Allocation of risk capital in a cost cooperative game induced by a modified Expected Shortfall

Abstract

The standard theory of coherent risk measures fails to consider individual institutions as part of a system which might itself experience instability and spread new sources of risk to the market participants. In compliance with an approach adopted by Shapley and Shubik (1969), this paper proposes a cooperative market game where agents and institutions play the same role can be developed. We take into account a multiple institutions framework where some of them jointly experience distress events in order to evaluate their individual and collective impact on the remaining institutions in the market. To carry out this analysis, we define a new risk measure (), generalising the Expected Shortfall of Acerbi (2002) and we characterise the riskiness profile as the outcome of a cost cooperative game played by institutions in distress (a similar approach was adopted by Denault 2001). Each institution’s marginal contribution to the spread of riskiness towards the safe institutions in then evaluated by calculating suitable solution concepts of the game such as the Banzhaf–Coleman and the Shapley–Shubik values.

Keywords: Cooperative market game, Shapley Value, risk measures, Value–at–Risk, expected shortfall, systemic risk.

1 Introduction

The assessment of financial risk in a multi–institution framework

when some institutions are subject to systemic or non–systemic

distress is one of the main topics of the latest years which

received large attention from scholars in Mathematical Finance,

Statistics, Management, see, e.g., Adrian and Brunnermeier (2011, 2016), Billio et al. (2012), Acharya et al. (2012), Girardi and Ergün (2013), Hautsch et al. (2014), Engle et al. (2014), Lucas et al. (2014), Bernardi and Catania (2015), Sordo et al. (2015), just to quote a few of the most relevant approaches. For an extensive and up to date survey on systemic risk measures, see Bisias et al. (2012), while the recent literature on systemic risk is reviewed by Benoit et al. (2016). Especially since 2008, Lehmann Brothers’ collapse and the subsequent debt crisis contagion across Europe

raised crucial issues and questions to be addressed by new

macroeconomic and financial models. In particular, such events and

the related consequences provoked a wide increase in investigation

of instruments possibly suitable for risk evaluation, thereby

targeting the occurrence of contagion among institutions in distress

(see, among others, Drehmann and Tarashev 2013 on the

theoretical side and Huang et al. 2012a and Huang et al. 2012b on the

empirical side).

In this paper we are going to investigate circumstances where one or

more market institutions undergo financial distress and may spread

the contagion to the remaining safe institutions in the market.

Financial distress has a straightforward meaning: a condition of

dramatic financial instability of an institution, or lack of ability

to fully repay its creditors, or even the preliminary to bankruptcy

or liquidation. Although “financial distress” and “default” are

sometimes used interchangeably, there may be some differences, often

depending either on each country’s specific bankruptcy law or on the

institution’s rating and so on (see Altman and Hotchkiss 2010 for an extensive discussion).

When a financial distress takes place in the market, each distressed

institution affects the safe ones and individually contributes to

the systemic risk. A crucial aspect of the contagion frameworks is

the assessment of each agent’s (i.e. each institution’s) marginal

effect on systemic risk. In order to evaluate such contributions, a

natural and intuitive tool is the Shapley value (see

Shapley 1988), as well as the Banzhaf value (see

Banzhaf III 1965 and Owen 1995). It is interesting to note that,

although his world famous theories did not concern financial markets

specifically, L.S. Shapley, Nobel Laureate in Economic Sciences

in 2012, proposed a relevant application to market analysis in a paper with M. Shubik in 1969 (see Shapley and Shubik 1969). In that paper, Shapley and

Shubik defined and investigated the direct markets (see

Shapley and Shubik (1969), pp. 15–18), i.e., markets where, since each trader

possessed one initial unit of a personal commodity, traders might be

identified with commodities. As the Authors put it literally,

“A canonical market form – the direct market – is introduced,

in which the commodities are in effect the traders themselves, made

infinitely divisible…” (p. 11), hence that was the first attempt

to model a cooperative game where agents had a twice nature: traders

and assets at the same time.

Hence, classical solution concepts widely used in Cooperative Game

Theory such as the Shapley value and the Banzhaf value fit our

evaluation purposes. In more recent times, cooperative game theory

has already been employed for risk capital allocation by

Denault (2001) and in the latest years by

Csóka et al. (2009) and Abbasi and Hosseinifard (2013)111A

mechanism for allocation of risk capital to subportfolios of pooled

liabilities has been proposed by Tsanakas and Barnett in 2003 (see

Tsanakas and Barnett 2003) and by Tsanakas in 2009 (see Tsanakas 2009),

based on the Aumann–Shapley value.. However, in none of the above

papers a characteristic value expressing the difference between an

expected value in a non–distressed case and an expected value in a

distressed–case has been taken into account.

The financial setup we are going to investigate involves a set of

possibly distressed institutions (for example a set of banks) and a

set of safe institutions. Our purpose is an assessment of the

contagion risk, i.e., the extent to which the safe institutions can

be affected and damaged by the financial distress of the unsafe

ones. For this purpose, risk measures have been

extensively theorized and analyzed, giving rise to a rich strand of

literature. Some of them might provide helpful techniques for risk

allocation among a number of distinct systemic agents. In this

respect, the coherent risk measures have been and are a crucial tool

for the assignment of risk capital, both for the richness of

properties due to their axiomatic structure and for their

adaptability to fit several financial frameworks. The basic studies

on coherent risk measures have been published by Artzner et al. (1999) in 1999, who first provided an axiomatic characterization. Subsequently, in 2001 Denault (2001)

developed the analysis by taking into account a cooperative game

structure, where players are the firms involved in risky financial

activities, and the risk induced by the net worth of firms is the

value of the characteristic function of the game, and the

subadditivity axiom naturally induces a cost cooperative game.

The coherence of the Expected Shortfall (ES, hereafter) was taken into account by

Acerbi and Tasche (2002) in 2002, whereas an axiomatic approach was

adopted in 2005 by Kalkbrener (2005), to characterize the

related capital allocation procedures in portfolio management or

performance measurement. In recent years, further mathematical

results were achieved by Stoica (2006) (equivalence between

properties of some coherent measures with no arbitrage conditions),

Csóka et al. (2007, 2009) (refinement of measures

in a general equilibrium setup, stability of risk allocations),

Kountzakis and Polyrakis (2013) (applications to general

equilibrium models). Other relevant results in risk allocation

theory were provided in Drehmann and Tarashev (2013) and

Csóka and Pintér (2016). Furthermore, as a slightly different tool, distortion risk measures

have been applied to a financial contagion framework

by Cherubini and Mulinacci (2014).

The new approach we are going to propose builds on an alternative

risk measure which is an extension of ES and which is supposed to

incorporate the effect of the distressed institutions on a safe one.

Such a measure, denoted by

, represents the

expected value of a non–distressed institution conditional upon a

set of institutions under distress, given two

different thresholds , specifically related to the institutions’

returns. Subsequently, in order to evaluate the marginal contribution of each

distressed institution to overall systemic risk, we will construct a

cost function. Such a function aims to measure the cost of risk by

evaluating the mean of the differences between the standard Expected

Shortfalls and the values of of all non–distressed

institutions. This formula will be the characteristic value of a

cooperative game played by distressed institutions. Adopting a

classical approach, we will examine the properties of the game and

calculate the marginal impacts of each distressed institution,

pointing out the differences between the Shapley value and the

Banzhaf value of the game.

The introduced risk measurement framework is then adopted to empirically analyze the evolution of the risk measure and the output of the associated cooperative game of risk for eight Eurozone sovereign Credit Default Swaps (CDS) over the period 2008–2014. Our example assumes the Germany as the “safe” country, and explores how the evolution of the remaining countries’ debt conditions affect the health and financial stability of Germany considered as a “proxy” for the overall European system. As a byproduct of the proposed risk framework, the evolution of the total impact of the failure of the European system is monitored. Our results show that the risk of failure of the European system displays a transitory high level during period in between the Greece and Portugal bailouts (November 2010 – May 2011), but effectively remains at high levels when the ECB president Mario Draghi announces the implementation of the Outright Monetary Transactions (OMT) and the European Stability Mechanism (ESM) in the months thereafter. It is only after the implementation of the OMT, and the ESM, that the systemic risk of Germany settles more permanently at a level that is roughly 60% lower than during the crisis.

The remainder of the paper is structured as follows. In Section 2 the basic concepts about risk measures will be recalled, together with some axiomatic

details of coherent measures. Section 3 introduces the indicators

that will be crucial to our analysis, whereas in Section 4 the

cooperative game of risk and its solution concepts are exposed and

discussed. Section 5 is devoted to the empirical application and Section 6, conclusions and possible future developments are laid out.

2 Risk measures in portfolio management

Here we will outline the standard notation for risk measurement in recent literature, largely borrowed from the seminal paper by Artzner Artzner et al. (1999) and Kalkbrener (2005).

Consider a finite set of states of nature , whose cardinality is . Call a random variable indicating the final net worth of a position in state after a certain time interval, i.e., the possible profit and loss realization of a portfolio in state . We can identify the set of all real-valued functions (which can also be viewed as the set of all risks) on as , whose elements are of the kind . In the rigorous construction proposed in Artzner et al. (1999), a measure of risk is a mapping such that corresponds to the minimum amount of extra cash an agent has to add to her risky portfolio, in order to ensure that this investment is still acceptable to the regulator222This property relies on the acceptance sets, which are axiomatized in Artzner et al. (1999). when using a suitable reference instrument. The basic requirement concerns the price of the asset: 1 is the initial price of the asset and is the total return on the reference instrument at a final date , in all possible states of nature. In Artzner et al. (1999) the Definition of a coherent measure is then provided based on an axiomatic structure.

Definition 1.

A function is called a coherent measure of risk if it satisfies the following axioms:

-

-

Monotonicity (M): for all such that (i.e. for almost all ), .

-

-

Subadditivity (S): for all , .

-

-

Positive Homogeneity (PH): for all and , .

-

-

Translation Invariance (TI)333Property TI is sometimes denoted as Risk Free Condition (RFC).: for all and ,

We have to point out that the Value-at-Risk () satisfies all of them except Subadditivity, as is precisely exposed in Artzner et al. (1999) as well as the standard Definition of , which is recalled here:

Definition 2.

Given and the return on a reference instrument , the at level of the final net worth with probability is the negative of the quantile at level of , i.e.

Without loss of generality, in the remainder of the paper, will be normalized to .

Back to coherent measures, when the outcomes are equiprobable, i.e. when the state of nature occurs with probability and , a special and relevant case can be treated, as was investigated by Acerbi (2002). In particular, we take into account an ordered statistics given by the ordered values of the -tuple , i.e. , rearranged in increasing order: . The definition of spectral measure of risk we are going to present is due to Csóka et al. (2007), who slightly modified Acerbi’s original definition by employing a positive discount factor , not necessarily equal to 1 as in Acerbi (2002).

Definition 3.

If the outcomes are equiprobable, given a vector and a discount factor , the risk measure defined as follows:

| (1) |

is called a spectral measure of risk if satisfies the following axioms:

-

-

Nonnegativity (N1): for all .

-

-

Normalization (N2): .

-

-

Monotonicity (M): is non-increasing, i.e. for all , implies .

A well-known spectral measure of risk is the one indicating the discounted average of the worst outcomes, i.e. the -Expected Shortfall of . For all , it is given by

| (2) |

When is a continuous random variable, its formula reads as follows:

| (3) |

where is the law of and is the related confidence level. The proof of the coherence of in the continuous random variable setup can be found in Acerbi and Tasche (2002).

3 The as a risk measure

Here we propose a generalisation of the Adrian and Brunnermeier (2016)’s and , namely System– () and System– (). The proposed risk measures aim to capture interconnections among multiple connecting market participants which is particularly relevant during periods of financial market crisis, when several institutions may contemporaneously experience distress instances.

Let be a set of institutions, and assume that the conditioning event is the distress of a subset of . Call the set of institutions potentially under distress, whose cardinality is such that , hence meaning that at least one institution is not under distress and that at least one is under distress. If we consider a set of distressed institutions, such set represents a group of institutions picked among the ones that may be under distress. As is usual in typical Cooperative Game Theory literature, we will denominate any group as a coalition.

Given the confidence levels , we are going to define the of institution for all institutions not belonging to as follows. We are going to assume that at least one distressed institution has a negative return, i.e., that there exists at least one , to ensure possible positivity of the Expected Shortfall as has been defined by (2), when .

Call the joint cumulative density function of institution conditional on the set of institutions being under distress. Denote with the distribution function of the group of institutions , provided that the involved random variable coincides with the sum of all returns of the institutions in .

Definition 4.

Let be a vector of institution returns with probability . Given a set of institutions in distress and , for all , the is the following value:

| (4) |

where .

An alternative Definition of is the following one.

Definition 5.

Let be a vector of institution returns with probability . Given a set of institutions in distress and , for all , the is the maximum value taken by such that

| (5) |

Basically, is the Value-at-Risk of an institution subject to the condition that the sum of the realizations of the institutions under distress do not exceed the Value-at-Risk of their sum, when two different confidence levels are in general taken into account. The two following Remarks aim to point out two circumstances where coincides with the marginal .

Remark 6.

In this context it is quite natural to consider the sum as aggregated measure of risk since we are considering profits and losses. Of course alternative definitions are possible, as for example, the maximum loss of the distressed institutions, see, e.g., Bernardi et al. (2016) and discussion therein.

Remark 7.

If all the returns of the institutions in are independent of all the returns of institutions in , then the joint c.d.f. becomes , i.e. the c.d.f. of institution . Consequently,

Remark 8.

When no institution is under distress, , i.e. for all . In this case, (5) is well-defined too and in particular it collapses to the standard VaR. Namely,

The is particularly useful to formulate the risk measure we are going to investigate.

Definition 9.

Given and a set of institutions in distress, the is the expected value of institution , provided that it does not exceed and conditional upon the set of institutions being at the level of their joint -level:

| (6) |

As in Remark 8, (6) can be evaluated when no distress occurs too, collapsing to the standard Expected Shortfall:

A short explanation may be helpful to clarify the formulation of (6): the condition is always verified when all . On the other hand, just one negative institution return is enough to determine an open interval for such that the condition holds. More precisely, if are negative, where for , the condition boils down to: . Such an estimate is trivially true whenever all institution returns in a coalition are negative444Also note that the estimates on are as many as the possible coalitions except the empty set, i.e. , hence there are at most levels of that must be exceeded. Because the choice of in the definition of (2) is arbitrary, taking the maximum level among such values implies that such condition in (6) is always satisfied, consequently for all ..

Getting to analyze possible relations between and , we can prove some results.

Proposition 10.

Given two coalitions , if the following hypotheses are verified:

-

1.

;

-

2.

;

-

3.

,

then .

Proof.

If , the first hypothesis ensures that

whereas the second and the third hypotheses guarantee that and are well-defined, consequently

∎

In the remainder of the paper, whenever there is no misunderstanding, we are going to simply denote the above quantities with , , and , to lighten the notation.

4 A cooperative game for risk allocation induced by

The risk allocation problems were introduced by Denault (2001), where the problem of allocating the risk of a given firm, as measured by a coherent measure of risk, among its constituents, was taken into account, closely resembling the typical Cooperative Game Theory approach. In Denault (2001) cooperative games of cost were employed to model risk allocation problems, and the chosen solution concepts were the Shapley value and the Aumann–Shapley value. Such approach was subsequently adopted and improved in Csóka et al. (2009), where risk allocation games and totally balanced games are compared to ensure the existence of a stable allocation of risk. In particular, they define a risk environment characterized by a set of portfolios, a set of states of nature, a discrete probability density of realization of states, a matrix of realization vectors and a coherent measure of risk, from which they construct and analyze a risk allocation game. In both approaches, the portfolios of a firm are looked upon as the players of a subadditive cooperative game.

In our setting, we are ready to apply the measures defined in Section 3 to institutional circumstances where distress occurs, and in particular we are going to rely on some typical tools borrowed from Cooperative Game Theory. In more details, we will look upon any possible set of distressed institutions as a coalition of a cooperative game (or TU-game, see Owen 1995). The effect of distress on the remaining institutions, corresponding to risk of contagion, will be evaluated by means of a cost function.

Call the set of institutions not belonging to , i.e. . We can evaluate the cost of risk induced by any coalition by taking a weighted arithmetic mean over all differences between the unconditioned and the for all institutions in , i.e.

| (7) |

where for all , , for all .

In the frame of risk allocation, we introduce a cooperative game , where represents the the set of involved portfolios and is as in (7), and assigns a cost to each coalition .

The cooperative game approach appears very suitable, in that in an uncertain financial framework it allows to take into account all possible combinations of institutions undergoing distress.

Moreover, the couple actually defines a

cooperative game. In fact, when no institution in is

under distress, then because all the differences

in the numerator of (7) vanish. Essentially, this hypothesis,

which is necessary to define a cooperative game on ,

may have a clear-cut financial interpretation: all the safe

institutions are collected in , meaning that all of them are

secured beyond a reasonable doubt. They can be viewed as states or

companies issuing either government bonds or securities guaranteed

by top-quality collateral, namely all the kinds of agents which do

not involve any risk factors. Also note the positive sign in

(7): in standard payoff cooperative games such sign is

reversed. But because we are assuming that below the confidence

level some realizations are negative, positivity

of is ensured, hence the level of risk induced

by distress can be positive. However, it may occur that for some

coalition , is non-positive, but this would mean that

the contagion is even less likely to spread from such a group of

institutions to the non-distressed ones.

Formula (7) needs some further explanation, in terms of what the

differences between and actually measure. Each

difference provides the spread between the standard risk and the

risk which is correlated to the distress of a coalition ,

composed of one institution at least. In order to completely assess

the risk effect caused by any coalition , the sum of those

differences is taken over the whole set of safe institutions .

Perhaps some structural differences may occur among the safe

institutions, including insurance contracts, implementation of

hedging strategies, and so on. Such heterogeneity can be captured by

weights in (7), which can also be interpreted as

directly dependent of each single institution, in compliance with

its size or its systemic relevance. In order to lighten the

notation, we are going to hypothesize a simplified scenario where

all institutions’ weights are equal, then we are going to posit

.

The issue concerning the properties of the game (7) is

somewhat complex, due to the fact that the of an institution

subject to an external distress is a kind of measure of correlation,

or also a measure of how distress spreads its contagion towards

non-distressed institutions. Consequently, the standard axioms

associated to coherent risk measures can hardly be demonstrated.

Instead of an axiomatization, we are going to outline some

characteristics of , which are listed in the next

Propositions. Some of these properties resemble the axioms stated by

Denault (2001).

Proposition 11.

Given two coalitions , if the following hypotheses are verified:

-

1.

;

-

2.

;

-

3.

,

then .

Proof.

It follows directly from the inequality in Proposition 10. ∎

In the following Proposition, the expression means that all the institution returns in are multiplied by , i.e. , for all .

Proposition 12.

For each , .

Proof.

Applying Definition 5 to , for all , implies that is the maximum such that

By the positive homogeneity of (see either Artzner et al. 1999 or McNeil et al. 2015, p. 74), that expression coincides with

(5), hence .

For all , linearity of can be employed in the

expression of :

Finally, can be written as follows:

| (8) |

∎

Proposition 13.

For all such that all the returns , where , are independent of all returns , where , .

Proof.

For all institution returns which are independent of all (see Remark 7), where and , we have that . If this holds for all , the proof is complete. ∎

Subadditivity is a key feature of cost allocation games. Recall that is subadditive when its cost function is subadditive, i.e. for all such that , (e.g. Anily and Haviv 2014). As is shown in the next Proposition, the game is not always subadditive. In particular, some assumptions on the related and are supposed to hold.

Proposition 14.

If , and is superadditive, i.e.

then is subadditive.

Proof.

By definition of subadditivity, we can note that for all , where :

then, if , and is superadditive, i.e.

then is subadditive. ∎

However, it is difficult and restrictive to impose this condition, because the very definition of allows both its possible positivity and negativity, depending on the level at which the worst outcomes are taken.

4.1 Risk allocation

A typical and well-known application of cooperative games is the determination of suitable allocations among players who get a share of a total amount, which is a benefit when they play a payoff game (generally superadditive) and a cost when they play a cost game (generally subadditive). In this case, by Proposition 14, subadditivity is not ensured, but the characteristic function of the game represents a contagion risk induced by distress of some institutions, hence its interpretation as a cost game sounds intuitive and natural.

A complete presentation of the several solution concepts and allocation rules in cooperative games can be found in Owen (1995). The two main values we are going to apply to our setup are the Shapley-Shubik (first introduced in 1953, see Shapley 1988) and the Banzhaf-Coleman (which was formulated in 1965, see Banzhaf III 1965) values. What follow are the expressions of such allocation principles when employing the characteristic function .

The Shapley value of the game is given by the -dimensional vector such that:

| (9) |

for all .

On the other hand, the Banzhaf value of is the -dimensional vector such that:

| (10) |

for all .

Their respective axiomatizations555There exists a large number of contributions on axiomatizations of values in literature, see for example Feltkamp (1995) and van den Brink and van der Laan (1998). point out a crucial difference between (9) and (10): the Shapley value satisfies the efficiency axiom666Nonetheless, some recent contributions have been published on the Shapley value without the efficiency axiom, see Einy and Haimanko (2011) for simple voting games and Casajus (2014) for different classes of games., i.e. , whereas the Banzahf value does not, except when . On one hand, such axiom conveys the idea that there is an aggregate amount of risk capital to be apportioned among institutions in distress. On the other hand, perhaps it is helpful to avoid thinking of risk as a unique object to be divided, given its specific characteristics. Loosely speaking, we stress that both values can be employed based on good motivations.

Clearly, we can say that is a dummy institution if and only if , , . The economic meaning of a dummy institution is simple: its marginal contribution to overall contagion is always zero.

A special discussion should be devoted to the so-called no undercut property (see Denault (2001), Def. 3), which can be reformulated as follows: given an allocation for the game , for all , the inequality

| (11) |

must hold. The condition (11) has a twofold meaning. The first one is technical: any allocation satisfying it for all is in the core of the cooperative game, consequently if at least one allocation of this kind exists, the core is non-empty. The second meaning is strictly connected to a financial aspect (see Denault (2001)): an undercut happens when a portfolio allocation exceeds the risk capital that the whole group of institutions would face.

Relying on previous results, we can establish some sufficient conditions for positivity of and , i.e. to ensure that all their coordinates are non-negative, meaning that each distressed institution brings a positive marginal contribution to systemic risk.

Proposition 15.

If for all and for all the following hypotheses are verified:

-

1.

;

-

2.

;

-

3.

,

then and for all .

5 Application

To illustrate how the risk measure behaves in

practice we examine the evolution of European Sovereign Credit

Spreads (CDS) over a period that includes the Eurozone sovereign

debt crisis of 2012. Specifically, we investigate the evolution over

time of the Shapley–Value induced by the cooperative Game

where the Germany acts as the only “safe” country, as

described in the previous sections. The potentially distressed

countries are: Belgium, France, Greece, Italy, Netherlands, Portugal

and Spain. We consider a panel of daily CDS spreads over the period

from July 21st, 2008 to December 30th, 2014 except for the Greece

for which the data are available only until March 8, 2012. We use

US–denominated sovereign CDS for each country using data

obtained from Datastream. Our aim is to assess how the events

related to the European sovereign debt crisis impact the safety of

the most important economy in the Euro area, using the provided risk

measure and the associated risk measurement framework based on the

cooperative game. A similar empirical investigation has been conducted by

Bernardi and Catania (2015) using stock market data of the major European financial indexes,

Lucas et al. (2014) using dynamic Generalised Autoregressive Score (GAS) models on CDS, and Engle et al. (2014) again using stock market data of European individual institutions, and Blasques et al. (2014) using spatial GAS models on European sovereign debt CDS.

Major financial events affecting the Euro area

during the considered period are collected in Table

2. Since EU countries have been affected by the crisis to different

degree, sovereign credit spreads in Europe are strongly correlated.

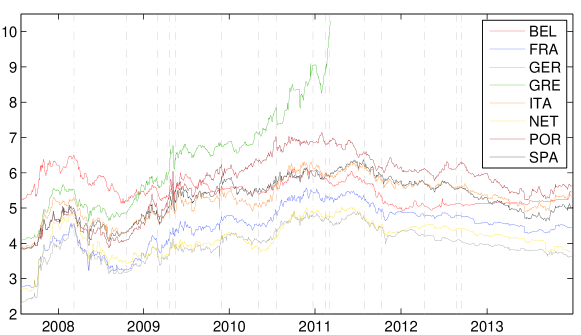

Figure 1 shows the evolution of the credit default

spreads in log basis points for the period covered by our analysis.

Visual inspection of the series reveals clear common patterns

particularly between Netherlands and Germany on the one hand and

Italy and Spain on the other hand. As expected, the evolution of the

Greek CDS strongly differs from those of the other countries in the

sample. Summary statistics of log CDS returns multiplied by

are reported in Table 1.

In order to calculate the risk measure a parametric

assumption about the joint distribution of the involved CDS

log–returns should be made. Although not always supported by the

empirical evidence, we assume that the CDS returns are jointly

Gaussian. The Gaussian assumption is not only convenient but it represents also a

common choice for practical applications, and it favours the interpretation of the estimation

results as the output of a graphical model, see Koller and Friedman (2009). Nevertheless the Gaussian distribution can be easily replaced by either another parametric distribution or by more involved dynamic models that describe the evolution over time of the CDS, see, for example, Bernardi and Catania (2015). Proposition 16 in Appendix

Appendix provides the analytical formulas to

calculate , , and under the Gaussian

assumption. As far as parameter estimation is concerned we apply the

Graphical–Lasso algorithm of Friedman et al. (2008), which allows for sparse covariance estimation. The tuning parameter that regulates the amount of sparsity in the covariance structure has been fixed at , where denotes the sample size, as suggested by the theory Ravikumar et al. (2011), see also Hastie et al. (2015) and references therein.

To analyse more deeply the impact of the recent European

Sovereign debt crisis, we estimate recursively the SCoES over the

sample period using a rolling window.

| Name | Min | Max | Mean | Std. Dev. | Skewness | Kurtosis | 1% Str. Lev. | JB |

|---|---|---|---|---|---|---|---|---|

| Belgium | -21.912 | 13.854 | -0.049 | 2.726 | -0.422 | 12.144 | -7.999 | 5477.445 |

| France | -23.002 | 18.643 | 0.023 | 3.155 | -0.213 | 10.068 | -9.525 | 3257.265 |

| Germany | -33.747 | 30.839 | -0.017 | 3.367 | -0.368 | 21.499 | -9.535 | 22264.754 |

| Greece | -48.983 | 23.611 | 0.401 | 5.183 | -1.029 | 17.169 | -13.700 | 6081.685 |

| Italy | -42.675 | 34.358 | 0.011 | 4.237 | -0.579 | 17.933 | -12.229 | 14571.710 |

| Netherlands | -25.672 | 18.572 | -0.047 | 3.028 | -0.466 | 13.130 | -9.669 | 6721.984 |

| Portugal | -61.177 | 26.909 | 0.064 | 4.320 | -1.616 | 33.500 | -10.911 | 61104.578 |

| Spain | -35.180 | 27.174 | 0.020 | 4.137 | -0.078 | 11.616 | -11.781 | 4824.268 |

| Date | Event |

|---|---|

| Mar. 9, 2009 | the peak of the onset of the recent GFC. |

| Oct. 18, 2009 | Greece announces doubling of budget deficit. |

| Mar. 3, 2010 | EU offers financial help to Greece. |

| Apr. 23, 2010 | Greek Prime Minister calls for Eurozone–IMF rescue package. |

| Apr. 23, 2010 | Greece achievement of 18bn USD bailout from EFSF, IMF and bilateral loans. |

| Nov. 29, 2010 | Ireland achievement of 113bn USD bailout from EU, IMF and EFSF. |

| May 05, 2011 | the ECB bails out Portugal. |

| July 21, 2011 | Greece is bailed out. |

| Dec. 22, 2011 | ECB launches the first Long-Term Refinancing Operation (LTRO). |

| Feb. 12, 2012 | Greece passes its most severe austerity package yet. |

| Mar. 1, 2012 | ECB launches the second LTRO. |

| July 26, 2012 | unexpectedly, the ECB president Mario Draghi, announces that |

| “The ECB is ready to do whatever it takes to preserve the euro”. | |

| Oct. 8, 2012 | European Stability Mechanism (ESM) is inaugurated. |

| April 07, 2013 | the conference of the Portuguese Prime Minister regarding |

| the high court’s block of austerity plans. | |

| Aug. 23, 2013 | the Eurozone crisis leads to more bankruptcies in Italy. |

| Sep. 12, 2013 | European Parliament approves new unified bank supervision system. |

Moreover, to obtain results more robust to temporary

short–term shocks affecting the considered economies, we consider

weekly log–CDS returns. Specifically, at each point in time we

estimate the risk measure using a window of more recent

weekly observations, and then we run the cooperative game to get the

Shapley Value with . It is worth mentioning that, with institutions, we are going to estimate parameters. The Graphical–Lasso method of Friedman et al. (2008) delivers consistent estimates of the parameters even when the number of parameters is greater than the dimension of the sample, see Hastie et al. (2015) and Tibshirani (1996, 2011) for further details.

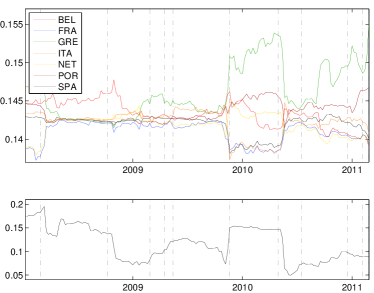

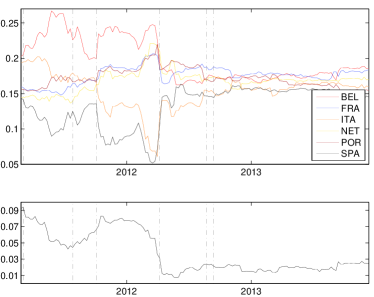

Results are reported in Figure

2, for the period before the onset of the

Greek crisis (2a), as well as for the

subsequent period (2b). For both

periods, the bottom panel reports the overall impact of the distress

of the remaining countries over the German economy as measured by

the . Throughout the sample period, the overall risk of

Germany due to the potential distress of one or more of the

remaining European countries is high, until mid 2011. At that

time, the level suddenly decreases to the lower level of about 0.09,

as a consequence of the bailouts of Portugal and Greece, in May and July 2011, respectively. The overall risk still remain at the level of 0.09 till the April 2013 a few months later the announcement of the implementation of the of the Outright Monetary

Transactions (OMT) and the European Stability Mechanism (ESM) in October 2012. If is worth noting that the launch of the first Long–Term Refinancing Operation (LTRO) by ECB in December 2011 and the second LTRO in March 2012 only had a moderate impact on the overall risk that decreased till mid 2012 and the unexpected strongest defence of the Euro of the ECB President Mario Draghi (July 26, 2012), did not contribute to reduce the risk of the Germany.

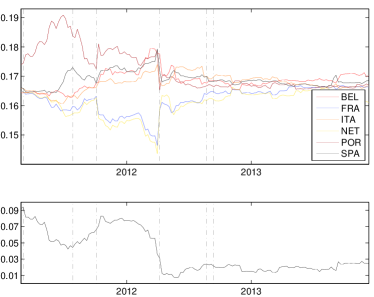

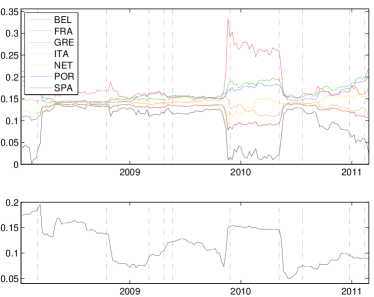

Concerning the evolution of the Shapley values reported in the top

panel of Figure 2 and the Banzhaf Value in Figure 3, they can be interpreted

as the normalised country risk factors. As expected, the two approaches provide different contributions to risk, in particular during the onset of the European crisis, reflecting their different properties. More precisely, the Shapley solution, suggests that, during the

period in between the bailout of Ireland (November 29, 2010) and the

bailout of Portugal (May 5, 2011), the most severe source of risk

for the Germany’s economy is represented by the Greece, while Spain,

Italy and France contribute less, see Figure 2. The picture by Banzhaf is a little bit different since, during the same period, the most important source of risk for Germany is Belgium, followed by Greece, a result which is a little bit surprisingly. Afterwards, the overall

contributions of European countries converge, for both methods. The failure of the

Greek austerity package in February 2012 suddenly increases the

riskiness of Greece which is comparable only with that of Portugal

at the beginning of 2011. Interestingly, the proposed approach is able to capture the most important events that happened during European sovereign debt crisis of 2012, as reported in Table 2.

6 Conclusions and further developments

This paper presents a cooperative game among distressed institutions

to assess the potential damage done by all possible coalitions in

distress. At this aim, a new risk measure which features some

properties of the standard Expected Shortfall in a financial

framework where some institutions are distressed and contagion

threatens the remaining safe institutions is developed. Standard

solution concepts like Shapley value and Banzhaf value can be

helpful to measure the marginal contributions to systemic risk.

Our study of the European sovereign debt crisis of 2012 provides empirical support for

the ability of the proposed cooperative Game approach to systemic

risk measurement to effectively capture the dynamic evolution of the

overall riskiness of the European countries. Furthermore, the proposed risk measurement

framework is able to identify the major sources of risk and the risk

contributions.

Further extensions of such a theoretical setup can be

conceived, in terms of more complex and precise cost functions to be

employed in the cooperative game. Moreover, a detailed analysis of

correlations among distressed institutions might give rise to

different game structures, such as a priori unions or bounded forms

of cooperation which can be described with the help of graphs. In such cases, a

model with some constraints might be necessary to determine the

characteristics of risk transmission and the related consequences on

the systemic risk. It is possible that a given structure with

certain links among institutions can minimize the contagion risk.

Acknowledgements

This research is supported by the Italian Ministry of Research PRIN 2013–2015, “Multivariate Statistical Methods for Risk Assessment” (MISURA), and by the “Carlo Giannini Research Fellowship”, the “Centro Interuniversitario di Econometria” (CIdE) and “UniCredit Foundation”. We would like to thank Rosella Castellano, Umberto Cherubini, Rita D’Ecclesia, Fabrizio Durante, Piotr Jaworski, Viviana Fanelli, Gianfranco Gambarelli, Sabrina Mulinacci, Roland Seydel, Marco Teodori, the audience at CFE-ERCIM 2014 in Pisa (Italy), and then audience at EURO 2016 in Poznan (Poland) for their valuable comments and suggestions. The usual disclaimer applies.

Appendix

In this Appendix we provide analytical formulas for the computation of the , , and , as formally defined in the previous sections, under the assumption of the joint Gaussian distribution of the involved variables.

Proposition 16.

Let where is a vector of location parameters and is a – symmetric variance-covariance matrix. Consider the transformation , for , then , with

| (12) | ||||

| (13) |

where denotes the covariance between and , and denotes the variance of . Under the previous assumptions the VaR, ES, of , for are calculated as follows:

| (14) | ||||

| (15) |

see, Nadarajah et al. (2014) and Bernardi (2013), while the SCoVaR and SCoES becomes

| (16) | ||||

| (17) |

for , where denotes the joint cdf of the random variables .

Equation (16) implicitly defines the as the value of that solves the conditional cdf of the involved variables equal to . The solution always exists and is unique because the involved random variables are absolutely continuous.

References

- Abbasi and Hosseinifard (2013) Babak Abbasi and S. Zahra Hosseinifard. Tail conditional expectation for multivariate distributions: A game theory approach. Statistics & Probability Letters, 83(10):2228 – 2235, 2013. ISSN 0167-7152. doi: http://dx.doi.org/10.1016/j.spl.2013.06.012. URL http://www.sciencedirect.com/science/article/pii/S0167715213002174.

- Acerbi (2002) Carlo Acerbi. Spectral measures of risk: A coherent representation of subjective risk aversion. Journal of Banking & Finance, 26(7):1505 – 1518, 2002. ISSN 0378-4266. doi: http://dx.doi.org/10.1016/S0378-4266(02)00281-9. URL http://www.sciencedirect.com/science/article/pii/S0378426602002819.

- Acerbi and Tasche (2002) Carlo Acerbi and Dirk Tasche. Expected shortfall: A natural coherent alternative to value at risk. Economic Notes, 31(2):379–388, 2002. ISSN 1468-0300. doi: 10.1111/1468-0300.00091. URL http://dx.doi.org/10.1111/1468-0300.00091.

- Acharya et al. (2012) V.V. Acharya, R.F. Engle, and M. Richardson. Capital shortfall: a new approach to ranking and regulating systemic risks. American Economic Review, 102:59–64, 2012.

- Adrian and Brunnermeier (2011) T. Adrian and M.K. Brunnermeier. Covar. Working paper, 2011.

- Adrian and Brunnermeier (2016) Tobias Adrian and Markus K. Brunnermeier. Covar. American Economic Review, 106(7):1705–41, July 2016. doi: 10.1257/aer.20120555. URL http://www.aeaweb.org/articles?id=10.1257/aer.20120555.

- Altman and Hotchkiss (2010) Edward I Altman and Edith Hotchkiss. Corporate financial distress and bankruptcy: Predict and avoid bankruptcy, analyze and invest in distressed debt, volume 289. John Wiley & Sons, 2010.

- Anily and Haviv (2014) Shoshana Anily and Moshe Haviv. Subadditive and homogeneous of degree one games are totally balanced. Oper. Res., 62(4):788–793, August 2014. ISSN 0030-364X. doi: 10.1287/opre.2014.1283. URL http://dx.doi.org/10.1287/opre.2014.1283.

- Artzner et al. (1999) Philippe Artzner, Freddy Delbaen, Jean-Marc Eber, and David Heath. Coherent measures of risk. Mathematical finance, 9(3):203–228, 1999.

- Banzhaf III (1965) John F Banzhaf III. Weighted voting doesn’t work: A mathematical analysis. Rutgers L. Rev., 19:317, 1965.

- Benoit et al. (2016) Sylvain Benoit, Jean-Edouard Colliard, Christophe Hurlin, and Christophe Pérignon. Where the risks lie: A survey on systemic risk. Review of Finance, 2016. doi: 10.1093/rof/rfw026. URL http://rof.oxfordjournals.org/content/early/2016/06/01/rof.rfw026.abstract.

- Bernardi (2013) M. Bernardi. Risk measures for skew normal mixtures. Statistics & Probability Letters, 83:1819–1824, 2013.

- Bernardi and Catania (2015) Mauro Bernardi and Leopoldo Catania. Switching-gas copula models with application to systemic risk. arXiv preprint arXiv:1504.03733, 2015.

- Bernardi et al. (2016) Mauro Bernardi, Fabrizio Durante, Piotr Jaworski, Petrella Lea, and Gianfausto Salvadori. Conditional risk based on multivariate hazard scenarios. working paper, 2016.

- Billio et al. (2012) M. Billio, M. Getmansky, A.W. Lo, and L. Pellizon. Econometric measures of connectedness and systemic risk in the finance and insurance sectors. Journal of Financial Econometrics, 101:535–559, 2012.

- Bisias et al. (2012) Dimitrios Bisias, Mark Flood, Andrew W. Lo, and Stavros Valavanis. A survey of systemic risk analytics. Annual Review of Financial Economics, 4(1):255–296, 2012. doi: 10.1146/annurev-financial-110311-101754. URL http://dx.doi.org/10.1146/annurev-financial-110311-101754.

- Blasques et al. (2014) Francisco Blasques, Siem Jan Koopman, Andre Lucas, and Julia Schaumburg. Spillover dynamics for systemic risk measurement using spatial financial time series models. Tinbergen Institute Discussion Paper 14-107/III, 2014.

- Casajus (2014) André Casajus. The Shapley value without efficiency and additivity. Math. Social Sci., 68:1–4, 2014. ISSN 0165-4896. doi: 10.1016/j.mathsocsci.2013.12.001. URL http://dx.doi.org/10.1016/j.mathsocsci.2013.12.001.

- Cherubini and Mulinacci (2014) Umberto Cherubini and Sabrina Mulinacci. Contagion-based distortion risk measures. Appl. Math. Lett., 27:85–89, 2014. ISSN 0893-9659. doi: 10.1016/j.aml.2013.07.007. URL http://dx.doi.org/10.1016/j.aml.2013.07.007.

- Csóka and Pintér (2016) Péter Csóka and Miklós Pintér. On the impossibility of fair risk allocation. B. E. J. Theor. Econ., 16(1):143–158, 2016. ISSN 2194-6124. doi: 10.1515/bejte-2014-0051. URL http://dx.doi.org/10.1515/bejte-2014-0051.

- Csóka et al. (2007) Péter Csóka, P. Jean-Jacques Herings, and László Á. Kóczy. Coherent measures of risk from a general equilibrium perspective. Journal of Banking & Finance, 31(8):2517 – 2534, 2007. ISSN 0378-4266. doi: http://dx.doi.org/10.1016/j.jbankfin.2006.10.026. URL http://www.sciencedirect.com/science/article/pii/S0378426607000404.

- Csóka et al. (2009) Péter Csóka, P. Jean-Jacques Herings, and László Á. Kóczy. Stable allocations of risk. Games and Economic Behavior, 67(1):266 – 276, 2009. ISSN 0899-8256. doi: http://dx.doi.org/10.1016/j.geb.2008.11.001. URL http://www.sciencedirect.com/science/article/pii/S0899825608002042. Special Section of Games and Economic Behavior Dedicated to the 8th ACM Conference on Electronic Commerce.

- Denault (2001) Michel Denault. Coherent allocation of risk capital. Journal of risk, 4:1–34, 2001.

- Drehmann and Tarashev (2013) Mathias Drehmann and Nikola Tarashev. Measuring the systemic importance of interconnected banks. Journal of Financial Intermediation, 22(4):586 – 607, 2013. ISSN 1042-9573. doi: http://dx.doi.org/10.1016/j.jfi.2013.08.001. URL http://www.sciencedirect.com/science/article/pii/S1042957313000326.

- Einy and Haimanko (2011) Ezra Einy and Ori Haimanko. Characterization of the Shapley-Shubik power index without the efficiency axiom. Games Econom. Behav., 73(2):615–621, 2011. ISSN 0899-8256. doi: 10.1016/j.geb.2011.03.007. URL http://dx.doi.org/10.1016/j.geb.2011.03.007.

- Engle et al. (2014) Robert Engle, Eric Jondeau, and Michael Rockinger. Systemic risk in europe. Review of Finance, 2014. doi: 10.1093/rof/rfu012. URL http://rof.oxfordjournals.org/content/early/2014/03/29/rof.rfu012.abstract.

- Feltkamp (1995) Vincent Feltkamp. Alternative axiomatic characterizations of the Shapley and Banzhaf values. Internat. J. Game Theory, 24(2):179–186, 1995. ISSN 0020-7276. doi: 10.1007/BF01240041. URL http://dx.doi.org/10.1007/BF01240041.

- Friedman et al. (2008) Jerome Friedman, Trevor Hastie, and Robert Tibshirani. Sparse inverse covariance estimation with the graphical lasso. Biostatistics, 9(3):432–441, 2008. doi: 10.1093/biostatistics/kxm045. URL http://biostatistics.oxfordjournals.org/content/9/3/432.abstract.

- Girardi and Ergün (2013) G. Girardi and A.T. Ergün. Systemic risk measurement: Multivariate garch estimation of covar. Journal of Banking & Finance, 37:3169–3180, 2013.

- Hastie et al. (2015) Trevor Hastie, Robert Tibshirani, and Martin Wainwright. Statistical Learning with Sparsity: The Lasso and Generalizations. CRC Press, 2015.

- Hautsch et al. (2014) Nikolaus Hautsch, Julia Schaumburg, and Melanie Schienle. Financial network systemic risk contributions. Review of Finance, 2014. doi: 10.1093/rof/rfu010. URL http://rof.oxfordjournals.org/content/early/2014/03/24/rof.rfu010.abstract.

- Huang et al. (2012a) Xin Huang, Hao Zhou, and Haibin Zhu. Systemic risk contributions. Journal of Financial Services Research, 42(1):55–83, 2012a. ISSN 1573-0735. doi: 10.1007/s10693-011-0117-8. URL http://dx.doi.org/10.1007/s10693-011-0117-8.

- Huang et al. (2012b) Xin Huang, Hao Zhou, and Haibin Zhu. Assessing the systemic risk of a heterogeneous portfolio of banks during the recent financial crisis. Journal of Financial Stability, 8(3):193 – 205, 2012b. ISSN 1572-3089. doi: http://dx.doi.org/10.1016/j.jfs.2011.10.004. URL http://www.sciencedirect.com/science/article/pii/S1572308911000544. The Financial Crisis of 2008, Credit Markets and Effects on Developed and Emerging Economies.

- Kalkbrener (2005) Michael Kalkbrener. An axiomatic approach to capital allocation. Math. Finance, 15(3):425–437, 2005. ISSN 0960-1627. doi: 10.1111/j.1467-9965.2005.00227.x. URL http://dx.doi.org/10.1111/j.1467-9965.2005.00227.x.

- Koller and Friedman (2009) Daphne Koller and Nir Friedman. Probabilistic graphical models: principles and techniques. MIT press, 2009.

- Kountzakis and Polyrakis (2013) C. Kountzakis and I. A. Polyrakis. Coherent risk measures in general economic models and price bubbles. J. Math. Econom., 49(3):201–209, 2013. ISSN 0304-4068. doi: 10.1016/j.jmateco.2013.02.002. URL http://dx.doi.org/10.1016/j.jmateco.2013.02.002.

- Lucas et al. (2014) André Lucas, Bernd Schwaab, and Xin Zhang. Conditional euro area sovereign default risk. Journal of Business & Economic Statistics, 32(2):271–284, 2014. doi: 10.1080/07350015.2013.873540. URL http://dx.doi.org/10.1080/07350015.2013.873540.

- McNeil et al. (2015) Alexander J McNeil, Rüdiger Frey, and Paul Embrechts. Quantitative risk management: Concepts, techniques and tools. Princeton university press, second edition, 2015.

- Nadarajah et al. (2014) Saralees Nadarajah, Bo Zhang, and Stephen Chan. Estimation methods for expected shortfall. Quantitative Finance, 14(2):271–291, 2014. doi: 10.1080/14697688.2013.816767. URL http://dx.doi.org/10.1080/14697688.2013.816767.

- Owen (1995) Guillermo Owen. Game theory. Academic Press: New York, third edition, 1995.

- Ravikumar et al. (2011) Pradeep Ravikumar, Martin J. Wainwright, Garvesh Raskutti, and Bin Yu. High-dimensional covariance estimation by minimizing -penalized log-determinant divergence. Electron. J. Statist., 5:935–980, 2011. doi: 10.1214/11-EJS631. URL http://dx.doi.org/10.1214/11-EJS631.

- Shapley (1988) Lloyd S. Shapley. A value for -person games [from contributions to the theory of games, vol. 2, 307–317, Princeton Univ. Press, Princeton, NJ, 1953; MR 14, 779]. In The Shapley value, pages 31–40. Cambridge Univ. Press, Cambridge, 1988. doi: 10.1017/CBO9780511528446.003. URL http://dx.doi.org/10.1017/CBO9780511528446.003.

- Shapley and Shubik (1969) Lloyd S. Shapley and Martin Shubik. On market games. J. Econom. Theory, 1:9–25 (1970), 1969. ISSN 0022-0531.

- Sordo et al. (2015) Miguel A. Sordo, Alfonso Suárez-Llorens, and Alfonso J. Bello. Comparison of conditional distributions in portfolios of dependent risks. Insurance: Mathematics and Economics, 61:62 – 69, 2015. ISSN 0167-6687. doi: http://dx.doi.org/10.1016/j.insmatheco.2014.11.008. URL http://www.sciencedirect.com/science/article/pii/S0167668714001607.

- Stoica (2006) George Stoica. Relevant coherent measures of risk. J. Math. Econom., 42(6):794–806, 2006. ISSN 0304-4068. doi: 10.1016/j.jmateco.2006.03.006. URL http://dx.doi.org/10.1016/j.jmateco.2006.03.006.

- Tibshirani (1996) Robert Tibshirani. Regression shrinkage and selection via the lasso. J. Roy. Statist. Soc. Ser. B, 58(1):267–288, 1996. ISSN 0035-9246. URL http://links.jstor.org/sici?sici=0035-9246(1996)58:1<267:RSASVT>2.0.CO;2-G&origin=MSN.

- Tibshirani (2011) Robert Tibshirani. Regression shrinkage and selection via the lasso: a retrospective. J. R. Stat. Soc. Ser. B Stat. Methodol., 73(3):273–282, 2011. ISSN 1369-7412. doi: 10.1111/j.1467-9868.2011.00771.x. URL http://dx.doi.org/10.1111/j.1467-9868.2011.00771.x.

- Tsanakas (2009) Andreas Tsanakas. To split or not to split: Capital allocation with convex risk measures. Insurance: Mathematics and Economics, 44(2):268 – 277, 2009. ISSN 0167-6687. doi: http://dx.doi.org/10.1016/j.insmatheco.2008.03.007. URL http://www.sciencedirect.com/science/article/pii/S0167668708000425.

- Tsanakas and Barnett (2003) Andreas Tsanakas and Christopher Barnett. Risk capital allocation and cooperative pricing of insurance liabilities. Insurance Math. Econom., 33(2):239–254, 2003. ISSN 0167-6687. doi: 10.1016/S0167-6687(03)00137-9. URL http://dx.doi.org/10.1016/S0167-6687(03)00137-9. Papers presented at the 6th IME Conference (Lisbon, 2002).

- van den Brink and van der Laan (1998) René van den Brink and Gerard van der Laan. Axiomatizations of the normalized Banzhaf value and the Shapley value. Soc. Choice Welf., 15(4):567–582, 1998. ISSN 0176-1714. doi: 10.1007/s003550050125. URL http://dx.doi.org/10.1007/s003550050125.