Portfolio Benchmarking under Drawdown Constraint and Stochastic Sharpe Ratio

Abstract

We consider an investor who seeks to maximize her expected utility derived from her terminal wealth relative to the maximum performance achieved over a fixed time horizon, and under a portfolio drawdown constraint, in a market with local stochastic volatility (LSV). In the absence of closed-form formulas for the value function and optimal portfolio strategy, we obtain approximations for these quantities through the use of a coefficient expansion technique and nonlinear transformations. We utilize regularity properties of the risk tolerance function to numerically compute the estimates for our approximations. In order to achieve similar value functions, we illustrate that, compared to a constant volatility model, the investor must deploy a quite different portfolio strategy which depends on the current level of volatility in the stochastic volatility model.

Keywords and phrases. portfolio optimization, drawdown, stochastic volatility, local volatility

AMS (2010) classification. 91G10, 91G80

JEL classification. G11

1 Introduction

1.1 Background and motivation

In the vast and long-dated literature on dynamic portfolio optimization, different types of terminal utility paradigms under various portfolio constraints have been considered to understand investor behaviour (see, for instance, Rogers [19] for a detailed exposition). The solutions to these problems provide optimal investment strategies which aid institutional investors, and at times help to reveal deep insights about market observed phenomenons. The classical problem of continuous-time portfolio optimization dates back to Samuelson [20] and Merton [16, 15]. In his seminal paper, Merton [16] considered a market where the prices of risky assets are given by geometric Brownian motions (with constant volatilities), and the objective is to maximize the expected utility of terminal wealth by investing capital between the risky assets and a risk-free bank account. For constant relative risk aversion utility (CRRA) functions, the author showed that the optimal strategy is a “fixed mix” investment in the risky assets and the bank account.

Merton’s landmark result provided structural market insight but the restrictive problem setting – investor objective and market dynamics – prevented application of the results to practical situations. As a result, subsequent research has focused upon relaxing the assumptions made in [16], incorporating various market constraints and considering more realistic model settings.

Portfolio managers typically use a stop-loss level on the portfolio value to prevent a complete wipe-out of wealth in the face of falling prices. This is also known more commonly as the drawdown constraint. Under this constraint, the wealth in the portfolio must always remain above a certain fraction of the current maximum wealth value achieved. Furthermore, in several instances, portfolio managers commit a certain percentage of the starting wealth to the pooling investors. This situation is also covered by imposing a drawdown constraint on the portfolio wealth.

In this article, we propose a new framework to study the dynamic portfolio optimization under a drawdown portfolio constraint in a stochastic volatility market model. In many empirical studies it has been well established that stochastic volatility is a reasonable asset price modelling tool to capture the market observed volatility smiles and volatility clustering. Our principal innovation is to introduce a new terminal investor objective paradigm which allows for a reduction in the dimensionality of the problem. As our central objective in this work is to numerically study the impact of stochastic volatility on the value function and optimal portfolio strategy, the dimensionality reduction serves as a crucial feature to allow for an efficient implementation of the numerical procedures used to solve the problem and study the effects of stochastic volatility.

1.2 Literature review

Several authors have considered the optimal portfolio problems under drawdown constraint. Grossman and Zhou [9] were the first to comprehensively study this problem over infinite time horizon in a lognormal market model. They investigated to maximize the long term growth rate of the expected utility of the wealth and used dynamic programming principle to solve the problem. Cvitanic and Karatzas [5] streamlined the analysis of Grossman and Zhou [9] and extended the results to the case when there are multiple risky assets whose dynamics are governed by a lognormal model with deterministic coefficients. By defining an auxiliary process, they were able to show that the solution of optimization problem with drawdown constraint can be linked to an unconstrained optimization problem whose solution follows from the work of Karatzas et al. [11]. They further showed that in the case of logarithmic utility function, the results hold even if the coefficients in the lognormal model are random and satisfy some ergodicity condition. In [21], Sekine carried forward the arguments and results of Cvitanic and Karatzas [5] to a multi-asset market model with single stochastic volatility factor. More recently, Cherny and Obłój [4] have studied the optimal portfolio problem in an abstract semimartingale model with a generalized drawdown constraint. They utilized the properties of Azéma-Yor processes to show that the value function of the constrained problem, where the investor objective is to maximize the long term growth rate of the expected utility, has the same value function as an unconstrained problem with a suitably modified utility function. Moreover, they showed that the optimal wealth process can also be obtained as an explicit pathwise transformation of the optimal wealth process in the unconstrained problem.

The portfolio optimization problem with drawdown constraint has also been studied in a continuous-time framework with consumption. Roche [18] studied the problem of maximizing the expected utility of consumption over an infinite time horizon for a power utility function under a linear drawdown constraint. This analysis was performed in the setting of a lognormal model with single asset. Elie and Touzi [7] subsequently generalized the result to a general class of utility functions in the setting of zero interest rates and obtained an explicit representation of the solution. Elie [6] also studied a finite time version of the same problem and in the absence of analytical representation, he provided a numerical solution to the problem.

In the financial literature, different problem settings with a drawdown constraint have received considerable attention due to their significance. Magdon-Ismail and Atiya [14] considered the problem of optimal portfolio choice when the drawdown is minimized in the single asset lognormal market model. Chekhlov et al. [2] analyzed the portfolio optimization problem in discrete time where the investor objective is to maximize the expected return from the portfolio subject to risk constraints given in terms of drawdowns. They considered a multi-asset market model and reduced the problem to a linear programming problem which can be solved numerically. In the insurance literature, drawdown constraint has been incorporated to study problems of lifetime investments. In [3], Chen et al. considered the optimization problem of minimizing the probability of a significant drawdown occurring over a lifetime investment, i.e. the probability that portfolio wealth hits the drawdown barrier before a random time which represents the death time of a client.

1.3 Our contributions

In this article, we consider an investor who at any time is worried about her wealth falling below a fixed fraction of the running maximum wealth and, thus, is only interested to maximize the ratio of these two quantities at the end of a fixed investment horizon. As the investor is cautious about the drawdown, consequently it is not possible to achieve an unreasonable amount of wealth by looking at an unbounded terminal utility. Therefore, it is sensible to consider a bounded terminal utility. The proposed investor objective paradigm is also motivated from the perspective of portfolio benchmarking and fixed target problems. In our setting, we start from an initial value of the maximum wealth which satisfies the drawdown constraint. The portfolio strategy in our problem allows the portfolio wealth to hit the level of initial maximum wealth by investing in the risky asset thus hitting the target or benchmark. Heuristically, it can also be deduced that the optimal portfolio strategy will liquidate the position in the risky asset once the maximum wealth is reached. This mimics the logic of classical Merton strategy which suggests to sell the risky asset close to the highest value of the portfolio.

We consider the basic setting of a frictionless financial market with a single underlying asset and a risk-free money market account. We study this problem in a stochastic volatility environment to demonstrate how uncertainty in the volatility impacts the optimal portfolio strategy. This problem has no explicit solution and thus, we look for accurate approximations to the value function and optimal strategy. We use the technique of coefficient expansion to formulate separate problems for different terms in the expansion of value function. The solutions to these problems allow us to derive an expansion for the optimal portfolio strategy. Due to the presence of portfolio constraints, the expansion terms in the value function approximation are not available in closed-form. We numerically solve for the leading term in the value function approximation and use the regularity properties of the so-called risk tolerance function to compute the remaining higher order expansion terms. The numerical estimates for the optimal portfolio strategy are derived similarly.

We show that the leading terms in the expansion of value function and optimal strategy are related to the solution of our problem in a lognormal asset pricing model with constant volatility. The optimal strategy in this case suggests to liquidate the risky position when portfolio wealth approaches its maximum value. Also, close to the drawdown constraint, the optimal strategy instructs to steadily build up a position in the risky asset to drive away the portfolio value from the lower barrier. The stochastic volatility correction term for the value function suggests very small loss or gain due to the uncertainty in volatility. However, we observe that depending on the current level of stochastic volatility, the optimal strategy with volatility correction is remarkably different than the case with constant volatility. Close to the maximum wealth value, the corrected optimal strategy suggests to hold onto the risky assets longer than in the constant volatility case. This clearly illustrates the impact of stochastic volatility on the optimal investment strategy. However, near the drawdown barrier, the behavior of corrected optimal strategy depends on the level of current stochastic volatility in the model when compared to the optimal strategy in the constant volatility case.

1.4 Organization

In Section 2 we introduce the continuous-time model setting and formulate the problem. We derive the HJB equation for the optimal portfolio problem and give the analytical formula for the optimal portfolio strategy in terms of the value function. We provide the approximation formulas for the value function and optimal portfolio strategy in Section 3 and summarize our main results. In Section 4, we discuss the numerical implementation of our results and provide practical insights with the help of popular numerical examples considered in the literature. Section 5 concludes the article and suggests directions for future research. The proofs are included in Appendix A.

2 Problem Formulation

We consider a complete filtered probability space endowed with a two dimensional Brownian motion and suppose there is a risky asset whose dynamics under is given by the following local stochastic volatility (LSV) model:

where and are standard Brownian motions under measure with correlation From Itô’s formula, the log price process is described as following:

where and

We assume that the model coefficient functions and are Borel-measurable and possess sufficient regularity to ensure that a unique strong solution exists for which is adapted to the augmentation of the filtration generated by

Further, we suppose the existence of a frictionless financial market with the price of a single risky asset given by and the risk-free rate of interest given by a scalar constant In this market, we denote the wealth process of an investor by who invests units of currency in risky asset at time and the remaining units of currency in the risk-free bank account. Then, the self-financing portfolio, satisfies the following stochastic differential equation (SDE)

The running maximum wealth in time dollars is given by In this work, we propose an investment framework that encourages exiting the market in the face of a sizable drawdown, while also targeting a benchmark that is related to the running maximum, or high watermark of the investment performance. The investor’s risk preferences are given by a utility function satisfying:

Assumption 1.

The terminal utility function is smooth: It is also strictly increasing and strictly concave.

We solve the utility maximization problem at finite with the drawdown constraint:

2.1 The discounted formulation

We look to formulate the problem in the setting where the wealth process is discounted with respect to the risk-free rate of interest. This allows us to clearly study the impact of stochastic volatility on the optimal strategy and value function. For this purpose, we define, and The discounted wealth process satisfies the following SDE

where is the risky-asset trading strategy.

Now, we are ready to express the investor’s utility maximization problem by defining the value function

| (1) |

where the admissible strategies are given by

We define the domain in as where

The above value function is defined for any tuple .

We recall that on Then, for and following the usual dynamic programming principle (see, for example, Pham [17, Chapter 3 ]), we obtain the Hamilton-Jacobi-Bellman (HJB) equation

where is the generator of the process with

By inspecting the quadratic expression above in it is clear that the optimal strategy is given as

| (2) |

where the subscripts indicate partial derivatives. The HJB equation becomes

| (3) |

with the nonlinear term given as

where

| (4) |

is the Sharpe ratio function. The boundary conditions are

| (Terminal condition): | (5) | |||

| (Neumann condition): | (6) | |||

| (Drawdown Dirichlet condition): | (7) |

The above Dirichlet condition signifies that when the drawdown constraint is hit, the investor stops trading in the risky asset In the discounted formulation when the investor stops trading, it signifies that the wealth process stops varying and the investor accepts the utility which is given at the drawdown barrier.

2.2 Dimensionality reduction

The nonlinear PDE in (3) with boundary conditions (5), (6) and (7) is difficult to solve numerically because the domain is a wedge in space requiring a non-rectangular finite-difference grid. However, we notice that given the structure of our problem, we could perform a change of variable which reduces the dimensionality of the problem. We introduce

which results in a new non-linear PDE for

| (8) |

where

and the boundary conditions are

| (9) |

Apart from providing a reduction in dimensionality, the above change of variable also transforms the problem domain from a high-dimensional cone to a semi-rectangular domain which typically helps to get more accurate numerical estimates for the solution.

3 Value Function and Optimal Strategy Approximation

Even under the constant volatility lognormal asset model, no closed form solution is available for the nonlinear PDE (8) and one needs to rely on accurate numerical approximations. In this paper, we propose to find an approximation for the value function as

| (10) |

as well as an approximation for the optimal investment strategy

| (11) |

by using the coefficient expansion technique. This approach has been developed for the linear European option pricing problem in a general LSV model setting by Lorig et al. [13], and for the classical (unconstrained) Merton problem by Lorig and Sircar [12].

3.1 Coefficient polynomial expansions

The main idea of the coefficient expansion technique is to first fix a point and then for any function which is locally analytic around define the following family of functions indexed by

where

Note that for , is a constant. We can observe that is the Taylor series expansion of about the point Here, is seen as a perturbation parameter which is used to identify the successive terms in the approximation.

To apply this technique in PDE (8), we first replace each of the coefficient functions

with their respective series expansion for some and . Next, to obtain approximations as in (10) and (11), we define a series expansion of value function as linear operator and replace the non-linear operator by which involves series expansions for the coefficient functions and the value function. Then from (8), we consider the PDE problem

3.2 Zeroth and first order approximation

The first term in the approximation (10) is obtained by collecting the zeroth order terms w.r.t. in the expansion of (12). We get

| (14) |

with

| (15) |

and the corresponding order boundary conditions are

| (16) |

As the linear operator has only constant coefficients and the boundary conditions do not depend on , the solution is independent of Therefore, in this case we get:

Definition 1.

The leading order term satisfies the following nonlinear PDE

| (17) |

with the boundary conditions

| (18) |

It can be seen (and also shown later) that the zeroth order term actually corresponds to the value function of our investor problem which arises in the case of a constant volatility and growth rate lognormal asset price market model, with constant Sharpe ratio . Due to the presence of boundary conditions, an explicit formula for is inaccessible, even for a power utility function, and we estimate the quantity through numerical techniques. This is explained in detail in Section 4.

Assumption 2.

In the unconstrained case, with no drawdown restrictions, the PDE (17) is simply the constant Sharpe ratio Merton value function PDE on the half-space , where would denote the wealth level. As is well-known, given a smooth and strictly concave utility function satisfying the usual conditions ( and ), smoothness of the value function follows from Legendre transform to a linear parabolic PDE. In our restricted drawdown problem we assume regularity of the solution when restricted to a finite domain. Our value function approximation, summarized in Section 3.2.2, and our optimal portfolio approximation in Section 3.3, are given in terms of (up to th order) partial derivatives of .

In order to find the first order correction term, we introduce the following risk tolerance function

| (19) |

This function has been well studied in the unconstrained case by Källblad and Zariphopoulou [10] and has been recently used to study the classical Merton problem in a stochastic volatility environment by Fouque et al. [8]. It satisfies an autonomous PDE of fast-diffusion type:

Proposition 1.

The risk tolerance function satisfies the nonlinear PDE

| (20) |

with the boundary conditions

| (21) |

The proof is given in Appendix A.2.

As we show later in Section 3.3, Proposition 1 is also crucial to compute the leading order terms in the approximation of optimal strategy Next, we define the differential operators

| (22) |

which allows us to write equation (17) as

| (23) |

Next, we collect the first order terms w.r.t. in the expansion (12). As does not depend on , the linear term contributes

and the nonlinear term contributes

Definition 2.

The first order correction term satisfies the following PDE

| (24) |

with linear operator given as

| (25) |

and the source term

The terminal and boundary conditions (13) for are already satisfied by , and so we have

| (26) |

In Section 3.2.1, we show that can be expressed in terms of partial derivatives of and

3.2.1 Explicit expression for first order correction term

We now employ a transformation that enables us to find an explicit expression for in terms of partial derivatives of . For this purpose, we first note that is a monotone function from the following result on the zeroth order term.

Lemma 1.

is a non-decreasing and concave function in the variable.

The proof is given in Appendix A.1. This result allows us to define a change of variable which is given as:

Definition 3.

On , define,

and let

It is clear from the boundary condition (18) that we have Then, we obtain the following PDE problem for .

Proposition 2.

satisfies the following linear PDE

and the terminal and boundary conditions are

The proof is given in Appendix A.3.

Lemma 2.

Denote Then, on we have

where

| (27) |

The above result follows from the calculations performed in the proof of Proposition 2 (also see [12, Lemma 3.3]).

Next, we set and in Lemma 2. Further we know that does not depend on and and the last two terms in have derivatives w.r.t. Then, we get the constant coefficient heat equation by applying the operator as in Proposition 2. On , we have

Finally, we define from as

| (28) |

Proposition 3.

The alternative representation of the first order correction term satisfies

| (29) |

where

| (30) |

The boundary conditions are

| (31) |

The above result follows from Definition 2. The solution to (29) with boundary conditions (31) is given in terms of derivatives of in the following proposition.

Proposition 4.

The proof is given in Appendix A.4.

3.2.2 Summary of the first order value function approximation results

3.3 Optimal strategy approximation

Once we have the estimates for and in the approximate expansion (10) of the value function , we can find the first order approximation of the optimal strategy from the formula in (2). In terms of the optimal strategy is given by

To express the approximation for in terms of and their spatial derivatives, we first replace by in the above formula, use the results in (33) and the following Lemma.

Lemma 3.

From the definition (19) of , we have the following identities:

Proof.

(i) We have,

The above result and the distributive property of operator completes the proof.

(ii) We have,

This gives,

The final conclusion follows from (i).

(iii) Using the previous calculations, we get

The sum of above two results concludes the proof. ∎

Thus, we obtain the optimal strategy approximation as

| (34) | ||||

| (35) |

4 Examples and Numerical Implementation

In this section, we consider the stochastic volatility model as in Chacko and Viceira [1] with their calibrated set of parameters and provide a detailed discussion of the numerical implementation of our results obtained in Section 3. We discuss the effect of stochastic volatility on value function and optimal strategy for the case of power utility function and a mixture of two power utility functions, as introduced in [8]. The latter allows for relative aversion that declines with wealth, while for the former it is constant across wealth levels.

Under the considered stochastic volatility model [1, Section 1], the coefficients in Section 2 are independent of and are given as

The market calibrated values of the constants are

| 0.0811 | 0.3374 | 27.9345 | 0.6503 | 0.5241 |

We numerically solve for backward in time via explicit finite-difference Euler scheme. We approximate the domain with a uniform mesh given as

where Let denote the numerical approximation of . Then the discretized equation for in the interior is written as

| (36) |

We start with the guess , and the boundary conditions are

| (37) |

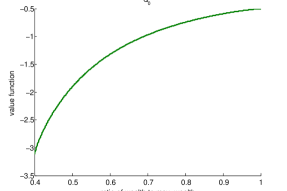

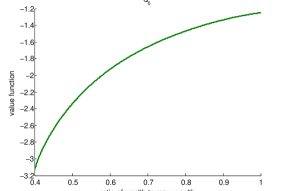

In Figure 1 and 2, we plot the numerical solution for the leading order expansion term obtained from (36). We can see that the zeroth order term is concave and non-decreasing as expected from Lemma 1.

To find the first order correction term, we refer to formula (33). We can directly use from Proposition 1 in the formula instead of taking derivatives of We note that to obtain , we need to set the value for reference level We set the current value of the stochastic volatility factor. This gives us

| (38) | ||||

| (39) |

We use the regularity properties of and to compute the above expression. We obtain estimates of by numerically solving (20) with boundary conditions (21) via explicit finite-difference Euler scheme. The discretized equation in the interior is written as

| (40) |

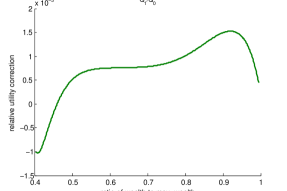

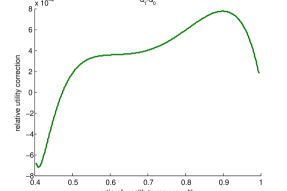

and the boundary conditions , and . As we solve the scheme backward in time, we start with the guess In our market calibrated stochastic volatility model, we set and plot the relative utility correction in Figure 1 and Figure 2. We observe that the change in the value function due to the introduction of stochastic volatility is negligible.

Next, we calculate the approximation to optimal strategy whose different terms are given from (3.3) as

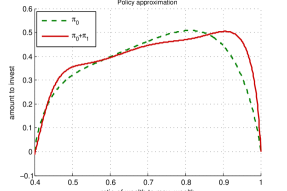

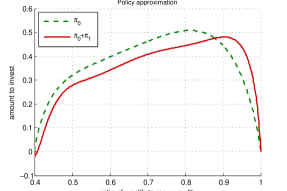

We suppose that the initial value of maximum wealth is unity, i.e. we set and plot numerical solution to the leading order term and to the first order approximation in Figure 3 and 3. It is interesting to note that to achieve similar value functions without and with the stochastic volatility correction, i.e. and we clearly need to employ two very different investment policies, namely and

In Figure 3 and 3, we note that as the current wealth approaches to the maximum wealth value, the optimal strategy is to gradually liquidate the position in the risky asset. In the presence of stochastic volatility, the optimal strategy approximation suggests to hold the risky position longer than without the stochastic volatility correction as in The corrected strategy also suggests to sharply liquidate the position in the risky asset to safeguard from the downside risk of stochastic volatility. On the other hand, when the current wealth moves away from the drawdown barrier, the optimal strategy approximation suggests to build up a position in the risky asset at about the same trading rate to that in the case of constant volatility approximation

From the above results, we deduce that even in the presence of stochastic volatility, the investor does not lose much value in his portfolio. However, to achieve similar value functions, the investor has to deploy a remarkably different strategy corrected for stochastic volatility when compared to the constant volatility strategy The larger position in the risky asset when moving away from the drawdown barrier suggests leveraging the possible upside due to stochastic volatility while holding on to the risky asset longer than in the constant volatility case when close to the optimal level suggests caution towards a possible downside risk.

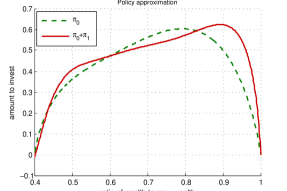

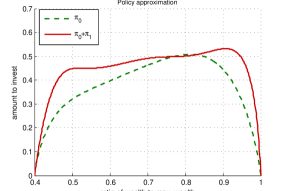

In the above results, we have set the level of stochastic volatility factor to be the same as the long term value As it is clear that the level of stochastic volatility plays a crucial role in the correction terms, we studied the effects when moves in either direction away from its long term value We observed that even in these new cases, the relative utility correction remains small. However, the optimal strategy in these cases exhibit remarkably different behaviors. When the current level of volatility is higher than the long-term average , in Figure 4 the optimal strategy approximation suggests to invest more in the risky asset compared to the strategy without stochastic volatility correction. Also, as the portfolio wealth moves away the drawdown barrier, the corrected optimal strategy suggests to build up the position in risky asset at a much higher rate than suggested by Whereas, in the case when the current level of volatility is lower than the long-term average , in Figure 4 the optimal strategy approximation suggests to invest less in the risky asset compared to the strategy without stochastic volatility correction. Still close to the maximum wealth value, the corrected strategy suggests to hold more risky asset than the constant volatility strategy suggests.

5 Conclusion

We studied the impact of stochastic Sharpe ratio in a dynamic portfolio optimization problem under a drawdown constraint. We proposed a new investor objective framework which allows for a dimensionality reducing transformation. This new setting allowed us to employ coefficient expansion technique to solve for different terms in the approximation of the value function and optimal strategy. With the help of a nonlinear transformation we derived value function expansion terms which can be numerically calculated and used to approximate the optimal portfolio strategy. In a popular stochastic volatility model with market calibrated parameters, we illustrated the remarkable differences between optimal strategies with and without stochastic volatility correction.

The current problem requires further investigation which can be performed along the following directions:

-

1.

Approximation error analysis: In this work, we focussed our attention to capture the first order effects of stochastic volatility on value function and optimal portfolio strategy. We observed that the stochastic volatility correction to value function is small whereas the corrected optimal strategy exhibited remarkably different behavior than the constant volatility optimal strategy. This calls for an investigation of the higher order terms to look for possible other interesting effects on the optimal strategy.

-

2.

Multi-asset market model: We studied the portfolio optimization problem under drawdown constraint in a stochastic volatility model which provides a sensible guide towards informed investment decisions. However, in order to completely capture the market conditions, we plan to tackle the same problem in a multi-asset model setting and study the effect of stochastic volatility on investment strategies.

Appendix A Proofs

A.1 Proof of Lemma 1

Proof.

Let us consider a market with a risky asset whose dynamics is given by a lognormal model

With this risky asset in the market, we once again formulate our investor’s portfolio optimization problem (see Section 2.1)

where the admissible strategies are given by

and is the augmentation of the filtration generated by We define the constant Sharpe ratio as and the space domain as Then, by proceeding as in Section 2.1, it can be shown that for we have the following nonlinear PDE

and the boundary conditions are

Similar to Section 2.2, we perform a change of variable It is then clear that the leading order term in expansion (10),

To first show that is a non-decreasing function, we recall that in the constant volatility model, for a portfolio strategy the discounted wealth process is given as

where is the starting wealth value. Let denote the maximum of wealth process over the time period Now, we consider for a fixed value of such that Then, for we choose such that we have

| (41) | ||||

| (42) |

Add to both sides of the inequality above to write

which gives that Thus, we get For and this gives us

Next, it follows from the arguments presented in Lemma 3.2 Elie [6] that is non-increasing in variable Thus, for fixed and such that we have Once again by defining and we get

Therefore, we have shown that is non-decreasing.

In order to show concavity of value function we take motivation from the arguments presented in Lemma 3.2 Elie [6]. First, we fix and choose Our aim is to show that is concave in its second argument, i.e.

| (43) |

where for a fixed value of we set and Now, suppose (43) is true. Then by reversing the change of variables, we get in (43)

which gives us concavity of It remains to show that (43) is indeed true.

We define process as the wealth process with starting wealth and portfolio strategy Similarly, we define the process with starting wealth and portfolio strategy Then, we have by definition

This gives us that From concavity property of utility function , it follows

Next, we intend to show that

| (44) |

Consider the following possible scenarios where we compare the respective terms with and find the maximum

| Case 1 | |||

|---|---|---|---|

| Case 2 | |||

| Case 3 | |||

| Case 4 | – |

It is clear that the inequality in (44) holds for Case 1–3 and we only need to consider Case 4. We know from the optimality condition that for strategies and which attain the maximum, the position in the risky asset becomes zero thereafter as the maximum possible utility is achieved. It follows that for such strategies, we have

Then, we get

due to

Thus, we have shown that (44) is indeed true. This gives us

As, are arbitrary, we have have shown (43). This concludes the proof for concavity of ∎

A.2 Proof of Proposition 1

Proof.

From the calculations performed in the proof of Proposition 2, we know that

| (45) |

Differentiating (19) w.r.t. gives

| (46) |

Differentiating (45) w.r.t. we get

Plugging back the above result and (45) into (46) gives the PDE for The terminal condition at is straightforward from the terminal condition for At the boundary, which due to the continuity of across the boundary gives that Then, due to the continuity of derivatives w.r.t. space variables across the boundary, from (17) we get at

As it gives that

We know from our calculations in the proof of Lemma 1 and Section 3.3 that the optimal strategy corresponding to the value function is given as It is clear that as the portfolio wealth approaches to its maximum value, i.e. at the optimal strategy suggests to unwind the risky position, This give us the right boundary condition for as ∎

A.3 Proof of Proposition 2

Proof.

In the definition we differentiate w.r.t. on both sides to write

It is also straightforward to check from definition (22) of differential operators that

| (47) |

Next, we observe that PDE (23) can also be written as Differentiating this w.r.t. we get

Further, from the definition of we get which after differentiating w.r.t. gives

Thus, we have

Finally, we collect all the expressions for and in terms of to write

which gives us the desired PDE.

For the terminal boundary condition for it follows from the definition of and terminal condition (18) that

The left boundary condition in (18) can also be easily transformed. Next, for the right boundary condition in (18), we first note that

Now, as , it holds only if in the above relation we have

This completes the proof. ∎

A.4 Proof of Proposition 4

We first consider the PDE problem with a terminal condition

| (48) |

where is a constant coefficient linear operator

We suppose that the source term is of the following special form

| (49) |

where the sum has a finite number of terms, and is a solution of the homogeneous equation .

Further, define the commutator of operators and ( is the identity operator), as

which from the definition of (15) and (27) gives

| (50) |

Similarly, define , which gives

| (51) |

Using and we also define

Using these definitions, we first give the following result related to the homogeneous solution , from [12, Lemma 3.4]. Here, we provide the proof for the sake of completeness.

Lemma 4.

For integers we have,

Proof.

We proceed by induction. We first calculate

where we have used the definition of the commutator the fact that and commute as they are constant coefficient operators and that Thus, we can then iterate over integer to show Similarly, we can show that for integer Finally, we have ∎

Lemma 5.

The solution of equation (48) with zero terminal condition is

| (52) |

Proof.

This can be shown by using the form of source term (49) and Lemma 4. Let us suppose that the source term consists of a monomial and is given as In this case, from our claim, the solution should be given as

We verify by computing

It is also easy to see that for the form of solution proposed in (52), the terminal condition at is satisfied. The result follows from linearity of the PDE problem. ∎

Finally, we give the proof of Proposition 4.

Proof.

We first observe that, since solves , then also solves the homogeneous equation, as the operator has constant coefficients. We set . From (30), the source term is

and so from Lemma 5, we obtain the solution

| (53) | ||||

| (54) |

From the expansion for we get

Putting back the expression of and from (50) and (51) into (54), we get the expression in (32). The terminal condition at is clearly satisfied.

It remains to check the boundary conditions for . We show that the boundary conditions for , corresponding to the original variables , are satisfied. Using (28) and (47), we obtain (33). Now, due to the zero boundary condition at for the risk-tolerance function we get from (33) that , which means that the left boundary condition in (26) is satisfied. Consequently, the left boundary condition in (31) is satisfied for

Next, we calculate

| (55) |

From our Assumption 2 on the boundedness of for , we have

Then, we can use the boundary condition of and at to conclude from (A.4) that

which means that the right boundary condition in (26) is satisfied. This implies that the right boundary condition in (31) is satisfied for . ∎

References

- Chacko and Viceira [2005] G. Chacko and L. M. Viceira. Dynamic consumption and portfolio choice with stochastic volatility in incomplete markets. Review of Financial Studies, 18(4):1369–1402, 2005.

- Chekhlov et al. [2005] A. Chekhlov, S. Uryasev, and M. Zabarankin. Drawdown measure in portfolio optimization. International Journal of Theoretical and Applied Finance, 8(01):13–58, 2005.

- Chen et al. [2015] X. Chen, D. Landriault, B. Li, and D. Li. On minimizing drawdown risks of lifetime investments. Insurance: Mathematics and Economics, 65:46–54, 2015.

- Cherny and Obłój [2013] V. Cherny and J. Obłój. Portfolio optimisation under non-linear drawdown constraints in a semimartingale financial model. Finance and Stochastics, 17(4):771–800, 2013.

- Cvitanic and Karatzas [1995] J. Cvitanic and I. Karatzas. On portfolio optimization under "drawdown" constraints. IMA Volumes in Mathematics and its Applications, 65:35–35, 1995.

- Elie [2008] R. Elie. Finite time merton strategy under drawdown constraint: a viscosity solution approach. Applied Mathematics and Optimization, 58(3):411–431, 2008.

- Elie and Touzi [2008] R. Elie and N. Touzi. Optimal lifetime consumption and investment under a drawdown constraint. Finance and Stochastics, 12(3):299–330, 2008.

- Fouque et al. [2015] J.-P. Fouque, R. Sircar, and T. Zariphopoulou. Portfolio optimization and stochastic volatility asymptotics. Mathematical Finance, 2015.

- Grossman and Zhou [1993] S. J. Grossman and Z. Zhou. Optimal investment strategies for controlling drawdowns. Mathematical Finance, 3(3):241–276, 1993.

- Källblad and Zariphopoulou [2014] S. Källblad and T. Zariphopoulou. Qualitative analysis of optimal investment strategies in log-normal markets. Available at SSRN 2373587, 2014.

- Karatzas et al. [1987] I. Karatzas, J. P. Lehoczky, and S. E. Shreve. Optimal portfolio and consumption decisions for a "small investor" on a finite horizon. SIAM Journal on Control and Optimization, 25(6):1557–1586, 1987.

- Lorig and Sircar [2016] M. Lorig and R. Sircar. Portfolio optimization under local-stochastic volatility: Coefficient taylor series approximations & implied sharpe ratio. SIAM J. Financial Mathematics, 7:418–447, 2016.

- Lorig et al. [2015] M. Lorig, S. Pagliarani, and A. Pascucci. Explicit implied volatilities for multifactor local-stochastic volatility models. Mathematical Finance, 2015. ISSN 1467-9965.

- Magdon-Ismail and Atiya [2004] M. Magdon-Ismail and A. F. Atiya. Maximum drawdown. Risk Magazine, 17(10):99–102, 2004.

- Merton [1969] R. C. Merton. Lifetime portfolio selection under uncertainty: The continuous-time case. The Review of Economics and Statistics, pages 247–257, 1969.

- Merton [1971] R. C. Merton. Optimum consumption and portfolio rules in a continuous-time model. Journal of Economic Theory, 3(4):373–413, 1971.

- Pham [2009] H. Pham. Continuous-time stochastic control and optimization with financial applications, volume 61. Springer Science & Business Media, 2009.

- Roche [2006] H. Roche. Optimal consumption and investment strategies under wealth ratcheting. Preprint, 2006. URL http://ciep.itam.mx/~hroche/Research/MDCRESFinal.pdf.

- Rogers [2013] L. C. Rogers. Optimal investment. Springer, 2013.

- Samuelson [1969] P. A. Samuelson. Lifetime portfolio selection by dynamic stochastic programming. The Review of Economics and Statistics, pages 239–246, 1969.

- Sekine [2013] J. Sekine. Long-term optimal investment with a generalized drawdown constraint. SIAM Journal on Financial Mathematics, 4(1):452–473, 2013.