Qiang and Bayati

Dynamic Pricing with Demand Covariates

Dynamic Pricing with Demand Covariates

Sheng Qiang \AFFStanford University Graduate School of Business, Stanford, CA 94305, \EMAILsqiang@stanford.edu \AUTHORMohsen Bayati \AFFStanford University Graduate School of Business, Stanford, CA 94305, \EMAILbayati@stanford.edu

We consider a generic problem in which a firm sells products over periods without knowing the demand function. The firm sequentially sets prices to earn revenue and to learn the underlying demand function simultaneously. A natural heuristic for this problem, commonly used in practice, is greedy iterative least squares (GILS). At each time period, GILS estimates the demand as a linear function of the price by applying least squares to the set of prior prices and realized demands. Then a price that maximizes the revenue, given the estimated demand function, is used for the next time period. The performance is measured by the regret, which is the expected revenue loss from the optimal (oracle) pricing policy when the demand function is known. Recently, den Boer and Zwart (2014) and Keskin and Zeevi (2014) demonstrated that GILS is sub-optimal. They introduced algorithms which integrate forced price dispersion with GILS and achieve asymptotically optimal performance.

In this paper, we consider this dynamic pricing problem in a data-rich environment. In particular, we assume that the firm knows the expected demand under a particular price from historical data, and in each period, before setting the price, the firm has access to extra information (demand covariates) which may be predictive of the demand. Demand covariates can include marketing expenditures, geographical information, consumers socio-economic attributes, macroeconomic indices, weather, etc. We prove that in this setting the behavior of GILS is dramatically different and it achieves asymptotically optimal regret of order . We also show the following surprising result: in the original dynamic pricing problem of den Boer and Zwart (2014), Keskin and Zeevi (2014), inclusion of any set of covariates in GILS as potential demand covariates (even though they could carry no information) would make GILS asymptotically optimal. We validate our results via extensive numerical simulations on synthetic and real data sets.

dynamic pricing, exploration and exploitation, demand covariates \HISTORYThis version appeared on April 14, 2016.

1 Introduction

Companies launch new products periodically without accurate prior knowledge of the true demand. One method to learn the demand function is price experimentation, where companies adaptively modify prices to learn the hidden demand function and use that to estimate the revenue-maximizing price. Nevertheless, proper price experimentation is a challenging problem due to the potential revenue loss during the learning horizon that can be substantially large. In fact optimally balancing the trade-off between randomly selecting prices to expedite the learning versus selecting prices that maximize the expected earning has been subject of recent research in the operations management literature. Learning and earning are also known by exploration and exploitation respectively. In particular, den Boer and Zwart (2014), Keskin and Zeevi (2014) studied greedy iterated least squared (GILS), a popular heuristic used in practice, which works by greedily selecting the best price based on the most up-to-date estimation of the demand at any time. GILS pricing policy is also known by myopic pricing or certainty equivalent pricing. den Boer and Zwart (2014), Keskin and Zeevi (2014) showed that GILS is sub-optimal and suffers from incomplete learning. In addition, they introduced algorithms that integrate forced price dispersion with GILS and achieve asymptotically optimal regret. Despite these results, in most applications, greedy policies such as GILS are popular due to their simplicity and due to the common perception of the firms that price experimentation could lead to substantial revenue loss.

On the other hand, thanks to growing availability of data and advances in statistical learning, estimation problems such as the aforementioned demand learning can be solved much more accurately in data-rich environments. The most common approach in boosting the accuracy is through introduction of covariates (or predictors or features) and finding a function that accurately maps the covariates and price to the outcome of interest (demand in our case). Examples of covariates for the demand estimation could be market size, macroeconomic indices, seasonality, or geographic indicators.

In this paper we study the impact of including demand covariates on the aforementioned trade-off between learning and earning. While adding these covariates is a natural step to improve the demand estimation and hence to expedite the learning, we show an additional and surprising benefit; inclusion of the demand covariates in the popular GILS approach automatically solves the incomplete-learning problem. In other words, no pro-active learning is required and the companies can focus all of their attention to earning. We provide general sufficient conditions for asymptotically optimality of GILS with demand covariates. A technical part of our analysis is proving sharp concentration inequalities for the minimum singular value of the least squared design matrix and relies on a recent concentration inequality for sum of matrix martingales by Tropp (2011).

In addition, we prove that even if the demand covariates are irrelevant and do not improve the demand estimation, their inclusion is beneficial and makes GILS asymptotically optimal. In other words, the process of learning which covariates have coefficients equal to zero (feature selection) which is usually performed separately by data scientists, if combined with GILS pricing policy, dramatically improves the performance. The added uncertainty from not knowing which variables are predictive, creates automatic price experimentation that solves the incomplete learning problem of GILS.

Finally, via extensive numerical simulations on synthetic and real data sets, we demonstrate robustness of our results to the assumptions required by the theory.

1.1 Organization of the paper

The remainder of the paper is organized as follows. Section 2 surveys related research and it is followed by formal definition of the problem and GILS policy in Section 3. Analysis of the regret and our main theoretical results are presented in Section 4 while empirical simulations are given in Section 5. Section 6 covers final remarks and discussions, and all proofs are provided in Appendix 7. In Appendix 8 we explain how the proofs can be extended when our modeling assumptions on covariates and demand uncertainty are generalized.

2 Related Literature

The trade-off between learning and earning has long been a focus of attention in statistics (Lai and Robbins 1979, 1985), computer science (Auer et al. 2002, Auer 2003), and economics (Segal 2003, Kreps and Francetich 2014). There has also been recent interest in this topic in the operations management community, especially in the field of dynamic pricing and revenue management. An admittedly incomplete list of such papers is (Kleinberg and Leighton 2003, Carvalho and Puterman 2005, Araman and Caldentey 2009, Besbes and Zeevi 2009, 2011, Harrison et al. 2012, den Boer and Zwart 2014, Keskin and Zeevi 2014, Johnson et al. 2015, Chen et al. 2015). We defer the reader to the recent survey by den Boer (2015a) and references therein for a complete list and thorough discussion.

Among these, the most related papers with our paper are (den Boer and Zwart 2014, Keskin and Zeevi 2014). Keskin and Zeevi (2014) study the balance between learning and earning if the expected demand is a linear function of the price while den Boer and Zwart (2014) consider a more general case– when the expected demand is a generalized linear function of the price. These papers propose novel variants of the greedy policy, namely controlled variance pricing (CVP) by den Boer and Zwart (2014) and constrained iterative least squared (CILS) by Keskin and Zeevi (2014), which enforce price dispersion within GILS and achieve asymptotically optimal regret. Keskin and Zeevi (2014) also provide lower bounds for any pricing policy. Our work is closer to (Keskin and Zeevi 2014), since similar to them, we study the situation where demand at a single incumbent price is known to the firm with high accuracy. Our main contributions compared to these papers is studying the problem in a data-rich environment (when demand covariates are available), showing how this addition fundamentally changes behavior of GILS, and that it does not need any forced price dispersion like in CVP and CILS. Similar to (Keskin and Zeevi 2014), we also show a lower bound for performance of any pricing policy in presence of demand covariates. Hence we show that GILS is asymptotically optimal.

This result is surprising since as shown by Lai and Robbins (1982), the parameter estimates computed under an iterative least squared policy may not be consistent, and the resulting controls are sub-optimal. This fact is also shown by den Boer and Zwart (2014), Keskin and Zeevi (2014) in the dynamic pricing problem (without demand covariates) and is termed incomplete learning which motivated the novel policies CVP and CILS. Although, it is worth noting that a certain Bayesian form of iterative least squared (when parameters to estimate have a probability distribution with a prior) converges to the optimum values (Chen and Hu 1998).

Another related setting is dynamic pricing with demand uncertainty where the demand function is not static and changes over time. Variants of this setting have been studied by den Boer (2015b), Keskin and Zeevi (2013). Although, at a first look one can consider our demand function that depends on price and covariates as a changing demand function, however our setting is a substantially different problem. The reason is that the information provided by the demand covariates in our model is hidden in demand shocks. In particular, if the covariate information is not available to the firm, our setting can be exactly mapped to the case of static dynamic pricing where demand shocks have higher variance.

In the learning and earning framework, beyond dynamic pricing, there are few papers that consider how covariates may help the decision maker to improve the performance. This problem was first studied in the statistics literature by Woodroofe (1979), Sarkar (1991) where a simple one-armed bandits problem with a covariate was considered and they showed that a myopic policy is asymptotically optimal. Much later, a machine learning paper by Langford and Zhang (2007) considered a more general problem of learning and earning with covariates. Their problem was inspired by online advertising where a platform such as Facebook, Google, MSN, or Yahoo needs to match publishers to viewers in order to maximize the expected number of user clicks. They modeled the problem as a -armed bandits problem, with the contexts (covariates) which may predict the revenue of each arm. This pioneered an active research area (contextual bandits). Examples of papers studying contextual bandits are (Dudik et al. 2011, Chu et al. 2011, Seldin et al. 2011, Li et al. 2014, Badanidiyuru et al. 2014, Goldenshluger and Zeevi 2007, 2011, 2013, Rigollet and Zeevi 2010, Perchet et al. 2013, Bastani and Bayati 2015). The main difference between these papers and our paper is that in our model the reward is a quadratic function of the action (price) and covaraites. But these papers either consider -armed bandits or linear bandits where the reward function is linear in covariates and the action. In addition, none of these contextual bandit papers show optimality results for the greedy policy which is popular among practitioners. In fact, the greedy-type policies studied by these paper, similar to CVP and CILS, have a degree of forced experimentation where greedy policy is used in fraction of the periods to maximize the reward and the remaining fraction of periods are dedicated to forced experimentation to improve learning. The value of is reduced over time to avoid a linear regret.

Our results are also related to the recent growing literature in Operations Management that studies benefits of combining statistical estimation with decision optimization (Liyanage and Shanthikumar 2005, Levi et al. 2015, Rudin and Vahn 2014, Bertsimas and Kallus 2015). The main difference is that these papers focus on a static decision making task while here we are considering a dynamic decision making problem. In particular, our focus is on the impact of combining statistical estimation with price optimization on creating enough price dispersion (exploration) which is required for the pricing policy.

While writing this paper, we became aware of a very recent paper by Cohen et al. (2016) that also studies dynamic pricing with covariates. For the following reasons the two papers are fundamentally different. Cohen et al. (2016) assume that demand is equal to if price is less than a linear function of the covariates which is interpreted as valuation of the customer. If the price is greater than the valuation then demand is . But our demand function is quadratic in price and linear in covariates. In addition, our demand function includes stochastic demand shocks. Due to the threshold form of the demand function in (Cohen et al. 2016), estimating the problem parameters (coefficients of the covariates) can no longer be solved by a simple procedure such as least squared. On the other hand, their demand function is deterministic and does not contain demand shocks which are the core reason behind the difficulty of demand estimation studied by us. Cohen et al. (2016) consider adversarial covariates while our covariates are stochastic. Finally, we provide both upper bounds and lower bounds for the regret of a popular algorithm in practice (GILS) while Cohen et al. (2016) introduce new algorithms for their setting and prove only upper bounds for the regret. Another paper at the intersection of dynamic pricing and contextual bandits is by Amin et al. (2014) which considers a problem similar to Cohen et al. (2016) that is different from ours.

3 Problem Formulation

Consider a firm that sells one type of product over time. In each period, the firm can adjust price of the product. Customer demand for the product is determined by the price and some other factors (demand covariates), according to an underlying parametric demand function. The firm is initially uncertain about the parameters of the demand function but can use historical data on charged prices, realized demands, and observed values of the demand covariates to estimate the parameters. This is the problem of dynamic pricing with demand covariates.

3.1 Model Setting

Our model builds on the model of Keskin and Zeevi (2014). We assume the firm sells the product over a time horizon of periods. The total periods is a large number and is unknown to the seller, which prevents the firm from using as a decision factor. In each period , where is the set of positive integers, the seller observes some demand covariates of the market, that is a vector of covariates sampled independently from a fixed distribution . We assume that is absolutely continuous with respect to the Lebesgue measure on and has compact support, i.e. there is such that for all in . Then the seller must choose the price from a given feasible set , where . After that, the seller observes the demand in period . We assume the demand follows a linear function of the prices and covariates, which is commonly used in economic literature to illustrate the relationship between demand and price. Hence, the demand function is formulated as

| (1) |

where denotes the inner product of vectors and , is the basic market size, is the price coefficient (that is ), and is a vector of coefficients for the demand covariates. The parameters are assumed to be unknown to the seller. In addition, are unpredictable demand shocks, drawn independently identically from a distribution with zero mean, finite variance denoted by . Note that we assume there is a large enough inventory that any amount of demand can be fulfilled by the firm.

Next, without loss of generality, we assume that since any possible non-zero expectation can be moved to the intercept term . Additionally, we assume that the covariance matrix of demand covariates (denoted by ) is positive definite. To make the math cleaner, we also assume that each coordinate of is re-scaled so that the diagonal entries of are all equal to (i.e., all coordinates of have unit variance).

Remark 3.1

In Section 8.1 we will show that our main result (upper bound on performance of GILS with demand covariate) holds when the i.i.d. assumptions on sequences and are replaced by weaker assumptions that they are martingale differences with respect to the past.

We also assume that the seller has access to one more piece of prior information; through extensive use of an incumbent price in the past the seller knows the average demand at this incumbent price with high accuracy. More precisely, denoting the average historical demand as , the fact that shocks and have zero average help us to simplify the demand function because the expected demand satisfies . Therefore, with large number of uses of the incumbent price , the average value is close to its expected value by the strong law of large numbers. Thus, we can write which leads to the following modified demand function

We can treat as a given number . Hence, are final demand model is

| (2) |

in which is known, and are unknown parameters.

Remark 3.2

Throughout the rest of the paper when we use the phrase “dynamic pricing problem” it is implicitly assumed that we are referring to the case where an incumbent price is available, or equivalently, to problem (2) with known .

To simplify the notation, we let

be the column vector of demand model parameters, and express the demand vector in in terms of as follows

| (3) |

Here , , and is a matrix with its row equal to where

Without loss of generality, we assume that the prices include subtraction of production cost and we do not write them explicitly in the formula. Thus, the terms profit and revenue are used interchangeably. The seller’s expected single-period revenue function is

| (4) |

Next we define to be the price that maximizes the expected single-period revenue function given the demand covariates , i.e.

| (5) |

We assume that the true parameter is in the compact set

where is the norm. The condition on just means that the expected demand is strictly decreasing in price and we have an uncertain interval of negative numbers around it. We also assume that the optimal price corresponding to any such true parameter and any vector of demand covariates is an interior point of the feasible set . Similar assumption was made by den Boer and Zwart (2014) and Keskin and Zeevi (2014). The reason for the assumption is to avoid having the optimal price to be a corner solution of the interval so we can use first order conditions. In particular, the first-order condition for optimality would be

| (6) |

from which we deduce that

| (7) |

For the incumbent price , we consider there is a small positive constant , such that

| (8) |

This condition will guarantee that for any the following inequality holds,

3.2 Pricing Policies and Performance Metric

Let denote the observed demands, prices and the demand covariates before choosing a price and realizing demand at period . That is, . We define a pricing policy as a sequence of functions , where

for all , and is a deterministic function of . Now, we clarify the probability space for the performance. Any pricing policy induces a family of probability measures on the sample space of demand sequences as below. Given the parameter vector , the realized demand covariates , and a pricing policy , let be the probability measure with respect to the randomness of demand shocks, i.e.

| (9) |

Thus, , which implies that is completely characterized by , , and . Accordingly the -period expected revenue of the seller is

| (10) |

where is the expectation operator with respect to the randomness in demand shocks. The performance metric we will use throughout this study is the -period regret, which is a random variable depending on the realized demand covariates sequence , defined as

| (11) |

where is the optimal expected single-period revenue, given the demand covariates . After algebraic manipulation of the above expression for the regret, we can write the -period regret as

| (12) |

While deriving our lower bounds on best achievable performance, we will also make use of the worst-case regret, which is

| (13) |

The regret of a policy can be interpreted as the expected revenue loss relative to a clairvoyant policy that knows the true value of at the beginning; smaller values of regret are more desirable for the seller.

3.3 Greedy Iterated Least Squares (GILS)

Given the history of demands, prices, and demand covariates through the end of period , the least squares estimator of is given by

| (14) |

for . Using the first-order optimality conditions of the least squares problem (14), the estimator can be expressed explicitly. In particular, the simplified demand function (3) gives us

| (15) |

and the deviation from the true parameter is

| (16) |

Because lies in the compact set , the accuracy of the unconstrained least squares estimate can be improved by projecting it into the set . We denote by the truncated estimate that satisfies , where by assumption the corresponding price vector is an interior point of the feasible set . We call the policy that charges price in period the greedy iterated least squares (GILS) policy with demand covariates and denote it by . Throughout the rest of the paper we make the following assumption. {assumption} We only consider the subclass of GILS policies where the initial prices are selected so that the vectors for are linearly independent. Note that this is not a restricting assumption. In fact, if the initial prices are selected from any absolutely continuous distribution on interval with respect to the Lebesgue measure (e.g., uniform distribution) then given that the distribution of is also absolutely continuous with respect to the Lebesgue measure on , the matrix

will be invertible with probability . We defer to (Billingsley 1979) for further details on this.

4 Analysis of the Regret

In this section we start by providing a lower bound for the cumulative regret of any policy for the dynamic pricing problem with demand covariates. Then in Section 4.2 we prove an upper bound for the greedy policy when the seller has access to demand covariates. Finally, in Section 4.3 we will prove that in the case of dynamic pricing without demand covariates, the greedy policy can still be optimal if the firm uses some demand covariates (even though the covariates provide no information). While our proof of the upper bound which is the main technical contribution of this paper does not require any additional assumption on distribution of the demand shocks beyond having zero mean and finite variance, our proof of the lower bound which relies on proof of Keskin and Zeevi (2014) for the lower bound of any policy requires demand shocks to have a Gaussian distribution.

4.1 Lower Bound Analysis

If there is no demand shock in any period, then we can easily learn the true parameters by solving a system of linear equations. However, these shocks have a high impact on learning and consequently on the regret. We can statistically estimate the true parameters, but the estimation error will lead to an inevitably growing revenue loss (regret) over time. Formally, we can prove that the regret of any policy has a lower bound that grows with time.

Theorem 4.1 (Lower bound on regret)

Assume that the demand shocks are i.i.d. with distribution . There exists a finite positive constant such that for any pricing policy , any realized demand covariates , and time horizon .

For any realized demand covariates , Theorem 4.1 gives us a lower bound on the worst-case -period regret of any given policy . Therefore, if a policy achieves a regret of order , the same order as the lower bound, then we call the policy an asymptotically optimal policy.

Remark 4.2

Authors of Besbes and Zeevi (2009, 2011), Broder and Rusmevichientong (2012), Keskin and Zeevi (2014) also provide lower bounds for the regret in similar problems. However, in their settings, firm has no access to the demand covariates. Theorem 4.1 is a non-trivial extension since it shows that increasing the firm’s information, via adding the demand covariates that could potentially expedite the learning, does not improve the lower bound.

4.2 Greedy Policy is Asymptotically Optimal

In this section we focus on proving an upper bound for GILS policy. First we introduce a new notation. For a pricing policy , the expected regret over the uncertainty of demand covariates is defined by

| (17) |

Next, we state the main result of Section 4.2. Its proof is provided in Appendix 7.2.

Theorem 4.3 (GILS is asymptotically optimal)

Consider the dynamic pricing problem with demand covariates of Section 3 and assume that . The GILS policy achieves asymptotically optimal expected regret. In particular, there is a constant such that , for all large enough. In addition, the constant is equal to

| (18) |

where

and

Theorem 4.3 shows that the incomplete learning problem of GILS is fixed under the disturbance created by the demand covariates, justifying its popularity in practice.

4.3 Astrology Reports Assist Greedy

One of the most interesting findings of this paper is that Theorem 4.3 can be applied to a special case of the model when , that is for .

Corollary 4.5

Under the same assumptions as in Theorem 4.3, the GILS policy achieves asymptotically optimal expected regret, that is , even when demand covariates have no information (i.e., when ).

In this situation, the demand covariates are not predictive of the demand. Thus, the optimal price is the same optimal price as in the case of not having any demand covariates. However, the presence of the demand covariates in the estimation procedure fundamentally impacts performance of GILS policy. Without the demand covariates, GILS policy has a regret which grows linearly with the total periods. With the uninformative demand covariates, GILS policy achieves the asymptotically optimal performance.

The above analysis demonstrates an interesting approach to the original dynamic pricing problem – when there is no demand covariate in the demand function. The firm can keep using GILS policy and add some potential demand covariates, as long as they contain random fluctuations, even if they are completely uninformative. The key point is that the firm assumes the covariates could possibly have a predictive power, and uses the covariates to predict the demand function. Then over time, the greedy policy automatically screens out the useless covariates as their estimated coefficients will converge to zero. However, since the coefficients are not exactly zero, the random perturbations provided by them leads to a natural price experimentation which will rescue GILS from incomplete learning. This is why we describe the scenario as “astrology reports” help greedy achieve the asymptotic optimal performance.

5 Empirical Analysis

In this section, we provide three numerical illustrations of the GILS policy with demand covariates. First, in Section 5.1 we demonstrate, on synthetic data, performance and dynamics of GILS with demand covariates. Then in Section 5.2 we consider the case of dynamic pricing without covariates and demonstrate the value of irrelevant covariates (i.e., the astrology reports setting) using synthetic data. Finally, as a robustness check we look at performance of GILS on real data from hotel bookings were the assumptions on distribution demand covariates fail.

5.1 Performance of GILS with demand covariates

We generate data by considering the following parameters: , , , , , and . For the demand covariates, we assume there are 10 relevant covariates (), and each of them is independently drawn from uniform distribution on interval where . The true coefficient of demand covariates is taken to be . This means the total variance of all demand covariates would be . Finally, we set the bound of the parameter as . Recall that will be used in truncating ’s.

We simulate GILS policy for periods and record the results. Then we repeat the simulation 50 times and present the average performance as well as its 95% confidence interval, shown via a shaded region, for several metrics as described below.

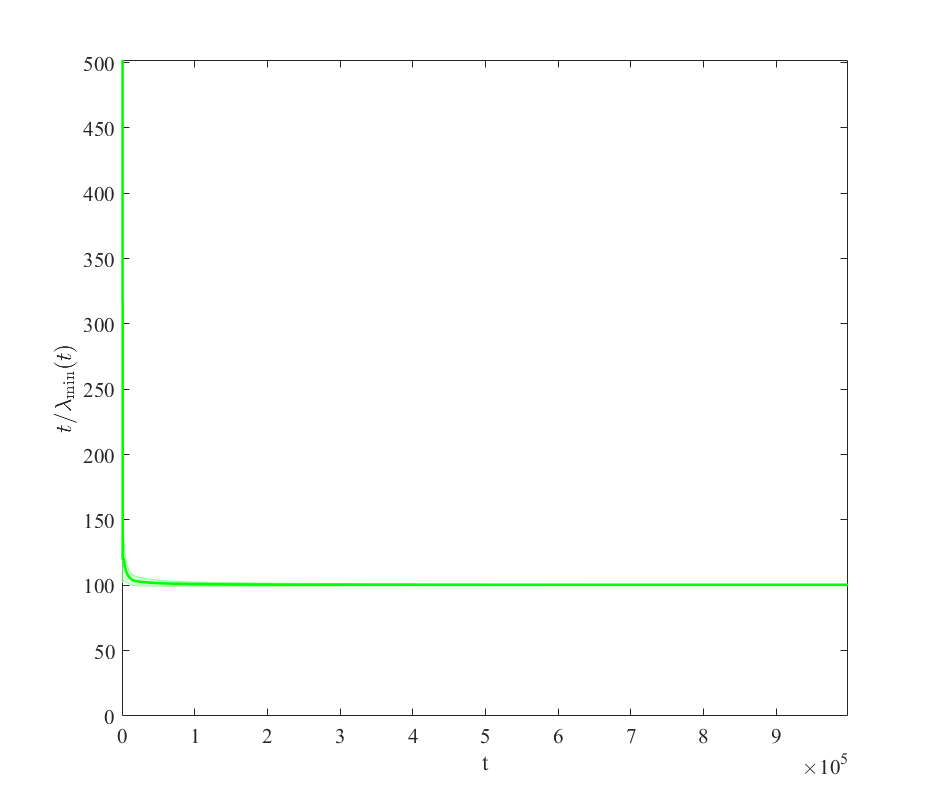

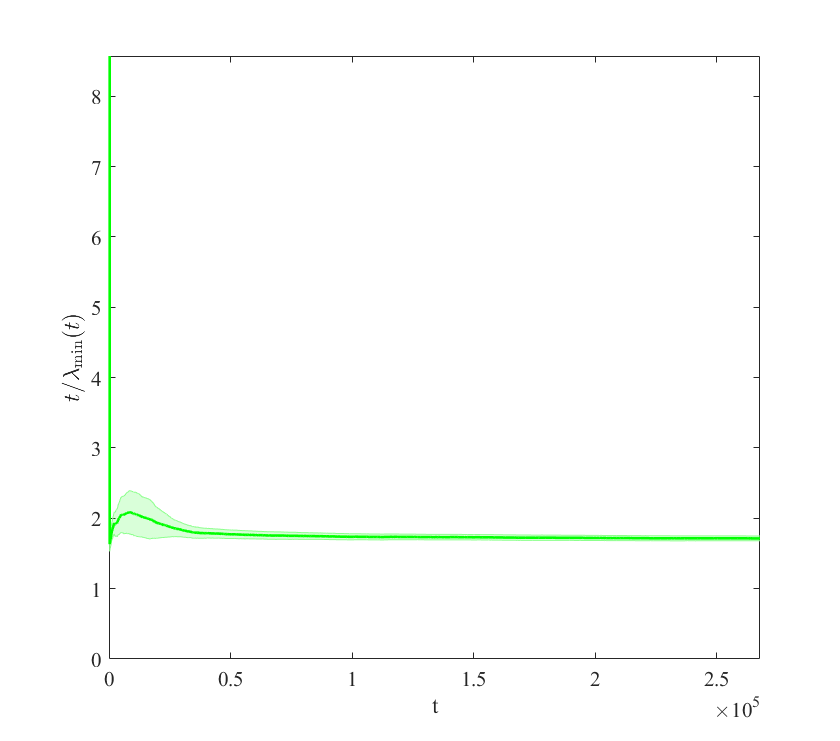

Figure 1 shows the re-scaled minimum eigenvalue of the matrix over the total horizon. If refers to the time period (), the figure shows that is asymptotically bounded near a constant ( here). This means that grows linearly with time periods. Proving this fact rigorously is the main part of our proofs for Theorems 4.3.

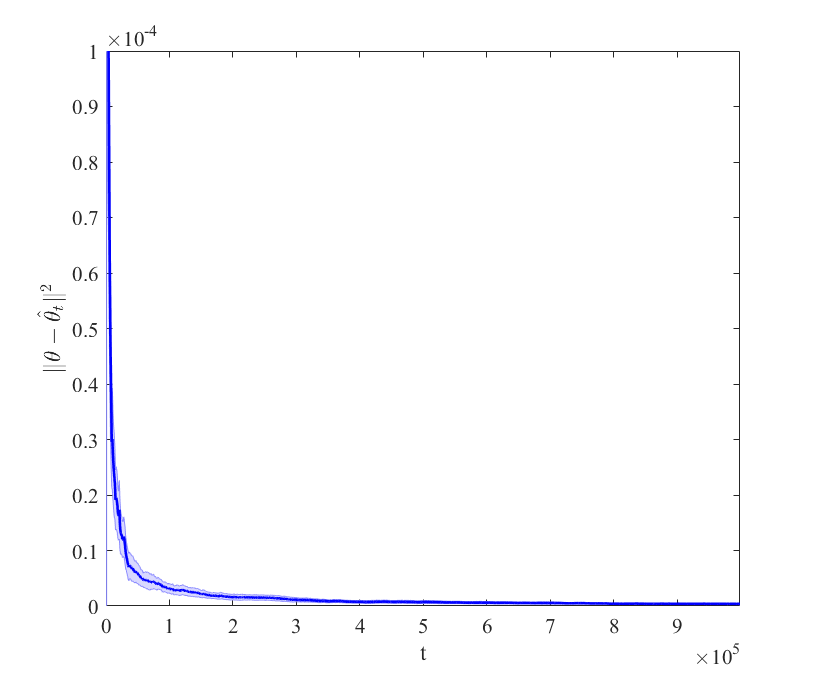

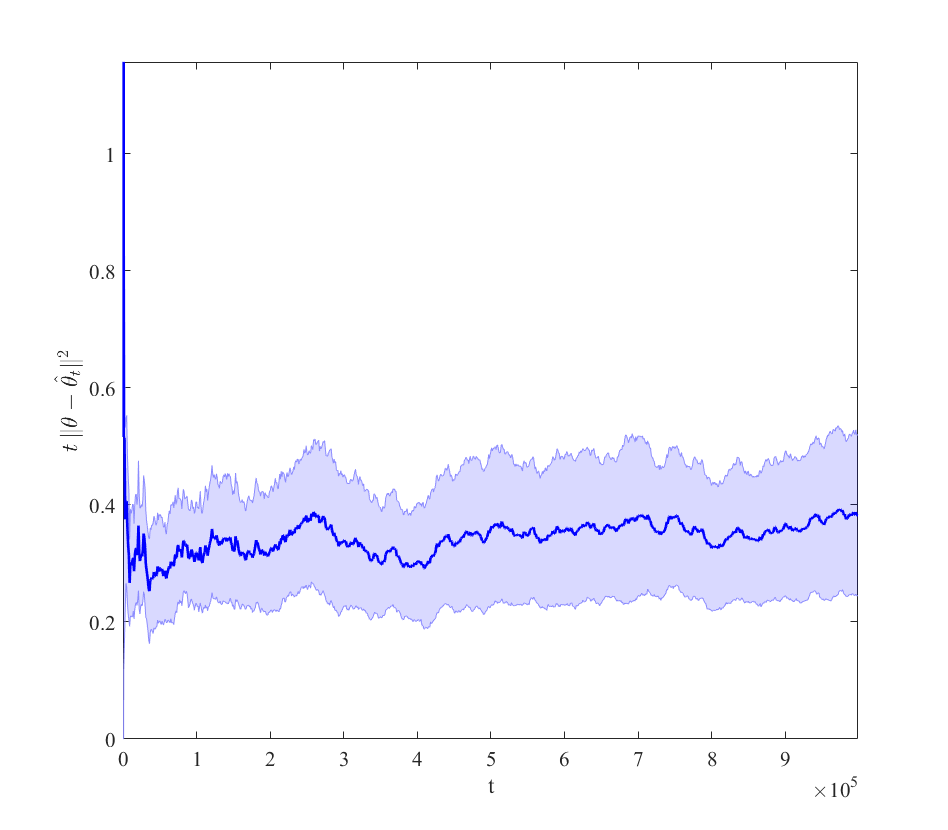

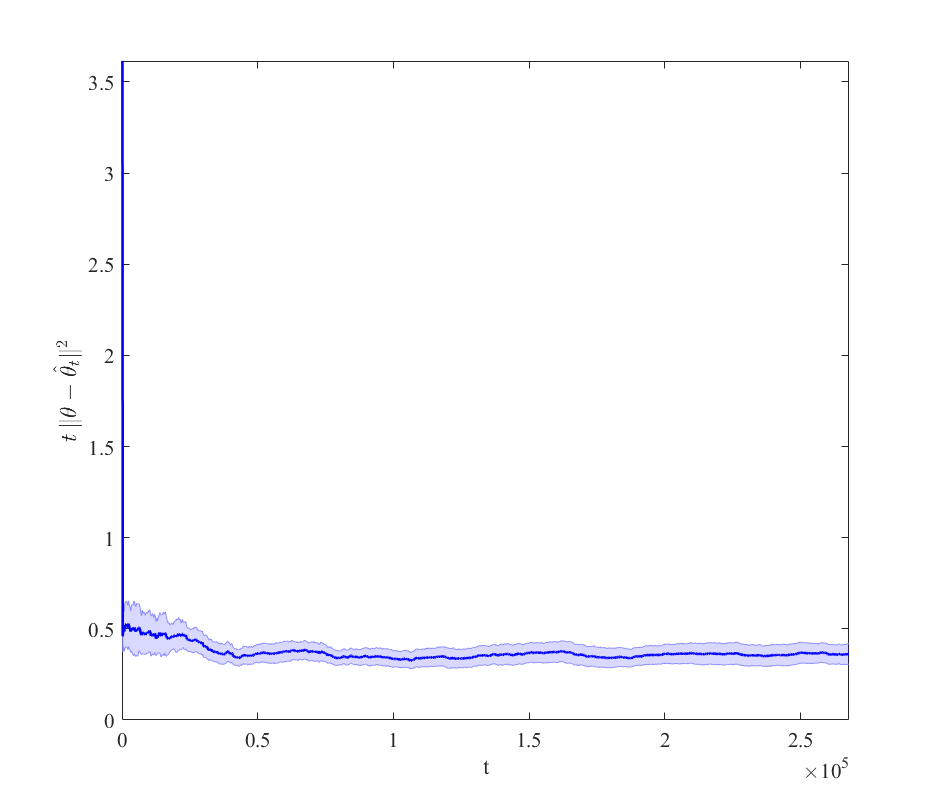

Figure 2 shows the estimation error of the parameter vector . The left plot shows that the error converges to zero. We re-scaled the error by the time period parameter in the right plot, and fluctuates but stays bounded which means that converges to zero with the rate .

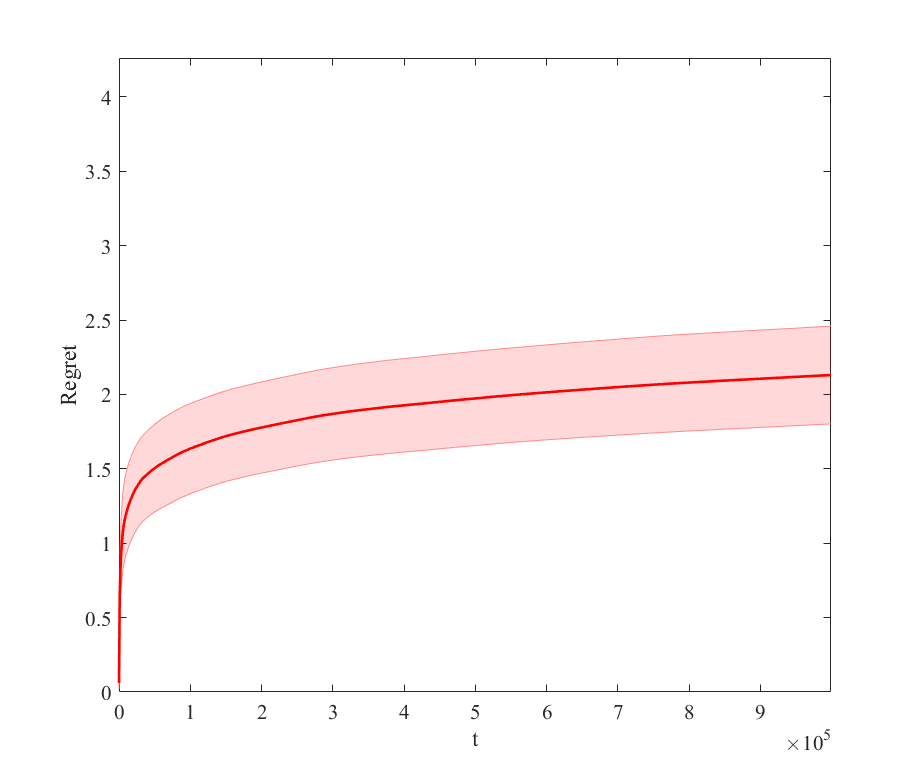

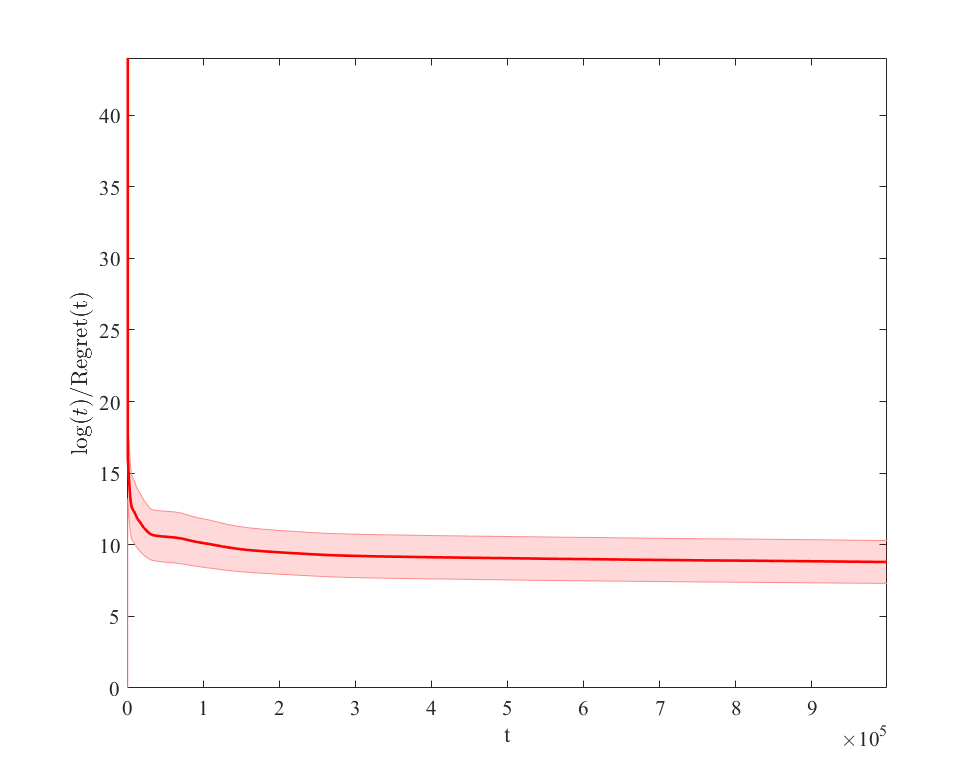

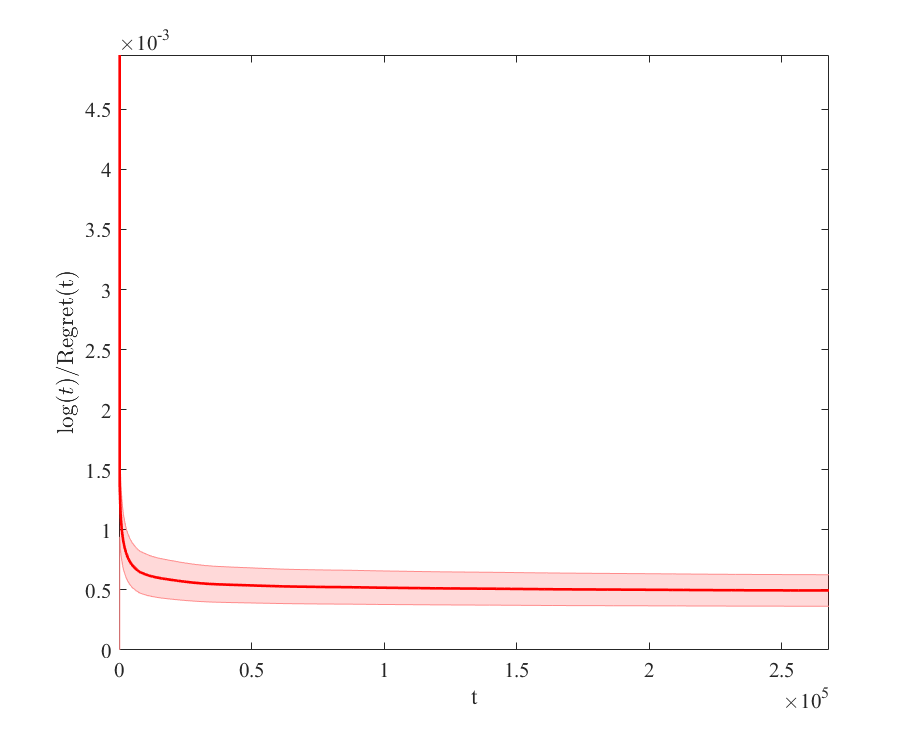

Figure 3 shows dynamics of the accumulated regret over the periods. The left plot shows the logarithmic growth of the regret. To see this better, re-scaling the regret to /Regret() in the right plot, we see that the curve has a positive lower bounded which means the accumulated regret has a growth of order .

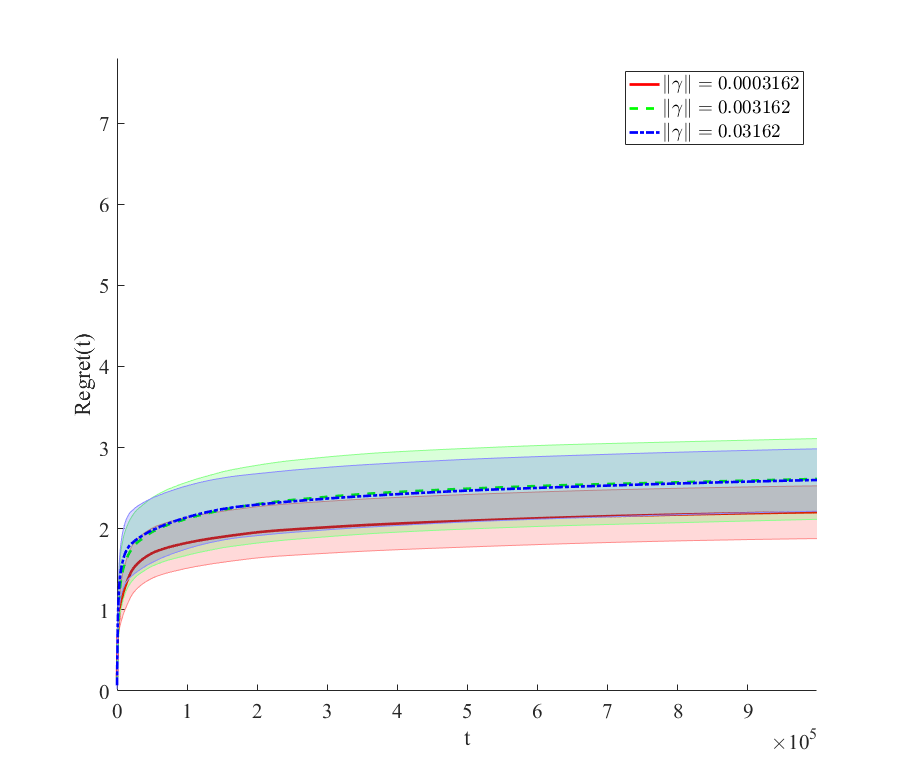

Figure 4 shows regret of GILS when the effect of demand covariates is varied. In particular, by choosing the parameter from the set

and keeping all the other parameters as before. We see that when the demand covariates have higher predictive power (larger ) the performance is better.

5.2 Performance of GILS with astrology reports

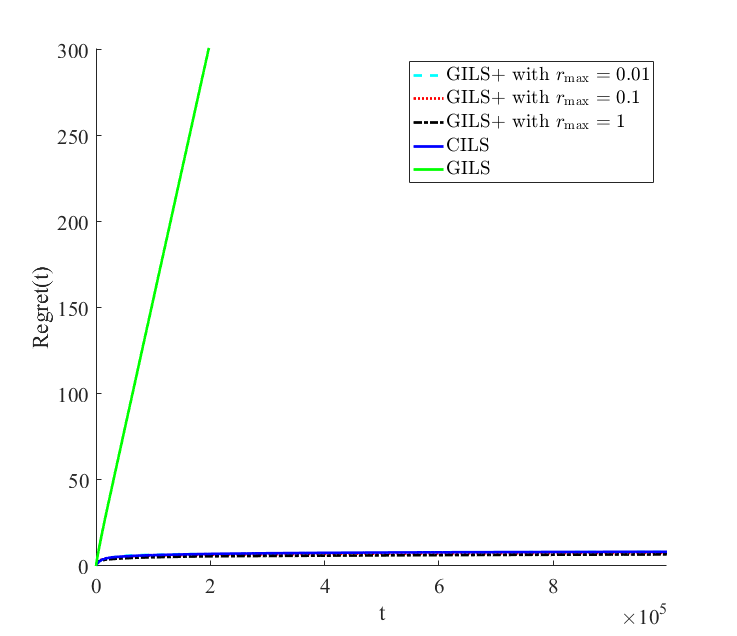

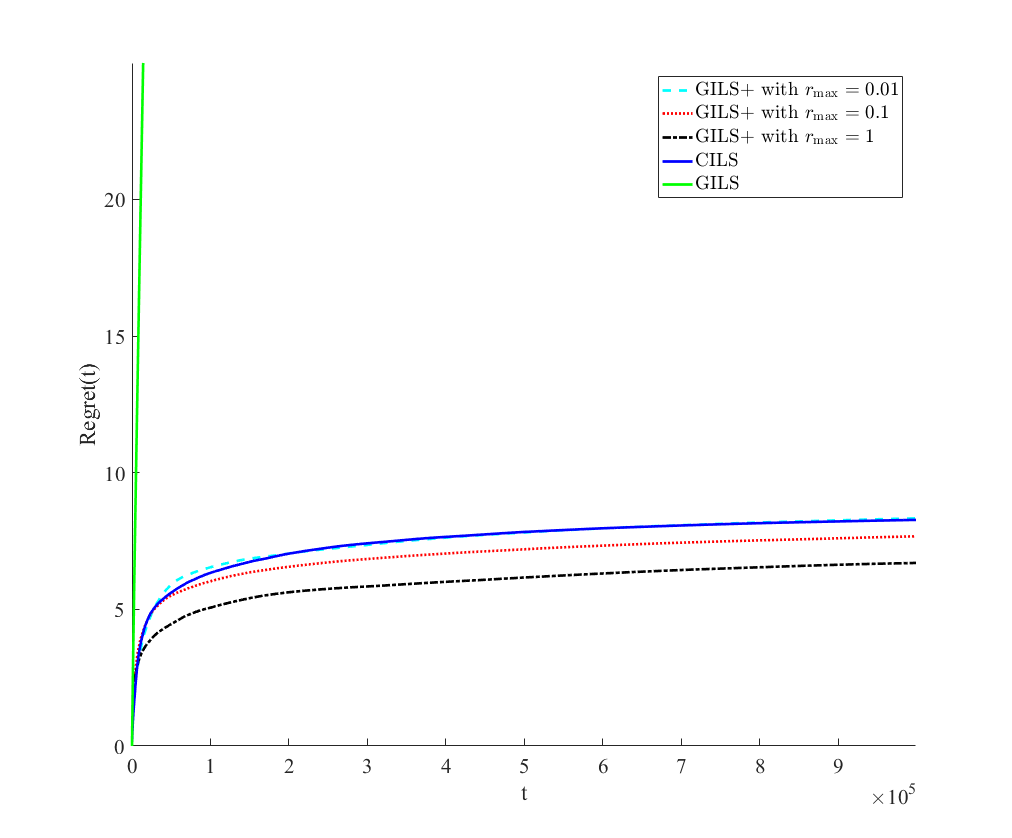

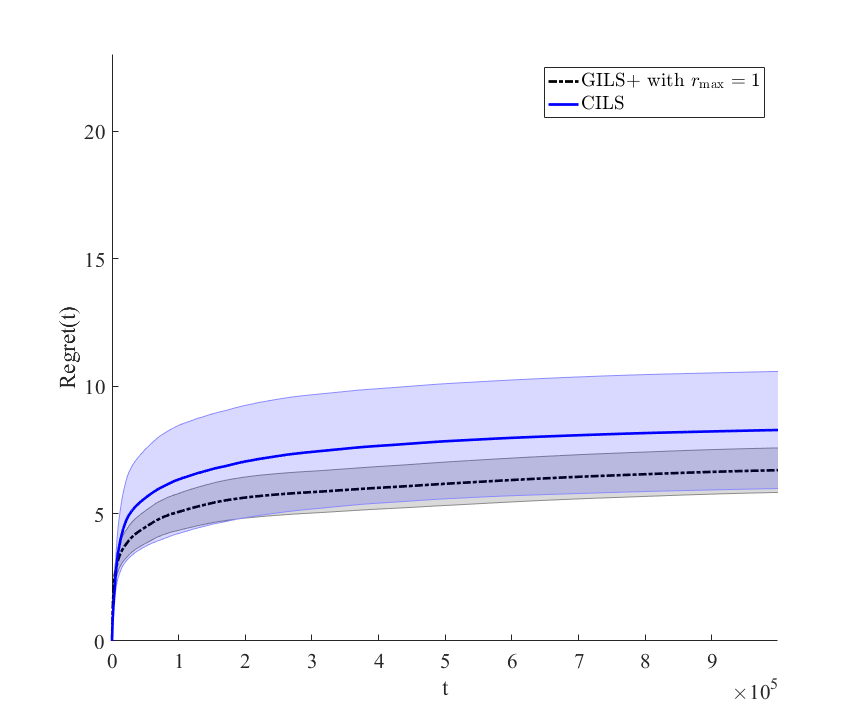

In this section, we consider the dynamic pricing problem (with incumbent price) studied by Keskin and Zeevi (2014) when there are no demand covariates. We will empirically show that “astrology reports” (irrelevant demand covariates) fix the incomplete learning problem of GILS. We also simulate the base version of GILS (the one without covariates) for comparison. To avoid confusion, we denote GILS with astrology report by GILS+.

We use the same parameters as in (Keskin and Zeevi 2014) that is , , , , , and the parameter of CILS is set to . We consider a single demand covariate (astrology report variable), drawn randomly from the same uniform distribution as in Section 5.1 and varying . Each algorithm is simulated 50 times up to time and average regret (across 50 simulations) is plotted versus time. The results are shown in Figure 5. Note that in subfigures (a) and (b) we do not show 95% confidence regions to reduce the clutter on the graphs since most algorithms have very comparable performance. Figures 5(a)-(b) represent the same result with two different scaling of the -axis. From Figure 5(a) it is clear that GILS is the worst policy with a regret that grows linearly in time. After re-scaling the -axis, in Figure 5(b), we can see that GILS+ has a fundamentally different behavior than GILS, irrespective of the order of and it seem to marginally outperform CILS. However, in Figure 5(c), comparing CILS and even the best GILS+ by depicting the 95% confidence region across the 50 simulations we see that the observed difference is not statistically significant.

5.3 Results on Hotel Bookings Data

The objective of this section is to test robustness of our main result, demand covariates fix the incomplete learning problem of GILS, by using real data from hotel bookings on Expedia (a large online travel agency). Although we are not considering some important aspects of the real-life dynamic pricing such as inventory constraints, our goal is to provide complementary simulations as in Section 5.1 where most parameters of the model are not synthetic and the distributional assumptions on demand covariates may fail.

Our data is from Expedia, Inc. which is an American-based parent company to several global online travel brands including Expedia.com, Hotels.com, Hotwire.com, Orbitz.com, and a several more travel websites. The data contains user searches and booking records for 65,000 hotels during November, 2012 to July, 2013. The data is publicly available111https://www.kaggle.com/c/expedia-personalized-sort and in addition to search and booking records, contains demand covariates such as price competitiveness, hotel characteristics, location attractiveness, aggregated statistics on purchase history of users, etc. We limited ourselves to search results that satisfied the following constraints:

-

•

User looked for one room only for one or two adults (no children).

-

•

The length of stay is one night.

-

•

The price per night for the hotel is below $1000.

-

•

The search occurred within 7 days of the booking date.

These conditions provide a more homogeneous data set by removing search results of strategic customers, complications around multi-night discounts, special requirements for travelers with a large family, or extremely expensive bookings, such that the final data matches better with our dynamic pricing problem.

We also aggregate the search results and bookings for each (day, hotel) pair as follows. The total number of booked rooms for each hotel on that day is taken as a proxy for the demand and the average displayed price is taken as a proxy for the price. We also select several demand covariates from the data. They are the Star rating of the hotel, the average Review score of the property, whether the hotel is part of a major Brand chain, hotel’s Position on search results page, whether the check-in day is a Weekend, a score for the desirability of a hotel’s Location and whether the booking date is in Summer season. This led to our final data set with rows of (day,hotel) pairs. Table 1 demonstrates samples from the final data set with the demand covariates. However, for our simulation we will standardize all covariates to have mean a and and variance of .

| Demand Covariates | ||||||||

| Demand | Price ($) | Star | Review | Brand | Position | Weekend | Location | Summer |

| 2 | 144 | 4 | 3.5 | 1 | 15 | 0 | 0.0058 | 1 |

| 2 | 95 | 3 | 4 | 1 | 29 | 0 | 0.0157 | 1 |

| 3 | 182.16 | 4 | 4.5 | 1 | 14 | 0 | 0.28724 | 0 |

| 3 | 68 | 2 | 4 | 0 | 16.3 | 1 | 0.0667 | 0 |

| 3 | 154 | 4 | 4 | 1 | 9.75 | 1 | 0.1249 | 1 |

| 0 | 146.3 | 3 | 4 | 0 | 15.25 | 0 | 0.0414 | 1 |

| ⋮ | ⋮ | ⋮ | ⋮ | ⋮ | ⋮ | ⋮ | ⋮ | ⋮ |

The data also contains average historical price for all these hotels prior to November, 2012 () that we use as incumbent price. That is .

To obtain the true parameters of the demand model, known to a clairvoyant seller, we use a linear regression on all rows. The result is shown below.

where all coefficients are statistically significant with p values less than . After estimating the true parameters, in order to simulate a pricing policy, we will ignore the columns Demand and Price and only focus on the (standardized) demand covariates. For each of the 50 simulation runs, we randomly permute rows of the data and assume they are sequentially realized over time. Then GILS will dynamically adjust the price according to the demand covariates, and estimates the parameter vector . At each time period, we use the true parameters from Eq. (5.3) to calculate the realized demand for the price (suggested by GILS). Similarly, we can calculate the optimal price for that realization of demand covariates via the true parameters and hence can calculate the regret of that time period.

Finally, we measure the accumulated regret up to time period that all samples are observed. We repeat the simulation 50 times (each time with a different random permutation of the rows) to obtain the average and a 95% confidence region around the average for the , , and . We note that since a random permutation of the same data set is used each time, the 50 samples are not independent and hence the provided confidence regions are not correct 95% intervals. We only plot them as a rough measure of statistical fluctuations. Other parameters in the model are , and . Note that these values are selected very conservatively which leads to a very large range of parameters . This choice is done to demonstrate robustness of the results, but in practice one can use domain knowledge or prior data to choose a smaller region.

Results are shown in Figure 6; shows that has a constant upper bound, (b) illustrates that is asymptotically strictly positive i.e., the regret grows by a constant times , and (c) shows that has a constant upper bound. All of these are in-sync with simulation results of Section 5.1 as well as our theoretical results even though most of the assumptions of the model are not satisfied. For example, the assumption on distribution of demand covariates is not guaranteed or condition (8) does not hold. This demonstrates robustness of the results.

6 Conclusions and Discussion

This paper considers a dynamic pricing problem when the demand function is unknown. The firm leverages extra information – demand covariates – to determine the price in each period, in order to maximize cumulative revenue over time. A popular approach in practice for this problem is GILS that focuses only on mazimizing the revenue and ignores learning of the demand function. But it has been shown theoretically and empirically that GILS has a suboptimal performance when the demand function does not contain demand covariates. In this paper, we proved that GILS is asymptotically optimal when there are demand covariates. This result holds even when the predictive power of the demand covariates becomes negligible. An interesting corollary of this result is that, when the demand covariates have no predictive power, including them in GILS will fix the incomplete learning problem of GILS and help it achieve the asymptotically optimal performance. The results are shown to be robust using simulations on synthetic and real data sets, in particular in situations where our modeling assumptions fail.

The phenomena that demand covariates assist GILS to achieve the asymptotic optimal performance can be extended in several ways. First, while the linear demand model is well accepted in the economics literature and revenue management practice, it is too simple and restrictive. Therefore, extending the results to the cases with a more complex demand model with covariates is a promising future research direction. Examples would include generalized linear demand models, as studied by den Boer and Zwart (2014), or models with more general dependence on demand covariates. Second, this paper focuses on the simple case that firm only sells one type of products. We expect generalizations to the cases with multiple products, as in (Keskin and Zeevi 2014, den Boer 2014), to be valid and plan to pursue them. Third, the interesting phenomena that disturbances obtained from the demand covariates save the greedy policy from converging to a local (wrong) optimal point, is an intriguing direction to study in other sequential decision making problems.

The authors are grateful to Michael J. Harrison for encouragements and insightful discussions throughout this study and to Yonatan Gur, Dan Iancu, and Stefanos Zenios for guidance and suggestions.

In addition, M. Bayati acknowledges the support of NSF awards CCF:1216011 and CMMI:1451037.

7 Proofs

7.1 Proof of Theorem 4.1

Proof 7.1

To obtain the lower bound on the regret, we build upon the result of Keskin and Zeevi (2014). Our argument is by contradiction. Assume the contrary, that there is a realized sequence of demand covariates and a special policy where for each , with , and is such that for any there exist a with

| (20) |

Now using the fact that , the inequality (20) would mean that for all ,

| (21) |

Now, we consider a very special case of , i.e., , and the new parameter is . In this case, the demand does not rely on demand covariates any more, that is,

Therefore, if we consider the dynamic pricing problem without demand covariates and with the unknown parameter then the policy , even though it may use the irrelevant information provided by the covariates, is a feasible policy for this problem. Thus, we have the regret of the dynamic pricing problem without demand covariates satisfying

for any and any where is projection of to its first coordinate (the coordinate corresponding to the coefficient of price). This means we have

for any constant . But, the above statement contradicts Theorem 3 in (Keskin and Zeevi 2014), where they show that there is a positive constant such that for all feasible policies for the dynamic pricing problem without demand covariates () and for all ,

| (22) |

This finishes our proof of Theorem 4.1.

7.2 Proof of Theorem 4.3

Proof 7.2

First, we notice that can be written as below:

| (23) |

Here is bounded, and recall that the expectations and are with respect to the randomness of and respectively. In order to prove an upper bound on the regret, we provide an upper bound on each term separately, and then sum them up. Also, for simplicity, throughout this proof we will use a single expectation notation to refer to both expectations. We also fix the policy to be the greedy policy and assume the parameter is fixed.

Second, note that the revenue loss of the greedy policy is due to the least squares estimation errors. To see this we note that the expected value of squared pricing error in period is given by

| (24) |

where is the truncated least squares estimate calculated at the end of period . Further, denoting the coordinates of by , we can bound the expectation (only with respect to ) of squared price deviation by

| (25) |

where . Also, recall that is the history without the current demand covariates . Thus, and are determined (measurable) with respect to , while is a random variable with , . Next, we will find upper bounds for the right hand side of Eq. (25). In particular, using

and

we have

| (26) |

where

Since , and is projection of onto , we have . Therefore, we will try to find an upper bound for . To do this, we express the estimation error in terms of the error vector and according to equation (16). In particular,

| (27) | |||||

where is the minimum eigenvalue of the matrix . The last inequality is a consequence of

| (28) |

where matrix inequality means is positive semi-definite.

Since and , we have

| (29) |

Next, we will prove a lower bound for using the following variant of matrix Chernoff inequality for adapted sequences from Tropp (2011).

Theorem 7.3 (Theorem 3.1 in (Tropp 2011))

Let be a probability space. Consider a finite sequence of positive-semidefinite matrices with dimension that is adapted to a filtration , i.e.

Now suppose that

almost surely. Then, for all and all ,

In order to apply Theorem 7.3 we need to define the filtration and the adapted sequence. Let and, for , let be the sigma algebra generated by random variables and let . Then we have, for all

where we introduced two new variables

Next we state the following result on the minimum eigenvalue of .

Lemma 7.4

We have where

Applying Lemma 7.4, we have that

| (30) |

and we note that, the maximum eigenvalue of each matrix is upper bounded by a constant uniformly,

| (31) | |||||

Now, combining Eqs. (30) and (31) with the fact that each matrix is positive semi-definite we can use Theorem 7.3 with and obtain

| (32) | |||||

Now, we have enough tools to finalize proof of Theorem 4.3. First we recall from Eq. (26) that the expected price deviation at time is upper bounded by and that . We also use the fact that and belong to to get the bound

Combining all of these we have,

| (33) | |||||

Next, we notice that for any , is independent of , and , thus is independent of . With and , we have

| (34) | |||||

Thus, we see that

| (35) | |||||

Summing up both sides of Eq. (35), we get

| (36) |

in which the summation is upper bounded by the integral . This finishes the proof of upper bound on the regret. We can also see that the constant in is at most

where we used the fact that diagonal entries of are which means its trace is .

7.2.1 Proof of Lemma 7.4

Our proof strategy is to show that for any vector the following holds

| (37) |

To simplify the notation we will drop sub-indices , , and . Next we write where and which gives

| (38) |

Combining (38) with the following inequality

we obtain

which finishes the proof.

8 Extensions

8.1 Extension to non-iid covariates and shocks

In this section we show that our assumptions on the demand covariates and demand shocks can be generalized.

Demand shocks.

The only assumptions required on the sequence for our proof to go through are that, for all ,

-

1.

is independent of , , and .

-

2.

.

-

3.

There is a finite constant such that .

In particular, does not need to be an iid sequence and can be for example a martingale difference sequence with respect to and with finite conditional variance.

Demand covariates.

Similarly, the only assumptions required on the sequence for our proof to go through are that, for all ,

-

1.

.

-

2.

where the sequence of covariance matrices are all positive definite with minimum eigenvalues that are uniformly bounded (from below) away from and maximum eigenvalues that are uniformly bounded from above.

References

- den Boer and Zwart (2014) Arnoud V. den Boer and Bert Zwart. Simultaneously learning and optimizing using controlled variance pricing. Management Science, 60(3):770–783, 2014.

- Keskin and Zeevi (2014) N Bora Keskin and Assaf Zeevi. Dynamic pricing with an unknown demand model: Asymptotically optimal semi-myopic policies. Operations Research, 62:1142–1167, 2014.

- Tropp (2011) Joel A Tropp. User-friendly tail bounds for matrix martingales. Technical report, DTIC Document, 2011.

- Lai and Robbins (1979) T L_ Lai and Herbert Robbins. Adaptive design and stochastic approximation. The annals of Statistics, pages 1196–1221, 1979.

- Lai and Robbins (1985) Tze Leung Lai and Herbert Robbins. Asymptotically efficient adaptive allocation rules. Advances in applied mathematics, 6(1):4–22, 1985.

- Auer et al. (2002) Peter Auer, Nicolo Cesa-Bianchi, Yoav Freund, and Robert E Schapire. The nonstochastic multiarmed bandit problem. SIAM Journal on Computing, 32(1):48–77, 2002.

- Auer (2003) Peter Auer. Using confidence bounds for exploitation-exploration trade-offs. The Journal of Machine Learning Research, 3:397–422, 2003.

- Segal (2003) Ilya Segal. Optimal pricing mechanisms with unknown demand. The American economic review, 93(3):509–529, 2003.

- Kreps and Francetich (2014) David M. Kreps and Alejandro Francetich. Choosing a good toolkit: An essay in behavioral economics. Preprint, 2014.

- Kleinberg and Leighton (2003) Robert Kleinberg and Tom Leighton. The value of knowing a demand curve: Bounds on regret for online posted-price auctions. In Foundations of Computer Science, 2003. Proceedings. 44th Annual IEEE Symposium on, pages 594–605. IEEE, 2003.

- Carvalho and Puterman (2005) Alexandre X Carvalho and Martin L Puterman. Learning and pricing in an internet environment with binomial demands. Journal of Revenue and Pricing Management, 3(4):320–336, 2005.

- Araman and Caldentey (2009) Victor F. Araman and René Caldentey. Dynamic pricing for nonperishable products with demand learning. Operations Research, 57(5):1169–1188, 2009.

- Besbes and Zeevi (2009) Omar Besbes and Assaf Zeevi. Dynamic pricing without knowing the demand function: Risk bounds and near-optimal algorithms. Operations Research, 57(6):1407–1420, 2009.

- Besbes and Zeevi (2011) Omar Besbes and Assaf Zeevi. On the minimax complexity of pricing in a changing environment. Operations research, 59(1):66–79, 2011.

- Harrison et al. (2012) J Michael Harrison, N Bora Keskin, and Assaf Zeevi. Bayesian dynamic pricing policies: Learning and earning under a binary prior distribution. Management Science, 58(3):570–586, 2012.

- Johnson et al. (2015) Kris Johnson, David Simchi-Levi, and He Wang. Online network revenue management using thompson sampling. Available at SSRN, 2015.

- Chen et al. (2015) Boxiao Chen, Xiuli Chao, and Cong Shi. Nonparametric algorithms for joint pricing and inventorycontrol with lost-sales and censored demand, 2015. manuscript.

- den Boer (2015a) Arnoud V. den Boer. Dynamic pricing and learning: historical origins, current research, and new directions. Surveys in operations research and management science, 20(1):1–18, 2015a.

- Lai and Robbins (1982) TL Lai and Herbert Robbins. Iterated least squares in multiperiod control. Advances in Applied Mathematics, 3(1):50–73, 1982.

- Chen and Hu (1998) Kani Chen and Inchi Hu. On consistency of bayes estimates in a certainty equivalence adaptive system. IEEE Transactions on Automatic Control, 43(7):943–947, 1998.

- den Boer (2015b) Arnoud V. den Boer. Tracking the market: dynamic pricing and learning in a changing environment. European journal of operational research, 247(3):914–927, 2015b.

- Keskin and Zeevi (2013) N Bora Keskin and Assaf Zeevi. Chasing demand: Learning and earning in a changing environment. 2013. Preprint, SSRN 2389750.

- Woodroofe (1979) Michael Woodroofe. A one-armed bandit problem with a concomitant variable. Journal of the American Statistical Association, 74(368):799–806, 1979.

- Sarkar (1991) Jyotirmoy Sarkar. One-armed bandit problems with covariates. The Annals of Statistics, pages 1978–2002, 1991.

- Langford and Zhang (2007) John Langford and Tong Zhang. The epoch-greedy algorithm for contextual multi-armed bandits. Advances in neural information processing systems, 20:1096–1103, 2007.

- Dudik et al. (2011) Miroslav Dudik, Daniel Hsu, Satyen Kale, Nikos Karampatziakis, John Langford, Lev Reyzin, and Tong Zhang. Efficient optimal learning for contextual bandits. arXiv preprint arXiv:1106.2369, 2011.

- Chu et al. (2011) Wei Chu, Lihong Li, Lev Reyzin, and Robert E Schapire. Contextual bandits with linear payoff functions. In International Conference on Artificial Intelligence and Statistics, pages 208–214, 2011.

- Seldin et al. (2011) Yevgeny Seldin, Peter Auer, John S Shawe-taylor, Ronald Ortner, and François Laviolette. Pac-bayesian analysis of contextual bandits. In Advances in Neural Information Processing Systems, pages 1683–1691, 2011.

- Li et al. (2014) Lihong Li, Wei Chu, John Langford, and Robert Schapire. Contextual-bandit approach to personalized news article recommendation, August 25 2014. US Patent App. 14/468,130.

- Badanidiyuru et al. (2014) Ashwinkumar Badanidiyuru, John Langford, and Aleksandrs Slivkins. Resourceful contextual bandits. arXiv preprint arXiv:1402.6779, 2014.

- Goldenshluger and Zeevi (2007) Alexander Goldenshluger and Assaf Zeevi. Performance limitations in bandit problems with side observations. Technical report, Citeseer, 2007.

- Goldenshluger and Zeevi (2011) Alexander Goldenshluger and Assaf Zeevi. A note on performance limitations in bandit problems with side information. Information Theory, IEEE Transactions on, 57(3):1707–1713, 2011.

- Goldenshluger and Zeevi (2013) Alexander Goldenshluger and Assaf Zeevi. A linear response bandit problem. Stochastic Systems, 3(1):230–261, 2013.

- Rigollet and Zeevi (2010) Philippe Rigollet and Assaf Zeevi. Nonparametric bandits with covariates. arXiv preprint arXiv:1003.1630, 2010.

- Perchet et al. (2013) Vianney Perchet, Philippe Rigollet, et al. The multi-armed bandit problem with covariates. The Annals of Statistics, 41(2):693–721, 2013.

- Bastani and Bayati (2015) Hamsa Bastani and Mohsen Bayati. Online decision-making with high-dimensional covariates. Preprint, available at SSRN: http://ssrn.com/abstract=2661896, 2015.

- Liyanage and Shanthikumar (2005) Liwan H. Liyanage and J.George Shanthikumar. A practical inventory control policy using operational statistics. Oper. Res. Lett., 33(4):341–348, 2005.

- Levi et al. (2015) Retsef Levi, Georgia Perakis, and Joline Uichanco. The data-driven newsvendor problem: New bounds and insights. Operations Research, 63(6):1294–1306, 2015.

- Rudin and Vahn (2014) Cynthia Rudin and Gah-Yi Vahn. The big data newsvendor: Practical insights from machine learning. Preprint, SSRN 2559116, 2014.

- Bertsimas and Kallus (2015) Dimitris Bertsimas and Nathan Kallus. From predictive to prescriptive analytics. Preprint, 2015.

- Cohen et al. (2016) Maxime C. Cohen, Ilan Lobel, and Renato Paes Leme. Feature-based dynamic pricing. Preprint, SSRN 2737045, 2016.

- Amin et al. (2014) Kareem Amin, Afshin Rostamizadeh, and Umar Syed. Repeated contextual auctions with strategic buyers. In Advances in Neural Information Processing Systems (NIPS), pages 622–630. 2014.

- Billingsley (1979) P. Billingsley. Probability and measure. Wiley series in probability and mathematical statistics. Probability and mathematical statistics. Wiley, 1979.

- Broder and Rusmevichientong (2012) Josef Broder and Paat Rusmevichientong. Dynamic pricing under a general parametric choice model. Operations Research, 60(4):965–980, 2012.

- den Boer (2014) Arnoud V. den Boer. Dynamic pricing with multiple products and partially specified demand distribution. Mathematics of Operations Research, 39(3):863–888, 2014.