Efficient posterior inference on the volatility of a jump diffusion process

Abstract

Jump diffusion processes are widely used to model asset prices over time, mainly for their ability to capture complex discontinuous behavior, but inference on the model parameters remains a challenge. Here our goal is posterior inference on the volatility coefficient of the diffusion part of the process based on discrete samples. A Bayesian approach requires specification of a model for the jump part of the process, prior distributions for the corresponding parameters, and computation of the joint posterior. Since the volatility coefficient is our only interest, it would be desirable to avoid the modeling and computational costs associated with the jump part of the process. Towards this, we consider a purposely misspecified model that ignores the jump part entirely. We work out precisely the asymptotic behavior of the Bayesian posterior under the misspecified model, propose some simple modifications to correct for the effects of misspecification, and demonstrate that our modified posterior inference on the volatility is efficient in the sense that its asymptotic variance equals the no-jumps model Cramér–Rao bound.

Keywords and phrases: Bernstein–von Mises theorem; credible interval; Gibbs posterior; model misspecification; uncertainty quantification.

1 Introduction

Jump diffusion models have gained considerable attention in the last two decades, especially in finance and economics, where they are used to model asset prices as a function of time. An advantage of these models, over the classical Black–Scholes models (e.g. Musiela and Rutkowski, 2005), based solely on a continuous Brownian motion, is their ability to accommodate the rapid—seemingly discontinuous—changes in asset prices often seen in applications. In fact, several authors have concluded that neither a purely-continuous nor purely-jump model is sufficient for real applications (e.g., Aït-Sahalia and Jacod, 2009, 2010; Barndorff-Nielsen and Shepard, 2006; Podolskij, 2006). More specifically, by comparing the observed behavior of at-the-money and out-of-the-money call option prices near expiration with their analogous theoretical behavior, Carr and Wu, (2003) and Medvedev and Scaillet, (2007) argued that both continuous and jump components are necessary to explain the implied volatility behavior of S&P500 index options. In this paper we consider a continuous-time process over a fixed and finite time horizon that can be decomposed as

| (1) |

where is a continuous diffusion—with the drift coefficient, the volatility coefficient, and a standard Brownian motion—and is a pure jump process with finite activity and independent of . We emphasize here that we only assume that, with probability 1, the jump process has a finite number of jumps in and that each jump is finite. For example, the results herein cover the case where is a compound Poisson process. The quantity of interest here is the volatility coefficient , a fundamentally important measure of uncertainty or risk (Musiela and Rutkowski, 2005). Our goal is to construct a (Bayesian) posterior distribution or, more generally, a data-dependent measure, on that can be used to provide valid uncertainty quantification about the volatility coefficient.

If the entire process were observable, then we could immediately identify the jumps and, by subtraction, this could be converted to a standard problem. However, here, as is typically the case in practice, the process is not fully observable; in particular, we can only observe at fixed times , like in, e.g., Aït-Sahalia and Jacod, (2009) and Figueroa-López, (2009). Having only discrete-time observations means that the continuous and jump parts cannot be separated with certainty, which forces us to deal with the jump part of the process in some way, even though our interest is only in the volatility of the continuous part. A Bayesian approach would proceed by modeling all unknowns, using Bayes’s theorem to get a posterior distribution for all the unknowns, and then evaluating the marginal posterior for inference on . While this approach is straightforward in principle, there are a number of challenges faced in practice. For models more complex than that in (1), where the volatility depends on the sample path itself, sophisticated computational tools and/or approximation methods are needed to evaluate the likelihood function and sample from the full posterior (e.g., Gonçalves and Roberts, 2014; Johannes and Polson, 2009; Beskos et al., 2006; Aït-Sahalia, 2002, 2006; Golightly, 2009; Casella and Roberts, 2011). Even in the relatively simple model (1), being obligated to model the jump process has some undesirable consequences, especially since we are only interested in the volatility coefficient . Indeed, developing a sound model for , and specifying reasonable priors for the corresponding model parameters, is a non-trivial task—how large and how frequent are the jumps? is the jump size and rate constant in time? etc—and the quality of marginal inference on depends critically on the quality of this posited model, which is unverifiable. Rifo and Torres, (2009), for example, in a setting similar to ours in (1), propose a Bayesian model that assumes is a Poisson process, which certainly would not be appropriate for all applications. To avoid potential bias from model misspecification, one could go semi-parametric, e.g., characterize by its Lévy measure/density and put a prior on that, but this severely complicates the posterior computation and, furthermore, the addition of an infinite-dimensional nuisance parameter may affect the efficiency of the marginal inference on . Frequentist approaches (e.g., Aït-Sahalia and Jacod, 2014) are available to estimate without specifying a model for , so it would be desirable to have a Bayesian(-like) counterpart that provides a full posterior distribution for uncertainty quantification.

Towards this Bayesian counterpart, we consider, in Section 2, a purposely misspecified model that completely ignores the jumps, basically treating the observations as if they arise from a simple diffusion model. This misspecified model is highly regular and computationally convenient, so if not heavily influenced by misspecification, then perhaps it would suffice for valid inference on . A special case of our Theorem 1 says that the misspecified posterior is asymptotically normal but the misspecification has some undesirable effects, namely, the center is off-target and the spread is too large. Rather than abandon the misspecified model, we propose, in Section 3, to correct for the effects of misspecification, by making two simple adjustments: a suitable scaling of the log-likelihood to correct the spread, and a location shift. Both of these adjustments rely on us having a suitable estimator of the quadratic variation of the jump process . We then show, in Theorem 2, that the corresponding modified posterior is asymptotically normal, centered around a consistent estimator of the true volatility, with variance equal to the Cramér–Rao lower bound for optimal/ideal case when there are no jumps, i.e., when the misspecified model is correct. As a consequence, no proper Bayesian approach—with a parametric or nonparametric model for —can do better asymptotically than our proposal. Our particular modification is easy to implement and we present some simulation results in Section 4 to illustrate the validity of our modified posterior credible intervals.

“Misspecification on purpose” is a general idea which is both practically useful and theoretically interesting, with applications beyond the constant-volatility, jump diffusion setup considered here. Our choice to demonstrate the benefits of this general idea in a relatively simple setting is only for the sake of clarity and conciseness. Similar analysis applies in more complex situations but, naturally, the details (work in progress) are more involved and would potentially distract from the general idea.

2 A misspecified model

Assume that we observe the continuous-time process at distinct time points , i.e., our observations are ; for notational convenience later on, set and . For notational simplicity, we will assume that the time points are equally spaced, so that each time difference equals ; the case of non-equally spaced sampling can be handled similarly. To avoid dealing directly with the jump component of the model (1), we consider a purposely misspecified model that ignores both the drift111Ignoring the drift part here is only for simplicity; if the drift is also of interest, it is straightforward to carry out the subsequent analysis on a joint posterior. and the jump part, i.e., it assumes that the differences , , are iid for some . This misspecified model is easy to work with and has no nuisance parameters so, if it—or a simple modification thereof—also provides valid inference on the volatility, then it ought to be useful. The likelihood function for this misspecified model, up to proportionality constants, is given by

| (2) |

where

is the maximum likelihood estimator. Just like in the familiar Bayes approach, we introduce a prior distribution for , with density function . Here we consider a generalization of the Bayesian setup, defining the (pseudo-)posterior distribution as

| (3) |

where is a suitable (possibly stochastic) sequence to be specified. The distribution in (3) is sometimes referred to as a “Gibbs posterior” (e.g., Zhang, 2006a ; Zhang, 2006b ; Jiang and Tanner, 2008; Grünwald and van Ommen, 2016; Syring and Martin, 2016; Bissiri et al., 2016) and is a “temperature” parameter; the case corresponds to the usual Bayes posterior. Unlike in the well-specified Bayesian setting, where posterior consistency is typical, our model being misspecified means that we cannot expect to converge to a point mass at the true volatility coefficient. Therefore, some correction will be needed to point our posterior towards the true volatility coefficient, but first we need to understand how in (3) behaves without any intervention on our part.

A fundamental result in Bayesian asymptotics is the Bernstein–von Mises theorem, which states that, under certain regularity conditions, a suitably centered and scaled version of the posterior will resemble a normal distribution, in the sense that the total variation distance between that normalized posterior and the normal distribution converges to zero in probability. This classical version is typically used in the case of a well-specified model, but recently there has been work on a version of the Bernstein–von Mises theorem for misspecified models. In particular, Kleijn and van der Vaart, (2012), in their Theorem 2.1, give a Bernstein–von Mises theorem when the model is misspecified. Our result that follows is based on their approach.

Before stating the result, we need to introduce some notation. Let denote the distribution of the differences , with , under the jump diffusion model, and the corresponding conditional distribution, given the jump part of the process (1). Also, let and denote the true drift and volatility coefficients, and define the expectation, conditional expectation, variance, and conditional variance as , , , and , respectively. We consider a “high-frequency” scenario (e.g., Aït-Sahalia and Jacod, 2014), so is large and it is safe to assume that, with probability 1, the time windows contain at most one jump. Therefore, for almost all , under , we have that are independent, , where

| (4) |

For a given , let denote the quadratic variation of the jump process , and let denote the set of indices such that the window contains a jump, i.e., if and only if . We assume that the process (1) has finite jump activity, so with -probability 1. We also assume that is a stochastic sequence and that there exists , possibly depending on , such that in -probability for the given . Finally, the point around which the posterior will concentrate is

Note that both and are constants with respect to the conditional distribution .

Theorem 1.

Consider the pseudo-Bayesian posterior in (3) based on a prior and the misspecified model with likelihood in (2). If the prior density is continuous and positive in a neighborhood of , then, for -almost all , the posterior is asymptotically normal in the sense that

where is the total variation distance. The above conclusion also holds unconditionally, i.e., the above convergence is also in -probability.

Proof.

See the Appendix. ∎

The theorem asserts that, for the “high-frequency” setting where is large, if the data-generating process (1) has finite jump activity, then the posterior will resemble a normal distribution centered around . Since converges to (see the proof of the theorem), it follows that the posterior will resemble a normal distribution centered at . This is different from the usual Bernstein–von Mises theorems found in the Bayesian literature in that the point around which the posterior concentrates depends on both parameters and a hidden portion of the data, namely, .

There are two seemingly undesirable consequences of misspecification. The first, as alluded to above, is that is biased in the sense that the point around which concentrates is instead of the true volatility coefficient . The second is more subtle and concerns the spread of . Kleijn and van der Vaart, (2012, Sec. 1) point out that the asymptotic variance in their Bernstein–von Mises theorem may not agree with that for based on M-estimation theory (e.g., van der Vaart, 1998, Ch. 5). Indeed, the maximum likelihood estimator for the misspecified model can be viewed as an M-estimator and will, therefore, be asymptotically normal, with asymptotic variance given by the so-called “sandwich formula” which, in this case, gives

This follows from the calculations leading up to (12) in the Appendix. Up to order , this closely resembles the asymptotic variance in Theorem 1; in particular, if were equal to the term in braces above, then the two variance formulas agree. Note that the genuine Bayes posterior has and, therefore, will have asymptotic variance larger than that in the above display. Consequently, the Bayesian posterior credible intervals would be too large, making the inference inefficient. Section 3 below describes how we can correct for these two undesirable consequences of misspecification.

3 Correcting for misspecification

As discussed above, there are two effects of the model misspecification on , both depending on the quadratic variation of the jump portion of the process. To deal with these effects, we will need a suitable estimator of the quadratic variation . Intuitively, those observed differences which are of relatively large magnitude are likely due to jumps, so a reasonable estimator is

| (5) |

where is a sequence that vanishes sufficiently slow, and is the indicator function. We claim that if for some , then

| (6) |

for -almost all . Results of this type for Lévy processes are available in the literature (e.g., Aït-Sahalia and Jacod, 2014, Fact 3.7), but the proof of (6) given in the Appendix under only the finite jump activity assumption is relatively simple. With a suitable estimator in hand, now we are ready to address the effects of misspecification.

Towards constructing a modified posterior for the volatility, we must consider the following question: what is the “correct/optimal” asymptotic variance in the normal approximation? Of course, the best possible inference obtains if the model is not misspecified, i.e., there are no jumps; this is equivalent to the case where the sample path of the process is fully observed since, in that case, the jumps are visible and can be removed. An easy calculations reveals that, in this ideal case, the asymptotic variance is the Cramér–Rao bound, . This optimal variance obtains in Theorem 1 if

This suggests we choose in (3) as

| (7) |

so that, by (6), in -probability for -almost all . With this understanding, we define a “modified” Bayesian posterior as the distribution of when is distributed as in (3), with as in (7). In other words, if is the density function corresponding to , then has density function

| (8) |

Then we have the following Bernstein–von Mises theorem for .

Theorem 2.

Proof.

The first observation is that, since is a consistent estimator of , the modified posterior is concentrating around the true volatility coefficient, as desired. Furthermore, by our choice of the sequence , the asymptotic variance agrees with that achieved in the ideal case where there are no jumps present or, equivalently, when the sample path of the process is fully observed. The remaining question is if the posterior variance agrees with the variance of the center under . Proposition 1 in Aït-Sahalia and Jacod, (2010) reveals that, in the present setting, under , the estimator satisfies a central limit theorem, with asymptotic variance . Therefore, the credible intervals coming from the modified posterior will be asymptotically valid under , i.e., the coverage probability of the % credible intervals will converge to for -almost all . It follows immediately from the dominated convergence theorem that the coverage probability converges to under as well. It turns out that the finite-sample performance depends on the choice of threshold in (5) and we address this in Section 4.

4 Numerical results

An important question is how to choose the threshold . The theory says that we need for some and some but, in finite samples, and are not independent parameters; that is, only the value of matters, not the particular . This point is discussed at length in Aït-Sahalia and Jacod, (2014, Sec. 6.2.2), and they suggest one reasonable strategy for choosing . We consider here a simpler approach based on outlier detection. That is, let denote the interquartile range of the observed increment magnitudes ; this value is likely to be small since almost all of the increments correspond to the diffusion part of the process. Take to be some value that lower-bounds the set of all s that exceeds some cutoff, say, . We make no claims that this approach is “optimal” in any sense, only that it is both simple and reasonable.

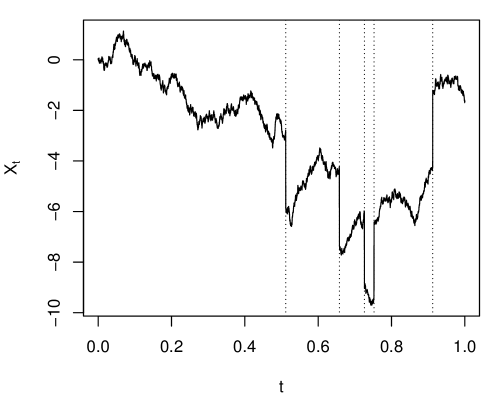

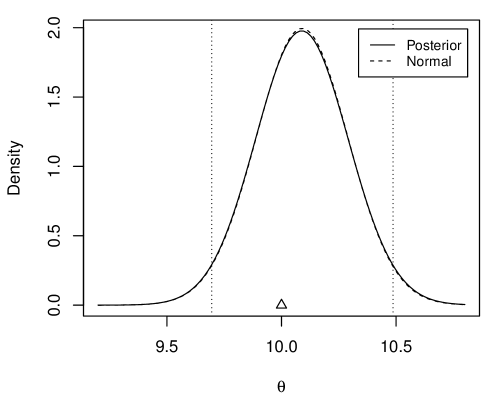

For illustration, consider the model (1) with drift , volatility , and compound Poisson process jumps with a rate of jumps per unit time and jumps sampled from the discrete uniform distribution on with . We simulate equally spaced observations from this process. A plot of the observed sample path on the interval is shown in Figure 1(a) with the jump times highlighted by vertical lines. For the misspecified Bayes model, we consider a conjugate inverse gamma prior with shape and rate ; the presence of the temperature parameter does not affect conjugacy. We also fix based on the interquartile range strategy described above. Figure 1(b) shows the posterior density function (8), the corresponding 95% credible interval for the volatility, and the density function of the normal approximation in Theorem 2. The key observations here are that modified posterior density is centered very close to the true volatility in this case, and hence the credible interval contains it, and also that the posterior density and the normal approximation are very similar. Since the the normal approximation has variance equal to the Cramér–Rao lower bound under the benchmark no-jumps model, the plot Figure 1(b) reveals the overall efficiency of the modified posterior inference.

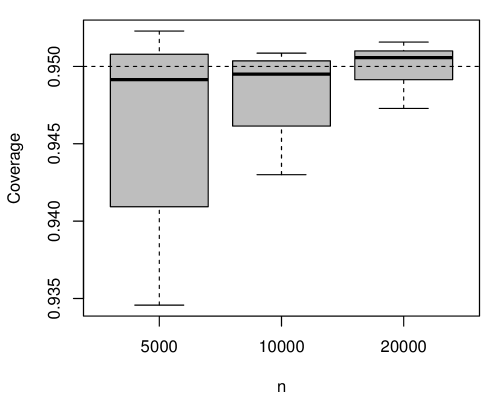

To further investigate the finite-sample properties our proposed approach for inference on the volatility, we consider a simulation study. Using the same model as above, but varying the jump rate , the jump magnitude , and the sample size , we investigate the coverage probability of the modified pseudo-Bayesian credible intervals, based on the choice of threshold mentioned above. Figure 2 displays the empirical coverage probability, based on 5000 Monte Carlo simulations in each setting, summarized over the jump rate and standard deviation, for several values of . This plot reveals that the choice of threshold based on the interquartile range performs reasonably well in this setting, giving coverage probabilities very close to the nominal 95% level.

5 Concluding remarks

In this paper we considered the construction of a (Bayesian-like) posterior for inference on the volatility coefficient in a jump diffusion model where the distribution for the jump part of the process is left unspecified. By working with a “purposely misspecified” model we avoid the difficulties of modeling the jump part, as well as the corresponding computations, but the cost is some misspecification bias. We correct for this bias by making two modifications: a non-trivial scaling of the likelihood, followed by a location shift. We prove that this modified posterior is asymptotically normal and optimal in the sense that the asymptotic variance agrees with the Cramér–Rao lower bound under the no-jumps model. Aside from the asymptotic results, these modifications are easy to implement and, as shown in Section 4, gives valid inference in a range of examples.

Of course, this “misspecification on purpose” strategy could be used in many other problems to provide valid uncertainty quantification for the parameters of interest without having to specify a complete model for the possibly very complex nuisance parameters, which is very attractive. Furthermore, when one has reliable prior information about the interest parameter, it is straightforward to incorporate this into the proposed analysis compared to a fully non-Bayesian approach, say, using M-estimation with bootstrap.

For this particular model, there are several extensions that one could consider. For example, if the drift parameter was also of interest, then, instead of ignoring as we did here, it would be relatively straightforward to construct the same modified posterior for the pair . More interesting is the case where the volatility parameter is not a scalar constant but, instead, a function . Certain functionals of , in particular, the average volatility , can be inferred directly using virtually the same techniques as presented here. Inference on the function itself would be more involved, but the analysis would be similar. Application of the “misspecification on purpose” strategy in the case where the volatility is a function depending on the sample path itself, i.e., , is an interesting open problem.

Appendix A Proofs

A.1 Proof of Theorem 1

Without loss of generality, we will assume in the proof that and . To prove the Bernstein–von Mises theorem, follow the approach described in Theorem 2.1 of Kleijn and van der Vaart, (2012). Our first objective is to show that

for any sequence of constants . To establish this, we need only to study the posterior mean and variance. That is, if denotes expectation with respect to the posterior , then, by Markov’s inequality, we have

| (9) |

To show that the expectation of the left-hand side in the above display vanishes, it suffices to show that

| (10) |

Towards this, we will use the Laplace approximation which says that, for suitable functions , the posterior mean of is

Therefore, in our case, if we apply the above to , then we have

Since the log-likelihood function for our misspecified model has a unique maximum in the interior of the -space and satisfies , the big-oh term above is uniform in observations, i.e., the term in the above display is a function of that can be uniformly bounded by a constant times and, in particular, the scaling by does not affect this conclusion. Therefore, to get (10), it suffices to show that

| (11) |

Towards showing (11), we recall that where, under , are independent with

and are defined in (4). It follows that has the same distribution as times a non-central chi-square random variable, , with degrees of freedom and non-centrality parameter . In particular,

If we let denote variance with respect to , then we have that

Plugging in the formulas for the mean and variance of and simplifying, gives

| (12) |

This is clearly , so we have established (11). Note that this derivation depends on only through and . Since (11) implies (10), we have proved the claimed posterior concentration rate result.

Next, we need to demonstrate that the model is suitably regular. More specifically, Theorem 2.1 in Kleijn and van der Vaart, (2012) require that the model satisfies a certain local asymptotic normality property, i.e., the log-likelihood ratio has a quadratic approximation locally around the specified . Since the misspecified model is so nice, it is a straightforward exercise to show that

where and . The above display holds uniformly on compact subsets of , and it follows from (11) that is bounded in -probability. Therefore, the assertion in Theorem 1 follows from Kleijn and van der Vaart’s.

The extension of these results to the unconditional distribution, , is also straightforward. Based on the finite jump activity assumption, all that we demonstrated above holds with -probability 1. In particular, we have that, for any ,

Since this sequence is bounded and converges almost surely, it follows from the dominated convergence theorem that

i.e., in -probability.

A.2 Proof of the claim in Equation (6)

For -almost all , we have that are independent under with

where are given in (4) and only for those indices . To prove the claim in Equation (6), we split the indices to those that contain a jump (in ) and those that do not (in ). Then we get

Take absolute value of both sides, apply the triangle inequality, and then take expectation. This yields the inequality

We will proceed by showing, one by one, that each of the four terms in the upper bound above is . First, note that

are iid and hence its fourth moment is bounded by a constant independent of . Then we have, by the Cauchy–Schwartz inequality

It is clear that is of order . So we only need to find a good bound for the tail probability. Assume, for the moment, that . Using the usual normal tail probability bounds, we get

So, if , for , then the upper bound for the above tail probability is for any positive integer . Hence it follows easily

the same conclusion can be reached if . Next,

and, similarly, using Cauchy–Schwartz,

For the last term, we need to bound . Again, without loss of generality, if we assume that and , then we get

which, using the normal tail probability bound again, is bounded by

Since is a fixed constant, the above quantity vanishes exponentially fast, so

All four terms have been shown to be , completing the proof of (6). Finally, note that the result holds for all such that and are finite. Since this is a -probability 1 event, (6) holds for -almost all .

References

- Aït-Sahalia, (2002) Aït-Sahalia, Y. (2002). Maximum likelihood estimation of discretely sampled diffusions: a closed-form approximation approach. Econometrica, 70(1):223–262.

- Aït-Sahalia, (2006) Aït-Sahalia, Y. (2006). Likelihood inference for diffusions: a survey. In Frontiers in statistics, pages 369–405. Imp. Coll. Press, London.

- Aït-Sahalia and Jacod, (2009) Aït-Sahalia, Y. and Jacod, J. (2009). Testing for jumps in a discretely observed process. Ann. Statist., 37(1):184–222.

- Aït-Sahalia and Jacod, (2010) Aït-Sahalia, Y. and Jacod, J. (2010). Is Brownian motion necessary to model high-frequency data? Ann. Statist., 38(5):3093–3128.

- Aït-Sahalia and Jacod, (2014) Aït-Sahalia, Y. and Jacod, J. (2014). High-Frequency Financial Econometrics. Princeton University Press.

- Barndorff-Nielsen and Shepard, (2006) Barndorff-Nielsen, O. and Shepard, N. (2006). Econometrics of testing for jumps in financial economics using bipower variation. J. Financ. Economet., 4(1):1–30.

- Beskos et al., (2006) Beskos, A., Papaspiliopoulos, O., Roberts, G. O., and Fearnhead, P. (2006). Exact and computationally efficient likelihood-based estimation for discretely observed diffusion processes. J. R. Stat. Soc. Ser. B Stat. Methodol., 68(3):333–382. With discussions and a reply by the authors.

- Bissiri et al., (2016) Bissiri, P. G., Holmes, C. C., and Walker, S. G. (2016). A general framework for updating belief distributions. J. R. Stat. Soc. Ser. B. Stat. Methodol., 78(5):1103–1130.

- Carr and Wu, (2003) Carr, P. and Wu, L. (2003). What type of process underlies options? a simple robust test. J. Finance, 58(6):2581–2610.

- Casella and Roberts, (2011) Casella, B. and Roberts, G. O. (2011). Exact simulation of jump-diffusion processes with Monte Carlo applications. Methodol. Comput. Appl. Probab., 13(3):449–473.

- Figueroa-López, (2009) Figueroa-López, J. E. (2009). Nonparametric estimation of Lévy models based on discrete-sampling. In Optimality, volume 57 of IMS Lecture Notes Monogr. Ser., pages 117–146. Inst. Math. Statist., Beachwood, OH.

- Golightly, (2009) Golightly, A. (2009). Bayesian filtering for jump-diffusions with application to stochastic volatility. J. Comput. Graph. Statist., 18(2):384–400.

- Gonçalves and Roberts, (2014) Gonçalves, F. B. and Roberts, G. O. (2014). Exact simulation problems for jump-diffusions. Methodol. Comput. Appl. Probab., 16(4):907–930.

- Grünwald and van Ommen, (2016) Grünwald, P. and van Ommen, T. (2016). Inconsistency of bayesian inference for misspecifed llinear models and a proposal for repairing it. Unpublished manuscript, arXiv:1412:3730.

- Jiang and Tanner, (2008) Jiang, W. and Tanner, M. A. (2008). Gibbs posterior for variable selection in high-dimensional classification and data mining. Ann. Statist., 36(5):2207–2231.

- Johannes and Polson, (2009) Johannes, M. and Polson, N. (2009). MCMC methods for financial econometrics. In Y., A.-S. and Hansen, J., editors, Handbook of Financial Econometrics, volume 2, pages 1–72. Elsevier, Oxford.

- Kleijn and van der Vaart, (2012) Kleijn, B. J. K. and van der Vaart, A. W. (2012). The Bernstein-Von-Mises theorem under misspecification. Electron. J. Stat., 6:354–381.

- Medvedev and Scaillet, (2007) Medvedev, A. and Scaillet, O. (2007). Approximation and calibration of short-term implied volatilities under jump-diffusion stochastic volatility. Rev. Financ. Stud., 20(2):427–459.

- Musiela and Rutkowski, (2005) Musiela, M. and Rutkowski, M. (2005). Martingale Methods in Financial Modelling, volume 36 of Stochastic Modelling and Applied Probability. Springer-Verlag, Berlin, second edition.

- Podolskij, (2006) Podolskij, M. (2006). New theory on estimation of integrated volatility with applications. PhD thesis, Ruhr-Universität Bochum.

- Rifo and Torres, (2009) Rifo, L. L. R. and Torres, S. (2009). Full Bayesian analysis for a class of jump-diffusion models. Comm. Statist. Theory Methods, 38(8-10):1262–1271.

- Syring and Martin, (2016) Syring, N. and Martin, R. (2016). Calibrating general posterior credible regions. Unpublished manuscript, arXiv:1509.00922.

- van der Vaart, (1998) van der Vaart, A. W. (1998). Asymptotic Statistics. Cambridge University Press, Cambridge.

- (24) Zhang, T. (2006a). From -entropy to KL-entropy: analysis of minimum information complexity density estimation. Ann. Statist., 34(5):2180–2210.

- (25) Zhang, T. (2006b). Information theoretical upper and lower bounds for statistical estimation. IEEE Trans. Inform. Theory, 52(4):1307–1321.