Two-step wavelet-based estimation for mixed Gaussian fractional processes ††thanks: The first author was partially supported by grant ANR-16-CE33-0020 MultiFracs. The second author was partially supported by the prime award no. W911NF-14-1-0475 from the Biomathematics subdivision of the Army Research Office, USA. The second author’s long term visits to ENS de Lyon were supported by the school. ††thanks: AMS Subject classification. Primary: 62M10, 60G18, 42C40. ††thanks: Keywords and phrases: fractional stochastic process, multivariate, operator self-similarity, demixing, wavelets.

Abstract

A mixed Gaussian fractional process is a multivariate stochastic process obtained by pre-multiplying a vector of independent, Gaussian fractional process entries by a nonsingular matrix . It is interpreted that is observable, while is a hidden process occurring in an (unknown) system of coordinates . Mixed processes naturally arise as approximations to solutions of physically relevant classes of multivariate fractional SDEs under aggregation. We propose a semiparametric two-step wavelet-based method for estimating both the demixing matrix and the memory parameters of . The asymptotic normality of the estimators is established both in continuous and discrete time. Monte Carlo experiments show that the finite sample estimation performance is comparable to that of parametric methods, while being very computationally efficient. As applications, we model a bivariate time series of annual tree ring width measurements, and establish the asymptotic normality of the eigenstructure of sample wavelet matrices.

1 Introduction

Numerous data sets from a wide range of applications in science, technology and engineering have been analyzed by means of fractional processes or models. Examples include natural systems (hydrodynamic turbulence, Mandelbrot (?); geophysics, Foufoula-Georgiou and Kumar (?); heart rate variability, Ivanov et al. (?); infraslow – i.e., below 1Hz – brain activity, Ciuciu et al. (?)) and artificial systems (e.g., Internet traffic, Taqqu et al. (?), Fontugne et al. (?)). Self-similar processes form a subclass of fractional processes that has been widely studied and used in applications. A univariate stochastic processes is called self-similar when it satisfies the scaling relation

| (1.1) |

for some Hurst exponent , where denotes the equality of finite dimensional distributions. In particular, fractional Brownian motion (fBm) is the only Gaussian, self-similar, stationary increment stochastic process (e.g., Embrechts and Maejima (?), Taqqu (?)). The probability theory and statistical methodology for univariate self-similar and related processes is now voluminous (e.g., Mandelbrot and Van Ness (?), Taqqu (?, ?), Dobrushin and Major (?), Granger and Joyeux (?), Hosking (?), Fox and Taqqu (?), Dahlhaus (?), Beran (?), Robinson (?, ?), Beran et al. (?), Bardet and Tudor (?), Clausel et al. (?), Pipiras and Taqqu (?), to name a few).

In modern applications, however, data sets are often multivariate, since several natural and artificial systems are monitored by a large number of sensors. Accordingly, the literature on multivariate fractional processes has been expanding at a fast pace. The contributions include Hosoya (?, ?), Lobato (?), Marinucci and Robinson (?), Shimotsu (?), Becker-Kern and Pap (?), Robinson (?), Hualde and Robinson (?), Nielsen (?), Sela and Hurvich (?) and Kechagias and Pipiras (?, ?), in the time and Fourier domains, and Wendt et al. (?), Amblard and Coeurjolly (?), Amblard et al. (?), Coeurjolly et al. (?), Achard and Gannaz (?), Frecon et al. (?), Abry and Didier (?), in the wavelet domain (see also Marinucci and Robinson (?), Robinson and Yajima (?), Nielsen and Frederiksen (?), Shimotsu (?) on the related fractional cointegration literature in econometrics).

In this paper, we propose a new semiparametric statistical method for a subclass of multivariate fractional processes, i.e., those of the form

| (1.2) |

where is a nonsingular matrix and

| (1.3) |

is a vector of independent Gaussian fractional processes. The process is assumed observable. On the other hand, can be interpreted either as a hidden process whose components get scrambled by a mixing matrix parameter , or as one occuring in a different system of coordinates (see Remark 2.4 on nonsquare matrices ). One key statistical challenge is to retrieve the fractional information (e.g., on Hurst exponents or memory parameters) contained in . If, for example, is a vector of (independent) fBm entries

| (1.4) |

where , , denote the individual Hurst exponents, then the univariate-like statistical analysis of each entry of will often generate estimates that are undetermined convex combinations of Hurst exponents or, at large scales, estimates of the largest Hurst exponent (c.f. Abry and Didier (?), Introduction).

It has been shown (Tsai et al. (?)) that processes of the form (1.2) naturally arise as approximations to solutions of physically relevant classes of multivariate fractional SDEs under aggregation (this is recapped in Section 2.1). In addition, it is well known that many real data sets – e.g., tree ring widths, economic output, river flows, or rainfall – are obtained through aggregation over a certain time interval, which points to the usefulness of the model (1.2). Multivariate fractional processes of the form (1.2) are also closely related to the so-named operator self-similar (o.s.s.) random processes and fields (Laha and Rohatgi (?), Hudson and Mason (?)), a topic that has attracted much attention recently (e.g., Maejima and Mason (?), Mason and Xiao (?), Biermé et al. (?), Xiao (?), Guo et al. (?), Didier and Pipiras (?, ?), Clausel and Vedel (?, ?), Li and Xiao (?), Dogan et al. (?), Puplinskaitė and Surgailis (?), Didier et al. (?, ?)). In the context of o.s.s. and related processes, the estimation of the matrix is itself of great interest, since it makes up the system of coordinates of the Hurst matrix (see Example 2.1).

The class (1.2) further provides an extension to the framework of fractional processes of the so-named mixed processes from the blind source separation literature in signal processing, the latter being well-established in traditional settings such as that of ARMA-like signals (e.g., Belouchrani et al. (?), Cardoso (?), Pham and Cardoso (?), Moreau (?), Yeredor (?), Parra and Sajda (?), Stone (?), Ziehe et al. (?), Choi et al. (?), O’Grady et al. (?), Fevotte and Godsill (?), Li et al. (?), Common and Jutten (?)).

In the preliminary study Didier et al. (?), presented without proofs, the hidden process is given by (1.4) and a demixing estimator is proposed for that draws upon the diagonalization of sample covariance matrices. In this paper, we consider the broad framework where each (independent) entry of in (1.3) is a continuous time fractional process with stationary increments of some order, possibly zero (i.e., is stationary). In addition, it is not assumed that, entrywise, is exactly self-similar as in (1.1) (see (2.9), (2.10) and (2.13) and the discussion in Example 2.1). We construct a semiparametric two-step wavelet-based method for the estimation of the demixing matrix and the individual memory parameters that can be summed up as follows.

-

demixing step (change of coordinates): generate an estimator by jointly diagonalizing two wavelet variance matrices (i.e., at two different octaves ; see (3.3)) of the mixed process ;

-

memory parameter estimation step: estimate by applying univariate wavelet regression to each entry of the demixed process (Veitch and Abry (?), Bardet (?), Moulines et al. (?, ?, ?)).

The use of a wavelet framework has the benefit of computational efficiency (Daubechies (?), Mallat (?)), while being a natural choice for stochastic systems with stationary increments of arbitrary order. In fact, for a large enough number of vanishing moments (see (2.17)), wavelet coefficients are stationary in the shift parameter at every octave (see (2.17), (3.1) and Remark 2.6). In addition, basing step on wavelet variance matrices of ensures that the demixing estimator is consistent and asymptotically normal (Theorem 3.2). The latter property does not generally hold for estimators based on sample covariance matrices; indeed, it is in part a consequence of the quasi-decorrelation property of the wavelet transform (Flandrin (?), Wornell and Oppenheim (?), Masry (?), Bardet and Tudor (?), Clausel et al. (?)). The estimator of the vector of Hurst parameters generated at step is also consistent and jointly asymptotically normal (Theorem 3.3). With a view toward hypothesis testing, the consistency and asymptotic normality of the estimators generated at both steps and are shown to hold under mild assumptions even in the presence of equal Hurst parameters (Corollary 3.1). Moreover, under the more realistic assumption that in (1.2) is observed in discrete time, the asymptotic properties of the proposed estimators do not qualitatively change (Theorems 4.2, 4.3 and Corollary 4.1).

We conducted broad Monte Carlo experiments for instances where is made up of independent fractional Brownian motion components. In dimension 4, the results show that the performance of the proposed two-step estimation method is similar to that for univariate estimators of Hurst parameters over finite samples. Moreover, notwithstanding its semiparametric and hence more general nature, the method’s performance is comparable to that of fully parametric Whittle-type maximum likelihood estimation in terms of mean squared error, while bearing the advantage of being computationally very fast. In addition, an application of the two-step method to a bivariate data set from bristlecone pine tree rings from California shows that the latter can be reasonably modeled by means of the mixed form (1.2).

It should be noted that the two-step nature of the estimation method makes it rather flexible. Although step , as proposed, involves applying entrywise a univariate wavelet estimator, in principle the wavelet-based demixing technique in step can be combined with any other univariate method such as Whittle, local Whittle or spectral log-regression estimation (see, for instance, Bardet et al. (?)).

This paper is organized as follows. In Section 2, we lay out the notation, assumptions and theoretical background of the paper. Section 3 contains the main mathematical results of the paper, including the properties of wavelet analysis, assuming measurements in continuous time. In particular, in Sections 3.2 and 3.3, we construct steps () and () of the two-step estimation method, respectively. In Section 4, we extend the two-step estimation method to the context of discrete time measurements. Section 5 contains all Monte Carlo studies. In Section 6, we provide two applications. We analyze and model the aforementioned tree ring data set, and establish the asymptotic normality of the eigenstructure of the sample wavelet variance matrix at fixed scales, which is of independent interest. All proofs can be found in the Appendix, together with auxiliary results.

2 Preliminaries

The dimension of the mixed process is denoted by throughout the paper.

We shall use the following matrix notation. is the vector space of all real-valued matrices, whereas is a shorthand for . is the general linear group (invertible matrices), is the orthogonal group of matrices such that , where ∗ represents the matrix adjoint and T is reserved for vector transpose. , and are, respectively, the space of symmetric, the cone of symmetric positive semidefinite and the cone of symmetric positive definite matrices. The symbol represents a vector or matrix of zeroes. A block-diagonal matrix with main diagonal blocks or times repeated diagonal block is represented by

| (2.1) |

respectively. The symbol represents a generic matrix or vector norm. The entrywise norm of the matrix is denoted by

| (2.2) |

The Fourier transform of any function is defined by

For , let

| (2.3) |

In other words, the operator vectorizes the lower triangular entries of , vectorizes the diagonal entries of , and vectorizes all the entries of . Note that the expressions in (2.3) are defined as row vectors; this will make the notation simpler in several statements. When establishing bounds, denotes a positive constant whose value can change from one inequality to the next.

2.1 Aggregation and mixed processes

Recent work (Chan and Tsai (?), Tsai et al. (?)) has established the connection between aggregation and the emergence of mixed processes. We sketch the basic idea for the reader’s convenience. A natural multivariate extension of Langevin-type dynamics is given by the SDE

| (2.4) |

where is a vector of independent fBm entries with Hurst parameters

| (2.5) |

The solution of (2.4) can be written a.s. as

| (2.6) |

which generalizes the univariate fractional Ornstein-Uhlenbeck process (Cheridito et al. (?), Prakasa Rao (?)). Consider the case where the continuous time process defined by (2.6) is digitalized by aggregation over interval , i.e.,

Then, as ,

| (2.7) |

where denotes convergence of the finite dimensional distributions. Therefore, for large , the aggregate process can be approximated by the mixed process

| (2.8) |

Recall that fractional Gaussian noise (fGn) is the increment process of fBm. In (2.8), is a vector of independent fGn entries with Hurst parameters (2.5) and . Note that the process (2.8) is a particular case of (1.2), with the latter restricted to discrete time.

2.2 Assumptions

Unless otherwise stated, we will make the following assumptions on throughout the paper. Assumptions (1), (2) and (3) describe, respectively, the covariance structure of the hidden process , the conditions on the mixing matrix and the regularity properties of high frequency components.

Assumption (1): the observed process has the mixed form (1.2), where , , in (1.3) is either a -th () order (covariance) stationary process with harmonizable representation

| (2.9) |

or a (covariance) stationary process (i.e., ) with harmonizable representation

| (2.10) |

By convention, the so-named memory parameters are ordered as

| (2.11) |

In (2.9) and (2.10), is a Gaussian random measure satisfying and .

Assumption (2):

| (2.12) |

Assumption (3): the -valued functions in (2.9) and (2.10) are bounded and satisfy

| (2.13) |

for any for some small . In (2.13), and satisfies

| (2.14) |

for some

| (2.15) |

Example 2.1

If the high frequency functions are constant and , , then the observed process satisfies the so-named operator self-similarity property. In other words, , , where is the Hurst matrix with Hurst eigenvalues

| (2.16) |

and is defined by the matrix exponential

If, in addition, , , then is an operator fractional Brownian motion, namely, a Gaussian, operator self-similar, stationary increment process (Mason and Xiao (?), Didier and Pipiras (?, ?)).

Example 2.2

The framework provided by assumptions (1–3) is quite general. For example, one arbitrary entry , , of the hidden process can be a fBm, a fGn, or a fractional Ornstein-Uhlenbeck process. These processes are associated, respectively, with the high frequency function instances (), (), and () for some . The instance and corresponds, in discrete time, to FARIMA() (e.g., Taqqu (?)).

Remark 2.1

Remark 2.2

Remark 2.3

In (2.11), one incurs no loss of generality by assuming that the memory parameters are disposed in ascending order. This fact can be easily illustrated in dimension . Suppose that the mixed process has the form , where , , are independent fractional processes defined in (2.9) or (2.10) with parameters . Let

Then, , whence can be treated as the mixing matrix with unit vector columns.

Remark 2.4

Mathematically speaking, it is natural to ask how useful it is to consider the model (1.2) with a full rank matrix , where . However, both cases and fall outside the scope of this paper. When , the observed process is improper, namely, its finite dimensional distributions are contained in a proper subspace of for some (even if, in addition, the high frequency functions , , are constant, cannot be operator self-similar: see Example 2.1 or Hudson and Mason (?)). When , the spectral densities involved are potentially much more complicated, with added power laws. Either situation calls for the construction of particular methods.

Remark 2.5

Assumption (3) is typical in a semiparametric estimation setting (e.g., Robinson (?) and Moulines et al. (?, ?)). Note that larger values of correspond to greater smoothness of the functions , , around the origin.

In Section 3, we will implicitly make the following assumptions on the underlying wavelet basis, hence they will be omitted from statements.

Assumption : is a wavelet function, namely,

| (2.17) |

for some number of vanishing moments, where is as in (2.9) or (2.10).

Under (2.17), (2.18) and (2.19), is continuous, is everywhere differentiable and its first derivatives are zero at (see Mallat (?), Theorem 6.1 and the proof of Theorem 7.4). The condition () is equivalent to asserting that the first derivatives of vanish at the origin. This implies, using a Taylor expansion, that

| (2.20) |

Example 2.3

If is a Daubechies wavelet with vanishing moments, (see Mallat (?), Proposition 7.4).

Remark 2.6

Assumption requires using a number of vanishing moments larger than the unknown integration order . In practice, though, the latter parameter is rarely greater than 2, so the requirement is easily met even for low values of .

3 Wavelet-based estimation: continuous time

In Section 3.1, we establish basic as well as the asymptotic properties of the wavelet transform of the process at fixed scales. Sections 3.2 and 3.3 contain the main mathematical results of the paper. In the former and in the latter, respectively, the demixing step and the post-demixing Hurst parameter estimation step are laid out in full detail, and their asymptotic properties are shown. Note that only involves wavelet analysis at fixed scales, while generally requires taking a coarse scale limit , due to the lack of exact self-similarity in (2.9) and (2.10). Recall that, throughout this section, we are implicitly assuming that conditions (–3) hold.

3.1 Wavelet analysis at fixed scales: properties and asymptotic theory

For a wavelet function with a number of vanishing moments, the vector wavelet transform of is naturally defined as

| (3.1) |

provided the integral in (3.1) exists in an appropriate sense. It will be convenient to make the change of variable , and reexpress

The wavelet domain process is stationary in (Proposition 3.1). The wavelet spectrum (variance) at scale is the positive definite matrix

| (3.2) |

and its natural estimator, the sample wavelet variance, is the random matrix

| (3.3) |

for a total of

| (3.4) |

The next proposition describes some properties of the wavelet coefficients (3.1) as well as the general form of the wavelet spectrum (3.2).

Proposition 3.1

The following theorem establishes the asymptotic distribution of the vectorized sample wavelet spectrum at a fixed set of octaves.

3.2 Wavelet-based demixing (step )

The joint diagonalization of two matrices is a well-known problem. For the case of symmetric matrices, its description and full characterization can be stated as follows (see Theorem 4.5.17, (b), in Horn and Johnson (?)). Suppose and are symmetric and is nonsingular. Then, there are a nonsingular and complex diagonal matrices and such that

| (3.11) |

if and only if the matrix is diagonalizable (in its Jordan form). In light of this, we can cast a joint diagonalization algorithm in the form of pseudocode.

| Pseudocode for exact joint diagonalization (EJD) |

| Input: , are symmetric matrices and the former is positive definite; |

| Step 1: set so that ; |

| Step 2: compute in the spectral decomposition ; |

| Step 3: compute the demixing matrix ; |

| Step 4: stop and exit. |

Example 3.1

Remark 3.1

Steps 1–4 of the EJD algorithm should not be confused with steps and of the proposed wavelet-based estimation method).

The proposed wavelet-based estimator of a demixing matrix is defined next.

Definition 3.1

( demixing step, continuous time) Consider two octaves for which

| (3.12) |

For , the wavelet-based demixing estimator is the output of the EJD algorithm when setting

| (3.13) |

In Theorem 3.2, stated next, we establish the consistency and asymptotic normality of the estimator put forward in Definition 3.1. The result involves characterizing the set of solutions provided by the EJD algorithm. In view of (3.8), this relies on reexpressing

| (3.14) |

where

| (3.15) |

and then making use of the matrix polar decomposition of . Then, consistency and asymptotic normality stem from obtaining the behavior of the sample counterparts and vis-à-vis (3.14) by means of Proposition LABEL:p:4th_moments_wavecoef and Theorem LABEL:t:eigen, plus the Delta method when developing limits in distribution.

Theorem 3.2

For , let be as in (3.9). Also let

| (3.16) |

-

()

Then,

(3.17) is the set of matrix solutions produced by the EJD algorithm when setting

(3.18) -

()

in addition, assume condition (3.12) holds. For some estimator sequence and some matrix ,

(3.19) -

()

an estimator sequence as described in () satisfies

(3.20) for some matrix , where the covariance matrix is a function of , and is defined in Theorem 3.1, with .

Remark 3.2

Remark 3.3

Remark 3.4

By (3.19), any sequence has a limit in probability of the form , , , i.e., involving a non-identifiability factor post-multiplying the mixing matrix . However, note that , i.e., the columns of consist of (non-unit) eigenvectors of the memory matrix . Consequently, is a natural estimator of the latter, where are univariate (e.g., wavelet-based) estimators of the individual Hurst exponents obtained from the demixed process.

Remark 3.5

More precisely, the covariance matrix in the limit (3.20) can be written as , where and are given by expressions (LABEL:e:Sigma_2) and (LABEL:e:A3), respectively. It is clear that the expression for is quite intricate, and the construction of theoretical confidence intervals is a matter for future investigation (cf. Wendt et al. (?)).

3.3 Wavelet-based estimation of memory parameters after demixing/changing the coordinates (step )

Throughout this section, a scaling factor is assumed to be a dyadic sequence such that

| (3.21) |

where satisfies (2.14) (see Remark 3.7 below on the choice of in practice).

We start off with the output of step of the proposed two-step method (Section 3.2). Let be the demixing matrix described in (3.19). Then, the demixed process is defined by

| (3.22) |

of which only (wavelet) data points are available (c.f. (3.4)). For , let

| (3.23) |

be the sample wavelet variance of and the wavelet variance of the hidden process , respectively. Proposition LABEL:p:xhattox in the Appendix establishes the asymptotic normality of when centered at . So, we are now in a position to define an estimator for the vector of memory parameters of the hidden process .

Definition 3.2

( Memory parameter estimation step, continuous time) Let

| (3.24) |

be the -th entries of the matrices and , respectively. Consider the regression weight vectors

| (3.25) |

where

| (3.26) |

The wavelet-based estimator of the memory parameters in (2.11) is obtained by regressing the main diagonal terms on the scale indices , , i.e.,

| (3.27) |

The asymptotic distribution of the estimator is provided in the following theorem.

Theorem 3.3

Remark 3.6

Theorem 3.3 shows that the individual memory estimators are asymptotically independent. In fact, the joint asymptotic distribution of , estimated from the demixed process , is equal to that of the joint entrywise wavelet-based estimators of obtained from the hidden process (see Remark LABEL:r:demix=orignal). In other words, asymptotically, the demixing step () washes out the effect of the mixing matrix on the estimation procedure.

Remark 3.7

In practice, the choice of involves a statistical compromise. A large value of with respect to implies a relatively small bias, but also a relatively large variance. Simulation results suggest the ratio should be no less than .

Remark 3.8

Removing the condition (2.11) can alter the limits (3.28). For example, suppose there are two blocks of equal memory parameters

and the high frequency functions are identically constant for . Then, in Step 2 of the EJD algorithm, . Thus, the eigenvectors of do not have a limit in probability. In this case, the demixed process takes the form (see expression (LABEL:e:matrix_D) for the definition of the matrix ), where the random matrix satisfies

and and do not have a limit in probability. Therefore, we can write

where

and is the -th diagonal entry of , . Thus, each entry of the processes and has memory parameter and , respectively. Even though we cannot retrieve the mixing matrix, we can still estimate the memory parameters and obtain an asymptotically normal distribution. However, corresponding to each block of parameters, the estimators among each set and are asymptotically dependent (though independent across sets).

3.4 On the case of blocks of equal memory parameters

With a view toward hypothesis testing, we also consider the case where some, or all, memory parameters are equal. In light of Remark 3.8, we will need make some change to our assumptions. However, to attain consistency and asymptotic normality in steps and , it suffices to add minor constraints on the high frequency functions , , and hence replace (1) and (3) with the following assumptions.

Assumption (): the observed process has the mixed form (1.2), where each component , , of the hidden process in (1.3) has the form (2.9) or (2.10), and the memory parameters can be ordered as

Assumption (): In addition to satisfying (3), the high frequency functions , , are such that the matrix has pairwise distinct diagonal entries.

4 Wavelet-based estimation: discrete time

In practice, only observations in discrete time are available, which renders the computation of the theoretical wavelet coefficients impossible. In this section, we study the asymptotic performance of the two-step wavelet-based methodology under the assumption that only wavelet data points from a discrete time sample

| (4.1) |

of (1.2) are available (c.f. (3.4)). In Section 4.1, we lay out the notation and assumptions. In Section 4.2, we develop the asymptotic distribution of the two-step wavelet-based method estimators.

4.1 Notation and assumptions

Throughout this section, we suppose the wavelet approximation coefficients stem from Mallat’s pyramidal algorithm, under a multiresolution analysis of (MRA; see Mallat (?), chapter 7). Accordingly, we need to replace () with the following more restrictive condition.

Assumption (): the scaling and wavelet functions and , respectively, are compactly supported, integrable and

We also add the following condition.

Assumption (): the function

is a polynomial of degree for all .

Remark 4.1

The Daubechies scaling and wavelet functions satisfy (), () and (-4) (Moulines et al. (?), page 1927).

Throughout this section, we assume that the conditions (), () and () hold. In particular, conditions () and () imply that

| (4.2) |

4.2 Asymptotic theory for the two-step wavelet-based method (steps and )

Given (4.1), we initialize the algorithm with the vector-valued sequence

also called the approximation coefficients at scale . At coarser scales , Mallat’s algorithm is characterized by the iterative procedure

where the filter sequences , are called low- and high-pass MRA filters, respectively. Due to (), only a finite number of filter terms is non-zero, which is convenient for computational purposes (Daubechies (?)). The normalized wavelet coefficients are defined by

| (4.3) |

Let

| (4.4) |

be the wavelet variance matrix and its sample counterpart, respectively, where is as in (3.3). The following theorem is the discrete time analogue of Theorem 3.1 and establishes the asymptotic distribution of the wavelet variance matrices at fixed octaves.

Theorem 4.1

Note that can be recast as

| (4.6) |

where

| (4.7) |

(see Proposition LABEL:p:covdis in the Appendix). As in continuous time, expression (4.6) indicates that an estimator of can be generated by jointly diagonalizing and , for .

Definition 4.1

( demixing step, discrete time) Consider two octaves for which

| (4.8) |

For , the wavelet-based demixing estimator is the output of the EJD algorithm when setting

| (4.9) |

As a consequence of Theorem 4.1 and by following the same argument as in the proof of Theorem 3.2, we obtain the limiting distribution of .

Theorem 4.2

Remark 4.2

Let

| (4.11) |

be the demixed process, of which (wavelet) data points are available (see (4.1)). As with its continuous time counterpart (see (3.23)), the sample wavelet variance is asymptotically normal when centered at the matrix (see Proposition LABEL:p:xhattox_dis in the Appendix, and also expression (LABEL:e:Dtilde) for the definition of ). We are now in a position to define the estimators of the memory parameters .

Definition 4.2

In the following theorem, the asymptotic normality of the estimator is established.

Theorem 4.3

The next result is the discrete time analogue of Corollary 3.1, i.e., for the case where some, or all, memory parameters are equal. Note that the assumptions on the process do not change from continuous to discrete time.

Corollary 4.1

Remark 4.3

All results in continuous time hold if we allow the components to be stationary with memory parameter . In discrete time, all results hold if we assume that , since in this case the second and the third terms, respectively, in expressions (LABEL:eq:fstar) and (LABEL:e:triplesummation) are identically zero.

5 Monte Carlo studies

5.1 Performance over finite samples

We studied the performance of the two-step wavelet-based method over finite samples assuming the hidden process is made up of 4 independent fractional Brownian motion components observed in discrete time. For notational simplicity, denote , (see Example 2.1). Recall that, in this case, the relation (2.16) holds between the memory parameters and the individual Hurst exponents. We simulated sample paths of with sizes ranging from to (results are reported for the smallest and largest sample size only) with individual Hurst parameters and mixing matrix

| (5.1) |

(see also Remark 5.2 on the choice of ). The entrywise Hurst exponents are denoted by , , , whereas , , denotes the Hurst exponents of the demixed sequence for normalized demixing matrix estimates .

The results consist of comparisons of the Monte Carlo log-averages of the sample wavelet variance , and ( denotes for Monte Carlo average) for each of the components for the sample sizes and (Figures 1 and 4); boxplots for , and , (Figures 2 and 5); and boxplots for the entries of (Figures 3 and 6). Following the procedure described in Remark 3.4, the columns of were adjusted as to eliminate the non-identifiability factor. In all cases, the sample wavelet variance matrices were computed based on Daubechies wavelet filters with vanishing moments. Using a different wavelet with yields similar conclusions.

In Figures 1 and 4, as expected for the mixed data all components of display patent departures from the original data . After demixing, all components of remarkably superimpose those of , with the possible exception of a few coarse scales for and 0.4. In addition, the boxplots in Figures 2 and 5 show that the Monte Carlo distributions for resemble those of , which illustrates the successful demixing of . Figures 3 and 6 further indicate that is very well estimated with negligible biases. In all comparisons, as expected the observed estimator properties improve significantly when passing from the relatively small sample size to the large sample size , hence reflecting the asymptotic statement of Theorem 3.2, (). In addition, simulation results not displayed also show that the standard deviation of the estimates decreases with the sample size according to the scaling ratio for some , as anticipated.

Remark 5.1

Theorem 4.2 leaves open the question of how to optimally choose the octaves . For multiple choices of wavelet octaves, namely, (which involves the largest number of sum terms in (3.3)) and , Table 1 shows the performance of the individual Hurst exponents’ estimators in terms of Monte Carlo bias, standard deviation and (square root) mean squared error. For sample sizes and , the results indicate that for low values of the Hurst exponents, the use of two widely separated wavelet octaves produces better results in terms of mean squared error, whereas for large values of the Hurst exponents the choice of octaves has little impact on the estimation.

| bias | sd | bias | sd | ||||||

|---|---|---|---|---|---|---|---|---|---|

| () | () | ||||||||

| 0.20 | 1,2 | 0.25 | 0.05 | 0.04 | 0.06 | 0.31 | 0.11 | 0.10 | 0.14 |

| 1,3 | 0.22 | 0.02 | 0.03 | 0.04 | 0.25 | 0.05 | 0.08 | 0.10 | |

| 1,4 | 0.22 | 0.02 | 0.03 | 0.03 | 0.24 | 0.04 | 0.08 | 0.09 | |

| 1,5 | 0.21 | 0.01 | 0.02 | 0.03 | 0.23 | 0.03 | 0.08 | 0.09 | |

| 1,6 | 0.21 | 0.01 | 0.02 | 0.03 | 0.22 | 0.02 | 0.08 | 0.08 | |

| 0.40 | 1,2 | 0.40 | -0.00 | 0.02 | 0.02 | 0.45 | 0.05 | 0.08 | 0.10 |

| 1,3 | 0.40 | -0.00 | 0.01 | 0.02 | 0.41 | 0.01 | 0.07 | 0.07 | |

| 1,4 | 0.39 | -0.01 | 0.01 | 0.02 | 0.40 | 0.00 | 0.07 | 0.07 | |

| 1,5 | 0.40 | -0.00 | 0.01 | 0.01 | 0.40 | 0.00 | 0.07 | 0.07 | |

| 1,6 | 0.39 | -0.01 | 0.01 | 0.01 | 0.40 | -0.00 | 0.07 | 0.07 | |

| 0.60 | 1,2 | 0.59 | -0.01 | 0.01 | 0.02 | 0.60 | -0.00 | 0.07 | 0.07 |

| 1,3 | 0.59 | -0.01 | 0.01 | 0.02 | 0.58 | -0.02 | 0.07 | 0.07 | |

| 1,4 | 0.59 | -0.01 | 0.01 | 0.02 | 0.58 | -0.02 | 0.07 | 0.07 | |

| 1,5 | 0.59 | -0.01 | 0.01 | 0.02 | 0.58 | -0.02 | 0.07 | 0.07 | |

| 1,6 | 0.59 | -0.01 | 0.01 | 0.02 | 0.58 | -0.02 | 0.07 | 0.07 | |

| 0.80 | 1,2 | 0.79 | -0.01 | 0.01 | 0.02 | 0.76 | -0.04 | 0.07 | 0.08 |

| 1,3 | 0.79 | -0.01 | 0.01 | 0.02 | 0.77 | -0.03 | 0.07 | 0.07 | |

| 1,4 | 0.79 | -0.01 | 0.01 | 0.02 | 0.77 | -0.03 | 0.07 | 0.07 | |

| 1,5 | 0.79 | -0.01 | 0.01 | 0.02 | 0.77 | -0.03 | 0.07 | 0.07 | |

| 1,6 | 0.79 | -0.01 | 0.01 | 0.02 | 0.77 | -0.03 | 0.07 | 0.07 |

Remark 5.2

Simulation studies not included show that the choice of the mixing matrix (5.1) does not substantially affect the finite sample results. Moreover, the demixing estimator is very robust with respect to the condition number of the mixing matrix . The distributions of the estimated scalar Hurst eigenvalues after demixing are barely affected for condition numbers of the order of at least .

5.2 Two-step wavelet-based and maximum likelihood estimation: a comparative study

Due to its wide applicability and well-known asymptotic properties, maximum likelihood estimation is a natural choice and the associated methodology in a multivariate framework has been constructed by several authors (see references in the Introduction). In this section, we conduct Monte Carlo experiments to compare the statistical and computational finite sample performances of two-step wavelet-based and maximum likelihood (ML) estimation. For the sake of illustration, we opt for Whittle-type estimation for fitting a mixed bivariate operator fractional Gaussian noise. This involves reexpressing the likelihood function in the Fourier domain and using some approximations. For the reader’s convenience, we provide a brief description of the method; for more details see, for instance, Hosoya (?, ?), Robinson (?) and Tsai et al. (?).

In (1.2), suppose is a vector of two independent fractional Gaussian noise entries with Hurst parameters , . Then, the (negative) Whittle log-likelihood function of can be approximated by

| (5.2) |

where , , , for some large integer , , , , and are the Fourier frequencies. The (Whittle) ML estimator is defined by

| (5.3) |

In (5.3), is given by (5.2), and we write . The estimator (5.3) was implemented in Matlab using the function fminsearch.m to minimize with respect to the unknown parameters , and .

For the simulation study, we picked the parameter values

| (5.4) |

Monte Carlo averages for the two-step wavelet-based and ML estimators for the parameters , and are reported in Table 2.

| method | parameter | bias | sd | |

|---|---|---|---|---|

| ML | 0.1479 | 0.1705 | 0.2257 | |

| -0.0358 | 0.0761 | 0.0841 | ||

| -1.1076 | 1.2362 | 1.6598 | ||

| 4.5516 | 1.2604 | 4.7229 | ||

| 4.6128 | 1.2244 | 4.7725 | ||

| -1.1042 | 1.1772 | 1.6140 | ||

| two-step wavelet method | 0.0522 | 0.0954 | 0.1088 | |

| -0.1125 | 0.0919 | 0.1452 | ||

| -0.0207 | 0.2592 | 0.2600 | ||

| 0.0182 | 0.3841 | 0.3845 | ||

| 0.0196 | 0.2462 | 0.2469 | ||

| -0.0170 | 0.3686 | 0.3690 |

The simulation study shows that the semiparametric two-step wavelet-based and the parametric Whittle-type ML methods display comparable finite sample performances as measured by Monte Carlo bias, standard deviation and . In fact, the former method estimates and slightly more accurately, whereas the latter does better with . However, the two-step wavelet-based method is far more computationally efficient. In fact, the ML estimator requires minimizing (5.2) with respect to unknown parameters, which can be numerically very difficult in higher dimension . As shown in Table 3, the computational time per realization of ML grows rapidly as a function of the path size , and the ratio between computational times for the two methods grows exponentially fast. Furthermore, our computational studies indicate that the minimization procedure required by ML is somewhat sensitive to the initial guess.

In all fairness, the computational performance of ML can be surely improved by replacing the all-purpose fminsearch.m with a special optimization algorithm. Nevertheless, this computational study illustrates the fact that the potential numerical hurdles in the construction of viable maximum likelihood estimation for mixed fractional processes are significantly more stringent than those for the proposed two-step wavelet-based method. In addition, the computational robustness of the latter with respect to the sample path size is striking.

| time in seconds (per realization) | time ratio | ||

|---|---|---|---|

| sample path size | ML | two-step wavelet | (ML/two-step wavelet) |

| 2.5 | 0.0035 | 720 | |

| 22.0 | 0.0050 | 4400 | |

| 216.0 | 0.0100 | 21600 | |

| 2495.0 | 0.0120 | 213870 | |

6 Applications

We now provide two applications of the method constructed above.

In Section 6.1, we illustrate the two-step wavelet-based method by fitting a bivariate series of annual tree ring measurements from bristlecone pine trees in California. The data can be found in the Time Series Data Library, which is available on the website DataMarket (https://datamarket.com/data/list/?q=provider:tsdl). The so-named White Mountain and Methuselah pine tree data sets are provided by C. W. Ferguson, E. Schulman and H. C. Fritts, and by D. A. Graybill, respectively. In Section 6.2, we draw upon the results in Section 3.1 to establish the asymptotic normality of the eigenstructure of the sample wavelet variance matrix at fixed scales. This is of independent interest because sample wavelet variance matrices do not generally follow a Wishart distribution. This results from the presence of residual correlation after the application of the wavelet transform.

6.1 Modeling tree ring data

Many tree ring data sets exhibit long range dependence properties (Tsai and Chan (?)). Annual tree ring width measurements can be modeled as aggregates of the underlying continuous time growth rate process over time intervals between two consecutive sampling time points. Assuming reasonable physical models, the latter, in turn, can be approximated by a mixed fractional process, as explained in Section 2.1. Although the full data set covers the period 5142 BC – 1962 AD, we focus instead on the subperiod 4141 BC – 1962 AD, since preliminary wavelet-based analysis revealed stationarity in the latter. The time series are displayed in Figure 7, top plots.

Data analysis is conducted both in the time and wavelet domains. We examine the data by means of sample autocorrelation and cross-correlation functions (ACFs and CCFs, respectively), main diagonal wavelet scaling plots and (see (4.4)) as functions of , as well as the so-named sample wavelet coherence function , . The latter is a wavelet version of the CCF and can also be used to check the cross-correlation in bivariate data. For each , the associated term is defined by

(see Whitcher et al. (?)).

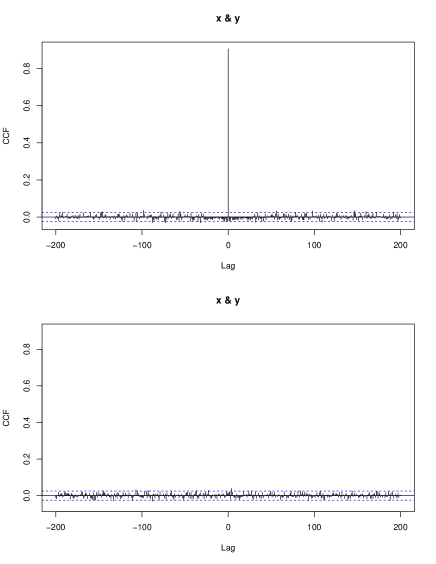

Because it is well known that spurious cross-correlation may occur as a result of the presence of fractional memory in each time series, it is pivotal to pre-whiten the data (e.g., Cryer and Chan (?), Section 11.3). The corresponding sample ACFs, shown on the lower panel in Figure 7, suggest that the time series have long memory. This is confirmed by wavelet analysis, as displayed in Figure 9 (left plot). Indeed, both and suggest scaling behavior with Hurst parameters that clearly depart from , i.e., long memory. Moreover, the fact that both curves resemble each other (namely, close Hurst parameter values) can be explained as the preponderance of one of the two underlying scaling laws (see the discussion in the Introduction). The upper panel in Figure 8 displays the sample cross-correlation (for pre-whitened data). It reveals that the sequences are contemporaneously strongly correlated but not cross-correlated at any nonzero lag values. This is confirmed by the wavelet coherence function (Figure 9, right plot), which shows significant and nearly constant correlation across all scales.

The demixing step of the proposed wavelet-based method yields the following estimated demixing matrix

Demixed ring tree time series are computed by applying to the original data. Inspection of the sample cross-correlation function for the demixed tree ring data (after pre-whitening) reveals that the proposed wavelet-based method successfully decorrelated the data (lower panel in Figure 8). This is further confirmed by the wavelet coherence function (Figure 9, right plot), which evidences near zero correlations at all scales but a few of the coarsest. In addition, both functions and (for demixed data) still display scaling behavior. However, the Hurst exponents seem quite distinct and bounded away from . This is confirmed by the proposed estimation method. After demixing, the memory parameter estimation step yields the parameter estimates , (using scales ()=(3,7)), and , (using scales ()=(3,9)) (recall that, in this case, the relation between the Hurst and memory parameters and , respectively, is given by (2.16)). In other words, there is little sensitivity of the parameter estimates to the choice of octave range. Table 4 further reports a Monte Carlo study of the sample mean and sample standard deviation of for the case . The difference between the estimated Hurst parameters for the demixed tree ring data is , which lies far outside the confidence interval. In other words, there is evidence for the hypothesis in the demixed ring tree data. Note that this could not have been detected had we skipped step (), i.e., if Hurst exponent estimation had been conducted directly on the original data.

| true | parameter | mean | sd |

|---|---|---|---|

| =0.7 | 0.6985 | 0.0183 | |

| 0.7229 | 0.0176 | ||

| 0.0244 | 0.0185 | ||

| =0.8 | 0.7957 | 0.0191 | |

| 0.8229 | 0.0195 | ||

| 0.0272 | 0.0202 |

6.2 Asymptotic theory for the eigenstructure of sample wavelet variance matrices

In order to state Theorem 6.1 below, consider the matrix spectral decompositions

| (6.1) |

where , , , have columns , , respectively, for , and

| (6.2) |

In other words, the eigenvalues appearing on the main diagonal entries of and are ordered from smallest to largest, and the entries on the first row of and are all nonnegative, which makes these orthogonal matrices identifiable. Following Magnus and Neudecker (?), p. 427, we recall the definition of the so-named duplication matrix . It consists of the (unique) operator D that performs the transformation

| (6.3) |

where . Moreover, for with ordered eigenvalues and their respective normalized eigenvectors , we further define the operator

| (6.4) |

where we can apply the relation

| (6.5) |

(see Lemma 3.7, (), in Magnus and Neudecker (?)). The proof of Theorem 6.1 relies on Proposition LABEL:p:4th_moments_wavecoef, Theorem LABEL:t:eigen (on the weak convergence of eigenvalues and eigenvectors) and the Delta method.

Theorem 6.1

Remark 6.1

Note that the conclusion in Theorem 6.1 also holds when replacing by .

Appendix A Asymptotic theory for the wavelet variance of univariate Gaussian fractional processes

In this section, we establish the asymptotic normality of the wavelet variance of univariate Gaussian fractional processes (n.b.: the framework of Moulines et al. (?, ?, ?) is for discrete time processes). Throughout the section, we assume the underlying wavelet function satisfies the conditions (–3), the underlying process has the form (2.9) or (2.10), and satisfies assumption (3). The main result, Theorem LABEL:t:varianceuni, is used in the proof of Proposition LABEL:p:xhattox.

The wavelet transform of the univariate process is defined by

The wavelet variance at octave and its natural estimator, the sample wavelet variance, are denoted by, respectively,

| (A.1) |

and

| (A.2) |

Let be the total number of available (wavelet) data points. Throughout this section, we take a sequence of scaling factor satisfying (3.21).

The following lemma will be used in the subsequent proposition.

Lemma A.1

For any two fixed octaves ,

| (A.3) |

where