Kernel estimation of the intensity of Cox processes

Nicolas Klutchnikoff

IRMAR, Université de Rennes 2, CNRS, UEB

Campus Villejean (Rennes)

Place du recteur Henri Le Moal

CS 24307

35043 Rennes cedex

nicolas.klutchnikoff.univ-rennes2.fr

Gaspar Massiot

IRMAR, ENS Rennes, CNRS, UEB

Campus de Ker Lann

Avenue Robert Schuman, 35170 Bruz, France

gaspar.massiot@univ-rennes1.fr

1 Introduction

Counting processes and in particular Cox processes have been used for many years to model a large variety of situations from neuroscience [see 2, 7, 10] to seismic [see 12], financial [see 11], insurance [see 1] or biophysical data [see 9]. Recall that a Cox process with random intensity is a counting process such that the conditional distribution of given is a Poisson process with intensity . In all the previous situations one of the main problem can be summarized as the estimation of the intensity of the process [see 14].

Note that when Cox process data arise the intensity of the process is mainly not directly observed but a co-process is observed instead. Returning to one of the previous example, in single-molecule experiments only the peaks inducing the counting process and an underlying process are observed [see 9]. Another example can be found in car insurance [see 1] where the counting process models the occurrence of car crash that are subject to weather conditions. In these cases the counting process that naturally raises is accompanied with a co-process such that the conditional law of given is a Poisson process with intensity where is a deterministic function. By a slight abuse we shall call Cox process such a counting process. From a statistical point of view one of the major issue is to estimate the deterministic function using independent copies of . However, such an approach is subject to the curse of dimensionality as the covariate takes its values in an infinite dimension space as seen in O’Sullivan [13].

When dealing with practical problems it is often unnecessary, or at least not strictly required for the modeling, to observe the full trajectory of the co-process. One can instead observe the values taken by the co-process at some well chosen random times that cover most of the information in the co-process. In this model the co-process is observed at a finite number of random times thereby circumventing the curse of dimensionality.

In this paper we consider the following model: let be a counting process and be a -valued co-process. We assume that admits a random intensity which depends on and on the observations of at random times .

More precisely, given the -algebra generated by these times, is a Cox process with intensity

| (1.1) |

where is the counting process associated to , for any function , denotes the projection and is a function from into .

In the sequel we consider that given , are independent and identically distributed (i.i.d.) copies of . The goal of this paper is to construct and study the statistical properties of a kernel-type estimator of using these data. Note that the dimension of our estimation problem, which depends on the counting process , increases with . This potentially leads to a deterioration of the accuracy of any estimation procedure as the time variable increases.

We consider a substantial data set of historical prices of companies and the crude oil prices over a period of roughly one year and two months (from 17th April, 2014 to 23rd June, 2015). The Cox process data consist of the count of the number of times when the percent returns of said companies go below a certain threshold with the counting rate depending on the stochastic dynamics of the company market capitalization. In this example the company market capitalization is represented by the action’s trade volume normalized increments and is observed when the percent return of the crude oil action goes below another threshold. By analyzing this count, we aim to learn the financial properties of this companies system.

The paper is organized as follows. Section 2 presents the estimator we propose and its asymptotic properties. In Section 3 we proceed to a simulation study. Then in Section 4 we apply the proposed estimator on the real data set presented above. Technical proofs of the asymptotic properties are postponed to Section 5.

2 Estimation strategy and results

2.1 Estimation strategy

Let and be fixed. In this section we present the main ideas behind the construction of our estimator of .

As an introduction to our methodology we consider the ideal case where we observe for all . Then our problem of estimation can simply be viewed as a regression estimation problem where is the regression function. In this context, the Nadaraya-Watson estimator writes

where denotes the multivariate product kernel where is a kernel, that is such that , is an -measurable positive random variable (called a bandwidth) and .

In practice can be estimated using the observations. Indeed, conditionally to and the -algebra generated by the co-processes , is a non-homogeneous Poisson process with intensity function , a natural estimator of this intensity is given by

where denote the jumping times of the trajectory , is a kernel and is a bandwidth. Denoting

we define the plug-in estimator by

For the sake of stability [see 4] we consider a trimmed version of the previous estimator

| (2.1) |

where and is an -measurable real-valued positive decreasing sequence.

2.2 Results

In this paper we are interested in the local behaviour of our estimator. We thus consider the pointwise mean squared error defined by

| (2.2) |

and we make local regularity assumptions on the model.

Remark that, almost surely, . For any and is defined from into .

-

1.

Given , for any , admits a conditional density defined from into ;

-

2.

and are positive continuous functions;

-

3.

and are twice differentiable and there exists a random variable depending on the dimension such that for all ,

and for all ,

where is the euclidean norm;

-

4.

There exists positive constants , and such that and

We also make technical assumptions on the kernels, the sequence and

-

1.

is a kernel of order (that is, for all from to , and ), and ;

-

2.

is a kernel of order , and ;

-

3.

for some ;

-

4.

There exists a positive constant such that . Moreover, for any , there exists a positive constant such that .

We are now in position to state our main results. Define the pointwise conditional mean squared error by

Theorem 1.

Note that the optimal choice of the -measurable bandwidths and for the pointwise conditional mean squared error is then . This leads to the following corollary for the control of the pointwise mean squared error.

Corollary 2.

Under the assumptions of theorem 1, the pointwise mean squared error writes

| (2.4) |

We can get the consistency of our estimator under weaker assumptions as shown in the following proposition.

Proposition 3.

Theorem 4 shows the asymptotic normality of our estimator.

Theorem 4.

Assume that 1 to 4 are satisfied. Let and be two -measurable bandwidths such that , , , , and a.s. as then for any such that

Remarks. Corollary 2 gives the tools to define optimal bandwidths in terms of pointwise asymptotic mean squared error. Assumptions must however be made on the process to conclude on the convergence rate since the depends on the quantity . In what follows we assume that is a renewal process with inter-arrival times distributed accordingly to a strictly increasing cumulative distribution function . The behaviour of the considered expectation is linked to the local behaviour of around . The two following examples give incentive on the performances of our estimator for close to around .

Example 1.

Example 2.

Let and be two positive constants such that and assume that around . Then,

where . So that (2) gives

Remark that if we formally take , we get back to the situation of Example 1 and the upper bounds coincide as the previous upper bound writes

Note that the rate of convergence of the mean squared error is in-between the traditional finite-dimensional rate [see 8], and the rates obtained by Biau et al [3] in the infinite-dimensional setting. This is explained by the particularity of our model which is itself in-between the finite and infinite-dimensional settings.

3 Simulation study

In this section we aim at studying the performances of our estimator from a practical point of view. To this end we study our estimator over replications of Monte Carlo simulations. The squared error, its mean (MSE) defined in (2.2), median, first and third empirical quartiles as well as the normalized root mean squared error (NRMSE) defined as follows

| (3.1) |

are used as indicators of the performances of our estimator and are calculated over a grid of times in .

3.1 Experimental design

The Monte Carlo replications are simulated according to the model (1.1) presented in the introduction where and are chosen as follows. On the one hand the inter-arrival times of the counting process have the same distribution function than with for , putting ourselves in the situation of Example 1. On the other hand

| (3.2) |

where with , is a vector of same dimension as and denotes the euclidian inner product of vectors and . The co-process is simulated according to a Brownian motion.

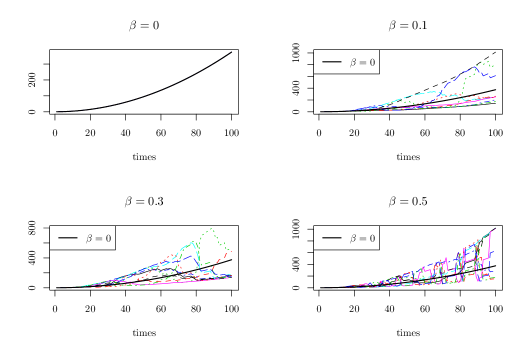

Note that the intensity is a modified version of the proportional hazards intensity function that models the dependence of our counting process on the past of the co-process . For , can be viewed as a stochastic perturbation of the intensity of a Weibull process as presented in Figure 1. Remark that for the replications look too irregular for a kernel estimator to capture their behaviour properly. It is due to the increasing impact of the covariates which we chose to be Brownian.

As is an inhomogeneous Poisson process conditionally on and , we can simulate its jumping times by applying the inverse function of to the jumping times of a homogeneous Poisson process with intensity . In our case this inverse function writes

where is such that and . This allows us to simulate the data according to our model.

3.2 Results

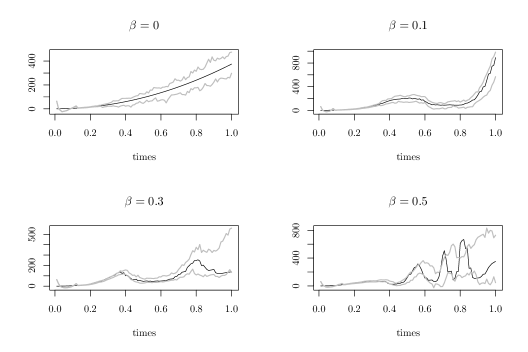

Figure 2 represents the theoretical intensity (solid) versus the first and third empirical quartiles (dashed and dotted) of Monte Carlo replications of our estimator for and (top left), (top right), (bottom left) and (bottom right). The case is the one of the estimation of the intensity of a Weibull process. As increases, the counting process deviates from this simple case to a point where the signal is almost chaotic due to the influence of the co-process for (see Figure 1). As expected our estimator is less accurate for high values of (i.e. high dimensionality) and quickly varying objective function (e.g. ). We also note an artifact for the estimation around zero. It is a well known issue with kernel estimation on the edges of the support of the objective function.

In the following we fix .

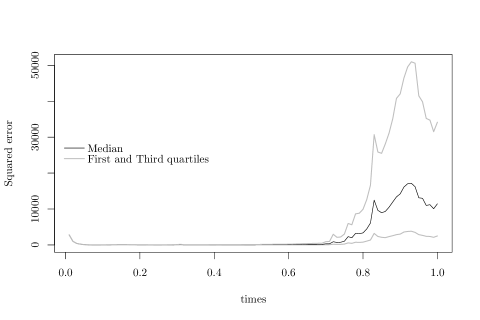

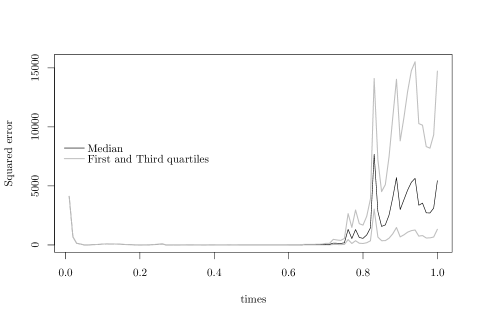

Figure 3 represents the median (solid line) and the first and third empirical quartiles (dashed and dotted lines) of the squared error of our estimator for Monte Carlo replications of our estimator for (Figure 3(a) and (Figure 3(b)). As expected, the results are far better for where the third quartile does not exceed compared to a maximum of for . Remark that these maxima are always attained near to . That is explained by the fact that as increases, the dimension of the estimation problem increases.

In Table 1 the results are obtained for Monte Carlo replications of our model for different times and different values of . The dimensionality of our estimation problem increases quickly towards at time . This shows the difficulty of the estimation for small . We observe nevertheless an increase in performance for bigger values of . For the indicator stays below after time . At this point we seem to have attained the asymptotic property for the MSE described in Section 2.2.

| Estimate | MSE | NRMSE | ||||

|---|---|---|---|---|---|---|

| 0.5 | 33 | 36.21 | 38.15 | 4.7E+03 | 1.89 | |

| 100 | 0.7 | 47 | 110.17 | 97.50 | 1.2E+05 | 3.14 |

| 0.9 | 59 | 763.96 | 675.75 | 6.5E+06 | 3.34 | |

| 0.5 | 33 | 36.21 | 38.26 | 3.4E+02 | 0.51 | |

| 250 | 0.7 | 47 | 110.17 | 92.28 | 1.3E+03 | 0.33 |

| 0.9 | 59 | 763.96 | 717.24 | 3E+06 | 2.27 | |

| 0.5 | 33 | 36.21 | 38.37 | 96 | 0.27 | |

| 500 | 0.7 | 47 | 110.17 | 91.51 | 9.4E+02 | 0.28 |

| 0.9 | 59 | 763.96 | 649.71 | 4.8E+07 | 9.06 | |

| 0.5 | 33 | 36.21 | 38.03 | 54 | 0.20 | |

| 1,000 | 0.7 | 47 | 110.17 | 92.05 | 7.1E+02 | 0.24 |

| 0.9 | 59 | 763.96 | 732.71 | 7.2E+04 | 0.35 | |

| 0.5 | 33 | 36.21 | 37.84 | 11 | 0.09 | |

| 10,000 | 0.7 | 47 | 110.17 | 92.39 | 3.8E+02 | 0.18 |

| 0.9 | 59 | 763.96 | 743.70 | 2.9E+03 | 0.07 |

4 Application to real data

We study a data set constituted of historical prices of companies as well as the crude oil prices over a period of roughly one year and two months (from 17th April, 2014 to 23rd June, 2015). The companies data are taken from the website Yahoo Finance so that every company considered composed the S&P500 index on the 23rd June, 2015. The crude oil prices are taken from the website Investing.com. The Cox process data consist of the count of the number of times when the percent returns of said companies go below a certain threshold with the counting rate depending on the stochastic dynamics of the company market capitalization. In our case the company market capitalization is represented by the action’s trade volume normalized increments and is observed when the percent return of the crude oil action below another threshold. By analyzing this count, we aim to learn the financial properties of this companies system.

| Date | Open | High | Low | Close | Volume | Adj.Close |

| 2015-06-23 | 39.89 | 39.95 | 39.42 | 39.60 | 2053600 | 39.60 |

| 2015-06-22 | 39.81 | 40.01 | 39.73 | 39.81 | 3901700 | 39.81 |

| 2015-06-19 | 39.80 | 39.94 | 39.49 | 39.49 | 2581000 | 39.49 |

| 2015-06-18 | 39.80 | 40.06 | 39.72 | 39.90 | 1865000 | 39.90 |

| 2015-06-17 | 39.76 | 39.80 | 39.32 | 39.60 | 1519400 | 39.60 |

| 2015-06-16 | 39.59 | 39.81 | 39.38 | 39.79 | 1422600 | 39.79 |

| 2015-06-15 | 39.63 | 39.63 | 39.25 | 39.52 | 2320100 | 39.52 |

| 2015-06-12 | 40.33 | 40.49 | 39.74 | 39.84 | 2764200 | 39.84 |

| 2015-06-11 | 40.57 | 40.60 | 40.29 | 40.53 | 1566000 | 40.53 |

| 2015-06-10 | 40.40 | 40.59 | 40.27 | 40.52 | 1787900 | 40.52 |

| Date | Price | Open | High | Low | Vol. | Change |

| 2015-06-23 | 61.01 | 60.21 | 61.49 | 59.55 | 336.22K | 1.04% |

| 2015-06-22 | 60.38 | 59.75 | 60.63 | 59.27 | 255.31K | 1.29% |

| 2015-06-19 | 59.97 | 60.88 | 60.93 | 59.24 | 299.89K | -1.40% |

| 2015-06-18 | 60.82 | 60.10 | 61.33 | 59.67 | 171.48K | 0.81% |

| 2015-06-17 | 60.33 | 60.52 | 61.81 | 59.34 | 232.09K | -0.20% |

| 2015-06-16 | 60.45 | 60.01 | 60.81 | 59.88 | 129.30K | 0.75% |

| 2015-06-15 | 60.00 | 60.33 | 60.42 | 59.19 | 128.26K | -0.66% |

| 2015-06-12 | 60.40 | 60.92 | 61.06 | 60.18 | 91.96K | -1.34% |

| 2015-06-11 | 61.22 | 61.56 | 61.91 | 60.65 | 150.62K | -0.97% |

| 2015-06-10 | 61.82 | 61.00 | 62.22 | 60.88 | 188.78K | 2.00% |

Tables 2 and 3 present the layout of the raw data directly taken from the websites Yahoo Finance and Investing.com. We denote the Open columns of the Yahoo Finance raw data. It represents the daily open prices of the actions of the companies. We define the percent returns as follows for . Denote the Open column of the Investing.com raw data. In the same way as for the Yahoo Finance raw data it represents the daily open prices of the crude oil action. We define its percent returns by . The Volume columns of the Yahoo Finance data are denoted . Its normalized increments are defined for by .

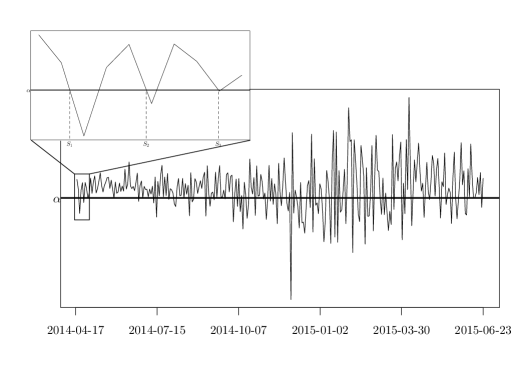

Random times as well as the counting process are deduced from these transformed data sets. They are defined such that is the first time at which goes below , is the second time, etc. and the process counts the number of times goes below . Figure 4 represents the trajectory of and gives an illustration of the construction of . With this construction we get a total of times of observation. Remark that these thresholds represent a drop for the percent returns of the crude oil action and a drop for the percent returns of the companies action.

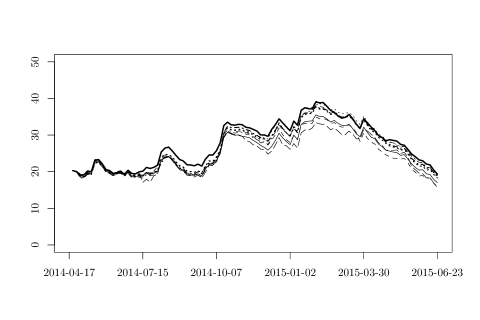

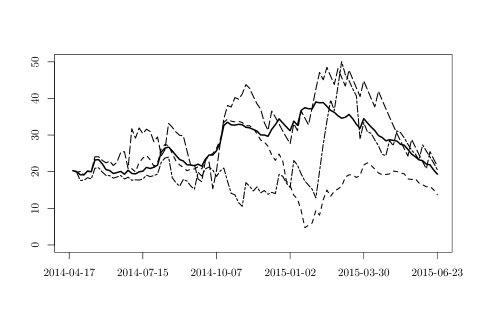

We aim to compare the inhomogeneous Poisson model with our model (1.1). To this end we compute our estimator over the time span defined by the data and for chosen trajectories of the covariate process . The resulting estimated intensities are given in Figure 5. In most cases ( out of ), we estimate the same intensity as in the inhomogeneous Poisson model. In the second graph we observe that for trajectories of , taking covariates into consideration in the model provides estimations that stays close to the inhomogeneous Poisson model at first and deviates from it after a short moment.

5 Proofs

In the sequel, denotes a positive constant that can change of values from line to line, , and respectively stand for , and . For fixed and , we define

and .

5.1 Proof of Theorem 1

Proof.

Define for the trimmed version of the Nadaraya-Watson weights as

and consider

with .

Using these notations we have

| (5.1) |

where

Decomposition (5.1) gives

| (5.2) |

On the one hand, since are independent trajectories of a conditional local martingale given and ,

As is a conditional Poisson process with cumulative intensity function given and , the quadratic variation of is the process . The Itô isometry hence gives

So that

| (5.3) |

Combining (5.2), (5.3), lemma 6 and lemma 7, theorem follows.

∎

5.2 Proof of Proposition 3

5.3 Proof of Theorem 4

Proof.

Define

where

On the one hand,

and

usual properties on kernel estimation of the density [see 5] gives

Combining these results with Slutsky lemma gives

| (5.4) |

On the other hand,

with the product kernel of and and

Applying Lemma 5 with kernel and function gives

where is a finite constant since and are compactly supported. As and ,

Combining this result with Lemma 9 and Slutsky lemma gives

| (5.5) |

As

using (5.4) and (5.5), we have

Combining this result with the dominated convergence theorem, theorem follows.

∎

6 Appendix

In the sequel denotes a positive constant under that can change of values from line to line and stands for . For simplicity, we may use the notations , , and instead of , , and respectively.

Lemma 5.

Let be a bounded, compactly supported -variate kernel satisfying

Let be such that and all entries of approach zero as tends to . Also, we assume that the ratio of the largest and smallest eigenvalues of is bounded for all .

Denote

Let be a -variate function. Also, let be the vector of first-order partial derivatives of and be the Hessian matrix of . Let’s assume that for all ,

where is a positive constant depending on dimension .

Then

Proof.

By the multivariate version of Taylor’s theorem with Lagrange remainder, for some ,

as and . ∎

Lemma 6.

where , and depend only on , , , , , and .

Proof.

Since

we have

To control the conditional expectation of this quantity we need to control

We have

On the one hand, as , applying Lemma 5 with kernel and function gives

On the other hand define

Then

The ’s are conditional i.i.d. random variable given so that for , Jensen inequality gives

For , by Khintchine inequality [see 6]

where is the global constant in Khintchine inequality depending only on . Lemma follows. ∎

Lemma 7.

Proof.

Since

we have

Note that for ,

where on the one hand, with the product kernel of and and

Applying Lemma 5 with kernel and function gives

where and is a finite constant since and are compactly supported. On the other hand define

Then

The are conditional centred random variables given so that for , by Jensen inequality

For , Khintchine inequality gives

Using Lemma 6 to control for , lemma follows. ∎

Lemma 8.

Under the assumptions of Proposition 3, almost surely

Proof.

We have

with the product kernel of and and

Applying Lemma I.4 from [5], with kernel and function gives

| (6.1) |

Also,

As is a conditional Poisson process given and ,

Define

and a -variate function such that for all Then

Applying Lemma I.4 from [5], with kernel and function , kernel and function and using (6.1) gives

∎

Lemma 9.

Under the assumptions of Theorem 4,

Proof.

Denote

and

so that . The variables are conditional independent random variables given and

To conclude it remains to check that the Lyapunov condition

| (6.2) |

is satisfied for some . Remark that

and Lemma 8 gives

so that as . It suffices to show that tends to for some to get the Lyapunov condition (6.2) satisfied. Let us take , then

Basic martingale properties as well as the Burkholder-Davis-Gundy inequality give

where the constant depends only on , , , , , , and . We can conclude that as . Lemma follows. ∎

Acknowledgement

References

- Asmussen and Albrecher [2010] S. Asmussen and H. Albrecher. Ruin probabilities, volume 14. World Scientific Publishing Company, 2010.

- Bialek et al. [1991] W. Bialek, F. Rieke, R. De Ruyter van Steveninck, and D. Warland. Reading a neural code. Science, 252(5014):1854–1857, 1991.

- Biau et al. [2010] G. Biau, F. Cérou, and A. Guyader. Rates of convergence of the functional-nearest neighbor estimate. Information Theory, IEEE Transactions on, 56(4):2034–2040, 2010.

- Bickel [1982] Peter J Bickel. On adaptive estimation. The Annals of Statistics, pages 647–671, 1982.

- Bosq and Lecoutre [1987] D. Bosq and J. P. Lecoutre. Théorie de l’estimation fonctionnelle, volume 21. Economica, 1987.

- Bretagnolle and Huber [1979] J. Bretagnolle and C. Huber. Estimation des densités: risque minimax. Probability Theory and Related Fields, 47(2):119–137, 1979.

- Brette [2008] R. Brette. Generation of correlated spike trains. Neural computation, 21(1):188–215, 2008.

- Györfi et al. [2002] L. Györfi, M. Kohler, A. Krzyżak, and H. Walk. A distribution-free theory of nonparametric regression. Springer Science & Business Media, 2002.

- Kou et al. [2005] S. C. Kou, X. Sunney Xie, and J. S. Liu. Bayesian analysis of single-molecule experimental data. Journal of the Royal Statistical Society: Series C (Applied Statistics), 54(3):469–506, 2005.

- Krumin and Shoham [2009] M. Krumin and S. Shoham. Generation of spike trains with controlled auto-and cross-correlation functions. Neural Computation, 21(6):1642–1664, 2009.

- Merton [1976] R. C. Merton. Option pricing when underlying stock returns are discontinuous. Journal of financial economics, 3(1):125–144, 1976.

- Ogata [1988] Y. Ogata. Statistical models for earthquakes occurences and residual analysis for point processes. Journal of the Royal Statistical Society, 44:102–107, 1988.

- O’Sullivan [1993] F. O’Sullivan. Nonparametric estimation in the cox model. The Annals of Statistics, pages 124–145, 1993.

- Zhang and Kou [2010] T. Zhang and S. C. Kou. Nonparametric inference of doubly stochastic poisson process data via the kernel method. The annals of applied statistics, 4(4):1913, 2010.