Taras Bodnara, Yarema Okhrinb and Nestor Parolyac,

a Department of Mathematics, Stockholm University, Roslagsvägen 101, SE-10691 Stockholm, Sweden

b Department of Statistics, University of Augsburg, Universitätsstr. 16, D-86159 Augsburg, Germany

c Department of Applied Mathematics, Delft University of Technology, Mekelweg 4,

2628 CD Delft, The Netherlands

Abstract

In this paper we estimate the mean-variance portfolio in the high-dimensional case using the recent results from the theory of random matrices. We construct a linear shrinkage estimator which is distribution-free and is optimal in the sense of maximizing with probability the asymptotic out-of-sample expected utility, i.e., mean-variance objective function for different values of risk aversion coefficient which in particular leads to the maximization of the out-of-sample expected utility and to the minimization of the out-of-sample variance.

One of the main features of our estimator is the inclusion of the estimation risk related to the sample mean vector into the high-dimensional portfolio optimization. The asymptotic properties of the new estimator are investigated when the number of assets and the sample size tend simultaneously to infinity such that . The results are obtained under weak assumptions imposed on the distribution of the asset returns, namely the existence of the moments is only required.

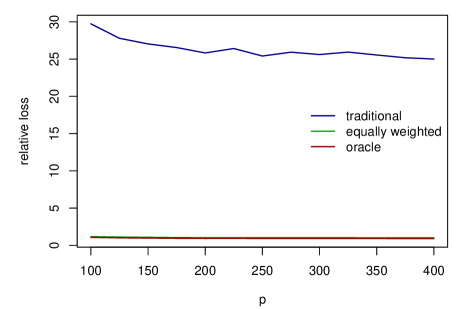

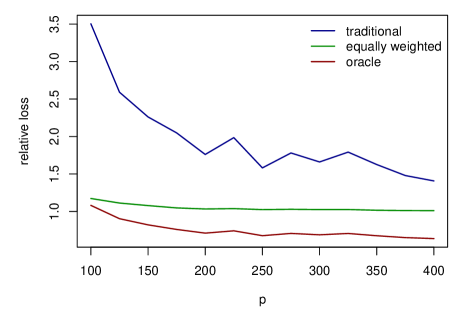

Thereafter we perform numerical and empirical studies where the small- and large-sample behavior of the derived estimator is investigated. The suggested estimator shows significant improvements over the existent approaches including the nonlinear shrinkage estimator and the three-fund portfolio rule, especially when the portfolio dimension is larger than the sample size. Moreover, it is robust to deviations from normality.

JEL Classification: G11, C13, C14, C58, C65

Keywords: expected utility portfolio, large-dimensional asymptotics, covariance matrix estimation, random matrix theory.

1 Introduction

In the seminal paper of Markowitz, (1952) the author suggests to determine the optimal composition of a portfolio of financial assets by minimizing the portfolio variance assuming that the expected portfolio return attains some prespecified fixed value. By varying this value we obtain the whole efficient frontier in the mean-standard deviation space. Despite of its simplicity, this approach justifies the advantages of diversification and is a standard technique and benchmark in asset management. Equivalently (see, Tobin, (1958), Bodnar et al., (2013)) we can obtain the same portfolios by maximizing the expected quadratic utility (EU) with the optimization problem given by

|

|

|

(1.1) |

where is the vector of portfolio weights, is the -dimensional vector of ones, and are the -dimensional mean vector and the covariance matrix of asset returns, respectively. The quantity determines the investor’s behavior towards risk.

It must be noted that the maximization of the mean-variance objective function (1.1) is equivalent to the maximization of the exponential utility (CARA) function under the assumption of normality of the asset returns. In this case equals the investor’s absolute risk aversion coefficient (see, e.g., Pratt, (1964)).

The solution of the optimization problem (1.1) is well known and it is given by

|

|

|

(1.2) |

where

|

|

|

(1.3) |

and

|

|

|

(1.4) |

is the vector of the weights of the global minimum variance (GMV) portfolio. By changing the risk-aversion coefficient we obtain the set of optimal portfolios. Merton, (1972) proved that this set is a parabola in the mean-variance (R-V) space (cf. Bodnar and Schmid, (2009)) given by

|

|

|

(1.5) |

where

|

|

|

(1.6) |

are the expected return and the variance of the GMV portfolio, and

|

|

|

(1.7) |

is its slope parameter. The quantity is always non-negative since is a positive semidefinite matrix. Moreover, when is equal to zero, then the efficient frontier degenerates into a straight line with the GMV portfolio being the only optimal portfolio.

In practice, however, the above mentioned approach of constructing an optimal portfolio frequently shows poor out-of-sample performance in terms of various performance measures. Even naive portfolio strategies, e.g., equally weighted portfolio (see, DeMiguel et al., (2009)), often outperform the mean-variance strategy. One of the reasons is the estimation risk. The unknown parameters and have to be estimated using historical data on asset returns. This results in the ”plug-in” estimator of the EU portfolio (1.2) which is a traditional and simple way to evaluate the portfolio in practice. This estimator is constructed by replacing the mean vector and the covariance matrix with their sample counterparts in (1.2). Okhrin and Schmid, (2006) derive the expectation and the variance of the sample portfolio weights under the assumption that the asset returns follow a multivariate normal distribution, whereas Bodnar and Schmid, (2011) obtain the exact finite-sample distribution. Recently, Bodnar et al., (2016) extended these results to the case .

The estimation of the parameters has a negative impact on the performance of the asset allocation strategy. This is noted in a series of papers with Merton, (1980), Best and Grauer, (1991), Chopra and Ziemba, (1993) among others. Several approaches have arisen to reduce the consequences of the estimation risk. One strand of research opts for the Bayesian framework and using appropriate priors takes the estimation risk into account already while building the portfolio. The second strand relies on the shrinkage techniques and is related to the method exploited in this paper. A straightforward way to improve the properties of the estimators for and is to use the shrinkage approach (see, Jorion, (1986), Ledoit and Wolf, (2004)). Alternatively, one may apply the shrinkage estimation to the portfolio weights directly. Golosnoy and Okhrin, (2007) consider the multivariate shrinkage estimator by shrinking the portfolios with and without the riskless asset to an arbitrary static portfolio. A similar technique is used by Frahm and Memmel, (2010), who construct a feasible shrinkage estimator for the GMV portfolio which dominates the traditional one. At last, Bodnar et al., (2018) suggest a shrinkage estimator for the GMV portfolio which is feasible even for the singular sample covariance matrix.

An important issue nowadays is, however, the asset allocation for large portfolios. The sample estimators work well only in the case when the number of assets is fixed and substantially smaller than the sample size . This case is known as the standard asymptotics in statistics (see, Le Cam and Lo Yang, (2000)). Under this asymptotics the traditional sample estimator is a consistent estimator for the EU portfolio. But what happens when the dimension and the sample size are comparable of size, say and ? Technically, here we are in the situation when both the number of assets and the sample size tend to infinity. In the case when tends to some concentration ratio this asymptotics is known as high-dimensional asymptotics or “Kolmogorov” asymptotics (see, e.g., Bai and Silverstein, (2010)). If is close to one the sample covariance matrix tends to be close to a singular one and when it becomes singular.

Thus it is very unstable and tends to under- or overestimate the true parameters for smaller but close to 1 (see, Bai and Shi, (2011)). As a result, the sample estimator of the EU portfolio behaves badly in this case both from the theoretical and practical points of view (see, e.g., El Karoui, (2010); Rubio et al., (2012)). For the inverse sample covariance matrix does not exist and the portfolio cannot be constructed in the traditional way.

Taking the above mentioned information into account the aim of the paper is to construct a feasible and simple shrinkage estimator of the EU portfolio which is optimal in an asymptotic sense and is additionally distribution-free. The estimator is developed using the fast growing branch of probability theory, namely random matrix theory. The main result of this theory is proved by Marčenko and Pastur, (1967) and further extended under very general conditions by Silverstein, (1995). Now it is called Marenko-Pastur equation. Its importance arises in many areas of science because it shows how the true covariance matrix and its sample estimator are connected asymptotically. Knowing this we can build suitable estimators for high-dimensional quantities which depend on . In our case this refers to the shrinkage intensities. Note however, that the optimal shrinkage intensity depends again on the unknown characteristics of the asset returns. To overcome this problem we derive consistent estimators for specific functions (quadratic and bilinear forms) of the inverse sample covariance matrix and mean vector. Furthermore, we succeed to provide consistent estimators for the optimal shrinkage intensities too. Additional advantage of our approach is the simultaneous treatment of estimation risks of both the covariance matrix and the mean vector. In particular we contribute to the existent literature (see, Ledoit and Wolf, 2017a ) by weakening the assumption imposed on the mean vector of the asset returns.

It is worth mentioning that there are clear links between the subject of the paper and classical methods in statistical signal processing. The data generating process considered in the paper encompasses a broad range of system configurations described by the general vector channel model. Moreover, as for the aforementioned mean-variance portfolio optimization problem, usual linear filtering schemes solving typical signal waveform estimation and detection problems in signal array processing and wireless communications are based on the estimation of the unknown population covariance matrix. Famous example is the equivalence of the GMV portfolio to the so-called Capon or minimum variance distortionless response (MVDR) beamformer (see, Verdú, (1998); Van Trees, (2002)).

The rest of paper is organized as follows. In the next section, we construct a shrinkage estimator for the optimal portfolio weights obtained by shrinking the EU portfolio weights to an arbitrary target portfolio. The oracle shrinkage intensity and the corresponding feasible bona-fide estimators for and are established as well. The derived results are evaluated in Section 3 in extensive simulation and empirical studies. All proofs are moved to the Appendix presented in the supplementary material.

2 Optimal shrinkage estimator of mean-variance portfolio

Let be the data matrix which consists of vectors of the returns on assets. Let and for . We assume that as . This type of limiting behavior is known as ”the large dimensional asymptotics” or ”Kolmogorov asymptotics”. In this case the traditional sample estimators perform poorly or even very poorly and tend to over/underestimate the unknown parameters of the asset returns, e.g., the mean vector and the covariance matrix.

Throughout the paper it is assumed that there exists a random matrix which consists of independent and identically distributed (i.i.d.) real random variables with zero mean and unit variance such that

|

|

|

(2.1) |

It must be noted that the observation matrix has dependent rows but independent columns. Broadly speaking, this means that we allow arbitrary cross-sectional correlations of the asset returns but assume their independence over time. Although this assumption looks quite restrictive for financial applications, there exist stronger results from random matrix theory which show that the model can be extended to (weakly) dependent variables by demanding more complicated conditions on the elements of (see, Bai and Zhou, (2008)) or by controlling the number of dependent entries as dimension increases (see, Hui and Pan, (2010), Friesen et al., (2013), Wei et al., (2016)). Although our findings can still be used when weak serial dependence structure is present between the observation vectors, like in the case of uncorrelated GARCH (generalized autoregressive conditional heteroscedastic) processes or similar ones (see, e.g., the simulation study in Bodnar et al., 2021a ), we suspect substantial changes in the analytical expressions stated in the theorems for strongly correlated observation vectors, like in the case of VAR (vector autoregressive) processes. In such situations, the estimator will depend on the autocorrelation matrices of the underlying stochastic model and the theoretical results of the paper must be adjusted correspondingly. This interesting and important topic is not treated in the paper and is left for future research.

Nevertheless, if the entries of matrix are weakly dependent or so called -dependent, this will only make the proofs more technical, but leave the results unchanged. For that reason we assume independent in time asset returns only to simplify the proofs of the main theorems and make them as transparent as possible. The three assumptions which are used throughout the paper are the following:

-

(A1)

The covariance matrix of the asset returns is a nonrandom -dimensional positive definite matrix.

-

(A2)

The elements of the matrix have uniformly bounded moments for some .

-

(A3)

The efficient frontier is asymptotically a non-degenerate object, i.e. for its slope parameter it holds that uniformly in .

All of these regularity assumptions are general enough to fit many real world situations. The assumption (A1) together with (2.1) are usual for financial and statistical problems and they impose no strong restrictions. The assumption (A2) is a technical one. Although we demand the existence of moments of order a bit higher than four, this is solely due to the fact that the almost sure convergence is employed in the formulation of the theoretical results. In case of the convergence in probability the existence of exactly the fourth moment is sufficient. Indeed, it can be easily shown that this extra follows from the Borel-Cantelli lemma (see Rubio and Mestre, (2011)[Proof of Lemma 4]). The assumption (A3) has an important financial interpretation. It ensures that the efficient frontier is a parabola in the mean-variance space as defined in (1.5) and it does not degenerate into a line parallel to the variance axis (cf., Bodnar and Bodnar, (2010)). In the latter case, the only optimal portfolio is the GMV portfolio (1.4), a special case of the EU portfolio (1.2) with , and its shrinkage estimators have already been developed in Frahm and Memmel, (2010) and Bodnar et al., (2018). The assumption (A3) can be tested in practice by using Theorem 1 of Bodnar et al., 2021c .

The sample covariance matrix is given by

|

|

|

(2.2) |

where the symbol stands for the -dimensional identity matrix. The sample mean vector becomes

|

|

|

(2.3) |

2.1 Oracle estimator. Case

In this section we consider the optimal shrinkage estimator for the EU portfolio weights presented in the introduction by finding the shrinkage parameter and fixing some target portfolio .

The resulting estimator for is given by

|

|

|

(2.4) |

where the vector is the sample estimator of the EU portfolio given in (1.2), namely

|

|

|

(2.5) |

with

|

|

|

(2.6) |

The target portfolio is a given nonrandom (or random, but independent of ) vector with .No assumption is imposed on the shrinkage intensity which is the object of our interest.

The aim is now to find the optimal shrinkage intensity for a given nonrandom target portfolio . For that reason we introduce a unified mean-variance objective function in order to calibrate the shrinkage intensity . Consider the following optimization problem

|

|

|

(2.7) |

Obviously, the mean-variance objectives (1.1) and (2.7) coincide if . Other special values of which lead to widely used out-of-sample performance measures we summarize in the following proposition

Proposition 2.1 (Calibration criteria).

The optimization problem (2.7) is equivalent to

-

(i)

maximization of the mean-variance objective (1.1) if ,

-

(ii)

minimization of the out-of-sample variance if ,

The proof of Proposition 2.1 follows from the fact that all optimal mean-variance portfolios can be obtained by maximizing the expected quadratic utility function with a specific risk aversion coefficient. As a result, the global minimum variance portfolio is a partial solution of the optimization problem (1.1).

The presentation of the calibration criterion (2.7) provides an elegant way how to find the optimal shrinkage intensity in a unified manner for several popular out-of-sample loss functions and compare them just by changing the parameter .

In Section 2.3, we provide consistent estimates of these quantities under high-dimensional asymptotic regime for .

It is worth mentioning that the coefficient has an interesting interpretation from statistical point of view. While coefficient controls for investor attitude towards financial risk (”in-sample risk”), the parameter stays for controlling the estimation risk (”out-of-sample risk”). This implies that even the mean-variance investor with arbitrary could choose if she/he is interested, for example, in the minimization of the out-of-sample variance of the estimated portfolio.

The unified calibration criterion (2.7) can be rewritten as

|

|

|

|

|

|

(2.8) |

Next, taking the derivative of with respect to and setting it equal to zero we get

|

|

|

From the last equation it is easy to find the optimal shrinkage intensity given by

|

|

|

(2.9) |

To ensure that is the unique maximizer of (2.7) the second derivative of must be negative, which is always fulfilled. Indeed, it follows from the positive definitiveness of the matrix , namely

|

|

|

(2.10) |

In the next theorem we derive the asymptotic properties of the optimal shrinkage intensity under large-dimensional asymptotics.

Theorem 2.1.

Assume (A1)-(A3). Then it holds that

|

|

|

with

|

|

|

(2.11) |

where the parameters of the efficient frontier , and are given in (1.6) and (1.7),

respectively. The quantities and denote the expected return and the variance of the target portfolio .

Next, we assess the performance of the classical estimator of the portfolio weights and the optimal shrinkage weights . As a measure of performance we consider the relative increase in the utility of the portfolio return compared to the portfolio based on true parameters of asset returns. The results are summarized in the following corollary.

Corollary 2.1.

(a) Let and be the mean-variance objectives in (1.1) for the true EU portfolio and its traditional estimator. Then under the assumptions of Theorem 2.1, the relative loss of the traditional estimator of the EU portfolio is given by

|

|

|

(2.12) |

for as .

(b) Let be the expected quadratic utility for optimal shrinkage estimator of the EU portfolio. Under the assumptions of Theorem 2.1, the relative loss of the optimal shrinkage estimator is given by

|

|

|

(2.13) |

for as with is the relative loss in the expected utility of the target portfolio .

2.2 Oracle estimator. Case .

Here, similarly as in Bodnar et al., (2018), we will use the generalized inverse of the sample covariance matrix . Particularly, we use the following generalized inverse of the sample covariance matrix

|

|

|

(2.14) |

where denotes the Moore-Penrose inverse. It can be shown that is a generalized inverse of satisfying and . However, is not exactly equal to the Moore-Penrose inverse because it does not satisfy the conditions and . In case the generalized inverse coincides with the usual inverse . Moreover, if is a multiple of identity matrix, then is equal to the Moore-Penrose inverse . In this section, is used only to determine an oracle estimator for the weights of the EU portfolio. The bona fide estimator is constructed in the next section.

Thus, the oracle estimator for is given by

|

|

|

(2.15) |

where the vector is the sample estimator of the EU portfolio given in (1.2), namely

|

|

|

(2.16) |

with

|

|

|

(2.17) |

Again, the shrinkage intensity is the object of our interest. In order to save place we skip the optimization procedure for as it is only slightly different from the case . The optimal shrinkage intensity in case is given by

|

|

|

(2.18) |

In the next theorem we find the asymptotic equivalent quantity for in the case as .

Theorem 2.2.

Assume (A1)-(A3). Then it holds that

|

|

|

with

|

|

|

(2.19) |

where , , , , and are defined in Theorem 2.1.

Next, as for the case , we provide here the expression for the relative losses.

Corollary 2.2.

(a) Let and be the mean-variance objectives in (1.1) for the true EU portfolio and its traditional estimator. Then under the assumptions of Theorem 2.2, the relative loss of the traditional estimator of the EU portfolio is given by

|

|

|

(2.20) |

for as .

(b) Let be the expected quadratic utility for the optimal shrinkage estimator of the EU portfolio. Under the assumptions of Theorem 2.2, the relative loss of the optimal shrinkage estimator is given by

|

|

|

(2.21) |

for as with is the relative loss in the expected utility of the target portfolio .

2.3 Estimation of unknown parameters. Bona fide estimator

The limiting shrinkage intensities and are not feasible in practice, because they depend on , , , , and which are unknown quantities. In this subsection we derive consistent estimators for and . These results are summarized in two propositions dealing with the cases and , respectively. The statements follow directly from the proofs of Theorems 2.1 and 2.2 that are provided in the supplement of the paper.

Proposition 2.2.

The consistent estimator for the limiting optimal shrinkage intensity under large dimensional asymptotics is given by

|

|

|

(2.22) |

where , , , and are given by

|

|

|

|

|

(2.23) |

|

|

|

|

|

(2.24) |

|

|

|

|

|

(2.25) |

|

|

|

|

|

(2.26) |

|

|

|

|

|

(2.27) |

which are also ratio consistent estimators for , , , , and , respectively, while , and are traditional plug-in estimators.

Using Proposition 2.2 we can immediately construct a bona-fide estimator for the expected utility portfolio weights in case . It holds that

|

|

|

(2.28) |

with given in Proposition 2.2. The expression (2.28) is the optimal shrinkage estimator for a given target portfolio in the sense that the shrinkage intensity tends almost surely to its optimal value for as

The situation is more complex in case . Here we can present only oracle estimators for the unknown quantities , and .

Proposition 2.3.

The consistent estimator for the limiting optimal shrinkage intensity under large dimensional asymptotics is given by

|

|

|

(2.29) |

where , , are given by

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

where , and are the traditional plug-in estimators based on the generalized inverse from (2.14) and and are given in (2.26) and (2.27), respectively.

Note that from Proposition 2.3 is not the bona fide estimator for the unknown shrinkage intensity , since the matrix depends on the unknown quantities. Thus, we propose a reasonable approximation using the application of the Moore-Penrose inverse .

As a result, the bona fide estimators of the quantities , and in case are approximated by

|

|

|

(2.30) |

respectively. The application of (2.30) leads to the bona fide optimal shrinkage estimator of the EU portfolio in case expressed as

|

|

|

(2.31) |

with

|

|

|

(2.32) |

where and are given in (2.26) and (2.27), respectively; and is the Moore-Penrose pseudo-inverse of the sample covariance matrix .

5 Appendix: Proofs

Here the proofs of the theorems are given. Recall that the sample mean vector and

the sample covariance matrix are given by

|

|

|

(5.1) |

and

|

|

|

(5.2) |

respectively. Later on, we also make use of defined by

|

|

|

(5.3) |

and the formula for the 1-rank update of usual inverse given by (c.f., Horn and Johnsohn, (1985))

|

|

|

(5.4) |

as well as the formula for the 1-rank update of Moore-Penrose inverse (see, Meyer, (1973)) expressed as

|

|

|

|

|

(5.5) |

|

|

|

|

|

First, we present an important lemma which is a special case of Theorem 1 in Rubio and Mestre, (2011).

Lemma 5.1.

Assume (A2). Let a nonrandom -dimensional matrix and a nonrandom -dimensional matrix possess a uniformly bounded trace norms (sum of singular values). Then it holds that

|

|

|

(5.6) |

|

|

|

(5.7) |

for as , where

|

|

|

(5.8) |

with

|

|

|

(5.9) |

Proof of Lemma 5.1:.

The application of Theorem 1 in Rubio and Mestre, (2011) leads to (5.6) where is a unique solution in of the following equation

|

|

|

(5.10) |

The two solutions of (5.10) are given by

|

|

|

(5.11) |

In order to decide which of two solutions is feasible, we note that is the Stieltjes transform with a positive imaginary part. Thus, without loss of generality, we can take and get

|

|

|

(5.12) |

which is positive only if the sign is chosen. Hence, the solution is given by

|

|

|

(5.13) |

The second assertion of the lemma follows directly from Bai and Silverstein, (2010).

∎

We note here that Lemma 5.1 is a special case of Theorem 1 in Rubio and Mestre, (2011), where one has uniform convergence in the statement of the theorem. Although it is not precisely written in the statement of Theorem 1 in Rubio and Mestre, (2011), this observation follows from its proof on page 600 where after showing pointwise convergence Rubio and Mestre additionally proved the uniform convergence by applying Montel’s theorem. In short, they first show that the random sequence of analytic functions of interest forms a normal family and, thus, by Montel’s theorem there exists a subsequence of it, which converges uniformly on each compact subset of to an analytic function and this one vanishes almost surely on . And so, the entire sequence converges uniformly to zero on every compact subset of .

Furthermore, it is mentioned on page 348 of Rubio et al., (2012) that the convergence in Theorem 1 of Rubio and Mestre, (2011) is in fact uniform.

Moreover, the following result (see, e.g., Theorem 1 on page 176 in Ahlfors, (1953)), known as the Weierstrass theorem on the uniform convergence, will be used in a sequel together with Lemma 5.1 in the proofs of the technical lemmas.

Theorem 5.1 (Weierstrass).

Suppose that is analytic in the region , and that the sequence converges to a limit function in a region , uniformly on every compact subset of . Then is analytic in . Moreover, converges uniformly to on every compact subset of .

Because the convergence in Lemma 5.1 is uniform over on every compact subset of , the Weierstrass theorem allows us to interchange any derivative with respect to and the limit . We will consider compact subsets, which are the small neighbourhoods of zero with (without loss of generality) because all of the times we will let in order to get specific limiting expressions of interest. For example, one may take as a unit disk and as a disk for some as . The analyticity of the function follows immediately from the properties of the Stieltjes transform.

Lemma 5.2.

Assume (A2). Let and be universal nonrandom vectors with bounded Euclidean norms. Then it holds that

|

|

|

|

|

(5.14) |

|

|

|

|

|

(5.15) |

|

|

|

|

|

(5.16) |

|

|

|

|

|

(5.17) |

|

|

|

|

|

(5.18) |

|

|

|

|

|

(5.19) |

.

Proof of Lemma 5.2:.

Since the trace norm of is uniformly bounded, i.e.

|

|

|

we get from Lemma 5.1 that

|

|

|

Furthermore, the application of as leads to

|

|

|

which proves (5.14).

For deriving (5.15) we consider

|

|

|

|

|

|

|

|

|

|

where the last equality follows from the Woodbury formula (e.g., Horn and Johnsohn, (1985)). The application of Lemma 5.1 and Theorem 5.1 lead to

|

|

|

for as where is given by (5.8). Setting and taking into account we get

|

|

|

The result (5.16) was derived in Pan, (2014) (see, p. 673 of this reference).

Next, we prove (5.17). It holds that

|

|

|

|

|

where . From Lemma 5.1 tends a.s. to as . Furthermore,

|

|

|

(5.20) |

Consequently, using Lemma 5.1 and Theorem 5.1 we conclude

|

|

|

Let and . Then

|

|

|

where

|

|

|

|

|

|

|

|

|

|

. Hence, application of Lemma 5.1 and Theorem 5.1 reveals

|

|

|

.

Finally, we get

|

|

|

.

∎

Lemma 5.3.

Assume (A2). Let and be universal nonrandom vectors with bounded Euclidean norms. Then it holds that

|

|

|

|

|

(5.21) |

|

|

|

|

|

(5.22) |

|

|

|

|

|

(5.23) |

|

|

|

|

|

(5.24) |

|

|

|

|

|

(5.25) |

|

|

|

|

|

(5.26) |

.

Proof of Lemma 5.3:.

From (5.4) we obtain

|

|

|

|

|

following (5.14)-(5.16). Similarly, we get (5.22) and (5.23).

In case of (5.23), we get

|

|

|

|

|

|

|

|

|

|

. Similarly,

|

|

|

|

|

|

|

|

|

|

and

|

|

|

|

|

|

|

|

|

|

.

∎

Lemma 5.4.

Assume (A2). Let and be universal nonrandom vectors with bounded Euclidean norms and let where is a universal nonrandom vectors with bounded Euclidean norm. Then it holds that

|

|

|

|

|

(5.27) |

|

|

|

|

|

(5.28) |

|

|

|

|

|

(5.29) |

|

|

|

|

|

(5.30) |

|

|

|

|

|

(5.31) |

|

|

|

|

|

(5.32) |

.

Proof of Lemma 5.4:.

It holds that

|

|

|

|

|

following (5.21). Similarly, we get

|

|

|

|

|

and

|

|

|

|

|

.

The rest of the proof follows from the equality

|

|

|

and Lemma 5.3.

∎

Proof of Theorem 2.1:.

Let . We get that uniformly in , since and uniformly in by Assumption (A3).

The optimal shrinkage intensity can be rewritten in the following way

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

where

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

and

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

In the formulas for and the factors and are bounded by one. Moreover, since for any with , we also get .

The Euclidean norms of the following vectors

|

|

|

are all equal to one. As a result, using and and applying Lemma 5.3 we get

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

.

Furthermore, from Lemma 5.3 and 5.4 using the equalities

|

|

|

with we obtain with

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

.

Substituting the above results into the expressions of and , we get that

|

|

|

with

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

and

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

Let . Then,

|

|

|

Using the notations , , , and making some technical manipulations we get the statement of Theorem 2.1.

∎

Proof of Corollary 2.1:.

(a)

We first compute with given by

|

|

|

|

|

where

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

and

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

.

Finally, the equality

|

|

|

implies the statement of the first part of the corollary.

(b) It holds that

|

|

|

|

|

|

|

|

|

|

where the asymptotic values of and are fund in part (a) and

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

.

Hence,

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

.

∎

For the proof of Theorem 2.2 we need several results about the properties of Moore-Penrose inverse which are summarized in the following three lemmas. Similarly as the proof of Lemma 5.2, we will use Lemma 5.1 and Theorem 5.1 in a sequel every time a derivative must be interchanged with the limit .

Lemma 5.5.

Assume (A2). Let and be universal nonrandom vectors with bounded Euclidean norms. Then it holds that

|

|

|

|

|

(5.34) |

|

|

|

|

|

(5.35) |

|

|

|

|

|

(5.36) |

|

|

|

|

|

(5.37) |

|

|

|

|

|

(5.38) |

|

|

|

|

|

(5.39) |

|

|

|

|

|

(5.40) |

|

|

|

|

|

(5.41) |

|

|

|

|

|

(5.42) |

.

Proof of Lemma 5.5:.

It holds that

|

|

|

and, similarly,

|

|

|

Let . It holds that

|

|

|

|

|

|

|

|

|

|

The application of Woodbury formula (matrix inversion lemma, see, e.g., Horn and Johnsohn, (1985)),

|

|

|

(5.43) |

leads to

|

|

|

|

|

|

|

|

|

|

From the proof of Lemma 5.2 we know that the matrix possesses the bounded trace norm. Then the application of Lemma 5.1 leads to

|

|

|

|

|

|

|

|

|

|

for as , where is given in (5.9).

Let us make the following notations

|

|

|

Then the first and the second derivatives of are given by

|

|

|

(5.44) |

Using L’Hopital’s rule, we get

|

|

|

(5.45) |

|

|

|

(5.46) |

and

|

|

|

|

|

(5.47) |

|

|

|

|

|

which implies

|

|

|

(5.48) |

Combining (5.44), (5.45), (5.46), and (5.48), we get

|

|

|

and

|

|

|

Hence,

|

|

|

|

|

|

|

|

|

|

Taking into account that

|

|

|

we get (5.36). Similarly, using

|

|

|

|

|

we get

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

for as , where .

Using that the elements of are independent and identically distributed and the fact that from Lemma 5.1 and Theorem 5.1 we get that

|

|

|

Thus,

|

|

|

which proves (5.37). Furthermore, we get

|

|

|

with

|

|

|

and, consequently,

|

|

|

In order to prove (5.39), we compute

|

|

|

where

|

|

|

Hence,

|

|

|

For (5.40) we consider

|

|

|

|

|

Because of (5.16), it holds that is uniformly bounded as . Moreover, as following Kolmogorov’s strong law of large numbers (c.f., Sen and Singer (1993, Theorem 2.3.10), since has a bounded Euclidean norm. Hence, .

Finally, in the case of (5.41) and (5.42), we get

|

|

|

|

|

|

|

|

|

|

.

∎

Lemma 5.6.

Assume (A2). Let and be universal nonrandom vectors with bounded Euclidean norms. Then it holds that

|

|

|

|

|

(5.49) |

|

|

|

|

|

(5.50) |

|

|

|

|

|

(5.51) |

|

|

|

|

|

(5.52) |

|

|

|

|

|

(5.53) |

|

|

|

|

|

(5.54) |

.

Proof of Lemma 5.6:.

From (5.5) we get

|

|

|

|

|

|

|

|

|

|

following (5.34)-(5.36). Similarly, we get

|

|

|

|

|

|

|

|

|

|

and

|

|

|

|

|

|

|

|

|

|

.

Now, we consider the equality

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

Hence,

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

and

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

.

∎

Lemma 5.7.

Assume (A2). Let and be universal nonrandom vectors with bounded Euclidean norms and let where is a universal nonrandom vectors with bounded Euclidean norm. Then it holds that

|

|

|

|

|

(5.55) |

|

|

|

|

|

(5.56) |

|

|

|

|

|

(5.57) |

|

|

|

|

|

(5.58) |

|

|

|

|

|

(5.59) |

|

|

|

|

|

(5.60) |

.

Proof of Lemma 5.7:.

It holds that

|

|

|

|

|

following (5.34). Similarly, we get

|

|

|

|

|

and

|

|

|

|

|

.

The rest of the proof follows from the equality

|

|

|

and Lemma 5.6.

∎

Proof of Theorem 2.2:.

Let . From Assumption (A3) get that uniformly in , since and uniformly in .

In case of , the optimal shrinkage intensity is given by

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

where

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

and

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

Using the equalities

|

|

|

the facts that , , and that the Euclidean norms of the following vectors

|

|

|

are equal to one, the application of Lemma 5.6 yields

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

.

Finally, from Lemma 5.6 and 5.7 as well as by using the equalities

|

|

|

with we obtain

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

.

Substituting the above results into the expressions of and , we get that

|

|

|

with

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

and

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

Let . Hence,

|

|

|

This completes the proof of Theorem 2.2.

∎

Proof of Corollary 2.2:.

(a)

With we get

|

|

|

|

|

where from the proof of Theorem 2.2 we have

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

and

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

.

Finally, using that

|

|

|

we obtain the statement of the first part of the corollary.

(b) It holds that

|

|

|

|

|

|

|

|

|

|

where

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

.

Hence,

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

.

∎