the rigorous description of non-stationary time series models is that of local stationarity, in which the data are modelled locally as approximately stationary (Dahlhaus, , 1997, 2012). We now illustrate the main idea of the paper using a simple example of a locally stationary time series model, the time-varying autoregressive model (of order 1)

with denoting the sample size, being some suitable function and being an i. i. d. sequence with mean zero and variance one. Typically, to forecast future observations, one would require an estimate of , see e. g. Chen et al., (2010). Before constructing a suitable estimator, some analysts would wish to test if was indeed time-varying, and there exist a vast amount of techniques to validate the assumption of a constant second-order structure in this framework; see von Sachs and Neumann, (2000), Paparoditis, (2009), Dwivedi and Subba Rao, (2010), Paparoditis, (2010), Dette et al., (2011), Nason, (2013), Preuß et al., (2013) or Vogt and Dette, (2015). If the process was found to be non-stationary, it would be tempting to estimate by a localised estimate based on the most recent observations of . This localisation would most likely reduce the bias of the estimator if the true dependency structure was indeed time-varying, but also increase its variance. However, if, for example, the function was varying only slowly over time, this estimation procedure might result in sub-optimal estimation from the point of view of the mean squared prediction error, yielding inferior forecasts compared to the classical stationary AR(1) model. This would be particularly likely if the test of stationarity employed at the start was not constructed with the same performance measure in mind (i. e., mean squared prediction error) and was therefore ‘detached’ from the task in question (i. e., prediction). One of the findings of this paper is that even if the function varied over time, one should in some cases treat it as constant in order to obtain smaller prediction errors, or in other words, ‘prefer the wrong model’ from the point of view of prediction.

The main aim of this paper is to propose an alternative model choice methodology in time series analysis that avoids the pitfalls of the above-mentioned process of testing followed by model choice. More precisely, our work has the following objectives:

-

•

To propose a generic procedure for finite-sample model choice which avoids the path of hypothesis testing but instead chooses the model that offers better empirical finite-sample performance in terms of prediction on a validation set, with associated performance guarantees for the test set of yet unobserved data. Although the procedure is proposed and analysed theoretically in the framework of choice between stationarity and local stationarity and in the context of prediction, the procedure is applicable more generally whenever a decision needs to be made between two competing approaches, and can therefore be viewed as model- and problem-free. At the end of Section 3.2, we provide two examples of other situations in which the general principle of our procedure can be applied.

-

•

To suggest ‘rules of thumb’ indicating when the (wrong) stationary model may be preferred in a time-varying, locally stationary situation from the point of view of forecasting; and when a time-varying model should be preferred.

Our procedure validates and puts on a solid footing the possibly counter-intuitive observation that it is sometimes beneficial to choose the ‘wrong’ (but possibly simpler) model in time series analysis, if that model relies on more reliable estimators of its parameters than the right (but possibly more complex) model. While we stop short of conveying the message that simplicity in time series should always be preferred, part of our aim is to draw time series analysts’ attention to the fact that particularly complex time series models may well appear attractive on first glance as they have the potential to capture features of the data well, but on the other hand can be so hard to estimate that this makes them inferior to simple and easy-to-estimate alternative models, even if the latter are wrong.

We now briefly describe related recent literature. The work of Xia and Tong, (2011), who, while discussing time series prediction, select the model based on the minimisation of up to -step ahead prediction errors (rather than the usual 1-step ahead ones) also appears to carry the general message that different models may be preferred for the same dataset depending on the task in question, or, in the language of the authors, on the ‘features to be matched’. Besides similarities in this general outlook, our model-fitting methodology and the context in which it is proposed are entirely different. Forecasting in the presence of structural changes is a widely studied topic in the econometrics literature, see e. g. the comprehensive review by Rossi, (2013) and the references therein. In particular, Giraitis et al., (2013) also use the minimisation of the 1-step ahead prediction error as a basis for model choice under non-stationarity, but, unlike us, do not consider the question of how this may lead to the preference for the ‘wrong’ model in finite samples. Das and Politis, (2018) apply the model-free prediction principle of Politis, (2015) in the context of locally stationary time series and construct 1-step-ahead point and interval predictors.

Instead of pursuing the cross-validation approach, McDonald et al., (2016) evaluate the upper bound on the generalisation error in time series forecasting, and use its heuristically estimated version to guide model choice. We note, however, that this approach requires the estimation of some possibly difficult to estimate parameters, unlike cross-validation-based approaches. The empirical mean squared prediction error (MSPE) which we will employ in our method is closely related to the population MSPE under parameter uncertainty. The strand of literature discussing this population quantity includes Baillie, (1979) and Reinsel, (1980), where approximating expressions were derived for stationary VAR time series. For locally stationary tvMA() processes, Palma et al., (2013) discuss optimal -step ahead forecasting, in terms of the true model characteristics. Yet, they do not take parameter uncertainty into account.

While the main question we are concerned with is whether a stationary or a time-varying autoregressive model should be used for prediction, a nested question is what order the stationary or non-stationary model should have. Traditionally, order selection is done via minimisation of an information criterion, see, e. g., Brockwell and Davis, (1991), p. 301. Zhang and Koreisha, (2015) develop an adaptive criterion for model selection based on predictive risk. Akaike, (1969) introduced the Final Prediction Error (FPE) as a figure of merit for a potential predictor and adopts a decision theoretic approach, called the minimum FPE procedure, where the predictor with the best FPE is chosen. In practice, the decision is then based on an estimate of the FPE. In Akaike, (1970) a theoretical basis of the procedure is provided. Peña and Sánchez, (2007) derive and compare MSPE for univariate and multivariate predictors when the parameters are known. They then define and estimate a criterion (a measure of predictability) to choose between these two prediction options. Their approach is similar to ours in spirit, but, firstly, it chooses between univariate and multivariate models while we consider stationary and non-stationary models and, secondly, their methodology works with the population MSPE (which moves the focus away from the observed data to the postulated model), while we work with the corresponding empirical quantity directly. This difference in approaching the problem also holds for another, more general class of special-purpose-criteria: the focused information criteria (FIC), which were introduced in Claeskens and Hjort, (2003). The FIC methodology with the focus on choosing the model best suited for prediction was then applied in the field of time series analysis in Claeskens et al., (2007), where the best AR() model for prediction is chosen, in Rohan and Ramanathan, (2011), where the best ARMA(,) model for this purpose is chosen, and in Brownlees and Gallo, (2008), where models for volatility forecasting are chosen. The idea of the FIC is that the model which minimises the asymptotic MSPE is the best one and the FIC is then based on an estimator of that asymptotic MSPE. Contrary to this, our approach is based on the empirical MSPE directly, which we believe to be the more relevant quantity in many applications. Contrary to the FIC which is based on the large-sample theory of the estimators involved, we provide finite-sample exponential bounds that imply a performance guarantee for our method. This approach can be advantageous, when it is preferred that the model choice also depends on the size of the sample, which in our view should be a natural requirement.

Our paper is organised as follows. In Section 2 we provide a simple motivating example. In Sections 3.1 and 3.2 we introduce and comment on our new time series model choice methodology. The statistical properties of our procedure are discussed in Section 3.3, where also the performance guarantee (Theorem 3.1) is provided. The results of a simulation study and the analysis of three empirical examples can be found in Sections 4 and 5. In Section 6 we discuss statistical properties of the local Yule-Walker estimator and prove its strong uniform consistency under local stationarity (Corollary 6.2). We conclude with a summary in Section 7. Proofs, technical details, additional tables and figures from the simulations section are gathered in Appendices A–J. Note that Appendices F–J are only available in the arXiv’ed version of the manuscript (Kley et al., , 2019).

2 Motivating example

We consider the time-varying autoregressive (tvAR) model of order 2:

where , , and is Gaussian white noise. is a non-stationary process which lies in the locally stationary class of Dahlhaus, (1997). We will now compare different forecasting procedures for , where . The predictor that minimises the mean squared prediction error is given by

Yet, since in practice the underlying model is unknown, the analyst needs to

-

(1)

make assumptions regarding the model, and

-

(2)

estimate the assumed model’s parameters.

For the purpose of this illustration, we discuss four possible models. In the first two models we falsely assume that the data were stationary and model to satisfy a traditional, autoregressive (AR) equation.

-

•

In the first of the two cases we assume an AR(1) model and

-

•

in the second case we assume the model to be an AR(2) model.

We further, discuss cases 3–4, where the correct class of models (tvAR) is assumed. Yet,

-

•

in case three, we falsely assume a tvAR(1) model, before

-

•

in case four, we correctly assume the model to be a tvAR(2) model.

Note that the true model, the tvAR(2) model, is the most complex one of the four choices. In each of the models we estimate the parameters by solving the empirical Yule-Walker equations. In the case of the tvAR models we localise by using the segment . In the case of the traditional, stationary AR models we use all available observations . Details on the estimation are deferred to Section 3.1.

Denoting the localised Yule-Walker estimates of order by and the ones of order by and we obtain the predictors

where corresponds to the models of order and corresponds to the models of order . The segment length will be chosen as in the AR models and strictly smaller than this in the tvAR models.

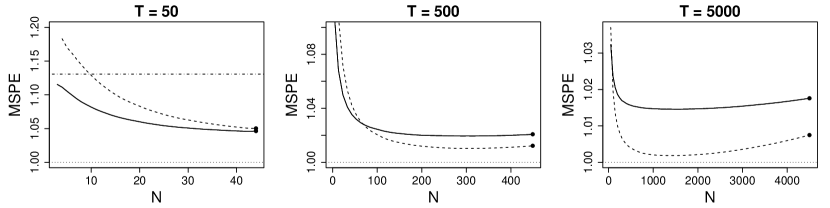

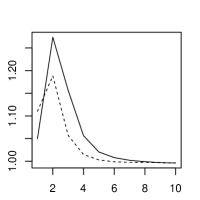

In Figure 1, we observe that the predictors associated with the simpler, stationary AR model perform better than or similarly well as the predictors associated with the more complex, locally stationary tvAR model if or . If the predictor associated with the locally stationary tvAR model performs visibly better in terms of its MSPE when the segment size is chosen appropriately. In conclusion, this example illustrates how it can be advantageous to assume a wrong, but structurally simpler model when only a short time series is available. In particular, the model chosen should depend on the task at hand (here: prediction) and on the amount of data available. For the best result is obtained by assuming the AR(1) model which is the simplest of the four candidates. When the more complex AR(2) model becomes advantageous. Note that this model is more complex than the AR(1) model and thus provides a better approximation to the true tvAR(2) mechanism, but is still simplifying, because it does not take the time-varying characteristics into account at all. Only when even more data (here: ) are available, then the variability of the parameter estimates of the tvAR(2) model is small enough not to overshadow the modelling bias, which in this example is rather small.

Obviously, the bias-variance trade-off is at work here, which is well-known but interestingly, to our knowledge, has previously been unexplored in the important context of stationary versus non-stationary modelling for prediction. The observation to be made here, thus, is that finding the ‘right’ model may not always be a suitable way of proceeding when it comes to the prediction of future observations. We point out that this observation was made in other contexts of time series analysis. For example, basic exponential smoothing is a widely used forecasting and trend extrapolation technique, and although it is well-known that it corresponds to standard Box-Jenkins forecasting in the ARIMA model, it is also frequently used for data that does not follow it.

This paper investigates the question of what is the best model in terms of forecasting performance in the context of the choice between stationarity and non-stationarity. To ask this question explicitly instead of applying a test for stationarity is important since the smallest sample size needed to reject the null hypothesis of stationarity may be smaller than the sample size needed to obtain improvement in terms of our task of interest, namely forecasting. In the following section, we will elaborate more on this question. Further, in Section 4, we see, as results of a simulation study, under which conditions using the true model is advantageous and when it can become disadvantageous.

3 When (not) to use locally stationary models under local stationarity: the new model choice methodology

3.1 Precise description of the procedure

We work in the framework of general locally stationary time series (a rigorous definition is deferred to Section 3.3), in which the available data is a finite stretch from an array of random variables with mean zero and finite variances. Our aim is to determine a linear predictor for the unobserved from the observed .

Our proposal is to compare candidate -step ahead predictors in terms of their empirical mean squared prediction error and choose the predictor with the best forecasting performance. To this end, we proceed as follows:

Step 1. Separate the final observations from the available observations. The observations with indices , and will be referred to as the training set, first validation set and second validation set, respectively. The set of unobserved data with the indices will be referred to as the test set. The size of the separated sets will be small in comparison to the sample size (and hence also to the training set). Comments on why we require two distinct validation set are deferred to Section 3.2.

Step 2. Compute the linear -step ahead prediction coefficients

| (1) |

( denotes the transposed vector ) for , , and ,

| (2) |

and

| (3) |

The set of possible model orders , with and , and the set of possible segment lengths , with , are parameters to be specified by the user. Further comments on how they are to be chosen are deferred to Section 3.2.

Step 3. Compute the linear -step ahead prediction coefficients

| (4) |

where is defined in (1), denotes the first canonical unity vector of dimension and denotes a Jordan block with all eigenvalues equal to zero; cf. equation (39), in the appendix. Comments on an equivalent, recursive definition are provided in Section 3.2. Next, define , and, for and , compute

| (5) |

| (6) |

In Figure 2, a time line is shown that illustrates the relation of the sets , and the quantities , , and .

Step 4. Amongst predictors (5) select , with

and, amongst predictors (6) select , with

Note that and are the forecasts of type (5) and (6) that minimise the empirical MSPE (on ) within the classes of tvAR and AR models of orders , respectively.

Step 5. Use as -step ahead forecast of , with , if

| (7) |

holds for , and otherwise, where

| (8) |

with indicating the corresponding model (we write ‘loc.’ for the locally stationary approach and ‘stat.’ for the stationary model) and is a parameter by which the user of the procedure specifies which degree of superiority of the more complex procedure is required before it is preferred over the simpler alternative (cf. the end of Section 3.2).

3.2 Remarks on the procedure

Some further explanations regarding the procedure are in order now. Our comments are organised according to the steps of the previous section.

Step 1. While it is common practice to separate one validation set when tuning the model parameters to avoid over-fitting, we require two such sets. This is necessary, because we would otherwise compare candidates in an unbalanced situation where stationary predictors compete with locally stationary ones. In our procedure, where we first choose the hyper-parameters by minimising the mean squared error on the first validation set and then choose between the two model classes by minimisation of the mean squared error on the second validation set, we achieve a fairer competition of the two model classes.

Step 2. The coefficients (1) are estimates for the coefficient functions if the data follows the tvAR() model

| (9) |

(see, for example, Dahlhaus and Giraitis, (1998)). Recall that is usually assumed to be white noise and that is non-stationary if at least one of the functions , , or is non-constant. A recursive algorithm to estimate the parameters was described and analysed in Moulines et al., (2005).

We are interested in linear forecasts that will perform well for time series possessing a general dependency structure. The tvAR() model (9) is a natural choice to approximate the linear dynamics of the observed, non-stationary time series, because in this model the coefficient functions at time coincide with the -step ahead prediction coefficients (of order ) which define the best linear predictor. In Section 6, we show that from Step 2 can be used as estimates for the 1-step ahead linear prediction coefficients

also when the observations do not satisfy (9). A forecasting procedure derived within the tvAR() model can therefore be expected to behave reasonably, irrespective of whether the tvAR() model is true or just an approximation to the truth. Note that we use the tvAR() model to approximate the dynamic structure of the data in Section 3.2 and most of our examples in Section 4 are of this kind, but we do not assume that the data actually satisfies it.

Step 3. Linear -step ahead predictors can either be obtained by iterating model equation (9) or by using a separate model for each in which the indices of the sum on the right hand side run from . These approaches have been referred to as the plug-in method and the direct method, respectively. A comparison of the two approaches can, for example, be found in Bhansali, (1996), where results for a class of linear, stationary processes were derived. We employ the plug-in method.

The coefficients defined in (4) can be computed efficiently via the recursion:

From the previous comments it can be seen how the predictors and relate to the choice of modelling the time series’ dynamics by a tvAR() or AR() model, respectively. In each of these model classes, increasing the order will give a better approximation of the dynamics, but increase the complexity of the model, and make it more difficult to deal with under parameter uncertainty.

The parameters and are sets of integers to be chosen by the user. The choice should depend on . determines the order of the tvAR() model that is used to approximate the dynamics. determines the degree of locality in the estimation of the coefficients. The parameters and will influence the degree of bias and variance of the predictor. Our selection mechanism will balance them implicitly.

Traditional choice of . It is obvious that the variance of the estimator can decrease when a larger segment is used, but that the non-stationarity will potentially inflict an additional bias that increases with . Under the condition that , Dahlhaus and Giraitis, (1998) derive asymptotic expansions for the local Yule-Walker estimator’s bias and variance for a centred sample. It follows from their results, that for the one-sided sample we require for forecasting, should be chosen at the order of , with the constant depending on the second derivatives of the true model quantities, which are unknown and difficult to estimate. The choice of should thus, ideally, be such that , for all . In practice, since the true model parameters are unknown, this rate provides very little guidance to the user of the method. We recommend, though, to adhere to two facts: the upper and lower bound of should be bounded away from and , respectively. In other words, we recommend to choose with large enough, for the performance guarantee to be valid (cf. Theorem 3.1) and being substantially smaller than , to ensure that there is a clear boundary between the locally stationary and the stationary approach. Richter and Dahlhaus, (2017) propose to adaptively choose a bandwidth for local M-estimators by minimising a cross-validation functional.

Traditional choice of . As described in the beginning of this section we use the tvAR() model to approximate the dynamic structure of the data. Intuitively, we have that the larger the order the better the approximation to the true dynamic structure. In opposition to the previously discussed question of how to choose the segment length , we here have that a smaller will inflict a modelling bias, while a larger will typically be accompanied by an inflation of the variance of the estimation, because it implies that more parameters need to be estimated. Traditionally, the model order is chosen by minimizing information criteria as for example AIC or BIC. Claeskens et al., (2007) propose to use a version of the focused information criterion (FIC, see Claeskens and Hjort, (2003)) to select the model order of a stationary AR() model optimal with respect to forecasting when the true model is known to be AR(). However, as mentioned in the introduction, the FIC-based methods employs an estimator of the asymptotic MSPE, while our approach is based on the empirical MSPE, which facilitates our focus on the finite sample performance.

Step 4 and 5. Our procedure performs two stages of selections. Firstly (in Step 4), it selects the model order and, for the locally stationary approach, the segment length by comparing predictors within each class of models under consideration (i. e., time-varying or non-time-varying autoregressive models). The parameters and are chosen such that the empirical MSPE (predicting observations from ) is minimised. Secondly (in Step 5), a final competition of the winners is performed to select among the two classes of models. The procedure that minimises the empirical MSPE (predicting ) is selected and used for forecasting of the test set (). In our theoretical analysis of the next section (see, in particular, Theorem 3.1) we show that the proposed procedure will, with high probability, choose the same class of models on the validation as on the test set, implying that the procedure with the best empirical performance will be selected.

The parameter . By introduction of the parameter the user is given additional control over which model the procedure prefers. In the simplest case, , this reduces to a straight choice between the two model classes, whereby the time-varying model is chosen if it performs better or equally well. Choosing introduces penalisation against the choice of more complex models. In this case, the predictor derived from the more complex, locally stationary model is only chosen if it performs at least better than the one derived from the simpler, stationary model.

Generalisations. Besides linear predictions for stationary or locally stationary time series models, the general principle of our method can also be applied in many other situation. To illustrate this, we outline two examples below.

Non-linear predictions with neural networks. In this scenario we either choose a neural network trained with the most recent observations (i. e., loc.) or with all available observations (i. e., stat.). To this end proceed as follows: with the available data partitioned as described in Step 1, consider a range of candidate networks (with different network topologies) suitable for forecasting the observations from the first validation set. Train them either with the most recent observations (loc.) or with all available observations (stat.). After first choosing the network for which we see the smallest MSPE on the first validation set within each class (loc. or stat.), we then choose that class for which the winner from the previous step obtains the best performance on the second validation set.

Predictors obtained from locally stationary or long-memory time series models. Long-range dependence and non-stationarity can lead to the same stylised facts in financial time series; cf. Mikosch and Starica, (2004). Choosing a test, for example from Preuß and Vetter, (2013), to distinguish between the two model classes seems to be a sensible approach, but this might not lead to the best choice if the aim is to choose a model for the purpose of prediction. With the model choice methodology in this paper, one proceeds as follows: first, fit a set of long-range dependence models and a range of locally stationary models, use the implied predictors to forecast the observations from the first validation set and choose the model with the best forecasting performance within each model class. Then, choose between the two model classes by comparing the winning models within each class with respect to their empirical performance in predicting the observations from the second validation set.

3.3 Performance guarantee: theoretical result for the general case

In this section, we establish theoretical results that will facilitate our analysis of the model choice suggested by decision rule (7). We show that the probability of choosing different models on the validation and the test set decays to zero at an exponential rate, which can be viewed as a performance guarantee of our model choice methodology.

To rigorously prove the results, some definitions and assumptions are in order. Throughout this paper, we work with the doubly indexed process . The first index (i. e., ) refers to the time. The second index (i. e., ) indicates how well the covariance structure of can be approximated locally by the autocovariance function of a stationary process. We will assume that, for large , segments of observations with their indices are approximately weakly stationary. The parameter is continuous and often referred to as the rescaled time. If the index coincides with the number of observations in a time series, then (cf. Dahlhaus, (1996)). This restriction is not necessary and in fact, because we will consider unobservables (to be forecast) in addition to the observations (available at the time when the forecasting is done) it is more convenient to allow , as was also done by Roueff and Sanchez-Perez, (2018).

The following definitions from Roueff and Sanchez-Perez, (2018) are required for our assumptions. For an array with finite variances, the time-varying covariance function is defined for all and as

| (10) |

A local spectral density is a function, -periodic and locally integrable with respect to the second variable. The local covariance function associated with the time-varying spectral density is defined for by

| (11) |

The first five assumptions are specific to the kind of data we may apply our result to.

Assumption 1 (Local stationarity, Roueff and Sanchez-Perez, (2018)).

Let the array of random variables have finite variances. We say that is locally stationary with local spectral density if the time-varying covariance function of and the local covariance function associated with satisfy

| (12) |

where is a constant.

Assumption 2 (Geometrically -mixing).

There exist constants and such that, for every ,

| (13) |

Assumption 3.

The local spectral density is bounded from above and below:

| (14) |

Assumption 4.

The local spectral density is continuously differentiable with respect to the first argument and the partial derivative is uniformly bounded. More precisely, assume the existence of such that

| (15) |

Assumption 5 (Bernstein-type condition).

There exist and , such that

The assumptions are reasonable and non-restrictive in the sense that many popular and widely used time series models (e. g., a wide range of tvARMA models) satisfy the full set of assumptions. The notion of local stationarity we impose (Assumption 1) goes beyond that of locally stationary linear processes and, in particular, we do not require the data to be tvAR. Assumption 1 is satisfied for second order stationary process (then we have ), the general (linear) locally stationary process introduced by Dahlhaus, (1996), but also non-linear processes as elaborated by Roueff and Sanchez-Perez, (2018). Assumption 2 is satisfied for a broad class of (linear and non-linear) locally stationary time series models; see, for example, Fryzlewicz and Subba Rao, (2011) or Vogt, (2012). Assumptions 3 and 4 can be verified by considering the local spectral density when it is given explicitly. For example, in the tvAR model that we used to motivate our prediction approach in Section 3.2, see (9), and as examples in Section 4, the local spectral density and local covariances are naturally those of the stationary AR process when the parameter of the coefficient functions is chosen as . We will refer to these AR processes as the tangent processes of the tvAR process. Similar assumptions with respect to the local spectral density are common in the literature; cf. Dahlhaus, (1997). Processes with sub-Gaussian marginal distributions satisfy Assumption 5; cf. Lemma E.8 in the appendix. We recall, from Section 3.2, that the tvAR() model is used to approximate the linear dynamic structure of the data, but that we do not assume that the data actually satisfies it. Thus our results apply in a more general context. We require Assumptions 2 and 5 to prove that the probabilities in our results decay at an exponential rate.

As a consequence of Assumptions 1 and 3, we have

| (16) |

Further, by Assumption 4 and Leibniz’s integral rule, we have that exists and has the following form

| (17) |

which, in particular, implies that .

Assumptions 6 and 7, which we state below, are more specific to our procedure. They concern minimum requirements for the size of the validation sets and the minimum segment size which are used to compute the forecast as well as the number of observations required to be available at the time the forecasts are to be determined. To precisely state the final two assumptions, we will define that quantifies the difference between the two approaches in terms of their expected empirical mean square prediction error forecasting performance.

To make the definition of precise in an accessible manner we now present it from the inside outwards. At the core we have the local covariance function defined in (11) and averaged versions

| (18) | ||||||

If or and , then the entries in and are approximations for the expectation of the lag autocovariance estimate computed from ; cf. Lemma D.1. This seemingly complicated construction is necessary, because we do not require that is negligible. By allowing we can capture the evolving second moments of the processes. Further note that, for every and , the averaged local autocovariances form the autocovariance function of a stationary process that can be seen as an average of the stationary approximations over the local times in . Solving the Yule-Walker equations for this average process yields

| (19) |

As can be seen from Theorem 6.1 and Lemma B.2, is an approximation to the limit of the Yule-Walker estimate obtained from . It further is related to the 1-step ahead linear forecasting coefficients, as can be seen from Lemma B.1. The -step ahead counterpart of is defined as

| (20) |

where and are the same as in (4). Then, for , , the functions are defined as

| (21) |

where and, for , with ,

| (22) |

From Lemmas A.1 and A.3, it can be seen that

concentrates around with , and . Note that two arguments and are required to allow for the averaging of possible effects due to non-stationarity originating from (a) either the computation of the forecasting coefficients or (b) the computation of the mean squared prediction errors. The quantity approximates the MSPE of defined in (5). In the case of 1-step ahead forecasts we can simplify the expression in (22) to

| (23) |

where is the best linear 1-step ahead forecast for and denotes the quadratic form associated with . Decomposition (23) is into two non-negative quantities. The first term only depends on the characteristics of the stationary tangent process and will be a decreasing sequence with index for any . The second term is the squared weighted difference of the forecasting coefficients obtained from the stationary approximation at time and the forecasting coefficients obtained from the non-stationary data; more precisely from the stationary approximations “averaged” over .

The final two assumptions require that the size of the validation sets, the smallest segment size from which locally stationary forecasting coefficients are computed, and the number of available observations are large enough in relation to the maximum model order , the forecasting horizon , and the minimum possible difference of performance of stationary and locally stationary forecasts in terms of MSPE, which we measure by

| (24) |

where .

Assumption 6 requires the size of the validation sets and the smallest possible segment lengths from which to estimate the forecasting coefficients to be ‘large enough’.

Assumption 6 (Minimum size for and ).

Let . For , , , such that , , and , assume that

and

| (25) |

Assumption 7 requires the sample size to be ‘large enough’.

Assumption 7 (Minimum sample size ).

The intuition behind the final two assumptions is that if two forecasts exist, one stationary and one locally stationary, that behave similarly well in terms of approximations to their expected empirical mean squared errors, then and need to be large enough (in relation to , and ). Further, we require that exceeds a specified level (depending on , and ) to be able to provide bounds of the error of approximation of the local stationary process with the tangent process. The specific form of Assumptions 6 and 7 are due to technical reasons in our proof and, in fact, our simulation results in Section 4 suggest that the probability bounded in Theorem 3.1 will also be large for smaller than the threshold, as long as is chosen appropriately. The quantity is constructed to measure the difference between the MSPEs of the stationary predictors for different and the MSPEs of the locally stationary predictors for different scaled by a factor of . Assumptions 6 and 7 are slightly stronger than necessary, as we do not only require only those procedures to perform differently for the and that yield the best result, but we require it for any combination. This is due to our method of proof. On the other hand, it is obvious that some condition like this is required for consistency of the procedure, because if there is no difference in performance either approach may equally likely be chosen. It is important to note that in the situation where both approaches perform equally well we do not need the selection to be consistent.

The quantity depends on the model under consideration and, as and get larger, may potentially tend to zero. Thus, to employ Theorem 3.1 in practice, one has to analyse to determine the right bounds stated in Assumptions 6 and 7. In Section 3.4 we show how this can be done in the special case where and . There we show that if is chosen large enough or, in the case where the true model is non-stationary, if is chosen small enough, then is bounded away from . If , then, even in an asymptotic framework where and do not need to be bounded and as , then condition (25) will hold for large enough, if

Note that, and . Therefore, if , we have that condition (25) will hold for large enough, if and .

For the finite sample case, the quantity can easily be computed for any tvAR() model. A function performing the necessary calculations is provided in our R package forecastSNSTS. Numerical illustrations are provided in Section 4.

We are now ready to state the main result that guarantees that our procedure will, with high probability, choose the predictor that achieves the best empirical performance on the test set.

Theorem 3.1.

The proof of Theorem 3.1 is long and technical and therefore deferred to Section A. The probability in Theorem 3.1 tends to one if and , where we have used the notation for , as . Thus, Theorem 3.1 provides a “performance guarantee” of our model choice methodology in the sense that it asserts that, with high probability, the method which we have observed to perform better empirically in forecasting the observations from the second validation set will also perform better empirically in forecasting the future, not yet observed values of the test set.

3.4 Theoretical results for a simple, special cases

To illustrate the usefulness of Theorem 3.1 we now discuss the special case in which the model order is pre-determined to be 1, for both locally stationary and stationary forecasts, and the forecasting horizon is 1-step ahead; i. e., and . Though this special case is usually not of practical interest, restricting ourselves will allow to illustrate how the general conditions simplify and can more easily be understood. For the simplification we proceed by finding lower bounds for (uniformly in and ) which in turn allows us to state more explicit conditions that imply Assumptions 6 and 7.

To apply Theorem 3.1, we require that the MSPE of the stationary predictors are not to close to times the MSPE of the locally stationary predictors (cf. Assumption 6). Therefore, we now consider the following two cases:

-

(a)

The parameter is chosen large enough.

-

(b)

The parameter is chosen small enough and the true model is non-stationary.

To make the requirements precise, we define

| (26) |

| (27) |

and

| (28) |

where and are the local autocovariances from Assumption 1. The suprema and the infimum are with respect to points of the second validation set. Averaging of autocovariances in the first terms of and is across the training set and first validation set. Note that and that is a measure for the non-stationarity of the training set. In particular, it will vanish if the data stems from a stationary process. Further, note that is a measure for the strength of serial dependence.

The simplified conditions that imply Assumptions 6 and 7 for the special case, will be stated in terms of , and . Note that, also in the case where , the quantity in Assumptions 6 and 7 depends on , but the , and only depend on , , and . Therefore, the conditions in Lemmas 3.2 and 3.3 are indeed simpler than Assumptions 6 and 7. Further note that the local autocovariances can be determined easily for many time series models. If, for example the data stems from a tvAR(1) process with coefficient function , then we have , .

We now state two results about the special case of the procedure for -step ahead forecasting. The first result illustrates that the modified procedure will be consistent if is chosen large enough:

Lemma 3.2.

Further more, we have as a second result that if the true model is non-stationary in the sense that the quantity is large compared to for all , then we also have consistency for ’s that are small enough:

Lemma 3.3.

By Lemma 3.2 we have that, in the case where , and have been fixed, Assumption 6 will hold if and are chosen larger than some constant. This requirement is not restrictive, in the sense that we would typically consider and to diverge as diverges, such that by Theorem 3.1 the probability for consistent model choice will tend to one. In Lemma 3.3 the restrictions on and are even weaker, as in a typical application will tend to 0. In both Lemmas 3.2 and 3.3 the condition that implies Assumption 7 to hold is that is chosen larger than a multiple of , which is eventually satisfied if tends to zero.

Remark 3.4.

In Lemmas 3.2 and 3.3 a lower bound of the form

| (30) |

is proven, for the special case where and . This lower bound implies that Assumption 6 holds, but it is in fact stronger, as Assumption 6 allows for tending to 0, as and increase, as long as and are increasing fast enough. Under condition (30) and the conditions of Theorem 3.1 we have the following, stronger result:

which can be proved along the same lines of the proof of Theorem 3.1, together with inequality (70) from the proof of Lemma A.2, which is available in the arXiv’ed version of the manuscript (Kley et al., , 2019).

In particular, when the parameters , and are bounded sequences ( also bounded away from zero), we get the following bound:

| (31) |

where are constants that do not depend on or and is the constant from Assumption 5 (e. g., for sub-Gaussian processes: ).

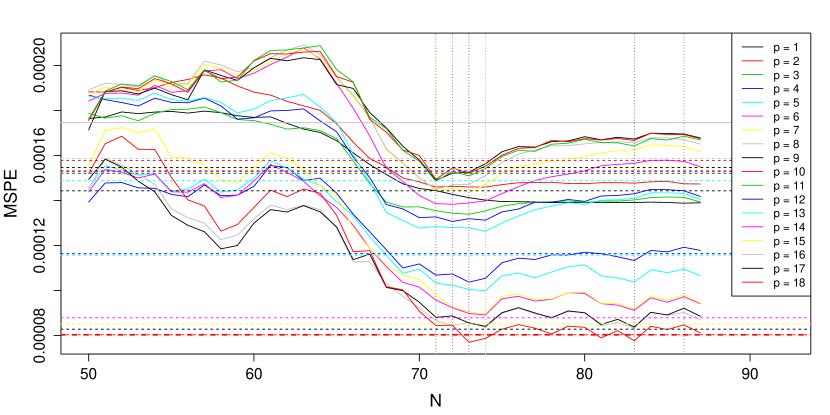

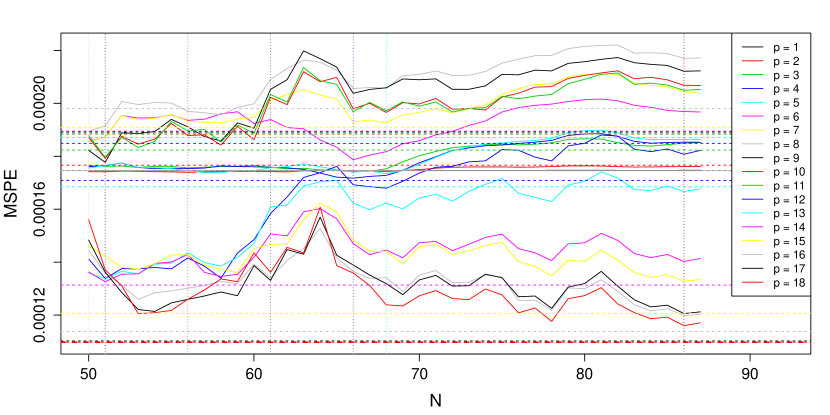

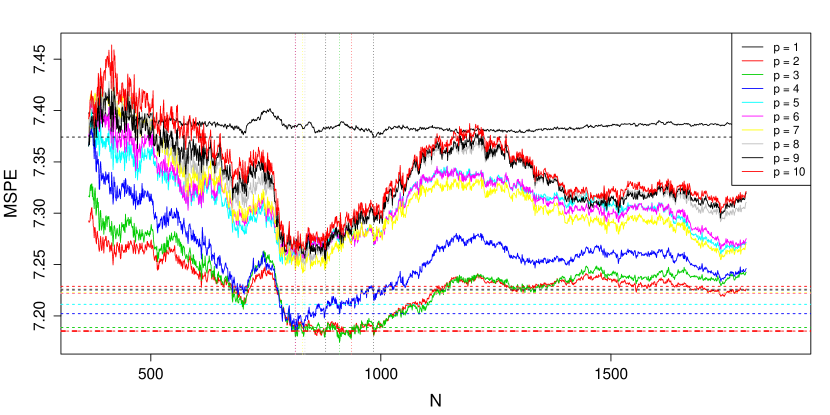

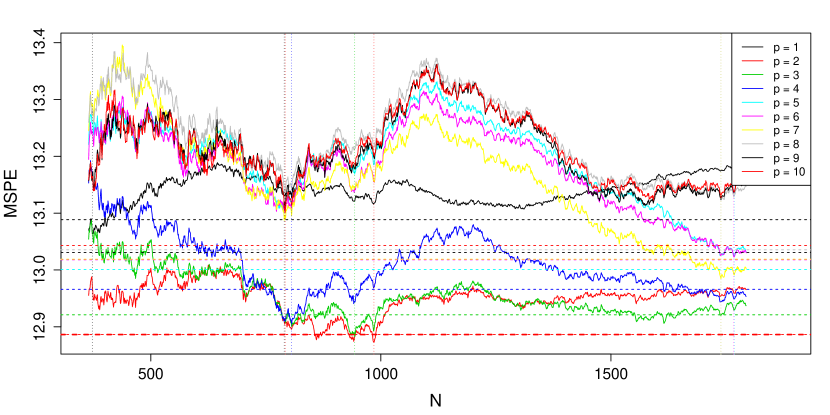

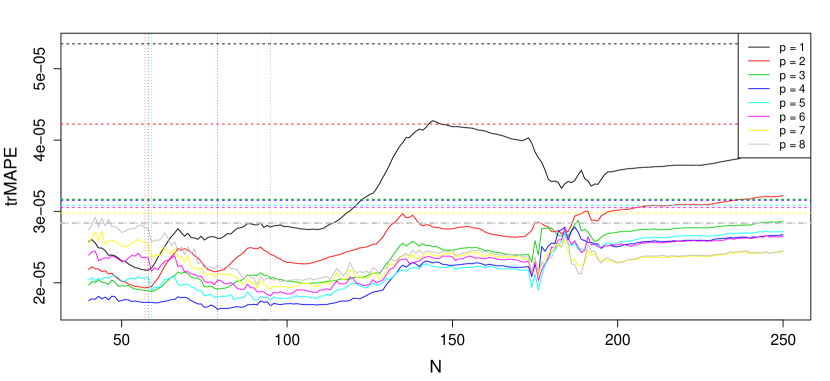

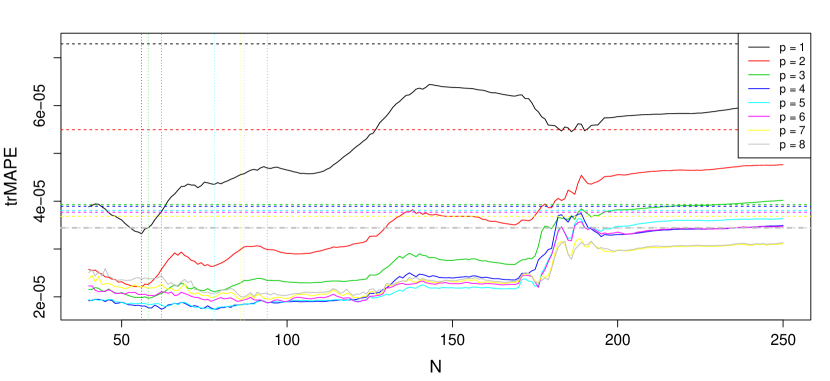

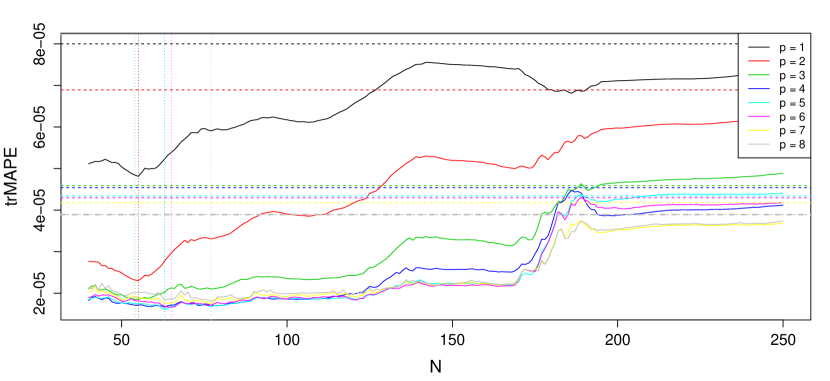

4 Simulations

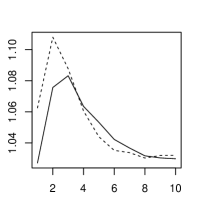

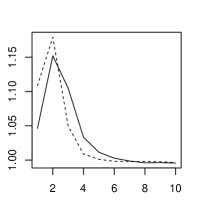

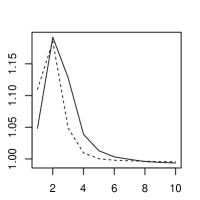

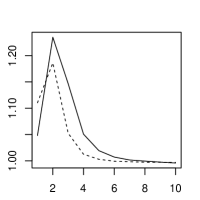

In this section we discuss finite sample properties of the estimates , defined in (7), and their population counterparts . The simulation study was conducted with the R package forecastSNSTS (R Core Team, , 2016; Kley et al., , 2017), available from The Comprehensive R Archive Network (CRAN). In particular, we investigate the performance of decision rule (7). To this end, we have considered 15 different tvAR models. Three of the models are stationary, the other 12 are non-stationary. Amongst the non-stationary processes we have some where the covariance structure changes quickly and some where the covariances change slowly. Further, we will have examples where the processes given by the parameters at some local time are almost unit root and some where they are not.

For each of the models we proceed as follows. We simulate sequences of length . The observations, with and as in Section 3, contain the training, validation and test set. We separate the test and validation sets of length . Thus, , , mark the end indices of the training set, the validation sets and the test set, respectively. We have chosen as a function of in such a way that and , as . The sizes of the three sets therefore are , and for the different sequence sizes, respectively.

As described in Section 3.1 we then, for any , determine linear -step ahead predictions for with . We determine the ‘stationary predictions’, with coefficients estimated for a given , from by from Step 3 of the procedure. For simplicity, we have chosen the same for every . We further determine ‘locally stationary predictions’ where the coefficients are used for and

where and . Instead of considering every integer between and as a possible segment size, we restrict the number of possible values for to a maximum of 25 elements to reduce computation time. The results did not change significantly when a larger number of elements was used. We then compare the predictors with respect to their empirical mean squared prediction error (MSPE) on the first validation set and, according to Step 4 of the procedure, choose the stationary predictor with that minimises the MSPE on amongst all stationary predictors and the locally stationary predictor with which minimizes the MSPE on amongst all the locally stationary predictors.

For those two predictors we then determine the empirical mean squared prediction errors and , defined in (8), on the validation and test set, respectively. We record seven pieces of information: , , , , , and . We replicate the experiment times.

Now we define the first two models. Both are tvAR(1) models defined by two periodic coefficient functions, namely the models are

| (32) | ||||

| (33) |

The innovations are i. i. d Gaussian white noise. In this section we discuss the above two models in detail. The remaining processes are defined in Appendix J (Kley et al., , 2019), where to also the corresponding tables and figures for them are being deferred.

6 Analysis of the localised Yule-Walker estimator under general conditions and local stationarity

In this section we discuss the probabilistic properties of the localised Yule-Walker estimator defined in (1). We believe the results to be of independent interest and therefore present them in this separate section. They are also key results for the proofs of the result in Section 3.3. Our results will hold under Assumptions 1–5 (cf. Section 3.3). The assumptions are not restrictive and, in particular, the concentration result in this section will hold for a broad class of locally stationary processes and, in particular, does not require that the data come from a tvAR() model. Further, we allow for any and, in particular, allow for a diverging model order , as . We do not, as do for example Dahlhaus and Giraitis, (1998), require that .

The main result of this section (Theorem 6.1) provides a non-asymptotic bound for the Euclidean distance of to the following population quantity:

| (35) |

The Yule-Walker estimator is widely used in practice and and its properties have been studied in detail under various conditions. Bercu et al., (1997, 2000) and Bercu, (2001) derive large deviation principles for Gaussian AR processes when the model order is 1. A simple exponential inequality, also for model order 1, is given in Section 5.2 of Bercu and Touati, (2008). Yu and Si, (2009) prove a large deviation principle for general, but fixed, model order. Jirak, (2012, 2014) derives simultaneous confidence bands. The cited results all require that the underlying process is stationary. Dahlhaus and Giraitis, (1998) analyse the bias and variance of the localised Yule-Walker estimator in the framework of local stationarity. They do not, however, provide an exponential inequality, and, as far as we are aware, no result as the one we provide below is available at present. The exponential inequality in Theorem 6.1, which we now state, is explicit in terms of all parameters and constants. We make use of the explicitness to derive Corollary 6.2, by which the localised Yule-Walker estimator is strongly, uniformly consistent, even when the model order is diverging as the sample size grows.

Theorem 6.1.

Theorem 6.1 is a key ingredient to the proof of Lemma A.1 which is essential to the proof of the performance-guarantee-result (Theorem 3.1) of our procedure. Further, it implies

Corollary 6.2.

Remark 6.3.

For any stationary AR() model we have that corresponds to the vector of coefficients. This can be seen from Lemma B.2 and the fact that if the model is stationary. Thus, choosing and , our result yields the same rate as Theorem 1 in Lai and Wei, (1982), by which the (least squares) estimator is strongly consistent with rate . An early consistency result for the Yule-Walker estimate with diverging model order is Theorem 6 in Hong-Zhi et al., (1982). Under the assumption that , or , sufficiently large, they prove that the rate of convergence is .

7 Conclusion

In this paper, we have presented a method to choose between different forecasting procedures, based on the empirical mean squared prediction errors the procedures achieve. Using the empirical rather than the asymptotic mean squared prediction error, our procedure automatically takes into account that different models should be preferred depending on the amount of data available, which is an important difference to the Focused Information Criterion by Claeskens and Hjort, (2003). Working in the general framework of locally stationary time series we choose from two classes of forecasts that were motivated by approximating the serial dependence of the time series by time-varying or traditional autoregressive models. The procedure implicitly balances the modelling bias (which is lower if the model is more complex) and the variance of estimation (which increases for more complex models). Our two step procedure automatically chooses the number of forecasting coefficients to be used and the segment size from which the forecasting coefficients are estimated.

In a comprehensive simulation study we have illustrated that it is often advisable to use a forecasting procedure derived from a simpler model when not a vast amount of data is available. In particular, in the tvAR models of our simulations, if the variation over time is not very pronounced and when the tangent processes are not close to being unit root it is advisable to work with the simpler stationary model, even when the data are non-stationary.

As an important side result of our rigorous theoretical analysis of the method, we have shown that the localised Yule-Walker estimator is strongly, uniformly consistent under local stationarity.

References

- Akaike, (1969) Akaike, H. (1969). Fitting autoregressive models for prediction. Annals of the Institute of Statistical Mathematics, 21(1):243–247.

- Akaike, (1970) Akaike, H. (1970). A fundamental relation between predictor identification and power spectrum estimation. Annals of the Institute of Statistical Mathematics, 22(1):219–223.

- Baillie, (1979) Baillie, R. T. (1979). Asymptotic prediction mean squared error for vector autoregressive models. Biometrika, 66(3):675–8.

- Bapat and Sunder, (1985) Bapat, R. and Sunder, V. (1985). On majorization and Schur products. Linear Algebra and its Applications, 72:107 – 117.

- Bercu, (2001) Bercu, B. (2001). On large deviations in the Gaussian autoregressive process: stable, unstable and explosive cases. Bernoulli, 7(2):299–316.

- Bercu et al., (2000) Bercu, B., Gamboa, F., and Lavielle, M. (2000). Sharp large deviations for Gaussian quadratic forms with applications. ESAIM: Probability and Statistics, 4:1–24.

- Bercu et al., (1997) Bercu, B., Gamboa, F., and Rouault, A. (1997). Large deviations for quadratic forms of stationary Gaussian processes. Stochastic Processes and their Applications, 71(1):75 – 90.

- Bercu and Touati, (2008) Bercu, B. and Touati, A. (2008). Exponential inequalities for self-normalized martingales with applications. The Annals of Applied Probability, 18(5):1848–1869.

- Bhansali, (1996) Bhansali, R. J. (1996). Asymptotically efficient autoregressive model selection for multistep prediction. Annals of the Institute of Statistical Mathematics, 48:577–602.

- Birr et al., (2017) Birr, S., Volgushev, S., Kley, T., Dette, H., and Hallin, M. (2017). Quantile spectral analysis for locally stationary time series. Journal of the Royal Statistical Society: Series B, 79(5):1619–1643.

- Bosq, (1998) Bosq, D. (1998). Nonparametric statistics for stochastic processes: estimation and prediction. Springer, New York, 2 edition.

- Brillinger, (1975) Brillinger, D. R. (1975). Time Series: Data Analysis and Theory. Holt, Rinehart and Winston, Inc., New York.

- Brockwell and Davis, (1991) Brockwell, P. J. and Davis, R. A. (1991). Time Series: Theory and Methods. Springer, New York.

- Brownlees and Gallo, (2008) Brownlees, C. T. and Gallo, G. M. (2008). On variable selection for volatility forecasting: The role of focused selection criteria. Journal of Financial Econometrics, 6:513–539.

- Chan and Wei, (1987) Chan, N. H. and Wei, C. Z. (1987). Asymptotic inference for nearly nonstationary AR(1) processes. Ann. Statist., 15(3):1050–1063.

- Chen et al., (2010) Chen, Y., Härdle, W., and Pigorsch, U. (2010). Localized realized volatility modeling. Journal of the American Statistical Association, 105(492):1376–1393.

- Claeskens et al., (2007) Claeskens, G., Croux, C., and Van Kerckhoven, J. (2007). Prediction-focused model selection for autoregressive models. Australian & New Zealand Journal of Statistics, 49(4):359–379.

- Claeskens and Hjort, (2003) Claeskens, G. and Hjort, N. L. (2003). The focused information criterion [with discussion]. Journal of the American Statistical Association, 98:900–916.

- Dahlhaus, (1996) Dahlhaus, R. (1996). On the Kullback-Leibler information divergence of locally stationary processes. Stochastic Processes and their Applications, 62(1):139 – 168.

- Dahlhaus, (1997) Dahlhaus, R. (1997). Fitting time series models to nonstationary processes. Annals of Statistics, 25(1):1–37.

- Dahlhaus, (2012) Dahlhaus, R. (2012). Locally stationary processes. In Rao, T. S., Rao, S. S., and Rao, C., editors, Time Series Analysis: Methods and Applications, volume 30 of Handbook of Statistics, pages 351 – 413. Elsevier.

- Dahlhaus and Giraitis, (1998) Dahlhaus, R. and Giraitis, L. (1998). On the optimal segment length for parameter estimates for locally stationary time series. Journal of Time Series Analysis, 19(6):629–655.

- Das and Politis, (2018) Das, S. and Politis, D. N. (2018). Predictive inference for locally stationary time series with an application to climate data. ArXiv:1712.02383.

- Demmel, (1997) Demmel, J. W. (1997). Applied Numerical Linear Algebra. siam, Philadelphia.

- Dette et al., (2011) Dette, H., Preuß, P., and Vetter, M. (2011). A measure of stationarity in locally stationary processes with applications to testing. Journal of the American Statistical Association, 106(495):1113–1124.

- Doukhan, (1994) Doukhan, P. (1994). Mixing: Properties and Examples. Springer, New York.

- Dwivedi and Subba Rao, (2010) Dwivedi, J. and Subba Rao, S. (2010). A test for second order stationarity based on the discrete fourier transform. Journal of Time Series Analysis, 32:68–91.

- Dzhaparidze et al., (1994) Dzhaparidze, K., Kormos, J., van der Meer, T., and van Zuijlen, M. (1994). Parameter estimation for nearly nonstationary AR(1) processes. Mathematical and Computer Modelling, 19(2):29 – 41.

- Fryzlewicz and Subba Rao, (2011) Fryzlewicz, P. and Subba Rao, S. (2011). Mixing properties of ARCH and time-varying ARCH processes. Bernoulli, 17(1):320–346.

- Giraitis et al., (2013) Giraitis, L., Kapetanios, G., and Price, S. (2013). Adaptive forecasting in the presence of recent and ongoing structural change. Journal of Econometrics, 177(2):153–170.

- Goldenshluger and Zeevi, (2001) Goldenshluger, A. and Zeevi, A. (2001). Nonasymptotic bounds for autoregressive time series modeling. Annals of Statistics, 29(2):417–444.

- Gray, (2009) Gray, R. M. (2009). Toeplitz and Circulant Matrices: A review. now publishers, Boston.

- Hallin, (1978) Hallin, M. (1978). Mixed autoregressive-moving average multivariate processes with time-dependent coefficients. Journal of Multivariate Analysis, 8(4):567 – 572.

- Hong-Zhi et al., (1982) Hong-Zhi, A., Zhao-Guo, C., and Hannan, E. J. (1982). Autocorrelation, autoregression and autoregressive approximation. Annals of Statistics, 10(3):926–936.

- Jirak, (2012) Jirak, M. (2012). Simultaneous confidence bands for Yule-Walker estimators and order selection. Annals of Statistics, 40(1):494–528.

- Jirak, (2014) Jirak, M. (2014). Simultaneous confidence bands for sequential autoregressive fitting. Journal of Multivariate Analysis, 124:130 – 149.

- Johnson and Nylen, (1990) Johnson, C. R. and Nylen, P. (1990). Cases of equality for the spectral norm submultiplicativity of the hadamard product. Linear and Multilinear Algebra, 27(2):121–127.

- Kley et al., (2017) Kley, T., Fryzlewicz, P., and Preuß, P. (2017). forecastSNSTS: Forecasting for Stationary and Non-Stationary Time Series. R package version 1.1-1.

- Kley et al., (2019) Kley, T., Preuß, P., and Fryzlewicz, P. (2019). Predictive, finite-sample model choice for time series under stationarity and non-stationarity. ArXiv:1611.04460v3.

- Lai and Wei, (1982) Lai, T. L. and Wei, C. Z. (1982). Least squares estimates in stochastic regression models with applications to identification and control of dynamic systems. Annals of Statistics, 10(1):154–166.

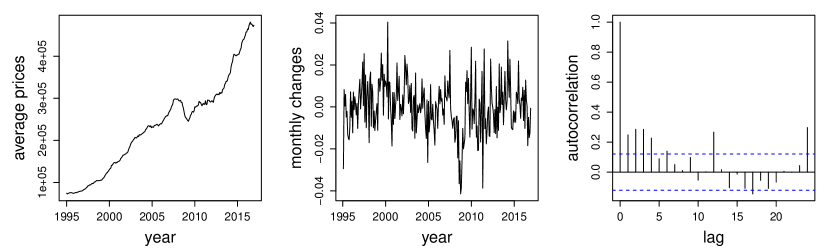

- Landregistry, (2019) Landregistry (2019). Uk house price index. http://landregistry.data.gov.uk/app/ukhpi. Accessed: 2019-01-11.

- Magnus and Neudecker, (1988) Magnus, J. R. and Neudecker, H. (1988). Matrix differential calculus with applications in statistics and econometrics. Wiley.

- McDonald et al., (2016) McDonald, D. J., Shalizi, C. R., and Schervish, M. (2016). Nonparametric risk bounds for time-series forecasting. ArXiv:1212.0463.

- Mikosch and Starica, (2004) Mikosch, T. and Starica, C. (2004). Non-stationarities in financial time series, the long range dependence and the IGARCH effects. The Review of Economics and Statistics, 86:378–390.

- Moulines et al., (2005) Moulines, E., Priouret, P., and Roueff, F. (2005). On recursive estimation for time varying autoregressive processes. Annals of Statistics, 33(6):2610–2654.

- Nason, (2013) Nason, G. (2013). A test for second-order stationarity and approximate confidence intervals for localized autocovariances for locally stationary time series. Journal of the Royal Statistical Society: Series B, 75:879–904.

- Palma et al., (2013) Palma, W., Olea, R., and Ferreira, G. (2013). Estimation and forecasting of locally stationary processes. Journal of Forecasting, 32:86–96.

- Paparoditis, (2009) Paparoditis, E. (2009). Testing temporal constancy of the spectral structure of a time series. Bernoulli, 15:1190–1221.

- Paparoditis, (2010) Paparoditis, E. (2010). Validating stationarity assumptions in time series analysis by rolling local periodograms. Journal of the American Statistical Association, 105:839–851.

- Peña and Sánchez, (2007) Peña, D. and Sánchez, I. (2007). Measuring the advantages of multivariate vs. univariate forecasts. Journal of Time Series Analysis, 28(6):886–909.

- Politis, (2015) Politis, D. N. (2015). Model-Free Prediction and Regression: A Transformation-Based Approach to Inference. Springer.

- Preuß and Vetter, (2013) Preuß, P. and Vetter, M. (2013). Discriminating between long-range dependence and non-stationarity. Electron. J. Statist., 7:2241–2297.

- Preuß et al., (2013) Preuß, P., Vetter, M., and Dette, H. (2013). A test for stationarity based on empirical processes. Bernoulli, 19(5B):2715–2749.

- Priestley, (1965) Priestley, M. B. (1965). Evolutionary spectra and non-stationary processes. Journal of the Royal Statistical Society. Series B (Methodological), 27(2):204–237.

- Priestley, (1981) Priestley, M. B. (1981). Spectral Analysis and Time Series. Academic Press.

- R Core Team, (2016) R Core Team (2016). R: A Language and Environment for Statistical Computing. R Foundation for Statistical Computing, Vienna, Austria.

- Reinsel, (1980) Reinsel, G. (1980). Asymptotic properties of prediction errors for the multivariate autoregressive model using estimated parameters. Journal of the Royal Statistical Society: Series B, 42(3):328–333.

- Richter and Dahlhaus, (2017) Richter, S. and Dahlhaus, R. (2017). Cross validation for locally stationary processes. ArXiv:1705.10046.

- Rohan and Ramanathan, (2011) Rohan, N. and Ramanathan, T. V. (2011). Order selection in arma models using the focused information criterion. Australian & New Zealand Journal of Statistics, 53(2):217––231.

- Rossi, (2013) Rossi, B. (2013). Advances in forecasting under instability. In Elliott, G. and Timmermann, A., editors, Handbook of Economic Forecasting, volume 2B, pages 1203–1324. Elsevier.

- Roueff and Sanchez-Perez, (2016) Roueff, F. and Sanchez-Perez, A. (2016). Locally stationary processes prediction by auto-regression. ArXiv:1602.01942v1.

- Roueff and Sanchez-Perez, (2018) Roueff, F. and Sanchez-Perez, A. (2018). Prediction of weakly locally stationary processes by auto-regression. ArXiv:1602.01942v3.

- Saulis and Statulevičus, (1991) Saulis, L. and Statulevičus, V. A. (1991). Limit Theorems for Large Deviations. Kluwer, Dordrecht.

- Stroock, (2011) Stroock, D. W. (2011). Probability Theory: An Analytic View. Cambridge University Press, New York, 2 edition.

- Subba Rao, (1970) Subba Rao, T. (1970). The fitting of non-stationary time-series models with time-dependent parameters. Journal of the Royal Statistical Society. Series B (Methodological), 32(2):312–322.

- Vogt, (2012) Vogt, M. (2012). Nonparametric regression for locally stationary time series. Annals of Statistics, 40(5):2601–2633.

- Vogt and Dette, (2015) Vogt, M. and Dette, H. (2015). Detecting smooth changes in locally stationary processes. Annals of Statistics, 43(2):713–740.

- von Sachs and Neumann, (2000) von Sachs, R. and Neumann, M. H. (2000). A wavelet-based test for stationarity. Journal of Time Series Analysis, 21:597–613.

- Xia and Tong, (2011) Xia, Y. and Tong, H. (2011). Feature matching in time series modeling. Statistical Science, 26(1):21–46.

- Yu and Si, (2009) Yu, M. and Si, S. (2009). Moderate deviation principle for autoregressive processes. Journal of Multivariate Analysis, 100(9):1952 – 1961.

- Zhang and Koreisha, (2015) Zhang, Y. and Koreisha, S. (2015). Adaptive order determination for constructing time series forecasting models. Communications in Statistics - Theory and Methods, 44(22):4826–4847.

Appendix

In Section A we provide proofs of the results in the main text. In Section A.3, we provide a proof for Theorem 3.1, the performance guarantee of our model selection procedure. The proof relies on properties of the empirical mean squared prediction errors for fixed model order and segment (Lemmas A.1–A.3) which we state in Section A.2. Theorem 6.1 which is about concentration properties of the localised Yule-Walker estimate under local stationarity, is proved in Section A.4. Corollary 6.2 which is about the strong consistency of the localised Yule-Walker estimate is proved in Section A.5. Lemmas 3.2 and 3.3, which fascilitate our discussion of the special case of our procedure are proved in Section A.6.

In Sections B–D we provide technical results about the properties of quantities related to the second order moments. In Section B we state results about the vector , defined in (19), around which the localised Yule-Walker estimator concentrates. We also discuss how it is related to the mean square minimising 1-step ahead forecasting coefficients. In Section C we discuss properties of , the -step ahead version of . Further, we establish properties of and from the definition of that is important for Assumptions 6 and 7. In Section D.2, we provide approximation results for expectations of Toepliz matrices of empirical localised autocovariances , defined in (3) and in Section D.3 we establish concentration results. In Section E we state a number of technical lemmas that we use in the proofs of our results. We state these results in a separate section, because we believe that they are useful for proving similar results in the future.

Sections F–J that are only available in the extended, arXiv’ed version of the manuscript, cf. Kley et al., (2019), contain supplementary material. In Section F we provide the proofs of Lemmas A.1–A.3. In Section H we cite two results from Saulis and Statulevičus, (1991) which we use for our proof in Section G.4. In Sections I–J we provide additional material for our simulation and empirical study.

Appendix A Proofs of Theorems 3.1 and 6.1, of Corollary 6.2, and of Lemmas 3.2 and 3.3

A.1 Outlook

In this section we provide the proofs of the results from Sections 3.3 and 6. In Section A.2 we state and discuss three auxiliary results (Lemmas A.1–A.3) which facilitate the proof of our main result (Theorem 3.1). The auxiliary results are about the empirical mean squared prediction error. Their proofs are deferred to Section F (Kley et al., , 2019). The proof of Theorem 3.1, by which our model selection procedure chooses models consistently with high probability, is then stated in Section A.3. Because the proof of Lemma A.1 heavily relies on our result about the Yule-Walkers estimators (Theorem 6.1), our proof of Theorem 3.1, implicitly, also depends on it. The proof of Theorem 6.1 and its corollary (Corollary 6.2), by which the localised Yule-Walker estimator is uniformly, strongly consistent, are stated in Sections A.4 and A.5, respectively. For the proof of Theorem 6.1 we employ some of our results about the localised empirical autocovariance estimate from Section D and a technical result from Section E. For the readers convenience, we include Figure 10 in which the dependence of the various results is illustrated graphically.

A.2 Three technical lemmas for the proof

We now introduce two quantities that combine constants from the assumptions. Stating the results in terms of these constants will help to better interpret the bounds and significantly shorten otherwise complicated expressions. To this end, we define

| (36) |

The constant can be interpreted in terms of the strength of serial correlation. Note that will be smaller if there is little variation (uniform in local time) of the spectral density with respect to frequency. In particular, it will be minimal if the spectral density is constant. This would corresponds to the case of white noise. The constant can be interpreted as divergence from stationarity. In particular, note the meaning of the two summands of the first factor. The constant corresponds to the rapidity of changes in stationarity and will vanish in case of stationarity. The constant corresponds to the quality of locally approximating the correlation structure with a stationary processes correlation structure. It, also, vanishes if the underlying process is stationary.

The aim of the auxiliary results is to approximate general mean squared prediction errors of the form

| (37) |

with defined in (4) and .

The first auxiliary result (Lemma A.1) entails that the quantity defined in (37) is, with high probability, close to

| (38) |

with

| (39) |

where is defined in (35), denotes the first canonical unity vector of dimension and denotes a Jordan block with all eigenvalues equal to zero. The second auxiliary result (Lemma A.2) provides a simplified probability bound for the result in Lemma A.1 that can be applied in an especially relevant case.

By our third auxiliary result (Lemma A.3) we have that in turn can be approximated by , where is the quantity defined in (21), with continuous time indices and . Note that this quantity also appears in defined in (24) which is a relevant component of Assumptions 6 and 7.

Some comparison of , defined in (38), and , as defined in (21) are in order: Note that is defined as the expectation of a modified version of , the modification being that is exchanged by . As before, we will denote .

We have that approximates , with defined in (5). Therefore, the expectation of the empirical mean squared prediction error (37) we are considering is naturally an average of these quantities:

We now state the results that the quantities defined in (37) and (38) are close, with high probability.

Lemma A.1.

In a typical application the bound will be small. More precisely, the following, more accessible bound for , proved in Section F (Kley et al., , 2019), will be useful

Lemma A.2.

There exist constants and , defined in the proof, such that for any

| (40) |

we have

Note that we are interested in the scenario where may be small. Therefore, if we allow that and may be large, we have to require and to be of a minimum size.

We now state the result that the quantities defined in (38) and (21) are close. The quality of the approximation depends on the parameters , and , but is uniform with respect to , and :

Lemma A.3.

The proofs of the three lemmas are long and technical. We therefore defer them to Section F (Kley et al., , 2019).

A few comments about Lemma A.3 are in order. Note that the approximation error is zero in case of a stationary time series, as then . Note further, that the approximation will be better, if and are small compared to . More precisely, if , then the difference will vanish asymptotically. In particular, if , then it would suffice to assume that , for the approximation error to vanish asymptotically.

A.3 Proof of Theorem 3.1

The constants , and are defined as

| (41) |

where and

| (42) | ||||

with . In the definitions, we have and the constants from Assumption 2, and the constants from Assumption 3, and and the constants from Assumption 5.

To compact notation, we denote , by and by . Further, denote and by and , respectively. Further, we abbreviate and .

First note that Assumptions 6 and 7 imply that

Therefore, the conditions of Lemmas A.1 and A.3 are satisfied. Further, note that since

and because for all , we have that the bound from Lemma A.3 can again be bounded

| (43) |

Finally, note that by Assumption 7, we have

which implies that (a quantity related to the bound from Lemma C.4(iv)) can be bounded

| (44) |

Now, for the proof of the Theorem, note that

| (45) |

We now bound the part of the right hand side of (45) that involves the quantity . Using the fact that

we have the first inequality of

| (46) | |||

| (47) |

where and . For the inequality in (46) we have used the definition of and . For the first inequality in (47) we have used Lemmas A.1 and A.3 and (43) to obtain

| (48) |

and

| (49) |

For the second inequality in (47) we have used that

and .

We now bound the part of the right hand side of (45) that involves the quantity . We have

| (50) |

Note that we have

where the first two terms can be bound by an application of (48) and the indicator function vanishes for all satisfying the condition of the Theorem, because

where Lemma C.4(iv) was employed to obtain (44) for the last inequality.

An application of Lemma A.2 finishes the proof of the theorem.

Remark A.4.

Equations (48)–(49), which are immediate consequences of Lemmas A.1 and A.3, can be used to derive the almost sure convergence of

under appropriate conditions, using a classical Borel-Cantelli argument.

This asymptotic view of and , in particular, implies that we may interpret as an approximation of the expectation of the empirical MSPE for an -step ahead linear forecast of order , where observations up to (local) time have been made. The and are (localised) length which are related to the segment length of observations used for the estimation of the forecasting coefficients and the segment from which the observations that are being forecasted are taken, respectively.

We now proceed with the proofs of the results from Section 6.

A.4 Proof of Theorem 6.1

Let , , , and . By Lemma D.3(ii-c) we deduce that is invertible for , because it is positive definite with smallest eigenvalue larger or equal to . An application of Lemma E.6, with the spectral norm as the matrix norm and the Euclidean norm as the vector norm yields

where we have use Lemma D.3(ii-c) again to bound . In the last step we employed that . Further, we have used that satisfies

Thus, by Hölder’s inequality

For the Euclidean norm we have used

Finally, by Corollary D.2(iii) and Lemma D.3(i-b), we have

where the second inequality holds for , which is the case, as is assumed. Here we also have used that , as all entries of are between 0 and 1. Applying Lemma D.4 yields the assertion, because

where , and the third line follows from the fact, for any two integers and with we have that is an increasing sequence. This is easy to see: . Note that , such that this condition of Lemma D.4 is met.

A.5 Proof of Corollary 6.2

Note the fact that, if is a sequence with , as , then

Thus, employing the Borel-Cantelli lemma, it suffices to show that, for any given and sequence with , we have

This follows, since we have

for large enough. In the second inequality we have used the fact that, due to , there exists a such that , for large enough. Note that we have , from , and , such that, in the third inequality, Theorem 6.1 can be applied, where we have also used the fact that, under the assumptions made

implying that, for large enough, we have

This completes the proof.

A.6 Proofs of Lemmas 3.2 and 3.3

For the proof of Lemma 3.2 it suffices to show that

Likewise, to show Lemma 3.3, we bound with on the right hand side.

To find the lower bound we want, it therefore suffices to proof lower bounds, for every , of the following difference

| (51) |

For Lemma 3.3 we will bound . For notational convenience we omit the ’s and denote

By elementary considerations it can be shown that

| (52) |

By (28), we have and by (27), we have . Further, we have that , uniformly with respect to , which can be seen as follows: first, note that

Further, note that we have and thus

| (53) |

where we have used that and . Employing (52), we have now brought the tools together to prove Lemma 3.2:

For the first inequality we have used the fact that and the definitions of and . For the second inequality we have used the condition imposed on .

Finally, employing (52) again, we prove Lemma 3.3:

where in the first inequality we have used

as we have and thus follows from condition (29). For the second inequality we have used the definition of and again condition (29), by which we have . Finally, for the third inequality we have used that by assumption in the Corollary .

The first bound, , implies that if

and

then Assumption 6 holds, and if

then Assumption 7 holds. Hence, we have proven Lemma 3.2 where the constants can be chosen as

and

The second bound, , implies that if

and

then Assumption 6 holds, and if

then Assumption 7 holds. Hence, we have proven Lemma 3.3 where the constants can be chosen as

and

Appendix B Lemmas regarding

B.1 Outlook