Kallus and Udell

Dynamic Assortment Personalization in High Dimensions

Dynamic Assortment Personalization

in High Dimensions

Nathan Kallus \AFFCornell University and Cornell Tech, \EMAILkallus@cornell.edu \AUTHORMadeleine Udell \AFFCornell University, \EMAILudell@cornell.edu

We study the problem of dynamic assortment personalization with large, heterogeneous populations and wide arrays of products, and demonstrate the importance of structural priors for effective, efficient large-scale personalization. Assortment personalization is the problem of choosing, for each individual (type), a best assortment of products, ads, or other offerings (items) so as to maximize revenue. This problem is central to revenue management in e-commerce and online advertising where both items and types can number in the millions.

We formulate the dynamic assortment personalization problem as a discrete-contextual bandit with contexts (types) and exponentially many arms (assortments of the items). We assume that each type’s preferences follow a simple parametric model with parameters. In all, there are parameters, and existing literature suggests that order optimal regret scales as . However, the data required to estimate so many parameters is orders of magnitude larger than the data available in most revenue management applications; and the optimal regret under these models is unacceptably high.

In this paper, we impose a natural structure on the problem – a small latent dimension, or low rank. In the static setting, we show that this model can be efficiently learned from surprisingly few interactions, using a time- and memory-efficient optimization algorithm that converges globally whenever the model is learnable. In the dynamic setting, we show that structure-aware dynamic assortment personalization can have regret that is an order of magnitude smaller than structure-ignorant approaches. We validate our theoretical results empirically.

Personalization, Contextual bandit, Assortment planning, Discrete choice, High-dimensional learning, Large-scale learning, First-order optimization, Recommender Systems, Matrix completion

1 Introduction

In many commerce, e-commerce, and advertising settings, customers or users are presented with an assortment of products, ads, or other offerings. Customers choose which to products to buy, ads to click, or (generically) items to interact with, from among the assortment that is presented. Firms choose which assortment to present to the customer, and collect the revenue (or other benefit or loss) resulting from each customer’s choice. Choosing the assortment that maximizes expected revenue is a central problem in revenue management. This problem goes by the name assortment planning or assortment optimization. When assortments are tailored to each individual customer or to each consumer segment, the problem is known as assortment personalization. Successful personalization, which is key to e-commerce and online advertising operations, hinges on learning the preferences of each customer for each offering.

This paper shows how to learn customer preferences and manage revenue under realistic assumptions about the problem data available and the structure of customer preferences. We suppose that we must rely on transactional data to estimate customer preferences; and that we rely only on the discrete context of each customer’s type (usually, each customer’s unique id) to infer their preferences, for we lack covariates that precisely predict customer outcomes. These assumptions make our problem challenging. We show how to achieve good performance using the one key structural assumption: that customer preferences are low rank. We provide both new algorithms and new results for this setting that enable efficient assortment personalization in the face of high dimensions.

1.1 Problem setting

We next explain the problem setting and discuss the practical importance of each of the main assumptions. The problem setting we consider in this paper is, we believe, the relevant one for most commerce and e-commerce settings.

Transactional data.

Transactional data — which customer selected which product — is abundant and easy for retailers to collect, whereas detailed information about customer attributes (such as gender, age, ethnicity, and preferences) cannot be directly harvested from the retailer’s data. It is natural and even expected that a data driven modern retailer will record transactional data, whereas retailers who buy information on their customers’ attributes face extra costs as well as data quality and privacy concerns. Moreover, these covariates are not directly related to the task at hand: predicting which products the customer will buy, and maximizing revenue. In particular, they may be too coarse to understand customer preferences precisely. For example, even if gender and age information is available, providing the same personalized assortment to all women aged 30 may not be a good strategy when preferences differ. Instead, our approach requires no side information about the attributes of the customers. We rely exclusively on transactional data and focus on personalization at the finest level of segmentation offered by the recorded data (usually, the individual level), using past behavior rather than characteristics to predict future behavior.

Discrete context

In this paper, we define the customer’s type to be the smallest group that is uniquely identifiable given the available data, or anything coarser. This notion is easily applied to the e-commerce setting: here, the retailer records a unique user id as part of each transaction, so each type corresponds to a single customer. This e-commerce setting is the focus of our paper, and the key issue we address is that the number of both types and items may be very large. In a less common setting also covered by our framework, multi-location brick-and-mortar stores with very many locations, one may consider type to be the store location itself with the intent of aggregating data to learn geographically-varying tastes. An algorithm relying exclusively on transactional data lacks any context to use to predict a customer’s behavior other than the type (e.g., customer id) of that customer. Hence we refer to our assortment choice problem as having a discrete context corresponding to this distinct identity. This contrasts usual contextual variables that are continuous vectors related to one another in terms of metric proximity.

Regret analysis.

This paper presents a regret analysis of assortment choices in the discrete-contextual setting. In this setting, ours is the first algorithm that can achieve regret which grows sublinearly not only in the horizon but also in the number of parameters (item-type combinations). The regret of an algorithm is the difference between its cumulative performance and the performance of an idealized method which knows the individual preferences of the customer and always takes the optimal action. (Regret is defined formally in Sec. 2.) That our regret grows sublinearly in the number of item-type combinations means that our time-average performance reaches optimality even in the high-dimensional regime where the number of item-type combinations is large in comparison to the horizon. We further show that no algorithm that ignores the low rank structure of the problem can achieve sublinear regret in the number of item-type combinations. Therefore, since regret in our context amounts to a difference in revenues, the additional revenue generated by our algorithm relative to these is linear in the time horizon in the high dimensional regime.

Low-rank structure.

Our method makes use of one key structural assumption — that preferences are (approximately) low rank — that has been extensively verified in a wide variety of practical applications. These applications range from its earliest uses, in psychology (Spearman 1904, Hotelling 1933), to modern applications in marketing (Funk 2006), genomics (Witten et al. 2009), and healthcare (Schuler et al. 2016). Indeed, under a very natural model for preferences — roughly, as long as customers and products are iid (independent and identically distributed), and there exists some function mapping customer attributes and product attributes to latent utilities — then a table of customer preferences will be approximately low rank (Udell and Townsend 2017). This low-rank structural assumption provides two advantages over previous approaches.

First, it undergirds our regret bound, which guarantees that the regret incurred by our algorithm grows sublinearly in the number of parameters. This result provides a significant advance with respect to the previous literature in both assortment optimization and in matrix sensing. Relative to existing results in assortment optimization, our analysis provides a better scaling as the dimension of the problem grows. Indeed, we prove that any structure-ignorant method must incur regret that grows linearly in the number of preference parameters. Relative to existing results in matrix sensing, our analysis provides the first regret bounds for matrix sensing under bandit feedback. Furthermore, we show how to provably learn a preference matrix in the realistic setting of transactional data, in which we see only which product (if any) the customer has chosen to purchase, rather than a full preference list or a forced choice.

Second, our algorithms make use of the low rank structural assumption to scale to extremely large data sets while preserving provable optimality guarantees. As a result, our methods are well suited to use in practical applications, and can easily be used by any modern retailer. While the assumptions that underly our theoretical guarantees cannot be verified directly, these results demonstrate that the algorithms we propose are effective in practice.

1.2 Our approach

In this paper, we propose a new approach to assortment personalization. To enable tractable estimation of a personalized model with limited data, we propose a new structural model. In this model, the choices of each type are governed by its own personalized preference vector (with one dimension for every item); but these preference vectors span (or lie close to) only a low-dimensional subspace. We demonstrate how to estimate the parameters of this model with computationally tractable algorithms, and provide a proof of recovery with high-probability from few samples (sublinear in number type-item combinations). Numerically, we show that given the same data, our estimator performs much better than standard maximum likelihood estimators.

We then leverage our new model to tackle the dynamic assortment personalization problem: starting with no data, how should we choose assortments to offer to different types to maximize total profit, or equivalently, to minimize total regret? We show theoretically and numerically that our algorithm achieves regret orders of magnitude smaller than standard methods based either on a single multinomial logit (MNL) model or several decoupled MNL models for each type, which we call “structure-ignorant” methods. For example, when the parameter matrix has rank , we achieve regret of order after interactions, where ignoring structure would have yielded regret of order . (Note that for these to make sense, we let , , and all vary simultaneously.) Our results demonstrate that assortment personalization enables orders of magnitude better performance than competing approaches, and can be achieved with a tractable, efficient estimator.

All proofs are given in the appendix.

2 Problem statement

In this section we describe the problem of dynamic assortment personalization. We consider a problem with types and items. During each interaction, a consumer arrives; the retailer presents the consumer with an assortment of no more than items; and the consumer chooses one of the items presented or chooses nothing, which we refer to as choosing the item. The expected revenue generated when type chooses item is and is 0 if no item is chosen. A problem instance is also described by two additional parameters and that are not known and must be estimated from data. The parameter describes how often each type arrives, while the matrix of preference parameters governs MNL choice models, one for each type. The number of parameters in the model is .

The problem proceeds as follows. At first, the retailer knows only , , and . Then for each interaction :

-

1.

Customer of type arrives with probability . The retailer observes the type.

-

2.

The retailer chooses any subset of products with .

-

3.

The customer chooses an item from with probability proportional to

The retailer observes the choice .

-

4.

The retailer collects a random reward with expectation

Notation.

For convenience, define a set of random variables for independent of all variables above. These random variables allow for randomized dynamic assortment personalization algorithms. Define the filtration

is the smallest algebra generated by all variables known at step 2 at time – it captures all information known before the retailer chooses . An algorithm is an assignment to the random variables so that, for every , is measurable with respect to . Given a problem instance and an algorithm , let and be the probability and expectation measures under algorithm : that is, when the sets are selected according to algorithm .

Define the -greedy algorithm, , which chooses

The -greedy algorithm always chooses the assortment that would maximize revenue if were the true choice parameter matrix.

Definition 2.1

Given an instance , the regret of the algorithm at time is

Results.

One of our main results will be to construct an algorithm that exploits low-rank structure in to achieve order-lower regret compared with structure-ignorant algorithms.

Theorem 2.2 (Informal)

If and under some additional technical conditions,

Here we see that the regret grows sublinearly in the dimension of the problem, for fixed rank. We contrast this result with the best rate achievable by an algorithm that ignores the low-rank structure of the problem. A second result extends Theorem 1 of Sauré and Zeevi (2013) to a setting with many types.

Theorem 2.3 (Informal)

If is a structure-ignorant algorithm and under some additional technical conditions,

2.1 Related Work

Assortment personalization requires a good understanding of how consumer tastes vary. Can a retailer learn customer preferences by observing their choices? Discrete choice models posit answers to this question in the form of a probability distribution over choices. Luce (1959) proposed an early discrete choice model based on an axiomatic theory, resulting in the basic attraction model.

Usually, the number of interactions between the firm and customer is limited, so efficient estimation of customer preferences is critical. But estimating customer preferences is no easy task: there are combinatorially many assortments of items, and so without further assumptions, combinatorially many quantities to estimate. To enable tractable estimation, customer preferences are generally modeled parametrically, often using the multinomial logit (MNL) model, which was introduced following the work of McFadden (1973) on random utility theory.

The MNL model posits that customer choices follow a logistic model in a vector of customer preference parameters. Fitting a single MNL model is as simple as counting the number of times an item is chosen relative to the other offerings. (These counts give the maximum likelihood estimate for the model.) The simple MNL model posits a single nominal vector of preferences which governs the choices of all consumers. Individual differences are modeled as random, homogeneous deviations from these universal preferences, and treated as noise. However, these one-size-fits-all models offer no opportunity for personalization and fit heterogeneous populations poorly.

Learning a personalized model often improves performance. A personalized model segments the population into types, and fits a separate model for each type. In the e-commerce and brick-and-mortar settings discussed above, the type is both discrete and known. When the number of types is extremely large, this model is at least as flexible as one which attempts to estimate a unknown type from data. In fact, it is possible to interpret a latent parameter matrix with rank as identifying continuous features which describe each type’s preferences (Udell et al. 2016). Factoring the matrix of preference parameters with and , we may interpret the rows of the left factor as continuous features corresponding to each type, from which preferences may be deduced as a linear function (by multiplying by ). We distinguish these continuous features, which are implicit in our formulation, from the explicit, discrete, and known user type. Our model also generalizes the common latent-class model (Maillard and Mannor 2014): for example, each row of may have exactly one nonzero entry. The index of this entry may be interpreted as indicating the customer segment (Udell et al. 2016).

When each type represents a single customer, the number of observations per type (e.g., the number of distinct purchases) may be quite small. The paucity of data on each type poses a problem for estimation methods which require a number of observations equal to or exceeding the number of products on offer. One solution is to aggregate customers into less fine-grained types using demographic information. Another solution is to use methods, such as those proposed in this paper, that require few observations per type. One surprise in this paper is that the number of observations per type necessary for accurate estimation may be extremely small: for example, simulated data shown in Figure 2 provides evidence that a small number of observations per type — a few tens — can be sufficient, even as the number of types and products increases! Of course, these two approaches can also be used in conjunction: for example, Bernstein et al. (2017) considers how to dynamically cluster customers so as to increase the number of clusters when enough data is available. Jagabathula et al. (2017) provides an alternative approach to combining estimation with customer segmentation.

The MNL model has some more refined variants. For example, the mixture of MNLs (MMNL) model models consumer choice as a mixture of MNL models with different parameters. With sufficiently many mixture components, an MMNL model can approximate arbitrarily closely any choice model that arises from a distribution over individual preferences (McFadden and Train 2000, Farias et al. 2013, van Ryzin and Vulcano 2014). However, the number of interactions needed to estimate a MMNL model is linear in the product of the number of types and the number of items. This is an astronomical figure in most e-commerce and online advertising contexts, where types and items both number in the millions. At the same time, each user can view only so many webpages or consider only so many products — generally, far fewer than the number available. The data from each of these interactions is also limited to a single solitary choice (or lack thereof) out of the assortment. Our main focus in this paper is to develop a new effective method to learn and exploit a personalized preference model despite these limits on the number of observed interactions and the limited nature of the feedback.

Other derivatives of the MNL model can be used to address product substitutes and complements. These include the nested logit model (Williams 1977) and its extensions (McFadden 1980). Recently a new choice model was proposed that arises when substitutions from one good to another are assumed to form a markov chain (Blanchet et al. 2013). Our paper focuses on the issue of personalization and does not consider more complex relationships between products than is modeled by MNL; extending our methods for large-scale personalization to these more nuanced models is a fascinating and important open challenge.

Choosing the optimal assortment can be computationally hard or computationally easy depending on the choice model. Under the MNL model, it is easy to optimize assortments: Talluri and Van Ryzin (2006) show that presenting items in revenue sorted order is always optimal. On the other hand, it is NP-hard to optimize a single assortment to be offered to one MMNL population, even with only two mixture components, but approximation schemes exist (Rusmevichientong et al. 2014). Assortment optimization over the nested MNL model is computationally hard in general (Davis et al. 2014) but easy in some cases (Li et al. 2015). Optimizing an assortment of constrained cardinality under the MNL model is easy (Megiddo 1979, Rusmevichientong et al. 2010), while optimizing an assortment with weighted budget constraint is hard (Désir and Goyal 2014).

Assortment optimization with limited inventory is even more complex. Such problems need to be solved over multiple periods, a different assortment offered each period to take into account possible future stockouts. Talluri and Van Ryzin (2006) solve the classic problem with a single MNL model, while Bernstein et al. (2011), Golrezaei et al. (2014) solve a corresponding problem with a mixture model, representing a few customer segments. In all of these, all preferences of all populations are assumed known.

When preferences are unknown and are to be learned simultaneously with assortment optimization, we can conceive of assortments as bandit arms and consumer choice as bandit feedback to get the problem of dynamic assortment optimization (without context). Rusmevichientong et al. (2010) formulated this problem when choices are governed by a single MNL model and showed that their algorithm has regret upper bounded in order by for items and interactions. Sauré and Zeevi (2013) improved this to and showed that this order is optimal. Earlier, Caro and Gallien (2007) were the first to conceive of dynamic optimization of assortments under learning by studying a related but different problem. Their problem differs in that the demand to be learned is assumed exogenous and independent of the combination offered and other items. The assortments constitute a simultaneous play of multiple arms, rather than an optimal assortment from which a customer chooses zero or one items.

Our dynamic assortment personalization is an instance of a contextual bandit problem with discrete contexts. It arises when at each interaction, a different context, drawn from some finite set, is observed. Based on this discrete contextual information, the problem is to personalize the assortment to target each context as well as possible, while also learning to improve performance. In particular, a good algorithm will use lessons learned in one context to improve performance in other contexts. To the best of our knowledge, we are the first to consider this dynamic assortment personalization problem, and in particular the first to consider any stochastic bandit with discrete contexts, rather than continuous contexts with a functional relationship to rewards (such as linear). Lai and Robbins (1985) posed the classic stochastic multi-armed bandit problem, in which each of arms has an initially-unknown bounded reward distribution and in each time step one chooses one arm to pull with the overall goal of minimal regret: the expected difference in reward between the prescient policy that always pulls the best arm and one’s actual performance. An alternative formulation of the multi-armed bandit problem involves rewards that, instead of being distributed according to a fixed unknown distribution, may change adversarially in response to the choice of arm. For a discussion of the differences between stochastic and adversarial bandits we refer the reader to Bubeck and Cesa-Bianchi (2012). In this paper we focus solely on the stochastic bandit. Examples of contextual stochastic bandits include Rigollet and Zeevi (2010), Perchet and Rigollet (2013), Goldenshluger and Zeevi (2013), Slivkins (2014), Bastani and Bayati (2015), which all focus on the setting with generally unrelated arms, where each arm is associated with a regression function that governs the expected reward conditioned on a continuous vector of covariates representing context. The former two papers assume a general non-parametric functional dependence; the latter three assume a linear regression function. In all these papers, the context is parametrized by a continuous (scalar or vector) quantity; in other words, the relation between different contexts is embedded topologically and known in advance.

In contrast, in the dynamic assortment personalization, the relation between different contexts must be learned from the data. Contexts are discrete; they correspond to rows of an unknown parameter matrix which governs consumer choice. The observation of choice can be likened (imperfectly) to the noisy observation of an entry of the matrix. This analogy brings to mind the problem of matrix completion: the problem of (approximately) recovering an (approximately) low rank matrix from a few (noisy) samples from its values.

Udell et al. (2016) consider how to optimize the convex losses that arise in a general class of entry-wise matrix observation models, such as noisy observation of a few entries of a low-rank matrix. The conditional MNL choice model developed in the present paper moves beyond the models considered in Udell et al. (2016), as each observation depends on several entries in the parameter matrix. Furthermore, we develop new statistical guarantees and dynamic extensions that are beyond the scope of (Udell et al. 2016).

Some of our results are in the same vein as statistical matrix completion bounds. Following groundbreaking work on exact completion of exactly low rank matrices whose entries are observed without noise (Candès and Tao 2010, Candès and Recht 2009, Recht et al. 2010, Keshavan et al. 2010), approximate recovery results have been obtained for a variety of different noisy observation models. These include observations with additive gaussian (Candès and Plan 2009) and subgaussian (Keshavan et al. 2009a) noise, 0-1 (Bernoulli) observations (Davenport et al. 2014), observations from any exponential family distribution (Gunasekar et al. 2014), and observations generated according to the Bradley-Terry-Luce model for pairwise comparisons (Lu and Negahban 2014, Oh et al. 2015). These are most related to our Theorem 3.1, which explores the static estimation problem.

Our Theorem 3.1 differs from previous work on matrix recovery in at least three critical ways. First, the data for our problem consists of choices from an assortment, rather than entrywise observations of ratings, pairwise comparisons, or full rankings; second, Theorem 3.1 holds when assortments are subsets of the full set of items, rather than chosen iid with replacement so that duplicate items sometimes appear; and third, customers in our model can choose not to purchase any item from the presented assortment. In sum, Theorem 3.1 shows how high dimensional parameters can be recovered from a sublinear number of transactional observations of consumer choice.

A variety of techniques have been developed in the literature to analyze the recovery of high dimensional parameters using regularized maximum likelihood. Our proof of Theorem 3.1 uses the machinery of restricted strong convexity originally developed by Negahban and Wainwright (2011), Negahban et al. (2012) and applied to the case of noisy matrix completion and other entrywise observation models. The present paper leverages this machinery and extends it to our setting, where we observe assortment choices rather than individual entries of the matrix of preference parameters, and thereby moves beyond the sorts of entrywise models analyzed in Negahban and Wainwright (2011), Negahban et al. (2012). As reviewed in Section 3.2.3, because observations depend on several entries of the parameter matrix, this extension relies on a multivariate Rademacher comparison lemma (Bertsimas and Kallus 2014, Lemma 7) to establish the desired restricted strong convexity. This lemma occurred as a technical lemma in an unrelated result in Bertsimas and Kallus (2014), which studies conditional stochastic optimization given continuous contextual information using local reweighting schemes. Beyond Theorem 3.1, which studies the recovery of from a static dataset, this paper further shows how to use this static result in a dynamical setting. In Section 2, we describe the high-dimensional contextual dynamic assortment personalization problem for which this paper provides a novel algorithm and analysis.

3 The Low-Rank Conditionally Multinomial Logit Choice Model

In this section we describe the low-rank conditionally multinomial logit choice (LRCMNL) model, study the static estimation problem under observing only choice, propose an estimator, prove recovery bounds, and develop a fast algorithm for computing the estimator from large-scale data.

The conditionally MNL (CMNL) model over types and items is parameterized by and and describes two random variables: type and choice . Type is assumed to be distribution according to

For any given assortment , choice is assumed to be distributed according to the following model

| (1) | ||||

where represents the choice not to choose from – an option that is always available for any assortment .

The LRCMNL model posits a CMNL model in which the parameter has low rank:

We will also consider the case where has approximately low rank:

where is the sum of the singular values of smaller than the largest singular value, i.e.,

| (2) |

3.1 Implications of the LRCMNL Model

Let us consider when the choice distribution should follow a LRCMNL model.

Suppose that each individual in the population makes rational choices: that is, choices maximize utility with respect to a vector of utilities randomly distributed over the population. This is called a random utility choice model. The approximation results of McFadden and Train (2000) show that for any random utility choice model, there is a variable such that the choice distribution is approximately MNL conditioned on . If is an observed variable, then this corresponds to a CMNL model. More generally, this result suggests that for any sufficiently fine partition of types , the CMNL model forms a reasonable approximation of the choice model. That is, while a large population may have a complex choice model due to heterogeneity of individuals, the MNL choice model should provide a good approximation for the decisions made by a single individual.

Conversely, any CMNL model, including the LCMMNL model, inherits an interpretation as a random utility choice model from the MNL model. Let be the mean utility type enjoys from item . Let us suppose that the utility of each customer of type is the sum of the mean utility of type together with a random idiosyncrasy distributed according to the Gumbell (extreme value) distribution, and that each customer chooses an item by maximizing her utility among the items on offer:

| (3) |

The LRCMNL model (1) can therefore arise in either of two ways. It describes choice behavior when customers are clustered into types within each of which customers have a private, idiosyncratic utility distributed as in (3) and the heterogeneity of the population is described by the varying mean utilities over types . The LRCMNL model also describes choice behavior when each customer is her own type. The random idiosyncrasies associated with each choice event reflect human inconsistencies in decision making or slight variations over time in preferences (Kahneman and Tversky 1979, DeShazo and Fermo 2002).

Learning the preferences of multiple, heterogeneous customer types simultaneously is difficult without additional structure. Both Bernstein et al. (2011) and Golrezaei et al. (2014) study multi-period assortment optimization problems with multiple, heterogeneous customer types assuming full knowledge of the distribution of consumer choice. Both undertake case studies in which they estimate these distributions from static data in order to evaluate the performance of their optimization algorithms on distributions that mimic real data. However, in both cases, they allow only a few segments (3 and 10, respectively). One reason for this choice may be that estimation becomes intractable for models with many more segments. Our model, by contrast, can tractably estimate distributions with large numbers of types and items. We overcome limitations of previous models by assuming that the underlying dimension of the model is small in the sense that our parameter matrix has (approximate) low rank.

If has (approximate) rank , we may factor to find vectors for such that is (approximately) equal to . The right factors can be thought of as latent item features, and the left factors as latent type weights which characterize how much type values feature . When has (approximate) low rank, we can be sure that just a few latent features suffice to (approximately) explain consumer choice, and these latent features need not be measurable or have a physical interpretation. Indeed, the number of features that matter for decision making may be constrained by cognitive load: to consider many features would require proportional time and energy. However, even if consumer utility is a non-linear function of item features, and even if the number of features required to describe an item is extremely large, Udell and Townsend (2017) prove that large enough preference matrices are still approximately low rank so long as types and items are drawn iid from some population.

In summary, the LRCMNL model is implied by the assumption that choice is rational with a utility distribution with means that depend on only a few (possibly unknown) features. Usually very few features suffice due to the finite range of human perception and rationality or simply due to concentration of measure.

3.2 The Static Estimation Problem

Next, we describe an observation model and the problem of estimating the LRCMNL parameters from observed data. We suppose that we have observations where is sampled uniformly at random from the set of subsets of of size , the sequence is arbitrary (possibly random) satisfying , and are iid according to the model (1). We also assume that for purely technical reasons. The assumption of (normalized) bounded entries assumption is standard in many matrix completion recovery results (see Section 2.1) and is necessary for our proof of recovery with high probability; see below.

It is important to highlight that our observation model consists of observing only the choice made by customers. In practical applications, this is typically the only observation possible. Moreover, it is generally truthful since it is utility maximizing, unlike reporting rankings in a survey or focus group.

3.2.1 Our Estimator

Define the negative log likelihood of the observations given parameter as

| (4) |

We define our estimator for as any solution of the nuclear norm regularized maximum likelihood problem

| (5) |

where is a tuning parameter and the nuclear norm is the sum of the singular values of . We use to denote the solution to this problem.

The constraint appears purely as an artifact of the proof; we recommend to omit this constraint in practice. We omit this constraint both in our specialized algorithm (Section 3.3) and in our numerical results (Section 5); the good practical performance on examples demonstrates the practical irrelevance of this constraint.

Problem (5) is convex and hence can be solved by a variety of standard convex methods that take advantage of the special structure of the problem (Cai et al. 2010, Parikh and Boyd 2014, Hazan 2008, Orabona et al. 2012). In Section 3.3 we provide a specialized first-order algorithm that, in fact, works on the non-convex, factored form of the problem for increased speed, but still guarantees convergence to the global optimum with high probability.

Our estimator for the customer type distribution is the empirical frequencies of each type:

3.2.2 Recovery Guarantee for the Parameter Matrix

In this section, we bound the error of the estimator . Our bound depends on the following quantities, which capture the complexity of learning the preferences of all customer types over all items.

-

•

Number of observations. The bound decreases as the number of observations increases.

-

•

Number of parameters. The bound grows with the dimensions of the parameter matrix .

-

•

Underlying rank dimension. For any , our bound decomposes into two error terms. The first error term is the error in estimating the top “principal components” of the parameter matrix. This error term grows with and captures the benefit of learning only the most salient features instead of all parameters at once. The second error term is the error in approximating the parameter matrix by only its top “principal components.” In particular, if is exactly rank , then this second error term vanishes. More generally, however, we may be interested in estimating parameter matrices that are only approximately low rank, i.e., with quickly decaying singular values past the top . In this case, our bound depends on the sum of the remaining singular values.

-

•

Size of parameters. Our bound grows with the (scaled) maximum magnitude of any entry .

-

•

Size of assortments. Our bound grows with the maximum size of the assortments.

Theorem 3.1

Let be given, be such that , and be such that . Fix . Suppose . Then under the observation model in Section 3.2 and for any integer , with probability at least , any solution to Problem (5) satisfies

where is the sum of the remaining singular values of smaller than the largest singular value, as defined in eq. (2).

A few remarks on this theorem are in order.

-

•

If were exactly low rank (), then a number of observations scaling slightly faster than are needed in order to obtain a consistent estimate for . That is to say, if the number of products is growing no faster than the number of types and rank is bounded , then the number of observations per type, , needed in order to estimate everyone’s preferences consistently is logarithmic, .

-

•

The first term in the bound represents the estimation error: the difficulty of estimating the top rank- approximation to from only samples. The second term in the bound represents the approximation error in the model: the error incurred because the target rank is smaller than the true rank of . This term is zero when and is small when the singular values of that are smaller than the smallest one are small.

-

•

The choice of does not depend on and the result holds for any . That means that it is not necessary to know the rank or approximate rank of – as long as it has (approximate) low rank for some unknown but not too large , our algorithm will be able to recover with high fidelity.

-

•

The proof of this theorem requires a bound on the maximum number of observations used to fit the estimator. From a practical perspective, this upper bound presents no difficulties: generally, the estimation problem is hard when few observations are available; whereas when simpler approaches such as maximum likelihood estimation can perform well and give consistent estimates. Furthermore, in high-dimensional settings it is generally impossible to exhaustively sample all type-item pairs; hence as a practical matter, we will always have that holds. We discuss this at greater length in the dynamic setting in Section 4.2.

-

•

The parameter controls the probability of the result. Choosing , we see the theorem already holds with extremely high probability, which converges to as either or grow. Other values for give greater generality to the theorem. We will see a more sophisticated use of this probability control in the proof of Theorem 4.4.

A closely related result to Theorem 3.1 appeared in our preliminary work (Kallus and Udell 2016), which focuses only on the static estimation problem and only in the absence of the no-choice option. In assortment personalization, we must consider estimation in the permanent presence of a no-choice option in any assortment and where the mixtures are not necessarily uniform, and we must also consider the decision problem involved in dynamically offering personalized assortments. None of these appear in our brief preliminary work.

3.2.3 Proof sketch for Theorem 3.1

In low dimensions, a standard proof that the minimizer of a loss function is close to the true parameters shows 1) the loss function is strongly convex, and 2) the the true parameters achieve low loss. Since the loss is strongly convex, any near-optimal parameter must be close in Euclidean distance to the optimal one. However, the loss function we use is not strongly convex, nor can it be until every item has been offered to every type.

Instead, we argue as follows. 1) The nuclear norm of the error controls its square Frobenius norm. The proof of this uses random sampling to show that the Bregman divergence of the loss function is (with high probability) strongly convex around , and uses the form of the objective to bound this Bregman divergence above by the nuclear norm. 2) The Frobenius norm of the low rank matrix controls its nuclear norm. We combine these statements to bound the Frobenius norm of the error .

The three key steps in our proof use the three important ingredients in our method: random sampling, regularized empirical risk minimization, and an approximately low rank parameter matrix.

-

0.

Our proof fundamentally relies on establishing the following inequality

(6) which shows that the nuclear norm of the error controls the square Frobenius norm of the error. We begin our proof by defining a set so that eq. (6) holds by definition for any :

(Recall holds by assumption.)

The rest of our proof will show that eq. (6) holds, with high probability, even when .

-

1.

Our main task is to show restricted strong convexity: our loss function is strongly convex around when is restricted to . This is established by proving that (with high probability, for every ) the Bregman divergence of our loss function,

bounds (a constant times) the square Frobenius error .

-

(a)

We first prove that this bound holds in expectation. In Lemma 8.1, we use Taylor’s theorem to show

The expectation of the empirical process is at least because the observed sets are sampled randomly.

-

(b)

The second step, and the key to our proof, is to show that this process concentrates uniformly around its expectation for all . A major difficulty arises due to our particular observation model: depends on several entries of at once. This dependence is key to modeling a realistic e-commerce setting where customers do not purchase more than one similar item and where customers retain the option not to purchase any item at all. We are not aware of other related work that can handle this dependence. For example, (Oh et al. 2015) avoid the problem by sampling items with replacement and without a no-purchase option.

Our proof proceeds as follows. We first peel by intersecting it with concentric spherical shells: where , , and . In Lemma 8.8, we study in each peel separately the maximal deviations of the empirical process from its expectation,

We first show that is itself concentrated near its expectation, so we need only bound its expectation. Using a symmetrization argument, we let be iid Rademacher variables (equiprobably ) and show that , known as the Rademacher complexity. Computing this quantity is made difficult because a) depends on multiple elements of and b) the identity of these elements is not independent because sampling is without replacement. We therefore use a multivariate Rademacher comparison lemma (Bertsimas and Kallus 2014, Lemma 7) in order to prove that

where are new iid Rademacher variables. This latter complexity is much simpler and amenable to analysis. Using the concentration of random matrices (Tropp 2012), we control it by the norm of , which is bounded by the peeling construction.

-

(c)

In Lemma 8.2, we use a union bound over the peels to obtain the desired restricted strong convexity: with high probability,

(7)

-

(a)

-

2.

In Lemma 8.4, we show that our choice of nuclear-norm-regularized log likelihood objective allows us to bound the Bregman divergence above as follows

This quantity is controlled by the optimality of in the log likelihood objective in terms of its first-order condition. In Lemma 8.3, by leveraging random matrix concentration bounds (Tropp 2012), we show that is near optimal with high probability:

where the last inequality is by our choice of . Combining , our choice of , and eq. (7) shows that eq. (6) holds even for (with high probability).

-

3.

Finally, in Lemma 8.5, using a spectral decomposition argument, we show that, if is low rank or approximately low rank and also near-optimal in that , then the nuclear norm of is tightly controlled by the Frobenius norm of :

(8)

3.2.4 Recovery Guarantee for the Customer Type Distribution

In this section, we bound the error in our estimator for the true customer type distribution .

Theorem 3.2

Let and be given. With probability at least ,

The second term in the above min is immediate from applying Hoeffding’s inequality to each component and using the union bound. For and any , however, the Hoeffding-based bound diverges for any (in general it goes to zero only for ). We derive the first term using a Rademacher complexity argument. The first term goes to zero for any as long as grows superlinearly in . This first term is critical for showing that can be estimated consistently in the norm for . In particular, the theorem provides for -consistent estimation of the type distribution in the norm.

3.3 A Factored Gradient Descent Algorithm

In this section, we develop a specialized first-order algorithm for computing that works on the non-convex, factored form of the nuclear-norm regularized likelihood optimization problem. The algorithm is particularly economical with memory because (a) it does not keep all optimization variables in memory but rather only where is a guess at rank and (b) it eschews the use of any spectral computation such as SVD (or partial SVD) at each iteration. This makes the algorithm particularly useful for the large scale data encountered in e-commerce applications.

Our factored gradient descent (FGD) algorithm solves the problem

| (9) |

As discussed in Section 3.2, the algorithm we employ does not enforce any constraint on . A constraint of this form is necessary for the technical result in our main theorem, but is unnecessary in practice, as can be seen in our numerical results in Section 5.

In applications, one is interested in solving the problem (9) for very large . Due to the complexity of Cholesky factorization, this rules out theoretically-tractable second-order interior point methods. One standard approach is to use a first-order method, such as Cai et al. (2010), Parikh and Boyd (2014), Hazan (2008), Orabona et al. (2012); however, this approach requires (at least a partial) SVD at each step. An alternative approach, which we take here, is to optimize as variables the factors and of the optimization variable rather than producing these via SVD at each step; see, e.g., Keshavan et al. (2009b), Jain et al. (2013). To guarantee equivalence of the problems, we must take . However, if we believe the solution is low rank or if we want to enforce low rank, then we may use a smaller , reducing computational work and storage.

Our FGD algorithm proceeds by applying gradient descent steps to the unconstrained problem

| (10) |

This formulation has the advantage of being unconstrained, with a differentiable objective function, making it amenable to solution via simple optimization methods (Recht et al. 2010, 2011, Udell et al. 2016).

Lemma 3.3

Problem (10) is equivalent to

| (11) |

That is, Problem (10) is equivalent to Problem (9) subject to an additional rank constraint . If, for a particular choice of loss function , Problem (9) has a solution with rank less than , then the rank constraint is not binding, so Problem (9) is itself equivalent to Problem (10). (Recall that we defer all proofs to the Appendix.)

It is easy to compute the the gradients of the objective of (10). Since is differentiable,

We do not need to explicitly form in order to compute these; computing gradients implicitly reduces the memory required to implement the algorithm (see Algorithm 1). Similarly, we need not form to compute . Recent work has shown that gradient descent on the factors converges linearly to the global optimum for problems that enjoy restricted strong convexity (Bhojanapalli et al. 2015). In eq. (16) in the proof of Theorem 3.1 we establish restricted strong convexity for our problem with high probability. Hence with high probability, FGD converges to the global minimum of Problem (10), and hence to the global minimum of Problem (9) provided is chosen to be large enough.

We initialize our algorithm using a technique from Bhojanapalli et al. (2015), which only requires access to gradients of the objective of (9). Using the SVD, we write and initialize

where and , denote the first columns of , . We use an adaptive step size with a line search that guarantees descent. Starting with a stepsize of , the stepsize is repeatedly decreased by a factor until the step produces a decrease in the objective. We terminate the algorithm when the decrease in the relative objective value is smaller than the convergence tolerance .

4 The Dynamic Assortment Personalization Problem

We now return to the dynamic setting. First, we define some notation that will be useful in the following discussion. For , , , and , let

| the MNL choice probability under parameters , | ||||

| the expected revenue of assortment under , and | ||||

| the set of optimal assortments under for revenues . |

4.1 Structure-ignorant algorithms

An algorithm is structure-ignorant if it ignores any potential structure that connect the different contexts (rows of ). Therefore, a structure-ignorant algorithm is one that runs separate, independent algorithms for each context. Formally, we make the following definition.

Definition 4.1

An algorithm for the dynamic assortment personalization problem is structure-ignorant if, under , the variable is measurable with respect to only the historical data from type , , and the variables .

An algorithm is said to be consistent if it has sublinear regret in over all problem instances.

Definition 4.2

Fix . An algorithm is said to be consistent if for any , and , we have over all problem instances .

For brevity, we usually omit the subscript and abuse notation in referring to a family or sequence of algorithms simply as one algorithm .

If we run separate algorithms for each context then, in each context, we are solving the classic (non-contextual) dynamic assortment planning problem, precisely as studied by Rusmevichientong et al. (2010), Sauré and Zeevi (2013). Making use of Theorem 1 of Sauré and Zeevi (2013) we establish the following:

Theorem 4.3

Fix , , . Given any family (indexed by revealed problem parameters ) of structure-ignorant consistent algorithms , we have

over all times and problem instances such that

-

1.

grows superlinearly in the number of types : for some , .

-

2.

For every type :

-

(a)

Profit is bounded:

-

(b)

The type appears often enough and not too often:

-

(c)

The number of potentially optimal items grows linearly in :

-

(a)

4.1.1 Proof sketch for Theorem 4.3

To prove Theorem 4.3, we argue as follows. Let so that is the expected instantaneous regret at time , averaged over Let be the number of times type is encountered. We use a conditioning argument, a concentration bound on , and the fact that to argue that

This bound shows that the regret is at least half the sum of regrets incurred in each context seen at least times. We invoke Sauré and Zeevi (2013, Theorem 1) to provide a lower bound on the right hand side for each context when the algorithm plays each context independently.

4.1.2 Discussion of Theorem 4.3

Note that . We rewrite the product in this way to make the comparison with our structure-aware algorithm more clear: it depends on , but replaces the term by the rank of the parameter matrix .

Theorem 4.3 asserts that structure-ignorant algorithms for the dynamic assortment personalization problem have regret that grows linearly in the number of item-type combinations and logarithmically in the time horizon. That is, ignoring structure incurs enormous regret. In the sequel, we improve on this regret bound by developing a structure-aware algorithm.

4.2 A Structure-Aware Algorithm

In Section 3, we argued that imposing structure is crucial for learning the preferences of a very heterogeneous population and proposed an estimator that can leverage structure to learn the LRCMNL model in sublinear time. In this section, we use this estimator to develop a structure-aware algorithm that can achieve regret sublinear in problem size .

In Algorithm 2, we define an algorithm for dynamic assortment personalization with tuning parameters and . We refer to this algorithm as .

Every step of Algorithm 2 is computationally tractable, including the computation of the optimal assortment (Rusmevichientong et al. 2010) and of (Algorithm 1). The optimal assortments for each type need only be recomputed when the parameter estimate changes. These changes happen only on exploration steps, which occur a vanishing fraction of the time as increases. Hence we need only compute optimal assortments a vanishing fraction of the time.

Next we show that this achieves regret that is orders of magnitude smaller than a structure-ignorant algorithm when structure is present. Let

be the gap in revenue between the optimal assortment and any suboptimal assortment under MNL choice with parameter vector .

Theorem 4.4

Let be such that , be such that , be such that , be such that , and be such that . Choose as algorithm parameters

| (12) |

Then the regret of satisfies

for all .

4.2.1 Proof sketch for Theorem 4.4

To prove Theorem 4.4, we argue as follows. We first establish that expected revenue is smooth with respect to the parameter : . Therefore, for any two different parameter vectors and together with corresponding optimal sets and , the expected revenue under parameter cannot change much when we replace the set by :

Hence if is small enough, the optimal assortments for each are the same:

We combine this result with Theorem 3.1 (choosing ) to argue that the average instantaneous regret at any time when Algorithm 2 chooses to exploit must be bounded as

To complete the proof, note that Algorithm 2 chooses to explore no more than times.

4.2.2 Discussion of Theorem 4.4

Notice that the time horizon appears in Theorem 4.4, but does not appear in Algorithm 2. In particular, the horizon need not be known in advance to run Algorithm 2, and for any time Theorem 4.4 provides a valid regret bound on our horizon-independent algorithm. Specifically, this restriction applies in the high-dimensional setting of interest, with no more observations than the number of item-type combinations (). If Theorem 4.4’s restriction were violated, which is unrealistic in the high-dimensional setting, it would mean that there is enough time to leisurely learn each user’s preferences completely separately as even a structure ignorant algorithm can achieve vanishing time-average suboptimality: as . Thus, Theorem 4.4 exactly captures the regime of interest.

| Regret | Uninformative | High-dimension | Low-dimension |

| Linear | Sublinear | Sublinear | |

| Linear | Linear | Sublinear |

Comparing to Theorem 4.3, Theorem 4.4 shows that leveraging structure appropriately can lead to regret that is an order of magnitude smaller than that of structure-ignorant algorithms. Specifically, we find that the ratio of the regret of any structure-ignorant algorithm to that of our algorithm grows at least as fast as . Since , our algorithm performs at least as well as any structure-ignorant algorithm. And whenever the rank of grows more slowly than its side dimension, , our algorithm performs strictly better. The improvement is largest when the rank is constant: in this case, the regret ratio grows linearly in the side dimension . Whenever , because our regret grows more slowly, the difference between the regret of any structure-ignorant algorithm to that of our algorithm is . In other words, the additional revenue that our algorithm generates relative to any structure-ignorant algorithm grows at such a rate, highlight the revenue impact of our algorithm.

In order to understand the different regret regimes, let us consider a setting with equal side dimension, , and bounded rank, . If then we can only interact with each user at most a constant number of times. Therefore it is impossible to consistently learn the choice model, since the number of observations is of the same order of the number of parameters. Hence the regret of any algorithm must be linear in . We must have more observations () to learn the choice model consistently and just slightly more than that () to ensure sublinear regret. If the horizon is slightly longer than the number of users, , our algorithm, which incurs regret in this case, will achieve sublinear regret in . However, in the same setting, as long as , a structure ignorant algorithm incurs linear regret in (by Theorem 4.3). If the horizon is much larger than the number of user-item combinations, , than even algorithms that ignore structure can achieve sublinear regret: we have enough observations to learn each user’s preferences independently. Hence both our algorithm and any efficient structure ignorant algorithm (e.g., using the method of Sauré and Zeevi (2013) for each user separately) achieve sublinear regret.

We summarize the above observations in Table 1 in the more general unequal side dimension case. In the table we abbreviate as and similarly for . The table shows the three informational regimes: an uninformative regime where there can be no hope of linear regret, a high-dimensional regime where algorithms must use cross-user information and latent structure to achieve sublinear regret, and a low-dimensional regime where cross-user information is not required achieve sublinear regret.

Note that in Theorem 4.4, that the choice of parameters for Algorithm 2 depend on the lower bound, , on the revenue gap between the optimal assortment and any suboptimal assortment. This dependence agrees with previous work on dynamic assortment planning (Rusmevichientong et al. 2010, Sauré and Zeevi 2013), which also proposes algorithms and regret analyses that require prior knowledge of this gap. Removing this dependence in our Algorithm 2 is an important problem for future research. Recently, Agrawal et al. (2017) addressed this issue in the classic, non-contextual dynamic assortment planning problem, developing a new algorithm that does not depend on the optimality gap.

5 Experimental Results

In this section we demonstrate numerically the importance of structure and the power of our approach.

5.1 The Static Estimation Problem

First, we focus on the static estimation problem. We compare our estimate with the standard maximum likelihood estimate that solves

| (13) |

Note that, since it imposes no structure on the whole matrix , problem (13) decomposes into subproblems for each type (row of ), each solving a separate MNL MLE in variables. In our experiments, we use Newton’s method as implemented by Optim.jl to solve each subproblem.

To generate , we fix , let be an matrix composed of independent draws from a standard normal, take its SVD , truncate it past the top components , and renormalize to achieve unit sample standard deviation to get , i.e., . To generate the choice data, we let be drawn uniformly at random from , be drawn uniformly at random from all subsets of size , and be chosen according to (1) with parameter .

For our estimator we use Algorithm 1 with , , , and . This regularizing coefficient scales with , , , , and as suggested by Theorem 3.1, but we find the algorithm performs better in practice when we use a smaller constant than that suggested by the theorem.

We plot the results in Figure 1, where error is measured in root mean squared error (RMSE)

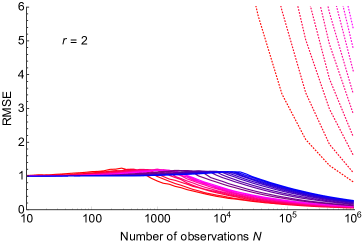

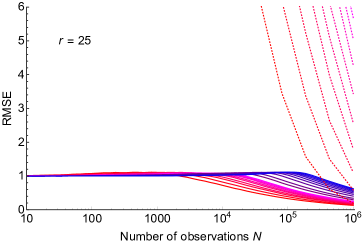

The results show the advantage in efficient use of the data offered by our approach. The results also show that, relative to MLE, the advantage is greatest when the underlying rank is small and the number of parameters is large, but that we maintain a significant advantage even for moderate and . For large numbers of parameters (), the RMSE of MLE is very large and does not appear in the plots. Only in the case of greatest rank (), smallest number of parameters (), and greatest number of observations () does MLE appear to somewhat catch up with our estimator.

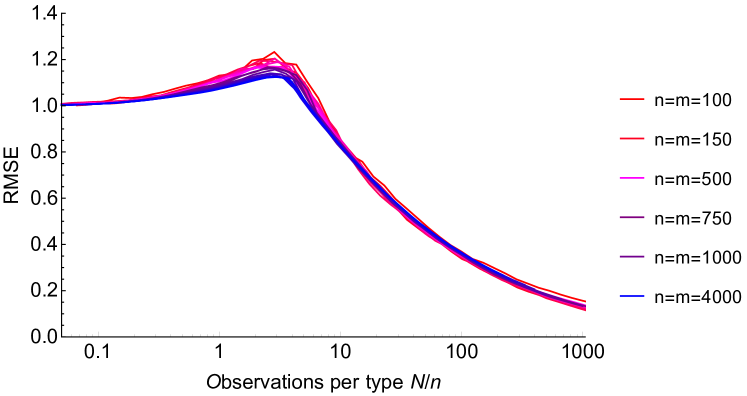

In Figure 2, we plot the RMSE of our estimator against the number of observations per type (or item) for a square problem with . We see nearly the same error curve traced out as we vary the problem size . This scaling shows that our estimator is able to leverage the low-rank assumption and require the same number of choice observations per type to achieve the same RMSE regardless of problem size. Thus, even in high dimensions, if customer behavior is dictated by a bounded number of (latent) factors, then our approach need only rely on a small number of observations per type.

5.2 The Dynamic Assortment Personalization Problem

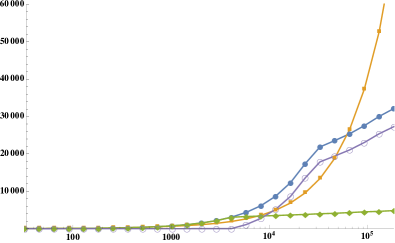

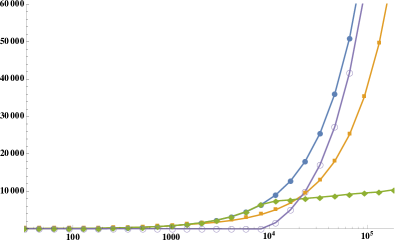

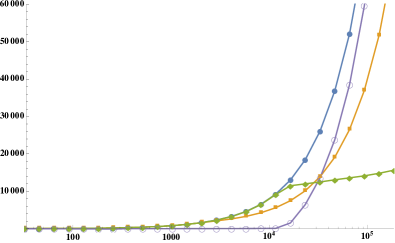

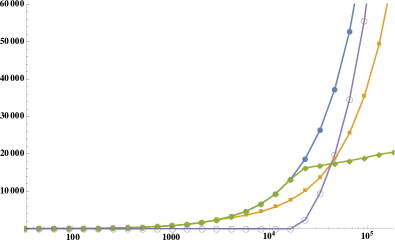

Next, we turn our attention to the dynamic assortment personalization problem. We compare our algorithm to two alternatives. One alternative () is the structure-ignorant algorithm in which we apply Algorithm 1 of Sauré and Zeevi (2013) to each type separately. Recognizing that one cannot learn a huge set of parameters from very few observations, the second alternative () tries to fit a single MNL model to the whole population, applying only one replicate Algorithm 1 of Sauré and Zeevi (2013) to all types simultaneously. We generate the problem exactly as in the previous section and run each of these algorithms on problem dimensions varying from 10,000 to 160,000 and for . We plot the regret of each of these algorithms over time in Figure 3. We also include the regret of relative to our (“Revenue impact”), which is just the difference of their regrets relative to the optimal policy since this baseline will cancel. This quantifies the revenue impact of our algorithm in terms of the additional revenue we can generate using our structure-aware algorithm.

Since the plots have a logarithmic horizontal axis, regret that is logarithmic in appears as a line in the figure whereas regret that is linear in appears as an exponential function. These plots reveal several interesting features of the algorithms.

We see that the structure-ignorant algorithm, which we know has logarithmic regret asymptotically, only achieves logarithmic regret for the smallest of the problems (). For larger problem sizes, regret appears to be linear for all horizons shown. The transition from linear to logarithmic regret is not visible because the problems are so large that the transition occurs for extremely large : on the scale of this plot, the term overwhelms the term.

In all of these larger problems, the context-ignorant algorithm performs better than the structure-ignorant algorithm. Both have linear regret in this parameter regime. In fact, the context-ignorant algorithm uses a misspecified model, and so has asymptotically linear regret. Hence for very large (not shown on this plot) it will be overtaken by the structure-ignorant algorithm, whose regret is asymptotically logarithmic. The success of the misspecified context-ignorant algorithm holds an important lesson: when time is limited, it is more effective to use a misspecified model with few parameters than a well specified model with many parameters.

On the other hand, our structure-aware algorithm exhibits logarithmic regret in each and every case, even at this relatively short time scale. The algorithm , as promised by Theorem 4.4, has logarithmic regret that does not explode astronomically with . Correspondingly, it achieves significant revenue impact relative to the structure-ignorant algorithm as shown in Figure 3.

6 Conclusion

To manage revenue, many retailers must solve a dynamic assortment personalization problem: they must learn customers preferences in real time, at scale, from customers’ choices from among the items on offer; and they must quickly use this information to present revenue-maximizing assortments. This paper explores a structural approach to enable large scale dynamic assortment personalization. We proposed algorithms using structural (low rank) priors to learn and exploit customer preferences. We presented theoretical and numerical evidence that these algorithms improve on the state of the art by orders of magnitude, and achieve performance suitable for use in practice.

The authors thank several anonymous reviewers for their guidance in improving this manuscript. NK was supported by the National Science Foundation under Grant No. 1656996. MU was supported by DARPA Award FA8750-17-2-0101 and by a fellowship awarded by the Center for the Mathematics of Information at Caltech.

References

- Agrawal et al. (2017) Agrawal S, Avadhanula V, Goyal V, Zeevi A (2017) Mnl-bandit: A dynamic learning approach to assortment selection. arXiv preprint arXiv:1706.03880 .

- Bartlett and Mendelson (2003) Bartlett PL, Mendelson S (2003) Rademacher and gaussian complexities: Risk bounds and structural results. The Journal of Machine Learning Research 3:463–482.

- Bastani and Bayati (2015) Bastani H, Bayati M (2015) Online decision-making with high-dimensional covariates. Available at SSRN 2661896 .

- Bernstein et al. (2011) Bernstein F, Kök AG, Xie L (2011) Dynamic assortment customization with limited inventories. Technical report, Citeseer.

- Bernstein et al. (2017) Bernstein F, Modaresi S, Sauré D (2017) A dynamic clustering approach to data-driven assortment personalization .

- Bertsimas and Kallus (2014) Bertsimas D, Kallus N (2014) From predictive to prescriptive analytics. arXiv preprint arXiv:1402.5481 .

- Bhojanapalli et al. (2015) Bhojanapalli S, Kyrillidis A, Sanghavi S (2015) Dropping convexity for faster semi-definite optimization. arXiv preprint arXiv:1509.03917 .

- Blanchet et al. (2013) Blanchet J, Gallego G, Goyal V (2013) A Markov chain approximation to choice modeling. EC, 103–104.

- Bubeck and Cesa-Bianchi (2012) Bubeck S, Cesa-Bianchi N (2012) Regret analysis of stochastic and nonstochastic multi-armed bandit problems. Machine Learning 5(1):1–122.

- Cai et al. (2010) Cai JF, Candès EJ, Shen Z (2010) A singular value thresholding algorithm for matrix completion. SIAM Journal on Optimization 20(4):1956–1982.

- Candès and Plan (2009) Candès E, Plan Y (2009) Matrix completion with noise. CoRR abs/0903.3131.

- Candès and Recht (2009) Candès E, Recht B (2009) Exact matrix completion via convex optimization. Foundations of Computational Mathematics 9(6):717–772.

- Candès and Tao (2010) Candès E, Tao T (2010) The power of convex relaxation: Near-optimal matrix completion. IEEE Transactions on Information Theory 56(5):2053–2080.

- Caro and Gallien (2007) Caro F, Gallien J (2007) Dynamic assortment with demand learning for seasonal consumer goods. Management Science 53(2):276–292.

- Davenport et al. (2014) Davenport M, Plan Y, van den Berg E, Wootters M (2014) 1-bit matrix completion. Information and Inference 3(3):189–223.

- Davis et al. (2014) Davis JM, Gallego G, Topaloglu H (2014) Assortment optimization under variants of the nested logit model. Operations Research 62(2):250–273.

- DeShazo and Fermo (2002) DeShazo J, Fermo G (2002) Designing choice sets for stated preference methods: the effects of complexity on choice consistency. Journal of Environmental Economics and management 44(1):123–143.

- Désir and Goyal (2014) Désir A, Goyal V (2014) Near-optimal algorithms for capacity constrained assortment optimization. Available at SSRN 2543309 .

- Farias et al. (2013) Farias VF, Jagabathula S, Shah D (2013) A nonparametric approach to modeling choice with limited data. Management Science 59(2):305–322.

- Funk (2006) Funk S (2006) Netflix update: Try this at home. URL http://sifter.org/~simon/journal/20061211.html.

- Goldenshluger and Zeevi (2013) Goldenshluger A, Zeevi A (2013) A linear response bandit problem. Stochastic Systems 3(1):230–261.

- Golrezaei et al. (2014) Golrezaei N, Nazerzadeh H, Rusmevichientong P (2014) Real-time optimization of personalized assortments. Management Science 60(6):1532–1551.

- Gunasekar et al. (2014) Gunasekar S, Ravikumar P, Ghosh J (2014) Exponential family matrix completion under structural constraints. Proceedings of the 31st International Conference on Machine Learning (ICML-14), 1917–1925.

- Hazan (2008) Hazan E (2008) Sparse approximate solutions to semidefinite programs. LATIN 2008: Theoretical Informatics, 306–316 (Springer).

- Hotelling (1933) Hotelling H (1933) Analysis of a complex of statistical variables into principal components. Journal of Educational Psychology 24(6):417.

- Jagabathula et al. (2017) Jagabathula S, Subramanian L, Venkataraman A (2017) A model-based projection technique for segmenting customers. arXiv preprint arXiv:1701.07483 .

- Jain et al. (2013) Jain P, Netrapalli P, Sanghavi S (2013) Low-rank matrix completion using alternating minimization. Proceedings of the forty-fifth annual ACM Symposium on the Theory of Computing, 665–674 (ACM).

- Kahneman and Tversky (1979) Kahneman D, Tversky A (1979) Prospect theory: An analysis of decision under risk. Econometrica: Journal of the Econometric Society 263–291.

- Kallus and Udell (2016) Kallus N, Udell M (2016) Revealed preference at scale: Learning personalized preferences from assortment choices. Proceedings of the 2016 ACM Conference on Economics and Computation, 821–837 (ACM).

- Keshavan et al. (2009a) Keshavan R, Montanari A, Oh S (2009a) Matrix completion from noisy entries. Advances in Neural Information Processing Systems, 952–960.

- Keshavan et al. (2009b) Keshavan R, Montanari A, Oh S (2009b) Matrix completion from noisy entries. Advances in Neural Information Processing Systems, 952–960.

- Keshavan et al. (2010) Keshavan RH, Montanari A, Oh S (2010) Matrix completion from a few entries. IEEE Transactions on Information Theory 56(6):2980–2998.

- Lai and Robbins (1985) Lai TL, Robbins H (1985) Asymptotically efficient adaptive allocation rules. Advances in applied mathematics 6(1):4–22.

- Li et al. (2015) Li G, Rusmevichientong P, Topaloglu H (2015) The d-level nested logit model: Assortment and price optimization problems. Operations Research 63(2):325–342.

- Lu and Negahban (2014) Lu Y, Negahban SN (2014) Individualized rank aggregation using nuclear norm regularization. arXiv preprint arXiv:1410.0860 .

- Luce (1959) Luce DR (1959) Individual Choice Behavior: a theoretical analysis (Wiley).

- Maillard and Mannor (2014) Maillard OA, Mannor S (2014) Latent bandits. International Conference on Machine Learning, 136–144.

- McFadden (1973) McFadden D (1973) Conditional logit analysis of qualitative choice behavior. Zarembka P, ed., Frontiers in Economics (Academic Press).

- McFadden (1980) McFadden D (1980) Econometric models for probabilistic choice among products. Journal of Business S13–S29.

- McFadden and Train (2000) McFadden D, Train K (2000) Mixed mnl models for discrete response. Journal of applied Econometrics 15(5):447–470.

- Megiddo (1979) Megiddo N (1979) Combinatorial optimization with rational objective functions. Mathematics of Operations Research 4(4):414–424.

- Negahban and Wainwright (2011) Negahban S, Wainwright MJ (2011) Estimation of (near) low-rank matrices with noise and high-dimensional scaling. The Annals of Statistics 1069–1097.

- Negahban et al. (2012) Negahban SN, Ravikumar P, Wainwright MJ, Yu B (2012) A unified framework for high-dimensional analysis of m-estimators with decomposable regularizers. Statistical Science 538–557.

- Oh et al. (2015) Oh S, Thekumparampil KK, Xu J (2015) Collaboratively learning preferences from ordinal data. Advances in Neural Information Processing Systems, 1909–1917.

- Orabona et al. (2012) Orabona F, Argyriou A, Srebro N (2012) Prisma: Proximal iterative smoothing algorithm. arXiv preprint arXiv:1206.2372 .

- Parikh and Boyd (2014) Parikh N, Boyd S (2014) Proximal algorithms. Foundations and Trends in Optimization 1(3):127–239.

- Perchet and Rigollet (2013) Perchet V, Rigollet P (2013) The multi-armed bandit problem with covariates. The Annals of Statistics 41(2):693–721.

- Raskutti et al. (2010) Raskutti G, Wainwright MJ, Yu B (2010) Restricted eigenvalue properties for correlated gaussian designs. Journal of Machine Learning Research 11(Aug):2241–2259.

- Recht et al. (2010) Recht B, Fazel M, Parrilo P (2010) Guaranteed minimum-rank solutions of linear matrix equations via nuclear norm minimization. SIAM Review 52(3):471–501, ISSN 0036-1445, URL http://dx.doi.org/10.1137/070697835.

- Recht et al. (2011) Recht B, Re C, Wright S, Niu F (2011) Hogwild: A lock-free approach to parallelizing stochastic gradient descent. Advances in Neural Information Processing Systems, 693–701.

- Rigollet and Zeevi (2010) Rigollet P, Zeevi A (2010) Nonparametric bandits with covariates. arXiv preprint arXiv:1003.1630 .

- Rusmevichientong et al. (2010) Rusmevichientong P, Shen ZJM, Shmoys DB (2010) Dynamic assortment optimization with a multinomial logit choice model and capacity constraint. Operations Research 58(6):1666–1680.

- Rusmevichientong et al. (2014) Rusmevichientong P, Shmoys D, Tong C, Topaloglu H (2014) Assortment optimization under the multinomial logit model with random choice parameters. Production and Operations Management 23(11):2023–2039.

- Sauré and Zeevi (2013) Sauré D, Zeevi A (2013) Optimal dynamic assortment planning with demand learning. Manufacturing & Service Operations Management 15(3):387–404.

- Schuler et al. (2016) Schuler A, Liu V, Wan J, Callahan A, Udell M, Stark D, Shah N (2016) Discovering patient phenotypes using generalized low rank models. Pacific Symposium on Biocomputing (PSB) URL http://psb.stanford.edu/psb-online/proceedings/psb16/schuler.pdf.

- Slivkins (2014) Slivkins A (2014) Contextual bandits with similarity information. The Journal of Machine Learning Research 15(1):2533–2568.

- Spearman (1904) Spearman C (1904) “general intelligence,” objectively determined and measured. The American Journal of Psychology 15(2):201–292.

- Talluri and Van Ryzin (2006) Talluri KT, Van Ryzin GJ (2006) The theory and practice of revenue management, volume 68 (Springer Science & Business Media).

- Tropp (2012) Tropp JA (2012) User-friendly tail bounds for sums of random matrices. Foundations of Computational Mathematics 12(4):389–434.

- Udell et al. (2016) Udell M, Horn C, Zadeh R, Boyd S (2016) Generalized low rank models. Foundations and Trends in Machine Learning URL http://dx.doi.org/10.1561/2200000055.

- Udell and Townsend (2017) Udell M, Townsend A (2017) Nice latent variable models have log-rank. arXiv preprint arXiv:1705.07474 .

- van Ryzin and Vulcano (2014) van Ryzin G, Vulcano G (2014) A market discovery algorithm to estimate a general class of nonparametric choice models. Management Science 61(2):281–300.

- Williams (1977) Williams HC (1977) On the formation of travel demand models and economic evaluation measures of user benefit. Environment and planning A 9(3):285–344.

- Witten et al. (2009) Witten D, Tibshirani R, Hastie T (2009) A penalized matrix decomposition, with applications to sparse principal components and canonical correlation analysis. Biostatistics kxp008.

Appendices

7 Dynamic Assortment Planning with a Heterogeneous Population

In this section we consider a non-contextual dynamic assortment planning problem where the target population is very heterogeneous. This is a departure from our focus on personalization, but theoretically our results can be extended to this additional setting that may be of independent interest.

This setting is appropriate when there is no potential for user-level personalization, such as in a single brick-and-mortar store, but where the consumer population is very heterogeneous and cannot be well described by only a single, or even a few, nominal preference vectors and where this heterogeneity can be explained by an post-purchase observable user type. This setting is similar to that considered in Rusmevichientong et al. (2010) and Sauré and Zeevi (2013) in that it is non-contextual, but in both those works the choice distribution is assumed to be MNL (or, generally, any random utility model with a single nominal preference vector, from which deviations are made at random in a homogeneous manner). Here we allow for a potentially heterogeneous population with choice governed by the LRCMNL model.

The problem proceeds as follows, in somewhat different order than the personalization problem presented in Section 2. At each :

-

1.

we choose any with ,

-

2.

a type is drawn at random from with probability proportional to weights ,

-

3.

an item is drawn at random from with probability proportional to weights

-

4.

if we get reward and otherwise we get reward .

Unlike before, we have to select before observing . Therefore, we cannot personalize.

Let us re-define

| the expected revenue of under , and | ||||

| the optimal assortment under . |