Estimation of multiple change points under a generalised Ornstein-Uhlenbeck framework

Abstract

The use of an Ornstein-Uhlenbeck (OU) process is ubiquitous in business, economics and finance to capture various price processes and evolution of economic indicators exhibiting mean-reverting properties. When structural changes happen, econo mic dynamics drastically change and the times at which these occur are of particular interest to policy makers, investors and financial product providers. This paper addresses the change-point problem under a generalised OU model and investigates the associated statistical inference. We propose two estimation methods to locate multiple change points and show the asymptotic properties of the estimators. An informational approach is employed in detecting the change points, and the consistency of our methods is also theoretically demonstrated. Estimation is considered under the setting where both the number and location of change points are unknown. Three computing algorithms are further developed for implementation. The practical applicability of our methods is illustrated using simulated and observed financial market data.

keywords:

Ornstein-Uhlenbeck process , sequential analysis , least sum of squared errors , maximum likelihood , consistent estimator , segment neighbourhood search method , PELT algorithm1 Introduction

We examine the change-point detection problem on the drift parameters of a generalised version of the Ornstein-Uhlenbeck (OU) process introduced in Dehling, et al. (2010); see also Dehling, et al. (2014) and Zhang (2015). Such a process is a solution to the stochastic differential equation (SDE)

| (1.1) |

where , ,

and denotes the transpose of a matrix. Here, is a one-dimensional standard Brownian motion defined on some probability space In particular, if then (1.1) is the SDE of the classical OU process, which is

commonly used to model the stochastic dynamics of various financial variables.

Many economic indicators, prices in the financial market as well as processes in the natural and physical sciences and engineering are captured sufficiently by the OU model. The classical work of Vasicek

(1977) employs an OU model for bond valuation. The importance of

this stochastic process is also demonstrated by its ubiquity in many fields.

For instance, the OU process is used in mathematical models of the electricity market (e.g., Erlwein, et al. (2010)), commodity futures market

(e.g., Date, et al. (2010)), weather derivatives (e.g., Elias,

et al. (2014)), central-bank rate setting policy (e.g., Elliott and Wilson (2007)), spreads between pairs of securities (e.g., Elliott (2005)),

stochastic control-driven insurance problems (e.g., Liang, et al. (2011)),

spot freight rates in the shipping industry (e.g., Benth, et al. (2015)), risk management (e.g.,

Date and Bustreo (2015), and power generation (e.g., Howell, et al. (2011)).

In the OU-modelling context, Tenyakov, et al. (2016) proposed a

signal processing-based approach to determine presence of market liquidity regimes.

Various applications of the OU process are also highlighted in biology (e.g., Rohlfs, et al. (2010)),

neurology (e.g., Shinomoto, et al. (1999)), survival analysis (e.g., Aalen and Gjessing (2004)),

physics (e.g., Lanský and Sacerdote (2001)), and chemistry (e.g., Lu (2003) and (2004)).

We note that the mean-reverting level of an OU process is constant, which can be a notable weakness for many financial datasets. This

may be rectified by introducing a generalised OU process where a time-dependent function

describes its level of mean reversion. Such a generalised version

incorporates time-inhomogeneity and seasonality of mean reversion simultaneously.

Dehling, et al. (2014) developed the framework to study a change-point phenomenon under

the generalised OU process. This allows the model to capture drastic changes at certain time points (e.g., drastic-moving interest rates

due to the outbreaks of financial crisis or war).

In practice, many data series are characterised by some potential changes

in their evolution structure, i.e., a sudden change in mean or variance and other model parameters.

It is then of interest to determine the (i) existence

and (ii) location of the change point. This implies segregating the data series

into different segments and analysing them in a less efficient but more accurate way.

Thus, our research contributions

support and complement the objective of papers employing regime-switching OU-process

as we provide a methodology to verify the switching phenomenon in the data.

We go further by precisely estimating where the switch occurred

and how many switches are possible given a data set. An instance of this

support and complementarity are depicted in Subsection 3.1 of Tenyakov, et al. (2016),

where a simple statistical testing of regime-switching in the data was performed.

Pioneering contributions to this field of change-point detection

were spearheaded by

Page (1954) and Shiryaev (1963). Advances in recent years

have tackled the (i) estimation of change points and coefficients

of linear regression models with multiple change points (Bai and Perron (1998);

Perron and Qu (2006); Lu and Lund (2007), Gombay (2010), and Chen and Nkurunziza (2015)); (ii) change-point

testing for the drift parameters of a periodic mean-reverting process (cf. Dehling,

et al. (2014)); (iii) applications in finance

(cf. Spokoiny (2009)); (iv) detection of malware within software

(Yan, et al. (2008)); (v) climatology (Reeves, et al. (2007), Robbins, et al. (2011), Gallagher et al. (2012));

and epidemiology (Yu, et al. (2013)).

The analysis of change points could be described more generally as a

hypothesis-testing problem for the existence of change points in various

locations. This could be viewed, from another perspective, as a model selection problem

where the change points are additional unknown parameters to be estimated.

The change-point problems

are typically examined depending on two alternatives: (i) the number of change points is known but their exact

locations are unknown (Perron and Qu (2006) and Chen and Nkurunziza (2015)) and

(ii) both the number and the exact locations

of the change points are unknown. The estimation methods under the first scenario only require

the identification of the exact locations of the change points. It is easier for the first alternative than for the second. Closed-form solutions

for the direct calculation of the change point are usually not available.

Current change-point estimation approaches are

normally constructed to perform a search at every possible location of

unknown candidate change points via some efficient computational algorithms

subject to some constraint or criteria.

Examples of well-known algorithms for

change point detection include: (i) the binary segmentation type algorithm

(Scott and Knott, (1974); Sen and Shrivastava, (1975)),

(ii) the segment-neighbourhood type algorithm (Auger and Lawrence, (1989);

Bai and Perron, (1998)) with adaption to the restricted regression

model (Perron and Qu, (2006)); and (iii) the optimal partitioning type algorithm (Jackson et al., (2005)) and its pruned version, PELT method by Killick, et al. (2012). Further details of these algorithms

can be found in Killick, et al. (2012) and Maidstone, et al., (2014).

The intents of our work are motivated by

two major research results. The first motivation is from Dehling, et al. (2010) that derives

a maximum likelihood estimator (MLE) for the drift parameters of the diffusion

process and establishes its asymptotic properties. This was extended in

Dehling, et al. (2014), where

there is one unknown change point and a likelihood-ratio test statistic was

constructed to

determine such change point. The second motivation is from

Zhang (2015) that establishes the asymptotic properties of both the unrestricted and restricted MLE for

the drift parameters of the generalised OU process with a single change point.

A James-Stein-type shrinkage estimator

for the drift parameters is proposed in Zhang (2015) as an improvement

and it is also shown that the previously established asymptotic properties also hold for any consistent

estimator for the rate of the change point.

Neither Dehling, et al. (2014) nor Zhang (2015) offer a specific methodology to identify the change point.

This led us to the three main contributions of this paper.

First, we extend the single-change point framework to the multiple-change point setting and present two consistent methods to estimate the unknown locations of change points.

Second, we prove the asymptotic normality of the drift parameters’ MLE.

Third, we employ information-based statistics to resolve the issue

of estimating the unknown number of change points and then created three

algorithms to implement the calculations. We validate

the performance of our estimation techniques using simulated and

real market data.

This paper is structured as follows.

In Section 2, we present the formulation of the multiple change-point problem.

Section 3 summarises the

results of Dehling, et al. (2014) and Zhang (2015)

on MLE and the related asymptotic properties, which provide an

impetus on the asymptotic performance of our proposed methods.

Two estimation methods are put forward to determine

the unknown locations of change

points in section 4 along with the discussion of the asymptotic properties of the estimators;

we find that

the asymptotic properties obtained in

in Zhang (2015) also hold in our proposed techniques.

Section 5 deals with

the problem of both the existence issue and location of the change points

using an information approach. We develop

computing algorithms in section 6 in order to implement the

proposed methods. In section 7, we assess the

applicability of our methods through numerical examples

on simulated and observed financial

market data. Finally, section 8 provides some concluding remarks.

2 Problem description in determining change points

We study the generalised version of the OU process with SDE representation given in (1.1). It is assumed that there exist () unknown change points , where and . To simplify the notation, we let and . In our setup with for and

| (2.1) |

with as the indicator function. Note that may also be a vector.

We start by assuming that the number of change points is known, but the exact value of each change point denoted by (and correspondingly the exact rates , ) are unknown. Furthermore, considering that we have multiple change points in the model, we posit that these change points are asymptotically distinct. We further impose the following assumptions.

Assumption 1.

, . We call the change points’ arrival rate, and if we have , the value is immediate.

Assumption 1 implies that the length of each regime is proportional to . The structure of the model in each regime is similar to that of the no-change point process studied in Dehling et. al (2010); see also Zhang (2015) for the case of a single change point. This means that the results established in the existing literature could also be adapted to the case of multiple change points.

MLEs

for the drift parameters and their asymptotic properties were shown

in Dehling, et al. (2010) for the case of no change point and

in Zhang (2015) for the case of one change point. Certainly, Zhang (2015)

is a special case of our study with

with . The next section reviews previous results and extends them

to the multiple change points problem.

3 Prior MLE-based results and our extension

The asymptotic normality for the MLE estimator of the drift parameters

in Zhang (2015) assumes that the estimator is already consistent. In our case,

we shall prove (rather than simply assume) that such an estimator of the change point is consistent.

In the subsequent discussion, we write “”, , and to mean convergence in probability, convergence in distribution, and convergence almost surely, respectively. The notation denotes the Frobenius norm for matrices. We use bold, unitalicised English or Greek letters in lowercase for vectors; and bold, unitalicised English or Greek letters in upper case for matrices.

The “” denotes the Landau symbol, also known as the “Big O” notation, which is used to describe the asymptotic behaviour of functions. So, for a set of random variables and a corresponding set of constants

, means is stochastically bounded. Formally, this means

On the other hand, the symbol involving “small o”, i.e., means converges in probability to zero as approaches an appropriate limit. So, since is equivalent to ,

convergence in probability is here defined as

3.1 Log likelihood function

The following assumption from Dehling, et. al. (2010) is also retained here.

Assumption 2.

, for all and elements of involved in given by equation (2.1).

3.2 Maximum likelihood estimators for the draft parameters

By setting the first partial derivatives with respect to each of the parameters of to 0, we obtain the MLE of the drift parameters, provided is invertible for each . When exists, Remark 3 of Dehling, et al. (2010) shows that must exist almost surely if is large enough. Moreover, Proposition 2.1.1. of Zhang (2015) is also adapted to give the positive definiteness of under the following assumption.

Assumption 3.

For any , the base function is Riemann-integrable on and satisfies two properties.

-

1.

Periodicity. That is, and is the period observed in the data.

-

2.

Orthogonality. That is, , is equal to if and 0 otherwise.

By Assumption 3, is bounded on (i.e. for some ) as for every the base function is bounded on and -periodic. The following result is obtained by reducing the time period from to , and utilising the same arguments as in Proposition 2.1.1 of Zhang (2015).

Proposition 3.1.

For the rest of this paper, we assume that the sample

size is an integral multiple of the period length ,

i.e., for some integer . Without loss of generality,

we let , implies that .

Using the results in Dehling, et. al (2010) and Zhang (2015), the MLE of the drift parameters based on the log likelihood function provided above are given by with

| (3.1) |

Substituting (1.1) into (4.5) and going through some algebraic computations will lead to

| (3.2) |

where for .

3.3 Asymptotic properties of the MLE

To study the asymptotic proprieties of the MLE in the next section, equation (4.5) to be precise, we review the established asymptotic results in Dehling, et al. (2010) for the case where there is no change point () and also the results in Zhang (2015) when there exists one change point ().

If there is no change point ( and for ), the solution of the SDE (1.1) has the explicit representation

| (3.3) |

where

and

Note that as the process is not stationary in the ordinary sense, it is impossible to apply the ergodic theorem directly. To circumvent this, a stationary solution, for instead of , was introduced in Dehling, et al. (2010). Consider

| (3.4) |

where , and denotes a bilateral Brownian motion, i.e.,

where and are two independent standard Brownian motions. Then, from Lemma 4.3 in Dehling, et al. (2010), the sequence of -valued random variables , , is stationary and ergodic. In this case, by Proposition 4.5 of Dehling, et al. (2010),

| (3.5) |

Moreover, under Assumptions 1-3, Lemma 4.4 in Dehling, et al. (2010),

| (3.6) |

Using (3.6), we have the following properties:

It follows from (3.5) that

Hence,

| (3.7) |

where

with and .

Furthermore, under Assumptions 1–3, the following properties for hold.

-

1.

is a martingale.

-

2.

.

-

3.

.

Detailed proofs of the above are elaborated in Zhang (2015). The above properties, together with Slutsky’s Theorem, yields

Zhang (2015) extended the above asymptotic properties to the case of a single change point. Using similar arguments, we extend these results in the context of multiple change points. We first present a result covering the coefficients of SDE (1.1).

Proposition 3.2.

Proof: See Appendix A.

Using Proposition 3.2 and similar methods employed for the proof of Proposition 2.2.1 in Zhang (2015), it may be verified that SDE (1.1) admits a strong and unique solution that is uniformly bounded in and

| (3.8) |

for some .

Employing (3.8), we (3.3) and (3.4) to their representations in context of multiple change points () given by

| (3.9) |

where and

| (3.10) |

Then

| (3.11) |

and

| (3.12) |

Using (3.6) and (3.8) and similar arguments in the proof of Propositions 2.2.2 and 2.2.3 in Zhang (2015), the following properties hold:

Thus,

So,

| (3.13) |

where

| (3.14) |

with and , . Further, by the Continuous Mapping Theorem,

| (3.15) |

So long as Assumptions 1–3 hold and with the aid of similar argument used in the proof of Proposition 2.2.6 in Zhang (2015), it may be shown that is positive definite.

Note that (3.13) and (3.15) are key elements in analysing the asymptotic properties of and its inverse, where is the estimator of .

Invoking the boundedness property of , we have

| (3.16) |

for and . Similarly, using (3.8),

| (3.17) |

From Proposition 1.21 in Kutoyants (2004) (see also Proposition 2.2.10 in Zhang, 2015), we get

| (3.18) |

where is a vector of zeros and . Combining (3.13), (3.15) and (3.18), along with Slutsky’s Theorem and some algebraic computations,

| (3.19) |

where .

The above asymptotic properties are established based on the exact values of the locations of the change points , . However, in practice, are often unknown. Hence, we shall devise

methods to estimate the unknown and investigate whether the above asymptotic normality still hold for the estimated change points.

4 Estimation of change points and pertinent asymptotic properties

In Subsections 4.1 and 4.2, we develop two techniques to estimate the unknown locations of change points. The asymptotic normality of based on the estimated change points is discussed in Subsection 4.3.

4.1 Least sum squared error method

We introduce the least sum of squared errors (LSSE) method then investigate the consistency

of our proposed estimator. Consider a partition on a time period with constant increment . Also, let and .

Due to the uncertain locations of estimated change points, the exact value of the drift parameters and the MLE may have different indices. For example, if , then for all , the associated exact value of the drift parameters is but the MLE is . So here, and refer to the exact value and MLE of the drift parameters at time point , respectively. In this case, and with

for . Then by the Euler-Maruyama discretisation method,

| (4.1) |

where is the error term , and is

the standard normal term. Therefore, we could now use the LSSE method to

estimate the change points.

From (4.1), the estimates for the multiple change points are given by

| (4.2) |

where

| (4.3) |

Consistency of the proposed estimator

Under Assumptions 1–3, for , the discretised versions of are both positive definite with probability 1 provided that the base

functions are incomplete. Moreover, using (3.13) (see also Proposition 2.2.6 of Zhang (2015)), one can show that converges in probability to some positive definite matrices for large , as do their respective discretised versions. Hence, for large , it is reasonable to impose a useful assumption in proving the consistency of the estimators of the change points.

Assumption 4.

For every , there exists an such that for all the minimum eigenvalues of and of , as well as their respective continuous-time versions and , are all bounded away from 0.

For the motivation of the above assumption, see Perron and Qu (2006) and Chen and Nkurunziza (2015). The next two propositions provide results characterising consistency.

Proposition 4.1.

Proof: See Appendix B.

Proposition 4.2.

Suppose the conditions in Proposition 4.1 hold. Then, for every , there exists a such that for large , , for every .

Proof: See Appendix B.

Proposition 4.1 shows that the estimated rate is consistent for , for . Proposition 4.2 gives the convergence rate of , . In reality we may encounter the case where the shift is time-dependent, and, in particular as tends to infinity, the shift may shrink towards 0 at rate , i.e., , where is independent of and . In this case, the validity of Propositions 4.1 and 4.2 depends on the speed . In fact, using similar arguments as in the proofs of these two propositions (see Appendix B), we have the following corollary.

Corollary 4.1.

Suppose that , where , is independent of and but for some . Then under Assumptions 1–4, we have (i) and (ii) for every , there exists a such that for large , .

Proof: See Appendix B.

4.2 Maximum log-likelihood method

We introduce an alternative method to estimate the location of the change points based on the maximum of log-likelihood function. Recall that the log-likelihood function for (1.1) with the exact change points is given by

| (4.4) | |||||

From (4.4), the estimator of the location of the change points is given

| (4.5) |

where is the MLE of based on the given change points .

In practice, the calculation of in (4.5) relies on numerical approximation methods (see Auger and Lawrence (1989)) to compute the integrals inside . For example, by approximating the Riemann sum based on a partition with , (4.5) is calculated as

| (4.6) |

The approximated version of (4.5) is then

| (4.7) |

Consistency of the proposed estimator

We now link results (4.7) and (4.2), which are

the respective results from the LSSE- and MLE-based methods.

Proposition 4.3.

Proof: See Appendix B.

Using the consistency properties, we can establish the asymptotic normality for the MLE of drift parameters based on the estimated change points.

4.3 Asymptotic normality of based on the estimated change points

Previously, we established the T-rate consistency of the estimated change points. Based on these asymptotic consistency results, we extend the asymptotic normality results in Zhang (2015) to the case of multiple change points.

Proposition 4.4.

Proof: See Appendix C.

Proposition 4.5.

Under the same conditions as in Proposition 4.4, we have that for ,

| (4.10) |

Proof: This follows from (3.8) and the similar arguments in the proof of Proposition 2.3.5 in Zhang (2015).

Employing Propositions 4.4 and 4.5, we have the following results.

Proposition 4.6.

| (4.11) |

where is defined in (3.14).

Proof: See Appendix C.

Proposition 4.7.

Proof: See Appendix C.

The next result following from Propositions 4.6 and 4.7 plays an essential role in proving the asymptotic normality of MLE of the drift paramter based on the proposed estimated change points.

Proposition 4.8.

Proof: See Appendix C.

From Proposition 4.8 together with Slutsky’s Theorem, the following corollary establishes the asymptotic normality for .

Corollary 4.2.

Proof: See Appendix C.

5 Estimating the number of change points

In the last section, we developed two consistent estimation methods for the case when

the number of change points is known. In this section, we extend our examination of the change-point

problem when the number of change points is also unknown. Hence,

we are interested in knowing the number of change points as well as their exact locations.

One popular methodology for detecting the

unknown number of change points is to treat this issue as a model-selection problem.

For instance, adding one change point into (1.1) brings extra drift parameters into the model. Thus, detecting the number of change points can be considered as selecting the most suitable statistical model from a series of candidate models with different number of change points, and this can be solved using an informational approach. Such approach deems the most appropriate model as the one which minimises the log-likelihood-based information criterion

| (5.1) |

In (5.1), is defined in (4.4);

is obtained via (4.5) corresponding to each ; if there is no

change in (or if there is a change in ); is a non-decreasing

function of , the length of the data set; and is the potential number of change points to

be determined.

Based on the asymptotic results for the Riemann sum approximation of the log-likelihood function , we use the criterion

| (5.2) |

where is given in (4.6).

Note that, if the number of change points is known, the term

is fixed and the approach covering (5.2) is equivalent to the maximum

log-likelihood method introduced in the previous section. The efficiency of

information criterion depends on the choice of the penalty criterion . For example, if ,

then (5.2) reduces to the well-known Akaike information criterion (AIC) [2]. However, in practice, a model selected by minimising the AIC may not

be asymptotically consistent in terms of the model order; see Schwarz (1978).

Modified information criteria were, thus, proposed to overcome this problem. One example is the Schwarz information criterion (SIC) [40], which

sets as the logarithm of the sample size.

The SIC has been

successfully applied to the change-point analysis in the

literature. As it gives an asymptotically consistent estimate

of the order of the true model, we also adapt the SIC for our theoretical development.

Note that the penalty term in SIC increases as the sample size increases. Hence, for large sample size SIC tends to ignore the relatively small changes in the process. This feature makes it useful for those who are mainly interested in studying only the major changes within certain time period. Further, based on the SIC, we have the following asymptotic results for (5.2).

Proposition 5.1.

Under Assumptions 1–4, we have that for large , (i) with probability 1 and (ii) with probability 1.

Proof: See Appendix D.

Proposition 5.1 tells us that, for large T, reaches its minimum value when and this allows us to detect the exact value of .

6 Computing algorithms

In this section, we put forward algorithms for computing (4.2) and (4.7) when is known. We also provide algorithms for computing (5.2) when is unknown. Based on these algorithms, a simulation study to examine the efficiency of the proposed methods for different time periods is presented in Section 7.1. Our numerical results will show that, with our sample parameter set, the proposed methods perform well for values of as small as .

6.1 Algorithm for (4.2) and (4.7) (with known )

In estimating the unknown locations of change points, a standard searching method is to compute the criteria, i.e., least squared errors for (4.2) or maximum log likelihoods for (4.7), through all possible locations of change points and search for the one that returns the optimal value. However, for change points the associated costs for the above searching procedure are of order . Thus, for large and small , the computations can be time consuming. To overcome this problem, we adopt to our two proposed LSSE and MLE methods

a dynamic programming algorithm due to Bai and Perron (2003), see also Perron and Qu (2006),

to reduce the computational cost to for change points. This algorithm is very efficient when .

Algorithm 1

Let be either , the least sum squared error for (4.2) or , the maximum Riemann sum approximation of log likelihood for (4.7)) computed based on the optimal partition of time interval that contains change points. Also, let be the SSE for (4.2) or Riemann sum approximation of log likelihood for (4.7)) computed based on a time regime . Further, we assume that Assumption 1 holds and let be the minimal permissible length of a time regime. Then (4.2) or (4.7) with known can be computed as follows.

-

1.

Compute and save for all time periods that satisfy .

-

2.

Compute and save for all by solving the optimisation problem

-

3.

Sequentially compute and save

for , and .

-

4.

Finally, the estimated change points are obtained by solving

and if .

The steps in Algorithm 1 can be viewed as a combination of two components. Step 1 computes all possible choices of , and the computations in this step are at most of order as there are at most different time periods in the dataset. This step is useful, since in the succeeding steps some pairs of will be visited more than once during the optimisation process, so using previously saved results for will be helpful to reduce computations. Steps 2-4 can be treated as an application of the Segment Neighbourhood Search (SNS) method introduced by Auger and Lawrence (1989). The goal of Steps 2–4 is to search for the global optimal locations of the change points and the total computation costs in these steps are also of . Note that when (a single change point), only the last step is needed to search for the optimal location of a change point, and the related computations costs are of .

When and is large, Algorithm 1 can be extremely time-consuming because of the computations, we aim to decrease the computational costs in this case. Apparently, some computations in Step 1 may be redundant. For example, in Step 2, the domain for the optimisation problem is for each

; so the calculations of for all in Step 1 become unnecessary as these results will not be used. Thus, the computations in Step 1 could be moved into Steps 2- 4 so that only the necessary are computed and stored. This means one could begin the algorithm from Step 2 by computing and storing for and for , , then solve for . In Step 3, for , one only needs to compute and save for ( before solving for . Finally, in Step 4, we compute and store for before solving for .

6.2 Algorithm for (5.2) (with unknown )

When is unknown, one may compute and compare the values of (5.2) and varies from up to for some The upper bound can also be predetermined from the descriptive analysis of the observed processes. For each , one can first apply Algorithm 1 to obtain the estimated change points and compute (5.2) accordingly. After the computations, the desired is the one that returns the minimum value of (5.2). By Proposition 5.1, is consistent when is large, provided .

If we directly apply Algorithm 1 to , the total computations will be of order . To further simplify the computations, we study the behaviour of Step 2–3 in Algorithm 1 when increases from to . In this case, the ranges of reduces from to for each . This implies that the stored optimisation results of Steps 2 and 3 in Algorithm 1 at the previous step () can also be used in the current step (). Therefore, with the previously stored results, the only step that needs to be updated for each is when and , and the associated computations are of order at and at . Based on these considerations, we tailor the SNS algorithm for (5.2) and the related computations for are of order .

Algorithm 2 (SNS method)

-

1.

Follows all steps in Algorithm 1 to search for the optimal locations of the estimated change points then store the computed value of for . Note that the results of for all such that as well as the optimisation results of for all and need to be stored for future use.

-

2.

For , first let and then compute and store . Next let and the estimated change points are obtained by solving , where and are defined in Algorithm 1. Finally, based on the estimated change points, compute and store .

-

3.

is obtained from that returns the smallest value of (5.2).

The advantage of SNS method is that it returns the optimal locations of change points for every . Hence, it is useful if one interested in investigating the relationships between the locations of change points and . However, for large and , the computational costs in the SNS method may be high.

In addition to SNS method, another dynamic programming algorithm for finding the unknown number of change points is called the Optimal Partitioning (OP) algorithm introduced by Jackson, et al. (2005). The related computational costs are of order for any ; hence, it is more efficient than SNS when is large. Based on the OP algorithm, Killick, et al. (2012) introduced the Pruned Exact Linear Time (PELT) method. Although the maximum computational costs for the PELT algorithm is still up to for a data set with size , the computations in the PELT method, which involved pruning of the solution space under some conditions can be much less than those required in the OP.

However, the PELT method introduced in Killick, et al. (2012) may not satisfy Assumption 1, which is essential for most of the theoretical properties developed in this paper. In fact, under Assumption 1: (i) there is no change point in time period , where is defined in Algorithm 1; (ii) if there is a change point , then there is no non-zero change point prior to ; and (iii) for any potential change point , the minimal distance between it and the most recent change point prior to this change point is at least . Based on these considerations, we use the following modified version of the PELT algorithm.

Algorithm 3 (Modified PELT method)

Let be the length of the data set based on the partition of time period with increment , and let . Set and for . Then, for , compute and store the values obtained from the following steps.

-

1.

For , compute and store , where is the Riemann sum approximation (midpoints) of the log likelihood (no change point) evaluated at time period with .

-

2.

For , compute and store: (i) ; (2). ; (3). .

-

3.

Denote . Then, the optimal change points can be obtained by solving with starts from and iterates recursively until .

7 Numerical demonstrations

The Monte-Carlo simulation technique will be used in Subsection 7.1

(i) to evaluate the comparative performance

of the two estimation methods, viz. LSSE in (4.2) and MLL in (4.7) to determine the unknown

location of change points assumed to already exist; and (ii) to test the method in (5.2) for detecting the unknown number of change points. In Subsection 7.2, we illustrate the various implementation details of our proposed methods on some observed financial market data.

7.1 Monte-Carlo simulation study

Our simulation considers two different scenarios (or cases). In the first case, we study the performance of the proposed methods under the classical OU process defined by

| (7.1) |

In the second case, the performance evaluation of the proposed methods is tested assuming a periodic mean-reverting OU process, with 2-dimensional periodic incomplete set of functions (which are orthogonal on [0,] with weight fixed to 1), given by

| (7.2) |

where is the increment for .

Each case consists of 500 iterations. Although an exact solution is available, we choose to use the Euler-Maruyama discretisation scheme to be consistent with the results of Zhang (2015). In each iteration,

we first generate a desired simulated process based on a given period with pre-assigned “true” parameters such as the number and location of change points and the model coefficients. To evaluate the performance of (4.2) and (4.7), we specify the number of change points to be known but the rate is unknown. Then, we estimate and record the change points’ arrival rates by applying (4.2) and (4.7) on the simulated process. The detailed simulation setup and results are reported in Subsection 7.1.1.

In Subsection 7.1.2, we also use the Monte-Carlo simulation method to investigate the performance of (5.2). That is, we assume that is unknown and apply (5.2) with ranging from to . Then, the that returns the minimum value of (5.2) is chosen as the estimated value for the number of change points. After 500 iterations, we analyse the performance of the proposed methods based on the recorded results.

7.1.1 Estimating the rate of change points

We first study the performance of (4.2) and (4.7) in estimating the rates of the change points with known . For the simulation setup, we consider the case where and with different time periods , respectively. The pre-assigned values of the coefficients are provided in Table 1.

| 2 change points (, ) | 3 change points (, , ) | |||||||

| Case | Coefficient | |||||||

| 1 | 0.08 | 2.50 | 0.08 | 0.08 | 2.50 | 0.08 | 2.50 | |

| 0.10 | 1.00 | 0.50 | 0.10 | 1.00 | 0.50 | 1.00 | ||

| 2 | 0.08 | 2.50 | 0.08 | 0.08 | 2.50 | 0.08 | 2.50 | |

| 0.02 | 1.20 | 0.02 | 0.02 | 1.20 | 0.02 | 1.20 | ||

| 0.10 | 1.00 | 0.50 | 0.10 | 1.00 | 0.50 | 1.00 | ||

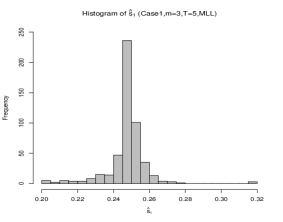

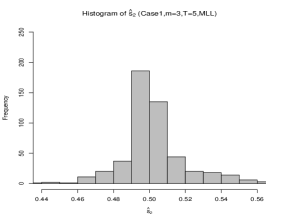

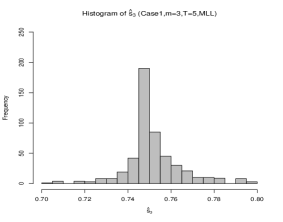

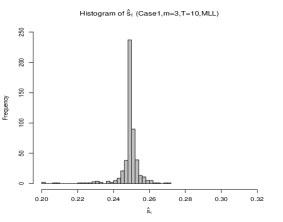

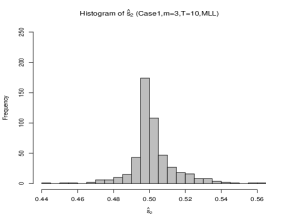

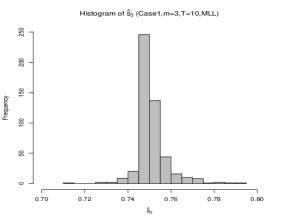

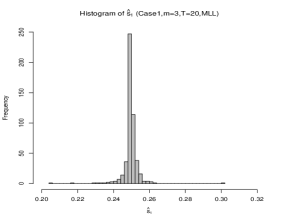

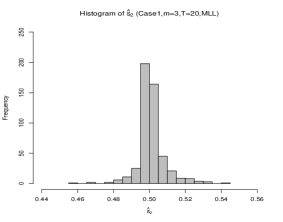

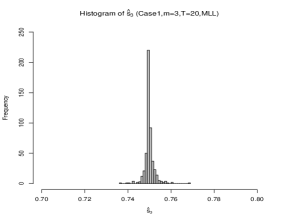

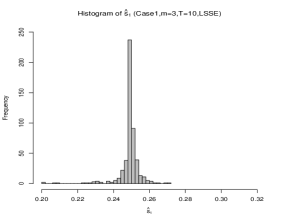

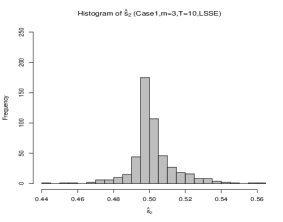

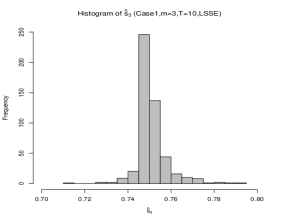

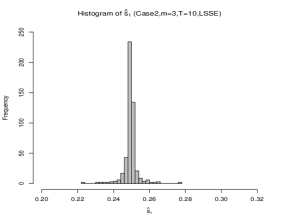

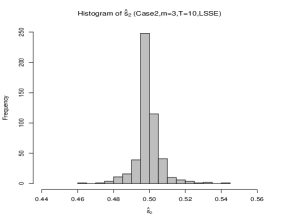

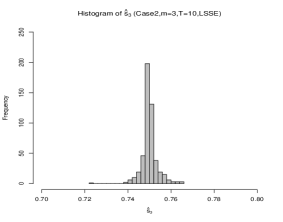

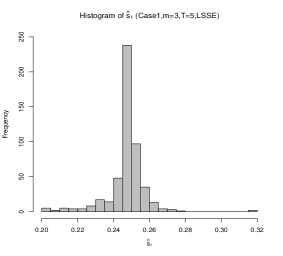

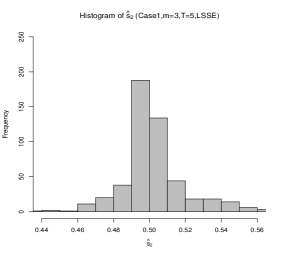

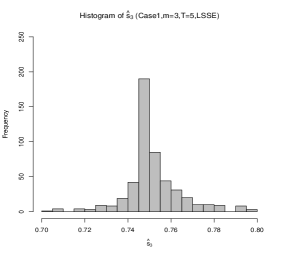

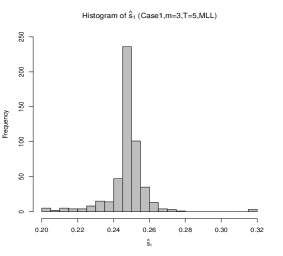

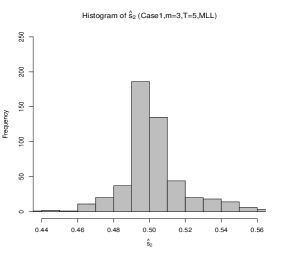

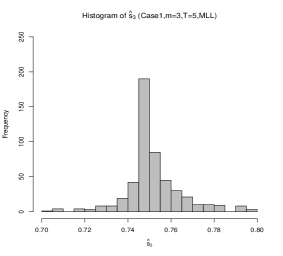

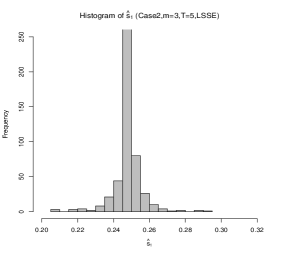

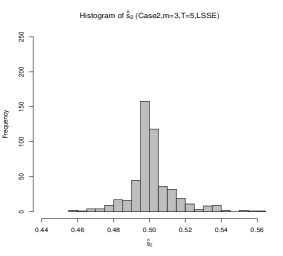

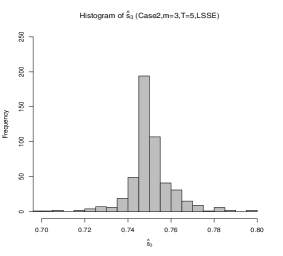

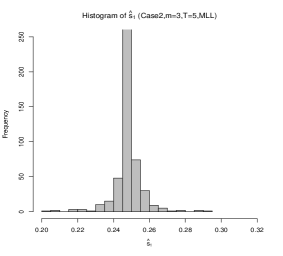

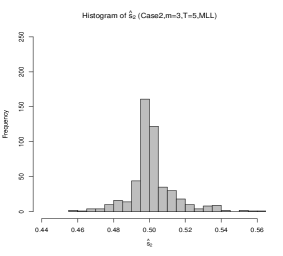

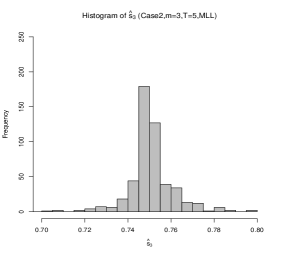

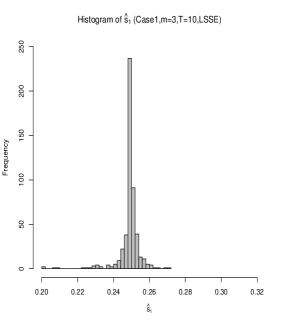

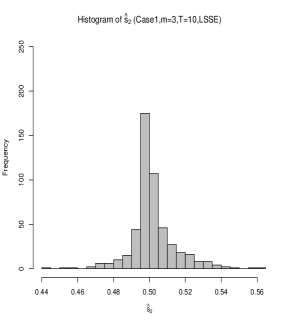

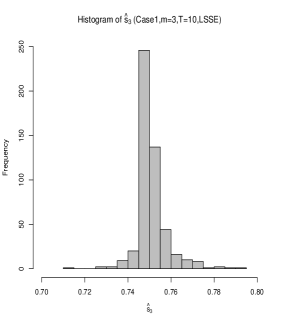

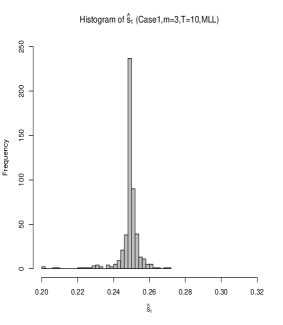

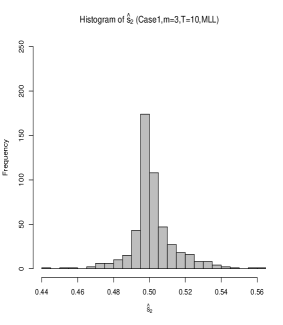

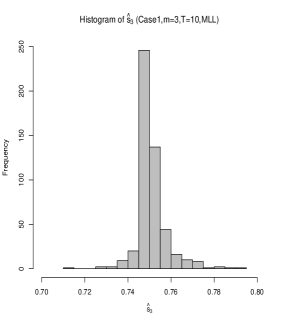

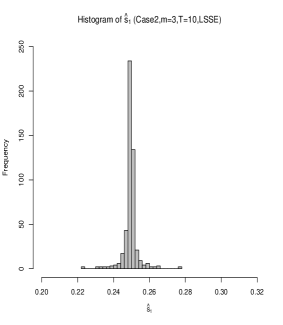

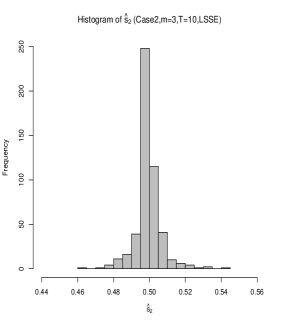

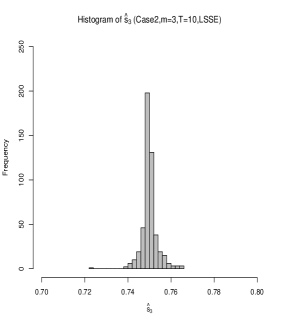

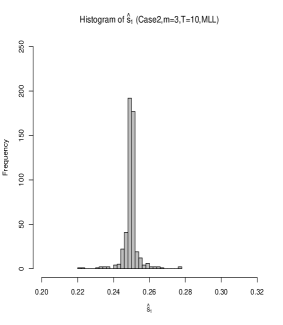

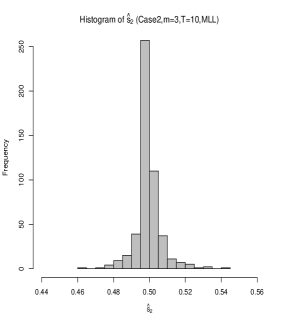

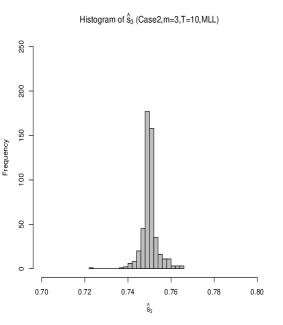

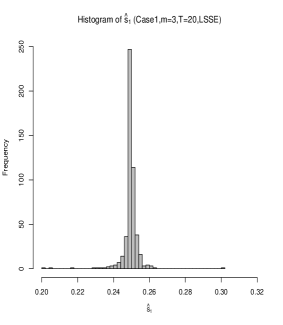

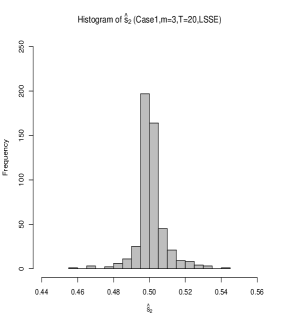

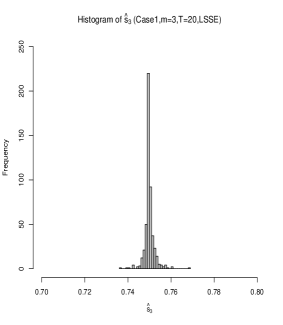

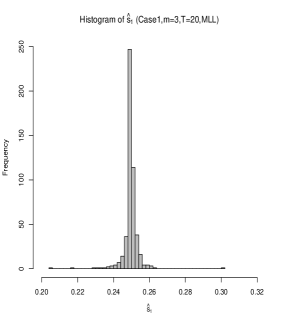

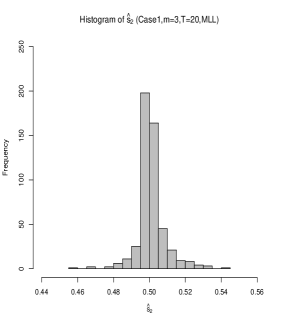

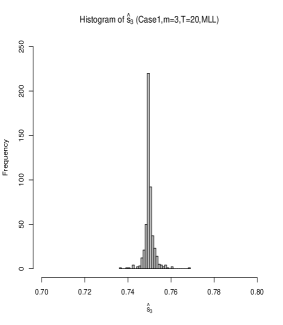

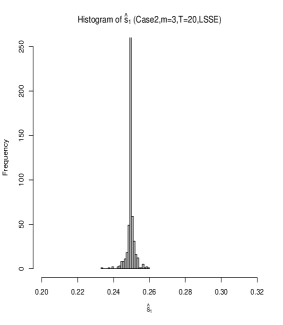

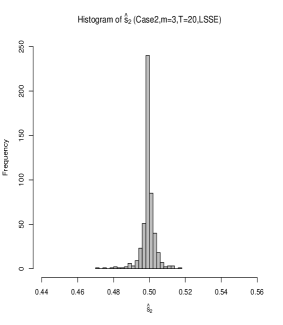

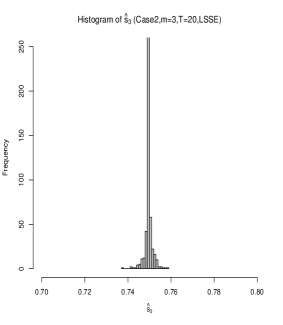

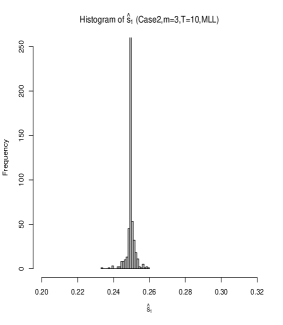

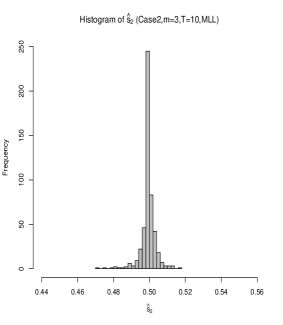

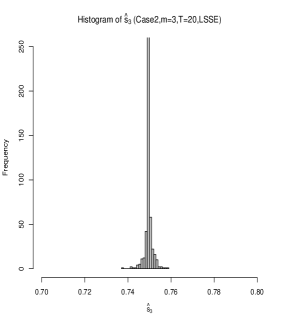

For each case, after 500 iterations we record the mean of the estimates based on (4.2) and (4.7), together with the empirical confidence interval (i.e., locating the and percentiles) and also the mean-squared error. The results are reported in Tables 2–5. In this section, we also report the following histograms: Figure 1 presents the histograms of the estimated rates based on MLL method for Case 1 with when increases from 5 to 20, which shows the behavior of the estimated rates as increases. Figure 2 shows the histograms of the estimated rates for the two cases under the same conditions (i.e. , and the rates are estimated by LSSE method). Moreover, for the convenience of the reader, all histograms of the estimated rates for are provided in Appendix E (Figures 8–10) for reference.

From Tables 2–5 (along with Figures 1, 2 and 8–10 in Appendix E), we see that in Cases 1 and 2, both proposed methods (4.2) and (4.7) estimate very accurately the exact rates of change points. In particular,

the sample means of the estimated change points’ arrival rates are close to the exact values, and the results obtained by the 2 proposed methods are very close, which confirms Proposition 4.3. We also clearly observe that as increases from 5 to 20, the lengths of the empirical confidence intervals and MSEs of the two estimators all decrease. This is well substantiated for example by the pertinent histograms in Figure 1, which shows that when MLL method is employed to estimate the change points’ arrival rates in Case 1 with , the central tendencies of the estimated rates are all close to their exact values, and the sample variances decrease as becomes larger. Similar evidences are shown for other choices of scenarios (different combinations of cases, methods and time period ) as illustrated in Figures 8– 10. Although not shown in this paper, the histograms for the case exhibit similar features. These outcomes confirm the theoretical findings regarding the asymptotic consistency of our two proposed methods.

Also, from Tables 2–5 and Figure 1 (see Appendix E as well), the lengths of the confidence intervals (C.I.’s), with corresponding MSEs, of the estimated rates for the first and the last unknown change points ( and ) are more accurate than those of the middle change point (). Moreover, the improved accuracy of and is more sensitive to the increase of as compared to that of .

This is because the unknown change point’s arrival rate satisfies

for .

For and , one of their boundaries is known (which are and , respectively),

whilst for the intermediate rates both the upper and lower bounds and are unknown.

Therefore, under the same condition, the uncertainties of the first and the last change points’ arrival rates would be lower than that in the middle.

For the comparisons between Case 1 and 2, we can see from the selected scenario (, , LSSE method) shown in Figure 2, along with the results in Tables 2–5 that under the same conditions, the lengths of the 95% empirical C.I. and MSEs in Case 2 are all smaller than those in Case 1. However, since the simulated processes in the 2 cases are generated from different SDEs, it may be inappropriate to make conclusion based only on the results shown in the provided tables and figures. In fact, note that the main difference between (7.1) and (7.2) is the number of coefficients in the models. Therefore, the comparison between the 2 models when fitting them to the same process can be considered as a model selection problem that has been well studied in the literature.

| =5 | =10 | =20 | |||||||

| Mean | C.I. | MSE | Mean | C.I. | MSE | Mean | C.I. | MSE | |

| , (LSSE) | 0.348 | (0.313, 0.371) | 1.75 | 0.349 | (0.333, 0.363) | 9.35 | 0.350 | (0.341, 0.356) | 3.47 |

| , (MLL) | 0.348 | (0.313, 0.371) | 1.76 | 0.349 | (0.333, 0.363) | 9.35 | 0.350 | (0.341, 0.356) | 3.75 |

| , (LSSE) | 0.701 | (0.638, 0.742) | 4.61 | 0.702 | (0.676, 0.736) | 1.76 | 0.700 | (0.682, 0.716) | 5.62 |

| , (MLL) | 0.701 | (0.638,0.742) | 4.61 | 0.702 | (0.676, 0.736) | 1.76 | 0.700 | (0.682, 0.716) | 5.19 |

| =5 | =10 | =20 | |||||||

| Mean | C.I. | MSE | Mean | C.I. | MSE | Mean | C.I. | MSE | |

| , (LSSE) | 0.349 | (0.333, 0.362) | 6.97 | 0.350 | (0.341, 0.358) | 1.51 | 0.350 | (0.344, 0.355) | 7.63 |

| , (MLL) | 0.349 | (0.332, 0.362) | 0.70 | 0.350 | (0.342, 0.358) | 1.53 | 0.350 | (0.344, 0.355) | 7.60 |

| , (LSSE) | 0.701 | (0.667, 0.734) | 1.97 | 0.700 | (0.684, 0.718) | 6.38 | 0.70 | (0.690, 0.707) | 1.76 |

| , (MLL) | 0.701 | (0.667, 0.733) | 2.01 | 0.700 | (0.684,0.718) | 6.40 | 0.70 | (0.690, 0.707) | 1.80 |

| =5 | =10 | =20 | |||||||

| Mean | C.I. | MSE | Mean | C.I. | MSE | Mean | C.I. | MSE | |

| , (LSSE) | 0.248 | (0.217, 0.263) | 1.23 | 0.249 | (0.231, 0.258) | 3.95 | 0.250 | (0.242, 0.256) | 2.66 |

| , (MLL) | 0.248 | (0.217, 0.264) | 1.32 | 0.249 | (0.231, 0.258) | 4.14 | 0.250 | (0.242, 0.256) | 2.18 |

| , (LSSE) | 0.502 | (0.468, 0.549) | 3.38 | 0.502 | (0.477, 0.532) | 1.58 | 0.501 | (0.485, 0.522) | 6.44 |

| , (MLL) | 0.502 | (0.468, 0.549) | 3.39 | 0.502 | (0.477, 0.532) | 1.58 | 0.501 | (0.486, 0.522) | 6.23 |

| , (LSSE) | 0.752 | (0.725, 0.785) | 1.74 | 0.751 | (0.740, 0.770) | 4.78 | 0.750 | (0.746, 0.755) | 5.65 |

| , (MLL) | 0.752 | (0.725, 0.785) | 1.73 | 0.751 | (0.740, 0.770) | 4.78 | 0.750 | (0.746, 0.755) | 5.65 |

| =5 | =10 | =20 | |||||||

| Mean | C.I. | MSE | Mean | C.I. | MSE | Mean | C.I. | MSE | |

| , (LSSE) | 0.248 | (0.231, 0.262) | 6.48 | 0.250 | (0.240, 0.259) | 1.93 | 0.250 | (0.244, 0.253) | 5.29 |

| , (MLL) | 0.248 | (0.233, 0.263) | 6.37 | 0.249 | (0.242, 0.259) | 1.83 | 0.250 | (0.244, 0.254) | 5.39 |

| , (LSSE) | 0.502 | (0.475, 0.539) | 1.94 | 0.500 | (0.483, 0.515) | 5.09 | 0.499 | (0.489, 0.506) | 1.72 |

| , (MLL) | 0.502 | (0.475, 0.539) | 1.94 | 0.500 | (0.484, 0.517) | 5.03 | 0.500 | (0.489, 0.507) | 1.73 |

| , (LSSE) | 0.750 | (0.727, 0.774) | 1.20 | 0.750 | (0.743, 0.760) | 1.39 | 0.750 | (0.746, 0.753) | 3.20 |

| , (MLL) | 0.751 | (0.727, 0.774) | 1.17 | 0.750 | (0.743, 0.760) | 1.42 | 0.750 | (0.746, 0.754) | 3.07 |

7.1.2 Estimating the number of change points

In this subsection, we study the performance of (5.2) in estimating the unknown number of the change points based on Algorithms 2 (SNS) and 3 (Modified PELT). For the simulation setup, we assume the exact value of , with different time periods . The pre-assigned coefficients are provided in Table 6.

Based on the simulated process, we apply Algorithms 2 and 3 with ranging from to to estimate the unknown number of change points. In Tables 7, we count and report the cumulative frequency (CF) of 500 iterations that return the correct estimates and the relative frequency (RF) .

| Case | Coefficient | |||

|---|---|---|---|---|

| 1 | 0.08 | 2.50 | 0.08 | |

| 0.10 | 1.00 | 0.50 | ||

| 2 | 0.08 | 2.50 | 0.08 | |

| 0.02 | 1.20 | 0.02 | ||

| 0.10 | 1.00 | 0.50 |

| =5 | =10 | =15 | =20 | ||||||

| Case | Algorithm | CF | RF | CF | RF | CF | RF | CF | RF |

| 1 | 2 (SNS) | 492 | 498 | 500 | 500 | ||||

| 2 | 2 (SNS) | 500 | 500 | 500 | 500 | ||||

| 1 | 3 (PELT) | 494 | 98.8% | 499 | 99.8% | 500 | 100.0% | 500 | 100.0% |

| 2 | 3 (PELT) | 497 | 99.4% | 500 | 100.0% | 500 | 100.0% | 500 | 100.0% |

For the estimated number of change points, one could see from Table 7 that, when , the proposed methods perform very well in both cases with different time periods. Furthermore, the accuracy of the estimating results in different cases all increase as increases. These results suggest that our proposed method is asymptotically consistent, which confirms the theoretical finding in Proposition 5.1.

7.2 Implementation on observed financial market data with discussion

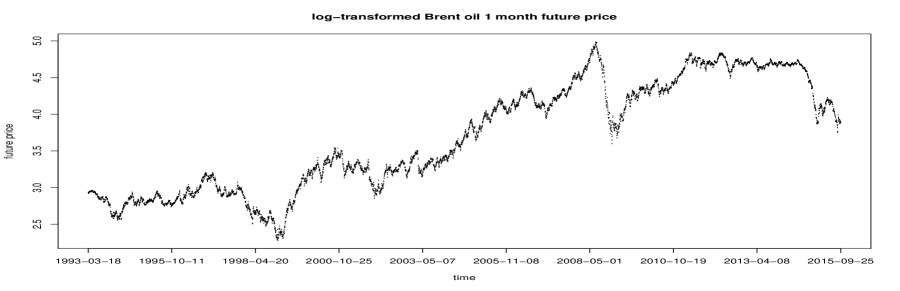

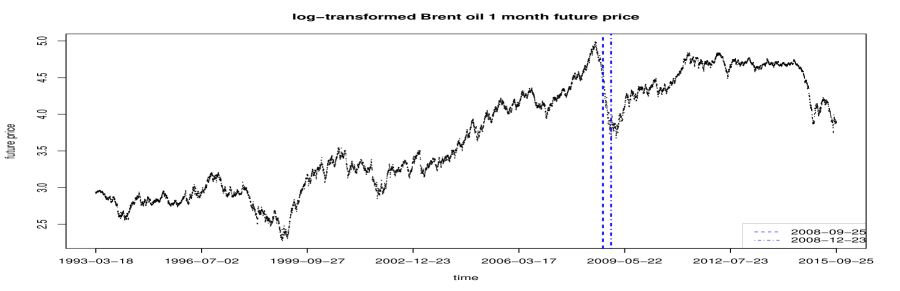

We apply the estimation methods to the Brent oil one-month futures settlement daily price data for the period 18 March 1993 to 25 September 2015. The data set is available

at www.quandl.com.

The empirical studies of Schwartz (1997) and Chen (2010) showed that mean-reversion features hold for prices of several commodities including oil. Hence, we use OU-types processes to model such price behaviour. We first fit the classical OU process without any change point, i.e., using the dynamics ), to the log-transformed data series with ’s estimate as the data’s realised volatility . The MLE of the drift parameters are given by and . Based on these MLE values, the log likelihood (via the Riemann-sum approximation) is about 1.02 and .

However, from the plot of the price series in Figure 3, there are several changes in the shapes of the price evolution. This observed feature suggests that it may be more appropriate to use (7.1) with unknown () change points.

The data set covers approximately 22.5 years giving a sample size of 5735 trading days. The recorded yearly number of trading days varies from year to year; so, for convenience, we let . Since the size of the data set is large, we apply Algorithm 3 using a minimum permissible regime-time length of trading days (quarterly). The algorithm detects change points, which occurs on 24 September 2008 and 23 December 2008, with a corresponding log likelihood increase (via Riemann-sum approximation) of 26.81 and lower than . To confirm the results, we also apply Algorithm 2 with LSSE and MLL methods respectively and set to be 10. The results are the same as that obtained from Algorithm 3.

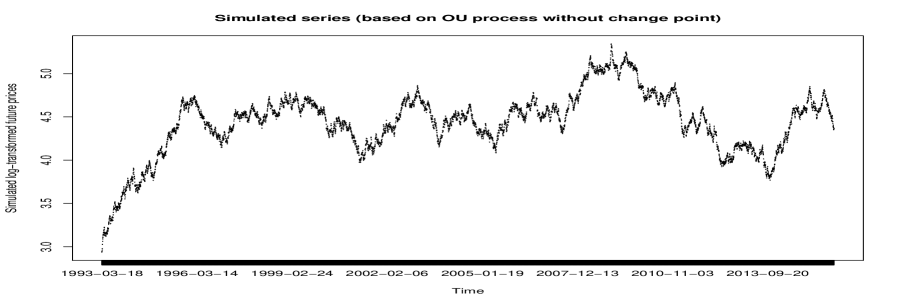

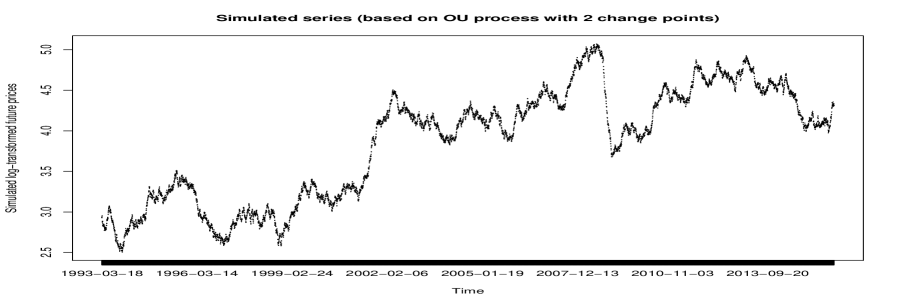

The plot of the price series, with change points indicated, is depicted in Figure 4. It shows that, from September 2008 to March 2009, there is a decreasing trend in the log-transformed futures prices and then the trend is slightly increasing after this period. Further, based on the estimated change points, the MLE of the drift parameters, and the associated statistics such as (long-term) means (i.e., ) and variances (i.e., ) are given in Table 8. From Table 8, there are huge changes in the MLEs of the drift parameters under different ’s. Based on the MLEs, we also plot two simulated series based on the OU process with and without change points; see Figures 5 and

6, respectively. As most notably expected, the simulated series based on the OU process with two change points is closer to the original series, especially during the period spanning 25 September–23 December 2008, than the simulated series based on the OU process without change point. Judging from these observed characteristics and taking into account the above-mentioned substantial improvements in the log likelihood and SIC values, we conclude that the OU-process with two change points occurring on 25 September 2008 and 23 December 2008 is the appropriate model for the data set that we analysed.

| Time period | ||||||

|---|---|---|---|---|---|---|

| 18 March 1993 to 25 September 2008 | 0.128 | 0.005 | 25.794 | 0.328 | 10.889 | 0.884 |

| 26 September 2008 to 23 December 2008 | 5.501 | 2.418 | 2.275 | 0.328 | 0.022 | 23.367 |

| 24 December 2008 to 25 September 2015 | 3.977 | 0.879 | 4.524 | 0.328 | 0.061 | 2.557 |

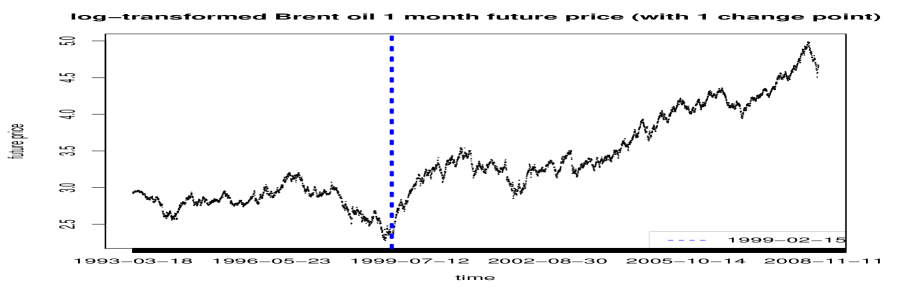

Moreover, we see from Figure 4 that from 18 March 1993 to 25 September 2008 (the first estimated change point), there are several noticeable changes in the series. For example, from 1996 to 1998 there was a fall in the futures price. However, based on the SIC, these changes are not significant enough to warrant the inference of a regime change and they are therefore ignored by the proposed methods. We take a closer look concentrating only on the 18-Mar-1993-to-25-Sep-2008 data set to see if there is any change point at all. This analysis is equivalent to reducing the sample size and the penalty term of the SIC accordingly. Algorithm 3 is re-applied to the reduced data set with a sample size 3928 and maintaining the same and as those in our other experiments. The resulting SIC indicates still no change point during the shortened period. Furthermore, we employ the estimated parameters and sample size in our reduced data set to run a simulation similar to that in Subsection 7.1.2 in assessing the performance of the proposed methods, and we obtained an RF of in producing the correct estimates.

The above result tells us that an OU process without a change point would be appropriate to model the data series from 18 March 1993 to 25 September 2008. However, from Table 8 the respective long-term mean and variance and are

and , which are both higher than those in the two other time periods. Such high statistics may be less preferable in practice, although they reasonably explain the increasing trend in the investigated time period. On the other hand, we know that imposing more change points, which is equivalent to increasing the number of coefficients in the model, can reduce the variance.

Hence, we examine the potential reduction in the variance by imposing a change point into this period. To this end, we fit an OU process with one change point to the series and use Algorithm 1 to estimate the location in the OU process. The estimated change point is at 15 February 1999, which is near the bottom of the series; see Figure 7.

Based on Table 9, by imposing a change point at 15 February 1999, the means

before and after the change point both strikingly decrease to 2.646 and 4.407, respectively, in comparison to the previous result of . Additionally, the variances for the time periods before and after the change point also markedly go down to respective values of 0.085 and 0.163. The approximate log likelihood increases correspondingly to 4.199 for the period 16 February 1999–25 September 2008.

This implies that imposing a change point (15 February 1999) into the model does improve the accuracy. Nevertheless, recall that our SIC-based method shows no change point at this time period. Therefore, we demonstrated

a strong potential for an over-fitting problem to arise when a change-point assumption is unnecessarily introduced into the model. This also reminds us of a trade-off between accuracy improvement and issue of over fitting that must be

avoided whenever possible.

| Time period | ||||||

|---|---|---|---|---|---|---|

| 18 March 1993 to 15 February 1999 | 1.688 | 0.638 | 2.646 | 0.328 | 0.085 | 0.762 |

| 16 February 1999 to 25 September 2008 | 1.450 | 0.329 | 4.407 | 0.328 | 0.163 | 4.199 |

8 Conclusion

The main contribution of this paper is

the development of MLL- and LSSE-based methods

in detecting the unknown number of multiple change points along with the

identification of their locations in a generalised univariate

OU process. Additionally, we showed that our proposed

estimators for the change points’ locations satisfy the

asymptotically consistent and normality properties under

certain suitable conditions that we painstakingly imposed. These results

guided the design of three computing algorithms customised for the efficient

implementation of our proposed methods. The numerical applications we showcased

covering both simulated and observed data illustrated the excellent performance

and accuracy of the estimation approaches that we created to handle change points detection.

The usefulness of our results have relevance to regulatory authorities’

policy-making, trading strategy’s construction by investors and provider’s of financial

products and services, and other scientific endeavours in the natural and social

sciences impacted by sudden and significant changes (e.g., break, jumps, shifts, etc)

in the time-series data.

This work provides impetus for the investigation and

development of methodology suited in tackling further the

multiple-change point problem for a multivariate OU process

and other closely related modelling challenges in the research literature and practice

that entail the statistical inference of stochastic processes.

Appendix Appendix A Proof of Proposittion 3.2

Proof of Proposition 3.2.

We first need to prove that the coefficients of (1.1) satisfy the space-variable Lipschitz condition. That is,

Given that is constant in our modelling framework, the second term above is 0. Hence,

Since for , there exists a such that . Then,

Next, we prove the spatial growth condition. That is,

Note that

Using the identity , we have

Since are bounded, we can find a constant such that

This gives

Moreover, let . Then

and

∎

Appendix Appendix B Proof of the propositions in section 4

Proof of Proposition 4.1.

Let be the residual of the th element based on the estimated change points , , i.e., , for , where and are defined in Section 4 as the true value and MLE of the parameters

based on the assigned estimated change points of the coefficients associated with the th element. Also, let be the residual of the th element based on the exact change points and

with .

The proof relies on investigating the behaviour of

| (Appendix B.1) |

where . By (4.2), with probability 1. Hence, it remains to show that if one of the change points is not consistently estimated, with positive probability yielding a contradiction.

Using the quadratic expansion and some algebraic computations, (Appendix B.1) can be expressed as

| (Appendix B.2) | |||||

We aim to show that if there exists a change point , , and it is not consistently estimated, the first term is larger than a positive constant with positive probability, whilst the rest of terms is of and hence, with positive probability. To this end, we first provide a lemma, which will be useful in deriving the asymptotic consistency of the estimated change points.

Lemma C.1 If at least one of the change points, say , can not be consistently estimated, then

for large ,

Proof.

If the change point is not consistently estimated, then with some positive probability there exists an such that there is no estimated change point in for some . Without loss of generality, let . Then, since for each ,

| (Appendix B.3) | |||||

Let and be the smallest eigenvalues of and , respectively. Then,

Using the convexity of a quadratic function, we have

Hence,

Under Assumption 4, and are both bounded away from 0 and is also bounded away from 0. Therefore, the right-hand side of the above inequality is positive. Then, the proof is complete by letting . ∎

Lemma C.2. directly follows from Proposition 2.2.6 in Zhang (2015) with and replaced by and , respectively. To emphasise again, both lemmas C.1 and C.2 are key in proving the asymptotic properties of the proposed estimators.

Next, note that for , , we have

and . Substituting these expressions into , we get

| (Appendix B.4) |

To proceed further, we first prove the following inequality. Suppose . By the Markov inequality, Itô’s isometry and (3.8), we have

| (Appendix B.5) |

Therefore, by letting , for some , the above probability tends to 0 as tends to infinity. This implies that for some ,

| (Appendix B.6) |

Now, continuing the proof of Proposition 4.1, we note that under Assumption 3, for . By similar argument used to obtain (Appendix B.6), we have for so that . Moreover, since is the discretised versions of , it similarly follows that . Also, is the discretised version of , thus the asymptotic results in (3.13) and (3.15) also hold for . Therefore, by the Cauchy-Schwarz inequality, (3.13) and (3.15) we have, after some algebraic manipulations,

| (Appendix B.7) |

It remains to investigate the quantity

| (Appendix B.8) |

Note that the structure of is affected by the location of the estimated change points. It is, therefore, difficult to substitute the expressions for into (Appendix B.8) directly. Without loss of generality, we consider (but the procedure can be extended to the general case ), and assume that . Other cases can be analysed in a similar manner. With , (Appendix B.8) reduces to

| (Appendix B.9) | |||||

where ,

,

, , , and .

Using the Cauchy-Schwarz inequality, (Appendix B.6), Lemma C.2 along with the Continuous Mapping Theorem, the first term in (Appendix B.8) is bounded above, i.e.,

Similarly, one can show that the rest of the terms in (Appendix B.8) are all of . Following these arguments, it can be shown that in the general case when , the terms in (Appendix B.8) are all of order . So, if one of the change points’ arrival rates, say , is not consistently estimated, (Appendix B.1) is dominated by the first term, which is larger than 0 with positive probability. This gives a contradiction. Therefore, for every . ∎

Proof of Proposition 4.2.

Without loss of generality, assume that . We provide an explicit proof dealing with the rate -consistency for only. The consistency analysis for and can be similarly completed. By Proposition 4.1, for each . For , define the set .

Let , where is the MLE of associated with the th element under the change point , and let . So, we have with probability 1. If we can show that for each , there exists a , such that for large and any , , this would imply that for some , the global optimisation can not be achieved on the set . Thus with large probability, .

Let .

Assume, without loss of generality, that . We now focus on the behaviour of

| (Appendix B.10) |

Applying the identity into (Appendix B.10) and then breaking the time period into different intervals, we have

| (Appendix B.13) | |||||

where

,

,

and

It remains to show that for large , is positive with probability 1. Note that this depends on the choice of ; can be instead of , and thus the arguments we used in the proof of Proposition 4.1 cannot be applied here directly. To overcome this problem, we need to expand each term in (Appendix B.13). We note that

So,

and

By Tobing and McGlichrist (1992), we have

| (Appendix B.14) |

Hence,

| (Appendix B.15) |

Using the asymptotic results in Proposition 4.1, we have that . Therefore,

Similarly,

Thus, . Furthermore, using the same argument above together with (Appendix B.6), we have

With the aid of the identity , (Appendix B.14) and the Cauchy-Schwarz inequality, we get

and

Combining the above results, we have

Similarly,

| (Appendix B.16) |

Note that So, from (Appendix B.5), for some . Moreover, , and by Tobing and McGlichrist (1992), . Again, when these results are combined,

one may verify that, with a suitable choice of , for large the order of is .

The above procedure can also be applied to investigate the behaviour of (Appendix B.13). For example,

with

and

Hence, for large ,

In an analogous manner, one can show that, with a suitable choice of , for large ,

Finally, we investigate the behaviour of the remaining term.

By Proposition 4.1, . Hence, applying again the Cauchy-Schwarz inequality and similar reasoning as before, we have

Also,

and

Moreover, it follows from the identity that

with

Now, suppose be the smallest eigenvalue of . With a suitable , is bounded away from 0. Hence,

with probability 1 and this dominates the rest of the terms in (Appendix B.10) when is large. This implies that (Appendix B.10) is positive with probability 1, which gives a contradiction and it indicates that with large probability cannot be in the set . ∎

Proof of Corollary 4.1.

Part (i) of Corollary 4.1 follows from the same arguments utilised in the proof of Proposition 4.1 with in (Appendix B.1) set to , together with the fact that and . On the other hand, part (ii) may be verified by employing similar arguments as in the proof of Proposition 4.2 in investigating the set instead of . ∎

Proof of Proposition 4.3.

To examine the behaviour of (4.7), we first define and . Then,

The term is non-negative. For an observed process with constant and known , is fixed and does not depend on the change points . Hence, finding the change points that maximise (4.7) is equivalent to the minimisation of the term

| (Appendix B.17) |

If , the structure of (Appendix B.17) is the same as in (4.3). The rest of the proof for Proposition 4.3 follows directly via the same arguments used in establishing Proposition 4.1 and 4.2. ∎

Appendix Appendix C Proof of the properties in section 4.3

Proof of Proposition 4.4.

Note that by (3.11) and (Appendix C.1) ,

and

| (Appendix C.1) |

In addition, invoking similar arguments found in the proofs of (B. 47) and (B. 67) in Zhang (2015), we have

| (Appendix C.2) |

and

| (Appendix C.3) |

Therefore, it suffices to prove that

| (Appendix C.4) |

Similarly,

| (Appendix C.5) |

Let . Then, it follows form Proposition 4.2 that

Therefore, we have

Since is equivalent to , and it follows that, for every ,

Hence,

| (Appendix C.6) | |||||

It then follows from the Markov’s inequality and Jensen’s inequality that

In the same vein,

Consequently,

Then, it follows from (3.8) that , for all . Also, under Assumption 3, . Therefore,

Hence,

Similarly, we have

| (Appendix C.7) | |||||

Again, using the Markov’s inequality,

| (Appendix C.8) |

Using the consistency properties of the estimators provided in Section 4, i.e., , we can choose arbitrarily small and such that

∎

Proof of Proposition 4.6.

Proof of Proposition 4.7.

Here we only prove that

| (Appendix C.11) |

The convergence of the remaining components may be proved analogously by the same approach.

Since by Proposition 4.2,

Without loss of generality, we assume that . Then,

| (Appendix C.12) |

With the same arguments as in the proof of (Appendix C.6), together with above inequality,

| (Appendix C.13) | |||||

| (Appendix C.15) | |||||

Then, by Markov inequality and Itô’s isometry,

which tends to 0 for an infinitesimal . Similarly, also tends to 0 by choosing an infinitesimal . Further, note that . So, again, by the Markov inequality and Itô’s isometry,

which goes to 0 for an infinitesimal . Similarly, also approaches 0 by choosing an infinitesimal . This implies that (Appendix C.15) tends to 0 for an infinitesimal and . ∎

Proof of Proposition 4.8.

Replacing the interval by and using similar argument as in the proof of Proposition 2.1.6 in Zhang (2015), we get

| (Appendix C.16) |

By Proposition 4.7,

| (Appendix C.17) |

Hence by Slutsky’s Theorem,

| (Appendix C.18) |

∎

Proof of Corollary 4.2.

Let , and let . Then, we have . By Propositions 4.6– 4.8 and application of Slutsky’s Theorem,

Next, we investigate the asymptotic behaviour of based on . Without loss of generality, we assume that for the th block, , we have . In this case, we have

Hence,

By Proposition 4.2, for some with probability 1. Invoking the Markov inequality,

and

Therefore, , which means

So,

and

∎

Appendix Appendix D Proof of Proposition 5.1

The proof of Proposition consists of two parts. In Part (i), we prove that , whilst in Part (ii) we prove that .

Part (i): .

From Proposition 4.3,

| (Appendix D.1) |

where , are obtained via (4.5). Next, we define

| (Appendix D.2) |

where was given in Appendix B. Since , , are obtained by maximising , or equivalently minimising , we have that with probability 1. Hence, we must show that

| (Appendix D.3) |

with probability 1.

For any positive integer such that , suppose that the estimated locations of these change points are , and the MLE of drift parameters associated with the th observation is , where . Furthermore,

| (Appendix D.4) | |||||

Since , there exists at least one change point that cannot be consistently estimated. Without loss of generality, let be the change point. With similar arguments utilised in the proof of Lemma C.1, we get

| (Appendix D.5) |

for some with probability 1. Therefore, with probability 1. This completes the proof of part (i).∎

Part (ii): .

Since , where is defined in Part (i), it remains to show that the difference is positive with probability 1.

Note that for the case where and the estimated locations of the change points are given by , we have

| (Appendix D.6) | |||||

where with . We note that , and from of these estimated change points, there are estimated change points that divide the time interval into regimes such that within each regime, the number of estimated change points is equal to the number of exact change points. For example, suppose that and with . Then, if we divide the given time interval into and , we can see that within these two intervals, the number of estimated change points is equal to the number of exact change points.

Denote the particular estimated change points by . Also, let and

. Then,

Thus, it remains to show that in each regime , ,

| (Appendix D.7) | |||||

is positive with probability 1.

Since within , the number of estimated change points and the number of exact change points are the same, we first consider the case where there is no any change points within . In this case, we have for some and . Then, and

.

Substituting the above expressions into (Appendix D.7), we have

| (Appendix D.8) | |||||

From the approach used in the proof of Propositions 4.1 and 4.2, we have

for some . Similar results also hold for the second and the third terms of (Appendix D.8).

Therefore, for large , (Appendix D.8) is dominated by , which is positive. This implies that for large , (Appendix D.6) is positive with probability 1.

Now, consider the case where there exist () exact change points (so are the estimated change points) in . We label these exact change points by

and similarly for the estimated change points, .

By the quadratic structure,

It follows from (Appendix B.7) that for some . By similar methods employed in the proof of Proposition 4.1, we have . Since for large , , we have that for large , is dominated by either or and they are both positive. This implies that for large , (Appendix D.6) is positive with probability 1. ∎

Appendix Appendix E Histograms of the estimated change points’ arrival rates (Section 7.1.1)

Acknowledgements: F. Chen and R. Mamon wish to thank the hospitality

and financial support of the Fields Institute for Research in Mathematical

Sciences, Toronto, Ontario, Canada, where this research was initially

conceived and partially conducted. Generous support

on this research collaboration from the Dean of Faculty of Science

is gratefully acknowledged.

References

References

- [1] O. Aalen , H. Gjessing, Survival models based on the Ornstein-Uhlenbeck process, Lifetime Data Analysis. 10(4), (2004), 407-423.

- [2] H. Akaike, Information theory and an extension of the maximum likelihood principle, in B. Petrov, F. Csáki, 2nd International Symposium on Information Theory, Tsahkadsor, Armenia, USSR, September 2-8, 1971, Budapest: Akadémiai Kiadó, (1973), 267-281.

- [3] I. Auger, C. Lawrence, Algorithms for the optimal identification of segment neighborhoods, Bulletin of Mathematical Biology. 51(1), (1989), 39-54.

- [4] J. Bai, P. Perron, Estimating and testing linear models with multiple structural changes, Econometrica. 66(1), (1998) 47-78.

- [5] F. Benth, S. Koekebakker, C. Taib, Stochastic dynamical modelling of spot freight rates, IMA Journal of Management Mathematics. 26(3), (2015), 273-297.

- [6] S. Chen, Modelling the dynamics of commodity prices for investment decisions under uncertainty, PhD Dissertation. University of Waterloo, (2010).

- [7] F. Chen, S. Nkurunziza, Optimal method in multiple regression with structural changes, Bernoulli. 21(4), (2015), 2217-2241.

- [8] P. Date, R. Bustreo, Value-at-risk for fixed-income portfolios: a Kalman filtering approach, IMA Journal of Management Mathematics. In press, (2015).

- [9] P. Date, R. Mamon, A. Tenyakov, Filtering and forecasting commodity futures prices under an HMM framework, Energy Economics. 40, (2013), 1001-1013.

- [10] H. Dehling, B. Franke, T. Kott, Drift estimation for a periodic mean reversion process, Statistical Inference for Stochastic Processes. 13, (2010), 175-192.

- [11] H. Dehling, B. Franke, T. Kott, R. Kulperger, Change point testing for the drift parameters of a periodic mean reversion process, Statistical Inference for Stochastic Process. 17(1), (2014), 1-18.

- [12] S. Ditlevsen, P. Lansky, Estimation of the input parameters in the Ornstein-Uhlenbeck neuronal model, Physical Review E. 71, (2005), 011907.

- [13] R. Elias, M. Wahab, F. Fung, A comparison of regime-switching temperature modeling approaches for applications in weather derivatives, European Journal of Operational Research. 232(3), (2014), 549-560.

- [14] R. Elliott, J. van der Hoek, P. Malcolm, Pairs trading, Quantitative Finance, 5(3) (2005), 271-276.

- [15] R. Elliott, C. Wilson, The term structure of interest rates in a hidden Markov setting, in R. Mamon, R. Elliott (eds), Hidden Markov Models in Finance. Springer, New York, (2007), 14-31.

- [16] C. Erlwein, F. Benth, R.S. Mamon, HMM filtering and parameter estimation of an electricity spot price model, Energy Economics, 32(5), (2010), 1034-1043.

- [17] C. Gallagher, R. Lund, M. Robbins, Changepoint detection in daily precipitation data, Environmetrics, 23(5), (2012), 407-419.

- [18] E. Gombay, Change detection in linear regression with time series errors, Canadian Journal of Statistics, 38(1), (2010), 65-79.

- [19] J. Hull, A. White, Pricing interest-rate-derivative securities, Review of Financial Studies. 3(4), (1990), 573-592.

- [20] S. Howell, P. Duck, A. Hazel, P. Johnson, H. Pinto, G. Strbac, N. Proudlove, M. Black, A partial differential equation system for modelling stochastic storage in physical systems with applications to wind power generation, IMA Journal of Management Mathematics, 22(3), (2011), 231-252.

- [21] B. Jackson, J. Scargle, D. Barnes, S. Arabhi, A. Alt, P. Gioumousis, E. Gwin, P. Sangtrakulcharoen, L. Tan, T. Tsai, An algorithm for optimal partitioning of data on an interval, IEEE Signal Processing Letters, 12, (2002), 105-108.

- [22] R. Killick, P. Fearnhead, I. Eckley, Optimal detection of change points with a linear computational cost, Journal of the American Statistical Association. 107(500), (2012), 1590-1598.

- [23] Y. A. Kutoyants, Statistical Inference for Ergodic Diffusion Processes, Springer Series in Statistics, London, (2004).

- [24] P. Lánský, L. Sacerdote, The Ornstein-Uhlenbeck neuronal model with signal-dependent noise, Physics Letters A. 285(3-4), (2001), 132-140.

- [25] Z. Liang, K. Yuen, J. Guo, Optimal proportional reinsurance and investment in a stock market with Ornstein-Uhlenbeck process, Insurance: Mathematics and Economics. 49( 2), (2011), 207-215.

- [26] R. Lipster, A. Shiryaev, Statistics of Random Processes I. Springer-Verlag, Berlin-Heidelber-New York (2001).

- [27] Q. Lu, R. Lund, Simple linear regression with multiple level shifts, Canadian Journal of Statistics, 35 (3), (2007), 447-458.

- [28] S. Lu, Ornstein-Uhlenbeck diffusion quantum Monte Carlo calculations for small first-row polyatomic molecules, Journal of Chemical Physics. 118(21), (2003), 9528-9532.

- [29] S. Lu, Ornstein-Uhlenbeck diffusion quantum Monte Carlo study on the bond lengths and harmonic frequencies of some first-row diatomic molecules, Journal of Chemical Physics. 120, (2004), http://dx.doi.org/10.1063/1.1639370.

- [30] R. Maidstone, T. Hocking, G. Rigaill, P. Fearnhead, On optimal multiple changepoint algorithms for large data, ArXiv e-prints. (2014).

- [31] R. Mamon, R. Elliott, Hidden Markov Models in Finance, Volume 104 of International Series in Operations Research & Management Science. New York, Springer (2014).

- [32] E. Page. Continuous inspection schemes, Biometrika. 41, (1954), 100-115.

- [33] P. Perron, Z. Qu, Estimating restricted structural change models, Journal of Econometrics. 134(2), (2006), 373-399.

- [34] J. Reeves, J. Chen, X. Wang, R. Lund, Q. Lu, A review and comparison of changepoint detection techniques for climate data, Journal of Applied Meteorology and Climatology. 46(6), (2007), 900-915.

- [35] M. Robbins, R. Lund, C. Gallagher, Q. Lu, Changepoints in the North Atlantic tropical cyclone record, Journal of the American Statistical Association, 106 (493), (2011), 89-99.

- [36] R. Rohlfs, P. Harrigan, R. Nielsen, Modeling gene expression evolution with an extended Ornstein-Uhlenbeck process accounting for within-species variation, Scandinavian Journal of Statistics. 37(2), (2010), 200-220.

- [37] E. Schwartz, The stochastic behavior of commodity prices: implications for valuation and hedging, Journal of Finance 52. (1997), 923-973.

- [38] A. Sen, M. Srivastava, On tests for detecting change in mean, Annals of Statistics. 3(1), (1975), 98-108.

- [39] A. Scott, M. Knott, A cluster analysis method for grouping means in the analysis of variance, Biometrics. 30(3), (1974), 507-512.

- [40] G. Schwarz, Estimating the dimension of a model, Annals of Statistics. 6(2), (1978), 461-464.

- [41] S. Shinomoto, Y. Sakai, S. Funahashi, The Ornstein-Uhlenbeck process does not reproduce spiking statistics of neurons in prefrontal cortex, Neural Computation. 11( 4), (1999), 935-951.

- [42] A. Shiryaev, On optimum methods in quickest detection problems, Theory of Probability and Its Applications. 8, (1963), 26-51.

- [43] W. Smith, On the simulation and estimation of the mean-reverting Ornstein-Uhlenbeck process. Version 1.01, CommodityModels.com, (2010).

- [44] V. Spokoiny, Multiscale local change point detection with applications to value-at-risk, Annals of Statistics. 37(3), (2009), 1405-1436.

- [45] A. Tenyakov, R. Mamon, M. Davison, Modelling high-frequency FX rate dynamics: A zero-delay multi-dimensional HMM-based approach, Knowledge-Based Systems. 101, (2016), 142-155.

- [46] A. Tenyakov, R. Mamon, M. Davison, Filtering of a discrete-time HMM-driven multivariate Ornstein-Uhlenbeck model with application to forecasting market liquidity regimes, IEEE Journal of Selected Topics in Signal Processing. 10(6), (2016), 994-1005.

- [47] H. Tobing, C. McGilchrist, Recursive residuals for multivariate regression models, Australian Journal of Statistics. 34(2), (1992), 217-232.

- [48] O. Vasicek, An equilibrium characterisation of the term structure, Journal of Financial Economics. 5, (1977), 177-188.

- [49] G. Yan, Z. Xiao, S. Eidenbenz. Catching instant messaging worms with change-point detection techniques, Proceedings of the 1st Usenix Workshop on Large-Scale Exploits and Emergent Threats. 6(8), (2008), 1-10.

- [50] Yu, X., Baron, M., Choudhary, P. Change-point detection in binomial thinning processes with applications in epidemiology, Sequential Analysis 32 (3), (2013),350-367.

- [51] P. Zhang, On Stein-rules in generalized mean-reverting processes with change point, Master’s Thesis. University of Windsor, Canada.