Mean Absolute Percentage Error for Regression Models

Abstract

We study in this paper the consequences of using the Mean Absolute Percentage Error (MAPE) as a measure of quality for regression models. We prove the existence of an optimal MAPE model and we show the universal consistency of Empirical Risk Minimization based on the MAPE. We also show that finding the best model under the MAPE is equivalent to doing weighted Mean Absolute Error (MAE) regression, and we apply this weighting strategy to kernel regression. The behavior of the MAPE kernel regression is illustrated on simulated data.

keywords:

Mean Absolute Percentage Error; Empirical Risk Minimization; Consistency; Optimization; Kernel Regression.1 Introduction

Classical regression models are obtained by choosing a model that minimizes an empirical estimation of the Mean Square Error (MSE). Other quality measures are used, in general for robustness reasons. This is the case of the Huber loss [1] and of the Mean Absolute Error (MAE, also know as median regression), for instance. Another example of regression quality measure is given by the Mean Absolute Percentage Error (MAPE). If denotes the vector of explanatory variables (the input to the regression model), denotes the target variable and is a regression model, the MAPE of is obtained by averaging the ratio over the data.

The MAPE is often used in practice because of its very intuitive interpretation in terms of relative error. The use of the MAPE is relevant in finance, for instance, as gains and losses are often measured in relative values. It is also useful to calibrate prices of products, since customers are sometimes more sensitive to relative variations than to absolute variations.

In real world applications, the MAPE is frequently used when the quantity to predict is known to remain way above zero. It was used for instance as the quality measure in a electricity consumption forecasting contest organized by GdF ecometering on datascience.net111http//www.datascience.net, see https://www.datascience.net/fr/challenge/16/details for details on this contest.. More generally, it has been argued that the MAPE is very adapted for forecasting applications, especially in situations where enough data are available, see e.g. [2].

We study in this paper the consequences of using the MAPE as the quality measure for regression models. Section 2 introduces our notations and the general context. It recalls the definition of the MAPE. Section 3 is dedicated to a first important question raised by the use of the MAPE: it is well known that the optimal regression model with respect to the MSE is given by the regression function (i.e., the conditional expectation of the target variable knowing the explanatory variables). Section 3 shows that an optimal model can also be defined for the MAPE. Section 4 studies the consequences of replacing MSE/MAE by the MAPE on capacity measures such as covering numbers and Vapnik-Chervonenkis dimension. We show in particular that MAE based measures can be used to upper bound MAPE ones. Section 5 proves a universal consistency result for Empirical Risk Minimization applied to the MAPE, using results from Section 4. Finally, Section 6 shows how to perform MAPE regression in practice. It adapts quantile kernel regression to the MAPE case and studies the behavior of the obtained model on simulated data.

2 General setting and notations

We use in this paper a standard regression setting in which the data are fully described by a random pair with values in . We are interested in finding a good model for the pair, that is a (measurable) function from to such that is “close to” . In the classical regression setting, the closeness of to is measured via the risk, also called the mean squared error (MSE), defined by

| (1) |

In this definition, the expectation is computed by respect to the random pair and might be denoted to make this point explicit. To maintain readability, this explicit notation will be used only in ambiguous settings.

Let denote the regression function of the problem, that is the function from to given by

| (2) |

It is well known (see e.g. [3]) that the regression function is the best model in the case of the mean squared error in the sense that minimizes over the set of all measurable functions from to .

More generally, the quality of a model is measured via a loss function, , from to . The point-wise loss of the model is and the risk of the model is

| (3) |

For example, the squared loss, is defined as . It leads to the risk defined above as .

The optimal risk is the infimum of over measurable functions, that is

| (4) |

where denotes the set of measurable functions from to . As recalled above we have

As explained in the introduction, there are practical situations in which the risk is not a good way of measuring the closeness of to . We focus in this paper on the case of the mean absolute percentage error (MAPE) as an alternative to the MSE. Let us recall that the loss function associated to the MAPE is given by

| (5) |

with the conventions that for all , and that . Then the MAPE-risk of model is

| (6) |

Notice that according to Fubini’s theorem, implies in particular that and thus that interesting models belong to , where is the probability measure on induced by .

We will also use in this paper the mean absolute error (MAE). It is based on the absolute error loss, defined by . As other risks, the MAE-risk is given by

| (7) |

3 Existence of the MAPE-regression function

A natural theoretical question associated to the MAPE is whether an optimal model exists. More precisely, is there a function such that for all models , ?

Obviously, we have

A natural strategy to study the existence of is therefore to consider a point-wise approximation, i.e. to minimize the conditional expectation introduced above for each value of . In other words, we want to solve, if possible, the optimization problem

| (8) |

for all values of .

We show in the rest of this Section that this problem can be solved. We first introduce necessary and sufficient conditions for the problem to involve finite values, then we show that under those conditions, it has at least one global solution for each and finally we introduce a simple rule to select one of the solutions.

3.1 Finite values for the point-wise problem

To simplify the analysis, let us introduce a real valued random variable and study the optimization problem

| (9) |

Depending on the distribution of and of the value of , is not always a finite value, excepted for . In this latter case, for any random variable , using the above convention.

Let us consider an example demonstrating problems that might arise for . Let be distributed according to the uniform distribution on . Then

If , we have

This example shows that when is likely to take values close to 0, then whenever . Intuitively, the only situation that leads to finite values is when as a finite expectation, that is when the probability that is smaller than decreases sufficiently quickly when goes to zero.

More formally, we have the following proposition.

Proposition 1.

for all if and only if

-

1.

,

-

2.

and

(10)

If any of those conditions is not fulfilled, then for all .

Proof.

We have

If then for all , . Let us therefore consider the case . We assume , the case is completely identical. We have

A simple upper bounding gives

and symmetrically

This shows that is the sum of finite terms and of . Because of the symmetry of the problem, we can focus on . It is also obvious that is finite if and only if is finite.

As pointed out above, this shows that, when , is finite if and only if both and are finite. We obtain slightly more operational conditions in the rest of the proof.

Let us therefore introduce the following functions:

We have obviously for all , . In addition

According to the monotone convergence theorem,

The link between and shows that either both and are finite, or both are infinite. In addition, we have

therefore is finite if and only if is finite. So a sufficient and necessary condition for to be finite is

A symmetric derivation shows that is finite if and only if

∎

The conditions of Proposition 1 can be used to characterize whether decreases sufficiently quickly to ensure that is not (almost) identically equal to . For instance, if , then

and the sum diverges, leading to (for ). On the contrary, if , then

and thus the sum converges, leading to for all (provided similar conditions hold for the negative part of ).

3.2 Existence of a solution for the point-wise problem

If the conditions of Proposition 1 are not fulfilled, is infinite excepted in and therefore . When they are fulfilled, we have to show that has at least one global minimum. This is done in the following proposition.

Proposition 2.

Under the conditions of Proposition 1, is convex and has at least one global minimum.

Proof.

We first note that is convex. Indeed for all , is obviously convex. Then the linearity of the expectation allows to conclude (provided is finite everywhere as guaranteed by the hypotheses).

As , there is , such that with either or . Let us assume , the other case being symmetric. Then for , . If , then for

Then

and therefore .

Similarly, if , then for

and then

and therefore .

Therefore, is a coercive function and has at least a local minimum, which is global by convexity. ∎

3.3 Choosing the minimum

However, the minimum is not necessary unique, as is not strictly convex. In general, the set of global minima will be a bounded interval of . In this case, and by convention, we consider the mean value of the interval as the optimal solution.

As an example of such behavior, we can consider the case where is a random variable on , such that , and . Then the expected loss is

and the figure 1 illustrates that there is an infinity

of solutions. Indeed when , becomes

Here we define by convention .

More generally, for any random variable , we have defined a unique value , which is a global minimum of . Moving back to our problem, it ensures that the MAPE-regression function introduced in 8 is well defined and takes finite values on . As is point-wise optimal, it is also globally optimal.

4 Effects of the MAPE on complexity control

One of the most standard learning strategy is the Empirical Risk Minimization (ERM) principle. We assume given a training set which consists in i.i.d. copies of the random pair . We assume also given a class of models, , which consists in measurable functions from to . Given a loss function , we denote .

The empirical estimate of (called the empirical risk) is given by

| (11) |

Then the ERM principle consists in choosing in the class the model that minimizes the empirical risk, that is

| (12) |

The main theoretical question associated to the ERM principle is how to control in such a way that it converges to . An extension of this question is whether can be reached if is allowed to depend on : the ERM is said to be universally strongly consistent if converges to almost surely for any distribution of (see Section 5).

It is well known (see e.g. [3] chapter 9) that ERM consistency is related to uniform laws of large numbers (ULLN). In particular, we need to control quantities of the following form

| (13) |

This can be done via covering numbers or via the Vapnik-Chervonenkis dimension (VC-dim) of certain classes of functions derived from . One might think that general results about arbitrary loss functions can be used to handle the case of the MAPE. This is not the case as those results generally assume a uniform Lipschitz property of (see Lemma 17.6 in [4], for instance) that is not fulfilled by the MAPE.

The objective of this section is to analyze the effects over covering numbers (Section 4.2) and VC-dimension (Section 4.3) of using the MAPE as the loss function. It shows also what type of ULLN results can be obtained based on those analyses (Section 4.4).

4.1 Classes of functions

Given a class of models, , and a loss function , we introduce derived classes, given by

| (14) |

and given by

| (15) |

4.2 Covering numbers

4.2.1 Notations and definitions

Let be a class of positive functions from an arbitrary set to . The supremum norm on is given by

We also define . We have obviously

Those definitions will also be used for classes of functions with values in (not only in ), hence the absolute value.

Let be a dissimilarity on , that is a positive and symmetric function from to that measures how two functions from are dissimilar (in particular ). Then can be used to characterize the complexity of by computing the -covering number of .

Definition 1.

Let be a class of positive functions from to and a dissimilarity on . For and a positive integer, a size -cover of with respect to is a finite collection of elements of such that for all

Then the -covering number of is defined as follow.

Definition 2.

Let be a class of positive functions from to , be a dissimilarity on and . Then the -covering number of , , is the size of the smallest -cover of . If such a cover does not exists, the covering number is .

The behavior of with respect to characterizes the complexity of as seen through . If the growth when is slow enough (for an adapted choice of ), then some uniform law of large numbers applies (see Lemma 1).

4.2.2 Supremum covering numbers

Supremum covering numbers are based on the supremum norm, that is

For classical loss functions, the supremum norm is generally ill-defined on . For instance let and be two functions from , generated by and (that is ). Then

If is not reduced to a single function, then there are two functions and and a value of such that . Then .

A similar situation arises for the MAPE. Indeed, let and be two functions from , generated by and in (that is ). Then

Thus unless is very restricted there is always , and such that and . Then for , has the general form with and thus .

A simple way to obtain finite values for the supremum norm is to restrict its definition to a subset of . This corresponds in practice to support assumptions on the data . Hypotheses on are also needed in general. In this latter case, one generally assumes . In the former case, assumptions depends on the nature of the loss function.

For instance in the case of the MSE, it is natural to assume that is upper bounded by with probability one. If then

and therefore the supremum norm is well defined on this subset.

In the case of the MAPE, a natural hypothesis is that is lower bounded by (almost surely). If , then

and therefore the supremum norm is well defined.

The case of the MAE is slightly different. Indeed when is fixed, then for sufficiently large positive values of , . Similarly, for sufficient large negative values of , . Thus, the supremum norm is well defined on if e.g. . In addition, we have the following proposition.

Proposition 3.

Let be an arbitrary class of models with and let . Let denote the supremum norm on defined by222Notice that while we make explicit here the dependence of the supremum norm on the support on which it is calculated, we will not do that in the rest of the paper to avoid cluttered notations. This restriction will be clear from the context.

Let , then

Proof.

Let and let be a minimal cover of (thus ). Let be the functions from associated to and let be the corresponding functions in . Then is a cover of .

Indeed let be an arbitrary element of associated and let be the corresponding function in . Then for a given , . We have then

For all , and thus

Then

and thus

which allows to conclude. ∎

This Proposition shows that the covering numbers associated to a class of functions under the MAPE are related to the covering numbers of the same class under the MAE, as long as stays away from too small values.

4.2.3 covering numbers

covering numbers are based on a data dependent norm. Based on the training set , we define for :

| (16) |

We have a simple proposition:

Proposition 4.

Let be an arbitrary class of models and a data set such that , , then for all ,

Proof.

The proof is similar to the one of Proposition 3. ∎

This Proposition is the adaptation of Proposition 3 to covering numbers.

4.3 VC-dimension

A convenient way to bound covering numbers it to use the Vapnik-Chervonenkis dimension (VC dimension). We recall first the definition of the shattering coefficients of a function class.

Definition 3.

Let be a class of functions from to and be a positive integer. Let be a set of points of . Let

that is the number of different binary vectors of size that are generated by functions of when they are applied to .

The set is shattered by if .

The -th shatter coefficient of is

Then the VC-dimension is defined as follows.

Definition 4.

Let be a class of functions from to . The VC-dimension of is defined by

Interestingly, replacing the MAE by the MAPE does not increase the VC-dim of the relevant class of functions.

Proposition 5.

Let be an arbitrary class of models. We have

Proof.

Let us consider a set of points shattered by , , . By definition, for each binary vector , there is a function such that . Each corresponds to a , with .

We define a new set of points, as follows. If , then . For those points and for any ,

and thus where .

Let us now consider the case of . By definition when and if . As the set of points is shattered (or will never be possible). In addition when then and when then . Then let . Notice that (as there is a finite number of binary vectors of dimension ). For such that , we have and thus , that is . For such that , and thus . Then .

This shows that for each binary vector , there is a function such that . And thus the are shattered by .

Therefore . If , then we can take to get the conclusion.

If then can be chosen arbitrarily large and therefore . ∎

Using theorem 9.4 from [3], we can bound the covering number with a VC-dim based value. If , , and , then

| (17) |

Therefore, in practice, both the covering numbers and the VC-dimension of MAPE based classes can be derived from the VC-dimension of MAE based classes.

4.4 Examples of Uniform Laws of Large Numbers

We show in this section how to apply some of the results obtained above.

Rephrased with our notations, Lemme 9.1 from [3] is

Lemma 1 (Lemma 9.1 from [3]).

For all , let be a class of functions from to and let . Then

If in addition

for all , then

| (18) |

A direct application of Lemma 1 to gives

provided the support of the supremum norm coincides with the support of and functions in are bounded.

In order to fulfill this latter condition, we have to resort on the same strategy used to define in a proper way the supremum norm on .

As in Section 4.2.2 let and let be such that almost surely, then

and

Then if (resp. ), Lemma 1 applies to (resp. to ).

Similar results can be obtained for the MAPE. Indeed let us assume that almost surely. Then if is finite,

and therefore for , Lemma 1 applies to .

This discussion shows that , the lower bound on , plays a very similar role for the MAPE as the role played by , the upper bound on , for the MAE and the MSE. A very similar analysis can be made when using the covering numbers, on the basis of Theorem 9.1 from [3]. It can also be combined with the results obtained on the VC-dimension. Rephrased with our notations, Theorem 9.1 from [3] is

Theorem 1 (Theorem 9.1 from [3]).

Let be a class of functions from to . Then for and

The expectation of the covering number is taken over the data set .

As for Lemma 1, we bound via assumptions on and on . For instance for the MAE, we have

| (19) |

and for the MAPE

| (20) |

Equation (20) can be combined with results from Propositions 4 or 5 to allow a comparison between the MAE and the MAPE. For instance, using the VC-dimension results, the right hand side of equation (19) is bounded above by

| (21) |

while the right hand side of equation (20) is bounded above by

| (22) |

In order to obtain almost sure uniform convergence of to over , those right hand side quantities must be summable (this allows one to apply the Borel-Cantelli Lemma). For fixed values of the VC dimension, of , and this is always the case. If those quantities are allowed to depend on , then it is obvious, as in the case of the supremum covering number, that and play symmetric roles for the MAE and the MAPE. Indeed for the MAE, a fast growth of with might prevent the bounds to be summable. For instance, if grows faster than , then does not converges to zero and the series is not summable. Similarly, if converges too quickly to zero, for instance as , then does not converge to zero and the series is not summable. The following Section goes into more details about those conditions in the case of the MAPE.

5 Consistency and the MAPE

We show in this section that one can build on the ERM principle a strongly consistent estimator of with minimal hypothesis on (and thus almost universal).

Theorem 2.

Let be a random pair taking values in such that almost surely ( is a fixed real number). Let be a series of independent copies of .

Let be a series of classes of measurable functions from to , such that:

-

1.

;

-

2.

is dense in the set of functions from to for any probability measure ;

-

3.

for all , ;

-

4.

for all , .

If in addition

and there is such that

then converges almost surely to .

Proof.

We use the standard decomposition between estimation error and approximation error. More precisely, for , a class of functions,

We handle first the approximation error. As pointed out in Section 2, implies that . Therefore we can assume there is a series of functions from such that

by definition of as an infimum.

Let us consider two models and . For arbitrary and , we have

and thus

and therefore

Then

As almost surely,

and thus

As is dense in there is a series of functions of such that . Then and thus . Let . By definition, .

Let . Let be such that . Then and . Let . As is an increasing series of sets, and thus for all , . This shows that .

The estimation error is handled via the complexity control techniques studied in the previous Section. Indeed, according to Theorem 1, we have (for )

with

Then using equation (22)

Using the fact that , we have

and

As ,

As ,

Therefore, for sufficiently large, is dominated by a term of the form

with and (both depending on ). This allows to conclude that . Then the Borel-Cantelli theorem implies that

The final part of the estimation error is handled in a traditional way. Let . There is such that implies

Then . By definition

and thus for all ,

By taking the infimum on , we have therefore

Applying again the hypothesis,

and therefore

As a consequence

The combination of this result with the approximation result allows us to conclude. ∎

Notice that several aspects of this proof are specific to the MAPE. This is the case of the approximation part which has to take care of taking small values. This is also the case of the estimation part which uses results from Section 4 that are specific to the MAPE.

6 MAPE kernel regression

The previous Sections have been dedicated to the analysis of the theoretical aspects of MAPE regression. In the present Section, we show how to implement MAPE regression and we compare it to MSE/MAE regression.

On a practical point of view, building a MAPE regression model consists in minimizing the empirical estimate of the MAPE over a class of models , that is to solve

where the are the realizations of the random variables .

Optimization wise, this is simply a particular case of median regression (which is in turn a particular case of quantile regression). Indeed, the quotient by can be seen as a fixed weight and therefore, any quantile regression implementation that supports instance weights can be used to find the optimal model. This is for example the case of quantreg R package [5], among others. Notice that when corresponds to linear models, the optimization problem is a simple linear programming problem that can be solved by e.g. interior point methods [6].

For some complex models, instance weighting is not immediate. As an example of MAPE-ing a classical model we show in this section how to turn kernel quantile regression into kernel MAPE regression. Notice that kernel regression introduces regularization and thus is not a direct form of ERM. Extending our theoretical results to the kernel case remains an open question.

6.1 From quantile regression to MAPE regression

6.1.1 Quantile regression

Let us assume given a Reproducing Kernel Hilbert Space (RKHS), , of functions from to (notice that could be replaced by an arbitrary space ). The associated kernel function is denoted and the mapping between and , . As always, we have .

The standard way of building regression models based on a RKHS consists in optimizing a regularized version of an empirical loss, i.e., in solving an optimization problem of the form

| (23) |

Notice that the reproducing property of implies that there is such that .

In particular, quantile regression can be kernelized via an appropriate choice for . Indeed, let and let be the check-function, introduced in [7]:

The check-function is also called the pinball loss. Then, the kernel quantile optimization problem, treated in [8, 9], is defined by:

| (24) |

where handles the trade-off between the data fitting term and the regularization term. The value of gives the quantile that the model is optimized for: for instance corresponds to the median.

6.2 MAPE primal problem

To consider the case of the MAPE, one can change the equation (24) to (25):

| (25) |

Notice that for the sake of generality, we do not specify the value of in this derivation: thus equation (25) can be seen as a form of “relative quantile”. However, in the simulation study in Section 6.3, we limit ourselves to the standard MAPE, that is to . The practical relevance of the “relative quantile” remains to be assessed.

Using the standard way of handling absolute values and using , we can rewrite the regularization problem (25) as a (primal) optimization problem:

| (26) | |||||

| subject to | |||||

where .

6.2.1 MAPE dual problem

Let us denote the vector regrouping all the variables of the primal problem. We denote in addition:

Then the Wolfe Dual of problem (26) is given by:

| (27) | |||||

| s. t. | |||||

where the are the Lagrange multipliers. Some algebraic manipulations show that problem (27) is equivalent to problem (28):

| (28) | |||||

| s. t. | (29) | ||||

| (30) | |||||

| (31) | |||||

| (32) | |||||

| (33) |

We can simplify the problem by introducing a new parametrisation via the variables . Then the value of is obtained from constraint (29) as . Constraints (30) can be rewritten into . Taking those equations into account, the objective function becomes

Using constraints (31) and (32), the last two terms simplify as follows:

and thus the objective function is given by

where is the kernel matrix. This shows that the objective function can be rewritten so as to depend only on the new variables . The last step of the analysis consists in showing that a similar property holds for the constraints. The cases of constraints (29) and (30) have already been handled.

Notice that given an arbitrary , there is always and such that . However, constraints (31) and (32) combined with and show that and (and thus ) cannot be arbitrary, as we need and . As , and thus . As , and thus . Conversely, it is easy to see that if satisfies the constraints , then there is for such that and such that the constraints (31), (32) and (33) are satisfied (take and ).

Then problem (28) is finally equivalent to

| (34) | |||||

| s.c. | |||||

6.2.2 Comparaison to the quantile regression

In the case of quantile regression, [8] shows that the dual problem is equivalent to

| s.c. | ||||

In comparison to problem (34), one can remark that the modification of the loss function (from the absolute error to the absolute percentage error) in the primal optimization problem is equivalent to changing the set of optimization in the dual optimization problem. More precisely, it is equivalent to reducing (resp. increasing) the “size” of the optimization set of if (resp. ).

Thus, the smaller is , the larger is the optimization set of . This permits to ensure a better fit on small values of (i.e. where the absolute percentage error is potentially bigger). Moreover, by choosing a very large value of (or ), one can ensure the same optimal value of each in MAE and MAPE dual problems. This surprising fact can be explained by noticing that a very large value of corresponds to a very small value of (or ). When goes to zero, the regularization in equations (24) and (25) vanishes, which leads to potential overfitting. When this overfitting appears, regardless of the loss function and thus the different loss functions are equivalent.

6.3 A simulation study

6.3.1 Generation of observations

In this section, we illustrate the efficiency of the kernel MAPE regression described in section 6.1 on simulated data, and we compare the results to the ones obtained by kernel median regression. Experiments have been realized using a Gaussian kernel.

As in [8], we have simulated data according to the sinus cardinal function, defined by

However, to illustrate the variation of the prediction according the proximity to zero, we add a parameter and we define the translated sinus cardinal function by:

For experiments, we have generated 1000 points to constitute a training set, and 1000 other points to constitute a test set. As in [8], the generation process is the following:

with and

To compare the results between the median estimation and the MAPE estimation, we have computed and for several values of . The value of the regularization parameter is chosen via a 5-fold cross-validation.

6.3.2 Results

| a | ||||

|---|---|---|---|---|

| (in %) | (in %) | |||

| 0.00 | 128.62 | 94.09 | 0.01 | 0.10 |

| 0.10 | 187.78 | 100.10 | 0.05 | 0.01 |

| 0.50 | 72.27 | 57.47 | 5.00 | 10.00 |

| 1.00 | 51.39 | 39.53 | 10000.00 | 1.00 |

| 2.50 | 10.58 | 10.98 | 5.00 | 1.00 |

| 5.00 | 4.80 | 4.89 | 5.00 | 10.00 |

| 10.00 | 2.39 | 2.40 | 5.00 | 100.00 |

| 25.00 | 0.96 | 0.96 | 5.00 | 100000.00 |

| 50.00 | 0.48 | 0.48 | 5.00 | 1000.00 |

| 100.00 | 0.24 | 0.24 | 5.00 | 10000.00 |

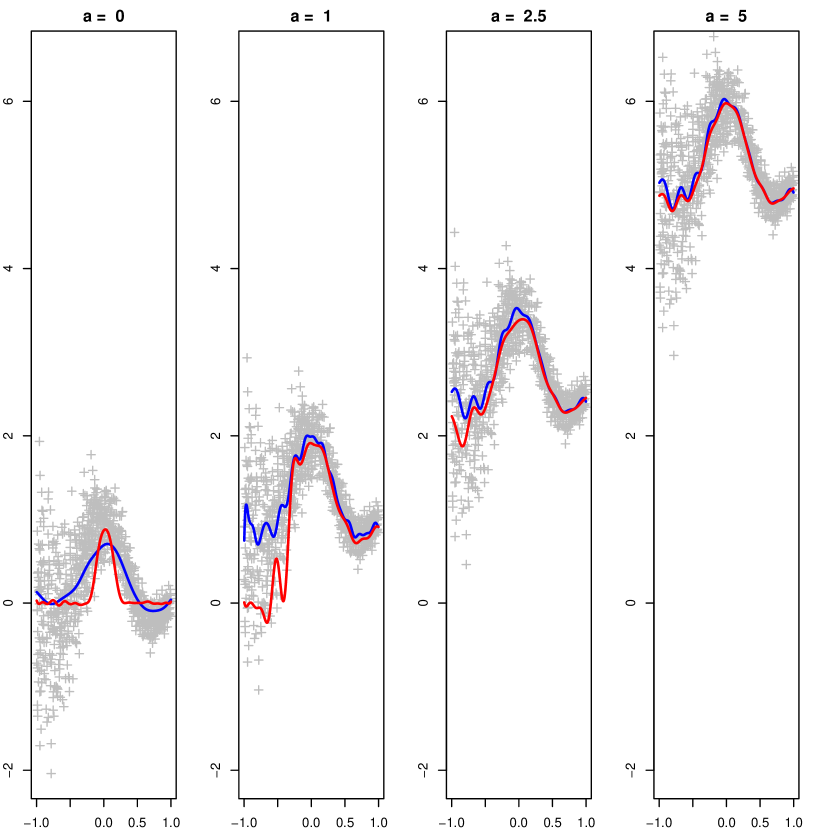

Results of experiments are described in the table 1. As expected, in most of the cases, the MAPE of is lower than the one of . This is especially the case when values of are close to zero.

6.3.3 Graphical illustration

Some graphical representations of and are given on Figure 2. This Figure illustrates several interesting points:

-

1.

When, for a given , may take both negative and positive values, (red curve) is very close or equal to 0 to ensure a 100% error whereas (blue curve) is closer to the conditional median, which leads to a strongly higher error (in MAPE terms).

-

2.

Up to translation, looks roughly the same for each , whereas the shape of is strongly modified with . This is because the absolute error (optimization criteria for the blue curve) remains the same if both the observed value and its predicted value are translated by the same value, whereas the MAPE changes.

-

3.

Red curves are closer to 0 than blue curves. One can actually show that, regarding to the MAPE, the optimal estimator (red) of a random variable is indeed below the median (blue).

-

4.

The red curve seems to converge toward the blue one for high values of .

7 Conclusion

We have shown that learning under the Mean Absolute Percentage Error is feasible both on a practical point of view and on a theoretical one. More particularly, we have shown the existence of an optimal model regarding to the MAPE and the consistency of the Empirical Risk Minimization. Experimental results on simulated data illustrate the efficiency of our approach to minimize the MAPE through kernel regressions, what also ensures its efficiency in application contexts where this error measure is adapted (in general when the target variable is positive by design and remains quite far away from zero, e.g. in price prediction for expensive goods). Two open theoretical questions can be formulated from this work. A first question is whether the lower bound hypothesis on can be lifted: in the case of MSE based regression, the upper bound hypothesis on is handled via some clipping strategy (see e.g. Theorem 10.3 in [3]). This cannot be adapted immediately to the MAPE because of the importance of the lower bound on in the approximation part of Theorem 2. A second question is whether the case of empirical regularized risk minimization can be shown to be consistent in the case of the MAPE.

Acknowledgment

The authors thank the anonymous reviewers for their valuable comments that helped improving this paper.

References

References

- [1] P. J. Huber, Robust estimation of a location parameter, The Annals of Mathematical Statistics 35 (1) (1964) 73–101.

- [2] J. S. Armstrong, F. Collopy, Error measures for generalizing about forecasting methods: Empirical comparisons, International Journal of Forecasting 8 (1) (1992) 69 – 80.

- [3] L. Györfi, M. Kohler, A. Krzyżak, H. Walk, A Distribution-Free Theory of Nonparametric Regression, Springer, New York, 2002.

- [4] M. Anthony, P. L. Bartlett, Neural Network Learning: Theoretical Foundations, Cambridge University Press, 1999.

- [5] R. Koenker, quantreg: Quantile regression. r package version 5.05 (2013).

- [6] S. Boyd, L. Vandenberghe, Convex optimization, Cambridge university press, 2004.

- [7] R. Koenker, G. Bassett Jr, Regression quantiles, Econometrica: journal of the Econometric Society (1978) 33–50.

- [8] I. Takeuchi, Q. V. Le, T. D. Sears, A. J. Smola, Nonparametric quantile estimation, The Journal of Machine Learning Research 7 (2006) 1231–1264.

- [9] Y. Li, Y. Liu, J. Zhu, Quantile regression in reproducing kernel hilbert spaces, Journal of the American Statistical Association 102 (477) (2007) 255–268.