Estimation in Tournaments and Graphs under Monotonicity Constraints

Abstract

We consider the problem of estimating the probability matrix governing a tournament or linkage in graphs from incomplete observations, under the assumption that the probability matrix satisfies natural monotonicity constraints after being permuted in both rows and columns by some latent permutation. We propose a natural estimator which bypasses the need to search over all possible latent permutations and hence is computationally tractable. We then derive asymptotic risk bounds for our estimator. Pertinently, we demonstrate an automatic adaptation property of our estimator for several sub classes of our parameter space which are of natural interest, including generalizations of the popular Bradley Terry Model in the Tournament case, the model and Stochastic Block Model in the Graph case, and Hölder continuous matrices in the tournament and graph settings.

Sabyasachi Chatterjeelabel=e1]sabyasachi@galton.uchicago.edu Sumit Mukherjeelabel=e2]sm3949@columbia.edu

1 Introduction

In this paper we consider two statistical estimation problems. We begin by describing the two set ups.

-

•

Consider the situation of teams playing in a league tournament where each team plays every other team once. The results of the tournament can be written as a data matrix of zeroes and ones by setting for if team wins against team , and otherwise. Let be the probability that team wins against team with whenever Set for all as a matter of convention. The upper triangular part of the data matrix is modeled as

(1.1) where in the upper triangular part is jointly independent and refers to the standard Bernoulli distribution.

The lower triangular part of the data matrix is filled in a skewsymmetric manner; that is

(1.2) The problem then is to estimate the pairwise comparison probability matrix based on the observed data matrix This setting can arise whenever the data is in the form of pairwise comparisons (see David (1963)), for example in analyzing customer preferences for items, citation patterns for journals (see Stigler (1994)). For convenience, we stick to the tournament terminology in this paper. Note that we have parameters to estimate and data points. Hence one needs structural assumptions on for consistent estimation to be possible. The classical approach in this problem is to assume that the pairwise probability matrix has the following structural form:

(1.3) where the vector is a vector of weights representing the skill/ability of the teams. This is the Bradley-Terry model (see Bradley and Terry (1952)) which is very popular in the ranking literature. It is then common to estimate by maximum likelihood (see Hunter (2004)) and plug it in to estimate The study of asymptotic estimation of in the Bradley Terry Model has a long history in Statistics (see Simons et al. (1999) and references therein).

We are interested in the problem of estimating the matrix of probabilities under an assumption commonly made in the ranking literature known as Strong Stochastic Transitivity (SST) (see Shah et al. (2016a) and references therein). This assumption posits the existence of an ordering among the teams which is unknown to the statistician. This ordering is then reflected on the probabilities as follows. Let team have a higher rank than team (i.e. team is better than team ). Then for any team , the probability of team defeating team would be no less than the probability of team defeating team , which gives

Even though the SST condition is classical, a formal study of estimation under this condition was done recently in Chatterjee (2015) and was termed as the Nonparametric Bradley Terry Model. The terminology is apt because it clearly generalizes the very commonly used Bradley Terry model. Any matrix of the Bradley Terry form in (1.3) satisfies the SST condition with the ordering given by the ordering of the vector. We refer to Proposition in Shah et al. (2016a) who show in a precise sense that the Nonparametric Bradley Terry Model is a significant extension of the usual Bradley Terry model.

In many realistic scenarios, we would not be able to observe all pairwise comparisons. Thus, it is of interest whether one can still estimate the pairwise comparison matrix in the situation where we observe only a fraction of all possible games that can be observed. In this paper we consider the missing data at random setting. In this setting we get to observe each entry above the diagonal with probability independently of other observations above the diagonal.

The purpose of this paper is to propose and analyze a computationally tractable estimator in this problem. The main focus of this paper is to obtain finite sample risk bounds (upto a constant factor) and study how small can be to still allow consistent estimation.

-

•

Consider now the situation of observing a random graph on nodes with no self loops. Let now be the probability of node and node being linked. Again we set for all as a matter of convention. The random graph can be now encoded as an adjacency matrix of zeroes and ones. Again, the upper triangular part of the adjacency matrix is modelled as

(1.4) where in the upper triangular part is jointly independent. The lower triangular part of the data matrix is now filled in a symmetric manner; that is

(1.5) Inspired by the SST assumption in the ranking literature, here we assume that that the vertices can be arranged in an order (unknown to the statistician) of increasing tendency of getting linked to other vertices. This assumption will again impose monotonicity constraints on the edge probabilities For example if node is more ”active” or ”popular” than node then for any node we must have For an example where such an assumption seems natural, consider a social network with people labeled where the person has a popularity parameter . The chance that person and person are friends is , where is increasing in both co-ordinates to signify that increasing popularity leads to more friendship ties. The function also needs to be symmetric, as the chance that and are friends is symmetric in . Indeed, in this case there is (at least) one ordering which sorts the nodes of the network in increasing order of popularity.

We pose and study the problem of estimating the edge probability matrix in this set up with missing data at random. We sometimes refer to this model of random graphs as the symmetric model, differentiating it from the skewsymmetric (tournament) case. Under our model assumptions, the problem of estimating the edge probabilities is very closely related to the problem of estimating graphons in the spirit of Gao et al. (2015) where we assume monotonicity (without smoothness) of the graphon in both variables, instead of smoothness assumptions made in Gao et al. (2015).

In this paper we look at the above two estimation problems in the skewsymmetric and the symmetric model in a unified way. In particular, we introduce and study the risk properties of a natural estimator which is described in subsection 1.2. Our estimator has the same form in both the models, and the technique of analyzing the risk properties of the estimator in both the models is the same.

1.1 Formal Setup of our problem

In this subsection we define two parameter spaces; one for the skewsymmetric model and one for the symmetric model.

Denote to be the set of all permutations on symbols. For any matrix and any permutation we define to be the matrix such that If denotes the permutation matrix corresponding to the permutation then we have where the RHS is usual matrix multiplication.

Let be the space of tournament matrices defined by

| (1.6) |

Any matrix in when only looked at the upper triangular part above the diagonal is non increasing in any row (as grows) and non decreasing in any column (as grows). The lower triangular part is just minus the upper triangular part and the diagonals are zero. In words, is the space of matrices which satisfy the SST assumption with known ranking where the ranking is such that player is the best, followed by player and so on. Then our parameter space for the skewsymmetric model can be written as

| (1.7) |

Similarly, define the space of matrices

| (1.8) |

Any matrix in when only looked at the upper triangular part above the diagonal is non decreasing in both rows and columns. The lower triangular part is symmetrically filled, and the diagonals are zero. Again, is the space of expected adjacency matrices which are consistent with the monotonicity restrictions imposed by the ordering where node is most popular followed by node and so on. Then our parameter space for the symmetric model can be written as

| (1.9) |

For or we study the problem of estimating the underlying matrix of probabilities . The loss function we consider is the mean Frobenius squared metric defined for any two matrices and as , where denotes the Frobenius norm of the matrix

1.2 The estimator

The purpose of this paper is a statistical study of the following estimator, denoted by of the true underlying mean matrix where , and where is the space of permutations on symbols. Construction of our estimator consists of several steps. Initially our data matrix will have some entries or and some entries would be missing. Let denote the proportion of non missing entries in our data, i.e. equals the number of observed games divided by

-

(a)

Filling

Fill the missing entries of the data matrix by . Henceforth let us denote to be the data matrix obtained after filling up the missing entries.

-

(b)

Estimate Ranking

Let be the row sum of the data matrix In this step we sort the vertices according to the row sums of the data matrix and obtain a permutation such that The inverse of the random permutation can be thought of as a proxy for the underlying In case there are ties in the vector break the ties uniformly at random while obtaining the sorting permutation

-

(c)

Debiasing

In this step we transform to where is a matrix with for any and for any

-

(d)

Sorting and Projecting

We then sort the debiased data matrix by applying to it the sorting permutation obtained from Step We then project onto the relevant parameter space. In the skewsymmetric model, we project onto the set and in the symmetric model, we project onto the set Both and are closed convex sets of matrices and hence there exists a unique projection onto them. Let the projection operator be denoted by in both cases. After this step we have the projection of a sorted and debiased data matrix

-

(d)

Unsorting

We now unsort the debiased, sorted and projected data matrix by applying to it the inverse of the sorting permutation .

-

(e)

Estimate by if too many missing entries

We now define our final estimator as follows:

(1.10)

Remark 1.1.

The transformation is merely a debiasing step in the following sense. Let be the identity permutation for simplicity. For any fixed the random variable thus takes the value with probability takes the value with probability and takes the value with probability Thus

Remark 1.2.

Note that in the skewsymmetric (tournament) model, the row sums of the data matrix correspond to the number of wins or victories for each player, and the column sums of the data matrix correspond to the number of defeats for each player. Hence our sorting step just sorts the teams according to the number of victories (or equivalently the number of defeats, as sum of victory and defeat of each player is ). Similarly, in the symmetric (graph) model, the row sums of the adjacency matrix correspond to the empirical degrees of the nodes in the graph. Therefore, our sorting step sorts the vertices according to the empirical degrees.

The first step of our algorithm just needs computation of the row sums and then sorting, which combined clearly will only take at most operations. The projection step is thus going to be dominating the computation time. Fortunately there are efficient ways of computing the projection. First of all, the projection by definition has to be zero on the diagonals and would be skew symmetric/symmetric according to our model. Hence in either of the models, it suffices to compute the projection for the upper diagonal part. It turns out that the spaces and without the constraint that all elements have to live in can be viewed as the space of Isotonic functions on an appropriate Directed Acyclic Graph (DAG) on the domain Isotonic functions on a DAG can only increase on following a directed path in the DAG. Recent results in Kyng et al. (2015) study how to compute such Isotonic projections on a general DAG. Their result imply an algorithm with runtime for our problem. More classically, the problem of computing this projection is closely related to computing what is called a Bivariate Isotonic Regression(see Chatterjee et al. (2016)). There exists efficient iterative algorithms for this purpose; see page 27 in Robertson et al. (1988). The focus of this paper therefore is not on computation of our estimator but rather on its statistical properties.

2 Main result

Having defined our estimator, we now make a couple of more definitions.

Definition 2.1.

Henceforth we will use the notation in place of or . The implication is that all results hold with replaced by either of the two parameter sets.

Setting , for any define the row sums for . Also for each and define the quantity

The quantity is an important quantity in our analysis. As will be clear from our subsequent analysis, matrices in with additional structure tend to have smaller We are now ready to state the main theorem of this paper.

Theorem 2.1.

Consider the estimator defined in (1.10). Let and let Then there exists a universal constant such that for any we have

| (2.1) |

Remark 2.1.

Theorem 2.1 gives an upper bound which is a sum of two terms. The first term scaling like can be thought of as the risk arising due to the shape constraint imposed by the SST condition. The second term involving can be interpreted as the risk arises because of our sorting step; it measures how much changes in a frobenius norm squared sense, if its rows/columns are permuted by a typical sorting permutation.

Remark 2.2.

The strength of Theorem 2.1 is that it is adaptive in the parameter , and gives tight asymptotic bounds for several sub-parameter spaces of interest. The term dominates the term in most cases of interest. Hence the quantity determines the rate of convergence of our estimator.

All our results will be derived as corollaries of our main theorem. We now begin to discuss the various consequences and implications of Theorem 2.1.

2.0.1 Worst case Risk Bound

As a first application of Theorem 2.1, we deduce the worst case risk of our estimator.

Corollary 2.1.

There is a universal constant such that for any and we have

| (2.2) |

Remark 2.3.

The brute force LSE in our problem achieves a MSE of upto log factors, which is minimax rate optimal (upto log factors) in the tournament setting (see Theorem 5(a) in Shah et al. (2016a)). The same fact can be shown to be true in the graph setting by an application of Lemma 3.1 in Chatterjee and Lafferty (2017). We do not carry this out in this manuscript.

Comparing Theorem 2.1 to the minimax rate, the rate achieved by our estimator is clearly worse than the minimax rate of estimation. However the only method known to achieve the minimax rate is the LSE, which is perhaps not computationally feasible. This raises the important question of whether there exists a computationally feasible estimator achieving the minimax rate in this problem. This question deserves further study and is beyond the scope of the current manuscript.

The authors in Shah et al. (2016a) (see Theorem ) improved the analysis of an estimator based on singular value threshholding proposed in Chatterjee (2015) and demonstrated its rate of convergence to be Hence our estimator matches the best known rate of convergence for computationally feasible estimators.

Remark 2.4.

It follows from Corollary 2.1 that the MSE converges to as soon as . On the other hand, if converges to a finite number , the known minimax lower bound implies that the MSE stays bounded away from .

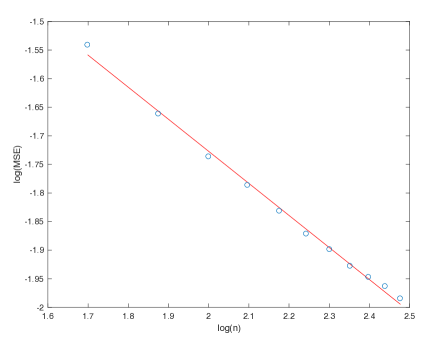

A natural question is whether the upper bound for our estimator in Corollary 2.1 is tight. The following example suggests that the given upper bound is tight at least when .

Define for any as

| (2.3) |

Simulations of the MSE (see figure 1) suggest that our exponent of in the upper bound in Corollary 2.1 is tight.

For the plot we have simulated our data when the true underlying parameter matrix is given by (2.3). We have simulated times for each sample size ranging from to in increments of A plot of log(n) (base ) versus log(MSE) clearly shows a linear behavior, and the best fitted line has slope , which is close to the predicted exponent

2.1 Adaptive Risk Bounds

The main reason for studying our estimator is that it exhibits automatic adaptation properties. By automatic adaptation we mean that even though our estimator achieves rate of estimation globally, it achieves provably faster rates of estimation for several subclasses of our parameter space which are of independent interest. We now describe some of these subclasses along with the associated risk bounds.

2.1.1 Block matrices

Let us consider the class of matrices within our parameter space which are a permuted version of some blockmatrix. This class of matrices (without the restriction of being within ) is popularly known as the Stochastic Blockmodel in Network Analysis. In the Tournament setting, one can think of the situation where there are teams but only levels of teams. Within each level, each team has the same ability. Therefore, assuming a block structure on the true pairwise comparison matrix is a natural way to impose sparsity in the model.

Definition 2.2.

For , let denote the subset of all block matrices with equal sized blocks, upto an unknown permutation.

Corollary 2.2.

There exists a universal constant such that for any we have

Remark 2.5.

In particular when is fixed, we get from corollary 2.2 that

The next theorem shows that the above upper bound is unimprovable in the sense that this is the minimax error rate for blocks of equal size, upto factors. In the case when the latent ranking is known, the estimation problem is essentially equivalent to Bivariate Isotonic Regression (see Chatterjee et al. (2016)), where the minimax error rate for block matrices (without a latent permutation) is shown to be This means that the latent permutation in our parameter space makes the statistical estimation problem fundamentally harder in a minimax sense.

Theorem 2.2.

Consider the subset of all equal sized block matrices. Then for some universal constant we have

The above theorem shows that when is fixed our estimator is minimax optimal upto logarithmic factors for the class

Remark 2.6.

It is instructive to compare with known results when Without the monotonicity constraint, it was shown in Gao et al. (2015) that for symmetric block matrices the minimax rate is . Thus for the minimax rate with and without monotonicity constraints are both . For the minimax rate with monotonicity is , whereas without monotonicity the minimax rate is strictly larger.

2.1.2 Generalized Bradley Terry model + Generalized model

In the Tournament setting, if the Bradley Terry model is correct, one can use the MLE of the weights vector to estimate It is known that this estimator attains a fast rate of convergence of (see Theorem in Shah et al. (2016a)). A natural question is whether our estimator attains this fast rate of convergence whenever the true matrix is actually of the Bradley Terry form. Our next corollary shows this to be true in a more general sense. Before stating the corollary, let us define the Generalized Bradley Terry Model contained within the class of SST matrices.

Definition 2.3.

Let denote the subset of all tournament matrices such that , where is a unknown symmetric distribution function on (i.e. ) with a continuous strictly positive density function function, and is a sequence of real numbers lying in a compact interval . It is not hard to check that the class indeed satisfies the SST condition. In particular, setting and (the normal distribution function) we get the usual Bradley Terry model and the Thurstone model (see Bradley and Terry (1952); Thurstone (1927)) respectively. Let us call this class of matrices the Generalized Bradley Terry Model.

Let us now define the analogous class of matrices in the symmetric model on graphs.

Definition 2.4.

Let denote the subset of all expected adjacency matrices such that , where is a distribution function on with a continuous strictly positive density function, and is a sequence of real numbers in . In particular for the choice gives the model on networks, which has originated from Social Sciences and has been studied in Statistics(c.f. Chatterjee et al. (2011), Mukherjee et al. (2016) and references there-in). The class generalizes the usual model to allow for a more general class of distribution functions.

With assumed to be known, estimation in the Generalized Bradley Terry model has been studied by Shah et al. (2016a). We present our next corollary treating as an unknown parameter.

Corollary 2.3.

There exists a universal constant such that for any we have

where and . The same risk bound holds for the Generalized Beta Model

If the distribution function is known, the authors in Shah et al. (2016a) (Theorem ) show that the estimator based on the MLE of achieves the minimax optimal rate , under the stronger condition that the density is strongly log concave and twice differentiable. This implies that our estimator is minimax rate optimal upto log factors for the bigger class without using the knowledge of . Obviously, computing the MLE takes into account the explicit knowledge of The estimator studied in this paper attains the same fast rate of convergence as the MLE upto log factors, but without the knowledge of

2.1.3 Smooth matrices

In the symmetric model (graph setting) there has been a tradition of studying estimation of graphons satisfying some smoothness condition (see Gao et al. (2015) and references therein). We think it is a natural question to ask what happens when the true pairwise probability matrix in the Tournament setting (in addition to satisfying SST) is a smooth matrix, upto an unknown permutation. This motivates us to define the following class of matrices satisfying a discrete version of the usual Holder smoothness conditions.

Definition 2.5.

For let denote the subset of all permuted versions of Holder continuous matrices with order and Holder constant , i.e. after being permuted in rows and columns, satisfies

for all .

The next corollary shows that our estimator provably attains faster rates of convergence than whenever the true matrix, upto an unknown permutation, satisfies smoothness conditions as above.

Corollary 2.4.

There exists a universal constant such that for any we have

Remark 2.7.

As the above corollary shows, the adaptation of our estimator depends crucially on the order of the Holder class . In particular, for the class of Lipschitz matrices (which correspond to the choice ) with no missing entries (which correspond to ), the corollary implies the following upper bound:

A natural question is whether the worst case MSE over actually scales like . We do not know the answer to this question. However, we do have an explicit example of for which the quantity actually scales like , which suggests that it is not possible to prove a better rate than with our proof technique.

Even though the worst case risk over the class of Lipschitz matrices is , under an extra assumption that is lower Lipschitz as well, we get an improved MSE of . More generally, the same holds for lower Holder continuous matrices as well. To make this precise we propose the following definition:

Definition 2.6.

For let denote the subset of all lower Holder continuous matrices with lower Holder constant , i.e. after being permuted in rows and columns by some permutation it satisfies

for all .

Corollary 2.5.

There exists a universal constant such that for any we have

Remark 2.8.

A similar estimator (consists of a sorting step and a smoothing step) as ours was proposed in Chan and Airoldi (2014) in the symmetric model, where the authors assume that the true is both lower and upper Lipschitz (but not necessarily monotonic). Under an extra assumption on the sparsity of the gradient of the histogram of , (Chan and Airoldi, 2014, Theorem 3) shows that their estimator has MSE scaling like . We obtain the same error bound without the sparsity assumption on the gradient, but under the extra assumption of monotonicity. Another point worth mentioning here is that monotonicity constraints make it possible for our estimator to be completely tuning parameter free while the estimator proposed in Chan and Airoldi (2014) has a bandwidth parameter that needs to be tuned.

2.2 Main Contribution

Our main contribution in this problem is to obtain a single result (Theorem 2.1) encapsulating our understanding of how the MSE varies with the underlying The upper bound in Theorem 2.1, being a sum of two terms, has a natural interpretation of being the minimax rate plus an extra term arising because of potential mistakes made in the sorting step. Operationally, Theorem 2.1 shows that a recipe to obtain an upper bound of the MSE at a particular is to upper bound the term which is a completely deterministic term. This recipe then furnishes several corollaries for submatrices of interest with the proofs of the corollaries now being very simple. Theorem 2.1 therefore shows adaptive rates are possible in our problem, even in the missing observations at random setting, when the true underlying matrix has additional structure. As of now, such adaptivity is not known to hold for the other competing estimator in this problem; the USVT estimator, proposed in Chatterjee (2015).

At the later stages of preparing this document, we became aware of an independent work by Shah et al. (2016b) who analyze a similar estimator as ours. A couple of comments are in order to relate the results obtained here to those in Shah et al. (2016b). Our estimator is not exactly the same as the CRL estimator proposed in Shah et al. (2016b) because they have an extra randomization step in constructing the sorting permutation. This helps in obtaining a MSE scaling like instead of for the very special case when is constant (or nearly constant). In terms of worst case risk the performance of both estimators is the same, and equals . However, for many sub parameter spaces of interest our results provides sharper results, demonstrating the adaptive nature of our estimate. For instance, when with equal sized blocks, Theorem in Shah et al. (2016b) give a upper bound while Theorem 2.1 attains the which is minimax rate optimal for upto log factors. The adaptation results for matrices of the Generalized Bradley Terry form or for matrices satisfying Holder smoothness conditions also do not follow from Theorem in Shah et al. (2016b). Moreover, all our results are in the missing observations at random setting while Shah et al. (2016b) work in the complete observations setting.

2.3 Scope of future Work

An important open question is whether there exists a polynomial time estimator achieving the minimax rate of estimation of (when there is no missing data). Another natural question is whether the upper bounds for our estimator given in Corollary 2.4 for Lipschitz matrices and other smooth matrices are tight. Finally, automatic adaptation properties of the Singular Value Threshholding estimator (proposed in Chatterjee (2015) and studied in Shah et al. (2016a)) also deserve attention.

3 Proof of corollaries

Proof of Corollary 2.1.

To begin, fix such that . Then we have

The above bound implies , which along with Theorem 2.1 completes the proof of the corollary. ∎

Proof of Corollary 2.2.

As before, it suffices to control the terms in . To this end let be the underlying matrix, i.e.

Now fix such that . Then with and we have

which in particular means

This gives

The required bound then follows from Theorem 2.1. ∎

Proof of corollary 2.3.

To begin, note that

Now fixing such that , we have

and so

which along with Theorem 2.1 completes the proof. ∎

Proof of Corollary 2.4.

As before it suffices to control the terms in . To this end, fix such that . We claim that

| (3.1) |

We first complete the proof of the corollary, deferring the proof of (3.1). To this end we have

from which the result follows on using Theorem 2.1.

It thus remains to complete the proof of (3.1). To this end, let , and let be such that . Then setting , for any such that an application of triangle inequality gives

This in turn implies

which is same as

∎

4 Proof of Theorem 2.1

To begin, note that the MSE of our estimator does not depend on the underlying true permutation , and so henceforth we assume that the true underlying latent permutation is the identity permutation. We now outline the proof of Theorem 2.1 in several steps.

4.1 Step 1

Recall that our estimator is of the form

on the set . We now show that it is sufficient for our purposes to analyse the estimator where is replaced by We now state a lemma making this precise.

Lemma 4.1.

Suppose

be the estimator constructed assuming known. If , then there exists a constant such that for all we have

Hence from now on, we will analyze the mean squared error of the estimator

4.2 Step 2

We now write the following inequality.

In this step we handle the first term above. Fix and define a random (depends on ) function by

Here the notation refers to the inner product of two matrices defined as The following proposition connects the term to the function

Proposition 4.1.

The function defined above is strictly concave with and converges to as . Denoting the unique maximizer of the function by we have . Moreover, if satisfies then

Proposition 4.1 is proved using a representation result for the projection of a vector onto a convex set as developed in Chatterjee (2014). Note that this is a deterministic result and does not depend on the distributional properties of For the sake of completeness we prove this result in the appendix. For a more general version of the above proposition see Lemma 3.1 in Chatterjee and Lafferty (2017), where the projection is onto sets which are a finite union of convex sets.

4.3 Step 3

Proposition 4.1 reduces the problem of upper bounding to the problem of finding a such that which in turn behooves us to find a good upper bound of for any fixed Proceeding to do this, define the mean zero random variables and note that

where is a matrix with on the non diagonals and zero on the diagonals. This implies

An application of the Cauchy Schwarz Inequality to the first term on the right side of the above inequality now gets us the following:

| (4.1) |

The control on is carried out in the following lemma. The proof is done by a chaining argument and is given in the appendix.

Lemma 4.2.

There exists universal positive constants such that for any we have

Combining Lemma 4.2 with (4.1) shows that with high probability as quantified in Lemma 4.2 we have

Setting it can be checked that An application of Proposition 4.1 then gives us with high probability, which in turn gives the following proposition:

Proposition 4.2.

There exists a positive constant such that for all and we have

The above proposition upper bounds the risk of our estimator by a sum of two terms. The first term scaling like term is essentially the minimax rate of our problem (upto logarithmic factors) which is attained by the global least squares estimate (c.f. (Shah et al., 2016a, Theorem 5)). The second term is the excess risk of our estimator as compared to the risk of the global least squares estimate. Thus it suffices to focus on controlling this excess risk term, which measures how much the sorting permutation changes .

4.4 Step 4

In this step we investigate the excess risk term Analyzing this term is one of the key contributions of this paper. We first prove the following lemma concerning the behavior of . Recall that for any we denote to be the th row sum of the matrix

Lemma 4.3.

Let Setting we have

| (4.2) |

Proof.

Define the vector of row sums of the data matrix as where for all Setting

| (4.3) |

we will first show that

| (4.4) |

With

we have

Thus an application of Bernstein’s inequality gives

A union bound then proves (4.4).

It thus suffices to show that after conditioning on the event we have for all

For this, setting , we split the proof into the following cases:

-

•

In this case we will show that

If not, then we have , and so the intervals and are disjoint, implying and thus giving . Now, for any we have by monotonicity. This implies that the intervals and are disjoint, and so which gives . Since this holds for every , the permutation maps the set to a subset of , which is impossible.

-

•

In this case we will again show that

If this does not hold, with we have . Consequently the intervals and are disjoint, and so . By construction of we have . Finally for any we have

and so the intervals and are disjoint as well. This gives , and consequently we have . Thus the permutation maps the set to a subset of , a contradiction.

∎

Remark 4.1.

The ideal case here is when the permutation is close to the identity permutation. In general though, need not be close to the identity permutation. For example, when is a constant matrix, is close to a uniformly random permutation. But Lemma 4.2 shows that and are always close irrespective of what is. For instance, when we have even though both and could be

If however the row sums are strictly increasing, one immediately gets concentration of towards identity. In particular when if is uniformly bounded away from , then Lemma 4.3 shows that high probability

Of course, if the row sums are not increasing, no concentration of towards identity is expected.

Remark 4.2.

We also note that both the bounds above are adaptive in terms of sparsity of the underlying graph. For e.g. if the entries of the matrix are mostly or small, the row sums will be small as well, thus giving a better bound.

Now we can now control the excess risk term This is done as follows.

4.5 Proof of Theorem 2.2

We need to use the following version of Gilbert Varshamov coding lemma (Varshamov (1957)). The proof of this lemma is provided in subsection 6.3.

Lemma 4.4.

[Gilbert-Varshamov] Fix any positive integer Let

There exists a subset with

| (4.5) |

such that for any we have

| (4.6) |

where refers to the Hamming distance between any two points of the hypercube.

We are now ready to prove Theorem 2.2.

Proof of Theorem 2.2.

We are going to prove this lower bound for the symmetric model and a similar proof can be constructed for the skew symmetric model. For any subset define a matrix as follows whenever

Take two different subsets of Denote by to be the symmetric difference of the two sets. Note that whenever and does not belong to or vice versa, we have

Therefore we have

| (4.7) |

Now we apply Lemma 4.4 to extract a finite subset satisfying (4.5) and (4.6). Note that a vector in can be thought of as a subset of by considering the indices which equal . With this identification, consider the set of matrices

Hence the cardinality is exactly the Hamming distance between the corresponding binary strings.

This implies that is a packing set of radius with cardinality atleast Proceeding to bound Kulback Leibler divergences, let the distribution of and under be denoted by and respectively. Choosing small ensures that , which in turn gives

| (4.9) |

The above inequality implies because each entry of is bounded in magnitude by A standard application of Fano’s lemma (see Chapter 13 in Duchi (2016)) with as our packing set and using (4.8) and (4.9), we obtain a minimax lower bound

Choosing appropriately small enough small enough finishes the proof of the theorem. ∎

5 Acknowledgements

We want to thank Bodhisattva Sen for introducing us to this problem, and for his helpful comments and suggestions.

References

- Boucheron et al. [2013] Stéphane Boucheron, Gábor Lugosi, and Pascal Massart. Concentration inequalities: A nonasymptotic theory of independence. Oxford university press, 2013.

- Bradley and Terry [1952] Ralph Allan Bradley and Milton E Terry. Rank analysis of incomplete block designs: I. the method of paired comparisons. Biometrika, 39(3/4):324–345, 1952.

- Chan and Airoldi [2014] Stanley H Chan and Edoardo M Airoldi. A consistent histogram estimator for exchangeable graph models. arXiv preprint arXiv:1402.1888, 2014.

- Chatterjee and Lafferty [2017] Sabyasachi Chatterjee and John Lafferty. Adaptive risk bounds in unimodal regression. 2017. To appear in Bernoulli.

- Chatterjee et al. [2016] Sabyasachi Chatterjee, Adityanand Guntuboyina, and Bodhisattva Sen. On matrix estimation under monotonicity constraints. 2016. To appear in Bernoulli.

- Chatterjee [2014] Sourav Chatterjee. A new perspective on least squares under convex constraint. The Annals of Statistics, 42(6):2340–2381, 2014.

- Chatterjee [2015] Sourav Chatterjee. Matrix estimation by universal singular value thresholding. The Annals of Statistics, 43(1):177–214, 2015.

- Chatterjee et al. [2011] Sourav Chatterjee, Persi Diaconis, and Allan Sly. Random graphs with a given degree sequence. The Annals of Applied Probability, pages 1400–1435, 2011.

- David [1963] Herbert Aron David. The method of paired comparisons, volume 12. DTIC Document, 1963.

- Duchi [2016] John Duchi. Lecture notes for statistics 311/electrical engineering 377. 2016.

- Gao et al. [2015] Chao Gao, Yu Lu, Harrison H Zhou, et al. Rate-optimal graphon estimation. The Annals of Statistics, 43(6):2624–2652, 2015.

- Gao and Wellner [2007] Fuchang Gao and Jon A Wellner. Entropy estimate for high-dimensional monotonic functions. Journal of Multivariate Analysis, 98(9):1751–1764, 2007.

- Hunter [2004] David R Hunter. Mm algorithms for generalized bradley-terry models. Annals of Statistics, pages 384–406, 2004.

- Kyng et al. [2015] Rasmus Kyng, Anup Rao, and Sushant Sachdeva. Fast, provable algorithms for isotonic regression in all l_p-norms. In Advances in Neural Information Processing Systems, pages 2701–2709, 2015.

- Mukherjee et al. [2016] Rajarshi Mukherjee, Sumit Mukherjee, and Subhabrata Sen. Detection thresholds for the beta-model on sparse graphs. arXiv preprint arXiv:1608.01801, 2016.

- Robertson et al. [1988] Tim Robertson, F. T. Wright, and R. L. Dykstra. Order restricted statistical inference. Wiley Series in Probability and Mathematical Statistics: Probability and Mathematical Statistics. John Wiley & Sons Ltd., Chichester, 1988. ISBN 0-471-91787-7.

- Shah et al. [2016a] Nihar B Shah, Sivaraman Balakrishnan, Adityanand Guntuboyina, and Martin J Wainwright. Stochastically transitive models for pairwise comparisons: Statistical and computational issues. In International Conference on Machine Learning, 2016a.

- Shah et al. [2016b] Nihar B Shah, Sivaraman Balakrishnan, and Martin J Wainwright. Feeling the bern: Adaptive estimators for bernoulli probabilities of pairwise comparisons. In Information Theory (ISIT), 2016 IEEE International Symposium on, pages 1153–1157. IEEE, 2016b.

- Simons et al. [1999] Gordon Simons, Yi-Ching Yao, et al. Asymptotics when the number of parameters tends to infinity in the bradley-terry model for paired comparisons. The Annals of Statistics, 27(3):1041–1060, 1999.

- Stigler [1994] Stephen M Stigler. Citation patterns in the journals of statistics and probability. Statistical Science, pages 94–108, 1994.

- Thurstone [1927] Louis L Thurstone. A law of comparative judgment. Psychological review, 34(4):273, 1927.

- van de Geer [2000] Sara A. van de Geer. Applications of empirical process theory, volume 6 of Cambridge Series in Statistical and Probabilistic Mathematics. Cambridge University Press, Cambridge, 2000. ISBN 0-521-65002-X.

- Varshamov [1957] RR Varshamov. Estimate of the number of signals in error correcting codes. In Dokl. Akad. Nauk SSSR, volume 117, pages 739–741, 1957.

6 Appendix

6.1 Proof of Lemma 4.1

6.2 Proof of Lemma 4.2

In order to prove the above lemma, we will need to make use of the following two standard results. We first set up some notations. For any set define its covering number at radius to be the minimum number of Euclidean balls of radius centred inside such that the union of the balls is a superset of Denote this covering number by where the Euclidean metric used is implicit.

Let us now define the space of matrices which are non decreasing in both rows and columns with entries between and as

Estimates of the metric entropy of are available in the literature. The next proposition shows that these metric entropy bounds of can be used to derive a similar bound for the covering number of

Proposition 6.1.

Fix a positive integer We have the covering number inequality for any

The same upper bound for the log covering number holds when is replaced by

Proof.

Let us prove the proposition for the set and the corresponding statement for will follow similarly. Let us define a map as follows:

Let us define another map as

Define the composition map Recall that is the space of monotone matrices with entries in It can now be checked that for all and is a one to one mapping. We now make the observation that for any belonging to we have

| (6.2) |

Now also note that is a continuous map and hence its image is a closed subset of Hence there exists a covering set of at radius with cardinality atmost This is because the set of projections of the covering set at radius onto the closed set forms a covering set of at radius Therefore it follows from (6.2) that the inverse image of under the mapping is a covering set of at radius Thus we can conclude,

The covering number for can be obtained using Lemma 3.4 in Chatterjee et al. [2016] and is written below. This result is proved by using the covering number results in Gao and Wellner [2007].

where and is a universal constant. The last two displays finish the proof. The same proof for goes through by defining to be the identity map. ∎

We are now ready to prove Lemma 4.2.

Proof of Lemma 4.2.

To begin, setting we claim that there exists a universal constant such that

| (6.3) |

We first prove the lemma, deferring the proof of (6.3). Note that by definition, each entry of is zero mean and lies between and Also in the skew symmetric model, for any we have , where we use the fact that we are filling the missing entries by Hence the contribution of the upper diagonal part to is the same as the lower part, and so

| (6.4) |

It is now not too hard to show that for any fixed is a Lipschitz function of with Lipschitz constant Invoking a concentration result for convex Lipschitz functions due to Michel Ledoux(see [Boucheron et al., 2013, Theorem 6.10]), we have

This, along with Lemma 6.3 shows that with high probability we have , which by a simple union bound argument gives

and so the proof of the Lemma is complete.

It thus remains to prove (6.3). For this, define

Recall that is a random matrix with independent zero mean entries in the upper diagonal and also each entry takes values in Hence an application of a standard chaining result (see van de Geer [2000]) for subgaussian random variables results in the upper bound

The upper limit of the integral is since the diameter (maximum Euclidean pairwise distance) of is bounded by Setting in the last equation we then obtain

Note that because the variable of integration ranges from to This then implies the upper bound

∎

6.3 Proof of Lemma 4.4

Proof.

Assume divides for simplicity. Let denote the Hamming distance on , i.e. for any we have

Take and , and . With and setting we claim that there exists a set such that , and for any we have . Given the claim, define as

and note that for any we have . Also

Since , the proof of the lemma is complete.

It thus remains to prove the claim. To this effect, let denote the largest packing set of of radius in Hamming distance, i.e. for any we have . Then using the maximaility of we have

which implies

| (6.5) |

where is a dimensional random vector with uniform distribution on . To bound the numerator in the RHS above, note that the vector is also distributed uniformly on , and so the RHS of (6.5) equals , where . Using Hoeffding’s inequality as whereas Stirling’s approximation gives Combining these two estimates and using (6.5), for all large we have , thus completing the proof of the lemma.

∎

Proof of Proposition 4.1.

This theorem actually holds for a general convex set and points The proof can be read by setting We first prove strict concavity of Let be defined as

If is positive, then we define whenever . It is easy to check that is concave, and hence the function strictly concave. Also we have and an application of Cauchy Schwarz inequality gives , and hence converges to as These facts then imply that has a unique maximizer which we denote by It thus remains to show , where denotes the unique projection of onto To this effect, noting that

we can write

where is defined by We will now show that is a unique maximizer of as well, for which first note that for all . Recall that Let be a point where is achieved. If , then we would have , contradicting the definition of . Hence , implying that . This shows that is a unique maximizer of as well, and so

thus finishing the proof of the lemma. ∎