Abstract

This paper constructs and studies the long-term factorization of affine pricing kernels into discounting at the rate of return on the long bond and the martingale component that accomplishes the change of probability measure to the long forward measure. The principal eigenfunction of the affine pricing kernel germane to the long-term factorization is an exponential-affine function of the state vector with the coefficient vector identified with the fixed point of the Riccati ODE. The long bond volatility and the volatility of the martingale component are explicitly identified in terms of this fixed point. A range of examples from the asset pricing literature is provided to illustrate the theory.

1 Introduction

The stochastic discount factor (SDF) is a fundamental object in arbitrage-free asset pricing models. It assigns today’s prices to risky future payoffs at alternative investment horizons. It accomplishes this by simultaneously discounting the future and adjusting for risk. A familiar representation of the SDF is a factorization into discounting at the risk-free interest rate and a martingale component adjusting for risk. This martingale accomplishes the change of probabilities to the risk-neutral probability measure. More recently Alvarez and Jermann (2005), Hansen et al. (2008), Hansen and Scheinkman (2009) and Hansen (2012) introduce and study an alternative long-term factorization of the SDF. The transitory component in the long-term factorization discounts at the rate of return on the pure discount bond of asymptotically long maturity (the long bond). The permanent component is a martingale that accomplishes a change of probabilities to the long forward measure. Qin and Linetsky (2017) study the long-term factorization and the long forward measure in the general semimartingale setting.

The long-term factorization of the SDF is particularly convenient in applications to the pricing of long-lived assets and to theoretical and empirical investigations of the term structure of the risk-return trade-off. In addition to the references above, the growing literature on the long-term factorization and its applications includes Hansen and Scheinkman (2012), Hansen and Scheinkman (2017), Borovička et al. (2016), Borovička et al. (2011), Borovička and Hansen (2016), Bakshi and Chabi-Yo (2012), Bakshi et al. (2015), Christensen (2017), Christensen (2016), Qin and Linetsky (2016), Qin et al. (2016), Backus et al. (2015), Filipović et al. (2017), Filipović et al. (2016). Empirical investigations in this literature show that the martingale component in the long-term factorization is highly volatile and economically significant (see, in particular, Bakshi and Chabi-Yo (2012) for results based on pricing kernel bounds, Christensen (2017) for results based on structural asset pricing models connecting to the macro-economic fundamentals, and Qin et al. (2016) for results based on explicit parameterizations of the pricing kernel, where, in particular, the relationship among the measures , and is empirically investigated).

The focus of the present paper is on the analysis of long-term factorization in affine diffusion models, both from the perspective of providing a user’s guide to constructing long-term factorization in affine asset pricing models, as well as employing affine models as a convenient laboratory to illustrate the theory of the long-term factorization. Affine diffusions are work-horse models in continuous-time finance due to their analytical and computational tractability (Vasicek (1977), Cox et al. (1985), Duffie and Kan (1996), Duffie et al. (2000), Dai and Singleton (2000), Duffie et al. (2003)). In this paper we show that the principal eigenfunction of Hansen and Scheinkman (2009) that determines the long-term factorization, if it exists, is necessarily in the exponential-affine form in affine models, with the coefficient vector in the exponential identified with the fixed point of the corresponding Riccati ODE. This allows us to give a fully explicit treatment and illustrate dynamics of the long bond, the martingale component and the long-forward measure in affine models. In particular, we explicitly verify that when the Riccati ODE associated with the affine pricing kernel possesses a fixed point, the affine model satisfies the sufficient condition in Theorem 3.1 of Qin and Linetsky (2017) so that the long-term limit exists.

In Section 2 we review and summarize the long-term factorization in Brownian motion-based models. In Section 3 we present general results on the long-term factorization of affine pricing kernels. The main results are given in Theorem 3.2, where the market price of Brownian risk is explicitly decomposed into the market price of risk under the long forward measure identified with the volatility of the long bond and the remaining market price of risk determining the martingale component accomplishing the change of probabilities from the data-generating to the long forward measure. The latter component is determined by the fixed point of the Riccati ODE. In Section 4 we study a range of examples of affine pricing kernels from the asset pricing literature.

2 Long-Term Factorization in Brownian Environments

We work on a complete filtered probability space . We assume that all uncertainty in the economy is generated by an -dimensional Brownian motion and that is the (completed) filtration generated by . We assume absence of arbitrage and market frictions, so that there exists a strictly positive pricing kernel process in the form of an Itô semimartingale. More precisely, we assume that the pricing kernel follows an Itô process ( denotes vector dot product)

with and the market price of Brownian risk vector such that the process

is a martingale (Novikov’s condition for each suffices). Under these assumptions the pricing kernel has the risk-neutral factorization

| (2.1) |

into discounting at the risk-free short rate determining the risk-free asset (money market account) and the exponential martingale with the market price of Brownian risk determining its volatility. We also assume that for all . The integrability of the SDF for any two dates ensures that that zero-coupon bond price processes

are well defined for all maturity dates ().

Since for each the -maturity zero coupon bond price process can be written as , where is a positive martingale on , we can apply the Martingale Representation Theorem to claim that

with some , and further claim that the bond price process has the representation

with the volatility process .

Following Qin and Linetsky (2017), for each fixed we define a self-financing trading strategy that rolls over investments in -maturity zero-coupon bonds as follows. Fix and consider a self-financing roll-over strategy that starts at time zero by investing one unit of account in units of the -maturity zero-coupon bond. At time the bond matures, and the value of the strategy is units of account. We roll the proceeds over by re-investing into units of the zero-coupon bond with maturity . We continue with the roll-over strategy, at each time re-investing the proceeds into the bond . We denote the valuation process of this self-financing strategy :

For each , the process is defined for all . The process extends the martingale to all . It thus defines the -forward measure on for each , where now has the meaning of the length of the compounding interval. Under the -forward measure extended to all , the roll-over strategy with the compounding interval serves as the numeraire asset. Following Qin and Linetsky (2017), we continue to call the measure extended to all for the -forward measure and use the same notation, as it reduces to the standard definition of the forward measure on .

Since the roll-over strategy and the positive martingale are defined for all , we can write the -forward factorization of the pricing kernel for all :

| (2.2) |

We now recall the definitions of the long bond and the long forward measure from Qin and Linetsky (2017).

Definition 2.1.

(Long Bond) If the wealth processes of the roll-over strategies in -maturity bonds converge to a strictly positive semimartingale uniformly on compacts in probability as , i.e. for all and

we call the limit the long bond.

Definition 2.2.

(Long Forward Measure) If there exists a measure equivalent to on each such that the -forward measures converge strongly to on each , i.e.

for each and each , we call the limit the long forward measure and denote it .

The following theorem, proved in Qin and Linetsky (2017), gives a sufficient condition that ensures convergence to the long bond in the semimartingale topology which is stronger than the ucp convergence in Definition 1 and convergence of -forward measures to the long forward measure in total variation, which is stronger than the strong convergence in Definition 2 (we refer to Qin and Linetsky (2017) and the on-line appendix for proofs and details).

Theorem 2.1.

(Long Term Factorization and the Long Forward Measure) Suppose that for each the ratio of the -conditional expectation of the pricing kernel to its unconditional expectation converges to a positive limit in as (under ), i.e. for each there exists an almost surely positive -measurable random variable which we denote such that

| (2.3) |

Then the following results hold:

(i) The collection of random variables is a positive -martingale, and the family of martingales converges to the martingale in the semimartingale topology.

(ii) The long bond valuation process exists, and the roll-over strategies converge to the long bond in the semimartingale topology.

(iii) The pricing kernel possesses the long-term factorization

| (2.4) |

(iv) -forward measures converge to the long forward measure in total variation on each , and is equivalent to on with the Radon-Nikodym derivative .

The process has the interpretation of the gross return earned starting from time zero up to time on holding the zero-coupon bond of asymptotically long maturity. The long bond is the numeraire asset under the long forward measure since the pricing kernel becomes under . The long-term factorization of the pricing kernel (2.4) decomposes it into discounting at the rate of return on the long bond and a martingale component encoding a further risk adjustment.

Suppose the condition (2.3) in Theorem 2.1 holds in the Brownian setting of this paper. Then the long bond valuation process is an Itô semimartingale with the representation

with some volatility process such that the process satisfying

with is a martingale (the permanent component in the long-term factorization). Thus, the long-term factorization Eq.(2.4) in the Brownian setting yields a decomposition of the market price of Brownian risk

| (2.5) |

into the volatility of the long bond and the volatility of the martingale . The change of probability measure from the data-generating measure to the long forward measure is accomplished via Girsanov’s theorem with the -Brownian motion

3 Long Term Factorization of Affine Pricing Kernels

We assume that the underlying economy is described by a Markov process . We further assume is an affine diffusion and the pricing kernel is exponential affine in and the time integral of . Affine diffusion models are widely used in continuous-time finance due to their analytical tractability (Vasicek (1977), Cox et al. (1985), Duffie and Kan (1996), Duffie et al. (2000), Dai and Singleton (2000), Duffie et al. (2003)). We start with a brief summary of some of the key facts about affine diffusions. We refer the reader to Filipović and Mayerhofer (2009) for details, proofs and references to the literature on affine diffusion.

The process we work with solves the following SDE on the state space for some with , where for :

| (3.1) |

where is a -dimensional standard Brownian motion and the diffusion matrix (here † denotes matrix transpose to differentiate it from superscript T) and the drift vector are both affine in :

| (3.2) |

for some -matrices and and -dimensional vectors and , where we denote by the -matrix with -th column vector , . The first coordinates of are CIR-type and are non-negative, while the last coordinates are OU-type. Define the index sets and . For any vector and matrix , and index sets , we denote by the respective sub-vector and sub-matrix. To ensure the process stays in the domain , we need the following assumption (cf. Filipović and Mayerhofer (2009))

Assumption 3.1.

(Admissibility)

(1) and are symmetric positive semi-definite for all ,

(2) ,

(3) for ,

(4) for for all

(5) , , and has non-negative off-diagonal elements.

The condition on the constant term in the drift of the CIR-type components ensures that the process stays in the state space . Making a stronger assumption ensures that the process instantaneously reflects from the boundary and re-enters the interior of the state space where for . For any parameters satisfying Assumption 3.1, there exists a unique strong solution of the SDE (3.1) (cf. Theorem 8.1 of Filipović and Mayerhofer (2009)). Denote by the law of the solution of the SDE (3.1) for , . Then defined for all , Borel subsets of , and defines a Markov transition semigroup on the Banach space of Borel measurable bounded functions on by . As shown in Duffie et al. (2003), this semigroup is Feller, i.e., it leaves the space of continuous functions vanishing at infinity invariant. Thus, the Markov process is a Feller process on . It has continuous paths in and has the strong Markov property (cf. Yamada and Watanabe (1971), Corollary 2, p.162). Thus, it is a Borel right process (in fact, a Hunt process).

We make the following assumption about the pricing kernel.

Assumption 3.2.

(Affine Pricing Kernel) We assume that the pricing kernel is exponential-affine in and its time integral:

| (3.3) |

where is a scalar and and are -vectors and † denotes matrix transpose.

The pricing kernel in this form is a positive multiplicative functional of the Markov process . The associated pricing operator is defined by

for a payoff of the Markov state. We refer the reader to Qin and Linetsky (2016a) for a detailed treatment of Markovian pricing operators. The pricing kernel in the form (3.3) is called affine due to the following key result that shows that the term structure of pure discount bond yields is affine in the state vector (cf. Filipović and Mayerhofer (2009) Theorem 4.1).

Proposition 3.1.

Let . The following statements are equivalent:

(i) for all fixed initial states .

(ii) There exists a unique solution of the following Riccati system of equations up to time :

| (3.4) |

In either case, the pure discount bond valuation processes (with unit payoffs) are exponential-affine in :

| (3.5) |

for all and the SDE initial condition .

Since in this paper our standing assumption is that for all , in this case the Riccati ODE system has solutions and for all , and the bond pricing function entering the expression (3.5) for the zero-coupon bond process

| (3.6) |

is defined for all and .

We next show that an affine pricing kernel always possesses the risk-neutral factorization with the affine short rate function.

Theorem 3.1.

(Risk-Neutral Factorization of Affine Pricing Kernels)

Suppose satisfies Assumption 3.1 and the pricing kernel satisfies Assumption 3.2 together with the assumption that for all and every fixed initial state .

(i) Then the pricing kernel admits the risk-neutral factorization

with the affine short rate

| (3.7) |

with

| (3.8) |

and the martingale

with the market price of Brownian risk (column -vector)

| (3.9) |

where is the volatility matrix of the state variable in the SDE (3.1) and

(ii) Under the risk-neutral measure defined by the martingale , the dynamics of reads

| (3.10) |

where is the standard Brownian motion under .

Proof.

(i) Define a process . It is also in the form of Eq.(3.3) with replaced by and replaced by . Thus, Proposition 3.1 also holds if we replace with , replace with and replace with , i.e. where

| (3.11) |

With the choice of and in Eq.(3.8), the solution to the above ODE is and , which implies . This shows that is a martingale. Furthermore, using the SDE for the affine state , we can cast in the exponential martingale form . with given in (3.9).

(ii) The SDE for under follows from Girsanov’s Theorem. ∎

We next turn to the long term factorization of the affine pricing kernel.

Theorem 3.2.

(Long Term Factorization of Affine Pricing Kernels) Suppose the solution of the Riccati ODE (3.4) converges to a fixed point :

| (3.12) |

Then the following results hold.

(i) Condition Eq.(2.3) is satisfied and, hence, all results in Theorem 2.1 hold.

(ii) The long bond is given by

| (3.13) |

where

| (3.14) |

is the positive exponential-affine eigenfunction of the pricing operator

with the eigenvalue with

| (3.15) |

interpreted as the limiting long-term zero-coupon yield:

| (3.16) |

for all .

(iii) The long bond has the -measure dynamics:

| (3.17) |

where the (column vector) volatility of the long bond is given by:

| (3.18) |

(iv) The martingale component in the long-term factorization of the PK can be written in the form

| (3.19) |

where

| (3.20) |

(v) The long-term decomposition of the market price of Brownian risk is given by:

| (3.21) |

where is the volatility of the long bond (3.18) and given in (3.20) defines the martingale (3.19).

(vi) Under the long forward measure the state vector solves the following SDE

| (3.22) |

where is the d-dimensional Brownian motion under , and the long bond has the -measure dynamics:

| (3.23) |

Proof.

Since the solution of the Riccati ODE converges to a constant as , the right hand side of Eq.(3.4) also converges to a constant. This implies that also converges to a constant. This constant must vanish, otherwise cannot converge to a constant. Thus, the right hand side of Eq.(3.4) also converges to zero. All these imply that is a stationary solution of the Riccati equation Eq.(3.4). Applying Proposition 3.1 to the affine kernel of the form , where is the process defined in (3.13), it then follows that defined in Eq.(3.14) is an eigenfunction of the pricing operator with the eigenvalue (3.15). We can then verify that

is a martingale (with ). We can use it to define a new probability measure

associated with the eigenfunction . The dynamics of under follows from Girsanov’s Theorem. We stress that is the eigenfunction of the pricing semigroup operator, rather than merely an eigenfunction of the generator. It is generally possible for an eigenfunction of the generator to fail to be an eigenfunction of the semigroup. That case will lead to a mere local martingale. In our case, is an eigenfunction of the semigroup by construction, and the process is a martingale, rather than a mere local martingale.

We now show that the condition (2.3) holds under our assumptions in Theorem 3.2. We first re-write it under the probability measure :

| (3.24) |

We will now verify that this indeed holds under our assumptions. First observe that by Eq.(3.5):

| (3.25) |

Since and , we have that

almost surely. Next, we show convergence. First, we observe that for any there exists such that for all

for all and

Thus,

Since remains affine under , by Theorem 4.1 of Filipović and Mayerhofer (2009) there exists such that is integrable under for all vectors such that . Thus, by the Dominated Convergence Theorem, Eq.(3.24) holds. This proves (i) and (ii) (Eq.(3.16) follows from Eq.(3.6) and the fact as ). (iii) follows from Eq.(3.13) and Ito’s formula.

The economic meaning of Theorem 3 is that the existence of a fixed point of the solution to the Riccati equation is sufficient for existence of the long term limit. The fixed point itself identifies the volatility of the long bond in Eq.(17) and the long-term zero-coupon yield in Eq.(16) via the principal eigenvalue (15).

We note that the condition in Theorem 3.2 of Qin and Linetsky (2017) is automatically satisfied in affine models. Indeed, from Eq.(3.6) when the Riccati equation has a fixed point , from Theorem 3.2 in this paper we have

and we can write , where is a slowly varying function of time for each . By Eq.(3.16), the eigenvalue is identified with the asymptotic long-term zero-coupon yield.

We note that since is a stationary solution of the Riccati ODE (3.4), the vector satisfies the following quadratic vector equation:

However, in general this quadratic vector equation may have multiple solutions leading to multiple exponential-affine eigenfunctions. In order to determine the solution that defines the long-term factorization, if it exists, it is essential to verify that is the limiting solution of the Riccatti ODE, i.e. that Eq.(3.12) holds. In this regard, we recall that Qin and Linetsky (2016) identified the unique recurrent eigenfunction of an affine pricing kernel with the minimal solution of the quadratic vector equation (see Appendix F in the on-line e-companion to Qin and Linetsky (2016)). We recall that, for a Markovian pricing kernel (see Hansen and Scheinkman (2009) and Qin and Linetsky (2016)), we can associate a martingale

with any positive eigenfunction . In general, positive eigenfunctions are not unique. Qin and Linetsky (2016) proved uniqueness of a recurrent eigenfunction defined as such a positive eigenfunction of the pricing kernel , i.e.

for some , that, under the locally equivalent probability measure (eigen-measure) defined by using the associated martingale as the Radon-Nikodym derivative, the Markov state process is recurrent. However, in general, without additional assumptions, the recurrent eigenfunction associated with the minimal solution to the quadratic vector equation may or may not coincide with the eigenfunction germane to the long-term limit and, thus, the long forward measure may or may not coincide with the recurrent eigenmeasure (the fixed point of the Riccati ODE may or may not be the minimal solution of the quadratic vector equation). Under additional exponential ergodicity assumptions the fixed point of the Riccati ODE is necessarily the minimal solution of the quadratic vector equation and . If the exponential ergodicity assumption is not satisfied, they may differ, or one may exist, while the other does not exist. We refer the reader to Qin and Linetsky (2016) and Qin and Linetsky (2017) for the exponential ergodicity assumption. Analytical tractability of affine models allows us to provide fully explicit examples to illustrate these theoretical possibilities. In the next section we give a range of examples.

4 Examples

4.1 Cox-Ingersoll-Ross Model

Suppose the state follows a CIR diffusion (Cox et al. (1985)):

| (4.1) |

where , , , and is a one-dimensional standard Brownian motion (in this case and ). Consider the CIR pricing kernel in the form (3.3). The short rate is given by (3.7) with and . For simplicity we choose and so that the short rate can be identified with the state variable, . The market price of Brownian risk is . Under the short rate follows the process (3.10), which is again a CIR diffusion, but with a different rate of mean reversion:

| (4.2) |

The fixed point of the Riccati ODE

with the initial condition can be readily determined. Since , we know that is between the two roots of the quadratic equation . This immediately implies that converges to the larger root, i.e.

| (4.3) |

where we introduce the following notation:

Thus, the long bond in the CIR model is given by

| (4.4) |

with

| (4.5) |

and the long bond volatility

Under the long forward measure the state follows the process (3.22), which is again a CIR diffusion, but with the different rate of mean reversion . The fixed point is proportional to the difference between the rate of mean reversion under the long forward measure and the data generating measure . It defines the market price of risk under via .

We note that if one selects in the specification of the pricing kernel, then and , so the margingale component in the long term factorization is degenerate, and the pricing kernel is in the transition independent form. In this case, so that the data-generating measure coincides with the long-forward measure. This is the condition of Ross’ recovery theorem (see Qin and Linetsky (2016) for more details).

Since the closed form solution for the CIR zero-coupon bond pricing function is available (Cox et al. (1985)), these results can also be recovered by directly calculating the limit

with the eigenvalue given by Eq.(4.5) and the eigenfunction .

Remark 4.1.

Borovička et al. (2016) in their Example 4 on p.2513 also consider an exponential-affine pricing kernel driven by a single CIR factor. However, their specification of the PK is in a special form such that in Eq.(4) for the short rate (which corresponds to the choice in our parameterization). Thus, all dependence on the CIR factor is contained in the martingale component in the risk-neutral factorization of their PK, with the short rate being constant. In this special case the long bond is deterministic and the long forward measure is simply equal to the risk-neutral measure since the short rate is independent of the state variable. In this special case the pricing operator has two distinct positive eigenfunctions. One of the eigenfunctions is constant. This eigenfunction defines the risk-neutral measure, which coincides with the long forward measure in this case due to independence of the short rate and the eigenfunction of the state variable. The second eigenfunction (Eq.(19) in Borovička et al. (2016)) defines a probability measure, which is distinct from the risk-neutral measure and, hence, distinct from the long forward measure as well. Depending on the specific parameter values of the CIR process, either one of the two eigenfunctions may serve as the recurrent eigenfunction. The eigenmeasure associated with the other eigenfunction will not be recurrent, as the CIR process will have a non-mean reverting drift under that measure.

4.2 CIR Model with Absorption at Zero: Exists, Does Not Exist

We next consider a degenerate CIR model (4.1) with , , and . When vanishes, the diffusion has an absorbing boundary at zero, i.e. there is a positive probability to reach zero in finite time and, once reached, the process stays at zero with probability one for all subsequent times. Consider a pricing kernel in the form of Eq.(3.3). The short rate is given by (3.7) with and . We assume and , so that short rate takes values in . The market price of Brownian risk is , and under the short rate follows the process (3.10), which is again a CIR diffusion with an absorbing boundary at zero, but with a different rate of mean reversion .

It is clear that under any locally equivalent measure, zero remains absorbing and thus no recurrent eigenfunction exists. Nevertheless, we can proceed in the same way as in our analysis of the CIR model to show that

with is the long bond and solves the CIR SDE (4.1) with and mean-reverting rate under . In fact, the treatment of the long bond and the long forward measure is exactly the same as in the non-degenerate example with , even though this case is transient with absorption at zero. The eigenvalue degenerates in this case, , and the asymptotic long-term zero-coupon yield vanishes, corresponding to the eventual absorption of the short rate at zero.

4.3 Vasicek Model

Our next example is the Vasicek (1977) model with the state variable following the OU diffusion:

with , (in this case , ). Consider the pricing kernel in the form (3.3). The short rate is given by (3.7) with and . For simplicity we choose and so that the short rate is identified with the state variable, . The market price of Brownian risk is constant in this case, . Under the short rate follows the process (3.10), which in this case is again the OU diffusion, but with a different long run mean

(the rate of mean reversion remains the same). The explicit solution to the ODE with the initial condition is

and the limit yields the fixed point Thus, the long bond in the Vasicek model is given by

with the long-term yield

and the long bond volatility

Under the long forward measure the short rate follows the process (3.22), which is again the OU diffusion, but with a different long run mean

(the rate of mean reversion remains the same).

4.4 Non-mean-reverting Gaussian Model: Exists, Does not Exist

Suppose is a Gaussian diffusion with affine drift and constant volatility

| (4.6) |

but now with , so that the process is not mean-reverting. Consider a risk-neutral pricing kernel that discounts at the rate , i.e. . Then the pure discount bond price is given by with

| (4.7) |

| (4.8) |

It is easy to see that the ratio does not have a finite limit as and, hence, does not converge as . Thus, the long bond and the long forward measure do not exist in this case. However, the recurrent eigenfunction and the recurrent eigen-measure do exist in this case and are explicitly given in Section 6.1.3 of Qin and Linetsky (2016). Under , is the OU process with mean reversion (since ):

| (4.9) |

4.5 Breeden Model

Our next example is a special case of Breeden (1979) consumption CAPM considered in Example 3.8 of Hansen and Scheinkman (2009). There are two independent factors, a stochastic volatility factor evolving according to the CIR process

| (4.10) |

and a mean-reverting growth rate factor evolving according to the OU process

Here it is assumed that , , , (so that a positive increment to reduces volatility), and (so that volatility stays strictly positive). Suppose that equilibrium consumption evolves according to

| (4.11) |

where is the logarithm of consumption . Thus, models predictability in the growth rate and models predictability in volatility. Suppose also that the representative consumer’s preferences are given by

| (4.12) |

for . Then the implied pricing kernel is

| (4.13) |

Using the SDEs for and it can be cast in the affine form (3.3):

| (4.14) |

where .

Proposition 4.1.

Proof.

In this model Eq.(3.4) reduces to

| (4.18) |

In this special case and are separated and thus can be analyzed independently. It is easy to see that if then converges to . When , is greater than the smaller root of the second order equation , which implies that converges to the larger root of the second-order equation for . The eigenvalue and the dynamics of the state variable can be computed accordingly. . ∎

The proof essentially combines the proofs in Examples 4.1 and 4.3. Similar to these examples, we observe that the rate of mean reversion of the volatility factor is higher under the long forward measure, , while the rate of mean reversion of the growth rate remains the same, but its long run level is lower under .

4.6 Borovička et al. (2016) Continuous-Time Long-Run Risks Model

Our next example is a continuous-time version of the long-run risks model of Bansal and Yaron (2004) studied by Borovička et al. (2016). It features growth rate predictability and stochastic volatility in the aggregate consumption and recursive preferences. The model is calibrated to the consumption dynamics in Bansal and Yaron (2004). The two-dimensional state modeling growth rate predictability and stochastic volatility follows the affine dynamics:

| (4.19) |

where are two independent Brownian motions. Here is the stochastic volatility factor following a CIR process and is an OU-type mean-reverting growth rate factor with stochastic volatility. The aggregate consumption process in this model evolves according to

| (4.20) |

where is a third independent Brownian motion modeling direct shocks to consumption. Numerical parameters are from Borovička et al. (2016) and are calibrated to monthly frequency (here time is measured in months). The representative agent in this model is endowed with recursive homothetic preferences and a unitary elasticity of substitution. Borovička et al. (2016) solve for the pricing kernel:

where the three-dimensional Brownian motion is viewed as a column vector.

We now cast this model specification in the three-dimensional affine form of Assumption 3.2. To this end, we introduce a third factor . We can then write the pricing kernel in the exponential affine form , where the state vector follows a three-dimensional affine diffusion driven by a three-dimensional Brownian motion:

| (4.21) |

where the numerical values for entries of the three-dimensional vector and -matrices and are given above.

We can now directly apply our general results for affine pricing kernels. First, by Theorem 3.1, the short rate is and depends only on the factors and and is independent of . The risk-neutral (-measure) dynamics is given by:

| (4.22) |

where

| (4.23) |

The vector solves the ODE (here ):

with . It is immediate that

and, since ,

To see convergence, notice that we can write , where . Since , we have . Since and it is easy to see that . Since , we have . We can check that has two negative roots. Denote the larger root , we see that . Combining these facts, we see that converges to . The exact value of has to be determined numerically. The numerical solution yields

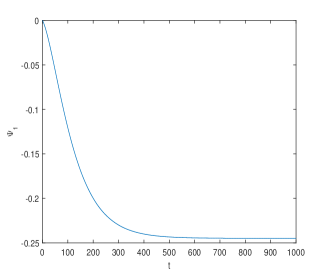

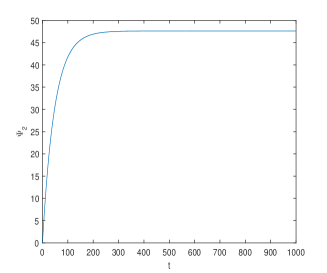

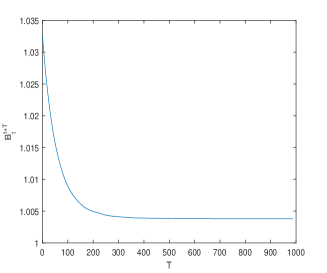

In Figure 1, we plot the functions and , as well as the gross return on the -bond over the period as a function of . In this numerical example we take months, so we are looking at the one-year holding period return, and assume that the initial state and the state are both equal to the stationary mean under . We observe that in this model specification and are already very close to the fixed point for around 30 years (360 months).

By Theorem 3.2, the eigenfunction determining the long bond is corresponding to the eigenvalue (note this is not annualized yield since time unit is in month)

the long bond is given by

the martingale component is given by

and the state vector has the following dynamics under the long forward measure :

| (4.24) |

As already observed by Borovička et al. (2016), in this model the state dynamics under the long forward measure is close to the state dynamics under the risk-neutral measure and is substantially distinct from the dynamics under the data-generating measure due to the volatile martingale component . However, our approach to the analysis of this model is different from the analysis of Borovička et al. (2016). We cast it as a three-factor affine model and directly apply our Theorem 3.2 for affine models that is, in turn, a consequence of our Theorem 2.1 for semimartingale models. We only need to determine the fixed point (3.12) of the Riccati equation. Existence of the long bond, the long term factorization of the pricing kernel, and the long forward measure then immediately follow from Theorem 3.2, without any need to verify ergodicity. In fact, the three-factor affine process is not ergodic, and not even recurrent, as is immediately seen from the dynamics of . In contrast, the approach in Borovička et al. (2016) relies on the two-dimensional mean-reverting affine diffusion . Namely, since the Perron-Frobenius theory of Hansen and Scheinkman (2009) requires ergodicity to single out the principal eigenfunction and ascertain its relevance to the long-term factorization, Borovička et al. (2016) implicitly split the pricing kernel into the product of two sub-kernels, a multiplicative functional of the two-dimensional Markov process and the additional factor in the form . The Perron-Frobenius theory of Hansen and Scheinkman (2009) is then applied to the multiplicative functional of the two-dimensional Markov process . In contrast, in our approach we do not require ergodicity and work directly with the non-ergodic three-dimensional process and verify that the Riccati ODE possesses a fixed point, which is already sufficient for existence of the long-term factorization in affine models by Theorem 3.2.

5 Conclusion

This paper constructs and studies the long-term factorization of affine pricing kernels into discounting at the rate of return on the long bond and the martingale component that accomplishes the change of probability measure to the long forward measure. It is shown that the principal eigenfunction of the affine pricing kernel germane to the long-term factorization is an exponential-affine function of the state vector with the coefficient vector identified with the fixed point of the Riccati ODE. The long bond volatility and the volatility of the martingale component are explicitly identified in terms of this fixed point. When analyzing a given affine model, a research needs to establish whether the Riccati ODE possesses a fixed point. If the fixed point is determined, the long-term factorization then follows. It is shown how the long-term factorization plays out in a variety of asset pricing models, including single factor CIR and Vasicek models, a two-factor version of Breeden’s CCAPM, and the three-factor long-run risks model studied in Borovička et al. (2016).

References

- Alvarez and Jermann (2005) F. Alvarez and U. J. Jermann. Using asset prices to measure the persistence of the marginal utility of wealth. Econometrica, 73(6):1977–2016, 2005.

- Backus et al. (2015) D. Backus, N. Boyarchenko, and M. Chernov. Term structures of asset prices and returns. Available at SSRN, http://ssrn.com/abstract=2762069, 2015.

- Bakshi and Chabi-Yo (2012) G. Bakshi and F. Chabi-Yo. Variance bounds on the permanent and transitory components of stochastic discount factors. Journal of Financial Economics, 105(1):191–208, 2012.

- Bakshi et al. (2015) G. Bakshi, F. Chabi-Yo, and X. Gao. A recovery that we can trust? deducing and testing the restrictions of the recovery theorem. Technical report, Working paper, 2015.

- Bansal and Yaron (2004) R. Bansal and A. Yaron. Risks for the long run: A potential resolution of asset pricing puzzles. Journal of Finance, 59(4):1481–1509, 2004.

- Borovička et al. (2011) J. Borovička, L. P. Hansen, M. Hendricks, and J. A. Scheinkman. Risk-price dynamics. Journal of Financial Econometrics, 9(1):3–65, 2011.

- Borovička et al. (2016) J. Borovička, L. P. Hansen, and J. A. Scheinkman. Misspecified recovery. Journal of Finance, 71(6):2493–2544, 2016.

- Borovička and Hansen (2016) J. Borovička and L. P. Hansen. Term structure of uncertainty in the macroeconomy. In Handbook of Macroeconomics: Volume 2B, chapter 20, pages 1641–1696. Elsevier B.V., 2016.

- Breeden (1979) D. T. Breeden. An intertemporal asset pricing model with stochastic consumption and investment opportunities. Journal of Financial Economics, 7(3):265–296, 1979.

- Christensen (2016) T. M. Christensen. Nonparametric identification of positive eigenfunctions. Econometric Theory, 31(6):1310–1330, 2016.

- Christensen (2017) T. M. Christensen. Nonparametric stochastic discount factor decomposition. Forthcoming in Econometrica, 2017.

- Cox et al. (1985) J. C. Cox, Jr J. E. Ingersoll, and S. A. Ross. A theory of the term structure of interest rates. Econometrica, 53(2):385–408, 1985.

- Dai and Singleton (2000) Q. Dai and K. J. Singleton. Specification analysis of affine term structure models. Journal of Finance, 55(5):1943–1978, 2000.

- Duffie and Kan (1996) D. Duffie and R. Kan. A yield-factor model of interest rates. Mathematical Finance, 6(4):379–406, 1996.

- Duffie et al. (2000) D. Duffie, J. Pan, and K. Singleton. Transform analysis and asset pricing for affine jump-diffusions. Econometrica, 68(6):1343–1376, 2000.

- Duffie et al. (2003) D. Duffie, D. Filipović, and W. Schachermayer. Affine processes and applications in finance. Annals of Applied Probability, 13(3):984–1053, 2003.

- Filipović and Mayerhofer (2009) D. Filipović and E. Mayerhofer. Affine diffusion processes: Theory and applications. Radon Series Computational and Applied Mathematics, 8:125–164, 2009.

- Filipović et al. (2016) D. Filipović, M. Larsson, and A. B. Trolle. On the relation between linearity-generating processes and linear-rational models. Available at SSRN 2753484, 2016.

- Filipović et al. (2017) D. Filipović, M. Larsson, and A. B. Trolle. Linear-rational term structure models. Journal of Finance, 72(2):655–704, 2017.

- Hansen (2012) L. P. Hansen. Dynamic valuation decomposition within stochastic economies. Econometrica, 80(3):911–967, 2012.

- Hansen and Scheinkman (2017) L. P. Hansen and J. Scheinkman. Stochastic compounding and uncertain valuation. In After The Flood, pages 21–50. The University of Chicago Press, 2017.

- Hansen and Scheinkman (2009) L. P. Hansen and J. A. Scheinkman. Long-term risk: An operator approach. Econometrica, 77(1):177–234, 2009.

- Hansen and Scheinkman (2012) L. P. Hansen and J. A. Scheinkman. Pricing growth-rate risk. Finance and Stochastics, 16(1):1–15, 2012.

- Hansen et al. (2008) L. P. Hansen, J. C. Heaton, and N. Li. Consumption strikes back? Measuring long-run risk. Journal of Political Economy, 116(2):260–302, 2008.

- Qin and Linetsky (2016) L. Qin and V. Linetsky. Positive eigenfunctions of Markovian pricing operators: Hansen-Scheinkman factorization, Ross recovery and long-term pricing. Operations Research, 64(1):99–117, 2016.

- Qin and Linetsky (2017) L. Qin and V. Linetsky. Long term risk: A martingale approach. Econometrica, 85(1):299–312, 2017.

- Qin et al. (2016) L. Qin, V. Linetsky, and Y. Nie. Long forward probabilities, recovery and the term structure of bond risk premiums. Available at SSRN, http://ssrn.com/abstract=2721366, 2016.

- Vasicek (1977) O. Vasicek. An equilibrium characterization of the term structure. Journal of Financial Economics, 5(2):177–188, 1977.

- Yamada and Watanabe (1971) T. Yamada and S. Watanabe. On the uniqueness of solutions of stochastic differential equations. Journal of Mathematics of Kyoto University, 11(1):155–167, 1971.