Pricing Perpetual Put Options by the Black–Scholes Equation with a Nonlinear Volatility Function

Abstract

We investigate qualitative and quantitative behavior of a solution of the mathematical model for pricing American style of perpetual put options. We assume the option price is a solution to the stationary generalized Black-Scholes equation in which the volatility function may depend on the second derivative of the option price itself. We prove existence and uniqueness of a solution to the free boundary problem. We derive a single implicit equation for the free boundary position and the closed form formula for the option price. It is a generalization of the well-known explicit closed form solution derived by Merton for the case of a constant volatility. We also present results of numerical computations of the free boundary position, option price and their dependence on model parameters.

Key words. Option pricing, nonlinear Black-Scholes equation, perpetual American put option, early exercise boundary

2000 Mathematical Subject Classifications. 35R35 91B28 62P05

1 Introduction

In a stylized financial market, the price of a European option can be computed from a solution to the well-known Black–Scholes linear parabolic equation derived by Black and Scholes in [5], and, independently by Merton in [26] (c.f. Kwok [23], Dewynne et al. [11], Hull [20]). A European call (put) option is the right but not obligation to purchase (sell) an underlying asset at the expiration price at the expiration time .

In contrast to European options, American style options can be exercised anytime in the temporal interval with the specified time of obligatory expiration at . A mathematical model for pricing American put options leads to a free boundary problem. It consists in construction of a function together with the early exercise boundary profile satisfying the following conditions:

-

1.

is a solution to the Black–Scholes partial differential equation:

(1) defined on the time dependent domain where . Here is the volatility of the underlying asset price process, is the interest rate of a zero-coupon bond. A solution represents the price of an American style put option for the underlying asset price at the time ;

-

2.

satisfies the terminal pay-off condition:

(2) -

3.

and boundary conditions for the American put option:

(3) for and .

Since the seminal paper by Brennan and Schwartz [9] American style of a put option has been investigated by many authors (c.f. Kwok [23] and references therein). Various accurate analytic approximations of the free boundary position have been derived by Stamicar, Ševčovič and Chadam [29], Evans, Kuske and Keller [12], and by S. P. Zhu and Lauko and Ševčovič in recent papers [33] and [24] dealing with analytic approximations on the whole time interval.

If the volatility in (1) is constant then (1) is a classical linear Black–Scholes parabolic equation derived by Black and Scholes in [5]. If we assume the volatility is a function of the solution then equation (1) with such a diffusion coefficient represents a nonlinear generalization of the Black–Scholes equation. In this paper we focus our attention to the case when the diffusion coefficient may depend on the asset price and the second derivative of the option price. More precisely, we will assume that

| (4) |

i.e. depends on the product of the asset price and the second derivative (Gamma) of the option price . Recall that the nonlinear Black–Scholes equation (1) with a nonlinear volatility having the form of (4) arises from option pricing models taking into account nontrivial transaction costs, market feedbacks and/or risk from a volatile (unprotected) portfolio. The linear Black–Scholes equation with a constant volatility has been derived under several restrictive assumptions like e.g., frictionless, liquid and complete markets, etc. Such assumptions have been relaxed in order to model the presence of transaction costs (see e.g., Leland [25], Hoggard et al. [19], Avellaneda and Paras [2]), feedback and illiquid market effects due to large traders choosing given stock-trading strategies (Frey [13], Frey and Patie [14], Frey and Stremme [15], Schönbucher and Wilmott [28]), imperfect replication and investor’s preferences (Barles and Soner [4]), risk from unprotected portfolio (Kratka [22], Jandačka and Ševčovič [21] or [30]).

In the Leland model (generalized for more complex option strategies by Hoggard et al. [19]) the volatility is given by where is the constant historical volatility of the underlying asset price process and is the so-called Leland number. Another nonlinear Black–Scholes model has been derived by Frey in [13]. In this model the asset dynamics takes into account the presence of feedback effects due to a large trader choosing his/her stock-trading strategy (see also [28]). The diffusion coefficient is again non-constant:

| (5) |

where are constants.

Next example of the Black–Scholes equation with a non-constant volatility is the so-called Risk Adjusted Pricing Methodology model proposed by Kratka in [22] and revisited by Jandačka and Ševčovič in [21]. In the Risk adjusted pricing methodology model (RAPM) the purpose is to optimize the time-lag between consecutive portfolio adjustments in such way that the sum of the rate of transaction costs and the rate of a risk from unprotected portfolio is minimal. In this model, the volatility is again non-constant and has the form:

| (6) |

where is a constant historical volatility of the asset price returns and where are nonnegative constants representing the transaction cost measure and the risk premium measure, respectively (see [21] for details). Recently, explicit solutions to the Black–Scholes equation with varying volatility of the form (5) and (6) have been derived by Bordag and Chmakova [6] and Bordag [7, 8].

Another important contribution in this direction has been presented by Amster, Averbuj, Mariani and Rial in [1], where the transaction costs are assumed to be a non-increasing linear function of the form , (), depending on the volume of traded stocks that is needed to hedge the replicating portfolio. In the model studied by Amster et al. [1] the volatility function has the following form:

| (7) |

A disadvantage of such a transaction costs function is the fact that it may attain negative values when the amount of transactions exceeds the critical value . The model (7) has been generalized to a class of nonnegative variable transaction cost function by Ševčovič and Žitňanská in [32].

In [3] Bakstein and Howison investigated a parametrized model for liquidity effects arising from the asset trading. In their model the volatility function is a quadratic function of the term :

| (8) |

The parameter corresponds to a market depth measure, i.e. it scales the slope of the average transaction price. The parameter models the relative bid–ask spreads and it is related to the Leland number through relation . Finally, transforms the average transaction price into the next quoted price, . An interesting generalization of the linear Black-Scholes equation with the volatility function polynomially dependent on has been proposed by Cetin, Jarrow and Protter [10].

Note that if additional model parameters (e.g., Le, ) are vanishing then all the aforementioned nonlinear models are consistent with the original Black–Scholes equation, i.e. . Furthermore, for call or put options, the function is convex in the variable.

The main purpose of this paper is to investigate qualitative and quantitative behavior of a solution to the problem of pricing American style of perpetual put options. We assume the option price is a solution to a stationary generalized Black-Scholes equation with a nonlinear volatility function. We prove existence and uniqueness of a solution to the free boundary problem. We derive a single implicit equation for the free boundary position and the closed form formula for the option price. It is a generalization of the well-known explicit closed form solution derived by Merton for the case of a constant volatility. We also present results of numerical computations of the free boundary position, option price and their dependence on model parameters. In the recent paper [17] we investigated the case when the volatility function may depend on and including other models proposed by Barles and Soner [4], Frey and Patie [14], Frey and Stremme [15]. However, for these models there is no single implicit equation for the free boundary position and numerical methods have to be adopted.

The paper is organized as follows. In the next section we recall mathematical formulation of the perpetual American put option pricing model. We furthermore present the explicit solutions for the case of the constant volatility derived by Merton. In Section 3 we prove the existence and uniqueness of a solution to the free boundary problem. We derive a single implicit equation for the free boundary position and the closed form formula for the option price. The first order expansion of the free boundary position with respect to the model parameter is also derived. We construct suitable sub– and supper–solutions based on Merton’s explicit solutions. In Section 4 we present results of numerical computations of the free boundary position, option price and their dependence on the model parameter.

2 Perpetual American put options

In this section we analyze the problem of pricing American perpetual put options. By definition, perpetual options are options with a very long maturity . Notice that both the option price and the early exercise boundary position depend on the remaining time to maturity. Recently, stationary solutions to generalized Black–Scholes equation have been investigated by Grossinho et al. in [16, 18]. Suppose that there exists a limit of the solution and early exercise boundary position for the maturity .

For an American style put option the limiting price and the limiting early exercise boundary position of the perpetual put option is a solution to the stationary nonlinear Black–Scholes partial differential equation:

| (9) |

and

| (10) |

Our purpose is to analyze the system of equations (9)–(10). In what follows, we will prove the existence and uniqueness of a solution pair to (9)–(10).

In the rest of the paper, we will assume the volatility function

| (11) |

is non-decreasing, and such that the function is smooth for . Under these assumptions there exists an increasing inverse function such that

| (12) |

which is an continuous and non-decreasing function such that , and for . As we have

| (13) |

where . Moreover, for any there exists such that

| (14) |

Notice that the transformation is a useful tool when analyzing nonlinear generalizations of the Black–Scholes equations. For example, using this transformation the fully nonlinear Black–Scholes equation with a volatility function can be transformed into a quasilinear equation for the new variable (see [21] and [31] for details).

2.1 The Merton explicit solution for the constant volatility case

In the case of a constant volatility the free boundary value problem (9)–(10) for the function and the limiting early exercise boundary position has a simple explicit solution discovered by Merton [27]. The closed form solution has the following form:

| (15) |

where

| (16) |

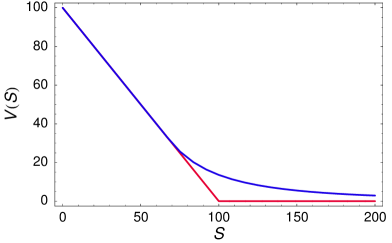

A graph of a perpetual American put option with the constant volatility is shown in Fig. 1.

3 Existence and uniqueness of solutions

In this section we will focus our attention on existence and uniqueness of a solution to the problem (9)–(10).

3.1 Explicit formula for the perpetual American put option price

Since is the inverse function to the pair is a solution to (9) if and only if

Let us introduce the following transformation of variables:

| (17) |

Since

the function is a solution to the initial value problem

| (18) | |||

| (19) |

The initial condition (19) easily follows from the smooth pasting conditions and . Equation (18) can be easily integrated. We have the following result:

Taking into account the estimates (13) and (14) we can summarize the useful properties of the function :

Lemma 2

The function is non-decreasing and . Furthermore, , , and, consequently, .

Since

by taking into account the boundary condition we conclude that the solution to equation (9) is given by

Using the substitution we have

As the expression for can be simplified as follows:

| (21) |

3.2 Equation for the free boundary position

Using the expression (21) we can derive a single implicit integral equation for the free boundary position . Clearly, if and only if

| (22) |

As we obtain

| (23) |

Therefore the free boundary position is a solution to the following implicit equation:

3.3 Main result

In this section we summarize the previous results and state the main result on existence and uniqueness of a solution to the perpetual American put option pricing problem (9)–(10).

Theorem 1

Suppose that the volatility function is non-decreasing, and such that the function is smooth for .

P r o o f. According to results in Section 3.2 it suffices to prove that (24) has the unique solution . To this end, let us introduce the auxiliary function:

we have . For a fixed we have for , and

Hence equation (24) has the unique solution . Clearly, because the right hand side of (22) is positive.

Since is a solution to (23) we have . Moreover, as

(see (17)) we obtain, for ,

Hence is a solution to the perpetual American put option pricing problem (9)–(10), as claimed.

Remark 1

In the case of a constant volatility function we have . It follows from equation (24) that

and,

because , and so . Hence the solution is identical with Merton’s explicit solution.

3.4 Sensitivity analysis

In this section we will investigate dependence of the free boundary position on model parameters. We consider the volatility function of the form:

Here and are specific model parameters. Our goal is to find the first order expansion of the free boundary position considered as a function of a parameter , i.e. .

First, we derive expression for the derivative of the inverse function . For we have and so

For we have . Therefore

The first derivative of the free boundary position can be deduced from the implicit equation (24). We have

Since, for we have we conclude

In summary we have shown the following result:

Theorem 2

If the volatility function has the form as , where , then the free boundary position of the perpetual American put option pricing problem has the asymptotic expansion:

Remark 2

In the case we have . It corresponds to the constant volatility model. Thus where . Hence

as claimed by Theorem 2.

3.5 Comparison principle and Merton’s sub– and super–solutions

In this section our aim is to derive sub– and super–solutions to the perpetual American put option pricing problem.

Let be positive constant. By we will denote the explicit Merton solution presented in Section 2.1, i.e.

| (26) |

where

| (27) |

It means that the pair is the explicit Merton solution corresponding to the constant volatility (see (15)).

Then, for the transformed function we have

Clearly,

| (28) |

Next we will construct a super–solution to the solution of the equation by means of the Merton solution where is the unique root of the equation

| (29) |

Since

we obtain

By taking the inverse function we finally obtain

With regard to (28) we conclude that

| (30) |

Similarly, we will construct the Merton sub–solution satisfying the opposite differential inequality. Let be given by

| (31) |

i.e. . Then

and so, by taking the inverse function we obtain . Then, from (28) we conclude that

| (32) |

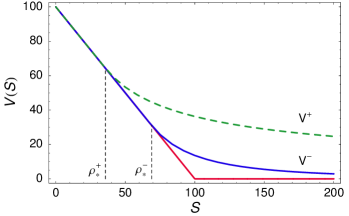

In Fig. 2 we plot Merton’s solutions corresponding to () and () where .

In what follows, we will prove the inequalities

| (33) |

where is the free boundary position for the nonlinear perpetual American put option pricing problem (9)–(10).

Denote

the inverse function to the function . As we have for any . Since

we conclude the inequality .

On the other hand, let

be the inverse function to the function . Then, for we have

Therefore, for we have and arguing similarly as before we obtain the estimate and so the inequalities (33) follows.

For initial conditions we have and so

Using the comparison principle for solutions of ordinary differential inequalities we have . Taking into account the explicit form of the function from Theorem 1 (see (25)) we conclude the following result:

Theorem 3

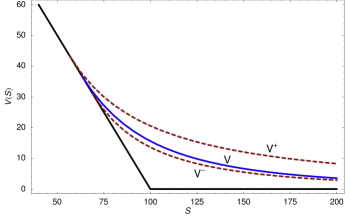

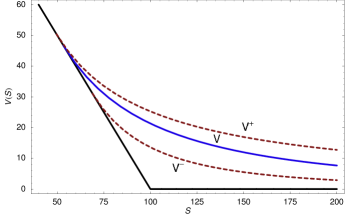

A graphical illustration of the comparison principle is shown in Fig. 6.

4 Numerical approximation scheme and computational results

In this section we propose a simple and efficient numerical scheme for constructing a solution to the perpetual put option problem (9)–(10).

Using transformation , i.e. and we can rewrite the equation for the free boundary position (see (24)) as follows:

| (34) |

Similarly, the option price (24) can be rewritten in terms of the variable as follows:

| (35) |

With this transformation we can reduce computational complexity in the case when the inverse function is not given by a closed form formula.

4.1 Numerical results

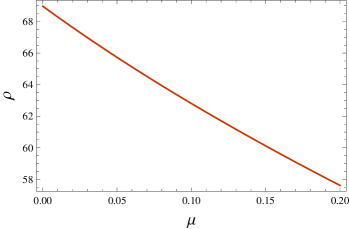

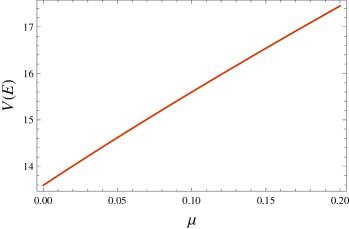

Results of numerical calculation for the Frey model (5) and the RAPM model (6) are summarized in Tables 1 and 3. We show the position of the free boundary and the perpetual option value evaluated at the exercise price . The results are computed for various values of the parameter for the Frey model and the RAPM model. Other model parameter were chosen as: and .

a) b)

| 0.00 | 0.01 | 0.05 | 0.10 | 0.15 | 0.20 | 0.22 | |

|---|---|---|---|---|---|---|---|

| 68.9655 | 68.2852 | 65.7246 | 62.8036 | 60.1175 | 57.6177 | 56.6627 | |

| 13.5909 | 13.8005 | 14.6167 | 15.5961 | 16.5389 | 17.4510 | 17.8083 |

In the Frey model (5) the nonlinear volatility function has the form:

The range of the parameter is therefore limited to satisfy the strict inequality . However, using the identity

we can approximate the Frey volatility function as follows:

| (36) |

where is sufficiently large. Interestingly, a similar power series expansion of can be found in the generalized Black-Scholes model proposed by Cetin, Jarrow and Protter in [10].

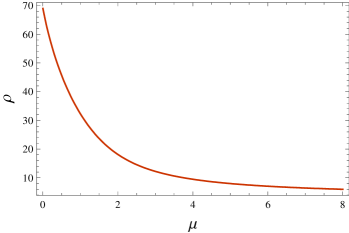

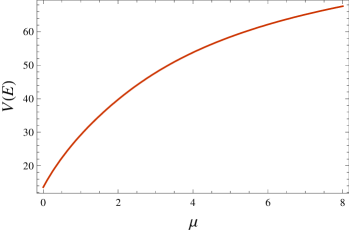

In computations shown in Fig. 4 and Tab. 2 we present results of the free boundary position and the perpetual American put option price for and larger interval of parameter values . Note that the results for small values computed from the original Frey volatility (5) and (36) are very close to each other.

a) b)

| 0.00 | 0.10 | 0.50 | 1.00 | 2.00 | 4.00 | 8.00 | |

|---|---|---|---|---|---|---|---|

| 68.9655 | 62.8037 | 45.3007 | 31.0862 | 16.3126 | 8.3818 | 5.4556 | |

| 13.5909 | 15.5961 | 22.4529 | 29.5719 | 41.0654 | 56.1777 | 70.2259 |

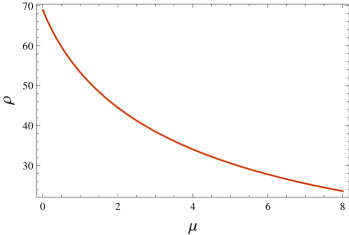

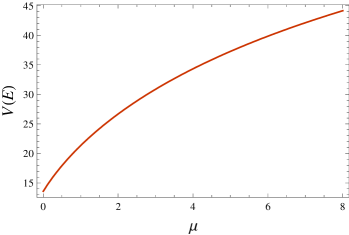

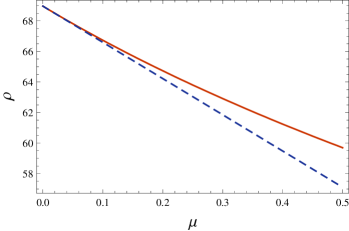

In our next computational example we consider the Risk adjusted pricing methodology model (RAPM). In computations shown in Fig. 5, a) and Tab. 3 we present results of the free boundary position and the perpetual American put option price for the RAPM model (see Fig. 5, b)). We also show comparison of the free boundary position and its linear approximation derived in Theorem 2 (see Fig. 5, c)).

a) b)

c)

| 0.00 | 0.10 | 0.50 | 1.00 | 2.00 | 4.00 | 8.00 | |

|---|---|---|---|---|---|---|---|

| 68.9655 | 66.7331 | 59.6973 | 53.3234 | 44.5408 | 34.0899 | 23.6125 | |

| 13.5909 | 14.5761 | 17.9398 | 21.3434 | 26.6857 | 34.3393 | 44.1774 |

a) b)

In the last examples shown in Fig. 6 we present comparison of the option price and the free boundary position for the Frey model (left) and the Risk adjusted pricing methodology model (right) with closed form explicit Merton’s solutions corresponding to the constant volatility.

5 Conclusions

In this paper we analyzed the free boundary problem for pricing perpetual American put option when the volatility is a function of the second derivative of the option price. We showed how the problem can be transformed into a single implicit equation for the free boundary position and explicit integral expression for the option price.

Acknowledgements

This research was supported by the European Union in the FP7-PEOPLE-2012-ITN project STRIKE - Novel Methods in Computational Finance (304617), the project CEMAPRE – MULTI/00491 financed by FCT/MEC through national funds and the Slovak research Agency Project VEGA 1/0251/16.

Competing interests

The authors declare that they have no competing interests.

References

- [1] Amster, P., Averbuj, C. G., Mariani, M. C., and Rial, D.: A Black–Scholes option pricing model with transaction costs. J. Math. Anal. Appl., 303 (2005), 688–695.

- [2] Avellaneda, M., and Paras, A.: Dynamic Hedging Portfolios for Derivative Securities in the Presence of Large Transaction Costs. Applied Mathematical Finance, 1 (1994), 165–193.

- [3] Bakstein, D., and Howison, S.: A non–arbitrage liquidity model with observable parameters. Working paper (2004), http://eprints.maths.ox.ac.uk/53/

- [4] Barles, G., and Soner, H. M.: Option Pricing with transaction costs and a nonlinear Black–Scholes equation. Finance Stochast., 2 (1998), 369-397.

- [5] Black, F., and Scholes, M.: The pricing of options and corporate liabilities. J. Political Economy, 81 (1973), 637–654.

- [6] Bordag, L. A., and Chmakova, A. Y.: Explicit solutions for a nonlinear model of financial derivatives. Int. J. Theor. Appl. Finance, 10(1) (2007), 1–21.

- [7] Bordag, L. A.: Study of the risk-adjusted pricing methodology model with methods of Geometrical Analysis. Stochastics: International Journal of Probability and Stochastic processes, 83(4-6) (2011), 333- 345.

- [8] Bordag, L. A.: Geometrical Properties of Differential Equations: Applications of the Lie Group Analysis in Financial Mathematics. World Scientific Publishing Co Inc, 2015.

- [9] Brennan, M. J., and Schwartz, E. S.: The valuation of American put options. Journal of Finance, 32 (1977), 449-462.

- [10] Cetin, U., Jarrow, R., and Protter, P.: Liquidity risk and arbitrage pricing theory. Finance and Stochastics, 8(3) (2004), 311–441.

- [11] Dewynne, J. N., Howison, S. D., Rupf, J., and Wilmott, P.: Some mathematical results in the pricing of American options. Euro. J. Appl. Math., 4 (1993), 381–398.

- [12] Evans, J.D., R. Kuske, and J.B. Keller: American options on assets with dividends near expiry, Mathematical Finance, 12(3) (2002), 219–237.

- [13] Frey, R.: Perfect option hedging for a large trader. Finance and Stochastics, 2 (1998), 115–142.

- [14] Frey, R., and Patie, P.: Risk Management for Derivatives in Illiquid Markets: A Simulation Study. Advances in Finance and Stochastics, Springer, Berlin, 2002, pp. 137–159.

- [15] Frey, R., and Stremme, A.: Market Volatility and Feedback Effects from Dynamic Hedging. Mathematical Finance, 4 (1997), 351–374.

- [16] Grossinho, M. R., and Morais, E.: A note on a stationary problem for a Black-Scholes equation with transaction costs. International Journal of Pure and Applied Mathematics, 51 (2009), 557–565.

- [17] Grossinho, M., Kord Faghan, Y., and Ševčovič, D.: Analytical and numerical results for American style of perpetual put options through transformation into nonlinear stationary Black-Scholes equations, In: Novel Methods in Computational Finance, Ehrhardt, M. Günther, M., ter Maten, J. (Eds.), Mathematics in Industry, Volume 25, 2017, Springer International Publishing, 129–142.

- [18] Fabiao, R. F., Grossinho, M. R., and Simoes, O.: Positive solutions of a Dirichlet problem for a stationary nonlinear Black-Scholes equation, Nonlinear Analysis, Theory, Methods and Applications, 71 (2009), 4624–4631.

- [19] Hoggard, T., Whalley, A.E., and Wilmott, P.: Hedging option portfolios in the presence of transaction costs. Advances in Futures and Options Research, 7 (1994), 21–35.

- [20] Hull, J.: Options, Futures and Other Derivative Securities, Prentice Hall, 1989.

- [21] Jandačka, M., and Ševčovič, D.: On the risk adjusted pricing methodology based valuation of vanilla options and explanation of the volatility smile. Journal of Applied Mathematics, 3 (2005), 235–258.

- [22] Kratka, M.: No Mystery Behind the Smile, Risk, 9 (1998), 67–71.

- [23] Kwok, Y. K.: Mathematical Models of Financial Derivatives. Springer-Verlag, 1998.

- [24] Lauko, M., and Ševčovič. D.: Comparison of numerical and analytical approximations of the early exercise boundary of American put options. ANZIAM journal, 51 (2011), 430-448.

- [25] Leland, H. E.: Option pricing and replication with transaction costs. Journal of Finance, 40 (1985), 1283–1301.

- [26] Merton, R.: Optimum consumption and portfolio rules in a continuous time model. Journal of Economic Theory, 3 (1971), 373 – 413.

- [27] Merton, R. C.: Theory of rational option pricing. The Bell Journal of economics and management science (1973), 141-183.

- [28] Schönbucher, P., and Wilmott, P.: The feedback-effect of hedging in illiquid markets. SIAM Journal of Applied Mathematics, 61 (2000), 232–272.

- [29] Stamicar, R., Ševčovič, D., and Chadam, J.: The early exercise boundary for the American put near expiry: numerical approximation. Canad. Appl. Math. Quarterly, 7 (1999), 427–444.

- [30] Ševčovič. D.: An iterative algorithm for evaluating approximations to the optimal exercise boundary for a nonlinear Black-Scholes equation. Canad. Appl. Math. Quarterly 15 (2007), 77–97.

- [31] Ševčovič, D., Stehlíková, B., and Mikula, K.: Analytical and numerical methods for pricing financial derivatives. Nova Science Publishers, Inc., Hauppauge, 2011, 309 pp.

- [32] Ševčovič, D., and Žitňanská, M.: Analysis of the nonlinear option pricing model under variable transaction costs, Asia-Pacific Financial Markets 23(2) (2016), 153–174.

- [33] Zhu, Song-Ping: A new analytical approximation formula for the optimal exercise boundary of American put options. Int. J. Theor. Appl. Finance, 9 (2006), 1141–1177.