Optimal Drift Rate Control and Impulse Control for a Stochastic Inventory/Production System

Abstract

In this paper, we consider joint drift rate control and impulse control for a stochastic inventory system under long-run average cost criterion. Assuming the inventory level must be nonnegative, we prove that a policy is an optimal joint control policy, where the impulse control follows the control band policy , that brings the inventory level up to once it drops to and brings it down to once it rises to , and the drift rate only depends on the current inventory level and is given by function for the inventory level . The optimality of the policy is proven by using a lower bound approach, in which a critical step is to prove the existence and uniqueness of optimal policy parameters. To prove the existence and uniqueness, we develop a novel analytical method to solve a free boundary problem consisting of an ordinary differential equation (ODE) and several free boundary conditions. Furthermore, we find that the optimal drift rate is firstly increasing and then decreasing as increases from to with a turnover point between and .

Keywords: drift rate control; impulse control; Brownian motion; inventory control

2010 Mathematics Subject Classification: 90B05, 93E20, 60J70,49N25, 49K15

1 Introduction

In this paper, we study a continuous-review stochastic inventory/production system, in which supply/production rate and inventory level can be adjusted. The netput inventory level process, capturing the difference of regular supply/production process and the demand process, has the following representation

| (1.1) |

where is the initial inventory level, is the drift rate at time and is a decision variable, is the variance, and is a standard one-dimensional Brownian motion with . The system manager can modify the drift rate at any time, and can also increase and decrease the inventory level at any time by any amount desired. Let denote the drift rate control process, and let be a pair of impulse controls with , , where () represents the th time to increase (decrease) the inventory level and () denotes the corresponding increment (decrement). Then, the controlled inventory level is given by

| (1.2) |

where denotes the number of adjustments of up to time . Moreover, the inventory level must be nonnegative at all times. There are three types of costs: the holding cost and drift rate cost are continuously incurred and depend on current inventory level and drift rate respectively, and the impulse control cost is incurred when the inventory is increased/decreased and depends on the increment/decrement. The objective is to find a control policy to minimize the average expected total costs over an infinite planning horizon.

The joint drift rate control and impulse control model described above has many applications of practical interest. The following are two examples.

-

(i)

Joint pricing and inventory control problems. For example, let denote the demand rate at time and depend on the current product price , i.e.,

and let denote the demand variance. Thus, the cumulative demand up to time is given by . In such problems, the manager controls the drift rate by adjusting the offered price, while he controls the inventory level by ordering and returning products. The joint pricing and inventory control problems with Brownian motion demand have been studied in the literature, e.g., [9, 30, 31]. However, only upward impulse control (i.e., ordering) is allowed in these works.

-

(ii)

Production-inventory problems. For example, let denote the cumulative customer demand up to time . The system produces products at rate for time . Besides this standard production, it also can place an expedited order to an outside supplier when the inventory level becomes too low and can return some products when the level becomes too high. In this kind of production-inventory problem, the drift rate in (1.2) becomes

Production-inventory problems also have been considered in the literature; see e.g., [8, 29] for dual production rate models.

Because of their importance in practice, both drift rate control and impulse control have been widely studied in the literature. Next, we first briefly review the literature on drift rate control, then review the literature on two-sided impulse control. Finally, we introduce the our work with joint drift rate control and impulse control. See Table 2 for the classification of the related literature.

| Impulse control | ||||

| None | One-sided | Two-sided | ||

| Drift rate control | None | NA | — | [11, 12, 13, 14, 19, 22, 26] |

| Two modes | [4, 15, 25, 29] | — | None | |

| Finite modes | [10, 23, 24, 28] | — | None | |

| Any value | [2, 18] | [9, 30, 31] | our paper | |

In the literature on drift rate control, two-mode models with positive switching costs have been widely studied; see e.g., [4, 15, 25, 29]. These four papers prove the optimality of an policy under different cost criteria. Under an policy, the system uses the lower drift rate mode once the system’s state reaches or exceeds , uses the higher drift rate mode once the system’s state drops to or below , and keeps the drift rate mode unchanged otherwise. Furthermore, finite drift rate modes (i.e., more than two modes) are considered in [10, 23, 24, 28], where simple Brownian motion models are considered in [10, 23, 24] while a general diffusion process model is studied in [28]. Note that all the works introduced above only consider the drift rate control in their models. Recently, models in which the drift rate can take any value have been studied in [2, 18]; Ghosh and Weerasinghe [18] study a joint drift rate control and singular control problem and explicitly solve it under a quadratic control cost structure.

Two-sided impulse control problems with constant drift rate also have been widely studied in the literature: Long-run average cost models are studied in [11, 13, 22] and discounted cost models are studied in [12, 14, 19, 26]. These works all prove the optimality of a control band policy , under which the state is immediately increased to level once it drops to and is decreased to level once it goes up to . The method for proving the existence of optimal policy parameters in these works is to obtain an explicit solution for a relative optimality equation represented by an ODE, and then to find parameters to satisfy some free boundary conditions derived from the optimal impulse control. However, this method cannot work for our problem, since it is difficult to obtain the explicit solution of the corresponding ODE due to the changeable drift rate. To overcome this difficulty, we prove the existence of an optimal control policy by analyzing the ODE with the associated free boundary conditions directly.

There are also some papers considering joint drift rate control and impulse control, all of which focus on the application to joint pricing and inventory control problems ([9, 30, 31]). There are two important differences between those papers and this one. First, their models only allow increasing inventory in the impulse control, while we allow both increasing and decreasing inventory. Second and more important, Chen et al. [9] and Zhang and Zhang [31] prove the existence of optimal parameters only when the price is constant in a certain inventory interval and when has a specific form, respectively. Although Yao [30] considers a general drift rate function like ours, he assumes the existence of optimal policy parameters for the optimality equation. We, however, completely prove the existence of optimal policy parameters by solving a free boundary problem, which is the main technical contribution in this paper.

This paper’s contribution can be summarized as follows. First, to the best of the authors’ knowledge, this is the first study of a stochastic inventory problem with joint drift rate control and two-sided impulse control. Further, the optimal control policy is completely characterized. Second, a novel method is provided to prove the existence and uniqueness of optimal policy parameters by solving a free boundary problem. This is the major technical contribution of this paper. Indeed, proving the existence of optimal policy parameters for Brownian control problems is usually important and difficult, and has been the major technical contribution of many publications; see e.g., [5, 6, 13, 14, 16]. However, in contrast with these works, this paper develops a very different method that does not require an explicit solution for the optimality equation. This methodology provides a more general roadmap to solve similar problems, especially when the explicit expression of the solution is unavailable or too complicated. Third, unlike the simple monotonic optimal drift rate studied in the literature (see e.g., [2, 18]), we find that the optimal drift rate function as a function of inventory level , is first increasing and then decreasing as the inventory level increases in .

The rest of this paper is organized as follows. In §2, we introduce the mathematical formulation of the joint drift rate control and impulse control problem in §2.1, and state our main results in §2.2. In §3, a policy is provided by proving the existence of its parameters, and §4 proves the optimality of proposed policy. Finally, the paper concludes in §5. We close this section with some frequently used notation. Let , , and be the space of continuous functions on that have continuous first derivatives. Let be a real-valued function defined on , and use to denote the left limit at time point .

2 Formulation and main results

2.1 Model formulation

Let be a filtered probability space and Brownian motion is adapted with respect to the filtration .

Consider an inventory system with a netput inventory level process given by (1.1). There are two controls for this system: a drift rate control and a two-sided impulse control with , . These two controls together form a policy . A joint drift rate control and impulse control policy is admissible if: i) is -measurable and must be in a compact set with the smallest element and the largest element ; and ii) is a stopping time and is -measurable. We note that might be a discrete point set or an interval and and are both finite. Let denote the set of all admissible policies. Under an admissible policy , the controlled inventory level process must be nonnegative and is given by (1.2).

We next introduce three costs in our system. The holding cost is continuously charged at rate when the inventory level is and the drift rate control cost is continuously charged at rate when the rate is . Furthermore, the impulse control cost is measured by the amount of adjustment, and cost is incurred when quantity is increased while cost is incurred when quantity is decreased, where , , , and are all strictly positive. Therefore, under an admissible policy , the system’s long-run average cost is

where is the initial inventory level and denotes the expectation with respect to the initial inventory level . Our objective is to find an admissible policy such that for any ,

| (2.1) |

To this end, we use the following assumptions about the holding cost function .

Assumption 1.

is strictly increasing and continuous in with and . Moreover, .

The assumptions for the function are quite standard and are satisfied in most applications of practical interest; see e.g., a linear cost function in [19, 22] and a convex function in [13]. Our assumptions are used to ensure the existence and uniqueness of optimal policy parameters, i.e., Theorem 2.1 and Corollary 1; see e.g., the proof of Lemma 3.2-3.4. It is worth noting that the “strictly increasing” may be relaxed to “weakly increasing” without jeopardizing the existence but losing the uniqueness of optimal policy parameters. Of course, this relaxation would require a tedious analysis. Also, the condition can be relaxed to for some without jeopardizing the main results.

Notice that no condition is imposed on the drift rate function . In this paper, we will see that the function is used only in Lemma 3.1 and the proof of Lemma 3.6 (b), which require no conditions on since the allowable drift rate set is assumed to be a compact set. However, if is no longer a compact set, e.g., , then we should impose some regular conditions on such as differentiability, convexity, , and , to guarantee the correctness of the main results. Moreover, our analysis relies on the finiteness of and . If either of them is infinite, some analysis must be changed accordingly and a more lengthy analysis is required.

Remark 2.1.

Notice that in our model, we assume that the drift rate can be controlled but the variance is a constant. There are two reasons for this assumption: First, because of the technical difficulties for the continuous adjustment when the variance is affected by the control, it is a common assumption in the literature; see e.g., [2, 4, 18, 23, 24]. Second, this assumption is reasonable for many situations in practice. For example, the uncertainty in demand of branded products (e.g., Intel processors) that exhibit substantial customer demand is mainly due to a random error that is independent of the decision variable ([21]).

2.2 Main results

In this subsection, the main results are presented. In Theorem 2.1, we determine a policy by solving an ODE with some boundary conditions. Then, in Theorem 2.2, we show that this policy is optimal for the joint drift rate control and impulse control problem (2.1).

For a policy, with denotes a two-sided impulse control policy and denotes a drift rate control policy. Under an impulse control policy , the inventory level is increased up to level instantaneously once it drops to level 0 and is decreased down to instantaneously once it rises to level . Thus, can be specified as

Since the initial inventory level may be higher than , a return with amount may happen at time 0. Therefore, can be specified as

The impulse control policy is called a control band policy in the literature (see e.g., [19, 22]). Note that under control band policy , the controlled inventory level is limited to for all . Under a drift rate control policy , the drift rate would be when the inventory level is at any time .

In developing the following theorem, we will determine a policy. To present the theorem, we first define some functions as follows. Let be a real-valued function on , and define

| (2.2) |

where we choose to be the smallest one if there are multiple minimizers.

Theorem 2.1.

Assume that satisfies Assumption 1.

-

There exist four parameters , , and with and , and a continuously differentiable function satisfying

(2.3) with boundary conditions

(2.4) (2.5) (2.6) (2.7) -

Define . Then is an admissible policy. Furthermore, there exists a number with such that is decreasing in and increasing in .

In this paper, (2.4)-(2.7) are called free boundary conditions since the boundary points , , and need to be determined, and problem (2.3) with conditions (2.4)-(2.7) is also called free boundary problem; see a similar definition in [13]. The optimality of the selected policy is shown in the following theorem.

Theorem 2.2.

Theorem 2.2 has shown that is the optimal cost and thus it is unique in Theorem 2.1. This in turn implies the uniqueness of optimal policy parameters , , and and the function in Theorem 2.1.

Corollary 1.

The optimal impulse control parameters , , and and the function in Theorem 2.1 are unique.

Finally, we give a heuristic derivation of the ODE (2.3) and free boundary conditions (2.4)-(2.7) that the optimal parameters should satisfy. For a given policy , let be the difference of the expected cumulative cost from state to state and the cost , where denotes the average cost under policy and is the first time when the inventory level hits starting from . In the literature, is also called the relative value function; see e.g., [22]. Let

First, the definition of implies that should satisfy and , which yield (2.4) and (2.5). Next, we show that should satisfy (2.3), (2.6), and (2.7) if is optimal. If is optimal, by the principle of optimality, for and a small time interval with length , should satisfy

with for . It follows from a standard argument for the dynamic programming equation (see e.g., [17]) that satisfies

which implies (2.3). Furthermore, starting from state , if it is optimal to jump state , then should be chosen by minimizing . The first-order optimality condition would be , which is the first equality in (2.7). Besides this, for , under the policy , we must have . By the principle of smoothness under the optimal policy, the left and right derivatives of at should be equal, i.e., ; that is the second equality in (2.7). Finally, a similar analysis gives us (2.6).

3 Existence of optimal policy parameters

In this section, we prove Theorem 2.1, which shows the existence of a policy (which by Theorem 2.2 is optimal) with parameters satisfying (2.3)-(2.7). Specifically, we prove Theorem 2.1 in two subsections. In §3.1, we solve the ODE (2.3) with given and a boundary condition , and provide the structural properties of with respect to , , and ; see Lemmas 3.2-3.4. Then, in §3.2, we determine by the five boundary conditions (2.4)-(2.7); see Lemmas 3.5-3.7. Note that Lemmas 3.2-3.7 are under Assumption 1, although for brevity we will not state this for each.

Before proving Theorem 2.1, recalling the definitions of and in (2.2), we first give the following lemma, the proof of which can be found in Appendix A.

Lemma 3.1.

is concave and Lipschitz continuous in , i.e., for any and , we have

| (3.1) |

where . Furthermore, is decreasing in .

3.1 Solving the ODE (2.3)

In this subsection, we will solve the ODE (2.3) for by assigning an initial value and fixing , which then allows us to characterize the structural and asymptotical properties of the solution .

Consider the following problem:

| (3.2) | |||

We denote the solution of the above problem by if it exists. For this problem, we first have the following lemma, which states the existence, uniqueness, and continuity of .

Lemma 3.2.

-

For any and , problem (3.2) has a unique continuously differentiable solution .

-

is continuous in and , and is continuous in , , and respectively.

Proof.

() Since is Lipschitz continuous (see Lemma 3.1) and is continuous (see Assumption 1), using an analog to the proof for Proposition 3 (i) in [3], we can use Picard’s existence theorem (see, e.g., Theorem 10 of §1.7 in [1]) to show that there exists a unique continuous solution to (3.2) on the interval .

It follows from (3.1) (by letting and ) and (3.2) that

| (3.3) | |||

| (3.4) |

which will be used in the following discussions.

The following lemma characterizes the monotonicity and asymptotical behaviors of with respect to and .

Lemma 3.3.

The following results hold:

-

For fixed and , is strictly increasing in and

(3.5) -

For fixed and , is strictly increasing in and

Proof.

() First, if , we show that for any fixed and . Fix . Suppose that for some . Define

The following proof is divided into two cases: or .

If , then it follows from the continuity of , , that and for all . By the continuity of , there exist two numbers with such that

| (3.6) |

where (see Lemma 3.1). Moreover, it follows from (3.2) that

| (3.7) |

Integrating (3.7) from to , we have

where the first and last inequalities follow from (3.6) and the second inequality follows from (3.1). This is a contradiction.

If , then there exists a sequence such that as and . Therefore,

Since , taking the limit as gives , which contradicts (3.7) with . Therefore, the contradictions for both and imply that is strictly increasing in for any given and .

Next, we prove that for any given and . Fix . There must exist a number such that for all , both

| (3.8) |

and

| (3.9) |

hold. We claim that for any fixed , it holds that

| (3.10) |

First, we show that for each , there exists a number (depending on and ) such that . If not, there exists a number with such that for all , and then (3.3) implies that for all ,

which implies that for all ,

where and the last inequality follows from (3.9), , and . This contradiction implies that for any given , there exists a number such that . It follows from (3.2) and (3.8) that for any and , if , we have . Thus, the continuity of and imply (3.10). Hence, (3.3) implies that for all and ,

and thus

for all . Letting in the inequality above yields .

Similar to the proof of , except that (3.4) is used instead of (3.3), one can show that . The detailed proof is omitted for brevity.

() Choose any two numbers and satisfying . We want to show that for all and . Fix . Obviously, the condition holds for . Suppose that for some . Define

Since , it follows from the continuity of and that , and for all . By the continuity of , there exists a number such that

| (3.11) |

Moreover, it follows from (3.2) that

| (3.12) |

Integrating (3.12) from to , we have

where the first inequality follows from and (3.1), and the last two inequalities follow from (3.11). This contradiction implies that is strictly increasing in for all and .

Finally, the proof of is quite similar to that of and is omitted for brevity. ∎

The following lemma characterizes the monotonic properties of with respect to when takes different values.

Lemma 3.4.

Fix . There exists an upper bound (possibly infinite) with such that the following holds.

-

If , then is strictly decreasing in and

(3.13) -

If , then is strictly increasing in and

(3.14) -

If , then there exists a unique number such that is strictly increasing in and strictly decreasing in . Furthermore, .

Remark 3.1.

For convenience, in the following sections, we let if and if .

Proof.

Before proving (a)-(c), we first claim the following property: There do not exist two numbers and with such that

| (3.15) |

This is because: it follows from (3.2) with and that

which is impossible considering (3.15) and (using Assumption 1). Therefore, we have

-

(i)

can-not have a local minimizer in ; and

-

(ii)

can-not be a constant in any interval with .

Next we use properties (i)-(ii) to prove (a)-(c). First, taking in (3.2) and noting , we have

| (3.16) |

() The proof of monotonicity is divided into two cases: or .

If , (3.16) implies that . The continuity of with respect to and properties (i)-(ii) immediately imply that is strictly decreasing in for .

If , using the results when and the continuity of in , we must have for , and property (ii) further implies that is strictly decreasing in for .

Next we show that . Otherwise, there exists a finite number such that and thus . Taking in (3.2) yields that , which contradicts with Assumption 1.

() Define

| (3.17) |

Part (a) implies that and thus is well defined although it might be . If , then by the definition of in (3.17) and the continuity of in , we have that for all . Then property (ii) implies that is strictly increasing in .

The proof of is similar to that of (3.13) and thus is omitted.

() First, we must have

Otherwise, there is a contradiction between part (a) and (b) when . Now, we consider the case when . First, we claim that for each , there exists a number such that . If no such exists, we have that for all . Using arguments similar to those used to prove (3.13) in part (a), we can obtain

| (3.18) |

On the other hand, using the definition of and the continuity of in , there exists a number such that for some . Then, we must have that is strictly decreasing for and

| (3.19) |

(the analysis is very similar to that of part (a) and thus is omitted). However, (3.18) and (3.19) contradict Lemma 3.3 with . Thus, we have proven that for each , there exists a number such that . Define

Since and is continuous in , we have , for and . Further, the properties (i)-(ii) imply that is strictly increasing in and strictly decreasing in .

Finally, the proof of is very similar to that of (3.13) and thus is omitted. ∎

3.2 Determining optimal parameters by (2.4)-(2.7)

In the previous section, we obtained structural and asymptotical properties of solution to (2.3). In this subsection, we use these properties to find the optimal policy parameters and auxiliary parameters such that the boundary conditions (2.4)-(2.7) are satisfied.

Specifically, in Lemma 3.5, we show that for any , there exist unique , , and with and such that

| (3.20) | |||

| (3.21) |

In Lemma 3.6, we prove that for any , there exist unique and with and such that

| (3.22) |

where is a number satisfying . Finally, in Lemma 3.7, we show that we can choose a number with such that

| (3.23) |

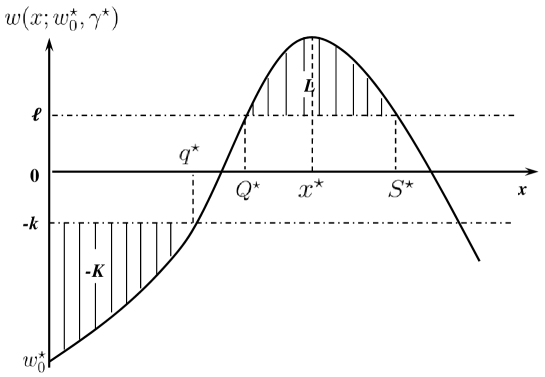

Let , , , , , and . Figure 1 depicts the function and the optimal policy parameters. Using Lemmas 3.5-3.7, we can prove Theorem 2.1 as follows.

Proof of Theorem 2.1.

Recall that is a continuously differentiable solution to (2.3), so (3.20)-(3.22) with (3.23) ensure (2.4)-(2.7). Besides, since , Lemma 3.4 (c) and imply , and then . Thus we have finished the proof of Theorem 2.1 (a). Furthermore, the facts that is decreasing (see Lemma 3.1) and is increasing in and decreasing in imply that is decreasing in and increasing in . This completes the proof of Theorem 2.1 (b). ∎

Remark 3.2.

It can be seen from the proof of Theorem 2.1 that if we can prove the uniqueness of in (3.23), then the uniqueness of parameters , , and can be immediately obtained. However, it is very difficult to prove the uniqueness of in (3.23) directly. Instead, we will first show the uniqueness of using Theorem 2.2, then the uniqueness of follows by noting that and that is strictly decreasing in . See the proof of Corollary 1.

Now, it remains to prove (3.20)-(3.23) by the following Lemmas 3.5-3.7. Recalling the definition of in Lemma 3.4, we first have the following lemma.

Lemma 3.5.

-

For any , there exists a finite number with such that for any , there exist two unique numbers and with satisfying

-

For any , there exists a unique finite number with such that

(3.24) where is strictly increasing in . Furthermore, is continuous and strictly decreasing in .

Proof.

(a) For any , define

It follows from Lemma 3.4 (c) and Remark 3.1 that

| (3.25) |

which, together with Lemma 3.3 (a) and (b), implies that is strictly increasing in both and . Furthermore, Lemma 3.4 implies that

Hence, is well defined, finite, and strictly decreasing in . Using the continuity of in , (3.25), the definition of , and the monotonicity of in , we also have

For , define

Then, it follows from Lemma 3.4 (c) and that both and are well defined, finite, and unique, and so and .

(b) Note that . Hence, Lemma 3.3 (a), Lemma 3.4, and the definitions of and imply that

and is strictly increasing in . Thus, we have

which, together with the continuity of in (the continuity of can be implied by the continuity of ), imply that there exists a unique such that .

It remains to prove that is continuous and strictly decreasing in . First, it follows from Lemma 3.3 (b) and the definition of that is strictly increasing in when . Also, is strictly increasing in . Hence, is strictly decreasing in as can be seen by noting that . Finally, the continuity of follows from the monotonicity of in , the continuity of in , and the Implicit Function Theorem (see e.g., Theorem 1.1 in [27]). ∎

Lemma 3.6.

-

For any , there exists a unique number with such that

(3.26) and for any , there exists a unique number with such that

-

There exists a number such that

(3.27) and for any , there exists a unique number satisfying and

(3.28) where . Furthermore, is continuous and strictly decreasing in , and

(3.29)

Proof.

() For any , define

| (3.30) |

Recall the fact that is strictly increasing in , tends to as goes to (from the argument after (3.25)), and tends to as goes to (see Lemma 3.4). Then, is well defined and unique, and satisfies (3.26). Moreover, . For , define

| (3.31) |

Since for and for (see Remark 3.1), we have that is well defined and unique, and satisfies .

() We first prove (3.27). Recall . If we can show that is strictly increasing in ,

| (3.32) |

then, by defining as

the continuity of implies that (3.27) holds. (the proof of the continuity of is similar to that for , and thus is omitted.) The proofs that is strictly increasing in and that (3.32) holds are in Appendix B.

We next prove that for any , there exists a unique number with such that (3.28) holds. First since is strictly increasing in , we have that for ,

| (3.33) |

Furthermore, (3.5) and the definition of in (3.31) imply that and then

which, together with (3.33) and the continuity of in , implies that there exists a unique with such that (3.28) holds.

We now prove that is continuous and strictly decreasing in . Similar to the proof used for , the continuity can be obtained by the Implicit Function Theorem and is omitted. If we can prove that is strictly increasing in and respectively, then implies that is strictly decreasing in . We next only prove that is strictly increasing in , and the proof for the monotonicity in is very similar and is omitted. Since is strictly increasing in (see Lemma 3.3 (a)) and is strictly increasing in (see Lemma 3.4 (b) and (c)), implies that is strictly decreasing in . Therefore, for any and satisfying , we have

where the first inequality follows from the fact that is strictly decreasing in and for , and the second inequality follows from being strictly increasing in (Lemma 3.3 (a)) and . Hence, is strictly increasing in .

We now prove (3.29). Suppose that it fails to hold. In that case, the fact that is strictly decreasing in implies that there exists a finite number such that

Since for , by the definition of , we have

where . It follows from (3.2) that for ,

which yields that for ,

| (3.34) |

where . Thus, letting and in (3.34) and using and , we have that for all ,

| (3.35) |

Define . Then for all ,

| (3.36) |

where the last inequality follows from (3.35). Let

and then (3.36) and imply that for all ,

| (3.37) |

Therefore,

where the first inequality follows from (3.37) and for , the second inequality follows from (3.34), and the last inequality follows from . Then, it follows from for all that

which contradicts . Thus, we have proven (3.29) and finished the proof. ∎

Lemma 3.7.

There exists a number with such that (3.23) holds.

Proof.

We use two steps to prove this lemma. First, we show that

| (3.38) |

Second, we prove that there exists a number such that

| (3.39) |

Thus, (3.38), (3.39), and the continuity of and imply that there exists a number such that (3.23) holds. We next prove (3.38) and (3.39).

First, we prove (3.38). It follows from (3.26) and that

| (3.40) |

which implies that is finite and thus . Thus, we have

| (3.41) |

where the second equality follows from Lemma 3.4 (c) and (3.40), the last equality follows from (3.24) and . Recall that is strictly increasing in in Lemma 3.5, and thus (3.41) yields (3.38).

Next we prove (3.39). Suppose that it fails to hold, i.e., for all , we have . Since is strictly increasing in , we have that for any ,

| (3.42) |

If we can show that for any fixed ,

| (3.43) |

then, for any fixed pair with , we have that

where the first inequality follows from for all , the second inequality follows from the properties of in for all cases in Lemma 3.4, and the last equality follows from (3.43). This contradicts (3.42), and so we get (3.39).

It remains to prove (3.43). Fix . First, (3.29) implies that there exists a number with such that for all and ,

| (3.44) |

Choose any fixed and with . Define

| (3.45) | ||||

Note that it follows from (3.29) that as . Hence, there exists a number with , such that for all with , we have .

Next we show that for each with , there exists a number with (here might depend on ) such that

| (3.46) |

Suppose that this does not hold. Then, there exists a number with such that for all . Then, (3.3) implies that for all ,

| (3.47) |

We consider two cases: or .

4 Optimality of the proposed policy

In this section, we prove Theorem 2.2 using the lower bound approach. First, in §4.1 we provide a lower bound for the cost under any admissible policy. Then, in §4.2 we show the cost under the proposed policy determined in §3 can achieve the lower bound and thus the proposed policy is an optimal one.

4.1 Lower bound

We give a lower bound for the cost under any admissible policy by using Itô’s formula as follows.

Proposition 4.1.

Suppose that there exists a constant and a function with absolutely continuous and bounded derivative and continuous second derivative at all but a finite number of points, satisfying

| (4.1) |

with

| (4.2) | |||

| (4.3) |

Moreover, suppose that is bounded below, i.e., there exists a finite number such that

| (4.4) |

Then for any admissible policy and initial state .

4.2 Optimality of proposed policy

In this subsection, Proposition 4.2 characterizes the cost under any policy , and then Theorem 2.2 is proved by showing that the cost under the proposed policy can achieve the lower bound in Proposition 4.1. Finally, Corollary 1 is proven.

Proposition 4.2.

Consider a policy with . Suppose that there exists a constant and a twice continuously differentiable function: satisfying

| (4.7) |

with boundary conditions

| (4.8) | |||

| (4.9) |

Then, the average cost for any initial state .

Proof.

If the initial state , there will be a one-time control to bring it to and thus the state will stay in forever under the policy . The one-time finite control cost can be ignored in the long-run average cost, thus it suffices to consider the case that the initial state .

Since is twice continuously differentiable on , it has a bounded derivative on . Furthermore, it follows from (4.8) and (4.9) that under policy , and . Since for all under policy , it follows from (4.5) and (4.7) that

| (4.10) | ||||

Note that , which implies

Dividing both sides of (4.10) by and letting , we have . ∎

We are now ready to prove Theorem 2.2. Recalling the solution to (2.3)-(2.7) in Theorem 2.1, i.e., , we define

Proof of Theorem 2.2.

Since satisfies (2.3)-(2.5) in Theorem 2.1, letting in Proposition 4.2, we have that is the average cost under . If we can prove that and satisfy the conditions in Proposition 4.1, then for any admissible policy and any initial state , and thus is the optimal average cost and is an optimal policy.

It remains to check the conditions in Proposition 4.1. First, it follows from (2.7) and the definition of that has an absolutely continuous and bounded derivative . Moreover, it follows from (2.3) that also has a continuous second derivative at all points in except maybe . Moreover, it follows from the definition of and that for all . Hence, (4.4) holds.

Next, we check (4.1). It follows from (2.3) and the definition of that (4.1) holds for . For , we have

where the first equality follows from and , the first inequality follows from Assumption 1 and , the second inequality follows from (2.7) and the fact that is strictly decreasing in at , and the second equality follows from (2.3) with .

We next check (4.2). For , the proof is divided into three cases: , , or . If , we have . If , we have

| (4.11) |

where the inequality follows from for and for (see Theorem 2.1), and the last equality follows from (2.4). When , we have

where the equality follows from and the inequality follows from (using (4.11) with ).

Finally, we check that (4.3) holds for all . This proof is also divided into three cases: , , or . If , we have . If , we have

| (4.12) |

where the inequality is due to for and for (see Theorem 2.1), and the last equality follows from (2.5). If , we have

where the inequality follows from (4.12) by letting . ∎

Finally, we prove Corollary 1.

5 Concluding remarks

In this paper, we considered a joint drift rate control and impulse control problem for a Brownian inventory/production system with the objective of minimizing the long-run average cost. We proved that an optimal policy has the structure by using the lower bound approach. The existence of the optimal policy parameters was shown by solving a free boundary problem, which is crucial in this paper. We provided a roadmap to solve this free boundary problem, which we believe can be used in other control problems with more general processes.

We next discuss one extension to our model. We have assumed in this paper that the inventory level must be nonnegative. In the analysis, the nonnegative constraint is needed to solve the ODE with initial condition . In fact, backlog is also allowed in many inventory problems. In the case of backlog, a similar result, such as the optimality of a policy with control band policy and drift rate control , is expected. However, analyzing the ODE from may be inappropriate. We may start from a point sufficiently small or large, so that all policy parameters can fall in the same side of this point, just like what have done in this paper.

There are several directions worthy of future research. First, future analysis could discuss a system whose netput inventory level is given by a compound Poisson demand process plus a Brownian motion with changeable drift. [5] and [6] consider this model when the drift rate is a constant and find a solution to the corresponding quasi-variational inequality by using the Laplace transform. However, in the presence of drift rate control, the previous analysis method can not work directly and a new analytical method must be introduced to handle this problem. Second, future research could also consider the problem of minimizing the discounted total cost rather than minimizing long-run average cost. In the discounted cost case, the ODE in dynamic programming equation will no longer be one-order, but will have a two-order form as follows

where is the optimal value function and is the discount rate. With such an ODE, the proof for the existence of optimal policy parameters requires an argument different from the one presented here.

Appendix A Proof of Lemma 3.1

Proof.

Since is linear in for any fixed , we know that is concave in because the concavity is preserved under the minimization operator; see e.g., §3.2.3 in [7].

Fixing any , we have

and thus is Lipschitz continuous.

Denote and . By the definition of , we have

Summing these two inequalities, we have and thus if . Hence, is decreasing in . ∎

Appendix B Auxiliary proof for Lemma 3.6

Proof.

First, we prove that is strictly increasing in . Let and be any two numbers satisfying . If we can prove

| (B.1) | |||

| (B.2) |

then

where the first inequality follows from (B.1) and for all (see (3.31)), and the second inequality follows from (B.2). Thus, is strictly increasing in .

We next prove (B.1). Recalling the definition of in Lemma 3.4 (c) and (3.26), we have

which, together with Lemma 3.3 (a) and (b), implies that

| (B.3) |

Furthermore, it follows from (3.26) and (3.31) that

| (B.4) |

which together with the properties of , yields

Then,

Thus, taking and in (3.2), we have

| (B.5) |

which, together with the monotonicity of and (see (B.3)), implies (B.1).

We next prove (B.2). Lemma 3.4 (c) and (B.1) imply that

| (B.6) | ||||

Define . Then

where the inequality follows from (B.6). Suppose (B.2) does not hold. Then, by the continuity of , there exists a number such that . It follows from (3.2) that

which, together with , imply that

| (B.7) |

where the inequality follows from (B.3). Hence, there exists an such that , which together with , implies that there must exist an such that

| (B.8) |

Furthermore, considering in a way, similar to the analysis of (B.7), the first part of (B.8) implies , which contradicts the second part of (B.8). Thus, we have proven (B.2) and have finished the proof that is strictly increasing in .

Letting , it follows from the definition of that and thus .

We next prove the second part of (3.32). First, we show that

| (B.9) |

If it fails to hold, then (B.3) implies that there exists a finite number such that for all . Hence, it follows from (B.5) and Assumption 1 that there exists a finite number such that for all . Therefore, we have that for all ,

| (B.10) |

where the equality follows from (see (3.26) and (3.31)) and Lemma 3.4 (c), and the inequality follows from and Lemma 3.3 (a). Hence, it follows from (B.4) that

for all . However, it follows from Lemma 3.3 (b) that as for any , which is a contradiction. Therefore, (B.9) holds.

Using (B.5) and , we have . If the second part of (3.32) fails to hold, then the fact that is strictly increasing in implies that there exists a number such that for all . For any fixed pair with , implies that there exists a such that for any ,

Then, it follows from Lemma 3.4 (c) that

which implies that . Furthermore, it follows from (3.3) and that for any and ,

which yields that for ,

where . Therefore, (B.9) immediately implies

However, it follows from and Lemma 3.4 (c) that . This contradiction implies the second part of (3.32). ∎

Acknowledgments

We thank Professor Hanqin Zhang at the National University of Singapore for discussions about this problem.

References

- Adkins and Davidson [2012] Adkins, William A., Mark G. Davidson. 2012. Ordinary Differential Equations. Undergraduate Texts in Mathematics, Springer.

- Ata et al. [2005] Ata, B., J. M. Harrison, L. A. Shepp. 2005. Drift rate control of a Brownian processing system. The Annals of Applied Probability 15(2) 1145–1160.

- Ata and Tongarlak [2013] Ata, B., M. H. Tongarlak. 2013. On scheduling a multiclass queue with abandonments under general delay costs. Queueing Systems 74(1) 65–104.

- Avram and Karaesmen [1996] Avram, F., F. Karaesmen. 1996. A method for computing double band policies for switching between two diffusions. Probability in the Engineering and Informational Sciences 10(4) 569–590.

- Benkherouf and Bensoussan [2009] Benkherouf, L., A. Bensoussan. 2009. Optimality of an () policy with compound Poisson and diffusion demands: a quasi-variational inequalities approach. SIAM Journal on Control and Optimization 48(2) 756–762.

- Bensoussan et al. [2005] Bensoussan, A., R. H. Liu, S. P. Sethi. 2005. Optimality of an policy with compound Poisson and diffusion demands: a quasi-variational inequalities approach. SIAM Journal on Control and Optimization 44(5) 1650–1676.

- Boyd and Vandenberghe [2004] Boyd, S., L. Vandenberghe. 2004. Convex Optimization. Cambridge University Press, Cambridge.

- Bradley [2004] Bradley, J. R. 2004. A brownian approximation of a production-inventory system with a manufacturer that subcontracts. Operations Research 52(5) 765–784.

- Chen et al. [2010] Chen, H., O. Q. Wu, D. Yao. 2010. On the benefit of inventory-based dynamic pricing strategies. Production and Operations Management 19(3) 249–260.

- Chernoff and Petkau [1978] Chernoff, H., A. J. Petkau. 1978. Optimal control of a Brownian motion. SIAM Journal on Applied Mathematics 34(4) 717–731.

- Constantinides [1976] Constantinides, G. M. 1976. Stochastic cash management with fixed and proportional transaction costs. Management Science 22(12) 1320–1331.

- Constantinides and Richard [1978] Constantinides, G. M., S. Richard. 1978. Existence of optimal simple policies for discounted-cost inventory and cash management in continous time. Operations Research 26(4) 620–636.

- Dai and Yao [2013a] Dai, J. G., D. Yao. 2013a. Brownian inventory models with convex holding cost, part 1: average-optimal controls. Stochastic Systems 3(2) 442–499.

- Dai and Yao [2013b] Dai, J. G., D. Yao. 2013b. Brownian inventory models with convex holding cost, part 2: discount-optimal controls. Stochastic Systems 3(2) 500–573.

- Doshi [1978] Doshi, B. T. 1978. Two-mode control of Brownian motion with quadratic loss and switching costs. Stochastic Processes and their Applications 6(3) 277–289.

- Feng and Muthuraman [2010] Feng, Haolin, Kumar Muthuraman. 2010. A computational method for stochastic impulse control problems. Mathematics of Operations Research 35(4) 830–850.

- Fleming and Soner [2006] Fleming, W. H., H. M. Soner. 2006. Controlled Markov Processes and Viscosity Solutions. Springer, USA.

- Ghosh and Weerasinghe [2007] Ghosh, A. P., A. P. Weerasinghe. 2007. Optimal buffer size for a stochastic processing network in heavy traffic. Queueing Systems 55(3) 147–159.

- Harrison et al. [1983] Harrison, J. M., T. M. Sellke, M. I. Taksar. 1983. Impulse control of Brownian motion. Mathematics of Operations Research 8(3) 454–466.

- Hsieh and Sibuya [1999] Hsieh, Po-Fang, Yasutaka Sibuya. 1999. Basic Theory of Ordinary Differential Equations. Universitext, Springer.

- Li and Zheng [2006] Li, Q., S. Zheng. 2006. Joint inventory replenishment and pricing control for systems with uncertain yield and demand. Operations Research 54(4) 696–705.

- Ormeci et al. [2008] Ormeci, M., J. G. Dai, J. Vande Vate. 2008. Impulse control of Brownian motion: the constrained average cost case. Operations Research 56(3) 618–629.

- Ormeci and Vande Vate [2011] Ormeci, M., J. Vande Vate. 2011. Drift control with changeover costs. Operations Research 59(2) 427–439.

- Ormeci et al. [2015] Ormeci, M., J. Vande Vate, H. Wang. 2015. Solving the drift control problem. Stochastic Systems 5(2) 324–371.

- Rath [1977] Rath, J. H. 1977. The optimal policy for a controlled Brownian motion process. SIAM Journal of Applied Mathmatics 32(1) 115–125.

- Richard [1977] Richard, Scott F. 1977. Optimal impulse control of a diffusion process with both fixed and proportional costs of control. SIAM Journal of Control and Optimization 15(1) 79–91.

- S.Kumagai [1980] S.Kumagai. 1980. An implicit function theorem: Comment. Journal of Optimization Theory and Applications 31(2) 285–288.

- Song et al. [2012] Song, Q., G. G. Yin, C. Zhu. 2012. Optimal switching with constraints and utility maximization of an indivisible market. SIAM Journal on Control and Optimization 50(2) 629–651.

- Wu and Chao [2014] Wu, J., X. Chao. 2014. Optimal control of a Brownian production/inventory system with average cost criterion. Mathematics of Operations Research 39(1) 163–189.

- Yao [2017] Yao, D. 2017. Joint pricing and inventory control for a stochastic inventory system with Brownian motion demand. IISE Transactions To appear.

- Zhang and Zhang [2012] Zhang, H., Q. Zhang. 2012. An optimal inventory-price coordination policy. Stochastic Process, Finance and Control, Advances in Statistics, Probability and Actuarial Science: Volume 1. Edited by S. N. Cohen, D. Madan, T. K. Siu and H. Yang 571–585.