Distribution-Constrained Optimal Stopping

Abstract

We solve the problem of optimal stopping of a Brownian motion subject to the constraint that the stopping time’s distribution is a given measure consisting of finitely-many atoms. In particular, we show that this problem can be converted to a finite sequence of state-constrained optimal control problems with additional states corresponding to the conditional probability of stopping at each possible terminal time. The proof of this correspondence relies on a new variation of the dynamic programming principle for state-constrained problems which avoids measurable selections. We emphasize that distribution constraints lead to novel and interesting mathematical problems on their own, but also demonstrate an application in mathematical finance to model-free superhedging with an outlook on volatility.

Key words. Optimal stopping, distribution constraints, optimal control, state constraints, robust hedging with a volatility outlook.

AMS subject classifications. 60G40, 93E20, 91G80.

1 Introduction

In this paper we consider the problem of choosing an optimal stopping time for a Brownian motion when constrained in the choice of distribution for the stopping time. While standard optimal stopping theory has focused primarily on unconstrained finite- and infinite-horizon stopping times (e.g. [22, 25]) and very recently on constraints on the first moment of the stopping time (e.g. [18, 21, 1]), there is a very limited literature on the problem of optimal stopping under distribution constraints.

It turns out that distribution-constrained optimal stopping is a difficult problem, with stopping strategies depending path-wise on the Brownian motion in general. This is to be expected because a constraint on the stopping time’s distribution forces the stopper to consider what he would have done along all other paths of the Brownian motion when deciding whether to stop. The main task at hand is to identify relevant state variables and then transform the problem so that it can be analyzed by standard methods.

In this article we illustrate a solution in the special case that the target distribution consists of finitely-many atoms. Our approach consists of iterated stochastic control problems wherein we introduce controlled processes representing the conditional distribution of the stopping time. We then characterize the value function of the distribution-constrained optimal stopping problem in terms of the value functions of a finite number of state-constrained optimal control problems. This dynamic approach to the problem in terms of a controlled process with unbounded diffusion is similar in flavour to recent results in non-linear optimal stopping [18] and control of measure-valued martingales in [10].

The key mathematical contributions of this paper lie in our proof of a dynamic programming principle relating each of the sequential optimal control problems. We provide an argument which avoids the use of measurable selections, similar to the proofs of weak dynamic programming principles in [7, 6, 3]. However, we deal with state-constraints in a novel way which relies on some a priori regularity of the value functions.

While the problem of distribution-constrained optimal stopping is mathematically-interesting in its own right, we emphasize that there is room for applications in mathematical finance and optimal control theory. For instance, we demonstrate an application to model-free superhedging of financial derivatives when one has an outlook on the quadratic variation of an asset price. Here, the distribution on the quadratic variation corresponds to that of a stopping time by the martingale time-change methods utilized recently in [5, 14]. Furthermore, the problem of optimal stopping under moment constraints on the stopping time reduces to the distribution-constrained optimal stopping problem in cases where there exists a unique atomic representing measure in the truncated moment problem (e.g. [11, 17]). There also appears to be a connection between distribution-constrained optimal stopping and inverse first passage-time problems (e.g. [27, 9]). We should also mention that after the publication of our preprint, [4] gave geometric descriptions of optimal stopping times using optimal transport theory.

This paper proceeds as follows. In Section 2, we provide our solution to distribution-constrained optimal stopping of Brownian motion. In particular, we characterize the solution via a finite sequence of iterated state-constrained stochastic control problems. The main result is provided by an induction argument in Theorem 1, but the heart of the argument lies mainly in the proofs of Lemma 3 and Lemma 4. We also provide a time-dependent versions of these results, which can be characterized as the viscosity solutions of associated HJB equations. The key arguments here lie in a Dynamic Programming Principle in Theorem 2. In Section 3, we demonstrate an application to model-free superhedging with an outlook on volatility. We convert this problem into a distribution-constrained optimal stopping problem where the volatility outlook corresponds to a distribution constraint for the stopping time. We demonstrate numerical results which provide some intuition for the behavior of the optimal stopping strategies. Finally, we provide complete proofs of our main results in Appendices A–D.

2 Main Results

2.1 Problem formulation

We consider a probability space supporting a standard Brownian motion . We take to be the natural filtration of augmented to satisfy the usual properties. We consider a given payoff function which is assumed to be Lipschitz continuous. We also use the notation

for any and .

In this paper, we are also given a target distribution , which is supported on and assumed to consist of finitely-many atoms. Without loss of generality, we assume the following representation

| (2.1) |

where , , , and . We also introduce the convenient notation for each .

The distribution-constrained optimal stopping problem we consider is

| (2.2) |

where we take to be the collection of all finite-valued -stopping times which are independent of . We let be some fixed starting value. That is, we choose a stopping time whose distribution is equal to in order to maximize the expected payoff of a stopped Brownian motion starting at .

2.2 Construction of distribution-constrained stopping times

There are multiple ways to naturally represent a stopping time satisfying a distribution constraint. In this section, we outline two particular such representations and illustrate how they immediately lead to constructions of such stopping times.

We first provide a characterization of distribution-constrained stopping times in terms of a partitioning of the path space into regions with specified measures. Later, we make a connection with controlled processes.

Lemma 1.

A stopping time has the distribution if and only if it is of the following form

almost-surely, where partition and, for each , is -measurable with .

Proof.

It is clear from the construction that such a is a -stopping time and . The converse follows by taking a stopping time such that and defining the sets for each .

∎

With this in mind, we can immediately explicitly construct a stopping time with given distribution.

Corollary 1.

There exists a stopping time such that .

Proof.

Define a partition of as

where is the cumulative distribution function of the standard normal distribution. It is clear that is -measurable with for each . Then, by Lemma 1, defines a stopping time with . ∎

The proof above constructs a stopping time which roughly stops when there are events in the left-tail of a distribution. However, one could easily modify the construction to stop in right-tail events, events near the median, or on the image of any Borel set of appropriate measure under .

While this construction may suggest converting the distribution-constrained optimal stopping problem into optimization over Borel sets of specified measure, we emphasize next that there is no reason to expect the stopping times to be measurable with respect to . In particular, in the next example, we show a construction of a distribution-constrained stopping time which is entirely path-dependent.

Corollary 2.

There exists a stopping time , independent of , satisfying .

Proof.

Define a sequence of random variables as

for each . Then each is the absolute maximum of a Brownian bridge over , scaled by the length of the time interval. In particular, each is -measurable, independent of , and equal in distribution to the absolute maximum of a standard Brownian bridge on , the cumulative distribution function of which we denote by .

Define a partition of as

It is clear that is -measurable with for each . Then, by Lemma 1, defines a stopping time with which is independent of . ∎

Clearly, the stopping time constructed above is an admissible stopping time in the distribution-constrained optimal stopping problem, but there is no hope to express it in terms of the value of the Brownian motion at each potential time to stop. While stopping times involving the Brownian bridge may seem unnatural at first, their use is a key idea in the proofs of Lemma 3 and Lemma 4.

Another useful result obtained from Lemma 1 is the following approximation result.

Proposition 1.

Fix satisfying and . For any such that

there exists such that

which satisfies

Proof.

Step 1: By Lemma 1, there exists a partition of such that each is -measurable with and

almost-surely. The goal is to define in terms of a related partition.

We first make a key observation: for any , , and -measurable set such that , there exists a real number such that

This follows immediately from the observation that the distribution of has no atoms, and thus when conditioning on an event of non-zero probability, the conditional distribution cannot have atoms.

Step 2: Define an -measurable set as

where are chosen such that

Notice, if , then and , so is well-defined. Similarly, if , then and , so is well-defined.

It is clear that by construction. The key property, however, is that either or . From this, we can immediately compute the measure of the symmetric difference of and ,

Step 3: Now, suppose that we have constructed already. Define

Define a -measurable set as

where are chosen such that

As before, the inequalities between and imply that and are well-defined when they are needed. Furthermore, it is clear that .

In this case, the key property becomes that either

| (2.3) |

or

| (2.4) |

First, we consider the case that (2.3) holds. Because each set in is disjoint, for any , we can bound the overlap between and by the symmetric difference of and ,

Using (2.3), we can compute

Using the previous inequalities we deduce

In the case that (2.4) holds, this same inequality immediately follows.

Step 4: By induction on , we construct a disjoint partition of such that is -measurable and . Furthermore, we obtain a rough bound

By Lemma 1, there exists a stopping time of the form

Then we can immediately compute111We emphasize that the preceding inequalities are hardly sharp. An immediate question is whether a sharper approximation result, with a constant that scales favorably as , exists.

∎

The technical importance of this result is, of course, that it allows us to obtain continuity in the problem with respect to changes in the distribution constraint on the stopping times.

While we have demonstrated that a lot can be said about distribution-constrained stopping times using the representation in Lemma 1, it turns out that we can obtain a more manageable representation if we introduce extra controlled processes which represent the conditional probability of the stopping time taking on each possible value. This vector-valued stochastic process is a martingale in a probability simplex. In the next result, we make clear the connection between this process and a distribution-constrained stopping time.

In the remainder of the paper, we define to denote the collection of all progressively-measurable, square-integrable, -valued processes which are independent of . We also denote

for all , , and . When needed, we will denote the th coordinate of this vector-valued process by . We will occasionally abuse notation and leave out superscripts when they are clearly implied by the context.

We also denote by the following closed and convex set

We then can state a lemma regarding a characterization of distribution-constrained stopping times in terms of a state-constrained controlled martingale.

Lemma 2.

A stopping time has the distribution if and only if it is of the form

almost-surely, for some such that

almost-surely, for all , and

almost-surely, for each .

Proof.

Step 1: Let be a control for which , almost-surely, for all and , almost-surely, for each . Define as

It is clear from the properties above that for every and , which implies that , almost-surely. Then , but we must check that it has as its distribution.

Fix and note that

Note that up to a set of measure zero because in the set , we have as well as for some . Because is a martingale constrained to , this implies , almost-surely, which contradicts . Then, we can conclude

because and is a martingale taking values zero and one at .

Step 2: Let be a stopping time such that . Then define the -valued process as

Note that . By the Martingale Representation Theorem, there exists a control for which , almost-surely, for all . We can then check that,

so for all , almost-surely. Finally, for any , we have because is -measurable.

Define a stopping time as

and suppose that there exists a set of non-zero probability on which . Then, for some such that , the set has non-zero probability.

Suppose that . Then on and because is a martingale constrained to , it follows that on , and consequently, , which contradicts on . On the other hand, suppose that . Then on , but because this also contradicts on . We conclude , almost-surely. ∎

2.3 Solution via iterated stochastic control

It is convenient to define a sequence of sets which will be important in the remainder of the paper. For each , define

Note that each set is closed and convex and for each .

We also introduce subcollections of stopping times and controls with additional independence properties, which will be used later in proofs of the Dynamic Programming Principle. In particular, for any we define a subcollection of stopping times

and a subcollection of controls

We then define a sequence of iterated distribution-constrained optimal stopping problems.

Definition 1.

For each , define a function as

| (2.5) |

Note that . We emphasize that while each is written as a function depending on an entire tuple , we have by the definition of .

Our goal is to convert these iterated distribution-constrained optimal stopping problems into iterated state-constrained stochastic control problems.

First, we record a growth and continuity estimate for each .

Proposition 2.

There exists , which depends only on and , for which

for each and all .

We do not specify the choice of norm in because it only affects the choice of constant.

Proof.

Recall that is assumed to be Lipschitz-continuous. Let be an arbitrary stopping time such that (such a stopping time exists by Corollary 1). Then, we have

Next, we compute

Lastly, by applying Proposition 1, we can construct a stopping time such that and

Then we can compute

Then the stated results hold because and were both arbitrary. ∎

In the remainder of the paper, it will prove useful to consider a type of perspective map on the sets . For each , define as

| (2.6) |

We note three key properties of this map.

-

1.

For any , we have ,

-

2.

For any , the th coordinate of is either zero or one, and

-

3.

The map is continuous on .

We now provide a dynamic programming lemma whose proof has the same flavour of the weak dynamic programming results in [7, 6, 3]. Compared to these previous results, we have a priori continuity of the value functions on the right-hand-side, so we do not need to consider upper- and lower-semicontinuous envelopes. We extend the ideas of a countable covering of the state-space by balls, each associated with a nearly optimal stopping time. To deal with the state-constraints, we employ an argument that utilizes the compactness and convexity of along with the continuity of . The proof of this lemma is the heart of the paper, but is quite involved, so it is relegated to the appendix.

Lemma 3 (Dynamic Programming).

For every and every , we have

| (2.7) |

Next, we demonstrate that we may relax the terminal constraint. The proof of this idea relies on a careful construction of a perturbed martingale which satisfies the terminal constraints of the previous problem, but does not significantly change the expected payoff. The proof of this result shares many key ideas with the previous lemma. For the sake of exposition, we provide this proof in the appendix as well.

Lemma 4 (Constraint Relaxation).

Note, even though , the right-hand-side of (2.8) is well-defined because is known to be bounded and continuous. Then, there is a unique continuous extension of the map from to . That is, taking the right-hand-side to be zero when .

With these lemmas in hand, we can now state the main result of this paper.

Theorem 1.

The function satisfies

for every .

For each , the function is the value function of the following state-constrained stochastic control problem

where is defined as in (2.6).

Of course, we then have

2.4 Time-dependent value functions

While, for the purposes of this paper, we may consider the results of Theorem 1 as a solution to the distribution-constrained optimal stopping problem, we can consider an additional time-dependent version of the state-constrained problem which is amenable to numerical resolution. In particular, the time-dependent value functions will correspond to viscosity solutions of Hamilton-Jacobi-Bellman (HJB) equations.

Definition 2.

Remark 1.

Using the properties of the time-independent auxiliary value functions deduced in Section 2.3, we can consider the terminal payoff as a given Hölder continuous function. Then this is a true state-constrained optimal stochastic control problem. In particular, we note that by the argument of Remark 5.2 in [7] we can equivalently define as a supremum over controls in which are not necessarily independent of .

We note an immediate relationship with the value functions of Section 2.3.

Corollary 3.

For each we have

for all .

Proof.

This result is obvious from the definition of and Theorem 1. ∎

Before stating a Dynamic Programming Principle for the time-dependent value functions, we first investigate their regularity. In particular, we aim to demonstrate that each is concave in and jointly continuous with estimates on its modulus of continuity.

Proposition 3.

For each , the function is concave for each .

Proof.

We proceed by backwards induction. Notice that the set is a singleton, so the functions and are both trivially concave in .

Suppose that is concave in for some . The key observation is that the map

is concave for every because it is the perspective transformation of the concave map (See Section 3.2.6 in [8]).

With this in mind fix any , , and . Let be arbitrary controls for which

almost-surely, for all . Define and . Then and

almost-surely, for all by the convexity of the set .

Then using the concavity of the perspective map, we can compute

But because were arbitrary, we conclude

Then is concave in , and hence so is by Corollary 3. Then the result holds by induction.

∎

We can go a step further and obtain a detailed estimate of the joint continuity of .

Proposition 4.

There exists , which depend only on and , such that for each , we have

for all .

The proof of this statement is relatively straightforward but long-winded, so we relegate it to the appendix. We do not claim that these Hölder exponents are sharp.

The upside of this representation as an optimal stochastic control problem is that we can characterize each time-dependent value function as a viscosity solution of a corresponding HJB equation. At this point, we can prove a Dynamic Programming Principle for the time-dependent value functions. While these are state-constrained stochastic control problems, we can directly use the a priori continuity of in and convexity of as in the proof of Lemma 3.

Theorem 2.

Fix , , and any such that . Let be a family of stopping times independent of and valued in . Then

From this result, we can immediately verify that each time-dependent value function is a viscosity solution of an HJB. Once we have the Dynamic Programming Principle in hand, this result becomes reasonably standard, so we direct the interested reader to [16, 6, 24].

We first define elliptic operators as

where

The intuition behind these definitions is that encodes admissible directions in which a state-constrained martingale starting from may evolve. In particular, a martingale constrained to lie in cannot have non-zero quadratic variation in the outer normal direction on the boundary. The elliptic operator shows up naturally from applying Dynamic Programming, while encodes the concavity in .

The main properties of and are that

Then following the arguments of [2], we can deduce that the value function is a viscosity solution of an equation involving an envelope with .

Proposition 5.

The function is the unique solution of the heat equation (in reversed time),

For each , is a continuous viscosity solution of the HJB equation,

| (2.9) |

The proof of this statement follows from a standard argument and an additional analysis of admissible controls on the boundaries. For more details on the introduction of the operator to obtain a variational inequality, we refer the interested reader to [2] or Section 4 in [23].

The more important question, of course, is whether or not one can obtain a uniqueness result for viscosity solutions of (2.9). It is standard to show that (2.9) admits a comparison principle when we have Dirichlet conditions on the boundary of . In the following, we demonstrate that we can prove uniqueness even with second-order boundary conditions using the special structure of the domain.

Theorem 3.

Of course the time-dependent value functions satisfy this linear growth constraint as a corollary of Proposition 4.

The key idea in this proof is that when we restrict a viscosity solution of (2.9) to the relative interior of any face of in the -coordinate, the restricted function is a viscosity solution of the same equation on a smaller state-space. In particular, when restricted to a vertex the equation reduces to the heat equation, for which we immediately have uniqueness. We then apply the comparison principle corresponding to the equation restricted to an edge using the fact that we have uniqueness on the vertices to deduce uniqueness on edges. We proceed as such on higher dimensional faces until we prove uniqueness on all of .

Sketch of Proof.

Fix and let be two continuous viscosity solutions of (2.9). Suppose that at some point. By the terminal condition, this must occur at some .

Suppose that there exists a vertex of the simplex such that at some point when restricting to in the -coordinate. By Proposition 6.9 in [26], we note that both and are viscosity solutions of the heat equation when restricting the the vertex in the -coordinate. But this contradicts uniqueness for the heat equation.

Let be a minimal dimension face of the simplex such that at some point when restricting to in the -coordinate. Again, by Propositon 6.9 in [26], we conclude that both and are viscosity solutions of the same equation on the relative interior of . Of course, the boundary of is the union of lower dimension faces of the simplex , so, by the assumed minimal dimension property of , we conclude that when restricting to the boundary of in the -coordinate. Then by applying the comparison principle for (2.9) with Dirichlet boundaries, we deduce that on .

The theorem then follows by considering the -dimensional face, itself.

∎

3 Application to Superhedging with a Volatility Outlook

In this section, we consider an application of distribution-constrained optimal stopping in mathematical finance. In particular, we consider the problem of model-free superhedging of a contingent claim with payoff using only dynamic trading in an underlying asset .

We assume that the price process is a martingale under some unknown martingale measure , but do not specify the exact volatility dynamics. However, in this problem, we assume that we have an outlook on the volatility in the form of the distribution of the quadratic variation, .222We note that, while it may seem unlikely that we have an atomic measure representing our volatility outlook, this is a reasonable starting place for two reasons. It is possible to approximate more general measures by atomic measures because it is possible to prove continuity of the value function in the Wasserstein topology (See Lemma 3.1 in [10]). Second, pricing by allowing only a finite number of scenarios, as opposed to specifying a full continuous-valued model, is standard in industry (e.g. the specification of rates, default, and prepayment scenarios in standard models for securitized products).

3.1 Model-free superhedging

We follow the model-free setting of [14, 5]. Let be the canonical space equipped with uniform norm , the canonical process, the Wiener measure, the filtration generated by , and the right-limit of .

Fix some initial value . Then, we denote

For any real-valued, -progressively measurable process satisfying , -a.s., we define the probability measure on ,

where

Then is a -local martingale. We denote by the collection of all such probability measures on under which is a -uniformly integrable martingale. The quadratic variation process is universally defined under any , and takes values in the set of all non-decreasing continuous functions from to .

3.2 Equivalence to distribution-constrained optimal stopping

We show that this problem is equivalent to distribution-constrained optimal stopping of Brownian motion.

Proposition 6.

We have

Proof.

This argument can be found in Theorem 2.4 of [5]. For completeness, we reproduce it below.

Let such that the -distribution of is . It follows by the Dambis-Dubins-Schwarz Theorem that where is a standard Brownian motion and is a stopping time with respect to the time-changed filtration with distribution (See Theorem 4.6 in [15]). Then .

Let be a stopping time such that . Define a process as

Note that is a continuous martingale on with , so induces a probability measure such that . Then the opposite inequality holds.

∎

Then one can obtain a model-free super-hedging price with a volatility outlook by solving the iterated stochastic control problem in Section 2.3.

3.3 Numerical example

In this section we obtain approximate numerical solutions of the distribution-constrained optimal stopping problem using finite-difference schemes.

In particular, we consider two potential outlooks on volatility. In the first, the binary outlook, we assume equal probability between a high- and low-volatility scenario

In the second, we augment the binary outlook with a third extreme volatility scenario which occurs with small probability

Our goal is to compute the model-free superhedging price of a European call option under each volatility outlook. Because we do not restrict to models where the price process is non-negative, we can take the payoff to be without loss of generality.

Then, as before, we define value functions for each outlook as

We solve the problem using the iterated stochastic control approach from Section 2.3. In particular, we obtain a viscosity solution of the corresponding Hamilton-Jacobi-Bellman equation in Section 2.4 using a finite-difference scheme. It is important to emphasize that, because of potential degeneracy due to the extra state-variables in and , it is critical to use a monotone numerical scheme.

In these results, we apply a version of the wide-stencil scheme introduced in [19]. In particular, we approximate the non-linear terms in each equation by monotone finite-difference approximations of the following form

where the set is a collection such that lies on nearby grid-points. For a rigorous analysis of wide-stencil schemes for degenerate elliptic equations, we refer the reader to [20, 13, 19].

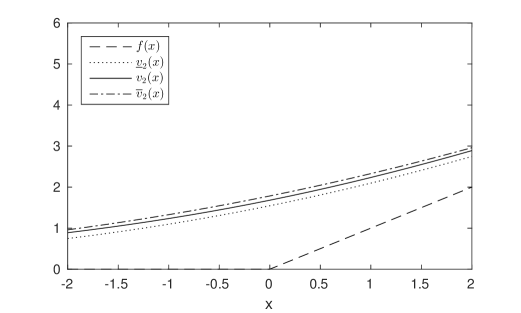

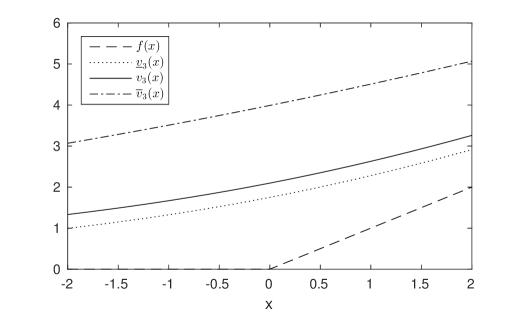

For comparison, we consider two main special cases, which we refer to as the “mean volatility” value and the “support-constrained” value. We define the mean volatility value as the model-free superhedging price obtained by assuming the quadratic variation will be equal to the mean of the distribution in the corresponding distribution-constrained problem. We define their corresponding value functions as and , respectively. On the other hand, we define the support-constrained value as the model-free superhedging price obtained when only restricting the quadratic variation to have the same support as that of the distribution in the corresponding distribution-constrained problem. We define their corresponding value functions as and , respectively.

We expect the following ordering:

and

Furthermore, we note that we can compute , , , and explicitly in terms of heat kernels (See Section 2.3 in [12]).

We illustrate the value function for the two- and three-atom problem in Figure 1 and Figure 2, respectively. As expected, we see a superhedging value which is increasing in the underlying asset price (or, equivalently, decreasing in the strike price) and respects the bounds implied by the support-constrained and average-volatility models. As expected, the bound provided by the support-constrained superhedging problem is particularly poor in the three-model volatility outlook, where we stipulate that the high volatility (high value) case is rare.

It is interesting to note that careful comparison of the two figures illustrates an increase in superhedging value between the two volatility outlooks which is roughly proportional to the increase in square-root of expected quadratic variation. For example, there is approximately a 25% increase in value at , which is essentially exactly in-line with the 25.2% increase in square-root of expected quadratic variation between the two outlooks. This matches our intuition that call option superhedging prices should be proportional to expected volatility to first order.

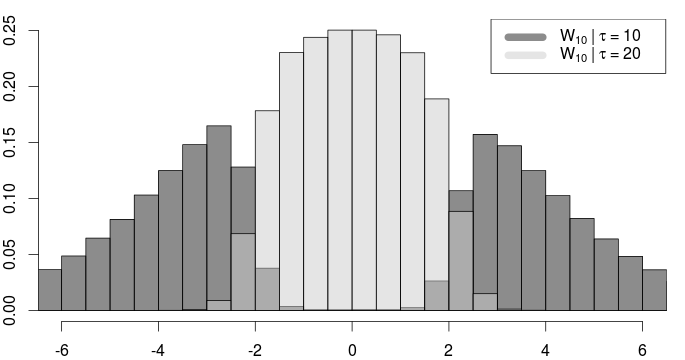

In Figure 3, we provide a probability density estimate of conditional on and for an approximate optimal stopping time for the two-atom volatility outlook model starting from . We obtain these estimates by performing Monte Carlo simulations with controls estimated from a numerical solution of the associated HJB equations. We use grid spacings , , and . We perform simulations and verify that relevant statistics from the Monte Carlo simulation match those from the finite-difference solutions (e.g., expected payoff, distribution and moments of the stopping time and stopped process) to within a reasonable margin of error.

The density estimates provide insight into the form of the optimal strategy. Recall that the payoff is locally-affine at all points except , where it is strictly convex instead. Then we expect an optimal stopping strategy to be one which maximizes local time accumulated at the origin. As expected, we find that the density of conditional upon is largely concentrated on points away from , at which the payoff process is unlikely to spend significant time as a submartingale if we were to choose not to stop.

It is interesting to note the lack of sharp cut-off between the two density estimates. One might expect the optimal strategy to be of a form where there exists a “stopping region” and a “continuation region.” On the contrary, the smooth overlap of the two density estimates is persistent even as we vary the resolution of the finite-difference solver, which suggests that the true optimal stopping strategy is not of the form . That is, the numerics suggest that optimal stopping strategies may be path-dependent even in simple examples.

Appendix A Proof of Lemma 3

This first argument is in the spirit of proofs of the weak dynamic programming principle which avoid measurable selection, as in [7, 6, 3]. In these arguments, the authors typically use a covering argument to find a countable selection of -optimal controls on small balls of the state-space. The main difficulty here is that, while a control may be admissible for the state-constrained problem at one point in state-space, there is no reason to expect it to satisfy the state constraints starting from nearby states.

The new idea in our approach is to cover with a finite mesh. We show that we can replace the process by a modified process , which lies on the mesh points almost-surely at the terminal time. We construct the new process in a measurable way using the Martingale Representation Theorem on a carefully constructed random variable. Then we show that, using the continuity of , that the objective function along is close to that along for a fine enough grid.

Once we know we can consider a perturbed process which lies on a finite number of points in at the terminal time almost-surely, we can construct -optimal stopping times using a standard covering argument in .

Proof.

Fix . For convenience of notation, define

In the remainder of this proof, we do not write in the superscripts of and because it is always fixed.

Step 1: Fix an arbitrary . Choose large enough that

Because is continuous on the compact set , we can find small enough that

for all and such that

Similarly, because is Lipschitz and is Lipschitz in uniformly in , we can find , possibly smaller than before, such that we also have

for all and such that

Step 2: We now construct a finite mesh on . Let be a finite subset of with the property that

-

•

The convex hull of is , and

-

•

Any point can be written as a convex combination of finitely-many points in , each contained in a -neighborhood of .

This is possible by compactness and convexity of . In particular, we can define a continuous function with the properties that

-

•

for all such that

-

•

for all , and

-

•

for all .

This corresponds to a continuous map from a point to a probability weighting of points in such that is a convex combination of nearby points in . Such a map can be obtained by an -minimization problem, for instance.

Step 3: Let be a countable and disjoint covering of with an associated set of points such that the -ball centered at contains the set .

For each and , let be a stopping time satisfying

such that

Note that above uses to denote the th entry of the vector .

By choice of in the first step and the definition of the sets , we have

for all .

Putting these inequalities together, we conclude that

for all , , and .

Step 4: Let be an arbitrary control for which for and almost-surely. For any , define two random variables, and , as

| (A.1) | |||||

Then and are -measurable and independent of each other. is equal in distribution to a standard normal distribution, the cumulative distribution function of which we denote by . Similarly, is equal in distribution to the absolute maximum of a standard Brownian bridge on , the cumulative distribution function of which we denote by . Furthermore, if we define

then is -measurable, while is independent of .

Define a random vector as

and

where we follow the conventions that , , and that sums over an empty set are zero. We denote the th through th entry in the random vector by . Then is -measurable and is constructed to have the key property that

almost-surely.

By the Martingale Representation Theorem, there exists for which almost-surely. It is clear by the construction that is independent of , so we can take . Then, by construction, for all , , and when , almost-surely.

We now perform a key computation. First note that

For the first term on the right-hand-side, we simply compute

We deal with the second term in a similar way, but the computation is more involved. Note that by construction we have

almost-surely in the set . Recall we also took small enough such that

for all and such that . But then we can compute

where comes from the growth bound from Proposition 2. With this in hand, we now complete the analysis of the second term

Using the continuity of , , and , along with the Dominated Convergence Theorem, we note

Then putting these results together, we see that for small enough

Step 5: Lastly, we intend to construct an -optimal stopping time using the covering from the second step. Define a stopping time as

By construction, we have . We proceed to make a careful computation. First, note that

We focus on the second term. In particular, we have

where the inequality follows from the construction in the third step and the independence of the stopping times with respect to .

Then we conclude

Combining this with the main inequality from the previous step, we obtain

Because and were arbitrary, then we conclude .

Step 6: Let be an arbitrary stopping time such that . Define a martingale as

for all and each . We can easily check that for each and

Then if we consider as an -valued martingale with for all , then we see for each . Finally, we have

Then by the Martingale Representation Theorem, there exists for which for all , almost-surely. We can compute

On the set , we have

for each . For almost every , we have

by the Strong Markov Property and stationarity properties of Brownian motion. Then we conclude

Because was an arbitrary stopping time, this implies

∎

Appendix B Proof of Lemma 4

The main idea of this argument is that we can take a controlled process , which does not satisfy , and modify it on an interval to a perturbed process with the properties that and . In particular, we may do this in a way that does not appreciably change the expected payoff.

One key idea, which we draw the reader’s attention towards, is the use of the Brownian bridge over in the construction. This construction is in the spirit of Corollary 2. While one might initially attempt a construction similar to Corollary 1, using a Brownian bridge instead of Brownian increments allows us to condition on at a key point in the argument.

Proof.

Fix . For convenience of notation, define

and

By Lemma 3, we have . In the remainder of the proof we withold the superscript on and for the sake of brevity.

Step 1: Let be an arbitrary control for which for and almost-surely. Note that on the set , almost-surely. Then

Because was arbitrary, we conclude .

Step 2: Let be an arbitrary control for which for , almost-surely. For any , define a random variable as

Then is -measurable and is equal in distribution to the absolute maximum of a standard Brownian bridge on , the cumulative distribution function of which we denote by . If we define , then is independent of .

Define a random vector as

and

where denotes the th through th element in the vector. Let for any . Then is -measurable and has the key property that . We also note that .

By the Martingale Representation Theorem, there exists such that for , , and almost-surely. We can then compute

But by the continuity and growth bounds of and , we can apply the Dominated Convergence Theorem to see

So then for any , we may take small enough that

Because and were arbitrary, we conclude .

∎

Appendix C Proof of Proposition 4

Proof.

We proceed in several steps, each relating the value function between nearby points. In the first three points, we consider a shift backwards in the time variable, a shift forward in time variable away from the terminal time, and lastly a jump onto the terminal time. In the fourth step, we discuss arbitrary perturbations in . In the fifth step, we discuss a perturbation inside the interior of some face of , including a possible jump off the face. In the sixth step, we consider a jump from an interior point onto a face of . Lastly, in the final step, we discuss how to put these together into one coherent bound.

Step 1: Fix and such that . Let be an arbitrary control for which for all , almost-surely. Define a new control as

for all . We can see that for all and , almost-surely. Then

where is at least as large as the Lipschitz constants in for and . But recall that for Brownian motion we can find such that

Using this and the fact that was arbitrary, we then conclude

Step 2: Fix and such that . Define

Let be an arbitrary control for which for all , almost-surely. Define new control as

where

for all . Note that by definition. Because , we then have so it is an adapted control. We can also check by the time-change properties of the Itô Integral that

Then for all , almost-surely, by the convexity of and the martingale property of . Then is an admissible control.

We can compute

Now we proceed to bound the final term in this inequality. First, note that by the convexity of , we can a bound

Furthermore, for large enough , depending only upon , we have for all . Then we can estimate

Putting these together and recalling that was arbitrary, we conclude

Step 3: Fix and let be an arbitrary control for which for all , almost-surely. By the Lipschitz continuity of and in we can compute

We can bound the error term by . By viewing the term containing as a perspective map applied to a concave function (See the proof of Proposition 3) and noting that the controlled process is a martingale, we can apply Jensen’s Inequality to see

But then because was arbitrary, we conclude that

Step 4: Fix and . Let be an arbitrary control for which for all , almost-surely. Then we immediately compute

where is at least as large as the Lipschitz constant in of and . Because was arbitrary we conclude

Step 5: Fix . Suppose for now that is not a vertex of , or equivalently that the value in each coordinate is less than one. Denote by

the disjoint collections of coordinates in which is zero and non-zero, respectively. Let

Let be any point satisfying . Let be an arbitrary control for which for all , almost-surely. Note that equals zero almost surely for each coordinate in .

Define a new control as

and note that by construction we have

for each . Similarly, we have

for all , almost-surely. This together with the observation that equals zero in each direction in implies that for all almost-surely. Furthermore, we have

| (C.1) | |||||

almost-surely, where is the diameter of the set .

Before proceeding with concrete bounds, we note an estimate regarding the perspective map. For any such that , we have

That is, the perspective map fails to be Lipschitz as . Using this along with the Hölder continuity and bounds on from Proposition 2, we can carefully bound

This bound is easily seen in the case and may be carefully checked when either equals zero exactly.

Then using the bound above as well as the growth bounds on , we check

Applying Hölder’s Inequality and the almost-sure bound in (C.1), we bound the last term by

Putting these all together and recalling that was arbitrary, we conclude

for large enough constant .

If is a vertex, then the only admissible control is , so we obtain the same bound (in fact a better bound) for any nearby directly from Proposition 2.

Step 6: Fix some at least small enough that . Fix such that at least one element of is in . Denote by

the disjoint collections of coordinates in which is zero, “small”, and “large”, respectively. Let be any point obtained from setting elements of in to zero and adding these values to a single index . Then is zero in all coordinates and non-zero (and “large”) in all coordinates . Furthermore, , so

Let be an arbitrary control for which for all , almost-surely. Note that equals zero almost surely for each coordinate in . Similarly, because each component of is a martingale, we conclude

for each . That is, , so the th coordinate of stays small with high probability.

Define by moving the values of at coordinates to the th coordinate. Note that, by construction,

and for all , almost-surely. Furthermore, we have

for each , and

for each . Lastly, we have

In summary, we have

Then using the same bounds as in the previous step, we can now compute

The first term on the right-hand-side may be bounded as

Similarly, the second term may be bounded as

Putting these all together and recalling that was arbitrary and , we conclude

for large enough constant .

Step 7: We now briefly remark how to put all of these estimates together. We consider the Hölder estimates in each coordinate separately as they can be combined in the end using triangle inequality. Note that the Lipschitz regularity in has already been proven.

In the time direction, fix and some small such that . If , then by Step 1 we have

If , then by Step 3 we have

Now suppose that . By Step 2, we have

In the next step, we critically see where the -Hölder coefficient appears. If then by an application of Step 1 and Step 3, we see

Lastly we consider the case . By an application of each of Steps 1 through 3, we see

Of course, by taking a large enough constant we can bound all terms by terms and obtain the -Hölder continuity result in .

The -Hölder continuity result follows by a similar approach by cases as in the time perturbation case. The key idea is that Step 5 and Step 6 tell locally how to perturb in a -Hölder way, including onto and off the boundaries. Then by a covering argument and the compactness of we can obtain a finite chain of local Hölder inequalities connecting any two points and obtain the result for sufficiently large constant. ∎

Appendix D Proof of Theorem 2

This argument is essentially a time-dependent version of that given in the proof of Lemma 3. The key idea here is to use the convexity of the set and the concavity of in to construct an -suboptimal control which satisfies the state-constraint as a convex combination of admissible controls starting from nearby points.

Proof.

Fix and . For convenience of notation, define and

The inequality is a standard result even in the case of these state-constraints. We refer the interested reader to Theorem 3.3 in [26] and instead focus on the opposite inequality.

Step 1: Fix an arbitrary . Choose large enough that

Because is continuous on the compact set , we can find small enough that

for all and such that

Similarly, because is Lipschitz and is Lipschitz in uniformly in , we can find , possibly smaller than before, such that we also have

for all and such that

Finally, take potentially even smaller so that

Step 2: We first construct a finite mesh on and which will be fine enough to take advantage the continuity of . Let be a finite collection of mesh points in with the key property that for any , there exists such that .

By the compactness and convexity of , we can obtain a finite subset of , , with the property that

-

•

The convex hull of is , and

-

•

Any point can be written as a convex combination of points in , each contained in a -neighborhood of .

In particular, we can find a continuous function with the properties

-

•

for all such that

-

•

for all , and

-

•

for all .

This corresponds to a continuous map from a point to a probability weighting of points in such that is a convex combination of nearby points in .

By the same type of covering argument as in the proof of Lemma 2, we can obtain a finite and disjoint covering of by measurable sets , each contained in a -ball, and controls with the key properties that for all and

for each , , , and .

Step 3: Fix an arbitrary control for which for all and let be the associated stopping time which is valued in . We are next going to construct a new control related to the suboptimal controls . In words, we will follow up to the stopping time , then set the control to zero until the first subsequent hitting time of . Then we will follow an appropriate convex combination of the controls .

To make this precise, define a stopping time

Define a collection of controls as

for each and all . Finally, define a control as

for all .

The control is adapted because the map is continuous. Similarly, it can be easily seen to be square-integrable. The key property, however, is that satisfies for all . In words, this follows from the convexity of the set and the fact that is a convex combination of controls, each of which satisfy the state-constraint.

Making this precise, we use the assumed properties of the map and the dynamics of to compute

Recall though that and almost-surely. Then the equality above and the convexity of demonstrate that for all almost-surely.

Step 4: We now proceed to make a very delicate series of estimates. First, we have

where the last term comes from known growth bounds on and . Of course, this term is bounded by by the choice of and use of Hölder’s Inequality. Next, rewriting each term in the sum above using the key property from the construction of in the previous step, we see

using the concavity of composed with the perspective function in (See the proof of Proposition 3). Next, by the suboptimality conditions of , we see

where we used the locality property of the map and continuity of assumed in the construction of . Lastly, summing over , we see

for sufficiently large . In this step, we used growth bounds on and the Hölder estimates from Proposition 4 together with the fact that by construction. By the choice of , however, we see this last error term is bounded by .

Putting all these computations together and recalling that and were arbitrary, we see

∎

References

- [1] S. Ankirchner, M. Klein, and T. Kruse, A verification theorem for optimal stopping problems with expectation constraints, Applied Mathematics & Optimization, (2017).

- [2] E. Bayraktar and M. Sirbu, Stochastic perron’s method for hamilton–jacobi–bellman equations, SIAM Journal on Control and Optimization, 51 (2013), pp. 4274–4294.

- [3] E. Bayraktar and S. Yao, A weak dynamic programming principle for zero-sum stochastic differential games with unbounded controls, SIAM J. Control Optim., 51 (2013), pp. 2036–2080.

- [4] M. Beiglboeck, M. Eder, C. Elgert, and U. Schmock, Geometry of Distribution-Constrained Optimal Stopping Problems, ArXiv e-prints, (2016).

- [5] J. F. Bonnans and X. Tan, A model-free no-arbitrage price bound for variance options, Appl. Math. Optim., 68 (2013), pp. 43–73.

- [6] B. Bouchard and M. Nutz, Weak dynamic programming for generalized state constraints, SIAM J. Control Optim., 50 (2012), pp. 3344–3373.

- [7] B. Bouchard and N. Touzi, Weak dynamic programming principle for viscosity solutions, SIAM J. Control Optim., 49 (2011), pp. 948–962.

- [8] S. Boyd and L. Vandenberghe, Convex optimization, Cambridge University Press, Cambridge, 2004.

- [9] R. Capocelli and L. Ricciardi, On the inverse of the first passage time probability problem, Journal of Applied Probability, (1972), pp. 270–287.

- [10] A. M. G. Cox and S. Källblad, Model-independent bounds for Asian options: a dynamic programming approach, To appear in SIAM Journal on Control and Optimization, (2017).

- [11] R. E. Curto and L. A. Fialkow, Recursiveness, positivity, and truncated moment problems, Houston J. Math., 17 (1991), pp. 603–635.

- [12] L. C. Evans, Partial differential equations, vol. 19 of Graduate Studies in Mathematics, American Mathematical Society, Providence, RI, second ed., 2010.

- [13] B. D. Froese and A. M. Oberman, Convergent finite difference solvers for viscosity solutions of the elliptic Monge-Ampère equation in dimensions two and higher, SIAM J. Numer. Anal., 49 (2011), pp. 1692–1714.

- [14] A. Galichon, P. Henry-Labordère, and N. Touzi, A stochastic control approach to no-arbitrage bounds given marginals, with an application to lookback options, Ann. Appl. Probab., 24 (2014), pp. 312–336.

- [15] I. Karatzas and S. E. Shreve, Brownian motion and stochastic calculus, vol. 113 of Graduate Texts in Mathematics, Springer-Verlag, New York, second ed., 1991.

- [16] M. A. Katsoulakis, Viscosity solutions of second order fully nonlinear elliptic equations with state constraints, Indiana Univ. Math. J., 43 (1994), pp. 493–519.

- [17] J. B. Lasserre, Moments, positive polynomials and their applications, vol. 1 of Imperial College Press Optimization Series, Imperial College Press, London, 2010.

- [18] C. W. Miller, Nonlinear PDE approach to time-inconsistent optimal stopping, SIAM J. Control Optim., 55 (2017), pp. 557–573.

- [19] A. M. Oberman, The convex envelope is the solution of a nonlinear obstacle problem, Proc. Amer. Math. Soc., 135 (2007), pp. 1689–1694 (electronic).

- [20] , Wide stencil finite difference schemes for the elliptic Monge-Ampère equation and functions of the eigenvalues of the Hessian, Discrete Contin. Dyn. Syst. Ser. B, 10 (2008), pp. 221–238.

- [21] J. L. Pedersen and G. Peskir, Optimal mean–variance selling strategies, Math. Financ. Econ., 10 (2016), pp. 203–220.

- [22] G. Peskir and A. Shiryaev, Optimal stopping and free-boundary problems, Lectures in Mathematics ETH Zürich, Birkhäuser Verlag, Basel, 2006.

- [23] H. Pham, Continuous-time stochastic control and optimization with financial applications, vol. 61, Springer Science & Business Media, 2009.

- [24] D. B. Rokhlin, Stochastic Perron’s method for optimal control problems with state constraints, Electron. Commun. Probab., 19 (2014), pp. no. 73, 15.

- [25] A. N. Shiryaev, Optimal stopping rules, vol. 8 of Stochastic Modelling and Applied Probability, Springer-Verlag, Berlin, 2008. Translated from the 1976 Russian second edition by A. B. Aries, Reprint of the 1978 translation.

- [26] N. Touzi, Optimal stochastic control, stochastic target problems, and backward SDE, vol. 29 of Fields Institute Monographs, Springer, New York; Fields Institute for Research in Mathematical Sciences, Toronto, ON, 2013. With Chapter 13 by Agnès Tourin.

- [27] C. Zucca and L. Sacerdote, On the inverse first-passage-time problem for a wiener process, The Annals of Applied Probability, (2009), pp. 1319–1346.